Abstract

We investigate if and how a peer’s bankruptcy affects financial reporting by other firms within the industry. Prior research documents that the bankruptcy filing of a peer firm has negative capital market effects on other firms within the industry (lower stock market value and higher cost of debt). We argue that firms within an industry experiencing peer bankruptcies modify their financial reporting to mitigate such negative capital market effects. However, tension arises as to whether such modification is toward more conservative accounting or the opposite. Using a large sample of firms from 1980 to 2018, we find that following a peer firm bankruptcy filing, other firms within the industry exhibit a rise in conditional conservatism in their financial reporting. Our findings are robust to a battery of tests including the exclusion of distressed industries, the 2000 dot-com crash period, and the 2008 financial crisis period as well as employing an alternative proxy for conditional conservatism. The results are not significant for placebo bankruptcies 1 and 2 years before actual bankruptcies. Further analyses show that the spillover effects are more pronounced for firms in homogeneous industries, which exhibit higher leverage, with strong governance mechanisms, and in industries that experience strong market reaction following peer bankruptcy announcements. We also find that the bankruptcy filing of larger and older firms leads to stronger spillover effects.

Introduction

In this study, we investigate how a salient event affecting a firm within an industry shapes the financial reporting strategy of other firms within the same industry. More specifically, we examine the intra-industry spillover effects of bankruptcy announcements on the use of conditional accounting conservatism by other firms. Prior research documents that investors generally react negatively to the announcement of a peer firm bankruptcy. For instance, they reduce stock market prices (Boone & Ivanov, 2012; Hertzel et al., 2008; Lang & Stulz, 1992) and raise the cost of debt (Benmelech & Bergman, 2011; Hertzel & Officer, 2012; Jorion & Zhang, 2007) of other firms within the industry, thus expressing their doubts regarding the surviving firms’ going concern prospects. Moreover, firms within an industry alter their behavior following a bankruptcy announcement by a peer firm by reducing their capital expenditures (Garcia-Appendini, 2018) or increasing their cash holdings (Le, 2012). Via financial reporting, firms may also signal to the market that their peer’s bankruptcy is an idiosyncratic event rather than a systematic industry-wide phenomenon. Such a signal could come in the form of more conservative reporting (Black et al., 2022) to show a financial situation that is robust enough to absorb shocks or in the form of income-increasing earnings management (Kedia et al., 2015) to enhance their financial picture.

A natural question thus arises as to if and how firms use financial reporting to mitigate the negative impact of an industry peer’s bankruptcy. Our focus on financial reporting is warranted considering its pivotal role in “instilling investor confidence” and enhancing market liquidity and efficiency (Levitt, 1998). One potential answer to this question is that managers subject to more governance oversight by a firm’s owners and directors choose a financial reporting strategy that provides more verifiable accounting numbers, thereby reducing uncertainty and alleviating the information asymmetries between insiders and outsiders. Such a strategy also signals that their peer’s bankruptcy does not have an impact on their financial situation. In this regard, previous studies suggest that conditional accounting conservatism is an effective reporting strategy for reducing information asymmetry and reassuring outsiders (e.g., Francis et al., 2013; Garcia Lara et al., 2014; Kim & Zhang, 2016; LaFond & Watts, 2008; Watts, 2003a, 2003b). Giesecke (2004) shows that spillover effects are reduced with greater transparency.

Furthermore, there is evidence that conditional conservatism increases debt contracting efficiency and reduces debt costs (Ahmed et al., 2002; Ball et al., 2008; Beatty et al., 2008; Ruch & Taylor, 2015; Watts, 2003a). Hence, conditional conservatism could serve as a tool to fight off increasing debt costs brought on by a peer’s bankruptcy, especially for firms with high leverage. A peer firm bankruptcy announcement, as a negative event, may also create a “deterrent” effect within an industry (e.g., Ashraf, 2022). That is, a peer firm bankruptcy may serve as a salutary lesson and reminder of the importance of conservatism in reducing distress risk, thereby enticing surviving firms to become more conservative. Hence, managers may consider raising the level of conditional conservatism in their financial reporting to counter any negative outcome, such as the higher cost of debt following a peer firm’s bankruptcy. Therefore, we hypothesize that there is a spillover effect from a peer firm bankruptcy with firms within that industry exhibiting a higher level of conditional conservatism following the bankruptcy. We also expect that such spillover effect is amplified for firms with strong governance oversight and high leverage.

However, there is some tension in our prediction. For instance, Gigler et al. (2009) and Guay and Verrecchia (2006) argue that conditional conservatism may lead to informational inefficiency by sending “false alarms.” Hence, an alternative answer is that managers may recognize gains more quickly to avoid sending “false alarms” in times of uncertainty following a peer firm bankruptcy announcement. Managers may also manipulate earnings upward to portray a better picture of a firm’s underlying economic health. For instance, Kedia et al. (2015) note that firms manage their earnings upward following a peer firm’s restatement.

To examine how a peer firm’s bankruptcy filing shapes the financial reporting strategy of other firms within an industry, we employ Basu’s (1997) model of conditional conservatism, which is widely used in the literature. Using the Lopucki Bankruptcy Research Database and Audit Analytics, we identify 2,077 corporate bankruptcies in non-financial industries that were filed between 1980 and 2018. Consistent with our hypothesis, we find that firms generally exhibit a higher degree of conditional conservatism following a peer firm’s bankruptcy announcement.

Furthermore, we document that the spillover effects of a peer firm bankruptcy filing are more pronounced among firms with stronger corporate governance as measured by the percentage of dedicated and quasi-indexer institutional ownership as well as the percentage of independent directors. In addition, we find that the spillover effects of peer firm bankruptcy are more prominent in homogeneous industries. In these industries, firms tend to track policies of each other and learn from the experience of their peers, implying that a peer firm bankruptcy may serve as a beneficial reminder of the importance of conditional conservatism in minimizing bankruptcy risk. We also observe that the effects of a peer firm’s bankruptcy announcement are more salient among highly leveraged firms. Furthermore, we find that the spillover effects of bankruptcy are more pronounced when the bankrupt firm is either larger or older than most firms in the industry and when surviving firms experience a strong market reaction to the peer firm bankruptcy announcement.

To rule out the possibility that industry conditions lead to both the peer firm bankruptcy filing and higher conservatism in reporting among non-bankrupt firms, we replicate our main analysis in subsamples of non-distressed industries, with similar results. Bankruptcy filings are concentrated during the 2000 dot-com crash and the 2008 financial crisis. We find that results continue to hold after excluding the two crisis periods (i.e., 2000–2004 and 2007–2010). We perform two placebo tests (falsification tests) by examining the intra-industry spillover effects of placebo bankruptcies 1 and 2 years before the actual event. We do not find evidence of the spillover effects of placebo bankruptcies. We also confirm the association between bankruptcy spillover effects of peer firms and conditional conservatism by employing Givoly and Hayn’s (2000) and Khan and Watts (2009) models of conditional conservatism.

Our study resembles but is different from Sun et al. (2022) who observe that firms become more conservative in financial reporting following a peer firm delisting from Chinese stock exchanges. Bankruptcies and delistings are distinct events. A delisting often happens when a firm is acquired by another firm (Brown et al., 2023). The findings of Sun et al. (2022) may be more related to studies on the reactions of firms to takeovers of peers. We examine U.S. companies, while Sun et al. (2022) examine an emerging economy, China. While institutional investors dominate U.S. stock markets, individual investors play a crucial role in Chinese markets. Ex-ante, it is unclear how institutional investors may influence the financial reporting policy of a firm following the bankruptcy of a peer firm. On the one hand, they may understand the need for conservative reporting in times of uncertainty caused by a bankruptcy announcement by a peer company. Hence, they may demand conservative reporting. On the other hand, they may be satisfied with the current level of conservatism, and since they have access to private information (Piotroski & Roulstone, 2004), they may not demand more conservatism. Thus, in our view, Sun et al.’s (2022) findings cannot simply be extended to U.S. companies.

Our study makes three main contributions to prior research. First, this article adds to the literature on the spillover effects of bankruptcy announcements in terms of the surviving firms’ actions to alleviate stakeholders’ concerns. Prior studies document that a peer firm bankruptcy filing influences firm value (e.g., Lang & Stulz, 1992), cost of debt (e.g., Benmelech & Bergman, 2011; Hertzel & Officer, 2012), investments (Garcia-Appendini, 2018), and cash holding policies (Le, 2012). However, there is scant evidence regarding the effects of such spillovers on firms’ financial reporting strategies. This study extends this literature by investigating how managers use financial reporting strategies to mitigate stakeholders’ negative sentiments associated with bankruptcy events.

Second, our study contributes to the literature on organizational learning. The organization learning literature in accounting mainly focuses on how disclosures reveal information that could be exploited to the detriment of the firm by competitors (for example, Dou et al., 2023; Roychowdhury et al., 2019). However, there is little research on the salutary effects of peer-related negative events. Two notable exceptions are Ashraf (2022) and Donelson et al., (2022) who document that after peer data breaches and litigations, firms alter their internal control and voluntary disclosure policies, respectively. 1 Our work complements and extends this line of research with respect to how peer firm bankruptcy may affect peer firms’ financial reporting policies.

Third, our study contributes to the literature that examines the determinants of accounting conservatism (e.g., Ahmed et al., 2002; Ahmed & Duellman, 2007; Ramalingegowda & Yu, 2012). Specifically, this study contributes to a subset of the literature that analyzes how different factors and events, such as accounting restatements (Ettredge et al., 2012), elections (Dai & Ngo, 2021), changes in investor sentiment (Ge et al., 2019), and acquisition of a peer firm(Chen et al., 2022), shape the degree of conditional conservatism. This study adds to that literature by showing that the bankruptcy of a peer firm may also lead to a higher degree of conditional conservatism in financial reports.

The article proceeds as follows. In the second section, we develop our empirical research question, and in the third section, we discuss the empirical model. In the fourth section, we introduce our sample and report the descriptive analysis and main study findings. In the fifth section, we report additional analysis results. We conclude in the sixth section.

Background and Hypothesis Development

Bankruptcy Spillover Effects: Prior Research

There is extensive evidence that a firm’s filing for bankruptcy within a given industry has serious economic intra-industry spillover effects. For instance, Lang and Stulz (1992) show that a bankruptcy announcement within an industry reduces the stock market value of a portfolio of competitors by 1%. They state that one potential explanation could be that the bankruptcy announcement raises outsiders’ perception of the risk carried by the same-industry firms even when they are economically healthy. This view is consistent with research showing that after a firm-specific event, investors update their beliefs regarding other firms’ prospects (Collin-Dufresne et al., 2002; Giesecke, 2004).

Furthermore, several studies document the spillover effect of bankruptcy on the cost of financing. For instance, Benmelech and Bergman (2011) find that bankruptcy filings materially affect the cost of debt financing of same-industry firms by reducing their collateral’s value. Hertzel and Officer (2012) investigate how the bankruptcy of rivals influences the terms of new and renegotiated bank loans. They find increases in spreads on new and renegotiated corporate loans within the 2 years that follow bankruptcy filings by industry rivals.

In an analytical study, Giesecke (2004) shows that investors’ lack of complete information is a major issue in the spillover effects of a salient event. His results also indicate that greater information transparency reduces the possibility of spillover effects due to incomplete information. Therefore, following a peer firm bankruptcy announcement, we can expect managers to choose a financial reporting strategy that increases transparency and reduces information asymmetry.

Bankruptcy Spillover Effect and Conditional Conservatism

There is evidence that conditional accounting conservatism alleviates information asymmetry (Garcia Lara et al., 2014; Ruch & Taylor, 2015). More formally, conditional accounting conservatism restrains managers in their ability to overstate accounting numbers and hide bad news and thus potentially reduces information asymmetry (Kim & Zhang, 2016; Watts, 2003a, 2003b). Consistent with this perspective, Garcia Lara et al. (2014) document that conditional accounting conservatism reduces information asymmetries. Furthermore, LaFond and Watts (2008) observe that firms report more conservative earnings following increases in information asymmetries. They theorize that conditional accounting conservatism is a strategy to mitigate value reduction due to the information asymmetries between managers and investors. They further argue that investors appreciate the verifiability of accounting information. 2 Thus, it is reasonable to expect that firms use conditional conservatism to reduce information asymmetry and mitigate the negative impact of a peer firm’s bankruptcy on their value. Investors may also demand conditional accounting conservatism to have verifiable information that reassures them about the firm’s current operations. Hence, we expect that among firms within industries with a peer firm bankruptcy, the level of conditional conservatism in financial reporting is amplified by strong governance oversight by their board and investors.

As conditional accounting conservatism reduces information asymmetries between firms and debtholders, it may represent an efficient mechanism for debt contracting (Ahmed et al., 2002; Liu & Magnan, 2016; Ruch & Taylor, 2015; Watts, 2003a). Given that the bankruptcy of a firm leads to tighter credit policies by debtholders of competing firms (e.g., Hertzel & Officer, 2012), we expect that firms will use conditional conservatism to reduce information asymmetries between managers and debtholders, and thus, lower their cost of debt. Since the news of bankruptcy makes debtholders wary of other firms within the same industry, they may also ask for more conditional conservatism from firms that engage in new debt negotiations (or that renegotiate current debt).

In an analytical study, Gox and Wagenhofer (2009) show that accounting conservatism is an optimal policy for a financially constrained firm that pledges assets to raise debt capital to finance a risky project. In this regard, there is widespread evidence that accounting conservatism can mitigate the negative effect of a firm facing financial difficulties. For instance, Biddle et al. (2022) find that accounting conservatism reduces bankruptcy risk by alleviating information asymmetry between firms and debtholders; it also helps firms hold more precautionary cash. Donovan et al. (2015) find that firms with a high degree of accounting conservatism have shorter bankruptcy periods and a greater likelihood of emerging from bankruptcy. They also find that creditors of firms with conservative reporting have higher recovery rates. If a peer firm bankruptcy filing serves as a salutary lesson and reminder of the importance of conditional accounting conservatism in reducing the likelihood of bankruptcy and financial distress, firms may use more conditional accounting in reporting. Prior research also documents similar deterrent effects following a negative event in an industry (e.g., Ashraf, 2022; Donelson et al., 2022). Given that a bankruptcy is a significant event, it is reasonable to expect that non-filing firms may become more conservative to reduce the risk of future financial distress.

In light of the above discussion, we propose the following hypothesis:

In addition, we expect that strong governance oversight from owners and the board as well as higher leverage further raise the level of conditional conservatism among firms subjected to a spillover effect from a peer firm bankruptcy within their industry.

Nevertheless, a firm’s bankruptcy filing may not necessarily lead to an increase in conditional conservatism in other firms, thus creating some tension as to the testing of our hypothesis. For instance, Kedia et al. (2015) suggest that firms engage in earnings management after a peer firm discloses a restatement, which contrasts with the notion of a deterrent effect that leads to governance or financial reporting improvements. Although numerous studies provide evidence that conditional accounting conservatism results in efficient debt contracting and that debtholders demand conditional conservatism, Gigler et al. (2009) analytically show that conservatism could result in inefficient debt contracting by increasing the probability of sending “false alarms.” They also argue that reported losses are less informative than reported gains under a conditional conservative system. Therefore, following a bankruptcy filing and the subsequent increase in financing costs, non-filing firms may be less conservative to avoid sending false alarms. Such an action could potentially increase debt contracting efficiency. The other possibility is that managers may more quickly recognize gains than losses to boost earnings and portray a better picture of the firm’s current performance. Several studies show that firms engage in upward earnings management to sustain or improve their image (e.g., Beneish et al., 2012; Garcia Lara, Osma, & Neophytou, 2009; C. Lin et al., 2014; Rosner, 2003; S. Zhang et al., 2021). Moreover, if conservatism acts as a substitute rather than a complementary governance mechanism to alleviate information asymmetries (Francis et al., 2013), a peer firm bankruptcy may not imply more conservatism among firms with strong governance oversight.

Method

Empirical Model and Variables

We employ Basu’s (1997) model to examine the influence of bankruptcy spillover on same-industry firms. Basu’s (1997) model of accounting conservatism is widely used to study the determinants of conditional accounting conservatism (e.g., Ahmed & Duellman, 2013; Ball et al., 2008; Basu & Liang, 2019; Ettredge et al., 2012; LaFond & Roychowdhury, 2008; J. Zhang, 2008). The intuition behind Basu’s (1997) model of conservatism is that stock returns incorporate all economic news; therefore, stock returns can be used to proxy for good or bad economic news. Under conditional conservatism, the recognition of economic bad news (losses) is timelier than economic good news (gains). Thus, it is expected that the association between reported earnings and bad economic news (measured by negative stock returns) will be higher than the association between reported earnings and good economic news. Basu’s (1997) model is as follows:

where

To examine bankruptcy spillover, we extend Basu’s (1997) model by adding control variables and Spillover which is an indicator variable that takes the value of one for a firm if there is a bankruptcy in the 4-digit Standard Industrial Classification (SIC) industry in year t as follows:

Our coefficient of interest is

Sample

Data emanates from several different sources. The primary data are from Compustat’s Annual North America database between 1980 and 2018. Data on buy-and-hold stock returns are obtained from CRSP. We employ two databases, the Lopucki Bankruptcy Research Database and Audit Analytics, to identify bankruptcy filings. Information for institutional ownership is obtained from Thomson Institutional Holdings, which contains institutional quarterly shareholding data from 13-F filings with the SEC. The institutional investor’s classification data are obtained from Professor Brian Bushee’s personal website. 3 Data on boards of directors are generated from Boardex. We find 2,077 bankruptcy filings of non-financial public firms from 1980 to 2018. Following previous studies (e.g., Lang & Stulz 1992), we examine the spillover effect of bankruptcies on the same 4-digit SIC industry firms. We find 1,395 unique industry (4-digit SIC) years in which at least one firm filed for bankruptcy.

This study is entirely based on U.S. firms, so we exclude non-U.S. firm years. We exclude observations related to firms that are not listed on NYSE, AMEX, or NASDAQ. We remove firm-year observations related to financial industries (SIC codes 6000–6999) because they are subject to different regulations and thus might behave differently in response to bankruptcy announcements. We also drop all observations related to bankrupt firms. We exclude firm years with missing data items that are required to calculate the variables in Equation 2. To mitigate the influence of extreme observations, all continuous regression variables are truncated at the upper and lower 1 percentile. The final sample comprises 88,384 firm-year observations.

Results

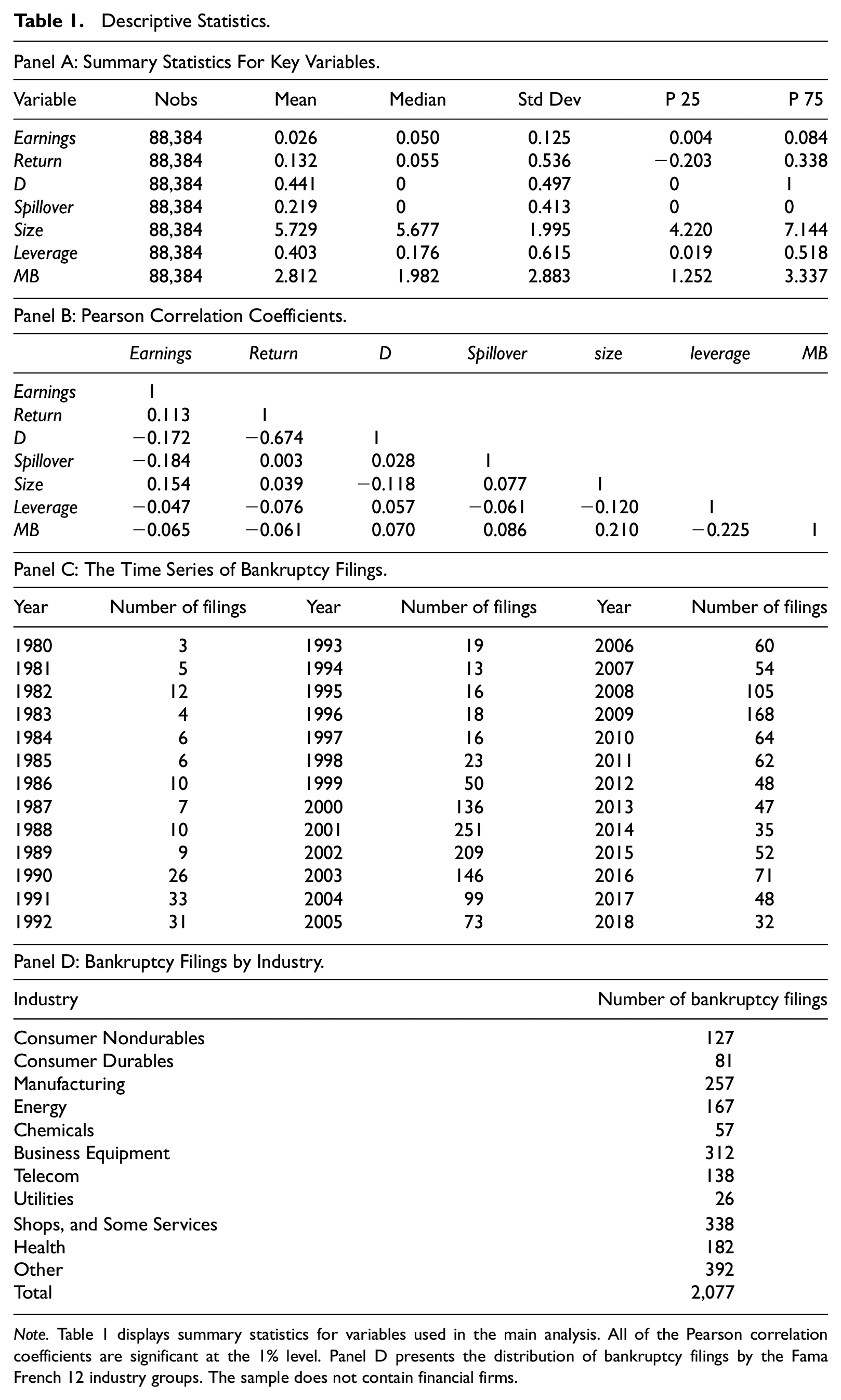

Descriptive Statistics

Panel A of Table 1 displays the descriptive statistics for the variables employed to estimate Equation 2. The mean of Return (annual buy and hold returns) is 0.132, which is similar to past studies (e.g., 0.121 reported in Garcia Lara, Osma, and Penalva (2009) and 0.163 documented in LaFond and Roychowdhury (2008)). The mean of

Descriptive Statistics.

Note. Table 1 displays summary statistics for variables used in the main analysis. All of the Pearson correlation coefficients are significant at the 1% level. Panel D presents the distribution of bankruptcy filings by the Fama French 12 industry groups. The sample does not contain financial firms.

Panel B of Table 1 presents the Pearson correlations between variables in Equation 2. All correlations are significant (p<.01) but none exceeds a level that would suggest potential multicollinearity (i.e.,>80%). Panel C of Table 1 presents the time series of bankruptcy filings. Bankruptcies are more frequent in economic crisis periods (i.e., the dot-com crash period and the financial crisis of 2007–2009). Panel D of Table 1 summarizes the bankruptcy filings distribution across industry classifications. To conserve space, bankruptcy filings are classified using the 12 Fama and French (1997) industry groups. We exclude financial industries.

Main Findings

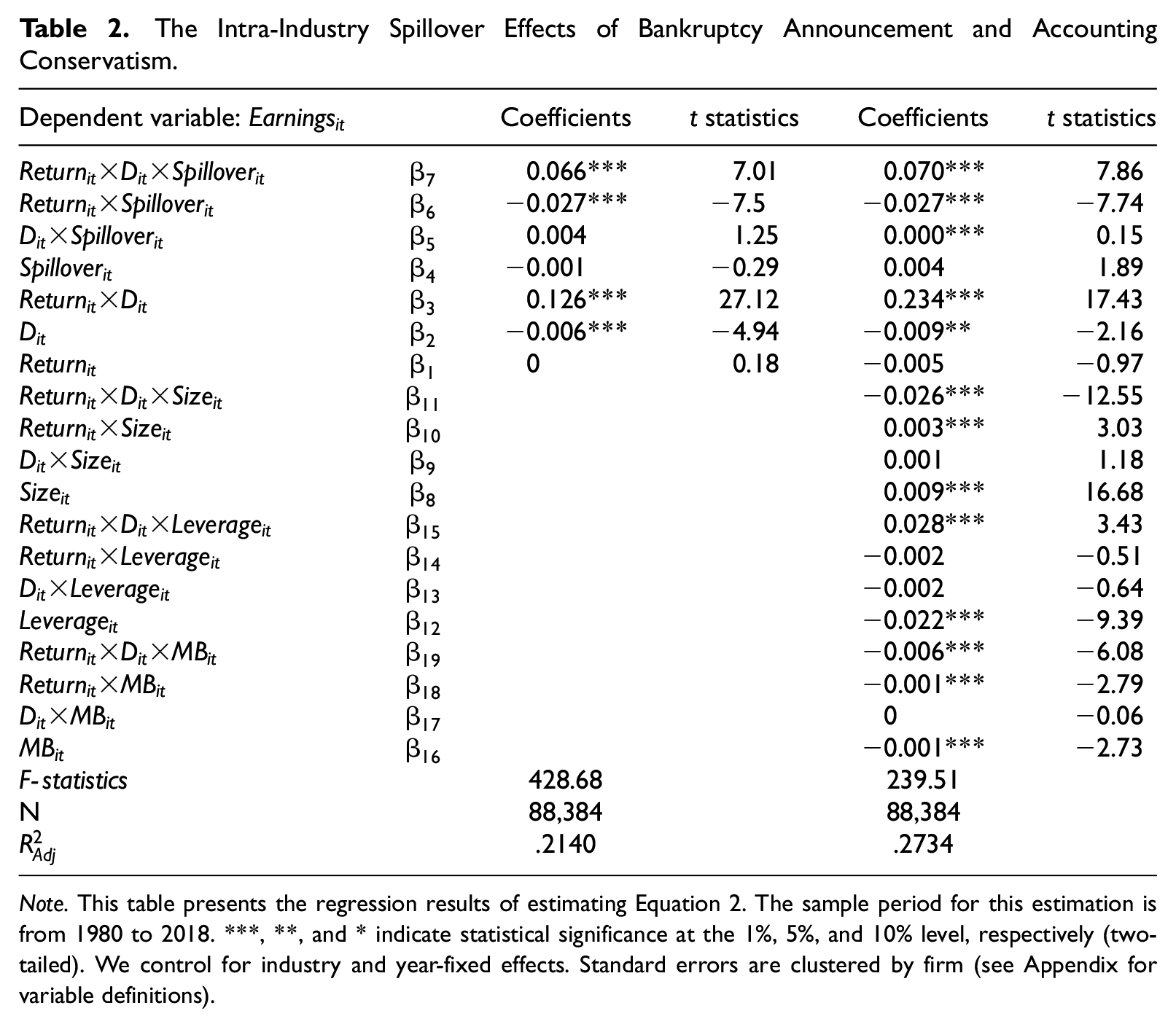

Table 2 presents the results of estimating Equation 2. Consistent with our hypothesis,

The Intra-Industry Spillover Effects of Bankruptcy Announcement and Accounting Conservatism.

Note. This table presents the regression results of estimating Equation 2. The sample period for this estimation is from 1980 to 2018. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

Other coefficient estimates are also consistent with prior studies on conditional accounting conservatism (e.g., Ahmed & Duellman, 2013). The coefficient on

The Role of Corporate Governance on the Spillover Effect of a Peer Bankruptcy

The literature suggests that strong corporate governance mechanisms are associated with higher conditional conservatism in financial reporting (e.g., Ahmed & Duellman, 2007; Garcia Lara, Osma, & Penalva, 2009). Corporate governance mechanisms demand conditional accounting conservatism because verifiable information allows corporate directors to more effectively monitor and advise managers, thus reducing agency costs (Ahmed & Duellman, 2007). Conditional accounting conservatism improves the efficiency of the compensation mechanism by providing more verifiable information (Watts, 2003a).

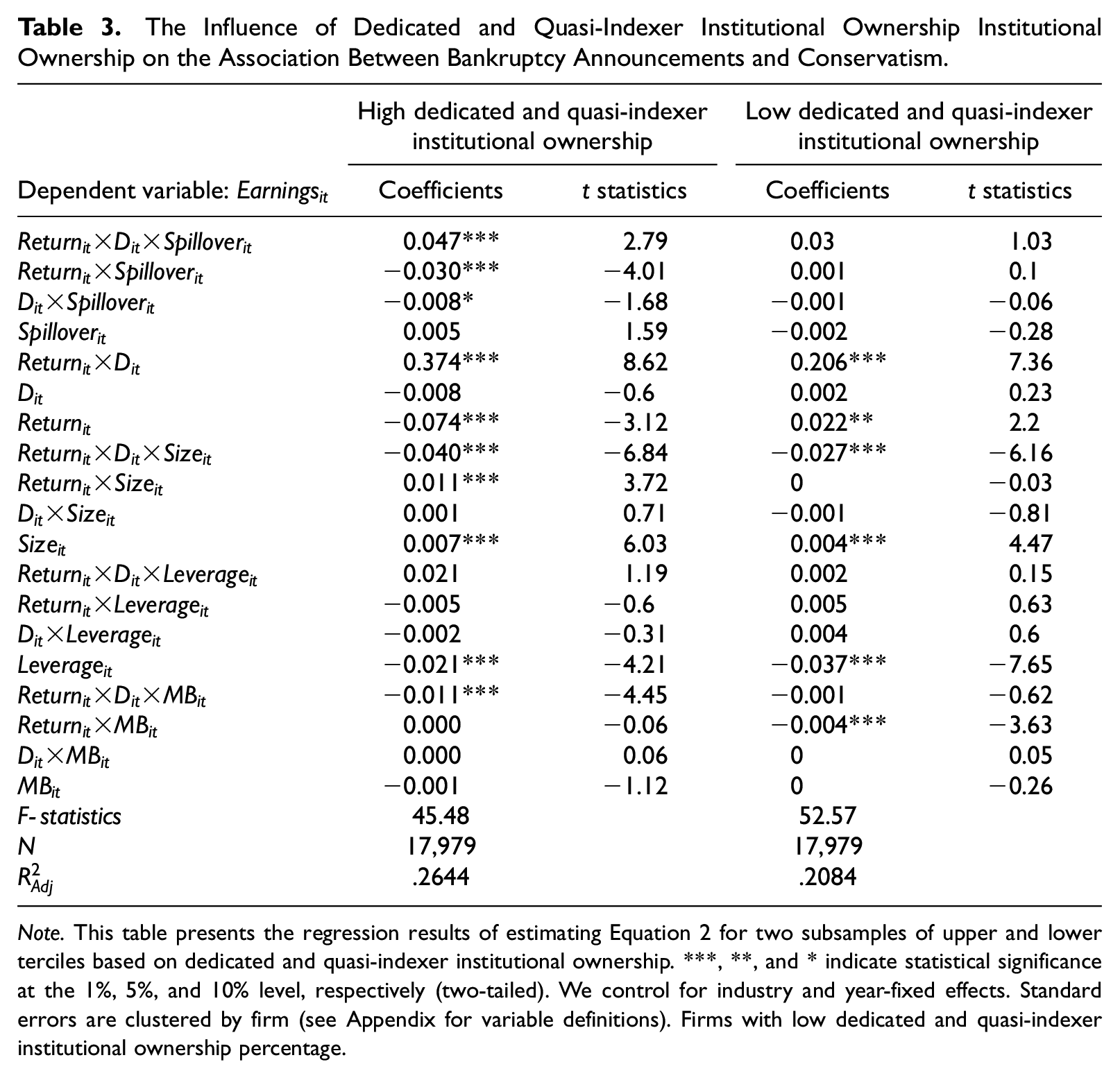

We examine how corporate governance mechanisms influence the spillover effects of bankruptcy filings on same-industry conservative reporting. We focus on institutional ownership and on the board of directors’ characteristics as our two main corporate governance mechanisms. Ramalingegowda and Yu (2012) contend that institutional shareholders have a better understanding of accounting numbers than individual investors and are aware of the benefits of conditional accounting conservatism for monitoring managers. Therefore, they demand a higher degree of conservatism in financial reporting to facilitate the monitoring of managers. Consistent with their hypothesis, they find a positive association between institutional ownership and conditional accounting conservatism. If news of a peer firm bankruptcy makes institutional shareholders wary of the firm, they may demand more conditional conservatism to help them monitor the CEO. Ahmed and Duellman (2007) examine the association between the characteristics of boards of directors and conditional accounting conservatism. They find that the percentage of outside (inside) directors is positively (negatively) related to the degree of conditional conservatism in financial reporting.

To examine the potential impact of governance mechanisms on the association between bankruptcy announcements and conditional accounting conservatism, we create subsamples based on the level of dedicated and quasi-indexer institutional ownership,

5

and percentage of board independence. Table 3 presents the results for the high and low dedicated and quasi-indexer institutional ownership subsamples, which are the highest and lowest terciles of dedicated and quasi-indexer institutional ownership, respectively. The coefficient on the three-way interaction term,

The Influence of Dedicated and Quasi-Indexer Institutional Ownership Institutional Ownership on the Association Between Bankruptcy Announcements and Conservatism.

Note. This table presents the regression results of estimating Equation 2 for two subsamples of upper and lower terciles based on dedicated and quasi-indexer institutional ownership. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions). Firms with low dedicated and quasi-indexer institutional ownership percentage.

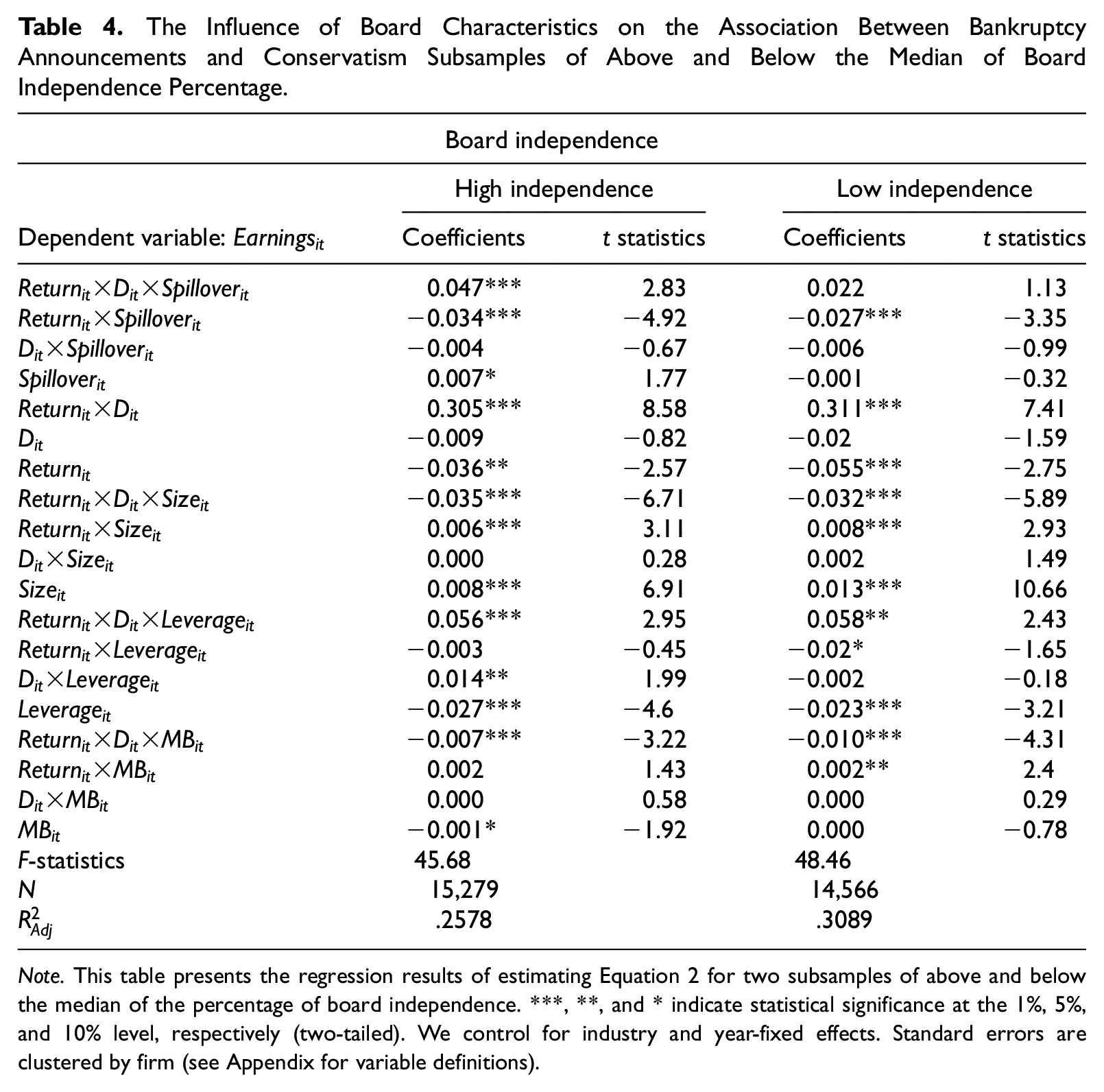

Table 4 presents the results for subsamples of high and low board independence (split as firms above and firms below the median of board independence percentage). The coefficient on

The Influence of Board Characteristics on the Association Between Bankruptcy Announcements and Conservatism Subsamples of Above and Below the Median of Board Independence Percentage.

Note. This table presents the regression results of estimating Equation 2 for two subsamples of above and below the median of the percentage of board independence. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

Overall, consistent with our prediction, strong governance oversight via owners or the board of directors accentuates the spillover effects of a peer bankruptcy by driving a firm to raise its level of conditional conservatism.

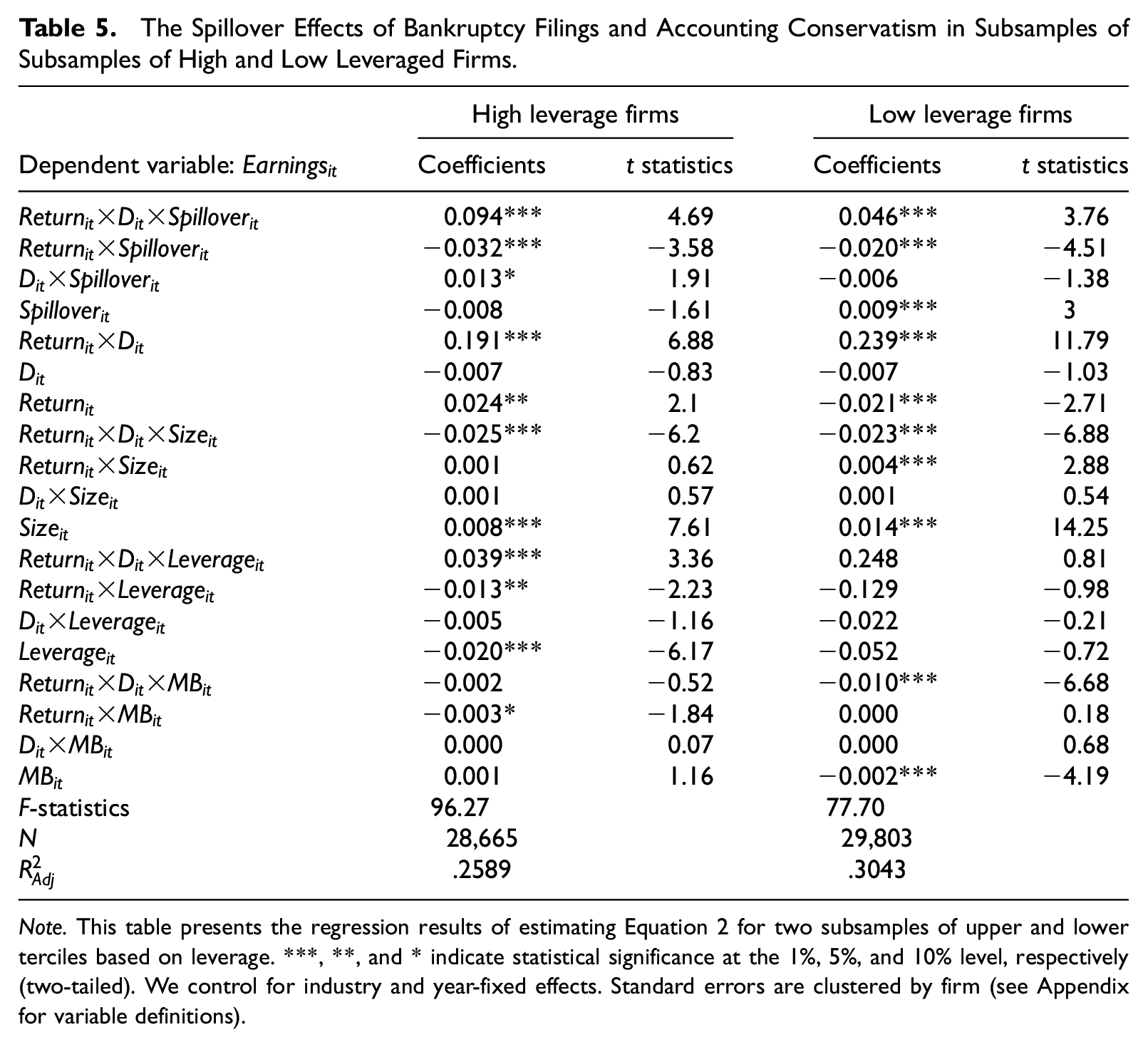

The Role of Leverage in the Spillover Effect of a Peer Bankruptcy

The high demand for accounting conservatism from debtholders is well documented in the literature (e.g., Ahmed et al., 2002; Ball et al., 2008; Beatty et al., 2008). Opler and Titman (1994) observe that when an industry is in a downturn, highly leveraged firms suffer more from market share declines than their low-leveraged rivals. Lang and Stulz (1992) find that the adverse spillover effects of bankruptcy filings on market value are higher among firms with high leverage. The literature on the spillover effects of bankruptcy documents higher costs of debt following a bankruptcy announcement (Benmelech & Bergman, 2011; Hertzel & Officer, 2012; Jorion & Zhang, 2007). We hypothesize that bankruptcy filings make debtholders wary of other firms in the same industry, and they demand more conservatism in financial reporting. Consequently, highly leveraged firms might exhibit high levels of accounting conservatism.

To investigate whether firm leverage affects the intra-industry spillover effects of bankruptcy on financial reporting, we create a subsample of high-leverage firm years, which consists of firm years in the highest tercile of the leverage distribution, and a subsample of low-leverage firm years, which are those in the lowest tercile. Table 5 presents the regression results for the subsamples of high and low-leverage firms. While the coefficient on

The Spillover Effects of Bankruptcy Filings and Accounting Conservatism in Subsamples of Subsamples of High and Low Leveraged Firms.

Note. This table presents the regression results of estimating Equation 2 for two subsamples of upper and lower terciles based on leverage. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

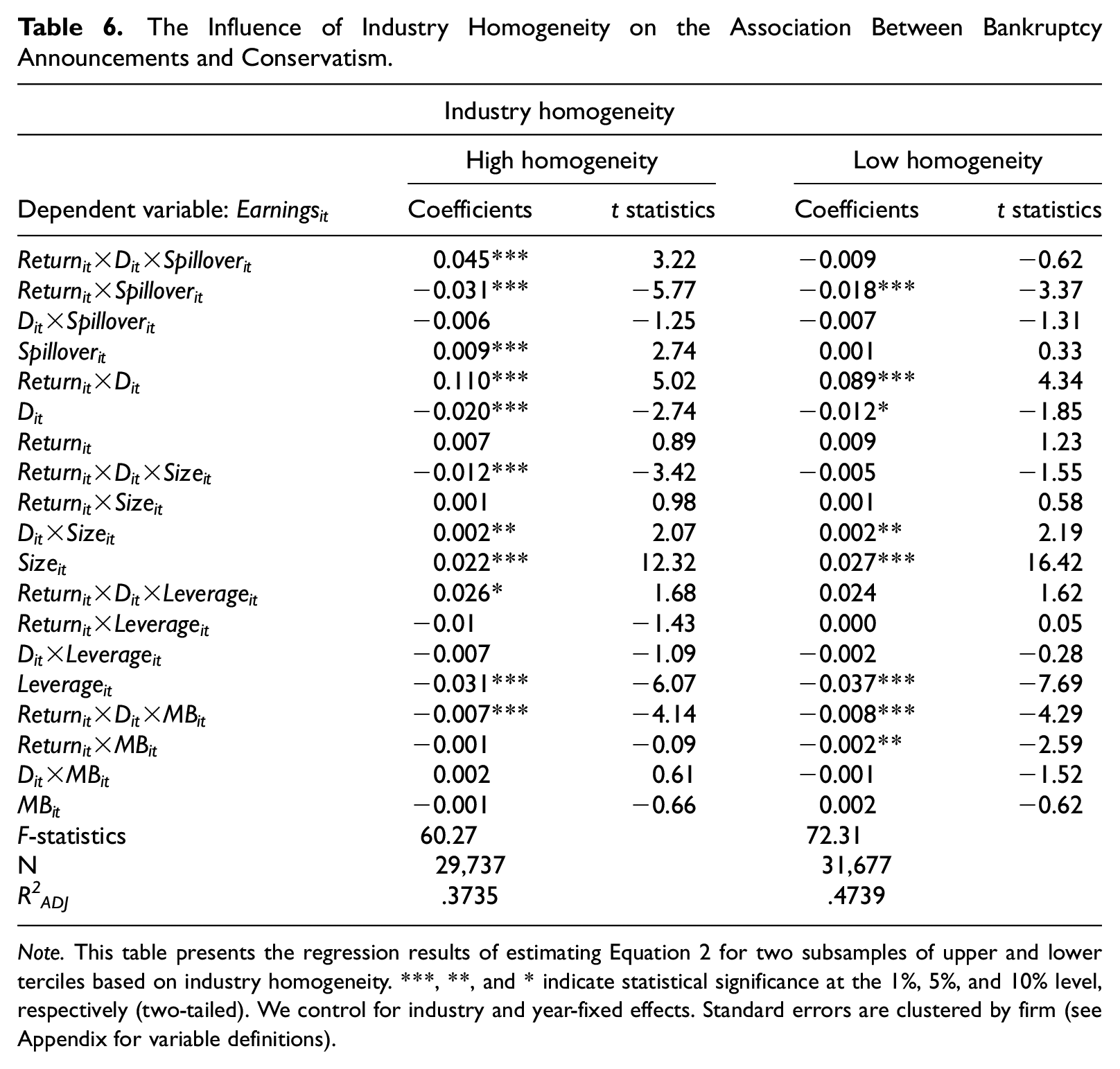

The Role of Industry Homogeneity

We argue, and so far provide empirical evidence, that investors demand more conditional conservatism following a peer firm bankruptcy announcement. However, a peer firm bankruptcy announcement may serve as a wake-up call to non-bankrupt firms and may affect their corporate policies as they do not wish to experience such a traumatic event. Prior research also documents that following peer negative events such as peer data breaches (Ashraf, 2022) and peer securities litigation filings (Donelson et al., 2022), firms take actions to reduce the likelihood of such events occurring. It is reasonable to assume that firms take steps to reduce bankruptcy risk in the wake of a peer firm bankruptcy filing. Prior studies find that conditional accounting conservatism helps firms that are financially in distress (Francis et al., 2013), reduces bankruptcy risk (Donovan et al., 2015), and helps firms emerge from bankruptcy (Biddle et al., 2022). The experience of a peer firm bankruptcy may thus serve as a salutary reminder and lesson on the importance of conditional conservatism in minimizing bankruptcy risk. We consider the salutary impact of a peer firm bankruptcy as the learning channel that leads to more conditional conservatism.

The theory of homophily, the tendency to learn from those with similar characteristics in individuals, teams, and organizations, has been widely recognized and studied in psychology, sociology, economics, and organizational behavior (e.g., Backmann et al., 2015; Ertug et al., 2022; Golub & Jackson, 2012; G. Peng & Mu, 2011). It is widely accepted that in the organizational learning literature, knowledge transfer, learning from experience, and imitation are all types of learning that occur when firms are similar to each other and related to one another (e.g., Boschma & Frenken, 2011; Luo & Deng, 2009; Raff & Verwijmeren, 2015). In other words, firms that are homogeneous track each other’s policies to improve their performance. For instance, there is some evidence that the R&D investment policy of a firm is affected by the policies of similar firms (Z. Peng et al., 2021). Furthermore, Raff and Verwijmeren (2015) find that firms tend to learn more about the investment strategy of their peers in homogeneous industries.

We expect the salutary impact of a peer firm bankruptcy filing to be more pronounced in homogeneous industries than in heterogeneous industries. To test this prediction, we created subsamples of highly homogeneous and low homogeneous industries. Industry homogeneity refers to the degree of similarity or correlation between individual firm returns and an industry index when controlling for market returns. It is calculated as the average partial correlation coefficient between a firm’s returns and an equally weighted industry index while holding market returns constant (Faleye et al., 2013; Naveen, 2006). Essentially, it measures how closely the performance of firms within the same industry aligns with the overall performance of that industry, independent of broader market trends.

To investigate how industry homogeneity influences the intra-industry spillover effects of bankruptcy, we re-run Equation 2 in subsamples of high- and low-homogeneous industries. More specifically, we split the sample into terciles based on industry homogeneity. Table 6 presents the results for the highest and lowest terciles of industry homogeneity. Results indicate that bankruptcy announcements induce conditional conservatism only in the subsample of highly homogeneous industries (0.045; p<.01). A Chow test also validates that the spillover effect of a peer firm bankruptcy filing is more pronounced among highly homogeneous industries.

The Influence of Industry Homogeneity on the Association Between Bankruptcy Announcements and Conservatism.

Note. This table presents the regression results of estimating Equation 2 for two subsamples of upper and lower terciles based on industry homogeneity. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

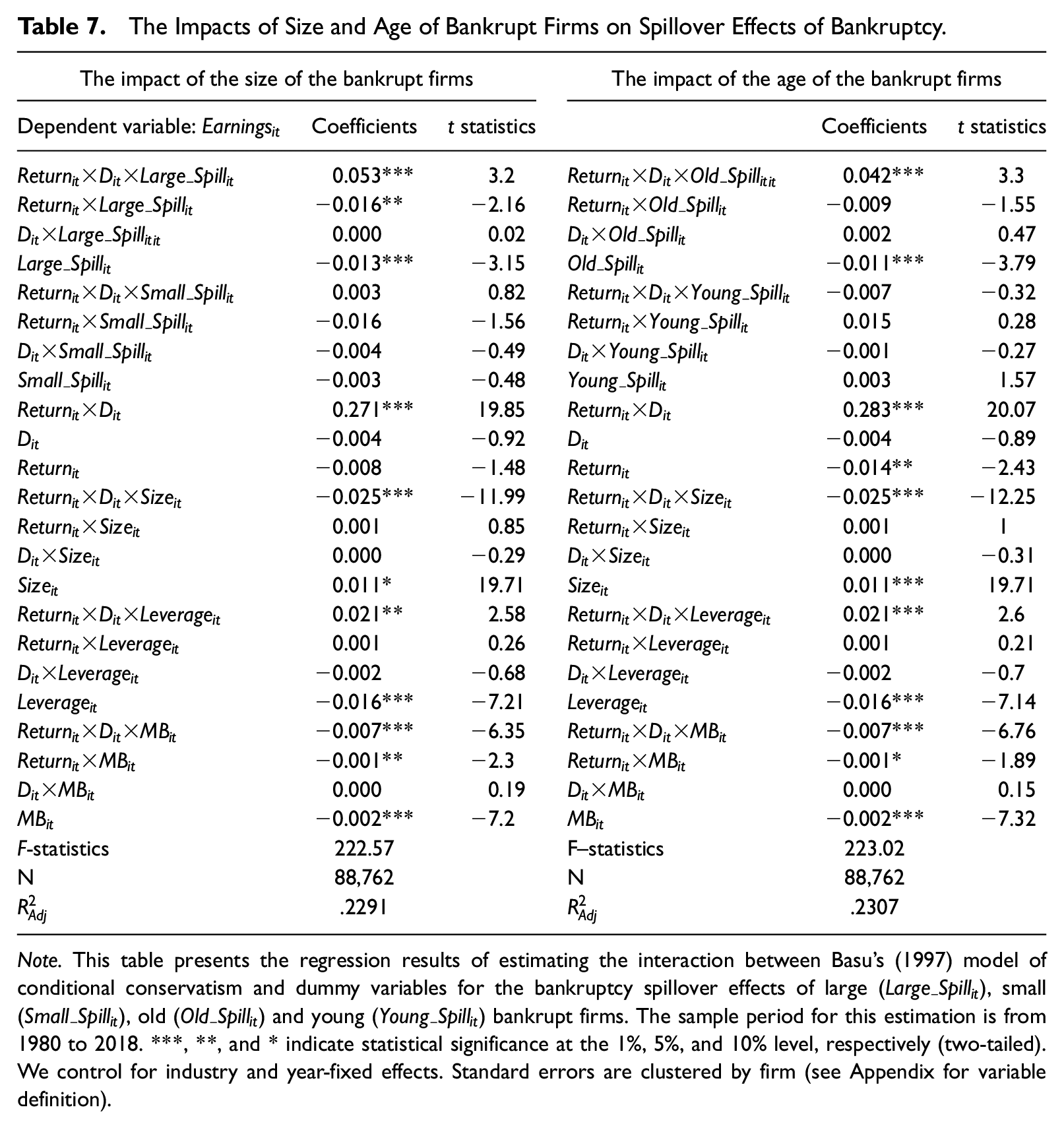

The Role of Size and Age of Bankrupt Firms

To shed more light on the impact of peer firm bankruptcy on conditional accounting conservatism, we investigate whether the degree of conservatism varies with the significance of peer firm bankruptcy announcements. It is reasonable to argue that the bankruptcy of a firm that is larger than most firms in the sector may have a significant impact on the policies of firms within that sector. Conversely, the news of the bankruptcy of a peer firm that is smaller than most firms in the industry may have little or no spillover impact on the industry. Older firms also tend to be larger and are often viewed as the flagships of the industry. Thus, bankruptcy filings by older firms will result in stronger spillover effects than bankruptcy filings by younger firms. Therefore, we predict that bankruptcy announcements by larger or older firms have a greater spillover effect than bankruptcy announcements by smaller or younger firms. To examine our prediction about the size and age of bankrupt firms, we examine the interaction between Basu’s (1997) model of conservatism and the following dummy variables:

Table 7 reports the results of the interaction between Basu’s (1997) model and the above dummy variables. The coefficients on

The Impacts of Size and Age of Bankrupt Firms on Spillover Effects of Bankruptcy.

Note. This table presents the regression results of estimating the interaction between Basu’s (1997) model of conditional conservatism and dummy variables for the bankruptcy spillover effects of large (

Additional Analyses

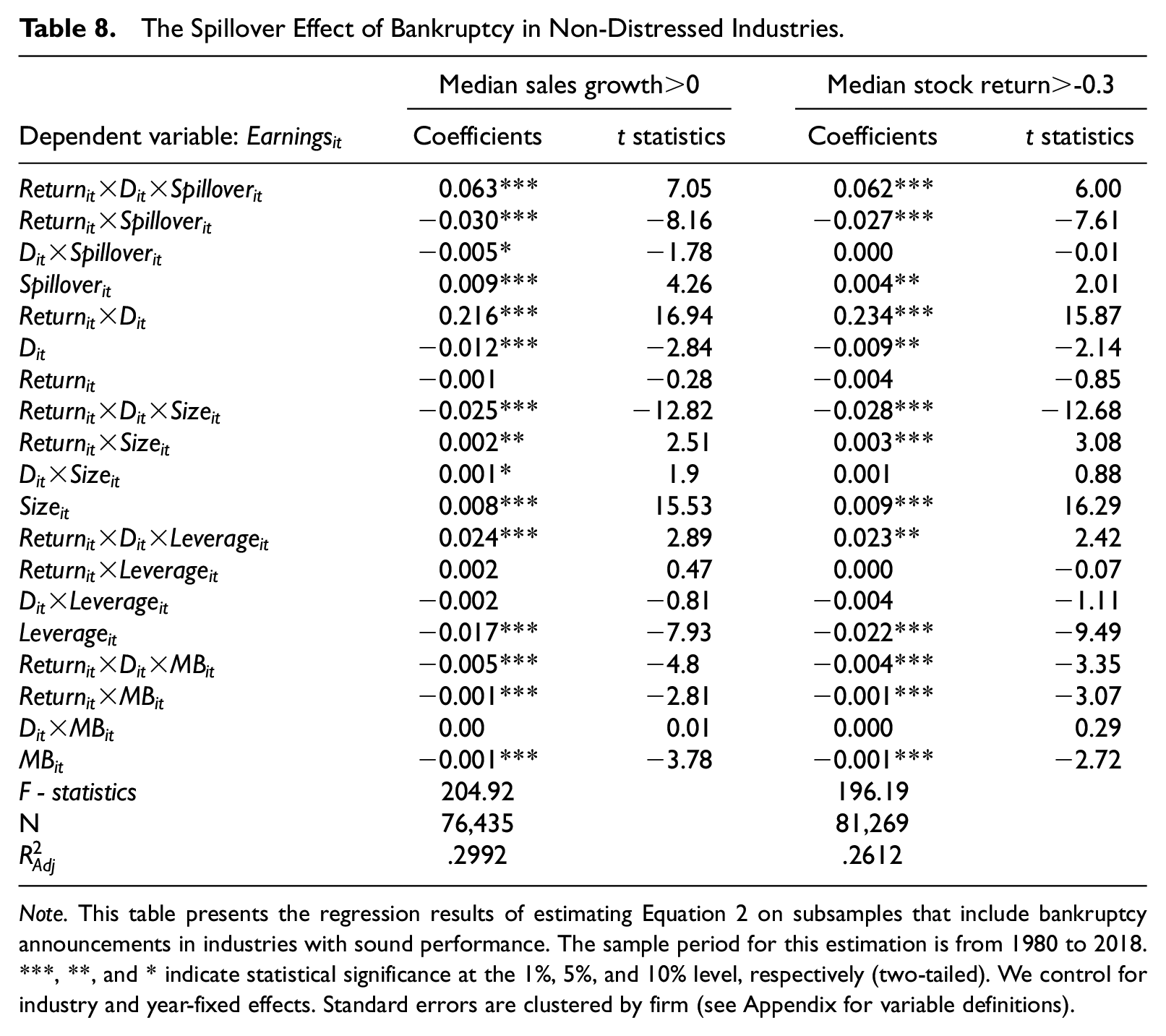

Distressed Industries

To the best of our knowledge, no prior study provides evidence that firms in distress exhibit more conditional conservatism in financial reporting. On the contrary, the literature on financial reporting suggests that firms in distress manage earnings upward to portray a better picture of the firm’s performance (e.g., Beneish et al., 2012; Garcia Lara, Osma, & Neophytou, 2009; C. Lin et al., 2014; Rosner, 2003).

Nevertheless, to mitigate any concern that both the bankruptcy filing and the increase in the degree of conditional conservatism are outcomes of economic distress in the industry, we examine the spillover effects of bankruptcies that occurred while industry performance was sound, and we drop industry years associated with bankruptcy in distressed industries. Consistent with Gopalan and Xie (2011) and Opler and Titman (1994), we define an industry as distressed when its median sales growth is negative, and the median stock return is less than −30%. Under these conditions, a bankruptcy filing could be the result of distress within the industry. Hence, we create subsamples by dropping distressed industries. Table 8 presents the results using subsamples of industries exhibiting sound performance. We find that the coefficients on

The Spillover Effect of Bankruptcy in Non-Distressed Industries.

Note. This table presents the regression results of estimating Equation 2 on subsamples that include bankruptcy announcements in industries with sound performance. The sample period for this estimation is from 1980 to 2018. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

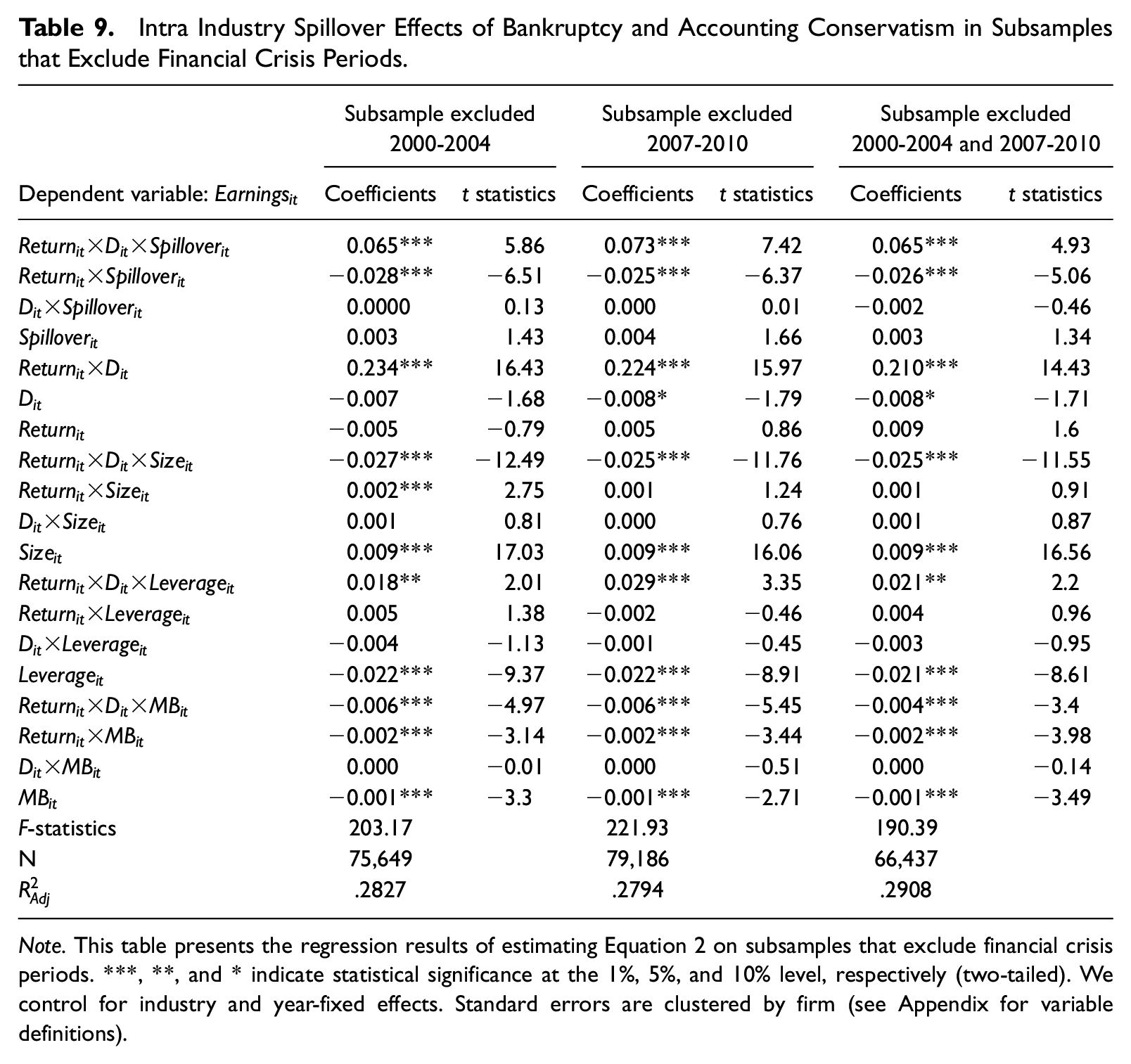

Financial Crisis Periods

In this section, we examine whether our results are robust to the exclusion of financial crisis periods. We exclude all firm years between 2000 and 2004 to examine the exclusion of the dot-com crash period from the sample. We also remove all observations between 2007 and 2010 to explore whether the results continue to hold after the exclusion of the recent financial crisis.

Table 9 reports results for three samples created by removing the dot-com crash period and the recent financial crisis period. The coefficients on

Intra Industry Spillover Effects of Bankruptcy and Accounting Conservatism in Subsamples that Exclude Financial Crisis Periods.

Note. This table presents the regression results of estimating Equation 2 on subsamples that exclude financial crisis periods. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

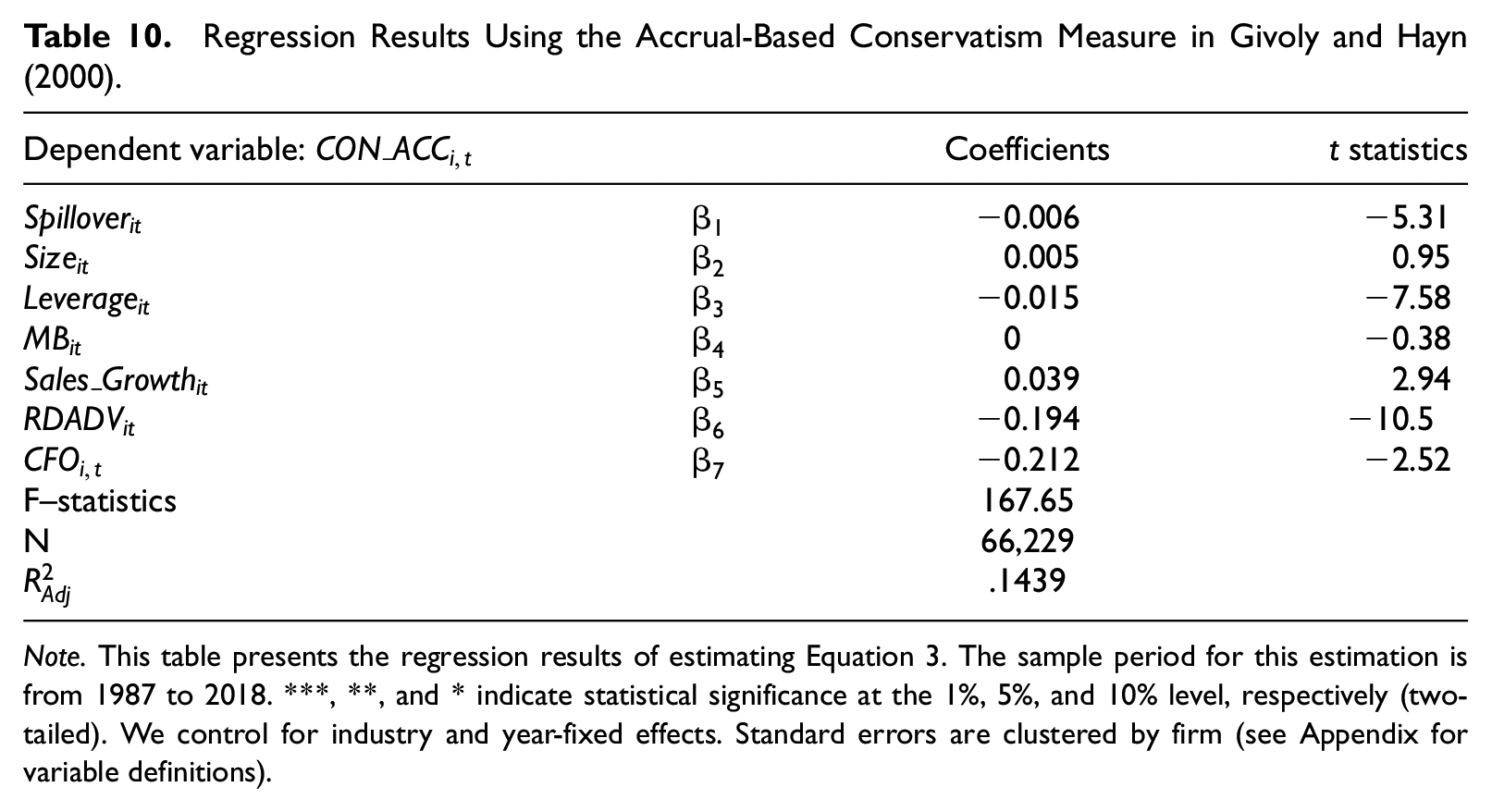

Alternative Proxies for Conditional Conservatism

To corroborate our findings, we employ the accruals-based model of Givoly and Hayn (2000) and the C-Score–based measure of conditional conservatism that is developed by Khan and Watts (2009) as alternative proxies for conditional conservatism. Givoly and Hayn (2000) proxy of conditional conservatism is based on the notion that reporting bad news (losses) more quickly than good news (gains) leads to negative accruals. To re-examine the spillover effects of peer firm bankruptcy on conditional conservatism, we employ the following model:

where

Regression Results Using the Accrual-Based Conservatism Measure in Givoly and Hayn (2000).

Note. This table presents the regression results of estimating Equation 3. The sample period for this estimation is from 1987 to 2018. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

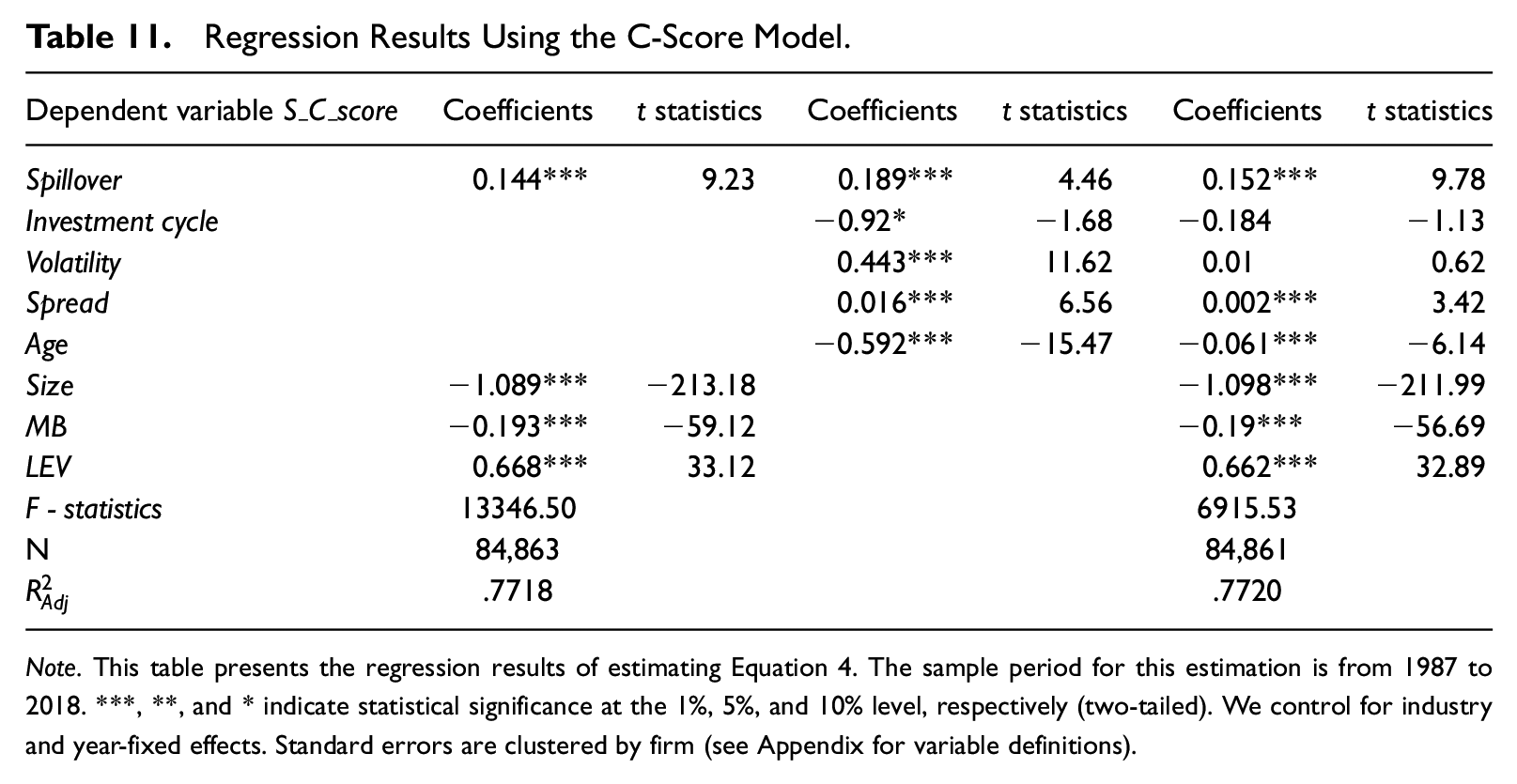

Next, we re-examine the impact of a peer firm bankruptcy filing on conditional conservatism using the C-Score based measure of conditional conservatism (Khan & Watts, 2009). This model has been employed by other studies on determinants of conditional conservatism such as (Ettredge et al., 2012; Kim & Zhang, 2016). We examine the association between a peer firm bankruptcy filing and C-Score using the following regression.

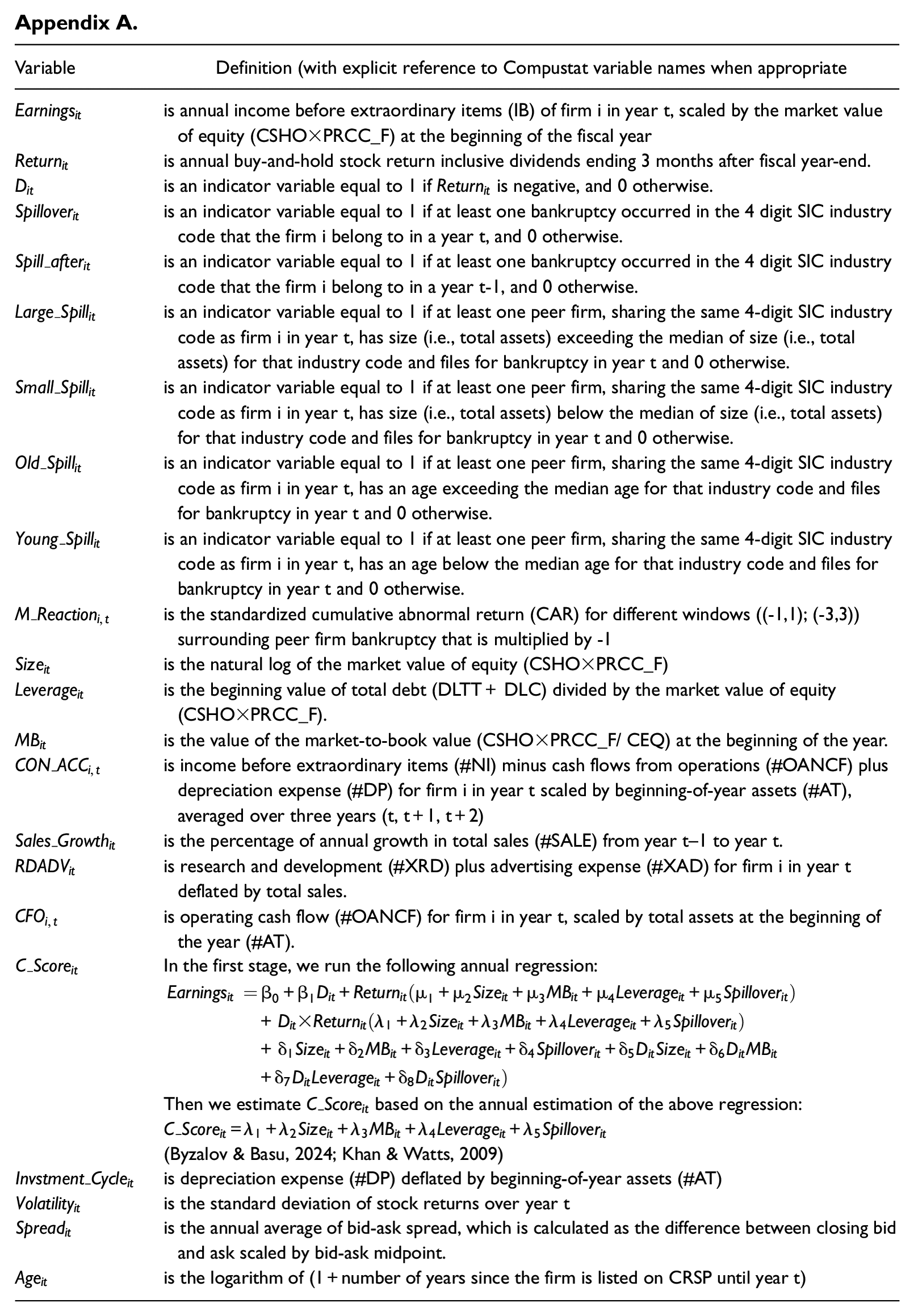

Following Khan and Watts (2009) and Ettredge et al. (2012), we control for the following variables: the length of the investment cycle (

Regression Results Using the C-Score Model.

Note. This table presents the regression results of estimating Equation 4. The sample period for this estimation is from 1987 to 2018. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year-fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

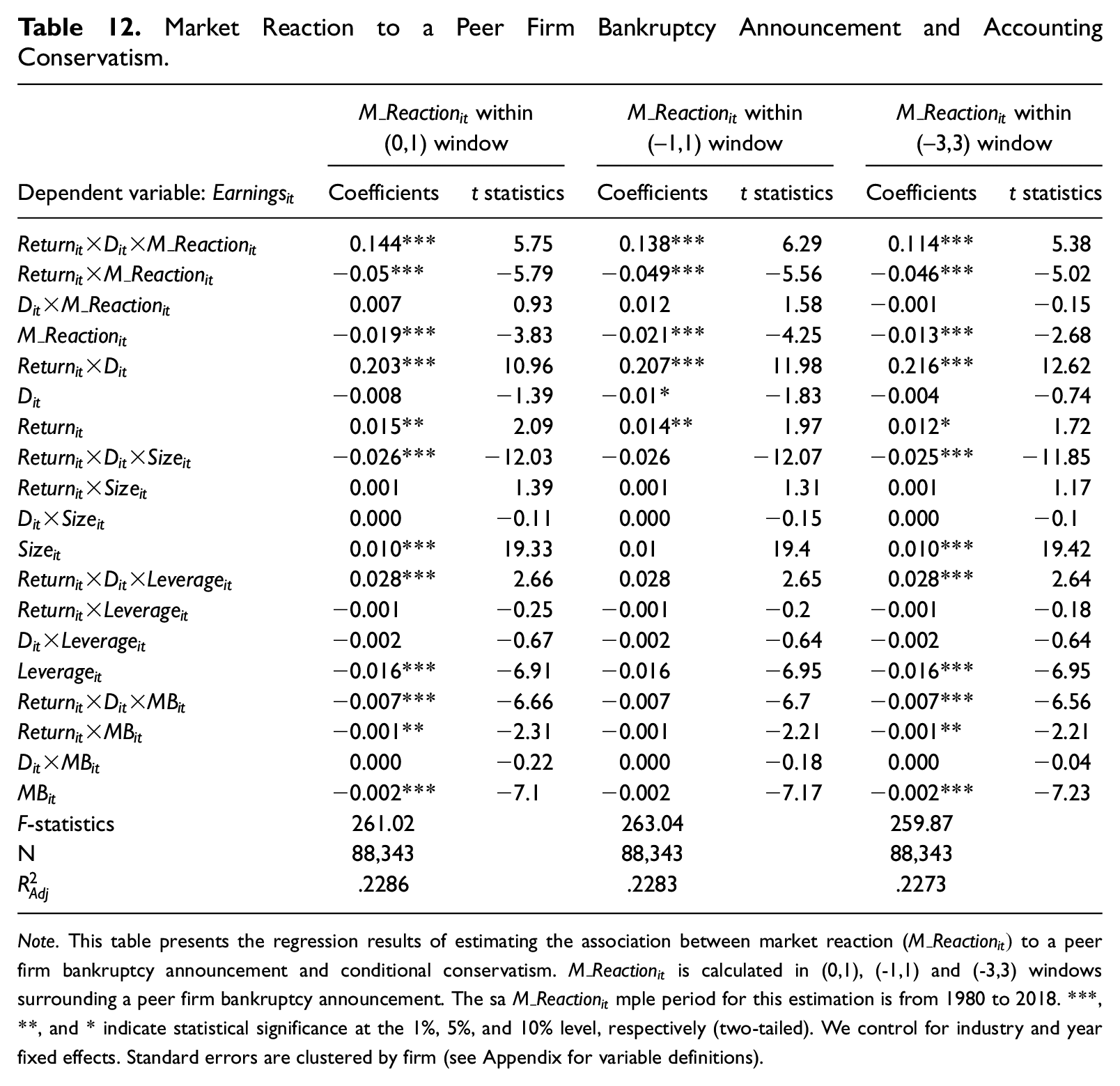

The Role of Market Reaction

This section examines whether conditional conservatism varies with the stock market reaction to a peer firm bankruptcy announcement. It is reasonable to assume that following a peer firm’s bankruptcy announcement, larger stock price declines for non-bankrupt firms indicate higher investor concerns about the non-bankrupt firms. We therefore expect that firms with higher stock price declines may exhibit a greater degree of conditional conservatism. Table 12 reports the results for specifications with

Market Reaction to a Peer Firm Bankruptcy Announcement and Accounting Conservatism.

Note. This table presents the regression results of estimating the association between market reaction (

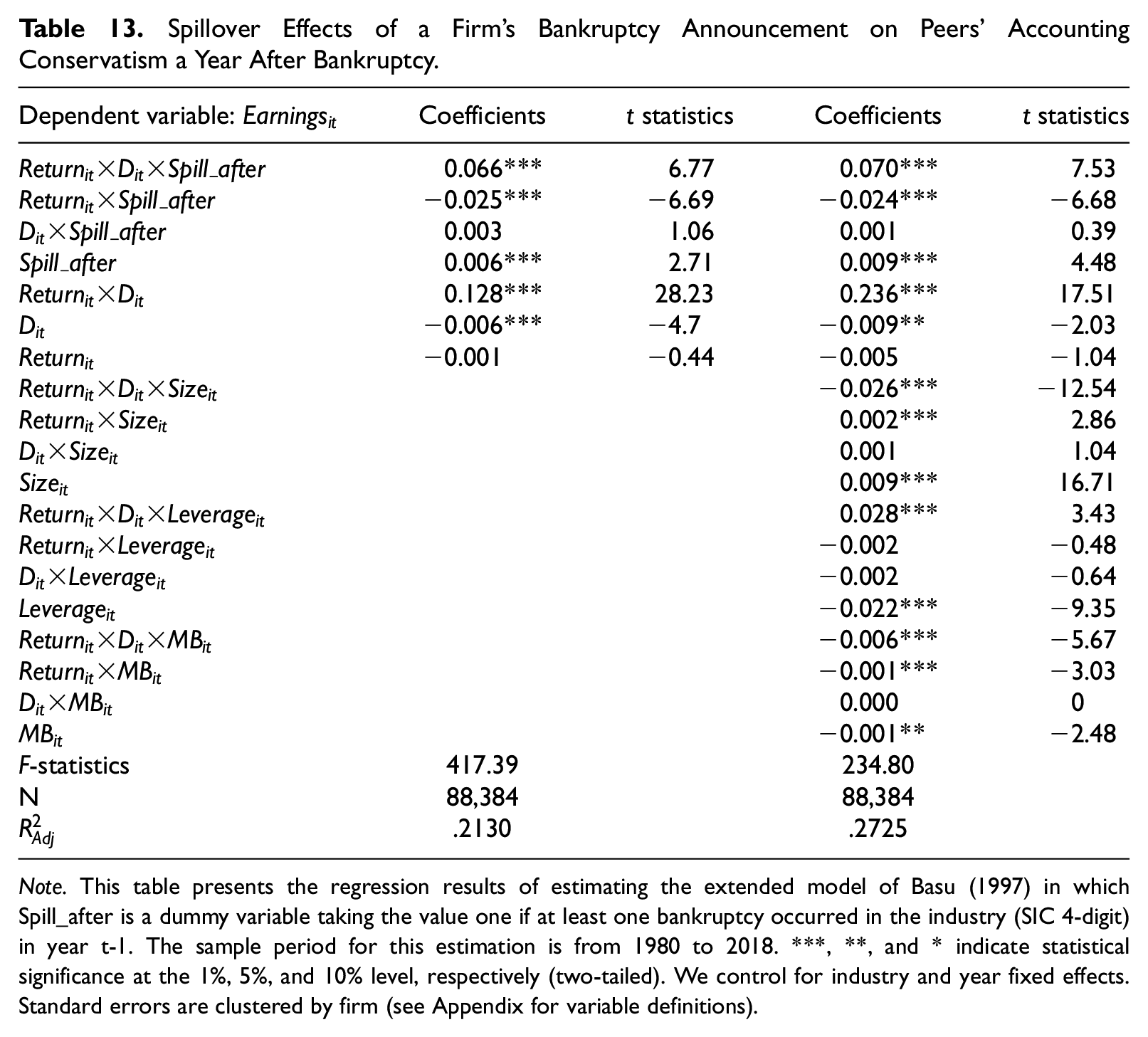

The Spillover Effects of a Peer Firm Bankruptcy Filing a Year After Bankruptcy

To explore the response of non-bankrupt firms a year after a bankruptcy filing, we re-estimate Equation 2 by replacing

Spillover Effects of a Firm’s Bankruptcy Announcement on Peers’ Accounting Conservatism a Year After Bankruptcy.

Note. This table presents the regression results of estimating the extended model of Basu (1997) in which Spill_after is a dummy variable taking the value one if at least one bankruptcy occurred in the industry (SIC 4-digit) in year t-1. The sample period for this estimation is from 1980 to 2018. ***, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively (two-tailed). We control for industry and year fixed effects. Standard errors are clustered by firm (see Appendix for variable definitions).

Conclusion

This study examines how a peer firm’s bankruptcy announcement affects accounting choices among other firms within that industry. It is well documented in the corporate finance literature that a bankruptcy filing negatively affects the stock prices of other firms in the same industry and increases their cost of debt regardless of their economic health. Our research question is if and how firms use financial reporting to mitigate the negative sentiment created by news of peer firm bankruptcy filings. Using a large sample of U.S. firms over the 1980–2018 period, we find that firms exhibit more conditional conservatism in financial reporting when faced with a bankruptcy announcement by a peer firm. The results are robust to the exclusion of distressed industries, the dot-com crisis period, and the global crisis of 2008. Placebo tests do not show a higher degree of conditional conservatism before the actual bankruptcies, suggesting the higher level of conservatism is induced by the peer firm bankruptcy filing. We corroborate our findings by using Givoly and Hayn’s (2000) and Khan and Watts’s models of conditional conservatism. Further analyses reveal that the spillover effects are stronger for firms in industries where firms track and learn from each other’s experiences, for highly levered firms, for firms that experience strong market reaction following peer bankruptcy announcements, and for firms with stronger corporate governance.

Overall, our study shows how a salient event for a peer firm influences firms’ financial reporting strategy. Moreover, we resolve a debate as to whether bad news (bankruptcy filing by a peer firm) induces firms within an industry to become more aggressive in their financial reporting (i.e., upward earnings management) or more conservative. This study has implications for standard setters and regulators by showing how there is a demand for conditional accounting conservatism, especially in times of uncertainty. This paper also extends the scope of the literature on the spillover effects of bankruptcy by showing that peer firm bankruptcy announcement has spillover effects on firms’ financial reporting.

One caveat to our findings is that our identification method of distressed industries may not identify all distressed industries. We do not examine the potential impact of the likelihood of the firm’s emergence from bankruptcy on other firms’ financial reporting strategies. Future research may provide evidence on how such a likelihood affects the spillover effects of a peer firm bankruptcy on financial reporting. Our paper highlights how the news of a firm’s bankruptcy filing influences the financial reporting of other firms in the same industry. Future studies could examine the potential impact of other news coming from a peer firm such as emergence from bankruptcy, product launch, product recall, and environmental crisis on financial reporting.

Footnotes

Appendix

| Variable | Definition (with explicit reference to Compustat variable names when appropriate |

|---|---|

| is annual income before extraordinary items (IB) of firm i in year t, scaled by the market value of equity (CSHO×PRCC_F) at the beginning of the fiscal year | |

| is annual buy-and-hold stock return inclusive dividends ending 3 months after fiscal year-end. | |

| is an indicator variable equal to 1 if is negative, and 0 otherwise. | |

| is an indicator variable equal to 1 if at least one bankruptcy occurred in the 4 digit SIC industry code that the firm i belong to in a year t, and 0 otherwise. | |

| is an indicator variable equal to 1 if at least one bankruptcy occurred in the 4 digit SIC industry code that the firm i belong to in a year t-1, and 0 otherwise. | |

| is an indicator variable equal to 1 if at least one peer firm, sharing the same 4-digit SIC industry code as firm i in year t, has size (i.e., total assets) exceeding the median of size (i.e., total assets) for that industry code and files for bankruptcy in year t and 0 otherwise. | |

| is an indicator variable equal to 1 if at least one peer firm, sharing the same 4-digit SIC industry code as firm i in year t, has size (i.e., total assets) below the median of size (i.e., total assets) for that industry code and files for bankruptcy in year t and 0 otherwise. | |

| is an indicator variable equal to 1 if at least one peer firm, sharing the same 4-digit SIC industry code as firm i in year t, has an age exceeding the median age for that industry code and files for bankruptcy in year t and 0 otherwise. | |

| is an indicator variable equal to 1 if at least one peer firm, sharing the same 4-digit SIC industry code as firm i in year t, has an age below the median age for that industry code and files for bankruptcy in year t and 0 otherwise. | |

| is the standardized cumulative abnormal return (CAR) for different windows ((-1,1); (-3,3)) surrounding peer firm bankruptcy that is multiplied by -1 | |

| is the natural log of the market value of equity (CSHO×PRCC_F) | |

| is the beginning value of total debt (DLTT+ DLC) divided by the market value of equity (CSHO×PRCC_F). | |

| is the value of the market-to-book value (CSHO×PRCC_F/ CEQ) at the beginning of the year. | |

| is income before extraordinary items (#NI) minus cash flows from operations (#OANCF) plus depreciation expense (#DP) for firm i in year t scaled by beginning-of-year assets (#AT), averaged over three years (t, t+1, t+2) | |

| is the percentage of annual growth in total sales (#SALE) from year t–1 to year t. | |

| is research and development (#XRD) plus advertising expense (#XAD) for firm i in year t deflated by total sales. | |

| is operating cash flow (#OANCF) for firm i in year t, scaled by total assets at the beginning of the year (#AT). | |

| In the first stage, we run the following annual regression: Then we estimate based on the annual estimation of the above regression: (Byzalov & Basu, 2024; Khan & Watts, 2009) |

|

| is depreciation expense (#DP) deflated by beginning-of-year assets (#AT) | |

| is the standard deviation of stock returns over year t | |

| is the annual average of bid-ask spread, which is calculated as the difference between closing bid and ask scaled by bid-ask midpoint. | |

| is the logarithm of (1+number of years since the firm is listed on CRSP until year t) |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors thank Agnes Cheng (the editor), two anonymous reviewers, Beatriz García Osma, Denis Cormier, Jorgen Hansen, Fani Kalogirou, Oveis Madadian, participants at the European Financial Reporting (EUFIN) 2023 conference, Journal of Accounting Auditing and Finance (JAAF) 2023 conference, and workshop participants at the University of Glasgow, NEOMA Business School, and Lakehead University for their comments and suggestions. Michel Magnan acknowledges the financial support of the Stephen A. Jarislowsky Chair in Corporate Governance and of the Institute for the Governance of Private and Public Organizations. Ahmad Hammami acknowledges financial support from the Social Sciences and Humanities Research Council of Canada.

Data Availability Statement

Data used in this paper are publicly available.

Open Access

This is an Open Access article distributed under the terms of the Creative Commons Attribution-NonCommercial-NoDerivatives License (![]() /), which permits non-commercial re-use, distribution, and reproduction in any medium, provided the original work is properly cited, and is not altered, transformed, or built upon in any way. The terms on which this article has been published allow the posting of the Accepted Manuscript in a repository by the author(s) or with their consent.

/), which permits non-commercial re-use, distribution, and reproduction in any medium, provided the original work is properly cited, and is not altered, transformed, or built upon in any way. The terms on which this article has been published allow the posting of the Accepted Manuscript in a repository by the author(s) or with their consent.