Abstract

It is now well-established that business groups (BGs)—an inimitable multifirm structure that enables legally distinct firms to take coordinated action—constitute a dominant organizational form in many economies around the world. The BG phenomenon has attracted sustained scholarly attention over the last three decades. Despite the shift in BG research toward BG heterogeneity and strategic performance outcomes, prior reviews and the last meta-analysis a decade ago focus narrowly on the question of whether BGs confer a financial performance advantage on affiliated firms. We provide a more extensive account of the BG effect and an in-depth review of the theoretical approaches used in prior work by focusing only on family-controlled business groups (FBGs)—the dominant type of BG. We make three contributions. First, we develop a parsimonious organizing framework to summarize extant FBG research in a nuanced way—specifying the relationships examined, theoretical explanations advanced, and empirical evidence adduced. This summary reveals that extant FBG theorizing is predominantly structurally focused. Second, we propose a reorientation of FBG research toward a microfoundations-based approach. We develop a scheme for theoretical “taking” and “giving” of relevant microfoundational frameworks from contiguous management subfields to systematically identify potential paths ahead for future FBG theorizing. Finally, we granularly discuss illustrative microfoundation-based frameworks, outlining how their application could both enrich and better integrate FBG research with contiguous management subfields such as entrepreneurship, family business, and strategy research. We thus consolidate our understanding of FBG research, identify gaps, and suggest promising pathways for future work.

Keywords

Business groups (BGs) constitute a salient organizational form in many economies around the world (Dau, Morck, & Yeung, 2021; La Porta, Lopez-de-Silanes, & Shleifer, 1999), with various names ranging from Japanese keiretsu, Korean chaebols, Taiwanese qiyejituan, Turkish families, and Latin American grupos to Indian business houses. BGs are broadly defined as “sets of legally separate firms bound together in persistent formal and/or informal ways” (Granovetter, 2005: 429) where the firms in question “are accustomed to taking coordinated action” (Khanna & Rivkin, 2001: 47). BGs have attracted sustained scholarly attention (see Table A1 of the online appendix) over the last three decades with scholars from multiple disciplinary backgrounds formulating theories as to why BGs exist and the firm-level consequences of BG affiliation.

The dominant theoretical account has been the economic explanation that BGs substitute for missing or underdeveloped institutions that are needed for effective functioning of factor markets for capital, labor, and other inputs (Caves, 1989; Khanna & Palepu, 2000a; Leff, 1978), as documented in the last comprehensive review of the BG literature by Khanna and Yafeh (2007). However, an empirical meta-analysis by Carney, Gedajlovic, Heugens, van Essen, and van Oosterhout (2011) also revealed a mismatch between the dominant theoretical lens (dubbed the institutional voids view) used to study BGs and the actual pattern of correlations across prior empirical studies. Although the dominant theoretical lens predicts a positive effect of BG affiliation, the meta-analysis suggested an average negative effect of BG affiliation, prompting Carney et al.'s (2011) cautionary plea for researchers to eschew mono-theoretical accounts of a complex phenomenon.

Subsequent to the anomaly revealed by Carney et al. (2011), empirical papers on BGs have since moved more toward examining BG heterogeneity and strategic performance outcomes as one way to explain the conundrum of average negative effects. However, we lack a systematic and in-depth review of what alternative theoretical accounts were used to investigate these linkages, the relative utility of these accounts, and hence potential future research paths for the field. Recent BG-related systematic reviews focus on specific strategic outcomes—such as the phenomenon of internationalization (e.g., Aguilera, Crespí-Cladera, Infantes, & Pascual-Fuster, 2020; Holmes, Hoskisson, Kim, Wan, & Holcomb, 2018) and the role played by BG structures in regulating such phenomenon—rather than examining in-depth the full range of phenomenon where BG structures are implicated and the theoretical approaches used to study those phenomena. Our paper complements these recent reviews in two ways: First, our approach is to examine the entirety of phenomena where BGs are implicated (e.g., financial outcomes, innovation, internationalization, diversification, M&A, and so forth) and go in-depth into the theoretical approaches used to study these diverse phenomena. Second, we focus only on those BGs where the controlling and coordinating core entity is a family—that is, family-controlled BGs (FBGs). Focusing in-depth on FBGs is theoretically and pragmatically reasonable for the following three reasons.

First, we find that FBG studies constitute about 70% of all the BG papers that we reviewed. This scholarly focus on FBGs is understandable given the importance of the phenomenon. Most businesses around the world are family controlled (La Porta et al., 1999; Sharma, Chrisman, & Gersick, 2012). Across a broad sample of firms from 45 countries, Masulis, Pham, and Zein (2011) found that 19 percent of publicly listed firms belong to FBGs and even go up to 40 percent in some emerging economies. For example, in Korea, the 20 largest FBGs account for over 85% of GDP in terms of both assets and sales (Murillo & Sung, 2013). Given the importance of FBGs to scholarship and practice alike, a review that focuses only on FBGs allows us to delve in-depth on the modal type of coordinating entity.

Second, construct clarity on the nature of the coordinating entity is crucial for a review that aims to go in-depth into theoretical approaches used in studying BG phenomenon. This is because a controlling family is different from a controlling bank, which is different from a controlling government in terms of the motivations, internal structure, and incentives of the actors that constitute the BG coordinating entity. Indeed, a reason for the mismatch noted by Carney et al. (2011) between the dominant theory's prediction and empirical evidence could simply stem from inappropriate clubbing of these three different types of coordinating entities into a single “BG effect”. Thus, our proposition is to divide and conquer—by focusing our review on FBGs we reduce the influence of confounding theoretical factors around the BG coordinating entity when drawing conclusions from cross-study comparisons.

Finally, focusing solely on FBGs allows us to identify salient patterns in modes of theorizing in extant research. Indeed, our in-depth review reveals that FBG research overwhelmingly involves structural modes of theorizing—using frameworks largely derived from economics, such as the institutional voids framework. By structural, we refer to modes of theorizing that give primacy to forces at the organizational or higher levels of analyses in explaining regularities in organizational behavior. A structural mode of theorizing gives short shrift to the attributes of actors (such as small groups or individuals) at lower level of analyses (Felin & Foss, 2005), whose appropriately aggregated actions may constitute a theoretical mechanism underlying the observed regularity in organizational behavior. We advocate for reorienting future FBG research toward microfoundational modes of theorizing that are more relevant and promising for family-controlled businesses (Devinney, 2013; Gedajlovic, Carney, Chrisman, & Kellermanns, 2012; Jaskiewicz, Combs, Shanine, & Kacmar, 2016). Given the disproportionate role of the controlling family (typically a small group) in FBGs—as founders, investors, board members, and operating executives, a microfoundations-based approach is more likely to result in elegant, nuanced, and generative theorizing because of a better match with the complexity of the FBG research context.

By sharply focusing only on FBGs but comprehensively including all their strategic implications and the theoretical approaches used to study them, our review advances the conversation on business groups in three ways. First, our review paints a nuanced and rich picture of prior FBG research both in terms of the linkages among core constructs examined by prior empirical work, as well as assessing the theoretical variety used to study these linkages. This allows us to identify that prior FBG research involves predominantly structural modes of theorizing. Second, our review suggests consistent microfoundations-based theoretical pathways for future FBG research. We develop a simple framework of theoretical “taking” and “giving” of relevant microfoundational frameworks from contiguous management subfields to systematically identify potential paths ahead for future FBG theorizing. We believe this reorientation will allow FBG scholars to look at thorny questions from multiple new perspectives and build useful theoretical bridges with contiguous scholarly communities, thus leading to cumulation and consilience in the management fields’ overall knowledge base. Third, we zoom in and discuss a few illustrative theoretical frameworks, consistent with a microfoundations approach. We outline how their application could enrich our knowledge base on relationships already identified in prior FBG research and allow for greater integration of FBG research with the contiguous management subfields of family business, entrepreneurship, and strategy research. We also propose ways in which FBG research consistent with a microfoundations approach can broaden the range of phenomenon that it examines.

Method for Systematic Review

To conduct a systematic review of FBG research, we first searched for published articles in the Financial Times list of 50 highly ranked business journals (FT50) in the year 2020. 1 We then used our judgment to complement this list with five other top management journals 2 that are likely to publish business group research: four from the list of journals in Carney et al. (2011), the American Journal of Sociology, Journal of Business, Management International Review, and Small Business Economics, and a high-quality outlet started in 2011 for international business, Global Strategy Journal. Details of the journals and sample collection procedures are reported in the online appendix (Table A2). Because we wanted the initial search to be broad, we searched for papers that included features of business groups in general, as either independent or dependent variables—irrespective of the level of analysis. The search terms we employed are consistent with Carney et al. (2011), and the time span for the search was 1995 to 2021. 3 The descriptive statistics of our systematic search efforts are presented in Table A1 of the online appendix. Our search process yielded a list of 183 published papers on business groups. From this list, we removed papers that did not explicitly test any hypothesis—for example, verbal theory-building papers or case-based inductive theory-building papers (23) and review, commentary, or descriptive papers (20)—to arrive at a list of 140 articles that met our initial screening criteria. Then, to identify FBG studies—that is, those that study BGs controlled and coordinated specifically by a family entity—we took the following steps. First, we read each article to find out if it explicitly stated whether the coordinating entity of the BGs under study was a family or a nonfamily entity (such as a bank or government). We were able to clearly identify the coordinating entity in 119 articles and classify 89 of these as FBG studies and 30 as non-FBG. Second, for the remaining 21 articles in which the focal BG coordinating entity was not clear, we noted the country (or countries in some cases) from which the study samples were drawn. Then we used data from Masulis et al. (2011) to identify countries in which family-controlled firms represent at least 10% of the stock market. 4 We used this list to categorize the remaining 21 articles as an FBG study if the empirical sample was drawn from a family-business-dominated country and a non-FBG study if otherwise. 5 This step yielded another 9 FBG studies and 12 non-FBG studies. We thus arrived at a final list of 98 FBG studies (= 89 + 9) for our review.

An Organizing Framework for Mapping Prior Empirical FBG Research

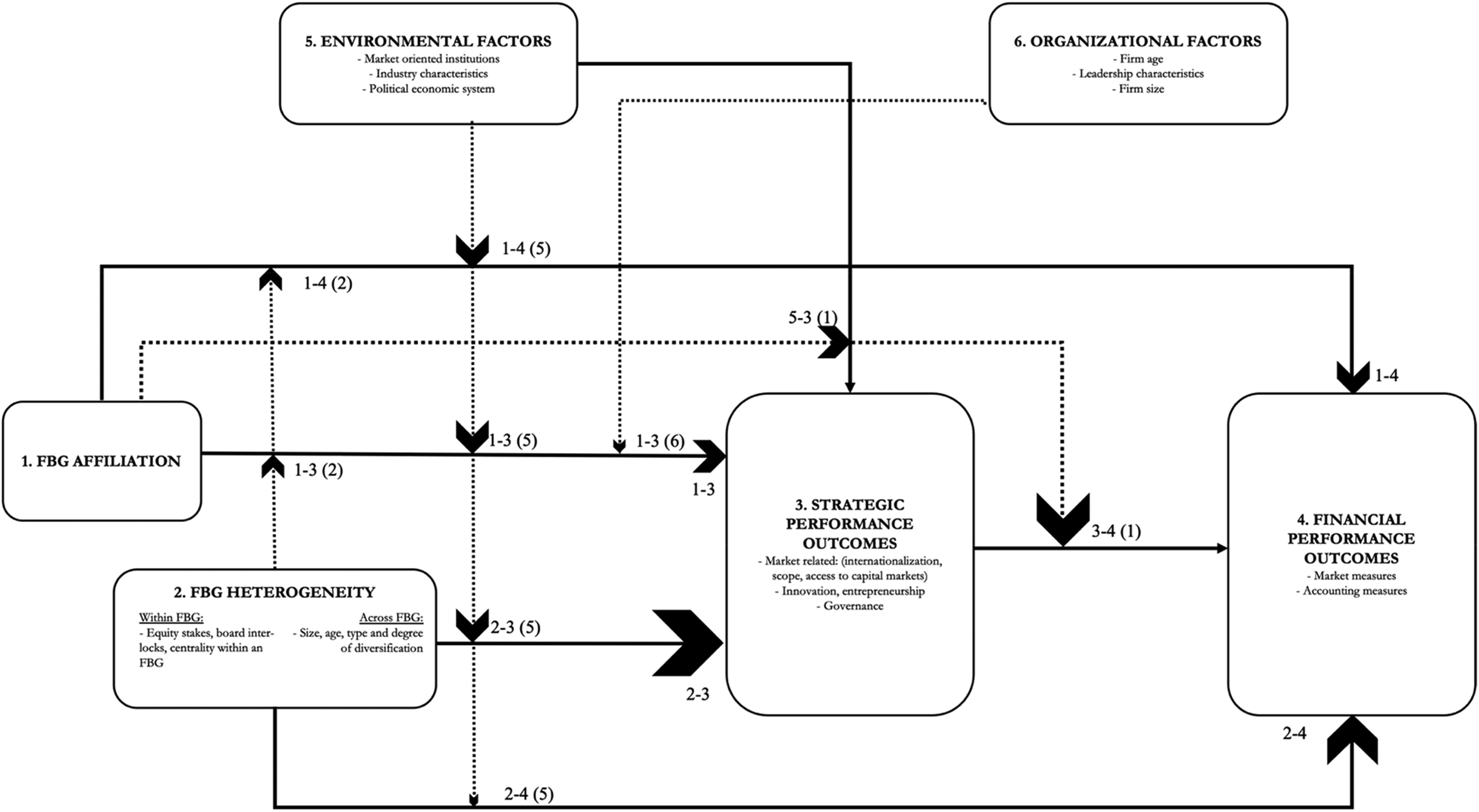

We fully reviewed these 98 papers and noted the key theoretical constructs in each paper. We then coded the linkages among the constructs and captured the directionality of FBG effect on the focal linkage under investigation in each study, if applicable. This resulted in the development of an organizing framework that integrates the linkages among the relevant constructs as independent variables (e.g., FBG affiliation, intra-, or inter-FBG heterogeneity), dependent variables (e.g., financial or strategic outcomes), and moderators (e.g., environmental or organizational influences) based on prior FBG research.

Figure 1 presents this framework consisting of the key constructs (labeled 1 through 6) and the dominant linkages among them (depicted through solid and dashed arrow lines, with the size of the arrowhead indicating the number of studies representing the link, and the framework depicts those links that were examined by three or more papers). Much FBG research focuses on the performance effects of business-group affiliation for firms and how they vary with the quality of the institutional environments in which they are located (e.g., Guillén, 2000; Khanna & Palepu, 2000a, 2000b; Mahmood & Mitchell, 2004). In addition to environmental factors, studies have also examined how various factors at the level of affiliate firms such as firm age, size, and type of leadership regulate FBG effects. Recent research has also underlined the significant heterogeneity that exists across FBGs (at the FBG level as well as across the affiliate firm level) in their resource endowments, organizational structure, and interorganizational ties. Further, studies have begun to examine the effects of FBG affiliation and FBG heterogeneity beyond financial performance and on other strategic outcomes such as product-market expansion, innovation, and governance.

Organizing Framework for Mapping Conceptual Linkages Examined in Prior FBG Research

The framework thus presents a comprehensive overview of existing FBG research as well as offers a visual representation of gaps that can guide future research. For instance, Figure 1 shows that a substantial volume of work has focused on understanding the effects of FBG heterogeneity on affiliated firms’ financial or strategic performance outcomes (depicted through arrows 2–4 and 2–3). We note that prior comprehensive reviews of BG research (Khanna & Yafeh, 2007) or empirical meta-analyses of BG effects (e.g., Carney et al., 2011) limit their focus to primarily the financial consequences of BG affiliation (Figure 1, link 1-4) and hence are not able provide the big-picture account of the various conceptual linkages examined by prior work, as we do in this review. In addition, the figure also highlights that prior research has largely overlooked the factors that lead to FBG emergence or to the various forms of inter- or intra-FBG heterogeneity. Although multiple theoretical explanations have been proposed for the emergence of FBGs rooted in institutional economics (Khanna & Palepu, 1997), sociology (Granovetter, 1994; 2005), political science, and entrepreneurship (Amsden, 1989; Guillén, 2000), extant empirical work takes FBGs as given and does not empirically examine their emergence. Table 1 provides an overview of the theoretical diversity in FBG research and captures the dominant theoretical perspectives used to examine the relationships among key constructs presented in panels A through E. 6 We describe and summarize the findings of key studies underlying each of the panels in the following sections.

Theoretical Perspectives in Prior Empirical FBG Research

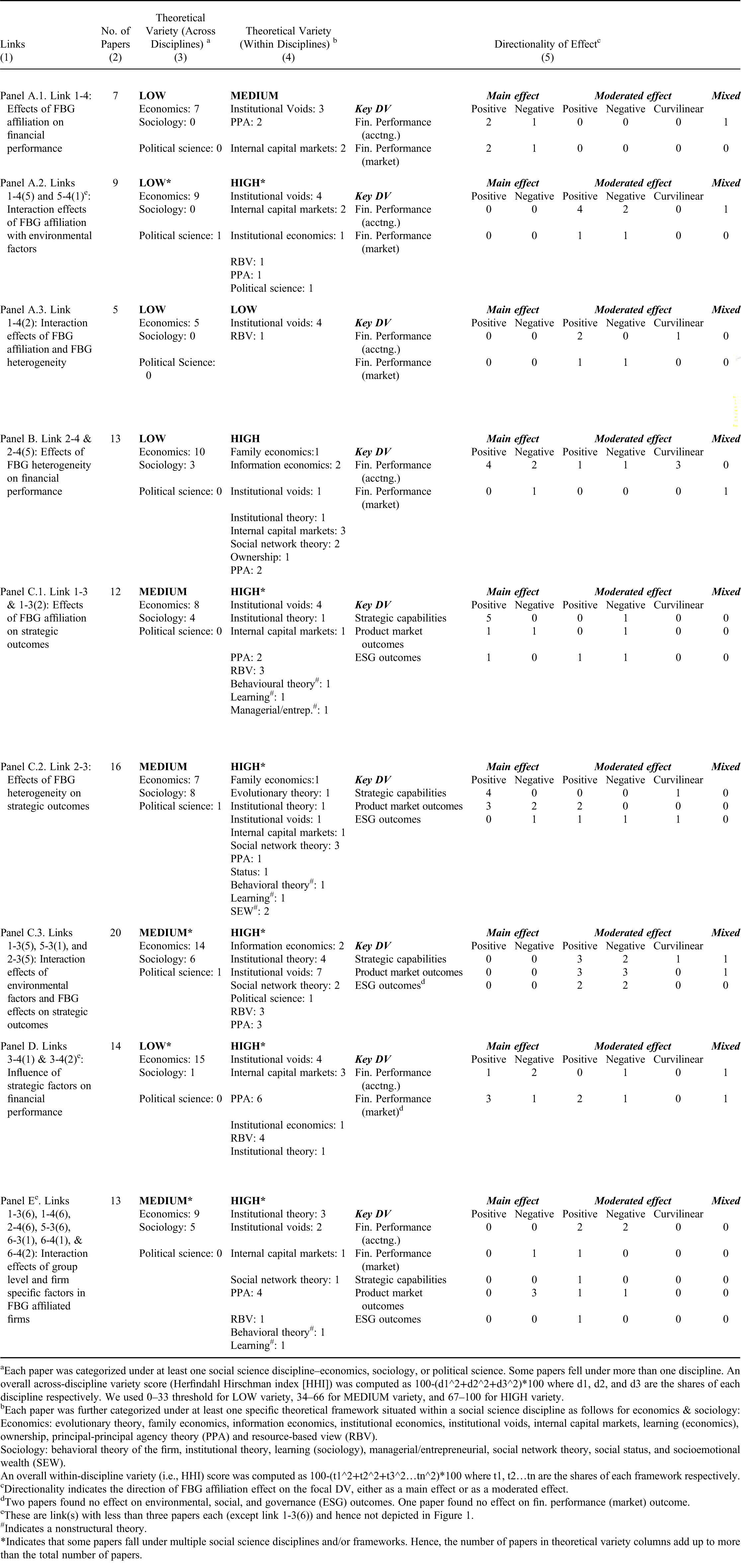

Each paper was categorized under at least one social science discipline–economics, sociology, or political science. Some papers fell under more than one discipline. An overall across-discipline variety score (Herfindahl Hirschman index [HHI]) was computed as 100-(d1^2+d2^2+d3^2)*100 where d1, d2, and d3 are the shares of each discipline respectively. We used 0–33 threshold for LOW variety, 34–66 for MEDIUM variety, and 67–100 for HIGH variety.

Each paper was further categorized under at least one specific theoretical framework situated within a social science discipline as follows for economics & sociology:

Economics: evolutionary theory, family economics, information economics, institutional economics, institutional voids, internal capital markets, learning (economics), ownership, principal-principal agency theory (PPA) and resource-based view (RBV).

Sociology: behavioral theory of the firm, institutional theory, learning (sociology), managerial/entrepreneurial, social network theory, social status, and socioemotional wealth (SEW).

An overall within-discipline variety (i.e., HHI) score was computed as 100-(t1^2+t2^2+t3^2…tn^2)*100 where t1, t2…tn are the shares of each framework respectively.

Directionality indicates the direction of FBG affiliation effect on the focal DV, either as a main effect or as a moderated effect.

Two papers found no effect on environmental, social, and governance (ESG) outcomes. One paper found no effect on fin. performance (market) outcome.

These are link(s) with less than three papers each (except link 1-3(6)) and hence not depicted in Figure 1.

Indicates a nonstructural theory.

*Indicates that some papers fall under multiple social science disciplines and/or frameworks. Hence, the number of papers in theoretical variety columns add up to more than the total number of papers.

Financial Performance Effects of FBG Affiliation

The broad question of whether and how business groups add financial value has motivated a significant portion of the FBG research and has been the core focus of prior reviews (Carney et al., 2011; Khanna & Yafeh, 2007; Yiu, Lu, Bruton, & Hoskisson, 2007). We found seven empirical studies in our review directly examining this relationship as represented by the link 1-4 in Figure 1 (summarized in online appendix Table A3 under panel A.1). In fact, most of the studies examining FBG affiliation effect have also considered interaction with environmental factors (links 1-4(5) and 5-4(1)) and FBG heterogeneity (link 1-4(2)), which we describe separately under subsections A.2 and A.3. Significantly, all the 19 studies in our review exploring the financial consequences of FBG affiliation are based on economic theories 7 (see Table 1), highlighting a critical need for a more diverse perspective.

Effects of FBG Affiliation on Financial Performance (Figure 1, link 1-4; Table 1, panel A.1)

Firm financial performance has been measured using both accounting profit measures (four studies) and capital market measures (three studies). While making the case for whether or not FBGs add financial value, this body of work highlights a variety of costs and benefits associated with FBGs for affiliated firms (see Table A5 of online appendix for a summary). One of the primary costs associated with FBGs stems from agency issues (Keister, 1998; Khanna & Palepu, 2000a; Morck & Yeung, 2003). Member firms tend to suffer from conflict of interests between controlling the family and the minority shareholders. It is plausible in many FBGs that the family has controlling stakes in several firms but still does not have significant cash flow rights in many of them (Morck & Yeung, 2003). This creates incentives for the family to expropriate and transfer profits across firms—from firms in which the family has low cash flow rights to firms where it has high cash flow rights—referred to as tunneling. Bertrand, Mehta, and Mullainathan (2002) report evidence that Indian business groups engage in tunneling, though Siegel and Choudhury (2012) raise questions about the reliability of these findings. Secondly, FBGs may serve to reduce bankruptcy risks to weaker affiliates but impose additional costs on stronger members (Ferris, Kim, & Kitsabunnarat, 2003). Another problem in the case of firms in which the family does retain a substantial ownership, and has family members in management, is that corporate governance mechanisms might be subverted, leading to problems of managerial entrenchment. This leads to controlling families interfering in both tactical and strategic decision-making of member firms. Further, because of inequity and nepotism, inefficient compensation systems tend to develop across group companies, with detrimental effects on the market for talent (Chen, Chittoor, & Vissa, 2021). Coupled with the security that affiliation to FBGs offers, managers of group-affiliated firms typically have weaker incentives to run their firms efficiently (Khanna & Rivkin, 2001).

Despite these costs, FBG affiliation also provides many benefits to individual firms. Most important, it is widely recognized that in the absence of well-developed economic institutions that support effective functioning of capital, labor, and product markets, FBG firms have access to internal alternatives for these resources within the FBG (Khanna & Palepu, 2000a, 2000b). Capital for new projects, management talent, and inputs to production may all be accessed at lower transaction costs within the FBG (Caves, 1989; Leff, 1978) than from external markets or intermediaries. Moreover, the internal hierarchical control of the FBG may also discipline the management of the affiliated firm in terms of how they actually utilize capital (Masulis et al., 2011). Khanna and Rivkin (2001) also suggest that FBGs may have superior access to the political power structure in the economy through their consolidated lobbying and influence efforts—and hence they may benefit from a richer pool of opportunities in the country. As with other forms of multibusiness organization, FBGs can potentially leverage economies of scale and scope, particularly those of a nonrivalrous nature (Chang & Hong, 2000; Mahmood & Mitchell, 2004). In addition, FBGs and their affiliates also represent a social structure characterized by repeated interaction, family ties, and rich information flows—consequently, the costs of transacting within the FBG may be lower than that for comparable transactions between independent firms (Granovetter, 1994; Guillén, 2000).

Although there is a fair degree of convergence in the literature on the list of potential costs and benefits of FBG affiliation (or because there are both costs and benefits), the theory and the empirical evidence are inconclusive in their net impact on an affiliated firm's financial performance. This may partly be the case because some of the costs imposed by FBGs on certain affiliate firms may show up as benefits for other affiliate firms (e.g., cross-subsidization). Moreover, the relationship between FBG affiliation and financial performance may be subject to many moderating factors or be mediated by the attainment of other factors such as strategic outcomes. Thus, it is not possible to characterize FBGs either as “paragons or parasites” (Khanna & Yafeh, 2007) or “avatars or anachronisms” (Granovetter, 2005), and the estimated affiliation effects observed across countries and studies show wide variance (Carney et al., 2011; Khanna & Rivkin, 2001). Consistent with an earlier empirical meta-analysis by Carney et al. (2011), our review finds ambiguous evidence for the relationship between FBG affiliation and firm performance with four studies indicating a positive relationship (for example, Khanna & Palepu, 2000a), a negative relationship in the case of two studies (such as Baek, Kang, & Park, 2004), and one indicating mixed effects across 14 emerging markets (Khanna & Rivkin, 2001). Three of these studies found a positive affiliation effect on indirect financial performance outcomes such as investments and financial performance post-1997 financial crisis in Korea (Almeida, Kim, & Kim, 2015); access to bank finance by small firms in Italy (Cainelli, Giannini, & Iacobucci, 2020); and likelihood of firm survival, also in Italy (Santioni, Schiantarelli, & Strahan, 2020). Importantly, all the seven studies examining the FBG affiliation effect use economic theories that are structural, predominantly the institutional voids perspective and internal capital markets (see Table 1), highlighting the need for using more diverse theoretical approaches. As many factors could potentially moderate or mediate the link 1-4, it may not be possible to establish a general valence for this link; hence, unlike prior reviews, we separately examine evidence from the studies that investigate such factors.

Interaction Effects of FBG Affiliation With Environmental Factors (Figure 1, link 1-4(5); Table 1, panel A.2)

If the primary benefit of FBG affiliation in emerging economies (and indeed the rationale for their existence) stems from the absence of strong economic institutions, a logical corollary would be that FBG affiliation effects are a function of the institutional context in which they are situated. How institutional environment moderates the relationship between FBG affiliation and financial performance is a question that has received significant attention, especially in the last 10 years. We found seven studies (for example, Castaldi, Gubbi, Kunst, & Beugelsdijk, 2019; Khanna & Palepu, 2000b) exploring the empirical evidence for the link 1-4(5) in Figure 1, where 5 represents environmental factors, such as market or political institutions, and industry factors. As most developing economies where FBGs have a dominant presence—such as India, Taiwan, and Latin America—have begun embracing economic reforms over the last three decades, the question arises of whether FBGs in these contexts would continue to add value. Examining this question in the context of the evolving economic environment in Chile, Khanna and Palepu (2000b) posit and find that group benefits atrophy over time as capital or product markets develop. In a similar finding, Minetti and Yun (2015) report that the pricing differences in loan contracts between chaebol and non-chaebol firms narrowed or disappeared once the government-influenced chaebol safety net was dismantled in the late 90s in Korea. Extending these arguments to the foreign subsidiary performance, Castaldi et al. (2019) find that FBG affiliation enhances subsidiary performance in host countries where institutions are underdeveloped. Instead of viewing market-oriented institutional change as a discrete event, Kim, Kim, and Hoskisson (2010) divide it into periods of institutional frictions and convergence, and they report, using evidence from a sample of Korean firms, that FBG firms profit from internationalization during institutional convergence but not when there are frictions or major changes.

Two studies (Chacar & Vissa, 2005; Guillén, 2000) explore the effect of institutional environment in an interesting way (link 5-4(1) 8 ). Guillén (2000) finds a positive association between FBGs’ market share and asymmetries in foreign trade across nine emerging economies. Examining persistence of firm performance in a developing country (India) and developed country (United States), Chacar and Vissa (2005) find that poor firm performance persists longer in India when compared to the United States while there is no difference in the persistence of superior firm performance. Further, they find that poor firm performance persists longer in firms affiliated to FBGs and MNCs compared to unaffiliated firms, thereby supporting the hypothesis that FBGs tend to prop up poorly performing firms by shuffling resources from better-performing firms.

Studies in a multicountry context by Khanna with other coauthors (Khanna & Rivkin, 2001; Khanna & Yafeh, 2005) find inconclusive evidence for the moderating role of market institutions on the FBG effect. Exploring whether FBGs help smoothen the variability of earnings for affiliated firms, using evidence from 12 emerging economies, Khanna and Yafeh (2005) conclude that the degree of capital market development does not explain the extent of risk sharing within FBGs. Some studies that are more recent report evidence opposite to that of the institutional voids hypothesis (Chittoor, Kale, & Puranam, 2015b; Lamin, 2013; Manikandan & Ramachandran, 2015; Siegel & Choudhury, 2012) with the FBG effect becoming more positive as market institutions develop. Multicountry studies (Khanna & Rivkin, 2001) and meta-analysis (Carney et al., 2011) do not find consistent support for a substitutive or complementary relationship between FBG affiliation and the degree of institutional development. We suggest two ways to address this puzzle in the section on suggestions for future research later: (a) to take into account the inter-connectedness of the economic selection environment and the prevalence of wealthy controlling families in an economy and (b) to break down the institutional environment into specific dimensions (as in Chittoor, Aulakh, & Ray, 2015a; Guillén, 2000), such as market institutions (equity and debt markets, labor markets, trade freedom, and so on), political economic factors, and industry factors. Remarkably, we find that with the exception of Guillén (2000) all the other studies examining the interaction effects of FBG affiliation with environmental factors are also built on structural economic theories (Table 1, panel A.2). Given the significant influence of the members of the controlling families in FBGs, there is a perceptible need to go beyond structural theories and bring in fresh theoretical perspectives with a more microfoundational lens not only to better understand the FBG effect but also to help reconcile the mixed findings of prior research.

Interaction Effects of FBG Affiliation and FBG Heterogeneity (Figure 1, link 1-4(2); Table 1, panel A.3)

Most BG studies, both on FBGs and others, have conceptualized and operationalized the BG effect by using a BG affiliation dummy—a coarse-grained measure. However, significant heterogeneity exists among FBGs in terms of family ownership, family presence and structure, political connections, variation in their diversification profile, etc. The number of FBG heterogeneity studies has increased by 77% from 1995–2010 to 2011–2021 (as compared to 69% increase in studies that operationalize the FBG effect as a dummy variable during the same time period, see Table A4 in the online appendix). Effects of heterogeneity factors have been studied at the level of firms within an FBG, which may exist in the form of differences in the degree of ownership by the controlling owner, the levels of ownership (direct versus pyramidal), board membership and interlocks, etc., and also across FBGs in terms of FBG size, age, degree of diversification, etc. Out of the 61 papers in our review delving into FBG heterogeneity, a majority of the papers (37) studied across-BG heterogeneity when compared to firm-level heterogeneity within FBGs (Table A4 in the online appendix).

In this section, we focus on studies that combine FBG affiliation effect with one or more variables of FBG heterogeneity, and in the next section delve more deeply into the effects of FBG heterogeneity. To begin with, the seminal study of Khanna and Palepu (2000a) on the benefits of FBG affiliation also reports its contingency with the level of diversification in the business group. Controlling for size effects, they find that firm performance initially declines with group diversification and subsequently increases once group diversification exceeds a certain threshold level. In a study of Korean FBGs between 1985 and 1996, Chang and Hong (2000) find a positive relationship between the profitability of an affiliated firm and the intangible and financial resources available with the affiliated FBG. In another study using the same dataset, Chang and Hong (2002) find that the positive effect of FBG affiliation on firm performance tends to be smaller in larger FBGs and decreases over time. Interestingly, Chu (2004) reports an opposite finding in the case of Taiwanese firms in that member firms affiliated with larger BGs show better financial performance. More recent studies report the positive influence of the degree of participation of the FBG firm in capital markets (Chittoor et al., 2015b). Extending the FBG effects to foreign markets, Castaldi et al. (2019) find a positive FBG influence on foreign subsidiary performance but only when the parent and the affiliate firm belong to the same industry. All the five studies marking the link 1-4(2) are based on economic theories, once again highlighting the need for more theoretical variety. These studies that combine the FBG affiliation effect with FBG heterogeneity, though limited in number, highlight the need for a more nuanced understanding of the FBG effect by going beyond its operationalization as a 0 or 1 dummy variable.

Effects of FBG Heterogeneity on Financial Performance (Figure 1, links 2-4 & 2-4(5); Table 1, panel B)

Initial studies examined the financial consequences of FBG size and scope (extent of diversification). In their meta-analysis study, Carney et al. (2011) examine the effect of BG size and BG product-market scope and report a positive effect of the former and a negative effect of the latter on firm financial performance. Our review identified 10 papers examining the empirical evidence for the link between various factors of FBG heterogeneity and financial performance (2-4 link); further three papers studied the moderating role of institutional environment as well (2-4(5) link). The positive effect of BG size finds support in FBG studies (e.g., Khanna & Palepu, 2000a) as in the case of other BGs (for example, with banks as the coordinating agency in Dewenter, Novaes, & Pettway, 2001). As to the effect of scope, Khanna and Palepu (2000b) find a curvilinear relationship between FBG scope and affiliated firms’ performance with a positive effect only beyond a threshold level. Our review revealed a number of interesting FBG studies examining heterogeneity using family ownership variables. Some of the family variables used as explanatory variables include marriage ties (Han, Shipilov, & Greve, 2017), generational involvement (Bertrand, Johnson, Samphantharak, & Schoar, 2008), and intra-group equity ties (Mahmood, Zhu, & Zaheer, 2017b). In a study of 93 Thai FBGs, Bertrand et al. (2008) find a positive effect of family involvement on firm performance, though it is limited to founder's generation and turns negative after the founder's death. They attribute this effect to the dilution of ownership and control over multiple generations, which creates a “race to the bottom” in tunneling resources out of the group firms. Yang and Schwarz (2016) also find a detrimental effect of excess control by family but report a weakening of this effect in FBGs governed by professional managers. Further exploring the effects of structure and control, Masulis et al. (2011) find that financing advantages are greater for FBG firms held in pyramidal rather than in horizontal structures, but group firm performance declines when dual-class shares and cross shareholdings are employed as additional control-enhancing mechanisms. Two studies explore and find spillover effects from one FBG firm to the rest: Bae, Cheon, and Kang (2008) in the case of announcement of earnings and Joe and Oh (2018) in the case of change of credit ratings—with negative spillovers having a more dominant effect than positive spillovers. Stressing the importance of disclosure and its heterogeneity among FBGs, Beaver, Cascino, Correia, and McNichols (2019) find that the availability of intragroup financial information is a key predictor of financial default of group firms, after controlling for firm's own financial information. Finally, a couple of studies (Buchuk, Larrain, Muñoz, & Urzúa, 2014; Kim, 2016) reinforce the internal capital markets hypothesis with evidence of higher investment, leverage, and financial performance by FBG firms that borrow internally. In a more nuanced study of this effect, during a seven-year period just after the Asian financial crisis in 1997, Kim (2016) finds that FBGs’ financial leverage led to a loss of market share for affiliate firms, and this negative consequence is more pronounced for firms in fast-growing industries. Our conclusion from the review of this link (2-4) is that while some recent research has begun to delve into FBG heterogeneity, this area holds immense promise for future research as we elaborate later through the usage of more microfoundational and behavioral theories.

We now turn to work that examines the moderating effect of environment on the link between FBG heterogeneity and firm performance (link 2-4(5)), which consists of three studies in our review pool. During market-oriented transition in Taiwan over a 24-year period, Luo and Chung (2005) find that family and prior social ties between top leaders within FBG firms have a positive effect on group performance, but family ties beyond a threshold tend to reduce group performance. On the other hand, in the same context, Mahmood et al. (2017b) find centralized intragroup equity ties improve affiliate performance, but this effect is found to weaken when the environment becomes more turbulent. In other words, there seems to be a difference in the effects of mere family ties and equity ties, and further, these effects are contingent upon the institutional environment. Similarly, in the financial default prediction model by Beaver et al. (2019) using a combination of information from affiliate firms and the business group, it is found that the predictive ability reduces as the financial reporting standards of the home countries improve in a dataset comprising over 100 countries. As highlighted earlier, these studies reinforce the need to delve separately into diverse elements constituting an institutional environment. Moreover, a majority of the studies examining FBG heterogeneity continue to use economic theories (10 out of 13), though there is more diversity in the variety of economic perspectives used. Given that family is a social institution, there is a need for more research that leverages sociological theories such as social network theory (two studies) and institutional theory (one study) to help us better understand both inter- and intra-FBG heterogeneity.

Shifting Focus Toward Strategic Performance Outcomes: Effects of FBG Affiliation on Strategic Outcomes (Figure 1, links 1-3 & 1-3(2); Table 1, panel C.1)

Prior reviews of the BG literature have primarily focused on the financial consequences of BG affiliation (Carney et al., 2011; Khanna & Rivkin, 2001), but our review of the FBG literature indicates a significant shift in the focus toward strategic performance outcomes. In the last 10-year period, only 23 FBG papers have focused on financial consequences when compared to 38 FBG papers on strategic consequences (see Table A4 of the online Appendix). This shift seems to be in the right direction, as FBG effects on strategic outcomes illuminates our understanding of how FBGs add financial value by delving into specific mechanisms.

We start with the FBG affiliation effects (Table A3, panel C.1). Our review revealed strategic outcomes in broadly three categories: product-market outcomes, such as market share, new market entry, internationalization, and so on; strategic capabilities, such as innovation and marketing capabilities, etc.; and finally, environmental, social, and governance (ESG) outcomes. We first examine the evidence for the FBG affiliation effect as represented by the link 1-3. With only seven studies for this link, spread across different settings and examining different strategic outcome variables, it is not possible to generalize the FBG effect on strategic outcomes, but we explore for any noticeable patterns. Examining the international expansion of Korean firms into China between 1987 and 1995, Guillén (2003) finds evidence for coordination and imitation among the firms belonging to the same FBG in their foreign entry mode choices. Kumar, Singh, Purkayastha, Popli, and Gaur (2020) also explore internationalization patterns of FBG and other unaffiliated firms from India and find that FBG firms tend to be less aggressive, as indicated by how quickly they conduct their first overseas M&A as family firms tend to be more conservative. Three more studies exploring this link focus on market-related outcomes and report advantages for FBG firms when compared to other firms. Vissa, Greve, and Chen (2010) find that FBG-affiliated firms are more externally oriented in setting performance aspirations and are more likely to respond to low performance in comparison to market. Iacobucci and Rosa (2005) and Manikandan and Ramachandran (2015) list several structural advantages that FBGs possess that enable them to leverage external growth opportunities better and report supportive evidence in Italian and Indian firms, respectively. The last two studies of this link highlight other strategic advantages of FBGs; Bena and Ortiz-Molina (2013) reaffirms financing advantages due to the pyramidal structure of FBGs whereas Ray and Ray Chaudhuri (2018) reports evidence for positive environmental and social sustainability orientation of FBG firms.

Five more studies explored how a few FBG heterogeneity variables moderate the FBG affiliation effect on strategic outcomes (link 1-3(2)). Examining international search behavior, Gubbi, Aulakh, and Ray (2015) find that FBG-affiliated firms that are younger and that occupy a prominent position within the group or industry are able to receive better support to undertake international search. Chang, Chung, and Mahmood (2006) report that FBGs’ ability to share technological knowledge and financial resources among affiliates enables them to promote innovation in affiliate firms, but the groups’ diversification inhibits their innovativeness. Even in a setting of small and medium enterprises, Guzzini and Iacobucci (2014) find a positive FBG effect on R&D intensity, and this effect is strengthened in firms of higher size and greater FBG ownership. Examining governance-related outcomes, Bonacchi, Cipollini, and Zarowin (2018) study earnings management practices and find that FBG firms are more likely to manage earnings using unlisted subsidiaries primarily to avoid reporting losses. In a similar vein, Choi, Jo, Kim, and Kim (2018) find that though FBG firms have higher CSR overall (as reported by Ray & Ray Chaudhuri, 2018), ownership disparity between cash flow and control by inside shareholders is associated with lower CSR.

Overall, this body of evidence clearly demonstrates a shift in the right direction toward strategic variables, which play an important mediating role on financial performance outcomes. Given their focus on a broad array of strategic variables, we find an increasing use of sociological theories (four) as compared to economic (eight) among the twelve studies representing links 1-3 and 1-3(2). The evidence is still limited to indicate a generic directionality for the FBG effect on any of the strategic outcomes, and as the following section indicates, identification of a combination set of factors when FBG affiliation can positively or negatively influence various strategic outcomes would be a better approach.

FBG Heterogeneity Effects on Strategic Outcomes (Figure 1, link 2-3; Table 1, panel C.2)

In line with the other shift in the literature from FBG affiliation to FBG heterogeneity studies, we found as many as sixteen studies focusing on the 2-3 link between FBG heterogeneity variables and strategic outcomes. A majority of the studies exploring the link (2-3) are more nuanced in terms of both the FBG characteristics (independent variables) and the strategic outcomes (dependent variables). This has resulted in a medium-to-high degree of diversity in the theoretical lens used in this stream of FBG research as borne out by Table 1. The dominant focus of most studies has been on product-market outcome variables (eight), followed by innovation outcomes (four) and a limited number of studies focusing on ESG variables (four). Studies highlight a number of FBG factors that positively affect an affiliate's potential to enter new markets, including inter-FBG marriage ties (Han et al., 2017), political connections with the ruling party (Zhu & Chung, 2014), internal capital markets within FBGs (Boutin, Cestone, Fumagalli, Pica, & Serrano-Velarde, 2013; Masulis, Pham, & Zein, 2020), and preservation of socio-emotional wealth (SEW) (Gu, Lu, & Chung, 2019). SEW refers to a key microfoundational construct used by scholars of family business (Gómez-Mejia, Cruz, Berrone, & Castro, 2011) to capture nonpecuniary benefits that a focal controlling family obtains from the firms it controls. Distinguishing the effects of a focused versus broad SEW, Gu et al. (2019) propose that controlling owners’ likelihood to pursue new industry entry is negatively affected by the exercise of family influence (used as a proxy for focused SEW) but is positively associated with the succession of family dynasty (a form of the broad SEW). Furthermore, these effects are found to be stronger when the founder generation is in control, strengthening the broad pattern of evidence that the family effects weaken over multiple generations (Bertrand et al., 2008). Chung and Luo (2008a) reaffirm the socioemotional influence of family ownership and report that family-dominated BGs are less likely to (a) divest of unrelated businesses and (b) make unrelated acquisitions. Examining the relationship between product diversification and internationalization, Kumar, Gaur, and Pattnaik (2012) find a negative relationship between the two in emerging market FBGs, indicating the need for a balancing act between the two. Extending the work on the FBG effect on internationalization, Santangelo and Stucchi (2018) propose that the coordination capabilities developed through an FBG's domestic geographic dispersion can be exapted (re-used) to enable outward FDI activities and find support in a longitudinal dataset of 693 Indian FBGs. Most of these studies throw light on the various mechanisms through which FBGs create advantages by leveraging internal social networks to confer benefits of product-market growth in affiliated firms.

How FBGs affect innovation outcomes is the next major theme addressed by FBG studies, and similar advantages of scope and within-FBG networks are found in this case, too. Mahmood and Mitchell (2004) argue that while FBGs facilitate innovation for member firms, they also discourage innovation at the overall economy level by creating barriers for non-FBG firms. Exploring the within-BG heterogeneity of the FBG effect on innovation capabilities, Mahmood, Chung, and Mitchell (2013) find that the density of buyer-supplier ties within an FBG has a positive impact on group's innovation. In another innovation study across FBGs, Mahmood, Zhu, and Zajac (2011) propose and find that the centrality of an affiliate's position in the intragroup director network and buyer-supplier network is positively related to its R&D capability. Defining innovation performance broadly, Mithas, Ramasubbu, and Sambamurthy (2011) identify intragroup information management capabilities as a key determinant.

Given that family ownership and control of BGs has unique and interesting implications for ESG outcomes, a few studies have begun to explore these. The size of the family owning the BG has a positive association with family involvement in ownership, control, and management, especially during subsequent generations of the founder (Bertrand et al., 2008). A recent study by Masulis et al. (2020) points out that motivations to retain family control shape how FBGs access capital through new public offerings (IPOs). Su and Tan (2018) report that FBGs, particularly those with more product and international diversity are more likely to use tax havens. Family ownership and intragroup transactions are found to influence firm CSR (Oh, Chang, & Kim, 2018) as well as the firm disclosures of environmental performance (Terlaak, Kim, & Roh, 2018). Overall, this stream of research indicates that while we understand the FBG effect on a few strategic outcomes such as product-market growth, internationalization, and innovation fairly well, our understanding of how FBGs affect other strategic factors such as ESG outcomes is still limited and can be aided by the usage of a wider theoretical lens that includes theories from political science and family business.

Interaction Effects of Environmental Factors and FBG Effects on Strategic Outcomes (Figure 1, links 1-3(5), 5-3(1), and 2-3(5); Table 1, panel C.3)

In the last two decades, the discipline of strategy has seen an increasing application of neo-institutional theory as economic and social institutions are found to have a significant influence on the strategies and performance of firms (Ahuja, Capron, Lenox, & Yao, 2018). A key theme under this stream has been how the institutional environment affects FBG affiliated and unaffiliated firms differently. We counted twenty studies from our review pool that focused on how the FBG effect on strategic outcomes varies across different environments (roughly divided equally between the links 1-3(5), 5-3(1) and 2-3(5)), and this stream also reflects reasonable diversity in the theoretical lens used (see Table 1). The strategic variables examined by these studies primarily consist of product market-related, innovation, governance, and capital market variables, and these effects are found to be contingent on the institutional and other environmental factors. Chang et al. (2006) demonstrate this by comparing and reporting differences in innovation outcomes between FBG and non-FBG firms in Korea and Taiwan, countries with distinctly different institutional systems in the early 1990s. Lamin (2013) proposes that FBGs offer advantages stemming from information and knowledge sharing among affiliate firms and that such advantages are found to boost international sales even in deregulated and globally competitive industries, such as information technology services in India. This finding is further reinforced by Manikandan and Ramachandran (2015) who find that improving market institutions have a positive impact on growth opportunities for FBG firms in India. Exploring how international search intensity of firms is affected by institutional changes in India, Gubbi et al. (2015) find that FBG firms suffer a disadvantage when there is a misalignment between how the institutional changes affect the specific affiliate firm's industry and the FBG as a whole. Using a dataset of M&As by firms from nine emerging economies over a 21-year period, Kim and Song (2017) find that the likelihood of the abandonment of M&A deals (after being publicly announced) is less when acquirers are affiliated with FBGs and that this effect decreases as external capital markets develop. Highlighting some unique approaches to foreign subsidiary management in FBG firms, a recent study by Chung, Dahms, and Kao (2021) finds that family managers are assigned to manage foreign subsidiaries when they have stronger operations outside the home region and in subsidiaries where there are strong institutional differences between home and host countries.

Complementing these studies, we found seven studies that examine the environmental effect as an independent variable and how it is affected by FBG affiliation (link 5-3(1)). For example, a study by Hoskisson, Cannella, Tihanyi, and Faraci (2004) proposes that firms undergo restructuring in response to country development, deregulation, and increased competition. They find that this response of restructuring to country development is much stronger among firms affiliated to FBGs as compared to independent firms, whereas the same response to deregulation and competition is stronger for independent firms. Another challenge that emerging economy firms face with increasing liberalization of borders is new competition from foreign MNEs. Dau, Ayyagari, and Spencer (2015) propose and find in the Indian context that firms affiliated to FBGs are more likely to respond to this threat and that within FBGs, firms that are professionally managed and hold more central positions in the groups (as measured by director networks) are more likely to respond. Exploring the link between outside directors and governance variables among Korean firms, Min (2016) finds that FBG affiliation has a positive moderating effect on regulatory compliance on financial leverage while restraining a firm's growth tendencies. Ray and Ray Chaudhuri (2018) report that dependence on fungible resources for sustainability orientation is found to be less among FBG firms. Two studies conducted using post-reforms data on Indian firms (Manikutty, 2000; Gopal, Manikandan, & Ramachandran, 2021) arrive at a similar conclusion that reforms led to reduced levels of unrelated diversification among FBGs. Examining environmental impacts on innovation, Bu and Cuervo-Cazurra (2020) propose that informal entrepreneurial settings impose costs on innovation even when informally created firms transition to more formal enterprises. But in a cross-country study involving firms from 71 emerging economies, they find that the persistence of informality costs on innovation are lower in MNEs and firms owned by FBGs, whereas they are higher in state-owned enterprises.

We found another seven studies that used broader FBG variables instead of just an affiliation dummy for examining the moderating effect of the environment (link 2-3(5)). In a study of firms in Korea and Taiwan during 1981–1995, in which Mahmood and Mitchell (2004) report an inverted-U relationship between the FBG market share in an industry and innovation, they also find that this effect is influenced by differences in the institutional environment between the two countries. In another study that establishes the contingent effect of the environment, the positive effect on innovation due to buyer-supplier tie density within an FBG is found to diminish with development of market environment in Taiwan (Mahmood et al., 2013). Examining how FBGs cope with institutional change during market-oriented transitions in Taiwan between 1986 and 1998, Chung and Luo (2008b) find that second-generation leaders, particularly those with management education from the United States, are able to reduce family presence in management and also are able to divest of unrelated businesses. Exploiting the context of political and economic liberalization in Taiwan between 1986 and 1998, Mahmood, Chung, and Mitchell (2017a) investigate and find that formal position interlocks with dominant party or senior government officials provide greatest benefits in a closed political-economic system, whereas informal social ties to a wider range of political actors, particularly legislators, provide greater benefits as the system becomes more open. Overall, the empirical evidence for these links seems to suggest that some of the FBG-related sources of strategic advantages are contingent upon the environment though there is a need to dig deeper and pin down the specific institutions with which they have a complementary and substitutive effects (for example, Chittoor et al., 2015b). Moreover, most of these studies, in particular those representing the link 5-3(1), clearly show evidence in support of the superior ability of FBGs to adapt and cope with market reforms and changes in their institutional environments.

Influence of Strategic Factors on Financial Performance (Figure 1, link 3-4(1); Table 1, panel D)

Why some firms perform better than others is the core question that binds strategy as a field, and the variables that help explain the heterogeneity in firm performance are termed strategic. Whether the affiliation of a firm to an FBG changes the prevailing strategy explanations (links 3-4(1) and 3-4(2) 9 ) proved to be a fertile ground for investigation for strategy scholars. For example, the prevailing well-accepted position on the negative consequences of unrelated diversification required revisiting given that many successful FBGs are highly diversified. We found 14 studies examining such links, with 12 papers representing the link 3-4(1) alone.

Examining the diversification-performance relationship, Chakrabarti, Singh, and Mahmood (2007) find that diversification improves performance for FBG firms only in the less-developed institutional environments, and it hurts firm performance in more developed environments. When it comes to the effect of internationalization on firm performance, two studies (Gaur & Delios, 2015, for international diversification; Gubbi & Elango, 2016, for cross-border acquisitions) find a positive moderating effect of FBG affiliation. In a more nuanced study of internationalization, Gaur, Pattnaik, Singh, and Lee (2019) find that FBG affiliation positively moderates the relationship between internalization (as measured by intersubsidiary sales and parent country national staffing) and subsidiary survival. Furthermore, they find that the size of the FBG and its degree of diversification enhances this effect even more (link 3-4(2)). Even though these studies indicate a strong positive FBG effect on outward (product-market) internationalization, when it comes to inward internationalization, Elia, Munjal, and Scalera (2020) find that FBG firms derive less benefit from inward foreign technology licenses as compared to nonaffiliated firms in a sample of Indian firms. In an interesting study that examines stock market reaction to corporate crimes in Korea, Song and Han (2017) find a negative effect that is quite intuitive but also find that the negative effect is significantly less for chaebol-affiliated firms; they surmise the reasons for it could be both positive (better reputation) or negative (crime by chaebols is quite expected). As many as six studies in the link 3-4(1) examine more deeply concerns related to tunneling (expropriation of minority shareholders by the dominant shareholders) in FBGs. Two studies by Kang and coauthors (Bae, Kang, & Kim, 2002; Baek, Kang, & Lee, 2006) highlight the different ways of tunneling engaged by FBGs. Acquisitions seem to serve as one of the mechanisms in context of chaebols, as they find that acquisitions made by Korean chaebol firms did not create value for the focal firm but increased the wealth of controlling shareholders by creating value for other group firms (Bae et al., 2002). Another mechanism was the issuing of private securities, also in the context of chaebol, where offer prices in intragroup deals were set to benefit the controlling shareholders (Baek et al., 2006). Dividend payout is also used as an indirect route for tunnelling as Gopalan, Nanda, and Seru (2014) report in their study using Indian firms where controlling shareholders distributed dividends from cash-rich firms and used it to increase their investment in other affiliated firms. In a more recent study of 106 Taiwanese business groups, Yang and Schwarz (2016) find that group-level excess control exhibits an inverted U-shaped relationship with group performance thus corroborating similar findings earlier by Carney and Gedajlovic (2002). These appropriation concerns are reflected in the valuation of FBG firms as the valuation impact of family control is negative in contrast to the impact of independent directors or foreign investors (Douma, George, & Kabir, 2006; Choi, Park, & Yoo, 2007). In a study that explores causation in a reverse direction (link 4-3(2)), Chang (2003) shows that performance determines ownership structure but not vice versa and provides evidence that controlling shareholders use insider information to take direct and indirect equity stakes in profitable or promising firms and transfer profits to affiliates through intragroup trade. All these studies are pointers to the strong possibility of nepotistic orientation in FBGs as argued recently by Chen et al. (2021). Although family ownership and control confers benefits such as long-term orientation and stewardship behaviors as argued by SEW scholars, future research must aim to identify conditions when negatives such as nepotism and tunneling could predominate.

Influence of Organizational Factors (Figure 1 links connecting box 6; Table 1, panel E 10 )

In addition to the intra- and inter-FBG heterogeneity factors, standalone organizational factors (Figure 1, box 6) have also been found to influence the FBG effect. Our review found seven studies in which organizational factors moderate the FBG effect and another six studies highlighting their influence in other ways. The first simple influencing factors that come up in this category are the firm's age and size. In their investigation of how FBGs influence firms’ international search behavior in a sample of Indian firms, Gubbi et al. (2015) find that member firms that are more distant from the group's founding year (i.e., younger firms) have a negative impact and the authors attribute this to firms’ lower centrality (with older firms being more central to the group). On the other hand, Kumar et al. (2020) find that firms founded after economic liberalization in India pursue more aggressive internationalization by conducting their first cross-border acquisition faster. This can be attributed to a distinctly different imprinting environment for these younger firms. Firm size is another such organizational factor. Examining innovativeness in small and medium enterprises, Guzzini and Iacobucci (2014) not only find that FBG firms engage in higher R&D but also that this effect is higher for larger firms (after carefully controlling for the fact that FBG firms in general tend to be larger compared to unaffiliated firms). Three studies highlight an important influence of a firms’ listing in stock exchanges (Chittoor et al., 2015b; Kim, Pae, & Yoo, 2019; Mahmood et al., 2017b). Chittoor et al. (2015a) argue that accessing capital markets by listing in a stock exchange complements the internal market advantages of FBGs (in addition to offering benefits of external scrutiny) and find a positive effect on firm performance in a sample of Indian firms (link 1-4(6)). Mahmood et al. (2017b) also find a significant influence of firm listing in the context of Taiwanese firms. They find that centralization of equity ties enhances affiliate firm performance, but that this effect is weaker for the listed firms as they accrue additional advantages from outside the FBG. Although finding that public firms make more charitable contributions than private firms, Kim et al. (2019) also find this effect to be more pronounced in FBG firms. Another organizational factor that is found to have a significant influence in the context of family firms is the degree of professional management. In the study that explores how domestic firms respond to MNE threats in a sample of Indian firms discussed earlier, Dau et al. (2015) find that the likelihood of the response is positively influenced by the degree of professional management. Similarly, Yang and Schwarz (2016) too report that the negative effect of firm-level excess control on firm performance is reduced when the FBG is governed by professional managers. We also found four papers examining the moderating effect of FBG affiliation or FBG heterogeneity while studying the strategic consequences of organizational factors; some interesting examples include CEO succession in terms of insider versus outsider CEO in Chung and Luo (2013); social ties between CEOs and financial analysts in Chen, Chittoor, and Vissa (2015); and impact of family CEOs as compared to professional CEOs in the case of Chittoor, Aulakh, and Ray (2019). Overall, the studies in this stream signal the possibilities of interesting interaction effects between standalone organizational factors and group-level factors.

To summarize, Figure 1 provides a snapshot of all aspects of the FBG phenomenon and their interrelationships that prior empirical research has examined. In addition, online appendix Table A3 offers rich details of the conceptual frameworks used, the research design to test the frameworks, and the key findings of prior research. Table 1 collates studies by the theoretical lens used (note the predominant deployment of structural theories) and directionality of effects to provide insights on the theoretical variety used to study FBG phenomenon. Taken together, this allows for some broad conclusions about the state of FBG research and potential paths forward—to which we now turn.

Springboards for Future FBG Research Based on a Microfoundations Approach

Based on our review of the FBG literature (encapsulated in Figure 1 and Table 1), we develop three springboards to catalyze future FBG research. First, we advocate that FBG research reorients from its current reliance on structural modes of theorizing toward a more microfoundations-oriented approach. Extant FBG work predominantly utilizes structural frameworks—derived mainly from economics, although some studies use structural frameworks derived from sociology or political science. A microfoundations approach is both relevant, given its topical importance in the broader management field (cf. Devinney, 2013), and necessary in the FBG context given the disproportionate role of the controlling family (a relatively small group) in the business as founders, investors, board members, and operating executives. We develop a simple framework of theoretical “taking” and “giving” to think more systematically about broadening the palette for future FBG research's modes of theorizing, in ways consistent with such a microfoundations approach. We believe this reorientation will allow FBG scholars to look at thorny questions from multiple perspectives and build useful theoretical bridges with contiguous scholarly communities, thus leading to cumulation and consilience in the management fields’ overall knowledge base. Second, we zoom in and discuss a few specific theoretical frameworks, consistent with a microfoundations approach, to illustrate how their application could enrich our knowledge base on relationships already identified in prior FBG research. Finally, we propose ways in which future FBG research, again, consistent with a microfoundations approach, can broaden the range of phenomenon that it examines—in other words, expand Figure 1 by identifying important new outcomes in the context of FBGs and study their causes and consequences. We elaborate in the following sections.

Why Does FBG Research Need to Broaden Its Theoretical Palette?

As we can see from column 3 of Table 1, FBG research is predominantly monodisciplinary, with 76% of all links in Figure 1 studied using an economics lens. Importantly, these economics-grounded theoretical frameworks (such as the popular institutional voids approach as well as others such as PPA, internal capital markets, institutional economics, RBV, etc.) are structural theories. However, the inconsistency in prior empirical findings belies the promise of utilizing such a structural, monotheoretical approach. For example, evidence on the directionality of the main and moderated relationships between FBG affiliation and financial performance (the main 1-4 link moderated by (2) or (5) in Figure 1) is unclear. Out of the 18 studies using an economics lens to study this relationship, seven studies report a positive directionality, three report a negative directionality, two report mixed findings, five report contingent findings, and one study reports both a positive and a contingent effect (for different links). This begs the question of what are the hidden contingencies that seem to flip the directionality of the effects.

To respond to these and other empirical inconsistencies, FBG scholars turned to noneconomic theories. Thus, the only other study to examine the 1-4 link, Guillén (2000) uses a political science approach to propose that structural features of certain national institutional environments allow for FBGs to thrive by developing capabilities for repeated industry entry. Likewise, some scholars (e.g., Chung & Luo, 2013; Mahmood et al., 2017b) have examined other links utilizing sociology-based lenses—such as institutional theory and social networks theory to theorize FBG phenomenon. We note that these alternative frameworks from political science and sociology also utilize a structural mode of theorizing. Thus, although we see the tentative moves to using noneconomic lenses as a welcome step to match the complexity of theorizing to the complexity of the phenomenon, we suggest that FBG scholars need to go much further by actively diversifying their theoretical palette into more behavioral perspectives, consistent with the recent microfoundations movement in the broader management literature (Devinney, 2013). In essence, we advocate for picking modes of theorizing (within the sociology or political science perspectives) that provide consistent microfoundations. This is important because consistent microfoundations provide clear causal logics and well-defined aggregation rules for the micro-macro link. A consistent microfoundations-based approach can also serve as a base from which we can look at questions from different, novel perspectives. This will in turn, over time, help resolve inconsistent findings and lead to cumulation of knowledge across silos and thus grow the knowledge base of the field.

There are diverse views on what constitutes a consistent microfoundations-based approach to theorizing (cf. Devinney, 2013, for a quick summary of the alternative views). Given that much of FBG research constitutes an instance of organizational phenomena, we build on Greve (2013) and suggest that an appropriate microfoundation for organizational phenomenon is a behavioral strategy approach. Such an approach involves mechanisms that reduce to the top layer of emergent properties but go no further, which are consistent with individual humans’ actor-hood while also allowing for meso-level (and not necessarily only individual-actor level) explanations. With these criteria of microfoundation as a touchstone, we develop below a simple framework to think more systematically about broadening the palette for future FBG research's modes of theorizing.

A “Giving” and “Taking” Approach to Broaden FBG Research's Theoretical Palette

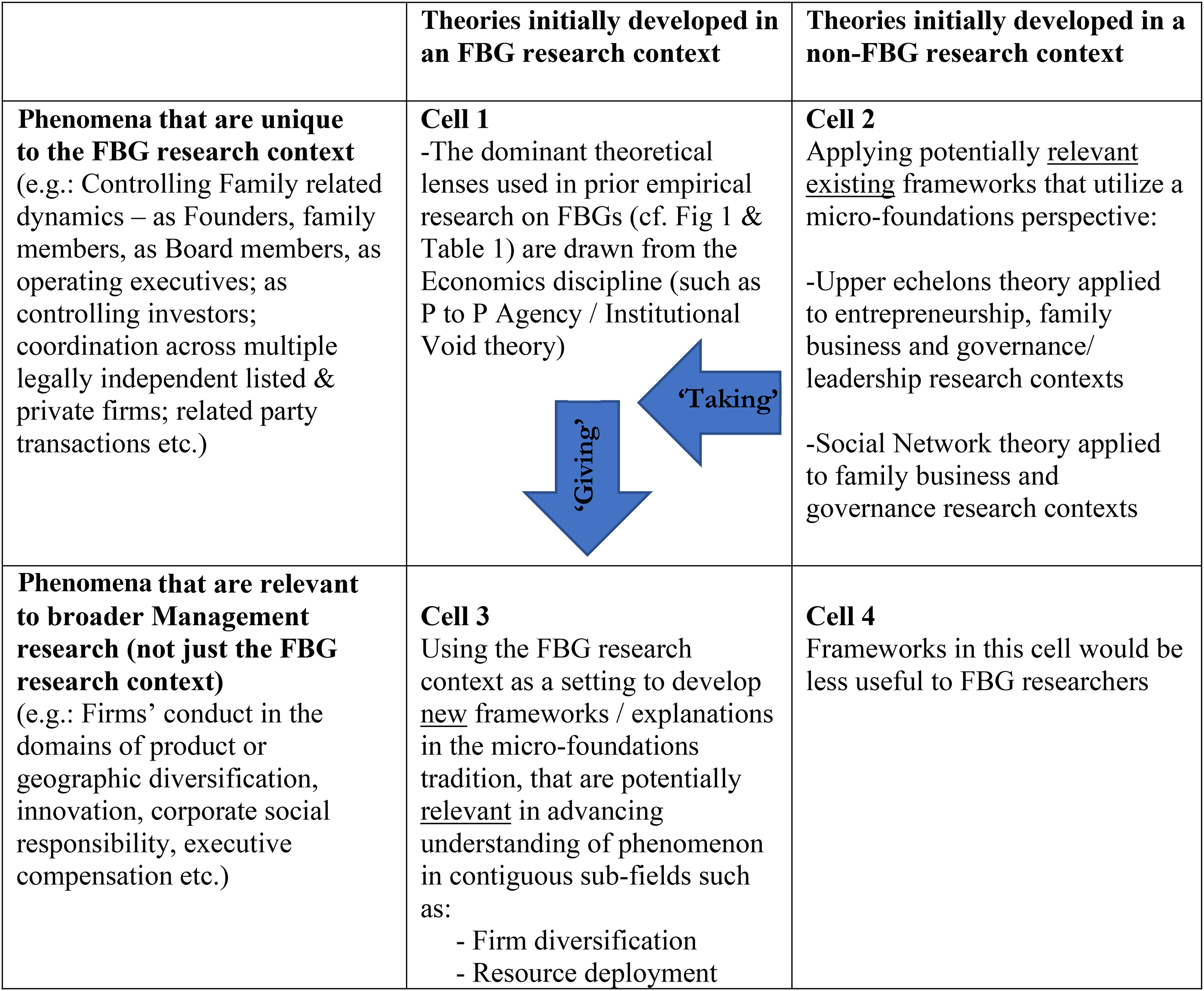

While Guillén (2000) developed novel theory ab-initio in the FBG research context to explain phenomenon that are unique to that context, we offer two other channels for increasing theoretical diversity in future FBG research, as we depict in a two-by-two matrix of Figure 2. One dimension in Figure 2 is whether a theory was initially developed in an FBG context (e.g., institutional voids theory was originally developed to explain unrelated diversification by FBGs in emerging economies) or in a non-FBG context (e.g., transaction cost economics was originally applied in management research to explain vertical integration decisions of large corporations in the United States). The other dimension is whether the phenomenon examined is unique to the FBG context or relevant for all firms. For example, phenomenon that involve issues around controlling family-related dynamics (as family members, as founders, board members, as operating executives, as controlling investors), coordination across multiple legally independent listed and private firms as well as related party transactions are unique to the FBG context. In contrast, phenomenon such as corporate behavior involving product or geographic diversification, innovation, corporate social responsibility, executive compensation, and so forth are applicable to all firms and not just FBGs.

Broadening the Theoretical Palette Associated With the FBG Research Context

Based on these two dimensions, we derive four cells as depicted in Figure 2. Cell 1 consists of theories initially developed in an FBG research context and applied to phenomenon unique to the FBG context. Examples of cell 1 frameworks include the p-p agency (Young, Peng, Ahlstrom, Bruton, & Jiang, 2008) and institutional void theory (Khanna & Palepu, 1997), which are dominant theoretical lenses and have been widely used in prior empirical research on FBGs (cf. Figure 1 and Table 1). Cell 4, on the diagonal side, includes theories initially developed in a non-FBG research context (such as real option theory) and applied to explain phenomena (such as investment flexibility) that are applicable to all types of firms and not just FBGs. Cell 4 theories are less relevant for this paper.

We focus on cell 2 and cell 3 of Figure 2, which are two channels that could help advance future FBG research. Cell 2 involves taking an existing microfoundational framework that was originally developed in a non-FBG context and applying that framework to a phenomenon that is specific to the FBG context (i.e., a “taking approach”). Adapting such potentially relevant microfoundational, behavioral strategy theories to provide novel explanations for FBG phenomenon could reinvigorate both FBG research and the theoretical framework in question. On the other hand, cell 3 presents an alternate channel to theoretical diversity by leveraging the FBG context to develop new microfoundational, behavioral strategy frameworks that could give insights to researchers studying relevant phenomenon in a broad array of other management subfields (i.e., a “giving approach”). These new “giving” frameworks will not only provide explanations that advance FBG scholarship but will also constitute novel explanations for important outcomes relevant for all firms and thus be of interest to a broader array of management scholars. Hence, this alternate channel constitutes an opportunity for FBG research to contribute or “give” to the broader pool of microfoundational frameworks available to management scholarship.

Broadening the theoretical palette of FBG research through these two channels shown in Figure 2, in ways that pay careful heed to the compatibility of fundamental assumptions (Shaw, Tangirala, Vissa, & Rodell, 2018), is useful in two ways. First, the resultant microfoundations-based theory is more likely to be elegant, nuanced, and generative because it is likely to appropriately match the complexity of the FBG research context. Second, the resultant “flow” of microfoundations-based frameworks in both directions will better integrate FBG research with contiguous research areas in the management field. In the next section, we propose candidate microfoundations-based frameworks along both channels and broad research questions drawn from those frameworks that could add salubrious theoretical variety to FBG research and enhance the intellectual integration of FBG research within the broader management field.

Leveraging Theoretical Diversity to Enrich Relationships Identified in Prior FBG Research

We examine microfoundations-based frameworks from cell 2 first and then move to cell 3. Our intent here is to be illustrative rather than exhaustively identify all frameworks that fit our criteria. Furthermore, the approach we advocate here is already starting to get implemented by multiple teams of FBG scholars—which we explicitly identify in the following sections. We believe that identifying and naming this movement and placing it within a broader framework opens new opportunities that tend to be overlooked when different communities of scholars who study contiguous phenomenon or theories do so in separate silos. It is thus an opportunity for fertile comparison and dialogue within and beyond the FBG scholarly community.

Illustrative examples of Cell 2 theories that could be relevant for the FBG research context

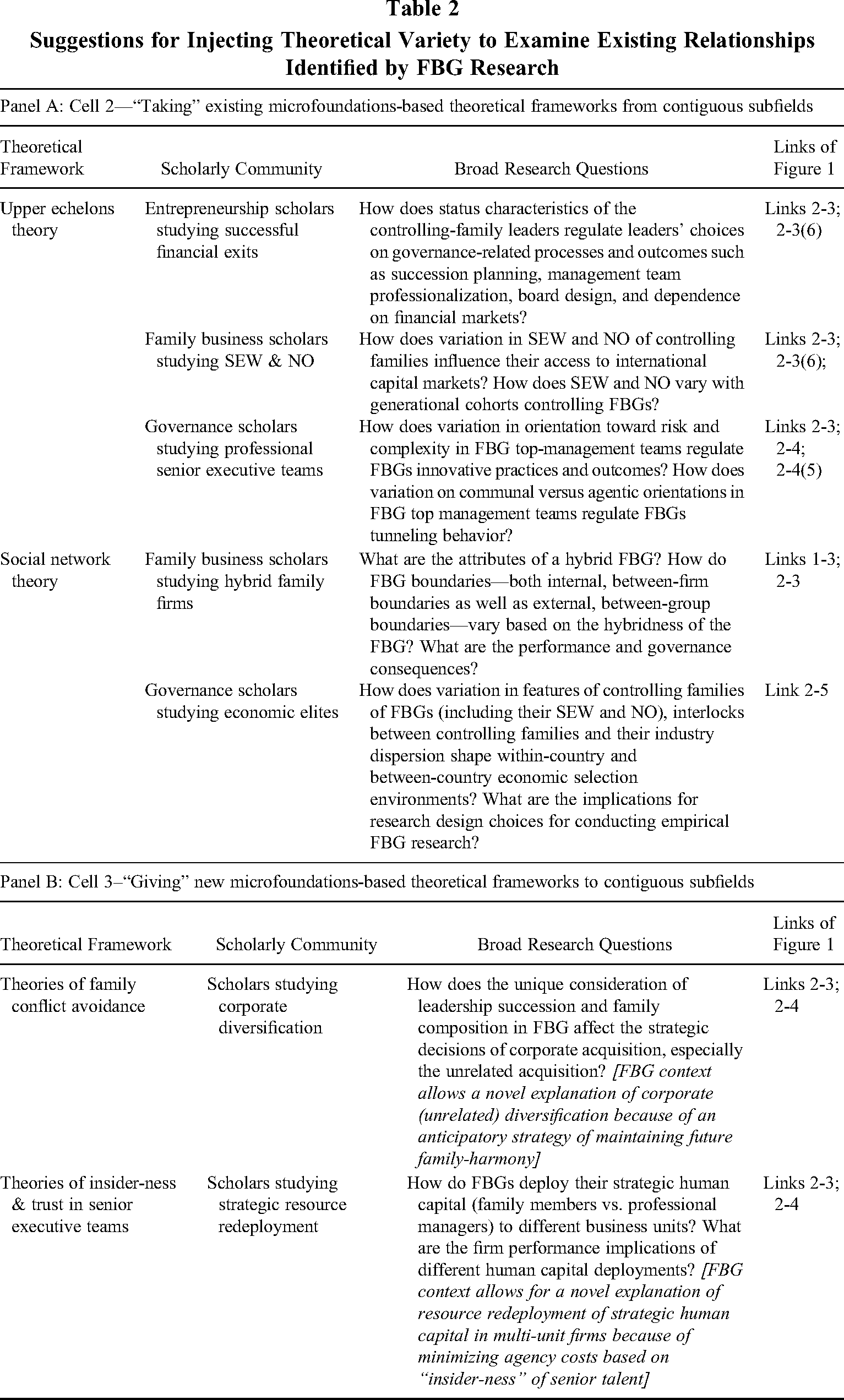

The two illustrative cell 2 microfoundations-based theories that we believe scholars can usefully leverage to enrich future FBG studies are upper echelons theory (UET) and social network theory (SNT). These two prominent theories are used by multiple contiguous scholarly communities as outlined in panel A, column 2 of Table 2. We briefly outline each theory and the relevant contiguous scholarly communities that have applied these theories, and we propose ways in which FBG research can leverage these frameworks to advance the field.

Suggestions for Injecting Theoretical Variety to Examine Existing Relationships Identified by FBG Research

Leveraging Upper Echelon Theory (UET) for FBG research

Since Hambrick and Mason (1984) published their seminal work, UET has been applied in various empirical contexts (Hambrick, 2007). UET research tries to understand how organizational leaders, such as CEOs and top management teams, use their own perspectives to screen, filter, and interpret information in forming the basis of “constructed reality” in their decision-making (Liu, Fisher, & Chen, 2018). Firm choices and outcomes are seen as influenced by these executives’ background, psychological orientation, and values, and therefore organizations become a reflection of their leaders (Hambrick & Mason, 1984). We focus on the successful application of UET in three contiguous areas relevant for FBG research: (1) entrepreneurship scholars studying successful financial exits; (2) family business scholars studying socioemotional wealth (SEW) and nepotistic orientation (NO) of controlling families; and (3) governance and leadership scholars studying professional senior executive teams. We outline how frameworks from these three areas could be leveraged to provide impetus for microfoundations-based theorizing in the FBG research context.

(1) Entrepreneurship research: Kinger Hans and Vissa (2022) use a UET perspective to theorize how successful entrepreneurs’ ascribed and achieved status characteristics (Ridgeway, 1991) regulate their propensity to engage in corporate philanthropy after achieving success. Their framework suggests that successful first-generation founders’ preferences and choices are regulated by their social backgrounds prior to achieving success in ways that may matter for other corporate social and economic outcomes. We propose that this framework of founders’ prior ascribed (such as gender, social class, ethnicity, etc.) and achieved (such as educational attainment, work experiences, industry exposure, etc.) status characteristics influencing firms’ socioeconomic outcomes could be extended to the FBG research context. For example, future FBG research can examine how these status characteristics of the controlling-family leaders, across generational cohorts, regulates leaders’ choices on crucial governance-related processes and outcomes such as succession planning—particularly the role of gender, management team professionalization, board design, and dependence on public and private financial markets.