Abstract

We study the bargaining game between a tax agency and a tax advisor-taxpayer team. Specifically, we focus on the factors that motivate tax aggressiveness, and the role of tax advisors in tax aggressiveness. We begin by characterizing the conditions under which tax advisors would give aggressive advice to their clients. Next, we analyze the optimal number of bargaining rounds for the tax agency. Third, we study the counteroffers that the tax agency makes in each round of the bargaining game. In addition, we investigate the conditions under which a high-tax taxpayer type would hire a reputable tax adviser. Last, we analyze when would the taxpayer accept or reject the tax advisor’s recommendation.

Introduction

The implementation of the tax code may require judgment when the tax issue is not clear cut, if the code is neither sufficiently detailed nor comprehensive. The latitude for interpretation matters as it may result in a multitude of legitimate tax payments. To navigate this ambiguity, taxpayers hire tax advisors. The government “expects tax professionals to assess accurately the strength of tax positions and imposes financial penalties on taxpayers and tax professionals when overly aggressive tax positions are claimed” (Cloyd & Spilker, 1999, p. 302). Taxpayers, on the contrary, expect their tax advisors to serve their interests ethically and within the boundaries of the law, and yet to their advantage.1,2 Weighing these expectations, tax advisors may be inclined to propose an aggressive tax strategy to reduce tax, but with an increased risk of rejection by the tax authority. 3

Applying a bargaining game model to focus on the bargaining process itself, we examine the role of tax advisors in aggressive tax planning and the consequent tax collection. It is crucial to note that this study focuses on the latitude legally allowed by the tax code, that is, tax avoidance, and not tax evasion. In our study, tax advisors fulfill the role of advising taxpayers—whether individuals or corporate entities—on tax liability. When required, they negotiate the tax liability on behalf of the client with the tax revenue agency or service. If negotiations between an advisor and the tax agency do not result in a mutual agreement, the final assessment of the tax payment is determined in court, either tax courts (in the United States and Canada) or civil courts (in other countries). This bargaining process and its dynamics have important implications for the tax revenue agency and, in turn, for public policy.

To examine the role of tax advisors in tax aggressiveness, this study considers the following research questions:

Under what conditions would a tax advisor give conservative advice (hence, possibly avoiding its reversal in court), or aggressive advice?

How many rounds of bargaining should the tax agency push for?

What counteroffers should the tax agency make to the taxpayer-tax advisor team?

Under what conditions does a high-tax type taxpayer hire a reputable tax advisor?

Under what conditions does a high-tax type taxpayer accept, or reject, the tax advisor’s recommendation?

These research questions largely arise from the asymmetry of information between the agency and the advisor-taxpayer team regarding the strength of a given case. To illustrate, imagine a case wherein the tax advisor recommends an aggressive tax strategy, the taxpayer adopts that strategy and files low taxes, and the tax agency responds by contesting the filing. Next, because it is in the interest of all parties, the players bargain. 4 If the advisor believes that the low tax payment is indisputable (i.e., it will most likely be upheld in court), rather than negotiate, the logical move is to fight the tax authorities so that the tax liability is not increased. The longer the tax advisor insists, the more credible an aggressive report appears to the tax agency. Likewise, an advisor who is less certain of the merits of a case may mimic this resoluteness, and thereby induce the agency to concede and accept the low return. 5

To position our contribution to the literature on tax advisors, we observe that three strands of research have emerged: empirical, experimental, and analytical. Empirical research focuses on the effect of tax advisors on tax payments and the dual role of tax advisors as auditors (e.g., Cook & Omer, 2011; Gleason & Mills, 2011; Hite & Hasseldine, 2003; Klepper & Nagin, 1989; Lassila et al., 2010; Omer et al., 2006). 6 Experimental research focuses on the decision-making of the tax advisor and the clients (see, for example, Cloyd & Spilker, 1999, and the citations therein). Analytical research commonly treats the tax advisor as a mechanism to settle ambiguous tax issues rather than as a strategic player (e.g., Beck et al., 1996; Melumad et al., 1994; Reinganum & Wilde, 1991; Sansing, 1993).7,8 In contrast, in our study the taxpayer can opt to reject aggressive advice in favor of a more conservative (and thus a possibly more costly) strategy. This is indirectly supported by Cloyd and Spilker’s (1999) findings that, on average, taxpayers are less aggressive than tax advisors.

Similar to Phillips and Sansing (1998), we find that tax professionals have an adverse effect on tax collection. Their results are driven by the advisors’ incentives when they are paid contingent fees. Our contribution is that we show that tax advisors are likely to push for more aggressive tax reporting even if they are not paid contingent fees.

De Waegenaere et al. (2015) examine the financial reporting effects of tax aggressiveness, particularly the effects of accounting-based compensation for tax managers on the aggressiveness of the tax reporting strategy that they adopt. They show that incentives that reward tax managers for tax positions that decrease cash taxes paid and penalize them for unrecognized tax benefits motivate advisors to take positions that efficiently attain the level of tax avoidance that the client prefers. Complementing De Waegenaere et al. (2015), this study looks at another determinant of the aggressiveness of tax avoidance: the involvement of tax advisors in the bargaining process and, moreover, their reputation.

The rest of this study is structured as follows: the next section presents the model, followed by the analysis of the equilibrium. Last, we present the conclusions of this study.

The Model

The Players and General Setting

We analyze the bargaining game between two risk-neutral players: the tax authority (T) and the taxpayer–advisor team (C-A), where C is the taxpayer (client) and A is the advisor, who prepares the tax return for C and advises on it. The C-A coalition’s overall objective is to minimize the expected tax payment, while T’s objective is to maximize it. Bargaining takes place between C-A and T when T does not accept the tax return of C. The source of conflict between T and C-A is the ambiguity of the tax code, which offers a plethora of legitimate tax payments. 9

There are two types of C’s in our model, based on their tax liabilities. These liabilities can either be high,

If bargaining fails and the case goes to court, we assume for the sake of simplicity that the court can determine with certainty if C is type

The Bargaining Game

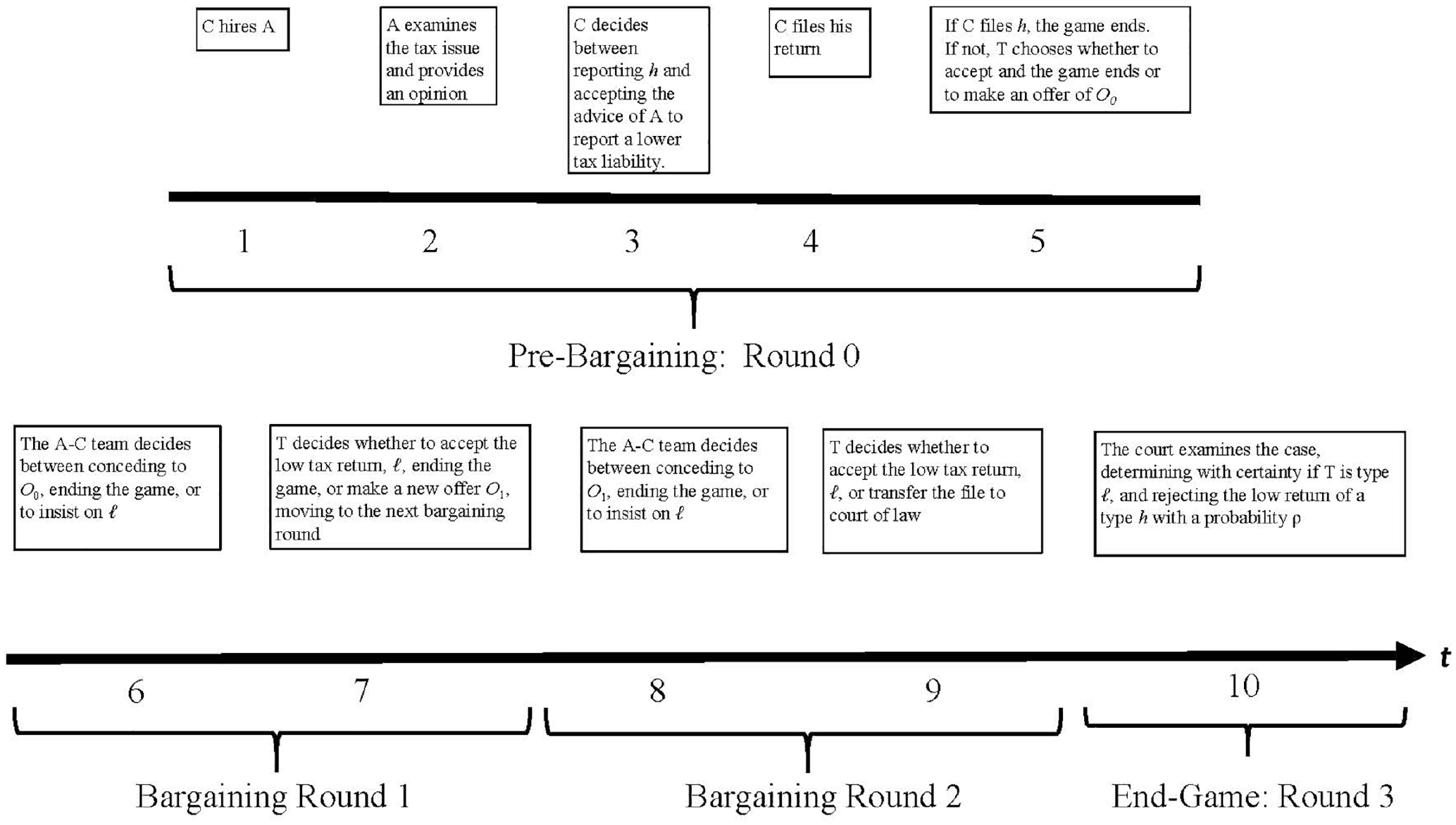

The timeline of the game is presented in Figure 1. It builds on the alternating offer, incomplete information game of Ordover and Rubinstein (1986). Let k denote a bargaining round with a maximum of three rounds of bargaining, k < K = 3.

11

The game starts at k = 0 when the taxpayer, C, must file a return. C is uncertain about the tax liability and selects an advisor, A, based on their reputation. For simplicity sake, we assume two types of advisors that differ only in terms of the reputational loss, that is,

Timeline of events in the game.

In each bargaining round prior to K (k = 1, . . ., 3), the C-A team examines the offer from the previous round,

If the bargaining does not conclude with an agreement by k = 2, T decides at k = 3, whether to accept the low return, which ends the game with C paying low return, or transfer the file to the court of law, which serves as the ultimate arbiter.

The Payoffs

Steps in modeling players’ payoffs

We first model the individual payoffs for C and A to formulate the payoff of the C-A coalition. We then model the payoff of T.

C’s payoff

We denote the periodical bargaining cost of the team as

If C is type

If, on the contrary, C is type

A’s payoff

We denote by

Consequently, the tax advisor’s problem is to maximize their fees, as follows:

such that

Equation 3 states that A maximizes their utility, made of the sum of their expected fees from all rounds, less expected reputational loss if their position is rejected in court, subject to a reservation utility constraint. For the sake of tractability, we assume that constraint (4) is binding and assumes the following form

The taxpayer-advisor team’s payoff

We treat the advisor and the taxpayer as a team whose objective is to minimize tax payment (e.g., Cloyd & Spilker, 1999). The C-A team’s problem is as follows:

The decision that the C-A team makes in each period, to maximize (6), is whether to concede at this period to T’s offer, or insist on their report. In essence, these decisions boil down to choosing xk in each period k subject to the choices made by T, as we discuss next.

We make the following technical assumption on the magnitude of the reputation loss,

T’s payoff

We denote the periodic bargaining cost for T as

Equation 8 states that T’s payoff is made of three elements: (1) the expected tax collection, (2) the expected total bargaining cost over all periods, and (3) the expected litigation costs for T,

To ensure that T does not give up on bargaining because T concedes at k = 1, we assume that

Analysis and Results

We begin by showing the existence of mixed-strategy equilibrium and ruling out the pure strategy equilibrium.

(a) The bargaining subgame has a mixed-strategy equilibrium wherein each stage is reached with some positive probability, that is,

(b) The bargaining game does not have any pure-strategy equilibrium.

All proofs that are not presented in the body of the article, are relegated to Appendix A.

Lemma 1’s importance lies in the fact that it precludes the possibility that any player will concede for sure at any bargaining round (i.e., the possibility of

We denote by

Lemma 2 establishes that reputable advisors’ fees exceed those of less reputable advisors. The intuition behind Lemma (2) is straightforward: High reputation tax advisors, that is, those whose reputational loss in period K is higher than others if the return is rejected, would charge a higher fee to compensate for their loss and meet their reservation utility constraint.

Next, we analyze the sustainable equilibrium underlying a type

Define

The intuition behind Proposition 1 is that whether a trial will only take place is based on the relation of

Next, we analyze the tax authority’s decision on the number of bargaining rounds.

Proposition 2 states that the agency will extend the bargaining to three rounds only if the probability of the C-A team conceding in round two,

The following Lemma examines the relationship between the probability of the C-A team conceding and the tax agency’s offer.

Lemma 4 states that the probability that the C-A team gives into the tax authority in each period decreases with increase in the offer made. The intuition is straightforward: the higher the counteroffer that the tax agency makes, the more attractive going to court becomes for the taxpayer-advisor team.

Next, we analyze the equilibrium counteroffers made by the tax authority. We denote the elasticity of

Proposition 3(a) states that the offer in period 0,

The next Lemma establishes that the probability that the tax agency concedes in period 2 increases with the reputation of the tax accountant.

The intuition behind Lemma 5 is that a high-reputation tax advisor who rejects the tax agency’s offer and proceeds to the second period incurs potentially a high reputational loss from a defeat in court in the third round. Consequently, the insistence of such an advisor itself erodes the tax authority’s resolve in the second round.

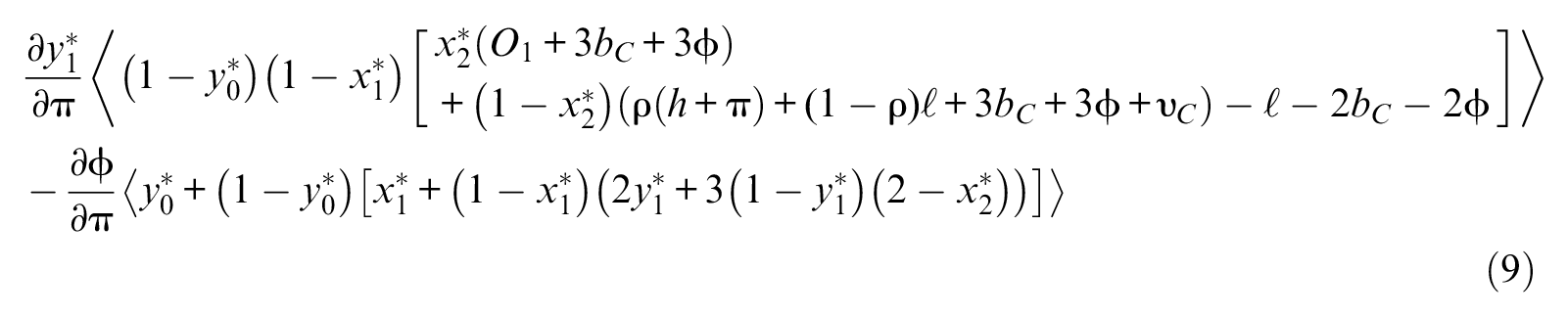

The first line in Equation 9 above is the improvement in the taxpayer’s payoff from choosing a high-reputation tax advisor, resulting from the increased probability of the tax agency conceding (as shown in Lemma 5). The second line in Equation 9 is the increased fees when hiring a reputable professional (as shown in Lemma 2). Consequently, Proposition 4’s intuition stems from the fact that the taxpayer chooses a high reputation tax advisor only as long as their incremental benefit from this choice exceeds the incremental costs of hiring such a tax advisor.

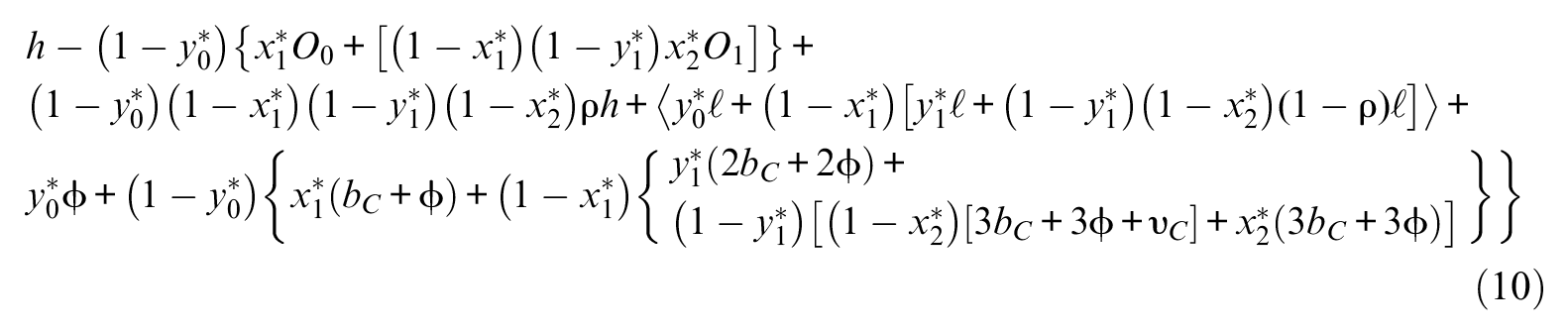

Proposition 5 states that a type

Concluding Remarks

It is widely accepted that the implementation of the tax code requires interpretation. Furthermore, in some instances, implementing the code to the letter would result in a lower tax liability than what the regulator intended. Thus, tax advisors play a two-fold role that benefits both the taxpayer and the tax agency. They advise taxpayers on how much to report and pay, and inform them of potential risks and repercussions (leaving it to the discretion of the taxpayer whether or not to follow the advice). Second, they bargain with the tax authorities to determine the correct interpretation of the tax code.

We use a bargaining model to focus on the bargaining process itself and obtain some insights beyond the extant literature on the research questions that we explore here.

First, we show the existence of a mixed strategy equilibrium and preclude the possibility of a pure strategy equilibrium. The importance of this finding lies in the fact that it precludes the possibility that any player will concede for sure at any bargaining round. Another important feature of this finding is that it precludes any player from avoiding bargaining and straightaway going to court.

Second, we find that high tax types will be aggressive in their tax reports at a frequency that depends on the tax agency’s beliefs on the taxpayer type.

Third, we analyze the tax agency’s decision on the number of bargaining rounds it should pursue. Our model demonstrates that the tax agency should aim for a longer bargaining process when the expected spread between the payoff from the agency’s offer and expected result in court exceeds the agency’s bargaining costs. However, the tax agency should shorten the number of bargaining rounds when the sum of this expected spread falls below the agency’s bargaining costs.

Fourth, we analyze the counteroffers that the tax agency should make during bargaining. The first counter-offer should consider its negative effect on the probability of the taxpayer-tax advisor team conceding, the agency’s bargaining costs, and its opportunity costs from not settling. The second counteroffer should consider its negative effect on the other party’s probability of conceding and expected payoff from going to court.

Fifth, we argue that the taxpayer chooses a high reputation tax advisor only as long as the incremental benefit to the taxpayer from the increased probability of the tax agency conceding exceeds the incremental costs of hiring such a tax advisor.

Finally, we show that the taxpayer’s decision whether to accept or reject the tax advisor’s recommendation to file a low return hinges on whether the high tax liability exceeds, or falls below, the sum of expected counter-offers from the tax agency, tax payments, and related costs (tax advisor’s fees, total bargaining costs, and litigation costs).

Future research on this issue may adapt this model and extend it to risk-averse tax advisors, or consider the costs to reputation as a factor in advisors’ decision-making. For our purposes, we assume that the players are risk-neutral, whereas it stands to reason that they might be risk-averse (Polinsky & Shavell, 1999). It seems intuitive that if advisors are risk-averse, they might be less inclined to be aggressive. We also ignore the possible correlation between the professionalism of the tax advisor and expected loss of reputation, as well as the budgetary constraints of the taxpayer, for the choice of the type of tax advisor. Our analysis indicates that the selection of an advisor hinges on the trade-off between lower tax payment, lower reputation, and possible costly negotiation, so that in equilibrium there could be highly reputable advisors who are not approached because they are too expensive. Indirect evidence for such a profile is provided by Lin (2000), who finds that the quality of returns prepared by tax advisors is higher than those prepared otherwise. It would be interesting to further explore these questions in the future.

We assume for sake of simplicity that courts can determine with certainty the existence of a low liability return but could err in determining a high tax liability. A possible extension of this study could embed a probability of the court erring also in determining a low tax liability, that is, allowing for both false negatives and false positives in the decision-making process of the court.

Another issue that is ignored in this study is the possibility of differential bargaining costs for taxpayers who hire reputable tax advisors, compared with those who hire other advisors. An interesting extension to this study could analyze this case as the higher costs associated with hiring reputable tax advisors might offset of the benefits of such advisors in the bargaining process.

This study uses binary alternative tax returns: high and low. Consequently, an extension to the study could embed a medium tax return, thus, allowing a more flexible cutoff for renegotiation that might make the game richer and more interesting.

In conclusion, this study provides significant contributions in several regards. First, contrary to the rich extant literature that is primarily concerned with tax evasion, this study focuses on compliance and tax avoidance. In this case, the tax liability is uncertain, even to the tax revenues agency. Second, our analysis explains the empirical findings of previous studies that show that tax professionals tend to be more aggressive than taxpayers. Third, we show that tax authorities could increase collection, even without obtaining costly information, through the design of the bargaining process. These findings offer significant implications for public policy and provide solutions that tax agencies may enact to allay and deter tax aggressiveness.

Footnotes

Appendix A

Appendix B

Acknowledgements

We would like to thank the Bharat Sarath, and anonymous reviewers, and Jeff Callen, Alex Edwards, Paul Halpern, Alexandra Mackay, Michael Marin, Jack Mintz, Jan Sweeney, and seminar participants at Ben-Gurion University and the Rotman School of Management for many helpful suggestions and comments. We would like to thank Editage (![]() ) for English language editing.

) for English language editing.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.