Abstract

This study examines the relationship between the degree of external social and environmental regulatory pressures and firms’ integration of corporate social responsibility (CSR) criteria into executive compensation contracts. Building on the notion that firms operate in settings in which external regulatory pressures and internal corporate governance conditions interact, we investigate how internal corporate governance mechanisms moderate the relationship between external regulatory pressures and adoption of CSR criteria in executive compensation contracts. The analysis of a worldwide, longitudinal sample of 2,328 firms listed in 37 countries during 2003 through 2015 reveals that the degree of regulatory pressure on firms to operate in socially and environmentally sound ways positively influences their adoption of CSR criteria in executive compensation contracts (i.e., conformity effect). Regulatory pressures evoke heterogeneous responses among firms within a country though, depending on their interaction in the corporate governance bundle. Corporate governance mechanisms have moderating effects: a greater degree of board independence strengthens the conformity effect, whereas blockholder ownership weakens it. This study advances understanding of how the corporate governance bundle of external regulatory pressures and internal corporate governance mechanisms affects the adoption of a relatively recent, important corporate governance practice in the boardroom.

Introduction

Corporate social responsibility (CSR) has rapidly risen up the corporate agenda and increasingly is of critical importance for firms across the globe. Broadly defined, CSR refers to “the integration of social and environmental concerns in their companies’ operations and in their interactions with stakeholders” (Cheng, Ioannou, & Serafeim, 2014: 1). 1 Although CSR is not a new topic (e.g., Bowen, 1953), it is clear that firms no longer can afford to solely focus on shareholders’ interests. For instance, at the end of 2019, the World Economic Forum (WEF) declared in its “Davos Manifesto” that the universal purpose of a company “is to engage all its stakeholders in shared and sustained value creation.” 2 Six months before this declaration, the Business Roundtable—an association of chief executive officers of leading U.S. firms—publicly agreed to share “a fundamental commitment to all of our stakeholders” (Business Roundtable, 2019: 1). As these declarations indicate, firms face increasing pressures to focus on the long-term interests of all stakeholders rather than just short-term shareholder value (Aguilera, Filatotchev, Gospel, & Jackson, 2008), and in response, as well as to strengthen their relations with stakeholders, firms increasingly adopt initiatives and policies to embrace CSR (Berrone & Gomez-Mejia, 2009; Walls, Berrone, & Phan, 2012; Wang, Tong, Takeuchi, & George, 2016).

A relatively recent but important trend marking these initiatives and policies is the integration of CSR criteria into executive compensation contracts, which we refer to as CSR contracting. These compensation policies link executive pay to social and environmental performance targets, such as reductions of greenhouse gas emissions, employee health and safety, employee satisfaction, and community development (Flammer, Hong, & Minor, 2019; Hong, Li, & Minor, 2016; Ikram, Li, & Minor, 2019). The underlying idea is that “[i]f . . . corporations are sincere about [corporate social responsibility], then they must link compensation for the senior executives directly to meeting goals such as cutting carbon emissions, and lowering water and energy use” (The Guardian, 2014). 3 These compensation policies signal firms’ embrace of CSR as an important element of corporate strategy and commitment to addressing stakeholders’ needs in their strategic decisions (Berrone & Gomez-Mejia, 2009; Flammer et al., 2019). Anecdotal accounts of global firms describe their plans for or existing CSR contracting. For example, in 2018, Royal Dutch Shell announced the integration of short-term carbon emissions targets into its executive compensation packages, subject to a shareholder vote in 2020 (BBC News, 2018); the Danish healthcare company Novo Nordisk also adopted CSR criteria in executive compensation because, according to its CEO, “In the long term, social and environmental issues become financial issues” (Ignatius & McGinn, 2015: 62). Indeed, for instance, Flammer et al.’s (2019) study reveals that CSR contracting is value enhancing, as indicated by an increase in Tobin’s Q, and also has important social and environmental effects, such as lower emissions of toxic chemicals and a higher degree of green innovations, although more recent evidence shows that the adoption of CSR contracting is likely to produce positive effects on the firm’s CSR performance starting from the third year after adoption (Derchi, Zoni, & Dossi, 2021).

Although CSR contracting thus is a growing, global corporate practice, research into it is scarce and mostly focused on the single institutional setting of the United States (Derchi et al., 2021; Flammer et al., 2019; Ikram et al., 2019). The comparative perspective of CSR suggests though that firms’ social and environmental policies depend on the institutional setting in which they are embedded (e.g., Aguilera & Jackson, 2003; Francoeur, Melis, Gaia, & Aresu, 2017; Jackson & Apostolakou, 2010; Matten & Moon, 2008). The diversity of institutional settings that exist around the world in turn raises concerns about the external validity of CSR contracting studies conducted solely in a U.S. context. To address this gap in prior literature, we undertake a systematic examination of CSR contracting among firms headquartered around the world, using a longitudinal sample of 2,328 unique firms (12,290 firm-year observations) from 37 countries over the period 2003 through 2015. In turn, we gain better understanding of an increasingly prevalent, real-world, under-researched phenomenon (Flammer et al., 2019).

In addition to addressing an empirical gap, from a theoretical perspective this study offers novel insights into the influence of institutional characteristics on the adoption of CSR practices by individual firms. A key premise of the comparative perspective of CSR (e.g., Jackson & Apostolakou, 2010; Matten & Moon, 2008; Walls et al., 2012) is that, due to differences in institutional settings, firms “experience divergent degrees of internal and external pressures to engage in [CSR] initiatives” (Aguilera, Rupp, Williams, & Ganapathi, 2007: 836). According to institutional theory, governments affect society’s expectations of what constitutes proper behavior by issuing rules and policies, such that they exert considerable pressure on firms (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). In turn, scholars suggest that regulatory pressure may drive firms’ adoption of CSR practices (Aguinis & Glavas, 2012; Campbell, 2007; Matten & Moon, 2008). Although prior institutional literature suggests mostly homogeneous organizational responses to regulatory pressures (e.g., DiMaggio & Powell, 1983, 1991), recent literature has questioned this notion and recognized that regulatory pressures are not necessarily “coercive” (e.g., Xie, Shen, & Zajac, 2021). Our study builds on these arguments and suggests that a heterogeneous organizational response might be expected in the CSR domain, where some rules and policies are designed to be coercive but others aim to encourage or stimulate behaviors, to facilitate desired outcomes (e.g., Albareda, Lozano, Tencati, Midttun, & Perrini, 2008; Knudsen & Moon, 2017; Steurer, 2010). Such rules and policies are not directly focused on CSR contracting, which is not mandated, so they likely generate heterogeneous organizational responses in terms of adoption. From a theoretical perspective, it remains unclear how firms engage with social and environmental regulatory pressures. Will they adopt CSR contracting to signal their conformity with societal prescriptions and expectations? Or does CSR contracting substitute for a relative lack of regulatory pressures, serving as an internal motivator to engage in CSR, in cases that require more incentivizing of CSR through executive compensation? Might the same regulatory pressures evoke homogeneous organizational responses among firms, or do they prompt heterogeneous responses, within any institutional environment, depending on each firm’s corporate governance?

This study helps advance the existing comparative approach to CSR (e.g., Aguilera, Desender, & Kabbach de Castro, 2012; Aguilera et al., 2007; Jackson & Apostolakou, 2010; Matten & Moon, 2008), which generally relies on the “varieties of capitalism” approach (Hall & Soskice, 2001) and assumes homogeneous organizational responses by all firms operating within the same type of political economy (e.g., liberal market economies or coordinated market economies, both of which comprise several countries). We propose a more nuanced, contextually embedded explanation of the adoption of CSR practices that considers diversity among countries in terms of regulatory pressures in the CSR domain, as well as in how firms respond to regulatory pressures within a country. Theoretically, it is unlikely that institutional pressures alone drive firms’ decisions to adopt CSR contracting, because such decisions involve a plethora of actors, including boards of directors and shareholders (Aguilera & Jackson, 2010; Xie et al., 2021), each of whom has its own CSR-related preferences for how to react to institutional pressures. This diversity creates a corporate governance “bundle” (Aguilera et al., 2012; Rediker & Seth, 1995; Yoshikawa, Zhu, & Wang, 2014) in which external regulatory pressures and internal corporate governance mechanisms interact (Johnson & Greening, 1999; Sullivan & Gouldson, 2017). By examining how regulatory pressures and their interaction with internal corporate governance mechanisms might explain the adoption of a relatively recent organizational practice, we can highlight patterned variations across firms and their institutional environments. In a theoretical sense, this insight addresses the need to understand how corporate governance bundles work (e.g., Aguilera et al., 2012; Schiehll, Ahmadjian, & Filatotchev, 2014; Yoshikawa et al., 2014), moving beyond universal approaches that assume a single set of relationships holds across all firms in the same institutional setting, or models can be applied universally to distinct institutional settings.

Theory and Hypothesis Development

Social and Environmental Regulatory Pressures: Why Firms Adopt CSR Contracting

To incentivize executives to address social and environmental impacts in their strategic decision-making, and thereby consider the needs of various stakeholders, an increasing number of firms has started to adopt CSR contracting, a compensation policy that links executive pay to social and environmental performance targets (e.g., reduction of greenhouse gas emissions, employee health and safety, employee satisfaction, community development; e.g., Flammer et al., 2019; Hong et al., 2016). 4

Institutional theory has been applied frequently to explain why firms adopt initiatives that embrace CSR as vital parts of their corporate strategies (Campbell, 2007; Ioannou & Serafeim, 2012; Pisani, Kourula, Kolk, & Meijer, 2017). According to this perspective, firms engage in CSR to safeguard their legitimacy and make sure that members of the society in which they operate perceive or assume firms’ actions are “desirable, proper, or appropriate within [the] socially constructed system of norms, values, beliefs, and definitions” (Suchman, 1995: 574). By adhering to prevailing beliefs, norms, and values in the institutional environment, firms signal that their values and actions align with those of society, such that they can secure continued access to important stakeholders and their resources (Berrone & Gomez-Mejia, 2009).

A key insight of institutional theory is that governments issue rules and policies in certain areas, so they directly and indirectly affect society’s expectations of proper behavior and exert considerable pressure on firms (DiMaggio & Powell, 1983, 1991; Meyer & Rowan, 1977). Governments’ attention to certain topics has a profound impact on firms’ decisions and actions (Aguinis & Glavas, 2012; Durand, Hawn, & Ioannou, 2019; Ioannou & Serafeim, 2012; Knippen, Shen, & Zhu, 2019; Oliver, 1991). Laws and policies issued by governments reflect social demands and expectations (Xie et al., 2021), such that the governments set “the norms of acceptable behavior in the larger social system” (Dowling & Pfeffer, 1975: 122) and prescribe whether the actions of an organization are legitimate (DiMaggio & Powell, 1983, 1991; Suchman, 1995). Another central tenet of institutional theory is that a firm’s ability to operate depends on an implicit contract with society, which may explain a general assumption that firms uniformly comply with regulatory pressures (Desai, 2016; Hillman & Hitt, 1999; Kassinis & Vafeas, 2006; Meyer & Rowan, 1977; Oliver, 1991). When firms are not sufficiently responsive to these pressures, governments can block their access to important resources (Durand et al., 2019; Hillman & Hitt, 1999). Firms also might suffer consumer, employee, or investor backlash (Luo, Lan, & Tang, 2012). Taken together, governments seemingly can coerce firms, if not de jure at least de facto, to adopt certain practices, which may also explain the “startling” homogeneity in firms’ responses to government regulations (DiMaggio & Powell, 1983: 148).

According to this rationale, firms adopt CSR contracting to signal their conformity with social and environmental governmental regulatory pressures. By adopting this publicly observable practice, firms exhibit their embrace of CSR as an important element of corporate strategy and signal that their executives are committed to stakeholders’ needs when making strategic decisions (Berrone & Gomez-Mejia, 2009; Flammer et al., 2019). That is, by adopting CSR contracting, firms display how they act in line with society’s prescriptions and expectations, which should contribute to safeguarding their legitimacy and sustain their license to operate, which prior research establishes as an important motive for CSR (e.g., Bansal, 2005; Bansal & Roth, 2000; Tashman, Marano, & Kostova, 2019). Therefore, from a conformity perspective, we expect: Hypothesis 1a: The degree of social and environmental regulatory pressures prevailing in a given country is positively associated with the likelihood that firms headquartered in that country adopt CSR criteria in their executive compensation contracts.

Firms also may regard external pressures and internal initiatives as substitutes for achieving some socially desired behavior. Prior corporate governance literature has theorized and empirically documented that the marginal role of a specific mechanism depends on the relative importance of other mechanisms (Booth, Cornett, & Tehranian, 2002; Melis & Rombi, 2021; Williamson, 1983). This perspective also is widely accepted in CSR literature (e.g., Jackson & Apostolakou, 2010; Knudsen, 2017; Knudsen & Brown, 2015); it suggests that external (social and environmental regulatory pressure) and internal (CSR contracting) CSR motivators substitute for each other in stimulating executives to pay attention to CSR. In that case, CSR contracting as an internal motivator could function like a counterweight for the relative lack of governmental social and environmental regulatory pressure as an external motivator. Firms operating in an institutional context with strong social and environmental regulatory pressures may be less inclined to incentivize their executives to pay attention to CSR, because these executives already are sufficiently motivated by existing CSR-related laws and public policies; if their firms do not reach some minimum standard set by the government, they will be penalized by important stakeholders, who will stop providing access to resources (Berrone & Gomez-Mejia, 2009) or even revoke the firm’s social license to operate. In relation to the adoption of CSR contracting, a counterweight perspective implies: Hypothesis 1b: The degree of social and environmental regulatory pressures prevailing in a given country is negatively associated with the likelihood that firms headquartered in that country adopt CSR criteria in their executive compensation contracts.

Moderating Role of Internal Corporate Governance Mechanisms

Regulatory pressures are not always coercive (e.g., Bice, 2017; Xie et al., 2021) and may not evoke uniform responses among firms, particularly in the CSR domain, which features increasingly active regulatory efforts, laws, and public policies (Albareda, Lozano, & Ysa, 2007; Brammer, Jackson, & Matten, 2012; Campbell, 2007; Flammer, 2013; Knudsen & Brown, 2015; Knudsen, Moon, & Slager, 2015). Some laws and public policies mandate certain behaviors; others encourage behaviors, such as by helping define areas of concern, creating minimum standards, or raising a sense of accountability (e.g., Albareda et al., 2008; Bice, 2017; Knudsen & Moon, 2017; Steurer, 2010). Moreover, regulatory pressures are not directly focused on CSR contracting, so they may generate heterogeneous organizational responses in terms of its adoption.

According to this view, the predictions based on the conformity and counterweight perspectives may have more or less explanatory power, depending on the circumstances. Specifically, our theorizing acknowledges that social and environmental regulatory pressures are unlikely to be sole, uniform drivers of decisions to adopt CSR contracting. Firms’ legitimization processes involve interactions of external regulatory pressures and internal corporate governance mechanisms (Aguilera et al., 2012; Schiehll et al., 2014). Their degrees of compliance with regulatory pressures vary (Desai, 2016), because decisions about how to respond to institutional pressures involve a plethora of actors, such as boards of directors and shareholders (Aguilera & Jackson, 2010), each of whom has individual preferences and ideas about whether and how to react to regulatory pressures. Within an institutional environment, according to the rules and regulations that prevail in it, firms may use their varying degrees of freedom to embrace distinct corporate governance practices (Aguilera et al., 2012). The result is a de facto corporate governance bundle (Schiehll et al., 2014; Yoshikawa et al., 2014) in which external regulatory pressures and internal corporate governance conditions interact (Johnson & Greening, 1999; Melis & Rombi, 2021; Sullivan & Gouldson, 2017).

Several internal corporate governance mechanisms might play a role in this corporate governance bundle. We focus on two of them, namely board independence and blockholder ownership, because both corporate governance mechanisms are crucial to monitor self-interested executives and hold them accountable (e.g., Aguilera, Desender, Bednar, & Lee, 2015; Martin, Wiseman, & Gomez-Mejia, 2019; Misangyi & Acharya, 2014; Neville, Byron, Post, & Ward, 2019; Oh, Chang, & Kim, 2018), and prior literature has shown that they play a fundamental role in designing executive compensation contracts (e.g., Devers, Cannella, Reilly, & Yoder, 2007; Hartzell & Starks, 2003; Van Essen, Otten, & Carberry, 2015), as well as in firms’ CSR engagement and performance (e.g., Dam & Scholtens, 2013; De Villiers, Naiker, & Van Staden, 2011; Faller & zu Knyphausen-Aufseß, 2018; Harjoto & Jo, 2011; Liao, Luo, & Tang, 2015). Considering their influence on the firm’s decision to adopt CSR contracting is important too, in that prior executive compensation literature indicates that executives generally prefer higher, less risky compensation delivered in the short-run that is less sensitive to future performance (Murphy, 2013; Shin, 2016; Van Essen et al., 2015), whereas CSR contracting tends to be riskier than traditional executive compensation contracts. Inter alia, “non-financial objectives are set over longer time horizons” and relate to “a recent trend, which implies that companies have much less experience” in setting performance targets (Ioannou, Li, & Serafeim, 2016: 1470). In addition, integrating CSR criteria into executive compensation contracts is likely to make executive compensation more sensitive to future performance, because CSR-related performance takes time to materialize, so executives face more uncertainty about outcomes (Berrone & Gomez-Mejia, 2009; Derchi et al., 2021; De Villiers et al., 2011). Therefore, executives may try to negotiate compensation contracts that minimize their risks by excluding requirements to reach predetermined CSR targets. The presence of either an independent board or a large blockholder is likely to affect the relationship between external social and environmental regulatory pressures and a firm’s decision to adopt CSR contracting.

Moderating role of board independence. Both national corporate governance codes and the agency theory on which they are based recommend that firms’ boards of directors should be composed of independent directors (Cuomo, Mallin, & Zattoni, 2016; Zattoni & Cuomo, 2008). Comparatively, these directors should be better at critically assessing, monitoring, and, if needed, challenging executives. Because independent directors have no recent employment history at their firms, have no other financial relationships with the firms, and do not depend on their firms for their careers, they are better positioned than other nonexecutive directors to limit executives’ influence in the pay-setting process and achieve compensation contracts that keep executives’ preferences at arm’s length (Shin, 2016; Van Essen et al., 2015). 5 Prior literature has documented how independent boards, comprised mostly of independent directors, tend to have stronger stakeholder orientations and longer-term perspectives and pay greater attention to achieving results in an environmentally and socially responsible manner (De Villiers et al., 2011; Johnson & Greening, 1999; Shaukat, Qiu, & Trojanowski, 2016). Compared with other directors, independent directors are less likely to be driven by the primacy of shareholder value, because they have little or no financial relationship with the firms they serve. Moreover, independent directors, as providers of both human and relational capital, can establish useful relationships with a firm’s stakeholders (De Villiers et al., 2011; Mallin, Melis, & Gaia, 2015), which encourage them to consider the expectations and interests of all constituencies and help promote CSR-focused strategies and policies (De Villiers et al., 2011; Johnson & Greening, 1999; Liao et al., 2015). More independent boards therefore may be more prone to adopt CSR contracting, despite executives’ preferences for more certain, short-term-focused compensation (Shin, 2016; Van Essen et al., 2015), which also would help boards signal that they can wield power in the pay-setting process and confirm their reputations as experts in decision control (Fama & Jensen, 1983).

As noted, firms use their varying degrees of freedom to respond to rules and regulations that prevail in a certain institutional environment when embracing distinct corporate governance practices (Aguilera et al., 2012). The conformity perspective suggests that they will adopt CSR contracting in response to strong social and environmental governmental regulatory pressures, to signal they act in line with society’s expectations about CSR. More independent boards may strengthen this tendency, because they focus on the longer term, are keener to respond to societal expectations, and have their reputation as experts in decision control at stake. Because boards with a greater degree of independence may regard CSR contracting as an effective mechanism to motivate executives to conform to social and environmental regulatory pressures, we expect that the internal and external mechanisms reinforce each other and predict: Hypothesis 2a: The positive association between country-level social and environmental regulatory pressures and the likelihood that firms adopt CSR contracting is stronger in firms with boards that are more, rather than less, independent.

The counterweight perspective regarding firms’ responses to external regulatory pressures instead suggests that internal CSR contracting and external regulatory pressures in the CSR domain act as substitutes (e.g., Jackson & Apostolakou, 2010; Matten & Moon, 2008). Social and environmental regulatory pressures could sufficiently motivate executives to focus on CSR, or firms might engage in CSR to address gaps in existing regulations (e.g., Matten & Moon, 2008). Then a negative association arises between the degree of social and environmental regulatory pressures and the likelihood that firms adopt CSR contracting. However, boards of directors likely have their own CSR-related preferences, so they might not acquiesce uniformly to institutional pressures and instead may prefer a more proactive approach. Noting again that more independent boards are sensitive to long-term environmental and social impacts of firms’ activities (De Villiers et al., 2011; Johnson & Greening, 1999; Shaukat et al., 2016), we expect that the negative effect of external regulatory pressures on the adoption of CSR contracting will be weakened as these boards will be more proactive to adopt CSR contracting. That is, we expect that predictions based on the counterweight perspective have less explanatory power when the firm’s board possesses a greater degree of independence: Hypothesis 2b: The negative association between country-level social and environmental regulatory pressures and the likelihood that firms adopt CSR contracting is weaker in firms with boards that are more, rather than less, independent.

Moderating role of blockholder ownership. Blockholders play a key role in corporate governance, because they help resolve the classic agency problem. Because of their sizable financial stakes in firms and the power they exert over executives, large blockholders have strong incentives to bear the costs of monitoring executives to ensure they focus on wealth-creating initiatives (Dalton, Hitt, Certo, & Dalton, 2007; Edmans, 2014). Prior literature also has pointed out that the “effectiveness of corporate governance mechanisms must be considered in light of contingencies related to the ownership structure of the firm” (Desender, Aguilera, Crespi, & García-Cestona, 2013: 840). Thus, it is highly likely that blockholders have a role in the corporate governance bundle (Desender et al., 2013); their presence may moderate the relationship between external regulatory pressures and the adoption of CSR contracting. However, given the complexity of the bundle, its directional effect in the bundle is difficult to predict.

On the one hand, large blockholders may require firms to pay more attention to CSR, because they expect to benefit in the long run from the positive effects of CSR on firms’ financial performance (Dam & Scholtens, 2013). Moreover, blockholders encourage executives to engage in CSR initiatives to serve their self-interests (Faller & zu Knyphausen-Aufseß, 2018); if the firm displays a lack of attention to CSR, a large blockholder—who is perceived to exert control over the firm—may be held accountable and become a target of external criticism by activists, the media, and other interest groups (Goergen & Renneboog, 2016). For example, after the 2018 Morandi Bridge collapse in Genoa (Italy), which claimed 43 victims, prominent financial media blamed the Benetton family, the controlling shareholder of Atlantia (the company that managed the bridge, through its subsidiary Autostrade per l’Italia). The family suffered a strong reputational backlash, even though they were not directly involved in the management of the company (The New York Times, 2019).

6

Considering how firms’ degrees of compliance with regulatory pressures vary (Desai, 2016), and decisions about how to respond involve actors, including blockholders (Aguilera & Jackson, 2010), the conformity perspective seems viable. Its underlying premise is that firms, in an attempt to safeguard their legitimacy, visibly show that they are acting in accordance with society’s expectations (e.g., Berrone & Gomez-Mejia, 2009; Flammer et al., 2019). Combined with the recognition that blockholders are specifically concerned about the reputational effects of adopting CSR contracting, we argue that the presence of a large blockholder may strengthen the firm’s tendency to conform to institutional pressures. That is, large blockholders of firms headquartered in countries with heightened regulatory pressures are more concerned about the impacts of such pressures on their firm’s (and their own) reputations. In such cases, firms are more likely to tie executive compensation to CSR targets, to signal to constituencies that they are responding to societal pressures, to ensure the firm’s legitimacy, and to uphold the firm’s and the blockholder’s reputations. However, the reasoning underlying the counterweight perspective is that regulatory pressures sufficiently motivate executives to pay attention to CSR, so CSR contracting is not needed. Adding the notion that blockholders may be particularly concerned about the reputational effects of CSR but also the long-term positive effects on financial performance leads us to predict a situation in which a large blockholder may stimulate the firm to go beyond what is expected of it in terms of CSR, in view of prevailing environmental and social regulatory pressures. Therefore, the negative association between social and environmental regulatory pressures and the adoption of CSR contracting might be weaker in the presence of a large blockholder. Formally, we expect: Hypothesis 3a: The positive (negative) association between country-level social and environmental regulatory pressures and the likelihood that a firm headquartered in the country adopts CSR contracting is strengthened (weakened) by blockholder ownership.

On the other hand, CSR initiatives usually involve short-term costs with initially uncertain outcomes (Cox, Brammer, & Millington, 2004; Faller & zu Knyphausen-Aufseß, 2018). These costs reduce the short-term profits available to shareholders, which tend to increase as blockholder ownership increases. That is, large blockholders must bear comparatively large amounts of the costs associated with future benefits for multiple shareholders and stakeholders (Faller & zu Knyphausen-Aufseß, 2018; Mackenzie, Rees, & Rodionova, 2013). Because the benefits of these efforts are uncertain and materialize in the long run (Berrone & Gomez-Mejia, 2009), large blockholders may perceive an increasing discrepancy between their costs and potential benefits (Barnea & Rubin, 2010). This discrepancy may decrease their support for CSR; ultimately, shareholders expect financial returns on their investments (Faller & zu Knyphausen-Aufseß, 2018; Jain & Jamali, 2016). If large blockholders focus mainly on the costs and uncertain outcomes of CSR initiatives, they could use their power in the executive compensation design process to ensure executives are not incentivized further to engage in CSR initiatives in institutional environments that do not require internal motivation for CSR, because executive discretion already is constrained by external social and environmental regulatory pressures. In this view, blockholders’ incentives to decrease CSR costs (here, those related to CSR contracting) are greater when they are “protected” by institutional contexts that already regulate social and environmental initiatives. Combining these arguments with the conformity perspective, we posit that the presence of a large blockholder could weaken a firm’s tendency to adopt CSR contracting to conform to societal regulatory pressures. However, if a firm acts in line with the counterweight perspective, the negative association between social and environmental regulatory pressures and the adoption of CSR contracting could be strengthened by the presence of a large blockholder. We expect: Hypothesis 3b: The positive (negative) association between country-level social and environmental regulatory pressures and the likelihood that a firm headquartered in the country adopts CSR contracting is weakened (strengthened) by blockholder ownership.

Method

Sample

We use Thomson Reuters’s (now, Refinitiv) ASSET4 database, which contains systematic and auditable environmental, social, and governance (ESG) information on listed firms worldwide. The database has been used widely in previous studies, suggesting the quality of the data (e.g., Barko, Cremers, & Renneboog, 2021; Hartmann & Uhlenbruck, 2015; Ioannou & Serafeim, 2012). The initial sample consisted of 37,342 firm-year observations, representing 5,051 unique firms listed in 49 countries over 2001 through 2015. After constructing our main dependent variable (first-time adoption of CSR contracting), we removed 428 firms (9,011 firm-year observations). 7 We also removed 1,051 firms (6,030 firm-year observations) to exclude countries with fewer than 40 observations in the period under examination and firms that operate in the financial industry (e.g., banks, insurance companies). To merge this data set with other country-level data sets, we discarded the first two years (2001 and 2002), due to missing country-level data, which resulted in the exclusion of another 891 firms (5,171 firm-year observations). Finally, we removed 353 firms (4,840 firm-year observations) because of missing data at the firm level. The final sample consists of 12,290 firm-year observations, comprising an unbalanced panel of 2,328 firms listed in 37 countries in 2003 through 2015.

Variable Measurement

Dependent variable. Because the presence of CSR-linked compensation policies could be sticky across years, we focus on a firm’s first-time adoption of CSR contracting. Data on CSR contracting come from ASSET4 and are based on the item “Is the senior executive’s compensation linked to CSR/Health&Safety/Sustainability targets?” 8 The dependent variable (CSR Contracting) equals 1 for the firm-year observation in which a firm adopts CSR contracting for the first time and 0 for the firm-year observations before the first adoption. If a firm never adopts a CSR-linked compensation policy during the period of analysis, we code CSR Contracting as 0 for all available years.

Independent variables of interest. The independent variable Pressure estimates the degree of external social and environmental regulatory pressures, measured as the combination of the widely used Environmental Performance Index (EPI) and Human Development Index (HDI) (e.g., Atlason & Gerstlberger, 2017; Berry, Kaul, & Lee, 2021; Chung & Beamish, 2012; Hoskisson, Cannella, Tihanyi, & Faraci, 2004; Xiao, Wang, van der Vaart, & van Donk, 2018). The EPI is produced by the Yale Center for Environmental Law & Policy and Columbia University’s Earth Institute in collaboration with the World Economic Forum; 9 it provides a multidimensional measure of countries’ environmental regulations and policies (Moldan, Janoušková, & Hák, 2012) according to two main factors, environmental health and ecosystem vitality, which in turn comprise 11 issue categories (e.g., air pollution, water and sanitation quality, and biodiversity and habitat protection). Values in the index range from 0 to 100, with higher scores expressing long-standing regulatory attention to protecting the environment. The HDI was developed by the United Nations Development Program (UNDP). This aggregate, country-level multidimensional indicator measures progress toward greater human well-being and is based on data on three key dimensions: a long and healthy life, knowledge (e.g., mean years of schooling), and a decent standard of living (Deb, 2015). Values range from 0 to 1, with higher values indicating a higher degree of regulatory attention to human protection. To construct our overall multidimensional measure of external social and environmental regulatory pressures, Pressure, we first standardize both EPI and HDI, such that they have mean values of 0 and standard deviations of 1 and are comparable in terms of scale. Then we sum the two standardized variables to arrive at an overall score, whose values range (on a continuous scale) from a minimum of −8.67 to a maximum of +2.39, capturing the various degrees of social and environmental regulatory pressure.

The independent variable Board Independence estimates the level of board independence, measured as the percentage of independent directors on a board (Ikram et al., 2019; Knippen et al., 2019; Kock, Santaló, & Diestre, 2012) (source: ASSET4). Then the independent variable Blockholder Ownership estimates the level of influence of a blockholder over a firm’s decision, measured as the ownership of the largest shareholder (Aslan & Kumar, 2012; Claessens, Djankov, Fan, & Lang, 2002). We define the largest shareholder as the largest owner by voting power (Crifo, Diaye, Oueghlissi, & Pekovic, 2016) (values range from 0 to 100) (source: ASSET4).

Country-level control variables. The control variable Corporate Governance Code Maturity reflects prior literature (Enrione, Mazza, & Zerboni, 2006; Haxhi & Aguilera, 2017) that suggests that the longer the period since the issuance of the first corporate governance code, the more the codes’ prescriptions become “institutionalized” (Haxhi & Aguilera, 2017). Because firms in countries with more mature codes tend to take for granted best practices related to executive compensation (Enrione et al., 2006), maturity of the corporate governance code may be positively associated with CSR contracting.

The control variable Common Law (La Porta, Lopez-de-Silanes, Shleifer, & Vishny, 1998) recognizes that legal origin can classify countries that follow a shareholder versus a stakeholder model. In common-law countries, shareholders’ interests are well protected and may prevail, potentially lowering executives’ efforts to address the interests of other stakeholders (Ioannou & Serafeim, 2012). However, in these countries, firms also are more likely to implement specific CSR measures to legitimize and enhance their images (Demirbag, Wood, Makhmadshoev, & Rymkevich, 2017). Thus, compensation policies that reward firms for CSR activities may be more likely.

The control variable Voice recognizes that in countries with higher perceptions of freedom of expression, freedom of association, free media, and citizens’ abilities to participate in selecting governments, firms face more reputational risks of public exposure because the press and other groups (e.g., NGOs) likely monitor and report their behavior (Hartmann & Uhlenbruck, 2015; Nikolaeva & Bicho, 2011). Therefore, firms headquartered in these countries are more likely to adopt CSR contracting to appease public opinion and safeguard their legitimacy and reputation.

Finally, the control variable Corruption acknowledges that in comparatively more corrupt countries, firms are more likely to engage in unethical activities for economic reasons (e.g., reducing production costs), and governments are less likely to punish socially irresponsible activities. Accordingly, firms may feel less pressure to adopt or incentivize CSR initiatives (Ioannou & Serafeim, 2012). The variable measures perceptions of the extent to which public power is exercised for private gain and includes both petty and grand forms of corruption.

Firm-level control variables. The control variable Controversies reflects prior literature that suggests firms subjected to more social or environmental controversies are under greater public scrutiny (Aouadi & Marsat, 2018). As part of a strategic reaction, these firms likely adopt compensation policies that improve their social and environmental reputations (e.g., Jackson & Apostolakou, 2010; Luo et al., 2012). In addition, the control variable Sensitive Industry recognizes that firms that operate in socially and environmentally sensitive industries (e.g., pharmaceutical, resource extraction; see Brammer & Millington, 2005) are more likely than other firms to value and be valued according to their social and environmental performances; they are likely to adopt CSR contracting sooner to signal they take their responsibilities seriously (Ikram et al., 2019). In turn, we include the control variable Social and Environmental Performance because firms with comparatively better social and environmental performance can compensate their executives accordingly, such that they are more likely to link executive compensation to social and environmental performance targets (Ikram et al., 2019).

The firm-level control variables Board Diversity and Board Size acknowledge that more diverse and larger boards are better able than other boards to balance the interests of multiple stakeholders and include social and environmental issues in board deliberations (De Villiers et al., 2011; Liao et al., 2015). Boards with these characteristics are more likely to adopt or incentivize CSR initiatives. We include a dummy variable (TSR) indicating whether the CEO’s compensation is linked to total shareholder return to control for the possibility that financial-based compensation elements may encourage the CEO to focus particularly on shareholder value creation and, hence, may be working toward opposite ends from an economic perspective. 10 With the control variable Firm Size, we also consider whether, compared with smaller firms, larger firms receive greater pressure from stakeholders and have more discretionary resources to allocate to CSR activities (Jackson & Apostolakou, 2010; Johnson & Greening, 1999), such that they might be more likely to incentivize executives according to CSR performance.

The firm-level control variable Sustainability Index recognizes that a firm’s presence in a sustainability index signals its attention to linking its market value to its CSR (Ioannou & Serafeim, 2012), so it is more likely than other firms to adopt CSR initiatives. Furthermore, Return On Assets recognizes that better performing firms are more likely to generate slack resources that can be used to reward executives for meeting sustainability goals (Chiu & Sharfman, 2011; Waddock & Graves, 1997), so they are more likely to adopt CSR initiatives.

Consistent with prior studies (e.g., Derchi et al., 2021; Flammer et al., 2019; Ikram et al., 2019), we include Leverage, measured as the ratio of total debt to total assets, as a control variable, because higher leverage may lower a firm’s resources available to CSR activities. We also control for Analyst Coverage, measured as the number of financial analysts following the firm, as analysts are considered to be an effective external governance mechanism, which increases the likelihood of CSR contracting (Ikram et al., 2019). Finally, we include year and industry effects to control for possible systematic differences in first-time adoption across years and sectors. We use the Fama-French classification to group firms in industries by considering 16 nonfinancial industries.

Estimation

We focus on first-time adoption of CSR contracting, which occurs at discrete points in time. For this reason, we remove a firm from the sample after the year in which it adopts CSR contracting. We use probit models for our main analysis, because our dependent variable is dichotomous; we add interaction terms to test H2a, H2b, H3a, and H3b, controlling for year and industry-fixed effects, and we cluster standard errors at the country and firm levels (Petersen, 2009). In line with prior research (e.g., Martin et al., 2019; Zolotoy, O’Sullivan, Martin, & Wiseman, 2021), we test each moderated relationship in a distinct model. 11

Results

Descriptive Statistics and Correlations

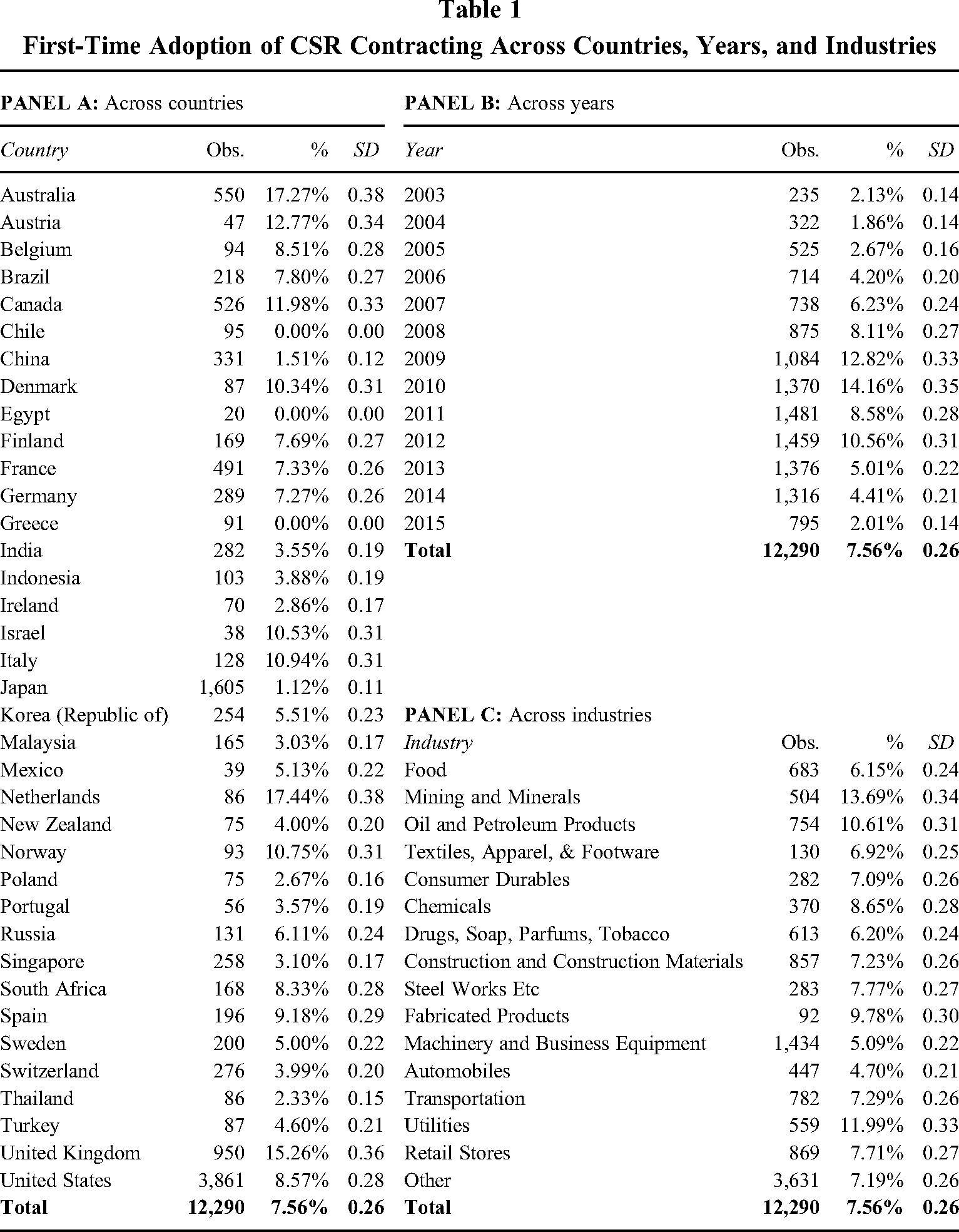

Table 1 presents the descriptive statistics for our dependent variable. In Table 1, Panel A, we note that 7.56% of firms in our sample decided to adopt CSR contracting for the first time, with a significant variation in the adoption rates across countries, time, and industries. The highest degree of first-time adoption occurred among firms headquartered in the Netherlands (17.44%), Australia (17.27%), United Kingdom (15.26%), Austria (12.77%), and Canada (11.98%). Table 1, Panel B, shows that the rate of adoption of CSR contracting increased during the years analyzed. This increase may reflect stronger external pressures on firms to engage with stakeholders, with compensation policies signaling stakeholder engagement (Flammer et al., 2019). The highest rate of adoption of CSR contracting occurred during 2009 and 2010; whereas only 2.13% of firms in our sample had adopted the policy in 2003, 14.16% of firms adopted it by 2010. Finally, Table 1, Panel C, shows that firms in environmentally sensitive industries (e.g., mining and minerals, oil and petroleum products, utilities) tend to adopt CSR contracting at a higher rate than other firms, whereas firms operating in automobile, machinery, and business equipment industries adopt CSR contracting at a lower rate.

First-Time Adoption of CSR Contracting Across Countries, Years, and Industries

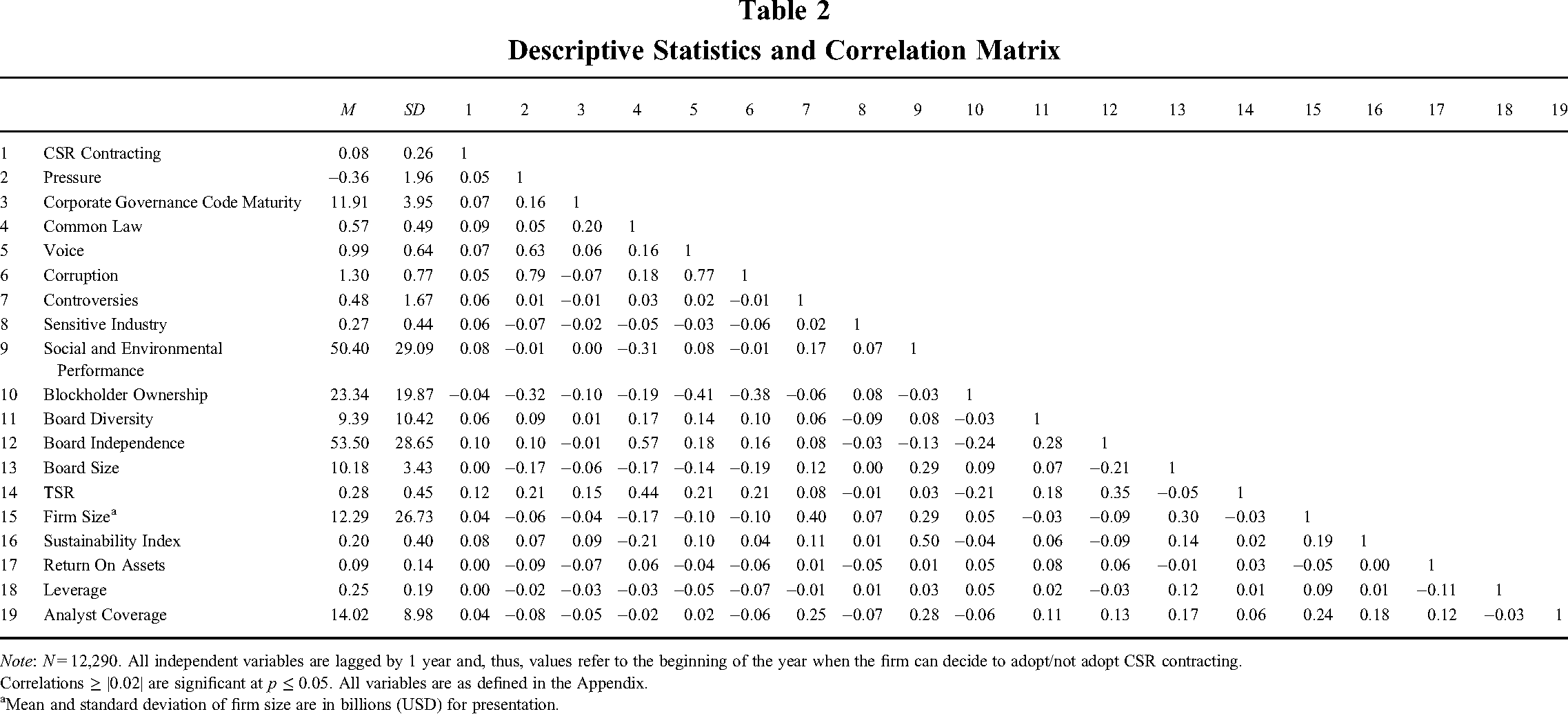

Table 2 contains the descriptive statistics and correlations. It shows Pressure has an average value of −0.36. 12 The average value of Board Independence is 53.5%, suggesting independent directors represent the majority of the board, and the largest owner (Block Ownership) has a stake of 23.34% of a firm’s shares, on average.

Descriptive Statistics and Correlation Matrix

Note: N = 12,290. All independent variables are lagged by 1 year and, thus, values refer to the beginning of the year when the firm can decide to adopt/not adopt CSR contracting.

Correlations ≥ |0.02| are significant at p ≤ 0.05. All variables are as defined in the Appendix.

Mean and standard deviation of firm size are in billions (USD) for presentation.

In terms of the control variables, the average value of Corporate Governance Code Maturity is approximately 12, suggesting that about 12 years have passed since a country adopted its first corporate governance code; about 57% of firms are headquartered in common law countries; the average Voice value of 0.99 implies that firms tend to be headquartered in countries in which perceived freedom is high; and the average value of Corruption is 1.30, with a minimum of −1.09 and a maximum of 2.55, where lower values reflect greater control over corruption.

Furthermore, though Table 2 shows that the number of social and environmental controversies in a year (Controversies) averages less than 1, some firms actually have had more than 30 media controversies; they likely fall under strong public scrutiny. Approximately 27% of firms operate in socially and environmentally sensitive industries (Sensitive Industry), and Social and Environmental Performance equals, on average, 50.40, with potential values ranging from 0 to 100. In terms of financial-based compensation, 31% of firms have a CEO’s compensation linked to TSR. The average board comprises 10 directors, of whom about 9% are women (Board Diversity). Approximately 20% of firms are included in at least one sustainability stock exchange index (Sustainability Index). The firms in the sample also are large (average total assets equaling approximately $12 billion), and they have an average Return On Assets of approximately 9%. Firms are followed, on average, by 14 analysts, and their debt-to-assets ratio is, on average, 0.25 (Leverage).

Table 2 reveals that Pressure and Board Independence are positively associated with first-time adoption of CSR contracting, whereas Blockholder Ownership is negatively associated with it. The correlations of the independent variables mostly are below |0.6|. In the few cases in which correlations are greater than |0.6|, multicollinearity is unlikely to be a critical concern, according to the low mean variance inflation factors (average VIFs are around 3.5 or lower; e.g., Neter, Wasserman, & Kutner, 1985; Oh et al., 2018).

Hypothesis Testing

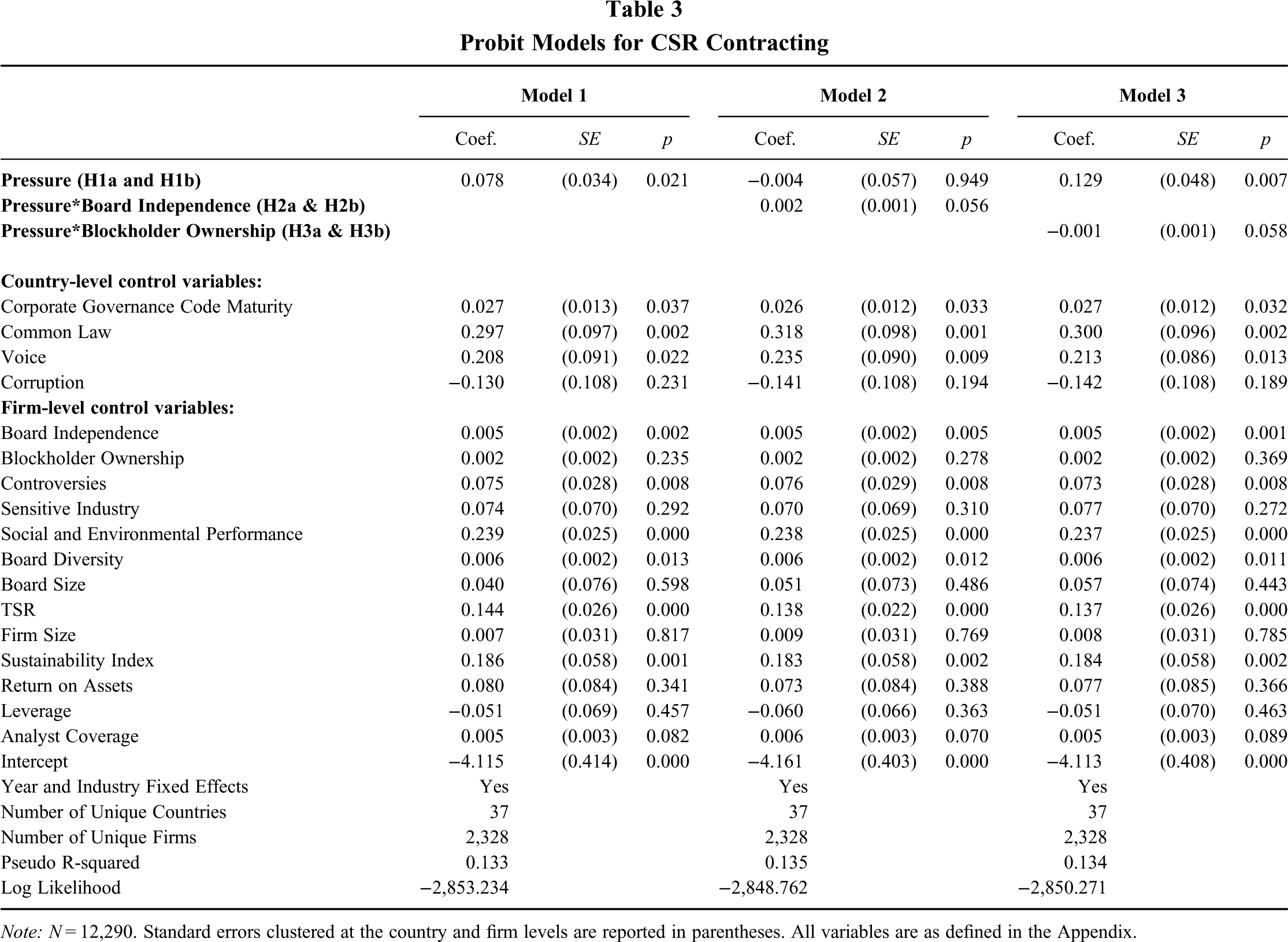

Table 3 presents the results of multivariate regression analyses. Model 1 indicates a significant positive association of external social and environmental regulatory pressure on the adoption of CSR contracting (p = 0.021), in support of H1 and the conformity perspective: firms headquartered in countries that exert stronger social and environmental regulatory pressures (i.e., countries that have more relevant laws, public policies, and regulations) are more likely to adopt CSR criteria in executive compensation contracts. Then, Model 2 documents the positive association between external social and environmental regulatory pressures, and first-time adoption of CSR contracting is strengthened by board independence (p = 0.056). Independent directors seem to contribute to the adoption of CSR contracting, particularly in institutional environments in which social and environmental regulatory pressures are higher. This finding provides support to H2a (conformity perspective), which also implies that H2b (counterweight perspective) should be rejected.

Probit Models for CSR Contracting

Note: N = 12,290. Standard errors clustered at the country and firm levels are reported in parentheses. All variables are as defined in the Appendix.

Model 3 in Table 3 indicates that the positive association between external social and environmental regulatory pressures and first-time adoption of CSR contracting is negatively moderated by blockholder ownership (p = 0.058). In institutional environments in which social and environmental regulation is greater, blockholder ownership weakens the effects of external social and environmental regulatory pressures on first-time adoption of CSR contracting. An explanation for this finding may be that controlling shareholders believe CSR initiatives involve costs, with uncertain outcomes that they must bear, whereas independent directors are unlikely to bear the financial costs of CSR initiatives. Large blockholders seem to function like substitutes, lowering the likelihood of CSR contracting in institutional environments that already value and regulate social and environmental performance. Taken together, this finding provides support of H3b, while H3a is rejected. The stronger tendency of a firm to adopt CSR contracting to conform to societal regulatory pressures (conformity perspective) is weakened by the presence of large blockholders.

In terms of country-level control variables, we find that firms headquartered in common-law countries and countries with more mature corporate governance codes, and higher levels of perceived freedom, are more likely to adopt CSR contracting. At the firm level, firms that have suffered more controversies covered by the media, with comparatively better corporate social and environmental performance, with more diverse boards, that belong to a sustainability index, and are followed by a larger number of analysts are more likely to adopt CSR contracting. We also find that CSR contracting is more likely when financial-based compensation elements (TSR) are in place, so incentives for both shareholder and stakeholder value creation can coexist.

Robustness Analyses

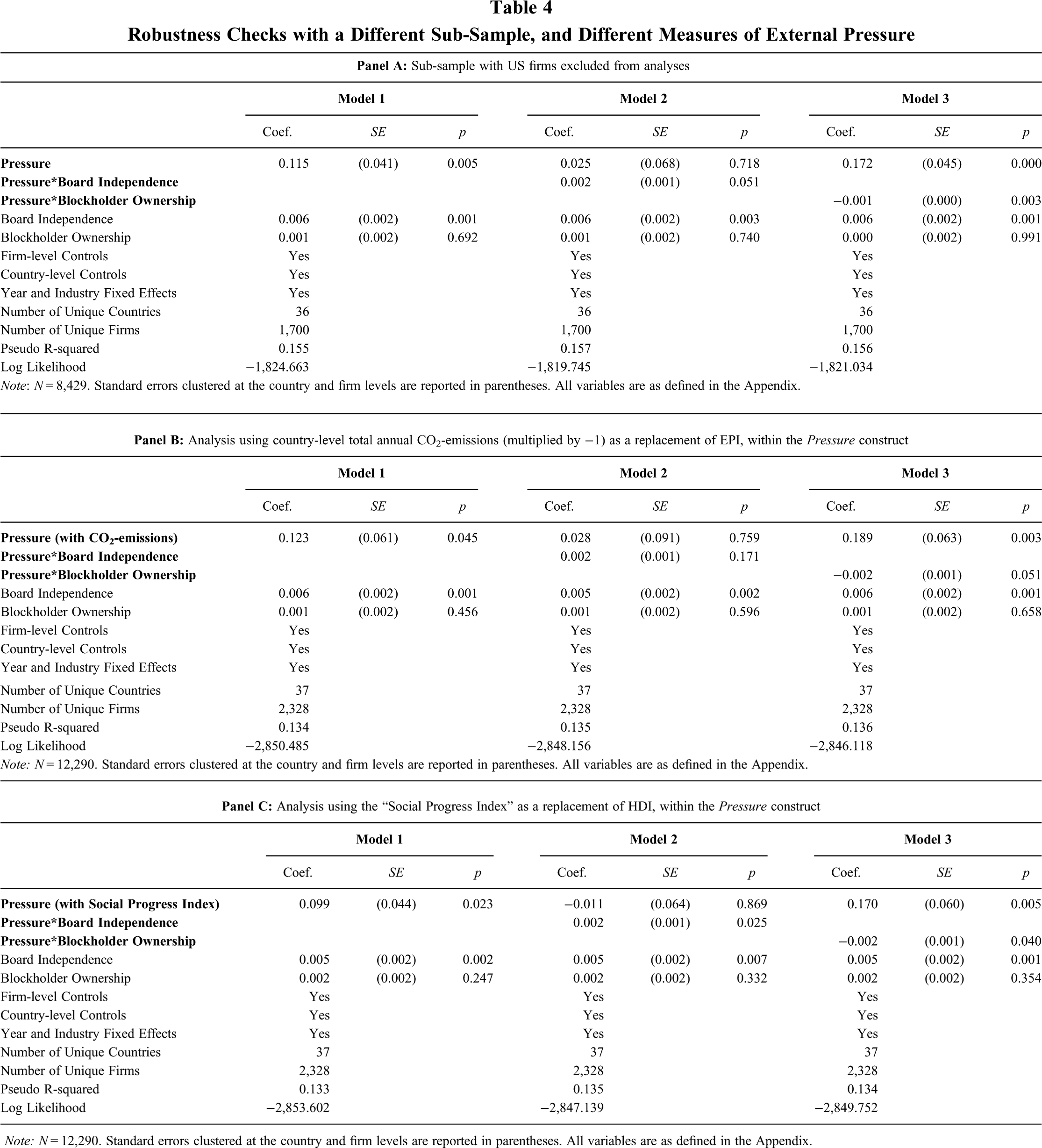

First, because our sample is unbalanced, with a particularly large number of firms headquartered in the United States, and because determinants of adoption of CSR contracting outside the United States have been unexplored, we repeat our analysis but exclude U.S. firms. Table 4, Panel A, presents the findings, which are consistent with the main results.

Robustness Checks with a Different Sub-Sample, and Different Measures of External Pressure

Note: N = 12,290. Standard errors clustered at the country and firm levels are reported in parentheses. All variables are as defined in the Appendix.

Second, to test the robustness of our results to the choice of our measure of the degree of external social and environmental regulatory pressure (Pressure), we first employ an alternative for EPI, namely, the level of CO2 emissions in a country (on an annual basis, taken from the World Bank), multiplied by −1. Recent research (Berry et al., 2021; Kim & Lyon, 2015) uses this measure as alternative for EPI, because lower levels of CO2 emissions in a country arguably can result from the country’s environmental stringency. As Table 4, Panel B, shows, the results remain consistent when we use this alternative measure of external environmental regulatory pressure, except that board independence no longer significantly strengthens the positive association between social and environmental regulatory pressures and the likelihood that firms adopt CSR contracting. Then, as an alternative to HDI, we use the Social Progress Index, which measures a country’s capacity to meet the basic human needs of its citizens, citizens’ well-being (education, healthy life), and the opportunities citizens have to reach their potential (Porter, Stern, & Green, 2014). It reflects the average of three dimensions: basic human needs, foundations of well-being, and opportunity. 13 In Table 4, Panel C, the results remain consistent with our main findings.

Third, we challenge our own estimation method. The results remain consistent when we replace our model with a random effects probit panel model, controlling for industry and year fixed effects (see Table 5, Panel A). 14 Fourth, in line with prior literature (e.g., Beck, Swaminathan, Wade, & Wezel, 2019; Chatterji, Cunningham, & Joseph, 2019), we also replicate our analysis using a complementary log-log model, a form of discrete event history analysis that is particularly useful when the probability of an event is small (e.g., Allison, 1982; Chatterji et al., 2019). Unlike probit analysis, it employs an asymmetric transformation (Chatterji et al., 2019; Coff, 2002). Compared with other discrete-time models, this model provides estimates consistent with those obtained from proportional continuous-time hazard models, with the advantage of accommodating exits (i.e., CSR contracting first-time adoption) measured in yearly intervals (Jenkins, 1995; Petersen, 1993). In Table 5, Panel B, the results remain consistent with our main findings. 15

Robustness Checks with Different Estimation Methods

Note. N = 12,290. Coefficients are expressed in terms of exponentiated coefficients to represent hazard ratios. Standard errors clustered at the country and firm levels are reported in parentheses. All variables are as defined in the Appendix.

Fifth, a potential drawback of our data set is that it may suffer from self-selection. Firms included in the sample are nonrandom in the sense that only firms that already have used performance-based pay to incentivize their executives can decide to adopt CSR contracting as part of their executive compensation contracts. To alleviate this concern, we run Heckman’s self-selection model (Certo, Busenbark, Woo, & Semadeni, 2016). In our case, some variables, not included in the model, may affect the probability of entering the sample (by affecting the presence of performance-based pay and thus CSR contracting). We control for the determinants of performance-based pay by considering a larger sample and rerunning our main models. Using the Stata “heckprob” command, we add a selection model, with performance-based pay as a dependent variable. 16 We also add Hofstede’s (2001) power distance as an instrument. 17 Theoretically, power distance may diminish the likelihood of performance-based pay, because firms that operate in countries in which power is more acceptable likely rely on pay structures that are not linked to performance (Tosi & Greckhamer, 2004), reflecting CEOs’ preferences for pay that is less uncertain. Untabulated results indicate that power distance is significantly, negatively correlated with performance-based pay but not CSR contracting. In Table 6, even after we control for potential self-selection biases, the results largely remain unchanged. Moreover, the Wald test of independent equations rejects the null hypothesis, so the outcome is significantly different from one obtained by fitting the probit and selection models separately.

Robustness Check with Heckman’s Self-Selection Model

Note: N = 12,060. Standard errors clustered at the country and firm levels are reported in parentheses. Power Distance is based on Hofstede (2001). The dependent variable in the first stage (Presence of performance-based pay) is a dummy variable that equals 1 if the company has a performance-based pay policy, and 0 otherwise (from: ASSET4). All other variables are as defined in the Appendix.

Sixth, another potential econometric issue relates to the interpretation of the coefficients of interaction terms in nonlinear models, such as probit models. In nonlinear models, the interaction effect cannot be evaluated simply by looking at the sign, magnitude, and statistical significance of the coefficient on the interaction term (Ai & Norton, 2003; Wiersema & Bowen, 2009). Also, the interaction term does not reflect the significance of the conditional effects of interest, as it does in linear models (Ai & Norton, 2003; Greene, 2010). Consistent with prior studies (e.g., Gupta, Mortal, Silveri, Sun, & Turban, 2020), we compute and graphically portray the marginal effect of the interacted variables’ change in our model, as well as the correct standard errors, using the “inteff” Stata command (Norton, Wang, & Ai, 2004). Figure 1 shows scatterplots of the interaction effect as a function of predicted probability of CSR contracting, as well as the z statistics for the interaction effect. Panel A refers to the moderating effect of board independence, and Panel B pertains to blockholder ownership. As it shows, the interpretation of our results remains consistent with interpretations in our main analysis.

Panel A: Interaction effects and corresponding Z-statistics on the interaction variable between external social and environmental regulatory pressures and board independence. Panel B: Interaction effects and corresponding Z-statistics on the interaction variable between external social and environmental regulatory pressures and blockholder ownership.

Seventh, the results (untabulated) do not change after we winsorize all continuous variables at the 1% to 99% level (overall sample and sample by year). Eighth and finally, we run two robustness tests with alternative proxies for board independence and blockholder ownership. That is, rather than considering the percentage of independent directors on the board as an alternative proxy, we include a dummy that assumes a value of 1 if the majority of members sitting on a firm’s board can be considered independent and 0 otherwise. Then, we rerun our analyses to consider the impact of all blockholders, rather than only the impact of the major one, to account for the impact of the strategic ownership structure on the firm’s decision-making processes (Aslan & Kumar, 2012; Dam & Scholtens, 2013). We determine the impact of strategic ownership structure by the well-known Hirschman-Herfindahl index, which is constructed by summing the squared shareholdings of all major blockholders of a company (Dam & Scholtens, 2013). A higher value on this variable implies more concentrated ownership, which arguably suggests greater impact of the blockholders on corporate decision-making processes. The results are qualitatively similar to the main findings when we use these alternative proxies for board independence and blockholder ownership.

Discussion

This study examines the combined roles of external social and environmental regulatory pressures and internal corporate governance in explaining firms’ decisions to adopt CSR contracting and integrate CSR criteria into executive compensation contracts. We analyze an international sample of 2,328 unique firms (12,290 firm-year observations) headquartered in 37 countries over a period from 2003 to 2015. This sample choice allows us to examine the impact of diverse institutional environments on firms’ decisions to adopt CSR contracting. We find that firms headquartered in countries with comparatively greater social and environmental regulatory pressures are more likely to adopt CSR contracting. Notably, firms do not acquiesce uniformly to external social and environmental regulatory pressures but respond according to their internal corporate governance. Specifically, board independence has supportive effects on the first-time adoption of CSR contracting for firms headquartered in countries with comparatively higher social and environmental regulatory pressures. We also find blockholder ownership has a dampening effect on the decision to adopt CSR contracting when social and environmental regulatory pressures are comparatively higher. This finding favors the view that large blockholders tend to focus on the costs and uncertain outcomes of CSR initiatives and use their power to ensure executives are not incentivized to engage in CSR initiatives in institutional environments in which external social and environmental regulatory pressures already constrain executive discretion.

Our theory and findings make several contributions to the literature. In particular, they contribute to emerging literature on a relatively new phenomenon in the boardroom: linking executive pay to social and/or environmental performance targets (Flammer et al., 2019; Hong et al., 2016; Ikram et al., 2019). Our study offers the first systematic attempt to expand the scope of extant CSR contracting research to a worldwide, longitudinal sample of firms headquartered in diverse institutional settings. Flammer et al. (2019) document that firms located in various U.S. states (e.g., Pennsylvania) that have enacted constituency statutes (i.e., directors are legally required to attend to the interests of all corporate stakeholders in their decision-making) are more prone to adopting CSR contracting, which indicates that institutions matter. We extend their findings in three important ways. First, whereas Flammer et al. (2019) focus on the effects of a single feature within the U.S. legal/institutional framework, we focus on the role of countries’ social and environmental regulations and policies beyond those enacted in law and thus establish that firms can be pressured through institutions other than strict laws, including policies and recommendations. Second, our measure does not assume a binary condition, featuring the presence or not of a regulatory pressure, and instead accounts for differences in the extent of regulatory pressure to attend to social and environmental issues. Third, we control for other institutional features, such as corruption and corporate governance maturity, apart from the stakeholder versus shareholder orientation (as reflected in our study by legal origin), that also may affect firms’ decisions to adopt CSR contracting.

Furthermore, our study shows that external social and environmental regulatory pressures positively affect the adoption of CSR contracting. This result is in line with the legitimacy-based conceptual approach to CSR (e.g., Bansal, 2005; Bansal & Roth, 2000; Tashman et al., 2019), according to which firms engage in CSR incentive plans to respond to social demands and expectations at the country level. In line with institutional theory, we find that firms respond to regulatory pressures (Desai, 2016; Hillman & Hitt, 1999; Kassinis & Vafeas, 2006; Meyer & Rowan, 1977; Oliver, 1991; Xie et al., 2021) by signaling they are practicing responsible and legitimate CSR behavior at the executive level. Thus, our results contrast with the perspective that sees firms’ CSR initiatives as substitutes for a lack of public social responsibility and regulation (e.g., Jackson & Apostolakou, 2010; Matten & Moon, 2008). This perspective would predict a mitigating role of social and environmental regulatory pressures, such that they reduce the need to incentivize executives to pursue greater CSR performance, because their discretion is already constrained and enforced by regulation. Instead, we find a conformity effect, and firms positively respond to institutional pressures by adopting CSR contracting to signal that their incentive structures align with social demands and expectations. Notably, our study extends prior literature that has traditionally assumed that firms uniformly comply with regulatory pressures to retain legitimacy (e.g., DiMaggio & Powell, 1983, 1991) and build on a theoretical, comparative approach to CSR (e.g., Aguilera et al., 2012; Jackson & Apostolakou, 2010; Matten & Moon, 2008) that assumes homogeneous organizational responses by all firms in the same type of political economy (Hall & Soskice, 2001). Not only does diversity exist among countries in the same type of political economy, in terms of regulatory pressures, but these same social and environmental regulatory pressures may evoke heterogeneous responses by firms within a country.

The overall picture that emerges from our study thus reflects a complex set of influences. Internal corporate governance mechanisms effectively help explain how firms respond to institutional pressures (Aguilera et al., 2007; Surroca, Aguilera, Desender, & Tribó, 2020). Firms with comparatively more independent boards are more likely to adopt CSR contracting in institutional environments that already favor socially and environmentally friendly behaviors; independent directors have a positive effect on tying executive compensation to CSR targets when signaling their firms’ responses to CSR regulatory pressures. We also find that the greater the degree of blockholder ownership in firms, the less likely the firms’ CSR contracting will be affected by external CSR regulatory pressures. Large blockholders lower the likelihood of CSR contracting in institutional environments that already value and regulate social and environmental performance, perhaps because they bear much of the costs of CSR activities, for which the benefits are uncertain (Faller & zu Knyphausen-Aufseß, 2018; Mackenzie et al., 2013). Meanwhile, our finding of a negative interactive effect of blockholder ownership supports the idea that controlling shareholders actually may favor CSR contracting that reduces conflicts of interest between managers and noninvesting stakeholders (Harjoto & Jo, 2011) in low regulatory pressure settings in which CSR conflicts of interest are likely to be greater. Thus, even if both blockholders and independent directors serve as monitoring mechanisms, they have different roles in the corporate governance bundle (Oh et al., 2018): they both perceive the benefits of CSR regulatory pressure, but they exploit these benefits in contrasting ways. Independent directors, who tend to have greater stakeholder orientation (De Villiers et al., 2011; Johnson & Greening, 1999; Shaukat et al., 2016), have their personal reputation at stake but do not bear any important financial cost of the decision, and they respond to countries’ CSR regulatory pressures by being more prone to adopt CSR contracting. Blockholders, who largely bear the financial costs, use their power to ensure managers are not incentivized to engage in CSR initiatives when institutional contexts already require them. This finding extends emerging literature on corporate governance bundles (Aguilera et al., 2012; Schiehll et al., 2014; Yoshikawa et al., 2014) that mainly has focused on the interplay of various firm-level monitoring mechanisms (Misangyi & Acharya, 2014; Rediker & Seth, 1995) or the moderating role of country-level effects in corporate governance–performance relationships (Surroca et al., 2020). We contribute to studies of “national governance bundles” (Schiehll et al., 2014) by arguing that country-level characteristics are the main effects, whereas firm-level corporate governance mechanisms have moderating and opposite roles. No previous study has examined the impact of country-level CSR regulatory pressure on the relationship of ownership and CSR initiatives either.

Understanding how country- and firm-level corporate governance mechanisms interact to influence executive compensation design—specifically, the integration of CSR targets into executive compensation—has implications for both corporate governance theory and practice. By integrating the lenses provided by legitimacy and institutional theories, we contribute to literature on executive compensation across different institutional contexts (Francoeur et al., 2017; Van Essen, Engelen, & Carney, 2013), revealing how firms respond to institutional pressures (Boiral, 2007; Knippen et al., 2019; Oliver, 1991) when deciding to link executive compensation to CSR criteria. Our analysis of diverse institutional settings with differing pressures (laws, support for intergovernmental organization initiatives) to implement CSR initiatives extends CSR contracting literature that has focused on single countries or given years (Flammer et al., 2019; Hong et al., 2016). Our findings thus contribute to comparative governance research (Aguilera & Jackson, 2010; Schiehll & Martins, 2016) by extending it to the increasingly important practice of CSR contracting.

Finally, we contribute to literature that investigates the interaction between external regulatory pressures and internal corporate governance mechanisms (e.g., Aguilera et al., 2015; Schiehll & Martins, 2016; Van Essen, Heugens, Otten, & Van Oosterhout, 2012). Specific corporate governance mechanisms alter the ways firms comply with regulatory pressures for sustainability. We also highlight the substantive, rather than symbolic, role of corporate governance in firms’ responses to CSR societal and regulatory expectations.

Our study has relevant practical implications too. First, it provides policy guidance for consulting with industry and government bodies to monitor executive compensation practices and develop effective best practices. Laws and public policies for sustainability should acknowledge that firms’ decision-making processes are unlikely to be uniform; rather, they stem from the interaction of country-level regulatory pressures and firms’ internal corporate governance mechanisms. Second, our study can help firms explain and justify to shareholders and stakeholders how the design of executive compensation, and specifically the integration of CSR criteria into executive compensation contracts, is determined.

Like any other study, our research is subject to limitations that should be considered when evaluating the findings and that offer opportunities for research. First, we investigate the determinants of CSR contracting adoption, because we are interested in analyzing whether firms, in line with the legitimization view of CSR (Bansal & Roth, 2000; Tashman et al., 2019), are affected by regulatory pressures when they decide how to incentivize executives. Further research could expand our study by focusing on the effectiveness of CSR contracting in unique institutional settings and/or on the mechanisms that influence a firm’s choice to stop using this practice once adopted for the first time. Second, our dependent categorical variable measures first-time adoption of a compensation policy linked to CSR targets, without specifying which CSR metrics are used and to what extent they affect the amounts paid. Thus, we cannot test whether the adoption of specific CSR targets (e.g., social targets) might be driven by specific forms of institutional pressure (e.g., social regulatory pressure). Depending on data availability at the international level, further research could investigate which metrics firms use, the relative weights they place on CSR contracting compared with financial performance targets, whether firms display preferences for focusing on people or on the planet, or how differences between firms might be explained by both country and firm-level effects. This would also allow another potentially interesting avenue for future research: the investigation of determinants of the use, rather than first-time adoption, of CSR contracting, which is probably stickier, and of changes in firms’ preferences for focusing on people or on the planet. Third, data limitations did not allow us to consider the extent to which governmental rules and policies aim to be coercive or more encouraging in protecting social and environmental targets in each country in a given year. Fourth, we focused on the formal independence of directors, which should enable directors to assess, monitor, or challenge executives, but we acknowledge that lack of social independence, for which data are not publicly available at the international level, might allow a CEO to affect his or her own compensation contract. If these data became available, researchers could examine the potential effect of a lack of social independence. Despite these caveats, this study represents a first, important step toward greater understanding of the underinvestigated global phenomenon of CSR contracting.

Footnotes

Acknowledgments

We appreciate the helpful comments from Luigi Rombi and two anonymous reviewers as well as the guidance and insights provided by Professor Pursey Heugens, the action editor. We gratefully acknowledge the financial support of Fondazione di Sardegna and of the University of Cagliari (UNICA) through its international Visiting Professor program sponsored by Regione Autonoma della Sardegna (RAS).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: this work was supported by the Regione Autonoma della Sardegna and the Fondazione di Sardegna.