Abstract

We start this article with the exploration of similarities between the resource-based view of the firm (RBV) and stakeholder theory at the time of their origination and then proceed with the conversation on what led to distinct developmental trajectories of the two theories. Though RBV has become a leading paradigm in the strategic management field, we argue that in its current form, RBV is yet incomplete. We suggest there are four aspects that stakeholder theory can offer to inform RBV: normativity, sustainability, people, and cooperation. Reconciling stakeholder theory and RBV is a promising path to advancing our understanding of management, and we provide a two-part guideline to management scholars and practitioners who would be willing to take this path.

The influence of the resource-based view of the firm (RBV 1 ) on the field of strategic management is enormous. One need look no farther than the existence of this special issue for evidence. Theoretical sophistication and empirical validation notwithstanding, the theory continues to undergo additional refinement. Important recent refinements surface—and attempt to ameliorate—the conspicuous absence of a role for stakeholders in RBV. This absence is especially conspicuous considering the recent stakeholder-oriented “Statement of Corporate Purpose” from the Business Roundtable (2019): The CEOs of 181 major corporations committed “to lead their companies for the benefit of all stakeholders—customers, employees, suppliers, communities and shareholders” (cf. Harrison, Phillips, & Freeman, 2020).

To date, scholars have incorporated some elements of stakeholder theory in RBV, including accounting for stakeholders in RBV’s model of rent appropriation (Barney, 2018; Coff, 1999) and exploring stakeholders as resources leading to competitive advantage (Harrison, Bosse, & Phillips, 2010; Litz, 1996). Pioneering though these works were, the paucity of such synthesis is all the more notable given the similar scholarly trajectories of RBV and stakeholder theory.

We do not pretend to a comprehensive reconciliation here, but in light of the 30th anniversary of the special forum on RBV published in this journal, we offer here some comments that may help guide or support this long-emerging convergence. We begin by briefly describing the parallel—yet diverging—scholarly paths that have led the theories to this point. We then move on to analyze how stakeholder theory can inform RBV and suggest a two-part guideline for reconciling stakeholder theory and RBV.

Some History

The intellectual histories of stakeholder theory and RBV have been presented elsewhere (Eskerod, 2020; Freeman, 1984; Freeman, Harrison, Wicks, Parmar, & De Colle, 2010; Harrison, 2011; Harrison, Barney, Freeman, & Phillips, 2019; Strand & Freeman, 2015), and we will not duplicate this effort here. There are, however, some interesting moments of convergence and divergence in this history that can inform how we understand these intellectual cousins.

Both theories originated in the same field—strategic management—around the same time. Though the seeds of conceptual divergence were present from the beginning, both theories concerned themselves primarily and explicitly with the leadership and management of for-profit business firms in the mid-1980s. RBV emphasized sustainable competitive advantage (Barney, 1986, 1991) and profit maximization (Wernerfelt, 1984). Though broader in scope, the title of Freeman’s (1984) influential book, Strategic Management: A Stakeholder Approach, provides a clear idea of the author’s intended audience.

Both RBV and stakeholder theory offered novel ideas about strategy. RBV examined a firm’s competitive advantage emerging from unique endowments of strategic resources at the time when “practicing managers were not aware of the argument on the resource-based view until 1990” (Wernerfelt, 1995: 171). Stakeholder theory’s distinctive twist on strategy was emphasizing the building and maintenance of sustainable stakeholder relationships as the key to firm performance. The stakeholder theory literature represented “an abrupt departure from the usual understanding of business as a vehicle to maximize returns to the owners of capital” (Freeman et al., 2010: xv).

Due to similar conceptual breadth of the concepts of stakeholders and resources, it took years of subsequent joint work of many scholars to define the boundaries of stakeholders and resources to avoid everybody becoming a stakeholder (Phillips, 2003) so “the notion of stakeholder risks becoming a meaningless designation” (Freeman et al., 2010: 208) or “everything in the firm becomes a resource and hence resources lose explanatory power” (Conner, 1991: 145). On the other hand, due to unique differences among stakeholders (Bridoux & Stoelhorst, 2014) and across resources (Conner, 1991), it has been similarly hard to generalize them.

One less obvious point of overlap between these two influential theories is that both RBV and stakeholder theory have been challenged about whether they are really “theories.” Barney (2001) defended RBV’s theory-ness against, for example, Priem and Butler’s (2001a, 2001b) critiques to the contrary. Scholars began referring to RBV as “resource-based theory” (RBT)—all the articles in the previous special issue on RBV in this journal in 2011 used the term “RBT.”

Similar concerns have “plagued stakeholder theory almost from its inception” (Freeman, Phillips, & Sisodia, 2018). We continue to maintain that this concern is more apparent than real. The framing suggests that being a “theory” creates some privileged position (namely, if it is not a theory, it is “merely” something else) and that arguments from such a position have immutable “essences.” Ironically, the question also assumes that there is universal theoretical agreement on what makes something a “theory,” even within positivism. . . . What this apparent tension seems intended to do is privilege certain varieties of evidence, method, and argument. (Freeman et al., 2018: 218-219)

Because the answer to whether either theory is a theory makes little difference, we will content ourselves with the observation that this was a (distracting) rearguard action in the intellectual history of both theories that seems to have had little effect on their respective influence, conceptual development, or findings. Besides, similar sentiments can be expressed in relation to the entire strategic management field (Meyer, 1991). 2

Similarities aside, RBV and stakeholder theory soon found themselves on discernably divergent paths. First, the two theories had contrasting views on the role of shareholder interests in managerial decision making. From the early development of stakeholder theory, its advocates challenged a shareholder-primacy view (Donaldson & Preston, 1995; Freeman, 1984; Phillips, 2003).

Second, particularly in the early days, stakeholder theorists deemphasized competitive advantage—a concept considered by many as a cornerstone of the strategic management field. As a result, “despite its influence on early development of the field, stakeholder theory is not widely used by strategic management scholars to explain competitive advantage” (Harrison, Bosse, & Phillips, 2007: 1). Instead, and third, proponents of stakeholder theory appealed to normative claims and the role of cooperation and shared values in improving performance (Evan & Freeman, 1988; Phillips, 2003; Wicks, Gilbert, & Freeman, 1994).

Challenging the dogma of fiduciary duty to shareholders and emphasizing cooperation and moral norms rather than competition were, for the most part, too radical for mainstream strategic management at that time. Stakeholder theory, did, however, find traction with scholars in the field of business, ethics, and society.

The farthest RBV scholars were willing to go beyond the interests of shareholders was an invisible-hand, welfare economics–influenced claim that a resource-based sustained competitive advantage maximizes social welfare (Barney, 1991) and a firm’s performance can be measured by created economic value (Peteraf & Barney, 2003) that is more than return to shareholders. During this divergence, RBV did not explicitly challenge a shareholder-primacy view.

In short order, RBV was widely accepted by the strategic management field and has become among its most influential theories to date, while “stakeholder theory was pushed to the side of a tangential theory associated with social responsibility and business ethics” (Freeman et al., 2010: 95).

Though RBV grew to become a dominant theory in the strategic management division of the Academy of Management (AoM), and stakeholder work found its home primarily in the social issues division, they both remained important, largely parallel conversations among management professors within the AoM. The embers of this touch point—including a subset of scholars who were able to straddle both conversations—provided just enough spark to reignite the mutual interest for scholars with backgrounds in both (Bosse, Phillips, & Harrison, 2009; Harrison et al., 2010; Jones, 1995; Jones & Wicks, 1999; Tantalo & Priem, 2016). This shared interest has recently shined a brighter light on important questions with which legacy theories of strategic management have struggled. Next, we hope to add fuel to these efforts.

How Stakeholder Theory Can Inform RBV

If we are correct, this nascent re-enmeshing of stakeholder theory and RBV is merely scratching the surface—much of the potential for insight at this confluence remains untapped. Though none of what follows features the level of detail and theoretical integration that will eventually be required to meet this potential, we will nevertheless take this opportunity to point toward some broad areas we believe worthy of tapping. Additionally, we acknowledge at the outset that some characterizations of both theories are impressionistic and may not precisely track with a specific scholar’s more nuanced understanding of either. Both theories are concerned with people and profit, positivism and practicality. Because we are attempting to highlight differences in emphasis more so than clear contrasts, we suffer some loss of resolution. 3 This fish-eye-lens approach may distort some details, but ours is an intentionally panoramic view.

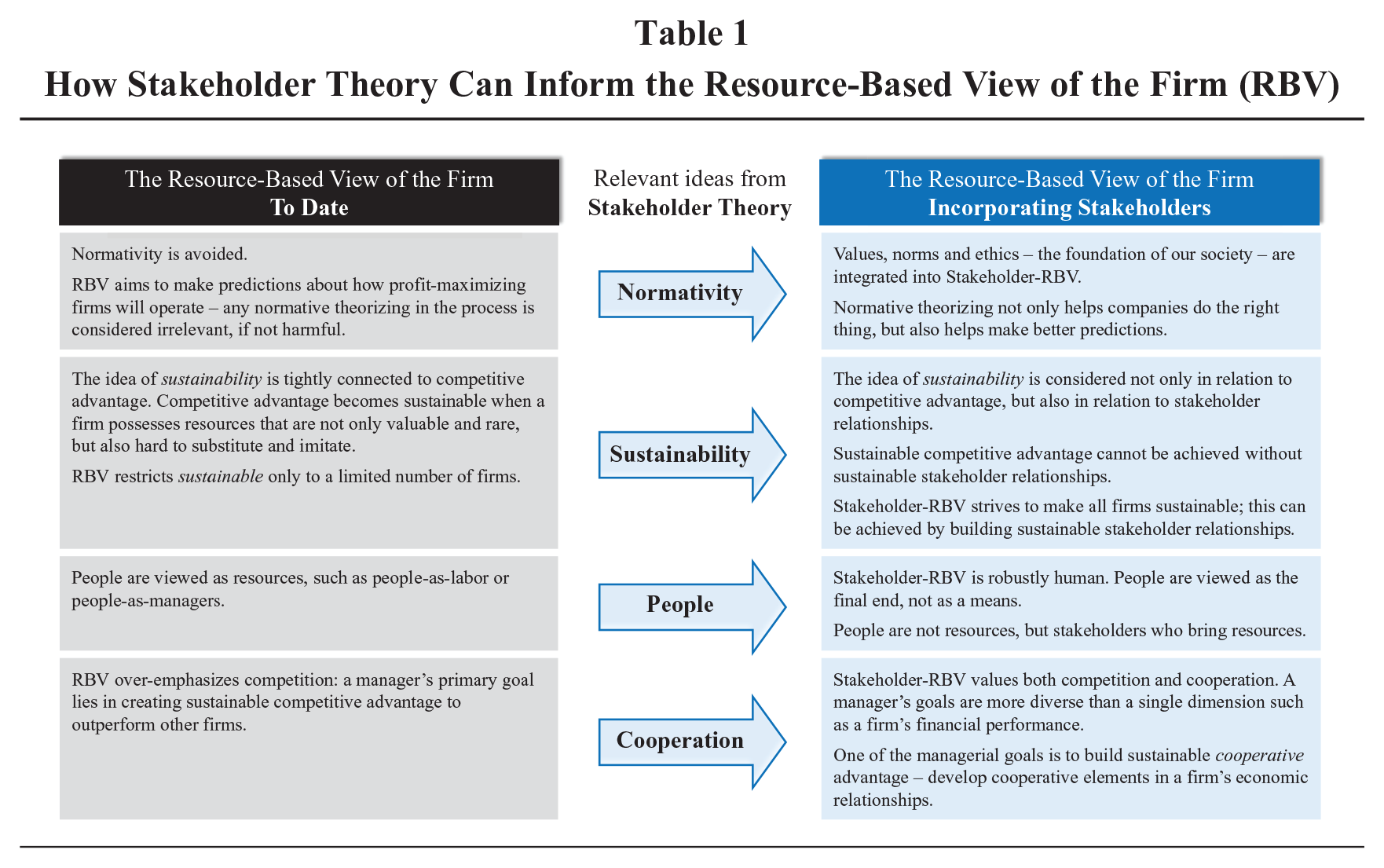

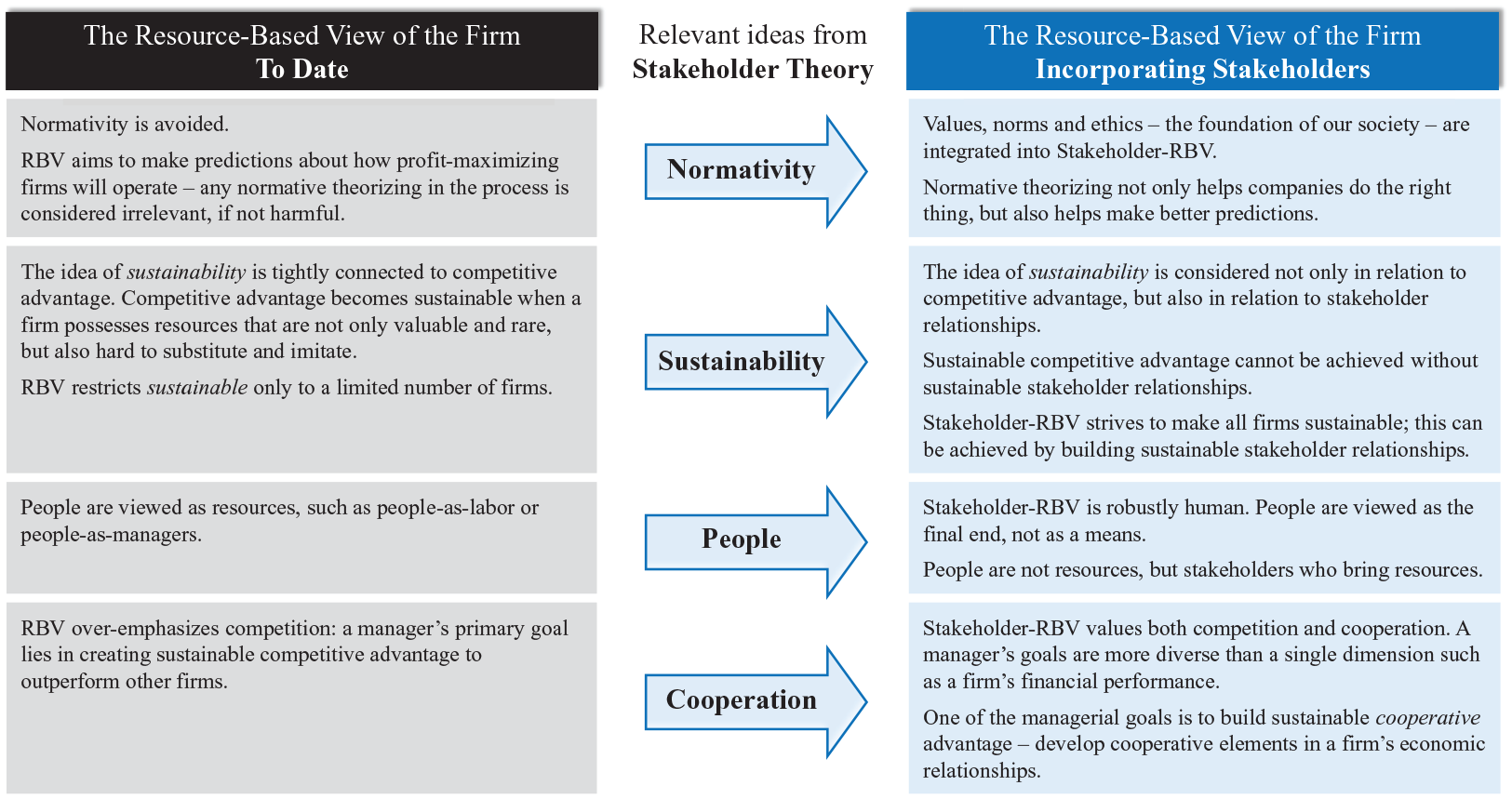

With this in mind, we turn now to discuss how normativity, sustainability, people, and cooperation present opportunities for a more nuanced understanding of strategic management at the juxtaposition of stakeholder theory and RBV. Our four main ideas are summarized in Table 1.

How Stakeholder Theory Can Inform the Resource-Based View of the Firm (RBV)

Incomplete Contracts and the Necessity of Norms

Consider Barney’s (2018: 3305) recent conclusion that “resource-based theory’s model of profit appropriation must incorporate a stakeholder perspective.” This conclusion emerges from the challenges manifested by reliance on incomplete contracts in RBV (among other theories of strategic management). Because “exchanges often evolve in ways that are difficult, if not impossible, to anticipate, these contracts are (almost) always incomplete” (Barney 2018: 3313). Much ink and energy have been devoted to understanding this pervasive contractual incompleteness and the implications of this Hobbesian social contract (or “just so”; cf. Dennett, 1995) story. For RBV, this social contract contains combinations of claims that are fixed, contingent, residual, and so on. So far, so good.

However, this social-contract variant of RBV also requires reference to informal or implicit contracts that are said to cover the eventual consequences of contractual incompleteness. This has the air of a giant error term (though RBV is not alone in this). The idea seems to be that granting stakeholders an access to a residual claim in the content of these unwritten, unspecified, tacit understandings will fill in the gaps where actual (almost always incomplete) contracts stand mute or contested. This large and growing error term of informal and implicit contracts presents a problem because residual claims cannot solve all ambiguousness of incomplete contracts. So what are the terms of these informal contracts?

Fortunately, sociologists, anthropologists, psychologists, and moral philosophers have been thinking about implicit contracts for a long time—referring to them often as values, norms, and ethics. And much of this work, particularly from the social sciences, is empirically validated; normative theorizing should fit quite comfortably within RBV. The creation and execution of incomplete contracts is impossible without full consideration of the underlying social norms and shared values that provide the context both for the initial agreements (the metaphorical whitespace on which the black letters of the contract are written) and their adjudication when terms are breached. Stakeholder-RBV relies on incomplete contracts; incomplete contracts rely on implicit contracts; implicit contracts rely on social and moral norms. In other words, nexus-of-contracts RBV must adopt normative theorizing.

Barney (2018: 3321), notably, disagrees with our argument and joins a long tradition in strategy of hoping to avoid, minimize, or reframe consideration of ethics, norms, and values in theorizing about managing organizations. Many in this tradition place these concerns in footnotes to their influential work. Some examples follow: I originally intended also to include a discussion of dignitarian values and how these influence economic organization. The effort was not successful, however. I regard this as a regrettable shortfall and hope that it will be remedied. Occasional reference to dignity appears in the text (mainly in conjunction with the employment relation and informal organization), and the issues are discussed in a more general way in Chapter 15. A more complete and systematic treatment of the ramifications of dignity for economic organization is sorely needed. The possibility that economic organization is sometimes distorted by excesses of optimism is introduced in section 5.2 of Chapter 1. This too needs development. (Williamson, 1985: 44) Property rights are of course human rights, i.e., rights which are possessed by human beings. The introduction of the wholly false distinction between property rights and human rights in many policy discussions is surely one of the all time great semantic flimflams. (Jensen & Meckling, 1976: 307) A producer’s wealth would be reduced by the present capitalized value of the future income lost by loss of reputation. Reputation, i.e., credibility, is an asset, which is another way of saying that reliable information about expected performance is both a costly and valuable good. . . .The reason, again, is that a reputation for “honest” dealings—i.e., for action similar to those that would probably have been reached had the contract provided this contingency—is wealth. (Alchian & Demsetz, 1972: 778 note 2) The legal concept of “employer and employee” and the economic concept of a firm are not identical, in that the firm may imply control over another person’s property as well as over their labour. But the identity of these two concepts is sufficiently close for an examination of the legal concept to be of value in appraising the worth of the economic concept. (Coase, 1937: 403 note 3)

Aiming to incorporate a stakeholder perspective in RBV, Barney (2018) argues that ethical and socially responsible considerations matter for decision making in business if and only if a particular stakeholder has a strong interest in them. However, if none of the stakeholders is interested in moral responsibility (i.e., all are psychopaths; cf. Bosse & Phillips, 2016: 292), or worse, if stakeholders are actively disdainful of the social norms governing civil society (e.g., put the word “honest” in scare quotes), then “in these settings, ethical or socially responsible decision-making may be much less important in the firm” (Barney, 2018: 3321). Barney seeks to avoid any normative, ethical considerations that would impose a moral standard, writing, Stakeholder resource-based theory takes less of a normative perspective, and much more of a positive perspective. That is, rather than attempting to provide a moral standard against which to judge a firm’s actions, stakeholder resource-based theory makes specific predictions about how profit-maximizing firms will operate. In fact, it generates two broad empirical propositions. . . . In some settings, these empirical assertions may also have prescriptive implications for managers. However, these prescriptions do not claim any moral or ethical superiority.” (Barney, 2018: 3321)

Barney seems to have in mind an absolutist notion of ethics. For example, Kant’s ethics is derived and justified a priori. Empirical considerations run afoul, for Kantians, of a hard distinction between “is” and “ought.” This is not how pragmatic stakeholder theory understands normativity. Empirical observations about coherence (how a set of norms hangs together) and usefulness drive the pragmatist’s understanding of ethics. As James (1907/2014: 78) writes, The greatest enemy of any one of our truths may be the rest of our truths. Truths have once for all this desperate instinct of self-preservation and of desire to extinguish whatever contradicts them. My belief in the Absolute, based on the good it does me, must run the gauntlet of all my other beliefs. Grant that it may be true in giving me a moral holiday. Nevertheless, as I conceive it,—and let me speak now confidentially, as it were, and merely in my own private person,—it clashes with other truths of mine whose benefits I hate to give up on its account. It happens to be associated with a kind of logic of which I am the enemy, I find that it entangles me and metaphysical paradoxes that are inacceptable, etc., etc. But as I have enough trouble in life already without adding the trouble of carrying these intellectual inconsistencies, I personally just give up the Absolute. I just take my moral holidays to me; or else as a professional philosopher, I try to justify them by some other principal.

Much of the resistance to normativity in strategic management, we suspect, is due to a misunderstanding of the role of ethics—particularly within a pragmatic stakeholder theory.

Other RBV scholars make normative prescriptions based on their analysis, calling it “normative implication” or “normative applicability” (Wernerfelt, 2011), suggesting some disparity within RBV regarding the role of values, norms, and ethics. 4 Closer acquaintance with pragmatist ethics may hold the key to reducing this disparity (Dmytriyev, Freeman, Kujala, & Sachs, 2017).

What Is Sustainable?

The term “sustainable” is a key element for both RBV and stakeholder theory. However, each theory offers its own understanding of what it means. RBV uses “sustainable” in a way typical for strategic management by linking “sustained” to competitive advantage. A resource with available substitutes or that is susceptible to imitation may provide a short-term competitive advantage, but competitors are able to accumulate these overlapping resources and eliminate the advantage—the advantage was not sustainable.

Stakeholder theory views “sustainable” as a function of building and maintaining sustainable stakeholder relationships (Freeman, Dmytriyev, & Strand, 2017). For stakeholder theory, sustainability “is determined, in large part, by the extent to which it considers the interests of its stakeholding communities” (Litz, 1996: 1358). Sustainability in stakeholder theory is something that is inherently good because it accounts for stakeholders’ well-being. Differently from RBV, stakeholder theory does not restrain what is good to only some organizations—stakeholder theorists would be the happiest if sustainable stakeholder relationships would be replicable to as many firms as possible, so the whole constellation of firms in the market could build a network of sustainable stakeholder relationships.

One might reasonably object that this is mere semantics. Putting aside the real differences words can make on theory and practice, this distinction evinces a key point of overlap between stakeholder theory and RBV. Sustained stakeholder relationships are themselves a source of sustainable competitive advantage. Seen as a resource, carefully nurtured, trusting stakeholder relationships are valuable and difficult (impossible) to imitate. A firm can attempt to outsource these relationships, but presumably, so can competing firms. To be truly inimitable, stakeholder relationships must be organically homegrown. That is, sustainable stakeholder relationships are a key source of sustainable competitive advantage. Work remains to discover how valuable stakeholder relationships are and whether such sustained stakeholder networks are rare or have effective substitutes.

Whole Foods is a great example of a company that has capably built and enjoyed sustainable stakeholder relationships. In 1981, the largest flood in 70 years covered Austin, Texas, and Whole Foods’s then only store went 8 feet underwater. The loss of all inventory and equipment amounted to $400,000 with no insurance to compensate for it. The founders thought they were out of business, but what happened next can be described as nothing but amazing: Without being asked, dozens of customers and neighbors came to the store the day after the flood to help fix it, employees offered to work for free until the business would be able to pay them again, suppliers offered to deliver goods on credit, and investors and the bank provided additional capital (Mackey & Sisodia, 2013). Well-nurtured, sustainable stakeholder relationships helped Whole Foods, which was on the verge of going bankrupt, get back on its feet and become a successful business with 500-plus stores and over 90,000 employees today.

People as Resources

The role of human beings in RBV is economic. People are often generalized by economists and placed at the same level with factors of production, which reminds us of “greedy reductionism” (Dennett, 1995) in that, instead of explaining a problem, it rather takes us away from it. RBV considers people either as people as labor or people as managers. The former has a long tradition in economics where an economic rent is derived from utilizing such factors of production (an economic term for resources) as land, labor, and capital (Ricardo, 1817/2004).

Today, a firm’s resource profile has become much broader than at the times of Adam Smith and David Ricardo and includes financial resources, physical resources, human resources, organizational resources, technological capabilities, and intangible resources (Mahoney & Pandian, 1992). However, people, as providers of labor, are still classified as human resources (Foss, 2011) or human capital (Coff & Kryscynski, 2011)—just another resource among many other types of resources at a firm’s disposal. This economic tradition is influential in the RBV literature, where people are viewed as “skilled assembly labor” and “unskilled labor” (Wernerfelt, 1984), with some variations, such as basketball players, including Michael Jordan, who are viewed as resources for the Washington Wizards (Molloy, Chadwick, Ployhart, & Golden, 2011).

Alternatively, people in RBV arrive as managers and are allotted the role of resource orchestration (Sirmon, Hitt, Ireland, & Gilbert, 2011), dealing with structuring, bundling, and leveraging firm resources. However, managers are also often viewed as resources when RBV scholars see “top management as a rent-generating resource within the firm” (Castanias & Helfat, 1991: 169) and admit that “top managers certainly are crucial firm resources” (Wan, Hoskisson, Short, & Yiu, 2011: 1353). At times, RBV scholars can emphasize “people as strategically important to a firm” (Barney, Wright, & Ketchen, 2001: 627), though this means that in some situations human resources are more important for achieving sustainable competitive advantage than other resources.

Conversely, in stakeholder literature, one would rarely find a reference to people as “human resources” or “human capital” because stakeholder theorists see people as stakeholders who have “names and faces” (McVea & Freeman, 2005). As mentioned earlier, reference to people as either “resources” or “stakeholders” is more than nomenclature and semantics: Different terms connote different attitudes. Stakeholder theory does not deny the presence of natural, financial, and technological resources in business, but behind these resources are people. Quoting Freeman et al. (2018: 12), The only contradiction arises if one believes that there are disembodied resources floating around that do not involve stakeholders in their acquisition, processing, and transfer—that is, value creation and trade. All resources come unavoidably with people attached. Another implication of pragmatism is that there is no value without valuers. Stakeholder theory puts these people at the center of the story.

Finally, RBV treats people instrumentally, as means to achieving competitive advantage and superior firm performance, while stakeholder theory sees stakeholders as ends in themselves—managers should serve the interests of all stakeholders as a final goal. As Evan and Freeman (1988: 100) argue, “each person has the right to be treated, not as a means to some corporate end, but as an end in itself.” Managing for stakeholders does not mean that a firm needs to compromise its financial performance. On the contrary, a multitude of research on stakeholder management has shown that a firm’s performance improves when it attends to the needs of its stakeholders (e.g., Agle, Mitchell, & Sonnenfeld, 1999; Berman, Wicks, & Jones, 1999; Choi & Wang, 2009; Ogden & Watson, 1999; Ruf, Muralidhar, Brown, Janney, & Paul, 2001).

With this said, the conception of the person in RBV has been evolving over time, and RBV is becoming more robustly human. Consider, for instance, the initial work of Castanias and Helfat (1991) was abundant with phrases such as “top management as a key resource.” Later, however, Castanias and Helfat (2001) wrote about “resources” relative to the skills and abilities that people possess rather than to people themselves. This evolution is rendered more explicit by Wan et al. (2011: 1353), who write, While considerable research attention has been paid to types of resources, the owners/controllers of the resources have yet to attract significant research attention. So far, the only groups of owners/controllers that have received substantial research attention are small, public shareholders and top managers.

We hope that this nascent shift, from people as resources to people as actors who bring resources and make decisions about resources, continues.

Southwest Airlines would be a good example of treating employees with utmost respect (Mackey & Sisodia, 2013) as its dedication to employees became even more vivid during the pandemic. The outbreak of COVID-19 substantially hit air travel, causing the majority of airlines to lay off thousands of employees. Southwest chose a different approach (Arnold, 2020), described well by Laurie Winters, its senior director of culture and engagement: We truly believe that if we take care of our employees, they in turn will take care of our customers. Other companies in our position immediately start thinking about downsizing. In our 49 year history, we have never had a layoff or furlough, and our executive team has made it very clear to our employees that that would be an absolute last resort. Have we been in a crisis? Yes. So that’s even more reason to do everything we can to support our employees. We view ourselves as a family and when times are hard, families take care of each other. (Lauchlan, 2020)

Balancing Competition and Cooperation

When the Journal of Management last took stock of RBV, Makadok (2011: 1316) opened his remarks by noting in the first line of the abstract, “As a theory of profit, resource-based theory is focused on a single causal mechanism—competitive advantage.” He moves from there to discussing the limitations of, and alternatives to, this narrow focus. Here, at the crossroads of RBV and stakeholder theory, we will follow suit by shining light on the prospects for sustainable cooperative advantage.

According to Freeman et al. (2018), For some—informed by Competitive Strategy—all business relationships are primarily, perhaps exclusively, competitive. Stakeholder theory takes a more nuanced view, recognizing that there are both cooperative and competitive elements to economic relationships.

The tension between competition and cooperation is among the most intriguing challenges confronting strategic management. Ambitious managers want the entire organization to succeed but also want to see themselves promoted ahead of others. Nor does the question become easier once the boundaries of the organization are called into question. As cooperation becomes increasingly important with actors previously thought to be outside the firm’s boundaries, managers are forced to reconsider how to manage such semicompetitive/semicooperative relationships. Models of strategic management emphasizing competition are ill suited for understanding complex, global, contemporary commerce.

A more nuanced perspective on this tension in strategic management is already emerging among stakeholder scholars (Bridoux & Stoelhorst, 2014; Bridoux & Vishwanathan, 2020; Bundy, Vogel, & Zachary, 2018; Garriga, 2009; Martin & Phillips, 2021). Makadok’s characterization of RBV above notwithstanding, the prospects for an RBV based on sustainable cooperative advantage is an intriguing prospect.

General Motors’s (GM) procurement strategy under the leadership of Jose Ignacio Lopez, the newly appointed head of purchasing operations, is a striking example of how overemphasis on competition at the expense of cooperation may become detrimental. Lopez shredded long-standing contracts with established suppliers demanding lower prices (Freeman et al., 2017). It worked in the short term by providing GM with over $3 billion in savings, but in the long run, the tension with the suppliers hit innovation and quality at GM, leading to the significant loss in its market share to Japanese carmakers.

Reconciling RBV and Stakeholder Theory

Arguably the first to open the black box that is the firm, Ronald Coase (1937: 393) envisioned such a synergetic effect when he mentioned that “a firm . . . consists of the system of relationships which comes into existence when the direction of resources is dependent on an entrepreneur.” Coase considered the combination of relationships and resources as the main reason for a firm’s existence. Relationships in an organization supersede the burden of contract costs that entrepreneurs would otherwise bear in an open market regulated by a price mechanism. That is why stakeholder relationships should be of utmost importance for the firm, since they define the firm’s existence in the first place.

Reconciling stakeholder theory and RBV is a promising path to advancing our understanding of strategic management. It provides a two-part guideline to management scholars and practitioners:

It is important to build sustainable stakeholder relationships because stakeholders enable a firm to exist (Coase, 1937), because stakeholders are vital to the survival and success of the firm (Freeman, 1984), and because it is simply the right thing to do from an ethical perspective (Donaldson & Preston, 1995).

Using the resource-based perspective of the firm is a powerful framework to build sustainable stakeholder relationships (Harrison et al., 2010; Tantalo & Priem, 2016) and to help a firm succeed (Barney, 1991; Wernerfelt, 1995).

If this twofold overarching guideline gives promise to better management practices and better society, then we need further scholarship to develop details on how the unified view will work in practice.

Conclusion

RBV and stakeholder theory are both fundamental theories in management, and their scholarship has grown exponentially over the past 35 years. However, their development paths, though started from the same origins, evolved in parallel. Only recently have the two theories received a chance to learn from each other.

In this article, we demonstrated that RBV, in its current form, is incomplete and can become a more comprehensive theory by incorporating four essential elements from stakeholder theory: (a) incorporating normativity, (b) recalibrating the idea of sustainability, (c) viewing people beyond resources, and (d) allotting more room for cooperative behaviors.

Though RBV and stakeholder theory are effective frameworks for addressing management issues on their own, we believe their greatest potential is in their combination. The unified approach can help explain raison d’être for a firm’s existence as well as deliver on its promise. Apparently, this is what the CEOs of Business Roundtable companies intended to achieve when they redefined the purpose of a corporation to promote the well-being of its stakeholders: customers, employees, suppliers, communities, and shareholders (Business Roundtable, 2019). Time will tell if these firms follow through on this rhetoric, but it is a promising move in what we feel is the right direction.