Abstract

We examine how passive institutional ownership affects the informational efficiency of stock prices. Because passive institutional investors prefer greater transparency, their presence encourages managers to enhance firm disclosure (Boone & White, 2015; Schoenfeld, 2017). Increased disclosure improves the information environment and reduces information uncertainty, leading to lower post-earnings announcement drift (PEAD) and greater price efficiency (Hung et al., 2015; Zhang, 2006). Accordingly, we predict that higher passive institutional ownership strengthens the contemporaneous market response to earnings announcements while mitigating PEAD. Using firm additions to the S&P 500 index as an exogenous shock, we document that increases in passive institutional ownership lead to greater firm disclosure. Consistent with our prediction, we find higher earnings response coefficients (ERC) and weaker PEAD among firms with greater passive institutional ownership. Decomposing earnings into firm-specific and systematic components, we further show that the higher ERC and weaker PEAD arise from the timely incorporation of both components into prices. Our findings contribute to the ongoing debate on whether the rise of passive investing enhances or impairs price efficiency.

Keywords

Introduction

This paper examines the impact of passive institutional investors on the informational efficiency of stock prices. The dramatic increases in ownership of U.S. firms by passively managed institutions raise an important question: How does passive institutional ownership affect price efficiency? 1 An important concern is that the rise of passive investing may distort stock prices and risk-return tradeoffs (Wurgler, 2010), although some claim that passive investing has not impaired market efficiency. 2 A growing body of literature documents the causal effects of passive institutional investors on firm disclosure and corporate governance (Appel et al., 2016; Boone & White, 2015; Schoenfeld, 2017). Building on this literature, we examine whether passive institutional investors affect firm disclosure and, more importantly, how passive ownership affects market reactions around earnings announcements.

Passive institutions prefer more firm information to reduce monitoring and trading costs. 3 However, the diverse holdings of passive institutional investors make it costly for them to collect firm-specific private information (Boone & White, 2015). Thus, passive investors demand more public disclosure. Managers are likely compelled to respond to passive funds’ preferences by providing more information because these institutions can exert considerable influence through various channels, such as proxy voting and engagement with management. Recent findings that passive institutions are active voters lend credibility to their influence on management decisions. 4 Increased firm disclosure reduces information asymmetry among investors, thereby fostering a more transparent information environment (Diamond & Verrecchia, 1991).

Enhanced firm disclosure and a richer information environment lower transaction costs and facilitate the more rapid incorporation of earnings information into stock prices. Firm disclosures also complement earnings announcements by promptly resolving uncertainty at the time of the earnings release (Beyer et al., 2010). When the information environment is strong, stock prices adjust efficiently to earnings news—typically exhibiting a large immediate price response, captured by a larger earnings response coefficient (ERC) and diminished post-earnings announcement drift (PEAD) (Blankespoor et al., 2020). Accordingly, we predict that firms with greater passive institutional ownership will exhibit stronger contemporaneous market reactions to earnings announcements and weaker PEAD. 5

We use firm additions to the S&P 500 index as an exogenous shock to passive institutional ownership. Our sample includes firm observations within the [−8 quarters, 8 quarters] window around each addition event. This setting enables us to assess the impact of passive institutional ownership because index-tracking investors purchase stocks added to the S&P 500 to replicate index performance, generating substantial variation in passive ownership. The 2-year window allows sufficient time for passive investors to establish relationships with managers and express their preferences for more public information, and also gives firms time to adjust their disclosure.

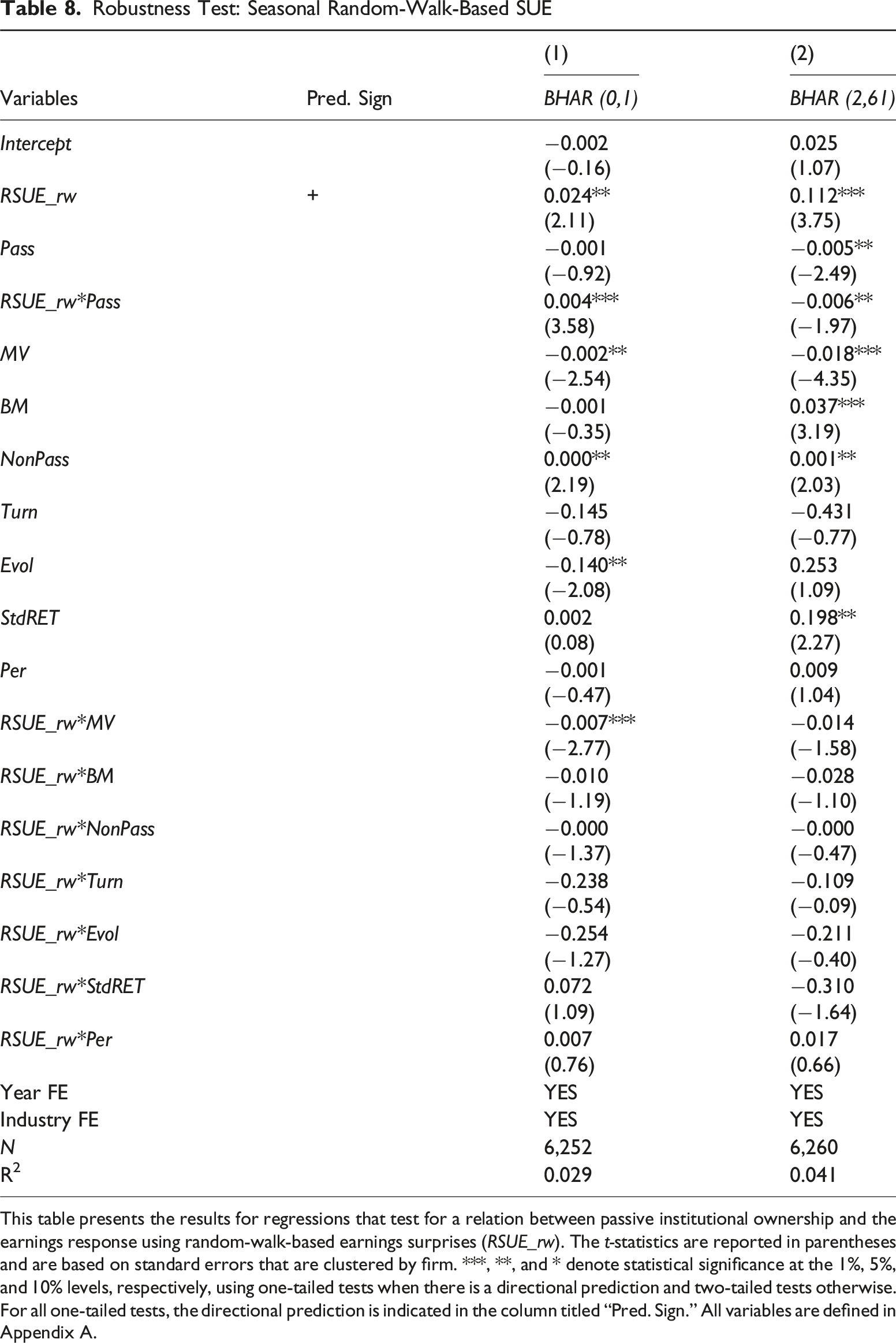

We find strong evidence to support our predictions. After documenting that higher passive institutional ownership is associated with greater disclosure, we find significantly higher ERC and lower PEAD in firms with higher passive institutional ownership. The magnitudes are economically meaningful: moving passive institutional ownership from the 25th percentile (1.491%) to the 75th percentile (4.870%) increases the ERC by 34% and reduces PEAD by 29%. These results suggest that passive investors play an important role in facilitating the production of public information and the incorporation of earnings information into prices. Our results are robust to using a matched sample, a seasonal random-walk model to compute earnings surprises, using quasi-indexers to define passive institutions (Bushee, 2001), and an estimation window without the addition quarter.

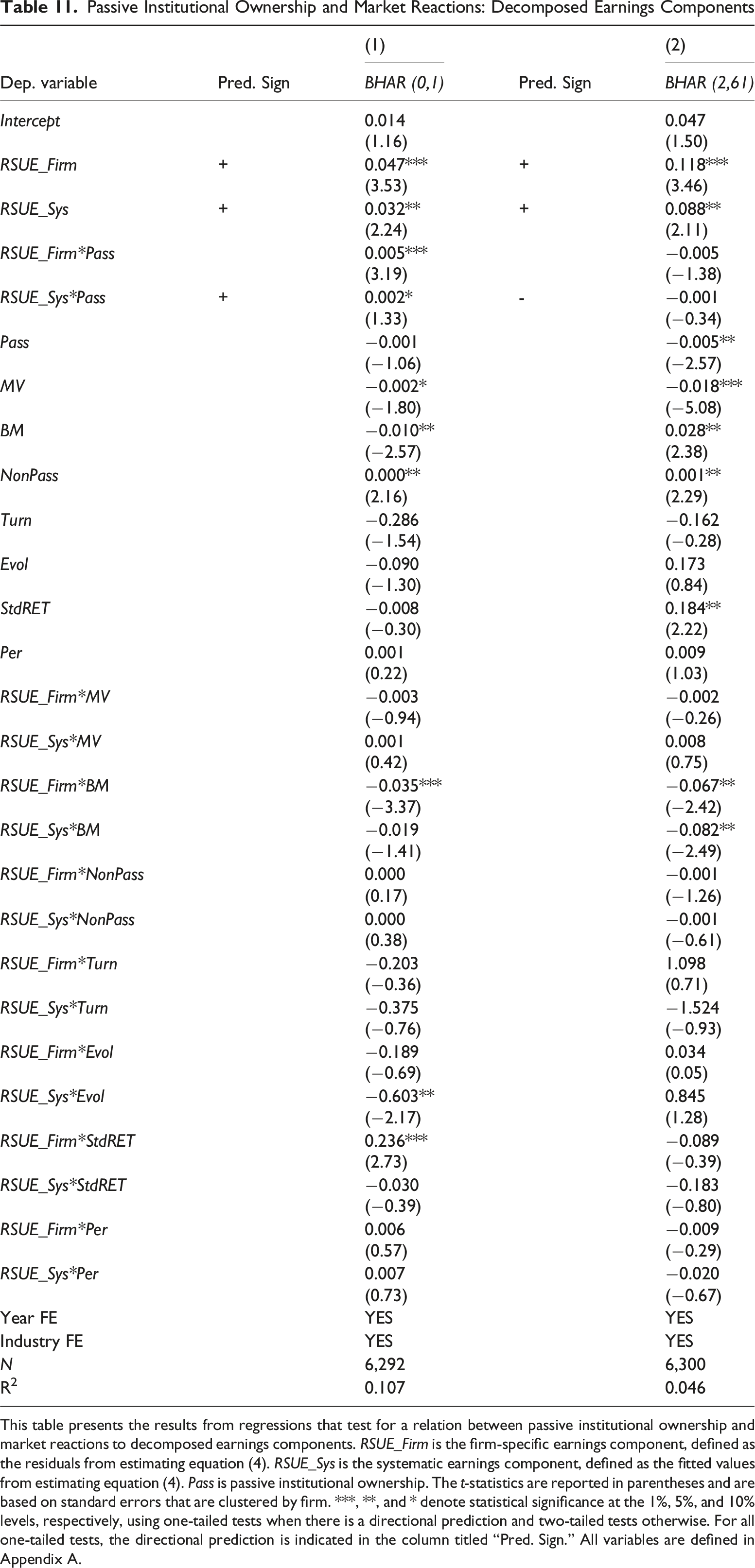

Passive funds facilitate trading across large baskets of securities, potentially enabling investors with systematic information to trade more efficiently and thereby increasing the speed with which stock prices incorporate systematic earnings information (Glosten et al., 2021). Therefore, we examine whether the documented stronger earnings responses are driven by the timely incorporation of firm-specific or systematic earnings information, or both. On the one hand, higher earnings responses may reflect the more rapid incorporation of firm-specific information, consistent with our finding that passive ownership enhances disclosure. On the other hand, stronger earnings responses could result from the timely incorporation of systematic information. Decomposing quarterly earnings into firm-specific and systematic earnings components, we find that market reactions to both components are stronger when passive institutional ownership is higher.

This paper makes several contributions to the literature. First, it contributes to a deeper understanding of the impact of passive institutional investors on market efficiency by examining an important market segment—the S&P 500. Coles et al. (2022), using the Russell index reconstitution as the setting, find no change in PEAD associated with index investing. However, their sample consists of firms that switch between the Russell 1,000 and 2,000 indices, which are substantially smaller in market capitalization than those in the S&P 500. 6 Because investors may pay limited attention to smaller firms moving in and out of the Russell 2,000, the effect of passive ownership on PEAD may be muted in that setting. 7 In contrast, additions to the S&P 500 index generate substantial variation in passive institutional ownership because index-tracking investors promptly purchase the added stocks to replicate index performance (Green & Jame, 2011; Ye, 2012). This setting, therefore, allows us to better identify the impact of passive institutional ownership on price efficiency.

Second, our study deepens the understanding of how passive institutional ownership affects market efficiency by introducing a new mechanism—the disclosure channel. Prior studies primarily examine how the trading behavior of passive investors affects pricing efficiency. For example, Glosten et al. (2021) argue that ETFs facilitate trading in baskets of securities, allowing prices to incorporate systematic information but not firm-specific information. Consistent with this view, they find a negative association between ETF activity and PEAD. Similarly, Israeli et al. (2017) show that increases in ETF ownership are associated with higher stock return synchronicity, indicating that prices reflect less firm-specific information. 8 They attribute this effect to higher transaction costs in underlying securities because uninformed traders migrate to ETFs, which discourages firm-specific information acquisition. In contrast, we focus on firm additions to the S&P 500 index—an event that reduces endogeneity concerns—and on large firms with complex information environments, where firm disclosure plays a critical role. We argue that higher passive ownership can enhance price efficiency by promoting more corporate disclosure, thereby facilitating the incorporation of public information into prices. Thus, our study broadens the literature by identifying and empirically validating the disclosure mechanism through which passive institutional investors improve price efficiency. Consistent with this mechanism, we find that the stronger earnings responses are driven by the timely incorporation of both firm-specific and systematic earnings components into prices.

Third, our study provides complementary evidence to Sammon (2025) on how passive ownership affects the incorporation of earnings information into prices. Sammon (2025) shows that passive ownership reduces preannouncement price informativeness, whereas we document that higher passive ownership is associated with stronger announcement-period price responses and weaker PEAD. Together, these findings suggest that passive ownership improves information incorporation around the earnings announcement date, with less preannouncement information leakage, more complete incorporation at the announcement, and reduced PEAD. This pattern is consistent with our disclosure-based mechanism: enhanced disclosure and transparency can reduce preannouncement information asymmetry by limiting the advantage of informed traders who might otherwise trade on leaked or private information while facilitating more efficient incorporation of earnings upon public release. In this way, our disclosure mechanism helps reconcile seemingly disparate findings in the literature and explains the distinct timing patterns documented across the two studies. The combined evidence from our study and Sammon (2025) suggests that passive ownership influences not only the efficiency of price discovery but also the timing and manner of the incorporation of earnings information.

Finally, our study contributes to the literature examining the relation between institutional investors and PEAD. Prior research (Bartov et al., 2000; Campbell et al., 2009; Ke & Ramalingegowda, 2005) documents that firms with more institutional investors or transient institutional investors have lower PEAD, presumably because these investors fully understand the time-series properties of earnings and their implications for stock prices. Glosten et al. (2021) find that ETF activity is associated with an attenuation of PEAD, whereas Coles et al. (2022) report no significant effect of index investing on PEAD. Building on recent evidence that passive institutional investors are engaged owners who demand more public disclosure, we find that higher passive institutional ownership is associated with weaker PEAD by using firms added to the S&P 500 index as an exogenous shock.

Prior Literature and Hypothesis Development

Literature Review

A large body of theoretical and empirical literature explores the relation between passive investors and market efficiency (Bond & Garcia, 2022; Cong & Xu, 2016; Glosten et al., 2021; Israeli et al., 2017; Liu & Wang, 2018; Subrahmanyam, 1991). However, the main takeaways are inconclusive. One strand of the literature suggests that the relation is ambiguous. In Subrahmanyam’s (1991) model, whether passive institutional investors increase or decrease market efficiency depends on the parameters (e.g., stock weights and the number of stocks in a portfolio). In addition, Liu and Wang (2018, p. 28) show that the effect of indexing investment on price discovery is determined by “the causes of the rise of indexing and the cost structure of information acquisition,” and Coles et al. (2022) find that index investing negatively affects information production but does not significantly affect price informativeness. Another strand of the literature supports the view that passive institutional investors reduce price efficiency. Israeli et al. (2017) report that increases in ETF ownership are associated with increases in trading costs, increased stock return synchronicity, and decreases in future earnings response. Bond and Garcia’s (2022) model shows that increases in indexing lead to decreases in individual stock trading and aggregate price efficiency. Similarly, Baruch and Zhang’s (2022) model shows that price efficiency decreases when indexers increase. Sammon (2025) shows that passive ownership decreases the amount of information incorporated into prices ahead of earnings announcements. The other research class claims that passive investment facilitates the incorporation of earnings information into prices. Cong and Xu (2016) argue that the introduction of composite securities results in higher systematic factor information in prices. Glosten et al. (2021) find that ETF trading increases informational efficiency for small stocks and stocks with imperfectly competitive equity markets by promoting the incorporation of systematic information. Lee’s (2020) model suggests that price efficiency improves as more investors invest in index funds. Ahn and Patatoukas (2022) show that index investing is positively related to the speed of price adjustment to news for microcap firms.

Our paper is also related to research on the relation between institutional investors and firm disclosure. Bushee and Noe (2000) find that higher disclosure rankings are associated with increased ownership of transient institutions and quasi-indexers. Ajinkya et al. (2005) show that firms with more outside directors and higher institutional ownership are more likely to issue earnings forecasts. These studies suggest that the link between institutional investors and disclosure is likely to be endogenous. To overcome endogeneity concerns, Boone and White (2015) use the Russell index reconstitution setting to test for an impact of institutional ownership on the information environment. They find that firms with higher institutional ownership have greater management disclosure, more analysts following, and higher liquidity. Schoenfeld (2017) finds that higher index fund ownership is associated with more voluntary disclosure and higher stock liquidity.

Finally, our paper is related to research on PEAD. Prior studies find that PEAD can be partially explained by: (1) a delayed response to information because investors fail to understand the implications of current earnings for future earnings (Bernard & Thomas, 1989, 1990), (2) investors’ overconfidence and limited attention (Hirshleifer et al., 2011; Liang, 2003), (3) transaction costs and market friction (Bhushan, 1994; Mendenhall, 2004; Ng et al., 2008), and (4) misspecification of the capital asset pricing model used to calculate abnormal returns (Ball et al., 1993; Foster et al., 1984). Our paper is related to research testing the relation between investor types and PEAD. Prior literature provides mixed evidence on whether individual investors cause PEAD (Battalio & Mendenhall, 2005; Hirshleifer et al., 2008). Hirshleifer et al. (2008) find no evidence that individual investors, or any subset in their sample, trade in a way that would cause PEAD. In contrast, Ayers et al. (2011) find that small traders contribute to seasonal random-walk-based PEAD, whereas large traders contribute to analyst-based PEAD. Some studies investigate whether institutional investors can reduce PEAD. Bartov et al. (2000) find that higher institutional ownership is associated with lower PEAD, suggesting that institutional investors trade on and quickly correct mispricing. Ke and Ramalingegowda (2005) find that transient investors exploit PEAD, and their trading accelerates the incorporation of earnings into prices. Recent studies also provide mixed evidence on how passive investors affect PEAD. Glosten et al. (2021) find that ETF activity is associated with an attenuation of PEAD, whereas by using potential switchers between the Russell 1,000 and 2,000 indices, Coles et al. (2022) find that index investing has no impact on PEAD.

Hypothesis Development

Passive institutional investors are characterized by diversified portfolios and limited incentives to engage in firm-specific information production. To reduce monitoring and transaction costs, these passive investors prefer more firm information (Chen et al., 2004). Because collecting private information for a large number of portfolio firms is costly, passive funds demand more public information (Boone & White, 2015). Managers are likely to respond to such demands because passive investors can exert considerable influence through their sizable ownership stakes and active participation in corporate governance, including proxy voting and direct engagement with management. For example, Matvos and Ostrovsky (2010) report that the Vanguard 500 index fund withheld its support for management-proposed directors in 17.2% of cases in 2003 and 2004, and BlackRock (2020) explicitly states its commitment to engage with firms when it deems their disclosure inadequate. Moreover, compared to active institutional investors, passive institutions tend to have longer investment horizons (Bushee & Noe, 2000), giving managers further incentives to provide additional disclosure to attract and retain their support.

Increased disclosure mitigates information asymmetry among investors and improves the overall information environment (Diamond & Verrecchia, 1991), which can enhance price efficiency by facilitating the more rapid incorporation of earnings information into stock prices. PEAD is a phenomenon in which stock prices underreact to earnings news so that prices are too low for positive earnings surprises and too high for negative earnings surprises. Therefore, positive (negative) earnings surprises are associated with higher (lower) subsequent returns (Hirshleifer et al., 2011). Prior research suggests that transaction costs and limited informed trading contribute to the persistence of PEAD (Ng et al., 2008). Enhanced disclosure can mitigate these frictions by lowering transaction costs, reducing uncertainty, and promoting informed trading (Boone & White, 2015). Furthermore, firm disclosure complements earnings announcements by providing context and resolving uncertainty about future earnings (Beyer et al., 2010). When managers disclose more decision-relevant information about firm performance and growth opportunities, investors can revise their beliefs more quickly and incorporate earnings news into prices more efficiently.

Taken together, these arguments suggest a sequential relation: higher passive institutional ownership leads to increased disclosure, and greater disclosure improves the firm’s information environment, thereby reducing transaction costs and facilitating informed trading. These effects collectively accelerate the incorporation of earnings information into stock prices. Accordingly, we propose our first hypothesis, stated in the alternative:

Higher passive institutional ownership is associated with higher ERC and lower PEAD.

However, this hypothesis is not without tension because increased disclosure may crowd out private information acquisition or create opposing effects on efficiency. For example, Diamond (1985) shows that public disclosure can reduce private information acquisition when public and private information are substitutes rather than complements. Gao and Liang (2013) show that although disclosure can improve trading efficiency by mitigating adverse selection, it may also reduce the informativeness of prices for decision-making by discouraging traders’ information production. Consequently, the net effect of passive institutional ownership on the informational efficiency of stock prices remains an empirical question.

If higher passive ownership is associated with stronger earnings responses, the effect could be attributable to the timely incorporation of firm-specific earnings information, systematic earnings information, or both. On the one hand, the higher earnings responses may reflect a timely incorporation of firm-specific information. To reduce monitoring and transaction costs, passive institutions are motivated to influence firms to provide more firm disclosure (Appel et al., 2016; Boone & White, 2015). Enhanced disclosure improves the overall information environment by reducing information asymmetry (Diamond & Verrecchia, 1991). A richer information environment benefits all investors, not just passive investors, by facilitating informed trading and accelerating the incorporation of firm-specific information into prices. Thus, if higher passive ownership leads to greater disclosure, stock prices should react more promptly to firm-specific earnings news, yielding stronger contemporaneous market reactions and weaker PEAD.

On the other hand, stronger earnings responses may also arise from the timely incorporation of systematic earnings information. Passive funds trade baskets of securities to track broad market indices. This trading structure links the prices of constituent stocks to market-wide information that affects many firms simultaneously. Investors who respond to that market-wide news can trade the passively managed index fund rather than trading individual stocks. Because such trading moves all constituent stocks together, systematic information is transmitted more rapidly into individual stock prices. In this way, passive funds act as a conduit through which market-wide information quickly flows into individual stock prices. Consistent with this mechanism, Glosten et al. (2021) find that ETF activity facilitates the incorporation of systematic earnings information into prices by enabling investors to efficiently trade diversified portfolios. Accordingly, we state the following two alternative hypotheses:

Higher passive institutional ownership is associated with stronger immediate market reactions to a firm-specific earnings component and lower PEAD.

Higher passive institutional ownership is associated with stronger immediate market reactions to a systematic earnings component and lower PEAD.

Similar to H1, greater firm disclosure may reduce private information acquisition or generate offsetting effects on market efficiency. Consequently, the net effect of passive institutional ownership on the informational efficiency of the firm-specific earnings component remains an empirical question.

Research Design

Using S&P 500 addition events as shocks to passive institutional holdings, we test the effect of passive institutional ownership on ERC and PEAD. Because the trading strategy of passive institutions is to replicate a particular index, there are small variations in passive institutional ownership in underlying stocks over a short period. However, the S&P 500 addition events generate substantial variations in passive institutional ownership because passive investors that benchmark against the S&P 500 index will quickly purchase added stocks to replicate the performance of the index (Green & Jame, 2011; Ye, 2012), allowing us to capture the impact of passive institutional ownership. We define the fiscal quarter when the stock is added to the S&P 500 index as event quarter 0. Our baseline sample covers the [−8 quarters, 8 quarters] window around each addition event.

To identify passive institutional investors, we use a method that closely follows Busse and Tong (2012) and Appel et al. (2016). We focus on domestic equity funds because these funds would be most affected by the index addition events. Specifically, we obtain fund names from the CRSP Mutual Fund database. We classify funds identified by CRSP as index funds or ETFs as passively managed institutions. A fund is classified as passively managed if its name includes a string that indicates it as an index fund or an ETF. 9 Thus, passive institutional investors in our sample include those identified by CRSP and those identified via a keyword search. Finally, we obtain passive institutional ownership data by merging the CRSP Mutual Fund database with the Thomson Reuters S12 database via the MFLINKS table. Non-passive equity mutual fund ownership is calculated as the total equity mutual fund holdings minus passive equity mutual fund holdings, scaled by the total number of shares outstanding.

Passive Institutional Ownership and Firm Disclosure

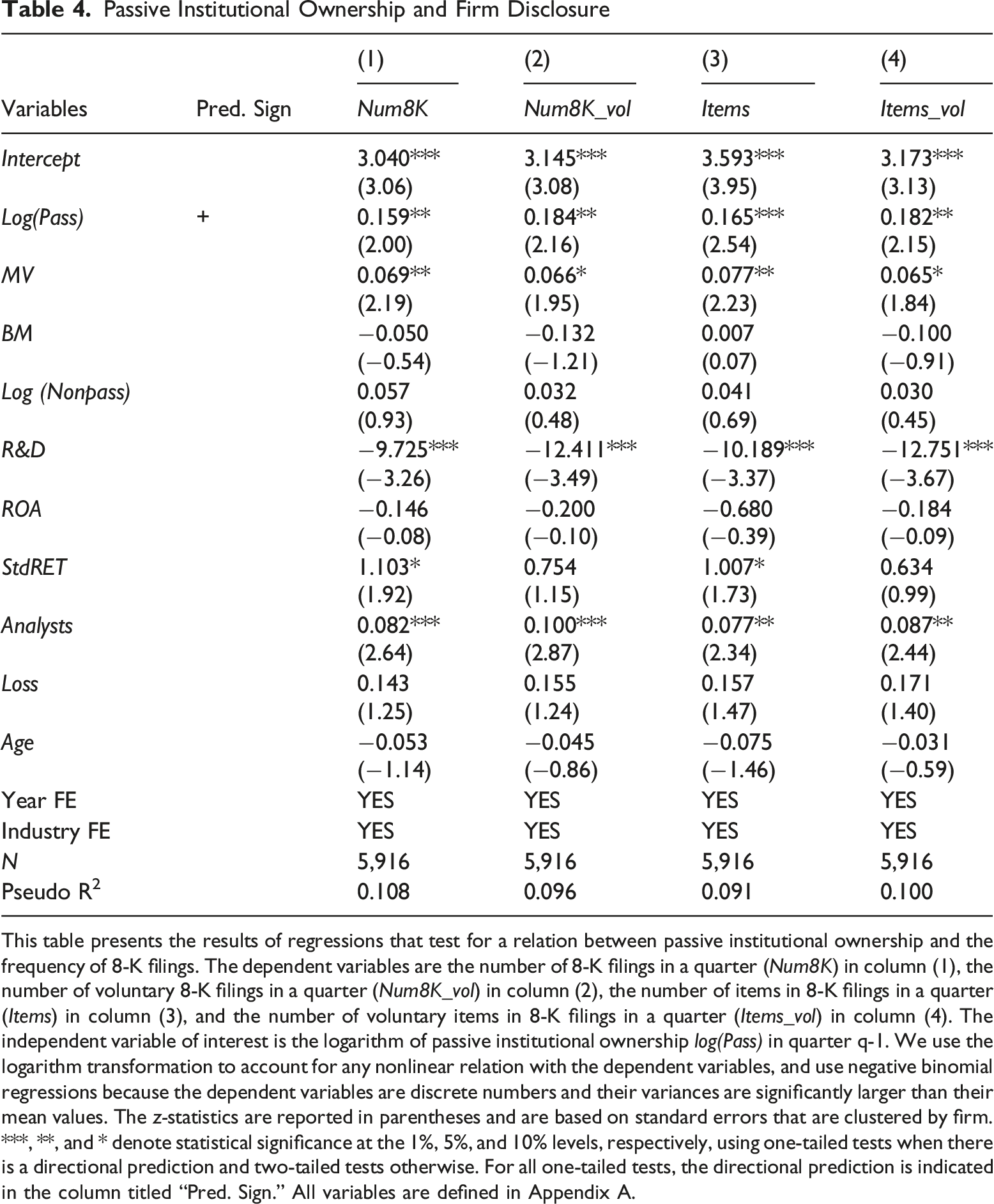

We first test whether passive institutional ownership affects firm disclosure. Following prior literature, we employ four firm disclosure measures by counting the number of 8-K filings (see Bao et al., 2019; Bourveau et al., 2018; Guay et al., 2016), and we obtain 8-K filings from directEDGAR. These measures are the number of 8-Ks (Num8K), the number of items (Items) in 8-K filings, the number of voluntary 8-K disclosures (Num8K_vol), and the number of voluntary items reported in 8-Ks (Items_vol).

10

Specifically, we estimate the following regression:

Because the number of 8-K filings or items included in 8-K filings are discrete variables and the variance of each variable is significantly larger than its mean value, we employ negative binomial regressions to estimate the effect. We take the logarithm of passive institutional ownership and non-passive institutional ownership to account for their nonlinear relation with the dependent variable. Following Rogers and Van Buskirk (2013) and Schoenfeld (2017), we include various controls. See Appendix A for detailed definitions. Firms without any 8-K filings in the pre- or post-addition period are excluded.

Passive Institutional Ownership and Earnings Responses

Next, we examine the impact of passive institutional ownership on earnings responses. The main regression models are as follows:

BHAR(0,1) and BHAR(2,61) are cumulative abnormal returns over the 2-day announcement window and 60-day window starting from 2 days after the earnings announcement, respectively. Abnormal returns are computed as the difference between a stock’s daily raw return and the return of a size-BM portfolio to which the stock belongs. The standardized unexpected earnings (SUE) is calculated as the difference between the actual earnings per share (EPS) and the median analyst forecast in quarter q, scaled by price per share at the end of quarter q. We keep forecasts issued within 90 days before the earnings announcement and the latest forecast for each analyst. RSUE is defined as follows: we standardize SUE by converting it to deciles, scaling it to a range between 0 and 1, and then subtracting 0.5 (Livnat & Mendenhall, 2006). We require that observations have at least 2 days of abnormal returns for the ERC analysis and 50 days for the PEAD analysis, respectively.

We also control for other factors that can explain market reactions following Hirshleifer et al. (2009). We include as controls (see Appendix A for detailed definitions): firm size (MV), book-to-market ratio (BM), non-passive mutual fund ownership (Nonpass), share turnover (Turn), earnings volatility (Evol), defined as the standard deviation of the quarterly earnings during the past 4 years, return volatility (StdRET), and earnings persistence (Per), measured as the first-order autocorrelation coefficient of quarterly earnings estimated over the past 4 years. We also include non-passive institutional ownership as a regressor to ensure that our results are not driven by the impact of non-passive institutional investors. We control for year and industry fixed effects. Based on H1, we expect α3 > 0 in equation (2) and β3 < 0 in equation (3).

Empirical Results

Sample Selection and Descriptive Statistics

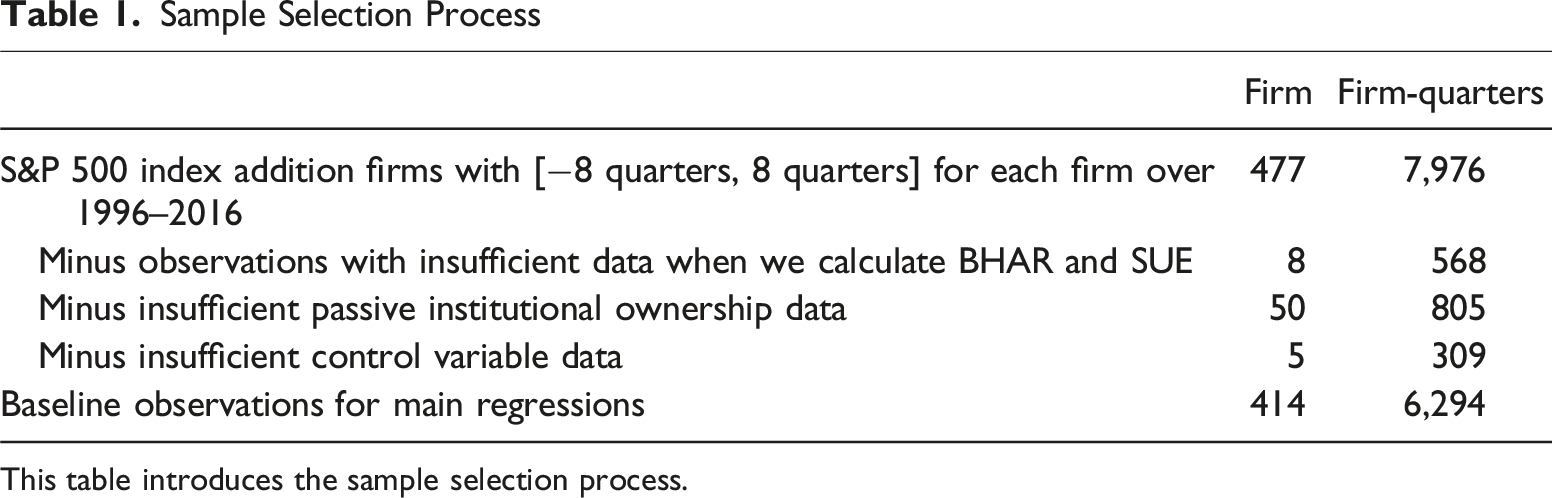

Our sample starts from 477 stocks added to the S&P 500 index from 1996 through 2016. It consists of a [−8 quarters, 8 quarters] window around each addition event, from 1994 through 2018. Our sample begins in 1996 because EDGAR filing data became available to the public in 1996 (Schoenfeld, 2017). Following Livnat and Mendenhall (2006), we require that the price per share at the end of the quarter be greater than $1 and that the market value of equity at the end of the quarter be greater than $5 million. We also require that each observation have sufficient data in I/B/E/S to calculate earnings surprises and in CRSP to measure cumulative abnormal returns. We collect mutual fund ownership from the Thomson Reuters Mutual Fund Holdings (S12) database. We obtain the earnings announcement date from Compustat and require that the absolute difference between the earnings announcement date in Compustat and that in I/B/E/S be less than 2 days. Finally, we winsorize all continuous variables at the 1st and 99th percentiles.

Sample Selection Process

This table introduces the sample selection process.

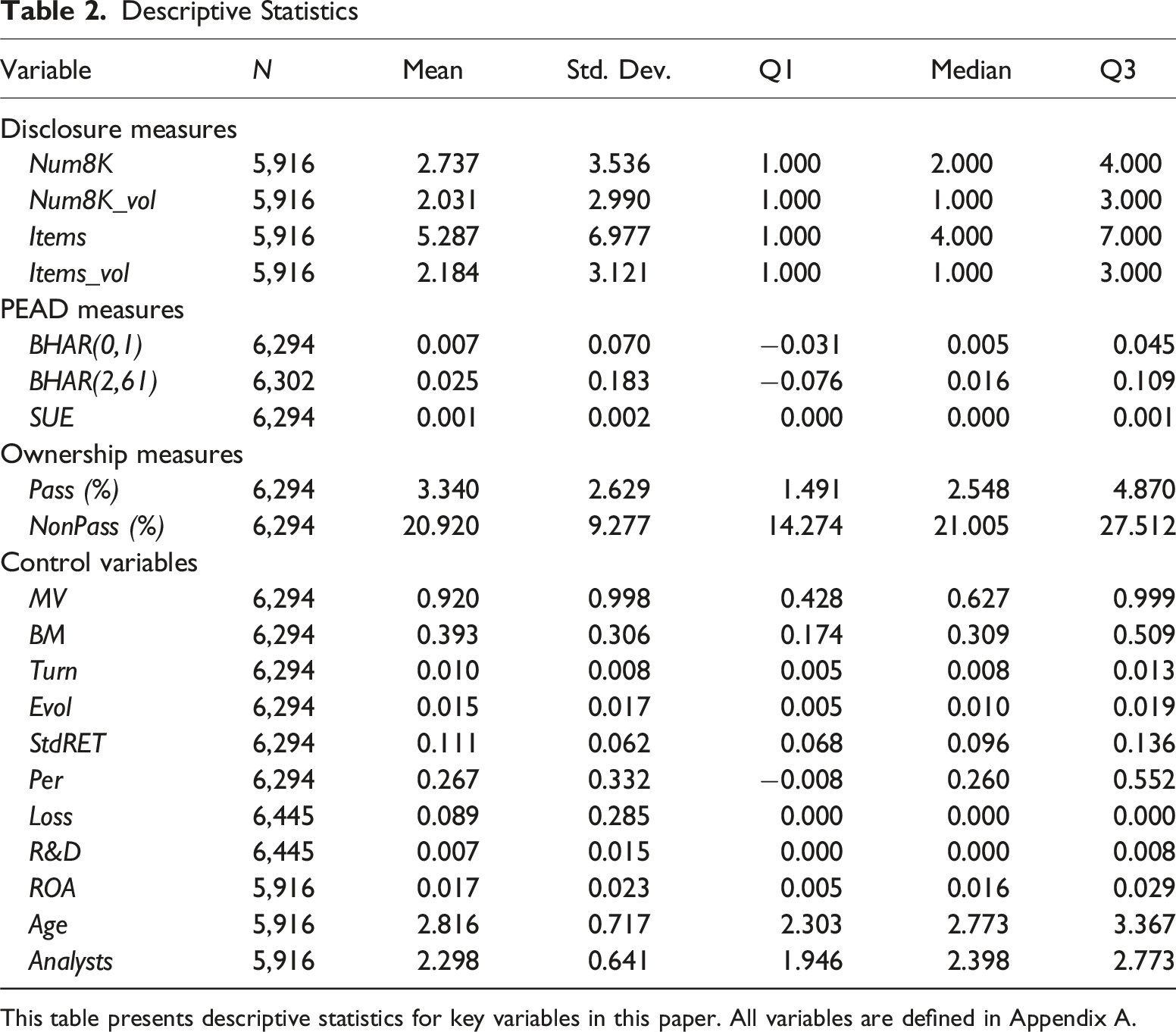

Descriptive Statistics

This table presents descriptive statistics for key variables in this paper. All variables are defined in Appendix A.

The mean (median) of passive mutual fund ownership is 3.340% (2.548%), which is comparable to Appel et al. (2016), who report that the mean (median) is 3.0% (2.6%). Related studies on passive investors have also used Bushee’s (2001) classification of quasi-indexers, which is based on Thomson Reuters 13F data aggregated at the fund family/institution level. Using the characteristics of a whole fund family, Bushee’s (2001) classification might add noise to the measure (Schmidt & Fahlenbrach, 2017). The ownership by quasi-indexers calculated in these studies is much higher than that in our study. Two reasons might explain the difference. First, we only focus on domestic equity mutual funds without including other institutional investors, such as banks, pension funds, and insurance companies. Second, we may miss some passively managed funds because of the keyword search method. Nevertheless, we believe that our method provides a conservative estimate of passive ownership. In the robustness test, when we use quasi-indexer classification to define passive institutional investors, our inferences are not affected.

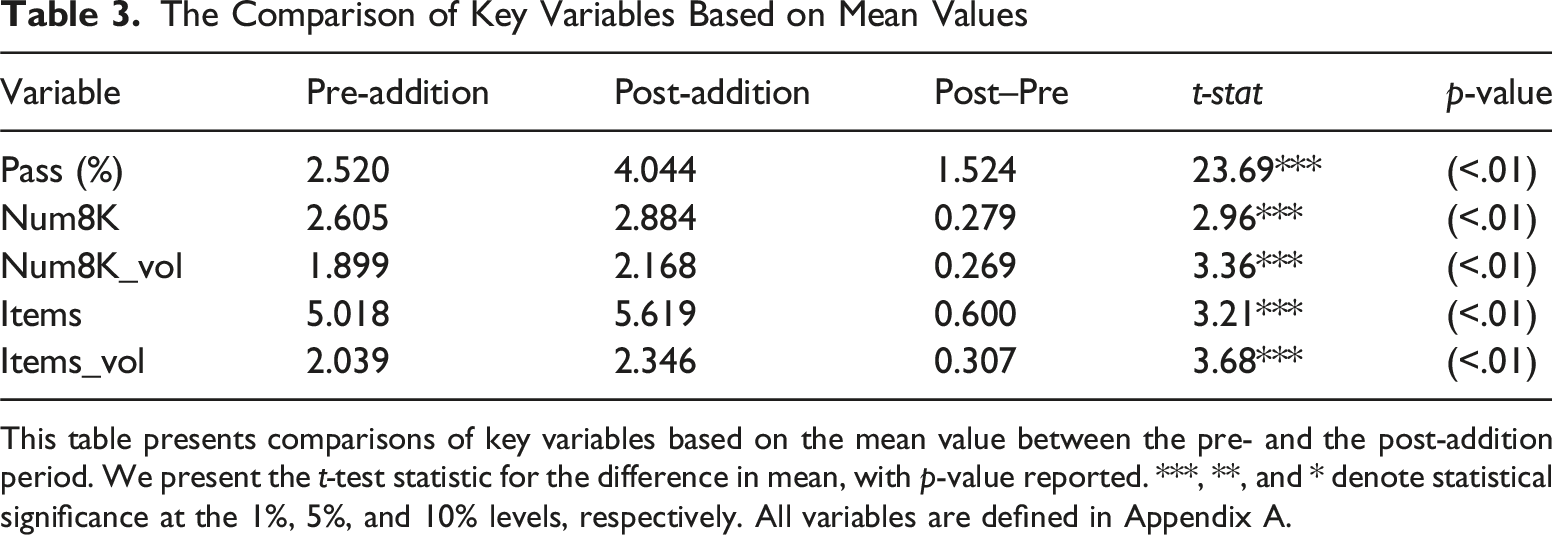

The Comparison of Key Variables Based on Mean Values

This table presents comparisons of key variables based on the mean value between the pre- and the post-addition period. We present the t-test statistic for the difference in mean, with p-value reported. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively. All variables are defined in Appendix A.

Regression Analyses

Passive Institutional Ownership and Firm Disclosure

Passive Institutional Ownership and Firm Disclosure

This table presents the results of regressions that test for a relation between passive institutional ownership and the frequency of 8-K filings. The dependent variables are the number of 8-K filings in a quarter (Num8K) in column (1), the number of voluntary 8-K filings in a quarter (Num8K_vol) in column (2), the number of items in 8-K filings in a quarter (Items) in column (3), and the number of voluntary items in 8-K filings in a quarter (Items_vol) in column (4). The independent variable of interest is the logarithm of passive institutional ownership log(Pass) in quarter q-1. We use the logarithm transformation to account for any nonlinear relation with the dependent variables, and use negative binomial regressions because the dependent variables are discrete numbers and their variances are significantly larger than their mean values. The z-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

For control variables, we find that MV is positively associated with the frequency of 8-K filings, consistent with large firms issuing more firm disclosures. In addition, the result shows that firms with higher stock volatility tend to issue more firm disclosures, suggesting that they disclose more information to resolve uncertainty regarding firm performance. We also document a positive relation between analyst following and firm disclosure.

Passive Institutional Ownership, ERC, and PEAD

Passive Institutional Ownership and ERC

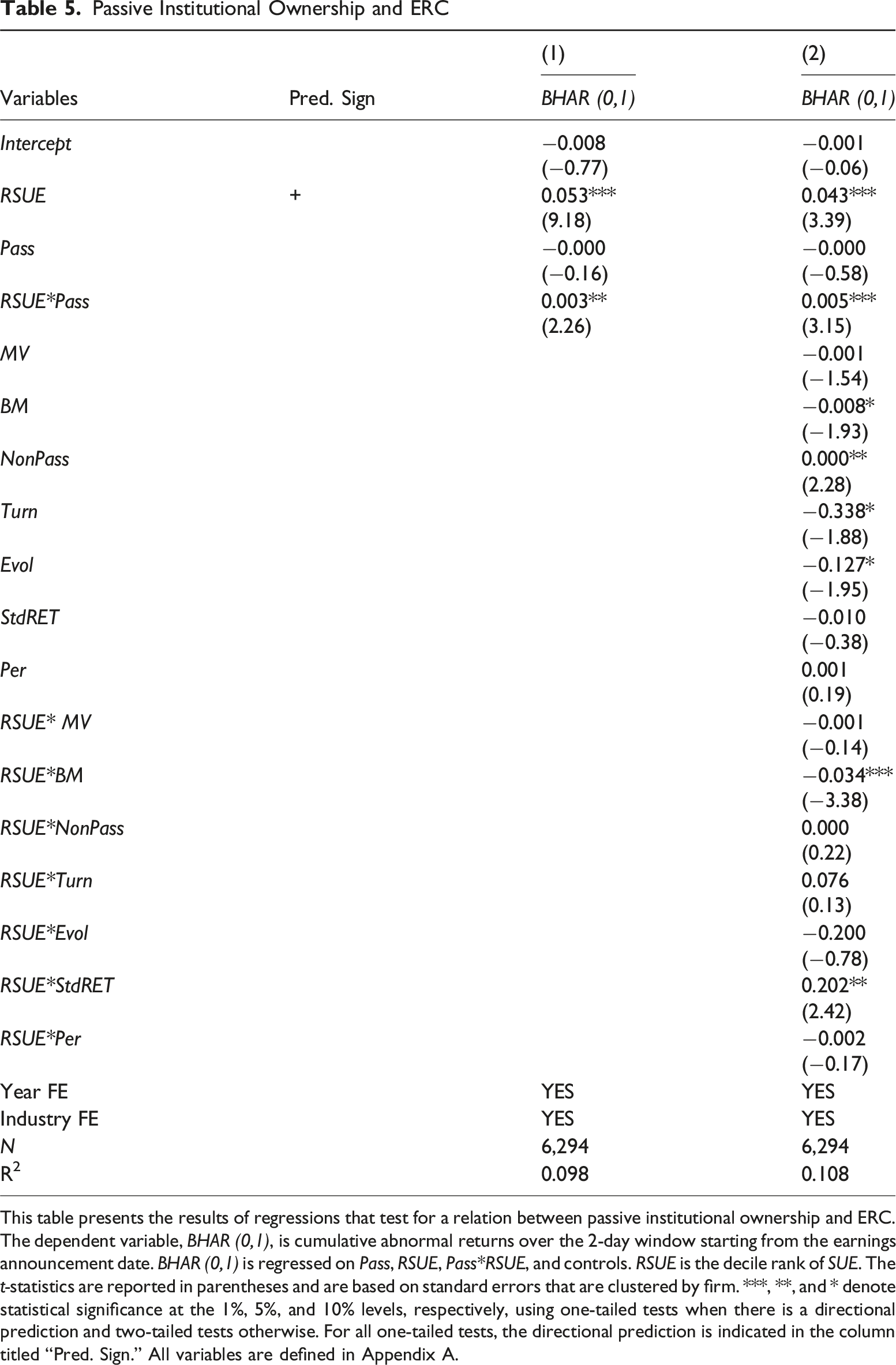

This table presents the results of regressions that test for a relation between passive institutional ownership and ERC. The dependent variable, BHAR (0,1), is cumulative abnormal returns over the 2-day window starting from the earnings announcement date. BHAR (0,1) is regressed on Pass, RSUE, Pass*RSUE, and controls. RSUE is the decile rank of SUE. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

In column (1) of Table 5, we regress BHAR(0,1) on the standardized earnings surprise (RSUE), passive institutional ownership (Pass), and the interaction term (RSUE*Pass). We find a significantly higher ERC for firms with higher passive institutional ownership (coeff. = 0.003, t = 2.26). In column (2), we include a set of control variables as well as their interactions with RSUE as additional explanatory variables. We find a significantly positive coefficient of the interaction term RSUE*Pass (coeff. = 0.005, t = 3.15), consistent with H1 that firms held by more passive institutional investors experience stronger initial market reactions to earnings announcements. For economic significance, the coefficients on RSUE and RSUE*Pass in column (2) imply that the market reactions are significantly more sensitive to earnings news by roughly 34% when passive institutional ownership moves from the 25th percentile (1.491%) to the 75th percentile (4.870%). (The sensitivity is 0.043 + (0.005 * 1.491) = 0.050 for the 25th passive institutional ownership percentile and 0.043 + (0.005 * 4.870) = 0.067 for the 75th passive institutional ownership percentile).

Passive Institutional Ownership and PEAD

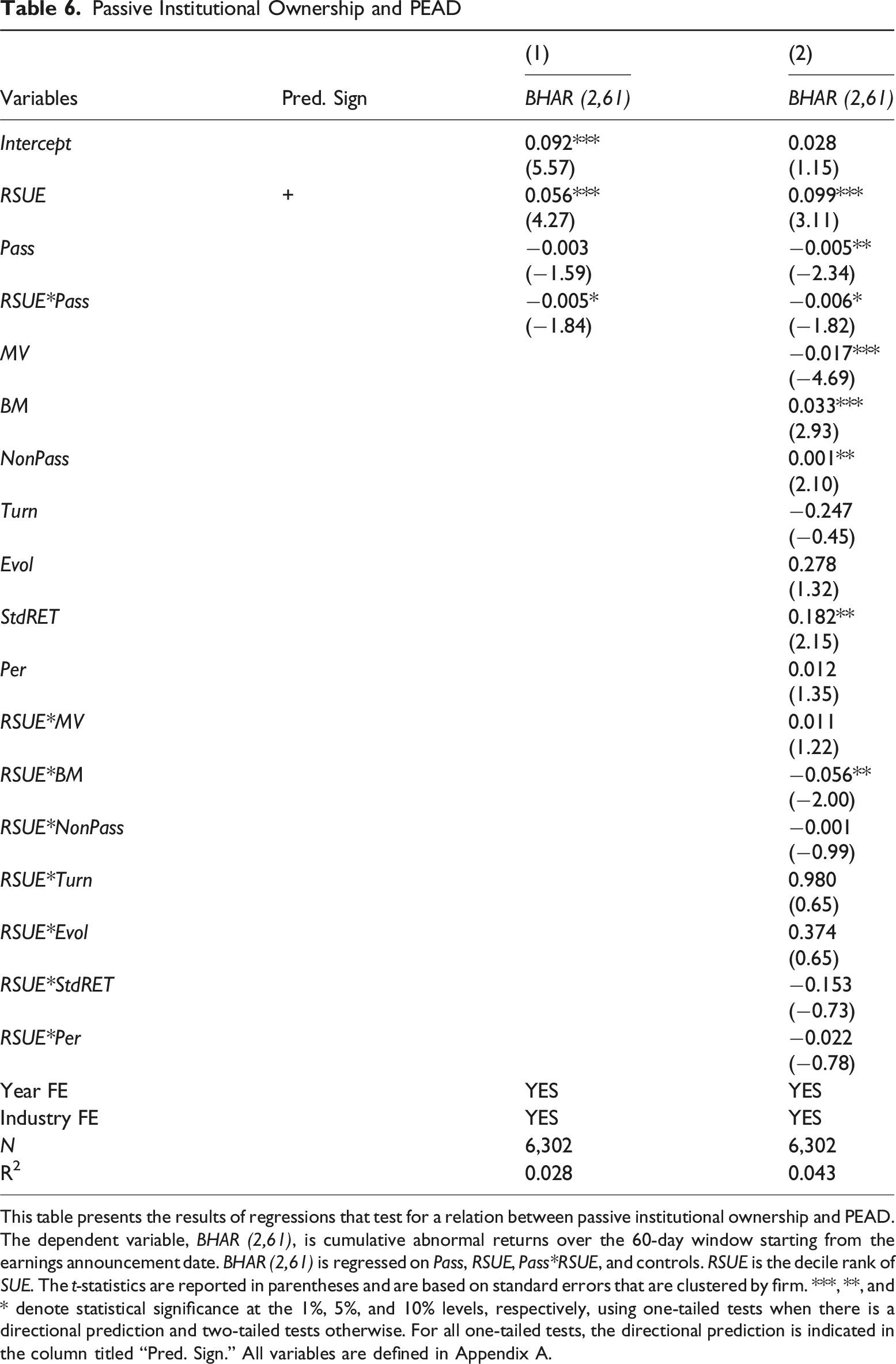

This table presents the results of regressions that test for a relation between passive institutional ownership and PEAD. The dependent variable, BHAR (2,61), is cumulative abnormal returns over the 60-day window starting from the earnings announcement date. BHAR (2,61) is regressed on Pass, RSUE, Pass*RSUE, and controls. RSUE is the decile rank of SUE. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

The above results are consistent with H1—that higher passive institutional ownership leads to lower PEAD by promoting firm disclosure and thereby facilitating the incorporation of firm information into prices. To provide further supportive evidence, we investigate whether the relation between passive institutional ownership and PEAD varies with changes in firm disclosure. Specifically, we conduct a change analysis and divide the sample based on whether the change in average disclosure from pre-addition to post-addition period is above zero. Consistent with our expectations, untabulated results show that the effect of passive institutional ownership on immediate market reactions is positive and statistically significant when the change in disclosure is above zero, whereas the effect is insignificant when the change in disclosure is below zero. 13

Robustness Tests

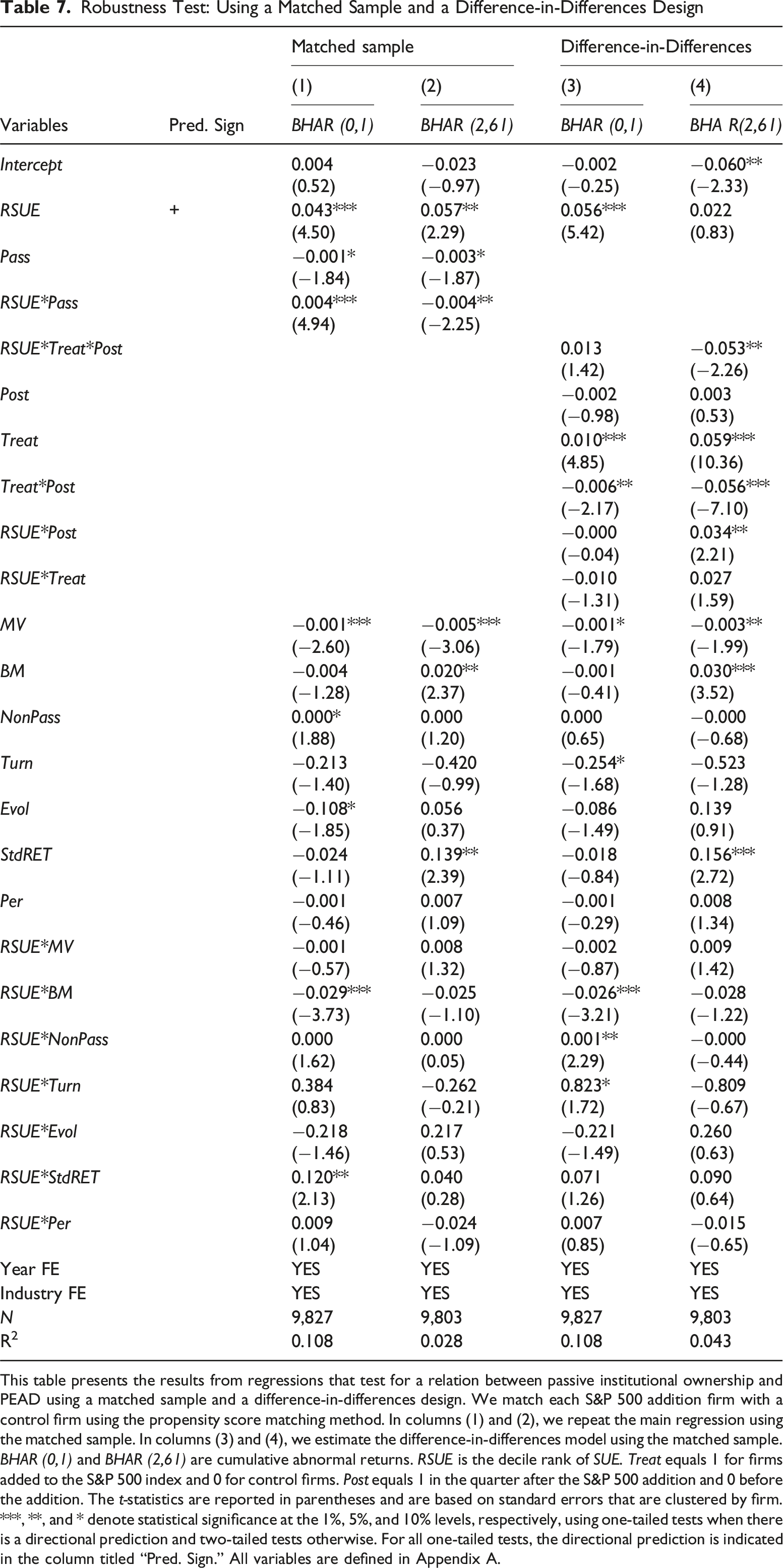

Robustness Test: Using a Matched Sample and a Difference-in-Differences Design

This table presents the results from regressions that test for a relation between passive institutional ownership and PEAD using a matched sample and a difference-in-differences design. We match each S&P 500 addition firm with a control firm using the propensity score matching method. In columns (1) and (2), we repeat the main regression using the matched sample. In columns (3) and (4), we estimate the difference-in-differences model using the matched sample. BHAR (0,1) and BHAR (2,61) are cumulative abnormal returns. RSUE is the decile rank of SUE. Treat equals 1 for firms added to the S&P 500 index and 0 for control firms. Post equals 1 in the quarter after the S&P 500 addition and 0 before the addition. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

Robustness Test: Seasonal Random-Walk-Based SUE

This table presents the results for regressions that test for a relation between passive institutional ownership and the earnings response using random-walk-based earnings surprises (RSUE_rw). The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

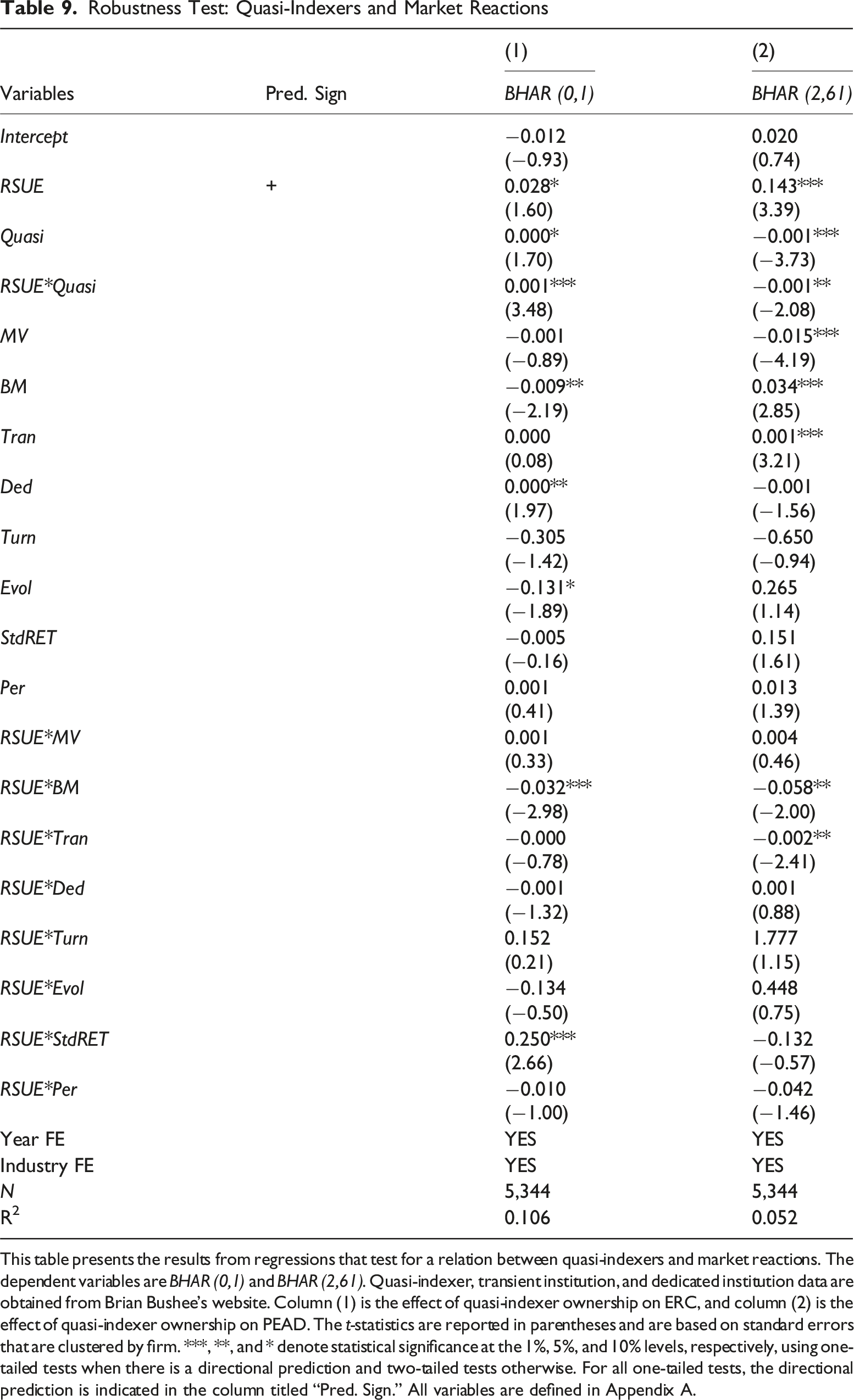

Robustness Test: Quasi-Indexers and Market Reactions

This table presents the results from regressions that test for a relation between quasi-indexers and market reactions. The dependent variables are BHAR (0,1) and BHAR (2,61). Quasi-indexer, transient institution, and dedicated institution data are obtained from Brian Bushee’s website. Column (1) is the effect of quasi-indexer ownership on ERC, and column (2) is the effect of quasi-indexer ownership on PEAD. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

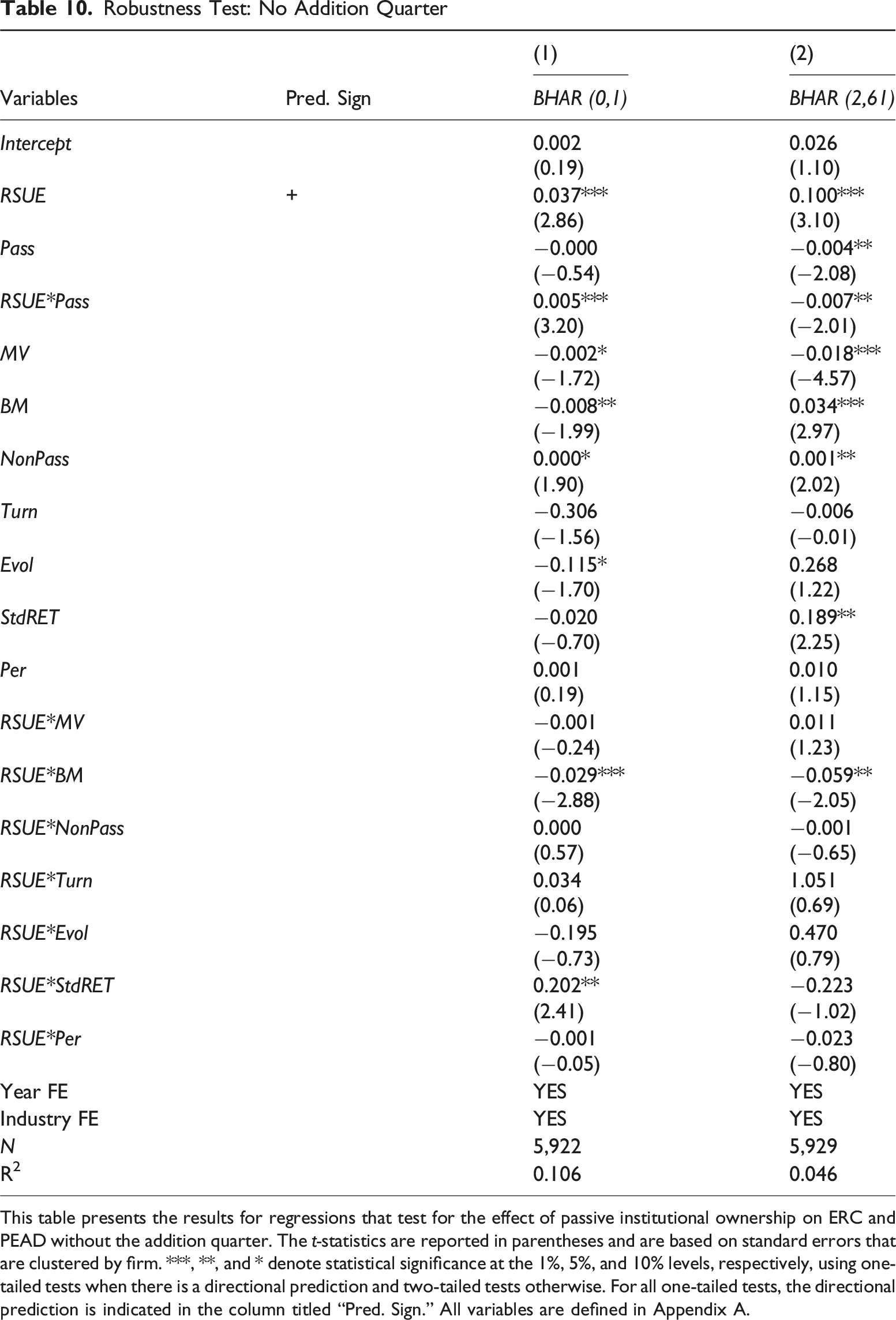

Robustness Test: No Addition Quarter

This table presents the results for regressions that test for the effect of passive institutional ownership on ERC and PEAD without the addition quarter. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

Market Reactions to Earnings Components

We decompose earnings surprises in each quarter into a firm-specific earnings component and a systematic earnings component by estimating equation (4) (Glosten et al., 2021; Israeli et al., 2017):

SUE_Mkt is calculated as the size-weighted average of earnings surprises for all firms in the market in quarter q. SUE_Ind is calculated as the size-weighted average of earnings surprises for all firms in the same two-digit SIC industry classification as firm i. Firm-specific earnings information (RSUE_Firm) and systematic earnings information (RSUE_Sys) are defined as the standardized residuals and fitted values estimated from the regression for firm i in quarter q, respectively.

Next, we regress cumulative abnormal returns on two decomposed earnings components (RSUE_Firm and RSUE_Sys) and two interaction terms between passive ownership and these two components (RSUE_Firm*Pass and RSUE_Sys*Pass). In equations (5) and (6), we are primarily interested in the coefficients of the two interaction terms. If the enhanced earnings response is due to the timely reflection of firm-specific earnings information (systematic earnings information) into stock prices, then we expect α4 > 0 (α5 > 0) and β4 < 0 (β5 < 0).

Passive Institutional Ownership and Market Reactions: Decomposed Earnings Components

This table presents the results from regressions that test for a relation between passive institutional ownership and market reactions to decomposed earnings components. RSUE_Firm is the firm-specific earnings component, defined as the residuals from estimating equation (4). RSUE_Sys is the systematic earnings component, defined as the fitted values from estimating equation (4). Pass is passive institutional ownership. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

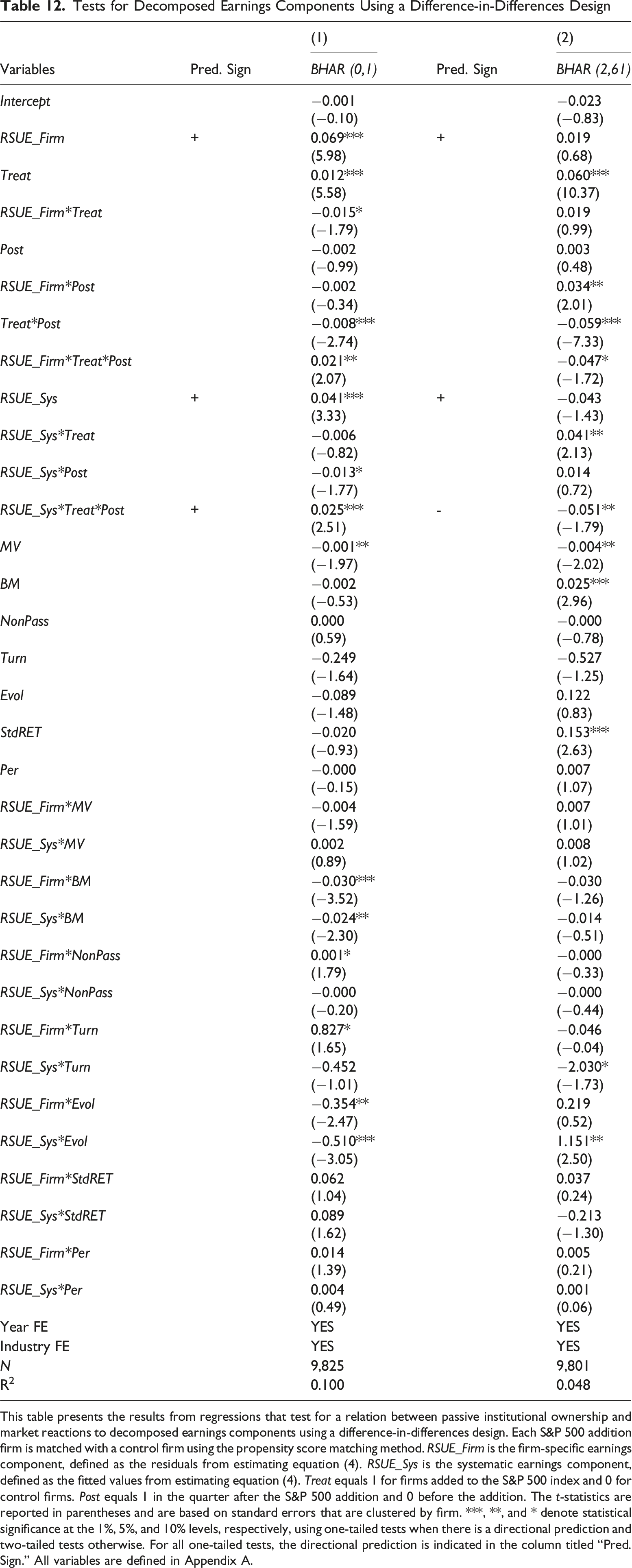

Tests for Decomposed Earnings Components Using a Difference-in-Differences Design

This table presents the results from regressions that test for a relation between passive institutional ownership and market reactions to decomposed earnings components using a difference-in-differences design. Each S&P 500 addition firm is matched with a control firm using the propensity score matching method. RSUE_Firm is the firm-specific earnings component, defined as the residuals from estimating equation (4). RSUE_Sys is the systematic earnings component, defined as the fitted values from estimating equation (4). Treat equals 1 for firms added to the S&P 500 index and 0 for control firms. Post equals 1 in the quarter after the S&P 500 addition and 0 before the addition. The t-statistics are reported in parentheses and are based on standard errors that are clustered by firm. ***, **, and * denote statistical significance at the 1%, 5%, and 10% levels, respectively, using one-tailed tests when there is a directional prediction and two-tailed tests otherwise. For all one-tailed tests, the directional prediction is indicated in the column titled “Pred. Sign.” All variables are defined in Appendix A.

Conclusion

This paper examines the impact of passive institutional ownership on market reactions to earnings announcements. Passive institutional investors favor more public information to reduce monitoring and trading costs. Managers are likely to supply more information because passive institutions can exert influence on investee firms due to their sizeable ownership stake. Because a richer information environment reduces information asymmetry and facilitates the incorporation of earnings information into prices, we predict that higher passive institutional ownership is correlated with stronger initial earnings responses and lower PEAD.

We use the S&P 500 addition setting to take advantage of large variations of passive institutional ownership around addition events. Using a sample of firms added to the S&P 500 index with a [−8 quarters, 8 quarters] window around each addition, we find that higher passive institutional ownership is associated with a higher frequency of 8-K filings. Our main analysis shows that higher passive institutional ownership is associated with a higher ERC around the earnings announcement window and lower PEAD. We also show that the enhanced market reactions are due to the timely incorporation of both firm-specific and systematic earnings news into the stock price. These findings suggest that passive institutional ownership induces a better information environment, accelerating the speed at which stock prices reflect earnings information.

Our paper extends the growing literature on the evaluation of passive institutional investors in the capital market by showing the channel through which passive institutional investors increase price efficiency—by promoting public information production. Our paper also adds to the literature on the relation between institutional investors and PEAD. Prior literature documents that transient institutional investors trade on PEAD but pays little attention to passive institutional investors. Our paper provides novel evidence on the effect of passive institutional ownership on PEAD.

Footnotes

Acknowledgments

This paper was previously titled Passive Institutional Ownership and Post-Earnings Announcement Drift. We thank our editor (Linda Myers) and two anonymous referees for many insightful suggestions. This paper also benefited from comments and suggestions from Derek Jerina, Jeff Kubik, Jim McKeown, workshop participants at Syracuse University, and conference participants at the JAAF conference.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received financial support from the Whitman School of Management at Syracuse University.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.