Abstract

The crossholding of multiple firms by major shareholders in the same industry is known as common ownership. In this article, we examine how common ownership affects the carbon-related disclosure practices of cross-held firms. We report that common ownership decreases a firm’s propensity to disclose carbon information as well as the quality of such disclosures. A one standard deviation increase in measures of common ownership decreases the likelihood of participating in the Carbon Disclosure Project (CDP) survey by as much as 19.4%. Our results are robust to exogenous events, such as changes in common ownership and robustness tests, including Heckman two-stage regression and the exclusion of the financial sector. Further analyses demonstrate that the negative impact of common ownership on carbon disclosures is stronger in carbon-intensive sectors than in other sectors and for hard than for soft disclosures.

Introduction

Climate change is unarguably a major political and economic challenge that must be faced by global political leaders and corporations. Meeting the goals set by the Paris Agreement requires significant investments in low-carbon and energy-efficient technology. For instance, approximately U.S.$130 billion in additional investments per year are needed to achieve countries’ Nationally Determined Contributions or the 2°C or 1.5°C targets globally (McCollum et al., 2018). As public finances alone cannot support this scale of investment, there is a call for financial institutions to mobilize their investments (OECD, 2018). In this regard, previous research investigates the role-played by institutional investors in promoting corporations’ environmental performance and disclosures. Prior research on institutional investors commonly considers them a homogeneous group (see Gillan et al., 2021 and Velte, 2020 for reviews), whereas recent studies attempt to differentiate between types of institutional investor according to characteristics, such as investment horizon, location, and sustainability policies (Ilhan et al., 2023; H.-D. Kim et al., 2019; I. Kim et al., 2019; Kordsachia et al., 2021). However, these studies do not consider that institutional investors can influence multiple firms in the same industry through common ownership. This ownership structure makes a firm’s decisions dependent on not only its own strategic plans but also its relationship with industry peers cross-held by common institutional investors. Such a relationship may induce cross-held firms to act on collective benefits for common owners and their portfolio firms (Azar et al., 2018). In this article, we focus on this concentration of institutional ownership among firms in the same industry (i.e., common ownership) and examine how this ownership structure affects the carbon-related disclosure practices of these firms.

Large multinational financial institutions, such as Blackrock, Vanguard, and State Street Global Advisors, are major shareholders of listed companies in the United States. For example, these Big Three financial institutions are now the largest shareholders of 88% of S&P 500 firms (Fichtner et al., 2017). There is concern that these major shareholders own shares of rival firms in the same industry, reducing competition among them. Prior studies suggest that these firms are likely to act on the collective benefits of commonly owned peer firms. For instance, Azar et al. (2018) show that airline ticket prices are higher on U.S. airline routes controlled by common owners. In addition, Cheng et al. (2022) show that reduced competitive pressure under common ownership discourages firms from engaging in corporate social responsibility (CSR) activities. In contrast, other studies show that such reduced pressure fosters product market collaboration, enhancing productivity (He & Huang, 2017). Moreover, common owner institutions provide stronger monitoring of their cross-held firms (He et al., 2019).

There is still limited evidence on how common ownership might affect the disclosure practices of individual firms that are cross-held. On one hand, it can promote voluntary financial disclosures of cross-held firms by alleviating concerns over proprietary costs. In line with this view, Park et al. (2019) demonstrate that such ownership increases the voluntary financial disclosures of cross-held firms. On the other hand, firms held by common owners may not be pressured to provide voluntary disclosures to external stakeholders, especially when disclosing the information is costly and its benefits are not financially clear. We focus on carbon disclosures to test these views because such disclosures have unique characteristics that are distinctive from those of financial reporting (Liao et al., 2015; Luo & Wu, 2019).

The disclosure of carbon emissions can involve higher costs to carry out tasks, such as tracking, measuring, and aggregating carbon-related data not only within the firm but also throughout the supply chain. Bolton and Kacperczyk (2021) suggest that firms’ incentives to disclose carbon information are different from those to provide financial information. They note that it is implausible to assume that firms risk revealing private information that competitors could exploit by disclosing their emissions information. Therefore, the findings of a study on common ownership and corporate disclosure practices (e.g., Park et al., 2019) are not directly applicable in the context of carbon disclosures. Moreover, the disclosure of a firm’s emissions levels may allow investors to use this information as a screening measure, making the firm less attractive for investments (Bolton & Kacperczyk, 2021). In fact, after carbon-related disclosures became mandatory in the United Kingdom, there was a higher level of divestment led by institutional investors (Bolton & Kacperczyk, 2021). In addition, carbon disclosures may attract unwanted scrutiny from external stakeholders, including regulators. In this study, we explore the multifaceted impacts of institutional ownership on carbon disclosure by focusing on common ownership. We further examine the type of carbon-related information that is more likely to be affected by the control of common owners.

Using Carbon Disclosure Project’s (CDP) data for U.S. firms from 2006 to 2018, we test the relationship between common ownership and a firm’s decision to disclose carbon information and its disclosure quality. Common ownership is measured using a dummy (i.e., the existence of common owners), the number of common owners, the number of firms cross-held by common owners, and the market value of common ownership. Overall, these variables are negatively associated with a firm’s propensity to disclose. Regarding economic significance, a one standard deviation increase in these common ownership measures, on average, decreases the likelihood of participating in the CDP survey by as much as 19.4%. Our results are robust to using public carbon disclosure as an alternative dependent variable, propensity score matching (PSM), controlling for institutional investors who have holdings in different industries, and excluding the financial sector. In addition, using Heckman two-stage regression, we demonstrate that common owners also reduce the quality of carbon information provided by cross-held firms that already participate in the CDP.

Furthermore, we investigate the specific types of carbon information disclosures that are particularly affected by common owners. To do this, we identify different categories of carbon disclosure, namely, hard disclosures, which require a strong commitment to carbon reduction, and soft disclosures, which contain rather vague information that is difficult to verify ex post. We find that the negative impact of common ownership on carbon disclosure is more pronounced for hard than for soft disclosures.

Finally, we examine the effect of changes in common ownership on carbon disclosure using brokerage house mergers and closures as exogenous events. When the number of common owners increases after a merger and closure event, a firm becomes less likely to participate in voluntary CDP disclosure. However, for a firm that already discloses carbon information, its disclosure quality does not change. In the opposite case, where common ownership decreases following divestment, firms respond by increasing their disclosure quality instead of initiating carbon disclosure. This could be because inaugural participation in the CDP requires firms to allocate considerable resources to carbon reporting. However, those who have already participated in the CDP could increase their disclosure quality relatively easily after the exit of common owners.

This article makes the following contributions. First, we provide new evidence of how institutional investors affect firms’ carbon disclosures via common ownership by incorporating their influence over rival firms in the same industry. Prior studies on institutional ownership and carbon disclosures mainly examine the overall institutional ownership level without differentiating among institutional investors (e.g., Acar et al., 2021). Other papers, including Ilhan et al. (2023), investigate different types of institutional investor. In particular, they identify climate-conscious institutional ownership and document its positive association with firm-level climate risk disclosure. In contrast, our focus is on institutional investors who can influence multiple firms in the same industry through their common ownership (i.e., common owners). This type of institutional investor may influence corporate disclosures in a unique way. When common owners control rival firms in the same industry, these firms are less pressured to compete with each other (Azar et al. (2018) and win market shares from other firms via additional carbon reporting and differentiation strategies. This effect of reduced competition can be more prominent, especially when disclosure is costly and the financial benefits of doing so are unclear, such as in the case of carbon reporting. In line with this view, our results confirm that common ownership decreases a firm’s propensity to disclose carbon information and the quality of such disclosures.

Moreover, no prior study examines the direct impact of common ownership on carbon-related disclosure. Some recent studies attempt to link common ownership with general CSR performance (Cheng et al., 2022; Dai & Qiu, 2020; DesJardine et al., 2023). However, CSR performance is a broad concept and does not specifically reflect confounding issues surrounding carbon-related disclosures. Importantly, carbon disclosure does not always align with carbon performance (Hrasky, 2012; Luo, 2019; Luo & Tang, 2022). For example, García-Sánchez et al. (2021) demonstrate that firms have incentives to provide inaccurate carbon information when they have poor carbon performance. In other words, a gap can exist between how a firm describes its carbon performance in disclosures and its actual performance. In addition, disclosing carbon-related information may risk attracting unwelcome political attention and higher divestment from environmentally conscious institutional investors (Bolton & Kacperczyk, 2021). Therefore, the findings of studies on common ownership, CSR performance (Cheng et al., 2022; Dai & Qiu, 2020; DesJardine et al., 2023), and corporate disclosure practices (Park et al., 2019) are not directly applicable to carbon disclosure.

In addition, prior studies on CSR performance and common ownership present competing arguments and findings. For instance, Dai and Qiu (2020) and DesJardine et al. (2023) find that common ownership improves the CSR performance of public firms. DesJardine et al. (2023) argue that common owners can create spillover effects by improving the CSR performance of firms in their portfolio and enjoy reduced systematic risk because of enhanced CSR performance. However, Cheng et al. (2022) report a negative relationship and argue that reduced competitive pressure caused by common ownership disincentivizes firms to invest more in CSR to gain a competitive advantage. These mixed empirical findings may be partly attributable to how CSR performance is measured. Arguably, the CSR performance of any given firm may differ across CSR rating agencies depending on how it is measured, complicating comparisons between firms (Christensen et al., 2021). Our study mainly focuses on a firm’s decision on whether or not to provide carbon-related information and provides a comprehensive analysis and discussion of how the presence of common ownership influences that decision. We also further classify the types of carbon disclosure—hard and soft information—to advance an understanding of corporate (dis)incentives to provide voluntary carbon information in the presence of common ownership.

The remainder of this article is structured as follows. The “Literature Review and Hypotheses” section presents a literature review and hypothesis development. The “Data and Methodology” section describes the research models and data. The “Results” section discusses the findings. The “Conclusion” section concludes the article.

Literature Review and Hypotheses

Institutional investors are a powerful stakeholder group for companies that provide capital for business operations and hold substantial voting rights. They often request high-quality information about climate change risks and opportunities from companies (Cotter & Najah, 2012; Kolk et al., 2008). However, previous studies that investigate the impact of institutional investors on corporate carbon disclosure produce mixed results. For instance, Stanny and Ely (2008) find a positive influence of institutional ownership on carbon disclosure, whereas Liesen et al. (2015) document a negative but nonsignificant association between carbon disclosure quality and institutional ownership as measured by pension funds. Acar et al. (2021) examine the impacts of both state and institutional ownership on environmental disclosures and show that they have opposite influences on such disclosures. That is, although firms with higher state ownership make more environmental disclosures, higher institutional ownership decreases such disclosures.

Notably, Gillan et al. (2021), in a review on environmental, social, and governance (ESG) and CSR research in corporate finance, highlight that while many studies examine the relationship between institutional ownership and firms’ ESG/CSR activities, not all of them “agree on the form or sign of the relationship” (p. 5). Another review on institutional ownership and ESG performance and disclosure by Velte (2020) emphasizes the need for a detailed examination of various characteristics of institutional owners to explain the mixed results. The authors of both reviews conclude that the categorization of institutional investors is important for understanding their diverse strategic objectives and influence on ESG activities. Velte (2020) notes that the ratio, nature, and type of institutional ownership may differently affect corporate ESG activities. In particular, regarding the nature of institutional investors, he identifies long-term versus short-term, active versus passive, and financial versus sustainable institutional ownership. A recent study by Ilhan et al. (2023) focuses on a specific type of institutional ownership (i.e., climate-conscious institutional ownership) and examines its relationship with carbon reporting. They identify climate-conscious institutional ownership in the following three ways: (a) institutional investors from countries with stewardship codes, (b) those based in countries with more climate-conscious norms, and (c) a universal owner. They demonstrate a positive association between climate-conscious institutional ownership and firm-level climate risk disclosure.

However, previous research on carbon reporting overlooks the distinctive traits of common institutional owners, who have the capacity to simultaneously affect multiple competing firms within the same industry. Prior research highlights the role of common owners as a connective link between competing firms and emphasizes their unique position to influence industry-wide carbon practices and policies.

By holding shares across competing firms, common institutional investors can potentially foster collaboration among rivals within their portfolios. For instance, He and Huang (2017) argue that firms with common ownership are more likely to internalize externalities for the collective benefit of firms in common owners’ portfolios. They argue that common owners can foster implicit and explicit coordination among cross-held rival firms through joint ventures, strategic alliances, acquisitions, or R&D investments. Through these collaborative activities, common ownership helps alleviate negative externalities by discouraging investment overlap in similar products and technologies among rival firms. Park et al. (2019) also show that common ownership increases firms’ voluntary disclosures of financial information by reducing proprietary costs. That is, if rival firms are under the control of the same common owners, the disclosing firm is less concerned about proprietary information being shared through disclosures, as its competing peer firms would not use this information to gain market share at the expense of the disclosing firm.

However, the crossholding of rival firms by common owners may lead to reduced competition within the industry, which can result in these firms exerting control over prices and goods and services provided to customers, further impeding firms’ CSR engagement. For instance, Azar et al. (2018) report that ticket prices are approximately 3% to 7% higher on average for US airline routes under the control of common owners than for other cases. In addition, studies find that competition within an industry may affect a firm’s CSR engagement. One motivation for firms to engage in CSR activities is to achieve a competitive advantage over their competitors by incorporating CSR attributes into their marketing strategies (Sen et al., 2006). Such differentiation tactics work more effectively in a competitive environment (Fisman et al., 2008; Johnson, 1966). Similarly, previous studies show that product market competition increases firms’ CSR engagement (Fernández-Kranz & Santaló, 2010; Flammer, 2015). In line with this literature, Cheng et al. (2022) investigate the effect of common ownership on firms’ CSR engagement. They argue that the expected benefits from CSR engagement are reduced in a less competitive industry, as common ownership reduces competition among cross-held rival firms. Accordingly, they find decreased CSR performance when common ownership is high.

These previous findings on the various impacts of common ownership on corporate activities also indicate that its influence on carbon disclosure can be ambiguous. When examining CSR disclosure, Ryou et al. (2022) discuss two competing views on the effects of product market competition. One stream of the literature argues that product market competition intensifies the proprietary costs of disclosing firms, leading to a reduction in voluntary CSR disclosures. Another stream of the literature notes that the strategic benefit of CSR is enhanced when competition is high, predicting a positive association between market competition and CSR disclosures. Similarly, firms under the control of common ownership may be less concerned about revealing their private information to their rivals via voluntary disclosure (Park et al., 2019), making them more willing to disclose carbon-related information. However, these firms also experience less product market competition by engaging in direct and indirect collative actions with rival firms induced by common owners (Azar et al., 2018; He & Huang, 2017). Doing so reduces the value of gaining a competitive advantage over rival firms (Cheng et al., 2022), making voluntary carbon disclosures a less attractive option for disclosing firms.

Moreover, carbon reporting has distinctive characteristics that differentiate it from other general CSR reports. Corporate carbon reporting can be costly because it requires thorough calculations, measurements, and reports of different types and intensities of carbon emissions(Haigh & Shapiro, 2012). In addition to these direct costs of preparing carbon disclosures, there are indirect costs. Giving investors readily available carbon information can be costly, as they can use it as a basis for exclusionary screening policies. That is, carbon disclosure may reveal a high level of emissions, which can cause environmentally conscious investors to divest. In fact, empirical evidence supports the concept that firms with higher disclosed emissions are less likely to attract institutional investors (Bolton & Kacperczyk, 2021). Indeed, U.K. firms experienced greater divestment by institutional investors after mandatory disclosure of carbon emissions was introduced (Bolton & Kacperczyk, 2021). Disclosing carbon information may also attract unwanted political attention if the level of carbon emissions revealed is too high or if the promised carbon reduction measures are not effectively implemented. Unlike general CSR disclosures, companies often outline specific carbon reduction targets and strategies in their carbon reports. Implementing these carbon reduction initiatives necessitates additional investments by firms, resulting in high long-term costs. Acar et al. (2021) also explain why institutional investors might discourage firms from sharing publicly available carbon-related information. Large institutional investors can access internal information that is not available to other shareholders (El-Diftar et al., 2017). These institutions may aim to preserve this information privilege by preventing the sharing of environmental information with external stakeholders.

In summary, carbon disclosures can provide valuable information to external stakeholders, allowing the disclosing firm to distinguish itself from its competitors. However, voluntary disclosures may lead to the sharing of private information with competitors. As common owners control rival firms within the industry, common ownership may alleviate the chance of proprietary information being exploited by competing peer firms. Thus, on one hand, common ownership may encourage cross-held firms in portfolios to voluntarily share more information with external stakeholders. On the other hand, disclosing costly carbon emissions can pose an additional risk of attracting increased political scrutiny and potential divestment. In addition, the benefit of disclosing carbon-related information is reduced when rival firms are controlled by common owners, as they do not have to fiercely compete with each other. In this case, firms are less likely to disclose carbon-related information when controlled by common owners. Based on these two contrasting arguments, we propose the following null hypotheses:

Data and Methodology

The CDP invites firms listed on the S&P 500 to participate on an annual basis. The original sample collected from the CDP from 2006 to 2018 consists of 5,986 observations of US firms that were invited to participate. 1 Carbon disclosure quality data are obtained from the CDP database, which is available only from 2007. Firms’ financial data are collected from Compustat. Additional data on corporate governance, environmental performance scores, and estimated levels of carbon emissions are retrieved from the Refinitiv ESG database. Institutional holding data are sourced from the Thomson Reuters’ 13F database. Matching with common ownership data produces 5,209 listed firm-year observations. Once all financial data are merged, the final sample consists of 3,724 firm-year observations.

Measurement of Common Ownership

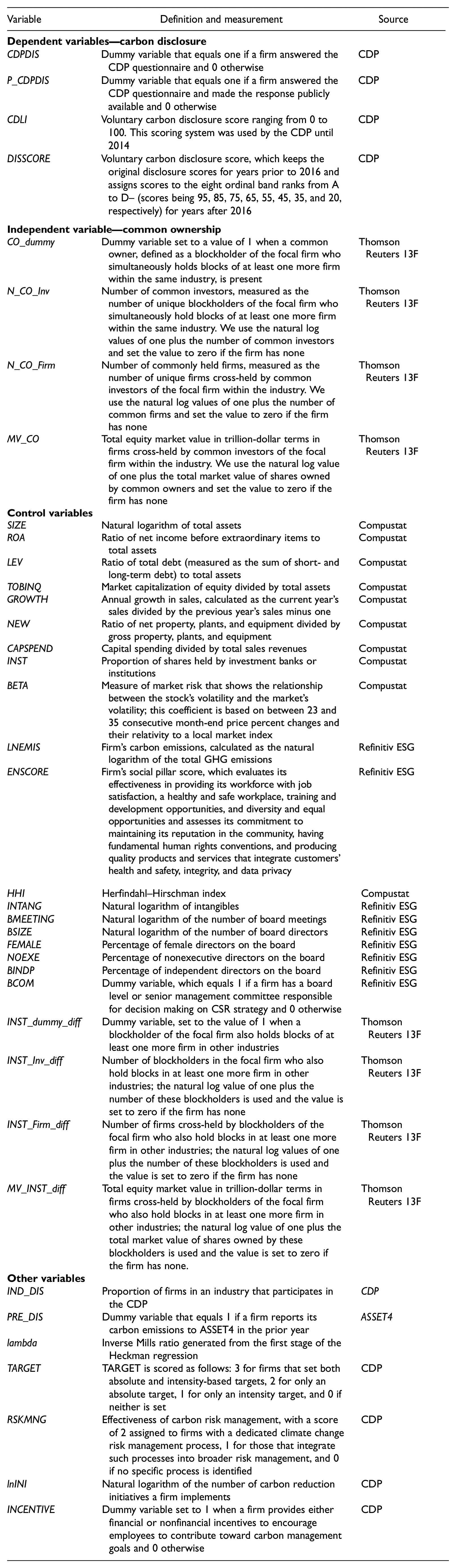

According to the literature (e.g., He & Huang, 2017; Park et al., 2019), a common owner is defined as an institutional investor who has significant holdings in two or more peer firms and can meaningfully influence the firms. Thus, measuring common ownership requires the identification of the blockholders of each firm who hold more than 5% of the outstanding shares. We use quarterly institutional holdings data for each institutional investor obtained from 13F to identify blockholders. Next, to identify peer firms, we adopt the industry classification suggested by Hoberg and Phillips (2010, 2016), which identify peer grouping based on firms’ own disclosure of products and services that they provide. Finally, for a focal firm, we construct four proxies of common holdings per year following prior studies on common ownership. The first variable used is a dummy variable, equal to 1 when a common owner is present for a firm in the year and 0 otherwise (CO_dummy). Therefore, at least one institutional blockholder of the focal firm exists, as well as a blockholder of peer firm(s). As there can be multiple institutional blockholders for the focal firm and its peers, the second variable is the number of common investors (N_CO_Inv), which measures the number of unique common owners for the focal firm. 2 We use the natural log values of one plus the number of common investors and set the value to zero if the firm has no common owner. Because the collaborative effect of common ownership across the industry could matter, we create a third variable, which represents the number of firms that share at least one common owner with the focal firm within the same industry during the year (N_CO_Firm). The higher the value of this variable, the higher the number of peer firms that share at least one common owner and that are more likely to decrease competition among peers. We use the natural log value of one plus the number of cross-held firms and set the value to zero if the firm has no common ownership. As pressure to collaborate among peer firms is stronger when the common owner has a larger stake held in the focal firm, we assess the ownership value rather than the percentage of holdings in the firm. The final variable is the natural logarithm of the total market value of shares owned by common owners of the focal firm (MV_CO). The variables CO_dummy, N_CO_Inv, and N_CO_Firm are averaged across four quarters prior to the fiscal year of interest (Park et al., 2019). See Appendix A for illustrations and explanations of the construct of common ownership variables.

Research Methods

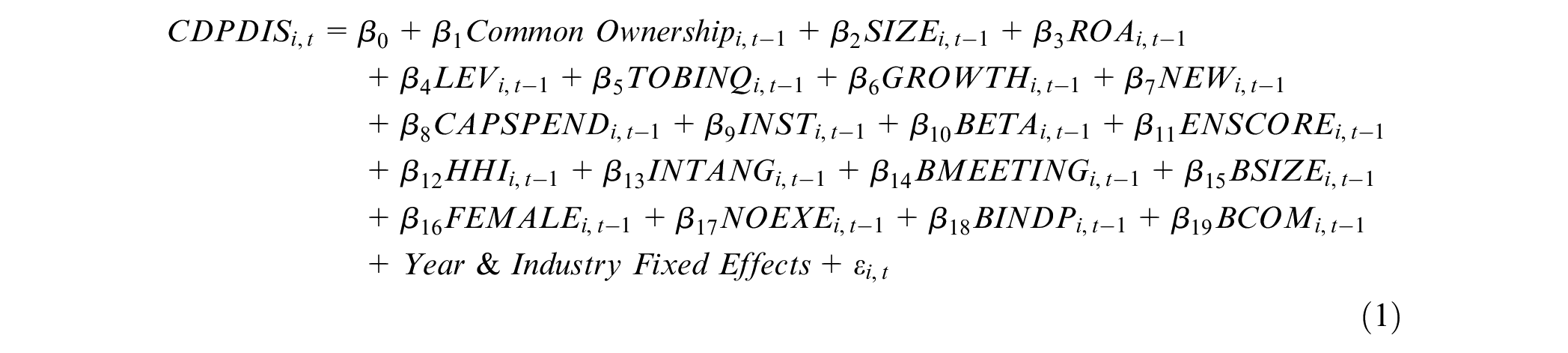

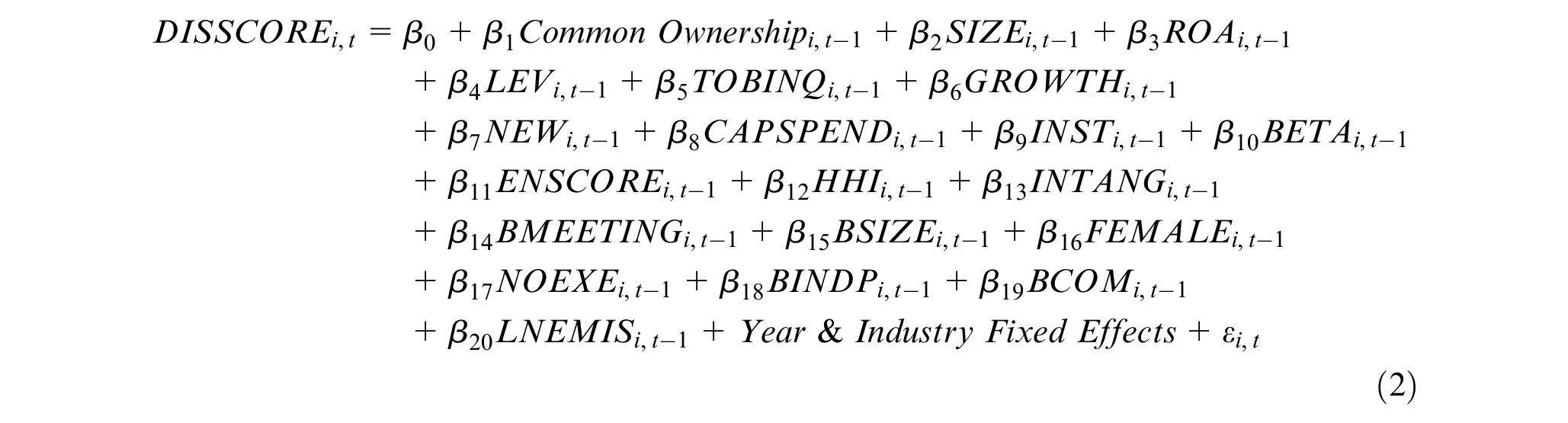

To test our hypotheses, we estimate the following models in which the dependent variables are (a) the propensity to disclose carbon-related information (i.e., whether a firm participates in the CDP survey) and (b) carbon disclosure scores for firms that provide such disclosures.

where i and t denote firm i in year t. The first measure used as a dependent variable in Equation (1) is a dummy for voluntary participation in the CDP. This variable has a value of 1 if a company voluntarily participates in the CDP survey and 0 if a firm is invited but declines to participate or does not respond to the invitation (CDPDIS). As a robustness check, we also examine a firm’s decision to make its disclosures public or not (P_CDPDIS), following Ott et al. (2017). As the dependent variable for the first regression is a dummy, a logit regression is used.

In Equation (2), we use the carbon disclosure score (DISSCORE) as a dependent variable to measure CDP disclosure quality (Clarkson et al., 2015; Griffin et al., 2017; Luo & Wu, 2019). 3 The CDP changed the disclosure quality measure from a continuous score of 0 to 100 to eight categorical band ranks (e.g., bands A, A–, B, B–, C, C–, D, and D–) starting in its 2016 reporting cycle, which typically reflects the emissions data of firms in the 2015 financial year. To maintain consistency across our sample period, we convert the later years’ ranks back into scores. In alignment with the approach proposed by Wang et al. (2021) for converting between scores and bands, we utilize the median values of specified ranges for disclosure scores as the point estimate for each rank. DISSCORE maintains the original disclosure scores for years prior to 2016 and assigns scores to the eight ordinal band ranks from A to D– (scores of 95, 85, 75, 65, 55, 45, 35, and 20) for years after 2016; thus, DISSCORE ranges from 0 to 100. 4 The specific scores assigned to each band rank (e.g., 95 for A, down to 20 for D–) are chosen to reflect the perceived quality differentials between the ranks. This scoring system aims to approximate the original continuous scoring methodology as closely as possible, preserving the ordinal nature of the ranks while providing a quantifiable measure of disclosure quality. The main independent variable of interest is common ownership, which is proxied by the common ownership dummy (CO_dummy), the number of common owners (N_CO_Inv), the number of firms cross-held by common owners (N_CO_Firm), and the total market value of common ownership (MV_CO). The “Measurement of Common Ownership” section details the measurements for these variables.

In addition, the following control variables are included. Larger firms tend to be subject to greater scrutiny from stakeholders and regulators (Clarkson et al., 2008). To control for this, firm size (SIZE) is measured as the log value of total assets. Consistent with Matsumura et al. (2014), we include return on assets (ROA) to measure firm performance. We also include leverage (LEV), which is calculated as the ratio of total debt (measured as the sum of short- and long-term debt) to total assets (Clarkson et al., 2008). Capital expenditure (CAPSPEND) and net change in property, plant, and equipment (NEW) are proxies for investments in clean technologies (Clarkson et al., 2008). Following Ott et al. (2017), two variables are included to capture growth potential: Tobin’s Q (TOBINQ) and sales growth (GROWTH). Institutional ownership (INST) is used to control for differences in firms’ ownership structure (Haque, 2017; Jo & Harjoto, 2012). Greater uncertainty may encourage firms to invest in CSR activities. We use the beta (BETA) calculated from monthly price fluctuations to control for price volatility and risk (Luo et al., 2012). Next, as firms might have different levels of environmental performance, which can affect their carbon reporting, environmental performance pillar scores from the Refinitiv ESG database (ENSCORE) are included as controls. As a proxy for industry concentration, we include the Herfindahl–Hirschman index (HHI) in our base model. We also control for intangible assets (INTANG), which are characterized by high risk and high uncertainty. In addition, corporate governance is found to play an important role in corporate carbon disclosure decisions (e.g., Choi & Luo, 2021). The following corporate governance variables are included in the model: number of board meetings (BMEETING), board size (BSIZE), number of female directors (FEMALE), number of nonexecutive directors (NOEXE), board independence (BINDP), and presence of a board CSR committee (BCOM). BMEETING (BSIZE) is calculated as the natural logarithm of the number of board meetings (board directors). FEMALE (NONEXE, BINDP) is the percentage of female directors (nonexecutive directors, independent directors) on the board. BCOM is a dummy variable that equals 1 if a firm has a board or senior management committee responsible for decision making on CSR strategy and 0 otherwise. Furthermore, a firm’s carbon emissions (LNEMIS) are additionally controlled for in the disclosure score model, Equation (2). LNEMIS is calculated as the natural logarithm of the total greenhouse gas (GHG) emissions retrieved from the Refinitiv ESG database. Industry and year fixed effects are included in all regressions. The standard errors are clustered by industry. The two-digit Global Industry Classification Standard (GICS) sector classification is used for the industry fixed effects. Robust standard errors are calculated for all regression models. To mitigate any bias due to outliers, all continuous variables are winsorized at the first and 99th percent levels.

Results

Summary Statistics

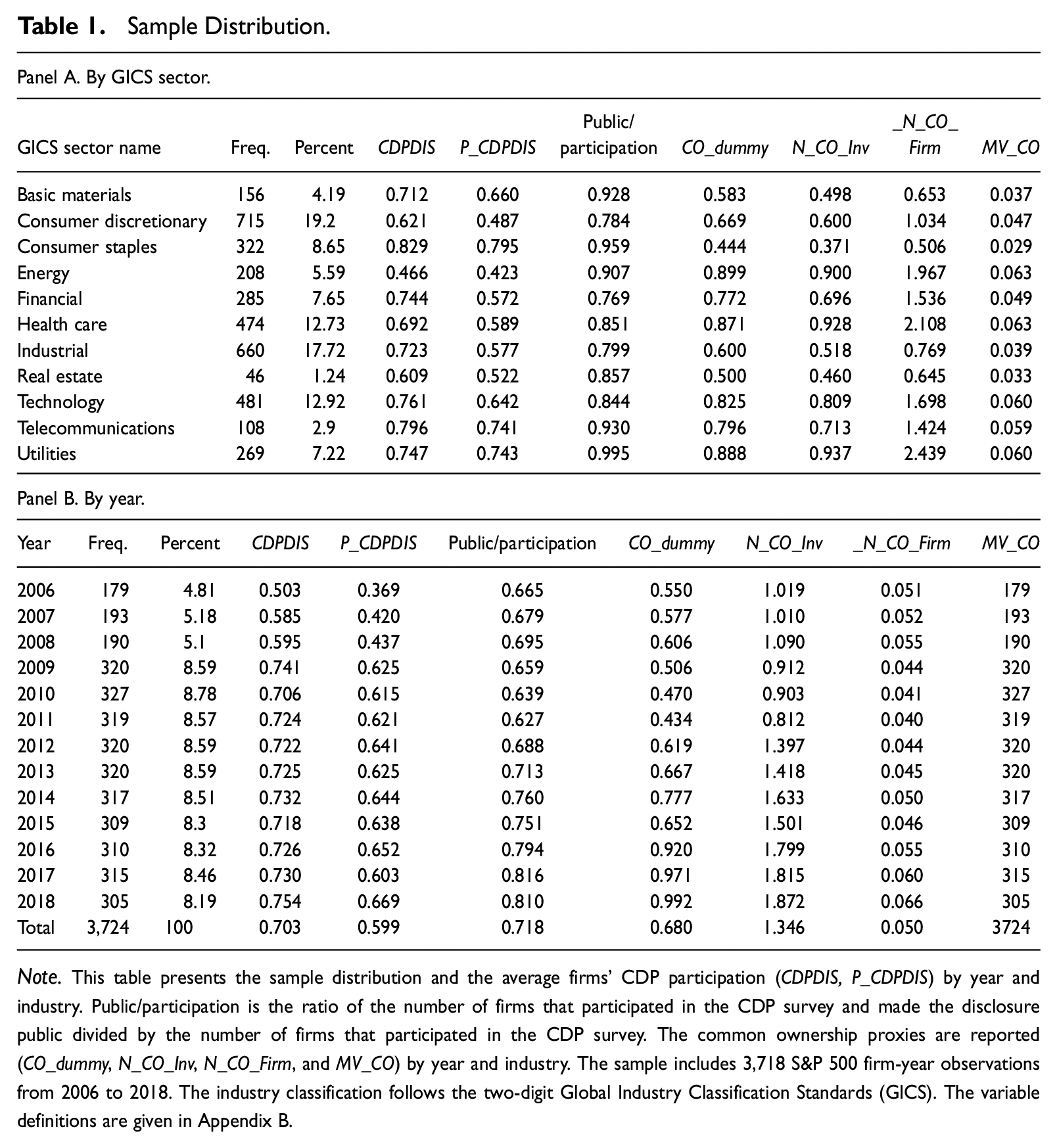

Panel A of Table 1 shows the sample distribution by GICS sector. The largest sector is consumer discretionary, followed by the industrial sectors. The smallest number of observations is from the real estate and telecommunications sectors. When the proportion of companies providing CDP disclosures is considered, energy—a heavy-emitting sector—has the lowest participation rate of 46.6%. In contrast, the consumer staples sector has a participation rate of 82.9%. The decision to make the firm’s carbon report publicly available depends on the sector and ranges from 78.4% (consumer discretionary) to 99.5% (utilities). Common ownership also varies among sectors; for example, 44.4% of the firms in consumer staples have common ownership, and 89.9% of the firms in sectors, such as energy have common ownership. Panel B of Table 1 shows the sample distribution by year. In the early years of our sample, the number of firms that participate is only half that in the sample, whereas from 2009, this number increases to 70% or more. The common ownership values also steadily increase throughout the years. The number of investors and firms and the market value of common ownership have an upward trend over our sample period.

Sample Distribution.

Note. This table presents the sample distribution and the average firms’ CDP participation (CDPDIS, P_CDPDIS) by year and industry. Public/participation is the ratio of the number of firms that participated in the CDP survey and made the disclosure public divided by the number of firms that participated in the CDP survey. The common ownership proxies are reported (CO_dummy, N_CO_Inv, N_CO_Firm, and MV_CO) by year and industry. The sample includes 3,718 S&P 500 firm-year observations from 2006 to 2018. The industry classification follows the two-digit Global Industry Classification Standards (GICS). The variable definitions are given in Appendix B.

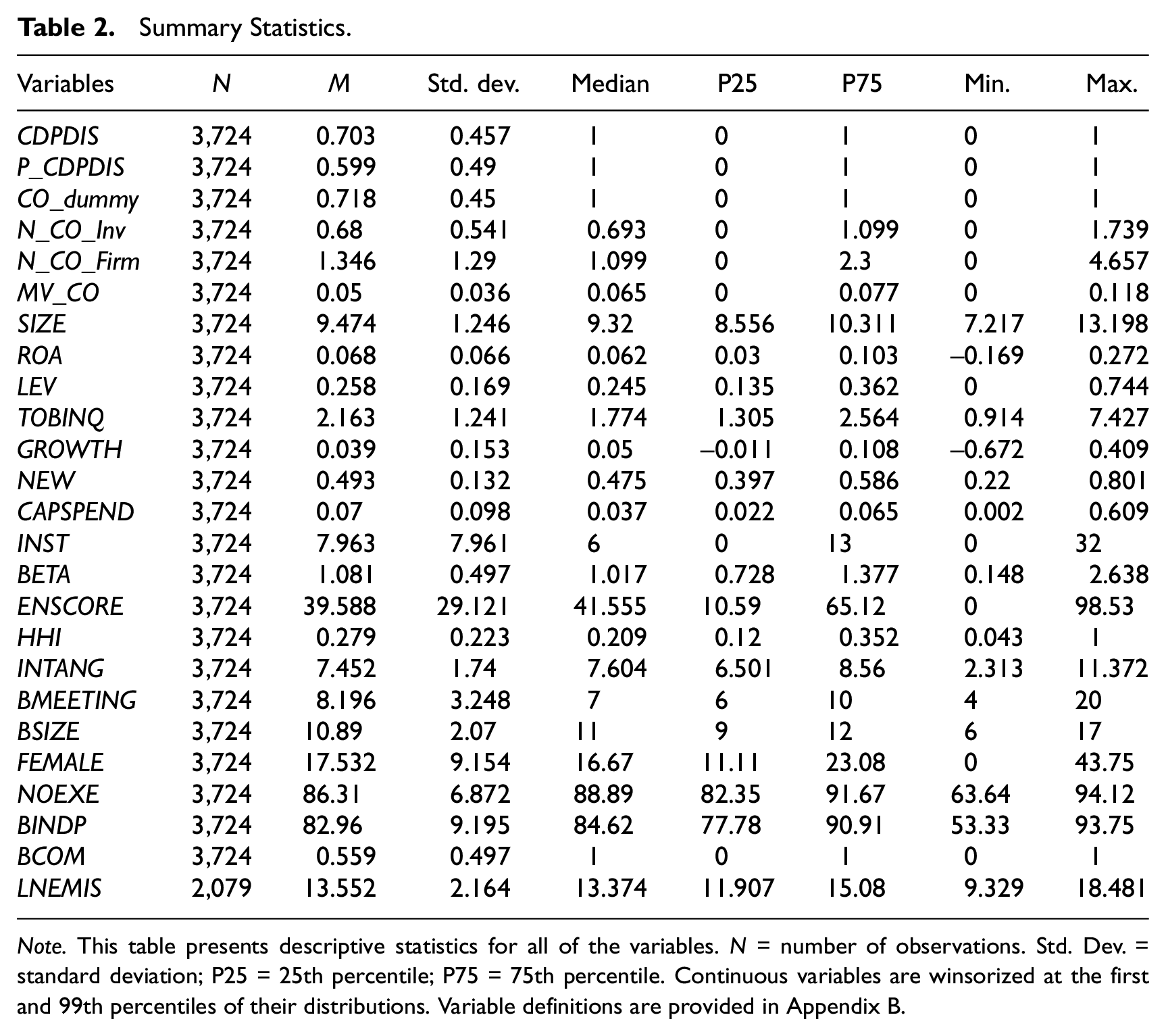

Table 2 shows the summary statistics. Our disclosure decision variables (i.e., CDPDIS and P_CDPDIS) show that approximately 70.3% of our sample firms participate in the CDP, and 59.9% of them make the information public. On average, 71.8% of firms have at least one common owner, and the average number of common owners for all sample firms is approximately one, where they hold approximately 2.84 firms together. The average market value of shares held by common owners is approximately U.S.$1 billion.

Summary Statistics.

Note. This table presents descriptive statistics for all of the variables. N = number of observations. Std. Dev. = standard deviation; P25 = 25th percentile; P75 = 75th percentile. Continuous variables are winsorized at the first and 99th percentiles of their distributions. Variable definitions are provided in Appendix B.

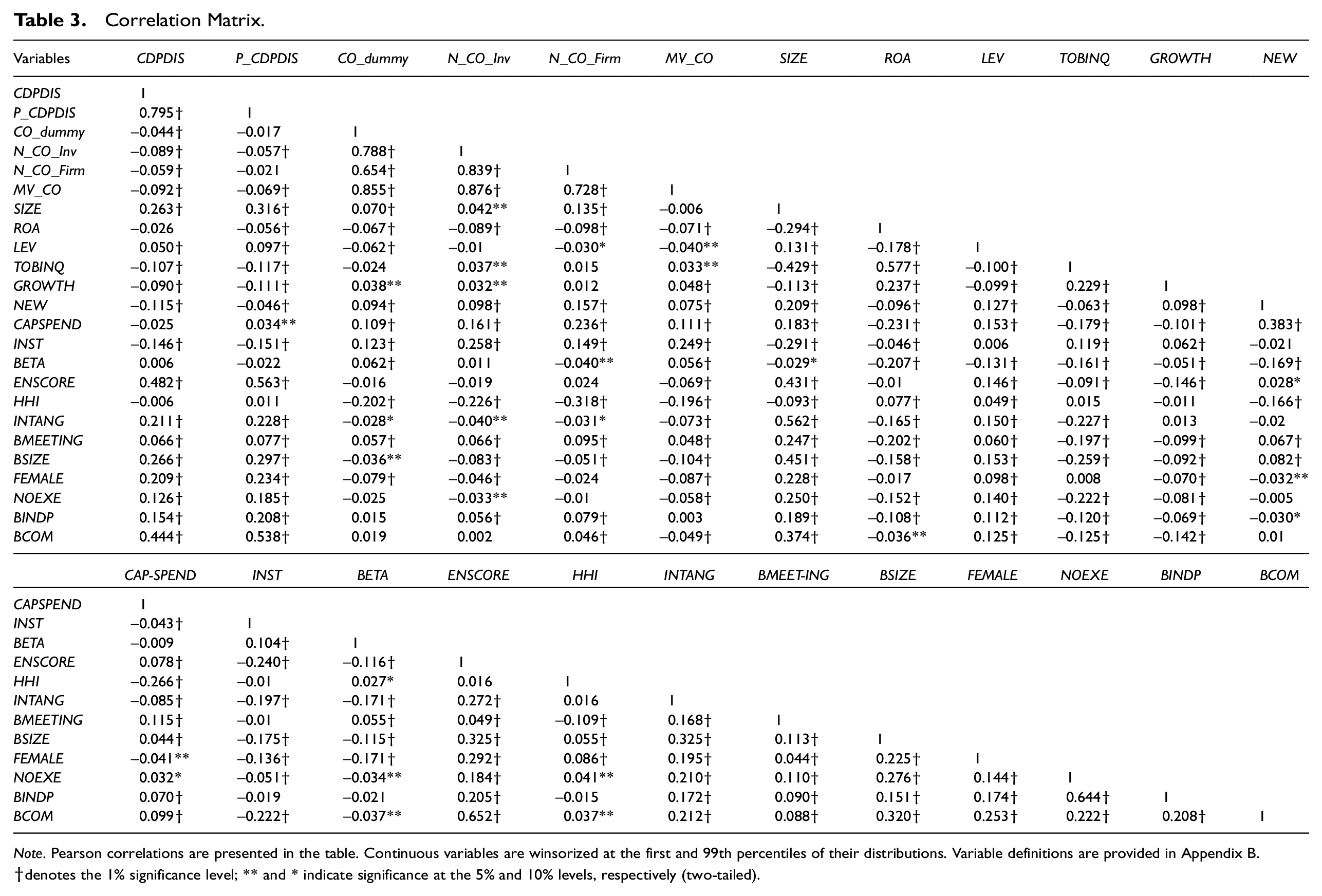

The correlation matrix of the variables used in our main analysis is presented in Table 3. The correlations between our CDP disclosure variable and common ownership variables are negative and statistically significant, suggesting that common ownership decreases a firm’s propensity to disclose carbon-related information. For the control variables, firm size, leverage, environmental performance scores, and corporate governance variables have a positive relationship with corporate carbon disclosure. On the other hand, growth potential, net investment in PPE, and the percentage of institutional ownership have a negative and statistically significant relationship with the propensity to disclose.

Correlation Matrix.

Note. Pearson correlations are presented in the table. Continuous variables are winsorized at the first and 99th percentiles of their distributions. Variable definitions are provided in Appendix B.

denotes the 1% significance level; ** and * indicate significance at the 5% and 10% levels, respectively (two-tailed).

Test of Hypothesis H1

Main Analysis

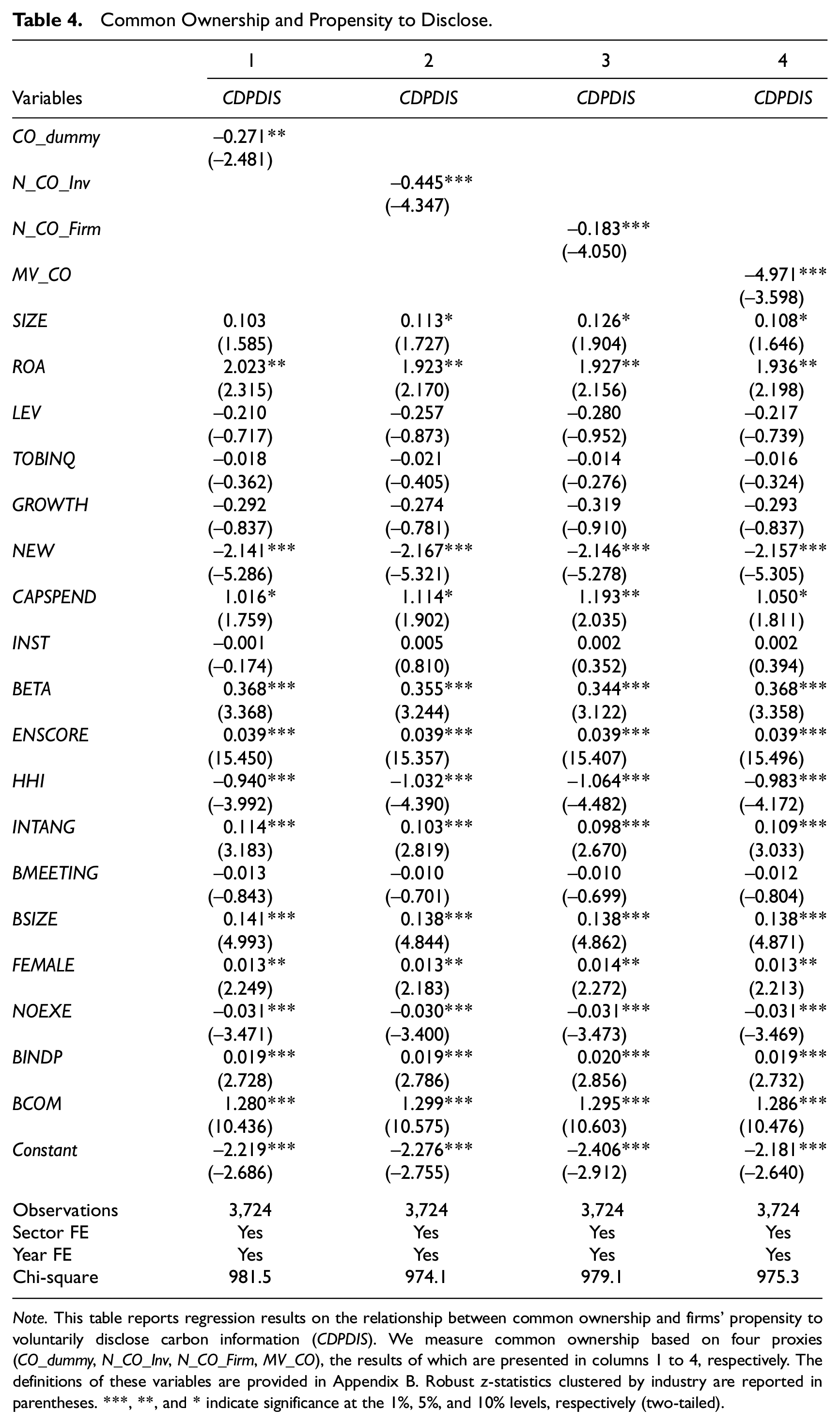

The results of estimating Equation (1) are presented in Table 4. The four common ownership proxies, that is, CO_dummy, N_CO_Inv, N_CO_Firm, and MV_CO, are presented in columns 1 to 4. We find that all proxies have negative and statistically significant results (coeff. = −0.271, −0.445, −0.183, and −4.971, respectively) at the 1% level, except for CO_dummy, for which the coefficient is significant at the 5% level. Regarding economic significance, a one standard deviation change in either of the four proxies results in a decrease in a firm’s propensity to disclose carbon information by 19.4%, on average. 5 Thus, we establish that common ownership has a statistically and economically significant negative impact on firms’ decision to participate in CDP reports, rejecting the null hypothesis, H1. Park et al. (2019) find that firms become less concerned about proprietary information when providing voluntary disclosure in the presence of common owners, as their competing peer firms would not use this information to gain market share at the expense of the disclosing firm. We find that this result does not hold when voluntary disclosure is related to carbon-related information. As common ownership lessens competition, the net benefit of gaining stakeholder support via voluntary carbon disclosure decreases. In particular, as common owners hold a significant number of shares within each firm, the disclosure of carbon information could create unintended scrutiny from external stakeholders (Bolton & Kacperczyk, 2021). Accordingly, common owners may coordinate cross-held firms to reduce potential costs associated with voluntary carbon disclosures by opting not to participate in the CDP and to hide carbon-related information that can be politically sensitive.

Common Ownership and Propensity to Disclose.

Note. This table reports regression results on the relationship between common ownership and firms’ propensity to voluntarily disclose carbon information (CDPDIS). We measure common ownership based on four proxies (CO_dummy, N_CO_Inv, N_CO_Firm, MV_CO), the results of which are presented in columns 1 to 4, respectively. The definitions of these variables are provided in Appendix B. Robust z-statistics clustered by industry are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively (two-tailed).

For controls, we find that size and past performance are positively related to carbon disclosure. This finding is consistent with larger firms being exposed to increased stakeholder pressure and their need to be active in disclosing carbon initiatives and information. Although capital expenditures have a statistically significant and positive coefficient, investment in new Property, Plant, and Equipment (PPE) has a negative coefficient. Overall, financial controls demonstrate that firms with more financial slack and capacity are more likely to afford extra resources and commit to carbon disclosures. The beta has a positive coefficient, which is consistent with the argument that lower firm risk is linked to better environmental outcomes for a company (Luo & Tang, 2021). The results show that higher environmental scores and stronger corporate governance are positively linked to firms’ decisions to disclose carbon-related information. In line with our conjecture that less competitive markets offer weaker incentives for firms to participate in carbon disclosure, the H–H index has a negative and statistically significant coefficient.

Robustness Checks

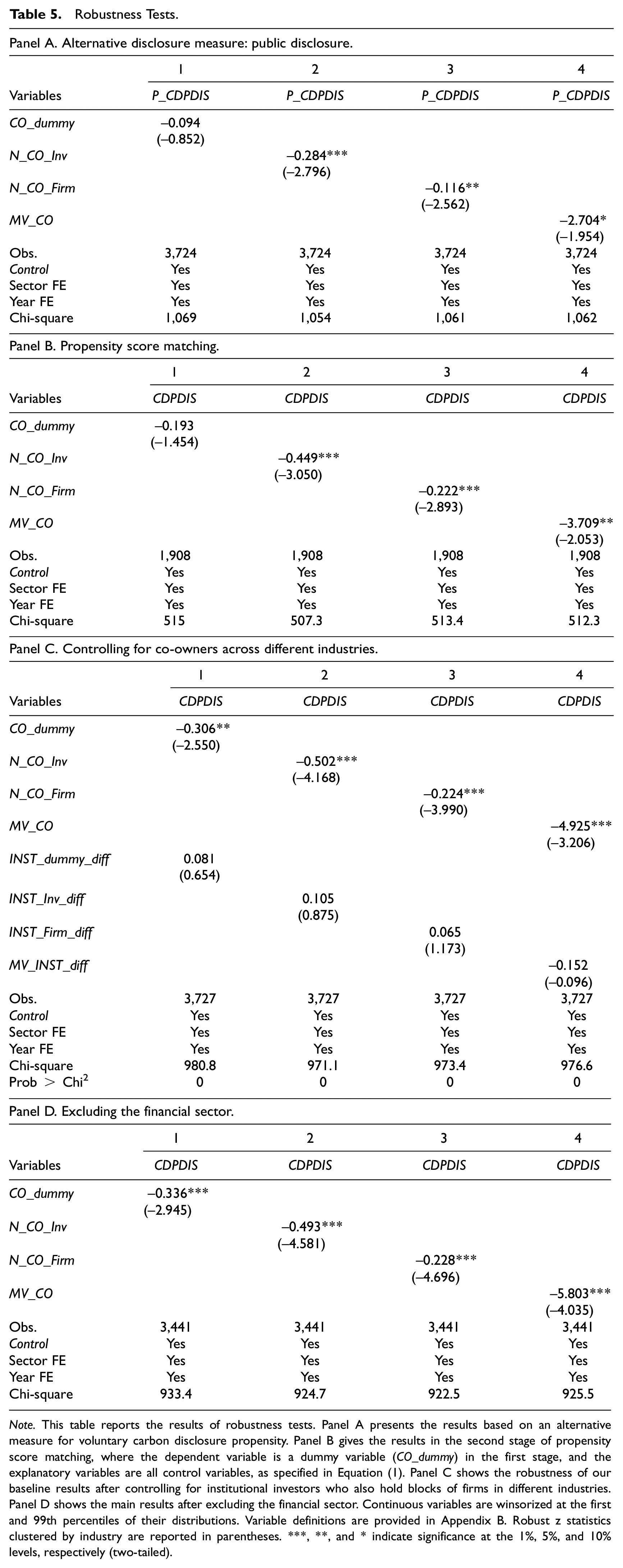

Table 5 provides the results of several robustness tests to further validate our main results. First, we use an alternative measure of a firm’s propensity to publicly disclose carbon information by re-estimating Equation (1). We employ the dummy variable for public disclosure (P_CDPDIS) as the dependent variable. Firms may choose to communicate their carbon-related information by making such information public via CDP rather than limiting information access to only CDP signatories. A comparison of CDPDIS with P_CDPDIS indicates that approximately 86% of the CDP participants decided to make their information available to the public. We test whether common ownership also explains firms’ decision to publicly disclose their information. The results, given in Panel A, are qualitatively similar to our main results shown in Table 4. The three common ownership variables, namely, number of investors, number of cross-held firms, and market value of total common ownership, are significantly negatively related to a firm’s likelihood of making public carbon disclosures. The average decline in the likelihood of publicly disclosing carbon information is −13.3% across the three statistically significant measures when either of the variables changes by one standard deviation.

Robustness Tests.

Note. This table reports the results of robustness tests. Panel A presents the results based on an alternative measure for voluntary carbon disclosure propensity. Panel B gives the results in the second stage of propensity score matching, where the dependent variable is a dummy variable (CO_dummy) in the first stage, and the explanatory variables are all control variables, as specified in Equation (1). Panel C shows the robustness of our baseline results after controlling for institutional investors who also hold blocks of firms in different industries. Panel D shows the main results after excluding the financial sector. Continuous variables are winsorized at the first and 99th percentiles of their distributions. Variable definitions are provided in Appendix B. Robust z statistics clustered by industry are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively (two-tailed).

Panel B reflects the adoption of the PSM approach to address endogeneity issues, acknowledging that both carbon disclosure and common institutional ownership might stem from unobservable firm characteristics. In line with previous studies (Nizar et al., 2024), we estimate the propensity scores using a logit model, whereby the dependent variable is a dummy variable (CO_dummy) in the first stage, and the explanatory variables are all control variables, as specified in Equation (1). Specifically, we match each treatment firm (where CO_dummy equals 1) to a control firm (where CO_dummy equals 0) based on the nearest propensity score, using a caliper of 0.03, and without replacement. The regression results in the second stage using the PSM sample, presented in Panel B, indicate that the coefficients for the three common ownership proxies (N_CO_Inv, N_CO_Firm, and MV_CO) remain significantly negative. These findings generally corroborate our baseline results.

Panel C reflects a test of whether our main results are robust after controlling for institutional investors who have holdings in different industries. Institutional blockholders can monitor corporate operations more effectively when they have multiple blockholdings (Kang et al., 2018). Our variables for common ownership may capture the effects of institutional investors who hold multiple stocks across industries. To test the effect of common ownership within the industry separately, we construct control variables for institutional investors who own shares of noncompeting firms in relation to a focal firm, that is, firms from different industries. Following Park et al. (2019), we assign a value of 1 for INST_dummy_diff if a firm has at least one institutional investor that also holds ownership in industries outside of the focal firm’s sector. Accordingly, additional control variables, such as INST_Inv_diff, INST_Firm_diff, and INST_diff, are constructed in a manner similar to our main common ownership variables but with a focus on ownership in noncompeting firms. The detailed definitions of these variables are provided in Appendix B. The results are consistent with our main findings from Table 4. In addition, these control variables for institutional ownership across different industries have no impact on the disclosure practices of the focal firm, suggesting that within-industry common ownership is the primary explanation for the decrease in carbon disclosures.

Panel D presents the results when the financial sector is excluded. As financial firms are typically not subject to carbon-related regulations, the number of financial firms that do not participate in the CDP survey may be greater than that of firms in other industries. We exclude the financial sector and rerun the main regressions. After excluding 68 firm-year observations from the financial sector, our results support our main findings in Table 4 that common ownership reduces the chances firms will participate in the CDP, leading to less emissions information being provided to the market.

Moderating Effect of the Carbon-Intensive Sector

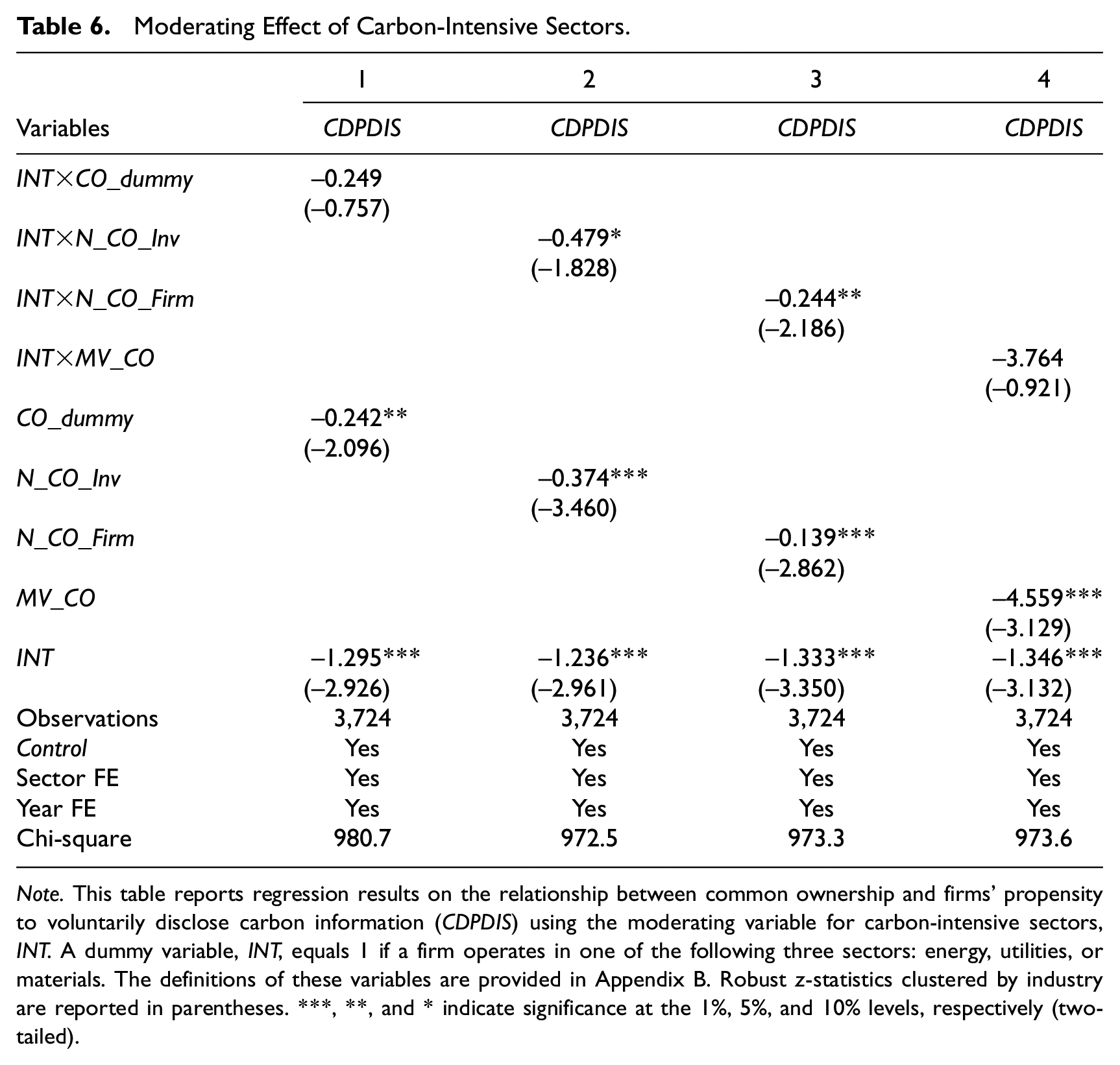

In this section, we examine the moderating effect of the carbon-intensive sector on the negative association between common ownership and carbon disclosure. Firms in carbon-intensive sectors face greater scrutiny from regulators, activists, and the public due to their significant environmental impact. Common owners in these sectors may prioritize minimizing regulatory burdens and attempt to avoid corporate disclosure, which can attract negative attention or regulatory actions that might be costly or detrimental to their operations. Accordingly, common ownership in carbon-intensive sectors might create a mutual understanding or informal agreements among peer firms to withhold detailed carbon information. Furthermore, in carbon-intensive sectors, the financial implications of transitioning to low-carbon operations are substantial. Common owners would be concerned that extensive carbon disclosures highlight the financial risks associated with necessary investments in cleaner technologies, potentially negatively affecting stock prices and investor perceptions. Given that carbon-intensive sectors are more sensitive to policy changes and shifts in public opinion regarding climate change, common owners may believe that less disclosure reduces the risk of market volatility in response to negative environmental news or regulatory changes aimed at reducing carbon emissions. Therefore, we expect that the negative association between common ownership and carbon disclosure is stronger for firms operating in carbon-intensive sectors than for other firms.

We define the carbon-intensive sector, INT, as a dummy variable that equals 1 if a firm operates in one of the following three GICS two-digit sectors: energy, utilities, and materials. We then interact this variable with our four common ownership proxies and add these interaction variables to our baseline regression model. Table 6 reports the results of this moderating effect. As shown, the coefficients of INT × N_CO_Inv and INT × N_CO_Firm are negative and significant, indicating a stronger negative association between common ownership and carbon disclosure in these sectors. However, the coefficients for INT×CO_dummy and INT×MV_CO, while still negative, are not statistically significant. Overall, the results support our arguments that common owners tend to see diminished financial advantages for their portfolio companies in carbon-intensive sectors by making extensive carbon disclosures.

Moderating Effect of Carbon-Intensive Sectors.

Note. This table reports regression results on the relationship between common ownership and firms’ propensity to voluntarily disclose carbon information (CDPDIS) using the moderating variable for carbon-intensive sectors, INT. A dummy variable, INT, equals 1 if a firm operates in one of the following three sectors: energy, utilities, or materials. The definitions of these variables are provided in Appendix B. Robust z-statistics clustered by industry are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively (two-tailed).

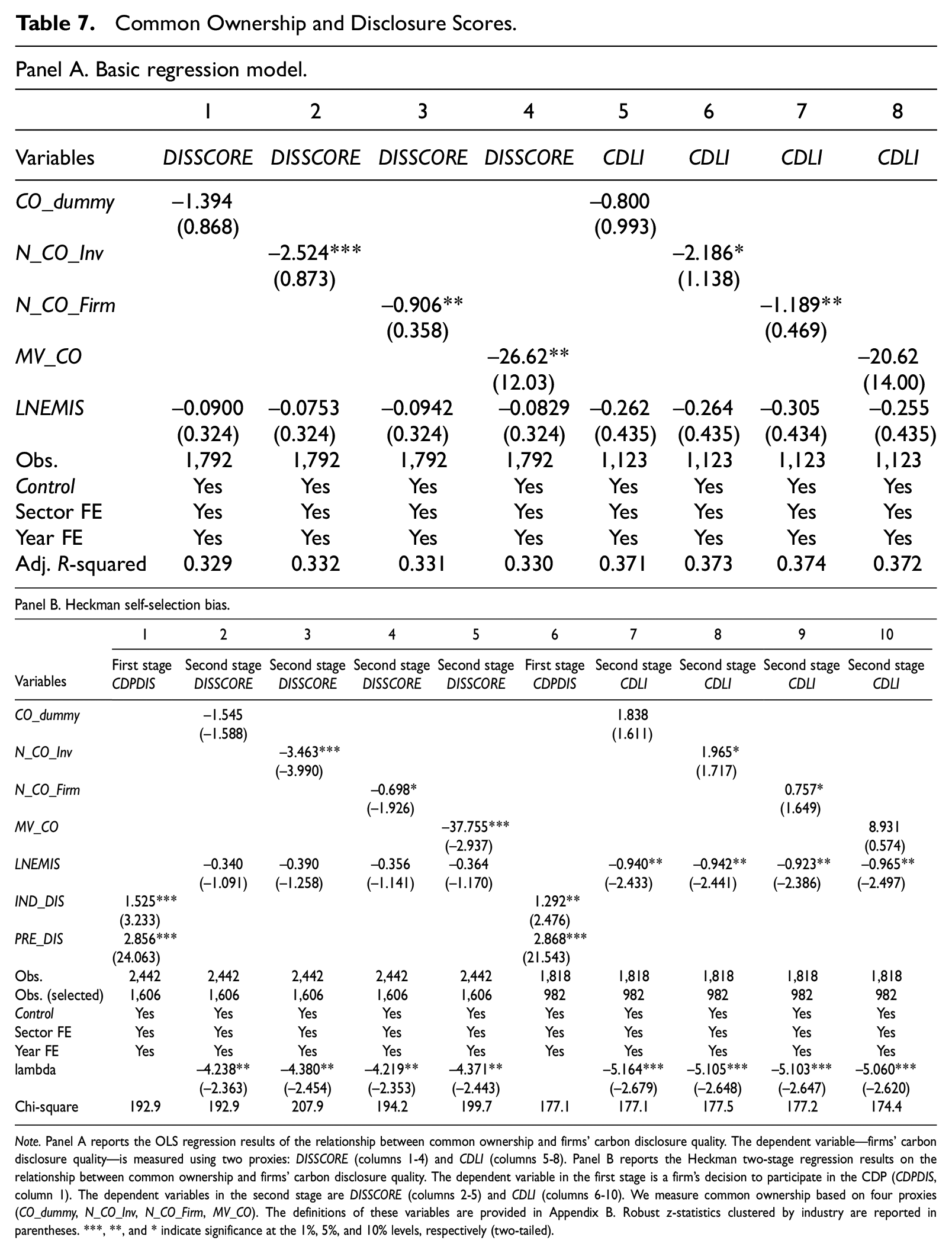

Test of Hypothesis H2

Next, we estimate Equation (2) using disclosure scores and present the results in Panel A of Table 7. 6 The first four columns employ standardized scores (DISSCORE) for our entire sample period, whereas the next four columns use the original CDP score provided by the CDP until 2015 (CDLI) based on our subsample before CDP changed its scoring system to performance bands. Consistent with Table 4, common ownership proxies have negative coefficients across models, which are statistically significant at the 1% level for the number of common investors and at the 5% level for the number of cross-held firms and the market value of common ownership. The coefficient of the common ownership dummy has a negative sign but is nonsignificant, which may suggest that it is not merely the existence of common ownership that deteriorates the quality of carbon reporting but rather the influence of common owners proxied by the number of common investors and cross-held firms and the value held by common owners that affects the scores. This finding is in line with the results given in Table 4, where the more influential common owners are, the more reluctant firms are to publish carbon information.

Common Ownership and Disclosure Scores.

Note. Panel A reports the OLS regression results of the relationship between common ownership and firms’ carbon disclosure quality. The dependent variable—firms’ carbon disclosure quality—is measured using two proxies: DISSCORE (columns 1-4) and CDLI (columns 5-8). Panel B reports the Heckman two-stage regression results on the relationship between common ownership and firms’ carbon disclosure quality. The dependent variable in the first stage is a firm’s decision to participate in the CDP (CDPDIS, column 1). The dependent variables in the second stage are DISSCORE (columns 2-5) and CDLI (columns 6-10). We measure common ownership based on four proxies (CO_dummy, N_CO_Inv, N_CO_Firm, MV_CO). The definitions of these variables are provided in Appendix B. Robust z-statistics clustered by industry are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively (two-tailed).

The results for the subsample given in columns 5 to 8 confirm the overall negative effects of common ownership on firms’ disclosure quality, although the statistical significance weakens. This could be attributable to our subsample, which mainly covers the early years of the CDP data period, when less attention is paid to corporate carbon disclosures. In columns 1 to 4, a one standard deviation change in either of the three common ownership variables results in a decrease in the disclosure score, ranging from −1.4% to −2.0%. Overall, we find that common ownership has a negative impact on carbon disclosure quality, again rejecting the null hypothesis, H2.

For the control variables, we find that a firm’s carbon emissions (LNEMIS) decrease its disclosure quality because high polluters are less likely to disclose the full scale of their environmental impacts (Luo, 2019). Consistent with Table 4, we find that larger firms and firms with high environmental scores provide better-quality disclosures. In addition, Tobin’s Q, capital expenditure, and the level of total institutional ownership (INST) increase a firm’s disclosure quality.

Carbon disclosure scores can be observed only if a firm voluntarily participates in the CDP. Such voluntary participation may introduce selection bias to our sample if a certain type of firm elects to participate. To control for this, we adopt a Heckman two-stage model and present the results in Panel B. The first step is to estimate the likelihood of participating in the CDP survey using Equation (1) as a base model. Then, following Matsumura et al. (2014), we include the following two new instrumental variables (IVs) in the equation: (a) the proportion of firms in an industry that participate in the CDP to capture the participation rate of industry peers (IND_DIS) and (b) a dummy variable that equals 1 if a firm reports its carbon emissions to CDP in the prior year (PRE_DIS). When choosing these IVs, we need to ensure that they meet both relevance and exogeneity criteria. The first IV, IND_DIS, is deemed exogenous because it reflects broader industry trends rather than the specific actions or characteristics of individual firms. Its relevance stems from the social and competitive pressures within industries; as more firms disclose their carbon emissions, it generates normative pressure on nondisclosing firms to also engage in disclosure. This dynamic helps to avoid negative perceptions among stakeholders, making IND_DIS a critical factor in understanding firm-level disclosure behavior. The second IV, PRE_DIS, captures the persistence of disclosure behavior over time, based on the premise that firms that engage in disclosure once are more likely to continue doing so. The rationale behind this variable’s exogeneity lies in its basis on past behavior that, although influenced by a firm’s internal decision-making processes, offers a predictable pattern that is distinct from the influences driving current-year disclosures. Overall, these variables fulfill the exogeneity criterion by being external to the firm’s current decision-making process or outcomes in the Heckman model while directly influencing the likelihood of participating in carbon disclosure practices. Columns 1 to 5 show the converted disclosure scores for the entire sample, whereas columns 6 to 10 depict the percentile scores until 2015. The results shown in Panel B are consistent with our findings from Panel A in that the four common ownership variables have a negative association with disclosure scores. The inverse Mills ratios from the first-stage Heckman regression are statistically significant at the 1% level for all columns, confirming that selection bias exists in the first stage.

Additional Tests

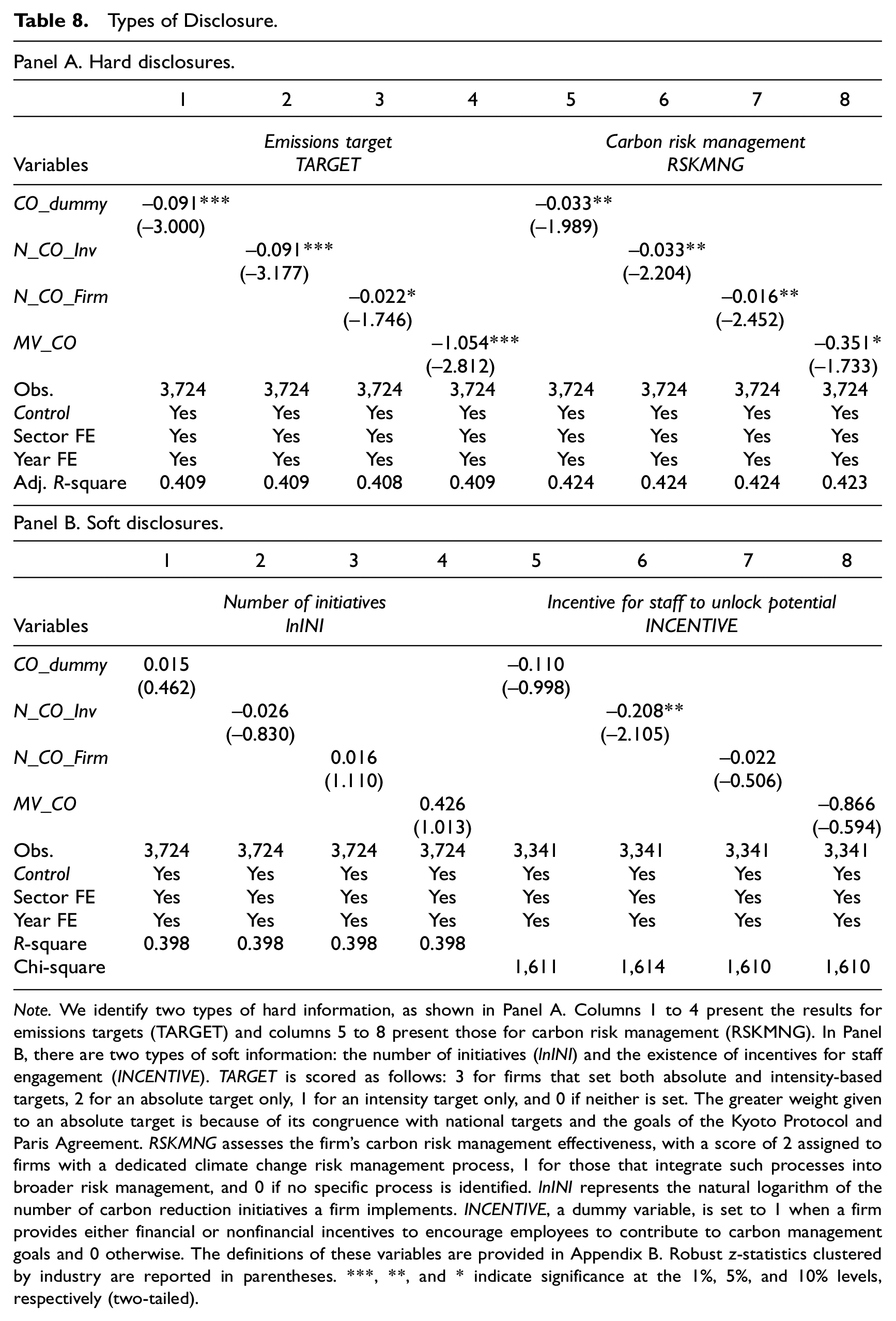

Type of Disclosures

In this section, we further investigate the motivations that may cause common ownership to discourage corporate carbon disclosures. One possible explanation is an attempt to avoid potential costs associated with providing disclosures and fulfilling commitments in carbon management and control. This suggests that common owners are less likely to incentivize the firms they hold to share hard information, which is observable and verifiable by external stakeholders. For instance, setting clear emissions targets could attract unnecessary public scrutiny. Moreover, firms may face adverse consequences if they fail to meet these targets. In contrast, soft disclosures tend to consist of vague and ambiguous information. For example, one of the survey questions in the CDP requires participating firms to disclose any emissions reduction initiatives that were active during the reporting year, including the total number of initiatives at various stages of development. This question does not differentiate the importance or scale of initiatives, making it challenging for external stakeholders to verify them. As a result, companies can report any number of initiatives without needing to consider the significance of their investments, enabling company managers to potentially inflate the number of disclosed initiatives to enhance stakeholders’ perceptions of their commitment to carbon neutrality.

Following Clarkson et al. (2008), we identify two types of hard information, namely, emissions targets (TARGET) and carbon risk management (RSKMNG), and two types of soft information, namely, the number of initiatives (lnINI) and the existence of incentives for staff engagement (INCENTIVE). 7

We score TARGET as follows: 3 for firms that set both absolute and intensity-based targets, 2 for an absolute target only, 1 for an intensity target only, and 0 if neither is set. The greater weight given to an absolute target is because of its congruence with national targets and the goals of the Kyoto Protocol and Paris Agreement. RSKMNG assesses the effectiveness of the firm’s carbon risk management, with a score of 2 assigned to firms with a dedicated climate change risk management process, 1 for those that integrate such processes into broader risk management, and 0 if no specific process is identified. Emissions targets can influence capital allocation, operational processes, and innovation strategies, while effective carbon risk management practices can mitigate financial risks associated with climate change. Information on emissions targets and carbon risk management practices is considered hard information because it is quantifiable, more directly observable, and often based on specific, measurable criteria that can be independently verified. For instance, emissions targets can be defined in absolute terms (e.g., tons of CO2-equivalent emissions to be reduced) or intensity targets (e.g., emissions per unit production), making it possible to assess a firm’s performance against these objectives. Similarly, carbon risk management practices can be evaluated based on whether a firm has specific processes in place and the extent to which these practices are integrated into its overall risk management framework.

lnINI represents the natural logarithm of the number of carbon reduction initiatives a firm has implemented. INCENTIVE, a dummy variable, is set to 1 when a firm provides either financial or nonfinancial incentives to encourage employees to contribute to carbon management goals and 0 otherwise. Companies may emphasize their carbon reduction initiatives or incentives for employees to improve their brand image and appeal to environmentally conscious consumers, investors, and other stakeholders, even when these efforts are not matched by significant environmental benefits. Their subjective nature makes it more difficult for external parties to verify the actual implementation or effectiveness of the reported initiatives and incentives. This verification challenge provides companies with an opportunity to use the information in crafting a green image without the risk of being detected by observable facts.

We conduct separate regressions for these four types of disclosure and examine the relationship between common ownership variables and each category. The results for hard disclosures are presented in Panel A of Table 8, whereas those for soft disclosures are given in Panel B. In line with our expectation, the negative impact of common ownership on carbon disclosures is more pronounced for hard than soft disclosure categories. These results indicate that common owners leverage their influence on steering firms toward disclosing less information on the hard aspects of carbon reduction commitment and management. By doing so, they can mitigate potential political and operational costs by avoiding scrutiny and verification from external stakeholders.

Types of Disclosure.

Note. We identify two types of hard information, as shown in Panel A. Columns 1 to 4 present the results for emissions targets (TARGET) and columns 5 to 8 present those for carbon risk management (RSKMNG). In Panel B, there are two types of soft information: the number of initiatives (lnINI) and the existence of incentives for staff engagement (INCENTIVE). TARGET is scored as follows: 3 for firms that set both absolute and intensity-based targets, 2 for an absolute target only, 1 for an intensity target only, and 0 if neither is set. The greater weight given to an absolute target is because of its congruence with national targets and the goals of the Kyoto Protocol and Paris Agreement. RSKMNG assesses the firm’s carbon risk management effectiveness, with a score of 2 assigned to firms with a dedicated climate change risk management process, 1 for those that integrate such processes into broader risk management, and 0 if no specific process is identified. lnINI represents the natural logarithm of the number of carbon reduction initiatives a firm implements. INCENTIVE, a dummy variable, is set to 1 when a firm provides either financial or nonfinancial incentives to encourage employees to contribute to carbon management goals and 0 otherwise. The definitions of these variables are provided in Appendix B. Robust z-statistics clustered by industry are reported in parentheses. ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively (two-tailed).

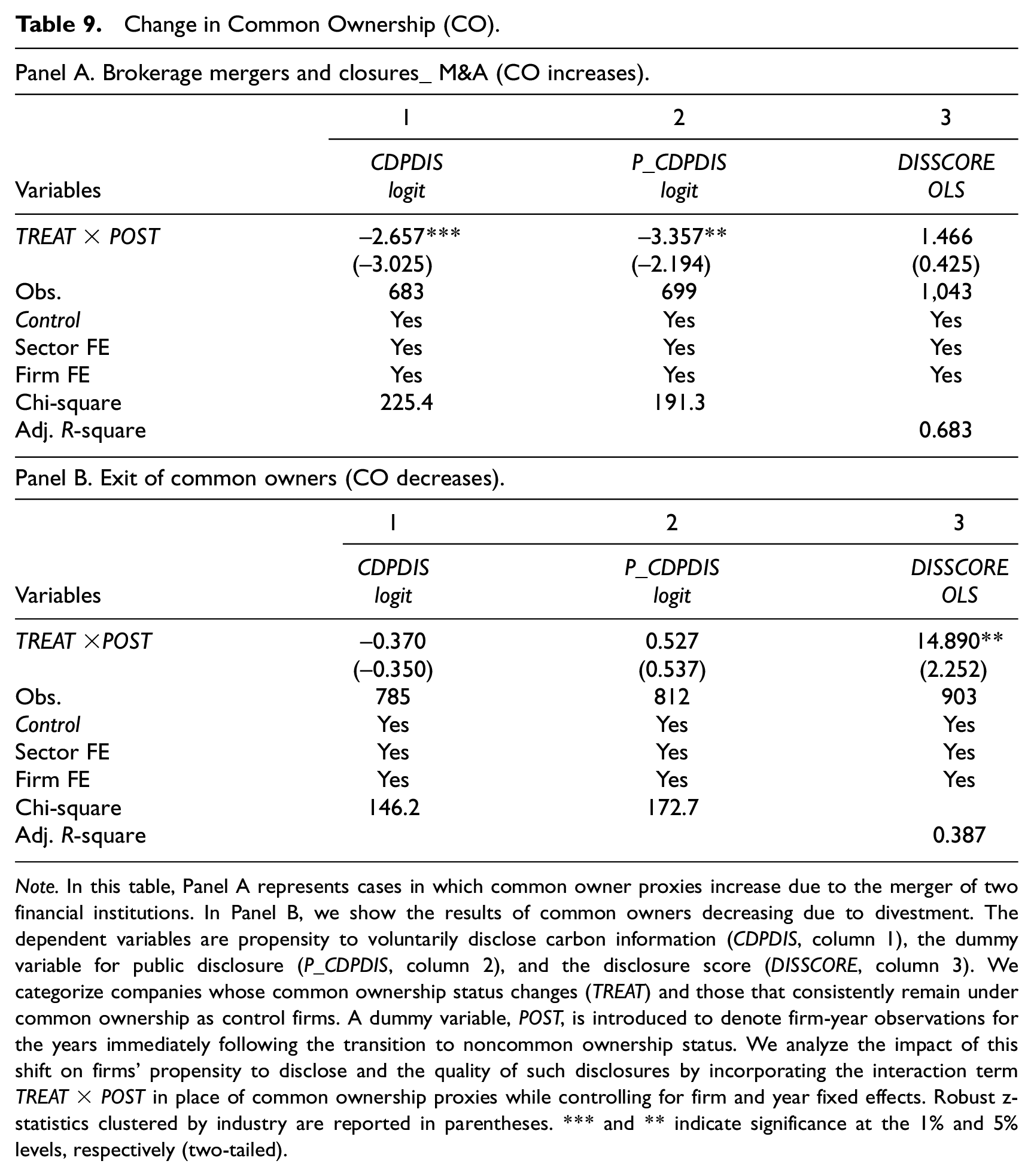

Change in Common Ownership

Next, we test whether our hypothesized relationship still holds when there is a change in common ownership. In particular, we separately examine cases in which common ownership increases and decreases. In both tests, we categorize companies whose common ownership status changes as treatment firms (TREAT) and those that consistently remain under common ownership as control firms. A dummy variable, POST, is introduced to denote firm-year observations for the years immediately following the year of changes in common ownership. We analyze the impact of this shift on firms’ propensity to disclose and the quality of such disclosures by incorporating the interaction term TREAT × POST in place of common ownership proxies while controlling for firm and year fixed effects.

In the first case, we use brokerage house mergers and closures to investigate exogenous cases in which common ownership increases. We closely follow Park et al. (2019) and use the blockholding information of financial institutions one quarter prior to the merger. In our setting, the treatment group includes cases in which one of the merging financial institutions is a blockholder of the focal firm and the other financial institution is not a blockholder of the focal firm but is a blockholder of a peer firm in the same industry. However, neither institution is a common owner of the focal firm before the merger. As a result of the merger, the merging institution becomes a blockholder of two competing firms in the same industry, becoming a new common owner of the treated firm (i.e., increased common ownership). The control group is made up of cases in which a control firm is held by the same blockholder as the treated firm; however, the merger does not change common ownership, as a financial institution being merged does not hold blocks of any peer firms in the industry of the control firm. The results of the TREAT × POST interaction in Panel A of Table 9 show that firms are less likely to participate in the CDP and less likely to make public carbon disclosures when an exogenous merger and closure event increases common ownership. This result supports our main finding that common ownership reduces the voluntary carbon disclosures of cross-held firms. However, we find no difference in disclosure scores, which suggests that treated firms opt to forgo providing any information by stopping the provision of CDP disclosures.

Change in Common Ownership (CO).

Note. In this table, Panel A represents cases in which common owner proxies increase due to the merger of two financial institutions. In Panel B, we show the results of common owners decreasing due to divestment. The dependent variables are propensity to voluntarily disclose carbon information (CDPDIS, column 1), the dummy variable for public disclosure (P_CDPDIS, column 2), and the disclosure score (DISSCORE, column 3). We categorize companies whose common ownership status changes (TREAT) and those that consistently remain under common ownership as control firms. A dummy variable, POST, is introduced to denote firm-year observations for the years immediately following the transition to noncommon ownership status. We analyze the impact of this shift on firms’ propensity to disclose and the quality of such disclosures by incorporating the interaction term TREAT × POST in place of common ownership proxies while controlling for firm and year fixed effects. Robust z-statistics clustered by industry are reported in parentheses. *** and ** indicate significance at the 1% and 5% levels, respectively (two-tailed).

Second, we examine cases in which common owners divest the firm, i.e., common ownership decreases. We focus on a subset of companies that remain under common ownership for the entire sample period and those that experience a transition from having common ownership to not having common ownership within a year during the study period. Companies whose common ownership status changes multiple times are excluded from our analysis for a clear comparison between treatment and control groups. The findings, presented in Panel B of Table 9, reveal that decreases in common ownership do not significantly influence the likelihood of carbon disclosure. However, when focusing on disclosure quality, the TREAT × POST interaction has a positive and significant effect. This suggests that firms improve their disclosure quality following the divestment of common owners rather than initiating new carbon disclosures. This pattern may be attributable to the substantial resources required to initiate carbon reporting as part of the CDP for the first time, whereas enhancing the quality of existing disclosures may be more feasible for firms following divestment.

Conclusion

We use CDP data to measure a firm’s decision to disclose carbon-related information and find that common ownership, proxied by its existence, the number of common owners, the number of cross-held firms, and its market value, has a negative impact on the propensity to disclose carbon information. A one standard deviation increase in these common ownership measures decreases a firm’s likelihood of participating in the CDP survey by as much as 19.4%. This result is robust to using public carbon disclosures as an alternative dependent variable, PSM, controlling for institutional investors who have holdings in different industries, and excluding the financial sector. The negative impact of common ownership on voluntary carbon disclosure is more pronounced in carbon-intensive sectors. Even for firms that participate in the CDP survey, their disclosure quality scores decrease when the number of common owners, number of cross-held firms, and market value of common ownership increase. When specific types of carbon information disclosure are considered, the negative association between common ownership and carbon disclosures is stronger for hard disclosures, which require a firm to make substantial investments in carbon reduction, than for soft disclosures, which contain information that is difficult for external stakeholders to verify. In addition, we find consistent results for cases that lead to changes in common ownership. After a merger and closure event with an increase in common ownership, a firm’s likelihood of providing voluntary carbon disclosure decreases, whereas a firm’s carbon disclosure quality increases following the divestment of common owners.

In the past three decades, the ownership concentration of public firms has increased significantly. A substantial proportion of public firm stock in the United States is owned by a small group of large institutional investors, increasing the number of competing firms controlled by the same institutional investors. When common ownership exists, the competition within the industry decreases. Reduced competitive pressure may have positive effects on firm operations via enhanced market collaboration and result in improved financial disclosures. However, how common ownership affects firms’ unregulated nonfinancial disclosures has not been fully explored in the literature. In that sense, our results provide implications to investors and other stakeholders that firms are reluctant to disclose their carbon-related information when controlled by common owners. The carbon information of individual firms may initiate unwanted scrutiny by regulators and other external stakeholders, such as nongovernmental organizations (NGOs) and activist groups. Firms are less motivated to disclose such information, especially when the pressure to disclose nonfinancial information from their major shareholders is reduced. Our findings are also of interest to regulators and standard setters. The world’s leading countries, including the G7 countries, are considering a mandatory climate change disclosure framework for companies. For instance, in March 2022, the U.S. Securities and Exchange Commission (SEC) proposed a new requirement for public companies to provide detailed climate-related disclosures in their annual reports. Our results indicate that the presence of common ownership could impede the voluntary carbon disclosures of individual firms and lead to lower-quality disclosures. This signifies the importance of the mandatory disclosure framework, especially for firms cross-held by large financial institutions. Our results are not without limitations. We employ CDP data for our analysis following previous studies (e.g., Cohen et al., 2023; Griffin et al., 2017; Matsumura et al., 2014). In the case of the United States, the CDP invites S&P 500 companies, limiting the available data to larger firms. Although previous studies employing CDP data, including Cohen et al. (2023), point out that the CDP is the largest global source of information on corporate carbon emissions, our findings derived from CDP data may not be generalizable to small- and medium-sized businesses.

Footnotes

Appendix A

Appendix B . Variable Definitions

| Variable | Definition and measurement | Source | |

|---|---|---|---|

|

|

|||

| CDPDIS | Dummy variable that equals one if a firm answered the CDP questionnaire and 0 otherwise | CDP | |

| P_CDPDIS | Dummy variable that equals one if a firm answered the CDP questionnaire and made the response publicly available and 0 otherwise | CDP | |

| CDLI | Voluntary carbon disclosure score ranging from 0 to 100. This scoring system was used by the CDP until 2014 | CDP | |

| DISSCORE | Voluntary carbon disclosure score, which keeps the original disclosure scores for years prior to 2016 and assigns scores to the eight ordinal band ranks from A to D– (scores being 95, 85, 75, 65, 55, 45, 35, and 20, respectively) for years after 2016 | CDP | |

|

|

|||

| CO_dummy | Dummy variable set to a value of 1 when a common owner, defined as a blockholder of the focal firm who simultaneously holds blocks of at least one more firm within the same industry, is present | Thomson Reuters 13F | |

| N_CO_Inv | Number of common investors, measured as the number of unique blockholders of the focal firm who simultaneously hold blocks of at least one more firm within the same industry. We use the natural log values of one plus the number of common investors and set the value to zero if the firm has none | Thomson Reuters 13F | |

| N_CO_Firm | Number of commonly held firms, measured as the number of unique firms cross-held by common investors of the focal firm within the industry. We use the natural log values of one plus the number of common firms and set the value to zero if the firm has none | Thomson Reuters 13F | |

| MV_CO | Total equity market value in trillion-dollar terms in firms cross-held by common investors of the focal firm within the industry. We use the natural log value of one plus the total market value of shares owned by common owners and set the value to zero if the firm has none | Thomson Reuters 13F | |

|

|

|||

| SIZE | Natural logarithm of total assets | Compustat | |

| ROA | Ratio of net income before extraordinary items to total assets | Compustat | |

| LEV | Ratio of total debt (measured as the sum of short- and long-term debt) to total assets | Compustat | |

| TOBINQ | Market capitalization of equity divided by total assets | Compustat | |

| GROWTH | Annual growth in sales, calculated as the current year’s sales divided by the previous year’s sales minus one | Compustat | |

| NEW | Ratio of net property, plants, and equipment divided by gross property, plants, and equipment | Compustat | |

| CAPSPEND | Capital spending divided by total sales revenues | Compustat | |

| INST | Proportion of shares held by investment banks or institutions | Compustat | |

| BETA | Measure of market risk that shows the relationship between the stock’s volatility and the market’s volatility; this coefficient is based on between 23 and 35 consecutive month-end price percent changes and their relativity to a local market index | Compustat | |

| LNEMIS | Firm’s carbon emissions, calculated as the natural logarithm of the total GHG emissions | Refinitiv ESG | |

| ENSCORE | Firm’s social pillar score, which evaluates its effectiveness in providing its workforce with job satisfaction, a healthy and safe workplace, training and development opportunities, and diversity and equal opportunities and assesses its commitment to maintaining its reputation in the community, having fundamental human rights conventions, and producing quality products and services that integrate customers’ health and safety, integrity, and data privacy | Refinitiv ESG | |

| HHI | Herfindahl–Hirschman index | Compustat | |

| INTANG | Natural logarithm of intangibles | Refinitiv ESG | |

| BMEETING | Natural logarithm of the number of board meetings | Refinitiv ESG | |

| BSIZE | Natural logarithm of the number of board directors | Refinitiv ESG | |

| FEMALE | Percentage of female directors on the board | Refinitiv ESG | |

| NOEXE | Percentage of nonexecutive directors on the board | Refinitiv ESG | |

| BINDP | Percentage of independent directors on the board | Refinitiv ESG | |

| BCOM | Dummy variable, which equals 1 if a firm has a board level or senior management committee responsible for decision making on CSR strategy and 0 otherwise | Refinitiv ESG | |

| INST_dummy_diff | Dummy variable, set to the value of 1 when a blockholder of the focal firm also holds blocks of at least one more firm in other industries | Thomson Reuters 13F | |

| INST_Inv_diff | Number of blockholders in the focal firm who also hold blocks in at least one more firm in other industries; the natural log value of one plus the number of these blockholders is used and the value is set to zero if the firm has none | Thomson Reuters 13F | |

| INST_Firm_diff | Number of firms cross-held by blockholders of the focal firm who also hold blocks in at least one more firm in other industries; the natural log values of one plus the number of these blockholders is used and the value is set to zero if the firm has none | Thomson Reuters 13F | |

| MV_INST_diff | Total equity market value in trillion-dollar terms in firms cross-held by blockholders of the focal firm who also hold blocks in at least one more firm in other industries; the natural log value of one plus the total market value of shares owned by these blockholders is used and the value is set to zero if the firm has none. | Thomson Reuters 13F | |

|

|

|||

| IND_DIS | Proportion of firms in an industry that participates in the CDP | CDP | |

| PRE_DIS | Dummy variable that equals 1 if a firm reports its carbon emissions to ASSET4 in the prior year | ASSET4 | |

| lambda | Inverse Mills ratio generated from the first stage of the Heckman regression | ||

| TARGET | TARGET is scored as follows: 3 for firms that set both absolute and intensity-based targets, 2 for only an absolute target, 1 for only an intensity target, and 0 if neither is set | CDP | |

| RSKMNG | Effectiveness of carbon risk management, with a score of 2 assigned to firms with a dedicated climate change risk management process, 1 for those that integrate such processes into broader risk management, and 0 if no specific process is identified | CDP | |

| lnINI | Natural logarithm of the number of carbon reduction initiatives a firm implements | CDP | |

| INCENTIVE | Dummy variable set to 1 when a firm provides either financial or nonfinancial incentives to encourage employees to contribute toward carbon management goals and 0 otherwise | CDP | |