Abstract

Background

While whistleblowing (WB) has attracted growing research interest in recent years, several critical WB-related issues remain underexplored.

Purpose

This study examines the impact of external WB allegations on a firm’s organizational capital (OC). Such allegations often indicate management’s failure to address employee concerns internally, spotlighting potential deficiencies in internal reporting systems, employee communication, training, and trust in organizational fairness. To mitigate reputational damage, restore employee trust, and prevent future incidents, we posit that WB firms respond by increasing OC investment.

Research Design

We employ a difference-in-differences approach, comparing OC changes in WB-targeted firms with those in a propensity score-matched control sample.

Study Sample

Our dataset includes employee WB allegations obtained from OSHA (via a Freedom of Information Act request) and a hand-collected sample from public media.

Results

We find that WB firms significantly increase OC in the post-allegation period. Additionally, higher OC investment is linked to fewer future WB incidents. The decision to strengthen OC is primarily influenced by employees, long-term institutional investors, and prior OC deficiencies, rather than by WB case credibility or CEO characteristics.

Conclusions

Our findings indicate the importance of aligning long-term investment strategies and employee benefits with broader corporate goals to foster a responsive and adaptive organizational culture.

Introduction

Employee whistleblowing (WB) refers to “the disclosure by organization members of illegal, immoral, or illegitimate practices under control of their employers, to persons or organizations that may be able to effect action” (Near & Miceli, 1985, p. 4). Whistleblowers are key to helping firms detect fraud and organizational deficiencies, because they are usually among the first to observe wrongdoing (Brief & Motowidlo, 1986; Dyck et al., 2010; Lee & Fargher, 2013). Employee whistleblowers typically prefer to report concerns internally. This is because external WB is associated with higher costs of retaliation, discrimination, and unemployment. Thus, external WB allegations often reflect management’s failure to address concerns internally, due to inadequate reporting systems, unclear policies, or a lack of employee trust in organizational fairness and justice (Lee & Fargher, 2013; Stubben & Welch, 2020). Once WB allegations surface publicly, the WB target firms (WB firms or target firms, hereafter) face greater scrutiny from the public and regulators, significant reputational penalties, and escalating litigation risk (Bowen et al., 2010).

This study extends the WB literature by examining the relation between external WB and target firms’ organizational capital (OC). OC comprises the cumulative knowledge and collection of business processes and systems that enable firms to operate more efficiently. It includes investment in workforce training, employee voice, communications, and work design (Black & Lynch, 2005; Lev et al., 2009; Li et al., 2018). We argue that external WB allegations likely reflect deficient internal reporting systems, unclear policies and communications, and underinvestment in employees to enhance their knowledge, capabilities, and trust in organizational fairness and justice. In other words, external WB allegations reflect inadequate investment in OC. Therefore, we expect target firms to respond to allegations by increasing investment in OC.

Building on prior research (e.g., Bowen et al., 2010; Kuang et al., 2021), we use two data sources to identify external WB allegations. First, we filed a Freedom of Information Act (FOIA) request with the Occupational Safety and Health Administration (OSHA) (under the U.S. Department of Labor) to obtain WB data. Under §806 of the Sarbanes-Oxley Act of 2002 (SOX), employees can file discrimination complaints with OSHA that stem from alleged financial misconduct. OSHA is then required to communicate these allegations to the U.S. Securities and Exchange Commission (U.S. Department of Labor, 2012). Second, we supplement the OSHA sample with a hand-collected sample of media-reported WB allegations.

Following Eisfeldt and Papanikolaou (2013) and Li et al. (2018), we measure OC as capitalized selling, general, and administrative (SG&A) expenses divided by total assets. To address any endogeneity concerns related to the non-random nature of WB allegations, we create a control sample of non-WB firms using a propensity score matching (PSM) procedure (PSM control sample). 1 We then use a difference-in-differences (DiD) research design to compare changes in WB targets’ OC with that of the PSM control sample.

Our univariate tests and multivariate regression results show that WB firms respond to allegations by increasing OC. The increase is statistically and economically significant. For an average WB firm in our sample, the change represents a $45.74 million increase in OC. To corroborate our PSM sample findings, we also conduct a robustness test using an entropy-balanced sample, and find that our inferences hold.

Concerns about using SG&A expenses to measure OC may arise due to potential measurement errors from unrelated costs, such as advertising, R&D, and legal expenses. These may introduce noise. To address this issue, we conduct multiple robustness checks using alternative OC measures. Following Li et al. (2018) and Danielova et al. (2023), we use the industry median-adjusted ratio of OC to total assets and the ratio of SG&A expenses to total assets. Additionally, we subtract legal expenses from SG&A, and recalculate OC in order to mitigate concerns that higher OC may reflect litigation-related expenses. We further remove litigation, advertising, and R&D expenses from SG&A, and reestimate our tests. The results confirm that WB firms increase OC investment post-allegation.

Another concern is that OC may not directly measure the costs of improving internal communication to prevent WB. Investments in WB hotlines, training, and corporate citizenship programs are rarely disclosed. To overcome this measurement challenge, we use qualitative measures of OC that are closely aligned with our underlying constructs. Specifically, we obtain four qualitative OC dimensions from the Refinitiv ESG database that capture a company’s WB communication tools and policies: business ethics, employee involvement, employee training, and anti-fraud activities. These measures reflect aspects of OC related to reinforcing employee knowledge and trust, improving corporate citizenship, and enhancing companywide policies against bribery, corruption, and fraud.

Our robustness checks indicate a strong correlation between the original measure of OC and each of the four qualitative dimensions, as well as the composite measure from their sum. Our main inferences remain unchanged when using (1) the composite qualitative OC measure, (2) each individual qualitative dimension, or (3) the expected value of OC estimated by regressing the composite qualitative OC on the original OC while controlling for fixed effects.

Overall, our results from the robustness tests using alternative measures align with our main results. External WB allegations prompt target firms to increase investment in OC by enhancing WB communications and policies related to business ethics, employee involvement, training, and anti-fraud activities. This, in turn, promotes good corporate citizenship and greater awareness of anti-fraud policies.

Next, given that 75.16% of WB firms in our sample increased OC post-allegation, we use logistic regressions to explore which factors influenced this action. The results suggest that labor intensity, negative market reactions to an allegation, lower levels of prior OC, and long-term institutional investors are the primary drivers of the decision to increase OC. In contrast, factors such as WB case merit, short-term institutional investors, and CEO factors like ownership, risk-taking incentives, gender, or duality did not affect the decision.

Thus, our findings demonstrate that WB firms that are more heavily reliant on labor are more responsive to employee concerns. Furthermore, WB firms with low levels of pre-allegation OC are motivated to adjust their inadequate investment in OC post-allegation. Finally, our results are in line with those of prior studies documenting the influential monitoring role of long-term institutional investors (e.g., Attig et al., 2012, 2013). We find they appear to encourage WB firms to focus on long-term goals by increasing investment in OC post-allegation.

We also examine how changes in OC affect the likelihood of future external WB incidents. If post-allegation investments in OC improve internal reporting, organizational processes, and communication, fewer external WB cases should follow. 2 Our findings show that WB firms that increase OC investments experience fewer WB incidences in the two years post-allegation. They also have a lower probability of being external WB targets than their counterparts that did not increase OC. Untabulated analyses show that WB targets exhibit a post-allegation increase in OC regardless of whether the employee concerns were reported to the media or to OSHA.

Finally, we examine whether WB targets increase brand capital (i.e., capitalized advertising expenses) post-allegation. We aim to determine whether they are making cosmetic changes to mitigate reputational harm, or trying to seriously address the root causes of the allegations. Our results show that the average WB firm in our sample does not increase brand capital. This suggests that the documented increases in OC are intended to address the inadequacies that led to the WB allegation.

Our paper contributes to the WB and OC literature in several key ways. First, prior research on WB focuses primarily on determinants (Andrade, 2015; Cheng et al., 2019; Culiberg & Mihelič, 2017; Gao & Brink, 2017; Hartman & Desjardins, 2008; Hoffman & Schwartz, 2015; Morrison & Milliken, 2000). There is only a limited focus on target firm responses to WB allegations. Notable exceptions include Wilde (2017), who finds that WB firms reduce financial misreporting and tax aggressiveness, and Bowen et al. (2010), who show that WB firms subsequently improve corporate governance. Some earlier studies (e.g., Gobert & Punch, 2000; Miceli & Near, 1992; Schmidt, 2005) argue that firms often view allegations as frivolous, and therefore fail to enact meaningful changes. However, the literature remains largely silent on whether and how WB firms adjust OC investments to facilitate internal reporting, strengthen control, and amplify employee voice. Our paper addresses this gap.

Second, our study enriches the OC literature by providing novel evidence on how WB firms respond to allegations. We demonstrate that external WB allegations often reflect deficiencies in internal reporting systems and communication, as well as underinvestment in employees. Our findings show that WB firms rectify these deficiencies by increasing OC investment.

Understanding the Whistleblowing Process

Institutional Background

WB allegations may be reported internally or externally. The academic literature generally supports the idea that WB is an effective mechanism for uncovering internal control weaknesses (Kuang et al., 2021), misconduct, and unethical practices (Dyck et al., 2010; Lee & Xiao, 2018). Since the passage of the False Claims Act of 1863, U.S. legislators have implemented various laws to protect whistleblowers from retaliation, and provide financial incentives as motivation to report wrongdoing (e.g., the Sarbanes-Oxley Act of 2002 (SOX) and the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank) of 2010). 3

Under SOX, public firms are required to establish appropriate systems to receive complaints from employees about questionable accounting or auditing matters (SOX §301). In addition, public firms are required to document in their annual reports how management maintains adequate internal control structures (SOX §404). Thus, the law requires WB firms to improve their internal reporting and monitoring systems.

However, despite this law, recent studies find that internal control systems are not always adequate (Soltes, 2020; Stubben & Welch, 2020). Some firms establish procedures simply for compliance (“window-dressing”), but do not invest adequate resources to ensure the controls function as intended. For example, legislation in the U.S. requires firms to offer employees a means to report accounting misconduct anonymously, but significant barriers to a smooth reporting process often remain. As Soltes (2020) notes, approximately one-fifth of firms have impediments to internal reporting of accounting irregularities, and about one-tenth fail to respond to internal allegations. In addition, rapidly growing firms tend to receive fewer internal WB reports per employee, with less information, and less follow-up by management (Stubben & Welch, 2020).

Whistleblowing Process

Employee perceptions of organizational justice, fairness, and transparency influence potential whistleblowers at various stages. In the first stage, employees observe the alleged misconduct or unethical practice. In the second stage, they consider the incentives and disincentives of reporting the misconduct, as well as past organizational responses. Here, explicit statements of a code of conduct, organizational support for ethical behavior, whistleblower protection, and financial rewards are incentives to report the misconduct internally. In contrast, perceptions that WB will not result in corrective actions, and may lead to potential discrimination or retaliation, are likely to influence employees to remain silent about the misconduct. Prior research shows that, if employees decide to report misconduct, they first make an internal report to supervisors or managers (Bjørkelo et al., 2011; Smith, 2010).

The third stage describes possible organizational responses once an internal report is filed. Acceptable responses include thorough investigations and corrective actions to stop the unethical activity. Unacceptable responses include ignoring the WB report, or subjecting whistleblowers to discrimination or retaliation at work.

The final stage encompasses the post-internal allegation period. Here, a favorable path would mean the whistleblower is satisfied with the internal outcome, and the process ends. An unfavorable path could mean the whistleblower feels demoralized and remains silent, or seeks resolution by reporting the misconduct externally to authorities or the media. If the WB process progresses along this path, financial and reputational costs to target firms can dramatically increase.

Prior Literature and Hypothesis Development

Whistleblowing has attracted significant attention from the public, regulators, and scholars in recent years. Prior research shows that WB is one of the most effective methods for exposing corporate malfeasance (Lee & Xiao, 2018). Dyck et al. (2010) find that employee whistleblowers are more effective than outside monitors at detecting corporate fraud. The Association of Certified Fraud Examiners (2020) reports that approximately 43% of detected fraud cases are identified by employee whistleblowers. Furthermore, recent studies show that WB allegations are taken seriously by regulators, law enforcement agencies, and WB target firms (Bowen et al., 2010; Call et al., 2018; Kuang et al., 2021; Stubben & Welch, 2020; Wilde, 2017).

Employees who observe misconduct typically prefer to report their concerns internally due to the higher costs associated with external WB, such as retaliation, discrimination, and unemployment. However, if internal reports do not receive adequate attention, or if management fails to take corrective action, employees may resort to external WB by going public or reporting to a government agency. Stubben and Welch (2020) analyze nearly 2 million internal WB reports, and find significant variation in the efficacy of the internal systems, which they attribute to managers’ differing views on the costs and benefits of these systems. Some firms implement WB systems solely to comply with SOX. But they fail to actively promote or use them. In other firms, managers worry that WB systems could be misused by underperforming employees to file frivolous complaints to gain legal protection as whistleblowers.

Soltes (2020) conducts a comprehensive field study on the functionality of internal WB systems. He finds significant obstacles to WB reporting, including disconnected phone lines, incorrect web redirects, and email bouncebacks in 20% of firms’ reporting systems. Approximately 10% of firms fail to respond promptly to reports. Importantly, merely implementing a WB reporting system does not necessarily fulfill the intended purpose of preventing fraud and misconduct. The system will remain ineffective if firms do not appropriately train and encourage employees to use it, or if employees do not trust management to address reported claims. Although there is some evidence on the functionality of internal WB systems, little is yet known about whether and how target firms respond to external WB allegations.

External WB allegations not only reflect management’s failure to internally address employees’ concerns, they also highlight possible deficiencies in internal reporting systems, communication to employees, and underinvestment in employee training. These issues are captured in the four components of organizational capital investment identified by Black and Lynch (2005): workforce training, employee voice, communication, and work design.

OC is generally defined as the cumulative knowledge and collection of business processes and systems that enable firms to utilize their input resources more efficiently (Black & Lynch, 2005; Lev et al., 2009; Li et al., 2018). Firms develop this intangible asset through investment in their workforce and their operational practices and systems. Underinvestment in OC can disrupt operating processes and communication in a multitude of ways (Atkeson & Kehoe, 2005; Eisfeldt & Papanikolaou, 2013; Lev et al., 2009; Lev & Radhakrishnan, 2005; Prescott & Visscher, 1980).

Prosocial organizational behavior theory suggests that the actions firms take to address employee concerns are crucial to restoring and building an organization-wide perception of integrity, fairness, and justice (Miceli et al., 2008). Trevino and Weaver (2001) and Rupp and Bell (2010) provide evidence that employees’ perceptions of justice influence their willingness to go beyond their job obligations to advocate for justice. This behavior is essential for maintaining a positive firm culture, promoting the safe reporting of unethical practices and misconduct, and motivating employees to identify problems that could negatively impact organizational goals. The likelihood of internal WB thus increases when employees perceive fairness in organizational WB procedures and outcomes, and in their interactions with supervisors (Seifert et al., 2010).

Establishing effective communication channels for employees to report problems without fear of discrimination, repercussions, or retaliation is essential for fostering trust and transparency within an organization. Effective internal reporting of misconduct also enables management to promptly address and resolve employee concerns, as well as avoid reputational damage and lengthy, costly investigations. Therefore, when an employee bypasses the internal WB system to report corporate misconduct externally, management should feel compelled to address internal deficiencies and underinvestment in OC. Hence, we conjecture that firms will respond to external WB allegations by increasing investment in OC:

Target firms increase investment in organizational capital in the post-allegation period.

Research Design

Measuring Organizational Capital

We follow prior literature (Eisfeldt & Papanikolaou, 2013; Lev et al., 2016; Lev & Radhakrishnan, 2005; Li et al., 2018), and measure a firm’s stock of OC by using capitalized SG&A expenses divided by total assets. SG&A expenses include communication expenditures (e.g., information technology, information systems, and distribution channels), consulting fees, investment in workforce training costs, work design, business processes, and systems, advertising and marketing expenses, and employee salaries, benefits, and promotions. These expenses aim to improve a firm’s body of knowledge and the synergy between combinations of labor and capital investments in OC (Eisfeldt & Papanikolaou, 2013; Li et al., 2018). We compute the stock of OC by using the perpetual inventory method. We recursively add the deflated value of SG&A expenses as follows:

Whistleblowing Sample

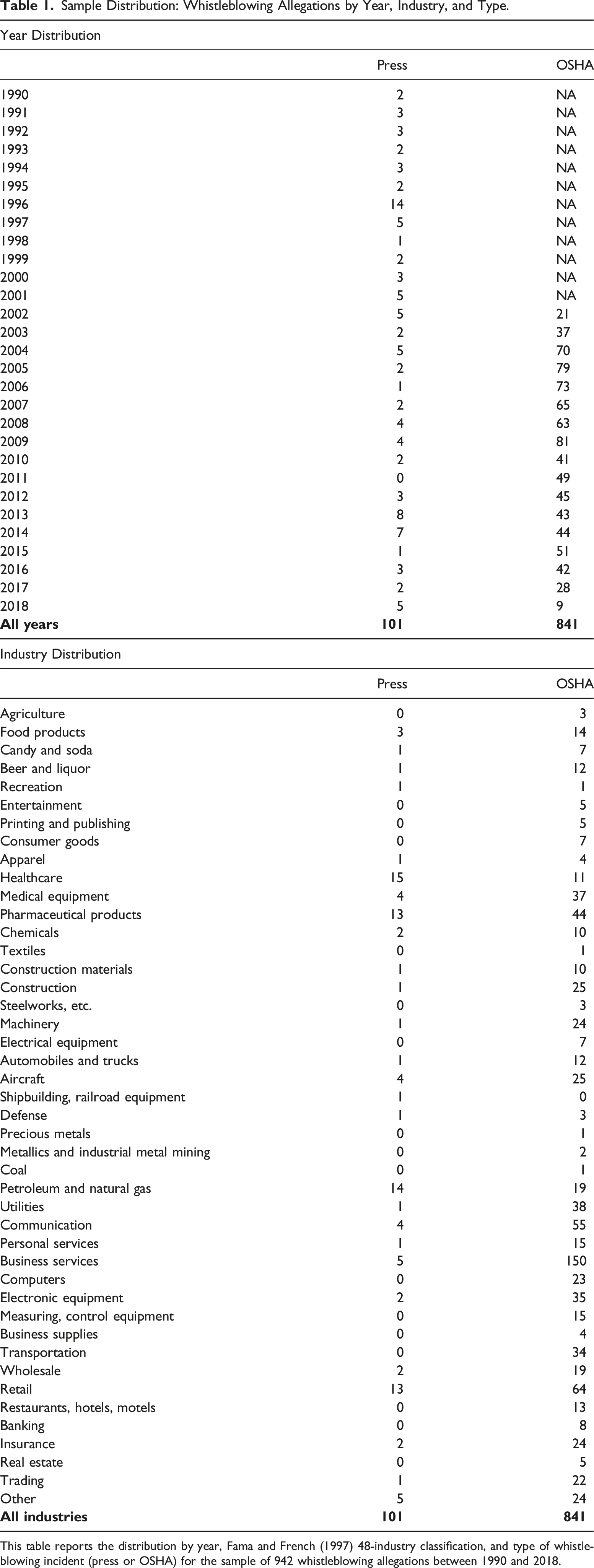

Following Bowen et al. (2010), we collect our sample of external WB allegations from two sources. The first is the press sample. We manually collect WB events related to financial misconduct reported in the media over 1990–2018 by searching LexisNexis for each combination of the following two groups of keywords: (1) “whistle,” “WB,” “whistle-blowing,” “whistleblower,” and “whistle-blower” and (2) “financial,” “accounting,” “reporting,” “fraud,” and “accounting fraud.” We then carefully read each media report and retain only those related to financial misconduct. We begin with 231 media-reported WB cases.

The second source is the OSHA sample. It consists of WB discrimination cases gathered from written requests to OSHA under the FOIA. A whistleblower can report perceived workplace discrimination to OSHA (e.g., demotions and terminations), or that an employer or anyone in the organization has retaliated against a whistleblower for voicing allegations of financial misconduct, such as a violation of SOX or the Consumer Financial Protection Act (CFPA, Title X of the Dodd–Frank Act). Although OSHA handles other types of WB allegations, we obtain data solely for allegations of financial misconduct from those who filed for protection under SOX or the CFPA over 2002–2018. Our OSHA sample consists of WB cases protected by §806 of SOX or Title X of the Dodd–Frank Act. We begin with 3,546 OSHA cases, and subsequently exclude 1,662 that have no CUSIP data in Compustat and 81 that are duplicates in the same firm-year.

We require that firms have non-missing data in Compustat, the Center for Research in Security Prices (CRSP), and I/B/E/S databases for year t − 1 for PSM and for our main analyses, where t is the year of the WB event. We exclude another 1,092 observations at this step, leaving us with a final sample of 942 WB cases from 518 unique firms for the 1989–2020 period.

Sample Distribution: Whistleblowing Allegations by Year, Industry, and Type.

This table reports the distribution by year, Fama and French (1997) 48-industry classification, and type of whistleblowing incident (press or OSHA) for the sample of 942 whistleblowing allegations between 1990 and 2018.

Propensity Score-Matched Sample

One concern related to making inferences about changes in OC investment following WB events is that the events may not be exogenous. Rather, they may be related to non-random activities linked to the allegations. Following prior studies (Bowen et al., 2010; Wilde, 2017), we use a propensity score-matched control sample to mitigate these concerns. This matching approach allows us to attribute observed outcomes to WB instead of to other allegation-related firm behaviors.

The PSM design can mitigate any misspecification of the functional form underlying the association between the variable of interest and a given outcome (Armstrong et al., 2010). We include the determinants of WB and OC in the matching model. We adopt a DiD design with the WB firms (WB, treatment sample) and the propensity score-matched sample (PSM control sample) that exhibit appropriate covariates in the pre-WB period.

Following Bowen et al. (2010), our determinants of WB (CONTROLS WB ) include: capital market pressure (CM_PRESSURE); sales growth (SALEGROWTH); unclear communication channels (COM); employee downsizing (DOWNSIZE); membership in an industry with monetary incentives to report misconduct (QUITAM); firm size (SIZE); internal control weaknesses (ICW); and external monitoring (ANALYST).

We also draw on prior research (Eisfeldt & Papanikolaou, 2013, 2014; Li et al., 2018) to identify factors associated with investment in OC (CONTROLS OC ). Accordingly, we control for investment in research and development (R&D), investment in fixed assets (CAPEX), cash holdings (CASH), dividend payments (DIV), share repurchase expenditures (REPO), past performance (ROA), and prior level of investment in OC (LAGOC).

To compute propensity scores, we estimate the following logistic regression:

Next, we refer to McFadden’s (1974) pseudo-R2 in order to assess the goodness of fit of the logistic model. McFadden (1974) suggests that a pseudo-R2 between 0.20 and 0.40 represents “an excellent fit.” Our model (3) estimation yields a McFadden’s pseudo-R2 of 23.92%, suggesting satisfactory goodness of fit in predicting the likelihood of WB events. We also validate the predictive power of our model by using the area under the receiver operating characteristic curve (ROC). Rice and Harris (2005) find that an ROC value of 0.70 or higher indicates a satisfactory model fit. The value for our model (3) estimation is 0.89. The PSM-balanced sample consists of 942 external WB observations and 942 PSM control observations.

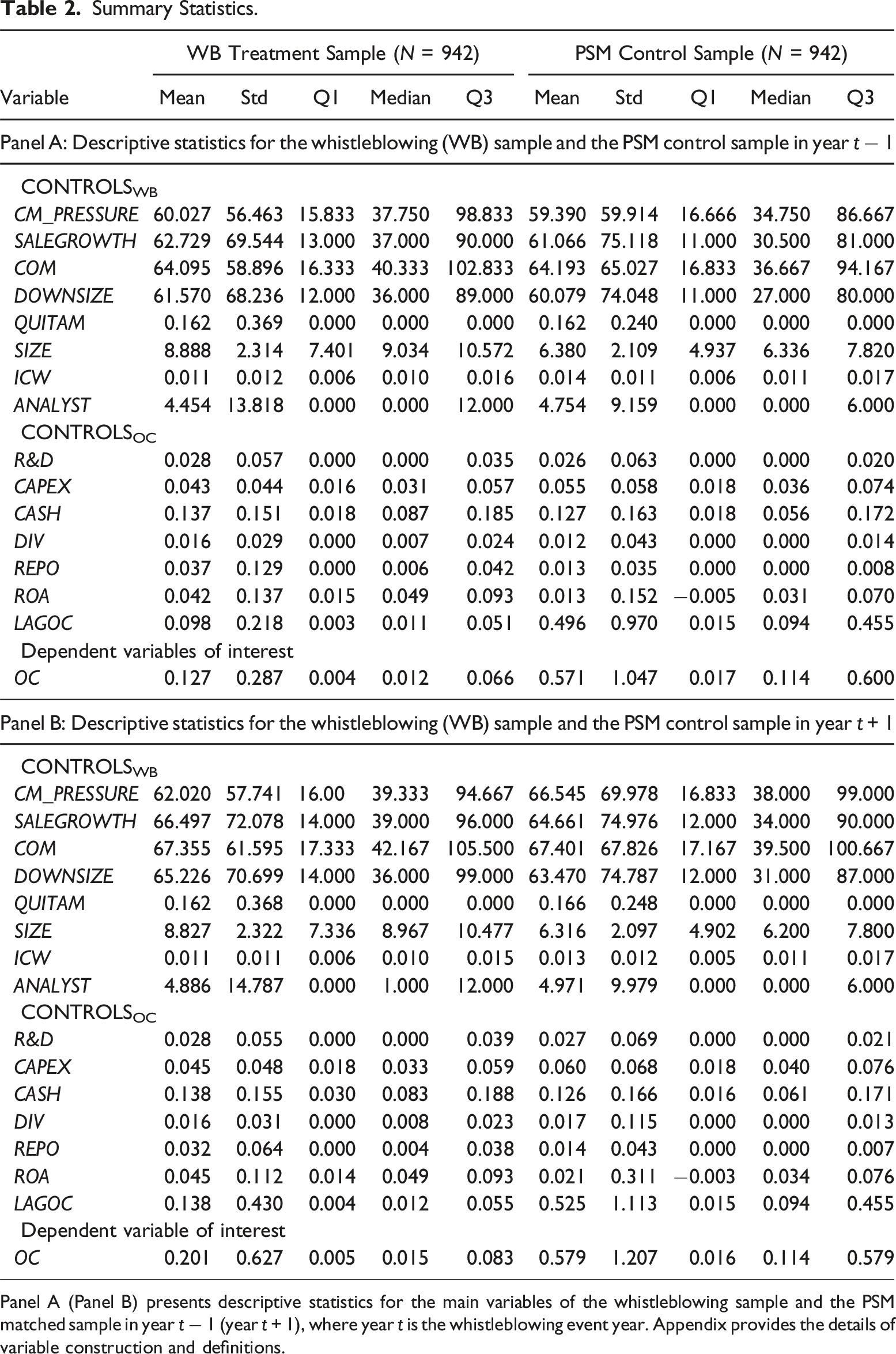

Summary Statistics.

Panel A (Panel B) presents descriptive statistics for the main variables of the whistleblowing sample and the PSM matched sample in year t − 1 (year t + 1), where year t is the whistleblowing event year. Appendix provides the details of variable construction and definitions.

Changes in Organizational Capital

We adopt a DiD approach to examine changes in OC investment from the pre- to post-allegation periods for the treatment versus PSM control firms. DiD estimation is appropriate when the event period is common across observations (Chen et al., 2015; Wilde, 2017). In our setting, the common event period is the year of the (pseudo-) allegation for the matched and control firms (despite the fact that individual WB events occur in different years). Following Caliendo and Kopeinig (2008) and Roberts and Whited (2013), we examine within-matched-pair variation to remove selection bias from non-random events and time-invariant unobservable attributes. This approach also addresses concerns that changes in OC, common to both types of firms, may drive the observed behaviors.

We estimate the following regression model:

Empirical Results

Changes in Organizational Capital: Main Results

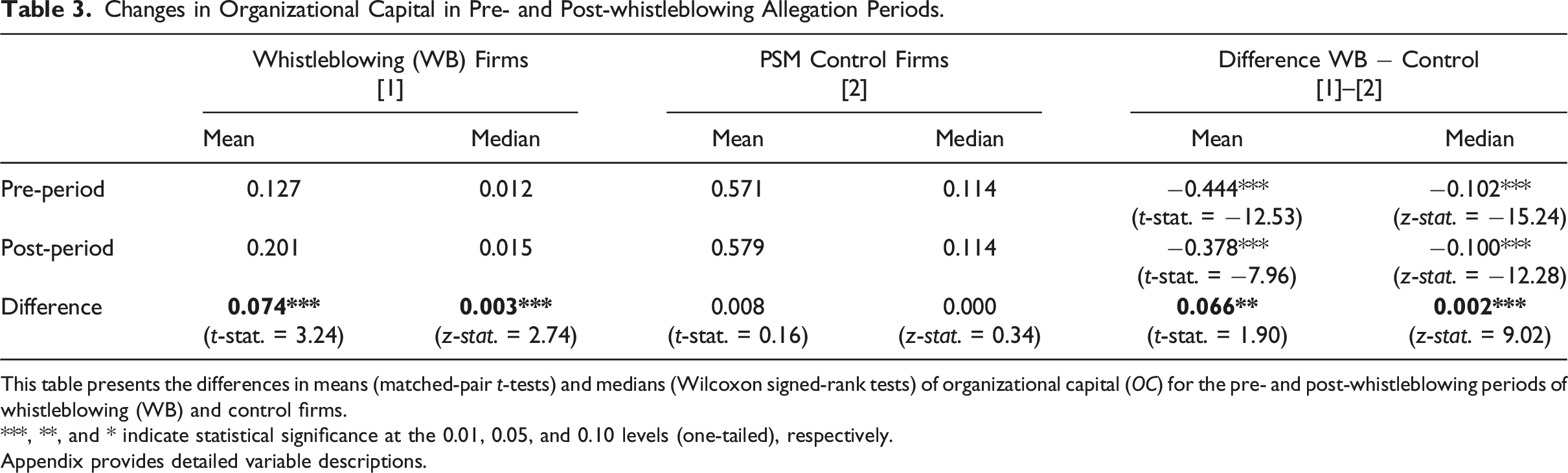

Changes in Organizational Capital in Pre- and Post-whistleblowing Allegation Periods.

This table presents the differences in means (matched-pair t-tests) and medians (Wilcoxon signed-rank tests) of organizational capital (OC) for the pre- and post-whistleblowing periods of whistleblowing (WB) and control firms.

***, **, and * indicate statistical significance at the 0.01, 0.05, and 0.10 levels (one-tailed), respectively.

Appendix provides detailed variable descriptions.

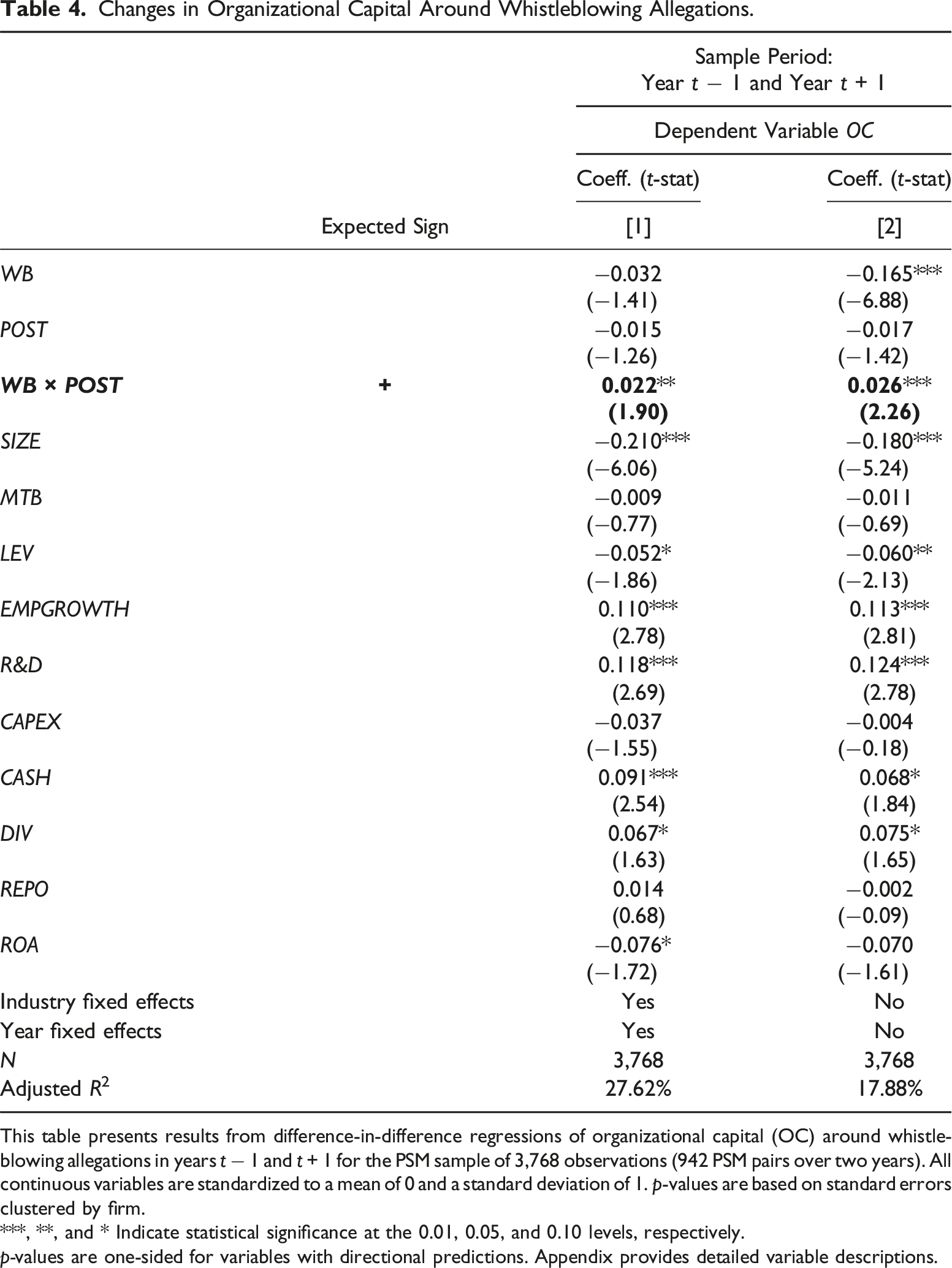

Changes in Organizational Capital Around Whistleblowing Allegations.

This table presents results from difference-in-difference regressions of organizational capital (OC) around whistleblowing allegations in years t − 1 and t + 1 for the PSM sample of 3,768 observations (942 PSM pairs over two years). All continuous variables are standardized to a mean of 0 and a standard deviation of 1. p-values are based on standard errors clustered by firm.

***, **, and * Indicate statistical significance at the 0.01, 0.05, and 0.10 levels, respectively.

p-values are one-sided for variables with directional predictions. Appendix provides detailed variable descriptions.

Alternative Measures of Organizational Capital: Robustness Check

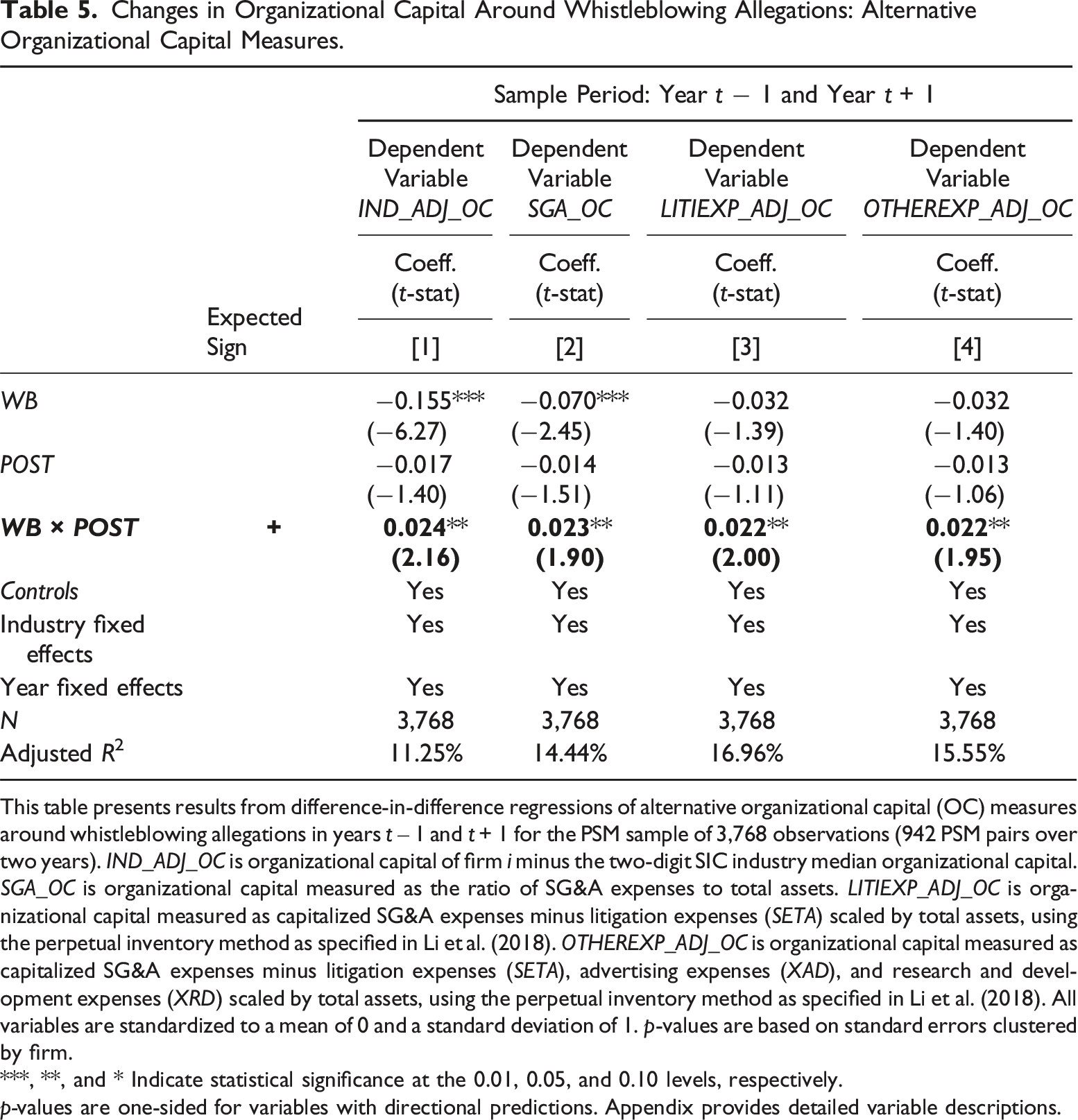

We note that concerns may arise when using SG&A to measure OC, because accounting treatments of SG&A expenses can vary across industries. They mainly reflect OC-related investments, such as employees’ training, welfare, and benefits, and communication and technology expenses. But they may also include unrelated expenses, like advertising, R&D, and legal fees. This may introduce noise into the OC measure. We address this issue by conducting a battery of robustness checks using multiple alternative OC measures.

First, following Li et al. (2018), we use the industry median-adjusted ratio of OC to total assets (IND_ADJ_OC). Second, we use the ratio of SG&A expenses to total assets (SGA_OC). Third, to account for the possibility that higher OC investment may stem from increased legal expenses related to WB allegations, we subtract legal expenses from SG&A (LITIEXP_ADJ_OC). Finally, for our fourth measure, we exclude litigation, advertising, and R&D expenses from SG&A expenses before calculating OC (OTHEREXP_ADJ_OC).

Changes in Organizational Capital Around Whistleblowing Allegations: Alternative Organizational Capital Measures.

This table presents results from difference-in-difference regressions of alternative organizational capital (OC) measures around whistleblowing allegations in years t ‒ 1 and t + 1 for the PSM sample of 3,768 observations (942 PSM pairs over two years). IND_ADJ_OC is organizational capital of firm i minus the two-digit SIC industry median organizational capital. SGA_OC is organizational capital measured as the ratio of SG&A expenses to total assets. LITIEXP_ADJ_OC is organizational capital measured as capitalized SG&A expenses minus litigation expenses (SETA) scaled by total assets, using the perpetual inventory method as specified in Li et al. (2018). OTHEREXP_ADJ_OC is organizational capital measured as capitalized SG&A expenses minus litigation expenses (SETA), advertising expenses (XAD), and research and development expenses (XRD) scaled by total assets, using the perpetual inventory method as specified in Li et al. (2018). All variables are standardized to a mean of 0 and a standard deviation of 1. p-values are based on standard errors clustered by firm.

***, **, and * Indicate statistical significance at the 0.01, 0.05, and 0.10 levels, respectively.

p-values are one-sided for variables with directional predictions. Appendix provides detailed variable descriptions.

Qualitative Measures of Organizational Capital: Robustness Check

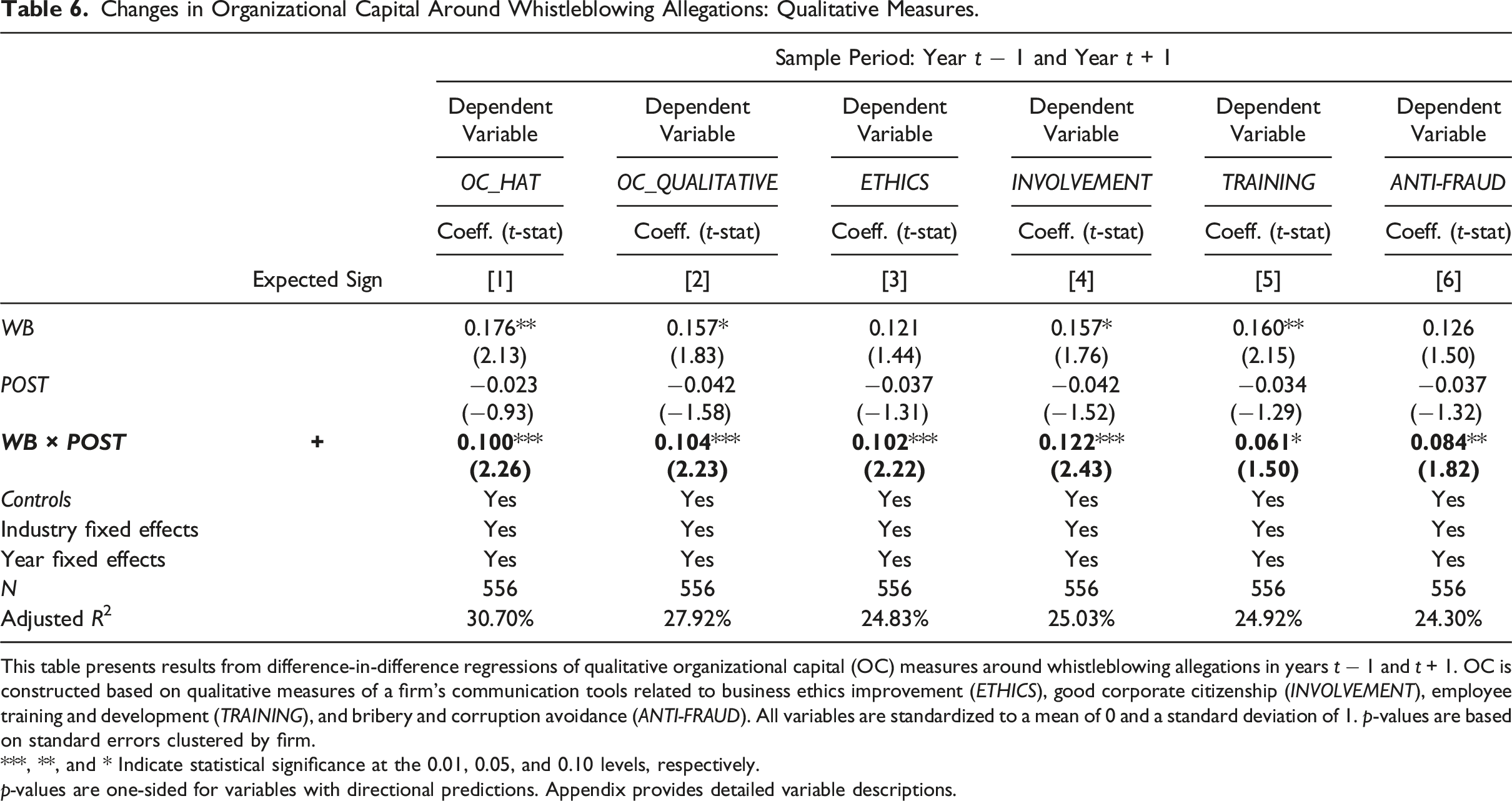

Another concern is that OC does not directly measure the costs associated with improving a firm’s internal communications environment. It can be challenging to identify the exact amounts invested in the various dimensions of OC, such as WB hotlines, corporate citizenship programs, or employee training initiatives. Such information is not typically publicly disclosed. To address this, we use qualitative disclosures of OC dimensions related to reinforcing employees’ knowledge of internal WB reporting systems, improving corporate citizenship, business ethics, and companywide anti-bribery, corruption, and fraud policies and activities. 4

We obtain four different qualitative OC dimensions: ETHICS, INVOLVEMENT, TRAINING, and ANTI-FRAUD from Refinitiv’s environmental, social, and governance (ESG) database. This database covers over 12,500 public and private companies globally, including more than 3,800 U.S. companies. The data are available from 2003 onward, with dimension scores ranked by industry. These dimensions fall under the workforce, human rights, and community categories within the social pillar of Refinitiv’s ESG scores. 5

According to Refinitiv, the business ethics (ETHICS) dimension measures a company’s internal communication tools and policies for improving business ethics. Employee involvement in the internal reporting system (INVOLVEMENT) measures the internal communication tools and policies related to whistleblowers, ombudsmen, suggestion boxes, hotlines, newsletters, websites, etc., that are designed to improve corporate citizenship. Employee training (TRAINING) measures the training on internal policies related to whistleblowers, ombudsmen, suggestion boxes, hotlines, newsletters, websites, etc. And the anti-bribery, corruption, and fraud (ANTI-FRAUD) dimension focuses on internal communication tools and policies to prevent bribery and corruption.

We aggregate these four dimensions into a composite measure of qualitative OC (OC_QUALITATIVE), and then merge it with our main sample. This results in 556 observations from 139 WB firms and their matched observations. We estimate the association between the original OC measure and the qualitative OC measure using the following regression model:

The (unreported) regression results show that the coefficient on OC_QUALITATIVE is positive and significant (the coefficient is 0.309; p-value <.01). This suggests that our original measure of OC is strongly correlated with the underlying constructs of OC that are related to communication with employees to improve business ethics, increasing employee involvement, enhancing training, and strengthening communication about anti-fraud activities. We then obtain the expected value of the dependent OC (OC_HAT) from model (5) above.

Changes in Organizational Capital Around Whistleblowing Allegations: Qualitative Measures.

This table presents results from difference-in-difference regressions of qualitative organizational capital (OC) measures around whistleblowing allegations in years t − 1 and t + 1. OC is constructed based on qualitative measures of a firm’s communication tools related to business ethics improvement (ETHICS), good corporate citizenship (INVOLVEMENT), employee training and development (TRAINING), and bribery and corruption avoidance (ANTI-FRAUD). All variables are standardized to a mean of 0 and a standard deviation of 1. p-values are based on standard errors clustered by firm.

***, **, and * Indicate statistical significance at the 0.01, 0.05, and 0.10 levels, respectively.

p-values are one-sided for variables with directional predictions. Appendix provides detailed variable descriptions.

Entropy-Balanced Sample: Robustness Check

The PSM approach is effective at producing appropriate covariate matching. However, in order to mitigate concerns about PSM’s sensitivity to design choice, we also use entropy balancing. This approach mitigates differences in observable covariates across the treatment and control groups (Hainmueller, 2012). We balance the sample using the same set of WB allegation determinants used in the PSM approach. We then equalize the first (mean), second (variance), and third (skewness) moments of each covariate distribution using a tolerance level of 0.015 for convergence. Consistent with our previous findings, WB firms exhibit higher levels of OC investment post-allegation. 6

Additional Analyses

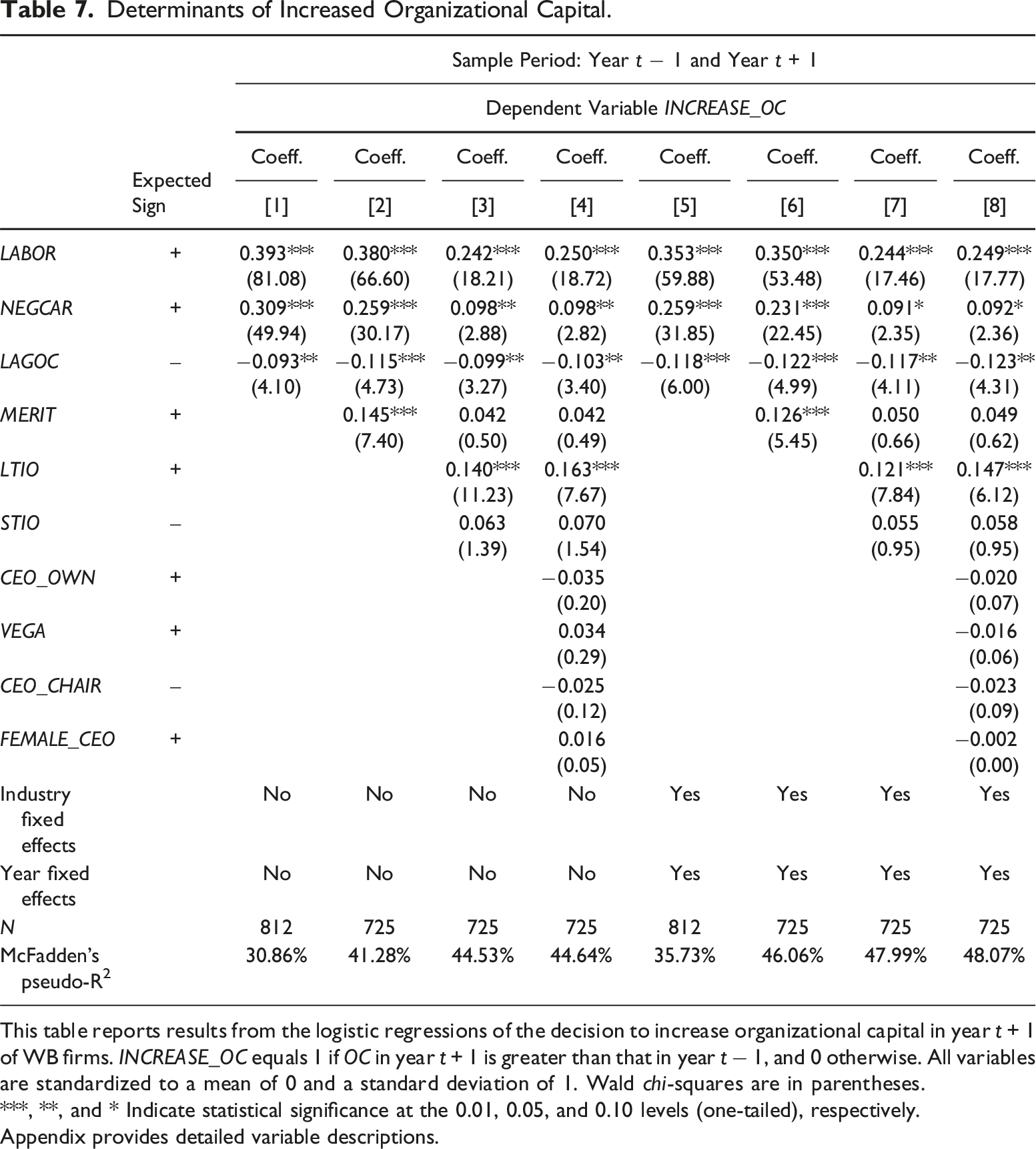

Determinants of Organizational Capital Improvement Decisions

The results from the previous sections indicate that WB firms on average increase their investment in OC during the post-allegation period. However, in our sample, only 75.16% of firms increased their OC from year (t − 1) to (t + 1). To explore which factors influence this decision, we examine several key determinants, including labor and shareholder influences, pre-allegation OC levels, WB case credibility, and CEO incentives.

To this end, we estimate the following regression model:

Labor-intensive firms by nature require larger investments in human capital-related components of OC (such as communication systems, workforce training, and worker welfare). Thus, we expect labor-intensive firms (measured using LABOR) to be more likely to increase OC investment in response to WB allegations. Furthermore, negative market reactions to WB allegations can cause significant losses for shareholders, prompting firms to act. We expect WB firms that experience negative market reactions (NEGCAR) to be more likely to increase OC.

Insufficient prior investment in OC can lead to lax internal controls, ineffective communications, and low employee morale, which may increase the odds of financial misconduct and subsequent external WB. Therefore, we expect WB firms with lower OC during the pre-allegation period (LAGOC) to be more likely to increase OC investment. Research has also found that some WB allegations reflect employees’ reckless assessments of a situation (Berger & Lee, 2022). Thus, credible allegations (MERIT) likely indicate OC deficiencies, and are more likely to motivate managers to increase OC investment. We expect that firms facing credible WB allegations will be more likely to increase investment in OC post-allegation. The sample size decreases because credibility information is only available for OSHA WB allegations.

Long-term institutional investors enhance managerial decision-making through their monitoring role. They help restrain financial fraud and improve investment decisions (Gaspar et al., 2005; Harford et al., 2018). Therefore, WB firms with a higher percentage of long-term institutional ownership are more likely to increase investment in OC. On the other hand, short-term institutional investors tend to prioritize immediate returns over long-term investments (Attig et al., 2013; Gaspar et al., 2005), thereby undermining their effectiveness in monitoring managers.

Following Gaspar et al. (2005), we use investor-level portfolio information from the 13F holdings compiled by Refinitiv to compute long-term institutional ownership (LTIO) and short-term institutional ownership (STIO). We expect to find a positive (negative) and significant coefficient on LTIO (STIO).

We also examine the impact of CEO factors such as equity ownership (CEO_OWN), and risk-taking incentives such as compensation’s sensitivity to stock return volatility (VEGA). This is because CEOs with significant ownership stakes should be more motivated to address the deficiencies highlighted by WB in order to protect their personal financial interests. Shen and Zhang (2013) find that firms with increased VEGA are more likely to increase R&D investments. Higher VEGA could also influence increases in OC investment, because higher sensitivities motivate CEOs to undertake riskier investments (Coles et al., 2006; Core & Guay, 2002). Thus, we expect to find a positive and significant coefficient on CEO_OWN and VEGA.

Prior literature suggests that CEO duality (where the CEO also serves as the chair of the board) can reduce a board’s CEO monitoring ability. This increases the likelihood of financial misreporting (Dechow et al., 1996; Doyle et al., 2007), which can result in suboptimal investment decisions (Masulis et al., 2007; Yermack, 1996). We therefore posit that CEO duality (CEO_CHAIR) will be associated with a lower likelihood that a CEO will address OC deficiencies.

Determinants of Increased Organizational Capital.

This table reports results from the logistic regressions of the decision to increase organizational capital in year t + 1 of WB firms. INCREASE_OC equals 1 if OC in year t + 1 is greater than that in year t − 1, and 0 otherwise. All variables are standardized to a mean of 0 and a standard deviation of 1. Wald chi-squares are in parentheses.

***, **, and * Indicate statistical significance at the 0.01, 0.05, and 0.10 levels (one-tailed), respectively.

Appendix provides detailed variable descriptions.

LABOR has the largest standardized coefficient. WB firms with higher labor intensity are more likely to increase investment in OC post-allegation. This suggests that employees play an important role in a WB firm’s decision to invest in OC, which reinforces the prediction of prosocial organizational behavior theory. We also find that WB firms with negative stock market reactions, higher long-term institutional ownership, and lower pre-allegation OC levels are more likely to increase OC investment even after controlling for industry and year fixed effects.

Note further that the positive coefficient on MERIT in columns (2) and (6) of Table 7 suggests that credible WB cases lead to increased OC investment. However, when we include both LTIO and MERIT, MERIT remains positive but becomes statistically insignificant. Therefore, credibility is not the primary driver of increased OC investment. This finding complements Kuang et al. (2021), who find that auditors charge WB firms higher fees regardless of WB case credibility. On the other hand, factors such as short-term institutional investors, CEO ownership, CEO risk-taking incentives, CEO duality, and CEO gender do not significantly influence the decision to increase OC post-allegation.

In sum, a firm’s decision to increase OC investment reflects a strategic response aimed at enhancing internal processes. This approach is likely driven by the interests of key stakeholders like long-term institutional investors and employees. It underscores the importance of adopting long-term strategic planning and aligning employee benefits with the company’s overarching objectives to cultivate a responsive and adaptive organizational culture.

Impact on Future External Whistleblowing Incidence

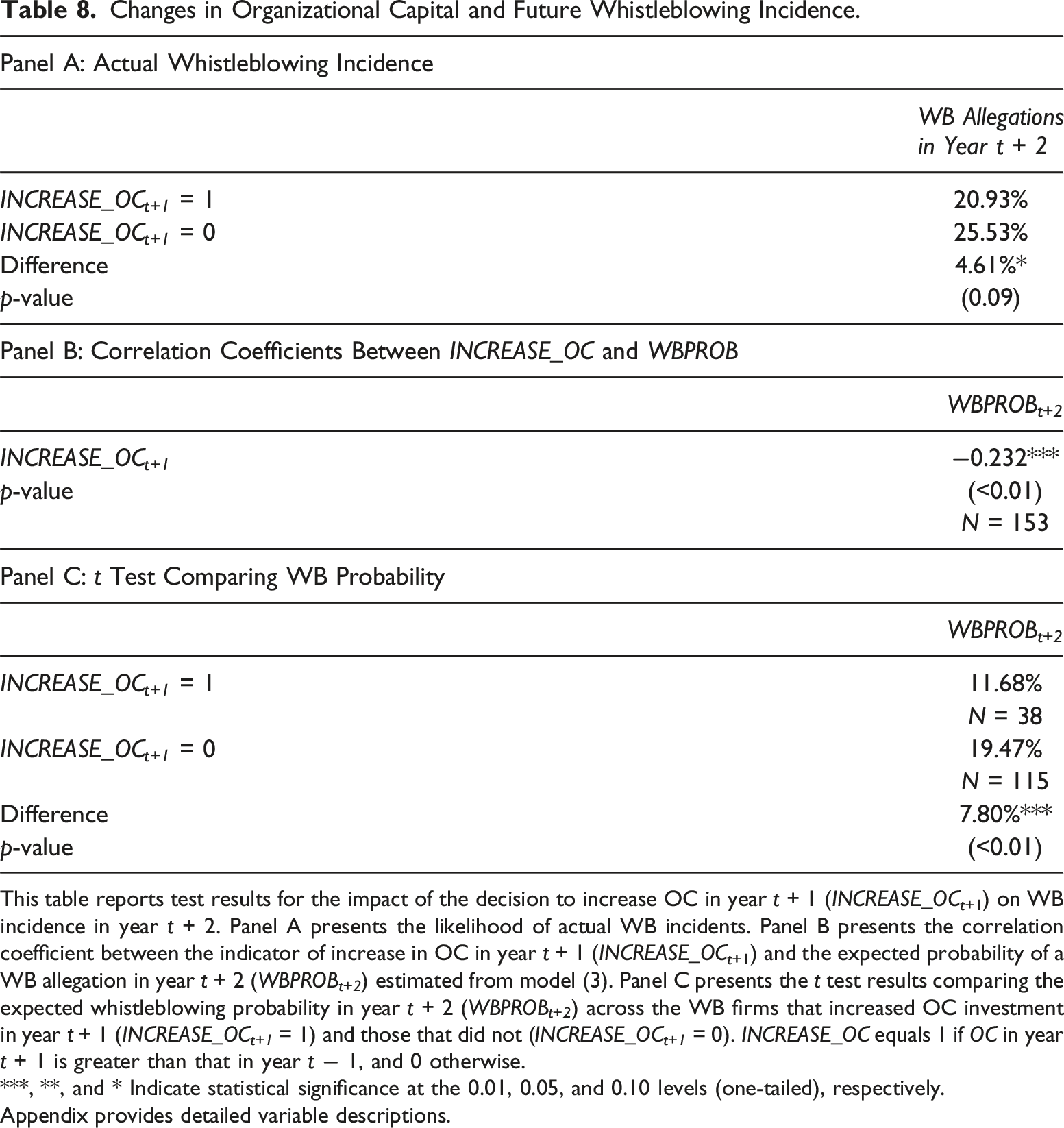

We next examine the relation between increasing OC and future WB incidences post-allegation.

Changes in Organizational Capital and Future Whistleblowing Incidence.

This table reports test results for the impact of the decision to increase OC in year t + 1 (INCREASE_OCt+1) on WB incidence in year t + 2. Panel A presents the likelihood of actual WB incidents. Panel B presents the correlation coefficient between the indicator of increase in OC in year t + 1 (INCREASE_OCt+1) and the expected probability of a WB allegation in year t + 2 (WBPROB t+2 ) estimated from model (3). Panel C presents the t test results comparing the expected whistleblowing probability in year t + 2 (WBPROB t+2 ) across the WB firms that increased OC investment in year t + 1 (INCREASE_OC t+1 = 1) and those that did not (INCREASE_OC t+1 = 0). INCREASE_OC equals 1 if OC in year t + 1 is greater than that in year t − 1, and 0 otherwise.

***, **, and * Indicate statistical significance at the 0.01, 0.05, and 0.10 levels (one-tailed), respectively.

Appendix provides detailed variable descriptions.

In Panel B, the correlation coefficient between INCREASE_OC in year t + 1 and the expected probability of whistleblowing (WBPROB) in year t + 2 estimated from model (3) is −0.232 (p-value <.01).

Panel C shows that WB firms that increase OC (INCREASE_OC = 1) post-allegation (year t + 1) face an average expected probability of WB of 11.68%, compared to 19.47% for those that do not (INCREASE_OC = 1), with the difference being statistically significant at the 1% level. These findings underscore the role of OC investment in reducing the likelihood of future WB allegations, providing support for prosocial organizational behavior theory.

Press and OSHA Subsamples

OSHA whistleblower cases offer protections against wrongful termination, discrimination, and retaliation, often reflecting deeper issues than just financial misconduct. Employees may avoid internal reporting due to distrust, lack of feedback, or fear of retaliation. This highlights potential problems with employee trust and the ethical environment.

To examine differences based on the reporting channel, we reestimate model (4) using the press (101 firm-year observations) and OSHA (841 firm-year observations) subsamples. The (unreported) results show that firms in both subsamples increase investment in OC after an allegation. This supports the conclusion that firms respond by enhancing OC investment regardless of the reporting channel.

Brand Capital Investment

We also examine changes in brand capital investment, which refers to consumer awareness of a company’s products or services. Prior research indicates that brand capital significantly impacts a company’s reputation (Belo et al., 2014). Because WB allegations can harm a firm’s reputation, firms may seek to restore consumer trust post-allegation. We measure brand capital investment as accumulated advertising expenses using the perpetual inventory method, similarly to our OC estimation.

Re-estimating model (4) using brand capital investment as the dependent variable, we find that WB firms tend to have higher brand capital investment than control firms. However, we observe no significant change post-allegation. This may suggest that investment in brand capital is seen as “cosmetic,” and does not directly address the internal deficiencies highlighted by WB issues.

Conclusion

Regulators have long viewed WB as an essential mechanism for detecting and exposing corporate misconduct and fraud. As a result, the topic has garnered increasing research attention in recent years. However, several important WB-related issues remain underexplored. Our study addresses one of these gaps: the impact of external WB allegations on OC investment.

External WB typically occurs when internal systems fail to address employees’ concerns, exposing firms to public scrutiny, reputational damage, and litigation risk. These allegations often signal deficiencies in internal controls, communication, and employee engagement—collectively referred to as OC deficiencies. We hypothesize that firms respond to WB allegations by investing in OC in order to rebuild trust and mitigate future misconduct.

Using a difference-in-differences research design with two unique WB datasets, we find that targeted firms significantly increase OC investments post-allegation. These results are robust to propensity score matching, entropy balancing, and alternative OC measures. We also identify key determinants of OC investment, including labor intensity, negative market reactions, pre-existing OC deficiencies, and long-term institutional ownership. These findings underscore the role of employees as internal monitors, and institutional investors as external monitors, in driving improvements.

Our study has several managerial and policy implications. Managers should prioritize addressing OC deficiencies, empowering employees, and fostering an ethical workplace culture to preempt misconduct and reduce the likelihood of external WB. For policymakers, our results affirm the efficacy of WB regulations, such as SOX §806, in exposing misconduct and prompting firms to implement meaningful changes. Enhancing such regulations could further improve their effectiveness.

While we acknowledge the lack of detailed expenditure data to assess the exact cost of OC improvements, our primary focus is on firms’ behavioral responses. Our findings highlight how WB allegations can lead to substantive organizational changes, reflecting the critical role of WB in improving corporate governance and ethical practices.

Footnotes

Author’s Note

We are grateful for helpful comments from two anonymous reviewers, Linda Myers (Editor), Najah Attig, Narjess Boubakri, Andy Call, Jung Ho Choi, Wolfgang Drobetz, Sattar Mansi, Xinming Li, He Wang, Ying Zheng, and participants at the 11th International Conference of the Journal of International Accounting Research, the 2024 Southwestern Finance Association Annual Meeting, the 2023 American Accounting Association Annual Meeting, the 2023 Financial Management Association Annual Meeting, and the 2022 Southern Finance Association Annual Meeting.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.