Abstract

We describe the interplay between the resource-based view (RBV) and strategic human resources (HR)/human capital (HC) literatures in select areas of particular interest. In each area, we aim to highlight key issues, review relevant evidence where available, and identify future research needs. We begin by reviewing research on HR-related firm heterogeneity. We then discuss best practices in HR, including evidence of the large apparent value they create. We also consider different views on the value and ease of imitation of best practices, including implementation challenges. Next, we briefly address the key roles of microfoundations and complementarity in helping understand the potential for value creation and value capture through the use of best practices. We then ask whether the use of best practices in the pursuit of competitive parity might warrant greater attention as this may be where the largest potential gains can be made. Finally, we consider a number of developments in the strategic HC literature, especially those related to firm-specific human capital (FSHC). We raise questions with views on issues such as the consequences of FSHC for workers; the definition and measurement of FSHC; whether worker immobility, a key to value capture, is good from a social return (or even a firm) return perspective; and the relative emphasis on value capture and value creation.

Overview: RBV Impact on Strategic HR and Human Capital (HC)

Traditionally, the study of human resources (HR) focused primarily on the individual level of analysis. That began to evolve to include higher levels of analysis, including the plant level in the 1980s, especially in related industrial relations work (e.g., Katz, Kochan, & Gobeille, 1983) and gained steam in the 1990s (e.g., Arthur, 1994; MacDuffie, 1995). Work studying HR effects on performance at the firm level followed, of individual practices (e.g., compensation, Gerhart & Milkovich, 1990), and then of systems of HR practices (e.g., Huselid, 1995).

In 1996, a forum followed in the Academy of Management Journal on HR and “Organizational Performance.” Jay Barney’s (1986, 1991, 1995) work on the resource-based view (RBV) of the firm was front and center, including that “firms can develop sustained competitive advantage only by creating value in a way that is rare and difficult for competitors to imitate” (Becker & Gerhart, 1996: 781). Further, “a complex social structure such as an employment system” (p. 781) or “HR system,” might be of particular interest because it might be “especially difficult to imitate . . . [if] deeply embedded in an organization.” Becker and Gerhart (1996) also highlighted Barney’s (1995: 56) argument that individual practices “have limited ability to generate competitive advantage in isolation [but] in combination . . . can enable a firm to realize its full competitive advantage,” pointing to the central importance of complementarity. Indeed, RBV took the importance of complementarity to another level, identifying its role not only in value creation but also in value capture, given that complementary practices would be more difficult to imitate than best practices, even if they fit generic business strategies.

Since the 1990s, the RBV has been a major influence on strategic HR and later strategic HC. Wright and McMahan (1992: 303) noted that “great potential exists for . . . resource-based theory in [strategic HR] research,” and Wright, McMahan, and McWilliams (1994) provided further advances. According to Kaufman (2015: 516-517), the “RBV . . . has been hugely influential . . . and most . . . agree that it is the central pillar [p. 516] of theory in the strategic HRM field.” He quotes Nyberg, Moliterno, Hale, and Lepak (2014: 319) that RBV is “the linchpin that connects the strategy and strategic HRM research literature[s].” Jiang and Messersmith (2018) documented this central role of RBV. Their metareview of 64 conceptual and 4 meta-analytic reviews in strategic HR identified the use of more than 20 theoretical perspectives. By far, the most frequently mentioned was the RBV. At the same time, there is acknowledgment that there are few if any direct tests of RBV in strategic HR (Kaufman, 2015; Wright, Dunford, & Snell, 2001), with RBV instead serving more “as a backdrop in SHRM and strategy research” (Delery & Roumpi, 2017: 4). Thus, one goal of ours is to point out opportunities for more direct tests.

In this paper, we describe the interplay between RBV and strategic HR/HC in specific areas that we consider especially important for attention and direct empirical investigations. We begin with research on HR-related firm heterogeneity. We then discuss best practices in HR, including evidence on the value they create, as well as different views on their ease of imitation. Related to this, we address microfoundation issues and consider whether competitive parity warrants greater attention. Given the central role of firm-specific human capital (FSHC) in strategic HC literature, we devote a good deal of attention to it, including some challenges to received wisdom. We identify future research needs along the way (summarized in Table 1).

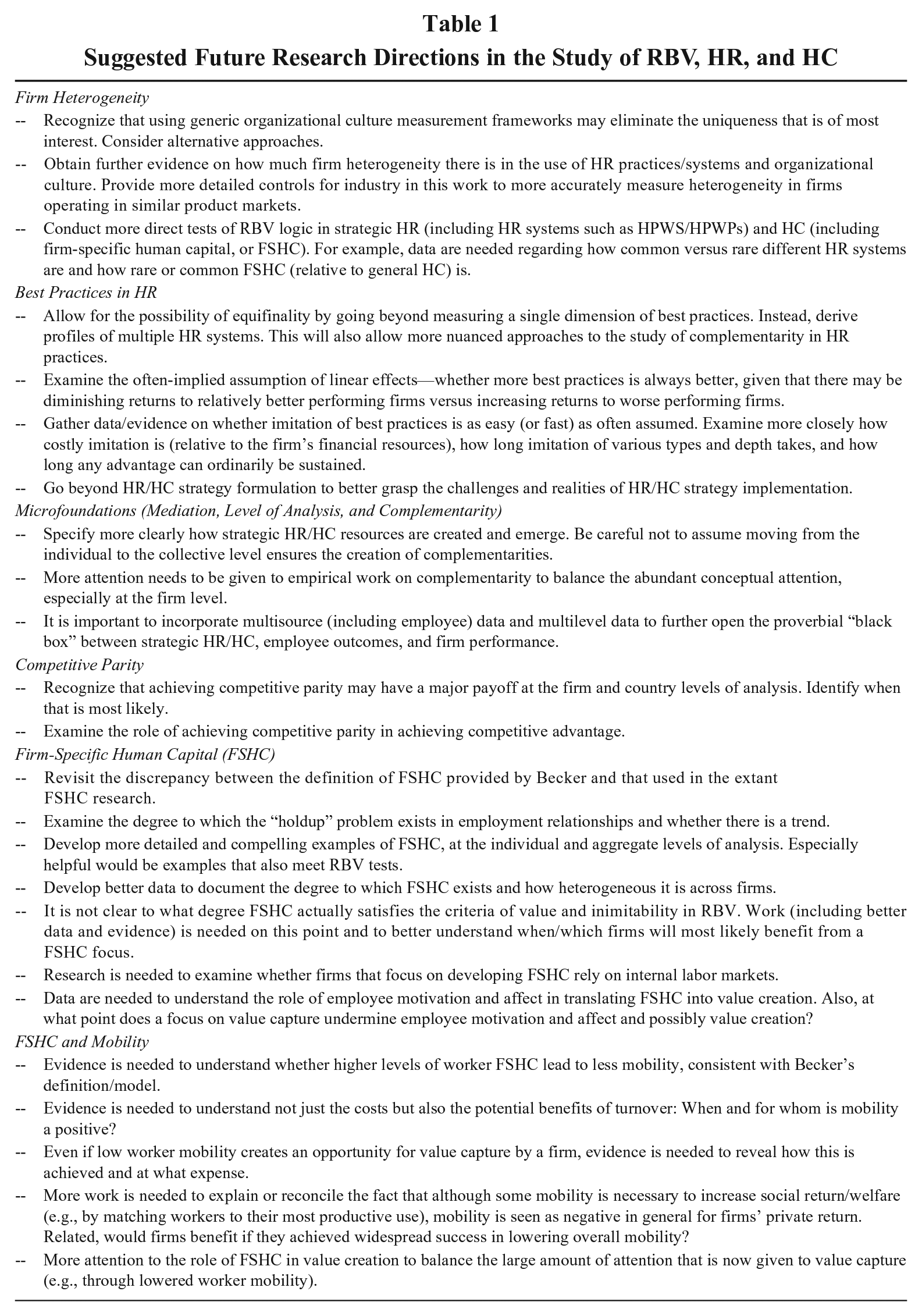

Suggested Future Research Directions in the Study of RBV, HR, and HC

Firm Heterogeneity: Evidence from HR

Firm heterogeneity in resources is a requirement of the RBV. However, much work focuses on how context constrains firms to become similar (e.g., Johns, 2006, 2017), whether due to market forces, institutional pressures, or legal systems (see review by Gerhart, 2009b). To date, the most common way to assess firm heterogeneity in strategy (and industrial-organizational economics) is to decompose variance in financial performance into industry and firm components (e.g., Schmalensee, 1985). Results vary, but overall there is substantial evidence of firm heterogeneity (e.g., the summary in Goddard, Tavakoli, & Wilson, 2009: Table 1).

Economists too increasingly see firm (and/or plant) differences in productivity as important. Fox and Smeets (2011: 961) observe that “measured differences in productivity across plants in the same industry are usually large . . . [and] persistent across time.” They add “. . . our results suggest that productivity mostly represents some attribute of a firm that cannot be easily bought and sold.” Likewise, Syverson (2011: 326) states that “[researchers] have documented, virtually without exception, enormous and persistent measured productivity differences . . . even within narrowly defined industry” and further that “. . . the evidence that management and productivity are related is starting to pile up.” These findings certainly fit well with the RBV.

HR research provides evidence on firm differences in employee attributes. Schneider, Smith, Taylor, and Fleenor (1998) found that 24% of the variance in four individual-level employee personality traits occurred between 142 organizations studied. Likewise, Oh, Kim, and Van Iddekinge (2015) found that 37% of the variance in individual level personality (using the “Big Five” traits) occurred between organizations. Evidence also documents (stable) organization differences in employee attitudes (Fulmer, Gerhart, & Scott, 2003; see also Hansen & Wernerfelt, 1989). The organizational culture literature is of particular interest given that Barney (1986) emphasized its likely key role. Gerhart (2009a) reanalyzed data from Chatman and Jehn (1994) and found that industry explained 19% of the variance in organization culture means (i.e., 81% was unexplained). Organization culture differences may partly correspond to the firm differences in employee attributes described above, which occur via matching. 1

A challenge is that organizational culture, like business strategies, is usually measured in terms of generic types. For example, Hartnell, Ou, Kinicki, Choi, and Karam (2019) report the following zero-order corrected correlations between strength of high performance work system (HPWS) and strength of clan (.46), adhocracy (.48), market (.44), and hierarchy (.45) organization cultures. Thus, the variance explained ranged from 19% to 23%. Similar, maybe too similar. Another issue is that almost by definition, coding cultures into a generic typology eliminates any uniqueness. Different culture data may be required.

Heterogeneity is assumed to exist in HR/systems. Cappelli and Crocker-Hefter (1996: 7) argue “there are examples in virtually every industry of highly successful firms that have very distinct management practices.” Actual evidence is limited but seems supportive. Based on Table 8 of Becker and Huselid (1998), we computed that 5% of the variance in their unidimensional HPWS index scores was explained by the eight industry categories. 2 Toh, Morgeson, and Campion (2008), by contrast, derived five different multivariable HR “bundles” (systems) and their frequencies across seven industry categories. Again, industry explained little of the firm heterogeneity, this time in use of different HR systems. 3 Thus, it would appear that industry did not explain firm differences in HR system use. Feng and Gerhart (2020) document stable firm differences in employee flow (the sum of hiring rate and exit rate).

Multicountry research provides a unique opportunity to examine RBV logic versus perspectives where constraints, whether industry or country dictates the management strategy that will best fit and thus result in heterogeneity (Gerhart, 2009b; Rabl, Jayasinghe, Gerhart, & Kühlmann, 2014). For example, Newman and Nollen (1996) argue that “differences in national cultures call for differences in management practices.” Johns (2006) argues that “national culture constrains variation in organizational cultures.” Part of the case for firm heterogeneity is evidence that external constraints are not as constraining as often assumed. In this vein, Rabl et al.’s (2014) meta-analysis of 35,767 organizations in 19 countries showed that the mean effect of HPWS on business performance was positive in every country and that the 95% confidence interval across the 19 countries was quite narrow (.20 to .25).

Gerhart (2009b) showed that in the multicountry GLOBE project, 77% of variance in organization culture variance was unexplained by country and 94% was unexplained by national culture specifically. Bloom, Genakos, Sadun, and Van Reenen (2012) report “in our manufacturing sample [in 20 countries] around 11.1% of our management practices [management quality] can be explained by country of location and about 11.9% by industry of operation (using 254 SIC, 1987 three-digit industry codes). Hence, most of the variation in management practices cannot be explained by either country or industry.” It would likewise be instructive to know how much firm heterogeneity there is in investment in HC, specifically general versus firm-specific. So far, this is something much discussed but rarely if ever empirically examined.

Best Practices in HR: Evidence of (Unexpectedly?) Large Effects

A common view in strategy described by Coff and Kryscynski (2011) is that “fully codified [HR] solutions are easily understood and, thus, unlikely to offer sustained competitive advantages on their own. . . .” This relates to “rules for riches” “that any firm can apply to gain sustained competitive advantages and economic rents” (Barney, Della Corte, Sciarelli, & Arikan, 2012: 133). Under RBV, “it is not possible to deduce rules for riches” because competitive advantage cannot be sustained in the presence of “well-known, widely understood managerial practices” that create value. Similarly, Teece (2014: 330) states “best practices alone are generally insufficient to undergird sustainable competitive advantage, except in weak competitive environments . . . because much of the knowledge behind ordinary capabilities can be bought through consultants or through a modest investment in training (Bloom et al., 2013).”

Thus, it is perhaps surprising that there appears to be quite a lot of evidence that HR practices and business performance are strongly positively related. In addition to well-known studies such as MacDuffie (1995) and others cited earlier, Combs, Liu, Hall, and Ketchen (2006) conducted a meta-analysis and they found a corrected r = .20 between high-performance work practices (HPWPs). (As noted, Rabl et al., 2014, obtained similar results.) Thus, according to Combs et al. (2006), an increase of 1 SD in HPWPs implies an increase of ROA from 5.1% to 9.7%, a 90% increase. Combs et al. also found a corrected r = .28 focusing only on HPWSs, which implied an increase of 1 SD in HPWSs would translate into an increase of ROA from 5.1% to 11.5%, a 126% increase. (Of course, causal inference is not typically a strong suit of meta-analysis.)

Bloom and Van Reenen (2007) collected data on medium-sized (employment of 50 to 10,000, median = 675) manufacturing plants/firms in four advanced economies: France, Germany, United Kingdom, and United States. They report the productivity of firms in the upper quartile of management quality is 32% higher than those in the lower quartile (a difference of roughly 1 SD). (Management quality includes HPWS practices but also the dimensions of targets and monitoring.) Later studies in their research program using more countries found similar results. A meta-analysis by Heugens and Lander (2009: 77) found “conformity to institutional ordinances” improved organizations’ performance while allowing some room for them to differentiate themselves from competitors.

Of course, not all firms are likely to benefit equally from best practices due to their different strategies and circumstances. In this regard, few studies have derived anything more than a single HR dimension, where high is good and low is bad. Exceptions include Ichniowski, Shaw, and Prennushi (1997), Toh et al. (2008), and Tsui, Pearce, Porter, and Tripoli (1997), who derive multiple profiles of employment systems. This opens up the opportunity for considering equifinality as well as more nuanced approaches to complementarity. Another issue is nonlinearity. It seems risky to imply that more best practices is always better. There may be diminishing returns to firms with higher levels of performance and/or HPWPs/management quality versus increasing returns to firms having lower levels. This would be consistent with our later review.

Is Imitation (and Implementation) as Easy (or Fast) as Often Assumed?

Evidence of large positive performance effects of best practices, at least in the HR domain, might indicate that imitation is often not that easy or fast. Evidence indicates (Rynes, Colbert, & Brown, 2002) that firms are often unaware of or do not follow academic research on HR best practices. Posen and Martignoni (2018) emphasize “the inherent difficulty in the transfer of practices within and across organizations” and note challenges such as “not-invented-here syndrome” and those identified in work on absorptive capacity. Organizational change, organization learning, and institutional theories also focus on the difficulty of imitation. Further issues arise in a global context. For example, even limited success in imitating a competitor in one country product market could translate into competitive advantage in other product markets where best practices have diffused less (Rabl et al., 2014).

Given that Barney and Wright (1998) used Southwest Airlines as an example of meeting RBV tests, we cannot help but observe it was only after decades and with the aid of bankruptcy that other carriers were able to match Southwest’s labor costs, even though labor costs arguably do not meet RBV tests. The Southwest advantage in customer outcomes has yet to be imitated (see Gerhart & Newman, 2020: Exhibit 7.2). Similarly, only through bankruptcy did U.S. automakers narrow (but not close) the labor cost gap with Japanese producers. Again, however, other advantages (e.g., car reliability) have still not been imitated (Gerhart & Newman, 2020: Exhibit 7.1). These examples show that even after decades, (substantive) imitation is not always easy. Although in these examples we are looking at decades, the duration necessary to qualify as sustained (e.g., Bromiley & Rau, 2014) does not seem to be precisely defined in the RBV. Again, imitation is not all or nothing, and it matters also how easy it is/how long it takes.

Teece (2014) cites Bloom et al. (2013) to support his conclusion (see above) that “ordinary capabilities” (aka best practices) “can be bought through consultants for . . . a modest investment. . . .” Bloom et al. (2013) conducted an intervention to raise management quality in a single industry (textiles) in a single, low productivity country: India. They found implementing higher quality management practices in 20 experimental plants (relative to 18 control plants) in India led to sizeable productivity gains (16.65%). As noted, Teece described what this took as “a modest investment in training.” In fact, Bloom et al. (2013: 13) note that the consulting service, which was subsidized, would have cost each firm about $250,000. The median firm had annual revenues (not profits) of $6,000,000. Desrani (2013) reported that average net profit/revenue during the 2008–2012 period for five Indian textile companies studied was 2.6%. On $6,000,000, that would be $156,000. Thus, the cost of the consulting required to raise productivity by 16.65% would have cost the equivalent of about $250,000/$156,000, or 1.6 times the annual profit. That does not sound like an easy or likely path (given the uncertain return to such a large investment) to adopting best practices.

Implementation

Jewell, Jewell, and Kaufman (2020) review a number of challenges. They start with Pfeffer’s (1994) one eighth rule: (1) Only one half of company leaders believe it works in practice, (2) only one half of those decide to try it, and (3) only one half of those successfully implement it (½ × ½ × ½ = ⅛). Delery and Roumpi (2017) describe the assumption that best practices will easily diffuse as “inherently flawed.” Jewell et al. (2020) state, “It is not obvious . . . what kind of actions companies should implement . . . which practices? what combination? . . .how far they should go with it, how it affects and fits with the other parts of the business, what are the revenue, cost, and return on investment implications, and why other firms looking to please their shareholders haven’t already grabbed this low-hanging fruit (Kaufman, 2015).” Jewell et al. (2020) continue: “No CEO or consultant is going to step in front of the board of directors and advise them to invest several hundred million dollars in a new HPWS facility on the basis on this kind of blunt and untrustworthy research evidence.” (Recall here our discussion of the Bloom et al. 2013 study in India.)

Is It “Imitation”? Uniqueness Introduced During Implementation

Best practices may be customized/hybridized during implementation to the new setting even where it appears to be simple imitation (Rabl et al., 2014). Pfeffer (1994: 64-65) argues there are best HR practices but offers an important qualification: “Obviously, how one would implement these practices will vary significantly, based on a given organization’s strategy and its particular technology and environment,” which he referred to as “the contingent nature of the implementation of these practices,” something “everyone would agree is necessary.” Ansari et al. (2010: 67) argue “management practices often cannot be adopted by user organizations as ‘off the shelf’ solutions’ but rather in the process of diffusion and implementation across firms, practices are likely to evolve . . . requiring custom adaptation, domestication, and reconfiguration to make them meaningful within specific organizational contexts.” Becker and Gerhart (1996) likewise noted that different firms adopting the same general principle could implement it in very different ways. Of course, best practice adoption varies in intensity and coverage and can be ceremonial rather than substantive (Oliver, 1991).

Barney (2001: 53-54) in an earlier retrospective on the RBV acknowledged that implementation had received too little attention in his 1991 article. This remains true 20 years later, especially if, as it appears, this is where significant firm-specificity is created. Perhaps this offers an opportunity for RBV research to better understand how competitive advantage is created. 4 Ketchen, Crook, Todd, Combs, and Woehr (2017: 284) observe examining “possession of strategic resources” is not sufficient. Examining “what a firm does with its resources” (Holcomb, Holmes Jr, & Connelly 2009: 461) is also critical. This helps explain growing attention to HR/HPWS/HC practices/systems, including microfoundations. Similarly, Bromiley and Rau (2014: 1249) state that “current strategy scholarship . . . rarely considers specific, actual techniques managers might use to develop strategies or generally applicable firm practices.”

Microfoundations: Mediation and Level of Analysis

We very briefly comment on two key issues related to the causality issue (e.g., Jewell et al., 2020 above). “Without intervening variables, one is hard pressed both to explain how HR influences firm performance and to rule out an alternative explanation” (Becker & Gerhart, 1996: 793). Jiang, Lepak, Hu, and Baer (2012) conducted a meta-analysis of the ensuing work on mediation. Using their Figure 4, we compute the total effect as a 1 SD increase in HPWSs is associated with a .40 SD increase in firm financial outcomes. Using their Figure 4, we also estimate 1% of that total HPWS effect is mediated by HC. A limitation is a lack of distinction between FSHC and general HC. Most (see their appendix) look to be general. See also the meta-analysis of the relationship between HC and performance by Crook, Todd, Combs, Woehr, and Ketchen (2011), which provides the best effort to distinguish between FSHC and general HC and found that FSHC better predicted firm performance.

Understanding level of analysis is another key in causal inference. Ployhart and Moliterno (2011: 127) state that “there is no fully articulated multilevel theory describing how the HC resource is created and transformed across organizational levels. While the recent strategic HR management (SHRM) literature [on mediating mechanisms] in some ways fills the gaps . . . it focuses primarily on organizational practices . . . and does not focus as much theoretical attention on how HC resources are created” (see also Gerhart, 2005). Coff and Kryscynski (2011: 1432) agree that “an excessive focus on firm-level HR practices has obscured the inherently multilevel nature of HC (Ployhart & Moliterno, 2011).” Likewise, it is “more than an individual-level construct” (Coff, El-Zayaty, Ganco, & Mawdsley, 2020: 58) due to “the socially constructed nature” (Ployhart, 2015).

Complementarity: Crucial But What About Evidence?

Becker and Gerhart (1996) highlighted the RBV concept of “complementary resources” and its key argument (Barney, 1995: 56) that individual policies or practices “have limited ability to generate competitive advantage in isolation [but] in combination . . . they can enable a firm to realize its full competitive advantage.” According to Milgrom and Roberts (1992: 108), “several activities are mutually complementary if doing more of any activity increases (or at least does not decrease) the marginal profitability of any other activity in the group.” Further, “a group of activities is strongly complementary when raising the levels of a subset of activities in the group greatly increases the returns to raising the levels of the other activities” (p. 109).

This idea of complementary resources (and related concepts such as fit and synergy) is fundamental to what developed in strategic HR and later in strategic HC (e.g., FSHC) to meeting RBV tests. Complementarity is uniquely important because it can result in both value creation and value capture (Chadwick, 2017). To satisfy the “creating high value” part, it seems likely, as noted, that FSHC must be, as Coff et al. (2020: 58; see also Chadwick, 2017) put it, “more than an individual-level construct” and rather “a co-developed resource between employees, firm resources, and other stakeholder, and accrues with time and experience in a focal firm” and probably also “insights from customer interactions and relationships” (e.g., Greer, Lusch, & Hitt, 2017). This seems logical and others agree. For example, Ployhart and Chen (2019: 363) state, reminiscent of Pfeffer (1994), that “any collective HC resource will necessarily be specific to a firm because of emergence processes, the nature of the performance outcomes, and the firm’s strategy (Kryscynski & Ulrich, 2015; Ployhart, Nyberg, Reilly, & Maltarich, 2014). Similarly, as Ployhart (2015) argued, the socially constructed nature of most meso-level constructs (particularly group and team processes) ensures that those resources are specific to a firm.”

The problem is that although it garners much attention, there is arguably little evidence that complementarity in HPWS or strategic HC, whether due to emergence processes or otherwise, actually exists at the firm level (Chadwick, 2010; Gerhart, 2007; Gerhart, Trevor, & Graham, 1996). 5 The Nyberg and Moliterno (2019) volume contains many chapters that address the theoretical importance of complementarity, but none appear to examine empirical evidence or even call for research to document and quantify its actual importance. (Brymer and Hitt, 2019, come the closest and their Table 15.1 is a nice way to think about complementarity.) In his 2010 review, Chadwick observes “despite widespread acceptance” that complementarity exists “current research suggests [it] . . . is not a given and that evidence . . . can, in fact, be overstated.” He continues, “no one has yet described where” complementarities “in HRM systems really come from. . . . Instead, synergy is most often invoked metaphorically . . . as a loose rationale for working with aggregations of HRM practices.” Brymer and Hitt (2019) similarly observe that “we have much to learn about human capital complementarities, how they are formed, and why they work (or do not).” 6

Competitive Parity: Does It Warrant Greater Attention?

The evidence on the large positive (main) effects of HR/HPWS best practices raises a broader question: Has the payoff to adopting best practices, which as we have seen is itself no small accomplishment, even if “just” to achieve competitive parity and/or to exceed competitive parity on a less sustained basis, been undervalued? The RBV focus on how firms achieve (sustained) competitive advantage is clearly important and interesting. So too, however, would be greater attention to the large (roughly one half) firms that have yet to achieve competitive parity. It may be that division of labor is efficient here and that it can perhaps be left to theories other than the RBV (e.g., organization learning) to focus on how firms get to parity.

However, there is a compelling reason not to overlook low-performing firms: The potential for new value creation may be greater for them and for the economy than in already high-performing firms. In their study of productivity in U.S. manufacturing, Baily, Hulten, and Campbell (1992) examined productivity growth in U.S. manufacturing. For plants that were observed for at least a 5-year period, only 5–14% of total industry productivity growth occurred in plants that were in the top two quintiles of productivity growth at the beginning of each 5-year period. The remaining growth (86–95%) came from plants that had been in the bottom three quintiles of productivity level at the beginning of each 5-year period. In low-productivity countries, growth by low-performing firms could be even greater, given the long tail of low-productivity firms in such countries (Bloom & Van Reenen, 2010).

At the country level, using 2019 gross domestic product (GDP) per employee, in constant dollars, adjusted for purchasing power, and looking at the five largest (in terms of GDP) economies in the world, the weighted mean productivity (weighted by GDP) in Germany, Japan, and the United States is $117,201, about 4 times as large as the $28,404 for China and India. At the same time, we also see that China and India have had much large productivity growth. For example, weighted mean productivity for China and India combined grew from 2000 to 2019 by a factor of 4.3, versus by a factor of 1.3 in Germany, Japan, and the United States. At those rates, productivity in China and India would double every 15 years, versus taking 55 years to double in the three more advanced economies. Again, the largest potential gains in productivity are in the least productive economies, which are composed of the least productive firms.

Both value creation and value capture, of course, are of vital importance. However, value creation is what makes everything go. Productivity levels and growth are a central focus because these hold the key to standard of living levels and growth. According to the World Bank in China, “since China began to open up and reform [and grow] its economy in 1978, more than 850 million people have been lifted out of poverty.” Thus, although it says income inequality “remains relatively high,” and there are still many with low income in China, the tremendous value creation has translated into a tremendous value capture as well for hundreds of millions of people. Achieving competitive parity is critical especially for relatively worse-performing firms, including in the less developed economies (Jayasinghe, 2016), given that productivity growth comes disproportionally from low productivity plants and countries. Teece (2014: 331) seems to agree in this instance: “I don’t mean to denigrate the importance of ordinary capabilities; they are often fundamental and can support competitive advantage for decade-long periods. Indeed, in developing countries, mastering existing technologies and practices may be more important than innovation.” Again, competitive parity can be an important achievement. 7

FSHC and Competitive Advantage

As nicely summarized by Coff et al. (2020: 58), under the RBV, “resources held by firms . . . generate and sustain competitive advantage by creating high value for the focal firm while remaining unavailable to other firms and being difficult to imitate, at least in the short run. . . .” It is easy to see why FSHC is seen as a prime candidate to satisfy these two criteria and thus received so much attention. As such, we also devote considerable attention to FSHC.

It is not clear that FSHC actually satisfies these two criteria. One challenge concerns how FSHC actually “creat[es] high value.” Presumably, the key to creating value (and rareness and nonsubstitutability) through FSHC involves creating complementarities. However, based on our earlier review, although there is much theorizing about complementarities, upon close inspection, there is not much compelling evidence to support their existence. Even more fundamental is the lack of both theory and data on when/which firms will benefit from a FSHC focus. Likewise, within firms, it is unlikely that the same HC approach will work for all employee groups (Lepak & Snell, 1999). There is more evidence on FSHC satisfying the “remaining unavailable” criterion, which we will address shortly.

Defining FSHC and Its Impact on Workers

Campbell, Coff, and Kryscynski (2012: 379) summarize a strand of thinking in the strategy literature, which appears to see firms capturing the value of FSHC investment returns at the expense of workers: “By investing in firm specific skills, workers increase their use value to their employers, without accompanying increases in their exchange value in the labor market . . . then workers face a dilemma . . . firms can retain workers with firm-specific HC for less than the full use value . . . [which has] led to the . . . assumption that [this] hinders workers mobility [and] it is assumed that workers may move [only] if they are willing to accept reduced wages.” One specific example of this argument is Morris, Alvarez, Barney, and Molloy (2017), who state “prior work suggests that firms will appropriate most of the value created by the firm-specific investments made by their employees (Becker, 1964).”

This view, however, appears to differ from Becker’s (1964/1973: 40) work on FSHC: “Completely general training increases the marginal productivity of trainees by exactly the same amount in the firms providing the training as in other firms. . . . Training that increases productivity more in firms providing it will be called specific training.” In Becker’s model, investment in FSHC is shared and benefits both firms and workers, as does less mobility. 8 “Employees with specific training have less incentive to quit, and firms have less incentive to fire them” (Becker, 1964/1973: 46), and “Both [employer and employee] will be made worse off by . . . separation,” and thus, “the parties attempt to minimize the loss from such separations by optimally sharing the investment” (Hashimoto, 1981: 475). To summarize, firms and workers share the investment costs and the return, and it is in the interest of both to avoid turnover. This remains standard in labor economics (e.g., Lazear & Gibbs, 2014: chapter 3).

Of course, there is almost always a possibility that a contract, whether explicit or implicit, will be violated, as agency and related theories (e.g., Milgrom & Roberts, 1992; Williamson, 1985) recognize the form of postcontractual opportunism (moral hazard), or the “holdup problem.” In the case of the shared investment in FSHC, Lazear and Gibbs (2014: 60) note that “the firm may be tempted to renege on its promise and renegotiate after the investment is made . . . to capture some of the profits from the investment that the worker made.” This is a major focus of the strategy literature in studying FSHC (Wang & Barney, 2006; Wang, He, & Mahoney, 2009). Lazear and Gibbs note sharing the benefits of the shared investment helps avoid the concern but does not eliminate it. They argue that “reputation and trust” become important (see also Wang et al., 2009) and essentially argue that in such cases “the employer will adopt policies that foster an internal labor force where employees are hired at the bottom and spend long careers working their way up the corporate ladder in the firm” (p. 67). In other words, firms will rely on internal labor markets (ILMs; Wachter & Williamson, 1978).

FSHC is a fundamental aspect of ILMs, which have traditionally been viewed as good for and sought out by workers. ILMs (Doeringer & Piore, 1971) are characterized by career jobs, promotion from within, and seniority as a major factor in promotion, layoff, and pay decisions. This all acts to reduce turnover/increase immobility. That this is desired by workers is evidenced by the fact that ILMs have traditionally been a bargaining goal for unions, not despite, but because they discourage worker mobility, especially competition from external candidates for higher level jobs obtained via promotion. Evidence does indeed document that ILMs are more likely to be found in unionized settings (Pfeffer & Cohen, 1984) and that declines in firm tenure in large organizations are strongly related to the decline in unionization (Bidwell, 2013).

Further Definitional Issues: Has Anyone Actually Seen FSHC in the Wild?

A definition is a first step, not the last step. Theory and definition guide measurement/observation, and those data are then used to improve theory and definition. If there is an actual in-depth example of FSHC that meets RBV tests, we have not seen it. In fact, the literature seems to be better at coming up with examples that do not meet RBV tests (e.g., “how to use the photocopier” and do “reimbursable expenses,” Chadwick, 2017: 505; “knowing where the bathrooms are or how to complete an expense report,” Raffiee & Coff, 2016: 782). Examples where FSHC is more likely to meet RBV tests sometimes have to do with customers (e.g., Greer et al., 2017). Here, more explanation is needed on whether this is individual- or firm-level FSHC (Chadwick, 2017) and how immobile the customer relationships are. Other examples use teams. Chadwick (2017: 507) described instances such as the following: “Teams of lawyers are needed to handle the volume and complexity of clients’ transactions . . . complementarities with coworkers that are particular to the firm create value for customers that goes beyond a simple aggregation of individual lawyers’ abilities.” (In such an example, firm-specificity is generated by combining/weighting general skills in a unique way, Lazear, 2009) That is promising. But how rare and nonsubstitutable is such a team of lawyers? Are there no similar lawyer teams elsewhere? Without better data, we do not know how rare/heterogeneous and meaningful FSHC is. Thus, it is not possible to know whether FSHC receives too much or too little attention. Frank and Obloj (2014) provide one of the most diligent attempts to actually measure and quantify FSHC (at the individual level), using ability to predict firm decisions.

HC is recognized to be a unique asset, which includes the need to address workforce motivation (Coff, 1997). Motivation, which, along with opportunity, determines how well skill translates into value creation, may be a good candidate to satisfy RBV tests (see, e.g., Southwest again or other companies with uniquely high workforce motivation or affect; Fulmer et al., 2003). Nevertheless, motivation/affect appears to receive little attention (Chadwick, 2017), even though “consummate cooperation” of employees is necessary (Williamson, Wachter, & Harris, 1975: 266).

Cautions Raised With FSHC Logic About Mobility

The relevance of FSHC has been called into question by the fact that managers seem not to think in terms of FSHC (Kryscynski & Ulrich, 2015) and that workers seem not to be able to accurately gauge the degree to which their HC is FSHC (Raffiee & Coff, 2016), which together have been interpreted to indicate that the firm specificity of their HC may not influence decisions by firms or workers regarding worker mobility. However, that managers do not self-report focusing on FSHC and that employees may not think in terms of FSHC in making turnover decisions does not rule out FSHC influencing actual turnover. Managers may be unaware of the historical origins of longstanding organization practices created over years. (See the concepts of path dependence and social complexity.)

In the case of an individual worker, there is no reason to expect his/her perception of labor market conditions to be predictive of his/her turnover (Gerhart, 1990). Most (80% in Lee, Gerhart, Weller, & Trevor, 2008) workers do not leave one job without having another actual job lined up. Second, one third of the 80% never searched for another job, instead receiving an unsolicited job opportunity via a “cold call” (Lee et al., 2008). This group had the highest job satisfaction and the highest relative pay level, compared to others who quit to take another job (and much higher than those who quit without another job lined up). In sum, worker perceptions of alternative job opportunities do not predict their turnover behavior at the individual level. The actual existence of an alternative more attractive job is what predicts their turnover. At the aggregate level, this becomes even clearer. Using U.S. Bureau of Labor Statistics data from the 2001-2019 time period, the correlation between national annual quit rate and national annual unemployment rate is quite high (r = .98). 9 Likewise, it is quite possible in the aggregate that in firms with higher levels of worker FSHC, there is less mobility, consistent with Becker’s model. 10

Assumption That Worker Immobility Is Good for Firms Generally

There are two issues with the centrally important requirement of the immobility of FSHC. One relates to the assumption about value creation and value capture, which we touched on above. We argued that Becker’s definition of FSHC did not appear to give firms a systematic advantage over workers in value capture. Thus, if value capture in the form of postcontractual opportunism by the firm (“holdup”) is a major rationale for striving for worker immobility, some rethinking may be necessary. There could also be value capture by the firm (but also by workers) if value is created through FSHC-related complementarity. Without value capture of some sort from FSHC, immobility is unimportant. This reinforces the need for more empirical attention (to go along with the large amount of discussion) to complementarity and FSHC.

Another concern is lack of attention to potential benefits of worker mobility for firms. Although potential benefits of low mobility under FSHC are understood, it is not clear (again, a shortfall of data) that shared investment in FSHC is so pervasive as to provide a rationale for a goal of low worker mobility in general. Absent perfect hiring decisions (unlikely), suboptimal matches will be discovered posthire and turnover best takes place before significant firm and worker investments in FSHC are made. Even if low worker mobility is an opportunity for value capture by a firm, it matters how this is achieved, at least from a social welfare perspective. Does the value capture come at the expense of value creation, which, in most models of the labor market, requires worker mobility to achieve efficient matching of workers to jobs/firms? If such models are valid, how is it possible for mobility to be seen as so (uniformly) negative for firms?

The average annual U.S. quit rate was 26% during 2000-2019. This level of mobility might come as a surprise. It may indicate (a) firms are not as focused on immobility as expected, (b) firms’ decisions are less than optimal and they need better advice, (c) firms see positives to some mobility, and/or (d) firms decided, correctly or not, the cost of reducing mobility exceeded the return. One situation where mobility will be less of a problem for firms is where they have developed a dynamic capability (Teece, Pisano, & Shuen, 1997) whereby their routines, processes, and systems are able to produce a workforce that maintains or evolves to have the required attributes (e.g., FSHC defined at the supra-individual level) with or without strong immobility, independent of specific employees. Thus, for example, instead of raising wage rates to reduce turnover (Gerhart & Newman, 2020: Exhibit 7.14 reviews elasticities), a firm may build a capability to efficiently find, train, and integrate workers.

Mobility and social return

Social welfare concerns about a lack of mobility are not new. In 1958, Arthur Ross asked, “Do We Have a New Industrial Feudalism?” and said “it is feared that workers have become badly immobilized. . . .” This was largely in reaction to the development of ILMs. Ross argued that “some people should quit their jobs to find more congenial kinds of work, more agreeable supervisors and fellow workers, and better advancement opportunities.” Further, “a serious economic problem” would arise should the workforce “become inflexible and immobile [because in] our dynamic economy, a great deal of movement . . . is required.” Similar ideas were later formalized in economic matching theory (Jovanovic, 1979), which highlights the positive (indeed, essential) role of employee mobility for workers and for social welfare. Only with adequate mobility can the labor market carry out its major function of matching, which works to “allow workers to move to their most productive use” (Lazear & Spletzer, 2012: 575). Turnover plays a major role because workers are seen as acquiring much of their information about match quality only after having actually been in a job for some time (i.e., match is an “experience good”). The limited amount of information available to firms and workers at the point of hire limits the quality of matches at that point. “Workers remain on jobs in which their productivity is revealed to be relatively high and . . . they select themselves out of jobs in which their productivity is evaluated to be low” (Jovanovic, 1979: 974). Jovanovic and Moffitt (1990: 828) estimate that economic output for the U.S. economy would be lower by 6% to 9% if employees “were not able to act on their match information by exercising their option to change jobs.” Likewise, they find matching through worker mobility also raises wages by 8.5% to 13%, consistent with the idea that mobility allows “workers to move to their most productive use.” Davis and Haltiwanger (1999: 2778) point to “low worker mobility rates” in “centrally planned economies . . . [that] choke off the productivity-enhancing role of worker sorting.”

Engbom (2020) raises a concern that, in fact, “reducing workers ability to find a job that fully utilizes their skills [i.e., reducing mobility] . . . discourage[s] workers from accumulating human capital.” In support of this, using panel data on 23 Organisation for Economic Co-operation and Development (OECD) countries, he found that “life-cycle wage growth and on-the-job training are greater in more fluid labor markets” and that “aggregate productivity is 30 percent lower in the least fluid labor market relative [to the most fluid] primarily due to a lower stock of human capital.”

The OECD (2019: 2) notes that barriers to exit, like barriers to entry, “weaken the market discipline of the competitive process, which . . . can lead to less efficient firms staying in the market” and “resources (both financial and HC) become trapped in existing firms instead of being relocated to their most efficient use. This can make it more difficult for efficient firms to expand and can crowd-out the growth of more innovative firms” and “can have an adverse impact on economic growth.” It is not clear why barriers to exit in the labor market, in the form of lower than optimal employee turnover (mobility), would be any less detrimental to aggregate productivity and economic growth. One can thus ask whether immobility is even good for firms, on average, as sometimes implied even beyond the case of investment in FSHC.

The HR literature, while long recognizing the potential for mobility to benefit the firm (e.g., Boudreau & Berger, 1985; Dalton, Krackhardt, & Porter, 1981), has of late primarily focused on how turnover is generally bad for firms (e.g., Bidwell, 2019; Nyberg & Ployhart, 2013; Trevor & Piyanontalee, 2020). 11 A meta-analysis by Park and Shaw (2013) reports a corrected correlation of -.15 between voluntary turnover and organizational performance. Thus, 2.3% of the variance (in a bivariate model without controls) is explained. The confidence interval does not include .00, but the credibility interval does. Of course, “internal” turnover/mobility in the form of promotion (as in an ILM), contrary to external mobility, is usually seen as positive (Bidwell, 2011). It is efficient to the degree higher ability employees are “matched” to higher impact jobs. Although perhaps disruptive to a unit that “loses” a valued employee to promotion in another unit, this loss is recognized as necessary. It also creates an opportunity for another person. Of course, the supply of internal candidates is limited, especially in a growing firm. Growing firms are also (all else equal) more efficient. Thus, if they induce turnover in other, less efficient firms to fill vacancies, it may be good for the growing firm, its hires, and social return.

Other research indicates that although employment is helpful to future entrepreneurs getting started, eventually turnover is necessary for them to move to their most productive use as an entrepreneur (Raffiee & Feng, 2014). Some turnover may be useful, as in when former employees maintain ties and these translate into new opportunities for the former employer (e.g., Carnahan & Somaya, 2013) or when “boomerang” employees leave and return after experiencing that matches elsewhere are not as good as at their original firm (Shipp, Furst-Holloway, Harris, & Rosen, 2014).

Thus, although what is efficient at the level of the economy is not necessarily what is efficient for particular firms, it is again difficult to understand how, if a significant share of firms actively seek to reduce employee mobility to a (too?) low of level, which would be expected to reduce social welfare by misallocating workers, which firms, on the whole, could still stand to benefit. This is a potentially important contradiction to be addressed in work that relies on FSHC and/or RBV logic to mostly depict turnover as bad for firms. Closing off exchange of resources (through immobility of workers and their HC in this case) with the environment can protect advantage, but it risks closing off future advantage. Teece et al. (1997) emphasize that it is also necessary to “renew competences to respond to shifts in the business environment.” Erecting barriers to mobility will not likely help in this respect.

As implied earlier, the argument that turnover is bad for employers does not seem to have been grasped by many employers. Kalleberg and Mouw (2018: 289) refer to “the decline of firm ILMs,” and state “employers rely more on the external labor market and so are less likely to provide training and be committed to their employees. Employers increasingly hire workers from outside the organization rather than develop their employees’ human capital internally.” (Some firms go a step further in this external strategy, outsourcing work as in the case of Apple and Foxconn). To the extent that is true, investment in FSHC/employees is likely going down, not up. Indeed, Waddoups (2016) reports that “the percentage of workers . . . in formal employer-sponsored training . . . fell” from 20.6% in 2001 to 14.9% by 2009, a 27.7% decline, what he terms “a significant disinvestment in the nation’s human capital.” To the extent the decline in ILMs is accurate and investment in training has likewise decreased, it would seem to suggest that employers have become less, not more concerned with achieving immobility. In a similar vein, employer use of defined benefit (“pension”) retirement plans has declined dramatically, despite being a major impediment to mobility. They survive primarily (and are open to new employee participants) in the public sector. (Financial risk of these plans also helps explains their decline.)

Value Creation and Value Capture

In strategy broadly, some have wondered whether there is too much emphasis on value capture, not enough on value creation. For example, Priem, Butler, and Li (2013: 472) cite Adner and Kapoor (2010: 309) that strategy research “has tended to assume away the question of how value is created in the first place,” and similarly, Nickerson, Silverman, and Zenger (2007: 211) note that “the vast majority of strategy research has focused on value capture and underemphasized the challenge of crafting organizations and strategies that continuously create value.” Certainly, a major part of the literature on RBV deals with value capture (e.g., Coff, 1997), as do other fields related to management, such as agency theory and industrial relations. Barbash (1984), in the Elements of Industrial Relations, noted that firms and workers “have a common interest in maximizing the total revenue which finances their respective returns, but they take on adversarial postures in debating how the revenue shall be divided as between wages and profits.” (Note that Barbash begins with value creation.)

The question is whether high growth in productivity and standard of living can be obtained if firms (and the ecosystem in which they operate) move too much toward value capture and if that comes at the expense of value creation by alienating other stakeholders. At the level of the firm, as is well-studied in strategy, market imperfections, frictions, barriers to entry, and so forth, whether created by firms, regulation, labor unions, or trade barriers, can reduce competition, which may benefit certain firms, though not generally aggregate economic output. As Mahoney and Pandian (1992: 364) observe, “the generation of above-normal rates of return (i.e., rents) is the focus of analysis for competitive advantage,” and “the existence and maintenance of rents depend upon a lack of competition in either acquiring or developing complementary resources.”

The “depend on lack of competition” is the concerning part. As Kaufman (2015: 530) points out, “in microeconomic [economic] theory, imperfect competition is undesirable because it results in inefficient use of resources and lower output.” As Kaufman (2015: 529) also points out, the RBV (Barney et al., 2012: 137) argues its focus on creating efficiency at the firm level by emphasizing how firms can create greater value from their internal resources. Further, RBV argues that if all firms do this, the result will be more economy-wide output. Of course, the net result depends on the degree to which RBV ultimately influences firms to focus on value creation and value capture in ways that achieve efficiency rather than in ways paved by erecting barriers to competition, in the product market, or in the labor market. Kaufman (2015: 532) further observes that “in effect, the Porter strategy hunts out and creates monopoly power in product markets to promote firm performance, and the Barney strategy hunts out and creates . . . monopsony power in the factor market. . . . Perhaps RBV has particular traction at this point since it may be easier for firms to create imperfect competition in labour markets (e.g. by investing in ILMs) than product markets, partly because the former are more local-based.”

As noted, ILMs are not necessarily anticompetitive and can be an efficient solution where FSHC is valuable, and transaction costs (including opportunism) must be controlled to encourage shared investment by firms and workers. However, also as noted, the emphasis in the strategic HC literature sometimes seems to be disproportionally focused on the value capture opportunity it sees (whether correct or not) arising from worker immobility and less on how FSHC might give rise to value creation. Other approaches to reducing mobility can be anticompetitive, with a focus on value capture at the expense of the worker, and thus may also reduce value creation. Some, such as noncompete contracts, have received some research attention (e.g., Starr, Ganco, & Campbell, 2018). 12

We know from the study of industrial relations that firms can collaborate with workers to reduce competition to their mutual benefit but perhaps to the detriment of the consumer and aggregate efficiency/output. At least that is one narrative for what happened to companies in legacy industries when deregulation, international competition, and other barriers to competition were removed and bankruptcies followed in industries like airlines and automobiles in the United States along with major declines in some. Capturing rents arising from constructing such barriers to competition can continue for many years. However, it is not sustainable in the face of stronger market forces and competition and ultimately fails on the (social) value creation criterion.

Conclusion

Clearly, the RBV has been a major influence on strategic HR and HC research and likewise in providing a framework to organize and understand even much work that does not explicitly use RBV as a conceptual map. At the same time, we concur with others that more direct empirical tests of specific propositions flowing from RBV would be useful and would provide a better balance and more productive interplay in the literature between theory and data. We have identified areas for research attention throughout our paper. As noted earlier, these are summarized in Table 1. Finally, although our focus has been on research, we wish to note, even if briefly, the major influence of RBV on teaching in strategic HR and HC also (e.g., Barney & Wright, 1998) and the invaluable role of RBV in enriching the analysis of companies, including classic cases such as Lincoln Electric, the SAS Institute, and Southwest.