Abstract

Many institutional investors are active political donors, but the impact that their political partisanship has on corporate practices and policies has mostly eluded academic examination. As political donations can reflect investors’ views and values, we theorize that the nature of investors’ political donations can shape managerial decision-making in important ways. We test this idea by examining changes in corporate social responsibility (CSR) activities, an area where managers have a high degree of discretion over how they account for investors’ views and values. Our theory introduces two focal constructs: political position, which captures the average political affiliation of actors within a group, and political dispersion, which captures the variance in political positions across group members. After hypothesizing a positive relationship between liberal-positioned investors and a firm's CSR activities, we argue that political dispersion among investors mitigates this positive effect. To account for between-group dispersion, we also suggest that liberal-positioned investors have a stronger positive effect on CSR in firms with more conservative managers. Our analysis of 19 years of shareholder political donations data for 2,062 U.S.-based firms supports our theory. This paper lays new groundwork for research on shareholder politics in management, and contributes to research on investor influence, political ideology, and CSR.

Keywords

Institutional investors are no strangers to politics. According to the Center for Responsive Politics (CRP), institutional investors and their affiliates in the finance industry have been the single largest source of political contributions in the United States over the past decade, donating over $800 million to various candidates and their parties in the 2020 election cycle alone. One of the most prominent investors, who claimed Trump would “turn out to be a transitory phenomenon,” George Soros donated nearly $130 million exclusively to Democrats. Importantly, anecdotal evidence suggests that depending on their political partisanship, investors seem to take different positions on major topics and issues. Such division was evident, for instance, in the early 2020s, in the heavily politicized debate on the purpose of the firm, where Democratic and Republican donors were pitted against one another on the role of corporations and their duties to the natural environment and society. Despite many investors’ strong political convictions, little is known about how shareholder politics affect management, leaving many unanswered questions that are ripe for academic investigation.

Foremost among these questions is whether managers account for investors’ political positions when making decisions. By political position, we refer to the average political affiliation of actors within a group—institutional investors, in our context. Research suggests that corporate managers pay close attention to investors’ preferences because they stand to gain personally by doing so (Connelly, Hoskisson, Tihanyi, & Certo, 2010; DesJardine, Zhang, & Shi, 2022b). However, scholars have not yet considered how institutional investors’ political positions, reflected in their donations to specific political parties, shape firm outcomes. This is both practically relevant as investors increasingly wade into politics, and academically important as scholars seek to unpack how investors affect corporate priorities (DesJardine, Grewal, & Viswanathan, 2022a).

Drawing on political ideology research, we investigate how investors’ political positions (i.e., political affiliations) tangibly shape corporate priorities. Based on the idea that liberal-leaning individuals tend to value resource equality and fairness, findings show increased CSR activity in firms with liberal-leaning individuals (Chin, Hambrick, & Trevino, 2013). However, such studies have focused on the political positions of insiders (i.e., CEOs, directors, and employees) and overlooked those of investors. Thus, an important question remains unexplored: Do the political positions of investors shape firm outcomes?

Beyond the role of investors, another dimension that has been overlooked in prior work is how political (mis)alignment within a group of actors affects corporate decision-making. Current theory suggests that organizational decisions follow the dominant political position of a particular group. For example, organizations with more liberal employees engage more in CSR activity. However, employees and other groups are not monoliths; they comprise many individuals with different and sometimes diverse political affiliations. In our context, investors with different political positions often coinvest in the same companies, forcing managers to decide whether they will take actions that align more with the prevailing views of liberal or conservative investors. This raises a second question: Does the degree of political alignment within a group affect how a firm responds to that group's political position?

A third aspect that warrants consideration is the political alignment between groups. High political alignment creates affinity and reduces friction among actors (Iyengar, Sood, & Lelkes, 2012; McPherson, Smith-Lovin, & Cook, 2001). Applied to our context, liberal-positioned investors may exert a stronger influence on firms with conservative managers, not only because these investors are inclined to intervene in conservative managers’ decision-making, but also because conservative managers find it more crucial to placate liberal investors than likeminded conservative investors. Considering between-group political alignment raises a third and final question: Does the degree of political alignment between groups affect firm outcomes?

We address these three questions with three hypotheses that examine the relationships between investors’ political affiliations and corporate decision-making. First, we propose that investors’ political positions shape firms’ CSR activities, such that having more liberal-leaning investors increases CSR. Not only do investors express their views and values to managers, but managers consider their investors’ preferences when making CSR decisions as a way to placate their dominant investor base. Second, by making it harder for investors to act collectively, we hypothesize that greater political dispersion (i.e., variance in political positions) among investors weakens the positive effect of liberal-leaning investors on firm CSR. Finally, because political misalignment between investors and managers can strengthen investors’ motivations to influence managers and managers’ motivations to placate investors, we argue that the positive effect of liberal-leaning investors on CSR is stronger for firms with more conservative-leaning managers.

Our analysis of political donations by institutional investors affiliated with 2,062 U.S.-based firms between 2000 and 2018 supports our hypotheses. Our quasi-exogenous experiment based on mergers and acquisitions (M&As) among institutional investment brokerages alleviates concerns that an omitted variable drives our results or that liberal investors choose to invest in firms with higher CSR (i.e., reverse causality). Our findings are further supported by supplemental tests to examine managers’ personal incentives to placate investors with varying political affiliations.

Our study makes several contributions. Foremost, we lay important groundwork for the study of shareholder politics in management and expand research on investor influence by documenting how investors’ political affiliations influence organizational decision-making. Scholars have long acknowledged that investors can shape corporate policies and practices, including CSR, but have overlooked the role of shareholder politics. Additionally, we extend research on political donations and ideologies in multiple ways. First, to our knowledge, this is the first study on how investors’ political positions affect firm outcomes. Second, we introduce political dispersion as an important dimension to consider in political affiliation and ideology research. Third, we document how interactions between different groups’ dominant political positions affect organizational outcomes.

Theoretical Background and Development

Investor Influence and Shareholder Politics

Extensive research has acknowledged that the composition and actions of investors can impact managerial decision-making and firm outcomes (Connelly et al., 2010; DesJardine & Bansal, 2019). Investor influence operates on a two-way street, whereby investors actively assert themselves in managerial decision-making and managers respond to changing ownership structures.

First, investors may leverage their equity positions to actively influence the decisions of top managers by meeting with them, filing shareholder resolutions, voting for or against managerial proposals, and sometimes even appointing their own directors to company boards (DesJardine et al., 2022b). During meetings with managers, for instance, investors can openly convey their values and voice their views on various corporate practices and policies (Solomon & Soltes, 2015). Quoted by Brown, Call, Clement, and Sharp (2016: 151), one investment analyst explained, “On a [private] call, it becomes my meeting. I can control the agenda.” When managers fail to make decisions that prioritize their interests, investors can threaten to sell their holdings. If executed, divestments by large institutional investors can depress firm stock prices and adversely affect managers’ compensation and job security (Shi, Ndofor, & Hoskisson, 2021).

Second, top managers recognize and respond to changing ownership structures because the power that some investors wield over their job security and compensation incentivizes them to pay close attention to their investors’ interests. As such, professional investor relations’ resources often coach managers on how to track their investors’ holdings and attend to those investors’ needs (e.g., Cunningham, 2020). By doing so, managers can become highly “aware of the composition of their investor base” (Dikolli, Kulp, & Sedatole, 2009: 740) and go to great lengths to placate their investors (Westphal & Bednar, 2008).

Given investors’ potential impacts on firm outcomes, scholars have devoted great effort to unpacking the range of investor characteristics that govern their influence. For example, based on Bushee's (1998) classification, investors’ investment horizons and portfolio holding concentrations have been shown to influence a range of firm outcomes, including time horizons (DesJardine & Bansal, 2019), competitive actions (Shi & DesJardine, 2022), and CEO dismissals (Connelly, Li, Shi, & Lee, 2020). In the context of CSR, numerous empirical studies show that ownership by longer-term shareholders, including pension funds (Johnson & Greening, 1999) and family owners (Kang & Kim, 2020), is associated with better treatment of stakeholders, whereas ownership by shorter-term shareholders, such as mutual funds (Johnson & Greening, 1999) and hedge funds (DesJardine & Durand, 2020), can undermine firm CSR. Other notable characteristics include investors’ common ownership (DesJardine et al., 2022a), investment experience (Boh, Huang, & Wu, 2020), and geographic location (Mun & Jung, 2018).

Within this literature, it is surprising that investors’ political positions have been overlooked. We define “political position” as the dominant political party to which an investor makes political donations. Finance scholars (Bolton, Li, Ravina, & Rosenthal, 2020; Kim, Wan, Wang, & Yang, 2019) have focused on understanding the role of investors’ political positions in shaping portfolio selection (i.e., the types of firms targeted for investment). Consequently, we have little to no understanding of whether and how investors’ political positions affect firm outcomes.

Yet, political positions are likely to matter because they can shape investors’ communication with managers, and because information about political donations can help managers discern and satisfy investors’ interests. The visibility of donations matters because few managers privately meet with all of their investors, limiting the amount of firsthand evidence they can gather on investors’ policy positions. Moreover, researchers have shown that individuals’ political giving can reflect their views and values on various topics and issues (Bonica, 2014), including their stances on economic equality and social justice (Jost, Federico, & Napier, 2009). Accordingly, investors’ political donations should reflect their views and values on a variety of corporate fronts, which is important information for discerning managers.

Investors’ Political Positions and CSR

A dominant finding in management research is that the political ideologies of CEOs, board members, and employees—as reflected in their political donations—can shape firms’ CSR activities. CSR refers to firms’ voluntary efforts to advance societal and environmental goals (Bansal & DesJardine, 2014). Noting the discretion managers have over their firms’ CSR activities, multiple empirical studies show that firms with more liberal-leaning CEOs engage in more CSR and stakeholder-friendly activities (Chin et al., 2013; Gupta, Nadkarni, & Mariam, 2019). For example, Chin and colleagues (2013) found that companies with liberal CEOs engage in more CSR activities, even when firm performance is low; Chin and Semadeni (2017) found that companies with liberal CEOs have less pay dispersion between CEOs and non-CEO executives; and Gupta and colleagues (2019) found that liberal-leaning CEOs are more likely to enact CSR practices and less likely to lay off employees than less liberal CEOs. Others have found similar pro-CSR outcomes when firms have more liberal-leaning board members or employees (Gupta, Briscoe, & Hambrick, 2017; Gupta & Wowak, 2017; Hutton, Jiang, & Kumar, 2015). Throughout this work, however, there is little understanding of whether investors’ political positions affect firms’ CSR activities.

We envision that investors’ political positions, indicated by their political donations and reflecting their broad views and values, influence managers’ CSR-related decision-making in two ways. First, politically active investors sometimes communicate their liberal or conservative views and values to management. As owners with formal authority, investors are regularly presented with opportunities to “channel” or voice their views and values on CSR-related issues to management. For example, investors can express their CSR-related values at least annually by voting for or against different proposals on corporate issues (e.g., related to executive renumeration or climate change action; Flammer, Toffel, & Viswanathan, 2021); they can voice their CSR preferences during personal meetings with management (DesJardine et al., 2022a); or they may broadcast those values in their investment prospectuses, websites, and other promotional materials (Aguilera, Bermejo, Capapé, & Cuñat, 2021). When a firm's CSR-related activities misalign with investors’ values, investors may express their disappointment by voting against managers, launching activism campaigns, or exiting the firm by divesting stock. As a result, when investors value CSR activities, managers likely invest more in CSR to avoid tensions.

Second, managers engage with investors to understand their orientations toward CSR. They may do this directly, through the same channels described above (i.e., meetings, proposals, and voting), or indirectly, by observing investors’ political giving to deduce their views on CSR-related topics and issues. Such analysis is most plausible when investors are large, active, and/or vocal donors. However, such an analysis is still possible with smaller and more reserved political donors, as political donations are publicly disclosed and data are easily accessible in several countries, including the United States. Moreover, an entire investor relations industry exists to help managers understand their investors’ holdings and interests. In 2020, for instance, the average investor relations department in large U.S.-based companies spent $715,000 on investor relations activities. 1 The resources that firms invest in managing investors corroborate studies that document deliberate and sometimes extensive efforts by managers to placate investors (e.g., Westphal & Bednar, 2008).

Because investors communicate their views and values to managers, and managers account for that information in their decision-making, we expect increased CSR engagement in firms with more liberal investors. As noted, liberal-leaning individuals tend to prefer increased engagement in CSR activity, regardless of the economic rationale (e.g., Gupta et al., 2017). Following this research, as a firm's investor base becomes more liberal, we expect managers to become more inclined to invest in CSR.

In contrast, managers will scale back CSR when their investors’ political positions are more conservative leaning. Conservatives differ from liberals in ways that could affect firm CSR (Jost et al., 2009; Swigart, Anantharaman, Williamson, & Grandey, 2020). Compared to liberals, conservatives have a stronger sense of personal responsibility and tend to hold the view that rewards should be directly proportionate to one's contributions to society or business. Because conservatives value property rights (Tetlock, 2000) and “place particular emphasis on order, stability, the needs of business, [and] differential economic rewards” (McClosky & Zaller, 1984: 189), conservative investors may not push so adamantly to advance other stakeholders’ interests through what they may view as “free handouts” in the form of CSR. In sum, we expect: Hypothesis 1 (H1): Firms increase their CSR when they have more liberal-positioned investors.

Political Alignment Among Investors

Beyond overlooking investors’ political donations, researchers have not considered whether dispersion in actors’ political positions affects firm outcomes. Thus far, scholars have studied the mean political affiliation among a firm's actors, what we call “political position.” For example, a top management team's political position lies somewhere between highly conservative and highly liberal, based on the average of their collective political donations. But averages conceal important information. We contend that the variance in political donations across a group of actors or between groups of actors is also important to consider. We refer to this as “political dispersion.” For example, two top management teams may have the same average political position (e.g., all moderately liberal), but a different political dispersion, which would affect their internal group dynamics. 2

Regardless of their average position along the political spectrum, investors with diverse political positions find it more difficult to work collectively. Drawing on the idea of values homophily (Lazarsfeld & Merton, 1954), numerous studies show that members of opposing political parties exhibit more negative attitudes toward individuals in the other party and more positive attitudes towards those in their own party (Iyengar et al., 2012; Iyengar & Westwood, 2015; Swigart et al., 2020). For example, conservatives may view other conservatives as “honest,” while viewing liberals as “unrealistic,” and liberals may view other liberals as “caring,” while viewing conservatives as “prejudiced” (Rothschild, Howat, Shafranek, & Busby, 2019). There is a general tendency to view others in different camps as less competent, reliable, or trustworthy (Hewstone, Rubin, & Willis, 2002; Kramer & Lewicki, 2010). Applied to politics, such stereotyping and negative attitudes can fuel conflict and dysfunction in politically diverse groups (Iyengar & Westwood, 2015). As such, and similar to other population groups, investors with diverse political positions are likely to view each another more negatively and to find it more difficult to work together than investors with similar political positions.

Yet, for their political positions to impact CSR, investors may need to act collectively to ensure that managers receive coherent messages regarding their preferences. Collective action, defined as actions taken by a group of individuals united to achieve a common objective (Marwell & Oliver, 1993), is necessary because even the largest investors rarely own enough shares to singlehandedly shape managerial priorities in ways that reflect their views (e.g., DesJardine, Marti, & Durand, 2021). The threat of exit, for instance, is much more concerning to managers when issued from a group of investors than from a single investor with few shares. When investors cannot act collectively, managers have more discretion to pursue their own plans and interests (Campbell, Campbell, Sirmon, Bierman, & Tuggle, 2012; Cremers & Ferrell, 2014).

By affecting group dynamics in ways that make it harder for investors to act collectively, political dispersion among investors diminishes the positive influence of liberal-positioned investors on CSR. Even though some investors with liberal views may unreservedly push for higher spending on CSR, others with different political positions register different views. For example, in meetings with managers, politically dispersed investors may voice divergent preferences on CSR, and, at annual shareholder meetings, they may vote differently on such issues. The greater the diversity, the more divergent the views. Such divergence makes it more difficult for liberal-positioned investors to send a unanimous message to managers about their stance on CSR, and for managers to incorporate these mixed views into a clear and coherent CSR strategy that placates those investors. Therefore, even in groups where the average political position among investors remains unchanged, greater political dispersion stifles the positive effect of liberal-positioned investors on CSR. Thus, we predict: Hypothesis 2 (H2): Investors’ political dispersion weakens the positive relationship between liberal-positioned investors and CSR.

Political Alignment Between Investors and Top Managers

The influence of liberal-positioned investors on CSR should hinge not only on the degree of political alignment among investors, but also on the political alignment between investors and top managers. Even when investors can act collectively, their degree of influence depends on their motivation to influence managerial decision-making and managers’ motivation to placate investors. To gain deeper insight into the impact of investors’ political positions on CSR, we also account for the degree of political (mis)alignment between investors and top managers. We propose that the impact of liberal-positioned investors on CSR is stronger in firms with conservative managers than in firms with liberal managers.

First, liberal-positioned investors are likely more motivated to intervene in and influence the decisions of conservative managers than the decisions of liberal managers. Research suggests that political misalignment between top managers and board members can improve board effectiveness because board members have less affinity for top managers whose values misalign with their own, making them more motivated to monitor those managers (Lee, Lee, & Nagarajan, 2014). In a similar vein, when investors are highly liberal and managers are conservative, investors are likely to be more motivated to closely monitor management and intervene in their decision-making to align decisions with their own preferences. They also are likely to be less forgiving when their preferences conflict with those of management. By comparison, because their values are aligned, liberal investors may be less motivated to monitor liberal managers and intervene in their decision-making, which would attenuate their influence on firm outcomes.

Second, managers are likely to be more motivated to placate investors whose political positions differ from their own. When managers and investors are both liberal leaning, the two may perceive each other as fellow members of an in-group rather than as members of an out-group (Ashforth & Mael, 1989; Riek, Mania, & Gaertner, 2006). Because likeminded investors are less likely to monitor managers and intervene in their decision-making, managers may perceive a weaker need to pacify them by actively altering corporate activities to align with their views and values. Indeed, such investors should be less likely to penalize fellow in-group managers who share their political convictions and may attend the same political events or social gatherings. In contrast, when managers are conservative and investors are liberal, relationships between the two groups may be more fraught with tensions and thus make CSR engagement seem more important to managers. Thus, much as in-group/out-group divisions between managers and directors can increase the perceived threat of board monitoring (Westphal & Zajac, 2013; Zhu, Shen & Hillman, 2014), intergroup divisions between investors and top managers can increase the perceived threat of investor control over CSR-related policies.

In sum, by affecting investors’ intentions to monitor managers, and managers’ perceptions of investors’ opposition to their decisions, we propose a substituting effect between investors’ and managers’ political positions: The positive influence of liberal-positioned investors on CSR is likely to be stronger in firms with more conservative top managers (and therefore greater investor-manager political misalignment) than in firms with more liberal top managers and less misalignment. Thus: Hypothesis 3 (H3): Political dispersion between investors and top managers strengthens the positive relationship between liberal-positioned investors and CSR. Specifically, the positive relationship between liberal-positioned investors and CSR is stronger for firms with conservative top management teams than for firms with liberal top management teams.

METHODS

Sample

Beginning with S&P 1500 firms headquartered in the United States in the year 2000, we obtained CSR data from MSCI KLD, which ends in 2018 and thus bounds our sample. We matched these firms to: political donation data from the Center for Responsive Politics (CRP); institutional investor ownership data from Thomson Reuters 13F Filings; investor classification data from Brian Bushee's website; executive-level data from ExecuComp; director-level data from BoardEx; and firm financial and accounting data from Compustat. After accounting for missing data across these databases, the final sample consists of 2,062 unique firms representing 12,267 firm-year observations from 2000 to 2018.

Dependent Variable

MSCI KLD (hereafter “KLD”) has been “the most widely used dataset” (Khan, Serafeim, & Yoon, 2016: 1701) to provide measures of firm CSR (e.g., DesJardine & Durand, 2020). 3 For the purposes of our study, KLD offers several advantages. First, because the database provides ratings along multiple dimensions pertaining to firms’ treatment of different stakeholder groups (e.g., employees or communities), we were able to create a broad measure of CSR that fits our theory. Second, because KLD has covered a broad universe of firms for a long time, using this database enabled us to construct larger samples than if we were to use other CSR data providers. Third, because KLD is considered to be the “best-researched” CSR data provider (Eccles, Lee, & Stroehle, 2020), using these data provided additional assurance of the validity of the CSR measures underlying our analyses.

For each dimension of CSR covered in the database, KLD provides a count of the positive (strengths) and negative (concerns) elements of a firm's CSR practices and policies toward that group. We retained the “strength” items of community, diversity, employee, environmental, and product dimensions to measure CSR (DesJardine et al., 2021). We used only strength indicators to measure CSR, because both liberal and conservative shareholders are risk-oriented and thus likely to be concerned about CSR related risks (Krueger, Sautner, & Starks, 2020) rather than actively intervening in firms’ CSR activities purely for pro-social reasons. Because the number of categories for strengths varied over time, comparing counts of these scores across years was not feasible. To address this issue, we divided the total number of strengths by the respective number of strength indicators evaluated for each firm in each year, and aggregated these scores to compute our final measure of CSR.

Independent Variable

The independent variable in our study is investor liberalism, which captures the political positions of investors on a scale from highly conservative to highly liberal. We constructed this variable using multiple data sources on U.S. institutional investors’ holdings and political donations. We focused only on institutional investors because they often have the strongest influence on managerial decision-making and because data are more readily available for institutional investors than for retail investors. We retained only U.S.-based institutional investors because U.S. campaign laws make it difficult for foreign nationals and corporations to make political campaign contributions.

We used political donation data from the CRP to measure each institutional investor's political affiliation. 4 To do so, we first identified all fund managers who worked for the same institution based on their employers’ names and their occupations. We considered fund managers with missing information in CRP to have made no contributions (Christensen, Dhaliwal, Boivie, & Graffin, 2015). We then summed donations from all fund managers to the Democratic Party (Republican Party) to measure donations to each party at the institutional level. Afterward, we measured each institutional investor's political position by calculating the institution's net donations made to the Democratic Party, equal to donations to the Democratic Party minus total donations to the Republican Party, scaled by total donations to both parties (Christensen et al., 2015; Park, Boeker, & Gomulya, 2020). The resulting values for each institutional investor's political position range between −1 (highly conservative) and +1 (highly liberal). We then measured a firm's investor liberalism by multiplying each institution's political position by its percentage of ownership in a firm.

Moderators

Our first moderator is investor political dispersion. Prior research has developed methods (e.g., the Blau index, coefficient of variation, and Gini coefficient) to measure diversity. Because institutional investors’ political positions represent separation along an attribute, we follow the guidance of Harrison and Klein (2007) to use standard deviation to measure investor political dispersion. Specifically, we calculated investor political dispersion for each firm as the standard deviation of all institutional investors’ political positions.

Our second moderator is top management team (TMT) liberalism. Following existing research (Christensen et al., 2015; Park et al., 2020), we measured TMT liberalism by collecting the names of the members of firms’ TMTs from ExecuComp, and information on those members’ political donations from the CRP. To measure a top manager's liberalism, we calculated the individual's net donations made to the Democratic Party, equal to total donations to the Democratic Party minus total donations to the Republican Party, scaled by total donations to both parties. Lastly, we measured a firm's TMT liberalism as the weighted average of top managers' liberalism, and the weight was the ratio of their compensation to the sum of all the top managers’ total compensation, which includes salaries, bonuses, other annual payments, total value of restricted stock granted, total value of stock options granted, long-term incentive payouts, and all other compensation, as reported in ExecuComp.

Control Variables

We controlled for various potential confounding effects in our models. Research (Chin et al., 2013) suggests that top managers’ political positions can also affect firms’ CSR, leading us to control for TMT liberalism. 5 Investors’ time horizons also can influence CSR, so we controlled for ownership by dedicated (long-term) and transient (short-term) institutional investors (Connelly et al., 2018; Shi & Hoskisson, 2021). Dedicated (transient) institutional ownership is measured as the percentage of a firm owned by dedicated (transient) institutional investors based on Bushee's (1998) classification. We also controlled for firm size, measured as the natural logarithm of total employees, because larger firms may have more resources to invest in CSR. Likewise, firms with lower performance may have fewer resources available for CSR, so we controlled for financial performance, measured as the ratio of operating income after depreciation to total assets, as well as market performance using market-to-book ratio, measured as the ratio of market value to book value. Firms with unencumbered resources may also have more leeway to improve CSR. We thus controlled for a firm's slack resources. We created a composite slack index that includes three types of slack: available slack (measured as the ratio of current assets to current liabilities), absorbed slack (measured as the ratio of working capital to sales), and potential slack (measured as the ratio of total equity to total debt). Lastly, we controlled for corporate social irresponsibility (CSiR) based on the “concern” items provided by KLD because firms with more CSR concerns can be more motivated to invest in CSR. CSiR equals the total number of concerns in the same KLD dimensions we used to measure CSR.

Next, we included several CEO-level control variables. Long-tenured CEOs are better able to cope with external pressures, which, in turn, could influence their attentiveness to CSR. Thus, we controlled for CEO tenure, which is measured as the number of years since an executive assumed the CEO role. CEO equity ownership and option pay can shape CEOs’ decisions to invest in CSR, leading us to include CEO equity ownership, measured as the percentage of a company's outstanding shares that are owned by a CEO, and CEO option pay, measured as the ratio of CEO option pay to total compensation (Feldman, 2016).

CEOs who also serve as board chairs face less external pressure (Tuggle, Sirmon, Reutzel, & Bierman, 2010), which may affect CSR. We thus controlled for CEO duality, assigning a value of 1 if a CEO also served as board chair, and 0 otherwise. Likewise, board members appointed by the CEO tend to be loyal and committed to the CEO (Coles, Daniel, & Naveen, 2014), which could help shield the CEO from external pressure. We thus controlled for directors appointed after CEO, measured as the ratio of board members appointed after the CEO to the total number of directors on the board. Finally, we controlled for female director ratio, measured as the ratio of female directors to board size, because female directors can affect CSR (Bear, Rahman, & Post, 2010).

Estimation Method

A Hausman test revealed that

RESULTS

Main Results

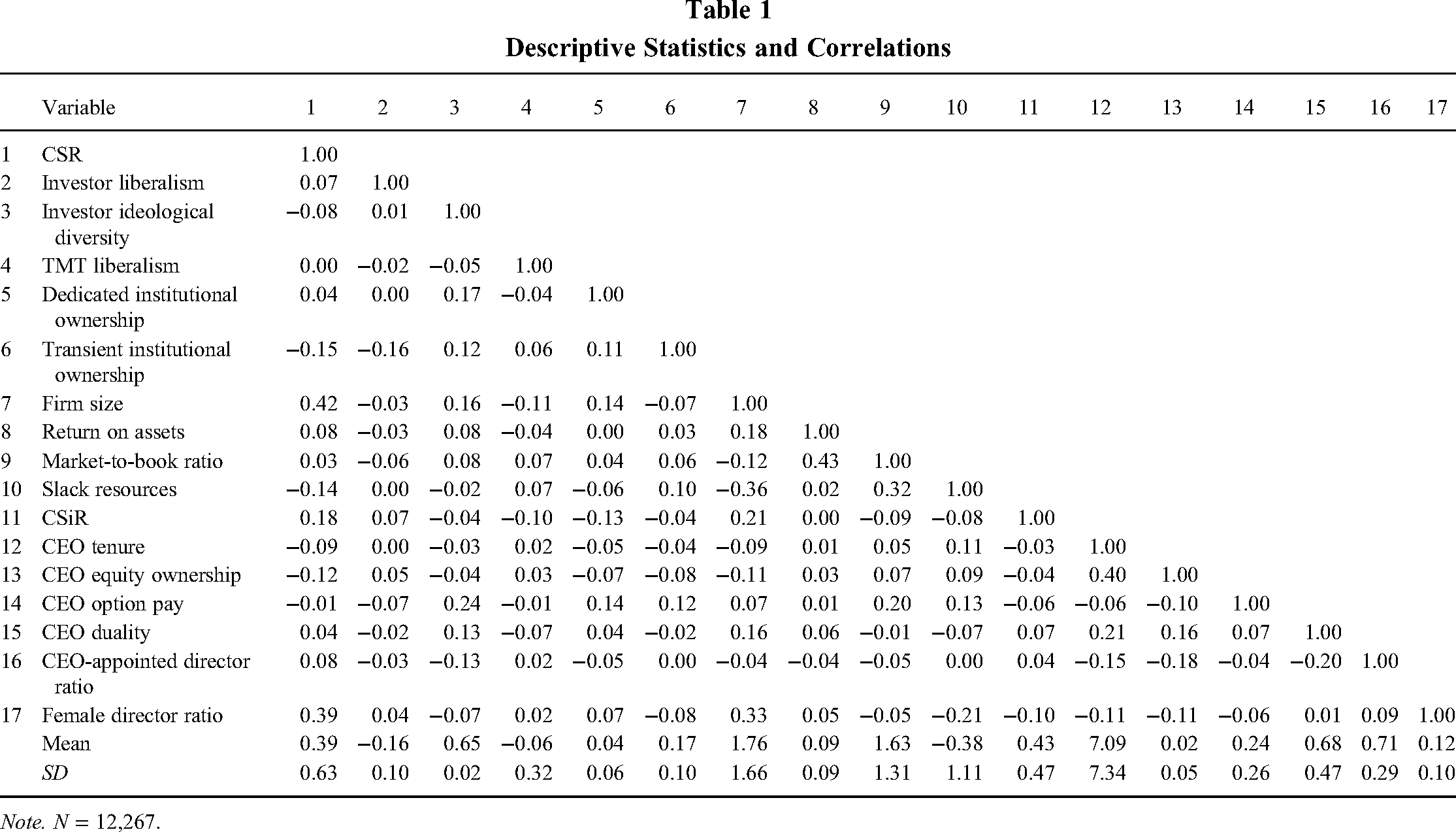

Table 1 shows descriptive statistics and bivariate correlations for all variables included in our study. The variance inflation factor (VIF) is 2.65, well below the conventional threshold of 10, suggesting that multicollinearity is not a concern.

Descriptive Statistics and Correlations

Note. N = 12,267.

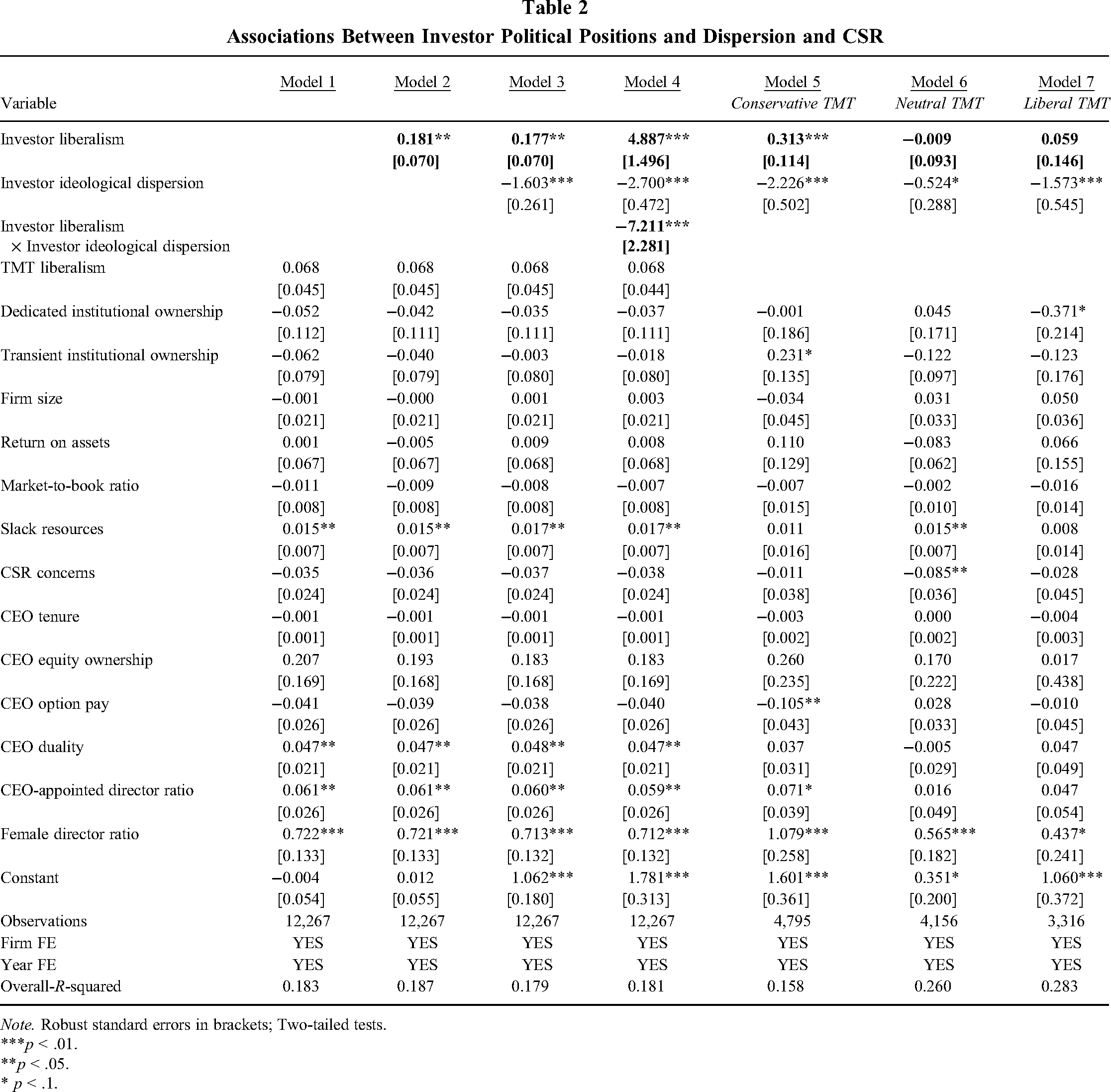

Table 2 reports results of the tests of our hypotheses. Model 1 includes only the control variables. As shown in Model 2, the coefficient for investor liberalism is 0.181 (p < .05), consistent with H1. In terms of economic magnitude, when investor liberalism increases from −1 SD to +1 SD, a firm's CSR increases by about 10%. This increase in CSR is economically on par with similar changes observed after companies are targeted by activist hedge funds (DesJardine & Durand, 2020), or after they experience a major regulatory change (Flammer & Kacperczyk, 2019). In Model 3, the coefficient for investor political dispersion is −1.603 (p < .01), suggesting a negative relationship with CSR.

Associations Between Investor Political Positions and Dispersion and CSR

Note. Robust standard errors in brackets; Two-tailed tests.

***p < .01.

**p < .05.

* p < .1.

Model 4 suggests that investor political dispersion weakens the positive association between investor liberalism and CSR. The coefficient for investor liberalism × investor political dispersion is −7.211 (p < .01), supporting H2. We also tested the moderating effect of investor political dispersion by calculating the marginal effect of investor liberalism when investor political dispersion takes different values (Busenbark, Graffin, Campbell, & Lee, 2022; Wiersema & Bowen, 2009). The marginal effect of investor liberalism on CSR is 0.71 (p < .01) at −1 SD for investor political dispersion, 0.27 (p < .01) at the mean for investor political dispersion, and −0.16 (n.s.) at +1 SD for political dispersion.

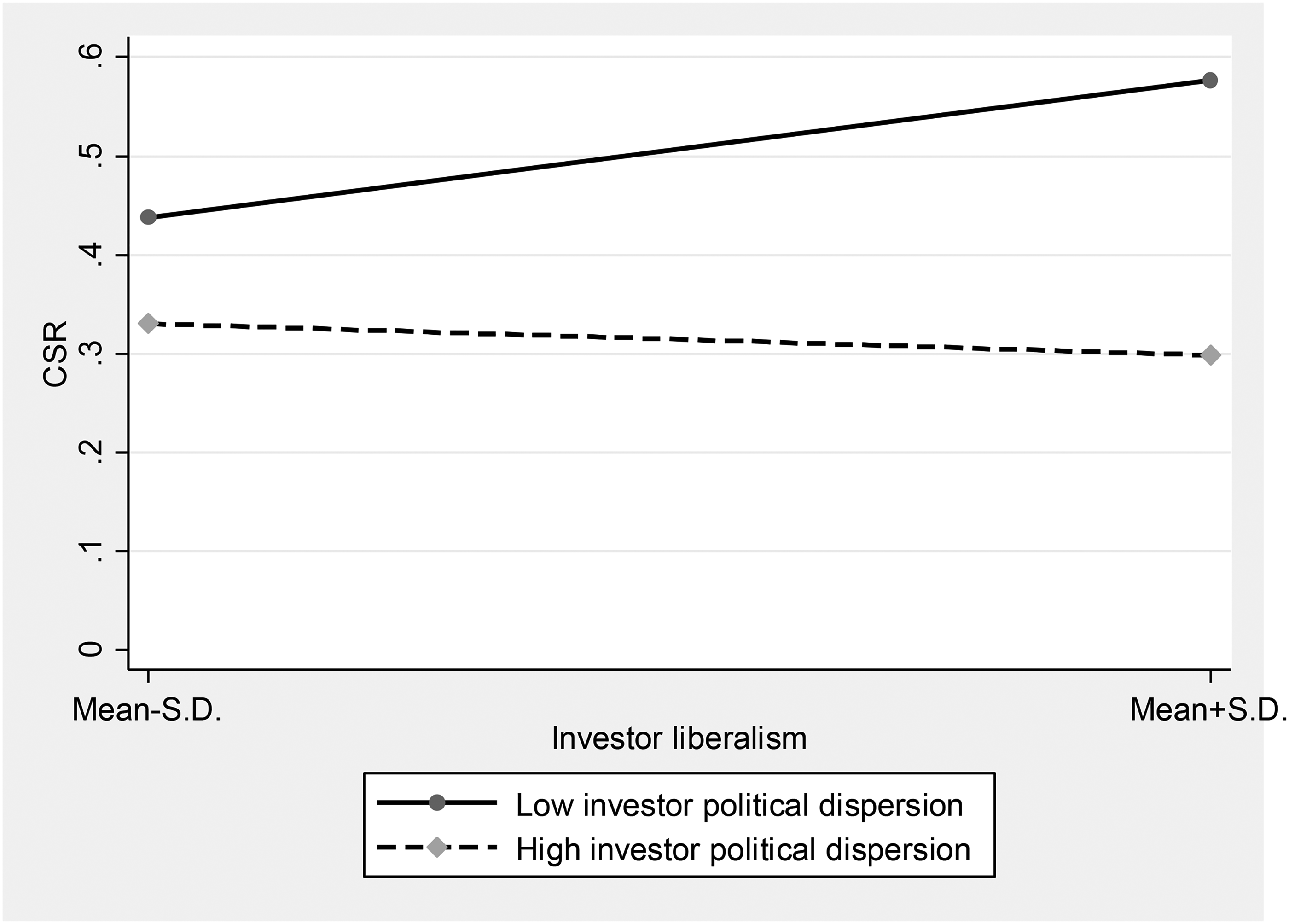

We also plotted the moderating effect of investor political dispersion. As shown in Figure 1, there is a strong positive relationship between investor liberalism and CSR when investor political dispersion assumes a low value (−1 SD, indicated by the solid line); yet, when investor political dispersion assumes a high value (+1 SD, indicated by the dotted line), the relationship between investor liberalism and CSR is negative.

Interaction Between Investor Political Positions and Investor Political Dispersion

H3 suggests that the influence of investor liberalism on CSR is stronger when a firm's TMT is conservative. Because TMT liberalism is largely time invariant 6 and we included firm fixed effects in our regressions, we tested this hypothesis by conducting subgroup analyses. Specifically, we separated our sample into three subgroups: conservative TMTs (TMT liberalism less than 0), politically neutral TMTs (TMT liberalism equal to 0), and liberal TMTs (TMT liberalism greater than 0). Reported in Table 2, the coefficient for investor liberalism in the conservative TMT subgroup (Model 5) is 0.313 (p < .01). In terms of economic magnitude, when investor liberalism increases from −1 SD to +1 SD, the CSR of a firm with a conservative TMT increases by about 15%, which is larger than the increase based on the full sample (i.e., Model 2 of Table 2). In contrast, the coefficient for investor liberalism is 0.009 (n.s.) in the neutral TMT subgroup (Model 6) and 0.059 (n.s.) in the liberal TMT subgroup (Model 7), indicating that investor liberalism may not affect firm CSR activities when managers are politically neutral or liberal leaning. Results from a t test indicate that the coefficient estimates for investor liberalism in Models 5 and 7 are significantly different (p < .05), further supporting H3.

Establishing Causality

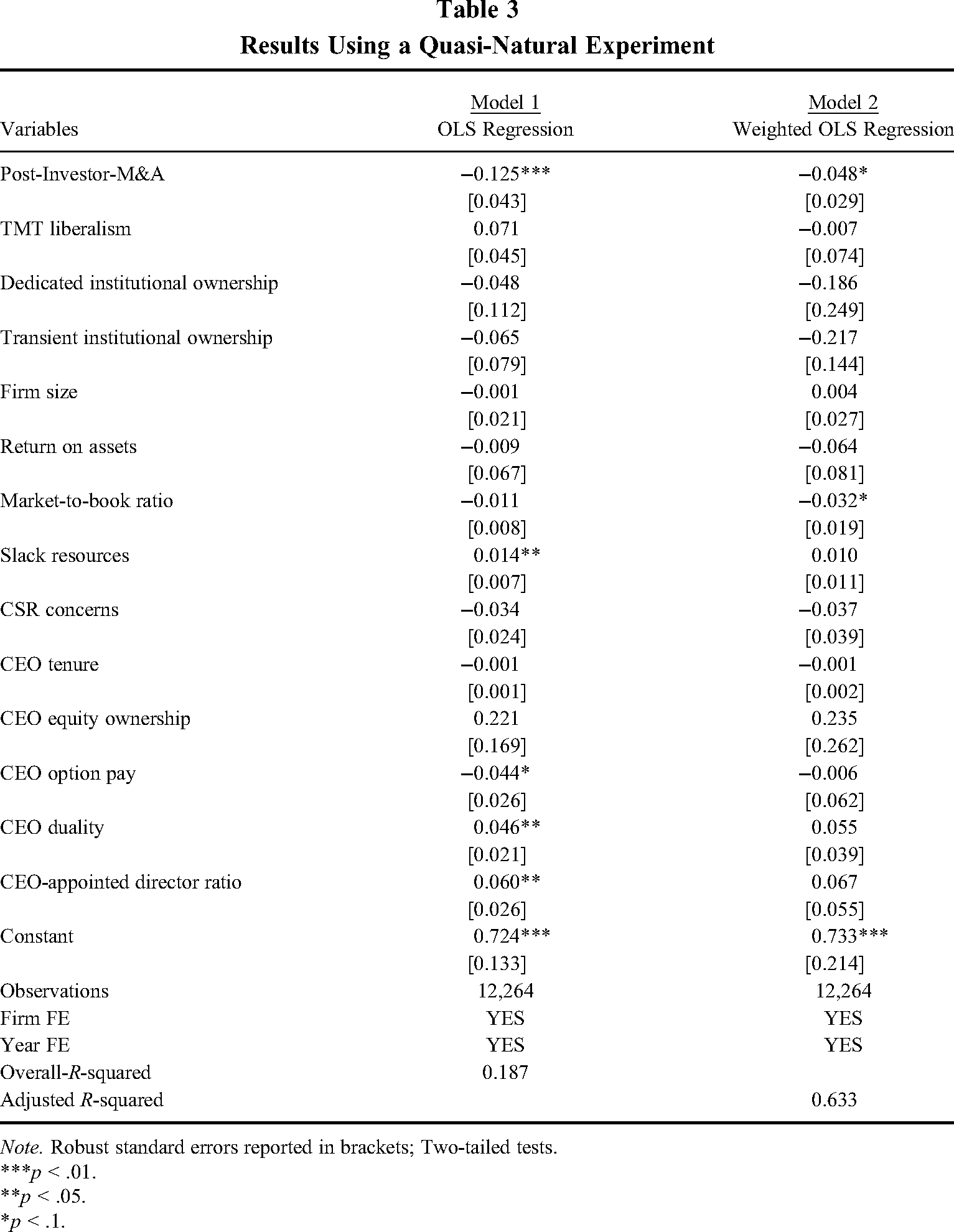

We conducted a quasi-exogenous experiment based on mergers and acquisitions (M&As) among institutional investment brokerages to alleviate the concern that liberal investors choose to invest in firms with high CSR. M&As can create exogenous shocks to a firm's ownership structure, as merging brokerages are driven by institutional investors’ personal strategies rather than the characteristics of firms in which those institutions invest. Thus, we used M&As to exploit exogenous changes in the composition of some firms’ institutional investors.

We used four criteria to identify cases where firms experienced exogenous changes in the extent of ownership by liberal institutional investors. First, we identified M&As among institutional investors between 2000 and 2018 based on data from the SDC Mergers and Acquisitions database. Second, we retained cases where the acquiring investor was conservative, and the target investor was liberal. We classified institutional investors with investor liberalism (based on their donations, as explained above) values above 0 as liberal, and below 0 as conservative. Third, to ensure firms experienced a significant drop in investor liberalism, we retained cases in which the absolute value of the difference between a target investor's liberalism and an acquiring investor's liberalism exceeded 1. 7 Fourth, since a firm may not experience a significant change in investor liberalism if the acquired liberal investor does not have substantial ownership in the firm, we excluded M&As where the acquired investor owned less than 1% of the target firm. Based on these criteria, we identified 141 firms that experienced an exogenous drop in investor liberalism triggered by acquisitions of liberal institutional investors by conservative institutional investors. 8

Using these data, we coded post-investor M&A as 1 for the firm-years after a firm experienced a significant drop in investor liberalism triggered by investment brokerage M&As, and 0 otherwise. As shown in Model 1 of Table 3, the coefficient for post-investor M&A is −0.125 (p < .01), suggesting that CSR decreases in firms after an exogenous drop in investor liberalism, consistent with our findings and theory.

Results Using a Quasi-Natural Experiment

Note. Robust standard errors reported in brackets; Two-tailed tests.

***p < .01.

**p < .05.

*p < .1.

Results from t tests suggest that treatment firms differ from control variables along several firm-level characteristics (e.g., firm size, firm performance, and female director ratio). Accordingly, firms that experienced a significant drop in investor liberalism (i.e., treatment firms) may not be comparable to firms that have not experienced a significant drop in investor liberalism (i.e., control firms). To alleviate this concern, we implemented entropy balancing, which reweights control observations so that the post-weighting means of treatment firms and control firms are nearly identical (Shi & DesJardine, 2022). Compared to propensity score matching and coarsened exact matching, entropy balancing is advantageous in that it ensures covariate balance without sacrificing observations (Hainmueller, 2012). We used weights generated from entropy balancing and conducted a weighted regression. As reported in Model 2 of Table 3, the coefficient for post-investor M&A using an entropy balanced sample is −0.048 (p < .10, two-tailed test), further confirming our main findings.

Supplementary Analyses

To test this idea, we measured CEO compensation as the natural logarithm of CEO total compensation, as reported in ExecuComp. We controlled for firm size, slack, market-to-book ratio, CEO tenure, CEO duality, CEO appointed director, dedicated institutional ownership, and transient institutional ownership, because these variables have been shown to predict CEO compensation (Shi, Connelly, Mackey, & Gupta, 2019). We also controlled for industry fixed effects (based on the Fama-French 17 industry classification) and year fixed effects, because CEO compensation can vary across industries and be subject to macro-economic factors.

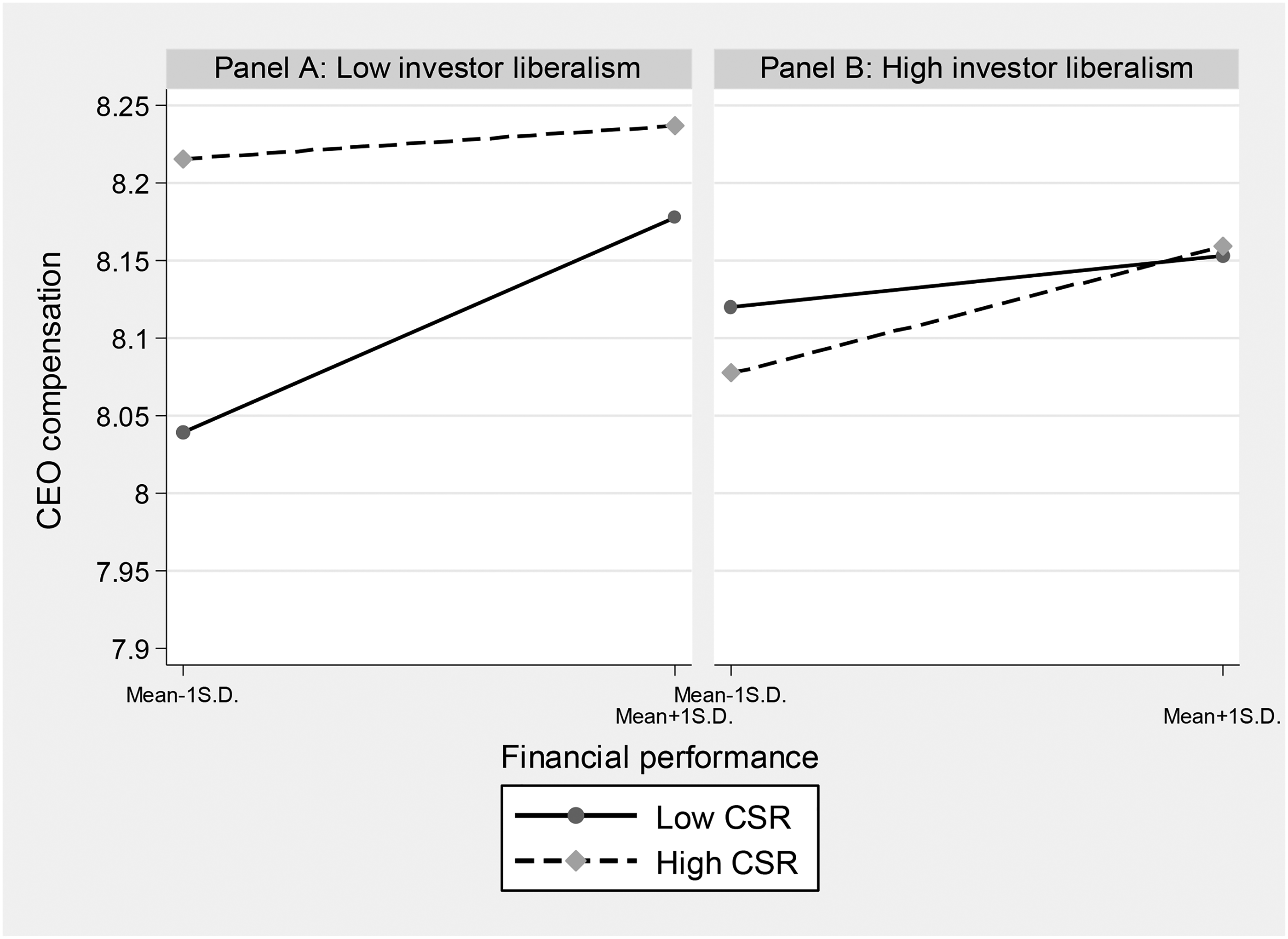

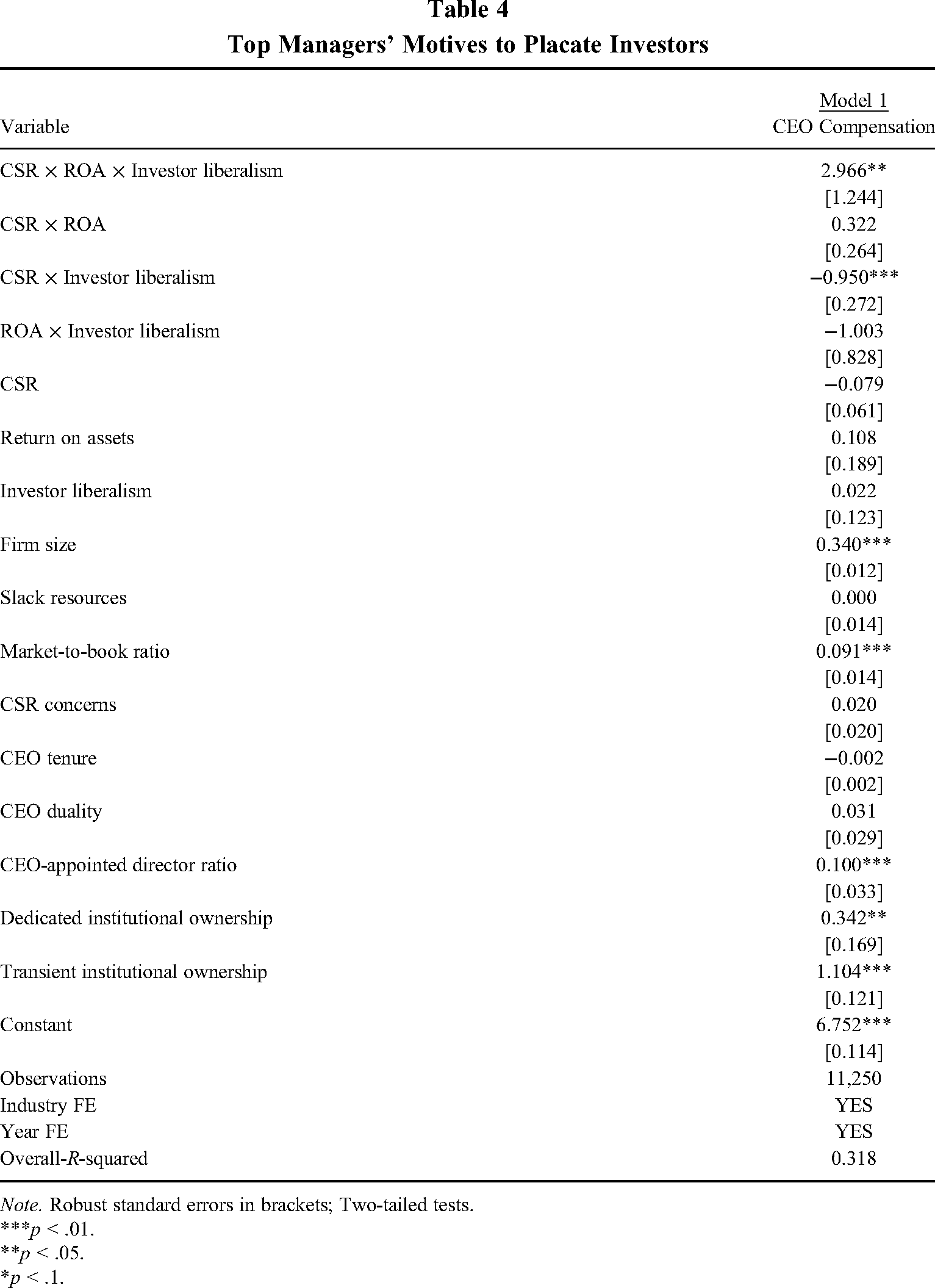

As shown in Model 1 of Table 4, where CEO compensation is the dependent variable in an OLS regression, the coefficient for CSR × financial performance × investor liberalism is 2.966 (p < .05). To facilitate interpretation, we plotted the triple interaction effect in Figure 2. As shown in Panel A, when investor liberalism is low, we observe a weak positive relationship between financial performance CEO compensation in the presence of high CSR, but a strong positive relationship between financial performance and CEO compensation in the presence of low CSR. As shown in Panel B, when investor liberalism is high, there is a stronger (weaker) relationship between financial performance and CEO compensation in the presence of high CSR (low CSR). In line with our theory, these findings suggest that CEOs are rewarded more for investing in CSR when their investor base leans more liberal.

Interaction Between Financial Performance and CSR With Different Political Positions of Investors

Top Managers’ Motives to Placate Investors

Note. Robust standard errors in brackets; Two-tailed tests.

***p < .01.

**p < .05.

*p < .1.

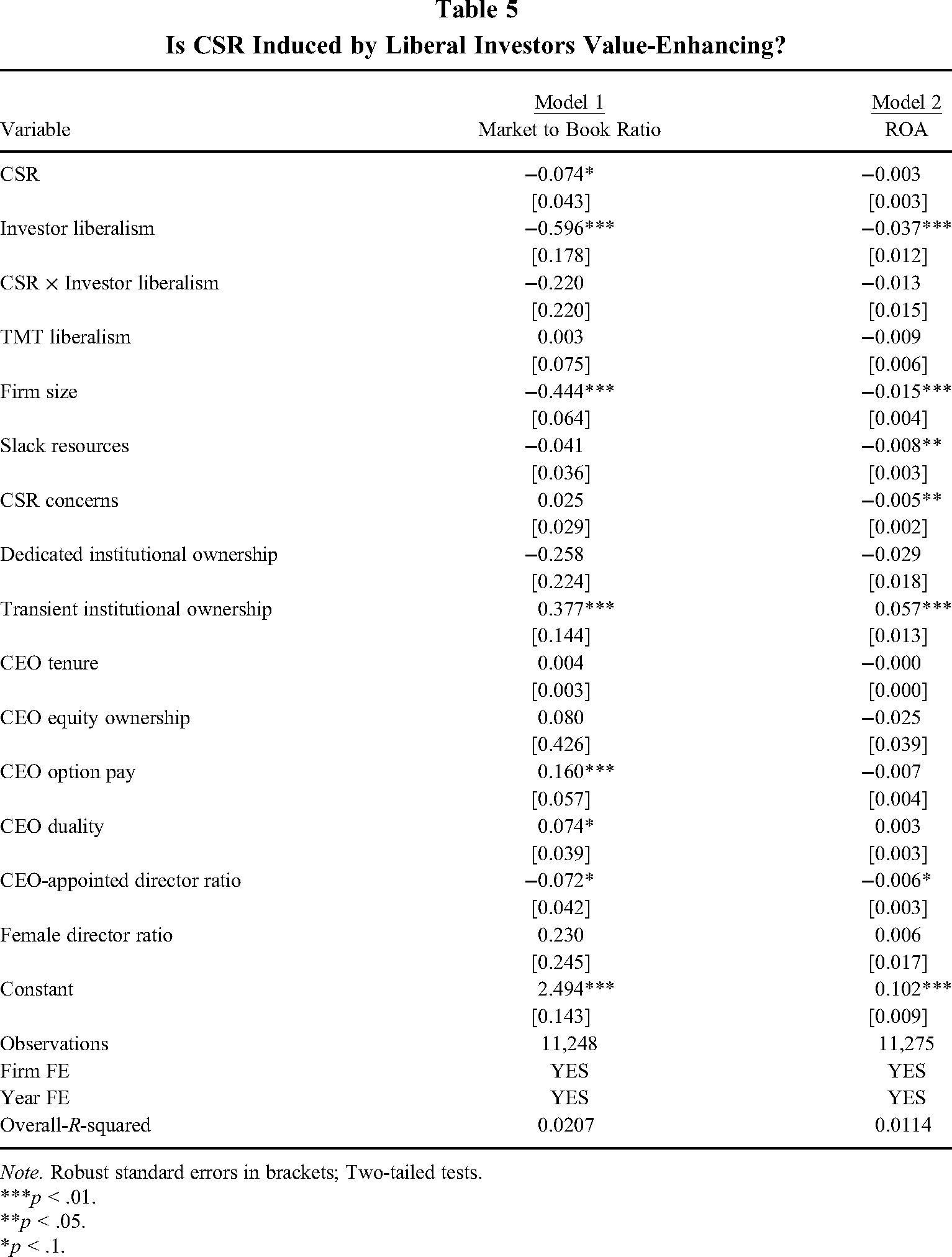

Reported in Table 5, Model 1 uses market-to-book ratio as the dependent variable and shows that the coefficient for CSR × investor liberalism is negative and statistically not significant. In Model 2, with ROA as the dependent variable, the coefficient estimate of this interaction term is also negative and statistically not significant. In addition, the coefficient for investor liberalism is negative and statistically significant in both models, suggesting that investor liberalism is negatively associated with firms’ future performance. These findings collectively suggest that CSR investment triggered by liberal institutional investors does not enhance shareholder value and firm profits.

Is CSR Induced by Liberal Investors Value-Enhancing?

Note. Robust standard errors in brackets; Two-tailed tests.

***p < .01.

**p < .05.

*p < .1.

DISCUSSION

Our study offers a first look at how shareholder politics can influence managerial decision-making and corporate activity. Acknowledging that institutional investors are some of the most active political players, and recognizing a dearth of research on their political loyalties, we identified a need to better understand the role of shareholder politics in management. We tested how investors’ political positions and political dispersion affect firm CSR, and argued that such influence occurs through two channels: investors actively shaping managerial decision-making based on their political preferences, and managers discerning their investors’ preferences based on their political partisanship.

Three findings emerged from our study. First, we found a positive relationship between liberal-positioned investors and firm CSR. Second, we found that this effect is weakened when investors’ political affiliations are more dispersed. When investors’ political positions are less aligned, managers find it difficult to discern their investors’ dominant views and values and to manage CSR accordingly. Third, we found that the positive effect of liberal-positioned investors on CSR is stronger for firms with conservative managers. Here, we reasoned that when both investors and managers are liberal, investors do not work as hard to monitor managers and shape their decisions, and managers are less concerned about satisfying these investors’ full range of preferences; however, when investors are dominantly liberal and managers are conservative, tensions between the two groups are elevated and CSR is used by managers as a tool to assuage them.

These findings provide initial evidence that investors’ political affiliations—reflected in their political donations—play an important role in business. Yet, given limited research on this topic, we contend that our findings should serve as just the starting point for a promising stream of research on shareholder politics. As we now discuss, many unanswered questions remain.

A Promising Future for Research on Shareholder Politics

We see great promise for the future of research on shareholder politics in management and organizational studies. Our view is grounded in two observations from research, and two from practice. Since Chin and colleagues (2013) studied how CEOs’ political ideologies affect CSR, management scholars have taken great interest in how the political donations of CEOs, board members, and employees can affect an array of firm outcomes (Swigart et al., 2020). In another burgeoning stream of research, scholars have sought to unpack how different aspects of investors’ orientations, including class, characteristics, and composition, can affect firm outcomes (DesJardine et al., 2022b). These two streams of research, however, have not yet been integrated to examine how investors’ political partisanship shapes their influence on firms.

From a practice perspective, institutional investors and their affiliates are now the most active contributors to political parties, and many investors are not shy about publicly sharing their political views and opinions. As CEOs and directors also donate to politics, how these different actors’ political positions play out and intersect in the management of public and private companies is multifaceted. Beyond the sheer amount of political giving among investors, a second observation from practice relates to increasing overlaps between the investment industry and politics. Reflecting the new and unusual ways these two worlds are coming together, politicians are increasingly joining or starting investment brokerages (e.g., in 2020, former White House Chief of Staff Mick Mulvaney started the hedge fund Exegis) and investment managers are increasingly becoming politicians (e.g., hedge fund manager Alan Grayson joined the U.S. Congress as a member of the Financial Services Committee). Given these emerging trends, it is time for management scholars to take seriously the challenge of understanding the changing world of shareholder politics and implications for organizational life.

Looking ahead, shareholder politics may be relevant for organizations of all sizes. In entrepreneurship, we see value in examining how shareholder politics shape the success and outcomes of entrepreneurial ventures. Are venture capitalists, for instance, more likely to fund start-ups led by founders who share their political convictions? Do venture capitalists consider the political alignment between founding team members in their funding decisions? And how do entrepreneurs’ political positions shape the types of businesses they start? With a stronger desire for tradition, conservatives might favor businesses in more conventional industries; however, liberal founders might favor businesses in more dynamic industries or seek to identify firms with potential to disrupt an industry. How the political positions of founding teams and the positions of their advisors and investors interact is an unexplored, but promising avenue for shareholder politics research.

Another avenue that holds promise is how shareholder politics shape coordination activities among investors in ways that affect their portfolio firms’ collaborative efforts. In particular, we suspect that collective action among investors with the same political position could translate into heightened collaborative activities among their portfolio firms. For example, if managers perceive that investors are inclined to support strategic collaboration with other firms owned by investors with the same political position, two firms owned by politically aligned investors could be more likely to pursue joint ventures, strategic alliances, or mergers, than two firms owned by politically opposed investors. Given the potential for common ownership to encourage coordination (Connelly, Lee, Tihanyi, Certo, & Johnson, 2019), it may also be that firms with more politically aligned investors are less willing to escalate competition with each other. Future work should consider whether politically aligned investors act as intermediaries that guide inter-firm competitive activities.

Relatedly, shareholder politics may also inform research on how executives manage their relationships with investors (DesJardine & Shi, 2022). Noting the power that institutional investors can wield, Westphal and Bednar (2008) showed that managers resort to ingratiation tactics with investors to extract private benefits for themselves. Our supplemental analyses show that CEOs can benefit from pursuing the types of activities (i.e., CSR) desired by liberal investors, suggesting the possibility that managers advance their personal interests by aligning their firms’ actions with investors’ political positions. This raises an interesting question: By motivating managers to undertake actions that placate some investors at the potential expense of others, can shareholder politics sow the seeds of agency problems? If so, how do the political positions of other actors affect the likelihood of such problems? Hambrick, Misangyi, and Park (2015), for instance, identified four characteristics that indicate the potential effectiveness of directors’ monitoring. Connecting shareholder politics to their model, it is possible that the effectiveness of board monitoring depends on board members’ political alignment with investors and the degree of political dispersion among board members.

Implications for Research on Political Giving and Ideology

Beyond providing a foundation for studying shareholder politics in greater depth, our study makes multiple contributions to several different bodies of literature, which we now discuss.

We have offered a first look at how investors’ political affiliations affect firm outcomes. Findings reported by finance scholars suggest that fund managers’ portfolio selection decisions reflect their political giving (Bolton et al., 2020; Kim et al., 2019). Meanwhile, in numerous management studies (e.g., Chin et al., 2013; Christensen et al., 2015), scholars have investigated how the ideologies of CEOs, board members, and employees (measured based on their donations to different political parties) affect various firm outcomes. Within this growing body of work, we know of no studies in which researchers have considered the effects of investors’ political affiliations as reflected in their donations to different political parties. As such, we have broadened this line of research to encapsulate investors.

Our findings provide two new insights into how political alignment within and between groups matters in managerial decision-making. First, we have shown how political alignment within groups, namely investors, can affect their influence on firm outcomes. Because individuals tend to view those in different political camps as less competent, reliable, or trustworthy (Iyengar & Westwood, 2015), diversity in political views and values can hamper their ability to cooperate and engage in collective action. Despite the potential effects of dispersion on group dynamics, management researchers thus far have focused on the average political position among a group of actors as a point estimate along the liberal-conservative spectrum. We have introduced the concept of “political dispersion” to showcase how variance in group members’ political views and values also affects their collective influence.

Second, we have shown how political alignment between groups, namely investors and managers, can shape firm outcomes. When considering a course of action based on the perceived preferences of others, an individual is likely to account for how those potential actions align with their own views and values. Applying this idea to our context, we found that the effect of investors’ political positions on firm outcomes is contingent on the managers’ own political positions. Specifically, strong alignment between investors and managers mitigates the influence of investors’ positions, while contrasting political positions between investors and managers leads to a greater perceived need to monitor activities and influence firm outcomes. Hence, by looking both within and between groups, our study provides a closer examination of how political (mis)alignment can regulate the influence of actors’ political partisanship on firm outcomes.

Implications for Research on Corporate Governance and Investor Influence

The body of research on how investors influence firm outcomes is large and growing. Within this work, scholars have identified various economic and strategic attributes of investors that can affect managerial decision-making and firm outcomes, including investors’ horizons and portfolio concentration, as well as investors’ investment experience, foreignness, and business ties (Connelly et al., 2010; DesJardine et al., 2022b; Shi & Hoskisson, 2021). Our findings provide a broader understanding of the attributes that can explain investors’ influence on firm outcomes by revealing the role of investors’ political affiliations.

More speculatively, our study may illuminate how shareholder politics can potentially give rise to principal–principal agency conflicts. The findings in our study raise interesting questions, particularly regarding whether liberal investors nudge firms to maximize the value of CSR, or push them beyond the threshold of value maximization to the financial detriment of companies and their shareholders. Since our main focus was on unpacking the degree of investor influence, we conducted supplementary analyses to consider the financial implications of investor liberalism on CSR. In untabulated results, we found that the interaction effect of investor liberalism and CSR on firms’ annual stock returns is insignificant. While preliminary, this finding suggests that increasing CSR investment in the presence of liberal investors does not necessarily create value, indicating that the CSR improvements that follow liberal investors might be predominantly ideologically driven, and may create conflicts between principals with different orientations. In line with our findings on investor political dispersion, investors who prioritize financial returns may push back when managers use corporate resources to placate liberal investors’ preferences for CSR.

Implications for Research on Corporate Social Responsibility

Our study contributes to research on CSR by demonstrating the influence of investors’ political positions on firms’ CSR activities. Among several other investor characteristics, existing research has shown that short-term investors can reduce investments in CSR and non-shareholding stakeholders (for a review, see DesJardine et al., 2022b). Integrating research on political ideologies (Chin & Semadeni, 2017; Gupta & Wowak, 2017) into this line of work, we have provided evidence that political partisanship also plays a role in shaping investors’ influence on CSR. Considering the role of political partisanship yields important insights because evidence shows that investors’ actions are driven not only by traditional investment objectives, but also by their broader views and values, as reflected in their political donations and positions.

Relatedly, prior research shows that investors can influence CSR by accumulating ownership stakes in firms (DesJardine & Durand, 2020) based on the argument that ownership grants investors power and influence (e.g., DesJardine et al., 2022a). In contrast, limited attention has been devoted to explaining variation in investors’ capacity to exert their influence once shares are acquired. Some scholars have examined the influence of different activism tactics (e.g., Eesley, Decelles, & Lenox, 2016), but this tells us little about how investors coordinate to exert influence over a focal company. This gap is noteworthy, because even investors who own a substantial portion of a firm's shares may have limited influence if other investors hold conflicting views, as evidenced by our finding that ideological dispersion constrains the influence of investor liberalism on firm outcomes.

Limitations and Opportunities for Future Research

Beyond opening many new avenues to explore shareholder politics in management, our study provides various other opportunities for future research, several of which stem from its limitations. As a starting point, although our theory should apply to various manifestations of shareholders’ values, we focused our hypotheses on political positions as reflected in investors’ political donations. In future work, scholars could examine whether our theory holds when other types of views and values diverge, such as positions on authority or liberty (Haidt, 2012).

Additionally, since we did not directly measure investors’ political ideologies, researchers might examine whether our theorizing holds with more direct measures. Using political donations to measure different actors’ ideologies has become commonplace. However, we have purposely refrained from using the term “ideology” because political donations do not necessarily reflect an individual's ideological beliefs. Especially in the business context, a CEO, director, employee, or investor's donation to a certain political party may be motivated by a desire to advance a business objective rather than ideological beliefs. Stuckatz (2022), for instance, recently found that a company's political goals can influence how employees allocate their political donations. Acknowledging this potential disconnect, we have used the terms “political position” and “political dispersion,” which we hope will guide researchers in future work. In particular, we believe that probing the decision-making process underlying donations to more conservative or liberal political entities in business contexts could yield important insights.

As managers balance various pressures and demands (Freeman, Harrison, Wicks, Parmar, & De Colle, 2010), other forces we have not considered may further shape how they attend to stakeholder interests amid different balances of ownership between liberal and conservative investors. For example, institutional forces, including legal, environmental, and societal developments, may alter the balance of power between managers, shareholders of different political affinities, and other stakeholders, changing the observed outcomes. Likewise, other factors, such as employee unionization, may enhance some stakeholders’ power and either subdue or reinforce the influence of investors’ political positions on certain dimensions of CSR, such as employee treatment.

CONCLUSION

Investors are active political donors with strong and sometimes strongly polarized political views and values. Understanding that political donations may reveal important information, managers seem to attempt to discern the views and values of investors based on their donations, and account for those preferences in their decision-making. Laying important groundwork for the study of shareholder politics in management, we have opened many opportunities for future research at the intersection of politics and business.

Footnotes

2.

Consider a top management team comprised entirely of moderately liberal executives and another comprised mostly of extremely liberal executives with a few extremely conservative executives. Even if the two management teams had the same average political position, their different political dispersions would likely result in very different internal group dynamics.

3.

We view CSR as a socially constructed attribute of firms, or collection of attributes, such that there may be some decoupling between general perceptions and evaluations of a firm’s CSR and actual environmental and social performance.

4.

A recent finance study by ![]() used proxy voting records to capture institutional investors’ political positions. Yet, such an approach is inappropriate in our research context for two reasons. First, proxy voting records are only readily available for mutual funds. Meanwhile, most mutual funds are passive shareholders whereas other types of institutional investors, such as pension funds or activist hedge funds, play a more active governance role (Del Guercio & Hawkins, 1999). Thus, relying on proxy voting records would limit our sample to only passive investors (mutual funds, in this case). Second, a shareholder’s voting records can be endogenous to our dependent variable. For example, firms with poor records of protecting the interests of employees likely would receive more employment and human rights proposals. We thus chose to identify institutional investors’ ideological positions based on fund managers’ political campaign contributions.

used proxy voting records to capture institutional investors’ political positions. Yet, such an approach is inappropriate in our research context for two reasons. First, proxy voting records are only readily available for mutual funds. Meanwhile, most mutual funds are passive shareholders whereas other types of institutional investors, such as pension funds or activist hedge funds, play a more active governance role (Del Guercio & Hawkins, 1999). Thus, relying on proxy voting records would limit our sample to only passive investors (mutual funds, in this case). Second, a shareholder’s voting records can be endogenous to our dependent variable. For example, firms with poor records of protecting the interests of employees likely would receive more employment and human rights proposals. We thus chose to identify institutional investors’ ideological positions based on fund managers’ political campaign contributions.

5.

We excluded TMT liberalism as a control variable when testing the moderating effect of TMT liberalism.

6.

The measure of each top manager’s political position is time-invariant; yet, top manager turnover can affect TMT liberalism.

7.

If we require the threshold of the difference to be less than 1, the difference in investor liberalism change may not be significant. However, if we require the absolute value of the difference to be greater than 1, we are unable to identify a meaningful number of M&As among investors.

8.

Results are similar if we use 2% as the cut off to identify sufficient institutional investor ownership. We do not use 5% as the cut off, as we can only identify four treatment firms in this scenario.