Abstract

This article draws on the cultural friction perspective to study the performance implications of cultural distance (CD) in international joint ventures (IJVs). In particular, I theorize about the cultural carriers, point of contact, exchange, and mitigating mechanisms through which CD affects the interactions and relationships between the different organizations involved in IJVs. I postulate that CD between the focal firm's home country and the partner firm's home country negatively influences the focal firm's abnormal returns, while CD between the focal firm's and the IJV's home countries and CD between the partner firm's and the IJV's home countries exert a positive impact. I further propose that prior IJV experience is an important mitigating mechanism that moderates these relationships, contingent on the level of the prior experience's success. Using data for 709 IJV announcements, I find that CD between focal firm and partner firm and CD between focal firm and IJV significantly influences market reactions to IJVs, while prior experience moderates the effect of CD between the parent firms. This study helps to resolve previously inconclusive findings by documenting that CD's impact fundamentally depends on whose CD is considered and what type of experience a firm possesses.

This study builds on the cultural friction perspective to examine the influence of cultural distance (CD) on international joint venture (IJV) market reactions. CD measures the extent to which two national cultures are similar or different and is a central concept in international management (Shenkar, Tallman, Wang, & Wu, 2020). A prominent area for its application are IJVs, which are firms with multiple parent firms, of which at least one is headquartered outside of the IJV's country of operation (Nippa & Reuer, 2019). Existing work on the role of CD in IJV success typically assumes that firms engage in IJVs by collaborating with local partners, that is, partners that are headquartered in the same country as the IJV. Thus, research frequently has examined the CD between the IJV parents’ home countries (Merchant & Schendel, 2000; S. Park & Ungson, 1997) but yielded inconsistent findings. Some studies reveal a negative impact of CD on IJV success (e.g., Hennart & Zeng, 2002; Merchant, 2000), while others find a positive (e.g., S. Park & Ungson, 1997; Pothukuchi, Damanpour, Choi, Chen, & Park, 2002) or no significant influence (e.g., Luo, 2002; Merchant, 2002).

My research draws on the cultural friction perspective as an overarching framework to help resolve some of the inconsistencies. The cultural friction perspective examines the actual cultural interaction in cross-border business activities and captures the nature and magnitude of interaction between the cultural systems engaged (Luo & Shenkar, 2011; Shenkar, 2012). As a result, the cultural friction perspective moves beyond viewing culture in terms of its differences, which has been done conventionally (Shenkar, 2001). Instead, the cultural friction approach emphasizes the different influences of cultural differences that are contingent upon the nature and characteristics of the cultural carriers, their point of contact, exchange, and the mechanisms that mitigate and alleviate cultural friction involved (Shenkar, Luo, & Yeheskel, 2008). By examining cultural carriers, point of contact, exchange, and mitigating mechanisms, I gain an understanding of the underlying relationships between the organizations involved in IJVs and account for two opposing effects of CD. That is, CD can hamper interaction and performance due to unfamiliarity with the foreign culture (Miller & Parkhe, 2002), but it can also be a source of gains and synergies by bringing together diverse resources and skills (Stahl & Tung, 2015).

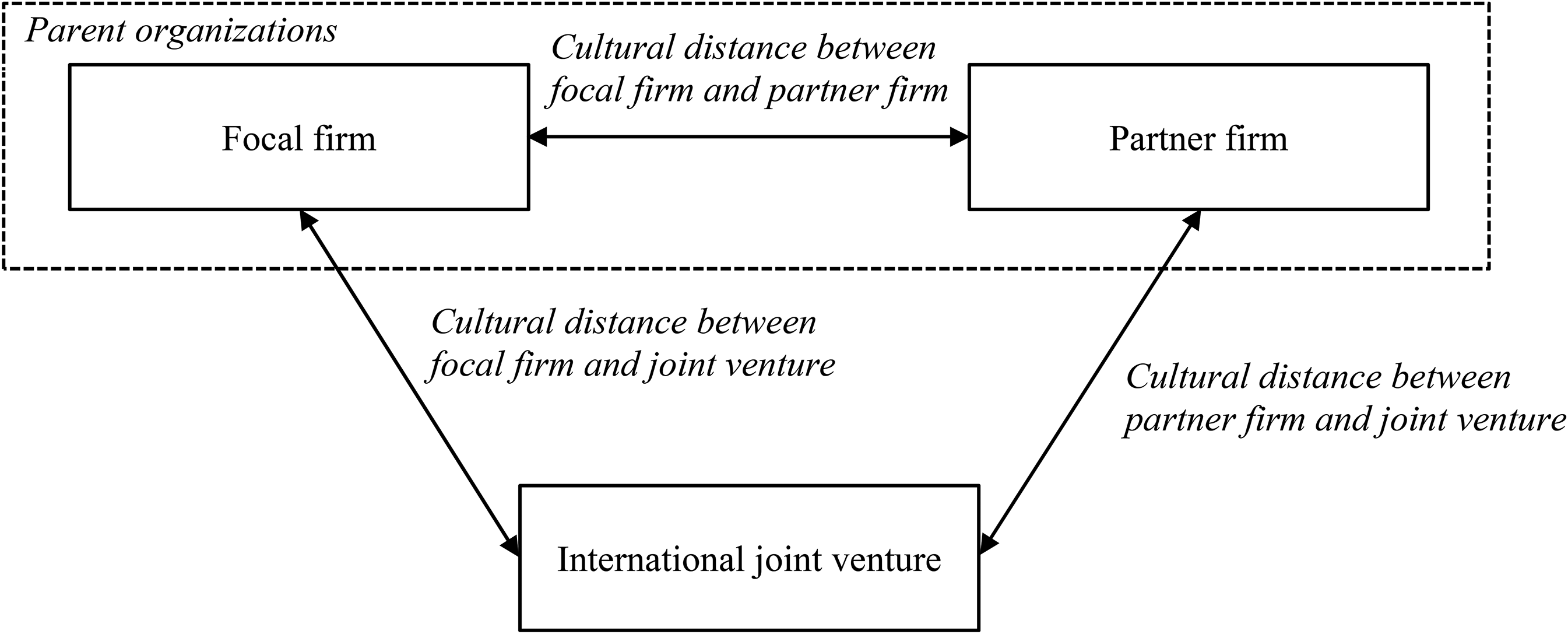

Employing the cultural friction perspective also enables me to account for the different country constellations in IJVs that have been largely neglected in prior work. For instance, parents that are headquartered in two different countries can establish an IJV in a third country, or parents from the same country may establish an IJV abroad (Makino & Beamish, 1998). Theorizing about the CD between the home countries of the parents alone while neglecting the IJV's own home country, as has typically been done in previous research, yields an incomplete, if not even flawed, picture of culture's influence that ignores the inherent differences between parent-parent and parent-IJV relationships (Ren, Gray, & Kim, 2009). By contrast, my approach captures CD's multifaceted role in the different relationships involved in IJVs and, thus, allows me to theorize more precisely on the mechanisms through which CD affects IJV performance. Figure 1 depicts the different CDs involved in an IJV with two parent firms.

Cultural Distance (CD) Involving Parent Organizations and International Joint Venture

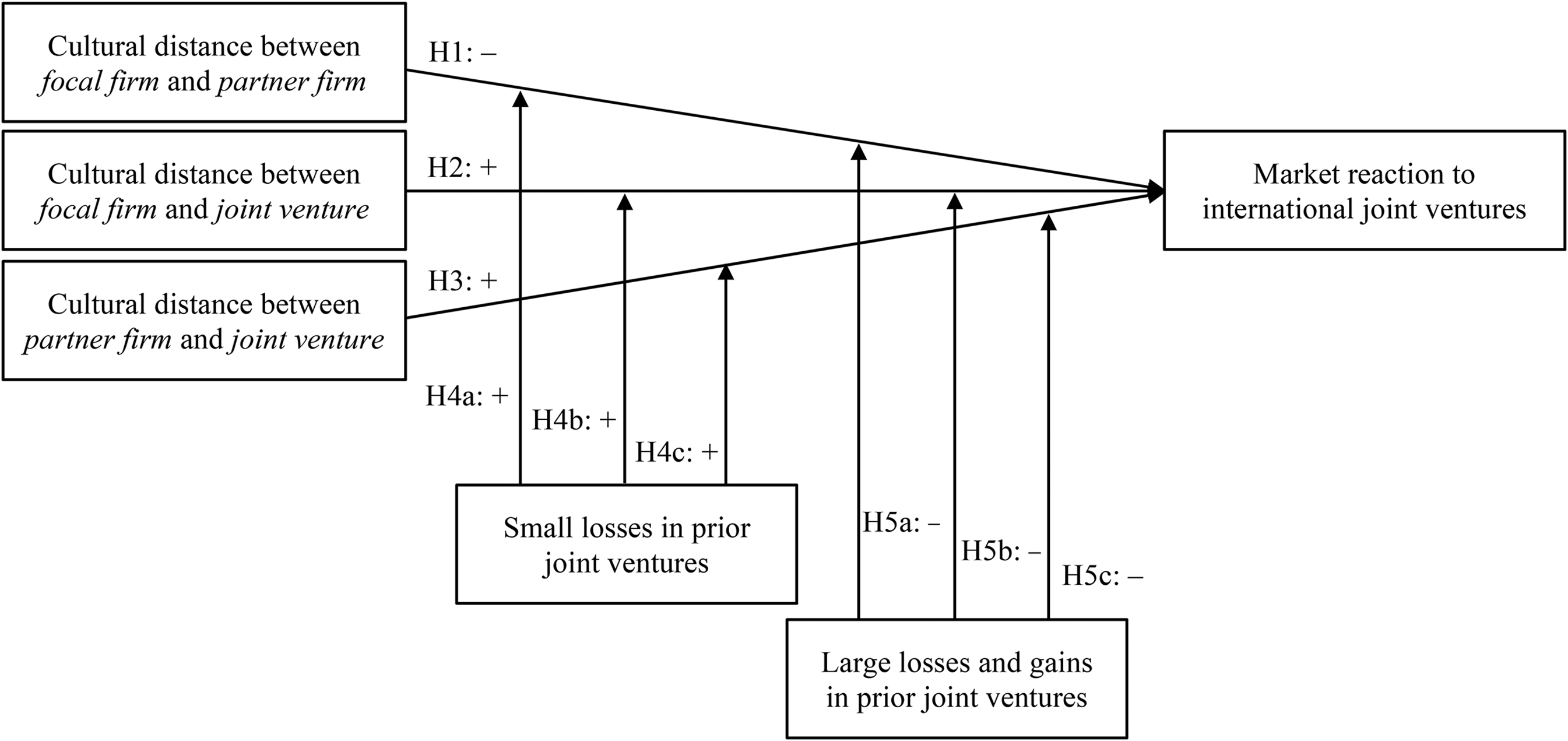

I theorize that the cultural friction perspective explains CD's role in IJVs, contingent on the different cultural carriers as well as points of contact and interorganizational exchanges involved. In particular, I argue that CD between the focal firm's home country and the partner firm's home country adversely affects a focal firm's market reaction to IJV announcements, while the CD between the focal firm's home country and the IJV's home country and the CD between the partner firm's home country and the IJV's home country favorably affect market reaction. I further postulate that previous IJV experience is a central mitigating mechanism of cultural friction that helps firms to better overcome and leverage CD by improving their communication, socialization, acculturation, and staffing abroad. However, I argue that this effect depends on the type of experience gained. Specifically, I theorize that prior experience influences the three relationships, such that small losses incurred in previous IJVs positively moderate them, whereas gains and big losses negatively moderate them.

I test my hypotheses based on a sample of 709 IJV announcements involving 42 countries from 1985 to 2019, and I find support for several of the hypotheses. The findings furnish evidence of the multifaceted ways in which CD and previous experience impact market reaction to IJV announcements. The results further highlight that capturing the various constellations of countries can offer a richer and more complete understanding of how CD affects IJV outcomes.

This study contributes to research on the influence of CD on IJV success. While CD has become a mainstay in international management, it has generated conflicting findings and has drawn criticism, including overly simplistic theorizing (Shenkar, 2001; Tung & Verbeke, 2010). Prior work has typically built on either the cultural familiarity lens or the positive organizational scholarship premise to explain cross-cultural activities while ignoring the other perspective (e.g., Hennart & Zeng, 2002; Huang, Zhu, & Brass, 2017). My study builds on the cultural friction perspective that systematically examines the cultural carriers, point of contact, exchange, and mitigating mechanisms involved and, in doing so, helps to reconcile some of these conflicting findings by capturing elements of both CD perspectives (Luo & Shenkar, 2011; Shenkar et al., 2008). This friction approach allows me to study the actual interactional process of engagement and, as a result, theorize more accurately on the underlying mechanisms through which CD affects performance outcomes of firms (Shenkar et al., 2020). I show that CD exerts both positive and negative influences on firm success, depending on the nature and traits of the cultural carriers, point of contact, exchange, and mitigating mechanisms involved.

I also advance IJV research, which has almost exclusively studied the CD between the home countries of the two parent firms (e.g., Merchant, 2002; S. Park & Ungson, 1997; see Larimo, 2007, for an exception). The predominant focus on parent firms neglects the different country constellations in IJVs. Given the inherent differences between parent-parent and parent-IJV relationships, accounting for the home country of the IJV as well as the home countries of its parent firms is necessary for accurate theory development and testing. In addition, my work carries implications for the organizational learning literature in international management research (Greve, 2021; Lord & Ranft, 2000). Prior international management theories, such as the influential Uppsala stage model, are based on the premise that previous experience is a central means for firms to gradually overcome the negative implications of cultural differences (Johanson & Vahlne, 1977). My research extends this premise and demonstrates that previous IJV experience can be boon and bane for the way firms deal with CD, contingent on whether the experience itself was successful or not.

Theory and Hypotheses

Cultural Friction Perspective

The cultural friction perspective studies the actual interaction in cross-cultural encounters and accounts for the nature and magnitude of the interaction between the cultural systems engaged in international business activities (Shenkar et al., 2008). The “base condition” of the friction perspective is CD (Luo & Shenkar, 2011), which measures the extent to which two national cultures, that is, the deeply rooted values and beliefs that are shared by a nation's individuals, are similar or different (Shenkar, 2001). Since culture profoundly shapes the decisions and strategies of firms (e.g., Hofstede, 2001; J. Li & Harrison, 2008), CD has been extensively used to theorize about cross-border interactions between firms (e.g., Lee, Shenkar, & Li, 2008; Siegel, Licht, & Schwartz, 2013). As a result, the management literature has applied CD as a central construct to international management activities, ranging from entry mode choice to multinational enterprise performance (e.g., Shenkar, 2001; Tung & Verbeke, 2010).

Two main perspectives have emerged to theorize about CD's influence in international management. The first premise builds on cultural familiarity theory, which views CD as an impediment to cross-cultural interaction and has been adopted by the majority of prior research due to its intuitive appeal (Shenkar, 2001, 2012). The premise predicts that CD, by default, hampers the interaction between international transaction partners because misunderstanding, inefficiency, and conflict, originating from the partners’ lack of knowledge of the distant culture, more likely emerge and intensify with growing CD (e.g., Luo & Peng, 1999; Miller & Parkhe, 2002). The second premise builds on the positive organizational scholarship lens (Cameron, Dutton, & Quinn, 2003) and considers CD an important source of gains that help firms become more competitive (Gomez-Mejia & Palich, 1997; Stahl & Tung, 2015). It draws on the notion that individuals and firms from different cultures possess a set of unique and diverse repertoires of skills that are embedded in their cultural environments and can complement and enrich each other, which results in more creative solutions and greater synergistic gains (Chua, 2018; Shenkar et al., 2008).

Most studies have picked one of the two lenses for their theory development without discussing the other, though some have attempted to account for or even reconcile both perspectives by identifying important moderators that determine CD's influence (e.g., Slangen, 2006) or by developing alternative cultural approaches altogether (e.g., Li, Brodbeck, Shenkar, Ponzi, & Fisch, 2017). By contrast, the friction perspective accounts for the different potential influences of CD, that is, positive and negative, by systematically examining the very nature and characteristics of the cultural carriers, point of contact, exchange, and “lubricants,” that is, mechanisms that help mitigate or alleviate the cultural friction, involved (Shenkar et al., 2008).

Cultural carriers refers to the “individuals, groups, and organizations that carry and transmit cultural content and signals” (Shenkar et al., 2008: 914). They may include expatriates and local employees of the home and host culture organizations who typically have the most intense contact in cross-cultural exchanges. The point of contact alludes to the domains in which the interaction between the cultural carriers occurs, while exchange refers to the process in which the carriers offer and receive different information, knowledge, and resources to and from each other (Shenkar et al., 2008). Moreover, lubricants are the mitigating mechanisms of cultural friction (Luo & Shenkar, 2011). They are organizational “prescriptions” that include communication, acculturation, socialization, and staffing and help organizations reduce the cultural friction they experience when operating in distant cultures (Luo & Shenkar, 2011). By examining cultural carriers, point of contact, exchange, and mitigating mechanisms, the cultural friction perspective moves away from the conventional view of CD as a static antecedent that automatically exerts either a positive or a negative influence based on the same set of mechanisms. Instead, the cultural friction approach suggests that culture's influence and whether and which mechanisms predominantly act in specific contexts fundamentally depend on critical contingency factors (Luo & Shenkar, 2011). Therefore, the friction perspective enables me to systematically investigate the underlying relationships and processes of the organizations involved in IJVs and how CD influences IJV market reactions.

IJVs

IJVs are ventures involving multiple parent firms, of which at least one is headquartered outside of the joint venture's country of operation (Gong, Shenkar, Luo, & Nyaw, 2007; Luo, 2005). Parent firms establish IJVs for different reasons, including entrance into new markets, creation of scale economies, reduction of risks, and learning of new skills and technologies, among many others (e.g., Nippa & Reuer, 2019; Tong & Li, 2013). Ultimately, firms enter into IJV agreements with their partners to create value, which, for public firms, typically is measured through the market's expectation about the realization of the IJV's economic value to the parent (Das & Teng, 2000; Kumar, 2010). Yet, IJVs do not always create value and, instead, often evoke negative market responses (Nippa & Reuer, 2019).

Since IJVs inherently involve the interaction between firms that are embedded in different national cultures, CD has been frequently featured as an explanatory variable for IJV value creation (e.g., Merchant, 2000; Nippa & Reuer, 2019). In order to more precisely develop my theoretical arguments about the impact of CD on market reaction to IJVs, I distinguish between the CD between the focal firm and partner firm, the CD between the focal firm and the IJV, and the CD between the partner firm and the IJV. This critical distinction accounts for the inherent differences between the relationship between focal firm and partner firm, the relationship between focal firm and IJV, and the relationship between partner firm and IJV with respect to the cultural carriers, point of contact, exchange, and mitigating mechanisms involved (Shenkar et al., 2008). Therefore, I will next systematically examine each of these elements and, building on the analysis, predict how CD affects the outcome of IJVs.

The Impact of Cultural Distance on Market Reaction to IJVs

CD between focal firm and partner firm. The cultural carriers in the relationship between focal firm and partner firm are the two (or more) parent firms, that is, a focal firm and its partner(s). While the parents have an equity stake in the IJV and thus strive for greater IJV performance, they typically own greater equity outside of the IJV. Thus, if achieving greater operating performance of the IJV would damage, for example, the parent firm's brand or leads to loss of valuable intellectual property, the parent would choose to protect its overall performance at the expense of the IJV's operations. As a result, the interests of the cultural carriers are typically not fully aligned, that is, success of one parent does not always translate to success for the other. Further, the cultural carriers are autonomous organizations. That is, they do not have formal decision-making power over each other, as parent firms usually do not have significant ownership stakes in each other (Chi, 2000). Thus, there normally is no clear leader-follower relationship between the parent firms with respect to who “has the final say,” even though one parent may hold greater equity in the IJV or contribute resources/expertise that are considered more valuable. The point of contact takes place when the parent firms come together, while the exchange predominantly occurs when the parents offer and receive information about their preferences and suggestions on how to define the IJV's goals, specify its structure, and appoint its management and personnel (Nippa & Reuer, 2019). Since the main value-creating operations typically occur within the IJV, the parent firms normally do not engage in exchange of resources with each other but, rather, negotiate and discuss with each other about how to manage and operate their joint venture prior to the IJV's establishment and during its operation (Luo, 1999, 2007).

CD between the parent firms affects the focal firm's gains from an IJV in several ways. First, CD influences the cultural carriers and determines the extent to which their preferences differ. For instance, firms from high-power-distance countries prefer clear hierarchies, whereas firms from low-power-distance countries value flat hierarchies (Huang et al., 2017). Similarly, while parents from high-uncertainty-avoiding cultures tend to value standardized processes and strict rules, those from low-uncertainty-avoiding cultures prefer greater flexibility. Furthermore, parents from individualist cultures tend to value individual accountability and decision-making, whereas parent firms from collectivist cultures tend to offer team-based incentives and prefer collective decision-making processes (Hofstede, 2001). The greater CD between the parent firms, the greater the differences between the interests of the cultural carriers. Differing preferences render interaction between the parent firms more cumbersome and difficult, leading to greater cultural friction between the parent firms. Overcoming this friction can prove difficult, since the cultural carriers do not have a clear leader-follower relationship and, thus, cannot simply and quickly overrule the other.

Second, CD affects the exchange at the point of contact, where the cultural carriers interact with each other. The exchange between the cultural carriers revolves around coordination and negotiation of their IJV's activities. The smoother the coordination and negotiation between the parents, the better the IJV performance, because the venture will receive a consistent mandate/message from its parent firms without much delay and enjoy their full support afterward. CD affects the exchange between the cultural carriers, because it influences the negotiation and communication styles of the parents and their executives (Gelfand & Realo, 1999). For example, negotiators from individualist and masculine countries tend to be confrontational and efficient, while those from collectivist and feminine countries tend to seek consensus and harmony (Gelfand & Brett, 2004; C. Li & Haleblian, 2022). Moreover, negotiators from high-uncertainty-avoiding countries are less prepared to accept compromises, whereas those from low-uncertainty-avoiding cultures are more willing to compromise (Hofstede, 2001). Greater CD, thus, obstructs the negotiation and coordination between the parents before the establishment of the IJV and during its operation (Salk & Shenkar, 2001). When CD increases, negotiation and communication styles become less compatible, thereby increasing cultural friction at the point of contact. As a result, misunderstanding more likely occurs, which leads to conflicts between the parent firms during their exchanges and inefficient management of the IJV, both of which hamper the IJV's performance and lower the focal firm's gains from the IJV. Hence, the market will react less favorably to a focal firm's IJV announcement. I postulate the following:

Hypothesis 1: CD between the focal firm's home country and the partner firm's home country negatively affects market reaction to a focal firm's IJV announcement.

CD between focal firm and IJV. The cultural carriers in this relationship are the focal firm and the IJV. Unlike the parent-parent relationship, the interests of the cultural carriers are even more aligned, since the parent firms completely own the IJV. Thus, success of the IJV directly translates to gains for the focal firm. Furthermore, the cultural carriers in the focal-IJV relationship have a clear leader-follower power structure, as the parents share ownership of the joint venture and have formal decision-making authority over the venture (Geringer & Hebert, 1991; Nippa & Reuer, 2019). Thus, the parent is the leader that gives directions, while the joint venture is the follower that abides by these directives (Geringer & Hebert, 1991). The point of contact and exchange between the parent and IJV also differ fundamentally from those between the parent firms (Nippa & Reuer, 2019). In the parent-IJV relationship, the focal firm and IJV typically interact with one another to exchange resources and skills. While the parent normally provides expertise, knowledge, and resources, the IJV usually conducts the main value-creating activities (Harrigan, 1986, 1988). For instance, the parent may offer blueprints of its products so that the IJV can adapt these products to local requirements and sell them, or the parent may provide knowledge so that the IJV can build on the knowledge to conduct research and development (R&D) and use the results or transfer them back to the parent (Choi & Contractor, 2016; Y. Zhang, Li, Hitt, & Cui, 2007).

CD between the focal firm and the IJV influences the extent to which the focal firm benefits from the IJV in several ways. First, CD affects the cultural carriers and their preferences. The greater CD between focal firm and IJV, the more strongly they differ with respect to how they prefer to run the IJV. However, these differences are significantly mitigated by the shared interests and clear leader-follower relationships. Since the focal firm co-owns the IJV, there is a clear understanding that the interests of the two cultural carriers are aligned, which helps reduce friction during the discussion of the structures and processes of the IJV. More importantly, since the focal firm is the leader, it can quickly overrule the follower, that is, the IJV, when needed, thereby reducing the time and effort required to come to an agreement. Hence, while CD influences the preferences of the cultural carriers, the focal firm's and IJV's alignment of interests and the clear leader-follower relationship drastically reduce CD's influence.

Second, CD influences the exchange between the focal firm and IJV at their point of contact. The exchange between focal firm and IJV revolves around the sharing of knowledge, resources, and skills (Harrigan, 1988). Typically, the focal firm offers its expertise and resources, such as intellectual property, while the IJV performs the value-creating activities, such as product development or sales (Choi & Contractor, 2016; Nippa & Reuer, 2020). Since the skills and resources of firms are embedded in their national cultures and, thus, are often unique to firms located in that culture (Barney, 1986), the focal parent gains access to a large and diverse pool of skills and resources that are embedded in the IJV's national culture, which can help it create better and more novel solutions and, thus, enhance its performance. In turn, the focal firm can contribute unique and diverse skills and resources to its IJV. These resources enrich the operations of the IJV, allowing it to develop superior products, more innovative solutions, and, thus, improve its performance, which translates to gains for the focal firm (Aggarwal, Hsu, & Wu, 2020; Zaheer, Schomaker, & Nachum, 2012). The more culturally distant focal firm and IJV, the more different the skills and resources the firms can obtain from one another. This tendency holds true to a certain degree, since locally preferred/valuable resources can become less valuable in international markets, for example, due to heterogeneous demands (X. Zhang, Xie, Li, & Cheng, 2019). Therefore, CD between focal firm and IJV benefits the focal firm by improving its IJV's performance and by providing the focal firm with rare and valuable resources, thereby drawing favorable market reactions to the focal firm's IJV announcement. I argue the following:

Hypothesis 2: CD between the focal firm's home country and the IJV's home country positively affects market reaction to a focal firm's IJV announcement.

CD between partner firm and IJV. The cultural carriers are the partner firm and the IJV. Similar to the focal firm–IJV relationship, the partner firm owns significant equity in the IJV. Thus, the interests between the two entities are largely aligned, while the leader and follower roles are also clearly defined (Geringer & Hebert, 1991; Nippa & Reuer, 2019). The point of contact and exchange also resemble those of the relationship between focal firm and IJV. That is, the partner firm predominantly engages with the IJV in order to provide the latter with resources and skills, whereas the IJV performs the value-creating, operating activities (Choi & Contractor, 2016; Y. Zhang et al., 2007).

I propose that CD between partner firm and IJV can influence the performance implications of the focal firm. While CD determines the preferences and operations of the partner firm vis-à-vis the IJV itself, the alignment of interests and hierarchical relationship largely mitigate the cultural friction that originates from cultural differences. However, CD does exert an influence on the synergistic effects of combining knowledge and resources from two organizations that are embedded in vastly different cultures (Morosini, Shane, & Singh, 1998). That is, the IJV is able to access the partner firm's unique and diverse resources that allow it to develop innovative solutions and improve its performance (Zaheer et al., 2012). In doing so, the focal firm can benefit from the performance gains of the IJV and, therefore, draws positive stock market reactions to the focal firm's IJV announcement. Hence, I propose the following:

Hypothesis 3: CD between the partner firm's home country and the IJV's home country positively affects market reaction to a focal firm's IJV announcement.

Previous IJV Experience

In addition to the cultural carriers, point of contact, and exchange, the cultural friction perspective posits that “lubricants,” that is, mitigating mechanisms that help firms reduce cultural friction at the point of contact, are the other main determinant of how CD affects cross-border business activities (Luo & Shenkar, 2011; Shenkar, 2012). Lubricants can help organizations overcome and leverage CD through improved communication, socialization, acculturation, and staffing in another culture (Shenkar et al., 2008). For example, firms can improve their communication by being more open and transparent, they may enhance acculturation by education and training, they can strengthen socialization by gaining knowledge of another country's social norms, and they may improve staffing by selecting expatriates who are familiar with the other country's culture (Luo & Shenkar, 2011). Building on the cultural friction perspective, I theorize that previous IJV experience is a main mechanism that serves as a lubricant for firms to bridge and manage CD.

International management theories have long viewed past experience as one of the most important mechanisms that help firms learn about culturally distant countries and bridge CD (e.g., Barkema, Shenkar, Vermeulen, & Bell, 1997; Johanson & Vahlne, 1977). Firms tend to draw inferences from past experiences and store the inferred material for future use (Chen, Wang, Cui, & Li, 2021; Levitt & March, 1988). In the context of IJVs, a focal firm can learn from its joint venture experience in a given country and assess what went well and what did not (Shenkar & Li, 1999). Building on this assessment, the focal firm may then improve its approach when establishing an IJV in that country again. In particular, a firm that has encountered difficulties in the past can build on its previous experience and improve its cross-cultural communication by increasing its openness and transparency, which are considered prerequisites for interactional and informational justice in the cross-cultural setting (Luo, 2001), toward its partner firm. Furthermore, firms may decide to facilitate acculturation of their executives and staff by implementing cross-cultural trainings that help them better understand and adjust to the other culture (Black & Mendenhall, 1990). In addition, firms can enhance socialization, which bolsters interfirm trust, attachment, and mutual support, which, ultimately, constrain the adverse effects of cultural differences (Luo & Shenkar, 2011). Moreover, firms may optimize their staffing decisions in subsequent international engagements by selecting managers that are familiar with another country's culture.

However, experience does not always benefit firms (Alcácer, Dezső, & Zhao, 2013; Zeng, Shenkar, Lee, & Song, 2013). While firms can use experience to learn how to become better at clearly defined problems, they may also draw erroneous inferences and, for example, oversimplify experiences that are not fully applicable to a new situation (Haleblian & Finkelstein, 1999; Zollo, 2009). Thus, I distinguish between the types of IJV experience to study their influence on the relation between CD and market reaction to a focal firm's IJV announcement. In particular, I account for the level of success of prior experience, due to its critical effect on organizational learning (Hayward, 2002; Madsen & Desai, 2010).

Experiencing small failures. A firm's IJV experience in a culturally distant country that resulted in small losses can help improve the firm's ability to manage the effects of CD in that country, since small losses stimulate the search for better approaches and, thus, reveal errors made in the past (Hayward, 2002). That is, if a firm performed slightly below its expectations or barely missed its goals, it will try to assess the situation and identify the mistakes it made in dealing with CD, since there seems to be very little missing for the firm to achieve positive results the next time around (Staw, 1981). Building on its assessment, the firm can then address its flawed approach through targeted communication, acculturation, socialization, and staffing measures that help it better deal with CD's influence.

For instance, a firm from an individualistic society may recognize that it has encountered challenges in communicating with firms from collectivistic cultures. Thus, the firm can consciously attempt to increase its openness and transparency in order to facilitate better communication in the future. A firm may also realize that implementing or improving cross-cultural trainings for executives and staff can help it better deal with cultural differences in IJV relationships. Moreover, a firm might conclude that managers without cross-cultural experiences were unable to deal with cultural differences properly. The firm may improve its staffing decisions by emphasizing the selection of executives with experience in the host country culture. As a result, these firms can improve interaction and negotiation with a partner firm from a culturally distant country or better leverage the unique resources of the IJV in order to develop more innovative products and solutions next time. Therefore, a firm that has encountered small failures in the past tends to carefully analyze its past approach and develop superior ones that it can apply in the future (Ariño & De La Torre, 1998; Tsang, 2002). I theorize the following:

Hypothesis 4: The number of small losses incurred in prior IJVs by the firm positively moderates the effect of CD between (a) the focal firm's and the partner's home countries, (b) the focal firm's and the IJV's home countries, and (c) the partner's and the IJV's home countries on the market reaction to a focal firm's IJV announcement.

Experiencing large failures and successes. A firm that experienced both gains and large losses in a country is often less able to draw correct inferences from its experience. Successful experiences promote “satisficing,” which stifles the search for new solutions, since firms tend to rest on their laurels and do not see the need to change their past approach, in line with the proverb “Don't change a winning team” (Cyert & March, 1963; Madsen & Desai, 2010). Thus, when firms have been successful in establishing IJVs in the past, they likely do not investigate carefully what they can do to improve their IJV approach or adapt it to different circumstances in order to better deal with CD's impact in the future. As a result, these firms often reuse their previous approach but overlook nuances and unique circumstances in dealing with CD, which leads to less successful IJV outcomes in future IJVs.

Very unsuccessful experience also prevents the search for better approaches, because major failures tend to involve greater complexity, which is a key contributor to causal ambiguity (Konlechner & Ambrosini, 2019; Reed & DeFillippi, 1990). Thus, firms are less able to identify the causes and effects that led to large failures. In addition, firms tend to attribute such painful failures to unique circumstances that are not worth any further or detailed investigation (Desai, 2015; Ford, 1985). Rather than trying to understand the underlying reasons for such painful events, firms often blame them on specific managers’ lack of competence, the partner firm's inability, or the unfortunate circumstances surrounding the event (Hayward, 2002; Kelley, 1972). As a consequence, firms miss out on the opportunity to genuinely learn about the actual reasons behind their failures and about CD's role in potentially contributing to such failures.

In both situations, firms do not develop the correct learning and do not adapt their communication, socialization, acculturation, or staffing decisions. Even worse, they may become overconfident and less cautious of cultural differences after having had success in the past; they may also worsen their staffing decisions after having experienced great failures by removing managers that have gained valuable experience that can help them manage CD. Hence, these firms will derive erroneous inferences that negatively influence CD's impact on IJV success, thereby drawing unfavorable market reactions to a firm's IJV announcement. I propose the following:

Hypothesis 5: The number of gains and large losses incurred in prior IJVs by the firm negatively moderates the influence of CD between (a) the focal firm's and the partner's home countries, (b) the focal firm's and the IJV's home countries, and (c) the partner's and the IJV's home countries on the market reaction to a focal firm's IJV announcement.

Figure 2 shows the research model.

Research Model

Methodology

I collect a sample of IJVs from the SDC Platinum database. I include all IJVs from the database that involve two parents, that is, the focal firm and the partner firm, and one IJV country. I remove all observations involving three or more parents or those with IJVs that operate in more than one home country, since CD cannot be unequivocally calculated for those cases. I also remove significant confounding events within the 3-day event windows around IJV announcements that may affect stock market reactions to announcements, such as other IJV or mergers-and-acquisitions (M&A) announcements. Since value creation in joint ventures is not necessarily symmetric for both parent firms, I do not randomly designate one of the parents as the focal firm but instead include each IJV announcement twice, that is, once for each parent as the focal firm, where data were available for the respective firm.

My final sample consists of 709 observations from 42 countries in the period 1985 to 2019. Of these observations, 316 involve a focal firm whose foreign partner is located in the same country as the IJV, while only 184 observations involve the opposite situation, that is, a focal firm that is located in the IJV's home country. The different numbers suggest that only 184 of the 316 IJVs were established between two public parent firms. Furthermore, 102 observations involve two parents that are from the same home country and that established an IJV in a different country abroad, while 107 observations involve a focal firm, partner firm, and IJV that are each located in different countries. Table 1 reports the 42 countries.

Home Countries

Note: The numbers for focal and partner firms are not identical, because international joint ventures involving a public and a private parent can be included only once in the sample.

Dependent Variable

Cumulative abnormal return (CAR). I employ established event study methodology to calculate the focal firm's CAR, which measures the market reaction to events (McWilliams & Siegel, 1997; Zachary, Connelly, Payne, & Tribble, 2021). CAR is an ex ante market-based measure of expected returns and has been widely used to assess value creation of joint ventures (e.g., Kalaignanam, Shankar, & Varadarajan, 2007; Kumar, 2010). The methodology is based on the efficient market hypothesis and provides an estimate of the corporate cash flow implications of parent firms’ IJV decisions (Reuer, 2000). CAR is suitable for my research context, since information on culture and CD is publicly available while market investors access relevant public information to help them evaluate different aspects of joint ventures (Reuer & Koza, 2000). I obtain daily stock prices for the focal firm around the announcement date, t0, and use a standard market model to calculate CAR (Yang, Zheng, & Zaheer, 2015):

Independent Variables

CD. I use the widely used Kogut and Singh (1988) index to calculate the CD measures: CD (focal-partner) measures the CD between the focal firm's and the partner firm's home countries, CD (focal-IJV) captures the CD between the focal firm's and the IJV's home countries, and CD (partner-IJV) captures the CD between the partner firm's and the IJV's home countries. The index aggregates cultural differences along Hofstede’s (2001) four dimensions, that is, power distance, uncertainty avoidance, individualism, and masculinity:

While the widely used Kogut and Singh index has received serious criticism (Shenkar, 2001; Tung & Verbeke, 2010), using it in this study is appropriate, as doing so allows for comparability with prior work, whose conflicting findings I attempt to reconcile (Zhu, Ma, Sauerwald, & Peng, 2019). Nevertheless, I also use Ronen and Shenkar’s (1985, 2013) cluster approach in order to test the robustness of my results.

Small losses in prior IJVs. To measure small losses in prior IJVs in a given country, I follow Hayward’s (2002) approach and count the number of times a focal firm (for Hypotheses 4a and 4b) or partner firm (for Hypothesis 4c) has recorded an IJV announcement loss of less than 3% prior to a focal IJV announcement in that country, measured by CAR as discussed earlier. For example, if a firm has engaged in five IJVs before a focal IJV announcement and has incurred stock market returns of +4%, +3%, −1%, −2%, and −5%, respectively, then the variable would take the value 2 (for the losses of −1% and −2%). This measure captures the market's view that the announced IJV was a small mistake and likely affects firm managers, since firm managers tend to follow the market's reaction to their firm's activities and announcements. I also included alternative cutoff thresholds of 2% and 4%, and I obtained robust results.

Gains and large losses in prior IJVs. In line with the previous variable, I measure gains and large losses in prior IJVs by counting the number of times a focal (for Hypotheses 4a and 4b) or partner firm (for Hypothesis 4c) has recorded either an IJV announcement gain, that is, a positive abnormal return, or an IJV announcement loss of more than 3% in a given country before a focal IJV announcement. In the previous example of a firm with five IJVs prior to a focal IJV announcement, the variable would take the value 3, due to the two IJVs with stock market gains of +4% and +3% and the large loss of −5%. I again used alternative cutoff thresholds of 2% and 4% and obtained similar results.

Control Variables

I include various control variables to rule out confounding factors that may affect abnormal returns to IJV announcements. I first add the variable equity stake, which measures the percentage equity held by the focal firm, because it can affect the partners’ vulnerability to each other's opportunistic actions (Luo & Park, 2004). I include a dummy, industry relatedness, by comparing the two-digit Standard Industry Classification (SIC) codes of both parents; the dummy has a value of 1 if the parents share the same two-digit SIC codes (C. Li, Brodbeck, Shenkar, Ponzi, & Fisch, 2017). Industry relatedness facilitates the transfer of competencies, technologies, and routines (Lu & Xu, 2006). I obtain data from SDC Platinum. I also enter a focal firm's number of employees and the number of the partner's employees, which are proxies for the size of the parents and their human capital (Bu & Wagner, 2016; Lyles & Baird, 1994). In addition, I add the focal firm's return on assets and its partner's return on assets, since strong past performance of the parents can help stabilize the IJV (Pan & Chi, 1999; Shi & Tang, 2015). Data are from Datastream. Further, I enter a dummy variable that indicates whether the IJV involves technology transfer. I collect the data from SDC Platinum.

I also add the difference in GDP per capita and political risks between the parents’ countries, which capture the economic contexts of the parents and their home country customers’ purchasing power and their political contexts, respectively (C. Li & Parboteeah, 2015; Reuer & Tong, 2005). I collect data from the World Bank and Henisz’s (2000) political constraint index, respectively. I further enter the geographic distance between the focal and partner firms’ home countries, since distant partners face challenges in coordination (Shaheer & Li, 2020; White, Fainshmidt, & Rajwani, 2018). Data are from Mayer and Zignago (2011). Moreover, I include two dummies that indicate whether the parents’ countries share a common legal origin or a common language, respectively, as sharing the same legal origin and language can facilitate communication (C. Li et al., 2017). Data on a country's legal origin are from La Porta, Lopez-de-Silanes, Shleifer, and Vishny (1999) and on its language are from Mayer and Zignago (2011). Finally, I include year, industry, and country fixed effects (Kalaignanam et al., 2007).

Method of Analysis

I employ multiple regression to study the impact of the explanatory variables on abnormal returns to IJV announcements. I include year, industry, and partner firm's home country dummies to account for unobserved heterogeneity. I further employ robust standard errors clustered by focal firms’ home countries. I also use alternative standard errors clustered by focal firms and the IJV's home country dummies, and I obtain similar results.

Results

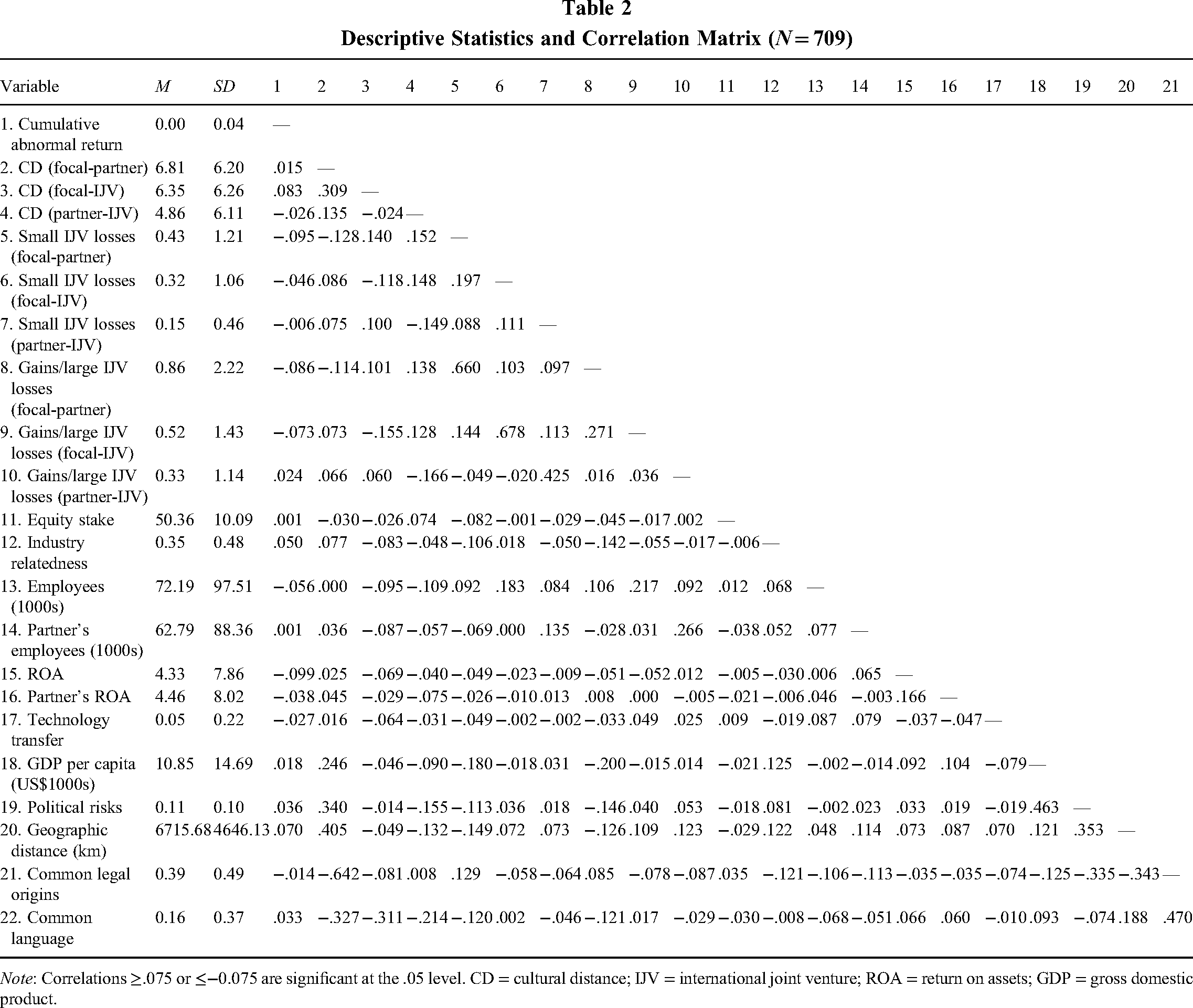

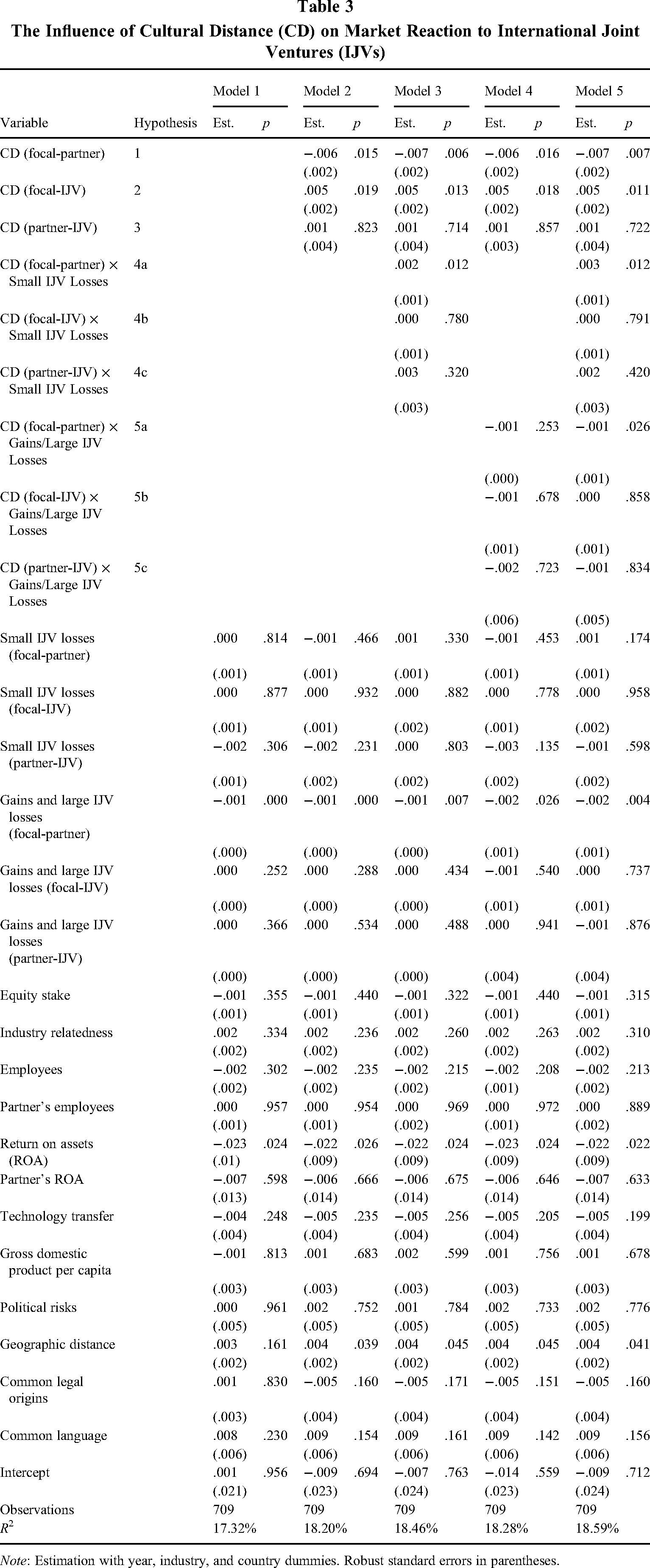

Table 2 reports the summary statistics and correlation matrix. Variance inflation factors are less than 2.6 for all variables, indicating acceptable multicollinearity levels. Table 3 reports the regression results for the dependent variable, CAR. Model 1 includes only the controls. I hypothesize that CD between the focal firm's and the partner firm's home countries negatively affects market reaction to IJV announcements (Hypothesis 1), while both CD between the focal firm's and the IJV's countries and CD between the focal firm's and the IJV's countries positively affect market reaction (Hypothesis 2 and Hypothesis 3). I enter the three CD variables in Model 2. I also suggest that small losses in prior IJVs positively moderate the three relationships (Hypotheses 4a, 4b, and 4c). I include the interaction terms in Model 3. Last, I propose that gains and large losses in prior IJVs negatively moderate the three relations (Hypotheses 5a, 5b, and 5c), and I enter the interaction terms in Model 4. Model 5 is the full model.

Descriptive Statistics and Correlation Matrix (N = 709)

Note: Correlations ≥.075 or ≤−0.075 are significant at the .05 level. CD = cultural distance; IJV = international joint venture; ROA = return on assets; GDP = gross domestic product.

The Influence of Cultural Distance (CD) on Market Reaction to International Joint Ventures (IJVs)

Note: Estimation with year, industry, and country dummies. Robust standard errors in parentheses.

I find that CD between the focal firm's and its partner's home countries negatively influences CAR (p = .007), while CD between the focal country and IJV country positively influences CAR (p = .011). CD also has an economically meaningful impact on CAR. I multiplied the beta coefficients (b = −0.007 and 0.005) with the average market cap of the focal firms ($22.5 billion), and I find that focal firms will see the amount of value they obtain decrease by US$146 million on average for a one-standard-deviation increase in CD between the parent firms, and increase by US$116 million for a one-standard-deviation increase in CD between the focal firm and the IJV. CD between the partner country and IJV country does not exert a significant influence on CAR (p > .1). Thus, Hypotheses 1 and 2 are supported, while Hypothesis 3 is rejected.

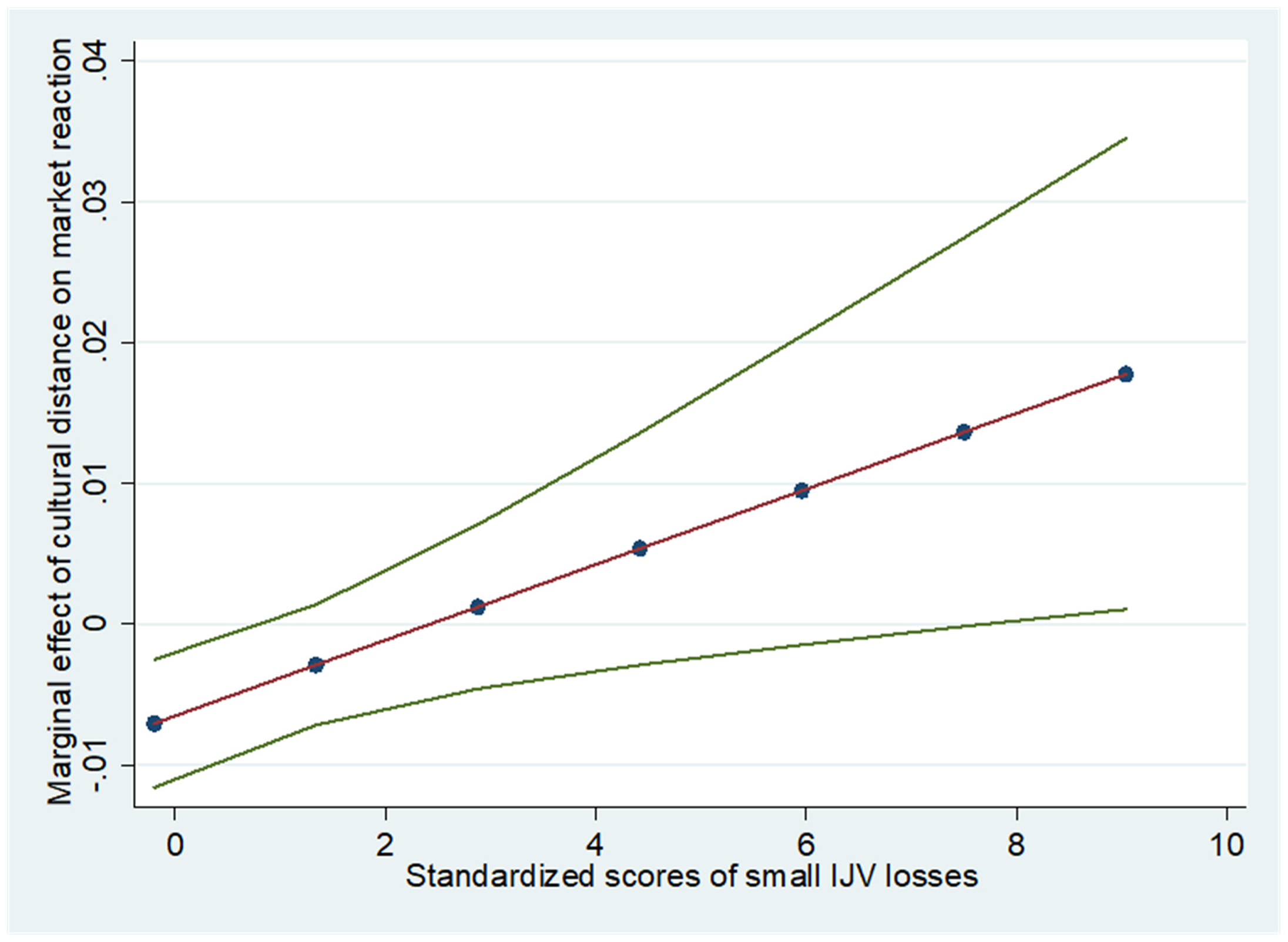

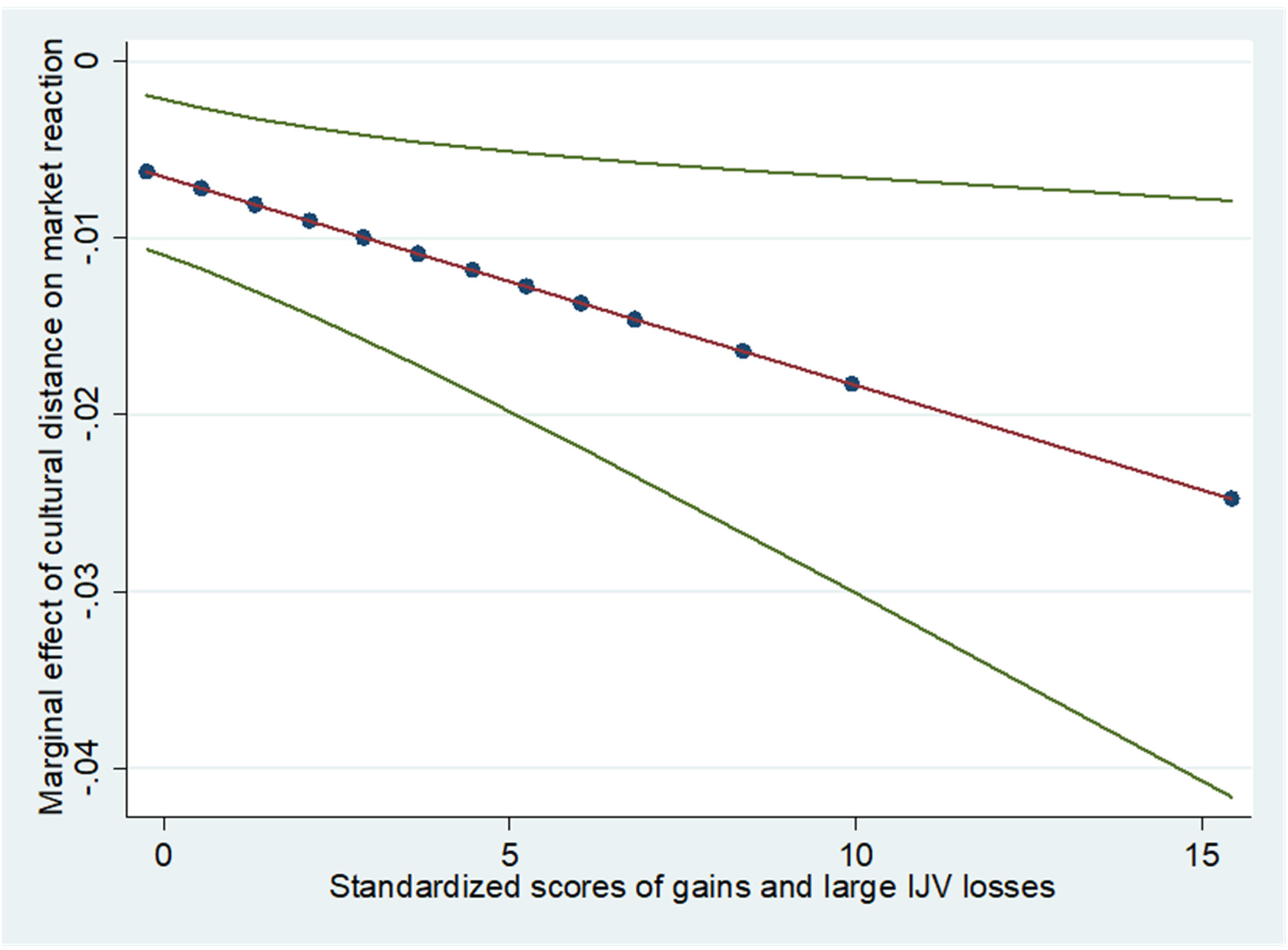

The interaction term between small losses in prior IJVs and CD between focal country and partner country is positive (p = .012). Figure 3 shows the marginal effects plot with 95% confidence intervals (Meyer, van Witteloostuijn, & Beugelsdijk, 2017). The two outer lines show the 95% confidence interval for the interaction line, which shows the marginal effect of CD on market reactions. The plot indicates that CD exerts a significant and negative influence on market reactions for low levels and a significant and positive influence for very high levels of experience. Thus, Hypothesis 4a is supported. This finding suggests that very experienced firms do more than simply try to avoid mistakes in cross-cultural interactions with their partner firms but are also able to develop creative solutions and approaches in the governance and management of the IJV by combining each parent's diverse resources that lead to favorable outcomes. The interaction term for CD between focal firm's and IJV's countries is negative and not significant. Hypotheses 4b and 4c are not supported. The interaction term between gains and large losses in prior IJVs and CD between focal firm's and partner's home countries is negative (p = .026) but insignificant in Model 4. Figure 4 displays the marginal-effects plot. The plot shows that CD exerts a significant and negative influence for all values of the moderator. Hypothesis 5a receives (weak) support. The interaction term involving CD between focal country and IJV country is positive and not significant. Hypotheses 5b and 5c are not supported.

Marginal-Effects Plot for Small International Joint Venture Losses (Cultural Distance Between Focal Firm and Partner Firm)

Marginal-Effects Plot for Gains and Large International Joint Venture Losses (Cultural Distance Between Focal Firm and Partner Firm)

Robustness Tests

I conduct various tests to examine the robustness of my results. First, I use N. Park’s (2004) approach to calculate an alternative specification of the dependent variable, CAR. N. Park suggests accounting for the global integration of equity markets, as stock returns for companies that significantly operate globally seem to be affected by international market activities. Thus, I follow N. Park's suggestion and I add Financial Times Stock Exchange World Index as the world market index and account for the change in foreign currency exchange rates to calculate CARs.

Second, I replace the main independent variable, CD, with several alternative specifications. I first replace Hofstede's cultural scores with GLOBE's cultural scores, which are theory driven and have been collected more recently (House, Hanges, Javidan, Dorfman, & Gupta, 2004). I then use Ronen and Shenkar’s (1985, 2013) cultural cluster approach to calculate CD. The cluster approach helps to overcome some of the hidden assumptions of the Kogut and Singh index, such as its assumption of equivalence, which equally emphasizes all cultural dimensions even though some dimensions may be more influential than others in a given context (Shenkar, 2001).

Furthermore, I include alternative measures for the moderators small losses in prior IJVs and gains and large losses in prior IJVs. More specifically, I first use variables that capture different time spans, as firms can retain knowledge from prior experiences for longer or shorter time spans than 5 years (Sampson, 2005). I also employ different cutoff points that are used to specify the threshold for (un-)successful prior experiences. In particular, I use 2% and 4%, respectively, instead of 3% (Hayward, 2002).

Moreover, I test for self-selection. I first examine self-selection with respect to foreign entry mode choice, since CD has taken a prominent role in the entry mode literature (Shenkar, 2001). I estimate a first-stage model for firm's selection of IJV versus nonequity alliance, and I use industry growth, that is, World Bank's retrospective 5-year growth rate in the partner country prior to entry, as the exclusion criterion (Wolfolds & Siegel, 2019). The instrument mimics the one used by Shaver (1998) and has been employed in prior work (Hennart & Park, 1993; Zejan, 1990). It also falls in line with transaction costs economics’ prediction of factors that determine foreign entry mode choice (Buckley & Casson, 1976; Luo, 2001). I then include the correction for self-selection in the second-stage model. The results of the robustness tests are very similar to the original but, at times, show weaker support for Hypothesis 4a, suggesting that firms account for some of the experience effects when deciding between joint ventures versus acquisitions. That is, firms may preemptively consider their previous experiences in their entry mode decisions, leading to weaker experience effects thereafter. Next, I study self-selection regarding partner choice by estimating a first-stage model for firm's selection of its IJV partner versus an industry peer of similar size that has engaged in an IJV in the IJV country in a given year. I again use industry growth as the exclusion criterion, since it affects the number of potential IJV partners. I then include the correction for self-selection in the second-stage model. The results are very similar to the original findings. The results of the robustness tests are available upon request.

Discussion

My work makes several theoretical contributions to research on CD in IJVs and beyond. First, it helps to resolve some of the inconsistent results on CD's influence on IJV success. While prior work in this area has made very valuable contributions, findings have revealed negative (e.g., Hennart & Zeng, 2002; Merchant, 2000), positive (e.g., S. Park & Ungson, 1997; Pothukuchi et al., 2002), and no significant relationships between CD and IJV success (e.g., Luo, 2002; Merchant, 2002). To shed light on these seemingly inconsistent results, I draw on the cultural friction lens to argue that CD can have both a negative and a positive influence on market reaction to IJV announcements. However, this influence fundamentally depends on whose CD is considered and the very nature and traits of the cultural carriers, point of contact, and exchange involved (Shenkar et al., 2008). By carefully examining and theorizing about the specific elements that underpin the interactions between the different organizations involved in IJVs, I show that CD between parent firms is detrimental to IJVs, since it hampers the coordination and negotiation between two autonomous organizations, whereas CD between focal parent and IJV is beneficial, as it helps pool diverse resources for parent and IJV. In so doing, my work reconciles the fundamental tension between the positive and negative influences of CD in IJV research.

Interestingly, CD between the partner firm and the IJV does not exert a significant influence on the focal firm's stock market reactions following IJV announcement. This finding might imply that greater CD between partner and IJV allows the partner to access unique resources and skills but does not necessarily mean these resources and skills are equally unique and valuable to the focal firm. Thus, the finding reinforces the notion that an important benefit from the CD between the focal parent firm and its IJV is the opportunity for the focal parent to gain access to a large and diverse pool of skills and resources from the IJV, which are embedded in the IJV's home country culture. In other words, the impact of CD between the partner and the IJV does not evoke significant market reactions to a focal firm's IJV announcement, because the focal firm does not benefit from the skills and resources that originate from the CD between partner firm and IJV the same way its partner firm does.

Further, this study offers a more complete picture of CD's impact on IJVs. Existing research typically has examined the home countries of the parent firms and, at the same time, relied on samples with “local partners” that are headquartered in the same country as the IJV (Merchant & Schendel, 2000; S. Park & Ungson, 1997). Thus, extant work has “pooled’ the negative influence of the CD between the parents and the positive influence of the CD between a focal parent and its IJV. Pooling these CDs mixes their opposing effects and, in doing so, neglects the various country constellations in IJVs (Makino & Beamish, 1998). By contrast, my work examines the different CDs individually and shows that doing so is critical for precise theory development and testing, as the cultural carriers, point of contact, and exchange involved in the focal-partner, focal-IJV, and partner-IJV relationships are inherently different.

More broadly, I advance research on CD in international management. International management research has typically relied on either the cultural familiarity premise—which suggests that differences in culture lead to negative outcomes (Lee et al., 2008)—or the opposite, positive organizational scholarship notion—which proposes that cultural differences can have synergistic effects (Stahl & Tung, 2015)—without discussing the other or why one assumption is more applicable to a given context. My research builds on the cultural friction perspective, which accounts for the cultural familiarity lens and positive organizational scholarship and shows that cultural carriers, point of contact, exchange, and mitigating mechanisms determine which theoretical lens is most relevant and for what reasons. Hence, my work illustrates the importance of nuanced and precise theory development in international management, in line with prior calls by other scholars that have criticized the implicit or explicit use of either the cultural familiarity or positive organizational scholarship lens without further explaining/justifying its application (Siegel et al., 2013; Tung & Verbeke, 2010), demonstrating the usefulness of the cultural friction approach for the international management field.

Finally, this study sheds light on the dual role of previous experience as both lubricant and obstacle to CD. International management research has long considered experience a central mechanism that helps firms bridge differences between countries, perhaps most notably within the Uppsala stage model (Johanson & Vahlne, 1977). However, experience can also be detrimental to firms (Haleblian & Finkelstein, 1999; Zeng et al., 2013). My study makes two main contributions to extant literature by revealing under what circumstances prior IJV experience can improve or worsen CD's influence on market reaction to IJVs. First, I show that small failures in the past can help firms better overcome CD's negative effect by encouraging them to reassess and improve their IJV approaches, whereas gains and large failures in the past amplify the negative impact of CD between focal firm and partner firm. Second, I find that experience affects neither the influence of CD between focal parent and IJV nor that of CD between partner firm and IJV on focal firm's market reaction to IJVs. This absence of influence suggests that firms may not adapt their approaches in dealing with CD when CD has a positive or insignificant effect, irrespective of the type of experience they have made in the past. Hence, my work offers nuance to the understanding of how failure affects learning in firms (e.g., Hayward, 2002; Madsen & Desai, 2010).

Managerial Implications

My article carries several managerial implications. Managers typically understand that CD can significantly affect their firms; however, they may not always be tuned to the differing effects of cultural differences. While CD can hamper interaction and collaboration between two autonomous firms with potentially diverging interests, such as the parent firms, practitioners need to recognize that CD can also help create value, such as in the parent-IJV relationship. Thus, managers can actively attempt to mitigate the destructive influence of CD while fostering its beneficial effect. One such means is by leveraging the previous experience of firms. Yet, executives need to be aware that their firms and employees tend to learn valuable lessons from minor mishaps in the past but derive erroneous learnings from positive or very negative experiences. Hence, they need to pay particular attention in situations involving the latter to help their firms and employees learn from positive and very negative experiences. For example, managers can introduce specific initiatives to help their firm systematically analyze why it has experienced great failures or successes in the past in order to understand the underlying and nuanced reasons for the outcomes and improve its approaches in the future.

Limitations and Future Research

This study also has limitations that provide avenues for future research. First, I measure the market reaction of IJV announcements using CARs. CARs reflect how the stock market evaluates the long-term cash flow implications of an event and, thus, should be strongly associated with the long-term performance of the focal firm (McWilliams & Siegel, 1997). However, previous work in the M&A context has revealed that abnormal returns are not always related to other long-term performance measures of firms, such as return on assets (Zollo & Meier, 2008). While this discrepancy could point to a fundamental difference between collective stock market reactions and the actual long-term performance implications of events, it could also be rooted in measurement issues, since long-term accounting measures can be distorted by confounding events and the different lengths of time it takes for an event to exert its performance influence. Hence, it could be interesting for future research to examine whether or to what extent investors’ collective and short-term interpretation of an IJV announcement is associated with the long-term performance of the focal firm.

Second, I use an aggregate conceptualization of the CD construct that combines differences in multiple cultural dimensions into one measure (Shenkar, 2001). While using an aggregate CD construct allows for comparability with previous findings and is consistent with the conceptual logic underlying my study, which captures CD in its entirety, assuming that all cultural dimensions are almost equally relevant for IJV outcomes is not always justified (Brock, Shenkar, Shoham, & Siscovick, 2008). For instance, the uncertainty avoidance dimension might be more relevant for knowledge transfer in IJVs, as uncertainty avoidance critically affects innovation and R&D activities of firms (Shane, 1995). Thus, I encourage scholars to disaggregate CD, where sensible, in order to study the influence of select cultural dimensions on specific IJV phenomena in the future.

Third, I cannot observe the underlying mechanisms and processes that determine CD's impact on IJV stock market reactions, in line with previous research. Thus, I built on the friction perspective to carefully develop my hypotheses. In particular, I argue that the exchange between parent firms mainly revolves around coordination activities, while the exchange between parent firm and IJV predominantly comprises the exchange of knowledge and resources. Arguing that CD has different effects in different contexts is key to the cultural friction perspective (Shenkar et al., 2008). Yet, I am unable to observe to what extent significant exchange of resources and coordination occurs between parent firms and between parent and IJV, respectively. Therefore, subsequent research could attempt to observe the underlying processes that determine the impact of CD on IJVs.

Fourth, I do not include IJVs with more than two parent firms, because I would need to include such IJVs as many times as there are parent firms, and doing so would inflate their influence disproportionately on the results. It would also be difficult to calculate an accurate CD measure if the other partner firms are located in different countries. Nevertheless, future research can consider accounting for IJVs with multiple parent firms, especially when the IJV's performance is being measured rather than the performance of its parent firms. Doing so can offer a more complete understanding of CD's role in IJVs and the coordination and communication hazard among multiple partner firms.

Fifth, I do not account for various other selection issues, even though I run a two-stage model to account for self-selection with respect to entry mode choice. Yet, there are other selection issues, such as the parent firm's choice to engage in foreign entry strategy in the first place or its selection to collaborate with a specific partner firm in a given country. These limitations may present interesting avenues for future research endeavors.

Conclusion

My work draws on the cultural friction perspective to examine CD's influence on market reaction to IJVs. I show that CD between parent firms tends to be destructive, while CD between focal parent and IJV is largely beneficial and CD between partner firm and IJV has no significant influence. Furthermore, the influence of CD between parent firms is also contingent on the focal parent's prior IJV experience, insofar as small IJV losses mitigate the negative influence of the CD between the parents, while gains and large losses in prior IJVs amplify its negative effect. My findings demonstrate the importance of not only having experience but also the type of experience in managing CD in IJVs. My study opens new research avenues that help to connect cultural differences, experiential learning, and international collaborations.