Abstract

The resource-based view of the firm has become dominant within the field of strategic management, yet it has had surprisingly little influence within organization theory. In this article, we document the divide between strategy and organization theory and propose an interpretation. Choices of theories are largely driven by a researcher’s dependent variables, and the questions “Why do firms do what they do?” and “Why do some firms perform better than others?” can have distinct answers. Thus, strategic management scholars and organization theorists are like howler monkeys and spider monkeys, coexisting peacefully in the same ecosystem by dining on different dependent variables. We further speculate on the looming existential crisis for both fields as traditional firms are increasingly unsustainable due to the transformation wrought by the digital revolution in product markets and the markets for capital, labor, and supplies.

The resource-based view of the firm (RBV) has been one of the most successful theoretical approaches in the field of strategic management. Along with the five-forces model, it has achieved a dominance rarely seen in any academic domain. Moreover, its dominance extends to both research and teaching, where it is taught in nearly every required course on business strategy. (It is less obvious what effect it has had on service.) After 30 years, RBV has assured its place in the intellectual history of business strategy.

One place where it has been far less visible, however, is in organization theory. To an outsider, the academic fields of strategy and organization theory look like conjoined twins. Newcomers to the Academy of Management might wonder why there are different divisions for Strategic Management and Organization and Management Theory since they seem to be studying the same thing. In many business schools, a single management department encompasses scholars of both persuasions, who often publish in each other’s journals. Yet to a shocking extent, when it comes to published research, the fields barely acknowledge each other’s existence. In particular, organization theorists seem to have almost no knowledge of RBV. What gives?

In this article, we document this puzzle and propose some interpretations. In short, organization theorists explain why firms look and act the way they do, while strategy explains what effect these have on performance. Because strategy is downstream from organization theory in the intellectual value chain, while organization theorists have little concern with what factors shape performance, the fields seem to see little need to connect. We then broach a subject that should pose existential dilemmas for both organization theory and RBV and that may provide common ground for greater dialogue: the death of the firm as a social institution.

How Has RBV Shaped Organization Theory, and Vice Versa?

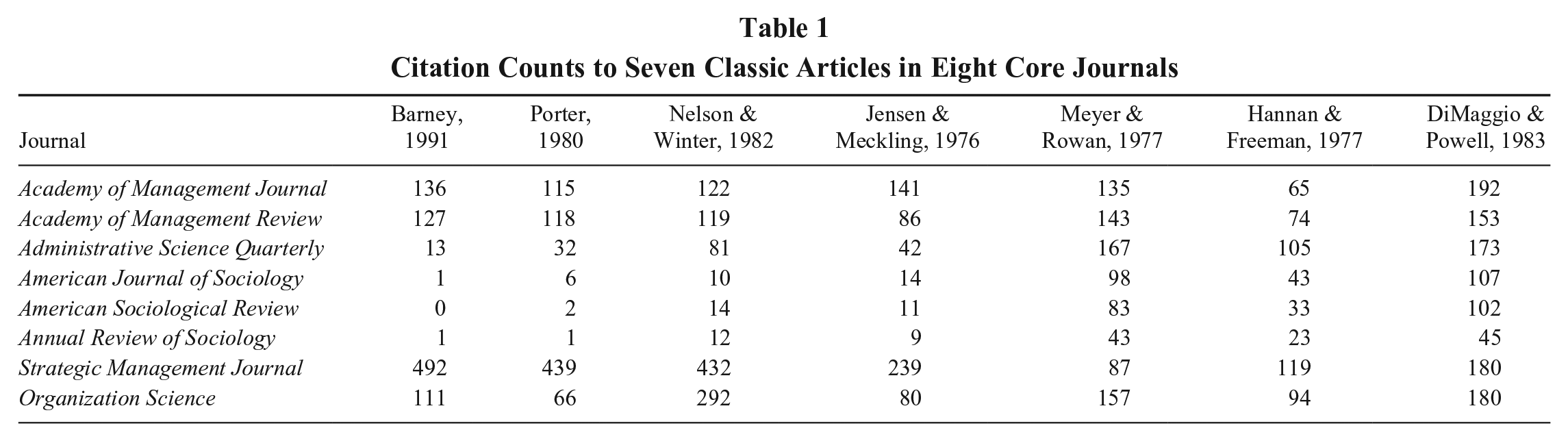

Let’s start with an empirical puzzle. Evidence from citation counts shows that while strategy scholars occasionally draw on canonical works of organization theory, organization theorists allude only minimally to RBV and to strategy more generally.

Table 1 shows cumulative citations from initial publication to August 2020 for three classic statements in the field of strategic management, according to the Web of Science: Michael Porter’s (1980) book, Competitive Strategy; Nelson and Winter’s (1982) book, An Evolutionary Theory of Economic Change; and Jay Barney’s (1991) article, “Firm Resources and Sustained Competitive Advantage.” For comparison, we also include three classics of organization theory—Meyer and Rowan (1977), Hannan and Freeman (1977), and DiMaggio and Powell (1983)—as well as Jensen and Meckling’s (1976) self-published theory of the firm.

Citation Counts to Seven Classic Articles in Eight Core Journals

The Strategic Management Journal reflects the consensus view of the field of strategy. Here, Barney (1991) is the hands-down citation champion, besting two strategy landmarks that both had a decade head start as well as three organization theory classics and a finance ringer.

The Academy of Management Journal and Academy of Management Review are big-tent journals that cover all fields of management. Organization Science is similarly home to many flavors of management research. Across these journals there is rough parity in the citations of the classic works we examined, with the exception of Nelson and Winter’s (1982) richly abundant citation count in Organization Science.

Organization theory is perhaps best represented in Administrative Science Quarterly (ASQ) and in the most prominent journals of sociology, the American Journal of Sociology, the American Sociological Review, and the Annual Review of Sociology. It is immediately clear that sociology as a field is largely indifferent to strategic management as a field. Barney (1991) and Porter (1980) are essentially absent from the sociology journals and only modestly cited in ASQ. To a striking extent, RBV is dominant in strategy but nearly invisible within organization theory.

We must also acknowledge that organization theory is largely absent from the canonical statement of RBV. One might have expected to see references to March and Simon (1958), Cyert and March (1963), Thompson (1967), Pfeffer and Salancik (1978), and other central works of organization theory that arguably had things to say about organizational capabilities in Barney’s (1991) statement. All are absent. Hannan and Freeman (1977) are mentioned in passing on page 117 but are inexplicably absent from the reference section.

This seems like a lost opportunity. As Barney (1991: 116) points out, The resource-based model of strategic management suggests that organization theory and organizational behavior may be a rich source of findings and theories concerning rare, non-imitable, and non-substitutable resources in firms. Indeed, a resource-based model of sustained competitive advantage anticipates a more intimate integration of the organizational and the economic as a way to study sustained competitive advantage.

Yet somehow it appears that this integration has not taken place. Barney’s (1991) argument was with Porter, not with the organization theorists.

All of this raises a question: What is going on here? Management and strategy departments are right down the hall from each other. In many cases, they are housed in the same unit. Both focus on firms as units of analysis. And yet strategy appears to draw only minimally from organization theory, and organization theory is evidently completely innocent of the insights of RBV. What gives?

Why Is There Not More Interchange Between Strategy and Organization Theory?

The fields of organization theory and strategy both arose in part due to limitations of the theory of the firm in economics. In spite of its name, the “theory of the firm” for most of its existence was a theory about markets (Cyert & March, 1963) and had very little to say about firms as meaningful entities. Coase (1937) was a pioneer simply for asking the question, “Why does so much economic activity take place within the boundaries of hierarchies rather than on markets?”and gestured toward transaction costs as his answer—a theme that Oliver Williamson deepened and elaborated over several decades, ultimately yielding a Nobel Prize in economics. It took decades for economists to begin providing insightful answers into why there are firms at all (e.g., because of transaction costs, agency costs, or the hazards of team production) and how they might organize themselves internally (e.g., when firms should make vs. buy an input; which constituencies get decision rights for what kinds of choices; see Walker, 2016). And the question of why some firms were persistently more profitable than others was evidently uninteresting to economists. Certainly, the idea of figuring out answers to this question and sharing them with businesspeople was off the table.

Organization theory as a distinct field traces its lineage to a single book published in 1958: Organizations, by James March and Herbert Simon, which sought to explain why hierarchies are so pervasive in the modern world. The puzzle at the heart of this book was this: How is it possible that individual humans are boundedly rational, and sometimes downright dense, yet organizations composed of such flawed raw materials can accomplish so much? If a chain is only as strong as its weakest link, then how can a chain made up of all weak links be so strong? The book combined the latest insights from cognitive psychology with the institutional design orientation of political science (the home discipline of both authors) to provide an answer and launch a field. Notably, the animating question was not about firm performance but about organizational structure and the pervasiveness of hierarchy, an orientation that has dominated the field’s subsequent development.

Cyert and March (1963) followed with A Behavioral Theory of the Firm, intended as a behaviorally realistic approach to the kinds of enterprises that dominated the midcentury U.S. economy. The theory sought to investigate what industries consisting of oligopolists run by managers following simple decision rules might look like. From their perspective, the “representative firm” was not one that had little discretion because it operated in a highly competitive market but a “large, multiproduct firm operating under uncertainty in an imperfect market” (Cyert & March, 1963: 162). Moreover, the managers operating such a firm were not AP Calculus superstars but recognizable humans with cognitive limitations. Firm performance entered the story largely as a variable that explained subsequent management decisions. Firms set aspiration levels for performance based on what their prior aspiration was, how well they did, and how their peers had done last time. If they had met their aspiration, all was good; if they failed to achieve their performance target, they would search for solutions mostly in the approximate neighborhood of what they did before. Lather, rinse, repeat. Computer simulations using these basic decision rules produced results that looked a lot like the real world and promised a future theory of firms in markets that paired realistic behavioral assumptions with simulations. (Spoiler alert: Computer simulations did not replace calculus as a preferred method in economics.)

By 1967, James Thompson (the founding editor of ASQ) was ready to publish a brilliant synthesis that encompassed the insights that had accumulated in the emerging field over its first decade. The slim but powerful book contained dozens of propositions and hypotheses explaining things such as how technology and interdependence shaped the kinds of organization designs that performed best. But Thompson was a sociologist, and there was much room left for power, culture, and Potemkin Village displays detached from the firm’s real operations. Notably, “performance” itself was problematized, as the people running organizations sought to ensure that they were evaluated along dimensions where they were likely to shine and not according to criteria that would make them look bad.

The field’s next 15 years in large part consisted of footnotes to Thompson. Pfeffer and Salancik’s (1978) resource dependence theory analyzed the tactics and structures firms used in response to their power/dependence relations with other firms and made clear (following Thompson) that much of the action was driven by a quest by managers to limit uncertainty and increase their power, not to achieve maximum returns for shareholders. The misguided but pervasive conglomerate mergers of the 1960s and 1970s, for instance, seemed best explained by a quest for growth and greater stability rather than profitability. Hannan and Freeman’s (1977) population ecology argued that in the modern world, societal demands limited how much organizations were able to change what they did. Once they had chosen which form to take, it was very difficult for firms to change, and the vast majority failed anyway. Thus, why bother studying heroic managers making bold choices when almost all the action was in the factors influencing the birth and death rates of firms? And DiMaggio and Powell’s (1983) new institutional theory pointed out that societal forces in the modern world, particularly the demands of the state and professions, led firms to adopt similar structures regardless of the environmental demands they faced or the performance consequences of those choices. Over time, organizations staffed by MBAs from the same schools and guided by consultants from the same firms had all come to look the same, like a sea of undergrads clad in identical North Face jackets. In contrast to the ecologists, these authors noted that many of society’s dominant organizations were essentially too big to fail, as long as they managed to keep up with the latest managerial fads.

In each case, the point of theory was to explain organizational structures and practices. Researchers might ask, “When do firms adopt a multidivisional form?” or “What explains the diversity of phone company start-up rates across states?” or “Which kinds of banks appoint well-connected directors to their boards?” The question was not, however, “How does the performance of M-form firms differ from that of other forms?”

Subsequent theoretical work extended beyond the organization to examine networks and organizational fields (roughly similar to industries) and how firm-level actions aggregated up to collective outcomes. Notably, theories from decades back continued to exercise a strong influence on research, even as studies were more strongly driven by empirical problems than gaps in the literature (Davis & Marquis, 2005). Moreover, although one might imagine that after four decades we would have figured out which theory best explains why organizations look the way they do, that has not happened (Davis, 2010). There is no critical test or horse race that can falsify any of the competing theories; rather, one’s choice of theory is driven more by the kind of problem the researcher is addressing. Make or buy decisions? Use transaction cost economics (Williamson, 1975). Who gets appointed to boards, or which firms create alliances with each other? Resource dependence theory (Pfeffer & Salancik, 1978). Births and deaths? Population ecology (Hannan & Freeman, 1977). Rampant organizational silliness? New institutional theory (Meyer & Rowan, 1977). Like PCBs in the Hudson River, theories from the late 1970s seem to live on forever.

Meanwhile, strategic management set off on a different path. Jemison (1981: 633) defined strategic management at the dawn of the field as “the process by which general managers of complex organizations develop and use a strategy to coalign their organization’s competences and the opportunities and constraints in the environment.” A quarter-century later, Nag et al. (2007: 942) created a six-element definition of the academic field, based on surveys of scholars and content analysis of articles: The field of strategic management deals with (a) the major intended and emergent initiatives (b) taken by general managers on behalf of owners, (c) involving utilization of resources (d) to enhance the performance (e) of firms (f) in their external environments.

Cutting to the chase, Jay Barney regularly states that strategic management as a scholarly discipline is united by a shared dependent variable: firm performance, and particularly what it is that distinguishes firms that persistently perform better than their competitors. Strategy is ecumenical: One can put almost anything on the right-hand side of the regression equation, as long as sooner or later you get to explaining why some firms perform better than others. Broadly, there have been two classes of answer: the characteristics of the industries that firms select themselves into (Porter, 1980) and the characteristics of the firms themselves (Barney, 1991). Strangely, after three decades of rivalry, both are still standing, and both are taught in every business strategy course.

Thus, it appears that strategy and organization theory fail to connect because of a basic intellectual division of labor. Organization theory explains why organizations have the structures and practices that they do, and strategy explains what effect this has on performance. Organization theory is like biology; strategy is like medicine. In the intellectual assembly line of the business school, these are evidently nonoverlapping magisteria.

What Happens if Firms Disappear?

RBV and organization theory both assume that firms are social institutions, more or less bounded vessels capable of containing members and other assets. Organization theory asks why they look and act the way they do; RBV asks what enables some to perform better than others over extended periods.

But what if ongoing firms cease to exist? After all, as Cyert and March (1963) point out, within traditional microeconomics the firm is just a set of decision rules, a construct that serves as a node in a system of information exchange. Indeed, until roughly 1970, the theory of the firm in economics had very little useful to say about core questions of organization theory and strategy, because firms were effectively placeholders in a theory about markets (Walker, 2016). And some contemporary theorists even denied that firms had the kinds of boundaries that organization theorists took for granted and that might allow the firm to serve as a “vessel” capable of containing resources. Jensen and Meckling (1976: 310-311) claimed, It is important to recognize that most organizations are simply legal fictions which serve as a nexus for a set of contracting relationships among individuals. . . . Viewed in this way, it makes little or no sense to try to distinguish those things that are “inside” the firm (or any other organization) from those things that are “outside” of it. There is in a very real sense only a multitude of complex relationships (i.e., contracts) between the legal fiction (the firm) and the owners of labor, material and capital inputs and the consumers of output.

During the heyday of new theory creation in organization theory and strategy, the U.S. economy was dominated by large, diversified, publicly traded corporations. Blue-chip firms seemed immortal: Nearly every firm in the Dow Jones 30 industrials in 1980 had been there since the early 1930s—American Tobacco, Bethlehem Steel, Eastman Kodak, General Foods, Westinghouse, Woolworth. The typical big firm offered career employment, health and retirement benefits, and support to the charitable sector in their hometown. Hostile takeovers and activist investors bothered only the smallest firms, and bankruptcy was almost unknown in the Fortune 500. Few could doubt that these generation-spanning behemoths were tangible social institutions.

Today, the situation is very different. One-third of the Fortune 500 disappeared through mergers and hostile takeovers during the 1980s, cementing a new ideology of shareholder value. Thousands of firms went public during the 1990s, but most did not last, and today there are fewer than half as many public corporations as there were in 1997. Few firms go public now, and when they do, they typically employ few people, and their life expectancy as independent entities is short. Moreover, few have substantial tangible assets, preferring instead to rent their supply chain rather than buy it.

We are living in a thought experiment: What happens if the transaction costs of using markets to create a firm go to zero? Coase (1937) contemplated this (far-fetched) possibility, and now it is happening in real time. Foss (2000: xxiv) points out that “with perfect and costless contracting, it is hard to see room for anything resembling firms (even one-person firms), since consumers could contract directly with owners of factor services and wouldn’t need the services of the intermediaries known as firms.” That future is now in sight.

How did we get here? To create a firm, one typically needs capital, labor, supplies, and a place to sell as well as some internal processes to put the parts together. Firms exist at the intersection of a set of markets. All the markets that comprise corporations have been transformed over the past 40 years by information and communication technologies (ICTs) that drive down the transaction costs of gathering inputs and selling outputs. The raw ingredients for creating an enterprise today are like a set of Legos sitting on the floor, ready to be turned into a pop-up enterprise.

ICTs Transform Capital Markets: Financialization

Those needing capital and those having capital to invest have endless ways to find each other thanks to ICTs that have made financial markets ubiquitous (a process known as “financialization”). Since 1980, financial markets have become pervasive over geography and ontology. Geographically, stock markets spread around the world after 1980 via “emerging markets.” Surprisingly few countries had stock markets in 1980; now almost all do in some form, including all the former Soviet bloc countries, and you can invest nearly everywhere in the world from your phone (Weber et al., 2009). Markets have also spread ontologically, via securitization. Anything with a cash flow can in principle be turned into a bond that can be sold on a market. Examples include mortgages, auto loans, student loans, corporate loans, business receivables, David Bowie’s future royalties, and your neighbors’ life insurance policies (known as “viaticals”).

What does this have to do with ICTs? First, emerging markets became widely accepted investment destinations with the advent of the Web, which enabled people to easily trade in markets around the world. And the essential ingredients for securitization are a spreadsheet to enable valuation and a way to share it, like the Web. (Movie fans will recall investment professionals in The Big Short poring over spreadsheets in which each row was a mortgage and each column a variable.) No spreadsheet, no asset-backed securities, no mortgage crisis.

ICTs Transform Supply Markets: Nikefication

For Coase (1937), one of the key costs of using markets was shopping for suppliers. Today, anyone can find a vendor for nearly any possible supply online. As a result—just as Coase might have predicted—firms en masse have elected to buy rather than make their inputs, following the lead of Nike. Indeed, almost nothing you buy today in North America is made by the company whose name is on the label.

Examples include televisions (the best-selling television brand in the United States in 2010 was Vizio, with just 200 employees), mobile phones (where Foxconn and other “electronics manufacturing services” vendors do assembly and supplier management for nearly all global brands), pet food (Ontario’s Menu Foods manufactures for most prominent U.S. brands), tomato sauce (LiDestri in Rochester, New York, manufactures dozens of brands in its highly automated factory, including Newman’s Own), the blood thinner heparin, and countless other product categories. There is now a vast sector of highly automated generic producers in every industry that stands ready to make whatever product you can design, and you can shop for them on Alibaba.com.

Anyone can be Michael Dell today. Dell’s insight back in his Texas dorm room was that the parts to assemble an IBM PC were readily available off the shelf and that he could greatly undercut IBM on price. This is true across industries now: If you have a credit card and a Web connection, you can set a factory in motion in Shenzhen making mobile phones, or a sweatshop in Bangladesh making your line of sportswear, or a tomato sauce factory in Rochester, New York, producing your grandma’s recipe. In almost any industry, it’s possible to find a contractor to carry out the actual work without having to build a factory or a server farm yourself. As long as you can share design specifications electronically, you can rent rather than buy.

ICTs Transform Labor Markets: Uberization

Uber has transformed the transit industry in the United States by recruiting hundreds of thousands of car owners to become impromptu taxi drivers. But the essence of Uber is the ability to recruit and pay labor by the task rather than having to hire a whole person as an employee. Uber and its ilk provide proof of concept that smartphone-enabled spot labor markets can recruit, evaluate, and pay labor at large scale. In the San Francisco Bay Area, there is an Uber for nearly everything now. Absolutely anything that one person can do for another can be recruited through an app, from mailing packages and walking dogs to on-demand X-ray interpretation.

There have always been spot labor markets and temporary employment, but smartphones enable spontaneous contracting at very low cost and at very large scale. At the level of the firm, we are seeing even large, brand-name firms, like Google, using temps, vendors, and contractors (TVCs) for core activities of the firm. As of 2019, Alphabet/Google had 102,000 employees but 120,000 TVCs—in other words, most people who worked at Google did not work for Google.

After COVID, the use of contractors is almost certain to become even more pervasive. Now that the virus has uncovered what work can be done from home and what must be done in the office, firms know much more what can be handed off to contractors.

ICTs Transform Product Markets: Amazon

Last, Amazon has transformed product markets by creating a ready channel for sales everywhere. Fulfillment by Amazon (FBA) is fully capable of overseeing the transport of products from warehouses at the port to the consumer’s home and collecting payment.

What can happen when capital, labor, supplies, and a selling market are all available at low cost on the Web? The Instant Pot. The Instant Pot has the distinction of being the first new indispensable kitchen appliance since the microwave oven, and its fan base is legion. It is well designed, well built, and easy to use and has a vast user community that eagerly shares recipes online and through YouTube videos—the culinary equivalent of the Python coding language.

The Instant Pot was designed, prototyped, and self-financed for $350,000 by Robert Wang, an unemployed computer engineering PhD in Ontario, and launched on Amazon. “Marketing” consisted of sending Instant Pots to 200 influential food bloggers and cookbook authors and paying attention to Amazon reviews. “Distribution” consisted of a listing on Amazon.com. “User research” and “engineering” were provided by Wang himself, who claims to have read every one of the tens of thousands of user reviews for insights on how to improve the product. In 2019 Amazon sold 300,000 Instant Pots on Prime Day, while the category overall sells $300 million in products per year.

Most impressive of all? Its producer employed just 50 people outside Ottawa. The firm was, essentially, a pop-up, able to grow to incredible scale with almost no assets and very few employees.

There is a strong foundation of theory undergirding the resource-based view (e.g., Demsetz, 1973; Penrose, 1959). Barney (1991) takes that rich history along with the strength of his contributions and simmers RBV down to an easily digestible concept that almost belies the complexity of the entire enterprise. But that concept, VRIO—valuable, rare, inimitable, and organized to exploit—gives us an understanding of the qualities of the resources that a firm would need to acquire through strategic factor markets in order to pursue potential economic rents in product markets. While the Instant Pot was not specifically considered by Barney, he does anticipate what should happen: The makers of the Instant Pot should enjoy a temporary competitive advantage.

Now a temporary competitive advantage does not on its face seem consistent with moving 300,000 units on Prime Day. But part of the Instant Pot’s initial success can be attributed to its first-mover advantage in the market. In RBV, such an advantage can appear when there are heterogeneous resources controlled by a firm in an industry (Barney & Clark, 2007). In this case, one of the heterogeneous resources was Wang’s unique insight regarding the opportunity to implement a strategy for a specialized cooking device, and he was able to execute this strategy before anyone else. The configuration of factors that came together into the Instant Pot were, for a point in time, valuable and rare. But eventually, Wang and his firm’s first-mover advantage should be eroded. The underlying technology was imitable, as was the sourcing of the materials.

The speed with which Wang was able to come to market with the Instant Pot was, in this case, the harbinger of forthcoming imitation. A first-mover strategy can turn into a sustained advantage if a firm is able to gain imperfectly imitable resources before other firms can execute similar strategies. Gaining access to distribution channels, setting up a complex supply chain, and cementing reliable branding strategies are the kinds of resources that are imperfectly imitable and may serve as barriers to entry for potential imitators. But in a time when one can marshal previously complex resources in short order, such as setting up a distribution channel on Amazon, spinning up a production chain in Shenzhen, and establishing a brand on Instagram at a low cost, barriers to imitability are in much shorter supply.

The Instant Pot is far from unique. Thanks to Amazon and Alibaba, there are now thousands of entrepreneurs launching countless new products and services aiming to “disrupt” any incumbent still able to charge a margin. In the technology sector, every scruffy bootstrapper has access to free, open-access tools and can easily scale up (or down) using Amazon Web Services. Even industry “giants” can get by without tangible assets: Netflix still rents server space from its competitor Amazon, and in spite of being a global brand operating in scores of countries, it has just 8,600 employees, all of whom understand that they have a job at Netflix only as long as they are indispensable. And TikTok built a global social media phenomenon with just 35 employees.

The entrepreneurial role of a Michael Dell is being increasingly automated, as algorithms search Amazon’s endless pages for products that seem overpriced—dongles, clothing, cosmetics, humidifiers—in order to snap together an insta-firm to design, prototype, manufacture, and distribute the product for the brief period when margins still exist.

ICTs Transform Internal Organization: The Webpage Enterprise

We have noted that ICTs have transformed the constituent markets that enable the creation of firms. The final threat to firms may come from the algorithmization of management itself: the webpage enterprise (Davis, 2016). A webpage enterprise coordinates inputs to create outputs through software and algorithms rather than via hierarchy, much as a webpage coordinates calls on resources to create the output on a browser. Coase (1937: 390) claimed that “the main reason why it is profitable to establish a firm would seem to be that there is a cost of using the price mechanism. The most obvious cost of ‘organising’ production through the price mechanism is that of discovering what the relevant prices are.” But of course today it is trivial to write a bot to shop for the cheapest vendors for capital, labor, and supplies and perhaps to create a software recipe to put the parts together (just as a webpage uses code to combine external resources to produce a “product”). We can only assume that at this moment there are clever entrepreneurs writing programs to search Amazon for any products that seem to yield a margin, contract with vendors on Upwork to design a reasonable knockoff, forward the design to vendors located on Alibaba.com to produce it, and get it shipped to FBA for distribution (Kellogg, Valentine, & Christin, 2020; Valentine, Retelny, To, Rahmati, Doshi, & Bernstein, 2017).

But what do we lose in a world of algorithmic coordination, supply chains for rent, and Amazon fulfillment on the fly? To deepen this point, let’s return to one of the theoretical forbearers of RBV. Penrose (1959) helped us to understand that by viewing a firm as the manifestation of a production function, we were abstracting away all of the deep and interesting theoretical action. And she showed that it can better be understood as a bundle of productive resources paired with an administrative function that coordinates and connects these complex productive resources. But what we are perhaps seeing today is an erosion of the need for the administrative function and the bundle of productive resources to be colocated within firm boundaries. As suggested earlier in this piece, when transaction costs go to zero, with production no longer at the technical core of the firm, and the coordination of productive resources being managed by fewer and fewer individuals, we see quite the opposite of the growth of the firm. In losing the pairing of the administrative function and productive resources, there is the potential for the loss of one strong source of inimitability: social complexity. Complex social interaction within a firm, which allows for the coordination of physical, financial, and human resources, is particularly difficult for any one person to manage or understand it in its entirety (Barney & Clark, 2007), and as a result, it is hard for that resource to be duplicated by, or transferred to, another firm. In some ways this resource, whether you refer to it as firm culture or distributed managerial capabilities, is one of the most imperfectly imitable resources as it is both obscured by and embedded in the human network. As a world of declining transaction costs results in the creation of fewer firms, we lose the firm as the vital substrate in which inimitable social complexity is grown. And while we may enjoy lower prices for products as a society, this may well mean fewer opportunities for economic rents to be gained by would-be business owners.

The Challenge of Disappearing Firms for RBV and Organization Theory

A world without organizations will, of course, be a challenge for organization theory. One of us has spent a career studying organizations and writing books and articles whose titles almost inevitably include the phrase “organization theory.” It is a challenge, to say the least, to encounter a world in which organizations are increasingly evaporating, to be replaced by impromptu assemblages. The language that we use to describe the world—“industry,” “firm,” “employee”—seems increasingly disconnected from the world that we encounter, which is both disorienting and exhilarating. Organization theory as a field has responded by replacing the noun “organization” with the verb “organizing.” Scholars increasingly study social networks, social movements, and the logics that guide action. A pickup basketball game is not the same as the NBA, but there are still rules that guide action and can be documented and understood.

But can RBV survive without firms as the vessel in which to house the resources? The answer to this question is likely yes. A strength of RBV is that it is not a theory of organizations (e.g., founding and structure) but a theory of how productive resources can be used to secure economic rents and attributes of resources that can help yield these persistent profits. So RBV’s relevance doesn’t require firms. It is rather that to date, firms housing lots of interacting humans have been the key site for developing resources that are valuable, rare and imperfectly imitable, using social complexity as the creative engine. Given the disappearing multiperson firm, a first question to ask about this future is, Can a firm of one have a sustainable advantage? Probably. The ability to both see and have better expectations around strategic opportunities is a resource that can be developed absent the firm context. Another name for this ability is simply “entrepreneurship.” We have already seen instances of the RBV and entrepreneurship literatures being pulled together (e.g., Alvarez & Barney, 2004).

A second question is, Other than firms, are there places where human social complexity can create inimitable resources? Though the firm as broadly conceived may be on the decline, alternative forms of organizing economic activity are on the upswing. Households, extended families; neighborhoods; industrial districts; online communities, such as Python users or Linux contributors—all may turn out to be sites characterized by VRIO, to greater or lesser extents.

A third question to pose about our evolving world is, Can firms take advantage of social complexity in extraorganizational settings? Theorists have pointed out that there are uniquely valuable resources that cannot be owned or controlled by the firm but that can nonetheless be a source of value, particularly if the firm is able to customize or co-specialize the resource (Jacobides, Winter, & Kassberger, 2012). Some firms benefit from communities around their products and brands. Lego has Lugnet, an internet-based user group for adult fans of Lego. Harley Davidson has the Harley Owners Group. Instant Pot users have a multimillion-member Facebook community that shares recipes specific to the Instant Pot. While the companies can provide support to these groups, the groups exist outside the boundaries of the firm, and their continued existence is a product of the social connections that are created and reaffirmed within the group context. And, much to the chagrin of companies that have tried to create such communities and failed, these groups are often imperfectly imitable and can increase people’s willingness to pay for the associated products. And as such, they can be part of a source of economic rents. These three questions are by no means exhaustive, but rather samples of questions that provide some directionality for future research.

Conclusion

In the Costa Rican rain forest, howler monkeys and spider monkeys coexist peacefully, with roving bands passing by each other amiably as they seek their food. From a distance, they seem similar in size and physique. How are both species able to survive in the same ecosystem? Why doesn’t one species outcompete the other? The answer is straightforward: Howler monkeys mostly eat leaves, while spider monkeys eat fruits. Thus, they are able to thrive on their distinct diets and mostly ignore each other, even when they are wandering around the same forest and eating from the same trees.

We opened with a puzzle: Why do the academic fields of strategy and organization theory have so little interaction? Why are ideas from organization theory scarcely used in strategy, and why does RBV have so little traction in organization theory? Our tentative answer is that they simply seek to answer different questions. Like spider monkeys and howler monkeys, they are dining on different dependent variables. But as the ecosystem for firms changes, both face a new existential threat. What is organization theory without organizations? Why explain firm performance if there are no more firms? This is, perhaps, a useful punctuation point to reconsider the mutual indifference between these two domains.

Footnotes

Acknowledgements

This article was written while Davis was a Fellow at the Center for Advanced Study in the Behavioral Sciences at Stanford. We thank Dave Ketchen for his thoughtful editing. Dick Nelson helped us think about organizations as vessels for collaborative routines, and Sid Winter gave insightful comments on the nature of organizational performance.