Abstract

Over the past two decades, scholars of management, finance, accounting, economics, and entrepreneurship have studied the concept and implications of executive confidence in diverse settings. Despite sustained scholarly attention, numerous definitions, interpretations, and operationalizations of executive confidence present a problem for understanding past research and informing future progress. Equally problematic is that past research remains scattered across multiple disciplines, lacking a cohesive and comprehensive integration. Based on an in-depth review of 118 executive confidence studies and 268 studies in the wider confidence literature, we marshal the literature into four overarching themes for an encompassing understanding: (i) conceptualization of executive confidence, (ii) governance mechanisms and pathways of influence, (iii) implications and outcomes, and (iv) origins and antecedents. We leverage the insights of our review to discuss a richer conceptualization of executive confidence and chart an agenda for future research across each of the four themes of our review.

Keywords

Executive confidence has received much attention from researchers and practitioners (e.g., Picone, Dagnino, & Mina, 2014). Strategy and finance researchers have examined its influence on various firm actions and outcomes—such as the level of acquisitiveness (Malmendier & Tate, 2008), R&D investment (Koh, Reeb, & Zhao, 2018), and product innovation (Simon & Houghton, 2003). Accounting researchers have examined whether confidence is associated with adverse firm outcomes such as accounting misstatements and earnings manipulations (Ahmed & Duellman, 2013; McManus, 2018). Entrepreneurship researchers have linked founders’ confidence to the willingness to start a new venture (Koellinger, Minniti, & Schade, 2007) and the ultimate success of the venture (Hayward, Shepherd, & Griffin, 2006; Lowe & Ziedonis, 2006). And organizational behavior and psychology researchers have examined the effects of confidence on diverse individual behaviors and outcomes with implications for understanding executive confidence—such as creativity (Hu, Erdogan, Jiang, Bauer, & Liu, 2018), risk perceptions (Li & Tang, 2010), and career success (Stajkovic, 2006).

Despite the proliferation of studies across multiple disciplines and significant empirical progress, our understanding of executive confidence has been thwarted by four interrelated ambiguities. The first is a lack of construct clarity concerning the essence of executive confidence and an unclear distinction from the related constructs of executive narcissism, hubris, core self-evaluation, optimism, and even humility. Although several prior efforts focus on the multifaceted nature of overconfidence (e.g., Brunzel, 2021; Moore & Healy, 2008; Stajkovic, 2006), the efforts consider only a subset of the problem (i.e., they focus on overconfidence rather than confidence generally and do not distinguish confidence from related constructs). The upshot has been an emphasis on narrow facets of confidence employing similar measures as those used to capture related constructs, resulting in a set of incommensurate findings. The second ambiguity concerns the explanatory mechanisms through which executive confidence influences firm behavior and outcomes. Currently, little work explicitly examines the governing mechanisms through which confidence operates and influences firm behavior and outcomes. A third ambiguity is whether and under what conditions executive confidence is ultimately beneficial or detrimental. And finally, it remains unclear how executive confidence forms, crystallizes, and evolves.

We synthesize and advance the current research and understanding on executive confidence using these four ambiguities as overarching themes to review the disparate literature on executive confidence. The review encompasses the core body of studies across several disciplines and the broader literature on confidence and related constructs such as hubris, optimism, narcissism, core self-evaluation, and humility. This review approach enables us to integrate and present the rich tapestry of research insights on the four themes and, in so doing, to offer a coherent and accurate portrayal of what is known, knowable, and unknown regarding executive confidence.

We then leverage those review results to offer an integrated set of proposals and future research directions for advancing each theme, including (a) conceptualizing executive confidence—its core meaning and underlying dimensions, including similarities and differences to related and overlapping constructs; (b) the attendant governing and causal mechanisms; (c) the influence of executive confidence on firm behavior and outcomes, including whether executive confidence ultimately adds or destroys value; and (d) the origins and antecedents of executive confidence. Together, our study can serve as a “one-stop shop” for a holistic insight into the vast and complex body of research on executive confidence and as an inspiration for future directions that can drive the next wave of research.

Review Method

The review method involved a multiphase process: systematically searching, content-coding, synthesizing, and interpreting individual studies and all studies together (Tranfield, Denyer, & Smart, 2003). We searched for published articles in select journals from 12 disciplines using a list of keywords such as confid*, underconfid*, and overconfid* across 62 journals (see Online Appendix 1 for a list of journals). Even though our focus is on executive confidence, we also review confidence studies more widely to capture relevant insights.

We selected journals from the top tier of publications using the Chartered Association of Business Schools (2018). Where there were a limited number of 4* journals in a discipline, we selected the tier immediately below 4*. We performed keyword searches across 62 journals resulting in an initial sampling frame of 1,999 articles. We reviewed the title, keywords, and abstract of each article. We subsequently eliminated articles where (a) confidence was not a central construct of interest; (b) confidence was discussed in the distal context of eyewitness testimony, motor skills, or in rating tasks; or (c) confidence was mentioned only in fleeting terms or referred to trustworthiness and other misassociations.

All told, we identified 386 articles where confidence was a significant construct of interest. Of these, 118 articles (31%) directly concerned executive confidence (or, in the case of new ventures or start-ups, entrepreneurial confidence). In terms of disciplinary coverage, half of the studies were published in accounting, finance, and economics journals, with the remainder published in general management journals (16.9%), strategic management and entrepreneurship journals (30.5%), and other journals (2.5%). We followed a two-phase approach to synthesize these 386 articles. We first conducted an in-depth content coding of the 118 articles on executive confidence. We then reviewed the remaining 268 wider confidence studies focusing primarily on their conceptualization of confidence.

Because executive confidence overlaps with several related constructs, we also performed a series of supplementary searches. Using the same set of 62 journals, we searched for articles on executive narcissism, hubris, core-self-evaluation, optimism, and humility. Upon reviewing these articles in detail, we found 65 dealt with at least one of these five related constructs in an executive population and incorporated the information gleaned from these articles into our review, where appropriate.

Findings on Four Interrelated Themes of Ambiguity

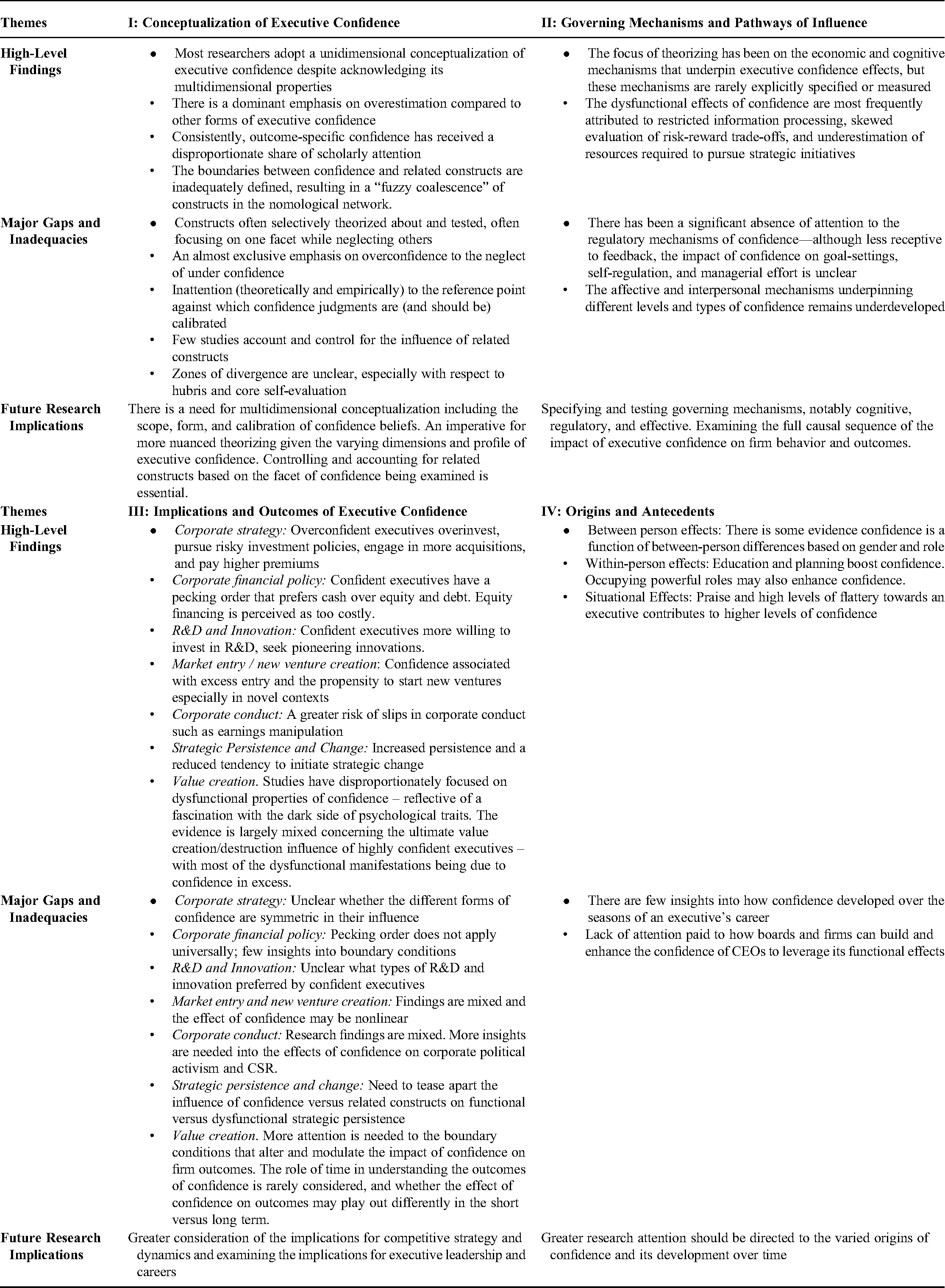

In this section, we present our findings concerning the before mentioned themes and supplement our discussion with a summary in Table 1. In the following section, we leverage these results to offer proposals and future directions to advance extant research by addressing each theme. The first theme focuses on conceptualizing executive confidence—its core meaning and underlying dimensions, including similarities and differences to the related and overlapping constructs. The second theme focuses on the attendant governing and causal mechanisms. The third theme is its influence on firm behavior and outcomes, including whether executive confidence ultimately adds or destroys value. The final theme focuses on the origins and antecedents of executive confidence.

An Integrative Synthesis of Research on Executive Confidence

Theme I: Conceptualization of Executive Confidence

Our review revealed an array of conceptualizations and accompanying measurements. Notwithstanding earlier efforts (e.g., Moore & Healy, 2008; Stajkovic, 2006), inconsistency in definitions and heterogeneity in measurement persist. A significant proportion of studies (39.8%) do not offer a formal or explicit definition of confidence. The propensity for authors to define confidence is higher in general management (70%) and strategic management or entrepreneurship (66.7%), than in accounting, economics, and finance (50.8%). A visual representation of disciplinary differences is provided in Online Appendix 2, and a list of definitions is provided in Online Appendix 3 and 4. Our review revealed two significant sources of heterogeneity in definitions—form and scope. We provide a summary of our key findings in Table 2. We then turn our attention to the issue of construct confounding.

Sources of Heterogeneity in Executive Confidence Definitions

Heterogeneity in the form of executive confidence

To Moore and Healy (2008), there are three forms of overconfidence: overestimation, overprecision, and overplacement. Overestimation pertains to an inflated perception of one’s actual “ability, performance, level of control, or chance of success relative” to objective standards (Moore & Healy, 2008: 502). Overestimation is observed when CEOs “generally think they are better than they are in terms of skill and judgment or in gauging the prospects of a successful outcome” (Ho, Huang, Lin and Yen, 2016: 195). Overprecision occurs when executives exhibit “excessive certainty” regarding the accuracy of beliefs (Moore & Healy, 2008). Overprecision is observed when executives provide specific point estimates with narrow confidence intervals in their forecasts or predictions of outcomes (Hackbarth, 2009; Hayward & Fitza, 2017; Hilary, Hsu, Segal, & Wang, 2016; Levi, Li, & Zhang, 2014). Overplacement occurs when “people believe themselves to be better than others, such as when a majority of people rate themselves better than the median” (Moore & Healy, 2008: 502).

Where there was enough information in each article to classify the form of executive confidence (n = 75, see Online Appendix 2 for a visual summary), we found that the preponderance of studies conceptualized overconfidence in the form of overestimation (57.3%), a tendency consistent across disciplines. Fewer conceptualized confidence as overplacement (17.3%) and overprecision (12%). Only a handful of studies embraced a multidimensional conceptualization (8%). We observed a similar pattern concerning the wider confidence literature where the preponderance of studies focused on overestimation (38.6%), and only a handful of studies embraced a multidimensional conceptualization. This pattern of findings highlights that most studies focus on a single subdimension of the confidence construct, raising the question of whether the empirical findings generalize across dimensions.

Heterogeneity in the scope of executive confidence

Several definitions summarized in Table 2 refer to confidence as an “overriding” (Chakravarty & Hegde, 2019) or general belief (Navis & Ozbek, 2016, 2017). Similarly, the broader literature often defines confidence as a general tendency that permeates time, tasks, and situations and constitutes deep-seated beliefs about one’s competence, capability, and acumen. About a fifth of studies (where classification was possible) conceptualize executive confidence as generalized in scope (21.6%). However, disciplinary differences exist—general management studies are more likely to embrace a generalized conception of executive confidence (30%) than accounting, economics, and finance studies (6.8%). This is particularly the case in studies that define confidence as a cognitive (Barbosa, Fayolle, & Smith, 2019; Li, Petruzzi, & Zhang, 2017; Lowe & Ziedonis, 2006) or behavioral bias (Bailey, Kumar, & Ng, 2011). Much attention has been placed on the generalized tendency of executives to overestimate perceptions of ability and competence relative to their actual ability (Hirshleifer, Low, & Teoh, 2012; Lee, Hwang, & Chen, 2017), or the ability of peer groups (Navis & Ozbek, 2016).

At the same time, confidence has also been conceptualized as specific to tasks (19.3%), outcomes (42.0%), and situations (3.4%). Task-specific confidence reflects beliefs in one’s ability or competence limited to a task domain (e.g., creating value from acquisitions) or a set of interrelated task domains (e.g., creating firm value). Among CEOs and CFOs, this frequently relates to the ability to create value from corporate activities such as acquisitions and capital investment programs (Benson & Ziedonis, 2010; Hilary & Hsu, 2011; Huang & Kisgen, 2013; Leung, Tse, & Westerholm, 2019; Malmendier & Tate, 2008).

Confidence can similarly be specific to situations and outcomes. In terms of the former, executives may exhibit confidence in particular contexts but not others—for example, a CEO may feel confident about a specific acquisition where the executive feels they can generate unique synergies (e.g., Devers, McNamara, Haleblian, & Yoder, 2013). In terms of the latter, confidence is often linked to expectancies, predictions, and forecasts of positive outcomes (e.g., Chen, Rennekamp, & Zhou, 2015; Cooper, Folta, & Woo, 1995). It also occurs when executives overestimate past or future performance relative to some standard (Adam, Burg, Scheinert, & Streitz, 2020; Chu, Dechow, Hui, & Wang, 2019; Hyytinen, Lahtonen, & Pajarinen, 2014), or the returns from projects and investments such as R&D expenditures (Koh et al., 2018).

Construct confounding

Confidence is often inadequately distinguished from related constructs in its nomological network (Podsakoff, MacKenzie, & Podsakoff, 2016). To Singh (1991), when concepts are not adequately distinguished from each other, it is likely to “(a) lead to confusion among researchers because some of them see the concepts as distinct entities and build streams of research around one of them, whereas other scientists treat them interchangeably and (b) raise questions about our cumulative understanding of the antecedents, correlates, and consequences of the concept (or concepts) of interest” (cited in Podsakoff et al., 2016: 166). Adding to the confusion, measures of confidence and related constructs frequently overlap. Some scholars have used specific measures interchangeably for different constructs, obscuring the meaning of any resultant findings.

We find that executive confidence particularly overlaps and covaries with the constructs of narcissism, hubris, core self-evaluations, optimism, and humility. Indeed, we encountered several studies where confidence was presented under the guise of another construct. For example, Chen, Rennekamp et al.’s (2015) study of forecast optimism and accuracy defined optimism as a general tendency for forecasts to be too high relative to actual outcomes. This conceptualization is synonymous with overestimation. Likewise, studies of hubris are often based on arguments centered on overconfidence while defining hubris more broadly as exaggerated self-pride and overconfidence (e.g., Hayward & Hambrick, 1997). And there is continuing confusion as to the exact conceptual boundaries between core self-evaluation and confidence (Hiller & Hambrick, 2005), where overconfidence ends and narcissism begins (Kim, Xiong, & Kim, 2018), whether humility represents the absence of confidence, or whether high levels of confidence represent the absence of humility (Dunn, Chen, Proul, Ehrlinger, & Savalei, 2021).

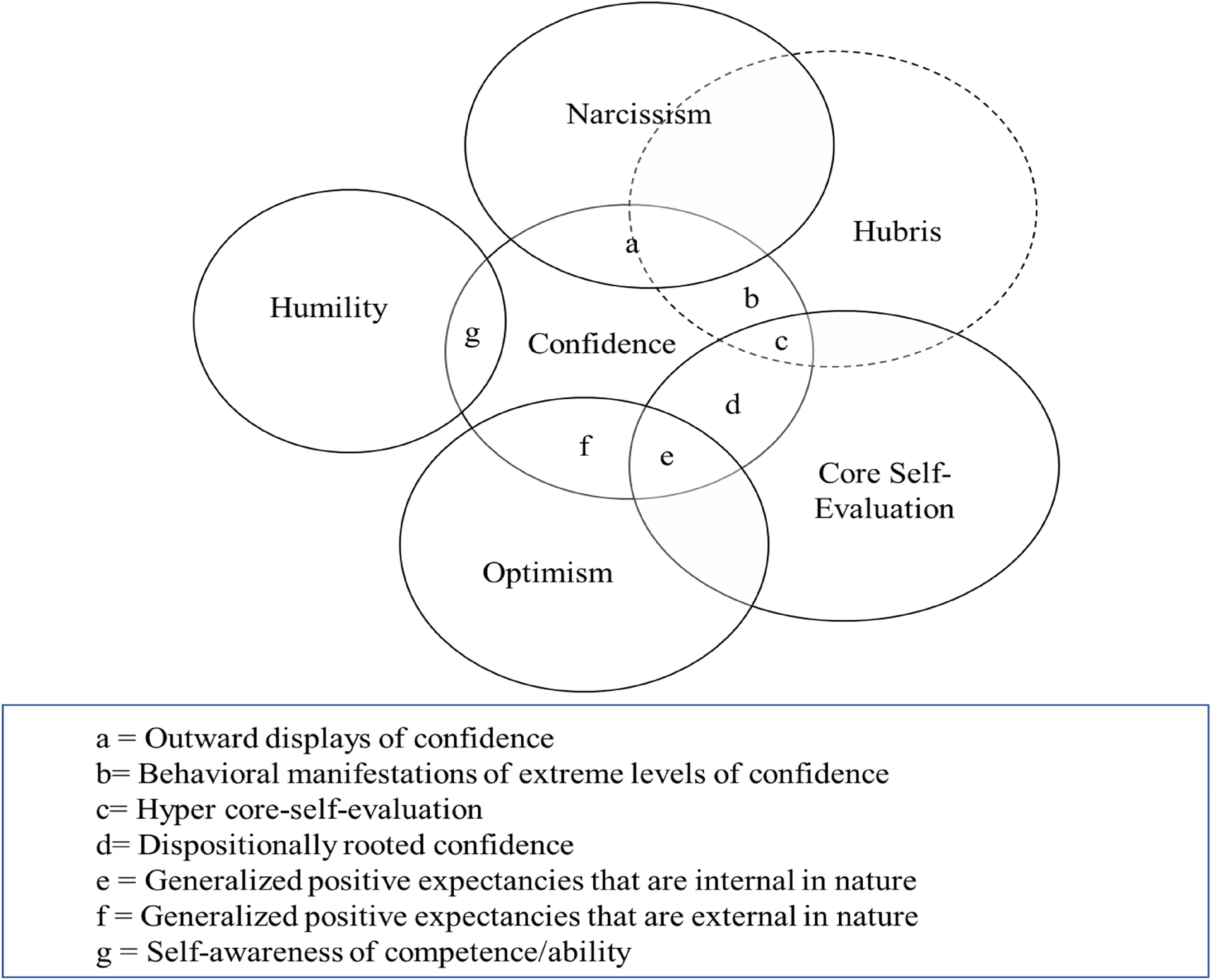

Therefore, it is imperative to differentiate and relate these constructs to executive confidence before proceeding to the remaining themes. As summarized in Table 3 and visualized in Figure 1, we submit that confidence is a common denominator among these constructs. Next, we discuss and delineate the zones of convergence and divergence of executive confidence and these other constructs in its nomological network.

Distinguishing Executive Confidence from Related Constructs

Disentangling Executive Confidence from Related Constructs Within Its Nomological Network a

Letters denoted in italics within the zones of convergence column correspond to the lettered areas identified in Figure 1.

Narcissism

Anglin, Wolfe and colleagues (2018: 780) define narcissism as an “exaggerated—albeit fragile—sense of one’s self-importance or influence,” characterized by a persistent preoccupation with success and grandiose thinking. For executives, narcissism can manifest in a constant need for acclaim and decision-making control (Chatterjee & Pollock, 2017). While narcissists undoubtedly engage in outward displays of confidence, there are three crucial differences. First, there is no theoretical or empirical basis for believing that narcissists are more confident than others. Indeed, a narcissist’s need for constant reaffirmation may instead indicate the absence of innate confidence. For instance, the documented tendency of narcissistic CEOs to hire lower status and less experienced executives (Chatterjee & Pollock, 2017) could be interpreted as a lack of confidence in their leadership abilities. Second, and perhaps more significantly, the conceptual territory of narcissism far exceeds that of confidence. According to the American Psychiatric Society, the clinical criterion for narcissism includes “a lack of empathy towards others, a sense of entitlement towards favorable treatment, preoccupation with fantasies of unlimited success, power, brilliance or beauty” (Brunzel, 2021: 590). Third, narcissism is a relatively stable trait (O'Reilly & Chatman, 2020; O'Reilly & Hall, 2021), whereas confidence can be steady or transient and particularized to tasks, outcomes, and situations.

Hubris

Hubris is an inherently nebulous construct that has not been extensively validated in measurement studies. Instead, as it relates to executive confidence, it is often a label applied to situations such as when a CEO overpays for an acquisition (Hayward & Hambrick, 1997; Roll, 1986) or otherwise engages in outsized, even ostentatious actions. Hubris has been commonly invoked as an explanation for the behavior of executives in the banking sector leading to the financial crisis (e.g., Brennan & Conroy, 2013; Lawrence, Pazzaglia, & Sonpar, 2011). Therefore, there has been a considerable variance in the definition of hubris. For example, whereas Aktas and colleagues (2011: 20) define hubristic CEOs as overestimating their “capacity to create value when buying targets,” other scholars have attached surplus meaning to the concept to include the “abuse of power” (Berger, Osterloh, Rost, & Ehrmann, 2020: 5) and “arrogance” (Sundermeier, Gersch, & Freiling, 2020: 1038). Thus, the term hubris could be applied to describe extreme confidence levels (e.g., Brunzel, 2021; Hayward et al., 2006), but it is all too often used to describe the behavioral manifestations of confidence as distinct from a particular level of confidence. Based on the balance of evidence we reviewed, hubris can be best characterized as the outward manifestations of excessive confidence levels or core self-evaluation (in the latter case, it may be most accurately referred to as hyper-core self-evaluation, Hiller & Hambrick, 2005).

Core self-evaluation

Hiller and Hambrick (2005: 299) defined core self-evaluation as a “deeply sourced dispositional trait that defines how we evaluate ourselves and our relationship with the environment” with individuals possessing this trait “characterized by self-confidence, self-worth, self-potency, and freedom from anxiety.” While core self-evaluation is deeply rooted, the focus of the overconfidence literature has been mainly on its nondispositional origins. Aside from the more varied origins and scope of executive confidence, core self-evaluation is a much broader construct capturing generalized self-efficacy, internal focus of control, self-esteem, and emotional stability (Chng, Rodgers, Shih, & Song, 2012). While confidence and core self-evaluation overlap conceptually in capturing positive evaluations of competence, we would hasten to add that confidence has more varied origins, may be less enduring (evaporating quickly in some instances), and does not necessarily imply high self-worth or emotional stability.

Optimism

At their core, optimists are “people who expect things to work out well for them; pessimists are people who expect things to work out badly” (Carver & Scheier, 2018: 214). Optimism thus represents the “belief that, in general, good things will happen in the future” (Purol & Chopik, 2021: 2). Fundamentally, optimism represents a set of generalized expectancies about the future that exists even when such longings are not rationally justified (Hmieleski & Baron, 2009). Critically, the focus is not on whether an individual can affect a favorable outcome through applying their abilities and influence. Instead, it is a more generalized expectancy regarding whether positive results will occur (Zuckerman, 2001). Even in the absence of confidence, optimists may forecast positive future performance, perhaps because of external factors. This might explain why optimism in the extreme is detrimental to firm performance (Campbell, Gallmeyer, Johnson, Rutherford, & Stanley, 2011; Hmieleski & Baron, 2009). Confident individuals are not necessarily optimistic but, instead, expect positive outcomes due to a subjective assessment of their ability to exert control and influence.

Humility

Finally, humility is grounded in a “self-view that something greater than the self exists” (Ou et al., 2014: 37). Humility is also multidimensional, manifesting in self-awareness, openness to feedback, appreciation for others, and self-transcendent pursuit (Ou et al., 2014). To our knowledge, there is no empirical evidence of significant overlap between the constructs of executive confidence and humility. The beneficial effects of humility in leadership empowerment, top management team integration, and middle managers’ job satisfaction (see Ou et al., 2014, 2017, 2018) have not been investigated concerning executive confidence, but this is an interesting path to pursue.

Having clarified the key sources of heterogeneity in confidence and demarcated its conceptual character vis-a-vis related constructs, we now turn to the governing mechanisms underpinning the influence of confidence on firm behavior and outcomes.

Theme II: Governing Mechanisms and Pathways of Influence

By extracting the mechanisms theorized to underpin the influence of executive confidence, we uncovered five categories of purported theoretical mechanisms: cognitive, economic, regulatory, resource, and affective. Where it was possible to classify these mechanisms, the focus of theorization is consistent with the disciplinary focus of prior research—economic (37.1% of studies) and cognitive (23.1% of studies) mechanisms, and to a lesser extent on resource mechanisms (20.6% of studies), which constitute the majority of studies. Far less attention has been devoted to the regulatory (8.2% of studies) and affective mechanisms (2.1% of studies). We discuss each mechanism category and supplement our discussion with further details by discipline in Online Appendix 2.

Cognitive mechanisms

These mechanisms refer to how executives notice relevant stimuli, interpret information, make decisions, and learn. A common argument in the literature on executive confidence—and the broader literature on confidence generally—is that highly confident individuals engage in restricted information processing (Audia, Locke, & Smith, 2000; Bloomfield, Libby, & Nelson, 1999) and are susceptible to cognitive blind spots (Scott, Dienes, Barrett, Bor, & Seth, 2014). This restriction leads them to overweight private information (Hayward, Rindova, & Pollock, 2004), take an inside view of problems (Hyytinen et al., 2014), and harbor illusions of knowledge (Barber & Odean, 2002). Others have suggested that overly confident executives deviate from the rational model of decision-making by adopting a narrow framing (Bailey et al., 2011), truncating search (Mahajan, 1992), considering a limited number of options (Vecchiato, 2020), and relying on heuristics to navigate uncertain environments (Malhotra, Morgan, & Zhu, 2018).

Economic mechanisms

These mechanisms capture executives’ perceptions of and preferences for elevated risk-taking, including how they quantify the upside and downside of initiatives with differing risk profiles. Studies across disciplines similarly invoke the argument that executives high in confidence underestimate the riskiness of courses of action (Adebambo & Yan, 2018; Simon & Houghton, 2003). In other cases, entrepreneurs fail to acknowledge the presence of risk in the first place fully. For example, Barbosa et al. (2019) find that when entrepreneurs are primed to think about positive outcomes and situations are framed to focus on probabilities of success, they tend to overestimate their odds of success, holding constant the odds of success they require to take a risk. Confidence may skew executives’ beliefs about the likelihood of success and failure in specific projects and endeavors, such as R&D (Benson & Ziedonis, 2010; Kim et al., 2018) and market entry (Navis & Ozbek, 2016, 2017; Simon, Houghton, & Aquino, 2000).

Confidence is also argued to influence executives’ risk preferences and their willingness to accept higher levels of risk (Hirshleifer et al., 2012; Ho, Huang, Lin, & Yen, 2016). For example, multiple studies have linked the presence of overconfidence with increased investments in R&D and, relatedly, a higher likelihood of innovation (Galasso & Simcoe, 2011; Kim et al., 2018; Simon & Houghton, 2003; Tang, Li, & Yang, 2015). Likewise, overconfidence (and the related construct hubris) is predictive of acquisitiveness in many settings (Hayward & Hambrick, 1997; Leung et al., 2019; Levi et al., 2014; Malmendier & Tate, 2008; Renneboog & Vansteenkiste, 2019). It is also predictive of corporate financing choices such as the choice to employ performance-sensitive debt (Adam et al., 2020), financing with short-term debt (Huang, Tan, & Faff, 2016), currency speculation (Beber & Fabbri, 2012), as well as aggressive accounting practices (Ahmed & Duellman, 2013) and fraud (Davidson, Dey, & Smith, 2015).

Regulatory mechanisms

Regulatory mechanisms represent how executives set goals, monitor different performance cues, and persist in the face of obstacles and feedback. There is little direct evidence that confident executives set more ambitious and audacious goals than those who are not confident. But the linkage between executive confidence and persistence, or commitment to previously selected goals and strategies is well-established. Overconfidence appears to dull the impact of feedback from prior errors (Chen, Crossland, & Luo, 2015), market reactions to products (Lowe & Ziedonis, 2006), and failed projects (Kim, Wang, & Zhang, 2016). Evidence also suggests that overconfidence may engender resilience that can be harnessed to productive ends by buffering social stress in high-pressure situations (Ronay, Oostrom, Lehmann-Willenbrock, Mayoral, & Rusch, 2019).

Resource mechanisms

Resource mechanisms capture executive assessments of relevant abilities, competence, and access to needed capital and labor. Highly confident executives tend to overestimate and overplace their competencies and capabilities (Moore & Healy, 2008) and, by extension, those of their firm (Hiller & Hambrick, 2005). As a result, overconfident leaders are posited to overestimate their abilities to manage (Hayward et al., 2006) while underestimating the information or resource requirements for successful execution (Chen, Ho, & Yeh, 2020; Cooper et al., 1995; Hayward & Hambrick, 1997; Kim et al., 2018). This mechanism manifests in the tendency of highly confident executives to focus on their abilities to the neglect of competitors (Artinger & Powell, 2016; Cain, Moore, & Haran, 2015). Consequently, overly confident executives risk expanding their firms into already crowded product and market arenas (Cain et al., 2015). In acquisitions, CEOs are willing to pay a premium for acquisition targets (e.g., Roll, 1986) because they perceive they can create more value than current management (e.g., Devers et al., 2013; Hayward & Hambrick, 1997).

Affective mechanisms

Finally, there has been some focus on the idea that confidence may influence behavior via positive emotions. In a series of studies investigating the relationship between overconfidence and competence perceptions, Ronay et al. (2019: 5) presented evidence of the role of affective robustness, “an individual difference that makes some individuals less susceptible to affective changes in response to stressful circumstances.” They found that affective robustness mediated the relationship between overconfidence and competence perceptions. Within the broader literature, some studies have shown that task confidence is positively associated with positive emotions and inversely related to negative emotions (Fisher, Minbashian, Beckmann, & Wood, 2013).

Theme III: Implications and Outcomes

A central thrust of theoretical and empirical effort has been understanding the implications and consequences of executive confidence for firm behavior and conduct. We organize and review this focus in terms of core areas of focus.

Corporate strategy

A key stream of research addresses how confidence might influence corporate investment, resource allocation, and mergers and acquisitions. Overconfidence among investors (both in executive and nonexecutive populations) has been associated with active, aggressive, and excessive trading (Barber & Odean, 2002; Doskeland & Hvide, 2011; Gervais & Odean, 2001; Graham, Harvey, & Huang, 2009; Grinblatt & Keloharju, 2009; Kyle & Wang, 1997; Odean, 1998). In one of the most influential executive confidence studies, Malmendier and Tate (2005: 2662) found that overconfident CEOs overinvest, partly because “overconfident CEOs systematically overestimate the return to their investment projects.” Confident executives are also more likely to pursue acquisitions and pay a premium for acquisitions than less confident executives (Chen, Hsu, Officer, & Wang, 2020; Croci & Petmezas, 2015; Leung et al., 2019; Malmendier & Tate, 2008; Yim, 2013). Malmendier and Tate (2008) find using multiple measures that not only are overconfident CEOs more likely to conduct acquisitions at any point in time, but a significant subset is likely to engage in acquisitions that do not warrant the premium paid. Because highly confident executives have conviction in their ability to create value from corporate transactions (Roll, 1986) and are susceptible to the “better-than-average effect” (Moore & Healy, 2008), overconfidence is associated with the payment of large premiums for acquisitions. Interestingly, while overplacement is often inferred in such studies, many of those studies tend to operationalize it as over-estimation.

Predicting gender differences in confidence, Huang and Kisgen (2013: 824) find that men undertake more acquisitions than women. Similarly, Levi et al. (2014) find that companies with female directors are less likely to initiate acquisition bids—and when they do, they are less likely to pay a premium for the target firms. Using a proxy measure of overconfidence, Leung et al. (2019) found that CEOs that trade more frequently are likely to acquire. More recently, in a study of high-technology acquisitions following industry awards, Chen, Hsu et al. (2020) found that award-driven acquisitiveness is more pronounced among firms with more confident CEOs.

While we have learned much about how confidence influences corporate strategy, blind spots remain. For example, it remains to be seen whether the influence of overestimation, overprecision, and overplacement are symmetric in their impact. Most studies blur these distinctions, but Roll’s (1986) hypothesis would imply that the premium paid for acquisitions is most likely to be influenced by overplacement. Likewise, the influence on confidence on the core processes of the corporate strategy remains unclear. Do overly confident executives fail by, for example, picking the wrong targets, evaluating them inadequately, and/or integrating them poorly?

Corporate financial policy

Researchers have also found that confidence influences how executives choose to finance their corporate investments. In general, a pecking order has been established that prioritizes internally generated cash. Overconfident CEOs prefer cash holdings to fund their investments because equity financing is thought to be costly (Malmendier & Tate, 2005), as confirmed by Malmendier, Tate, and Yan (2011). As a result, their investments are susceptible to cash flows (Malmendier & Tate, 2005). Perhaps because of their sensitivity to internal cash flow, firms with overconfident CEOs tend to derive more value from their cash holdings than those without, particularly in settings where underinvestment is common (Aktas, Louca, & Petmezas, 2019). Recent studies provide corroborating evidence. Huang et al. (2016) find that firms with overconfident CEOs have a higher proportion of debt with a short horizon maturation, likely because overconfident CEOs believe they can refinance the debt on more favorable terms than their counterparts. Likewise, Adam et al. (2020) reported that overconfident executives are more likely to use riskier performance-sensitive debt (PSD) for debt financing than their counterparts.

Despite progress, ambiguities remain. For example, some studies highlight the nonuniversality of the pecking order. Using measures of both overoptimism (growth perceptions bias) and overconfidence (risk perceptions bias), Hackbarth (2008) found that while managers displaying a growth perceptions bias perceive a higher cost to issuing equity compared to debt, managers with a risk perceptions bias viewed equity more favorable to debt. More research into the boundary conditions—such as governance regime and incentive structures—is needed, such as Dittmar and Duchin’s (2016) finding that professional experience tempers the influence of confidence on the aggressiveness of financial policies. A related question is whether executive confidence influences access to and favorability of funding, as research on optimism suggests (Dai, Ivanov, & Cole, 2017).

R&D and innovation

Consistent with the argument that overconfident executives underestimate the risks and overestimate the potential success of discrete initiatives, confidence is associated with higher levels of investment in R&D and innovation—specifically “big bets,” pioneering innovation. In a field study of small firms in the computer industry, Simon and Houghton (2003) found that overconfident managers were more likely to introduce pioneering rather than incremental products. Hirshleifer et al. (2012) find that overconfident CEOs invest more heavily in R&D and achieve greater innovative outcomes measured in terms of patent and citation counts than CEOs that are not overconfident, even after controlling for the level of R&D expenditures. This concords with Galasso and Simcoe’s (2011) finding that the arrival of an overconfident CEO is associated with a 25% to 35% increase in citation-weighted patent counts. Like Hirshleifer and colleagues, Galasso and Simcoe (2011) find that the relationship between executive confidence and innovation is stronger in certain industries. Most recently, Tang, Li et al. (2015) observed a robust association between executive overconfidence and innovation in a cross-sectional survey of Chinese CEOs in manufacturing firms and a longitudinal sample of U.S. high-tech firms.

Missing, however, are fine-grained insights into the types of innovation and R&D policies pursued by confident executives and how the motivation to invest in R&D and innovation may vary depending on the kind of confidence. There is some evidence that narcissists may be drawn to exploratory, discontinuous innovations—precisely because the pursuit of a discontinuous innovation gives the CEO the attention they crave (Gerstner, Konig, Enders, & Hambrick, 2013; see also, Kashmiri, Nicol, & Arora, 2017 for the effect of CEO narcissism on radical innovations). But confident executives may not necessarily share this motivation.

Market entry and new venture creation

Several studies have examined the influence of executive confidence on entry into new markets and on other entrepreneurial behaviors, such as entrepreneurial action (Brundin, Patzelt, & Shepherd, 2008) or venture creation (Simon et al., 2000). Cain et al. (2015) observed that overplacement rather than overestimation appears to explain excess market entry. This was due to a myopic self-focus on their abilities coupled with a tendency to underestimate the strengths of competitors. Artinger and Powell (2016: 1061) found that overconfidence plays a significant role in explaining excess market entry, which is likely to occur as overconfident people facing market entry choices “tend to focus on their abilities while neglecting the contingent moves of competitors.” At the same time, Hogarth and Karelaia (2012) suggest that excess entry does not necessarily imply overconfidence; instead, it can be driven by imperfect judgment. In another model of entrepreneurial entry and exit, Chen, Croson, Elfenbein, and Posen (2018: 1005) concluded that it is “precisely those entrepreneurs who perform worst after entry that are most likely to enter.” Other scholars have focused on the tendency of overconfident executives to create new ventures to commercialize entrepreneurial opportunities (e.g., Barbosa et al., 2019; Dimov, 2010; Hvide & Panos, 2014). Likewise, Navis and Ozbek (2016) argued that overconfident and narcissistic entrepreneurs tend to prefer novel venture contexts (i.e., high tech) as opposed to familiar venture contexts (i.e., traditional, established).

But the implications of confidence for entrepreneurial action are not as straightforward as commonly envisioned. Even though some studies show risk tolerance among overconfident individuals is associated with the willingness of entrepreneurs to start a new venture (Barbosa et al., 2019; Hvide & Panos, 2014), Simon, Houghton and Aquino (2000) found no significant association between overconfidence, risk perceptions, and the decision to start a venture. Engelen, Neumann, and Schwens (2016) report evidence of a curvilinear association. Further research into the boundary conditions that modulate the influence of executive confidence on entrepreneurial entry is needed.

Corporate conduct

There is evidence that overconfidence may result in questionable practices, including aggressive accounting (Ahmed & Duellman, 2013), lower quality forecasting (Hilary & Hsu, 2011), unethical business practices (Bianchi & Mohliver, 2016), and fraud (Davidson et al., 2015). Schrand and Zechman (2012) find overconfident CEOs are likely to make optimistic statements that put them in a position where they may be motivated to misreport earnings in the future. Likewise, Ahmed and Duellman (2013) found a negative association between CEO overconfidence and conservative accounting practices, observing that changes in overconfidence following a CEO change are also negatively associated with accounting conservatism. Other studies provide indirect evidence. Bianchi and Mohliver (2016) found that CEOs were more likely to backdate their stock option dates during good economic times than they were during a downturn. There is also evidence that narcissistic CEOs’ overconfidence leads them to involve their organization in protracted and damaging litigation (O'Reilly, Doerr, & Chatman, 2018).

Yet other studies provide a less conclusive picture. In a recent study, Chu et al. (2019) offer “weak and conflicting evidence” for the role of CEO overconfidence in explaining earnings manipulation. And some recent studies have reexamined the relationship between overconfidence and outcomes such as these and concluded that other variables serve as an alternative or perhaps superior explanation. For example, earnings manipulation was more strongly associated with pressure to beat earnings than overconfidence (Chu et al., 2019), while behavioral integrity was more predictive of audit fees (Dikolli, Keusch, Mayew, & Steffen, 2020), and risk preferences were better at predicting return skewness after an insider trade (Drobetz, Mussbach, & Westheide, 2020).

Even as there is growing scholarly attention to the role of CEOs in corporate political activism and social responsibility, the role of executive confidence is unclear. Still, some insights may be gleaned from research on related constructs. Concerning narcissism, theory and research suggest that narcissism among CEOs increases the extent to which CEOs of a political leaning will stake a stance on political issues (Hambrick & Wowak, 2021). Gupta, Nadkarni, and Mariam (2019) found that CEO narcissism bolstered the tendency of liberal CEOs to invest in corporate social responsibility initiatives. To satisfy their deep-seated desire for adulation (Gerstner et al., 2013), narcissistic CEOs invest heavily in corporate social responsibility initiatives (e.g., see Petrenko, Aime, Ridge, & Hill, 2016)—though interestingly, the effect of such initiatives on firm performance is mitigated among firms with highly narcissistic CEOs. But when such narcissistic desires for adulation are removed, there is no theoretical basis to expect a systematic positive association between executive confidence and corporate social responsibility. Indeed, Tang, Qian, Chen, and Shen (2015) found that hubristic CEOs engage in fewer socially responsible corporate activities and more irresponsible activities than those lacking hubris. As Tang, Qian et al. (2015: 1342) argue, “for hubristic CEOs who in general believe they are fully capable of managing risks without external assistance, the perceived need for insurance-like protection afforded by engaging in socially responsible activities is reduced.” And because they have an enduring belief in their problem-solving capabilities, “hubristic CEOs are easily seduced by the prospective payoff from engaging in socially irresponsible activities and less concerned about ensuing sanctions from stakeholders” (Tang, Qian et al., 2015: 1343).

Strategic persistence and change

Another research area deals with the tendency of overconfident executives to persist with strategies long after their efficacy is questioned. In archival and laboratory studies, Audia et al. (2000) found that managerial confidence mediated the influence of past success on strategic decision-makers’ persistence with strategies. Likewise, Hayward et al. (2004) theorized that celebrity CEOs might believe they can reverse undesirable outcomes by allocating additional resources and managerial effort toward the pursuit of the chosen strategy because of their overconfidence. In a similar vein, using a large sample of CEOs, top managers, and board members, Park, Westphal, and Stern (2011) found that high levels of flattery and opinion conformity increases CEOs’ overconfidence in their strategic judgment and leadership capabilities, reducing the tendency of those CEOs to initiate strategic change.

Relatedly, Navis and Ozbek (2016) argued that the combined effects of overconfidence and narcissism engender dysfunctional persistence, which hinders exploratory recognition, openness, curiosity, and experimentation associated with second-order learning. The tendency for confidence to be associated with less intense information search and processing (Cooper et al., 1995), increased speed of decision-making (Clark & Maggitti, 2012), and lower decision accuracy (Zacharakis & Shepherd, 2001) may exacerbate the maladaptive tendency toward dysfunctional strategic persistence. The use of multiple scenarios in decision-making may mitigate these tendencies and encourage greater strategic flexibility (Phadnis, Caplice, Sheffi, & Singh, 2015).

Value creation

The preceding discussion raises a natural question: Is executive confidence ultimately value-creating or destroying due to its functional and dysfunctional manifestations? Based on studies that examine the influence of executive confidence on some aspects of firm behavior and subsequent outcomes (and not just outcomes), we determined that just under half of the studies report dysfunctional manifestations of executive confidence (49% of studies), whereas less than a quarter reveal functional manifestations of confidence (23% of studies). While there is a definite bias towards investigating dysfunctional manifestations, this is most evident in accounting, economics, and finance studies (based on relative proportions).

There is some evidence that firms led by more confident executives create more value from their investments and enjoy higher levels of firm performance. Studies have found that overconfident CEOs positively influence the value of cash holdings (Aktas et al., 2019; Chen, Ho et al., 2020), suggesting that they create “more bang for their buck.” Hsu, Novoselov, and Wang (2017) found that firms run by overconfident CEOs employing conservative accounting practices exhibit better cash flow performance. Others provide indirect evidence. For example, using a proxy measure of overconfidence, Chakravarty and Hegde (2019) report that appointment of overconfident directors to the corporate board is positively associated with firm performance; the inferred causal mechanism is the personal confidence of directors. Ashford, Wellman, de Luque, De Stobbeleir, and Wollan (2018) suggest CEO vision articulation (a likely manifestation of confidence) enhances firm performance by boosting the potency of the top management team.

However, a large proportion of studies suggest that the link between overconfidence and more distal performance measures tends to be negative. One stream of research indicates that executive overconfidence is associated with dysfunction, including strategic inertia (Hayward et al., 2004; Vecchiato, 2020), higher risk of stock price crashes (Kim et al., 2016), lower survival prospects (Ho et al., 2016), and ultimately higher risk of organizational failure (Almandoz & Tilcsik, 2016; Hayward et al., 2006). A second stream indicates that firms run by overconfident executives experience higher costs. For example, overconfidence is associated with a higher cost of issuance (and less favorable terms) in initial public offerings (Boulton & Campbell, 2016). And confidence is associated with higher audit fees to offset litigation risks on behalf of the auditor (Hope, Hu, & Zhao, 2017). A third stream focuses on how CEOs may destroy shareholder value through investment policies and actions such as acquisitions (Banerjee, Humphery-Jenner, & Nanda, 2015; Benson & Ziedonis, 2010; Malmendier & Tate, 2008). Other studies suggest that overly confident entrepreneurs may hinder their venture’s performance by persisting with technologies that do not achieve commercial success (Lowe & Ziedonis, 2006).

In our evaluation, more attention is needed to the boundary conditions that modulate the influence of executive outcomes on firm outcomes. There is evidence that some of the more harmful effects of overconfidence may be kept in check using external and internal governance arrangements. For example, Banerjee et al. (2015) found that the passage of the Sarbanes-Oxley Act of 2002 (SOX) served to reduce overinvestment and risk-taking and that following SOX CEO’s acquisitions had significantly more value. Concerning internal governance, in a study of S&P 1500 firms between 1993 and 2007, Kim et al. (2018) found that firms with more robust regimes of corporate governance constrained the risk-taking preferences of highly hubristic CEOs.

Theme IV: Origins and Antecedents

The origins of confidence vary, but they have received limited attention relative to research on the three themes reviewed so far. We categorize extant findings into within-person, between-person, and situational effects.

Between-person effects

Concerning between-person effects, several studies sought to establish the presence of executive confidence within groups. For example, Ben-David, Graham, and Harvey (2013) showed that CFOs exhibited a high degree of overprecision in their estimates of future market performance. Using a policy-capturing approach, Zacharakis and Shepherd (2001) found that venture capitalists tend to exhibit overconfidence. Some studies use gender as a proxy for confidence (Huang & Kisgen, 2013; Levi et al., 2014), with initial evidence suggesting that women executives show fewer signs of overconfidence than men, on average (Levi et al., 2014). Being a founder has been used in a similar manner (Busenitz & Barney, 1997; Forbes, 2005; Lee et al., 2017; Simon & Shrader, 2012), and recent evidence suggests that founders are more likely to exhibit overconfidence compared to professional CEOs (Lee et al., 2017).

Within-person effects

Turning to within-person effects, a smaller group of studies have considered the lifecycle and trajectory of individuals as a means for assessing the origins of confidence. There is some evidence to suggest that preparations, such as receiving an MBA (Beber & Fabbri, 2012), creating formal plans or financial projections (Cassar, 2010), or prior experience (Dimov, 2010; Hayward et al., 2006), engender overconfidence. But the relationship between confidence and experience likely depends on the heterogeneity of experience (Zollo, 2009), including the level of failure experienced (Ucbasaran, Westhead, Wright, & Flores, 2010). Confidence may also increase as executives are afforded powerful roles—the subjective sense of power brought on by these roles may cause executives to become increasingly overconfident in their knowledge and managerial prowess (Fast, Sivanathan, Mayer, & Galinsky, 2012).

Situational effects

Only a few studies have considered the situational antecedents of executive confidence. In a study of 108 internet ventures in Silicon Valley, Forbes (2005) found that entrepreneurs exhibit greater overconfidence when their firms are more comprehensive in decision-making. This finding echoes an earlier finding by Zacharakis and Shepherd (2001) that venture capitalists’ confidence grows with access to information. Other scholars have considered the situational determinants of confidence, including praise for the CEO (Hayward & Hambrick, 1997) and high levels of flattery and opinion conformity toward the CEO (Hayward et al., 2004; Park et al., 2011).

While the extant literature provides some important clues about the origins of confidence in executives, there are significant gaps in our understanding. First, we are not aware of any studies that model an executive’s confidence throughout their career or even job tenure. Second, we know relatively little about how executives can build and develop confidence or how overconfidence can be curtailed. Third, we do not know much about precisely how it forms, crystallizes, and evolves, if at all.

Directions for Future Research

Our review was enjoined to assess and advance current research and understanding on executive confidence by examining four themes of ambiguity. Up to this point, we discussed the review results about each of these four themes and, in so doing, provided a set of insights into what is currently known, knowable, and unknown. In this section, we leverage these insights to discuss a set of proposals and directions for future research. For the sake of consistency, we organize the discussion using the same labels used in the prior section.

Theme I: Advancing Conceptualization

Our review revealed three significant challenges with the conceptualization and measurement of executive confidence. First, most studies treat it as a unidimensional construct (and where the measurement does not necessarily correspond with the theorizing). As a result, we know little about whether different forms of confidence are more (or less) advantageous in explaining firm behavior and outcomes—or whether the magnitude of such effects differs. Second, there is a systematic bias in the literature towards overconfidence. Few studies are concerned with average or low levels of confidence. But this raises a fundamental question: What is the reference point when one speaks of overconfidence among executives? And third, the concept is in danger of becoming “a suitcase construct,” packing the features of somewhat related but distinct constructs, including narcissism, hubris, core self-evaluations, optimism, and humility.

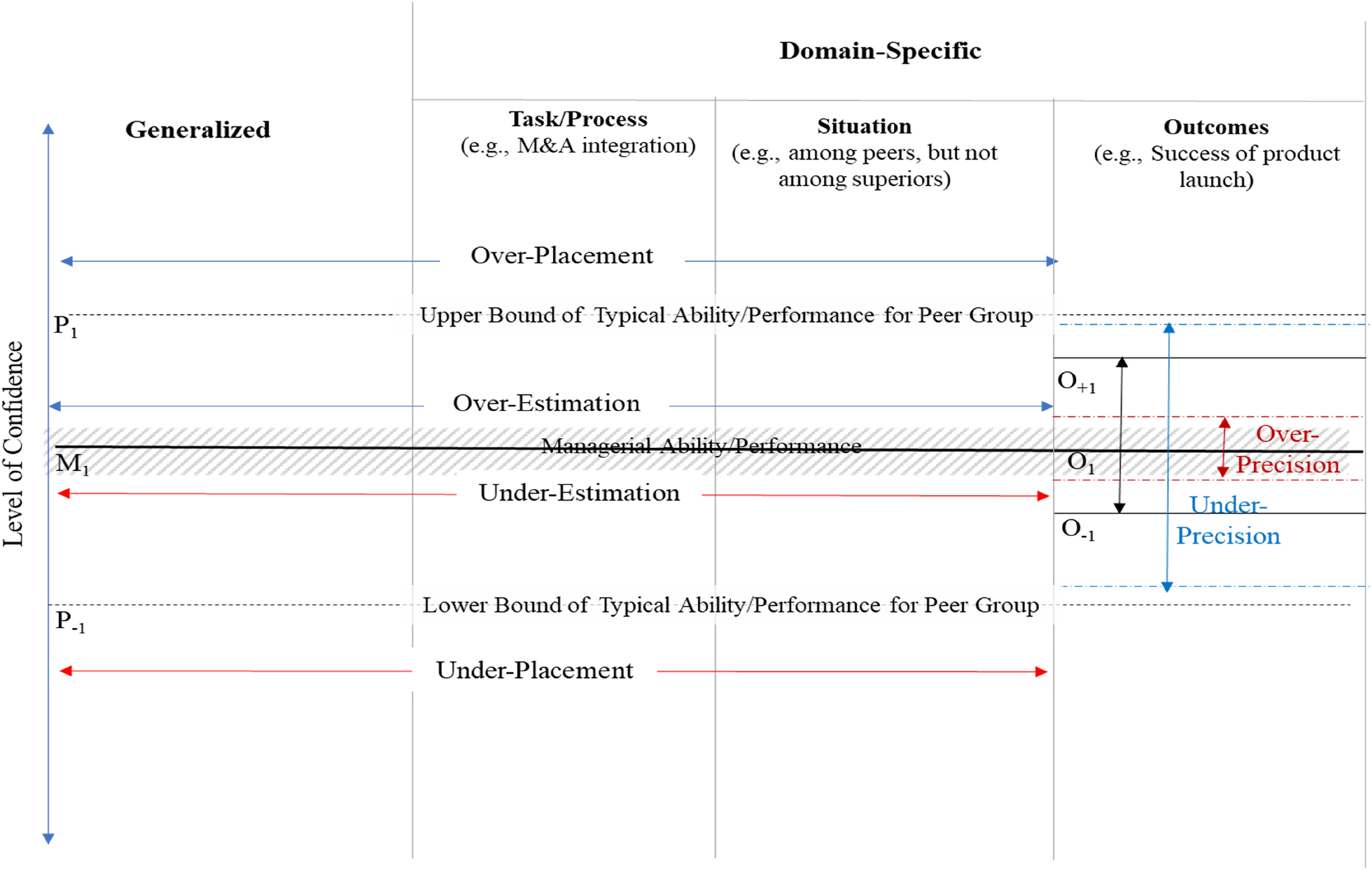

We propose a conceptualization that recognizes the many forms and varying scope of confidence to address these challenges, including the reference point against which confidence judgments are made. Specifically, we define executive confidence as an executive’s generalized or domain-specific conviction in their capability to complete tasks, influence events, and/or achieve outcomes. As illustrated in Figure 2, the definition recognizes that confidence beliefs can vary in form (estimation, precision, placement) and scope (generalized versus domain-specific). Additionally, it calls attention to the extent to which confidence beliefs are calibrated with actual levels of managerial ability. We hasten to add that Figure 2 provides a simplified representation of the multidimensional nature of the construct and the nonlinear differences across the different types of confidence. However, it serves as a valuable visual aid to depict the key features of the conceptualization.

A Unifying Conceptualization of Executive Confidence.

Conceptualizing confidence relative to objective managerial ability and performance suggests that confidence beliefs may be calibrated or miscalibrated to varying degrees. Calibrated beliefs occur when an executive’s confidence beliefs closely align with objective ability or performance levels. Miscalibrated beliefs thus occur when executives’ beliefs deviate significantly from objective levels of managerial ability and/or performance. The M1/O1 line in Figure 2 represents a theoretical level of managerial ability and performance in focal outcomes, respectively. 1 This theoretical quantity can refer to managerial experience (Kor, 2003), dynamic managerial capabilities (Adner & Helfat, 2003), or whatever may be appropriate to the research question and context. In the case of outcomes, it refers to known, achieved outcomes. Building on earlier efforts, our synthesis in Figure 2 discriminates between three types of miscalibrated confidence—under-/over-estimation, under-/over-precision, and under-/over-placement (Moore & Healy, 2008).

Miscalibration in estimation occurs when beliefs concerning ability or outcomes deviate from an objective indicator of ability or outcomes (Moore & Healy, 2008). Miscalibration in precision also occurs when executives are overly or insufficiently exacting in their confidence intervals given the average variation in the range of outcomes as denoted by O+1/O−1 in Figure 2 (overprecision is shown in red; underprecision depicted in blue). Miscalibration in placement occurs when executives over or under assess their ability and performance relative to the ability and performance of peer groups, the range of which is denoted as P+1/P−1. Miscalibration in placement would commonly occur, for example, when executives believe they can create more value from acquisitions and investments compared to other similarly competent CEOs.

Implications for theorization

The renewed conceptualization can stimulate a richer body of research by recognizing that the theorizing can take a binary (an executive is confident or not confident), continuous (one executive is more confident than another), or multidimensional form (an executive can have confidence in one domain, but not across domains). Moreover, it allows researchers to consider how confidence judgments calibrated to different reference points—perhaps based on different conceptions of managerial ability—may manifest in firm behavior and outcomes.

Relatedly, there is the opportunity for future research to be informed by the behavioral theory of the firm on aspirations. For example, researchers could look to the work combining confidence with organizational aspirations (e.g., Malhotra et al., 2018) and consider the effects of confidence on the motivations of operating near pertinent inflection points in organizational aspirations such as survival points (see, e.g., Schumacher, Keck, & Tang, 2020). Scholars could also apply the logic of organizational aspirations to confidence reference points to consider—for example, whether there are asymmetric effects for under- and overestimation of abilities or outcomes. 2

Additionally, the conceptualization encourages researchers to reconsider what is currently known. Using better specified concepts, researchers could pursue creative and constructive replications of earlier findings to see whether the effects of confidence vary across different forms and scopes of confidence or whether the results hold the appropriate reference point for ability is accounted for. For instance, the evidence base for executive confidence is strongest concerning corporate strategy, corporate finance policy, and market entry, but these findings are confined to a narrow slice of the conceptual terrain of confidence. We suspect that CEOs with calibrated confidence beliefs (i.e., congruent with the relevant reference point) are more likely to select strategic choices that fit their firm’s capabilities and maximize the advantages of first-order learning than those with miscalibrated confidence beliefs (Navis & Ozbek, 2016). Conversely, there is an elevated risk of misfiring in the presence of poorly calibrated confidence due to the cognitive, resource, and economic externalities (Adebambo & Yan, 2018; Audia et al., 2000; Hayward et al., 2004; Hiller & Hambrick, 2005; Vecchiato, 2020).

Implications for measurement

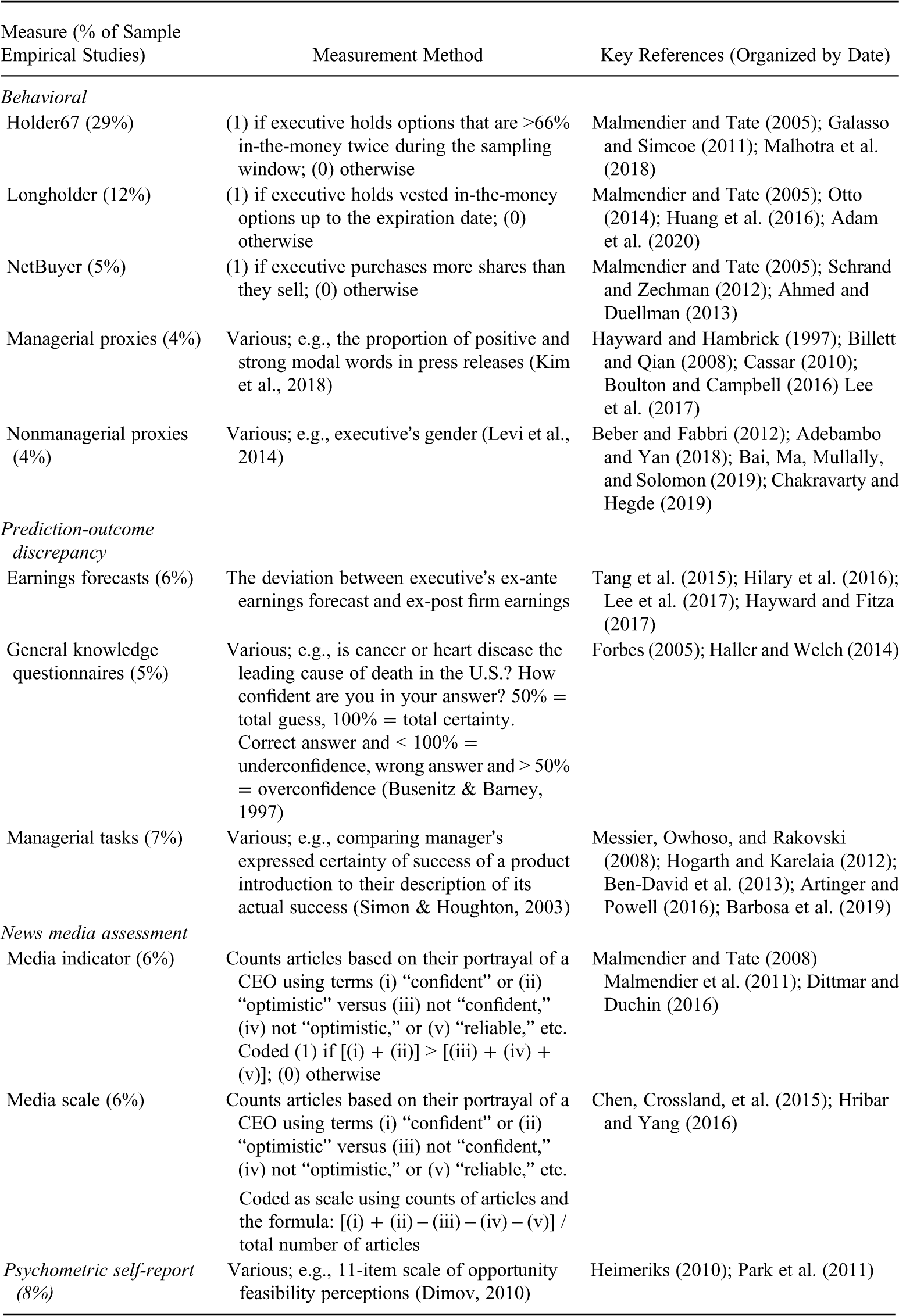

The employment of a range of measures in previous studies to capture confidence serves as both a blessing and a curse. As summarized in Table 4, consistent measures such as Holder67, Long-Holder, and Net Buyer have facilitated replicability and evidence accumulation. Such efforts have been complemented by a range of other proxies and behavioral signatures. At the same time, though, most measures of executive confidence reported in the prior literature and summarized in Table 4 neither capture whether confidence is appropriately calibrated nor recognize its variability. As a result, theorization and measurement appear misaligned in several studies.

A Summary of Measurement Methods for Executive Confidence

We offer three suggestions to improve construct validity and achieve greater methodological fit in the study of executive confidence. First, future studies should include measures of managerial ability and performance against which confidence judgments may be calibrated. But this is easier said than done—reliably and validly measuring managerial ability has long been a challenge, and we do not profess to have “a silver bullet.” But as a start, future research might start with Data Envelopment Analysis to measure that component of firm efficiency attributable to managers (e.g., Demerjian, Lev, & McVay, 2012). These types of measures capture a manager’s ability to generate higher revenues from a given set of resources than their counterparts in the same industry (Lee, Wang, Chiu, & Tien, 2018). Another approach would be to use the dynamic managerial capabilities framework to develop measures of managerial ability to determine whether such firms “adapt and change more successfully than firms whose managers have less effective or no dynamic managerial capabilities” (Helfat & Martin, 2015: 1304). A further approach may build on an increasingly intricate and detailed measures of managerial experience. Most approaches to date have focused on tenure as an indicator of managerial experience, but this tells us little about the qualitative nature of such experience (i.e., Tesluk & Jacobs, 1998). Thus, we encourage the adoption of future approaches that capture the different types of experiences, such as the number or size of successfully integrated acquisitions or the variety of executive career experiences (see Crossland, Zyung, Hiller, & Hambrick, 2014; Karaevli & Hall, 2006).

Second, despite growing recognition of the three major forms of overconfidence (i.e., Moore & Healy, 2008), research has been slow to measure these in an executive setting, perhaps because they are difficult to capture using archival data. Concerning under-/over estimation, we encourage developing measures that compare executives’ subjective assessment of ability or competences with objective indicators using mixed methods. For example, researchers might ask executives to assess their ability, competence, or experience across multiple domains—and gather archival proxies against which such assessments are compared. Another approach that may be amenable to archival data is to assess under-/over-estimation of firm capabilities vis-à-vis objective indicators of such capabilities. Likewise, assessment of under-/over-placement could build on these empirical efforts. Surveys could be extended to request that executives assess their ability, experience, and so on relative to other managers in the same industry or of the same firm type, size, and scope. It is also possible that comparing CEO assessments of ability to objective CEO ranking could assist in assessing the level of under-/over-placement. Under-/over-precision is more amenable to measurement in an executive setting. In surveys and interviews, this could be measured by asking CEOs and other executives to place confidence intervals around firm and market growth estimates and compare such estimates with true variability. Archival studies might tap into earnings guidance issued by CEOs and CFOs and how the precision of such guidance compares with actual results retrospectively.

Finally, researchers need to be sensitive to the scope of these measurements. It will be essential to appraise whether confident judgments are confined to specific domains or whether confidence is consistently exhibited across domains. This will require examining a broader set of archival evidence beyond shareholder letters—content analysis of speeches, interactions with stakeholders, interviews, media appearances, autobiographies, and so forth. By triangulating these sources, researchers will be better positioned to capture the scope of confidence beliefs.

Implications for construct confounding

One of the realities of executive confidence is that it is poorly differentiated within its nomological network. If confidence is to provide a distinct explanation of firm behavior and outcomes, then there is a need to account for the influence of other related constructs, but few studies have done so.

We have attempted to provide some clarity in Table 3 and Figure 1 and offer three additional recommendations. First, future research needs to add nuance to our understanding of the zones of convergence and divergence by examining these attributes in conjunction with each other. For example, consider Zhang, Ou, Tsui, and Wang’s (2017) investigation of the interactive influence of CEO narcissism and humility on firm innovation. Second, we need measurement studies that empirically validate these zones of convergence and divergence and meta-analyses to discern the strength and direction of correlations systematically. And third, we call on additional studies on how confidence differs from other related constructs used in prior studies. As visualized in Figure 1, the proposed conceptualization also helps to clarify further how and in what ways executive confidence is a common denominator among these constructs. Future efforts along these lines can help unpack the “suitcase construct” and reveal the specific meanings we can and should make of executive confidence.

Theme II: Advancing Governing Mechanisms and Pathways of Influence

Although confidence studies are often internally valid, the governing mechanisms underpinning confidence effects are rarely theorized and tested empirically. We also observed that scholars have rarely specified or tested the full (causal) pathways through which executive confidence influences the theorized focal behavior and outcomes. We discuss our suggestions for each issue in turn.

Specifying and testing coverning mechanisms

Our review identified five common mechanisms underpinning the influence of executive confidence on firm behavior and outcomes. Future studies should be precise in the theorization of these governing mechanisms and validating their existence. For example, while the preponderance of evidence suggests that confidence is associated with restricted information processing, some studies indicate that confident individuals demand more information than less confident individuals (e.g., Desender, Boldt, & Yeung, 2018). The core question of whether confidence restricts or stimulates information processing lingers. To make progress, researchers could use executive time-use and diary studies that provide fine-grained insight into the communication patterns of CEOs and other executives (e.g., Bandiera, Prat, Hansen, & Sadun, 2020).

We also see considerable merit in elaborating our understanding of self-regulatory mechanisms. Although there is evidence that individuals with positive self-concept set more ambitious goals and demonstrate commitment to them than those without a positive self-concept (Chang, Ferris, Johnson, Rosen, & Tan, 2012), no empirical research directly examines the influence of executive confidence on goal-setting. Future studies can explore the types of goals that confident executives set and whether their commitment to those goals (public or private) leads them to a path wherein ethical and legal boundaries become blurred. Alternatively, they can examine whether pursuing lofty aspirations leads to higher performance than would otherwise be achieved.

A third promising avenue is greater attention to affective mechanisms. Compared to research on macrolevel behaviors, there has been far less attention to the implications of confidence for how executives lead at close range. In a study combining field, archival, and experimental data, Ronay et al. (2019: 15) found a consistent positive relationship between overconfidence and leadership ratings. Others have found that executives displaying confidence convey a greater sense of control to investors (Hayward & Fitza, 2017) and engender higher commitments from organizational stakeholders (Phua, Tham, & Wei, 2018).

Another avenue for future research is to examine how confidence influences executives’ accumulation of power and wealth. There is emerging evidence that confidence is associated with status (Kennedy, Anderson, & Moore, 2013). Still, there is little understanding of how confidence may shape hard and soft tactics to increase power in and around the firm. The evidence indicates that confident people are more likely to be perceived as competent than people lacking confidence (Ronay et al., 2019) and powerful (Bitterly, Brooks, & Schweitzer, 2017). Do confident executives exploit these perceptions of competence and power to exert their influence and garner resources, accumulate further power, status, and wealth?

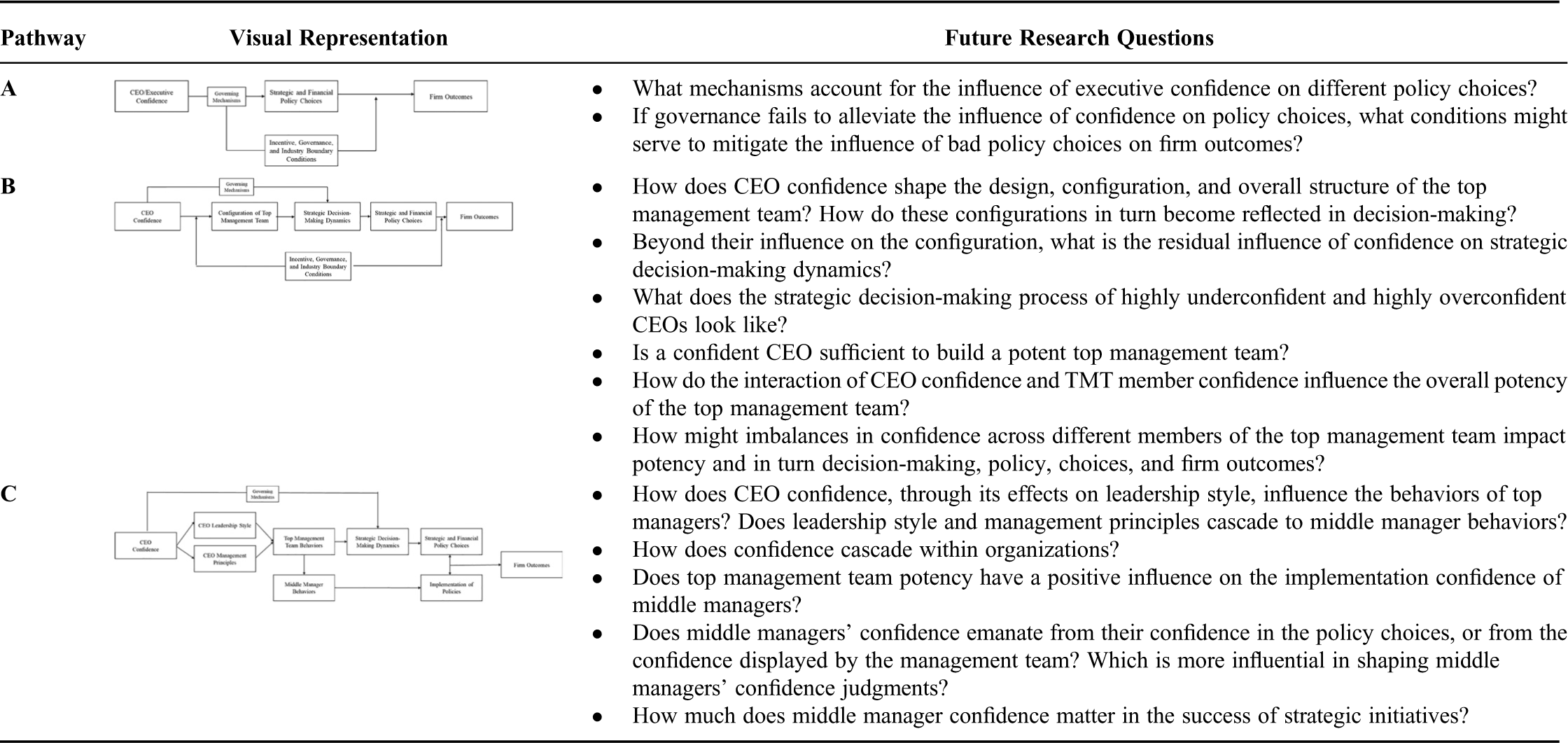

Clarifying the (causal) pathways of influence

The review revealed that a fully specified model that explicates the causal sequence linking executive confidence to relevant organizational outcomes remains a rarity among previous studies across disciplines. Put differently, not many studies have specified mediational models, moderated mediation models, or mediated moderation models when studying the consequences and implications of executive confidence. Most studies could be approximately represented by Pathway A in Table 5. Naturally, this is a simplification, but it represents the logic inherent to most studies—confident executives enact strategic choices that then result in varying levels of firm outcomes; the strength and direction of such effects are altered by the presence of boundary conditions or contextual contingencies. Even then, very few studies have directly investigated the entire set of causal linkages implied by Pathway A in the context of a single manuscript.

(Causal) Pathways of Influence for Executive Confidence

But other pathways are plausible and perhaps provide a more realistic and richer representation of the consequences and influence of executive confidence. For example, the second pathway (B) (Table 5) considers the influence of CEO confidence on the configuration of the top management team and emergent properties, such as potency or cohesion. It could, for example, be intriguing to consider whether overconfident CEOs establish smaller and less diverse top management teams based on overestimating their management abilities and underestimating the need for complementary perspectives (Pitcher & Smith, 2001).

A third pathway to explore (C) entails the role that confidence plays in a CEO’s leadership style and management principles. The psychology literature suggests that traits such as core self-evaluation are associated with a transformational style of leadership (Hu, Wang, Liden, & Sun, 2012), which may foster both empowerment and dependence (Chang et al., 2012). There is also the question of how confidence might influence a CEO’s management principles that they seek to instill in their firms. For example, Jeff Bezos, founder and the CEO of Amazon, has laid out a set of management principles that Amazon executives and managers live by such as “bias for action,” “have backbone; disagree and commit,” “insist on the highest standards,” and “think big among others.” Thus, leadership style and management principles may act as two central conduits through which CEOs of varying confidence influence the behaviors of their top managers.

Theme III: Advancing Implications and Outcomes of Executive Confidence

Although we have recommended that an initial thrust of research be on constructively replicating the findings of past studies using measures that tap the different profiles of executive confidence and studies of better specified models, we envision two promising opportunities for broadening the investigation of executive confidence effects.

First, there is a greater need to understand the intersection of executive confidence and competitive dynamics research. Although research has examined the effect of confidence on competitive entry into new markets, we know little about how different types of confidence may manifest in a firm’s profile, trajectory, and sequence of competitive actions—a stream of research at the heart of strategic management. Thus, future studies should examine the impact of different types of confidence on the level of competitive aggressiveness and the extent to which competitive actions are themselves calibrated to competitive demands (Andrevski, Richard, Shaw, & Ferrier, 2014; Connelly, Tihanyi, Ketchen, Carnes, & Ferrier, 2017).

A second thrust would be to examine the influence of executive confidence on executives’ careers, including mobility, progression, marketability, compensation, and awards. But confidence is also associated with several drawbacks as well, including irrational stock holding (Huang & Kisgen, 2013), lower investment performance (for individuals broadly, not executives in specific situations) (Bailey et al., 2011), higher rates of dismissal (Ho et al., 2016), and potentially lower CEO pay (Otto, 2014; Pandher & Currie, 2013). The last finding is particularly intriguing and appears to be the result of overconfident CEOs being willing to accept “convex” pay packages (i.e., ones with a higher proportion of incentive-based compensation) (Humphery-Jenner, Lisic, Nanda, & Silveri, 2016; Pandher & Currie, 2013). Since these executives have overly optimistic views of future performance, they may accept a pay package with a lower guaranteed compensation because they believe that they will realize performance objectives to secure their incentive-based pay (Otto, 2014).

Theme IV: Advancing Origins and Antecedents

As our review illustrates, there has been surprisingly little attention to the origins and antecedents of executive confidence. As a result, we currently have few insights into why executives display distinct levels and types of confidence. Here, we call attention to three lines of inquiry that build upon what we know so far.

First, a CEO’s early life and career experiences may serve as a source of generalized and dispositional confidence. For example, Chakravarty and Hegde (2019) provided evidence that board members passing the rigorous Joint Entrance Exam (JEE) in India tended to lead companies with higher firm performance, which they attributed to the boost of confidence that these board members received by achieving such a result on a challenging and well-known exam. More generally, CEOs from privileged families and educational backgrounds may internalize these advantages. Future studies might examine the background of CEOs to investigate whether early-life advantages translate into an enduring source of confidence—and importantly, to show this difference in confidence directly rather than inferring it from outcomes.

A second direction is to investigate CEO career experiences, successes, and setbacks. Do specific events, such as successful mounting a turnaround of a business division, the successful entry into an emerging market, or successful navigation of a crisis, economic or financial, shape the level and type of executive confidence? Do prior failures and forced departures temper or enhance confidence judgments? Such work can build upon and inform Hayward, Forster, Sarasvathy, and Fredrickson’s (2010) study of confidence and resilience—and perhaps provide insight into the potentially reciprocal relationship between confidence and resilience. For example, are confident executives more likely to be resilient in the face of a setback than unconfident executives, or is resilience after a setback a driver of confidence in the future since it provides the executive with information regarding their level of control over the environment?

A third direction is to examine how confidence evolves across the seasons of a CEO’s tenure and the role of specific governance interventions such as board mentoring (Shen, 2003) in this evolutionary process. In this way, confidence research may draw upon and contribute to work on the commitment to the status quo (Hambrick, Geletkanycz, & Fredrickson, 1993). By simultaneously considering the trajectories of confidence within executives as they move from firm to firm along with differences in confidence between executives working for the same company, a robust empirical specification of confidence effects may emerge (Certo, Withers, & Semadeni, 2017). Across all these potential avenues, confidence research has much to gain by focusing on how executives gain and lose confidence if only to understand how to manage the consequences of executive confidence through governance or personnel choices.

Conclusions

Our review of past research along four themes of the ongoing ambiguity has revealed several opportunities for advancing the study of confidence. To us the most promising and pressing among these is the conceptualization of confidence itself. Disentangling the basis, scope, and calibration of executive confidence beliefs (and associated behaviors) offers leverage for researchers to explain intrafirm and interfirm variations in firm behavior and outcomes. As well as being sensitive to variations in profiles of executive confidence, future studies should more deeply probe the causal mechanisms responsible for variations in value creation and destruction and trace the evolutionary and developmental antecedents and trajectories of executive confidence. By advancing the four reviewed themes of ambiguity using some of the suggestions outlined, we are confident that management researchers, to paraphrase an old television adventure series, will go where no one has gone before in the study of confidence construct.

Supplemental Material

sj-docx-1-jom-10.1177_01492063211062566 - Supplemental material for Executive Confidence: A Multidisciplinary Review, Synthesis, and Agenda for Future Research

Supplemental material, sj-docx-1-jom-10.1177_01492063211062566 for Executive Confidence: A Multidisciplinary Review, Synthesis, and Agenda for Future Research by Ciaran Heavey, Zeki Simsek, Brian Curtis Fox and Matt C. Hersel in Journal of Management

Footnotes

Acknowledgments

The authors thank the Editor and the two reviewers for their thoughtful guidance and valuable revision recommendations.

Supplemental material for this article is available with the manuscript on the JOM website.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.

Notes

Correction (August 2024):

This article has been updated online with missing references and minor terminology corrections since its original publication.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.