Abstract

Research on how shareholders influence the interests of stakeholders has proliferated in recent years, at pace with the active debate on the merits of “stakeholder capitalism.” This research has sought to unpack: (1) the types of shareholders that affect stakeholder-relevant firm outcomes, (2) the mechanisms through which shareholders exert their influence on stakeholders’ interests, (3) the types of stakeholders that are influenced by shareholders, and (4) the factors that moderate the influence of shareholders on stakeholder-relevant firm outcomes. However, this literature is highly fragmented, as it spans the boundaries of various disciplines, draws on different theoretical frameworks, and is based on diverse assumptions. Moreover, exsiting research discusses outcome variables that are relevant to stakeholders, but not from the perspective of stakeholder interests. A comprehensive review of the literature is essential for understanding the heterogeneity of shareholders in terms of their impact on other stakeholders. In the absence of such an endeavor, we systematically review, synthesize, interpret, and critique literature published over the past three decades in leading management, sociology, finance, and accounting journals. Focusing on articles about how shareholders influence stakeholder interests through firms' decisions and outcomes, we chart a promising path for future studies to more fully unpack the complex relationships between shareholders and various other stakeholders.

Keywords

There is a growing need for scholars to provide systematic evidence on how different shareholders influence the welfare of stakeholders. As “shareholder value maximization has become so well ingrained in the mindset of executives” (Goranova & Ryan, 2022: 576), shareholders occupy a privileged position to place formal demands on companies and their executives. Unlike many non-shareholding stakeholders, shareholders can often directly meet with executives to voice their interests, file proposals and vote on resolutions to make their preferences widely known, and divest their ownership to penalize management when their demands are not met (Fox & Lorsch, 2012). Accordingly, as managers are called to gear corporate decisions to encompass a broader set of stakeholder interests (Harrison, Phillips, & Freeman, 2020), how they cater to those interests is likely to be contingent on the composition of their companies’ shareholder base.

Moreover, discussions on the tradeoffs between shareholder and stakeholder interests and the purpose of the firm—often under the parlance of shareholder versus stakeholder primacy—have received significant scholarly attention in recent years (e.g., Goranova & Ryan, 2022; Inkpen & Sundaram, 2022). Yet, unlike early supporters of shareholder primacy, who propose shareholders have a single profit-maximizing objective function (Sundaram & Inkpen, 2004), recent studies reveal substantial variance in the characteristics and orientations of different shareholders, some of which prioritize long-term social returns. By mapping different shareholders and summarizing findings on how they differentially impact various stakeholders, a systematic review can provide a new angle on these discussions and better illuminate where shareholder and stakeholder interests collide, and where they do not. With this in mind, we ask: How does the influence of different shareholders affect how companies attend to the interests of their stakeholders?

Our review answers this question from a multi-shareholder and multi-stakeholder perspective. Specifically, we synthesize and critically assess the growing body of research on the role that different categories of shareholders play in shaping corporate practices and policies that can either advance or undermine the diverse interests of non-shareholding stakeholders (hereafter “stakeholders”). We define “influence” broadly, allowing our review to encompass studies that examine activist shareholder tactics (e.g., proposals or private meetings) as well as nonactivist trends (e.g., active or passive changes in ownership). Across the fields of management, sociology, finance, and accounting, scholars have been increasingly seeking to uncover how the influence that shareholders exert on corporate activities affects the interests of diverse types of stakeholders, including communities, customers, and creditors. However, because of the different theoretical frameworks and methodologies that are applied in different fields, this body of research is fragmented and in urgent need of a comprehensive review.

The most relevant reviews, summarized in Table OA1 of the online appendix, focus on (1) the effects of shareholder ownership on firms’ financial outcomes, (2) stakeholder theory, and (3) corporate social responsibility (CSR) in the shareholder–stakeholder context. None of these studies, however, adequately answers our focal research question, leaving us with an incomplete view of how different shareholders influence the welfare of stakeholders. Specifically, prior ownership reviews (Boyd & Solarino, 2016; Connelly, Hoskisson, Tihanyi, & Certo, 2010; Gomez-Mejia, Cruz, Berrone, & De Castro, 2011; Goranova & Ryan, 2014) mostly emphasize financial outcomes that are relevant to shareholders, such as the firm's performance, but overlook nonfinancial outcomes relevant to other stakeholders. Similarly, reviews of the literature on stakeholder theory (Laplume, Sonpar, & Litz, 2008; Parmar et al., 2010) synthesize studies that apply or extend stakeholder theory but omit much of the literature on shareholders and their influence on stakeholders. Yet, as we show, few of the studies that do examine the influence of shareholders on stakeholders actually use stakeholder theory. Finally, reviews that bring clarity to the literature on CSR (Aguinis & Glavas, 2012; Bansal & Song, 2017; Rao & Tilt, 2016) do not focus explicitly on the role of shareholders in this context. Although some of these reviews capture specific research on management, they overlook studies in related disciplines that need to be included in a comprehensive review.

Our review makes three focal contributions. First, our review provides new insights about how shareholders influence stakeholders. We achieve this by (1) introducing a framework for classifying different types of shareholders, (2) pinpointing the core mechanisms through which shareholders influence stakeholder interests, and (3) classifying the moderators that shape different forms of shareholder influence on stakeholders. We provide a detailed map of the literature to reveal the various channels through which different types of shareholders impact stakeholder-relevant firm outcomes. We use this map to further classify shareholders into four categories based on their investment horizons and orientations, and summarize how each category of shareholder differentially hinders or promotes varying stakeholder interests.

Second, we review the dominant theoretical lenses and perspectives that have been applied to study how shareholders influence stakeholder interests. We show that the most widely used theory by far is agency theory (e.g., Francis & Smith, 1995), followed at a distance by institutional theory (e.g., David, Bloom, & Hillman, 2007), and, lastly, by various other theories that have been sparsely applied, such as stakeholder theory (e.g., Wang, Jia, & Zhang, 2021), signaling theory (e.g., Ridge, Hill, & Ingram, 2018), or resource dependence theory (e.g., Shi, Gao, & Aguilera, 2021). All of these theories provide distinct assumptions about shareholders and postulate different mechanisms through which shareholders influence firm decision-making—what we term “the channels of shareholder influence.” We use these theories to categorize the main mechanisms through which shareholders shape corporate decisions related to stakeholder interests.

Third, on the basis of the insights gleaned from our review, we develop a promising agenda for future research. As we explain, certain types of shareholders (e.g., transient or dedicated shareholders) and channels of shareholder influence, such as voice (e.g., Kochhar & David, 1996) and exit (e.g., Liu, van Jaarsveld, Batt, & Frost, 2014), have received considerable attention from researchers, whereas other types of shareholders and influence channels have been largely overlooked. Similarly, whereas some theories have dominated the literature, others that have been largely overlooked hold potential to provide new insights. Finally, we recognize that different types of shareholders vary in terms of class, characteristics, and channels of influence, leading us to conclude our review by proposing a three-step process (the “three Cs”) that researchers can apply to dissect the subject of shareholder influence more systematically.

Methodological Scope and Review Process

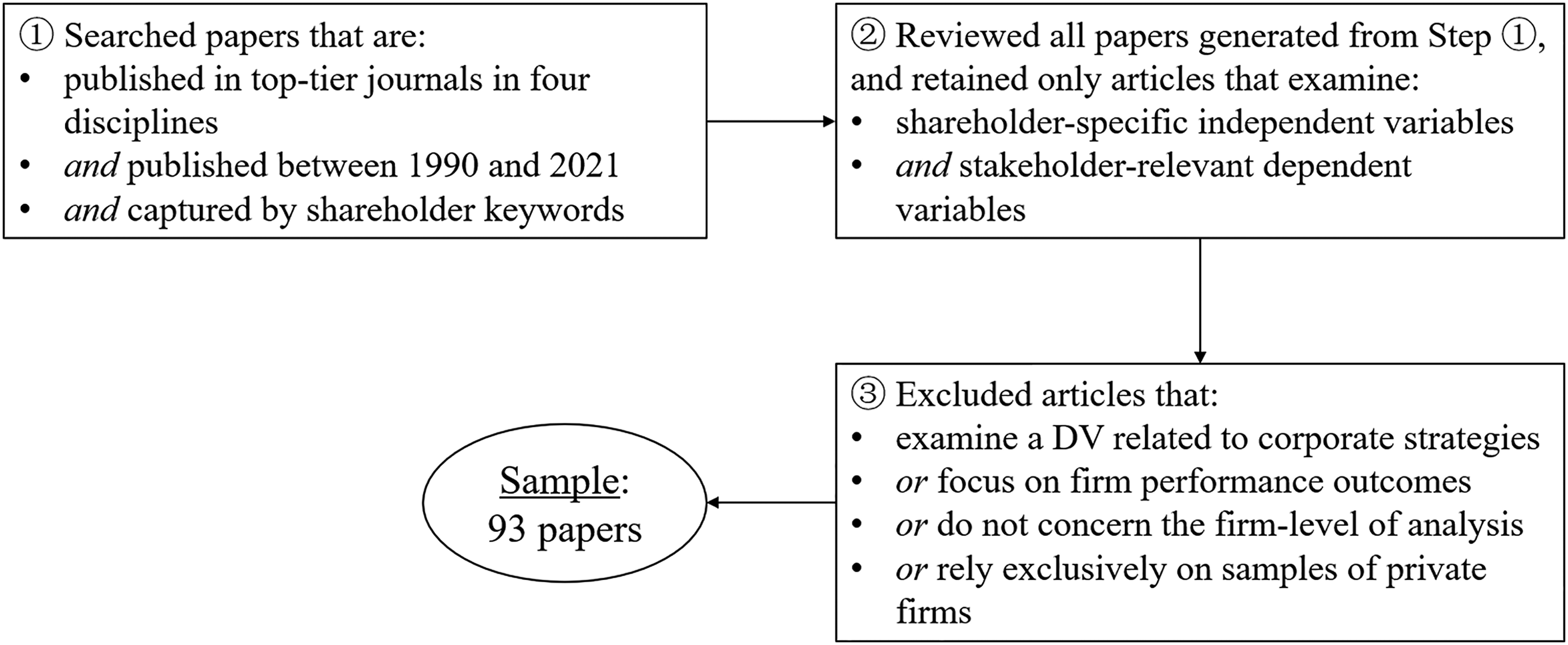

We conducted a systematic literature review (Hiebl, 2021; Tranfield, Denyer, & Smart, 2003) by collecting and reviewing studies that show how various forms of shareholder influence affect the interests of different stakeholders. Figure 1 outlines the process of our collection methods, and Table OA2 lists complete details of our inclusion and exclusion criteria. In addition to retaining articles published between 1990 and 2021, 1 we bound the scope of this review in three ways. First, we limited our search to top-tier management, sociology, finance, and accounting journals. 3 Second, we used broad keywords to capture works relevant to different types of shareholders. Third, we retained from the initial selection only articles that examine both an external shareholder-specific independent variable and a stakeholder-relevant dependent variable. Each included study must therefore discuss at least one dependent variable that directly or indirectly captures the interests of any of the following six stakeholder groups: communities, customers, creditors, employees, governments, and the natural environment. Our search yielded 93 papers.

Methodological Process for Collecting Relevant Studies on Shareholder Influence of Stakeholders

A Process and Typology for Mapping Shareholder Influence

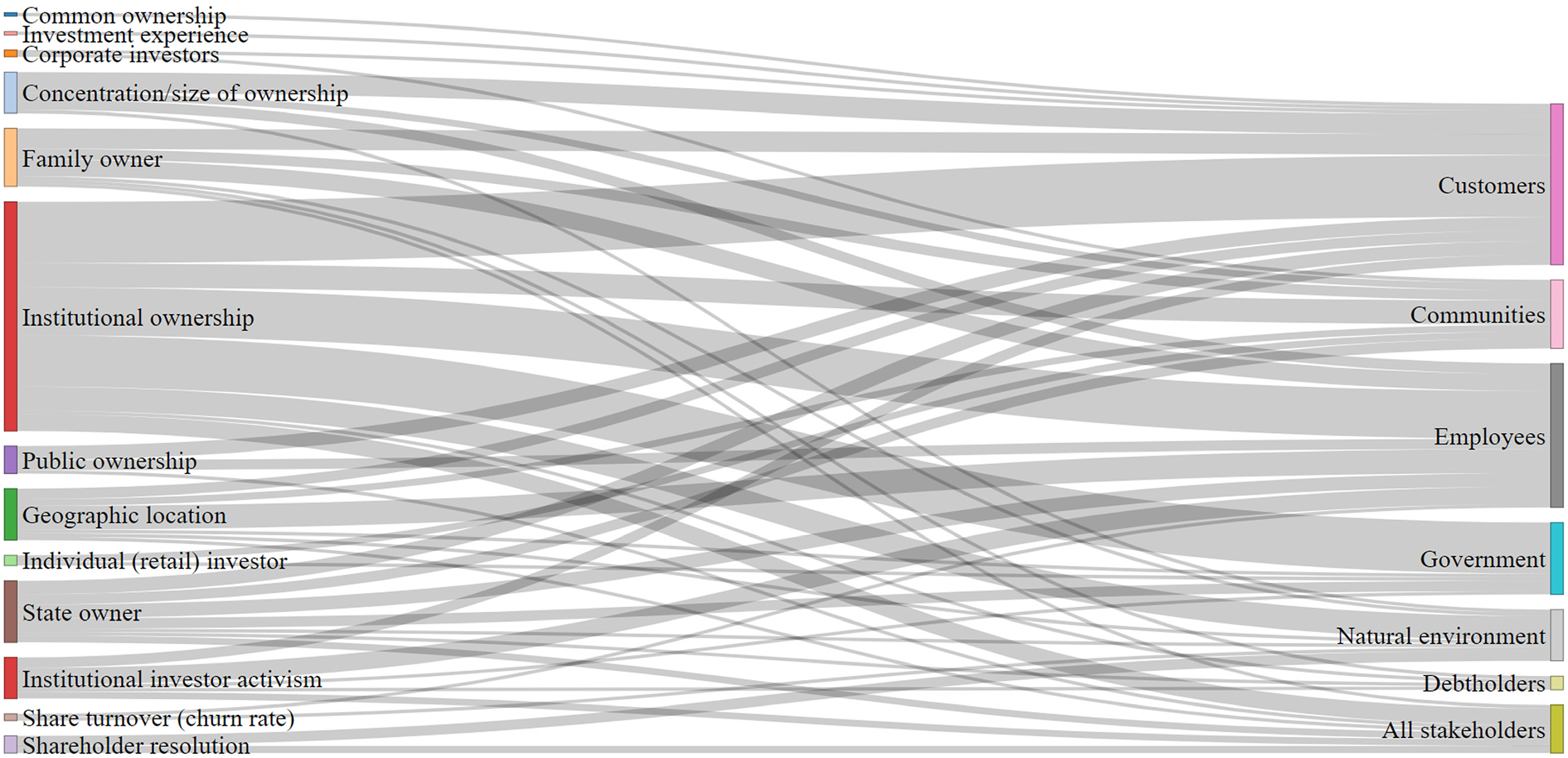

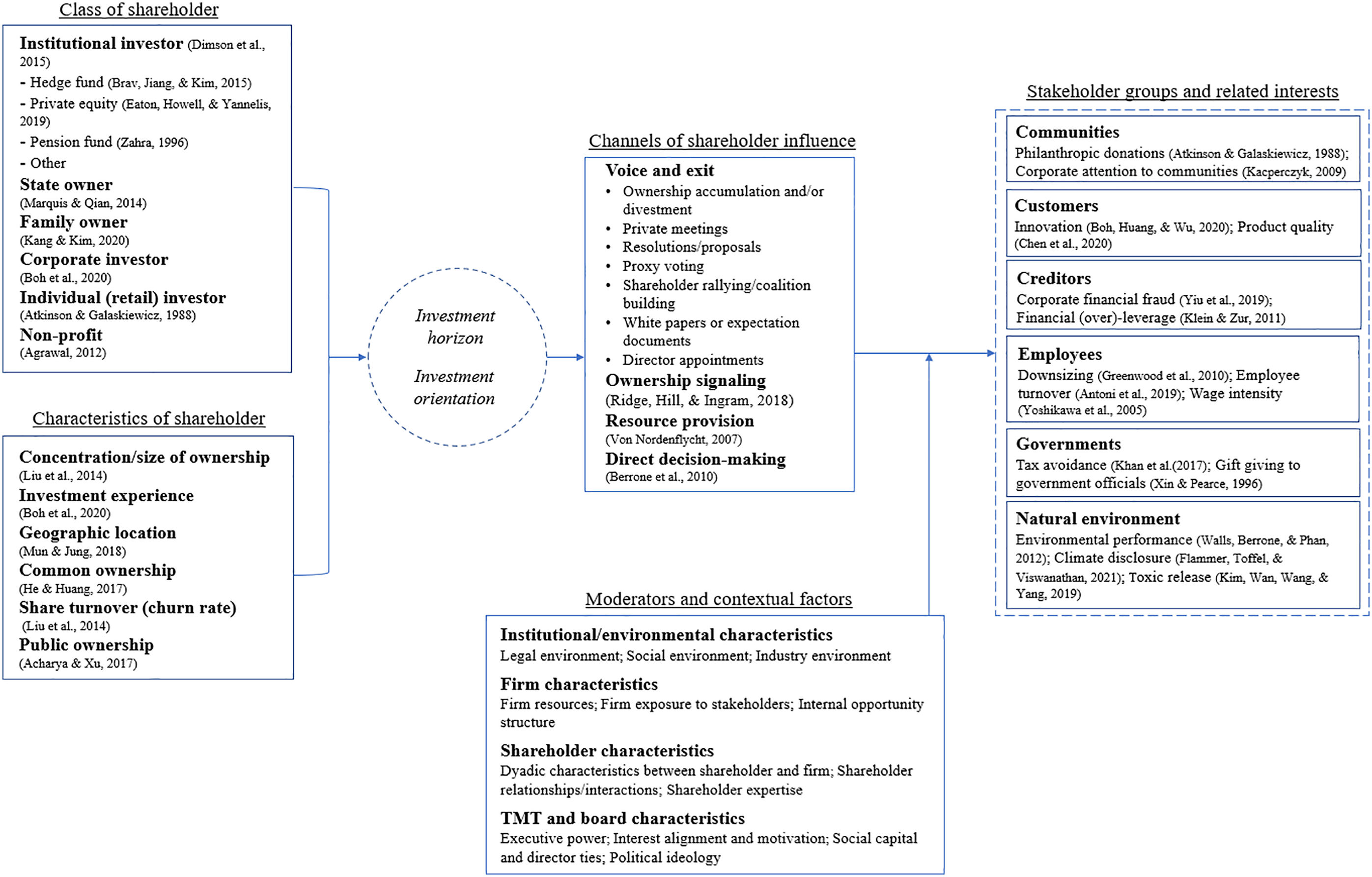

We summarize the studies included in this review in Table OA3 of the online appendix. Each study is categorized according to the class of shareholder, the characteristics of the ownership form examined, the main outcome variables and the group(s) of stakeholders affected by these outcomes, the various contingencies that moderate the focal relationships, and the nature of the sample. We visualize the number of papers that examine each shareholder-stakeholder pair in Figure 2. We also outline the theoretical process through which shareholders shape firm outcomes. Based on this information, we use Figure 3 to map how different shareholders studied in the literature influence different stakeholder-relevant firm outcomes.

Visualizing Studies That Examine How Different Shareholders Influence Stakeholders

Conceptualizing the Influence of Shareholders on Different Stakeholder Groups and Interests.

As shown on the left side of Figure 3, the literature has considered many types of shareholders, including different shareholder classes (e.g., private equity and pension funds) and characteristics (e.g., portfolio concentration and geographic location) of those shareholders. Depending on these classes and characteristics, shareholders differ in their investment horizon and investment orientation, which we summarize in Figure 3 just left of center. Shown right of center in Figure 3, based on the assumptions made about a given shareholder, scholars theorize about the mechanisms through which the shareholder can influence corporate activities and shape the various interests of different groups of stakeholders, displayed on the far-right side of Figure 3. Finally, presented in the bottom of the figure, scholars have shown that factors across the institutional/environmental, firm, top management team (TMT) and board, and shareholder levels of analysis moderate the degree to which the various shareholders influence the set of stakeholder-relevant firm outcomes.

Perusing this literature and examining Figure 3 make clear that shareholders are a highly heterogeneous group. Shareholders under study vary widely in terms of class, characteristics, and preferred channels of influence. Based on this review, we found that two dimensions, prevalent in nearly all reviewed studies, are paramount for comprehending how these differences shape heterogeneous shareholder influences on stakeholder interests: the shareholder’s investment horizon and investment orientation.

Investment horizon refers to the time over which a shareholder typically holds shares in a company. The shortest-term shareholders include high-frequency traders that are able to execute trades in nanoseconds to exploit anomalies in stock prices. More common are day traders or shareholders that turn over their portfolios weekly or monthly. At the other end of the continuum—sometimes referred to as providing “patient” capital—long-term shareholders hold their shares for multiple years, decades, or indefinitely. For example, family owners are often considered long-term shareholders in the literature because they invest with the intention of transferring their stockholdings to future generations.

Investment horizon is a key dimension of shareholder influence because the literature reveals that almost every aspect of a shareholder's interaction with a company partly depends on the shareholder's holding period. Shareholders with shorter horizons seem to suffer more from information asymmetry and may steer away from initiatives that are harder to evaluate (Oehmichen, Firk, Wolff, & Maybuechen, 2021), such as innovation-based activities. Shareholders with short horizons may also aggressively intervene in corporate affairs to quickly achieve their intended objectives but provide little knowledge and insight to managers in the process. Shareholders with longer horizons are comparatively more open to initiatives that are hard to evaluate and serve as a more valuable informational resource for managers (Connelly, Tihanyi, Certo, & Hitt, 2010).

Investment orientation refers to the shareholder's interest in nonfinancial outcomes. Almost all types of shareholders, even those most inclined toward nonfinancial outcomes, placed some value on financial returns. Therefore, investment orientation does not relate to a trade-off between financial and nonfinancial value but rather to a shareholder's concern about the nonfinancial impacts of a company's activities. Shareholders at one end of the continuum are oriented toward maximizing financial returns regardless of the implications of their investments for others. At the other end, shareholders consider the firm's social impact (e.g., employee rights) and may invest with nonfinancial goals in mind. As we illustrate, when considered in conjunction with their investment horizon, shareholders’ investment orientation provides insight into the bearing that different shareholders have on various stakeholders. 3

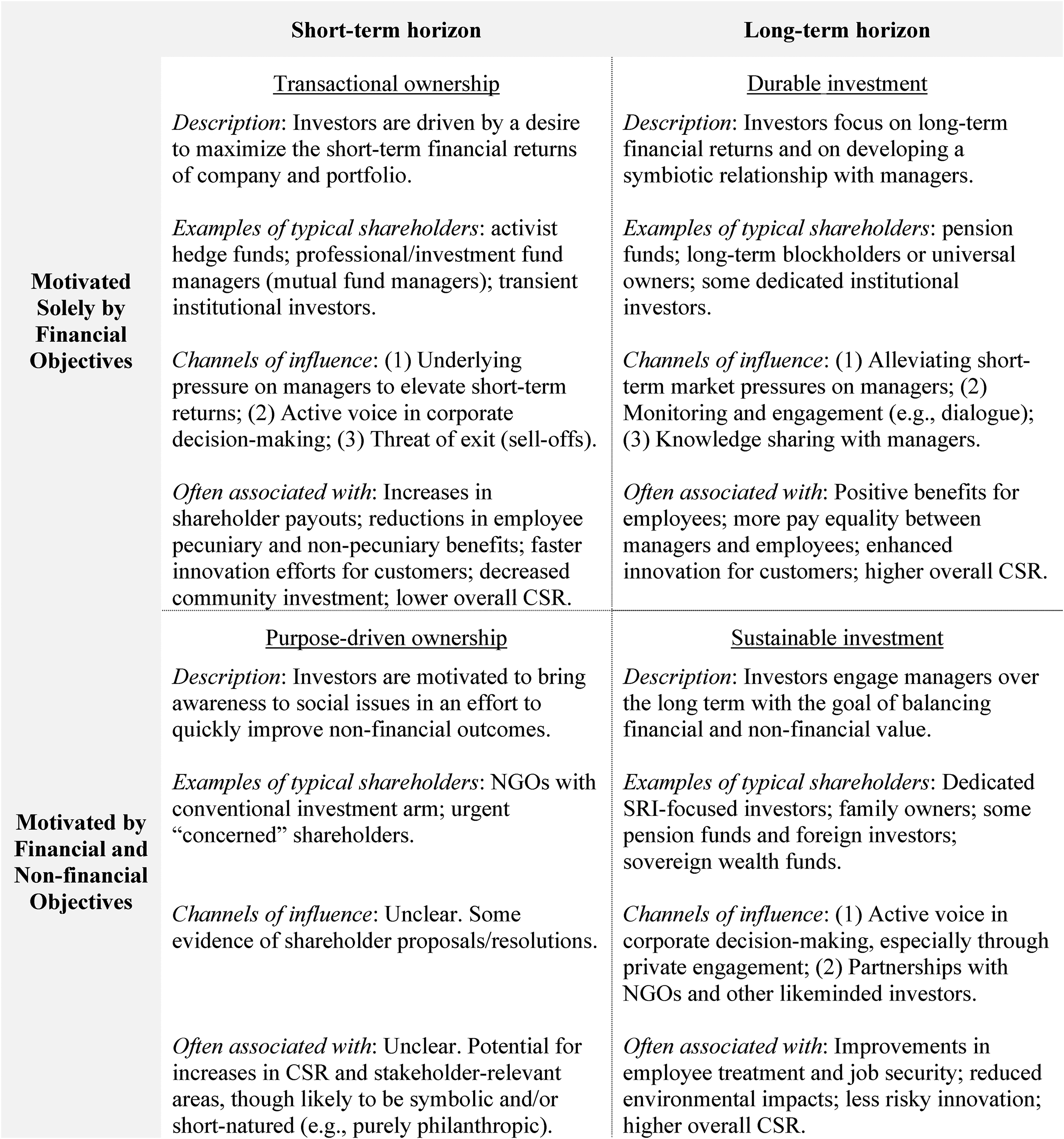

In Figure 4, we broadly classify shareholders according to their investment horizon and investment orientation to derive the following typology: (1) transactional ownership (short-term financial shareholders); (2) durable investment (long-term financial shareholders); (3) purpose-driven ownership (short-term multipurpose shareholders); and (4) sustainable investment (long-term multipurpose shareholders). This classification is central because it enables us to map how different types of shareholders influence the interests of different types of stakeholders.

Categorizing Shareholders to Dissect their Heterogeneous Influence on Stakeholders

Related to our typology, the literature also reveals four channels through which shareholders can influence stakeholders: (1) Voice and exit occurs when shareholders exert influence by threatening to sell their shares (exit) or actively expressing their preferences to managers (voice)—for instance, by filing shareholder proposals or meeting privately with management; (2) ownership signaling manifests from the presence of certain shareholders sending signals that affect managerial decision-making and firm outcomes. For instance, shares held by politicians can signal political support for the respective firm and influence corporate lobbying activities (Ridge et al., 2018), whereas ownership by activist investors can send a signal of shareholder discontentment to management of nontargeted firms (Shi, Connelly, Hoskisson, & Ketchen, 2019); (3) resource provision refers to the resources shareholders provide that influence stakeholder interests. Such resources include access to financing (Phillips & Sertsios, 2017), knowledge sharing (Connelly, Lee, Tihanyi, Certo, & Johnson, 2019), and legitimacy (Marquis & Qian, 2014); 4 and (4) direct decision-making describes the situation that shareholders make the decisions themselves, rather than use tactics to influence the decisions of managers from the outside (as with the other three channels), because firms are owned and directly managed by one dominant shareholder. Typical examples are family-owned firms and firms that are majority-owned by private-equity investors. As we will show, the four types of shareholders we classify utilize these four channels of influence in different ways. Importantly, these channels are not mutually exclusive, so the same shareholder may use multiple channels to influence management. For example, shareholders filing proposals can voice their preferences to managers through proposals while also sending a signal to managers of nontargeted firms (Reid & Toffel, 2009).

Shareholder Types and Stakeholder Interests

In this section, we discuss in detail each of the four quadrants of Figure 4, which we derived from our typology. We assigned the types of shareholders discussed in each study to one or more quadrants according to the authors’ assumptions about them. Some types of shareholders have been assigned to multiple quadrants, depending on those assumptions. 5

Transactional Ownership: Short-Term Financial Shareholders

Transactional shareholders (Figure 4, upper-left quadrant) seek to maximize financial returns over a short period, with little concern for nonfinancial goals. As high portfolio turnover tends to reflect a short horizon, it is often captured in studies examining “transient” investors (see the classification by Bushee, 1998) with prominent financial objectives. Some of the reviewed studies examine specific subtypes of this category of shareholders, such as financially driven activist hedge funds (DesJardine, Marti, & Durand, 2021) and activist short sellers (Shi & DesJardine, 2022). Transactional shareholders trade in and out of stocks relatively quickly to maximize the financial performance of their portfolios and discount future earnings more drastically than longer-term shareholders.

With regard to stakeholders, several studies show that transactional ownership hurts employees by reducing employment security and job prospects. Transactional shareholders can levy pressure on managers to reduce growth and transfer resources from employees to shareholders. Lin (2016) found that managers do this by replacing permanent employees with contract workers as ownership by transactional institutional shareholders increases. Antoni, Maug, and Obernberger (2019) reported that establishments reduce their workforce by about 9% following a private equity buyout and that job losses mostly affect employees who are least likely to find work elsewhere—arguably the most vulnerable. Likewise, ownership by transactional activist hedge funds can reduce firm growth and result in job losses (DesJardine & Durand, 2020), some of which are voluntary due to the depressed job prospects and workplace culture that the retained employees encounter (Chen, Meyer-Doyle, & Shi, 2021). Ahmadjian and Robbins (2005) argued that transactional foreign investors place little value on long-term employment security and instigate significant downsizing and job losses; David, O’brien, Yoshikawa, and Delios (2010) further confirmed these findings.

Transactional ownership can also lead to reductions in the pay and benefits of employees. A broad array of transactional shareholders, including but not limited to activist hedge funds (Agrawal & Lim, 2021), can lead companies to reduce their pension benefits for employees, especially when the shareholders are actively involved in corporate affairs (Cobb, 2015). Such shareholders can also flatten employees’ pay and work hours (e.g., Brav, Jiang, & Kim, 2015) and even increase employee injury and illness rates (Shi, Xia, & Meyer-Doyle, 2021). Providing one estimate of the financial cost to employees, Antoni et al. (2019) found that the average employee loses €980 in annual earnings following a private equity buyout.

Focusing on transactional shareholders, Liu et al. (2014) provided survey evidence that higher share turnover induces managers to invest less in employee-oriented human resource systems. Connelly, Haynes, Tihanyi, Gamache, and Devers (2016) found that such losses can benefit managers; specifically, the authors found that transactional ownership increases management-to-worker pay dispersion, whereby managers earn more as employees earn less.

Assuming the development of new and innovative products benefits customers, transactional ownership may also harm customer interests by impeding corporate R&D and product development efforts. Bushee (1998) was among the first to show that ownership by short-term transactional shareholders reduces firm R&D. Hoskisson, Hitt, Johnson, and Grossman (2002) found that professional fund managers, whose orientation, they argue, is transactional, pressure managers to focus on acquiring other businesses so as to quickly expand their product offerings, rather than taking the more time-consuming path of organically developing new products and innovating within the firm. Likewise, Zahra (1996) found that transactional institutional ownership leads companies away from internal product development and time-consuming and risky corporate entrepreneurship activities. Similarly, Chan, Chen, Chen, and Yu (2015) observed that firms with a high level of transactional ownership are prompted to avoid earnings surprises by reducing their R&D and advertising costs. As an exception, Giannetti and Yu (2021) concluded that transactional ownership can help firms adapt to changes in their industry's environment by introducing more new products and trademarks.

Transactional shareholders may also have a negative impact on the broader community—for example, by encouraging corporate tax avoidance (Chen, Huang, Li, & Shevlin, 2019; Cheng, Huang, Li, & Stanfield, 2012; Khan, Srinivasan, & Tan, 2017), which may hurt local governments and their citizens. In the context of education, Eaton, Howell, and Yannelis (2020) reported that schools owned by private equity prioritize short-term profits, which leads to lower education inputs, graduation rates, loan repayment rates, and earnings among school graduates. In a different context, Klein and Zur (2011) showed that transactional activist ownership increases company leverage and cash redistributions at the expense of creditors.

Several studies indicate that transactional shareholders can undermine corporate social responsibility (CSR), potentially harming the welfare of a broad range of stakeholders and the natural environment. DesJardine and Durand (2020) found that companies whose ownership passes largely to transactional activist hedge funds reduce their CSR activities, in line with the earlier findings of Neubaum and Zahra (2006) that transactional institutional ownership reduces CSR. Looking at specific subdimensions of CSR, Johnson and Greening (1999) showed that companies owned by transactional investment managers reduce CSR efforts oriented toward people (e.g., communities, women and minorities, and employees) and products.

Overall, research shows that the influence transactional shareholders exercise on their portfolio companies almost invariably has a negative impact on a broad array of stakeholders. By prioritizing the short-term maximization of shareholder wealth, transactional ownership seems to orient managers toward decisions that overlook the interests of other stakeholders. Of all stakeholders, employees suffer the most; however, transactional ownership may have a negative impact also on customers, communities, and creditors.

Other studies argue that transactional shareholders influence firm outcomes by selling their holdings when their interests are not met (e.g., Zahra, 1996). Some of these studies indicate that transactional shareholders apply both the mechanisms of “exit” (i.e., sell-offs) and “voice” (e.g., private meetings with management), whereas other studies (e.g., Bushee, 1998) suggest that the timespan over which they hold stock is so short that such investors are precluded from voicing their concerns to management, making exit the main influence channel (e.g., Connelly, Tihanyi, et al., 2010).

Overall, however, agency theory provides a somewhat simplistic view of the relation between transactional shareholders and managers, whose decisions implicate other stakeholders. The view that managers are inherently inclined to attend to stakeholder interests for self-serving reasons and are only restrained by transactional shareholders, who serve primarily the financial interests of the corporation, seems to conflict with research on the complexity of stakeholder management and financial returns. For example, Flammer and Kacperczyk (2016) find that attending to stakeholder interests can help companies innovate in ways that propel long-term financial performance. To better understand when transactional shareholders can have a positive impact on stakeholders, research would benefit from refreshing agency theory with new theories based on different assumptions about managerial self-interest or the factors that curtail it, such as stewardship theory (Davis, Schoorman, & Donaldson, 2018) or upper echelons theory (Hambrick & Mason, 1984).

Durable Investment: Long-Term Financial Shareholders

Durable shareholders (Figure 4, upper-right quadrant) aim to maximize financial returns over a long horizon, with limited concern for nonfinancial outcomes. As low portfolio turnover rates (i.e., churn rates) reflect long horizons, “dedicated” shareholders (Bushee, 1998) are classified as “durable” when they primarily seek financial returns. Pension funds (Johnson & Greening, 1999) that are mostly motivated by the financial performance of their portfolios may fit this classification, depending on the institutional context. Large owners, such as blockholding index investors, may also have long horizons, as their significant holdings make it hard to efficiently divest their shares (DesJardine, Grewal, & Viswanathan, forthcoming). Large holdings tie investors to the respective firms and, as Lee and O’Neill (2003: 215) put it, “[this] mutual dependence creates a long-term relationship between investors and managers.” Some studies argue that, because of their long horizons, durable shareholders may be more sensitive to the risk of negative corporate externalities and, as a result, may be motivated to engage companies on stakeholder-relevant issues purely for financial reasons (e.g., DesJardine et al., forthcoming).

If transactional shareholders harm employee interests, one might suspect durable shareholders have the opposite effect. This is indeed evident in some instances but not in others. Scholars have shown that durable shareholders can offset the pecuniary losses employees suffer because of transactional owners (Cobb, 2015) and soften the negative impact that analyst earnings pressures can have on corporate downsizing (Schulz & Wiersema, 2018). Connelly et al. (2016) found that durable ownership by dedicated institutional shareholders reduces pay dispersion between managers and employees and fosters more equal pay practices in organizations. Other studies indicate that durable foreign owners generally support new corporate investment in human capital (Bena, Ferreira, Matos, & Pires, 2017). However, Jung (2016) found that the presence of financially driven dedicated institutional investors intensifies downsizing and therefore reduces job security for employees.

Durable shareholders can serve the interests of customers insofar as they facilitate firm innovation and corporate entrepreneurial pursuits. For example, the negative impact of a reduced takeover threat on innovation is relatively limited for companies with durable shareholders (Atanassov, 2013). There is also evidence that, because durable shareholders expect long-term share appreciation, they generally support corporate R&D activities (Chowdhury & Geringer, 2001; David, Hitt, & Gimeno, 2001; Hansen & Hill, 1991). Hoskisson et al. (2002) showed that durable pension funds—motivated by long-term financial returns—facilitate internal innovation, rather than pushing managers to acquire innovation externally for quicker results. In a cross-national study, Lee and O’Neill (2003) found that blockholding durable shareholders bolster corporate R&D efforts in the United States but not in Japan, where, they argue, the interests of managers better align with those of long-term blockholders.

Some studies suggest that durable shareholders may also promote CSR efforts and environmental outcomes. Neubaum and Zahra (2006) found that holdings by long-term institutional shareholders are significantly and positively associated with a firm's CSR; more so when the shareholders use activist tactics to intervene in corporate decision-making. More recently, Chen, Dong, and Lin (2020: 496) found evidence supporting their claim that institutions with “long-term investment horizons are the main force to drive CSR improvement”; however, the authors did not directly measure the sampled investors’ orientation. It is possible that more conclusive evidence would arise from research on specific types of shareholders that can be classified as “durable.” Kacperczyk (2009), for instance, argued that the long horizons of financially oriented pension funds motivate them to pressure firms to attend to the interests of other stakeholders, which results in observable increases in CSR activities. Similarly, analyses of specific subdimensions of CSR indicate that durable shareholders can improve the environment and the welfare of communities (e.g., Johnson & Greening, 1999). Recently, Azar, Duro, Kadach, and Ormazabal (2021) showed that ownership by the “Big Three”—BlackRock, Vanguard, and State Street—which they position as durable shareholders, leads to reductions in the owned firms’ annual carbon emissions. The authors argue that these shareholders benefit from pushing for a reduction of emissions because doing so makes their investment vehicles more attractive to a broader class of socially minded clients. Taking a different view, DesJardine et al. (forthcoming) found causal evidence that long-term common owners enhance the CSR performance of their portfolio firms in order to promote financially material positive spillovers between firms’ CSR activities.

Durable investment can also promote transparency in a firm's stakeholder-related activities. Arguing that investors with long horizons are likely to view philanthropy as a form of investment, Wang et al. (2021) found evidence that financially motivated institutional investors with long horizons mitigate the concerns of managers that investors will view corporate philanthropic activities negatively. As a result, managers become more open to publicizing such initiatives. By comparison, Shi, Connelly, and Hoskisson (2017) argue that the durable shareholders’ direct oversight of corporate activities reduces managers’ intrinsic motivation to act ethically. This, the authors found, tends to increase corporate financial fraud, which, in severe cases, can harm not only governments and creditors but also a range of stakeholders whose welfare depends on an organization (e.g., employees or communities). Overall, in contrast to the effects of transactional shareholders on stakeholders, those of durable investors can be positive or negative, depending on the circumstances and context.

Some studies, however, argue that while durable shareholders may shield managers from other pressures, at the same time they influence managers by intensely monitoring managerial activities (Connelly, Tihanyi, et al., 2010). Other works suggest that monitoring—at least when mostly passive—does not afford durable institutional shareholders sufficient force to influence managers. Rather such shareholders need to use their voice to motivate management (Chen et al., 2020; David et al., 2001). In sum, some studies assume that durable shareholders influence managers by adopting a hands-off approach and relieving them of pressures from capital markets and other shareholders, whereas others assume that direct intervention is a precondition for shareholder influence.

Some scholars argue that durable shareholders are an important information source for managers. Because of their typically long investment horizon, durable shareholders have the experience and willingness to share their insights and ideas with the managers of their portfolio companies. For example, according to Connelly, Tihanyi, et al. (2010), these shareholders have special knowledge, which they accumulate by holding shares for long periods. Building on this view, Boh, Huang, and Wu (2020) argued that experienced and patient durable shareholders can assist firms with environmental scanning and promote innovation by providing relevant industry information. Where relevant, such information might influence the trade-offs managers make between the interests of shareholders and other stakeholders. In this vein, Oehmichen et al. (2021) suggested that the information durable shareholders provide could be especially useful in areas where evaluating outcomes is difficult, such as CSR.

Another stream of research on durable shareholders relies on a set of behavioral theories, including the behavioral theory of the firm and cognitive evaluation theory (Shi et al., 2017). According to these behavioral theories, managerial decision-making is influenced by external stimuli, such as earnings pressures and shareholder expectations (e.g., Schulz & Wiersema, 2018). Durable shareholders can either soften or amplify the effects such stimuli have on managers and thus alter how managers decide on activities related to stakeholders. For instance, although managers may feel pressured to downsize when firm performance falls short of analysts’ expectations, institutional shareholders with a long-term outlook can relieve managers of these pressures (Schulz & Wiersema, 2018).

As theoretical tools, behavioral theories help explain the tendencies and biases that find their way into managerial decision-making amid shareholder pressures and can therefore usefully complement research in this stream. However, few studies formally integrate behavioral theories with other theories that have been traditionally used to understand the influence of shareholders, such as agency theory (Eisenhardt, 1989) and stewardship theory (Davis et al., 2018). To provide a comprehensive account of how shareholders in general influence stakeholders, as well as deeper insights into how durable shareholders in particular influence managerial decision-making, research would benefit from integrating behavioral and nonbehavioral theories, rather than taking an “either/or” approach.

Purpose-Driven Ownership: Short-Term Multipurpose Shareholders

Purpose-driven shareholders (Figure 4, bottom-left quadrant) have short horizons over which they seek to accomplish financial and nonfinancial objectives, including prosocial outcomes. Of all four types, these shareholders are the rarest in the literature because there are relatively few of them to study before the 2010s, which is when the number of shareholder activists and shareholder resolutions with social objectives started to accelerate. Despite their rarity, as scant academic and anecdotal evidence suggests, such shareholders can have real effects on stakeholder-relevant corporate activities, making them worth review.

Another type of purpose-driven shareholder is the socially oriented or ESG (environmental-social-governance) activist hedge fund. Activist hedge funds have historically focused only on maximizing financial returns and increasingly use their ownership positions to achieve financially material sustainability objectives. Because these investors tend to have very short horizons, but can have considerable impacts on corporate priorities and activities (DesJardine & Durand, 2020), they present a formidable type of purpose-driven shareholder. Although several working papers are currently exploring the effects of purpose-driven activist hedge funds (e.g., Chu & Zhao, 2019), researchers need to investigate more campaigns to derive empirically robust insights.

As activist hedge funds begin to focus more on social and environmental issues in their campaigns, they gain access to new channels of influence. As noted earlier, activist hedge funds have short horizons but also deep financial reservoirs that they can leverage to build significant positions in target companies. For instance, six months after launching its campaign against ExxonMobil in December 2020, the ESG-oriented activist hedge fund Engine No. 1 was able to appoint three of the four directors it had proposed to the company's board, with the aim to transform Exxon into a more environmentally sensitive oil conglomerate (DesJardine & Bansal, 2021). Obtaining board representation is unlikely to be feasible for many other types of purpose-driven shareholders. In contrast, activist hedge funds inclined to pursue environmental and social ends are more likely to be able to enjoy privileged access to new channels of influence—a possibility that opens up an exciting avenue for future study.

Sustainable Investment: Long-Term Multipurpose Shareholders

Sustainable shareholders (Figure 4, bottom-right quadrant) integrate nonfinancial criteria into their long-term investment objectives. Such shareholders consider financial returns from a more balanced perspective than other types of shareholders. Importantly, the category of sustainable shareholders is not limited to the classic types of long-term investors who have been included in this quadrant because of their socioeconomic and multigenerational objectives—that is, investors who focus on ESG or socially responsible investing (SRI) objectives and family owners (Gomez-Mejia et al., 2011). For instance, government shareholders will also be included in this category when they approach companies with a sustainable investment orientation. Fiss and Zajac (2006: 1177) argue that some government shareholders “have to attend to the interests of several corporate stakeholders.” Some foreign institutional shareholders will also fall into this quadrant when they approach local companies from a global ESG perspective, as will universal owners with “long-term fiduciary responsibilities to their customers, beneficiaries, and the wider community” (Dimson, Karakaş, & Li, 2015: 3226).

Sustainable investment may benefit a broad range of stakeholders, as well as the natural environment. Kim, Wan, Wang, and Yang (2019) found that sustainable shareholders, such as SRI funds, public pension funds, and dedicated institutional investors, help reduce the toxic emissions of facilities to which they are closely located. In an earlier study, Berrone, Cruz, Gomez-Mejia, and Larraza-Kintana (2010) showed that sustainable family investment can help firms reduce their negative environmental impacts.

Sustainable foreign shareholders can also improve stakeholder welfare in areas where local firms fall short of global standards regarding specific issues. Mun and Jung (2018: 412) argued, “The growth of foreign institutional ownership has put new pressure on Japanese firms to embrace global CSR standards . . . particularly regarding gender diversity, given that Japanese firms fall far behind their global competitors on the issue.” However, as other research indicates, context matters. Yoshikawa et al. (2005) found that domestic sustainable shareholders improve employee welfare by increasing compensation and promoting employee development. In some contrast, Dyck, Lins, Roth, and Wagner (2019) reasoned that among sustainable shareholders, only those who originate in countries with strong community beliefs in the importance of environmental and social issues will increase a firm's environmental and social performance.

Surprisingly, despite the benefits sustainable shareholders create for a range of stakeholders, they may sometimes harm customers. Boh et al. (2020) observed that, because sustainable family shareholders emphasize control and influence over-invested firms, they undermine firm innovation. Other studies have found that, because sustainable family shareholders tend to be risk averse and avoid innovative experiments that may lead to failure, they put pressure on their firms to reduce R&D efforts (Chrisman & Patel, 2012; Duran, Kammerlander, Van Essen, & Zellweger, 2016) and new product development (Souder, Zaheer, Sapienza, & Ranucci, 2017).

Although institutional theory is useful for speculating about the broader pressures that can elicit change in organizations, its macro lens can miss the finer-grained channels through which sustainable shareholders engage companies on the ground. As research on the growing population of sustainable shareholders proliferates, scholars will need to integrate theories that unpack the dynamics between the sustainable shareholder, manager, and ecosystem of other actors.

An Agenda for Future Research

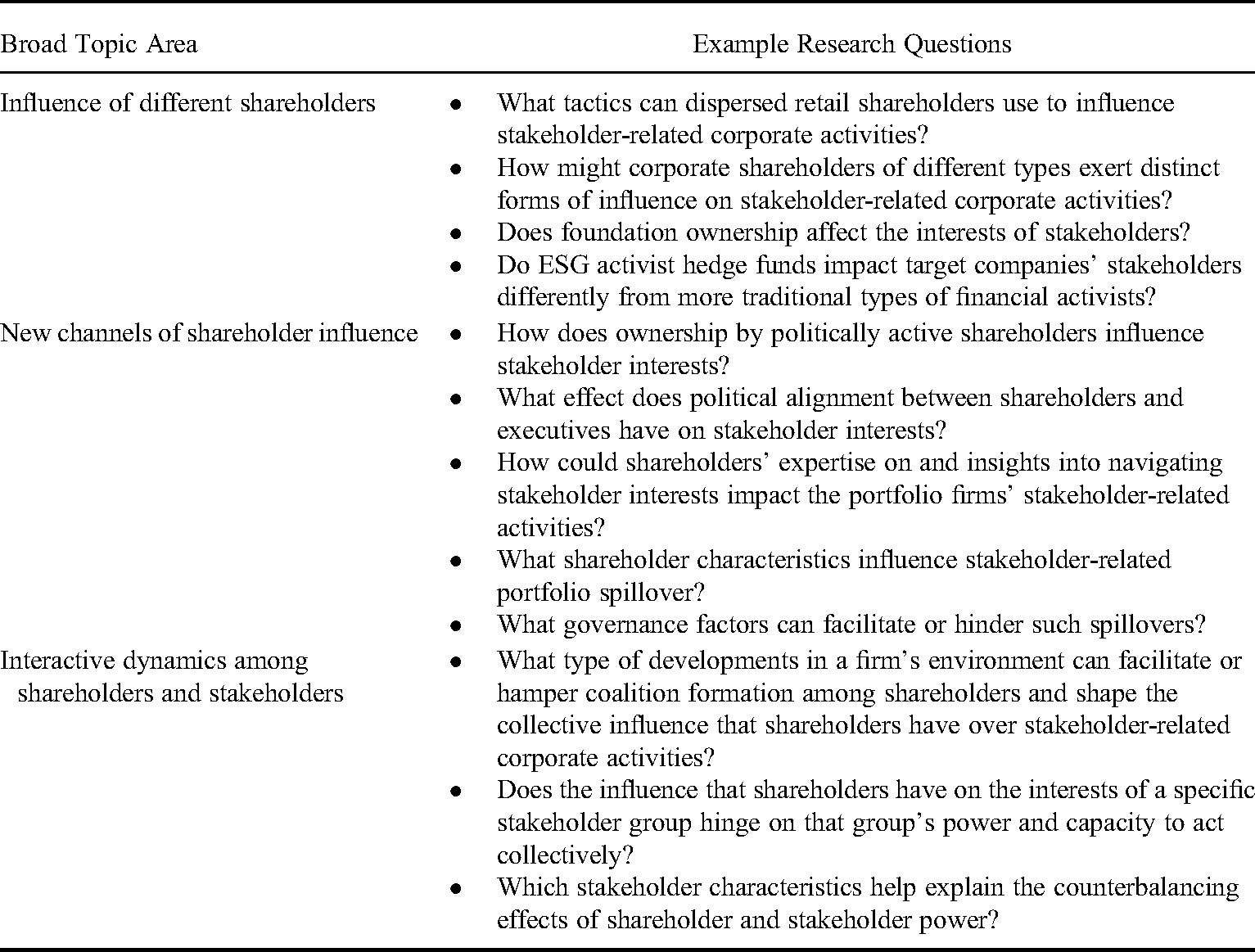

In this study, we reviewed cross-disciplinary research on the influence that shareholders have on stakeholder interests. Based on our review, we identified three overarching gaps in the literature, which now lead us to call for research that (1) explores the influence that different types of shareholders can have on stakeholders, (2) identifies new channels through which shareholders influence stakeholders, and (3) accounts for the interactive dynamics among shareholders and stakeholders. Table 1 outlines the three areas for future research and lists research questions associated with each theme.

Areas for Future Research

Explore the Influence of Different Types of Shareholders

Shareholders, as already suggested, are a widely heterogeneous group and therefore the tactics they employ and their relationships with firms and their stakeholders vary. Although scholars from different disciplines have studied a range of shareholder types, the literature is not yet comprehensive. Some shareholder categories and the influence they exert on stakeholders have been overlooked, including certain conventional classes (e.g., corporate investors) and emerging subclasses of shareholders (e.g., ESG activist hedge funds). In addition, because much existing research isolates either the “class” or “characteristics” of a shareholder, we know little about how the unique composition of different shareholder categories—defined by both their class and characteristics—may shape their influence on firm activities and stakeholder-related outcomes. To gain more complete insights into how shareholders influence stakeholders, we propose certain specific topics future research should further explore.

Retail shareholders are nonprofessional shareholders who buy and sell securities. As their ownership in firms is typically dispersed, they often lack the power and incentives to influence a firm's decisions. However, the participation and impact of retail shareholders in company governance seem to be evolving. From early 2020 to early 2021, trading by retail shareholders as a share of overall market activity nearly doubled from 15% to more than 30% (Fitzgerald, 2021). At the same time, anecdotal evidence suggests that these shareholders, aided by new technologies, can have a profound impact on markets and organizations. In early 2021, retail shareholders coordinated their activities via social media platforms and worked collectively to inject capital into the videogame retailer GameStop, increasing the company's stock by approximately 1,700 percent in a matter of days and leading legendary hedge fund manager Bill Ackman to exclaim, “It does show you the power of retail to move stock prices. The biggest investor in the world is retail. It's not the institutions.” 6 The rise of the retail shareholder and the increasing use of technology open up fruitful avenues for investigating what tactics dispersed retail shareholders may apply to influence stakeholder-related corporate activities.

Corporate shareholders are incorporated businesses that invest in other companies. Corporate ownership can take multiple forms. In some cases, companies may take a stake in other companies to capture value from an anticipated stock-price appreciation. In other cases, companies can use corporate funds to invest in external startup companies. Most research on this type of investment shows its effects on customer-relevant outcomes, such as firm innovation. Companies may also purchase minority shares in customers or suppliers to facilitate bonding (Fee, Hadlock, & Thomas, 2006). Given the potentially vast heterogeneity among corporate shareholders, in terms of location, size, and investment objectives (DesJardine, Shi, & Sun, 2021), more research is needed to unpack how they influence different types of stakeholders.

Our review reveals that existing research is mostly silent on how ownership by nonprofit organizations influences stakeholder welfare (for an exception, see McDonnell et al., 2015). This is surprising, given that nonprofit shareholders are likely to be highly attentive to stakeholder interests in their investment decisions. One way to advance this stream of research is to focus on ownership by foundations, which are institutions without formal shareholders or owners. Recent research suggests that the number of foundation-owned companies has increased significantly in the last decade, especially in Europe (Achleitner, Bazhutov, Betzer, Block, & Hosseini, 2020). Some foundation-owned firms, such as Bosch, Bertelsmann, Würth (all three headquartered in Germany), and Novo Nordisk (headquartered in Denmark), are global players that can have considerable influence on the welfare of an array of stakeholders.

The second subclass of institutional investor that requires more attention is private equity (PE). Although previous studies have investigated the influence of PE buyouts on employees’ interests (Antoni et al., 2019), most such research has neglected the potential heterogeneity of PE investors. Specifically, PE investors may differ in the emphasis they place on financial structure—that is, the strategic use of debt or equity in their portfolio firms—and in the scope of the firms in which they invest (Hoskisson et al., 2013). Such differences may translate into distinct ways of influencing the stakeholders of portfolio firms. Among PE investors, those with an equity financing structure and a narrow portfolio scope are likely to have “niche” experience that facilitates their advisory role. In that role, this type of PE investor may decide not to induce portfolio firms to generate value through unrestrained cost-cutting and employee layoffs. In contrast, PE investors with heavier debt financing may feel compelled to generate quicker financial returns, which could jeopardize the long-term interests of other stakeholders.

Among existing frameworks for classifying shareholders based on their portfolio turnover and portfolio concentration is Bushee’s (1998) typology of transient, quasi-index, and dedicated shareholders. However, this typology does not capture nuances regarding the class and subclasses of the specific shareholders. Indeed, before and for some time after Bushee’s (1998) classification was introduced, many scholars made finer distinctions about the classes of shareholders under study (Hoskisson et al., 2002; Johnson & Greening, 1999). For example, high-frequency traders, mutual funds, or certain hedge funds are all classified as transient shareholders, following Bushee’s (1998) typology. However, these types of shareholders will influence the firms in their portfolios in distinct ways. It is therefore necessary for research to capture the distinct characteristics of each class of shareholders.

We propose a three-step process that scholars who explore this avenue can use to dissect the composition of a shareholder class more precisely. Our hope is that future research can theorize more specifically about how a particular type of shareholder influences companies and their stakeholders. As Figure 3 indicates, the “three Cs,” as we describe the process we propose here, require that research specifies three shareholder dimensions—namely, (1) class, (2) characteristics, and (3) channels of influence.

Our first recommendation is that future studies select specific classes of shareholders to examine. At the broadest level, shareholders can be classified as institutional, family, governmental, retail, corporate, or nonprofit (e.g., Atkinson & Galaskiewicz, 1988; Fiss & Zajac, 2006). To refine this categorization, scholars could focus more closely on a particular subclass. For example, as Figure 3 shows, common subclasses of institutional investors include hedge funds, pension funds, and private equity, whereas corporate shareholders may be either large, established corporate venture capitalists or smaller start-ups investing in other firms. We anticipate that narrowing in on the class or subclass of shareholder can enable researchers to theorize more accurately about the type of shareholder, as well as their preferred influence channels and dynamics with management and other stakeholders.

Second, we suggest that scholars also outline the characteristics that vary among a shareholder class. For example, in the literature “foreign owners” are often broadly categorized together (Boubakri, Cosset, & Saffar, 2013; Shi, Gao, et al., 2021). However, such groupings make it impossible to identify the characteristics in which these types of shareholders differ. To see why this is problematic, consider that the effects of foreign foundation shareholders on companies are likely to differ vastly from those of foreign activist hedge funds. We recommend that scholars consider the following shareholder characteristics, listed on the left side of Figure 3: (1) concentration and size of ownership, (2) investment experience, (3) geographic location (e.g., foreign versus domestic investors or local versus geographically distant), (4) common ownership, (5) share turnover, and (6) public ownership.

Third and finally, we recommend that scholars clarify the channels a given shareholder utilizes to influence a firm's stakeholder-relevant decisions. Although half of the papers we reviewed theorize that shareholders influence firm outcomes through voice and exit, they do not always consider the specific mechanisms those shareholders employ (e.g., private meetings versus proposals are both considered “voice” but can have different effects). In this regard, we caution that the mechanisms of “voice” and “exit” that Hirschman (1970) first described made it too easy for scholars to avoid being specific about the actual channels shareholders use to influence companies. In our own research, we have found that interviews (DesJardine & Durand, 2020; DesJardine, Marti, & Durand, 2021; DesJardine, Shi, et al., 2021), both with managers and investors, are extremely helpful in identifying the common channels and tactics a shareholder uses. In many cases, these channels are related to the class and characteristics of the shareholder, which underscores the need to be specific about those two dimensions. Furthermore, as an investor will often rely on multiple channels concurrently, these channels are not mutually exclusive.

Develop Insights Into New Channels of Shareholder Influence

As already noted, our review indicates that most studies have adopted Hirschman’s (1970) dichotomy of “voice” and “exit” to theorize about the channels through which shareholders influence a firm's stakeholder-relevant outcomes. Although helpful, this approach limits the insights scholars can gain into influence channels that do not quite fit the voice/exit dichotomy, such as those we discuss here.

Funding political campaigns is the second major channel through which shareholders can influence stakeholder interests. For example, institutional investors have been consistently the largest monetary contributors to political campaigns in the United States, donating a total of $154.56 million in the 2019–2020 political cycle according to the CRP (2021b). Financial contributions enable institutional investors to influence whether Democratic or Republican political candidates are elected. Given that politicians with different political ideologies tend to prioritize stakeholders differently, shareholders can indirectly affect stakeholder welfare by funding political campaigns. However, academic research on CPA channels has been largely silent, leading us to call for future research to explore questions such as: What types of shareholders tend to engage in CPA? How does ownership by politically active shareholders influence stakeholder interests? And what influence does the political alignment between shareholders and executives have on stakeholder interests?

Account for Shareholder and Stakeholder Dynamics

Many existing theories of shareholder influence suggest that different types of shareholders will exert distinct forms of influence on stakeholder-related corporate activities (e.g., Johnson & Greening, 1999). Most studies that draw on these theories investigate how different types of shareholders influence the welfare of various stakeholders independently of each other, partly by aggregating ownership levels as proxies for the influence specific shareholders exercise (Bushee, 1998; Connelly, Tihanyi, et al., 2010). This approach, however, neglects the specific and important within-firm dynamics that may arise between different types of shareholders as well as between different stakeholder groups, leading us to propose two final research topics.

A second question future research could explore is whether shareholders’ political ideologies influence stakeholder-relevant firm outcomes and whether the dispersion of shareholder ideologies matters for stakeholders. Prior research has shown that shared ideologies among organizations can facilitate coalition formation (Altemose & McCarty, 2001; Cullen, 2015). Extending this logic, it would be helpful to know whether shareholders who share similar ideological views are more successful in forming coalitions and working together to influence firms than others who do not.

Lastly, future research can investigate what type of developments in a firm's environment, such as changes in ruling political parties or climate policies, can facilitate or hamper the formation of shareholder coalitions and shape the collective influence that shareholders have over stakeholder interests. Previous studies have already shown that opportunities and threats in broad institutional environments affect coalition formation (Hathaway & Meyer, 1993; Maney, 2000). In the case of ExxonMobil, it is likely that Engine No 1. was able to form a coalition with other shareholders in the institutional environment because those existing shareholders were aware of the association between fossil fuels and climate risks.

Conclusion

Stakeholder-focused management is largely contingent on the shareholders that compose a firm's ownership structure. In today's society, shareholders have special privileges that other stakeholders lack and that uniquely position them to influence the priorities and practices of corporations. If the welfare of society and the environment depend on orienting companies toward the interests of their stakeholders, then it is important that research examines in depth the shareholders of corporations. Our review, we hope, provides a broad foundation on which future studies on shareholder influence and stakeholder welfare can build.

Supplemental Material

sj-docx-1-jom-10.1177_01492063221126707 - Supplemental material for How Shareholders Impact Stakeholder Interests: A Review and Map for Future Research

Supplemental material, sj-docx-1-jom-10.1177_01492063221126707 for How Shareholders Impact Stakeholder Interests: A Review and Map for Future Research by Mark R. DesJardine, Muhan Zhang, and Wei Shi in Journal of Management

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.