Abstract

We examine whether borrowers who share the same auditor with a syndicate lender (i.e., shared auditors) have improved access to the syndicate loan market. We predict and find evidence that shared auditors reduce information asymmetries between lenders and borrowers as well as between lenders in a syndicate. We also find that borrowers who share auditors with lenders obtain better price and non-price terms compared with those without. Our empirical evidence also suggests that when borrowers and lenders share auditors, syndicates are less concentrated and more diverse, consistent with the prediction that shared auditors provide informational benefits on the syndicate market. Loan facilities with shared auditors are also more likely to be renegotiated with more favorable terms for borrowers. Taken together, our findings suggest that shared auditors contribute to the efficient functioning of debt markets by reducing the information asymmetries in debt contracting.

Introduction

Information asymmetries between lenders and borrowers affect debt contract design and syndicate ownership structure. Borrowers use various signals to demonstrate creditworthiness, including external audits by reputable firms. Such audits help constrain fraudulent reporting, reduce information asymmetries, and lower screening and monitoring costs for lenders (C. Becker et al., 1998; Teoh & Wong, 1993). High-quality audit services, particularly from Big N auditors, are associated with lower discretionary accruals and higher earnings response coefficients, leading to more favorable credit market terms for borrowers (B. B. Francis et al., 2017; Kausar et al., 2016; Kim, Simunic, et al., 2011; Mansi et al., 2004; Pittman & Fortin, 2004).

Because auditors accumulate a considerable amount of private information about a client, they can facilitate information flows between contracting parties, thus increasing the value generated from strategic relationships (e.g., Cai et al., 2016; Dhaliwal, Lamoreaux, et al., 2016; Dhaliwal, Shenoy, & Williams, 2016, for bidder–target and supplier–customer relationships). In this article, we extend the argument that auditors serve a verification and information intermediary role in debt contracting by creating an empirical setting where a lender shares the same auditor with a borrower (i.e., shared auditors). We conjecture that shared auditors reduce information asymmetries in debt contracting for the following reasons. First, a lender’s experience during the audit review may provide valuable information regarding the audit style. This information may prove valuable when evaluating credit conditions and designing optimal contracts with borrowers who share the same auditor and therefore comply with the same audit requirements. Second, shared auditors are likely to reduce monitoring costs by providing access to information and improving the information flow between lenders and auditors as part of the covenant compliance review.

The contribution of our article is threefold. First, research suggests that shared auditors play an important role in improving corporate investment decisions, such as mergers and acquisitions and supply chain relationships (Cai et al., 2016; Dhaliwal, Lamoreaux, et al., 2016; Dhaliwal, Shenoy, & Williams, 2016). We extend this argument and show that sharing auditors helps borrowers access debt under more favorable terms. Shared auditors enable borrowers to attract a larger number of lenders, compose more diversified syndicates, reduce the demand for loan arrangers to signal strong commitment by retaining a larger percentage of the originated loan, and by extension, reduce the interest spread. Bills et al. (2020) argue that firms may prefer to forego the benefits of selecting a more knowledgeable auditor when proprietary information spillovers are possible. Our results suggest that information spillovers from audit relations to debt contracts are beneficial for borrowers.

Second, our article contributes to the literature on the role of auditors in debt contracting. Previous research suggests that Big N auditors are likely to improve reporting quality for debt-contracting purposes. Borrowers with Big N auditors have a lower likelihood of fraud, discretionary accruals, and cost of debt and equity (e.g., C. Becker et al., 1998; Teoh & Wong, 1993). Because Big N auditors are likely to select lower risk clients (DeFond & Zhang, 2014; Johnstone & Bedard, 2004), it is an empirical challenge to disentangle the effect of audit quality from firm-specific characteristics. Our empirical design provides a promising setting to link debt contract provisions to audit relations. Using the audit relation between lenders and borrowers, we observe and explain the variance in debt contract terms across Big N audit firms, where audit services are arguably high quality. Our results show that price and non-price terms differ across clients of Big N audit firms and that sharing audit services with a lender reduces information asymmetry costs in debt contracting.

Third, we contribute to the literature on contract theory, focusing on loan renegotiations as a mechanism that creditors use to allocate decision rights with and without technical default. Research suggests that loans are frequently renegotiated to incorporate new information in debt contracts (e.g., Denis & Wang, 2014; Nikolaev, 2018). Our empirical findings suggest that loan facilities with shared auditors are more frequently renegotiated to effectively incorporate new information. Loan renegotiations for facilities with shared auditors are positively associated with favorable revisions in the available loan amounts and loan spreads. Our empirical findings are consistent with the prediction that shared auditors reduce information asymmetries upon and following loan initiation outside default states, thus contributing to the effective functioning of debt markets.

Literature Review and Hypothesis Development

Information asymmetries between lenders and borrowers, as well as between lenders on a syndicate loan, determine the optimal design of credit contracts and the ownership structure of syndicate loans. A major source of such asymmetries is a borrower’s credit quality, which may be partially inferred from public and private accounting information. Hence, contract features such as loan amount, loan spreads, loan maturity, and covenants are largely influenced by the quality of accounting information for debt-contracting and performance-monitoring purposes. Because the quality of financial information is often not observable prior to signing a contract, borrowers with presumably high-quality accounting frequently send signals to potential lenders. If credible, such signals allow borrowing firms to avoid paying a risk premium in the form of higher loan spreads and/or being constrained by unfavorable non-price contract terms such as strict covenants.

A credible and arguably strong signal in debt contracting is the choice of an external auditor. Existing theories explore the effect of external auditors on the quality of accounting information in general and on the properties of accounting information for debt-contracting purposes in particular. Empirical studies largely support the view that reputable external auditors are more likely to have clients with high-quality accounting. Empirical evidence suggests that compared with non-Big N auditors, Big N auditors are more likely to have clients with lower discretionary accruals and higher earnings response coefficients (e.g., C. Becker et al., 1998; Teoh & Wong, 1993). Furthermore, firms with high levels of uncertainty about reported earnings are more likely to hire a reputable auditor—empirically proxied by a Big N audit firm—to bolster the credibility of their financial statements (J. R. Francis et al., 1999). This result is consistent with the expectation that external monitoring constrains aggressive and potentially opportunistic financial reporting.

If reputable external auditors effectively constrain fraudulent accounting practices and reporting choices (e.g., C. Becker et al., 1998; DeAngelo, 1981), thus increasing the debt-contracting value of accounting information, borrowers with Big N auditors would be able to access credit with more favorable terms. Contracting theory posits that an independent audit reduces adverse selection and moral hazard issues between preparers and users of financial statements by objectively verifying the accuracy and credibility of the information contained in published financial statements (i.e., the verification hypothesis). Consistent with this expectation, Kim, Simunic, et al. (2011) find that borrowing firms with Big N auditors attract a larger number of lenders than those with non-Big N auditors. Pittman and Fortin (2004) show that audit quality, proxied by the Big 6, for young firms is crucial to access debt financing with favorable terms, especially during the first years on the debt market. Kausar et al. (2016) document that the voluntary choice to receive an audit significantly improves access to debt financing. Choi et al. (2018) show that auditor litigations at both the audit firm level and office level are associated with higher loan spreads, which is consistent with the expectation that audit quality affects a borrower’s credit risk assessment. Mansi et al. (2004) find that lenders value a close relationship between the borrower and the auditor and that the cost of debt finance decreases with auditor tenure, which is typically associated with higher financial reporting quality. Consistent with this result, B. B. Francis et al. (2017) show that an audit change increases screening and monitoring by lenders as reflected in higher spreads, higher upfront and annual fees, and an increased probability of pledging collateral following upward, lateral, and downward auditor changes. Chu et al. (2013) show that the effect of off-balance sheet disclosure regarding operating leases on loan spreads is more pronounced for borrowers who are not clients of Big 4 audit firms, which they attribute to the higher debt-contracting value of financial information provided by Big N clients.

Recent research argues that auditors verify financial statements and serve as information intermediaries (i.e., the information-transfer hypothesis). Auditors accumulate a considerable amount of information about their clients during audits and through informal discussions with top management. Empirical studies suggest that private information made available to external auditors may influence the outcomes of corporate investment decisions such as mergers and acquisitions and supply chain relationships. An interesting empirical setting to evaluate an auditor’s information intermediary role includes the provision of audit services to both sides of a business relationship (i.e., shared or common auditors). For example, Dhaliwal, Lamoreaux, et al. (2016) examine the impact of shared auditors, defined as audit firms that provide audit services to a target and its acquiring firm prior to an acquisition, on transaction outcomes. They argue that shared auditors are able to reduce transaction uncertainty by facilitating the flow of information between bidders and targets and find empirical evidence supporting the beneficial role of shared auditors on the M&A market. According to Dhaliwal, Lamoreaux, et al. (2016), shared auditor deals are associated with significantly lower deal premiums, lower target event returns, higher bidder event returns, and higher deal completion rates. Similarly, Cai et al. (2016) find that deals with shared auditors have higher acquisition announcement returns than deals without shared auditors. Empirical results suggest that shared auditors can enhance M&A quality more effectively when the acquirer and target are audited by the same local audit office. In a similar setting, Dhaliwal, Shenoy, and Williams (2016) show that shared auditors improve information flows in the client–customer relationship, thus alleviating the holdup problem and increasing relationship-specific investment. 1

If auditors can significantly reduce information asymmetries in debt contracting and improve resource allocation by both verifying the accuracy of financial statements and improving information flows, it is useful to examine which noncontractual arrangements enable the extraction of higher benefits from established client–audit relationships in debt contracting. Baylis et al. (2017) suggest that private lenders actively demand additional auditor assurance in private lending agreements and examine auditor covenant compliance assurance (CCA) clauses that require auditors to report borrower compliance with the financial covenants in the lending agreement. According to Baylis et al. (2017), CCA clauses are popular in private contracts (35% of 6,513 loan agreements) because lenders attempt to reduce agency problems and enhance contracting efficiency by extending auditor liability in case of a default. Apart from special contractual provisions, lenders can implicitly price perceived audit quality by deliberately favoring certain auditors. Bird et al. (2017) argue that lenders reveal their preference toward an external auditor by offering better contract terms to borrowers who are clients of their preferred auditors.

We extend the argument that lenders view auditor verification and information transfer as valuable in private debt contracting and examine the role of shared auditors on the syndicated loan market. Similar to J. R. Francis and Wang (2021), we conjecture that shared auditors play an important role in debt contracting by reducing ex ante and ex post contract frictions. Following J. R. Francis et al. (2014), we argue that the working rules of Big N auditors are an important mechanism through which GAAPs are operationalized and implemented by both auditors and their clients. Financial statement comparability, which affects both price and non-price terms in syndicated loans (e.g., Fang et al., 2016), is greater for firms that are clients of the same auditor (J. R. Francis et al., 2014).

We conjecture that lenders’ exposure to the working rules during the auditing process may provide valuable knowledge about the audit style, thus reducing information asymmetries related to the interpretation and implementation of accounting standards by borrowers in private debt contracting. Although audit processes are considerably more complex for financial institutions than for non-financial firms, the audit procedures followed by a lender are likely to reveal insightful information about the unique audit methodology and testing procedures followed by a Big N audit firm (e.g., materiality thresholds in applying accounting standards, the reliability of fair-value estimates, and the level of accounting conservatism in general), which may prove useful in designing optimal contract features. 2 Consequently, both pricing and non-pricing terms of loan facilities of both origination and renegotiation are likely to be affected when lenders and borrowers share auditors.

We argue that shared auditors are likely to reduce monitoring costs by providing access to auditors and plausibly improving the information flow between lenders and auditors ex ante as part of the covenant compliance review. 3 Baylis et al. (2017) show that demand by private lenders for independent assurance by auditors is stronger when information asymmetries in debt contracting are higher, namely, when (a) accounting measurement rules depart substantially from GAAPs; (b) agreements rely more on accounting data (in the form of either accounting covenants or accounting-based performance pricing provisions); (c) borrowers have high levels of harder-to-verify intangible assets; and (d) there are many lenders in the loan syndicate. We expect the increasing size of loan syndicates to further strengthen the demand for alternative non-contractual mechanisms in debt contracting, and shared auditors may effectively serve this purpose. Berger et al. (2017) argue that lenders’ exposure to certain industries brings expertise in a syndicated loan and find that past relationships with borrowers from a certain industry reduce the demand for audited financial statements. We extend this argument to suggest that shared auditors may reduce monitoring costs, thus contributing to the design of lending contracts with more favorable price and non-price terms:

Whereas information asymmetries between borrowers and lenders on a syndicated loan are reflected in price and non-price terms, asymmetric information between lenders are manifested in the ownership structure of the loan syndicate itself. According to Holmstrom and Tirole (1997), the lead arranger is an informed lender who is able to monitor and learn about the firm through unobservable and costly effort; in contrast, syndicate participants are uninformed lenders who rely on the information and monitoring provided by lead lenders to allocate funds across alternative projects. Participants in the syndicate anticipate that informed lenders are likely to reduce monitoring costs after the syndication formation and therefore ex ante decide to reduce their stakes in the loan. Because the monitoring efforts of lead lenders are not observable, they send a signal to syndicate participants by taking a large enough financial interest in the loan as an assurance that monitoring efforts before and after syndicate formation will be diligently exercised.

Consistent with Holmstrom and Tirole (1997), Lee and Mullineaux (2004) find that syndicates are more concentrated when the quality of information on borrowing firms is worse. They also find that firms with a higher default probability are likely to have a more concentrated syndicate structure. Ball et al. (2008) relate a borrower’s accounting information to monitoring costs ex ante and ex post loan initiation. They predict that more opaque borrowers can explain the demand for lead arrangers to retain a higher percentage of the loan, thus assuring uninformed lenders that monitoring efforts will be exerted. If accounting information timely reflects reductions in credit quality, informed lenders need not retain a larger portion of the originated loan. Consistent with this prediction, Ball et al. (2008) find that the proportion of the loan retained by the lead arranger is lower when the debt-contracting value of accounting information is high (i.e., low monitoring costs and by extension, low demand to provide assurance to uninformed lenders).

Previous research relates audit quality to syndicate compositions. Kim, Song, and Zhang (2011) show that auditor-attested SOX 404 disclosures affect the design of both contract terms and syndicate composition: Borrowers with disclosed internal control weaknesses are unable to access loans with favorable terms and fail to attract a large syndicate of lenders. Furthermore, Kim and Song (2011) find that the proportion of a syndicated loan retained by the lead arranger is smaller for loans extended to clients of Big N auditors. Empirical results are consistent with the notion that Big B auditors reduce information asymmetries between the borrower and potential lenders by improving the debt-contracting value of accounting information.

We extend this argument and suggest that shared auditors mitigate agency problems in a loan syndicate before and after loan initiation. Lead lenders with shared auditors may incorporate valuable insights about auditor-specific quality in the due diligence process. Consequently, ex ante information asymmetries in syndicated loans are likely to be lower. Furthermore, shared auditors can reduce monitoring costs by improving information flows after loan initiation. The syndicate composition is largely determined by expected monitoring efforts exerted by the lead lender. Uninformed lenders can observe the lead lender–borrower relation and anticipate that shared auditors are likely to favorably affect ex ante and ex post monitoring costs. Therefore, they are likely to be attracted to syndicates with shared auditors without the need for further assurance (i.e., higher portion of a loan retained by the informed lender[s]). In addition, they may decide to participate in debt contracts with borrowers without industry-specific knowledge and/or past relations, when shared auditors are present:

Because debt contracts are inherently imperfect, it is reasonable to expect that unexpected future market conditions enable borrowers to comply with contract terms. In addition, following loan initiation, undesirable management actions that are not contemplated in the design of the debt contract lead to higher credit risk for syndicate members. Traditionally, contracting contingencies, including covenants and performance pricing provisions, are used to allocate decisions rights to creditors, enabling them to initiate liquidation if desired. Over the past decades, however, debt contracts without traditional debt covenants (i.e., covenant-light or covenant-lite) have become preferable in both private and public debt markets (B. Becker & Ivashina, 2016; Billett et al., 2016; Gietzmann et al., 2023).

Recent research on optimal debt design suggests that contracting frictions can be more efficiently resolved in debt renegotiations when mutually beneficial revisions in the original contract terms are introduced. Roberts (2015), for example, finds that renegotiations are initiated by borrowers primarily in response to changing conditions, as opposed to lender interventions due to default. Nikolaev (2018) shows that the probability of loan renegotiations is higher for borrowers with previous renegotiations and worsening financial conditions. In contrast, borrowers with greater financial flexibility (e.g., lower leverage and high liquidity), investment growth options, and intangible assets are less likely to renegotiate their debt contracts. In addition, he shows that more concentrated syndicates are more likely to participate in loan renegotiations, consistent with the notion that conflicts between syndicate members make renegotiations costly. When performance pricing provisions are part of the original contract, the probability of loan renegotiations is lower.

We argue that shared auditors are likely to affect both the probability and the outcomes of loan renegotiations. If shared auditors facilitate access to high-quality information prior to loan initiation, we expect that original contracts will effectively price credit risk with price and non-price debt provisions. Debt contracts with and without shared auditors are inherently incomplete. Because unexpected future developments affect the probability that borrowers comply with contract conditions, we predict that loans with shared auditors are likely to reflect both favorable and unfavorable developments on a timelier basis, consistent with the information-transfer hypothesis. Debt contracts may also be revised to reflect favorable changes in the credit risk of borrowers in the syndicate loan market Denis and Wang (2014). We expect that loans with shared auditors are more likely to lessen the burden on borrowers by enabling them to access debt at more favorable terms:

Sample Description

Our primary data sources are as follows: (a) the Reuters Loan Pricing Corporation’s (LPC) DealScan for the characteristics of syndicated loans, informed and uninformed loan participants, and loan amendments; (b) Compustat for financial characteristics of borrowers and their auditors; (c) Compustat for auditors of loan participants; (d) Capital IQ for auditors of both borrowers and loan participants when Compustat data are not available; and (e) Schwert’s (2018) link tables. Following prior research, our sample starts in 1987 when syndicated loans became an increasingly important source of corporate finance.

To relate shared auditors to debt contract provisions, we examine syndicated loans and exclude corporate bonds because owners of corporate bonds are more dispersed and hence less likely to engage in monitoring (e.g., Amihud et al., 1999). In contrast to corporate bonds, syndicated loans require ex ante and ex post monitoring by syndicate members (e.g., Sufi, 2007). We conjecture that monitoring costs are favorably affected by shared auditors where information asymmetries, both between borrowers and syndicate members and between loan participants, are lower. Therefore, we focus on empirical settings where monitoring efforts are required and syndicated loans demand more intensive monitoring ex ante and ex post contract initiation.

Following the literature on syndicated loans, we filter the data on the following criteria: (a) the all-in-drawn spread is not missing; (b) LIBOR is the base rate; and (c) certain contracts are excluded (i.e., bankers’ acceptance, bridge loans, leases, loan style floating rate notes, standby letters of credit, step payment leases, bonds, notes, guidance lines, traded letters of credit, multi-option facilities, and other or undisclosed loans). These filters are introduced to generate comparable debt contracts. Using a combination of Schwert’s (2018) links and a manual check, we create borrower–lender pairs with and without shared auditors. We exclude loan facilities where such a pair could not be generated (i.e., auditors are not disclosed in Compustat or Capital IQ). In addition, we impose the requirement of at least one pair per loan facility. 4

To link debt contract features, monitoring efforts, and shared auditors, we consider the variation in loan participant profiles: informed and uninformed lenders. Similar to Jiang et al. (2010), we use the loan participant role, defined in the debt contract, to distinguish lenders with monitoring duties (i.e., active lenders). 5 Loan facilities with a shared audit have at least one active lender on the syndicate that shares an auditor with the borrower on loan origination (e.g., KPMG provides audit services to both active lenders and borrowers).

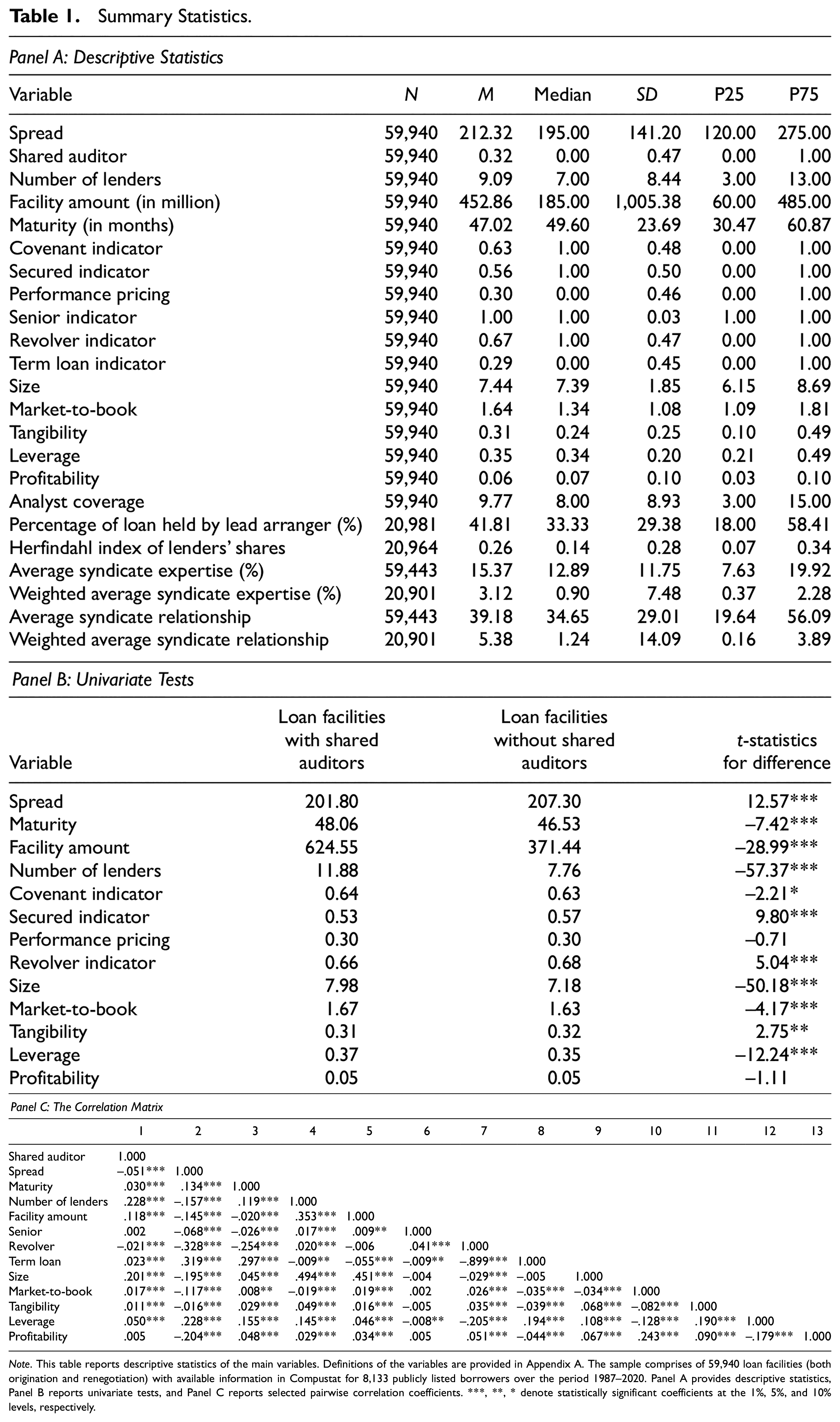

The final sample comprises 59,940 loan facilities issued by 8,133 publicly listed borrowers over the period 1987–2020. Table 1 provides summary statistics and Appendix A provides variable definitions. The average (median) loan spread, relative to LIBOR, is 212 bps (195 bps). Three of 10 loan facilities (32%) have at least one active lender in the syndicate with a shared auditor (i.e., facilities with Shared auditor). The average facility amount (maturity) is US$452 million (47 months). Approximately half of the sampled loans are secured, and approximately two thirds are revolvers, predominantly with a maturity of more than 1 year. The average (median) number of lenders in the syndicate is 9 (7).

Summary Statistics.

Note. This table reports descriptive statistics of the main variables. Definitions of the variables are provided in Appendix A. The sample comprises of 59,940 loan facilities (both origination and renegotiation) with available information in Compustat for 8,133 publicly listed borrowers over the period 1987–2020. Panel A provides descriptive statistics, Panel B reports univariate tests, and Panel C reports selected pairwise correlation coefficients. ***, **, * denote statistically significant coefficients at the 1%, 5%, and 10% levels, respectively.

Approximately 82% of the lenders in our sample are audited by Big N firms (22.80%: Ernst & Young [Ernst & Whinney from July 1, 1989, to September 29, 1989; Ernst & Ernst prior to July 1, 1989]; 18.41%: Deloitte & Touche; 30.07%: KPMG; 20.95%: PricewaterhouseCoopers [Price Waterhouse prior to the July 1, 1998, merger with Coopers and Lybrand]). 6 We argue that the concentration audit market is not a limitation. On the contrary, it presents an interesting setting to explore the variance in debt contracts within Big N audit firms. 7

Appendix B provides an example of a loan facility issued by the Consumers Energy Company (CIK: 0000201533) with and without a shared auditor. Back in 2007, the Consumers Energy Company replaced Ernst & Young LLP with their current provider—PricewaterhouseCoopers. In 2002, Consumers Energy Company accessed the syndicated loan market to obtain a term loan of US$300 million for working capital and other general corporate purposes. At the loan origination, the financial information of Consumers Energy Company was audited by Ernst & Young LLP—which was not the auditor of the syndicate administrative agents, Citibank and Salomon Smith Barney (i.e., both audited by KPMG). In 2012, Consumers Energy Company once again issued private debt on the syndicated loan market by signing a credit agreement with JP Morgan Chase Bank (agent), Barclays Bank, and Union Bank (co-syndication agents), and the Royal Bank of Scotland (documentation agent). Both Consumers Energy Company and JP Morgan Chase Bank (agent) were audited by PricewaterhouseCoopers (i.e., a shared auditor on the loan facility of 2012). The examples demonstrate that Big N auditors are likely to participate in borrower–lender relationships. However, despite the high concentration of audit services, borrower–lender relationships are not always characterized by the presence of a shared (Big N) auditor.

In Panel B of Table 1, we tabulate borrower characteristics of loan facilities with and without shared auditors. The univariate test is not conclusive concerning whether sharing auditors is more pronounced for borrowers with high information asymmetries. Loans with shared auditors are granted to more leveraged borrowers with a high book-to-market value and a low share of tangible assets. Those firm characteristics are likely to suggest high credit risk. Loans with shared auditors, however, are also large, granted by a larger syndicate and less likely to be unsecured. Because risky borrowers are less likely to attract lenders and receive large syndicate loans, we can conclude that shared auditors are likely to enter into debt contracts with low-risk borrowers.

Empirical Results

Information Asymmetries Between Borrowers and Lenders

To test Hypothesis 1, we estimate the following baseline model:

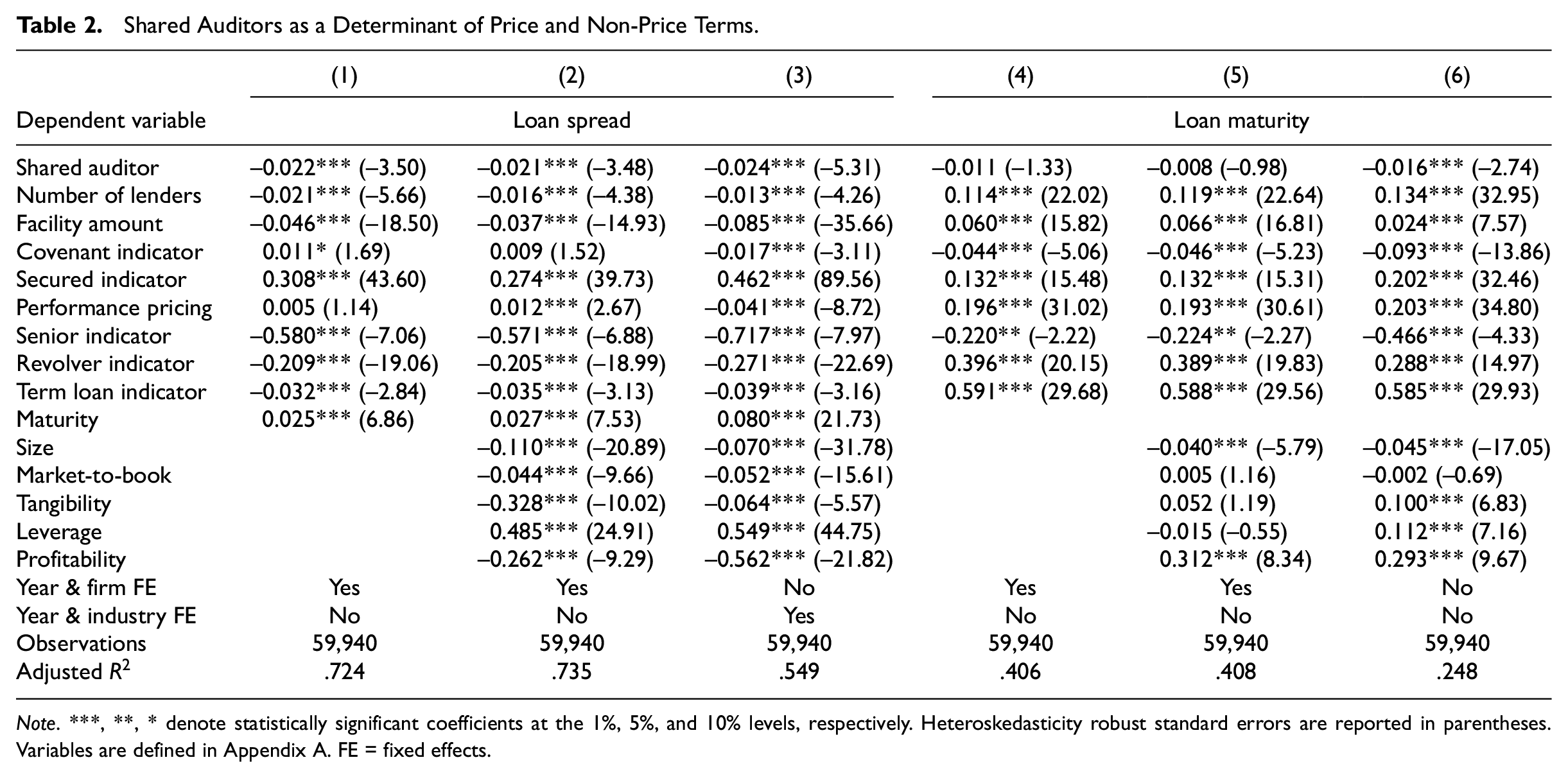

where Y is a loan condition (interest spread or loan maturity) for a firm in industry j at time t. The control variables (X) are loan- and firm-specific characteristics that determine loan contracts. The loan-specific controls are the number of lenders, facility amount, covenant indicators, secured indicator, performance pricing indicators, senior indicator, revolver indicator, term loan indicators, and loan maturity. The borrower-specific controls are size, market-to-book, tangibility, leverage, and profitability. The baseline model includes industry (three-digit SIC codes) fixed effects. To control for time-specific variation in loan conditions, the estimates are obtained with year fixed effects. In Hypothesis 1, we predict that loan facilities with shared auditors have lower loan spreads (

In Table 2, we tabulate the regression estimates obtained using an ordinary least squares (OLS) model. The predicted effect of shared auditors on loan spreads (maturity) estimated with Model (1) is presented in Columns (3) and (6). For robustness, we estimate the model using firm fixed effects (Columns (1) and (4)) and only loan-specific controls (Columns (2) and (5)). Our estimates suggest that loans with shared auditors have lower interest spreads after controlling for loan characteristics and borrower credit risk, as proxied by size, market-to-book, tangibility, leverage, and profitability. We confirm this finding using alternative model specifications, firm fixed effects, and a subset of controls. In contrast to loan spreads, we do not find robust empirical evidence that shared auditors are associated with longer contract maturity. If any, the effect of shared audit services is estimated to have a negative effect on maturity. Other determinants of debt conditions are highly consistent with theoretical predictions in prior literature. Interest spreads (maturity) are smaller (higher) for loan facility with a larger number of lenders (due to lender portfolio diversification) granted to large, less leveraged, more profitable, growing borrowers with a larger portion of tangible assets.

Shared Auditors as a Determinant of Price and Non-Price Terms.

Note. ***, **, * denote statistically significant coefficients at the 1%, 5%, and 10% levels, respectively. Heteroskedasticity robust standard errors are reported in parentheses. Variables are defined in Appendix A. FE = fixed effects.

Although our findings on loan maturity are not robust, we find strong empirical evidence that shared auditors affect the cost of debt and loan spreads. Our results are consistent with J. R. Francis and Wang (2021) and confirm that sharing auditors with active lenders have a favorable effect in debt contracting. The estimated effect supports the view that shared auditors are likely to reduce information asymmetries in debt contracting by verifying the accuracy of financial statements and improving information flows in lending relationships.

Information Asymmetries Between Syndicate Members

The empirical estimates in Table 2 confirm that loan facilities with shared auditors have lower loan spreads, suggesting that information asymmetries between lenders and borrowers are likely lower than loan facilities without shared auditors. We next empirically test whether shared auditors affect the syndicate structure. To test Hypothesis 2, we construct the following baseline model:

where Syndicate characteristics are the syndicate concentration and composition for a firm in industry j at time t. The control variables (X) are loan- and firm-specific characteristics that determine loan contract characteristics. Similar to Model (1), we include loan-specific controls (the number of lenders, facility amount, covenant indicators, secured indicator, performance pricing indicators, senior indicator, revolver indicator, and term loan indicators) and borrower-specific controls (size, market-to-book, tangibility, leverage, and profitability). We estimate the marginal effect of shared auditors with regression analysis using industry and year fixed effects.

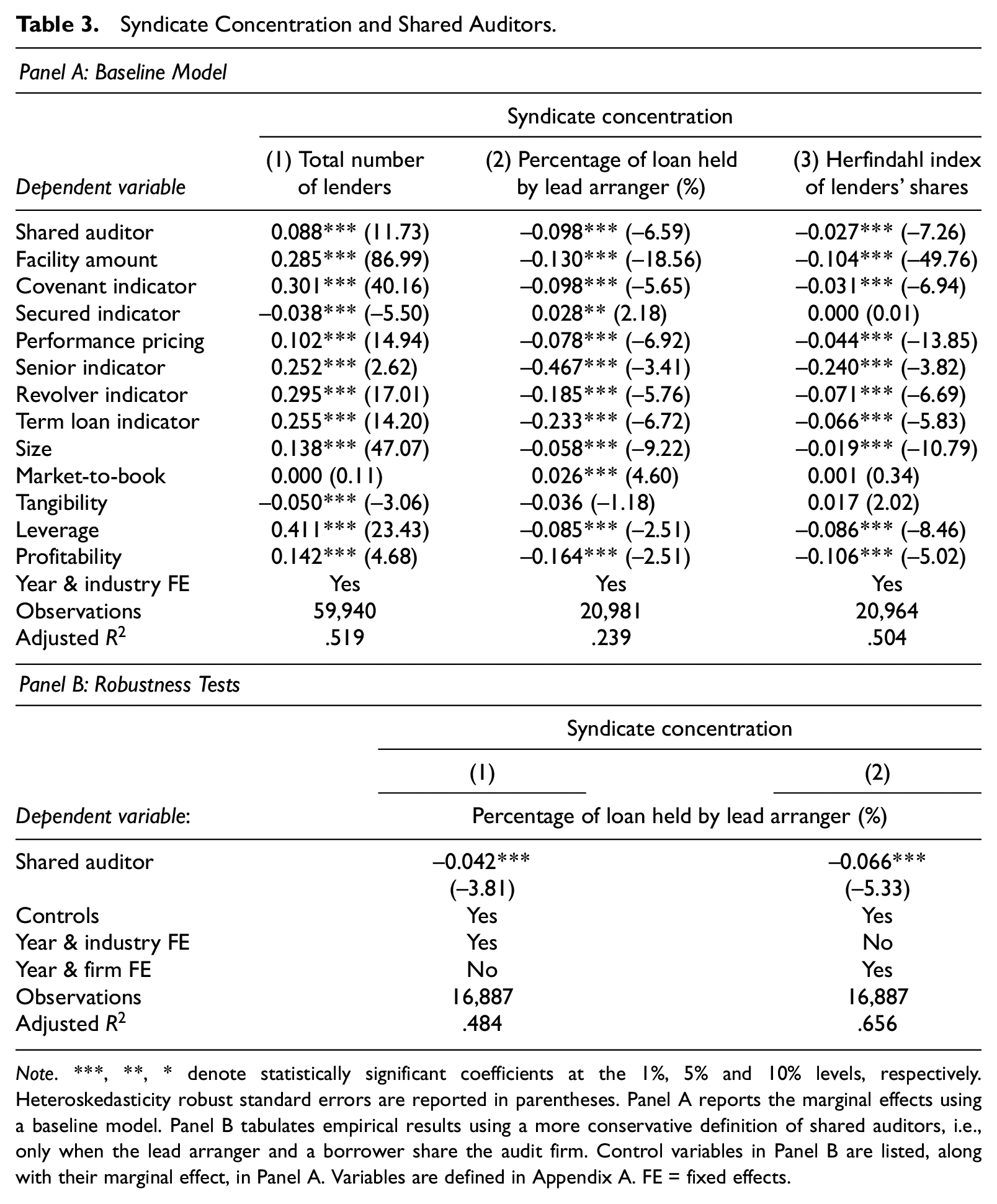

Panel A of Table 3 tabulates the estimated effect of shared auditors on syndicate concentration. Similar to Sufi (2007) and Lin et al. (2012), we construct several proxies for syndicate concentration: (a) total number of lenders (Column (1)), (b) percentage of loan kept by lead lenders (Column (2)), and (c) Herfindahl index of lenders’ shares (Column (3)). We predict that shared auditors are likely to reduce information asymmetries among lenders and therefore syndicate concentration. Across all columns, the presence of shared auditors is significantly related to the degree of syndicate concentration. Loans granted to borrowing firms with shared auditors have a less concentrated syndicate: a larger number of lenders are in the syndicate, the lead arranger holds a smaller share of the loan, and the lenders’ shares in the loan overall have a less concentrated distribution, as indicated by a lower Herfindahl index value.

Syndicate Concentration and Shared Auditors.

Note. ***, **, * denote statistically significant coefficients at the 1%, 5% and 10% levels, respectively. Heteroskedasticity robust standard errors are reported in parentheses. Panel A reports the marginal effects using a baseline model. Panel B tabulates empirical results using a more conservative definition of shared auditors, i.e., only when the lead arranger and a borrower share the audit firm. Control variables in Panel B are listed, along with their marginal effect, in Panel A. Variables are defined in Appendix A. FE = fixed effects.

Panel B in Table 3 presents the marginal effect of shared auditors on syndicate concentration using alternative estimation procedures. To obtain the estimates, we use an alternative, more restrictive definition of an informed lender, that is, a lender clarified as a “lead arranger.” In addition, we estimate the role of shared auditors on syndicate concentration with industry (Column (1)) and firm fixed effects (Column (2)). Our results confirm that loan facilities with shared auditors reduce the demand for informed lenders to signal commitment by retaining a larger share of the issued loan than loan facilities without shared auditors.

The results in Table 3 suggest that shared auditors reduce information asymmetries among syndicate lenders. Because informed lenders can reduce the required investment in loans issued to borrowers with shared auditors as a signaling mechanism to other uninformed lenders, they can liberate funds to grant loans to other borrowers in the lending market. Therefore, shared auditors enable lead lenders to not only compose more diversified loan portfolios but also make available funds to other borrowers, thus effectively reducing the risk exposure of lead lenders to certain borrowers and improving the functioning of the lending market.

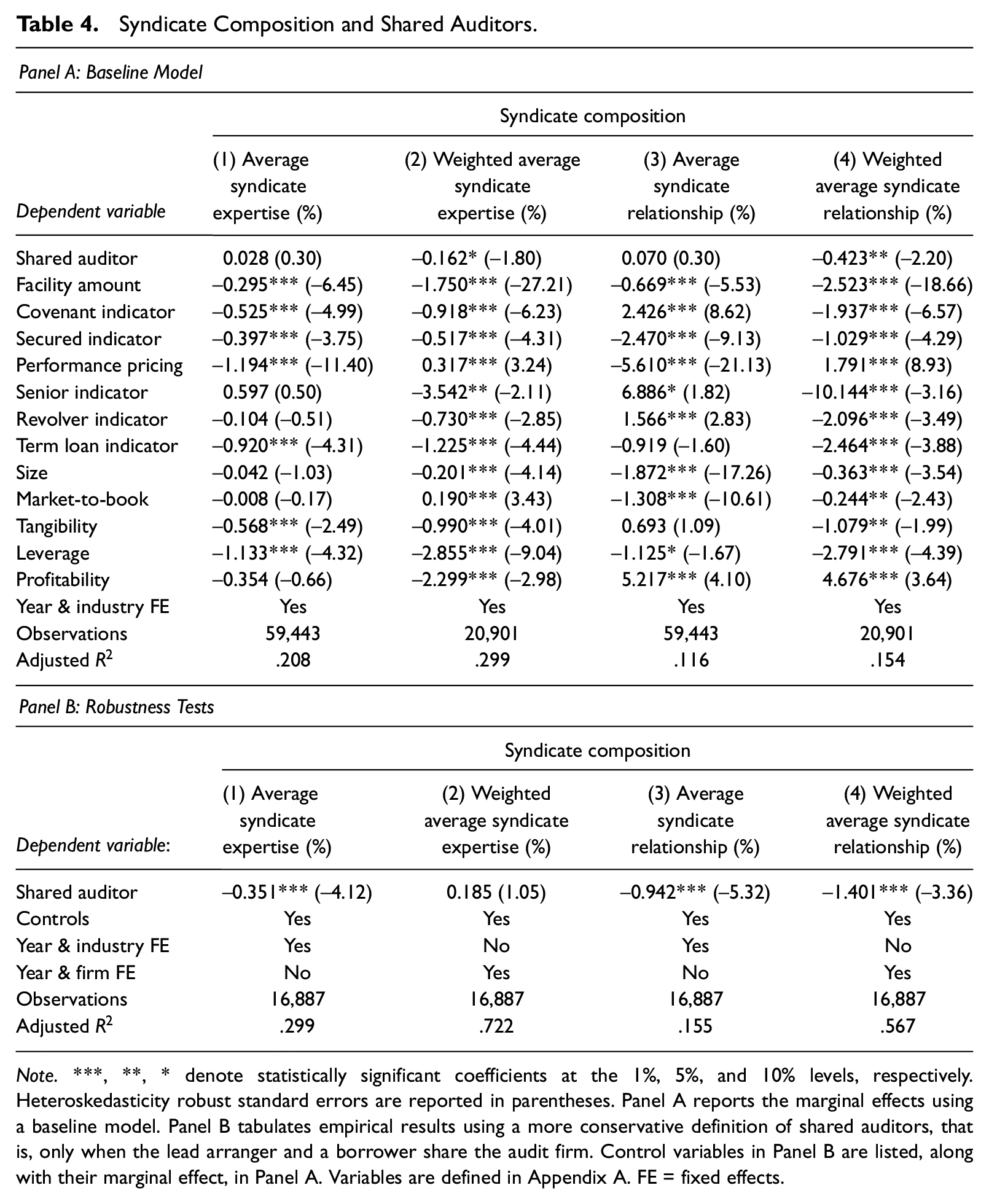

The results from the multivariate regression in Table 3 suggest that shared auditors have a significant impact on syndicate concentration. We next examine another dimension of syndicate structure, namely, syndicate composition. If shared auditors reduce information asymmetries between informed and uninformed syndicate members, we expect that past relationships and industry expertise will be less likely to determine the decisions of uninformed lenders to join a syndicate. To reduce credit risk, lenders are likely to grant loans to borrowers with previous lending relationships. When information asymmetries between lenders and borrowers are high, repeated lending relationship enables access to debt with favorable terms (e.g., Bharath et al., 2009). In addition, lenders concentrate their loan portfolios in a particular industry, thus taking advantage of the synergies in information collection and monitoring (e.g., Ivashina, 2009). We predict that the effect of shared auditors on syndicate composition is negative and significant (

Table 4 presents the marginal effect of shared auditors on syndicate composition. Similar to syndicate concentration, we use different proxies for syndicate composition: (a) average syndicate industry expertise (Column (1)); (b) weighted average industry expertise, where the share held by informed lenders is used as a weight (Column (2)); and (c) average syndicate relationships (Column (3)), and weighted average syndicate relationships, where the share held by informed lenders is used as a weight (Column (4)). We find empirical evidence to support the notion that uninformed lenders are less likely to participate in syndicates without past lending relationships and industry-specific experience. Although the results across different proxies of syndicate composition are not always significant, we find strong evidence that syndicate composition is different for loan facilities with shared auditors. Using the share of the loan held by lead lenders (Columns (2) and (4)), our estimates suggest that shared auditors have a significant negative effect on syndicate composition: The syndicate of loan facilities with shared auditors is less likely to have previous lending relationships with the borrower, and compared with loan facilities without shared auditors, the average industry expertise is low.

Syndicate Composition and Shared Auditors.

Note. ***, **, * denote statistically significant coefficients at the 1%, 5%, and 10% levels, respectively. Heteroskedasticity robust standard errors are reported in parentheses. Panel A reports the marginal effects using a baseline model. Panel B tabulates empirical results using a more conservative definition of shared auditors, that is, only when the lead arranger and a borrower share the audit firm. Control variables in Panel B are listed, along with their marginal effect, in Panel A. Variables are defined in Appendix A. FE = fixed effects.

Panel B in Table 4 tabulates the results of the robustness test, where only shared auditors with lead arrangers are considered and regression estimates are obtained using industry and firm fixed effects. Although the regression estimates in this panel are more conservative than those in Panel A, they confirm that shared auditors are associated with more diverse syndicates. Lenders without prior relations and less industry-specific expertise are more likely than other lenders to participate in syndicates where informed lenders share auditor services with the borrower. Lin et al. (2012) suggest that lead lenders are more likely to select participant lenders based on their familiarity with the industry section of the borrower, when the potential need for joint monitoring upon loan initiation is high. Our results suggest that both lead lenders and loan participants do not find additional benefits from leveraging borrower- and industry-specific expertise for loan facilities with shared auditors.

Information Asymmetries Upon Renegotiation

Our regression estimates suggest that shared auditors determine the interest spread and syndicate structure. In this section, we examine the role of shared auditors on the probability of both debt renegotiation and favorable renegotiation outcomes. To empirically test Hypothesis 3, we estimate the following baseline model:

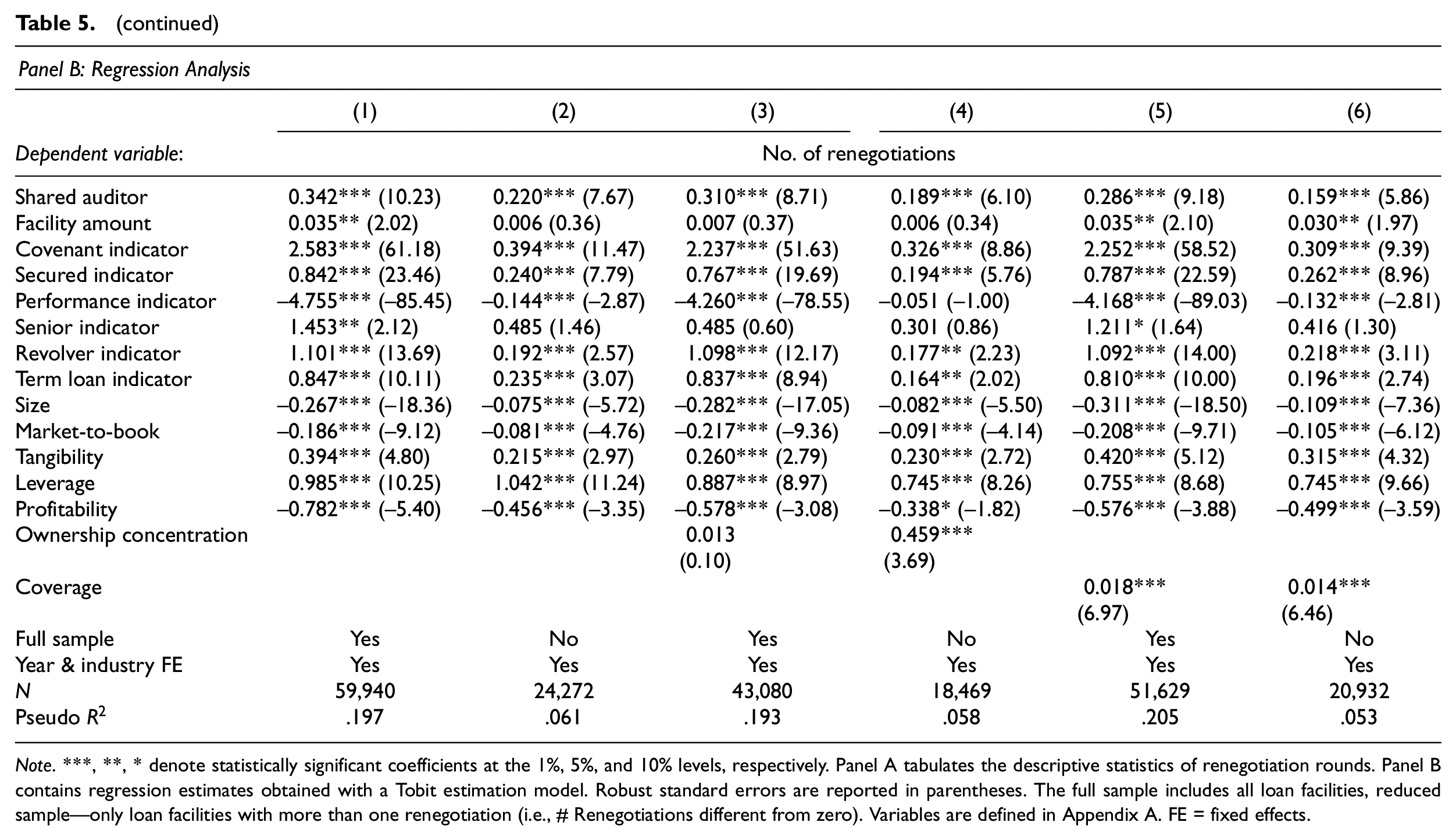

where Renegotiation represents the frequency and outcomes of debt renegotiations for a firm in industry j at time t. Control variables (X) are loan- and firm-specific characteristics that determine loan contract characteristics. Similar to Model (1), we include loan-specific controls (the number of lenders, facility amount, covenant indicators, secured indicator, performance pricing indicators, senior indicator, revolver indicator, and term loan indicators) and borrower-specific controls (size, market-to-book, tangibility, leverage, and profitability). We estimate the marginal effect of shared auditors in regression analysis using industry and year fixed effects.

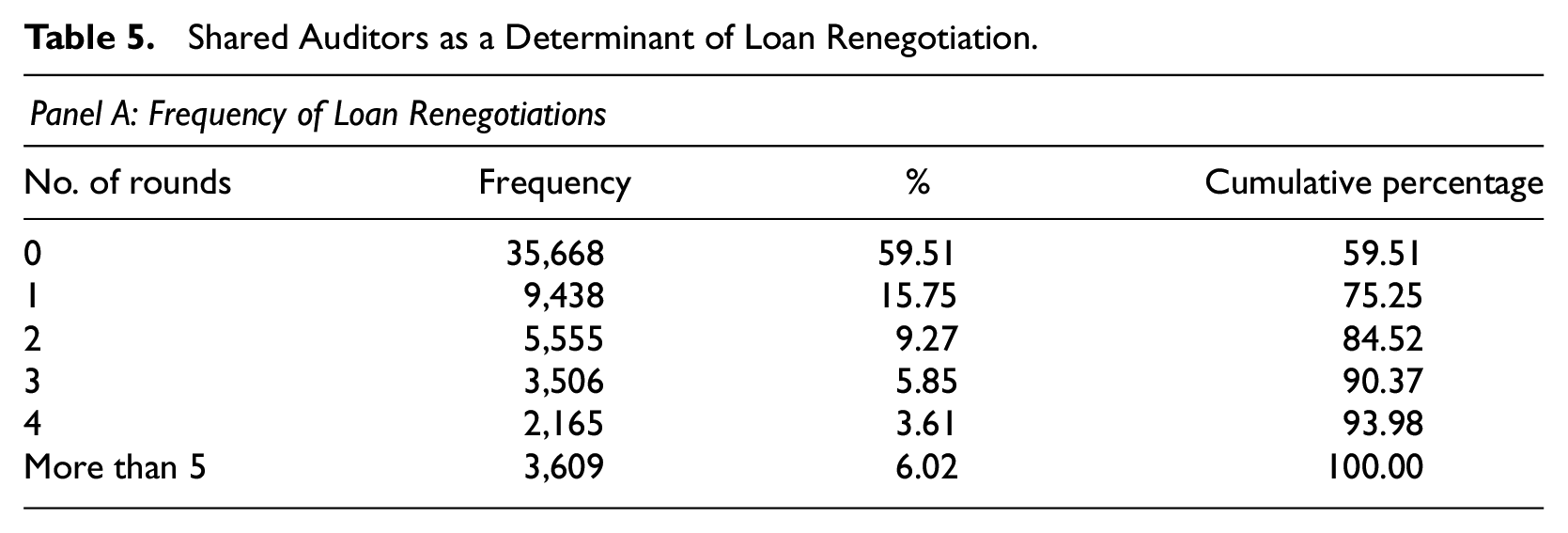

Panel A in Table 5 tabulates the descriptive statistics of loan renegotiation. Approximately 40% of the loan facilities are subject to renegotiation. A large portion of those facilities are renegotiated only once. However, approximately 15% of the loan facilities are renegotiated in multiple rounds.

Shared Auditors as a Determinant of Loan Renegotiation.

(continued)

Note. ***, **, * denote statistically significant coefficients at the 1%, 5%, and 10% levels, respectively. Panel A tabulates the descriptive statistics of renegotiation rounds. Panel B contains regression estimates obtained with a Tobit estimation model. Robust standard errors are reported in parentheses. The full sample includes all loan facilities, reduced sample—only loan facilities with more than one renegotiation (i.e., # Renegotiations different from zero). Variables are defined in Appendix A. FE = fixed effects.

We conjecture that the presence of shared auditors determines the demand for monitoring and hence the likelihood of loan renegotiations. Nikolaev (2018) suggests that renegotiations reduce information asymmetries in debt markets because they more effectively price unforeseen circumstances. Denis and Wang (2014) show that loans are renegotiated in the absence of any covenant violation and such revisions in debt contracts outside default states are mostly favorable for borrowers. Consistent with Nikolaev (2018) and Denis and Wang (2014), we argue that shared auditors affect information asymmetries upon and following loan initiation outside default states. If shared auditors enable lenders to more effectively allocate control rights for the arrival of new information following loan initiation, we expect loan renegotiations to be more frequent for loan facilities when informed lenders share auditors with borrowers. The positive effect of shared auditors on renegotiation frequency is consistent with the information hypothesis, where information flows are more relevant for debt contracting for loan facilities with shared audit services.

Panel B in Table 5 tabulates the marginal effect of shared auditors as a determinant of loan renegotiations. In Columns (1), (3), and (5), we explain the variance in renegotiation rounds using the full sample, including loan facilities that are never renegotiated. In Columns (2), (4), and (6), we relate the presence of shared auditors with renegotiation rounds only when the loan facility is renegotiated at least once. Consistent with Nikolaev (2018), we find that firms with high leverage and with growth prospects, as proxied with market-to-book ratio, are less likely to engage in loan renegotiations. After controlling for loan characteristics, we find that large borrowers are less likely to renegotiate their loans. Our results also suggest that the number of rounds is negatively associated with the presence of performance pricing and is positively related to other covenants, asset tangibility, institutional ownership concentration, and analyst coverage. Moreover, our estimates support the prediction that loan facilities with shared auditors are more likely to be renegotiated. The regression coefficients are robust to model specifications and sample filters.

The positive coefficient of shared auditors on loan renegotiation may suggest that such contracts do not effectively price risk factors upon initiation, thus demanding more frequent revisions. The empirical findings, however, largely support the view that renegotiations are more likely for less risky borrowers, such as those with tangible assets and high scrutiny over management decisions (i.e., institutional ownership and analyst following). Therefore, we conjecture that loan facilities with shared auditors are renegotiated to effectively incorporate new information and such revisions are not primarily introduced to correct mispricing of risk factors upon loan initiation.

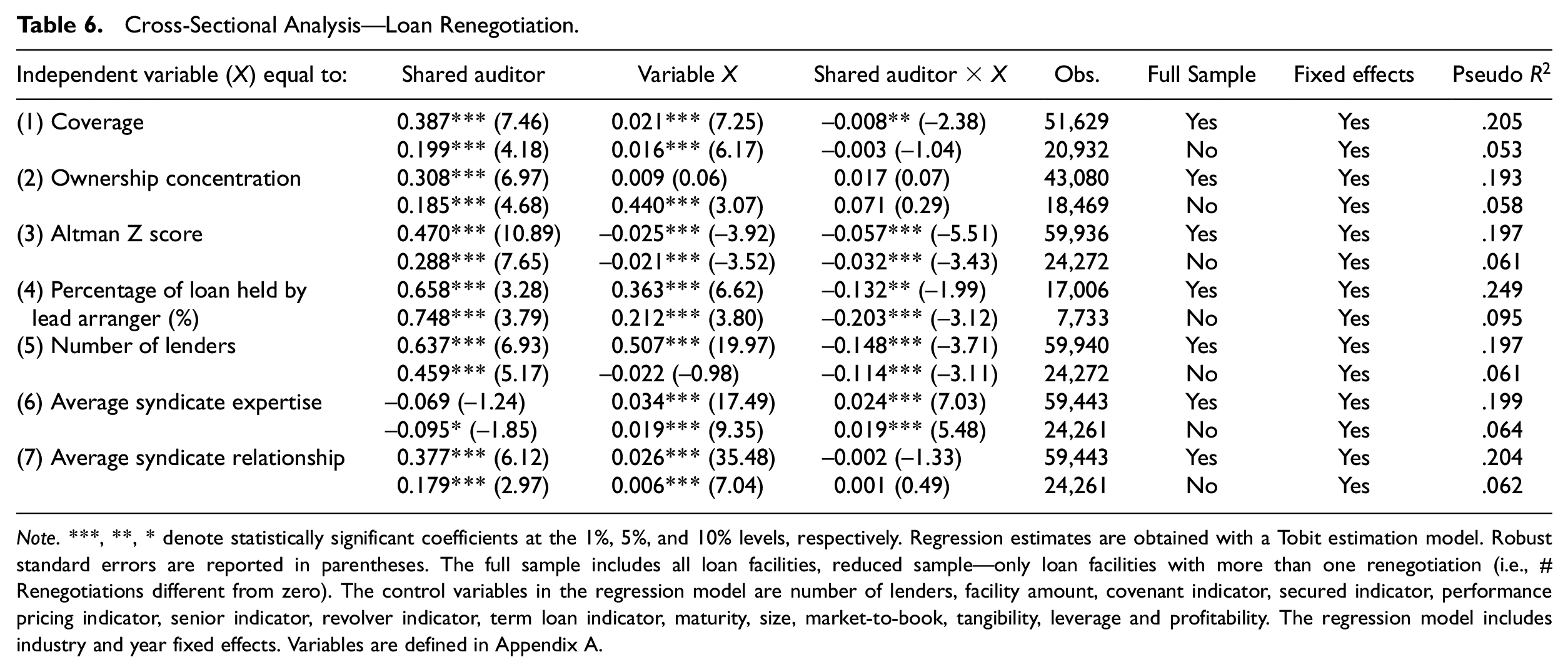

Table 6 presents the cross-sectional analysis with different sorting variables as determinants of the demand for monitoring. Consistent with prior research, we expect that monitoring efforts are likely to be more intensive when borrowers have a risky profile, such as lower analyst following (Part 1), higher institutional ownership concentration (Part 2), high Altman Z-score as a proxy for default risk (Part 3), a lower share of loan retained by the lead lender (Part 4), and large and less informed syndicates (Parts 5–7). If loan facilities with shared auditors are renegotiated to introduce favorable changes in debt contracts, we expect the interaction term to be negative for risky borrowers. We find empirical evidence, albeit not robust, that the effect of shared auditors on loan renegotiation is less pronounced for risky borrowers (i.e., lower coverage, high Z-score, and less concentrated syndicates).

Cross-Sectional Analysis—Loan Renegotiation.

Note. ***, **, * denote statistically significant coefficients at the 1%, 5%, and 10% levels, respectively. Regression estimates are obtained with a Tobit estimation model. Robust standard errors are reported in parentheses. The full sample includes all loan facilities, reduced sample—only loan facilities with more than one renegotiation (i.e., # Renegotiations different from zero). The control variables in the regression model are number of lenders, facility amount, covenant indicator, secured indicator, performance pricing indicator, senior indicator, revolver indicator, term loan indicator, maturity, size, market-to-book, tangibility, leverage and profitability. The regression model includes industry and year fixed effects. Variables are defined in Appendix A.

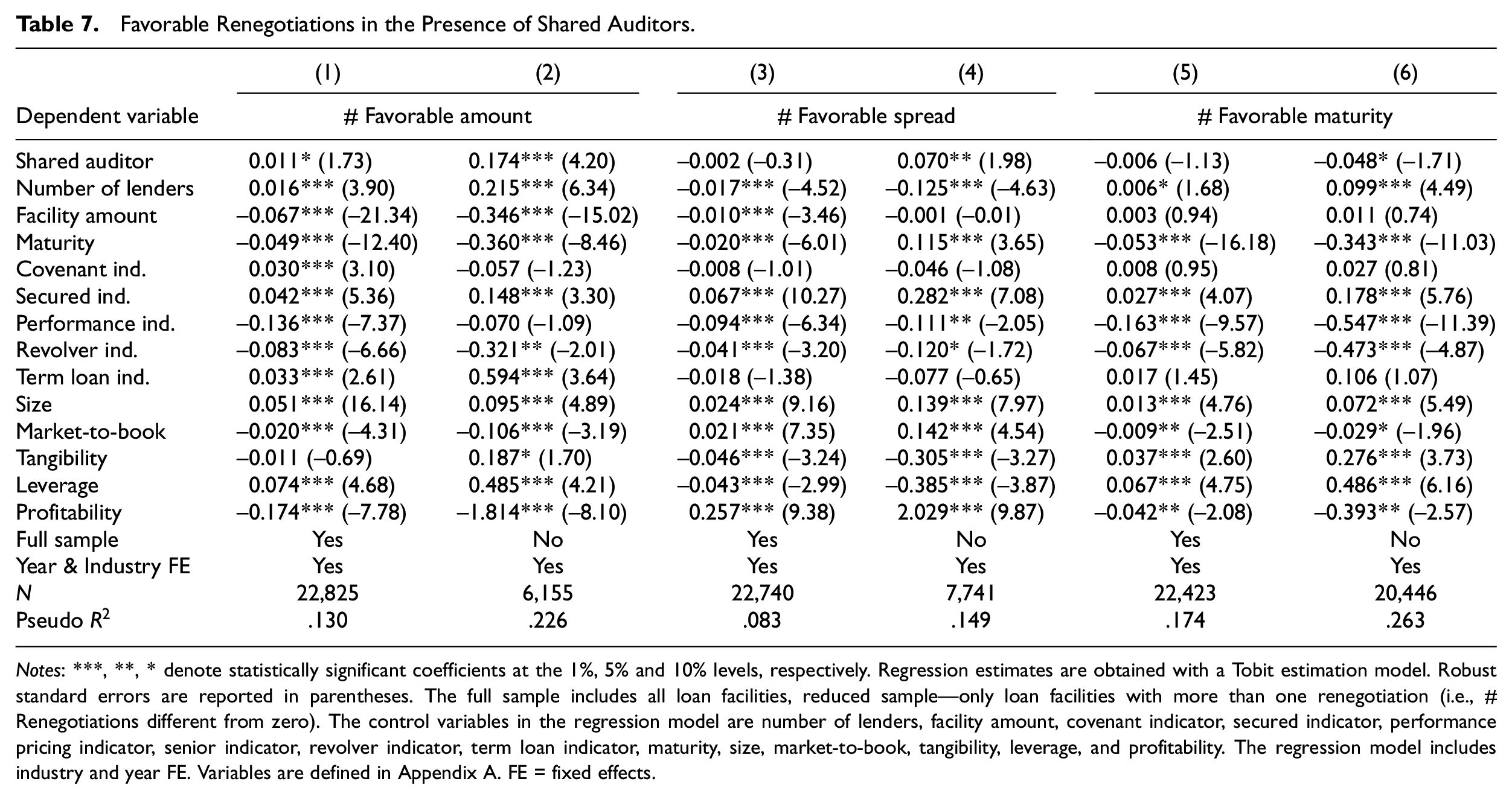

We next examine the contract conditions subject to debt renegotiation and Table 7 presents these results. For the regression analysis, we code the revisions as unfavorable when the renegotiation results in a reduced loan amount, larger loan spread, and lower loan maturity, for example, in Column 1, # Favorable amount = 0. Because not all contract characteristics are revised in loan renegotiations, we consider the reinforcement of previous conditions as a favorable change and obtain empirical results with full and partial samples (i.e., all loan facilities for the full sample and only loans with at least one renegotiation for the partial sample). By retaining loan contracts with zero changes in certain contract dimensions, we increase the power of the statistical tests with a larger sample.

Favorable Renegotiations in the Presence of Shared Auditors.

Notes: ***, **, * denote statistically significant coefficients at the 1%, 5% and 10% levels, respectively. Regression estimates are obtained with a Tobit estimation model. Robust standard errors are reported in parentheses. The full sample includes all loan facilities, reduced sample—only loan facilities with more than one renegotiation (i.e., # Renegotiations different from zero). The control variables in the regression model are number of lenders, facility amount, covenant indicator, secured indicator, performance pricing indicator, senior indicator, revolver indicator, term loan indicator, maturity, size, market-to-book, tangibility, leverage, and profitability. The regression model includes industry and year FE. Variables are defined in Appendix A. FE = fixed effects.

Our empirical estimates suggest that shared auditors are positively associated with favorable revisions in the available loan amounts. The coefficient is positive and significant, independent of the sample selection (Columns (1) and (2)). We find that loan facilities with shared auditors are also more likely to favorably revise loan spreads, conditional on loan renegotiations (Column (4)). We do not find that shared auditors enable borrowers to access funding over a more extended period. For contracts with at least one renegotiation, we find that the presence of shared audit services is negatively associated with a favorable revision in loan maturity (Column (6)). This result may suggest that borrowers who share the auditor with the informed lender are in a less favorable position. We argue, however, that this interpretation is not supported by our sample. Our results suggest that favorable changes are more likely for loans with shorter maturity (i.e., the regression coefficient of maturity is negative across all models, Columns (1)–(6)). Therefore, we conjecture that the lower maturity of renegotiated loans with shared auditors may result in future favorable revisions at the next round. Taken together, the empirical results suggest that shared auditors contribute to the introduction of contract revisions that are favorable for borrowers.

Conclusion

In this article, we examine the effect of shared auditors in lending relations on debt contract design. Because auditors are likely to possess value-relevant information for debt-contracting purposes, we argue that shared audit services between loan leaders (i.e., informed lenders on the syndicate) and borrowing firms have a beneficial effect on debt provisions, such as loan spread and maturity, both upon loan initiation and in the case of contract amendments. Because information asymmetries between lenders in the syndicate are drivers of the syndicate structure, with the associated effects on the contract design, we further suggest that shared auditors are likely to determine both syndicate concentration (e.g., the number of lenders on a syndicate and the amount of loan held by the lead lenders) and syndicate composition (e.g., the average industry expertise and lending relationship of syndicate participants).

Our results are consistent with the expectation that information asymmetry problems between lenders and borrowers, as well as between lenders on a syndicate loan, are lower when lead lenders share audit services with borrowers. We show that loan facilities with shared auditors have lower interest spreads after controlling for loan characteristics and borrower credit risk. We also find that informed lenders have a lower demand to retain a share of the loans issued to borrowers with shared auditors. This result supports the expectation that signaling commitment by lead lenders is not demanded by syndicate participants likely due to the lower information asymmetries between lenders in the syndicate. In addition, we find empirical evidence that loan facilities with shared auditors have a less concentrated syndicate as captured in the number of lenders in the syndicate and the concentration of their ownership stakes of the loan issued. Our results further suggest that lenders with shared auditors are more likely to attract syndicate participants who are less likely to have industry expertise and past lending relations, thus facilitating the effective functioning of the debt market. We also examine the effect of shared auditors on loan renegotiation and find convincing evidence that more favorable amendments are likely when lead lenders share audit services with borrowers.

Footnotes

Appendix A

Variable Definition

| Abbreviation | Definition | Data source |

|---|---|---|

| Loan characteristics: | ||

| Spread | Natural logarithm of the initial all-in-drawn spread is defined as the basis point coupon spread over LIBOR plus the annual fee and the upfront fee spread, if there is any | Loan Pricing Corporation Deal Scan |

| Facility amount | Natural logarithm of the loan facility amount | Loan Pricing Corporation Deal Scan |

| Maturity | Natural logarithm of the loan maturity in months | Loan Pricing Corporation Deal Scan |

| Secured indicator | An indicator variable equal to one if a loan is secured, and zero otherwise | Loan Pricing Corporation Deal Scan |

| Performance pricing | An indicator variable equal to one if a loan has performance pricing provisions, and zero otherwise | Loan Pricing Corporation Deal Scan |

| Covenant indicator | An indicator variable equal to one if a loan is secured, and zero otherwise | Loan Pricing Corporation Deal Scan |

| Revolver indicator | An indicator variable equal to one for revolving credit, and zero otherwise | Loan Pricing Corporation Deal Scan |

| Term loan indicator | An indicator variable equal to one for term loans, and zero otherwise | Loan Pricing Corporation Deal Scan |

| Number of lenders | Natural logarithm of the total number of lenders in a loan syndicate | Loan Pricing Corporation Deal Scan |

| Borrower characteristics: | ||

| Size | Natural logarithm of the borrower’s total assets (AT) | Compustat |

| Leverage | The ratio of total debt (DLTT) plus debt in current liabilities (DLC) to total assets (AT) | Compustat |

| Market-to-book | The ratio of market value of assets (AT + CSHO × PRCC_F – CEQ) to book value of total assets (AT) | Compustat |

| Tangibility | The ratio of net property, plant, and equipment (PPENT) to total assets (AT) | Compustat |

| Institutional ownership | The fraction of total institutional ownership in the borrower, measured in real numbers | Thomson-Reuters 13F Filings |

| Z-score | Altman bankruptcy Z-score is calculated , where is the working capital to total assets, —retained earnings to total assets, —earnings before interest and taxes to total assets, —market value equity to book value of total liabilities, and —sales to total assets (Altman 1968). Following Jiang et al. (2010), an adjusted version of the bankruptcy score is computed by excluding the term and all variables are winsorized at and | Compustat |

| Analyst coverage | The natural logarithm of the number of financial analysts following the borrower | I/B/E/S |

| Profitability | The ratio of income before extraordinary items (IB) plus depreciation and amortization (DP) to total assets (AT) | Compustat |

| Syndicate structure: | ||

| Total number of lenders | The total number of lenders in the syndicate | Loan Pricing Corporation Deal Scan |

| Percentage of loan kept by lead arranger | The percentage of the loan kept by the lead arranger. If the syndicate has more than one lead arranger, this is the total percentage of the loan kept by all the lead arrangers | Loan Pricing Corporation Deal Scan |

| Herfindahl index of lenders’ shares | The Herfindahl index of lenders’ shares in the loan, computed as the sum of the squares of each lender’s share in the loan | Loan Pricing Corporation Deal Scan |

| Average syndicate expertise | The average of the industry expertise ratios of all the lenders in the syndicate The industry experience ratio of a lender is defined as the total amount of loans it has made over the past 5 years in the three-digit Standard Industrial Classification (SIC) industry that the borrower belongs to, divided by the total amount of loans issued in the same industry over the same period by all the lenders in Deal Scan. | Loan Pricing Corporation Deal Scan |

| Weighted average syndicate expertise | The weighted average of the industry expertise ratios of all the lenders in the syndicate, with each lender’s share in the loan as its weight. The industry experience ratio of a lender is defined as the total amount of loans it has made over the past 5 years in the three-digit SIC industry that the borrower belongs to, divided by the total amount of loans issued in the same industry over the same period by all the lenders in Deal Scan. | Loan Pricing Corporation Deal Scan |

| Average syndicate relationships | The average of the relationship ratios of all the lenders in the syndicate. The relationship ratio of a lender is defined as the total amount of loans it has made over the past to the borrower, divided by the total amount of loans issued by the borrower over the same period from all lenders in Deal Scan. | Loan Pricing Corporation Deal Scan |

| Weighted average relationships | The weighted average of the relationship ratios of all the lenders in the syndicate, with each lender’s share in the loan as its weight. The relationship ratio of a lender is defined as the total amount of loans it has made over the past 5 years to the borrower, divided by the total amount of loans issued by the borrower over the same period from all lenders in Deal Scan. | Loan Pricing Corporation Deal Scan |

Appendix B

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Petya Platikanova acknowledges the financial support received by AGAUR (SGR 2017-640) and the Spanish Ministry of Science, Innovation, and Universities (PGC2018-099700-A-100).