Abstract

Understanding why some firms outperform others is central to strategy research. The resource-based view (RBV) suggests that competitive advantages arise due to possessing strategic resources (i.e., assets that are valuable, rare, nonsubstitutable, and inimitable), and researchers have extended this logic to explain performance differences. However, RBV is relatively silent about the actions managers could use to create or capitalize on a resource-based advantage. Enriching RBV, the resource orchestration framework describes specific managerial actions that use such resources to realize performance gains. After reviewing the conceptual evolution of these two literature streams as well as related streams, we use meta-analytic structural equation modeling to aggregate evidence from 255 samples involving 111,120 observations to answer outstanding research questions regarding the strategic resources–actions–performance pathway. The results show strong complementarity and interdependence between their logics. Additional inquiry drawing on their complementarity is a clear path toward enhancing scholars’ understanding of how and why some firms outperform others. We build on our findings to lay a foundation for such inquiry, including a call for theorizing centered on the interdependence of resources and actions, as well as new theoretical terrain that can help resource-based inquiry continue to evolve.

Keywords

Building knowledge about why some firms outperform others remains a central goal of strategic management research (Nag, Hambrick, & Chen, 2007). Over the past three decades, the resource-based view (RBV), formally introduced by Jay Barney in his 1991 Journal of Management (JOM) article, has been one of the most influential perspectives fueling progress toward this goal (Armstrong & Shimizu, 2007; Nason & Wiklund, 2018). Following formative steps by Penrose (1959), Wernerfelt (1984), and others, Barney (1991) delineated RBV by defining the key attributes that make resources “strategic” (Chi, 1994: 271)—that is, valuable, rare, inimitable, and nonsubstitutable—and highlighting their role in helping firms attain sustained competitive advantage. Given the difficulty of measuring competitive advantage, most subsequent studies assess strategic resources’ performance effects instead under the assumption that competitive advantages will confer performance advantages.

Barney (1991: 99) claimed that firms need to “exploit,” or use, the strategic resources they possess, yet his formulation of RBV did not describe the nature of these actions, and much of the empirical testing of RBV’s claims examines possible direct links between strategic resources and performance (Armstrong & Shimizu, 2007; Nason & Wiklund, 2018). Over a decade ago, a meta-analysis by Crook, Ketchen, Combs, and Todd (2008) quantified and supported this direct link yet concluded that “much work remains before theory can map out the many contingencies” (p. 1152) and choices that shape the nature of the resource-performance relationship. Indeed, as theorizing related to RBV evolved, the focus on a direct resource possession–performance relationship has been scrutinized. In a review of critiques leveled against RBV, Kraaijenbrink, Spender, and Groen (2010: 355) noted, “The possession of strategic resources is not sufficient, and it is only by being able to deploy these that [competitive advantage] can be attained.”

To bring attention to these intervening processes, Sirmon, Hitt, Ireland, and Gilbert (2011) integrated insights on resource management actions, grounded in the RBV tradition (Sirmon, Hitt, & Ireland, 2007), with insights on asset orchestration, grounded in dynamic capabilities (Helfat et al., 2007). In doing so, they introduced the resource orchestration framework (RO) and delineated orchestration actions (i.e., structuring, bundling, and leveraging) as key links through which strategic resources are used to realize the performance effects of resource-based advantages. Although the importance of such actions was mentioned in general terms in foundational work (e.g., firms need to “use different kinds of resources and processes . . . to undertake activities”; Penrose, 1959: 73), this was subsequently downplayed. Thus, RO contributed to resource-based inquiry by detailing resource-use processes and the importance of their synchronizing orchestration actions. Since then, RO has become prevalent in research on the links among strategic resources, actions, and performance.

While reviews for each literature stream exist, they stand apart (e.g., Barley, Treem, & Kuhn, 2016; Crook et al., 2008; Helfat & Martin, 2015; Nason & Wiklund, 2018). We contend, however, that a rich integration of these two streams’ logics would provide strong underpinnings to advance resource-based logic (Barney, Ketchen, & Wright, 2011). Thus, we first offer a conceptual integration of RBV and its focus on resource possession with RO and its focus on orchestration actions (i.e., what we dub resource use) to assess the state of knowledge surrounding strategic resources. This approach provides an evolutionary view of resource-based logic over time as we trace the development of resource use alongside resource possession in the intellectual lineage of resource-based inquiry.

Second, we assess our conceptual integration using meta-analytic structural equation modeling (MASEM) to synthesize evidence from 255 samples involving 111,120 observations. MASEM can aggregate large bodies of evidence and account for statistical artifacts, like sampling error, that can be problematic in single studies (Bergh et al., 2016; Cheung, 2021). MASEM is uniquely suited to the goals of this review and conceptual integration in that it enables the testing of webs of relationships that are rarely tested in a single study. We use MASEM to test the strategic resources–orchestration actions–performance pathway. This effort reflects questions regarding the merit of our integration, such as the following: (a) To what extent do strategic resources enable orchestration actions? (b) How do orchestration actions affect the nature of the strategic resources–firm performance relationship? and (c) How does synchronization among orchestration actions further change the nature of this relationship?

Overall, we seek to provide two contributions that build on each other. First, we develop an integrative conceptual model that leverages insights from both RBV and RO. This model offers researchers interested in explaining performance differences between firms an overarching framework depicting how orchestration actions, and their synchronization, link strategic resources and firm performance. Important in this effort is tracking the evolution of resource-possession and resource-use logics within resource-based inquiry and related streams of research (i.e., capabilities). Kraaijenbrink et al.’s (2010: 366) assertion that RBV’s “focus on the possession of resources” makes its conceptual insights “inherently static [and] not well equipped to explain” how resources affect competitive advantage creates a temptation to view RO as a potential replacement for RBV. By delineating how work on RO has, in many ways, returned resource-based thinking to its origins, we develop the idea that RO is not an alternative perspective of firm performance that could displace RBV, but rather, it provides a valuable specification of the processes through which strategic resources affect performance.

Second, building on this model, we provide strong empirical evidence, via MASEM, regarding the integration of RBV and RO. Specifically, we see that although strategic resources matter, performance differences are more based on interdependencies between the possession and use of strategic resources. In other words, the resources a firm possesses and the actions it takes to use them are jointly important determinants of performance advantages. While such interdependence has been argued and some work has addressed various interdependencies in limited ways, our study offers the first broad and comprehensive test of both resource-possession and resource-use logics as well as nuanced comparative tests that rule out alternative relationships, thereby providing increased confidence in the model. Together, these contributions take stock of the complementarity of RBV and RO and provide a foundation to propose new directions for future research. Thus, we build on our findings to lay a foundation for such inquiries, including a call for theorizing on the interdependence of resources and actions, as well as new theoretical terrain that can help resource-based inquiry continue to evolve.

Possession and Use in the Evolution of Resource-Based Inquiry

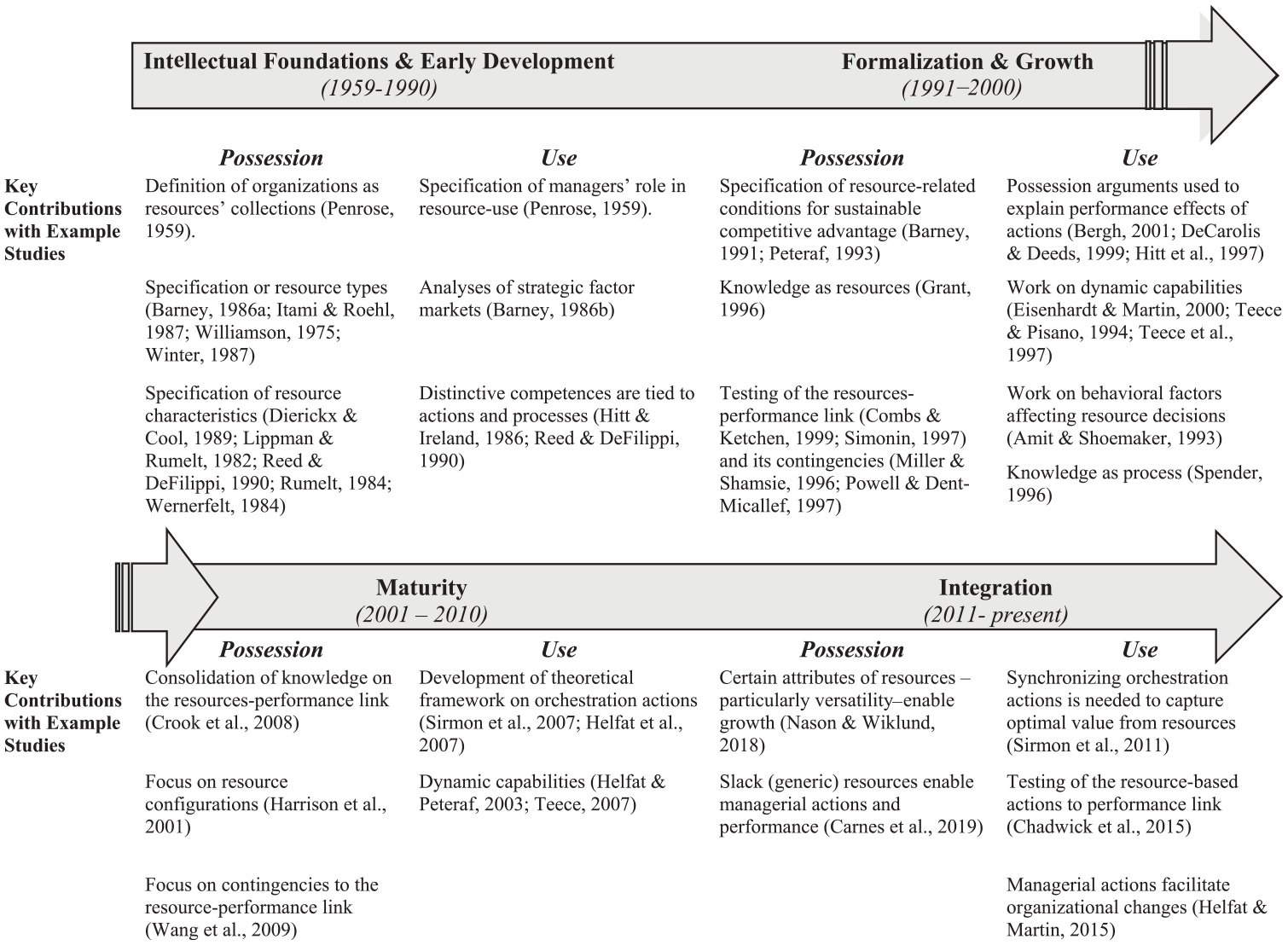

We briefly review the stages of resource-based logic to trace the evolution of the focus on resource possession and resource use. In so doing, we uncover that (a) in its early development, resource-based logic involved both resource possession and resource use; (b) in its formalization and subsequent growth stage, conceptual developments and inquiry proceeded with a strong focus on resource possession while providing only implicit recognition of the importance of resource use; (c) in its maturity stage, inquiry was primarily focused on resource possession, but recognition and meaningful research of resource use commenced; and (d) in the latest stage, theorizing and inquiry have become more focused on resource use. We depict these stages, and some of the major contributions that fueled them, in Figure 1. We then highlight the outstanding questions derived from our review.

Evolution of Resource-Possession and Resource-Use Theorizing

Intellectual Foundations and Early Development (1959–1990)

RBV’s intellectual foundations are often traced to Penrose’s (1959) The Theory of the Growth of the Firm, wherein she described firms as collections of “productive resources” (p. 24) that enable or constrain growth. Yet, her work also outlined elements of resource-use logic by describing the key role that managers play in cultivating and deploying resources. Although a firm is the collection of the resources it possesses, its primary function is to use those resources for the production of good and services. Thus, Penrose is often credited for her recognition that firms achieve success not only because they have resources but also because they use them for productive means. As such, this foundational work focused on resource possession and use not as distinct elements but rather as an interconnected conceptualization of firms and how they function in society.

Through RBV’s early development in the 1980s, both resource possession and use played key roles. For instance, attention was given to the importance of possessing specific resources, for example, physical capital (Williamson, 1975), organizational culture (Barney, 1986a), knowledge (Winter, 1987), and invisible assets (Itami & Roehl, 1987). Also, strides were made in identifying the characteristics that make resources a source of competitive advantage (e.g., Barney, 1986a). Specifically, this work highlighted isolating mechanisms (Rumelt, 1984) that allow firms to avoid the dissipation of advantages generated by their resource endowments, for example, time compression diseconomies, interconnectedness, mass efficiencies (Dierickx & Cool, 1989), and causal ambiguity (Dierickx & Cool, 1989; Lippman & Rumelt, 1982; Rumelt, 1987) generated by resource tacitness, complexity, and specificity (Reed & DeFilippi, 1990). In this view, firm resources are important if they create a barrier to other firms seeking to imitate them, especially when those resources and the strategies they enable serve as a basis of a competitive advantage (Lippman & Rumelt, 1982; Reed & DeFilippi, 1990; Rumelt, 1984, 1987; Wernerfelt, 1984).

However, during this period, resource use was also given attention. For example, the notion of a distinctive competence—defined as “a firm’s ability to complete an action in a manner superior to that of its competitors or to apply a skill that competitors lack” (Hitt & Ireland, 1986: 402)—was identified as critical to firm success. Moreover, attention was given to strategic-factor markets (Barney, 1986b) and the role that managers take to structure their resource portfolio. Although this is not to say resource use was well developed during this stage, these efforts began to highlight actions and processes as important for firm success (Hitt & Ireland, 1986; Reed & DeFillippi, 1990).

Viewed broadly, although the focus of this foundational work was on resource possession, it maintained the importance of resource use. As Rumelt (1984: 557) put it, a “firm’s competitive position is defined by a bundle of unique resources” and “the task of general management is to adjust and renew [them] as time, competition, and change erode their value.” Yet, within this period, declarative statements, such as “strategic choices should flow mainly from the analysis of its unique skills and capabilities” (Barney, 1986b: 1231), may have fostered a stronger focus on resource possession during the next stage of development in resource-based logic and inquiry.

Formalization and Growth (1991–2000)

A 1991 JOM special forum marked the formalization of RBV and, building on previous contributions regarding resource types and characteristics, yielded a new stage with a more decisive focus on resource possession. Although the forum offered several notable contributions (e.g., Conner, 1991; Harrison, Hitt, Hoskisson, & Ireland, 1991), Barney’s (1991) article is widely credited for formalizing RBV (cf. Barney et al., 2011). Here, he integrated prior work to formalize assumptions about the nature, types, and attributes of resources that allow firms to create sustained competitive advantages. Specifically, Barney (1991: 101) defined resources as the assets “controlled” by a firm and outlined that resources are heterogeneously distributed across firms and are costly to transfer. He specified three resource categories: physical (e.g., plant and equipment), human (e.g., managers’ and workers’ attributes), and organizational (e.g., structures and technologies). Perhaps Barney’s (1991) most leveraged insight was that resources that are valuable, rare, inimitable, and nonsubstitutable can enable sustainable competitive advantage. Augmenting the formalization provided by Barney’s (1991) work, Peteraf (1993: 183) clarified that “sustained competitive advantage requires that the condition of [resource] heterogeneity be preserved” through ex ante and ex post limits to competition as well as imperfect resource mobility. Thus, building on foundational work (e.g., Barney, 1991; Dierickx & Cool, 1989; Lippman & Rumelt, 1982), Peteraf provided a formal framework of the cornerstones of competitive advantage within resource-based logic.

Following this formalization, the field witnessed a proliferation of inquiry into the performance implications of resource possession. Researchers began to test the performance effects of different types of resources, such as reputation (Combs & Ketchen, 1999), experience (Simonin, 1997), technical competence (Henderson & Cockburn, 1994), and physical assets (Miller & Shamsie, 1996), among many others. Potential contingencies to the resource–performance relationship, such as environmental uncertainty (Miller & Shamsie, 1996), were addressed as was the role of complementarity in resource endowments (Powell & Dent-Micallef, 1997).

Alongside the dominant focus on resource possession, a few impactful efforts delved into resource use. First, work coalesced around a dynamic-capability view. Focusing attention on the capabilities firms need in changing environments (Teece & Pisano, 1994), proponents of this view suggested that under certain conditions (e.g., in highly competitive environments), core competencies can become core rigidities (Leonard-Barton, 1992). Thus, attention should be devoted to the capabilities that allow firms to gain and maintain competitive advantage in such environments. Dynamic capabilities was defined as processes within firms by which managers integrate, build, and reconfigure internal and external competences to address changing environments (Eisenhardt & Martin, 2000; Teece, Pisano, & Shuen, 1997). Second, some limited interest emerged around behavioral aspects affecting managerial decisions regarding resources and capabilities. For example, Amit and Shoemaker (1993: 44) leveraged insights from RBV and behavioral decision theory to build an understanding of the “managerial difficulty of identifying, developing, and deploying” resources and on the role that these managerial decisions have in determining heterogeneity in resource endowments. Their work represents a formative step toward more focus on resource use. Third, the knowledge-based view (KBV; Grant, 1996) emerged to describe the role that explicit and implicit knowledge have in creating value for organizations. Collectively, proponents of KBV leveraged resource-based thinking, organizational learning, and dynamic capabilities to point out the importance of knowledge as firm resource and of the processes associated with it, that is, sourcing, internal and external transfer, and integration (DeCarolis & Deeds, 1999; Eisenhardt & Santos, 2002). Last, research investigated the effect of resource possession on the relationship between performance and resource-use decisions, such as divestitures (Richard, 2000), acquisitions (Bergh, 2001), alliances (DeCarolis & Deeds, 1999), and diversification (Geringer, Tallman, & Olsen, 2000; Hitt, Hoskisson, & Kim, 1997), which effecitvely change the portfolio of resources available (i.e., structuring in RO). It is important to note that these studies did not focus theoretical attention on resource-use processes, yet they implicitly acknowledged the relevance of actions in the creation of potential value.

Maturity Stage (2001–2010)

The 2000s saw continued focus on resource possession but increased attention on resource use. The former included investigations of the performance effects of reputation (Roberts & Dowling, 2002); financial (C. Lee, Lee, & Pennings, 2001), social (Choi & Wang, 2009), and human capital (Hatch & Dyer, 2004); and organizational culture (Carmeli & Tishler, 2004). In a reflection of reaching maturity, meta-analytic evidence supported a relationship between the possession of strategic resources and firm performance (Crook et al., 2008). Attention also was given to resource configurations—with specific consideration of the effects of resource complementarity (Adegbesan, 2009; Harrison, Hitt, Hoskisson, & Ireland, 2001)—and to the contingencies that shape the nature of the resource possession–performance relationship (e.g., Barthélemy, 2008; Wang, He, & Mahoney, 2009).

As another mark of maturity, critiques of RBV became more explicit (cf. Kraaijenbrink et al., 2010). For instance, Priem and Butler (2001a) raised questions about whether the RBV’s theoretical logic was useful. At issue was how Barney (1991) described resource value. Priem and Butler (2001b: 58) observe that “the RBV statement ‘if a resource is valuable and rare, then it can be a source of competitive advantage’ is necessarily true by logic (i.e., a tautology) if ‘valuable’ and ‘competitive advantage’ are defined in the same terms.” They further commented that if value is defined as “increasing efficiency and/or effectiveness, and competitive advantage is defined as achieving increases in efficiency and/or effectiveness, a tautology exists” (Priem & Butler, 2001b: 58).

Barney (2001: 46) responded to this criticism by highlighting that the attributes that make resources “strategic” and are at the core of RBV formulation, including value, are parameterized in ways that can generate testable hypotheses. In line with this reasoning, he noted that “some studies found results that are inconsistent with resource-based expectations,” and “contrary empirical results would certainly not be possible if RBV in general and the 1991 argument in particular were purely tautological” (Barney, 2001: 46). Moreover, Peteraf and Barney (2003: 320) later explained that “while RBV is concerned with performance differentials, our frameworks (Barney, 1991; Peteraf, 1993) are most useful for identifying resource-based indicators of a potential for greater profitability,” highlighting the importance of “a variety of other intervening factors.” Addressing these intervening links appears important in attenuating the tautology concerns that have long been an issue.

Recognizing the need for a more complete picture of factors that intervene between possessing resources and performance, more work began to specify actions that firms can take to use their strategic resources. First, researchers attempted to distinguish more clearly and directly between resources and capabilities as related, but independent, research streams. Whereas a resource is defined as an asset that an organization owns, controls, or has access to on a semipermanent basis (Helfat & Peteraf, 2003), a capability is the ability of an organization to perform a coordinated set of tasks, using resources, to achieve particular goals (Barney, 2001; Helfat & Peteraf, 2003). This distinction provided grounding for more explicit recognition of the role of dynamic capabilities for the attainment of sustainable advantages (Teece, 2007). Collectively, this work advanced the understanding that a firm can achieve competitive advantage when it possesses value-generating resources and it employs them in uncommon ways (Peteraf & Barney, 2003). Indeed, research began to more directly show that what a firm does with its resources is at least as important as which resources it possesses (e.g., Haas & Hansen, 2005; Hansen, Perry, & Reese, 2004; Sirmon, Gove, & Hitt, 2008).

During the maturity stage, frameworks focused on specifying resource-based managerial actions flourished. Specifically, two main theoretical frameworks regarding resource use emerged: resource management (Sirmon et al., 2007) and asset orchestration (Helfat et al., 2007). Resource management (Sirmon et al., 2007) portrays three specific types of action—structuring, bundling, and leveraging—through which firms capture the value of their strategic resources. Structuring refers to the “management of the firm’s resource portfolio,” such as by acquiring resources from strategic factor markets as well as accumulating and divesting resources (Sirmon et al., 2007: 277). Bundling refers to actions that integrate resources to develop capabilities, such as making incremental improvements to existing resource stocks, extending resources to keep them up to date, and bringing together existing and new resources (Sirmon et al., 2007). Leveraging refers to the processes used to deploy the firm’s resources; this involves identifying and designing ways to exploit resources and then coordinating efforts to implement them in unique ways (Sirmon et al., 2007). While each type of action was theorized to be important individually, synchronization across the actions took center stage in Sirmon et al.’s (2007) theorizing. Similarly, asset orchestration logic involves two managerial processes: search/selection and configuration/deployment of resources (Helfat et al., 2007). The former consists of identifying strategic assets, investing in them, and designing organizational and governance structures to create a business model (Helfat et al., 2007). The latter consists of coordinating assets, providing a vision for those assets, and nurturing innovation (Helfat et al., 2007).

In general, these important theoretical developments provided fertile ground for relevant empirical research (e.g., Sirmon et al., 2008). On the one hand, research focused more directly on investigating the effects of resource-based managerial actions on firm performance (Cording, Christmann, & King, 2008; Gruber, Heinemann, Brettel, & Hungeling, 2010; Morrow, Sirmon, Hitt, & Holcomb, 2007). On the other, researchers began to investigate the idea that configurations of actions (not only of resources) may play an important role in creating competitive advantages. For example, Sirmon and Hitt (2009) investigated the contingent nature of resource investment and deployment decisions showing that synchronization between such decisions is important for firm performance.

Integration Stage (2011–Present)

In 2011, Barney et al. noted that the RBV had matured and wondered about its future. A major source of progress has been RBV’s conceptual integration with resource-use frameworks developed during the maturity stage (i.e., Helfat et al., 2007; Sirmon et al., 2007). Indeed, although some research in the current stage investigates how certain attributes enable stronger performance (e.g., Nason & Wiklund, 2018), today’s work adopts a markedly stronger focus on integrating resource possession and use than did work in the maturity stage (e.g., Ndofor, Sirmon, & He, 2011).

From a conceptual perspective, Sirmon et al. (2011) advanced RO by integrating insights from their work on resource management actions (Sirmon et al., 2007) and insights from Helfat et al.’s (2007) work on asset orchestration. In doing so, they promoted the need for a focus on “how managers affect resource-based competitive advantage” (Sirmon et al., 2011). The development of the RO framework spawned research focused on testing its claims, implicitly or explicitly. For example, researchers investigated the effect of human resource management practices (Chadwick, Super, & Kwon, 2015; Kim & Ployhart, 2018; Riley, Michael, & Mahoney, 2017) on firm performance. In so doing, they focused more strongly on the role of managers as decision makers in terms of the actions they take to use resources (Carnes, Xu, Sirmon, & Karadag, 2019; Ndofor et al., 2011).

Moreover, researchers investigated contingencies, such as institutional environments (He, Brouthers, & Filatotchev, 2013) and configurations of actions (Riley et al., 2017), to the action–performance relationship postulated in RO. Inquiry developed around the role that the resources already possessed by a firm play in future actions, such as investment decisions (Speckbacher, Neumann, & Hoffmann, 2015), recognizing that current resource stocks create asymmetries in competition for new resources so that small initial differences amplify over time (Wernerfelt, 2011). Also, researchers addressed the problem of what determines the ex ante—that is, before acquisition or accumulation decisions—assessment of the resource value, recognizing the role of complementarity with prior resources, knowledge, and managerial cognition (Garbuio, King, & Lovallo, 2011; J. Schmidt & Keil, 2013). In sum, although this last stage has seen conceptual developments and empirical inquiry mostly focused on resource use, it seems most appropriate to characterize this time period as moving toward a stronger integration of resource-possession and resource-use logics.

Outstanding Questions and Integrative Model

As described already, the topics of resource possession and use have played central roles in the evolution of resource-based logic. Conceptual developments have provided researchers with frameworks to integrate these insights, along with evidence, on the performance implications of both possessing and using resources. Yet, recent reviews mostly focused attention alternatively on the implications of resource possession (e.g., Nason & Wiklund, 2018) or resource use (e.g., Barley et al., 2016; Clough, Fang, Vissa, & Wu, 2019; Helfat & Martin, 2015; Zahra, Neubaum, & Hayton, 2020). Indeed, as we looked for evidence supporting (or in contrast to) a more integrated, and perhaps more contemporary, view of resource-based logic, we noticed that while RBV has long described that resources enable firms to conceive of and implement strategies and actions (Barney, 1991), there was not a comprehensive empirical review (i.e., meta-analytic assessment) connecting resource possession to use (e.g., orchestration actions). In particular, notwithstanding the recognition that prior resource endowments affect subsequent managerial actions (Speckbacher et al., 2015; Wernerfelt, 2011), there are no large-scale efforts (e.g., review or meta-analysis) geared toward understanding the size of the empirical link between possessing and using strategic resources. This raised our first research question: To what extent does possessing strategic resources enable orchestration actions?

In our review of the literature, we highlighted how resource possession and use have been relevant within resource-based logic. Moreover, recent developments (e.g., Sirmon et al., 2007, 2011), leveraging insights from RBV and dynamic capabilities, have provided a framework to more formally integrate resource-possession and -use logics while proposing a detailed and testable set of actions as important in the quest for firms to improve their performance (Sirmon et al., 2007, 2011). This suggests that models specifying a direct relationship between resource possession and firm performance are “underspecified” (Bergh, Ketchen, Boyd, & Bergh, 2010: 622) and that what we know about the performance implications of possessing strategic resources can be augmented by understanding how orchestration actions (i.e., structuring, bundling, leveraging) further shape this relationship. Specifically, from our review, we derive that actions are potentially important intervening mechanisms (mediators) between possessing resources and firms enjoying stronger performance. If this is the case, empirical questions remain regarding the extent and the nature (full or partial mediation) of action effects. This raises our second research question: How do orchestration actions affect the nature of the strategic resources–firm performance relationship?

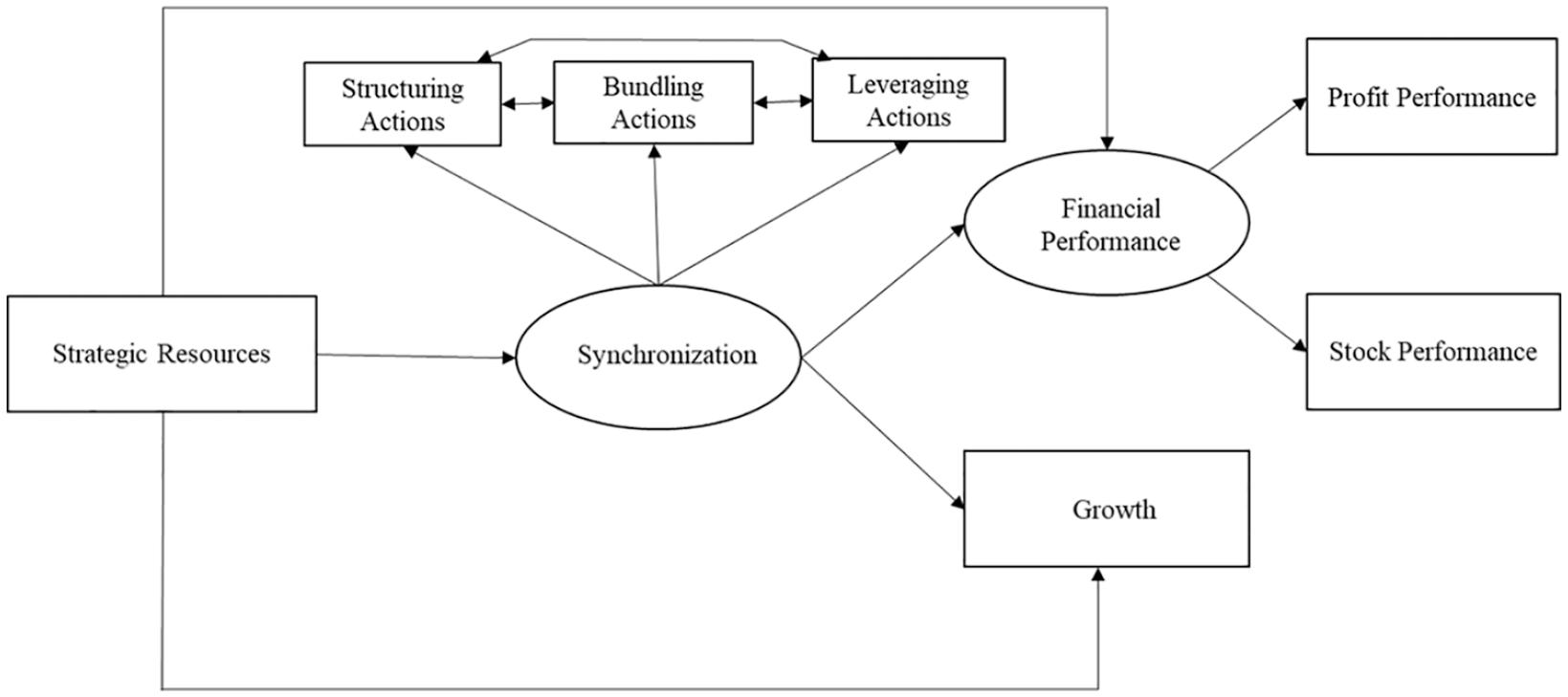

Finally, Sirmon et al.’s (2007) framework makes clear that although actions alone might shape performance, their potential is unleashed when they are synchronized such that they work in concert with one another. Also, empirical research has begun to investigate the role of configurations of action for performance (Sirmon & Hitt, 2009). If synchronization matters, then the complementary effects of orchestration actions on performance might be stronger than the effects of any one action alone. In addition, accounting for synchronizing might also put strategic resources to better use (i.e., have stronger effects). This raises our third research question: How does synchronization among actions further change the nature of the resource possession–firm performance relationship? To address these questions, we use MASEM to integrate insights from resource-possession and resource-use logics (see Figure 2). This model draws heavily on insights from Barney (1991) and Sirmon et al. (2007, 2011).

Integrative Model of Strategic Resources, Orchestration Actions, and Performance

Method

Data and Sample

We used MASEM (Bergh et al., 2016; Cheung, 2014, 2018; Cheung & Chan, 2005) to address these questions. MASEM is an analytical approach that aggregates bodies of evidence by first meta-analyzing bivariate relationships to produce estimates on the size of individual relationships and then using these estimates as inputs into structural equation models. A key decision point was choosing whether to be comprehensive or selective in gathering studies. An initial search across EBSCO Business Source Elite, JSTOR, Science Direct, and Google Scholar using the keywords “resource,” “orchestration,” “structuring,” “bundling,” “leveraging,” or “performance” and “correlation” (to limit the return of studies lacking correlations) uncovered over 100,000 possible studies across journals of various quality levels. Given that Aguinis, Dalton, Bosco, Pierce, and Dalton (2011) caution against including effects from low-quality studies because doing so might bias estimates, we drew from leading journals. Leveraging the Financial Times 50 list, we selected seven leading journals that routinely publish empirical strategic management research: Academy of Management Journal, Administrative Science Quarterly, JOM, Journal of Management Studies, Organization Science, Strategic Entrepreneurship Journal, and Strategic Management Journal. This approach allowed us to gather a “representative group” of high-quality studies for inputs into MASEM (F. Schmidt et al., 1985: 721).

We gathered relevant studies from this set of journals starting in 1991—the year of Barney’s foundational work. Studies seldom examine links among all three constructs (i.e., strategic resources, orchestration actions, and performance), so our task was to identify studies that included links among at least two. This yielded 252 primary studies involving 255 samples and 111,120 observations. Table 1 lists each study and the links tested within each.

Studies Included in Meta-Analytic Structural Equation Models

Note: AMJ = Academy of Management Journal. ASQ = Administrative Science Quarterly. JOM= Journal of Management. JMS = Journal of Management Studies. OS = Organization Science. SEJ = Strategic Entrepreneurship Journal. SMJ = Strategic Management Journal. N/A = not available. We coded whether each study contained a measure of strategic resources (R), orchestration actions (A), and/or performance (P).

Two authors coded each study for sample size and effect sizes between our constructs of interest; interrater reliability was 94.85%. All disagreements were discussed until resolved. We relied on the number of firms in each primary study’s sample as our input; thus, for longitudinal studies, we used the total number of firms, instead of the total number of observations (i.e., firm-years), to avoid potential interdependence among observations (Carnes et al., 2019).

Measures

In coding strategic resources, we consulted the procedure adopted in Crook et al. (2008) and Nason and Wiklund (2018) as well as the articles they used to guide their coding (e.g., Barney, 1995; Hoopes, Madsen, & Walker, 2003) to ensure that our analyses included only resources considered “strategic” (i.e., valuable, rare, and difficult to imitate or substitute; Barney, 1991). Specifically, we coded a resource as strategic when a measure captured value and represented a resource that is protected by at least one isolating mechanism. We first captured each resource measure wherein a study’s author(s) invoked RBV to assert that the resource was “valuable.” We then checked whether theory and evidence supported the author’s assessment. Thus, we did not code resource measures as valuable if there was strong theory and evidence (e.g., gender diversity; see Jin, Madison, Kraiczy, Kellermanns, Crook, & Xi, 2017) showing that the outcomes might not always exceed the costs.

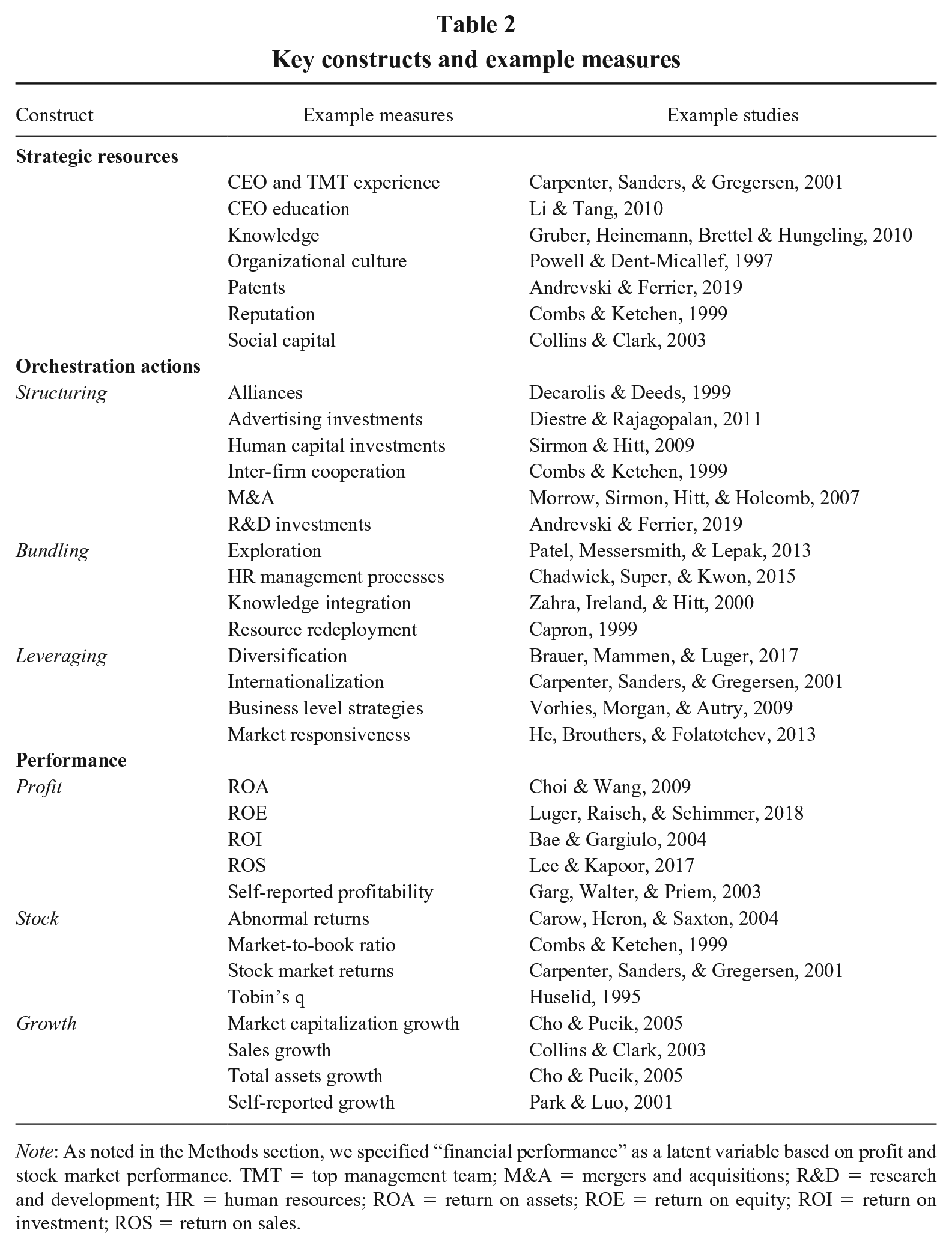

Second, we assessed inimitability based on the existence of (a) unique historical conditions, (b) causal ambiguity, and (c) social complexity. We then defined each isolating mechanism in operational terms so that it was clear to each coder. Following precedents in the literature (Crook et al., 2008; Nason & Wiklund, 2018), property-based resources that can be protected via law (e.g., patents and trademarks) and resources subject to time compression diseconomies (e.g., reputation) were deemed as characterized by unique historical conditions. Whenever a measure captured tacitness and/or a resource bundle, it was deemed as characterized by causal ambiguity. Last, measures that involved human or social capital as well as culture were deemed as socially complex. Like Nason and Wiklund (2018) and Crook et al. (2008: 1148), “we did not perform additional screens based on rareness and substitutability.” The underlying logic is that imitability and rarity are closely related because if a resource is inimitable, it is also rare (Hoopes et al., 2003). And, as Barney (1995) notes, substitution is best viewed as a type of imitation. Similar to Crook et al. (2008: 1148), we interpreted this to mean that “the screening approaches listed above are sufficient” to account for rarity and substitutability in coding strategic resources. Yet, at the same time, one key difference between our coding and Crook et al. and Nason and Wiklund (2018: 39) is that whereas they coded “allocation decisions,” such as research and development spending, as resources, we coded such measures as orchestration actions because these measures directly reflect spending flows and thus appear better viewed as actions. Table 2 reports examples of our coding for strategic resources and the other constructs.

Key constructs and example measures

Note: As noted in the Methods section, we specified “financial performance” as a latent variable based on profit and stock market performance. TMT = top management team; M&A = mergers and acquisitions; R&D = research and development; HR = human resources; ROA = return on assets; ROE = return on equity; ROI = return on investment; ROS = return on sales.

We coded orchestration actions by categorizing practices identified in Sirmon et al.’s (2007, 2011) work according to the structuring, bundling, and leveraging categories they described. Structuring actions refers to the management of the resource portfolio and include acquiring, accumulating, and divesting resources. Examples of actions in this category are research-and-development investments, mergers and acquisitions, and strategic alliances. Notably, these investment actions were considered structuring because they effectively change the portfolio of resources available to a firm (e.g., strategic alliances change the human, tangible, and intangible capital available to a firm) but do not necessarily allow “the application of a firm’s capabilities to create value for customers and wealth for owners” (Sirmon et al. 2007: 277) until other actions are taken to use the resources obtained. Bundling actions refers to configuring resources into meaningful sets that can be deployed via stabilizing, enriching, and pioneering actions. Workflow integration routines and innovation processes routines are examples of actions coded in this category. Leveraging actions refers to the exploitation of a firm’s resources through mobilizing, coordinating, and deploying actions. Diversification, internationalization, and business-level strategies (e.g., cost leadership positioning routines) are examples of actions in this category. To code for synchronization among actions, we captured the complementarity among the different actions by following the approach of previous meta-analytic research: creating a latent variable involving structuring, bundling, and leveraging actions (cf. Jiang, Lepak, Hu, & Baer, 2012). To further ensure the validity of our coding of orchestration actions, we contacted two of the authors of the seminal work on RO (Sirmon et al., 2007). We provided them with examples of operational measures of action-related constructs adapted from the studies in our sample. They were then asked to code measures regarding the specific RO actions (i.e., structuring, bundling, or leveraging) they belonged to. Notably, the authors were also given the option to code measures as not belonging to any of the RO actions. If disagreements were identified between our coding and that of the original authors, we discussed them until we reached consensus.

Firm performance has long been considered a multidimensional construct (Venkatraman & Ramanujam, 1986). Because researchers investigating the performance effects of strategic resources have distinguished profit (e.g., return on assets [ROA]) and stock performance (e.g., Tobin’s Q) effects from growth (e.g., year-over-year sales increases) effects (Crook et al., 2008; Nason & Wiklund, 2018), we created a latent variable—called financial performance—based on profit and stock performance (Crook et al., 2008), and we coded growth as a separate outcome of interest. As in Karna, Richter, and Riesenkampff (2016), objective and subjective measures were included.

Controls

We included control variables that may affect the availability of strategic resources, the type of actions that a firm is willing or able to undertake, and ultimately, firm outcomes. First, meta-analytic results provide evidence that firm size is related to the nature of a firm’s resources (Nason & Wiklund, 2018), innovation (Camisón-Zornoza, Lapiedra-Alcamí, Segarra-Ciprés, & Boronat-Navarro, 2004), and outcomes (Nason & Wiklund, 2018); thus we included it as a control in our model. Second, firm age can affect resources and orchestration actions because a firm’s history shapes its resource endowments as well as the ways in which it exploits them (Barney, 1991). For example, evidence suggests that younger firms are more likely to innovate (Huergo & Jaumandreu, 2004), yet older firms are better at balancing the different activities they pursue and enjoy stronger performance as a result (Mathias, McKenny, & Crook, 2018). To account for size and age, we calculated meta-analytic correlations linking them with strategic resource, orchestration action, and performance measures, and we used these as inputs into our MASEM.

Analytic Procedures

We closely followed MASEM guidance offered by Bergh et al. (2016). First, we used random-effects meta-analysis to derive weighted average effects sizes (correlations, or

Beyond addressing sampling error, Bergh et al. (2016) point out the need to also correct for measurement error (i.e., unreliability) because it biases effect size estimates. Because most studies do not report reliability coefficients, we used a correction of 0.80 to correct each

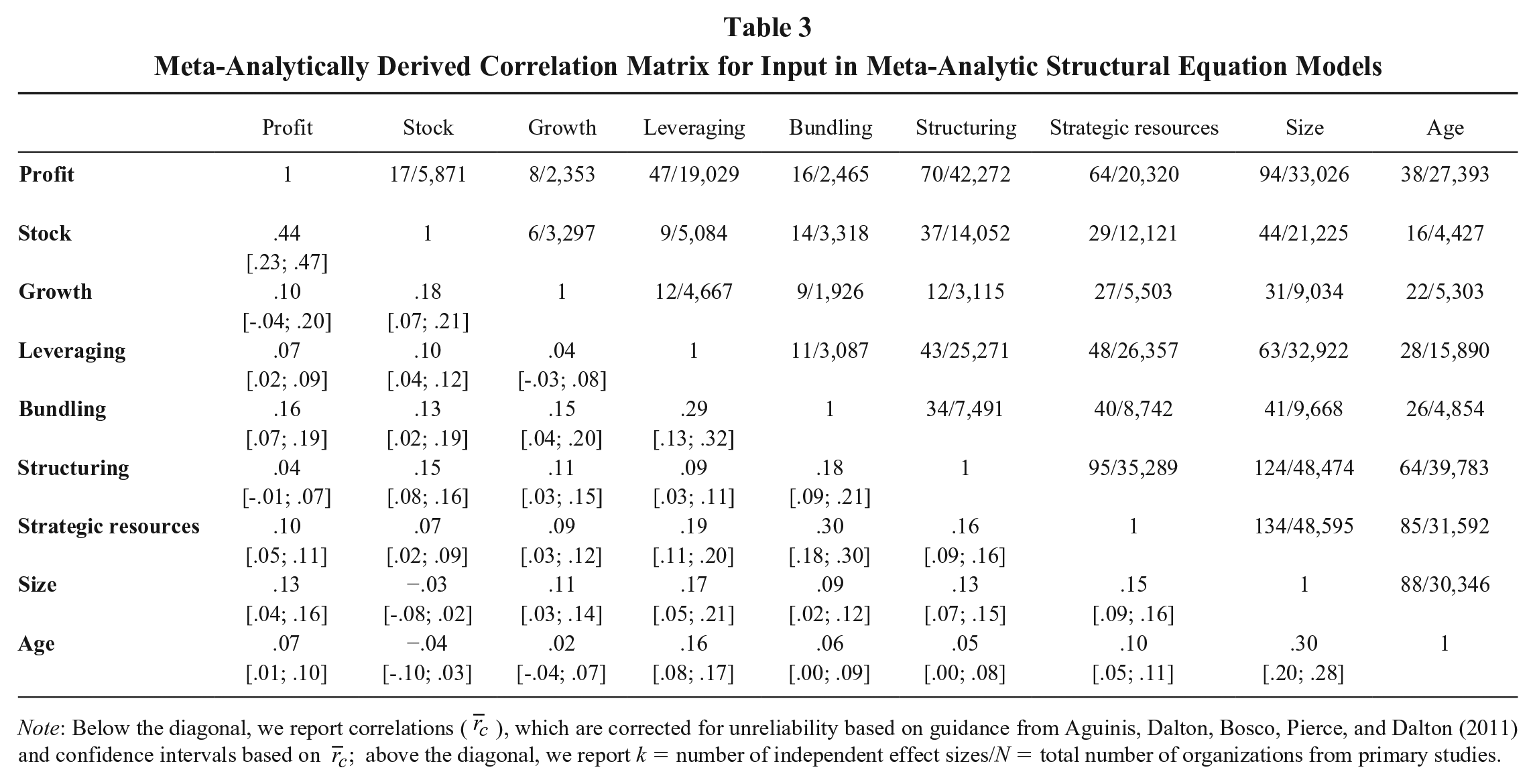

Meta-Analytically Derived Correlation Matrix for Input in Meta-Analytic Structural Equation Models

Note: Below the diagonal, we report correlations (

We then used the correlation matrix as the input into a structural equation model (Cheung & Chan, 2005). Doing so brings together the strengths of meta-analysis (e.g., avoiding bias associated with small sample sizes and improving external validity) with those of SEM—for example, investigating relationships and fit (Connelly et al., 2018). We conducted our MASEM with AMOS 24 using a harmonic mean of 6,965 and maximum likelihood estimation; the harmonic mean weights large individual study sample sizes less; thus, it is more conservative than the arithmetic mean (Bergh et al., 2016). We began by conducting a confirmatory factor analysis (CFA) to ensure that our indicator variables belong on the two latent variables we created. Then, for the CFA and all of our research questions and corresponding models, we assess standardized regression weights, significance levels, and overall model fit via the root mean square (RMR), the goodness-of-fit index (GFI), the normed fit index (NFI), and the comparative fit index (CFI).

Results

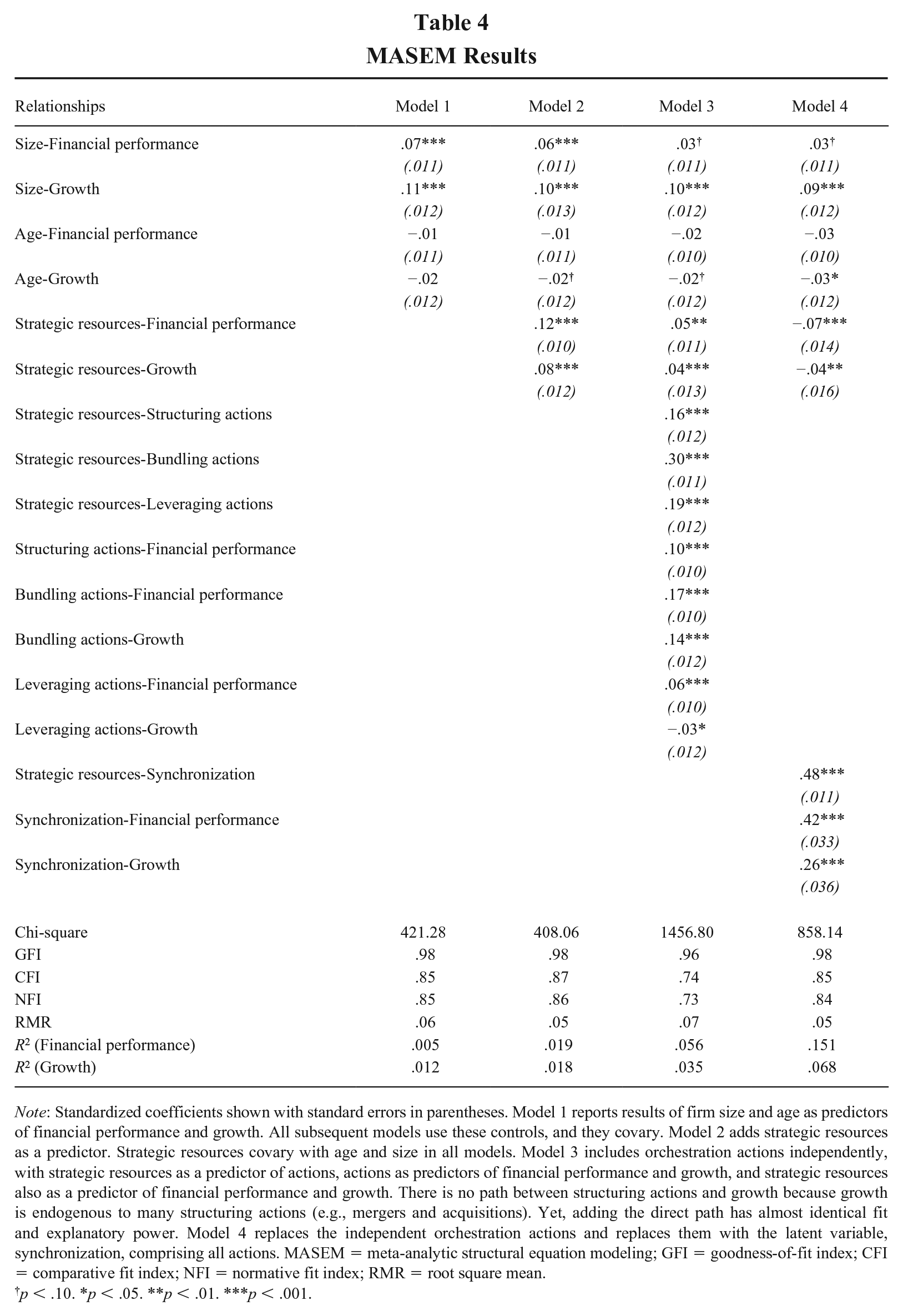

Our CFA included our two latent variables (i.e., financial performance and synchronization) in the same model. The evidence suggests that profit (β = 0.67) and stock performance (β = 0.66) belong on our latent “financial performance” and that structuring, bundling, and leveraging actions (β = 0.26, 0.70, and 0.40) belong on our latent “synchronization.” The model fit statistics (i.e., RMR = 0.03, GFI = 0.99, NFI = 0.95, CFI = 0.95) provided further evidence supporting these two variables (Hu & Bentler, 1999). Table 4 reports results involving our models (i.e., 1–4) surrounding the nature of the relationships among strategic resources, orchestration actions, and performance as well as our controls. Appendix 1—which is part of an online supplement—reports the figures related to each of the models presented in Table 4. The first model includes firm size and firm age as controls to predict financial performance (i.e., profit and stock) and growth. The fit statistics are RMR = 0.06, GFI = 0.98, NFI = 0.85, and CFI = 0.85, and the R2 statistics are .005 for financial performance and .012 for growth. Next, Model 2 adds strategic resources as a direct predictor of financial performance and growth. The results provide evidence that the possession of strategic resources is positively associated with performance (i.e., financial [β = 0.12, p < .001] and growth [β = 0.08, p < .001]). With fit statistics of RMR = 0.05, GFI = 0.98, NFI = 0.86, and CFI = 0.87, along with the R2 statistics for financial performance and growth increasing to .019 and .018, respectively, we see improvement over Model 1 but continued room for improvement.

MASEM Results

Note: Standardized coefficients shown with standard errors in parentheses. Model 1 reports results of firm size and age as predictors of financial performance and growth. All subsequent models use these controls, and they covary. Model 2 adds strategic resources as a predictor. Strategic resources covary with age and size in all models. Model 3 includes orchestration actions independently, with strategic resources as a predictor of actions, actions as predictors of financial performance and growth, and strategic resources also as a predictor of financial performance and growth. There is no path between structuring actions and growth because growth is endogenous to many structuring actions (e.g., mergers and acquisitions). Yet, adding the direct path has almost identical fit and explanatory power. Model 4 replaces the independent orchestration actions and replaces them with the latent variable, synchronization, comprising all actions. MASEM = meta-analytic structural equation modeling; GFI = goodness-of-fit index; CFI = comparative fit index; NFI = normative fit index; RMR = root square mean.

p < .10. *p < .05. **p < .01. ***p < .001.

Model 3 (see online supplement) then adds resource-use factors. Specifically, Model 3 includes age and size as controls as well as strategic resources as a direct predictor of (a) orchestration actions of structuring, bundling, and leveraging and (b) financial performance and growth, and actions as mediators of the strategic resource–outcome relationships. This model provides answers to the first two questions we posed: To what extent do strategic resources enable orchestration actions? and How do orchestration actions affect the nature of the strategic resources–firm performance relationship? For the first question, we found that strategic resources are positively and significantly related with structuring (β = 0.16, p < .001), bundling (β = 0.30, p < .001), and leveraging (β = 0.19, p < .001) actions. This provides evidence that resource possession and use are interdependent.

For the second question, our goal was to understand whether and to what extent each orchestration action mediates the strategic resource–firm performance relationship. Evidence for full mediation would exist if strategic resources no longer affect performance measures after accounting for actions, while evidence of partial mediation would exist if the resource–performance effects become smaller—but remain larger than zero—when actions are included (Aguinis, Edwards, & Bradley, 2017; James, Mulaik, & Brett, 2006). In this model, we specified actions as three separate mediating variables of strategic resources with financial performance and growth. Indeed, although RO depicts that structuring and bundling action effects are primarily felt through leveraging actions, it also allows for those actions to have direct effects on performance outcomes (Sirmon et al., 2007). Thus, in Model 3, we relax the assumption that the effects of structuring and bundling actions flow only through leveraging actions (see Post Hoc Analyses section for model where structuring and bundling effects flow through leveraging, as well). We find that structuring actions are positively associated with financial performance (β = 0.10, p < .001). We did not include a path between structuring actions and growth because growth is endogenous to many structuring actions (e.g., mergers and acquisitions). Bundling actions are positively related to financial performance (β = 0.17, p < .001) and growth (β = 0.14, p < .001), and leveraging actions are positively related to financial performance (β = 0.06, p < .001) but not to growth (β = −0.03, p < .05). Strategic resources’ effects on financial performance (i.e., β = 0.05, p < .01) and growth (i.e., β = 0.04, p < .001) remained positive and significant, providing evidence of partial mediation (Aguinis et al., 2017; James et al., 2006).

As in other meta-analytic studies (e.g., Drees & Heugens, 2013), we conducted Sobel tests to provide further mediation evidence (MacKinnon & Dwyer, 1993). We found that structuring (z = 5.67, p < .001), bundling (z = 10.37, p < .001), and leveraging (z = 3.88, p < .001) actions mediate the resource–financial performance relationship as well as that bundling (z = 10.54, p < .001) and leveraging (z = -2.07, p <.05) mediate the resource–growth relationship. With this model, fit fell (i.e., RMR = 0.07, GFI = 0.96, NFI = 0.73, and CFI = 0.74), but the R2 for financial performance rose from .019 to .056, and the R2 for growth increased from .018 to .035, indicating stronger explanatory power than Model 2 but still room for improvement.

To address our third research question (i.e., How does synchronization among orchestration actions further change the nature of the strategic resource-performance relationship?), we created Model 4 (see online supplement). Here, we specified that actions are synchronized in a complementary way, reflecting a single mediating latent variable of strategic resources and financial performance as well as growth relationships. Here, in line with RO logic, we found evidence of full mediation. In particular, strategic resources are positively and significantly related with synchronized actions (β = 0.48, p < .001), and synchronized actions are positively related to financial performance (β = 0.42, p < .001) and growth (β = 0.26, p < .001). In this model, strategic resources are no longer positively related with financial performance (i.e., β = −0.07) or growth (i.e., β = −0.04). We also conducted a Sobel test and found evidence that synchronized actions mediate financial performance (z = 11.87 p < .001) and growth (z = 10.46, p < .001). Taken together, this suggests that the effects of strategic resources with financial performance and growth are fully mediated by orchestration actions when they are synchronized (James et al., 2006). With fit statistics of RMR = 0.05, GFI = 0.98, NFI = 0.84, and CFI = 0.85 and the R2 for financial performance and growth increasing to .151 and .068 (from .056 and .035 in Model 3), we conclude that among our models, Model 4 best fits the data.

Post Hoc Analyses

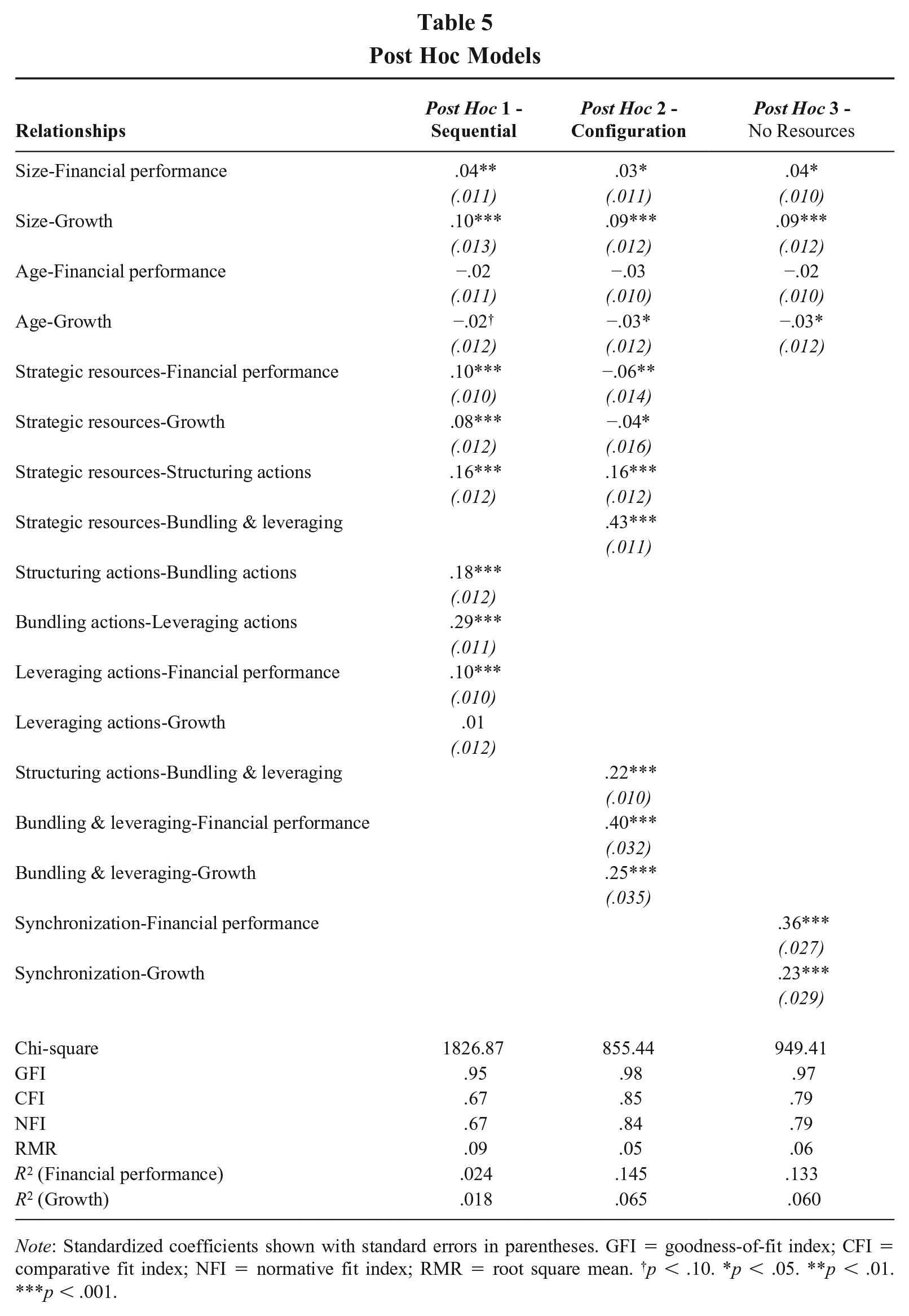

Table 5 and Appendix 2 (see online supplement) report the results and figures related to the post hoc analyses, respectively. While Sirmon et al. (2007: 275) stated that “the resource management process is at least partially sequential in nature” as firms need to have resources to bundle into capabilities, and that capabilities are necessary for leveraging actions, their framework does not mandate a sequential process and highlights feedback loops that allow synchronization to occur without a strict sequential mandate. However, there were several alternative model specifications possible; thus, we conducted a series of post hoc analyses to account for these possibilities. First, to address an alternative interpretation of RO logic as requiring a strict sequential treatment, we control for size and age and modeled structuring, bundling, and leveraging actions sequentially, with no direct structuring or bundling effects on outcomes (see Post Hoc 1 column in Table 5). Because this interpretation was not specified in RO’s original or subsequent theoretical treatments, it is not surprising that the results show that the fit and the explanatory power of this model fell (e.g., RMR = 0.09 and GFI = 0.95 with R2 = .024 [financial performance] and R2 = .018 [growth]) relative to Models 3 and 4.

Post Hoc Models

Note: Standardized coefficients shown with standard errors in parentheses. GFI = goodness-of-fit index; CFI = comparative fit index; NFI = normative fit index; RMR = root square mean. †p < .10. *p < .05. **p < .01. ***p < .001.

Second, because RO asserts that synchronization matters but does not specify which actions might work best together, we used our CFA results and the lower factor weight for structuring (i.e., β = 0.26) compared with bundling (i.e., β = 0.70) and leveraging (i.e., β = 0.40) to assess whether synchronizing bundling and leveraging together matters more than modeling all three actions alone (Model 3) or synchronizing them together (Model 4) (see Post Hoc 2 column in Table 5). Here, we control for firm size and age and include structuring as a separate action, with bundling and leveraging modeled together as a latent, and compare the R2 and model fit with our other models (with combined R2 of .09 [Model 3] and .22 [Model 4] for financial performance and growth). This post hoc model yielded a combined R2 of .21 and fit statistics of RMR = 0.05 and GFI = 0.98. While the R2 was twice as much as Model 3, it is slightly worse than Model 4, suggesting that Model 4—which includes the three orchestration actions synchronized together—best reflects the data.

Third, some researchers have highlighted how possessing strategic resources is not enough and have taken a strong position that actions are what matter (e.g., Ketchen, Hult, & Slater, 2007; Priem & Butler, 2001a). Thus, an open question is whether strategic resources matter when actions are considered, and the relationships reported earlier left open this question. Given this, we ran a separate analysis (i.e., Post Hoc 3) by removing strategic resources from Model 4. Compared with Model 4, removing strategic resources causes a combined 13% reduction in R2 as well as reduced fit (i.e., RMR = 0.06 vs. 0.05 [Model 4] and GFI = 0.97 vs. 098 [Model 4]), suggesting that both resource possession and use are necessary components of resource-based logic.

Fourth, though we followed Bergh et al.’s (2016) guidance, many researchers interested in meta-analyses have noted that results can be biased when there is substantial heterogeneity in effect sizes (Cheung, 2014, 2018; Yu, Downes, Carter, & O’Boyle, 2016, 2018). Two potentially important sources of heterogeneity include (a) effects within primary studies and (b) the possible exclusion of unpublished studies (lacking significant effects and results). We consulted Geyskens, Krishnan, Steenkamp, and Cunha’s (2009) review of meta-analytic practices for guidance to assess potential bias. To assess heterogeneity within the primary studies, we identified potential outliers by examining sample-adjusted meta-analytic deviancy (SAMD; Huffcutt & Arthur, 1995). When an effect size reported in a study was far outside the average—in this case, yielding a SAMD test statistic of 3.1 or more (see Huffcutt & Arthur, 1995: 331)—we followed Geysken et al.’s (2009) advice to eliminate such outliers, reexamine the results, and report the results both with and without outliers. Notably, we did not find evidence that effect size heterogeneity impacted the nature of our findings. The results of the analyses excluding outliers for all models are reported in Appendix 3 (see online supplement).

To examine potential publication bias, we followed Geyskens et al.’s (2009: 398) recommendation to use Rosenthal’s fail-safe N method to capture the potential effects of studies that might not be published because they were lacking statistically significant results. This process allows researchers to determine how many studies with null results would need to be uncovered and included in an analysis to change the conclusions. With the exception of the leveraging-to-stock-market-performance meta-analytically derived effect (

Besides specifying and comparing different models as well as assessing results for potential bias, a standard practice in meta-analytic studies is to conduct further analyses to ensure results’ robustness, especially when other factors might shape the nature of the relationships under investigation (e.g., Crook et al., 2008; Nason & Wiklund, 2018). We created subgrouping of studies based on the potential factor of interest and then used meta-analysis to derive weighted average effects sizes (i.e.,

Drawing on past research regarding contextual factors that can influence the links among strategic resources, actions, and performance (e.g., Oliver, 1997; Sirmon et al., 2007) and based on what our data would allow us to examine, our subgroup analyses focused on industry sector, country institutional environments, environmental dynamism, and environmental munificence. For industry, we created different subgroups based upon whether a primary study’s sample was drawn from the service versus manufacturing sector (Crook et al., 2008). For country institutional environment, we created two different sets of subgroups. The first involved creating subgroups wherein a study’s sample was drawn from the United States versus all other countries, and the second, wherein the sample was drawn from western versus Asian countries (Hitt, Lee, & Yucel, 2002). For environmental dynamism—that is, the rate of change or unpredictability (Dess & Beard, 1984)—we created subgroupings based upon whether the authors of a study described a sample as (a) dynamic or changing versus stable environments (Karna et al., 2016) or (b) high technology versus low technology. Mixed samples and those for which information on the two criteria was not available were excluded from this analysis. For environmental munificence (i.e., the relative abundance in the environment; Dess & Beard, 1984), we used data from the Economic Research Division of the Federal Reserve Bank on recessions from the Federal Reserve Economic Data database to create subgroups based on whether samples were drawn from countries where no recessions were reported during the sampling frame versus times when at least part of the sampling frame was characterized by a recession (Rosenbusch, Rauch, & Bausch, 2013). Of note, we examined two of Dess and Beard’s (1984) dimensions (dynamism and munificence) and not the third (i.e., environmental complexity), because complexity was not presented by Sirmon et al. (2007) as an influence on our focal relationships whereas the other two were.

In addition to these contextual factors, the RBV and RO highlight how possessing and using strategic resources enables competitive advantage (Barney, 1991; Sirmon et al., 2007). We identified 22 studies wherein their performance measures more closely captured competitive advantage (i.e., reporting industry-adjusted outcomes); we created one group of studies involving those measures. Then, we created another group with the remaining studies that captured performance (e.g., ROA) and growth (e.g., year-over-year change in sales) outcomes more generally.

After creating these subgroupings, we ran individual meta-analyses on all available relationships and examined confidence intervals to assess whether these factors substantively shaped the nature of the relationships among strategic resources and performance, strategic resources and actions (e.g., structuring), or actions and performance (Schmidt & Hunter, 2015). For these analyses, following Schmidt and Hunter’s (2015) guidance, comparisons are made only when three or more primary studies are available. The average number of primary studies per analysis is 17. Given this, we examine confidence intervals to explore potential differences among our factors of interest (e.g., manufacturing vs. service) because they are more robust than examining critical ratios (i.e., z scores) when dealing with smaller numbers of studies and observations (Schmidt & Hunter, 2015). To be as granular as possible, for all factors other than the analyses involving competitive advantage, we look at how performance effects are shaped by strategic resources and actions using profit, stock, and growth as three distinct outcome measures. When creating confidence intervals around such relationships, meta-analysts typically assess whether the intervals overlap (e.g., resources–financial performance in service sector vs. resources–financial performance in manufacturing sector). In particular, they view effects sizes within the subgroups as substantively different if there is at least 95% confidence that the intervals do not overlap (e.g., Crook et al., 2008).

Using these criteria, we found only five substantive differences at the p < .05 level involving the relationships examined across the subgrouping factors. The first difference is that the meta-analytically derived effect (i.e., weighted correlation) for the relationship between structuring actions and profit performance is larger (i.e.,

Discussion

We sought to help close the gap between what is known versus what needs to be known about the roles of resource possession and resource use in shaping why some firms outperform others. By continuing to integrate RBV with RO and providing evidence of the interdependence of possessing and using strategic resources, our study shed light on these and related literature streams (i.e., dynamic capabilities and KBV). Next, we detail ways in which they provide a foundation for future research related to these streams. We then offer ideas in emerging areas for resource-based inquiry.

Resources, Capabilities, and Knowledge

Whereas RBV has always acknowledged that resources need to be exploited (Barney, 1991), the perspective and inquiry drawing on its tenets had long been criticized for ignoring intervening paths between resources and performance (Priem & Butler, 2001a). Ketchen et al. (2007: 962) even went so far as to say that a “simple resources–performance link obviously lacks face validity. At the risk of being flippant, customers do not mail checks to a company just because the company possesses certain resources.” Integrating insights in the RBV and dynamic-capabilities traditions, RO specified several pathways—in the form of structuring, bundling, and leveraging actions—firms could take to exploit their strategic resources and thereby get customers to “mail checks” such that the firm could enjoy stronger performance (Sirmon et al., 2007, 2011). Results from our meta-analytic review integrating insights from RBV and the RO framework show possessing strategic resources is important not only because they positively affect firm performance (Crook et al., 2008; Nason & Wiklund, 2018) but also because—to a large extent—they enable managers to pursue an array of actions. Indeed, the more strategic resources firms possess, the more structuring (β = 0.16), bundling (β = 0.30), and leveraging (β = 0.19) actions they take. Without possessing strategic resources, firms thus appear ill equipped to take orchestration actions. This supports ideas from a range of influential resource-based theorists (e.g., Barney, 1991, 2001; Sirmon et al., 2007, 2011) and shows that resource possession and use are inextricably linked and thus interdependent on one another. Moreover, our results show that the performance effects of resources are felt—or partially mediated—by their effects via orchestration actions, when actions are considered separately (see Model 3). When actions are synchronized, the resource–performance relationship is fully mediated (see Model 4).

Moreover, the explanatory power of Model 4, compared with Model 3, is more than 160% larger for financial performance and 90% larger for growth. Examining synchronized actions substantially increases the ability to explain firm performance; this suggests that actions act in complementary ways. These results provide support for the importance of integrating RBV and the RO framework in future research aimed at explaining why firms outperform competitors. Although Model 4’s explanatory power may lead to the interpretation that it is only actions and their synchronization—not the possession of strategic resources—that matter, our post hoc analyses suggested otherwise. Specifically, when we remove strategic resources from our synchronization model (i.e., Model 4), both model fit and explanatory power fell in a nontrivial way. Thus, the possession of strategic resources remains an important component of the nomological network needed to explain why some firms outperform others. Building on these findings, we contend that RBV and RO are necessary but not individually sufficient antecedents of firm performance. Thus, we see great opportunities for future research in continued integration of insights from these perspectives.

First, both RBV and RO describe determinants of competitive advantage (Peteraf & Barney, 2003; Sirmon et al., 2007). Yet, integrating insights from these perspectives has the potential to extend them beyond their current focus on competitive advantage as the central mechanism for profit creation (Makadok, 2011). For example, our results suggest that strategic resources allow a firm to have an information advantage in strategic-factor markets (Barney, 1986b), thus affecting its ability to create value through structuring actions. As such, strategic resources generate an information advantage that becomes the source of a competitive advantage mainly after orchestration actions are undertaken. Similarly, strategic resources may allow firms to recognize market opportunities more quickly. This may enable them to take preemptive actions (Fiet, 2002) and to generate commitment timing advantages (Makadok, 2011). Different strategic resources and orchestration actions might even reinforce or undermine each other. Future research could seek to better understand how resources and orchestration actions may activate profit-generating mechanisms beyond competitive advantage.

Second, integrating RBV with RO puts managers at the center of the nomological network that characterizes the resource–performance relationships. This is important as it answers the call for specifying the microfoundations of resource-based theorizing (Foss, 2011). Specifically, our results suggest that strategic resources are important when they allow managers to engage in orchestration actions, especially when synchronized. We also suspect that knowledge in terms of managerial skills and experience may play a relevant role in dynamically informing resource-use decisions and firm performance differentials. In other words, although RBV does not “sufficiently recognize the role of the individual judgments or mental models of entrepreneurs and managers” (Kraaijenbrink et al., 2010: 356), such recognition becomes central when RBV is integrated with the RO framework. Thus, we believe that there is great promise in integrating insights from our model with KBV and the role of knowledge in managerial decisions and actions (Eisenhardt & Santos, 2002).

Third, the integration of RBV and RO has the potential to address some of the issues raised within the dynamic-capabilities literature (Barreto, 2010). Specifically, a limitation of the capabilities approach is that even the processes of resources development and deployment are—like the resources themselves—[often] conceptualized as capacities, inclining us to think in terms of their possessions rather than in terms of integration and application. (Kraaijenbrink et al., 2010: 360)

Our model provides a framework to distinguish the performance and growth effects of a firm’s resources from flows and processes that involve their development and deployment. Because of this, researchers appear equipped to continue to disentangle these effects and foster a greater understanding of the processes through which the stock of organizational abilities affects firm processes and performance.

In some ways, this brings our work back to the foundational roots of RBV and RO; long ago, Dierickx and Cool’s (1989) description of resource flows and stocks closely aligns with the need to integrate resource-possession and -use logics we describe. Their bathtub analogy explaining the distinction between stocks and flows—“at any moment in time, the stock of water is indicated by the level of water in the tub; it is the cumulative result of flows of water into the tub (through the tap) and out of it (through a leak)” (Dierickx & Cool, 1989: 4)—provided a metaphorical, yet formative, step to understand the differential effect of strategic resources and the processes associated with their development and deployment. Moreover, the use of RO allowed us to identify the differential effects of three orchestration subprocesses (structuring, bundling, and leveraging). We believe that future research focused on the interdependences between these processes has great promise. Indeed, one potentially important insight of our results is that there is a premium on the alignment of resource management processes. Thus, researchers interested in explaining firm performance are better off focusing on action configurations than on one action type at a time, similar to how human resource management research has found that examining high-performance work systems is more powerful than examining individual high-performance practices (Combs, Liu, Hall, & Ketchen, 2006).

Fourth, given the relevance of orchestration actions, especially when synchronized, we suggest that in line with the evolution of resource-based logic, future research extending RO could leverage insights from the competitive-dynamics literature to focus on actions’ attributes that affect their ability to generate competitive advantage and improve performance. For example, action complexity may be relevant in determining the value of certain actions as well as the time frame within which performance differentials should be expected (Carnes et al., 2019). Similarly, action visibility to external observers may affect the nature of their relationship with firm performance. For example, highly visible actions may provoke swift and meaningful competitive responses (Malhotra, Ku, & Murnighan, 2008), as competitors might respond via actions of their own, reducing value generated and captured from such actions. Last, firms do not act in a vacuum, and an action’s degree of conformity to social and institutional norms may affect its performance (Deephouse, 1999). Investigating how a firm’s resource management processes compare in terms of conformity and distinctiveness with those of its competitors may further understanding of the relationships among orchestration actions and firm performance.

Emerging Areas for Resource-Based Inquiry

We believe the results provide insights that have the potential to promote resource-based inquiry in other streams of research. When looking at the sizes of the strategic resource–action relationships, we find strategic resources’ effects on bundling (β = 0.30) are most potent (z = 8.86 and −6.63) as they are 88% and more than 58% larger than the effects of structuring and leveraging, respectively. One interpretation is that the nature of strategic resources’ relationship with bundling actions is materially different; such actions are more dependent on possessing strategic resources. This offers an interesting parallel to Penrose’s (1959) theorizing, wherein she portrayed firms as bundles of resources. Taken together, these points offer a view of executives’ jobs as simultaneously managing bundles of resources and orchestrating bundles of actions to help their firms prosper. One task for future inquiry could be developing a theory of firm performance centered on bundles and bundling, much like prominent finance theories view a firm as a nexus of contracts.

Second, the evidence also sparks questions about firm decision-making processes regarding resource endowments and allocations toward different orchestration actions. This leads us to believe future research should focus on how and when strategic resources affect orchestration actions. To do so, researchers could rely on the awareness-motivation-capability (AMC) perspective (Chen, 1996). Orchestration actions seem likely to depend on a firm’s awareness of potential structuring, bundling, and leveraging opportunities; motivation to undertake actions; and ability to do so. The possession of specific resources may affect each of these elements in different ways. For example, while relational capital may allow firms to have information advantages in strategic-factor markets (Barney, 1986b), thereby increasing the awareness of available structuring opportunities, it may also reduce the motivation to engage in leveraging actions that would extend the firm in areas where its relational capital is irrelevant (e.g., internationalization). Exploring the effects of strategic resources via an AMC lens has potential to offer a more nuanced understanding of their role as determinants of actions.

Third, we also see potential in integrating insights involving how managerial attention, like awareness, is directed within firms to build and cultivate resources as well as deploy them. Doing so would benefit by incorporating ideas from the attention-based view of the firm (Ocasio, 1997) to better understand allocation decisions to different orchestration actions. It could be the case that possession of a particular strategic resource (e.g., brand reputation) leads to proclivities toward undertaking certain actions (e.g., marketing initiatives) and thereby creating blind spots or core rigidities (Leonard-Barton, 1992) within an firm’s orchestration repertoire. Or group dynamics may play a role in such attention allocation. For instance, Ndofor, Sirmon, and He (2015) found that top-management-team fault lines affect resource-use tasks. Different fault lines could affect attention toward structuring, bundling, and leveraging as well as their synchronization.

Limitations and Other Directions for Future Research

Our results should be viewed in light of our study’s limitations. RO highlights the importance of feedback loops in managerial decisions regarding resource management and suggests that market feedback should influence each part of the process (Sirmon et al., 2007). Such feedback is considered necessary to activate meta-learning, wherein previous action-and-result combinations are taken into account to further future decisions (Lei, Hitt, & Bettis, 1996), fostering continuous adaptation (Sirmon et al., 2007). While a lack of available data prevented us from investigating such loops, future research could build understanding of how and when prior performance fosters learning that in turn shapes the links among strategic resources, orchestration actions, and performance in later periods.

Reporting practices within primary studies prevented us from capturing the quality of orchestration actions. If we had been able to capture distinctions between poorly and well-executed actions, we could have offered more clarity into the extent to which orchestration actions are best used to exploit strategic resources. Also, although we capture the range of firm actions described by Sirmon et al. (2007, 2011), other managerial actions that are outside of structuring, bundling, and leveraging types may play a role in shaping our focal relationships. In addition, perhaps these actions sets themselves could be further developed to build an understanding of specific underlying sets of subactions. Inquiry unpacking even more specific sets of resource management actions may further understanding of the relationships among strategic resources, orchestration actions, and performance.

Both RBV and RO are focused on competitive advantage. However, the lack of primary studies investigating performance differentials limited our ability to conduct a more “pure” test of these frameworks. Of the 183 samples in our analyses that included a performance measure, only 22 (12%) used measures that more closely capture competitive advantages. Although our post hoc analyses that indicated no differences in results between studies that operationalize performance using industry-adjusted measures are reassuring regarding the robustness of our findings, this limitation highlights the need for future research to adopt a more competitive-advantage-centered approach to the testing of these perspectives. This could include using industry-adjusted measures as well as devising new measures. One example of the latter would be having stock analysts or other industry experts assess firms’ competitive advantages (cf. Combs & Ketchen, 1999).

Although our other post hoc tests revealed substantial stability across most of the relationships we examined, we found differences in five relationships, indicating that contextual factors can shape firms’ abilities to benefit from their strategic resources and actions. For researchers interested in such factors, we point toward insights from Oliver’s (1997) work outlining the institutional contexts in which firms build and deploy their resources for future inquiry.

The inconsistent effects of leveraging compared with structuring and bundling also raise important questions. Although we found that leveraging complements structuring and bundling actions in important ways—to the extent that leveraging is synchronized with bundling actions, its effects on firm performance are nontrivial—our results show that leveraging actions by themselves are positively related to financial performance but not to growth. One potential reason is that many leveraging actions are highly visible to outsiders. As a result, they may provoke swift and meaningful competitive responses (Malhotra et al., 2008), as competitors might respond via leveraging actions of their own (e.g., entering similar markets or developing aggressive marketing campaigns). By doing so, competitors can reduce a firm’s ability to extract substantial value from such actions (Coff, 1999). Future research centered on the visibility of orchestration actions—and how it affects the relationships between strategic resources, orchestration actions, and performance—appears potentially useful.

Conclusion

The year 2021 marks 30 years since the publication of JOM’s landmark special forum on resource-based inquiry, a collection that included Barney’s (1991) specification of resource-based theory. With RBV now a well-established way of thinking about competition among firms, we chronicled the evolution of resource-based logic and noted the interconnectedness of resource-possession and resource-use logics in understanding why some firms enjoy higher performance than others. We then leveraged evidence from 255 samples involving 111,120 observations to conclude that both RBV and RO are necessary and complementary, but individually insufficient, for understanding these links. Looking to the future, we suspect that further progress toward understanding the roles that strategic resources and orchestration actions play in shaping performance differences between firms will be accelerated to the extent that RBV and RO are better integrated. We also urge future scholars to tackle the thorny issue of measuring competitive advantage given that its importance within RBV is not reflected in the amount of empirical attention devoted to it.

Supplemental Material