Abstract

This study offers a comprehensive and multidisciplinary review of the research on the antecedents of investor valuation in the management, accounting, and finance literature. Despite the growing recognition of the importance of investors and financial markets, our current understanding of the factors that drive investor valuation remains incomplete. To address this gap, we classify the existing literature on investor valuation into three perspectives: social, cognitive, and economic. The social perspective examines how social forces, such as institutional norms and pressure, shape investor valuation. The cognitive perspective focuses on the psychological underpinnings of investors’ valuation decisions, while the economic perspective emphasizes how investors determine the value of firms through rational cost-and-benefit calculations. This review compares the research on investor valuation in the management literature to that in the accounting and finance literature, identifying gaps in the management literature and discussing emerging trends that may influence investor valuation. The review also proposes an agenda for future research. In conclusion, this study illuminates the intricate and multifaceted nature of investor valuation, as well as the underlying factors that influence it.

Investors in a firm are individuals or organizations that provide capital to a firm with the expectation of receiving financial returns. There are many different types of investors. In this study, investors broadly refer to the following: individuals who trade securities (i.e., retail investors); professional organizations that trade securities on behalf of their clients (i.e., institutional investors); and financial intermediaries such as venture capital (VC) firms and angel investors, which provide capital to young startups. Since financial capital is the lifeblood that supports firms’ survival and growth, understanding those factors that determine investor valuations of a firm is undeniably important. Indeed, the study of investor valuation has gained considerable momentum over the last 3 decades. The number of publications in the management field that use investor valuation as a central construct follows a classic hockey-stick shape, with a sharp upward bend occurring around 2008. While recent years have seen some progress in understanding the factors that drive investor valuation, researchers from diverse literatures have mostly approached this topic through discipline-specific lenses. This highlights the pressing need for a comprehensive and multidisciplinary approach to integrate our knowledge of investor valuation.

This review of investor valuation research is anchored in the management literature but will also integrate recent developments in accounting and finance. It seeks to contribute to the existing literature in three ways. First, existing reviews related to investors tend to place greater emphasis on how various types of investors, such as institutional investors and activist investors, affect the decisions and actions of firms (Boyd & Solarino, 2016; Connelly, Hoskisson, Tihanyi, & Certo, 2010). For instance, Boyd and Solarino (2016) explored how various forms of corporate ownership affect firm outcomes and summarized a wealth of contingencies that may moderate the ways in which different owners influence firms. Connelly et al. (2010) offered an in-depth review of how the strategies, performance, and governance of firms can be influenced by the motivation of, and influence tactics used by, different owners. Although Connelly et al. (2010) touched upon how firm performance and firm attributes may act as signals to influence investors’ ownership decisions, they kept this discussion very brief. In contrast, we offer a review of how firm attributes, actions, and communications affect investor valuation from social, cognitive, and economic perspectives. Signaling is only one stream of research covered under the economic perspective of our review. Goranova and Ryan (2014) integrated insights from the financial and social activism research to identify the antecedents and consequences of shareholder activism. They also discussed stock market reactions to shareholder activism prior to 2012, which is one of the antecedents of investor valuation we will cover. Yet, our review focuses on more recent studies published in the accounting and finance literature after 2012. In summary, while previous reviews offer rich insights regarding how different types of owners affect firm behavior and outcomes, we nonetheless lack a systematic understanding of the determinants of investor valuation. To fill this research gap, after combing through 435 articles that examine the determinants of investor valuation, we categorize them into three perspectives: investors as social actors, investors as cognitive analyzers, and investors as economic agents.

Second, one important feature of the investor valuation literature is the plurality of theoretical perspectives. Compared with existing reviews, which primarily organized their discussions based on specific variables and relationships, our paper categorizes the literature based on different theoretical perspectives scholars employed to study investor valuation. For scholars who would like to contribute to this line of research, having a holistic view of the entire literature based on different theoretical perspectives is pivotal. Accomplishing this will help scholars better understand the theoretical mechanisms that drive the empirical findings within each perspective. More importantly, it will also help scholars to identify any imbalances in the research across different perspectives; discover cross-fertilization opportunities among different perspectives; and accord greater attention to the boundary conditions of studies within each perspective.

Third, an increasing number of management studies have begun to draw insights from the accounting and finance literature to better understand investor valuation. Yet, limited effort has been made to integrate theoretical insights and empirical findings from these disciplines to identify research gaps and suggest new directions for management research on investor valuation. In contrast, we compare investor valuation research in the management field with that in the accounting and finance fields based upon social, cognitive, and economic perspectives (see Figure 1). Consequently, we can recognize promising avenues for management research, both in terms of theoretical and empirical approaches.

Synthesis of Strategy, Accounting and Finance Research on Investor Valuation

Identifying the Relevant Literature

We conducted an extensive review of published works on investor evaluation. First, we searched the EBSCO database for relevant studies in management. Specifically, we searched for investor-related keywords (i.e., investor, shareholder, stockholder, venture capitalist, stock market) in the title, keywords, and abstract of articles published by the Financial Times’ Top 50 Journals in the management and entrepreneurship area (Academy of Management Journal, Academy of Management Review, Administrative Science Quarterly, Strategic Management Journal, Management Science, Organization Science, Journal of Management, Journal of Management Studies, Strategic Entrepreneurship Journal, Entrepreneurship Theory and Practice, Journal of Business Venturing, and Organization Studies).

Additionally, we searched the EBSCO database for relevant articles in accounting and finance. Studies devoted to investor valuation in accounting and finance are voluminous. To reflect the current state of the literature, we focused on articles published in the last 10 years (2012–2021 inclusive). Moreover, we focused on studies that accorded specific attention to the impact of firm attributes or behaviors on investor valuation, as opposed to studies that focused on the determinants of personal financing decisions (e.g., household debt), public financing decisions (e.g., sovereign debt, government bond holdings), and firms’ accounting policies, practices, and information. Using these two criteria, we obtained all of the studies published in the four leading finance journals (Journal of Finance, Journal of Financial Economics, Journal of Financial & Quantitative Analysis, and Review of Financial Studies) and the three leading accounting journals (Journal of Accounting Research, The Accounting Review, and Journal of Accounting and Economics), which included at least one investor-related keyword, as well as one firm-related keyword (i.e., firm, organization, corporation, company, enterprise, venture), in the abstract.

Next, we reviewed each article for relevance and excluded three sets of studies. First, because we focus on investor valuation as the dependent variable, we excluded studies that used investor valuation as the independent variable to examine its influence on firms and managers. Second, by definition, investor valuation means the act or process of determining the value and worth of a firm by investors. We excluded studies that used firm performance (such as return on assets, return on equity) and other non-valuation-related outcome variables (such as a firm's cost of capital and analyst forecast accuracy) as dependent variables. Third, we excluded studies that mentioned investor-related keywords only in fleeting terms and did not examine how firm strategy and behavior directly influence investor valuation.

Several metrics have been used by management scholars to assess investor valuation. Our review included studies using five commonly employed metrics of investor valuation: stock returns, Tobin's Q, IPO price premium, pre-money valuation, funding raised, and probability of investment. First, most management scholars have used changes in stock prices (i.e., abnormal stock returns) to capture investors’ valuations of a firm (e.g., Bettis & Weeks, 1987; Godfrey, Merrill, & Hansen, 2009). Abnormal stock return is a strong measure of investor valuation when it is used to study the impact of unexpected corporate decisions on the market value of a firm. Second, Tobin's Q, the ratio of a firm's market value of assets to the replacement value of assets, is another measure used by some scholars to capture investors’ perceived value of a firm's assets, such as innovation and reputation (e.g., Deb, David, & O’Brien, 2017; DesJardine & Durand, 2020). Third, in the initial public offering (IPO) setting, some scholars used the price premium (i.e., offer price beyond book value) investors paid for a firm at IPO to represent investors’ perceived future value of the firm (e.g., Bell, Filatotchev, & Aguilera, 2014; Certo, Daily, Cannella, & Dalton, 2003). Fourth, a few studies have used a firm's pre-money market valuation (i.e., the value of a firm before it goes public or receives external funding) to capture investors’ valuation (Gulati & Higgins, 2003; Stuart, Hoang, & Hybels, 1999). Compared with IPO price premium, which only considers changes in asset price, pre-money valuation takes into account changes in share price, as well as the number of shares offered in the IPO. Finally, in the context of entrepreneurial financing, some scholars have used the total amount of funding raised (e.g., Petkova, Rindova, & Gupta, 2013) and the probability of investment to estimate how venture capital and angel investors value a nascent venture (e.g., Chen, Yao, & Kotha, 2009).

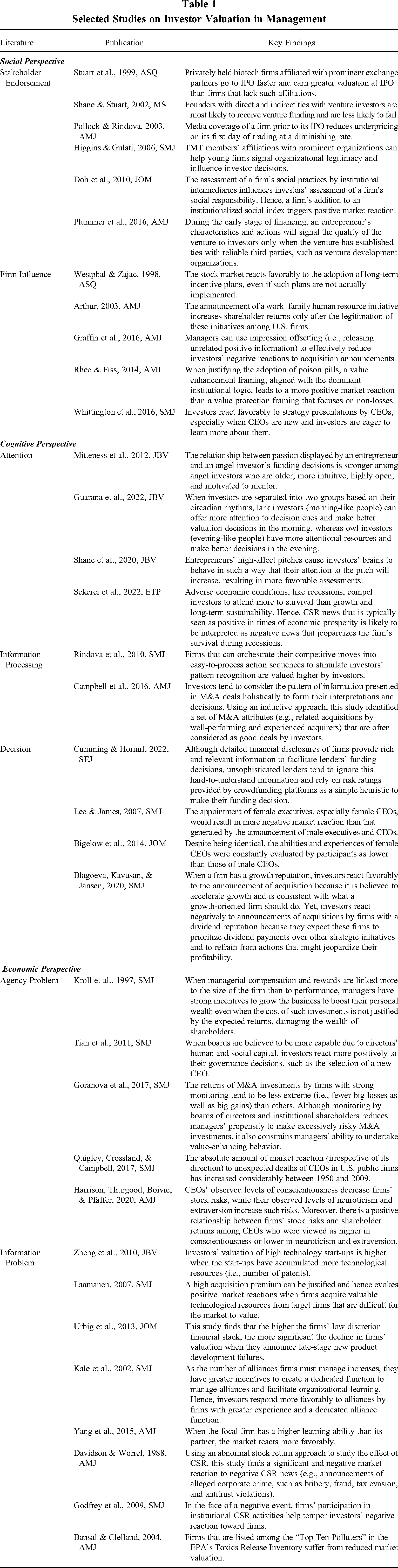

Finally, to ensure the inclusion of the most recent studies, we searched the websites of all journals previously identified for forthcoming papers on investor valuation and identified 29 additional studies. Hence, our final sample consists of 435 articles: 204 in management, 140 in finance, and 91 in accounting. Tables 1 and 2 summarize some of the key studies from these three disciplines.

Selected Studies on Investor Valuation in Management

Selected Studies on Investor Valuation in Accounting and Finance

Categorizating the Relevant Literature

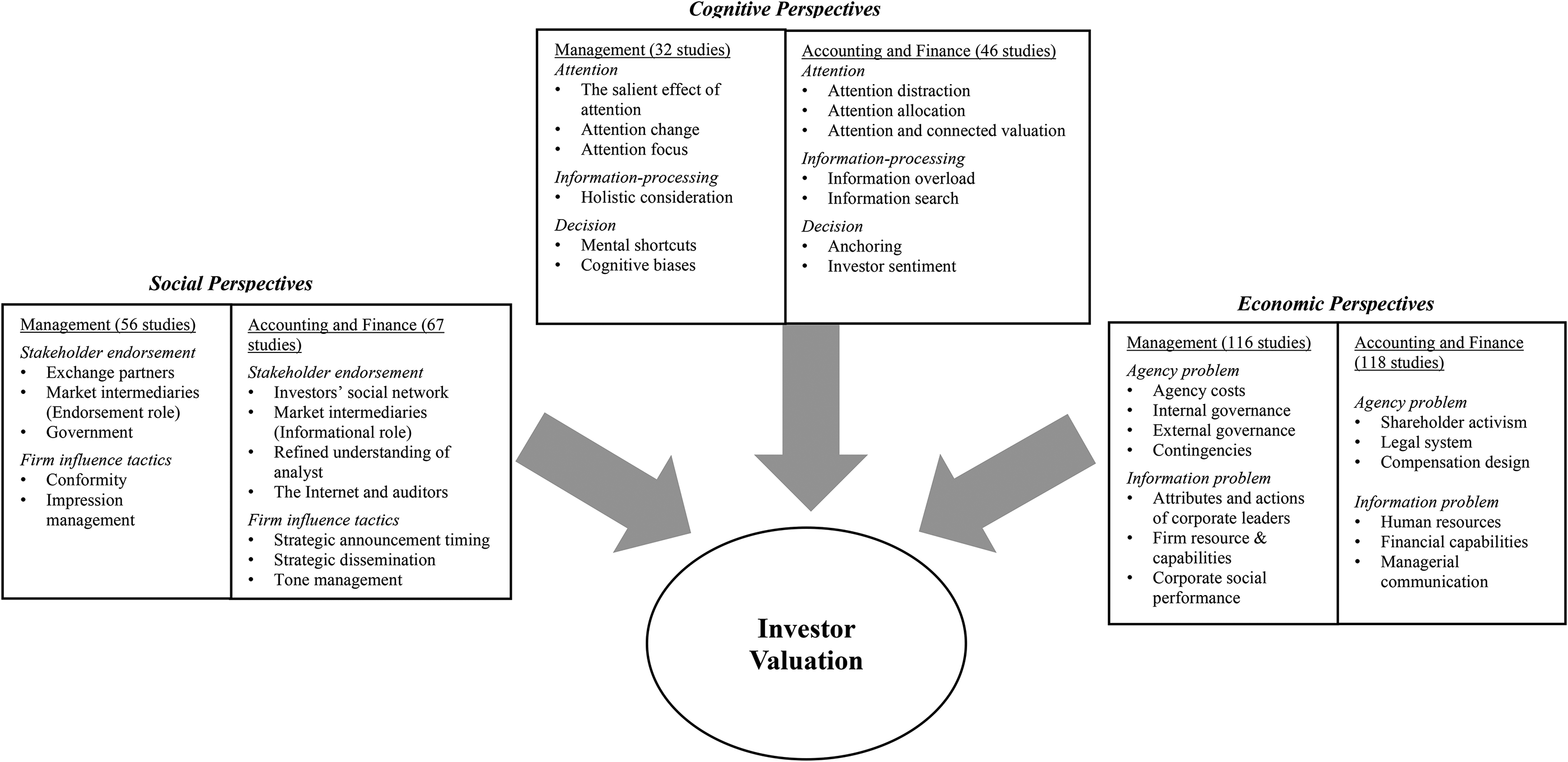

We followed three steps to categorize the 435 articles into three perspectives. First, based on the theories identified or the mechanisms used, we classified all of the articles into social, cognitive, and economic perspectives. 1 The perspective of investors as social actors strives to understand how investor valuation is shaped by social forces (e.g., institutional norms and pressure). These studies emphasized organizations’ need for legitimacy—that is, to be perceived as “desirable, proper, and appropriate” by broad stakeholder audiences (Suchman, 1995: 574) to gain investors’ support. They typically draw on theories with a sociological underpinning, such as the institutional theory, the social network theory, and the impression management theory. The perspective of investors as cognitive analyzers focuses on the psychological underpinnings of investors’ valuation decisions. These studies view investors as boundedly rational decision makers who are limited in their cognitive capacity to process all available information before rendering judgments. As a result, these studies focus on factors that influence investors’ cognitive processes. Commonly used theories in this literature are the information processing theory, the behavioral decision theory, and the social cognitive theory. The perspective of investors as economic agents emphasizes how investors determine the value of firms based on rational cost-and-benefit calculations of how firm behavior enhances or destroys shareholder values. These studies typically draw on theories derived from an economic tradition, such as the agency theory, the transaction cost theory, and the signaling theory.

Second, within each perspective, we further divided the corresponding literature into subcategories. We classified studies in the social perspective into research on stakeholders’ endorsement and firms’ influence tactics. These represent the two established methods through which firms can gain legitimacy. Studies of stakeholders’ endorsement emphasize how affiliations, support, and certification from high-status exchange partners and market intermediaries may help firms gain legitimacy and achieve a higher valuation. Studies of firms’ influence tactics, on the other hand, focus on how firms can gain legitimacy and reach a better valuation through conformity and impression management. Based on different types of cognitive processes examined, we classified studies in the cognitive perspective category into research on attention, information-processing, and decision. Studies of attention focus on how investors’ valuation of firms is driven by the type of information that garners the attention of investors. Studies of information-processing focus on how investors’ valuation is related to their ability to process and comprehend information provided by the firm. Studies of decision-making place greater focus on the mental shortcuts and cognitive biases that influence investors’ valuation decisions. Finally, based on the two fundamental issues faced by investors when they evaluate the value-creation potential of a firm and its activities, we classified studies in the economic perspective into research on agency problem and information problem. Studies of agency problem focus on how investors react positively to approaches taken by firms to mitigate agency problems and negatively to activities that elevate investors’ concerns about agency problems. Studies of information problem focus on how investors’ reactions to firm activities are dependent upon whether such activities increase or decrease the level of information asymmetry between investors and managers.

The review proceeds as follows. Beginning with the next section, we review the investor valuation literature under each of the three perspectives, as delineated above. Each perspective entails a summary of the principal findings from the management literature. Afterward, we discuss how accounting and finance scholars study the topic, highlighting the dissimilarities between their approach and that of management scholars. Lastly, we provide fresh avenues for research opportunities aimed at management scholars.

Investors as Social Actors

Taking a sociological approach, a large body of management research views investors and organizations as social actors embedded in an institutional environment. Institutions represent the “formal and informal rules, monitoring and enforcement mechanisms, and systems of meaning that define the context within which investors and organizations operate and interact with each other” (Campbell, 2004: 1). Research adopting a social perspective has placed considerable emphasis on firms’ quest for legitimacy to enhance investor valuation. Based on different methods firms can use to gain legitimacy, we categorize this perspective into research on stakeholders’ endorsement and firms’ influence tactics.

Stakeholders’ Endorsement

Gaining legitimacy in the eyes of investors can be facilitated through support from external stakeholders, including exchange partners, market intermediaries, and government. For nascent ventures with limited track records, previous research has highlighted the importance of social structures in business relationships as a crucial factor in attracting potential investors. More specifically, nascent ventures “endorsed” by prominent exchange partners (e.g., investors, underwriters, alliance partners) will earn a greater valuation than otherwise comparable firms that lack prominent associates (e.g., Gulati & Higgins, 2003; Plummer, Allison, & Connelly, 2016; Stuart et al., 1999). For example, Stuart et al. (1999) found that connections between nascent ventures and prominent alliance partners and equity investors can increase ventures’ market valuation at an IPO. Chahine, Filatotchev, Bruton, and Wright (2021) found that the reputation of venture capital firms associated with an IPO firm increases the valuation of the firm in the process of an IPO. When interorganizational connections are not yet established, research has shown that the personal ties between entrepreneurs and prominent investors can also serve as an endorsement, thereby increasing investors’ valuation of a firm (e.g., Ko & McKelvie, 2018; Shane & Cable, 2002; Shane & Stuart, 2002; Wuebker, Hampl, & Wüstenhagen, 2015).

Market intermediaries can also play a significant role in legitimizing organizations. Investors often face considerable difficulties in accurately assessing the value of a firm. As expert bodies that have gained substantial legitimacy, market intermediaries disseminate information and conduct evaluations to facilitate investors’ decision-making. They influence investors’ valuation of firms by directing investors’ attention and by signaling firms’ qualifications (Zuckerman, 1999). Three types of market intermediaries have been commonly studied in the management literature: media, financial analyst, and rating organizations. Journalists disseminate their perceptions and opinions on a large scale and are seen as authoritative sources of information (Deephouse, 2000). Since what the media chooses to cover is a key factor in determining what investors pay attention to, are familiar with, and value more, studies have shown that in the context of an IPO, investors accord greater attention to firms that receive more media coverage (e.g., King & Soule, 2007; Pollock & Rindova, 2003; Pollock, Rindova, & Maggitti, 2008). This literature also highlighted the media's framing power. Studies have shown that investors evaluate firms more positively when the media portrays those firms in a positive light during an IPO (e.g., Pollock & Rindova, 2003; Pollock et al., 2008).

Financial analyst is another type of market intermediary that is found to exert considerable influence over investors (e.g., Feldman, Gilson, & Villalonga, 2014; Luo, Wang, Raithel, & Zheng, 2015; Zuckerman, 1999). Since the nature of analysts’ work is to research firms and disseminate their professional assessment to facilitate investors’ valuations, their superior knowledge establishes their credibility and legitimacy. Research has shown that when analysts who specialize in a firm's industry deliberately choose not to cover the firm, this lack of coverage will lead investors to discount the firm's stock (e.g., Zuckerman, 1999). Other studies have found that firms which pursue unusual strategies that may heighten analysts’ costs of collecting and analyzing information to assess the firm's future value will receive less coverage and lower valuations (e.g., Litov, Moreton, & Zenger, 2012).

Rating organizations are well-recognized third-party agencies that monitor and assess firm activities and performance within a given domain. They provide certification, accreditation, and other similar designations to firms that attain certain standards (Desai, 2018). Existing research on rating organizations has yielded mixed findings. Some studies have demonstrated that when a firm is added to (deleted from) an institutionalized social index, investors’ valuations of these firms tend to rise (fall; e.g., Awaysheh, Heron, Perry, & Wilson, 2020; Doh, Howton, Howton, & Siegel, 2010; Ramchander, Schwebach, & Staking, 2012). However, other studies were unable to document such a legitimacy-conferring effect. For instance, using investor reactions to firms from 27 countries over 17 years that were added, deleted, or continued on the Dow Jones Social Index World, Hawn, Chatterji, and Mitchell (2018) demonstrated that investors’ response to endorsement by social index is limited and, on average, investors appear to punish rather than reward firms that are added to or continued on the index. Similarly, Lewis and Carlos (2019) found that among lower-ranked firms that barely meet the criteria of a ranking, gaining inclusion in a prominent ranking may trigger negative reactions from investors, since a categorical comparison may enhance the salience of the performance disparity between lower-ranked firms and higher-ranked firms.

Additionally, government and the regulatory environment of a firm's country of origin have been suggested as another critical source of organizational legitimacy that can influence investor valuation (e.g., Bell et al., 2014; Surroca, Aguilera, Desender, & Tribó, 2020). For instance, Bell et al. (2014) showed that the effect of a foreign IPO's governance mechanisms on investor valuation is contingent upon the strength of minority shareholder protection in the firm's home country. Moreover, in the United Kingdom, where interlocks between CEOs and directors are common, investors are likely to ascribe greater value to such connections than those in the United States, where such connections are strictly regulated (Filatotchev, Chahine, & Bruton, 2018).

Above, we have reviewed the research on stakeholders’ endorsement in the management literature. Research conducted in the fields of accounting and finance has affirmed the significance of reputable exchange partners and market intermediaries in endorsing companies (e.g., Borisov, Goldman, & Gupta, 2016; Brown & Huang, 2020). However, there exist notable distinctions in how these actors are examined in these two disciplines.

To begin with, management scholars have placed greater emphasis on how social networks of firms provide endorsements to sway investors’ valuations of them, while accounting and finance scholars are more intrigued by how investors’ own social networks affect their investment decisions (e.g., Han, Hirshleifer, & Walden, 2020; Heimer & Simon, 2015; Hong, Kubik, & Stein, 2004, 2005; Ivković & Weisbenner, 2007; Kaustia & Knüpfer, 2012). Since investment ideas can be transmitted from person to person, a number of studies have found that, regardless of whether they are professional or retail, investors tend to select stocks based on the choices of their friends and neighbors. For instance, Hong, Kubik, and Stein (2005) demonstrated that a mutual fund manager is more likely to buy (or sell) a particular stock if other managers in the same city are buying (or selling) the same stock. Ivković and Weisbenner (2007) also found that a 10% increase in purchases of stocks from an industry made by a household's neighbors is associated with an increase of 2% in the household's own purchases of stocks from that industry. Using rich data on investors’ trading history and communication, two recent studies identified investor bias in information transmission (i.e., investors tend to broadcast their investment successes while remaining silent after losses) as one of the mechanisms contributing to the neighbor effect (Han, Hirshleifer, & Walden, 2022; Lane, Lim, & Uzzi, 2020).

Additionally, in contrast to the view of media and analysts as institutional intermediaries that impart legitimacy to firms in the management literature, research in accounting and finance is more intently focused on their informational function (e.g., Bonsall, Green, & Muller, 2020; Bushee, Core, Guay, & Hamm, 2010; Drake, Guest, & Twedt, 2014; Fang & Peress, 2009). These studies revealed that greater media coverage increases investor informedness and reduces mispricing. Such an impact is primarily driven by the media's ability to help investors better understand the implications of accounting information. For instance, Bushee et al. (2010) found that greater media coverage of earnings announcements reduces information asymmetry among investors. Drake et al. (2014) documented that media coverage of earnings announcements influences investor valuation by mitigating cash flow mispricing (i.e., investors’ tendency to undervalue the cash flow component of earnings). Moreover, accounting and finance research has studied interactions among the objectives and incentives of managers, analysts, journalists, and other participants of information environment. For instance, Asay, Elliott, and Rennekamp (2017) found that when firms provide hard-to-understand disclosures, investors will incorporate more information provided by analysts and the media to inform their valuation judgments.

Furthermore, although the endorsement role of analysts is largely accepted in management research, accounting and finance research is still endeavoring to comprehend the impact of analyst coverage on investor valuation. For instance, using the closures and mergers of brokerage houses to identify changes in analyst coverage that are exogenous to corporate policies and performance, several studies found that firms which lost analyst coverage experienced a significant negative stock market reaction, and sophisticated investors such as hedge funds had to scale up information acquisition to make up for the loss of information (e.g., Chen, Kelly, & Wu, 2020b; Derrien & Kecskés, 2013; Ellul & Panayides, 2018; Mola, Rau, & Khorana, 2013). 2 Moreover, since analysts are individuals subject to the influence of decision fatigue, research has shown that investors react less strongly to revisions in analyst forecasts when analysts experiencing decision fatigue offer less accurate forecasts that herd toward consensus forecasts (Hirshleifer, Levi, Lourie, & Teoh, 2019). Finally, accounting and finance scholars have begun to explore how different types of analysts, such as buy-side analysts and governance analysts, uniquely influence investor valuation (Jung, Wong, & Zhang, 2018b; Lehmann, 2019).

Lastly, accounting and finance research has identified novel market intermediaries that have received little attention in management literature, such as the Internet and auditors (e.g., Antweiler & Frank, 2004; Bartov, Faurel, & Mohanram, 2018; Chen, De, Hu, & Hwang, 2014; Drake, Thornock, & Twedt, 2017; Grennan & Michaely, 2021; Huang, 2018; Lawrence, Ryans, Sun, & Laptev, 2018). Virtually any individual with Internet access can express opinions about firms. Given the rise of social media platforms and stock message boards, the Internet is becoming an enormous, constantly growing source of information for investors. Bartov et al. (2018) found that even after controlling for concurrent information from traditional media sources, the aggregate opinion from individual tweets on Twitter successfully predicts a firm's announcement returns. Since individuals posting information online have diverse backgrounds, expertise, and incentives, Drake et al. (2017) explored how the information provided by professional sources (e.g., Dow Jones Newswires) and unprofessional sources (e.g., nonfinancial websites and blogs) uniquely affects investors. They demonstrated that investors react positively to Internet coverage by professional sources and react negatively to coverage by unprofessional sources. More importantly, while coverage from professional sources increases the speed with which online news is incorporated into stock prices, evidence suggests that coverage from nonprofessional sources delays the speed of price formation. In addition to the Internet, accounting and finance scholars have demonstrated the informational role of auditors (e.g., Beneish, Billings, & Hodder, 2008; Elliott, Fanning, & Peecher, 2020). For instance, some studies have documented significant negative market reactions to the issuance of going-concern opinions by auditors, indicating that such opinions convey bad news to investors (Chen, Martin, & Wang, 2013a). Other studies have shown that investors ascribe value to firms that offer expanded auditor reports, particularly auditor commentary (Elliott et al., 2020).

Firms’ Influence Tactics

Studies of firms’ influence tactics focus on how firms can influence the perception and evaluation of investors with what they do and what they say. Two types of influence tactics are studied in the management literature, which we label as “conformity” and “impression management.” Conformity studies focus on how firms can gain legitimacy by conforming to institutional expectations. Specifically, prior research has demonstrated that investors react favorably to firms’ adoption of institutionalized policies, such as the adoption of work–family human resource initiatives (e.g., on-site child care and flexible work arrangements; Arthur, 2003) and long-term incentive plans (Westphal & Zajac, 1994, 1998). Research has also demonstrated that firms enjoy higher valuations when they engage in activities deemed desirable by stakeholders, such as corporate social responsibility activities and customer service. In contrast, firms’ valuation depreciates when they engage in socially undesirable activities, such as socially irresponsible actions (Bansal & Clelland, 2004; Davidson & Worrel, 1988; Godfrey et al., 2009; Ogden & Watson, 1999). For instance, according to Godfrey et al.'s (2009) study, a firm's involvement in CSR activities can produce moral capital that mitigates the punitive actions of investors during a negative event. Certainly there are caveats associated with conforming to institutional expectations. For example, some studies have found that managers who announce their adoption of an institutionalized practice in the middle of an industry wave may be viewed as blindly imitating the decisions of industry peers, triggering unfavorable stock market reactions (e.g., Brauer & Wiersema, 2012; Brauer & Zimmermann, 2019).

Impression management (IM) studies focus on managers’ efforts to create, maintain, protect, or even alter an image held by investors (Bolino, Kacmar, Turnley, & Gilstrap, 2008). Within this literature, two IM tactics have been identified as effective: the strategic use of noise, and the skillful management of communication content and style. On one hand, some scholars have studied the use of noise to safeguard an organization's image (e.g., Graffin, Carpenter, & Boivie, 2011; Graffin, Haleblian, & Kiley, 2016). For instance, Graffin et al. (2011) showed that organizations can influence investor reaction to controversial organizational events by strategically releasing other confounding information to minimize direct scrutiny. Graffin et al. (2016) introduced the concept of “impression offsetting” and demonstrated that when firms need to release bad news, they can strategically release unrelated good news simultaneously to distract investors from the bad news and mitigate the negative influence of such news.

On the other hand, prior research has explored how managers can shape investors’ perceptions by adroitly controlling the content and style of their public communications (e.g., Graffin et al., 2011, 2016; Pan, McNamara, Lee, Haleblian, & Devers, 2018; Whittington, Yakis-Douglas, & Ahn, 2016). In terms of communication content, some studies have found that self-serving attributions (i.e., taking credit for positive events while eschewing blame for negative events) used in letters to shareholders to justify organizational performance serve as an effective impression management tactic, which may lead to subsequent improvements in a firm's stock price (e.g., Salancik & Meindl, 1984; Staw, McKechnie, & Puffer, 1983). Other studies have found that stock market reactions to firms’ controversial actions will be more positive when managers use dominant institutional logic to legitimize such actions (e.g., Fiss & Zajac, 2006; Rhee & Fiss, 2014). For instance, Rhee and Fiss (2014) revealed that the stock market reacts more favorably when the adoption of “poison pills” is justified using a shareholder value enhancement framing that more closely aligns with the dominant institutional logic. In entrepreneurs’ investor pitch presentations, research has shown that entrepreneurs’ expressions of opinion conformity that affirm the opinions of investors, as well as self-promotion that highlights their abilities, increase the amount of funding they receive from angel investors (Sanchez-Ruiz, Wood, & Long-Ruboyianes, 2021).

In terms of communication style, prior research has shown that managers can build favorable impressions by managing the style of their communication (i.e., how they say things; e.g., Guo, Sengul, & Yu, 2021; König, Mammen, Luger, Fehn, & Enders, 2018; Pan et al., 2018; Whittington et al., 2016). For instance, Whittington et al. (2016) found that investors react favorably when newly appointed CEOs voluntarily offer strategy presentations to explain their broad plans for the future. Pan et al. (2018) revealed that managers’ use of concrete language makes them appear more competent and hence triggers a more positive market reaction. Furthermore, research on communication style has also underscored the differences in investors’ reactions to communicators with different characteristics. These studies revealed that the same content or style when used by communicators with different genders, races, sexual orientations, levels of charisma, and performance can result in different or even opposite reactions from investors. For instance, Sanchez-Ruiz et al. (2021) demonstrated that, although entrepreneurs’ use of flattery in investor pitches tends to trigger negative reactions from angel investors, the effect of flattery on funding becomes positive when such a style is used by entrepreneurs with high charisma or high performance. Moreover, Anglin, Wolfe, Short, McKenny, and Pidduck (2018) found that LGBTQ entrepreneurs generally raise more funds from crowdfunding investors when using language reflective of narcissistic characteristics (e.g., authority, superiority, exhibitionism, vanity, and self-sufficiency) than heterosexual entrepreneurs, while racial minorities (e.g., African American, Hispanic, Asian) underperform compared to Caucasian entrepreneurs when using narcissistic rhetoric. Zachary, Connelly, Payne, and Tribble (2021) found that investors’ reaction to unethical behavior is more negative for firms that present themselves as more virtuous than for those who do not make such claims. More interestingly, this study reveals the burden of impression management by showing that previous impression management efforts may set investors up for disappointment in the future.

Management scholars have examined the strategic use of noise and communication content and style to influence investor impression and valuation. In contrast, accounting and finance scholars have investigated various other manipulations firms employ to achieve the same objective. For instance, scholars in accounting and finance have discovered that managers time their earnings announcements to conceal unfavorable news and sway investor valuation (e.g., deHaan, Shevlin, & Thornock, 2015; Michaely, Rubin, & Vedrashko, 2016). For instance, Michaely et al. (2016) found evidence that firms switch announcements to Friday evening when they have bad news. Along the same line, prior research has shown that early announcements of firm earnings, caused by a calendar rotation unrelated to firm performance, tend to attract greater investor attention and enjoy more favorable responses (Noh, So, & Verdi, 2021). The research has also shown that the stock market is less responsive when negative news, such as performance shortfalls, is reported in the “missing month,” a stub period not covered by regular quarterly reports, earnings announcements, and analyst reports when public firms change their fiscal year ending date (Du & Zhang, 2013).

Additionally, research in this field indicates that managers’ distribution of information to the public can also be a strategic maneuver. For instance, Jung, Naughton, Tahoun, and Wang (2018a) showed that managers send fewer earnings announcement tweets when earnings news is bad. Elliott, Hodge, and Sedor (2012) revealed in an experiment that when CEOs accept responsibility for an earnings restatement, investors viewing CEOs’ explanations online via video make greater investments in the firm than investors viewing the same announcements via text-based press releases. In another experiment, research has shown that investors trust the CEO more and are more willing to invest in the firm when the CEO communicates bad news (e.g., negative earnings) through a personal Twitter account than when the news comes from the corporate website, the corporate Twitter account, or the firm's Investor Relations website (Elliott, Grant, & Hodge, 2018). Besides managing investors’ impressions of themselves, firms can also manage communication to influence investors’ impressions of other firms. For instance, using data on firm-initiated disclosures during an acquisition negotiations period, Kim, Verdi, and Yost (2020) found that acquiring firms can reduce the takeover price by strategically generating news to depress the target firm's stock price.

Furthermore, accounting and finance scholars have demonstrated that managers can manipulate the tone of their earnings releases to deceive investors (e.g., Davis, Ge, Matsumoto, & Zhang, 2015; Huang, Teoh, & Zhang, 2014). For instance, Huang et al. (2014) found that an abnormally positive tone in a corporate earnings release, unrelated to concurrent information about firm performance, incites an overly optimistic stock market response to the earnings announcement. More importantly, they showed that managers use an abnormally optimistic tone when they have strong incentives to bias investor perception upward (e.g., when firms barely meet analysts’ forecasts or when the likelihood of future earnings restatements, new equity issuances, or mergers and acquisitions is high). In contrast, when firms award stock options to CEOs, managers prefer to manipulate an abnormal tone downward to reduce share price.

Investors as Cognitive Analyzers

A second stream of research focuses on investors’ cognitive processes in determining the value of a firm. We label this perspective “investors as cognitive analyzers.” This body of work views investors as processors of information and recognizes investors’ limited cognitive capacity to process all available information before rendering judgments. We categorize this stream of research into three groups of studies: attention, information processing, and decision, which shape investors’ valuations of firms.

Attention

Investors have limited attention that can be used at any given time. When attention is allocated to some issues, the amount of attention available for other issues will be limited.

The research on investor attention has revealed three significant findings: (1) Investor valuation is influenced by attention; (2) changes in attention lead to changes in investor reactions; and (3) decision quality improves with a focused attention.

To start with, some studies have revealed that firms that capture a greater share of investors’ attention tend to receive higher valuations. For instance, using functional Magnetic Resonance Imaging (fMRI), Shane, Drover, Clingingsmith, and Cerf (2020) found that entrepreneurs’ high-affect pitches cause investors’ brains to behave in such a way that their attention to the stimulus (i.e., the pitch) will increase, resulting in more favorable assessments. Clarke, Cornelissen, and Healey (2019) showed that the skillful use of hand gestures by entrepreneurs attracts more attention from investors, enhancing investors’ valuation of the venture. Moreover, Mitteness, Sudek, and Cardon (2012) found that passionate entrepreneurs can obtain higher valuations from angel investors when the emotional content conveyed by their passion attracts increased attention from investors. Along the same line, Madsen and Rodgers (2015) demonstrated that investors will give higher valuations to firms for their corporate social responsibility activities only when stakeholders pay attention to such initiatives.

Moreover, changing areas of attention focus for investors can result in significant shifts in their reactions to a firm's actions or decisions. For instance, Gulati and Higgins (2003) found that the favorability of the equity markets determines the types of uncertainty salient to investors and influences how investors value an entrepreneurial venture's different forms of social ties. In hot equity markets, investors are more concerned about investing in worthless opportunities due to overly optimistic market sentiment. In cold markets, investors’ attention shifts toward the risks of missing solid investment opportunities due to market pessimism. As a result of such shifts in investor attention, this study revealed that endorsement ties with prestigious underwriters are more beneficial when markets are hot, whereas partnership ties with alliance partners are more beneficial when markets are cold. Taking a different path, Sekerci, Jaballah, van Essen, and Kammerlander (2022) found that adverse economic conditions, such as recessions, compel investors to focus more intently on survival and the immediate economic well-being of firms rather than growth and long-term sustainability. As a result, corporate social responsibility news that is typically seen as positive in times of economic prosperity is likely to be interpreted as negative news that jeopardizes firm survival during a recession.

Lastly, research indicates that enhanced attention and cognitive effort devoted by investors to valuing a firm can lead to improved accuracy in their valuation. Circadian rhythms are 24-hr cycles that regulate all systems of the body, including the sleep-wake cycle and individuals’ attention to and performance of various cognitive tasks. Guarana, Stevenson, Jeffrey Gish, Ryu, and Crawley (2022) showed that investors’ individual differences in circadian rhythms influence the amount of cognitive resources they can devote to decision cues during different times of the day. Lark investors (morning people) devote more attention to decision cues and make better valuation decisions in the morning, whereas owl investors (evening people) have more cognitive resources to support cognitive tasks and tend to make better investment decisions in the evening.

When comparing the literature on investor attention between management and accounting and finance, several differences emerge. Initially, while management scholars have explored ways for managers to capture investor attention and increase firm valuation, accounting and finance scholars have investigated factors that divert investor attention and result in neglect of important issues. The main argument of this stream of research is that because investor attention is limited, news released by other firms can distract investors from processing news released by the focal firm. For example, Hirshleifer, Lim, and Teoh (2009) showed that when a firm announces earnings on the same day as many other firms, the greater number of public disclosures by other firms competes for investor attention and causes a market underreaction to earnings surprises announced by the focal firm. Similarly, Drake, Roulstone, and Thornock (2012) found that investors devote less attention to focal firms when they are distracted by higher levels of competing earnings news. Moreover, accounting and finance scholars are interested in how external exogenous shocks, such as climate changes and nationwide lottery jackpot days, distract investor attention (e.g., Drake, Johnson, Roulstone, & Thornock, 2020; Madsen, 2017). For instance, Choi, Gao, and Jiang (2020) found that when the temperatures in a city are abnormally warm, the volume of Google searches for the topic of “global warming” increases significantly, and this increased attention to global warming translates into investor trading preferences for stocks with lower climate sensitivities in the financial markets.

In addition, while management research has examined the implications of investors’ limited attention span, accounting and finance research has focused on how investors cope with these limitations. The existing work predicts that when investors’ attention is limited, they will allocate more attention to market-level news that has a wider impact on different stocks in their investment portfolio than to firm-specific news (e.g., Peng & Xiong, 2006). The outcome of this attention division is that stock returns are more sensitive to market-level news and less sensitive to firm-specific news, leading to a higher return correlation among firms in the same market sector. For instance, Huang, Huang, and Lin (2019) found that on nationwide lottery jackpot days, when more of investors’ attention is drawn away from the financial market to the jackpot, investors allocate relatively more of their attention to market-level news and disproportionately reduce their attention to firm-specific news. As a result, stock returns co-move with the stock returns of other firms in the same industry; the reduced attention to firm-specific news also causes a weaker market response to firm-level earnings surprises.

Moreover, accounting and finance scholars have recognized investor attention as a mechanism that sometimes links the market value of firms, causing it to fluctuate collectively (e.g., Cao, Chordia, & Lin, 2016; Parsons, Sabbatucci, & Titman, 2020). Earnings announcements are generally scheduled and announced in advance, allowing investors to anticipate their occurrence. When the scheduled time of a firm's earnings announcement is approaching, the anticipation of the event may stimulate increased attention not only toward the disclosing firms, but also toward others who are affiliated with the disclosing firms, such as their major customers and suppliers. Accordingly, Madsen (2017) found that investor attention to a firm's publicly disclosed customers increases shortly before the firm announces its earnings. As a result, news and updates from these customers will trigger changes in the stock prices of these firms as well as the disclosing firms, creating an empirical connection between the stock returns of the customers and the disclosing firms.

Information Processing

Once they are noticed, external information stimuli need to be properly interpreted to influence investors’ valuation decisions (e.g., Schepker, Oh, & Patel, 2018). Prior research suggests that the way investors process and interpret external information matters greatly in terms of investor valuation. Especially in highly ambiguous environments, research has shown that investors are motivated to take a holistic view of firms’ activities to ease their interpretations of firms’ competitive strategies and advantages. For instance, Rindova, Ferrier, and Wiltbank (2010) demonstrated that firms which can orchestrate their competitive moves into easy-to-process action sequences to stimulate investors’ pattern recognition are more highly valued by investors. Similarly, in the context of mergers and acquisitions, Campbell, Sirmon, and Schijven (2016) found that investors tend to rely on mechanisms akin to expert heuristics as complex decision aids to holistically consider the pattern of information presented in mergers and acquisitions (M&A) deals. Using an inductive approach, these authors have identified a set of M&A attributes (e.g., related acquisitions by well-performing, experienced acquirers) that are often considered good deals by investors.

When we compare the research on information processing in the management literature with that in the accounting and finance literature, one difference is notable. A key finding of the management literature is that how investors process external information stimuli (either holistically or independently) has a considerable impact on how they value a firm and its activities. In contrast, research in accounting and finance is less concerned about how investors process information and more concerned about how information overload affects investors’ information processing and how investors use 10-K assessments and Internet searches to facilitate information processing.

In the financial markets, as the costs of producing and disseminating information have declined substantially over the past 3 decades, the amount of information being produced has increased considerably. Accordingly, some accounting and finance studies have shown that the sheer volume of information disclosed is a major factor that influences when and how investors respond to corporate news. For instance, Arif, Marshall, Schroeder, and Yohn (2019) documented that when firms disclose earnings announcements (EA) concurrently with a 10-K filing, market reaction to concurrent EA/10-Ks is muted relative to stand-alone EAs, because investors face increased difficulty in instantaneously processing a greater amount of information. Moreover, Cohen, Malloy, and Nguyen (2020) found that changes to 10-Ks influence stock prices in a large and significant way, but with a time lag. Due to the increasing length and complexity of financial statements, investors can only uncover changes in reports over time. Finally, Grant (2020) revealed that although information volume enhances the quality of investors’ judgments when firm disclosures are viewed on a standard computer screen, it harms investors’ judgments when disclosures are viewed on a smaller screen, such as a mobile device.

Moreover, a growing body of literature in accounting and finance has studied how Internet searches are changing the way investors access and process information. Some scholars have found that Internet searches enable investors to process information more effectively, thereby influencing the speed with which they react to corporate earnings news (e.g., Chen, Cohen, Gurun, Lou, & Malloy, 2020a; Drake et al., 2012; Hoopes, Reck, & Slemrod, 2015; Xu, Xuan, & Zheng, 2021). For instance, using Google search volume as a proxy for investor information demand, Drake et al. (2012) found that when investors use Google extensively to search for information related to firms in the pre-announcement period, investors can preempt the upcoming earnings news and take action in advance. Similarly, using Google's unexpected withdrawal of its search business from China as an exogenous shock to Chinese investors’ ability to search and process information, Xu et al. (2021) found that investors’ ability to take action before earnings announcements declined significantly, suggesting that Internet searches are a crucial factor in facilitating investors’ information gathering and processing. In addition to Internet searches, accessing the 10-K filings of a publicly traded firm is another way for investors to search for information (e.g., Chen et al., 2020a; Drake, Roulstone, & Thornock, 2015; Loughran & McDonald, 2017). Using the SEC's EDGAR server log of all filing requests, Drake et al. (2015) found that investors’ EDGAR requests tend to increase around important corporate events, such as earnings announcements, restatements, and poor stock performance, and they have a positive impact on the speed with which earnings news is reflected in stock prices.

Decision

Two important findings have emerged from the research on investor valuation decisions: (1) Investors rely on mental shortcuts to make valuation decisions; (2) investors’ valuation decisions are affected by various cognitive biases. Often, investors make valuation decisions in environments with extreme levels of uncertainty and ambiguity. Under such conditions, whether they are novices or experienced, investors tend to rely on various mental shortcuts to assess the value of firms and their activities (e.g., Cumming & Hornuf, 2022; Huang & Pearce, 2015; Scott, Shu, & Lubynsky, 2020). For instance, Huang and Pearce (2015) found that investors often do not rely on formal analysis and instead use sophisticated schemas, which they refer to as “gut feel,” to make decisions. When there is a difference between what the formal analysis and their schemas suggest, they discount the formal analysis to privilege their schema-based assessments. In addition, not all investors are equipped with the necessary knowledge and skills to assess the value of firms and their activities. In the context of crowdfunding, Cumming and Hornuf (2022) demonstrated that although detailed financial disclosures of firms provide rich and relevant information to facilitate lenders’ funding decisions, unsophisticated lenders tend to ignore this hard-to-understand information and use risk ratings provided by the platform as a simple and effective heuristic to make their funding decisions.

In addition to investors’ reliance on mental shortcuts, a large stream of research has documented the presence of various types of cognitive bias in investors’ decision-making, including representative bias, confirmation bias, and in-group bias. Representative bias occurs when people use similarities between objects, events, and people to categorize them and make judgments. Our brain categorizes objects, events, people, and companies into different mental prototypes. When we find something similar to a prototype in our mind, we have a tendency to jump to conclusions based on existing beliefs. Among the different types of representative bias, gender stereotypes have received considerable attention (e.g., Balachandra, Briggs, Eddleston, & Brush, 2019). Stereotypes are preconceived ideas about a person based on what people from a similar group might typically be like. When investors develop expectations of behaviors based on gender stereotypes, women in leadership roles are more negatively evaluated, because they violate gender-role expectations (since corporate leadership roles are primarily defined in masculine terms). For instance, Lee and James (2007) found that the appointment of female executives, especially female CEOs, will result in a more negative market reaction than that generated by the announcement of male executives and CEOs. Similarly, Bigelow, Lundmark, Parks, and Wuebker (2014) found in an experiment that, despite their identical nature, the abilities and experiences of female CEOs were constantly evaluated by experiment participants as lower than those of male CEOs. 3

Confirmation bias is the tendency to overvalue (undervalue) new evidence that confirms (disconfirms) one's existing beliefs. Research has shown that investors devaluate firms that violate their pre-established beliefs by engaging in inappropriate activities. Over time, investors develop specific beliefs about appropriate activities for different types of firms. These beliefs become the lens through which investors interpret the activities and performance of firms. Hence, a number of studies have shown that investors react differently when different firms engage in the same activities, depending on whether these activities are consistent with investors’ beliefs and expectations regarding these firms (e.g., Dorobantu, Henisz, & Nartey, 2017; Sekerci et al., 2022). For example, Hayward and Hambrick (2020) found that when a firm has a growth reputation, investors react favorably to the announcement of an acquisition, because an acquisition is believed to accelerate growth and is consistent with what a growth-oriented firm should do. However, investors’ reactions become negative when a firm with a growth reputation acquires a target with a dividend reputation.

In-group bias describes people's tendency to give preferential treatment to others who belong to the same group. Because foreign firms are likely to be viewed by local stakeholders as out-group members, Crilly, Ni, and Jiang (2016) found that when foreign firms engage in do-good CSR activities (i.e., proactive CSR activities that create societal values), local stakeholders tend to ascribe such positive behaviors to external causes and evaluate foreign firms less favorably. When foreign firms engage in do-no-harm CSR activities (i.e., less desirable CSR activities seeking to minimize the societal costs of business), local stakeholders tend to attribute such negative behaviors to internal causes and punish foreign firms more severely in their evaluations.

When it comes to decision bias, accounting and finance research diverges from the management literature in a couple of key aspects. One of the major cognitive biases that accounting and finance scholars have extensively examined is anchoring (e.g., George, Hwang, & Li, 2018; Huang, Lin, & Xiang, 2021; Li & Yu, 2012). Furthermore, a significant body of research has delved into how sentiment can affect investors’ valuations in this field. Anchoring bias describes people's tendency to rely too heavily on an “anchor” that serves as the starting point for estimates. When investors interpret new information from the reference point of an anchor, it can skew their judgment and prevent them from updating their estimates accordingly. A number of studies have investigated the anchoring effect created by the 52-week high price (e.g., Birru, 2014; Li & Yu, 2012; Ma, Whidbee, & Zhang, 2019). For instance, Huang et al. (2021) found that when a firm's stock price is near its 52-week high, this historical price can act as an anchor, slowing down investors’ belief-updating process. Specifically, when economically linked firms announce good news, investors cannot incorporate the good news to fully adjust their beliefs upward if a firm's stock price is at a high level near the 52-week high price. Similarly, for stocks with prices far from the 52-week high, when bad news about economically linked firms arrives, investors may respond slowly to bad news and avoid fully adjusting their beliefs downward.

It is well documented in the psychology research that individuals tend make overly optimistic (pessimistic) judgments when they experience positive (negative) emotions. Drawing on this insight, research in accounting and finance has developed the concept of investor sentiment 4 to capture the aggregated level of optimism or pessimism in financial markets that is not justified by underlying economic conditions and has found that it has a significant influence on stock prices (Baker & Wurgler, 2006). For instance, Mujtaba Mian and Sankaraguruswamy (2012) found that stock price sensitivity to strong earnings news is higher during periods of high sentiment when compared with periods of low sentiment, whereas stock price sensitivity to weak earnings news is higher during periods of low sentiment when compared with periods of high sentiment. Besides the generic positive/negative sentiment, prior research has also explored other types of investor sentiments, such as gambling sentiment (e.g., Naughton, Wang, & Yeung, 2019). For instance, Chen, Kumar, and Zhang (2021) found that an increase in the overall sentiment toward gambling is likely to generate a positive spillover effect on investor demand for lottery stocks. Moreover, they found that the effect of gambling sentiment on stock returns is stronger among U.S. states with a stronger gambling sentiment.

Investors as Economic Agents

A third stream of research emphasizes how investors act as economic agents who evaluate firms based on rational cost-and-benefit calculations of how various firm attributes and behaviors enhance or destroy shareholder values. These studies typically draw on theories derived from an economic tradition, such as the agency theory, the resource-based view, the signaling theory, and transaction cost economics. Agency problems arise in firms when self-interested managers take actions that do not necessarily maximize shareholder value. Accordingly, a body of work within this research stream focuses on circumstances that may give rise to agency problems and studies investors’ reactions to corporate decisions under those circumstances. Moreover, investors must often rely on information provided by managers to reveal the genuine quality of the firm and make valuation decisions. Hence, another body of work within this research stream focuses on situations in which information asymmetry between managers and investors is particularly high, and examines investors’ reactions to various signals that convey firm quality to influence investors’ valuations. Based on the type of investor problems examined, we categorize this research stream into two subthemes: agency problem and information problem.

Agency Problem

The management literature regarding agency problems has primarily focused on four areas. These include the market outcomes of agency issues, the efficacy of internal governance mechanisms, the effectiveness of external governance mechanisms, and important contingencies that must be taken into account when examining agency problems and their impact on investor valuation. The first key finding is that investors tend to react negatively to firms that experience agency issues. Prior research has provided considerable evidence that investors react negatively when managers pursue corporate strategies or undertake strategic investments to advance their personal interests rather than the interests of shareholders (e.g., Hayward & Hambrick, 1997; Meznar, Douglas, & Kwok, 1994; Shi, Zhang, & Hoskisson, 2017; Wright & Ferris, 1997). For instance, Shi et al. (2017) found that competitor CEOs of award-winning CEOs tend to engage in more intensive acquisition activities in the post-award period, and investors react negatively to such acquisitions driven by social comparison. Along the same line, a number of studies have shown that when firms adopt corporate strategies driven by political pressures rather than value-enhancement goals, investors react negatively (e.g., Meznar et al., 1994; Wright & Ferris, 1997). For instance, when there was moral outrage among Americans in response to the treatment of black South Africans by the minority white South African government, many American businesses divested their profitable South African business units, which triggered negative and significant reactions from investors (Wright & Ferris, 1997). Since slack resources may create opportunities for managers’ opportunistic behavior, Deb et al. (2017) found that investors react favorably to cash holdings by firms operating in industries that require rapid adaptation to uncertainties. Yet, cash holdings can be detrimental to shareholder wealth when used by firms that are poorly governed, diversified, or opaque.

Additionally, internal governance mechanisms, such as board independence, ownership concentration, and managerial incentives, have been found to effectively hold managers accountable and ultimately enhance firm value. The influence of boards, particularly board independence, on firm valuation has been extensively studied. Research has found that investors tend to react positively to strategic investments made by firms whose boards of directors are more vigilant (Feldman, Amit, & Villalonga, 2019; Goranova, Priem, Ndofor, & Trahms, 2017; Holl & Kyriazis, 1997; Kabir, Cantrijn, & Jeunink, 1997; Tian, Haleblian, & Rajagopalan, 2011). Ownership concentration is another subject of extensive research. Studies have found that investors tend to react positively to strategic investments made by firms whose owners are more powerful (i.e., have more concentrated ownership; e.g., Kroll, Wright, Toombs, & Leavell, 1997; Martin, Wiseman, & Gomez-Mejia, 2019). However, when more power is concentrated in the hands of managers, such as when managers assume two or three additional titles, investors tend to react negatively to firms’ investment decisions (e.g., Davidson, Nemec, & Worrell, 2001; Harris & Helfat, 1998; Martin et al., 2019; Rao, Baliga, & Moyer, 1996; Worrell, Nemec, & Davidson, 1997). Because monitoring is difficult and costly, the third governance mechanism studied by this literature is the alignment of managers’ financial interests with the interests of shareholders through equity ownership and equity-based compensation. These studies have found that investment decisions made by managers whose financial interests are more closely aligned with those of shareholders indeed create value for investors (e.g., Carpenter & Sanders, 2002; Certo et al., 2003; Nyberg, Fulmer, Gerhart, & Carpenter, 2010; Reuer & Miller, 1997; Steinbach, Holcomb, Holmes, Devers, & Cannella, 2017).

Research has also explored the role of external governance mechanisms, such as the market for corporate control and shareholder activism, in investor valuation. Early theories argued that hostile takeovers represent a mechanism that protects shareholders from poor management. Yet, empirical studies have shown that they rarely produce positive market returns because they often result in undesirable consequences, such as large-scale employee layoffs, which destroy shareholder value (e.g., Nixon, Hitt, Lee, & Jeong, 2004; Worrell, Davidson, & Sharma, 1991; King, Dalton, Daily, & Covin, 2004). Accordingly, in the event of a hostile takeover, antitakeover provisions that insulate managers from such events are found to increase rather than decrease firm value, because many takeovers are considered opportunistic attempts to take advantage of a firm's low stock price (Holl & Kyriazis, 1997; Humphery-Jenner, 2014; Kabir et al., 1997). Another important form of external governance studied in the management literature is activist investors, who proactively amass ownership stakes to influence managerial decision-making (Ahn & Wiersema, 2021; DesJardine & Durand, 2020). Although several studies have found that ownership by activist hedge funds enhances the market value of targeted firms in the short term (e.g., Chen & Feldman, 2018; DesJardine & Durand, 2020), a recent study revealed that targeted firms’ operating cash flow, investment spending, and social performance tend to deteriorate following the ownership of an activist hedge fund, suggesting that shareholder activism may undermine the financial sustainability of targeted firms in the long term (DesJardine & Durand, 2020).

Finally, the literature has identified several important contingencies that should be considered when examining agency problems and their impact on investor valuation. Several studies have explored how multiple governance bundles work interactively to generate firm value (Bell et al., 2014; Surroca et al., 2020). Goranova et al. (2017) revealed the downside of strong governance by showing that M&A investments by firms with strong governance are less likely to achieve superior returns, because strong governance not only reduces managers’ propensity to undertake risky M&A investments, but also constrains managers’ ability to engage in value-enhancing activities.

The literature on agency problems in management and accounting and finance exhibits two distinct differences. The first is that management literature primarily investigates the agency conflict between managers and investors (see Jia, Shi, Wang, & Wang, 2020 as a notable exception), whereas the accounting and finance literature extensively studies the agency conflict between controlling and minority shareholders. Because controlling shareholders hold a significant number of voting shares and have control over the affairs of a firm, the protection of minority shareholders against expropriation by controlling shareholders is of great importance. The accounting and finance scholars have identified two governance mechanisms to address this type of agency conflict: shareholder activism and legal systems.

Prior research offers mixed results regarding the effectiveness of shareholder activism. Some scholars have shown that shareholder activism can improve the performance of targeted organizations and create value for shareholders (e.g., Boyson & Pichler, 2019). Gantchev, Sevilir, and Shivdasani (2020), for example, found that hedge fund activists target firms engaged in empire building, and the stock market reacts favorably to announcements of their interventions. However, other scholars have warned against giving active shareholders too much power (e.g., Levit, 2020). They have argued that in settings where shareholders have different objectives than firm value maximization, offering too much power to shareholders can lower firm value (Goldman & Wang, 2021). For instance, Bhandari, Iliev, and Kalodimos (2021) found that, in general, being targeted by a shareholder-driven proxy-access proposal 5 is positively viewed by investors. However, the dispersed nature of shareholders constrains them from coordinating to support the implementation of such proposals in firms where they are needed the most. The adoption of proxy-access proposals occurs most frequently in large firms that are already well-governed, where the benefits of employing such a practice are limited. Hence, this study directly challenges the effectiveness of disciplining entrenched boards using shareholder proposals.

In addition to shareholder activism, prior research in accounting and finance has emphasized the importance of legal systems in protecting minority shareholders against expropriation by controlling shareholders (Agrawal, 2013; Basak, Chabakauri, & Yavuz, 2019; McLean, Zhang, & Zhao, 2012). A key finding from this body of work is that well-functioning legal systems can protect outside investors, which will, in turn, improve the ability of firms to raise external finances from investors. For instance, using data from 27 countries, La Porta, Lopez-De-Silanes, Shleifer, and Vishny (2002) found that investors are willing to give higher valuations to firms in countries where their rights are better protected by the law. Moreover, focusing on the passage of state investor protection statutes in the United States during the early 1990s, Agrawal (2013) found that improved investor protections in a state limit expropriation by controlling shareholders. In states where the law is passed, market valuations of firms rise immediately. Although the legal systems of a country are beyond the control of any individual firm, some studies have found that by cross-listing in the United States, foreign firms subjecting themselves to the strict laws and enforcement in the United States can increase investor protections and achieve higher valuations (Hail & Leuz, 2009). Cross-listing is thus one effective way for foreign firms to circumvent the negative influence of their home country's legal system and achieve higher valuations.

The second difference is that management research emphasizes the role of equity-based compensation in aligning the financial interests of managers and shareholders, while accounting and finance research focuses on designing equity-based compensation to achieve the expected effect. For instance, to avoid stock option backdating (i.e., the practice of granting an executive stock option that is dated before its actual issuance to help executives fix a lower exercise price and increase the value of their stock options), some firms have adopted scheduled option grants, which specify in advance the exercise price, size of the option, and vesting schedule. Yet, scholars have found that although scheduled option grants solve the issue of backdating, they create incentives for other types of opportunistic behavior. For example, Daines, McQueen, and Schonlau (2018) revealed that CEOs, aware of upcoming option grants, strategically release bad news to temporarily depress stock prices and obtain lower exercise prices. These CEOs will release good news after the scheduled grant, creating a V pattern of abnormal returns around the option grant dates (i.e., negative abnormal returns before the option grant dates and positive abnormal returns thereafter). They also found that these abnormal returns around the option grant dates are larger for CEOs, who have stronger incentives and a greater ability to behave opportunistically.

Information Problem

According to the signaling theory, when there is information asymmetry between two parties, the party with superior information may undertake actions to signal its underlying quality to the other party to reduce information asymmetry, which hampers the other party's selection ability (Akerlof, 1970; Spence, 1973). Drawing on signaling theory, scholars in management have investigated how firms use signals to influence investors’ perceptions and responses to organizational actions (Connelly, Certo, Ireland, & Reutzel, 2011). This research stream focuses on three distinct categories of signals, namely: the characteristics and behavior of corporate leaders; the resources and capabilities of a firm; and a firm's social performance.

One type of signal concerns the attributes and actions of corporate leaders, including the composition of a firm's top management team and board of directors (e.g., Certo, 2003; Chahine, Filatotchev, & Zahra, 2011; Mitra, Post, & Sauerwald, 2021; Solal & Snellman, 2019; Tian et al., 2011). These factors have been shown to play an important role in shaping investor perceptions and valuation. For instance, Chahine et al. (2011) showed that the valuation of an IPO firm is positively associated with founders’ and board members’ prestige. Solal and Snellman (2019) found that a gender-diverse board is sometimes interpreted by investors as revealing of firms’ stronger commitment to diversity and weaker commitment to shareholder value, causing the value of a firm to depreciate.

Managers can also signal the unobserved quality of their firms via observable actions (e.g., stock purchases and sales, certifications of financial statements; e.g., Coff & Lee, 2003; Wang & Song, 2016; Zhang & Wiersema, 2009). For instance, Woolridge and Snow (1990) showed that stock market reactions to public announcements of corporate strategic investments (e.g., formation of joint ventures, R&D projects, major capital expenditures, and diversification into new markets) are positive, indicating that the stock market rewards managers for developing strategies that increase shareholder wealth. Zhang and Wiersema (2009) found that the certification of a firm's financial statements by a CEO can send positive signals to investors and increase the valuation of the firm when observable attributes of the CEO enhance the credibility of his or her certification.

Another type of signal concerns the resources and capabilities of a firm, which can provide information about the firm's competitive position and potential for future success (e.g., Belderbos, Park, & Carree, 2021; Laamanen, 2007; Shan, Fu, & Zheng, 2017; Testoni, 2022; Yang, Narayanan, & De Carolis, 2014). For instance, Laamanen (2007) showed that a high acquisition premium evokes positive market reactions when firms acquire valuable technological resources from target firms that are difficult to value. Welbourne and Andrews (1996) found that investors react positively when firms allocate more scarce organizational resources to hire, train, and retain their employees. Zheng, Liu, and George (2010) found that investors’ valuations of high technology start-ups are higher when such firms have accumulated more technological resources, and this effect is stronger for older start-ups with more sophisticated organizational routines to extract value from technological resources.

In addition to resources, research has shown that a firm's learning and innovative capabilities are also crucial factors that can signal the firm's quality to investors (e.g., Gulati, Lavie, & Singh, 2009; Kale, Dyer, & Singh, 2002; Zaheer, Hernandez, & Banerjee, 2010). For instance, Yang, Zheng, and Zaheer (2015) found that investors react more favorably to the announcement of alliances by firms whose ability to learn from others is higher. Berry (2006) demonstrated that shareholders will not value a firm's investments in developing countries unless the firm has previous experience.

Finally, a firm's corporate social performance, which reflects its commitment to social responsibility and environmental sustainability, can also serve as a signal of quality and trustworthiness to investors (e.g., Dorobantu & Odziemkowska, 2017; Dowell, Hart, & Yeung, 2000; Werner, 2017). For instance, Dowell et al. (2000) found that adopting a higher global environmental standard will be positively viewed by investors, because doing so can serve as a new basis of differentiation to attract customers and suppliers and mitigate the risk of future environmental crises and penalties. Dorobantu and Odziemkowska (2017) examined the value of community benefits agreements (CBAs), which are signed by firms and local communities and designed to mitigate social conflict that disrupts access to valuable resources. They found that shareholders more positively evaluate CBAs involving local communities that are more likely to cause costly disruptions and delays for a firm.