Abstract

Extant research on CEO hubris has amassed substantial evidence on the positive association of this prominent managerial disposition and CEOs’ attraction to challenging and consequential strategic activities. Similarly, one may well anticipate more hubristic CEOs to strive for frequent transformations of their firms’ overarching trajectories as they overestimate their ability to reap the fruits of such challenging and highly consequential endeavors. In contrast to these arguments, however, higher levels of hubris might also lead CEOs to see little reason for scrutinizing and adapting extant paths in light of the magnificent prospects under their outstanding leadership. We explicate this theoretical obscurity surrounding the dispositional preference for change or steadiness associated with higher degrees of CEO hubris by carving out sets of competing hypotheses on the effect of CEO hubris on two key domains of change within the immediate purview of a CEO: strategic change and top management team (TMT) membership change. Empirically, we examine these arguments using a panel data set comprising 1, 197 S&P 1500 CEOs and find strong support for a negative effect of CEO hubris on a set of indicators of strategic change as well as on TMT membership change. Our results indicate that, beyond their attraction to manifold and challenging strategic activities, more hubristic CEOs exhibit a preference for steadiness that may prevail in the overall effect of hubris on certain organizational outcomes.

Few findings on CEOs’ firm-level impacts (Hambrick & Mason, 1984) are so pervasive as that CEOs featuring higher degrees of hubris, that is, those equipped with exaggerated self-confidence and a tendency to overestimate their abilities (hubris is hence sometimes referred to as overconfidence;1 Chen, Crossland, & Luo, 2015; Hill, Kern, & White, 2012; Li & Tang, 2010) cherish challenging and highly consequential endeavors (Hayward & Hambrick, 1997; Roll, 1986). Among others, they pursue ambitious acquisitions (Malmendier & Tate, 2008), venturous product innovations (Galasso & Simcoe, 2011; Hirshleifer, Low, & Teoh, 2012; Tang, Li, & Yang, 2015), and uncertain investment projects (Li & Tang, 2010; Malmendier & Tate, 2005). Those exemplary findings join the ranks of numerous studies and are attributable to a central proclivity of more hubristic CEOs: Excessive confidence in their own predictions and capabilities tempts them to chase even the most strenuous strategic activities. Yet, these insights from stand-alone strategic activities may not necessarily be effective in explicating the overarching directionality of these CEOs’ thrust. Much to the contrary, when it comes to higher-order transformations of their firms (e.g., in their corporate posture), theorizing on hubris may even suggest outcomes of opposite directions, corresponding to a dispositional preference either for change or for steadiness, i.e., constancy of conduct.

Specifically, CEOs’ inherent readiness and determination to pursue daring ideas and make highly consequential decisions are oftentimes considered key antecedents for abandoning established ways of doing business and changing organizational trajectories (Nadkarni & Herrmann, 2010; Wiersema & Bantel, 1992). In this vein, hubris has likewise come to be regarded as an incubator of change, e.g., leading CEOs to take “their firms in a new technological direction” (Galasso & Simcoe, 2011: 1469; Li & Tang, 2010). Yet beyond these suggestions and despite more hubristic CEOs’ attraction to challenging strategic activities, there is also reason to expect that CEO hubris induces steadiness, such that more hubristic CEOs chase challenging strategic activities simply for their inflated payoffs and without any intention to likewise bring about higher-order changes to their firms.

Specifically, higher degrees of hubris may lead CEOs to be overly confident not only regarding their ability to successfully navigate, for example, venturous product innovations (Tang, Li, et al., 2015) but also regarding their ability to master the firm's extant pathways. As such, they should see little merit in exhaustively deliberating alternative courses of action but instead exhibit a consistent directionality in the subjective absence of more superior paths to pursue. Thus, contrary to prior suggestions (Galasso & Simcoe, 2011; Li & Tang, 2010), there is also reason to expect more hubristic CEOs to prefer steadiness over change as they consider themselves capable and bound in mastering the established ways of doing business.

To address this obscurity, we adopt an upper echelons perspective (Hambrick & Mason, 1984; Hambrick, 2007) and theorize on how hubris would induce CEOs to cherish change or steadiness in their firms’ overarching trajectories. Specifically, we formulate sets of competing hypotheses on the effect of hubris on two key domains of change within the immediate purview of a CEO: strategic change and top management team (TMT) membership change. As such, we first resort to firms’ strategic change and, on the one hand, hypothesize that their overly positive self-assessment and their vigorous faith in the accuracy of their own judgment (Hayward & Hambrick, 1997) should lead more hubristic CEOs to overvalue the prospects of any alternative strategic direction they envision and of their abilities to lead such challenging transformations to success, rendering more hubristic CEOs particularly enticed into the pursuit of strategic change. Yet, on the other hand, we argue that even though more hubristic CEOs should be confident in their capabilities to lead strategic change to success, this does not necessarily imply that they are eager to stray from the overarching strategic path in the first place. Rather, these CEOs could be attracted to challenging strategic activities while adhering to the extant strategy itself.

We complement these divergent arguments on more hubristic CEOs’ aspiration for change or steadiness in the strategic domain by considering the effect of CEO hubris on TMT membership change, which demarcates transformations of CEOs’ immediate working environment and thus reflects more hubristic CEOs’ preference for social change or steadiness (Crossland, Zyung, Hiller, & Hambrick, 2014). Particularly, we argue that a preference for change respectively steadiness induced by higher degrees of hubris should generally lead such CEOs to either transform their TMT composition at their very convenience or to forgo the integration of novel perspectives into—and the dismissal of executives from—the TMT as they overestimate the merits of current organizational leadership instead. Moreover, because CEOs not only shape the degree of change to be pursued but also the frequency of such transformations (Ginsberg, 1988; Gordon, Stewart, Sweo, & Luker, 2000; Rajagopalan & Spreitzer, 1997), we conclude our theorizing by investigating the impact of CEO hubris on the fluctuation of strategic change and TMT membership change and posit that, regardless of how it shapes the respective degrees of change, more hubristic CEOs’ certainty as to the accuracy of their judgment should reduce the fluctuation of these degrees of change.

Analyzing a panel data set comprising 1,197 CEOs of S&P 1500 firms and employing a set of indicators of strategic change (changes in a firm's resource allocation, changes in business segments, and corporate restructuring) in conjunction with firms’ TMT membership change, we find comprehensive support for their negative associations with CEO hubris. In addition to these lower degrees of change, we also find support for our arguments that CEO hubris is associated with a lower fluctuation of change. In a post-hoc analysis, we assess the relevance and pervasiveness of more hubristic CEOs’ preference for steadiness more generally and demonstrate that it also carries over to a reduced fluctuation of firm performance.

We thus contribute to upper echelons theory (Hambrick & Mason, 1984) and research on strategic leadership and managerial biases (e.g., Finkelstein, Hambrick, & Cannella, 2009) by explicating more hubristic CEOs’ preference to change respectively not to change their firms’ overarching trajectories. In light of suggestions that higher levels of hubris should generally lead CEOs to strive for change (Galasso & Simcoe, 2011; Li & Tang, 2010), we highlight that a preference for steadiness qualifies as a viable tenet of executive hubris that manifests empirically in a negative association with strategic change and TMT membership change. Transcending these dimensions, our post-hoc analysis suggests that this preference for steadiness may also regulate the impact of CEO hubris on other organizational outcomes. As such, embracing more hubristic CEOs’ simultaneous preference for challenging strategic activities and for steadiness with regard to a firm's overarching trajectories might serve to capture the organizational ramifications of CEO hubris more comprehensively. Second, our findings contribute to the literature on the antecedents of strategic change and TMT membership change (e.g., Crossland et al., 2014; Finkelstein & Hambrick, 1990; Nadkarni & Herrmann, 2010). Prior research has gone to lengths to examine when and how chief executives overcome organizational inertia, path dependence, and “institutional imperatives” to change organizational trajectories (Chatterjee & Hambrick, 2007: 376; DiMaggio & Powell, 1983; Eggers & Kaplan, 2009; Hannan & Freeman, 1977; Helfat & Martin, 2014), and CEO hubris has generally been found to be pervasive in explaining firm outcomes. We contribute to this debate by highlighting that inertia may be self-imposed as more hubristic CEOs steadily eschew change. Third, we offer actionable advice to business practice by highlighting that it might be a false conclusion to expect more hubristic CEOs to generally strive for change. Rather, corporate boards should regard higher levels of CEO hubris as a proxy for a simultaneous attraction to challenging strategic activities and an inherent tendency for steadiness regarding firms’ overarching trajectories.

Theory and Hypotheses

Hubris and Upper Echelons

Having its origins in Greek mythology to describe the behavior of humans who foolishly challenged the gods, hubris nowadays refers to one's excessive self-confidence and the overestimation of one's abilities (Hayward & Hambrick, 1997; Roll, 1986). As such, this disposition manifests particularly in individuals’ decision-making processes: More hubristic individuals stand out due to an overly positive self-assessment that keeps them from recognizing their true boundaries (Hayward & Hambrick, 1997). They overestimate their own abilities relative to the average person (Camerer & Lovallo, 1999; Harrison & Shaffer, 1994), hold an inflated self-potency (Moore & Healy, 2008; Simon & Houghton, 2003), and demonstrate extreme confidence in their own predictions (Hilary & Menzly, 2006).

When manifested in senior executives, psychological dispositions, such as their level of hubris, will ultimately enter into their strategic choices within their organizations and thus be reflected in firm behavior and performance as executives perceive and interpret situational stimuli (Cyert & March, 1963; March & Simon, 1958). This perspective, as conceptualized in upper echelons theory (Hambrick & Mason, 1984; Hambrick, 2007), gave rise to substantial scholarly efforts explicating when and how CEOs’ dispositions impact organizational outcomes despite organizational inertia, path dependence, and “pressures to conform” (Crossland et al., 2014: 656; DiMaggio & Powell, 1983; Hannan & Freeman, 1977). Among the vast array of psychological dispositions to shape these ramifications, CEOs’ hubris has been found to be particularly pervasive in explaining strategic decision-making.

Respective studies find that more hubristic CEOs are drawn to uncertain investments (Goel & Thakor, 2008; Li & Tang, 2010; Malmendier & Tate, 2005) and pursue bold innovation projects (Galasso & Simcoe, 2011; Hirshleifer et al., 2012; Tang, Li, et al., 2015) and risky product introductions (Simon & Houghton, 2003). They are more likely to engage in acquisitions (Malmendier & Tate, 2008; Roll, 1986) and are willing to pay higher acquisition premiums (Hayward & Hambrick, 1997). Furthermore, CEOs featuring higher degrees of hubris were found to be associated with persistently overambitious management earnings forecasts (Chen et al., 2015; Hribar & Yang, 2016), heightened stock price crash risk (Kim, Wang, & Zhang, 2016), the underestimation of the importance of stakeholder support, and the subsequent engagement in socially irresponsible rather than responsible activities (Tang, Qian, et al., 2015; Tang, Mack, & Chen, 2018). Though shedding light on the effect of CEO hubris on various firm-level outcomes, the vast majority of studies thus shares the notion that excessive confidence in their own predictions and capabilities tempts more hubristic CEOs to chase challenging and highly consequential strategic activities.

More Hubristic CEOs’ Dispositional Preference for Change or Steadiness: A Tale of Two Stories

Yet, while the investigation of more hubristic CEOs’ impact on manifold strategic activities has substantially advanced our understanding of such CEOs’ fundamental inclinations and firm-level implications, it has led to a relative neglect of those inclinations and implications not necessarily observable in choices pertaining to stand-alone strategic activities. Picone, Dagnino, and Minà (2014: 448) even argue that, despite the comprehensive accumulation of organizational ramifications associated with CEO hubris, “prior research . . . has contributed to management debate in a pretty fragmented fashion” and thus runs the risk to “look at some trees and miss the whole forest” due to a respective focus on “a single (significant) manifestation of managerial hubris” along distinct strategic activities.

A central dilemma with regard to the generalization of prior findings is whether they imply more hubristic CEOs’ preference for change or steadiness. On the one hand, more hubristic CEOs’ pursuit of challenging strategic activities, such as acquisitions or new product introductions (Malmendier & Tate, 2008; Simon & Houghton, 2003), could be an expression of a more general desire to chase transformations. On the other hand, however, these activities could likewise constitute more hubristic CEOs’ means of pursuing extant goals, reflecting an attraction to challenging strategic activities without any intention to alter general trajectories. As such, the respective investigation of more hubristic CEOs’ impact on stand-alone strategic activities may not necessarily afford general inferences on these CEOs’ drive for changing firms’ overarching trajectories because such activities “are often substitutes for each other” (Chatterjee & Hambrick, 2011: 212) and would have to occur together with other, higher-order changes, for example in the firm's corporate posture, to do so (Albert, Kreutzer, & Lechner, 2015; Gioia & Chittipeddi, 1991).

To address this obscurity surrounding more hubristic CEOs’ preference for change or steadiness, we theorize on the effect of CEO hubris on two key domains of such higher-order change: strategic change and TMT membership change. As proposed by Crossland et al. (2014), both domains are among the central responsibilities of a CEO and thus enable a comprehensive understanding of the general preferences regulating the decisions of more hubristic CEOs—encompassing their firms’ strategic orientation as well as social changes in their immediate working environment.

Strategic Change

Arguably the most fundamental domain of change at a CEO's disposal concerns a firm's overarching strategic orientation (e.g., Rajagopalan & Spreitzer, 1997). Formally, a firm's strategy comprises “a set of interdependent choices regarding which activities to engage in and how to configure them” (Albert et al., 2015: 210; Gavetti & Rivkin, 2007; Porter & Siggelkow, 2008; Rivkin, 2000); that is, a firm's strategy is not represented by any single discrete economic process within a firm, such as an acquisition or a new product introduction, but by the system in which these interdependent and interactive strategic activities are configured and ultimately accumulate to a firm's productive output and value creation (Albert et al., 2015; Porter, 1985).

Firms differ largely in the extent of change in their strategic orientation, which has been the focus of keen scholarly interest referring to, for example, strategic change, dynamism, novelty, flexibility, renewal, or pivots (Agarwal & Helfat, 2009; Crossland et al., 2014; Meyer, 1982; Nadkarni & Herrmann, 2010; Wiersema & Bantel, 1992). Since prior literature has treated these concepts fairly synonymously (Crossland et al., 2014; Kirtley & O'Mahony, in press; Rajagopalan & Spreitzer, 1997), we adopt the term strategic change, generally defined as “a redefinition of organizational mission and purpose or a substantial shift in overall priorities and goals,” to describe firm behavior that alters the configuration of interdependent firm activities, structures, and outputs (Albert et al., 2015; Gioia, Thomas, Clark, & Chittipeddi, 1994: 364; Wiersema & Bantel, 1992).2

As such, strategic change is generally regarded a complex managerial endeavor, with ultimate ramifications highly contingent on both internal processes (e.g., Herrmann & Nadkarni, 2014; Zhang & Rajagopalan, 2010) and environmental influences (e.g., Kraatz & Zajac, 2001; Ndofor, Vanevenhoven, & Barker, 2013). In contrast to its ambiguity in repercussions, however, researchers assessing the antecedents of strategic change emphasize that the “primary responsibility for setting strategic directions and plans” lies with a CEO (Gioia & Chittipeddi, 1991: 433; Simons, 1994; Wiersema & Bantel, 1992). As such, the psychological dispositions integral to CEOs’ decision-making generally play a key role in the consideration of whether and to what extent a firm's overarching strategic direction will be changed (Hambrick & Mason, 1984; Herrmann & Nadkarni, 2014). In the case of more hubristic CEOs, this means that considerations as to the strategic configuration of their firm will be highly reflective of how these CEOs envision applying their (subjectively) superior skills and knowledge. However, competing predictions on the directionality of the impact of CEO hubris on strategic change ensue depending on whether or not more hubristic CEOs are willing and able to scrutinize their extant conduct and hence feature a preference for change or steadiness.

CEO Hubris and Strategic Change

On the one hand, there are compelling arguments why CEO hubris should be positively associated with strategic change. First, as Wiersema and Bantel (1992) illustrate, overcoming organizational inertia and engaging in strategic change requires the readiness to abandon established ways of doing business in order to pursue new strategic directions whose definite outcomes remain inherently unclear (Nadkarni & Herrmann, 2010; Shimizu & Hitt, 2004). Correspondingly, more hubristic CEOs feature an overly positive self-assessment (Hayward & Hambrick, 1997), disregard objective uncertainty in light of their subjectively superior judgment (Li & Tang, 2010), and thus regularly underestimate the challenges and pitfalls associated with their decisions (Camerer & Lovallo, 1999). That is, they envision their superior capabilities to allow them to successfully navigate (and exploit the opportunities of) even the most demanding endeavors and to control the respective processes and outcomes (Li & Tang, 2010; Malmendier & Tate, 2008). Thus, just as more hubristic CEOs come to overestimate resource endowments and demonstrate excessive confidence in the pursuit of venturous strategic activities (Tang, Li, et al., 2015; Tang, Qian, et al., 2015), they should overvalue the ambiguous prospects of the challenging, resource-intensive, and highly consequential changes to a firm's overarching strategy they conceive and thus be particularly enticed into the pursuit of strategic change.

Second, the initiation of strategic change requires a steadfast determination regarding the newly defined course of action in order to overcome any counterforces and doubts, particularly during its early instigation (Gioia & Chittipeddi, 1991; Gray & Ariss, 1985; Weiser, 2021). In this regard, their vigorous faith in the efficacy of their conduct and in the accuracy of their own judgment (Hilary & Menzly, 2006) typically induce more hubristic CEOs to not lose time in strategic analyses or consultations (Picone et al., 2014). Instead of extensively collecting additional information or evaluating alternative standpoints, more hubristic CEOs tend to overestimate the grandeur of their personal beliefs (in absolute terms and relative to others; Chen et al., 2015; Li & Tang, 2010), bringing about more centralized and fast-paced—or even impulsive—strategic decision-making (as well as “shallow strategic analyses”) aimed at immediately leveraging their (subjectively) outstanding intuition (Picone et al., 2014: 455; Wally & Baum, 1994). In other words, once these CEOs intuit a strategic decision, they will be rigorously convinced of its soundness, which is, for example, regularly observed in more hubristic CEOs’ tendency to pay overly high premiums once they designate an acquisition target (Hayward & Hambrick, 1997). One should thus expect more hubristic CEOs to also be predisposed to overcome (or ignore) any challenges to a novel strategic path they wish to tread, further facilitating their pursuit of strategic change.3

Similar to the preceding lines of thought, prior work has documented a dispositional drive to pursue strategic change among more narcissistic CEOs (Chatterjee & Hambrick, 2007). Narcissism induces an excessively positive self-image that, in contrast to hubris, requires continuous and external reinforcement (Campbell, Goodie, & Foster, 2004). Yet, although “hubris [thus] lacks key elements of the narcissistic personality” (Chatterjee & Hambrick, 2007: 357), both constructs reside upon one's overly positive self-assessment (Tang et al., 2018), which has led some authors to suggest that, just as it does for more narcissistic CEOs, this inclination should also lead more hubristic CEOs to strive for strategic change (e.g., Li & Tang, 2010). From this perspective, more hubristic CEOs’ strategic activities, such as acquisitions or product introductions, may thus be considered interdependent reflections of a general readiness and determination to pursue changes regarding their firms’ overarching strategic orientation. For example, upon finding that firms headed by more hubristic CEOs tend to have higher citation-weighted patent counts, Galasso and Simcoe (2011: 1469) suggest that these CEOs “are more likely to take their firms in a new technological direction,” which is regularly regarded an indicator of comprehensive strategic change (Agarwal & Helfat, 2009; Eggers & Kaplan, 2009). Correspondingly, one may anticipate more hubristic CEOs to exhibit a distinct preference for orchestrating higher degrees of strategic change and conversely attribute inertia to their less hubristic counterparts. We therefore posit: Hypothesis 1a: CEO hubris is positively associated with strategic change.

On the other hand, despite more hubristic CEOs’ inclination to engage in manifold and consequential strategic activities, these activities may be orchestrated in ways that do not necessarily alter a firm's overarching strategic path. Indeed, there is reason to expect higher levels of hubris to unfold in steadiness, i.e., constancy of conduct, as such CEOs assess their firms’ strategic orientation: Just as individual attributes—such as self-ascribed competence, self-efficacy, or self-confidence, all of which are elevated among more hubristic individuals—are usually associated with goal adherence rather than flexibility (e.g., Tenenbaum et al., 2005; Wood & Bandura, 1989), more hubristic CEOs may simply be too convinced of their genuine grandiosity for more superior courses of action to appear conceivable. Thus, in light of their self-ascribed grandness and vigorous faith in their ability to reach any set goals, a preference for steadiness may regulate more hubristic CEOs’ behavior and evoke a negative association between CEO hubris and strategic change despite their attraction to challenging strategic activities.

First, strategic change not only hinges on a CEO's confidence to successfully navigate new ways of doing business, but it also requires the proactive search and scanning for potentially superior strategies to pursue in the first place (Hambrick & Mason, 1984; Miller, 1994; Nadkarni & Herrmann, 2010). Yet, more hubristic CEOs are convinced not just of the success of their strategic activities but of the virtue of their entire conduct, which includes their ability to perfectly execute the firm's overarching strategy, i.e., their sanguine conviction in the long-term prospects of the company's current path under their leadership (Hayward & Hambrick, 1997). This inclination to overestimate future organizational conditions in light of their own outstanding managerial abilities is, for example, regularly reflected in more hubristic CEOs’ tendency to issue overly ambitious earnings forecasts (Hribar & Yang, 2016). Correspondingly, their overly positive self-assessment should make it unlikely for even more fruitful paths to appear conceivable, thus limiting the attention CEOs higher in hubris direct to proactive search and scanning for strategic alternatives.

Second, the initiation of strategic change depends, to a considerable degree, on information, interpretations, and ideas brought to the CEO's attention by employees or other managers of the firm (Herrmann & Nadkarni, 2014; Nadkarni & Herrmann, 2010). As noted earlier, however, more hubristic CEOs feature a pronounced self-importance that leads them to centralize decision-making processes to maintain ultimate authority over organizational decisions (Hayward & Hambrick, 1997; Miller & Dröge, 1986). Prior research documents that such “delusions of grandeur” and the corresponding centralization of authority impede creativity and thus restrict the flow of ideas and information within organizations (Hayward & Hambrick, 1997: 108; Miller, 1987). As a result, this lack of exchange and creativity permeating to more hubristic CEOs should further reduce their exposure to potential strategic alternatives.

Yet, even if such initiatives do permeate, there is reason to cast doubt on more hubristic CEOs’ receptivity. These CEOs overestimate their abilities relative to the average person and discount the capabilities and judgments of others relative to their own (Tang, Qian, et al., 2015). This self-conception is, for example, observable in more hubristic CEOs’ disproportionate tendency to pursue acquisitions as they overvalue their capabilities to leverage resulting synergies—despite unambiguous evidence refuting the effectiveness of acquisitions as a means to increase the acquirer's shareholder wealth (Malmendier & Tate, 2008; Roll, 1986). Hence, the very same complacency that may lead more hubristic CEOs to refrain from acknowledging valid opposition if they were to intuit merit in strategic change (Hypothesis 1a) should generally render such CEOs unreceptive to the potential upsides of others’ initiatives and thus reinforce their perceived merit in the extant strategic direction under their leadership.

In sum, initiating strategic change requires CEOs not only to take a challenge but also to actively investigate alternative courses of action in the first place and challenge extant beliefs and predictions on a regular basis (Nadkarni & Herrmann, 2010; Shimizu & Hitt, 2004). As such, it requires not only a reorganization of interdependent organizational activities and outputs but also a major “cognitive reorientation” as CEOs’ mental models, including their cause-effect logics and the conceived roles and competencies within the company, will inevitably need to be challenged and adapted to accommodate the considerable implications of prospective strategic change (Barr, Stimpert, & Huff, 1992; Floyd & Lane, 2000; Gioia et al., 1994: 363). Even before manifesting in definite changes of their firms’ strategic orientation, this means that CEOs must (be able to) acknowledge that an adaption of the way they currently make sense of organizational reality, i.e., a “fundamental alteration in [their] social construction of reality,” is necessary (Barr et al., 1992; Gioia et al., 1994: 363; Nadkarni & Herrmann, 2010).

Therefore, it is typically those CEO characteristics that elevate critical self-reflection and receptivity toward a broad range of stimuli that have been shown to encourage firm-level strategic change (e.g., Barr et al., 1992; Cho & Hambrick, 2006; Herrmann & Nadkarni, 2014; Nadkarni & Herrmann, 2010). More hubristic CEOs, however, are so deeply convinced of already possessing the very best abilities and organizational understanding to achieve success from the current strategic orientation that more superior courses of action may hardly appear conceivable. Accordingly, they rarely engage in critical self-reflection (Chen et al., 2015) and exhibit little flexibility in their extant, subjectively irreproachable conception of organizational reality, which inherently jeopardizes the potential for substantive cognitive and, subsequently, strategic change (Barr et al., 1992; Lant, Milliken, & Batra, 1992; Nadkarni & Barr, 2008).

This ultimately distinguishes the decision to engage in strategic change from decisions in the pursuit of a firm's strategy: As stand-alone strategic activities are of temporary nature and will ultimately be completed, CEOs do not need to alter their self-perception or admit prior errors in judgment when subsequently initiating other activities. To initiate comprehensive strategic change, however, more hubristic CEOs would need to embrace flux and be receptive to alternative strategic scenarios—which requires the willingness to question and adapt one's current conception of organizational reality (Barr et al., 1992; Gioia & Chittipeddi, 1991; Nadkarni & Herrmann, 2010). This may not be expected of more hubristic CEOs. To reinforce their grandiosity, they may rather actively avoid searching and scanning for strategic alternatives and passively impede the flow of ideas across the organization. In light of such a limited field of vision (Hambrick & Mason, 1984) and their keen complacency, one may thus anticipate higher levels of CEOs’ hubris to manifest in steadiness as these CEOs pursue the organization's extant strategy. Therefore, despite their attraction to manifold and consequential strategic activities, we posit: Hypothesis 1b: CEO hubris is negatively associated with strategic change.

TMT Membership Change

Beyond firms’ overarching strategic orientation, a dispositional preference for change or steadiness of more hubristic CEOs should likewise regulate their pursuit of changes in their firms’ TMT composition (Crossland et al., 2014). Comprised of CEOs’ closest executive peers, each of whom they engage with regularly and intensively (Hambrick, 2007), the TMT is the “dominant coalition at the apex of an organization charged with decision-making responsibility” (Crossland et al., 2014: 658; Cyert & March,1963) and, as Finkelstein (1992: 509) points out, “CEOs have high structural power over other members of [the TMT].” As such, CEOs are tasked with both “the selection and retention of TMT members” (Crossland et al., 2014: 658), that is, with the enforcement of changes in TMT membership, whenever they seem appropriate (Michel & Hambrick, 1992; Wiersema & Bantel, 1993).

Firms differ widely in the degree of TMT membership change (Wiersema & Bantel, 1993) and, although studies on respective antecedents are relatively scarce, this variance oftentimes exceeds instrumental reasons and is, instead, attributed to CEOs’ dispositional preferences (Crossland et al., 2014; Herrmann & Nadkarni, 2014). Correspondingly, we expect CEOs’ hubris to play a key role in the considerations to change or not to change their firms’ TMT compositions, such that the distinct assessment of the effect of CEO hubris on TMT membership change will complement our theorizing on the effect of CEO hubris on strategic change by affording a more comprehensive perspective on more hubristic CEOs’ dispositional preference for change or steadiness—not only in the strategic domain but also with regard to the social change in their immediate working environment. However, once more, competing predictions on the directionality of the impact of CEO hubris ensue depending on whether or not higher levels of hubris render CEOs willing to scrutinize their TMT's conduct.

CEO Hubris and TMT Membership Change

On the one hand, there are compelling reasons why more hubristic CEOs should exhibit a distinct preference for change in their immediate working environment and thus be enticed into the pursuit of TMT membership change. TMT replacements bear the potential of letting go of top managers the CEO deems ineffective or adding executives the CEO deems particularly suitable, yet constitute challenging interferences in organizational trajectories because both additions and departures of TMT members are typically associated with unclear organizational consequences (Cannella & Hambrick, 1993; Kesner & Dalton, 1994; Wiersema & Bantel, 1993; Williams, Chen, & Agarwal, 2017). Just as the departures of extant top managers will elicit losses in unique influence and knowledge that vanish from the CEO's disposal (Kotter, 1982; Wiersema & Bantel, 1993), the additions of new TMT members are intricate undertakings because the fit between their actual abilities and the requirements of their assignment remain inherently unclear even if their general credentials may be well reputed in advance. This is because “executives possess a panoply of potentially relevant attributes” for the manifold tasks at hand, only a subset of which hiring CEOs can effectively apprehend in advance, such that the installations of new TMT members will naturally be based on incomplete assessments of their true aptitude (cf., Khurana, 2002; Quigley, Hambrick, Misangyi, & Rizzi, 2019: 1455).

This should not deter more hubristic CEOs from TMT membership change, however. In light of their heightened belief in the superiority of their own judgment (Li & Tang, 2010), they should rather be inclined to disregard the imponderables of any top manager they personally designate as suitable, just as their overly positive self-assessment (Hayward & Hambrick, 1997) should lead them to overestimate their abilities to integrate (and leverage the virtues of) their desired TMT candidates. Moreover, since more hubristic CEOs are deeply convinced of their abilities to lead their decisions to success and to compensate any potential casualties (Li & Tang, 2010; Malmendier & Tate, 2008), they should also be inclined to disregard the losses in (explicit and tacit) knowledge as well as the (consequences of) the potential vacuum of tasks and responsibilities emerging as TMT members are let go (cf., Cannella & Hambrick, 1993; Kesner & Dalton, 1994). For these reasons, one may anticipate more hubristic CEOs to overvalue the ambiguous prospects of the challenging and highly consequential changes to the TMT they envision and thus to exhibit a dispositional preference for change in their immediate working environment. As such, more hubristic CEOs may seek to rigorously transform the TMT at their very convenience whereas more stable TMT compositions may, conversely, be attributed to their less hubristic counterparts. We thus posit: Hypothesis 2a: CEO hubris is positively associated with TMT membership change.

On the other hand, despite more hubristic CEOs’ dispositional confidence to easily orchestrate TMT membership change, they may not deem such changes necessary in the first place. Specifically, one key driver of the pursuit of TMT membership change is typically the willingness to dismiss top managers whose knowledge and abilities do not match CEOs’ conceptions anymore (Michel & Hambrick, 1992; Wiersema & Bantel, 1993). Yet to the degree that they tend to discount the general abilities of others (Chen et al., 2015), more hubristic CEOs should consider emergent misfits of extant TMT members with current organizational demands rather negligible as long as they themselves contribute their superior strategizing to the firm.

Moreover, TMT membership change also depends, to a considerable degree, on the additions of novel TMT members contributing “a wider range of experiences and viewpoints” to organizational leadership (Barker, Patterson, & Mueller, 2001; Crossland et al., 2014: 658; Williams et al., 2017). As noted earlier, however, more hubristic CEOs rarely perceive the locus of strategy making in anyone but themselves, discounting the contributions of others relative to their own (Picone et al., 2014). Hence, just as they may be unwilling or, respectively, unable to adapt their mental models when it comes to the consideration of, for example, transformations of their firm's corporate posture, they should see little merit in any consideration, discourse, and thus importation of additional ideas into the TMT. Much to the contrary, their subjective superiority should rather render more hubristic CEOs convinced that their outstanding leadership enables the extant TMT to thrive extraordinarily, such that the potential value added via the inclusions of novel top managers should hardly justify their tedious search, selection, and integration into well-attuned structures. Taking both arguments together, one may thus anticipate more hubristic CEOs to exhibit a distinct preference for steadiness in their immediate working environment and hence to abstain from TMT membership change. Therefore, we posit: Hypothesis 2b: CEO hubris is negatively associated with TMT membership change.

CEO Hubris and the Fluctuation of Change

CEOs can affect not only the degree of strategic change or TMT membership change (i.e., high vs. low levels of change) but also the fluctuation of change (i.e., continuous vs. erratic change). Specifically, some CEOs favor more continuous transformations with little year-on-year fluctuation of the general degrees of change, whereas others prefer periods of distinct reorientation, reflected in a higher year-on-year fluctuation (Gordon et al., 2000; Rajagopalan & Spreitzer, 1997). While our previous deliberations focused solely on more hubristic CEOs’ preferences for higher or lower levels of change, we hence proceed by explicating how these levels of change will vary over time.

In business reality, one can regularly observe a preference for more erratic over continuous change, since such an approach confines the concomitant strains to (and tensions between) organizational stakeholders during the delimited periods in which transitions are executed (Bentley & Kehoe, 2020; Kraatz & Zajac, 2001). Yet there is reason to expect more hubristic CEOs’ preference for change respectively steadiness to regulate their conduct consistently. Indeed, to more hubristic CEOs, “indulging” adversely affected stakeholders by confining strains should appear rather unreasonable. In light of their subjectively superior management skills, they would rather overestimate their competencies for orchestrating continuous change and overvalue their general endowment of stakeholder support (Tang, Qian, et al., 2015). Correspondingly, if more hubristic CEOs do engage in higher levels of change (Hypotheses 1a and 2a), they should not sway from the challenges associated with continuously leveraging their strategic and social intuitions. Vice versa, if their subjective superiority tempts more hubristic CEOs to refrain from such change (Hypotheses 1b and 2b), they should be convinced that any transition remains unnecessary as their current strategy or TMT composition will continue to pay off. In other words, more hubristic CEOs will be convinced either that it is continuous change that will ensure constant success under their superior steerage or that change will remain largely unnecessary given their outstanding abilities to master the firm's extant conduct. In either case, higher levels of CEO hubris should manifest in lower year-on-year changes rather than in regular fluctuations or “spikes” of change, such that, regardless of whether such CEOs engage in higher (Hypotheses 1a and 2a) or lower (Hypotheses 1b and 2b) degrees of change, one may anticipate steadiness in their fluctuation of change, as more hubristic CEOs constantly refrain from or engage in it. We thus posit: Hypothesis 3a: CEO hubris is negatively associated with the fluctuation of strategic change.

Hypothesis 3b: CEO hubris is negatively associated with the fluctuation of TMT membership change.

Method

Sample Selection

Our initial sample consists of all nonfinancial S&P 1500 firms (i.e., excluding Standard Industrial Classification industries 6000–6999) and covers the years 1996 to 2016. To test our hypotheses, we observe leadership transitions in the ExecuComp database and build a panel data set comprising annual data on all CEOs who assumed office between 1996 and 2014, excluding interim and co-CEOs.4 We obtain firm-level financial data from COMPUSTAT and action data from Capital IQ Key Developments, firm-segment data from COMPUSTAT Historical Segments, executive data from ExecuComp, ownership data from Thomson-Reuters 13(F), governance data from Institutional Shareholder Services (ISS), acquisition data from Securities Data Company (SDC), stock data from Center for Research in Security Prices (CRSP), and CEOs’ personal political contributions from the Federal Election Commission. Our final sample consists of 1,197 unique CEO–firm combinations contributing 6,945 observations. As described later, one of our dependent variables, corporate restructuring, carried missing data, leading to fewer observations in respective analyses. We provide extensive technical details on all variables in Online Appendix A.

Dependent Variables: Strategic Change

As an encompassing test of our hypotheses, we leverage three well-established indicators of strategic change, namely, a firm's (1) change in resource diversification, (2) business segment change, and (3) corporate restructuring (e.g., Crossland et al., 2014; Karim, 2006; Zajac & Kraatz, 1993). We examine the effect of CEO hubris on each of these widely used indicators of strategic change and explicate their operationalizations next.

Change in resource diversification. First, firms engaging in strategic change can be expected to display a higher annual variance in their relative resource allocation to and size of business units (Crossland et al., 2014; Harrison, Hall, & Nargundkar, 1993; Noda & Bower, 1996). If more hubristic CEOs engage in higher levels of strategic change (Hypothesis 1a), this should be reflected in regular transformations of their firms’ strategic posture, whereas if more hubristic CEOs engage in lower levels of strategic change (Hypothesis 1b), the challenging strategic activities they pursue should be arranged in ways that do not substantially alter the firm's overall portfolio but reflect their steady predictions regarding the relative importance of and corresponding resource allocation to business units.

Following prior work (e.g., Boeker, 1997; Crossland et al., 2014; Wiersema & Bantel, 1993), we operationalize changes in a firm's resource diversification as the (log-transformed) absolute year-on-year change in Jacquemin and Berry’s (1979) entropy measure of diversification:

Business segment change. Second, strategic change may also unfold as a comprehensive alteration of the products or services a company provides (Agarwal & Helfat, 2009; Albert et al., 2015). More hubristic CEOs are prone to push for innovations (Galasso & Simcoe, 2011; Hirshleifer et al., 2012; Tang, Li, et al., 2015) and, particularly, to engage in the development of new and risky products (Simon & Houghton, 2003). If these findings are reflective of general efforts toward strategic change (Hypothesis 1a), one would expect such activities to accumulate to revisions in a firm's business segments, reflecting the higher-order categories of goods and services a company provides (e.g., Karim, 2009). Yet, even though more hubristic CEOs are prone to develop and introduce new products or services (Simon & Houghton, 2003), their grandiosity beliefs may lead them toward nesting these additions into established business segments to avoid far-reaching alterations of their firms’ general operating structure (Hypothesis 1b). Mirroring the construction of our variable TMT membership change described later, we calculate business segment change as the annual additions and deletions in a firm's business segments divided by the number of segments in the previous year (see above cf., Crossland et al., 2014; Herrmann & Nadkarni, 2014; Karim, 2006).

Corporate restructuring. Third, corporate restructuring, including reorganizations and downsizings as well as spin-offs and divestitures (Shi, Connelly, Hoskisson, & Ketchen, 2020), lies at the heart of strategic change (Hoskisson & Johnson, 1992; Johnson, Hoskisson, & Hitt, 1993; Zajac & Kraatz, 1993) but requires the CEO's foresight (admittance) that previous configurations of company structures are insufficient to meet future (current) business demands (Floyd & Lane, 2000; Girod & Whittington, 2017; Pettit & Crossan, 2020). As such, more hubristic CEOs might consider significant corporate restructuring either a convenient and straightforward tool to reinforce organizational effectiveness and efficiency (Hypothesis 1a) or as largely unnecessary in light of their superior ability to successfully manage even convoluted corporate structures (Hypothesis 1b).

We follow Shi et al. (2020) and operationalize corporate restructuring based on the Capital IQ Key Developments database as the annual sum of announcements regarding business reorganizations, discontinued operations/downsizing, spin-offs/split-offs, and selling or divesting a business unit (Chen, Meyer-Doyle, & Shi, 2021). Even though the Capital IQ Key Developments database carries observations since 1964, considerable coverage of our sample firms begins with fiscal year 2000. Correspondingly, we perform respective analyses on the restricted sample of 967 CEOs (5,363 observations) who assumed office since then.

Dependent Variable: TMT Membership Change

We follow Crossland et al. (2014: 662) and operationalize TMT membership change as the sum of the annual “additions and deletions to the TMT . . . divided by the number of members in the previous year” to reflect the degree of change or steadiness within a firm's TMT composition (e.g., Cho & Shen, 2007; Keck & Tushman, 1993; Quigley & Hambrick, 2012).

Dependent Variables: Fluctuation of Strategic Change and TMT Membership Change

Following Chatterjee and Hambrick (2007), we use the absolute year-on-year difference in our indicators of strategic change and TMT membership change to depict their fluctuation.

Independent Variable: CEO Hubris

As a complex psychological construct, CEO hubris is generally difficult to assess directly since CEOs “are quite reluctant to participate in psychological batteries, at least in the numbers needed for an ongoing research program” (Hambrick & Mason, 1984: 196). Though noisier than direct psychological assessments, upper echelons research thus typically draws on unobtrusive proxies to capture “physical traces” of CEOs’ inherent dispositions (e.g., Chatterjee & Hambrick, 2007; Webb, Campbell, Schwartz, & Sechrest, 1966: 35). Prior literature has focused on an array of such physical traces as unobtrusive proxies of CEO hubris (e.g., Campbell, Gallmeyer, Johnson, Rutherford, & Stanley, 2011; Chen et al., 2015; Hayward & Hambrick, 1997; Malmendier & Tate, 2005; 2008; Tang, Qian, et al., 2015), and most importantly, this work is mixed in the application of option versus press-based measures (e.g., Ho, Huang, Lin, & Yen, 2016; Malmendier & Tate, 2008; Tang et al., 2018). Since press-based proxies are designed to “measure outsiders’ perceptions” of hubris and thus include potential impression management (e.g., Hill, Kern, & White, 2014; Malmendier & Tate, 2008: 42) frequently observed in the context of substantial changes in corporations (e.g., Whittington, Yakis-Douglas, & Ahn, 2016), we opt for the application of an option-based measure because our theory centers around hubris as an inherent disposition and, unlike merely voicing self-confidence and having it portrayed in the press, CEOs’ option-exercising behavior has direct and immediate implications for their personal wealth (Campbell et al., 2011; Hall & Murphy, 2002).

Their option-exercising behavior thus better suits our goal to quantify CEOs’ intrinsic level of hubris and has been frequently used and extensively validated in the literature (e.g., Campbell et al., 2011; Chen et al., 2015; Hirshleifer et al., 2012; Hribar & Yang, 2016; Malmendier & Tate, 2005; Pavićević & Keil, 2021). The underlying rationale is that the unwillingness to exercise exercisable in-the-money executive stock options is reflective of CEOs’ hubris, as more hubristic CEOs display higher confidence in their (subjectively) superior management skills and higher certainty in beneficial future market valuations of their firm (Malmendier & Tate, 2005). Less hubristic CEOs, however, would be more inclined to exercise those options timely in order to diversify their personal portfolios and reduce the exposure of their personal wealth to the performance of their firm (Hall & Murphy, 2002; Malmendier & Tate, 2005, 2008). As such, our measure of CEO hubris captures exactly the overestimation of firm prospects we invoke in our theorizing, corresponding to the call of Malmendier (2018: 349) to employ “a credible empirical measure that is not just ‘any’ proxy for the bias in question, but one that aims for situational similarities.”

Whereas earlier assessments of CEO hubris rely on a dichotomous operationalization based on the methodology of Campbell et al. (2011), observing whether or not a CEO repeatedly held onto exercisable executive stock options with a moneyness of more than 100% (e.g., Chen et al., 2015; Kim et al., 2016), we adopt a refinement of this operationalization in order to quantify a CEO's distinct level of hubris. This refinement overcomes the dichotomization of hubris in favor of a continuous and therefore more realistic (e.g., Oskamp, 1965) quantification by incrementing the degree of moneyness for which Campbell et al.'s (2011) assessment would classify a CEO as “hubristic.” The maximum threshold for which a CEO would yet be dichotomously identified as “hubristic” (i.e., the maximum moneyness for which a CEO repeatedly did not exercise in-the-money executive stock options) is then used as an indicator of a CEO's level of hubris:

To ease the interpretability of our coefficients, we standardize our CEO hubris variable. Also, in light of extant concerns regarding the use of option-based measures of CEO hubris (e.g., Hill et al., 2014; Jin & Kothari, 2008), we conducted several robustness checks on the suitability of our measure as a proxy for CEO hubris in our study and assess the validity of our results with regard to potential alternative explanations and using alternative measures of CEO hubris (please refer to our Robustness Checks section and Online Appendix B.2 for corresponding details).

Control Variables

In our analyses, we include a comprehensive set of controls at the CEO level, firm level, and industry level. First, we control for inherent firm tendencies by including the pre-entry condition of the respective indicator of strategic change or TMT membership change (each measured in the year prior to the beginning of a CEO's tenure; Chatterjee & Hambrick, 2007). At the firm level, we also include firm size (log of sales), due to its effect on firm resource availability (Boeker, 1997), and log-transformed firm age (based on web searches), to control for liabilities of newness, adolescence, and aging (Freeman, Carroll, & Hannan, 1983). We control for firm performance (industry-adjusted return on assets [ROA]) as a major antecedent of CEO behavior (Kish-Gephart & Campbell, 2015; Zhang & Rajagopalan, 2010) and include the degree of diversification (the entropy index), property ratio (property, plant, and equipment to employees), and leverage ratio (long-term debt divided by total assets) as boundary conditions for organizational capabilities (Shi et al., 2020). Finally, to control for a firm's governance conditions, we include board independence (independent directors divided by board size), remuneration committee insiders (number of executives listed in the compensation committee; Singh & Harianto, 1989), Delaware incorporation (coded 1 for firms incorporated in Delaware; Bebchuk, Cohen, & Ferrell, 2009), and institutional blockholding (percentage of shares owned by the largest institutional blockowner; Crossland et al., 2014).

At the CEO level, we use CEO age, CEO tenure, and CEO industry experience to control for confounding influences from CEOs’ experiences (e.g., Boeker, 1997; McClelland, Barker, & Oh, 2012). To control for a CEO's power to pursue change, we include an indicator variable, CEO duality, taking a value of 1 if the CEO also served as board chair in a respective year (Finkelstein, 1992), and the percentage of CEO ownership (relative to a firm's total shares outstanding). We also control for a CEO's incentive compensation, calculated as long-term incentive payouts, the Black-Scholes value of stock option grants, and the total value of stock option grants divided by total compensation (Harrison, Thurgood, Boivie, & Pfarrer, 2020), and include CEO conservatism, based on a CEO's personal political contributions to the Republican versus the Democratic party (Christensen, Dhaliwal, Boivie, & Graffin, 2015), to capture value-based preferences toward change (Jost, 2017). At the industry level, we follow prior research and control for market complexity, market competitiveness, and market munificence (e.g., Kish-Gephart & Campbell, 2015). We also include year and industry dummy variables and use a 1-year lag between our dependent variables (measured in year t + 1) and respective predictors (measured in year t).

Empirical Strategy

To test our hypotheses, we employ generalized estimating equations (GEE), which yield particularly appropriate maximum likelihood estimates in panel regressions with temporally stable independent variables (Liang & Zeger, 1986), as is the case for CEO hubris. Due to the enumerative nature of our corporate restructuring variable, we specify a negative binomial distribution of this dependent variable and a log link function in corresponding analyses (Chatterjee & Hambrick, 2007). In all other cases, we specify a Gaussian distribution and an identity link function. All regressions feature a covariance structure accounting for autocorrelation and robust standard errors (Huber, 1967; White, 1980).5

Data Analysis

Results

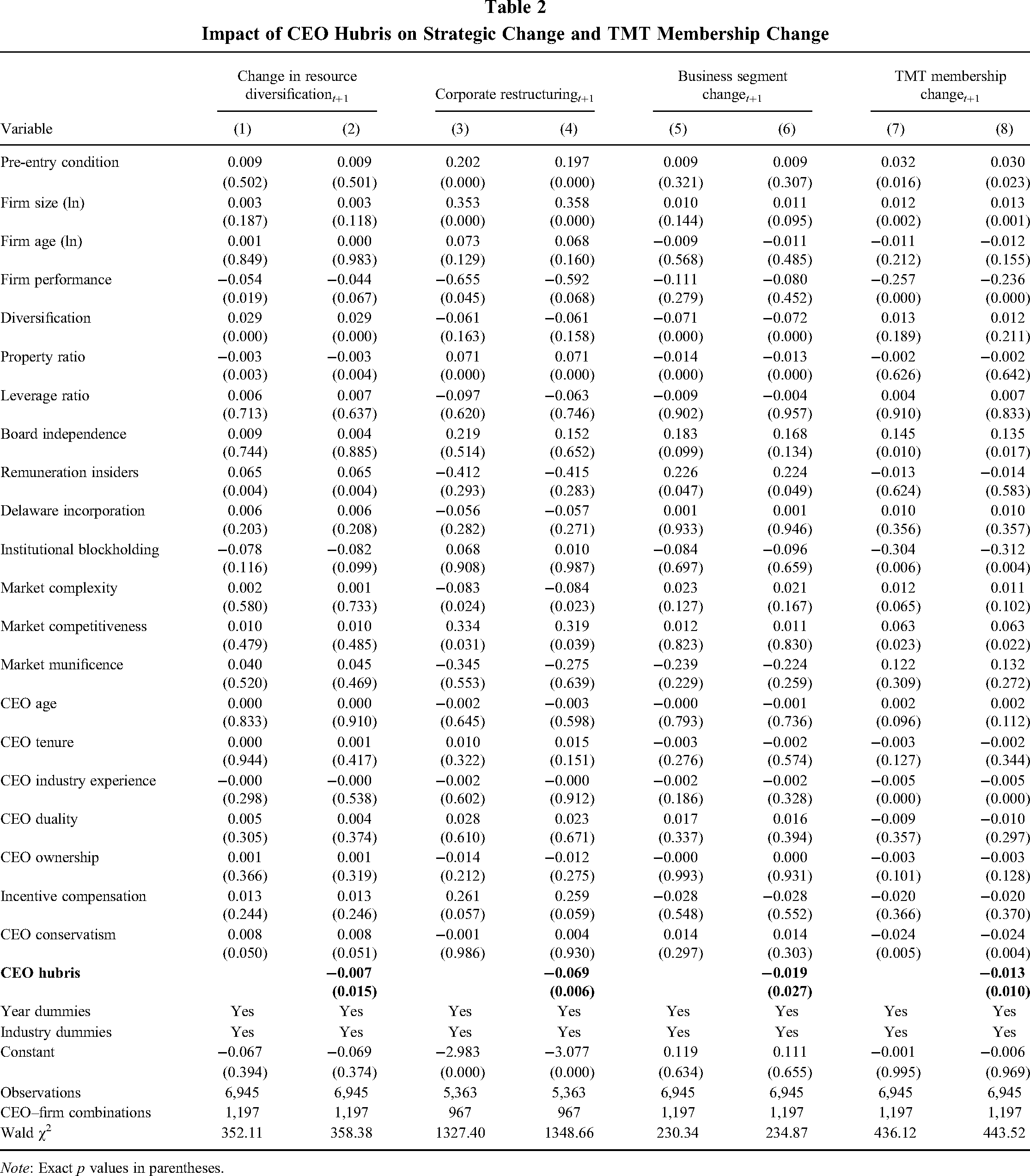

In Table 1, we report descriptive statistics and pairwise correlations. Table 2 reports the results of our regression analyses of the indicators of strategic change and of TMT membership change. Hypothesis 1a predicted that CEO hubris is positively related to strategic change, whereas Hypothesis 1b predicted the opposite, namely, that CEO hubris is negatively related to strategic change. The negative and significant coefficients on CEO hubris in Models 2, 4, and 6 of Table 2 provide support for Hypothesis 1b with regard to changes in a firm's resource diversification6 (Model 2, β = –0.007, p = .015), corporate restructuring (Model 4, β = –0.069, p = .006), and business segment changes (Model 6, β = –0.019, p = .027) as dependent variables. In practical terms, compared to a CEO with a hubris score one standard deviation above the mean, a CEO with a hubris score one standard deviation below the mean will, for example, be associated with an approximate increase of 23% in business segment changes. In Hypotheses 2a and 2b, we theorized on the directionality of the effect of CEO hubris on TMT membership change. In support of the negative association put forth in Hypothesis 2b, Model 8 of Table 2 shows that CEO hubris is negatively and significantly associated with TMT membership change (β = –0.013, p = .010).7 This means that, each year, the TMT membership change of a CEO with a hubris score one standard deviation below the mean will be approximately 8% higher compared with a CEO with a hubris score one standard deviation above the mean.

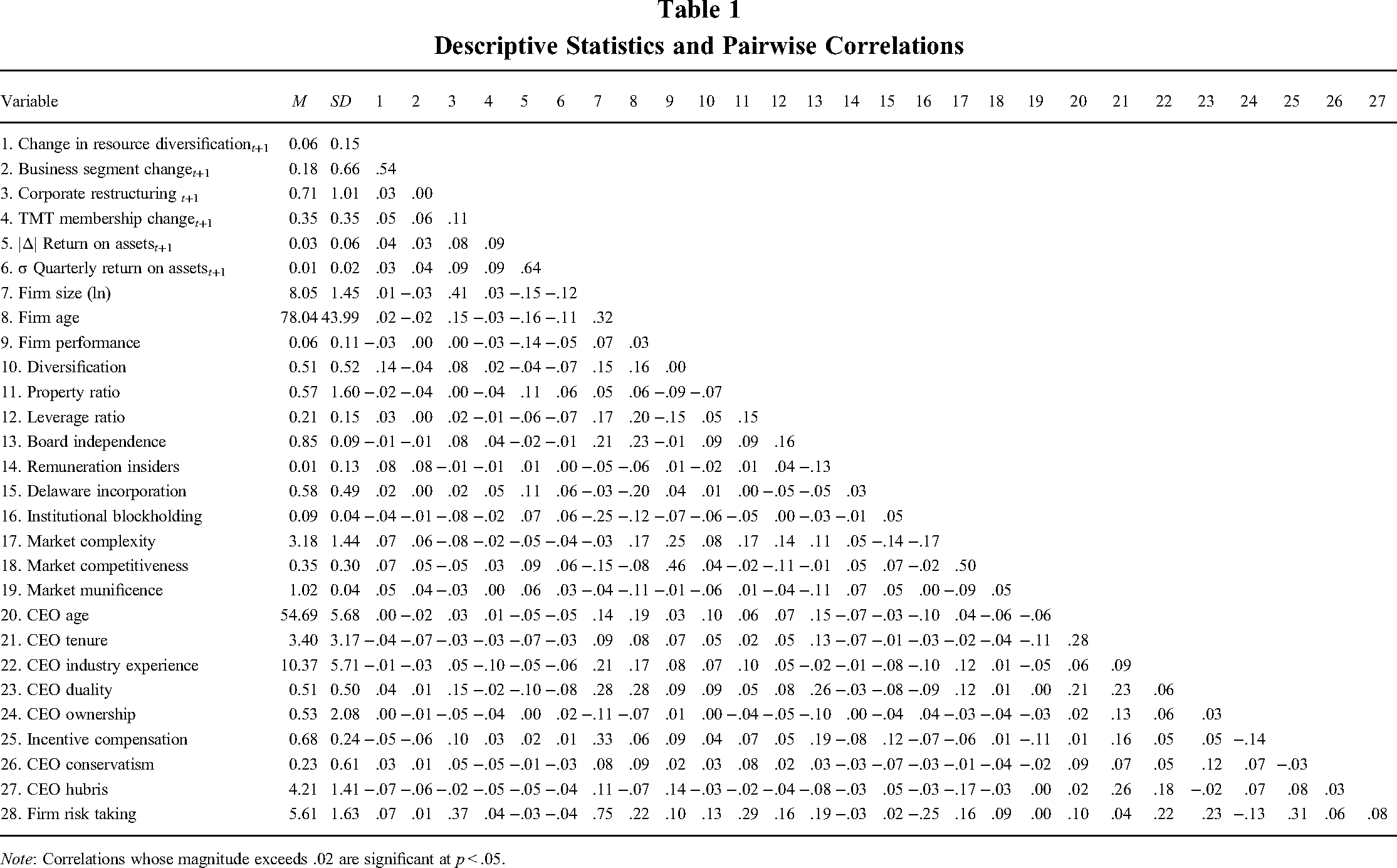

Descriptive Statistics and Pairwise Correlations

Note: Correlations whose magnitude exceeds .02 are significant at p < .05.

Impact of CEO Hubris on Strategic Change and TMT Membership Change

Note: Exact p values in parentheses.

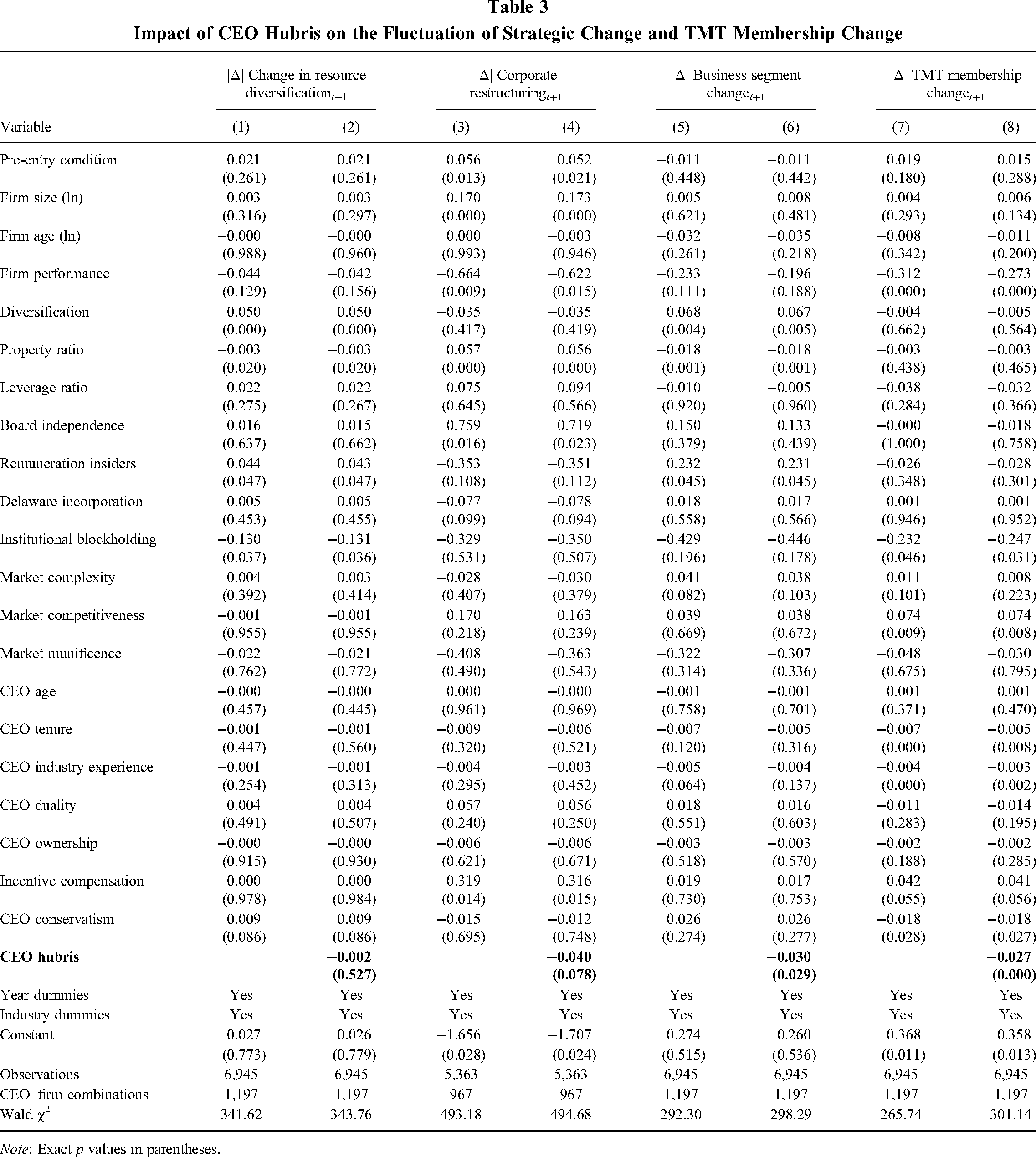

In Table 3, we report the results of our regression analyses of the fluctuation of the various manifestations of strategic change and of TMT membership change. Hypotheses 3a and 3b predicted that CEO hubris is negatively related to the fluctuation of strategic change and TMT membership change, respectively. We find support for these hypotheses in Models 4, 6, and 8 of Table 3 with a negative and marginally significant coefficient on CEO hubris in the regression of the fluctuation of corporate restructuring (Model 4, β = –0.040, p = .078) and negative and significant coefficients in the regressions of business segment changes (Model 6, β = –0.030, p = .029) and TMT membership change (Model 8, β = −0.027, p = .000). Contrary to our prediction, the coefficient on CEO hubris is negative but insignificant in Model 2 of Table 3 in the regression of the fluctuation of changes in a firm's resource diversification (β = –0.002, p = .527). Using our alternative measure based on the fluctuation of a firm's resource deployment, results are marginally significant (β = −0.030, p = .064), aiding limited empirical support to this association.

Impact of CEO Hubris on the Fluctuation of Strategic Change and TMT Membership Change

Note: Exact p values in parentheses.

Robustness Checks and Supplemental Analyses

Potential for endogeneity. We conducted a series of robustness checks and supplemental analyses and present them in detail in our Online Appendix to conserve manuscript space. Particularly, in Online Appendix B.1, we first discuss the rationale behind several potential sources of endogeneity in our analyses (Hill, Johnson, Greco, O’Boyle, & Walter, 2021): (1) the possibility that more hubristic CEOs may not be randomly appointed but specifically selected as a means to consistently inhibit change (endogenous selection of treatment), (2) autocorrelation in case prior strategic change or TMT membership change is related to CEOs’ subsequent option-exercising behavior as an indicator for their level of hubris, and (3) the existence of an unobserved variable as the actual driver behind the association between CEO hubris and strategic change respectively TMT membership change (omitted-variable bias). Although instrumental variables techniques offer a solution to these potential sources of endogeneity (Hill et al., 2021), Semadeni, Withers, and Certo (2014: 1076) urge scholars to verify biased coefficients first, “since endogeneity remediation in its absence yields less efficient estimates.” As a precursor to conducting the accordant Durbin-Wu-Hausman tests suited to verify the detriments of these potential sources of endogeneity, we confirm the amount of CEOs’ personal political contributions as a relevant and exogenous instrument for CEO hubris in Online Appendix Table 2 and in Panel A of Online Appendix Table 3 (cf., Bascle, 2008; Semadeni et al., 2014). The results of our Durbin-Wu-Hausman tests are reported in Panel B of Online Appendix Table 3 and suggest that, although theoretically constructible, concerns regarding the potential sources of endogeneity mentioned above appear empirically negligible in our regressions and do not warrant the inefficient application of two-stage instrumental variables regressions (Semadeni et al., 2014).

Moreover, in the remainder of Online Appendix B.1, we also assess the impact threshold of a confounding variable (ITCV) (Busenbark, Yoon, Gamache, & Withers, 2021; Frank, 2000) in Online Appendix Table 4, indicating that it is relatively unlikely that there exists a variable yet omitted from our models that would invalidate our inferences, and the robustness of our inferences to replacement (RIR) (Busenbark et al., 2021; Frank et al., 2021), indicating that, to invalidate our weakest causal inference, an omitted variable would still have to overturn more than 350 observations that are currently significant. As such, these additional analyses further support the conclusion that the potential sources of endogeneity discussed earlier do not induce a significant bias in our analyses.

Measurement of CEO hubris. Moreover, in Online Appendix B.2.1, we assess the validity of our results in the light of potential alternative explanations for the well-established CEO hubris measure we employ in our analyses. Specifically, one might argue that CEOs’ option-exercising behavior (as the key determinant of our quantification of CEO hubris) was driven not by their degree of hubris but by alternative factors, such as tax concerns or insider information. We assess such potential alternative explanations both theoretically and empirically, highlighting, among others, that our results are robust to a set of alternative model specifications specifically accounting for these alternative explanations (see Online Appendix Tables 5–8). Beyond ruling out potential alternative explanations, we then resort to alternative measurements of CEO hubris to confirm the validity of our results more broadly in Section B.2.2 of our Online Appendix. Particularly, we first resort to two alternative option-based assessments: an ordinal measure based on the moneyness thresholds set forth by Campbell et al. (2011)—above 100% for high hubris, between 30% and 100% for moderate hubris, below 30% for low hubris—as well as the more general option-based measure based on CEOs’ vested in-the-money options relative to their total compensation employed by, for example, Lee, Hwang, and Chen (2017) in Online Appendix Tables 9 and 10, respectively. Moreover, although our application of an option-based measure as a proxy for CEO hubris was strongly driven by the desire to ensure the very best fit between theory and empirics (i.e., capturing CEOs’ overestimation of firm prospects that we invoke in our theorizing; cf., Malmendier, 2018), prior work also resorted to press-based or composite measurements as proxies of CEO hubris (see Chen et al., 2015, for a review). In light of their vulnerability to impression management (Hill et al., 2014; Malmendier & Tate, 2008) that is frequently observed in the focal context of major changes (Whittington et al., 2016), however, press-based measures appear inappropriate in our research setting by design. In contrast, although composite measures of CEO hubris do not capture the overestimation of firm prospects as closely as option-based measures do, they are inherently less vulnerable to the aforementioned critique toward press-based measures. Therefore, following Hayward and Hambrick (1997), we also employed a composite measure of CEO hubris, comprising CEOs’ self-importance, success, and external praise in analysts calls (cf., Loughran & McDonald, 2011), in the remainder of Section B.2.2 of our Online Appendix and find further support for a negative association with firms’ degree and fluctuation of change (see Online Appendix Table 11).

Contextualization. Acknowledging that higher degrees of CEO hubris not only evoke smaller degrees but also a smaller fluctuation of both strategic change and TMT membership change, one may further raise the question of whether or to which degree the effect of more hubristic CEOs’ preference for steadiness may depend on other contingencies. We explore this possibility by testing whether market munificence, uncertainty, complexity, or a CEO's duality, tenure, or power more broadly (e.g., Shi, Connelly, Mackey, & Gupta, 2019) moderate the negative effect of CEO hubris on strategic change and TMT membership change. Whereas none of these interactions prove significant (cf., Online Appendix Tables 12–14),8 alternative facets of a CEO's personality itself may reinforce or cushion more hubristic CEOs’ preference for steadiness since personalities are complex in that traits, beliefs, and values interact in forming CEOs’ preferences (Gupta, Nadkarni, & Mariam, 2019; Hambrick & Mason, 1984). As such, more hubristic CEOs’ effect on strategic change and TMT membership change may become particularly evident as their preference for steadiness resonates with (or runs counter to) other dispositions. To explore this line of thought, we resort to CEOs’ political ideology, i.e., their stance on the liberal–conservative continuum, as a central determinant of their subjective ascription of merit to steadiness and transformation (Jost, 2017; Jost, Glaser, Kruglanski, & Sulloway, 2003) and indeed find comprehensive evidence suggesting that CEOs’ more conservative ideological leaning substantiates the negative effect of CEO hubris on strategic change and TMT membership change (see Online Appendix Table 15). Nevertheless, even a factor so consequential for CEOs’ perceived merit in transformation as a liberal ideological leaning (Jost, 2017) does not suffice to elicit a positive marginal effect of CEO hubris on either of these dependent variables. Rather, there seems to be a clear, negative effect that is stronger or weaker depending on CEOs’ political ideologies.

Post-hoc Analysis

On the Pervasiveness of More Hubristic CEOs’ Preference for Steadiness

Our research commenced with the rationale that, while more hubristic CEOs are regularly attracted to challenging and highly consequential strategic activities, it remains unclear whether these CEOs are regularly inclined to change or not to change their firms’ overarching trajectories. Explicating arguments on either directionality of this association, we then find broad and robust evidence that higher degrees of hubris induce CEOs to exhibit a preference for steadiness in their firms’ strategic orientation and TMT composition—a preference that follows directly from their unwavering conviction in their personal grandeur and likewise corresponds to research in psychology linking self-ascribed competence and elevated levels of self-efficacy and self-confidence (both of which apply to more hubristic individuals; Hayward & Hambrick, 1997) with goal perseverance (e.g., Tenenbaum et al., 2005; Wood & Bandura, 1989). As such, the preference for steadiness we observe with regard to their firms’ strategic orientation and TMT composition may even constitute a particularly pervasive tenet associated with higher degrees of hubris—one that shapes more hubristic CEOs’ perception and interpretation (as well as subsequent organizational outcomes) not just in the strategic and social domains we assessed but across administrative situations.

CEO Hubris and Firm Performance Fluctuation

One fundamental organizational outcome predestined to assess the pervasiveness of more hubristic CEOs’ preference for steadiness should be a firm's financial performance. Based on extant research, higher degrees of CEO hubris should, by and large, be associated with a greater fluctuation of firm performance, as the frequent engagement in high-stakes activities, such as acquisitions or innovation projects, inflates performance volatility (Chatterjee & Hambrick, 2007; Wiseman & Gómez-Mejía, 1998). In this vein, Hirshleifer et al. (2012) indeed find a positive association between CEO hubris and firm stock return volatility, casting some doubt on the pervasiveness of more hubristic CEOs’ preference for steadiness affecting organizational outcomes beyond strategic change or TMT membership change.

Yet, a potential explanation for this finding may be Hirshleifer et al.'s (2012) operationalization of performance fluctuation as a firm's daily stock return volatility. Stock returns reflect the market's assessment of how well a firm will be performing in the future. A high volatility of this assessment is hence reflective of a high volatility of the market's anticipation of future firm performance. The market might however be particularly susceptible to cues instigating the firm risk-taking typically associated with more hubristic CEOs (e.g., Li & Tang, 2010). Respective behaviors, such as acquisitions or new product introductions, are usually highly salient to market participants and suggest uncertainty in future firm value (Hirshleifer et al., 2012; Malmendier & Tate, 2008), whereas the steady pursuit of extant endeavors may not offer as large of a headline and thus may remain less salient to market participants. Additionally, while the body of literature on more hubristic CEOs’ engagement in risky strategic activities is substantial (Picone et al., 2014), their preference for steadiness, thus far, does not prevail in management research and hence might not have fully informed market participants yet (Ferraro, Pfeffer, & Sutton, 2005; Ghoshal, 2005). Notably, even analysts seem to be discordant with regard to more hubristic CEOs’ ultimate effects on firm value, as reflected in a greater forecast dispersion pertaining to such firms (Hribar & Yang, 2016). Assessing the fluctuation of accounting-based firm performance should thus better capture the internal processes of a firm and, if pertinent, underscore the relevance of more hubristic CEOs’ preference for steadiness. Specifically, while more hubristic CEOs undisputedly engage in acquisitions and other challenging strategic activities (e.g., Li & Tang, 2010; Malmendier & Tate, 2008), a pervasive preference for steadiness should serve to reduce volatility in other areas of distinct strategic concern. We hence expect that a preference for steadiness, if integral to CEO hubris, will elicit a negative effect on firms’ accounting-based performance fluctuation.

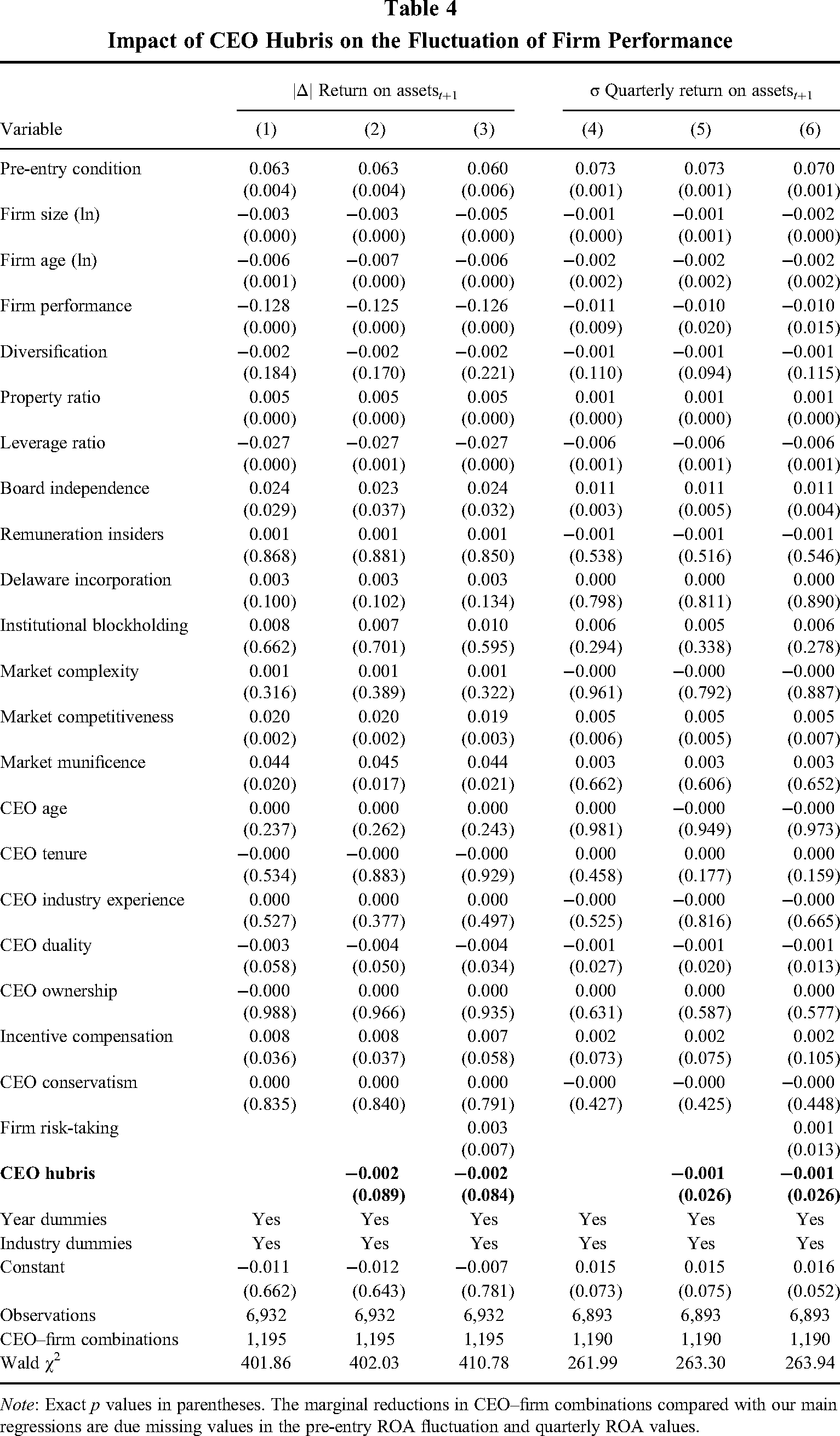

As a post-hoc analysis, presented in Table 4, we thus investigate the association between CEO hubris and a firm's accounting-based performance fluctuation. Following Chatterjee and Hambrick (2007), and in line with our operationalization of the fluctuation of strategic change and TMT membership change, we operationalize a firm's performance fluctuation as the absolute year-on-year difference in its ROA and employ the standard deviation of quarterly ROA as a supplement.9 Supporting the prevalence of more hubristic CEOs’ preference for steadiness in the domain of a firm's performance fluctuation, Table 4 shows a negative and marginally significant coefficient for CEO hubris on the year-on-year fluctuation of firms’ ROA in Model 2 (β = –0.002, p = .089) as well as a negative and significant coefficient for CEO hubris on the standard deviation of quarterly ROA in Model 5 (β = –0.001, p = .026). In economic terms, this refers to a 9% reduction in year-on-year ROA fluctuation for CEOs with a hubris score one standard deviation above the mean compared to their less hubristic counterparts (one standard deviation below the mean). Moreover, these results are robust to adding firm risk-taking as an additional control for more hubristic CEOs’ tendency to engage in manifold and challenging strategic activities, such as acquisitions or R&D investments, which, noteworthily, displays positive and highly significant coefficients as an explanatory variable in and of itself in Models 3 and 6, corroborating the preceding reasoning behind the likely drivers of more hubristic CEOs’ impact on firms’ performance fluctuation.10

Impact of CEO Hubris on the Fluctuation of Firm Performance

Note: Exact p values in parentheses. The marginal reductions in CEO–firm combinations compared with our main regressions are due missing values in the pre-entry ROA fluctuation and quarterly ROA values.

Discussion

More hubristic CEOs’ attraction to manifold strategic activities has repeatedly contributed to their depiction as incubators of change (Galasso & Simcoe, 2011; Li & Tang, 2010). Yet, inferences from stand-alone strategic activities may not always be sufficient to explicate such general preferences. By establishing sets of competing hypotheses on the effect of CEO hubris on strategic change and TMT membership change, this study aimed to provide a more comprehensive understanding of the inclinations associated with higher degrees of CEO hubris, highlighting that a preference for steadiness may well regulate their effect on certain organizational outcomes.

Using a panel data set of S&P 1500 CEOs, we find that higher degrees of CEO hubris persistently impede both strategic change and TMT membership change. Thus, more hubristic CEOs’ inflated self-assessment manifests not only in the pursuit of challenging strategic activities but also in a preference for steadiness regulating its impact on firms’ overarching trajectories. Appreciating this preference for steadiness as a central tenet of hubris emphasizes the need to move beyond the high-stakes activities typically associated with more hubristic CEOs and thus to acknowledge the intra-dispositional heterogeneity of CEOs’ complex psychological characteristics and its implications for organizational outcomes (cf., Gupta et al., 2019).

Implications

Our findings have implications for research on strategic management and organization science. First, our study contributes to upper echelons research (Hambrick, 2007; Hambrick & Mason, 1984) by resolving the obscurity surrounding more hubristic CEOs’ dispositional preference for change or steadiness as well as by highlighting both strategic change and TMT membership change as central mechanisms through which more hubristic CEOs impact their firms. In particular, we highlight that, despite their attraction to acquisitions, new product introductions, or risky investments (e.g., Hirshleifer et al., 2012; Malmendier & Tate, 2005; 2008), more hubristic CEOs steadily eschew change in their firm's strategic orientation and TMT composition. In light of theoretical arguments and scholarly suggestions endorsing positive associations (Galasso & Simcoe, 2011; Li & Tang, 2010), clarity on the directionality of these effects provides additional ammunition to research aiming to explain more macro-level outcomes, like firm performance or competitive behavior, without aggravating theoretical black boxes (Lawrence, 1997).

Second, our study thus extends research on strategic leadership and managerial biases (e.g., Finkelstein et al., 2009) by more holistically representing the tenets of CEO hubris. Specifically, demonstrating that more hubristic CEOs remain steady with regard to the extant strategic orientation and TMT composition even though they are particularly prone to pursue major strategic activities, such as acquisitions or product innovations (Malmendier & Tate, 2008; Tang, Li, et al., 2015), breaks with the implicit notion that these activities may cumulate in (and reflect more hubristic CEOs’ pursuit of) higher-order change. Instead, this accordance suggests that higher degrees of hubris induce a tendency to steadily pursue the firms’ extant paths via risky strategic activities. By also providing empirical evidence indicating its negative effect on firm performance fluctuation, we demonstrate that this preference for steadiness might constitute a particularly pervasive tenet of executive hubris reflected in outcomes at various levels of analysis. Moreover, we understand more hubristic CEOs’ preference for steadiness as distinct from alternative inhibitors of change, namely, commitment to the status quo and escalation of commitment. Specifically, more hubristic CEOs do not refrain from the pursuit of challenging strategic activities that may, at times, alter the status quo; yet, they refrain from the pursuit of higher-order changes, suggesting a preference for steadiness, i.e., constancy of conduct, instead. Moreover, from a steadiness perspective, more hubristic CEOs refrain from strategic change and TMT membership change because they are convinced that doing so will inevitably induce organizational success—a motivational component not necessarily incorporated in commitment to the status quo (Hambrick, Geletkanycz, & Fredrickson, 1993). Similarly, escalated commitment (Staw, 1976; Staw, Sandelands, & Dutton, 1981) falls short in explaining our results since our reasoning does not require otherwise indispensable elements, such as corporate deterioration (Trahms, Ndofor, & Sirmon, 2013) or corrective feedback (Chen et al., 2015), as antecedents for change.11