Abstract

Throughout their business life cycle, firms may experience financial distress. Successful emergence from such distress is important to their multiple stakeholders. Using a sample of publicly listed firms in China that emerged from Special Treatment (an indicator of delisting risk), we focus on the key actions such firms take prior to emergence, namely, fixing the core of the business and earnings management. We examine how these actions are associated with sustainable emergence, which we define as emergence from Special Treatment without reentry in the next 5 years. Consistent with the expectation that shortcut fixes to problems do not yield a long-term solution, we find that repairing the core of the business by improving operating efficiency is positively associated with sustainable emergence, whereas earnings management is negatively associated with it. We also find that the positive (negative) association between fixing the core (earnings management) and sustainable emergence is pronounced only for state-owned enterprises. Our article adds to the limited literature that examines issues related to distressed firms’ sustainable turnaround.

Introduction

During their business life cycle, firms may become financially distressed, with some ultimately going bankrupt. Financial distress adversely affects multiple stakeholders, including shareholders, creditors, employees, customers, and suppliers. Early research on distressed firms focuses on how to predict financial distress using financial ratios (e.g., Altman, 1968; Ohlson, 1980), while more recent work attempts to improve on these prediction models (e.g., Campello et al., 2011; Darrat et al., 2016; Hillegeist et al., 2004; Vassalou & Xing, 2004). Yet another strand of literature predicts emergence (e.g., Barniv et al., 2002; Bryan et al., 2002; Donovan et al., 2015; Kim et al., 2016) or examines management after financial distress by focusing on corporate governance (Gilson, 1990) and organizational efficiency (Wruck, 1990). However, scant research focuses on the factors that can lead to sustainable emergence, which can be defined as breaking free from distress without falling back into it. To the best of our knowledge, Hotchkiss (1995) offers the only examination of sustainable emergence. In her study of 197 U.S. firms that successfully restructure their business and emerge from Chapter 11, she documents that more than 40% of sample firms continue to experience operating losses and most of these firms later file for bankruptcy protection.

In this article, we extend the literature on sustainable emergence from distress by examining how firms’ actions on fixing the core business and upward earnings management are associated with sustainable emergence. We employ the unique setting of China’s Special Treatment (ST) system. Under this system, if a firm experiences two consecutive years of losses, its stock name is tagged with the designation “ST,” which alerts the public to the firm’s abnormal circumstances and delisting risk. Once a firm receives this designation, it has a short time frame to improve its financial condition. If it accomplishes this improvement, the ST designation is removed and the firm returns to a normal listing status. 1 Firms that cannot improve their financial condition within the designated period face delisting.

Most of the prior research using China’s ST system focuses on predicting the probability of financial distress (e.g., Y. Jiang & Jones, 2018; Y. Wang & Campbell, 2010), with some studies predicting emergence from ST (e.g., Kim et al., 2016). To our knowledge, no previous study uses the ST system to examine sustainable emergence. The ST system offers several research advantages. First, it has three well-demarcated phases: entry into ST, emergence from ST, and the postemergence period. Second, firms’ financial data are available for all three phases, allowing an investigation of how actions taken in one phase can affect a firm’s situation in the next. Hence, we can examine how distress-phase actions affect firms’ long-term postemergence survival. 2

Using a sample of 209 observations of emergence from ST between 1998 and 2013, we first identify the actions taken by firms prior to their emergence. In particular, we focus on two types of action: earnings management and fixing the core business. Earnings management is a shortcut that is strongly motivated by China’s accounting-based capital market regulations (e.g., S. Chen et al., 2009; K. C. Chen & Yuan, 2004; N. Du et al., 2015), while fixing the core is the more obvious and profound action for any firm in financial distress. We focus on four dimensions for fixing the core: (a) improvement in operating efficiency, (b) increase in market share, (c) changing the CEO, and (d) changing board directors. We employ a principal component analysis (PCA) to create composite fixing-the-core measures that can capture these dimensions. For earnings management, we focus on accruals-based upward earnings management by estimating the modified Jones (1991) model.

We then empirically examine the link between these actions and sustainable emergence, using a 5-year period. We consider a firm as having emerged sustainably if it is not redesignated as an ST firm within 5 years of emergence. Of the 209 observations in our final sample, 134 (64%) are categorized as sustainable emergences. Relying on multivariate regressions, we find that firms that take actions to fix the core are more likely to have sustainable emergence. This evidence is consistent with the notion that firms, especially those in trouble, must take significant steps to recover and to ensure their long-term survival.

We also document that firms that engage in upward earnings management are less likely to emerge sustainably from financial distress. This finding is consistent with future accruals reversal, a key limitation of accruals-based earnings management (e.g., DeFond & Park, 2001; Guay et al., 1996). Managing accruals upward can boost the earnings number and enable a firm to fulfill the conditions for emerging from ST. However, the improvement is only temporary, and problems occur when the future accruals reversal creates a downward pressure on future earnings. Our main findings—namely, the positive (negative) association between fixing the core (earnings management) and sustainable emergence—are robust to alternative measures of fixing the core, alternative definitions of sustainable emergence, and alternative regression models.

Next, we examine whether being a state-owned enterprise (SOE) moderates the relation between fixing the core, earnings management, and sustainable emergence. SOEs not only receive political favors (e.g., C. A. Cheng et al., 2015; Lin & Tan, 1999; Q. Wang et al., 2008) but also can enjoy other benefits such as positive signaling and business connections (Sun et al., 2002). We argue that being an SOE facilitates firms’ fixing the core of their business, and we therefore expect the positive association between fixing the core and sustainable emergence to be greater for SOEs. Due to SOEs’ weak monitoring and significant incentives and opportunities for earnings management (D. Chen et al., 2018; F. Du et al., 2012), any abnormal positive earnings they report, relative to non-SOEs, are more likely to be due to manipulative accounting practices that are not sustainable. Hence, we expect the negative association between earnings management and sustainable emergence to be greater for SOEs. Consistent with our prediction, we find that the positive (negative) association between fixing the core (earnings management) and sustainable emergence is pronounced only for SOEs.

In additional analyses, we first examine whether complementary or substitution effects occur between fixing-the-core actions and earnings management, but we find no evidence of such effects. We then examine several alternative outcomes of fixing the core and earnings management. Consistent with our main arguments, we find that fixing the core benefits firms’ operations and future performance, while earnings management harms firm value. Finally, using a sample of firms that experience a first-year loss, we document that both fixing the core and earnings management can help in avoiding the ST designation. This finding highlights the distinctive role of earnings management: it can serve as a shortcut solution for imminent problems, but it is detrimental to the firm’s long-run survival.

Our study contributes to the literature in several ways. First, it adds to the literature on restructuring troubled organizations (e.g., Hotchkiss, 1995; Wruck, 1990). In particular, our findings highlight the importance of these firms taking serious organizational restructuring action rather than opting for shortcuts such as earnings management. We provide evidence that actions taken to fix the core business help the firm emerge sustainably from financial distress. Our article also contributes to the SOE literature. For example, while we hypothesize that the positive effect of fixing the core on sustainable emergence should be more pronounced for an SOE due to government (explicit and implicit) support, we find that fixing the core through operation improvements increases the likelihood of sustainable emergence if and only if the firm is an SOE. This finding highlights the importance of government support to complement a firm’s efforts in improving its operations for long-term recovery from financial distress.

In addition, we exploit a unique Chinese setting to add to the literature on earnings management by providing further evidence that accrual-based earnings manipulation has an adverse effect on firms’ long-term performance (e.g., Teoh et al., 1998). To the best of our knowledge, we are the first to show that earnings management cannot lead to sustainable emergence from financial distress. Finally, we add to the small but growing literature on the Chinese ST system (e.g., Haw et al., 2008; Y. Jiang & Jones, 2018; Kim et al., 2016; Y. Wang & Campbell, 2010). Prior studies focus on predicting distress and emergence from it within the ST system. 3 Our study contrasts with and complements this vein of the literature by addressing a missing but important aspect of the system—the sustainability of firms’ emergence.

Background and Hypothesis Development

Among the few papers predicting sustainable emergence of firms from distress, Hotchkiss (1995) examines postbankruptcy performance and management control and finds that one third of the firms that emerge from financial distress fall back into it. Furthermore, Altman et al. (2009) find that two thirds of postbankruptcy firms underperform their industry peers, indicating how rocky the road to recovery can be. Wruck (1990) illustrates potential postdistress conflicts due to information asymmetry.

Conditional on emergence from distress, two postemergence outcomes are possible. First, a firm could continue to generate a negative cash flow, in which case the distress is a permanent problem. Alternatively, a firm could regain its profitability momentum and generate a positive cash flow again, in which case the distress is only temporary. When a firm is in financial distress, it can attempt to save itself by fixing its core business and/or by using strategic measures such as earnings management. Within the ST system, the use of earnings management can be especially attractive because ST firms are required to report profits before the designation is removed.

Fixing the Core and Sustainable Emergence

Our first hypothesis examines how fixing the core affects the likelihood of sustainable emergence. Core-fixing actions require stakeholders’ extensive involvement. Managers have to engage the entire organization in the plan and explain how the proposed actions will help the business recover. The plan requires support from the board of directors, outside shareholders, and creditors. The journey to recovery can be painful, as restructuring may cost some people their jobs. In this article, we focus on four actions: (a) improving operating efficiency, (b) increasing market share, (c) changing the CEO, and (d) changing board directors.

An obvious reason for firms becoming distressed is that they are inefficient, possibly due to agency problems. For example, some manifestations of agency problems include managers growing the firm beyond its optimal size and increasing personal utilities from status, power, compensation, and prestige (e.g., Jensen, 1986; Jensen & Meckling, 1976). One indication of inefficiency is the high operating expenses per dollar of sales generated (C. X. Chen et al., 2012). Hence, for a distressed firm that is trying to achieve a sustainable emergence, improving operating efficiency is likely to be important.

Firms in financial distress often lose market share to their competitors because customers typically have concerns about purchasing from distressed firms. Increasing market share, especially for distressed firms, requires a high level of effort because the firm must convince its customers that it can provide a quality product and/or service and will be able to fulfill implicit claims in the long run (Bowen et al., 1995; Roberts, 1999). Hence, to the extent that the firm is able to increase its market share, its ability to emerge sustainably from distress is improved.

Not surprisingly, management turnover is high when a firm is in financial distress (Gilson, 1989). Hudaib and Cooke (2005) emphasize that the leader that brought the business into distress is not fit to usher it to recovery. In addition, the dismissal of a poorly performing CEO will likely lead to turnover of top management, driven by the replacement CEO. Such actions can foster a faster recovery. Hotchkiss (1995) shows that the involvement of prebankruptcy management in the restructuring process is strongly associated with poor postbankruptcy performance. Distress can also drive changes in the board of directors. The board can be restructured, with old members being replaced by new ones who are more engaged and better able to lead the business to recovery.

When a distressed firm starts to implement actions to fix its core during times of distress and continues these actions upon emergence, the result is a stronger foundation that will help it avoid future distress. Therefore, our first hypothesis is as follows:

H1 is not without tension. While fixing the core is the typical mantra when firms are in financial distress, it is not easily accomplished and the firm may remain in financial distress for a prolonged period of time, especially given the rigid loss-based rules related to ST. For instance, once a firm is already in ST, it may already be too late to fix the core because the investors and creditors might want to cut their losses and the suppliers and customers might not want to transact with an ST firm. In addition, some actions to fix the core such as changing the CEO and board directors can be costly, which can make it harder for the firm to avoid another ST. The benefits from these actions, specifically profits, might also take time to materialize.

Earnings Management and Sustainable Emergence

Next, we consider the long-run consequences of using earnings management to save a distressed firm. Prior literature amply documents the strategic use of earnings management to avoid problems. For example, managers make accounting choices to increase income when their firms are close to debt covenant violations (e.g., DeFond & Jiambalvo, 1994; Jaggi & Lee, 2002), and banks use discretionary loan loss provisions to avoid earnings decreases and/or violations of regulatory capital minimums (e.g., Ahmed et al., 1999; Beatty et al., 1995).

In China, distressed ST firms manage earnings upward to maintain their listing status (X. Chen et al., 2008; P. Cheng et al., 2010). G. Jiang and Wang (2008) argue that the current earnings-based ST system drives financially healthy firms out of the stock market and induces listed firms to engage in rampant earnings manipulation behavior. However, earnings management can adversely affect firms’ future performance. Because accruals are mean reverting, earnings manipulations attributed to accruals reverse in the following years (Dechow, 1994; Dechow et al., 1995). Issuers reporting higher positive earnings and abnormal accruals are followed by poor long-run earnings and negative abnormal accruals (Cohen & Zarowin, 2010; Teoh et al., 1998). In particular, Cohen and Zarowin (2010) find that underperformance is driven by accrual reversals.

If delisting is imminent, managers may manipulate earnings to emerge from ST and thereby retain the firm’s near-term listing status. However, earnings management may provide only a temporary rescue for the distressed firm. That is, a firm using earnings management to emerge from financial distress is less likely to acquire long-run sustainability. We state our second hypothesis as follows:

Although we posit that accruals reversal makes upward earnings management unlikely to be effective for sustainably emerging from financial distress, a counter-argument can be made. For example, a firm can try to delay or soften the impact of accruals reversal by working hard to grow after ST emergence, especially if other stakeholders, perhaps attracted by the success of emergence from ST, are willing to provide support and/or do business with it. The firm can also manage the accruals reversal to avoid two consecutive periods of losses that would cause the firm to fall back into ST. This line of argument provides some potential tension to our H2.

The Moderating Effect of Being an SOE

Our third hypothesis focuses on the moderating effect of being an SOE. In China, which has many SOEs, the government plays an important role in the economy. When a distressed firm wants to fix its core, it likely requires some support as it navigates the difficult period of change. An important feature of SOEs is that by virtue of being owned by the government, these enterprises enjoy explicit and/or implicit support by various stakeholders. SOEs have favorable access to capital markets (C. A. Cheng et al., 2015), and they typically expect government support when they are in trouble (Lin & Tan, 1999; Q. Wang et al., 2008). For example, Lin and Tan (1999) note that because the state carries the burden of achieving policy goals, the enterprises that help shoulder it will bargain with the state for ex ante policy favors, such as access to low-interest loans, tax reductions, tariff protection, legal monopolies, and so on. In addition, SOEs enjoy favorable treatment from other parties, such as state-owned banks in particular. Brandt and Li (2003) and Firth et al. (2009) find strong evidence that state ownership helps firms obtain bank loans. Sun et al. (2002) suggest that beyond political and financial support, an SOE can have other benefits such as positive signaling and business connections. Hence, if an ST firm is willing to fix its core business and has the government’s support, we expect the likelihood of sustainable emergence to be greater.

Regarding the use of earnings management to emerge from ST, we expect its negative effect on sustainable emergence to be more pronounced for SOEs. The agency problem of earnings management is likely to be worse for them because of weak monitoring by the state, especially for poor-performing SOEs attempting to misreport their earnings number. This weak monitoring can be attributed to concerns that the state will be held accountable for the SOE’s poor performance (Lin & Tan, 1999). In other words, the interests between the state and the SOE are aligned in terms of earnings management. X. Chen et al. (2008) find that in China, collusion related to earnings management occurs between local governments and the listed firms that they control. Prior studies also highlight that managers of SOEs have significant incentives and opportunities to engage in earnings management (D. Chen et al., 2018; F. Du et al., 2012). Hence, any abnormal positive earnings reported by an SOE, compared with a non-SOE, are more likely to be due to the manipulation of the earnings numbers rather than real managerial efforts to improve the business. Manipulation of earnings numbers is unlikely to be sustainable for reasons such as accruals reversal.

We formally state the hypotheses on the moderating effect of SOEs in alternative form as follows:

Research Methodology

China’s ST System

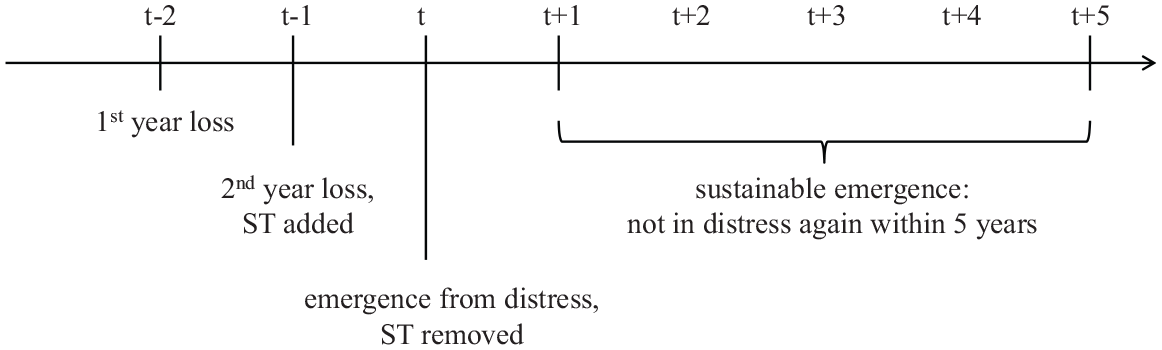

China offers a unique setting for testing our hypotheses. The Chinese stock market was established in the early 1990s and the China Securities Regulatory Commission (CSRC), founded in 1992, acts as the primary regulator (G. Chen et al., 2005). As a relatively new equity market with a higher percentage of individual investors, the CSRC established the ST designation in 1998 as a signaling scheme to warn investors about a firm’s financial distress or other unusual situation that might seriously affect its performance. Several circumstances can lead to ST, but the most common involves a firm reporting losses for two consecutive years, which suggests it is in financial distress. A stock labeled “ST” is limited to a ±5% daily price fluctuation, and ST firms must have their semi-annual financial reports audited (Haw et al., 2008; Kim et al., 2016). 4 The CSRC gives an ST firm 1 year to improve its financial performance to retain its listing status. If the ST firm reports a net profit in the following year, the ST designation is removed; that is, the firm emerges from distress. If the ST firm records another year of losses (i.e., three consecutive years of losses), the CSRC suspends its stock trading and gives it a maximum of 6 months to restructure and propose a reorganization plan to the CSRC. During this period, the firm must disclose monthly any particular action (or lack of action) taken for the purpose of being relisted. After the deadline, it can either emerge with a better performance, including through methods such as the shell game, or be delisted permanently from public trading.

In China, every firm has the same fiscal year end, December 31, and all listed firms must release their annual financial reports within the first 4 months of the subsequent year. In most cases, a firm in distress acquires the ST label immediately after it releases a financial report indicating 2 years of consecutive losses. Likewise, the removal of the ST designation occurs after an annual financial report shows financial improvement. We define year t as the fiscal year when the firm’s financial result is satisfactory and leads to the removal of its ST designation.

Figure 1 illustrates the timeline of the ST setting. Our focus is firms emerging from distress (i.e., successfully removing the ST designation in year t). We track each emerged firm for at least 5 years after its emergence to determine whether it emerges sustainably.

Timeline of the ST setting.

The China ST system differs substantially from the United States Bankruptcy Code (Chapter 11). Firms with the ST designation are not bankrupt, and the designation is not a result of legal enforcement action or an actual delisting. The designation merely signals that the firm is in distress. Because of the clear guidelines on what constitutes distress and how firms can emerge from it, the ST setting is better than many others for examining sustainable emergence. Furthermore, the ST firms’ financial data are available during the distress period. In contrast, a firm filing for Chapter 11 in the United States is no longer required to disclose financial information.

Measures of Fixing the Core

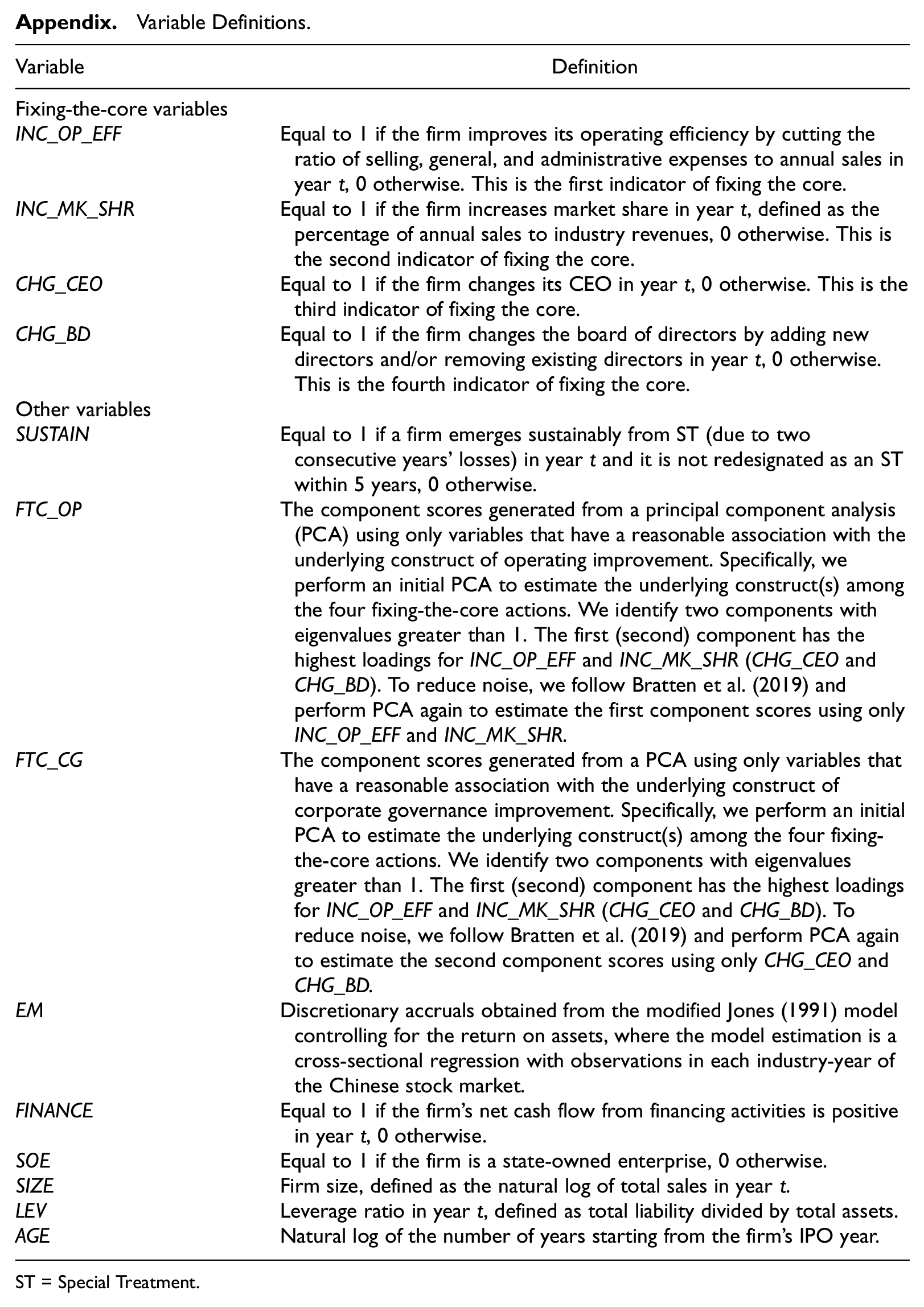

In this article, we focus on two types of action that ST firms take prior to emergence, namely, fixing the core of the business and earnings management. In terms of fixing the core of the business, we create four indicator variables as follows: (a) improvement of operating efficiency (INC_OP_EFF), which equals 1 if the firm improves its operating efficiency by cutting the ratio of selling, general, and administrative expenses to annual sales in year t, and 0 otherwise; (b) increase in market share (INC_MK_SHR), which equals 1 if the firm increases market share, defined as the percentage of annual sales to industry revenues, in year t, and 0 otherwise; (c) changing the CEO (CHG_CEO), which equals 1 if the firm changes its CEO in year t, and 0 otherwise; and (d) changing the board of directors (CHG_BD), which equals 1 if the firm changes board directors by adding new directors and/or removing existing directors in year t, and 0 otherwise.

To construct a composite measure of fixing the core, we conduct a PCA on the four indicators described above. 5 Based on the results of the PCA (section “PCA of Fixing-the-Core Actions”), we identify two components with eigenvalues larger than 1. The first (second) principal component has the highest loadings for the improvement of operating efficiency and the increase in market share (the change of CEO and the change of board directors). 6 To construct our primary measures of fixing the core, we adopt Bratten et al.’s (2019) approach to estimate component scores for these two components. Specifically, we perform a second round PCA to estimate component scores using only the two variables with the highest loadings on the first component. The first component essentially captures a firm’s operating improvement (i.e., the improvement of operating efficiency and the increase in market share), and the derived component scores are labeled FTC_OP. Similarly, we perform another PCA using only the two variables with the highest loadings on the second component to estimate component scores. The second component essentially captures a firm’s improvement in corporate governance (i.e., the change of CEO and the change of board directors), and the derived component scores are labeled FTC_CG. We include both FTC_OP and FTC_CG in all analyses for testing H1.

Measure of Earnings Management

We use signed discretionary accruals as our measure of earnings management (EM). Given that performance is an important determinant of total accruals (e.g., Dechow et al., 1995; Kothari et al., 2005), we control for current-year return on assets in the modified Jones (1991) model. 7 To derive the discretionary accruals, we first construct an estimation sample consisting of all available firm-year observations of all Chinese listed firms. We then estimate the modified Jones (1991) model separately for each industry-year subsample, and we require a minimum of eight observations. 8 By construction, the signed value of discretionary accruals is a proxy for upward earnings manipulation: A firm that more aggressively manipulates earnings upward will have a higher value of discretionary accruals.

Empirical Model

We use a logistic regression model to test H1 and H2, specified as follows:

The dependent variable for sustainable emergence (SUSTAIN) is a dummy equal to 1 if a firm emerges sustainably from ST, and 0 otherwise. A firm is considered to have emerged sustainably from ST in year t if it is not redesignated as an ST within 5 years. For example, as illustrated in Figure 1, if a firm emerges from ST in 2010 (year t), it is considered to have emerged sustainably if it does not fall back into distress between 2011 and 2015.

Our variables of interest include the first and second principal components of fixing-the-core actions (FTC_OP, FTC_CG) and earnings management (EM). Significantly positive coefficients on fixing-the-core actions (β1, β2) will be consistent with our prediction that fixing the core during the distress period increases the likelihood of sustainable emergence. Meanwhile, we expect the coefficient on earnings management (β3) to be significantly negative because accrual reversal decreases the chance of sustainable emergence.

We include several control variables in our baseline regression model. First, we include two proxies for external support. Financial support (FINANCE) is a dummy equal to one if the firm receives positive net cash flow from financing activities in year t, zero otherwise. Governmental support (SOE) is a dummy equal to one if the firm is an SOE, zero otherwise. We then control for several firm-level characteristics that can influence the likelihood of sustainable emergence. Firm size, SIZE, is the natural logarithm of a firm’s total sales in year t. 9 A larger firm can have more resources for restructuring and more assets to use as collateral when it needs capital. LEV is the liability ratio at the end of year t. Firm age, AGE, is defined as the natural logarithm of the number of years from the IPO year to year t. We expect a firm with a longer listing history to have more advantages because its brand and reputation may help it acquire financing or gain market share. Finally, we include year fixed effects and industry fixed effects. Industries are categorized according to the CSRC-issued Guidelines for the Industry Classification of Listed Companies (2012 Revision). Given that our final sample size is relatively small, we use the one-digit industry code for industry classification. We summarize the variable definitions in Appendix. We winsorize all continuous variables at the first and 99th percentiles.

Sample Selection and Descriptive Analyses

Sample Construction

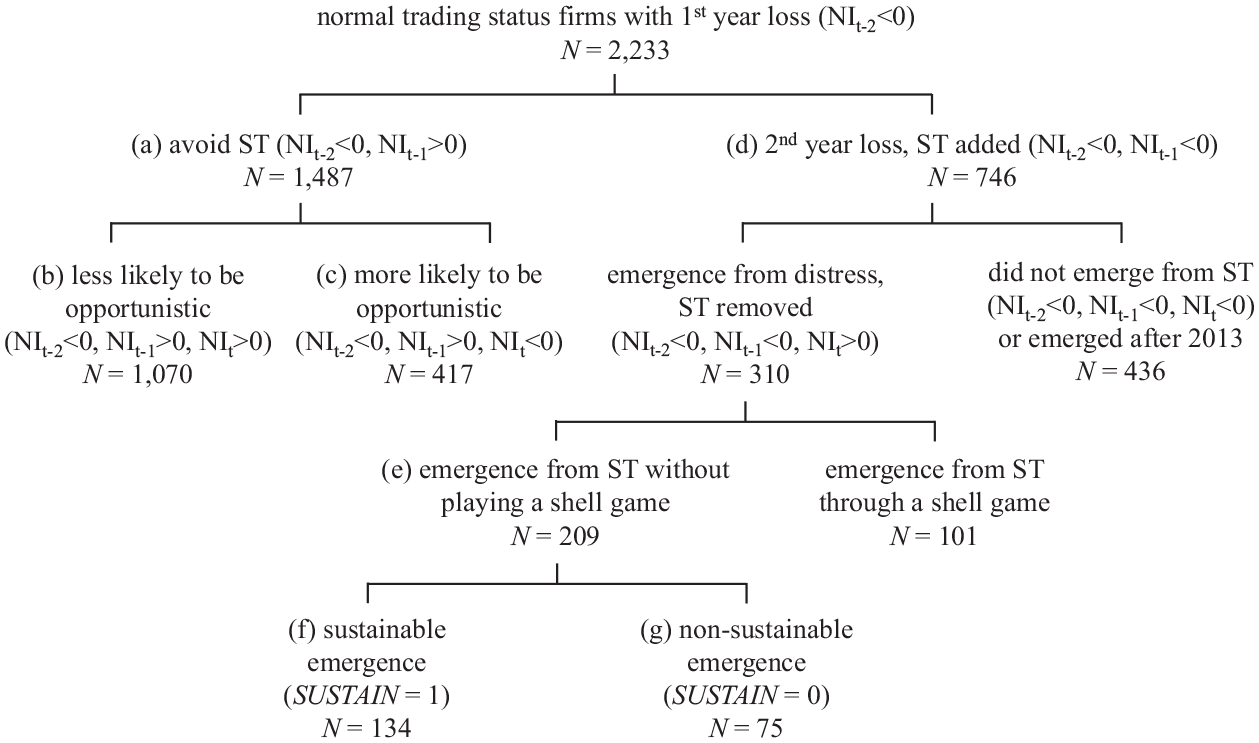

The China Stock Market and Accounting Research (CSMAR) database provides historical financial data and the trading status for each Chinese listed firm. We construct our sample from these data, as summarized in Figure 2. Since we focus on firms facing heightened delisting risk due to two consecutive years of losses, our sample selection starts with normal trading status firms (without any prefixes to their stock names) that experience their first-year loss during the period of 1998 to 2018. As depicted in Figure 1, we define the year when the firm experiences its first loss as year t− 2. This initial step leaves us with 2,233 firm-year observations, of which 1,487 avoid the ST designation by reporting a profit in year t− 1. The remaining 746 observations are subject to the ST designation. According to the ST regulation, a loss (profit) is identified if the firm’s reported net income (NI) is negative (positive). Therefore, the avoid-ST sample consists of firms with an earnings pattern of (NIt−2 < 0, NIt−1 > 0), while ST firms have an earnings pattern of (NIt−2 < 0, NIt−1 < 0).

Sample construction.

Next, we consider firms that emerge from ST by reporting a profit in year t, that is, firms with an earnings pattern of (NIt−2 < 0, NIt−1 < 0, NI t > 0). As we need 5 years of forward-looking data to identify a sustainable emergence, we restrict our final sample period to 1998 to 2013 and obtain 310 observations of emergence. We further exclude 101 firms that emerge from ST due to a shell game because their actions likely do not reflect fixes to the core of their business. A shell game is a reverse-merger transaction, through which a private firm is merged into a listed firm and the private firm’s shareholders gain control of the combined entity (Lee et al., 2015). To identify shell games, we mainly rely on the information of controlling shareholders, which is available in CSMAR database. When a change of direct or ultimate controlling shareholder occurs in the emergence year, we search the firm’s filings as well as the internet to confirm if the emergence results from a shell game. The final sample for our main analyses consists of 209 observations, including 134 sustainable emergences and 75 nonsustainable emergences. 10

Descriptive Analysis of Fixing-the-Core Actions and Earnings Management

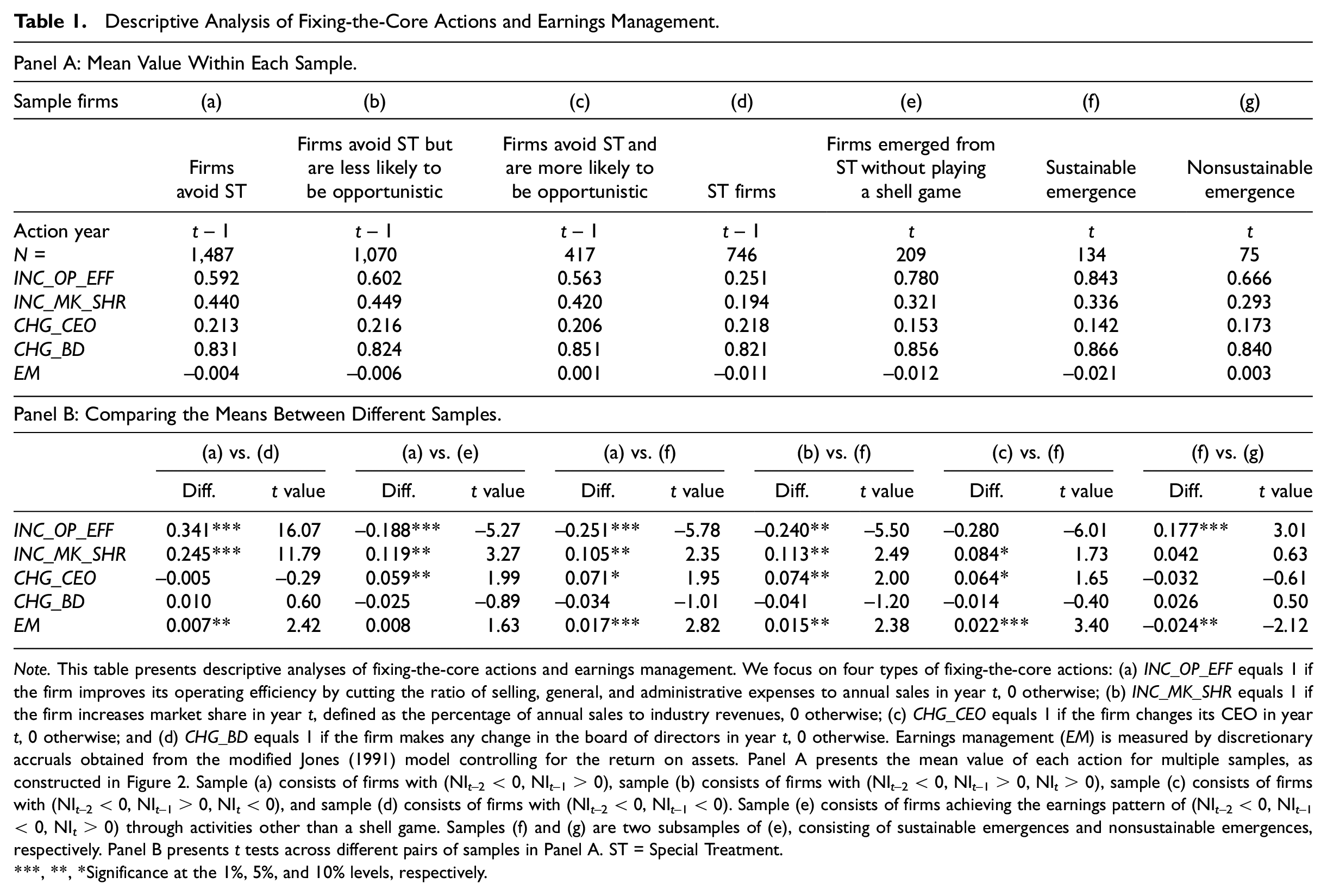

Based on the samples constructed as in Figure 2, we first conduct a descriptive analysis of the actions taken by the sample firms. In Table 1, Panel A presents the mean value of each fixing-the-core action as well as upward earnings management within each sample, and Panel B presents the results of t tests across different pairs of samples. Although our focus is the actions taken prior to ST firms’ emergence, we are also interested in whether firms that experience a 1-year loss will take similar actions to avoid the designation in the first place. We start by comparing the actions taken by firms to avoid ST with those of ST firms, that is, sample (a) versus sample (d). Consistent with the notion that both fixing the core and earnings management can help boost short-term earnings, firms avoiding the designation have a significantly higher frequency of improvement in operating efficiency (INC_OP_EFF) and an increase in market share (INC_MK_SHR) and use earnings management (EM) to a significantly greater extent.

Descriptive Analysis of Fixing-the-Core Actions and Earnings Management.

Note. This table presents descriptive analyses of fixing-the-core actions and earnings management. We focus on four types of fixing-the-core actions: (a) INC_OP_EFF equals 1 if the firm improves its operating efficiency by cutting the ratio of selling, general, and administrative expenses to annual sales in year t, 0 otherwise; (b) INC_MK_SHR equals 1 if the firm increases market share in year t, defined as the percentage of annual sales to industry revenues, 0 otherwise; (c) CHG_CEO equals 1 if the firm changes its CEO in year t, 0 otherwise; and (d) CHG_BD equals 1 if the firm makes any change in the board of directors in year t, 0 otherwise. Earnings management (EM) is measured by discretionary accruals obtained from the modified Jones (1991) model controlling for the return on assets. Panel A presents the mean value of each action for multiple samples, as constructed in Figure 2. Sample (a) consists of firms with (NIt−2 < 0, NIt−1 > 0), sample (b) consists of firms with (NIt−2 < 0, NIt−1 > 0, NI t > 0), sample (c) consists of firms with (NIt−2 < 0, NIt−1 > 0, NI t < 0), and sample (d) consists of firms with (NIt−2 < 0, NIt−1 < 0). Sample (e) consists of firms achieving the earnings pattern of (NIt−2 < 0, NIt−1 < 0, NI t > 0) through activities other than a shell game. Samples (f) and (g) are two subsamples of (e), consisting of sustainable emergences and nonsustainable emergences, respectively. Panel B presents t tests across different pairs of samples in Panel A. ST = Special Treatment.

, **, *Significance at the 1%, 5%, and 10% levels, respectively.

Next, we compare actions taken by sample (a) versus sample (e). Both groups of firms take actions to achieve positive NI, with sample (a) striving to avoid the ST designation and sample (e) aiming to emerge from ST. We find that, compared with sample (a), sample (e) has a significantly higher value of INC_OP_EFF but a significantly lower value of INC_MK_SHR. This finding suggests that when firms are already in trouble (e.g., already an ST firm), their first choice to achieve better performance is to improve operating efficiency. Only a small proportion can increase market share because it is extremely difficult for them to do so.

Moreover, we compare the actions taken by firms that avoid the ST designation with those of firms that sustainably emerged, that is, sample (a) versus sample (f). We find that sustainably emerged firms improve operating efficiency more frequently and are less likely to engage in upward earnings management. This finding is consistent with our expectation that sustainably emerged firms tend to take actions that can have long-term effects, while avoid-ST firms can rely on opportunistic behavior to inflate short-term earnings. To further uncover such behavior, we split sample (a) into samples (b) and (c). Sample (b) consists of firms with an earnings pattern of (NIt−2 < 0, NIt−1 > 0, NI t > 0), while sample (c) consists of firms with an earnings pattern of (NIt−2 < 0, NIt−1 > 0, NI t < 0). Relative to firms in sample (b), firms in sample (c) are more likely to be opportunistic in the sense that they avoid the ST designation by temporarily delaying reporting a loss. Focusing on the earnings management measure (EM), we then compare sample (f) with samples (b) and (c) separately. Consistent with our expectation, we find that the difference in means for (c) versus (f) (Diff. = 0.022, t value = 3.40) is even larger than that of (b) versus (f) (Diff. = 0.015, t value = 2.38). Taken together, compared with the firms that avoid ST, sustainably emerged firms put more effort into improving operating efficiency and engage in opportunistic behavior to a lesser extent.

Finally, we focus on our main sample (i.e., sample [e]) to examine the difference between sustainable emergence and nonsustainable emergence. By comparing samples (f) and (g), we find that the sustainable emergence sample has a significantly higher value for INC_OP_EFF (Diff. = 0.177, t value = 3.01) and a significantly lower value for EM (Diff. = −0.024, t value = −2.12), suggesting that sustainably emerged firms are more (less) likely to rely on operating improvement (earnings management) to remove the ST designation. We also find that sustainably emerged firms increase market share (INC_MK_SHR) and change board directors (CHG_BD) at a slightly higher frequency, although the differences are statistically insignificant. To show the dynamics of ST firms’ fixing the core and earnings management activities, in section 1.1 of the Online Supplemental Material, we provide statistics by year along the timeline of the ST setting.

PCA of Fixing-the-Core Actions

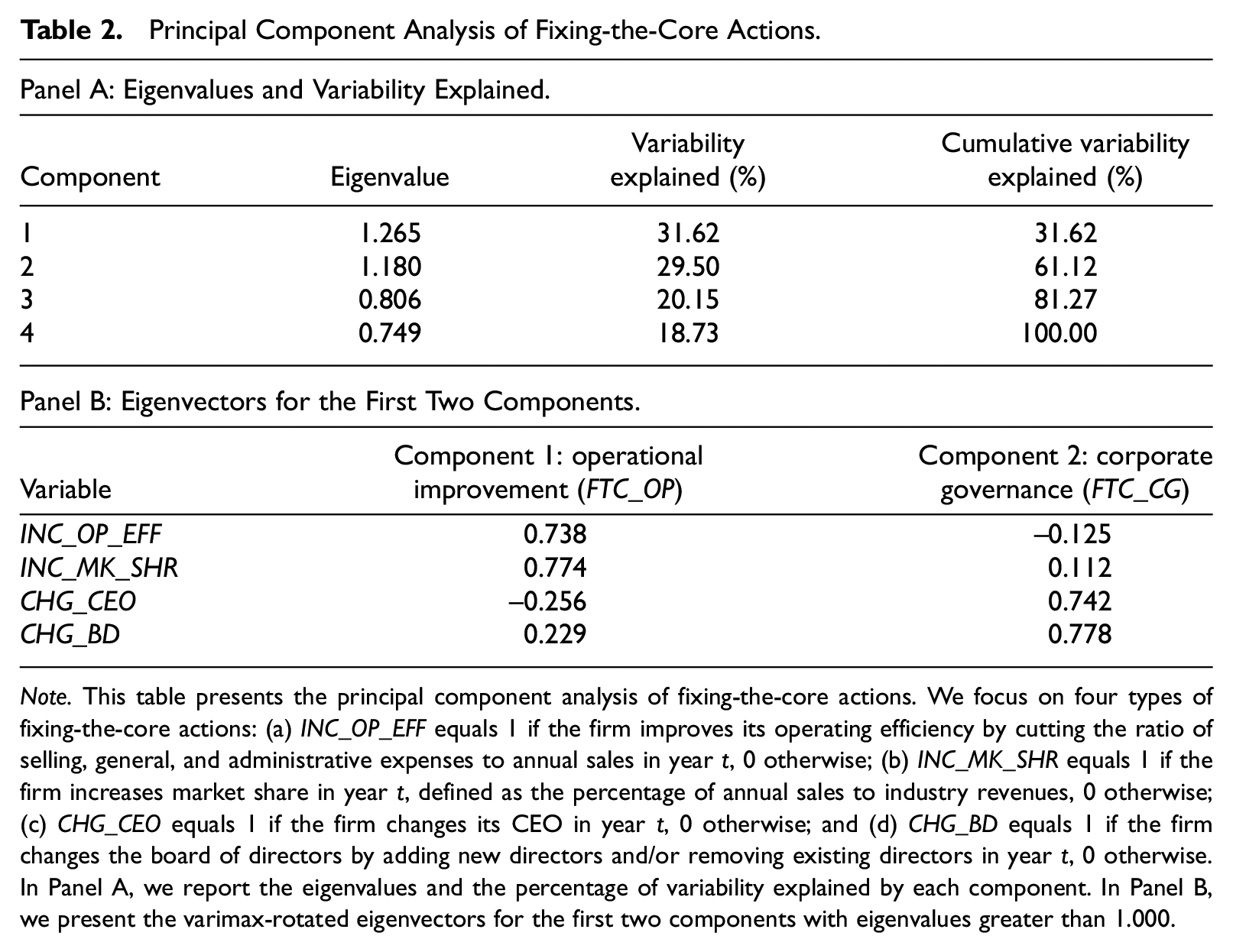

To ease the presentation and interpretation of the regression results, we apply a PCA to create a composite measure of fixing-the-core actions. By using a composite measure instead of multiple indicators for fixing-the-core actions in our regression analysis, we can also reduce any multicollinearity concern. In our final sample of 209 observations, we conduct a PCA on the four indicator variables for fixing-the-core actions (i.e., INC_OP_EFF, INC_MK_SHR, CHG_CEO, and CHG_BD), using SPSS CATPCA—Principal Components Analysis for Categorical Data. We present the results in Table 2. Panel A presents the eigenvalues of each component. The first (second) component has an eigenvalue of 1.265 (1.180) and explains 31.62% (29.50%) of the total variability. In our later analysis, we focus only on the first and second components because those two components both have an eigenvalue greater than 1.000, which is the rule-of-thumb cutoff in PCA (Jeffers, 1967).

Principal Component Analysis of Fixing-the-Core Actions.

Note. This table presents the principal component analysis of fixing-the-core actions. We focus on four types of fixing-the-core actions: (a) INC_OP_EFF equals 1 if the firm improves its operating efficiency by cutting the ratio of selling, general, and administrative expenses to annual sales in year t, 0 otherwise; (b) INC_MK_SHR equals 1 if the firm increases market share in year t, defined as the percentage of annual sales to industry revenues, 0 otherwise; (c) CHG_CEO equals 1 if the firm changes its CEO in year t, 0 otherwise; and (d) CHG_BD equals 1 if the firm changes the board of directors by adding new directors and/or removing existing directors in year t, 0 otherwise. In Panel A, we report the eigenvalues and the percentage of variability explained by each component. In Panel B, we present the varimax-rotated eigenvectors for the first two components with eigenvalues greater than 1.000.

In Panel B, we present the varimax-rotated eigenvectors for these two components. We find that while the improvement in operating efficiency (INC_OP_EFF) and the increase in market share (INC_MK_SHR) have high loadings on the first component, the change of CEO (CHG_CEO) and the change of board directors (CHG_BD) have high loadings on the second component. These results suggest that the first component essentially captures the operating improvement and the second component essentially captures the improvement in corporate governance. The loadings for CHG_CEO and CHG_BD (INC_OP_EFF and INC_MK_SHR) on the first (second) component are all below 0.3, a benchmark for a reasonable association between these variables and the underlying construct. Therefore, to construct our primary measure of fixing the core, we follow Bratten et al.’s (2019) approach of estimating component scores to reduce noise by considering only variables with loadings greater than 0.3. Specifically, to derive component scores of the first component, labeled FTC_OP, we perform PCA again using only INC_OP_EFF and INC_MK_SHR. We also perform a PCA on CHG_CEO and CHG_BD to estimate component scores of the second component, labeled as FTC_CG.

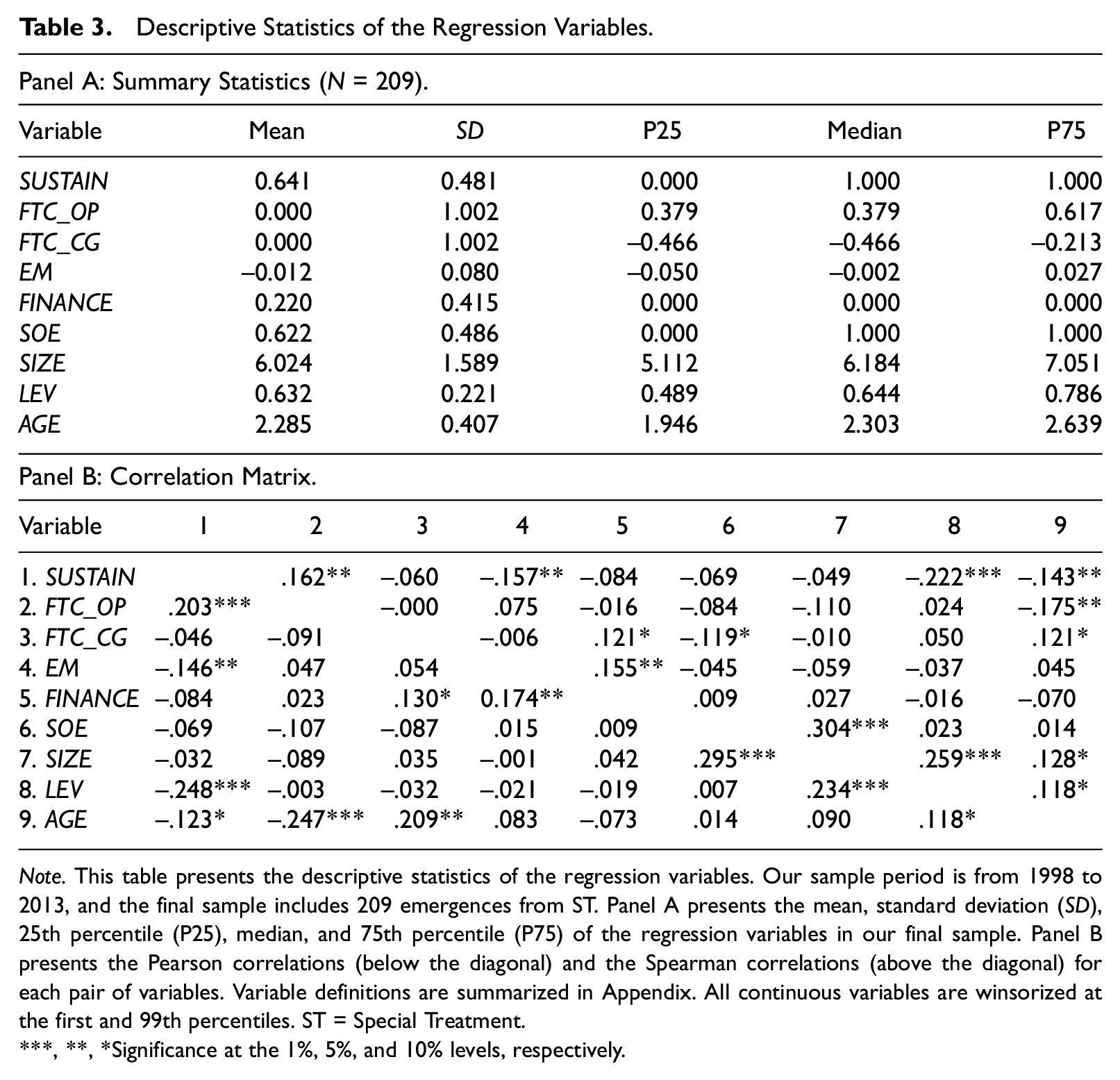

Descriptive Statistics of the Regression Variables

Table 3, Panel A presents the descriptive statistics for the regression variables. Of the 209 observations in our final sample, 134 (64%) are grouped as sustainable emergence (i.e., SUSTAIN = 1, defined earlier), while the other 75 (36%) are classified as nonsustainable emergence (SUSTAIN = 0). This split is similar to Hotchkiss’ (1995) finding that about one third of distressed firms fall back into distress. The first and second principal components of fixing the core (FTC_OP and FTC_CG) both have a mean value of 0 and a standard deviation of nearly 1.000. The mean and median values of the earnings management measure (EM) are close to 0 and its standard deviation is 0.080. We also note that 22% of our sample firms receive financial support in their emergence year and 62% of our sample firms are SOEs.

Descriptive Statistics of the Regression Variables.

Note. This table presents the descriptive statistics of the regression variables. Our sample period is from 1998 to 2013, and the final sample includes 209 emergences from ST. Panel A presents the mean, standard deviation (SD), 25th percentile (P25), median, and 75th percentile (P75) of the regression variables in our final sample. Panel B presents the Pearson correlations (below the diagonal) and the Spearman correlations (above the diagonal) for each pair of variables. Variable definitions are summarized in Appendix. All continuous variables are winsorized at the first and 99th percentiles. ST = Special Treatment.

, **, *Significance at the 1%, 5%, and 10% levels, respectively.

Table 3, Panel B reports the Pearson (Spearman) correlation coefficients below (above) the diagonal for the variables used in our main analyses. The correlation between SUSTAIN and FTC_OP is positive and statistically significant, which is consistent with our prediction that fixing the core of the business will help the firm emerge sustainably. The correlation coefficient between FTC_OP and FTC_CG is low and statistically insignificant because by construction, these two principal components are linearly uncorrelated with each other. We also note that earnings management (EM) and financial leverage (LEV) are negatively correlated with sustainable emergence. Multicollinearity is less of a problem in our later regression analysis as the largest correlation coefficient in the correlation matrix is only .304, that is, the Spearman correlation coefficient between SOE and firm size (SIZE). 11

Empirical Results

Tests of H1 and H2: Fixing the Core, Earnings Management, and Sustainable Emergence

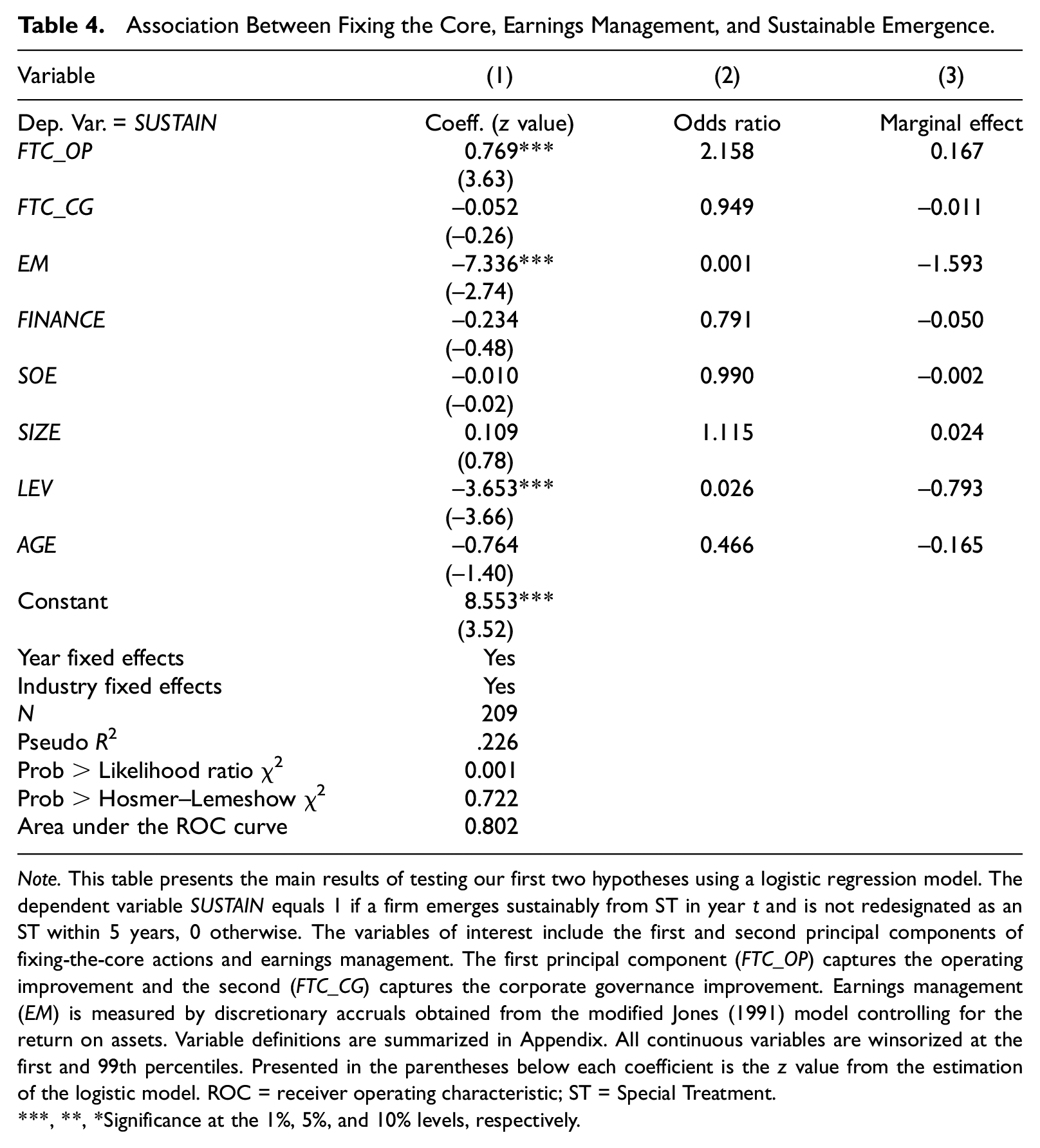

Table 4 presents the results of testing our first two hypotheses on whether and how fixing the core and earnings management are associated with sustainable emergence. Given the relatively small sample size, we start our discussion of the results by focusing on the logistic model as a whole. In terms of model fit, the pseudo R2 is .226 and the likelihood ratio χ2 test is significant at the 1% level (p = .001). We also employ Hosmer and Lemeshow’s commonly used test of goodness-of-fit, and the resultant p value of .722 indicates that our model fits the data well. 12 In terms of our prediction model’s discrimination ability, the area under the receiver operating characteristic (ROC) curve is 0.802. In summary, even though our analysis is based on a relatively small sample, our baseline logistic model has a moderate goodness-of-fit level and moderate predictive power.

Association Between Fixing the Core, Earnings Management, and Sustainable Emergence.

Note. This table presents the main results of testing our first two hypotheses using a logistic regression model. The dependent variable SUSTAIN equals 1 if a firm emerges sustainably from ST in year t and is not redesignated as an ST within 5 years, 0 otherwise. The variables of interest include the first and second principal components of fixing-the-core actions and earnings management. The first principal component (FTC_OP) captures the operating improvement and the second (FTC_CG) captures the corporate governance improvement. Earnings management (EM) is measured by discretionary accruals obtained from the modified Jones (1991) model controlling for the return on assets. Variable definitions are summarized in Appendix. All continuous variables are winsorized at the first and 99th percentiles. Presented in the parentheses below each coefficient is the z value from the estimation of the logistic model. ROC = receiver operating characteristic; ST = Special Treatment.

, **, *Significance at the 1%, 5%, and 10% levels, respectively.

In Table 4, Column (1), the coefficient on the first component of fixing-the-core actions, FTC_OP, is 0.769, which is statistically significant at the 1% level (z value = 3.63). Meanwhile, the coefficient on the second component of fixing-the-core actions, FTC_CG, is statistically insignificant. The coefficient on our earnings management measure (EM) is significantly negative (Coeff. = −7.336, z value = −2.74). Taken together, these results are consistent with our hypotheses. The significantly positive coefficient on FTC_OP suggests that fixing the core of the business is associated with a higher likelihood of sustainable emergence, while the significantly negative coefficient on EM indicates that emerging through upward earnings management eventually undermines the likelihood of long-term survival.

Because the magnitude of the coefficient in a logistic model cannot be directly interpreted, we also report the corresponding odds ratio and marginal effects in Columns (2) and (3), respectively. The odds ratio on FTC_OP is 2.158, which means that holding other prediction variables at a fixed value, the odds of achieving sustainable emergence would increase by 116% (= [2.158 − 1.000] × 1.002) if FTC_OP increases by one standard deviation (= 1.002). The results of marginal effects show that the probability of sustainable emergence increases by 16.7% (= 0.167 × 1.002) if a firm moves its FTC_OP value by one standard deviation from the sample mean. Given that the standard deviation of EM is 0.080, an increase by one standard deviation in EM is associated with a decrease of 8% (= [1 − 0.001] × 0.080) in the odds and a decrease of 12.74% (= 1.593 × 0.080) in the probability of sustainable emergence. Therefore, our main findings are not only statistically significant but also economically meaningful.

Regarding the control variables, the regression results are generally consistent with our expectations and the prior literature. For example, the significantly negative coefficient on financial leverage (LEV) suggests that firms with higher financial leverage are less likely to emerge sustainably. We also find a positive coefficient on firm size (SIZE), although it is statistically insignificant.

In the Online Supplemental Material, we show that our results are robust to (a) alternative measures of fixing the core (section 2.1); (b) alternative definitions of sustainable emergence (section 2.2); (c) alternative models, such as OLS and Probit models (section 2.3); and (d) multiperiod models on panel data (section 2.4).

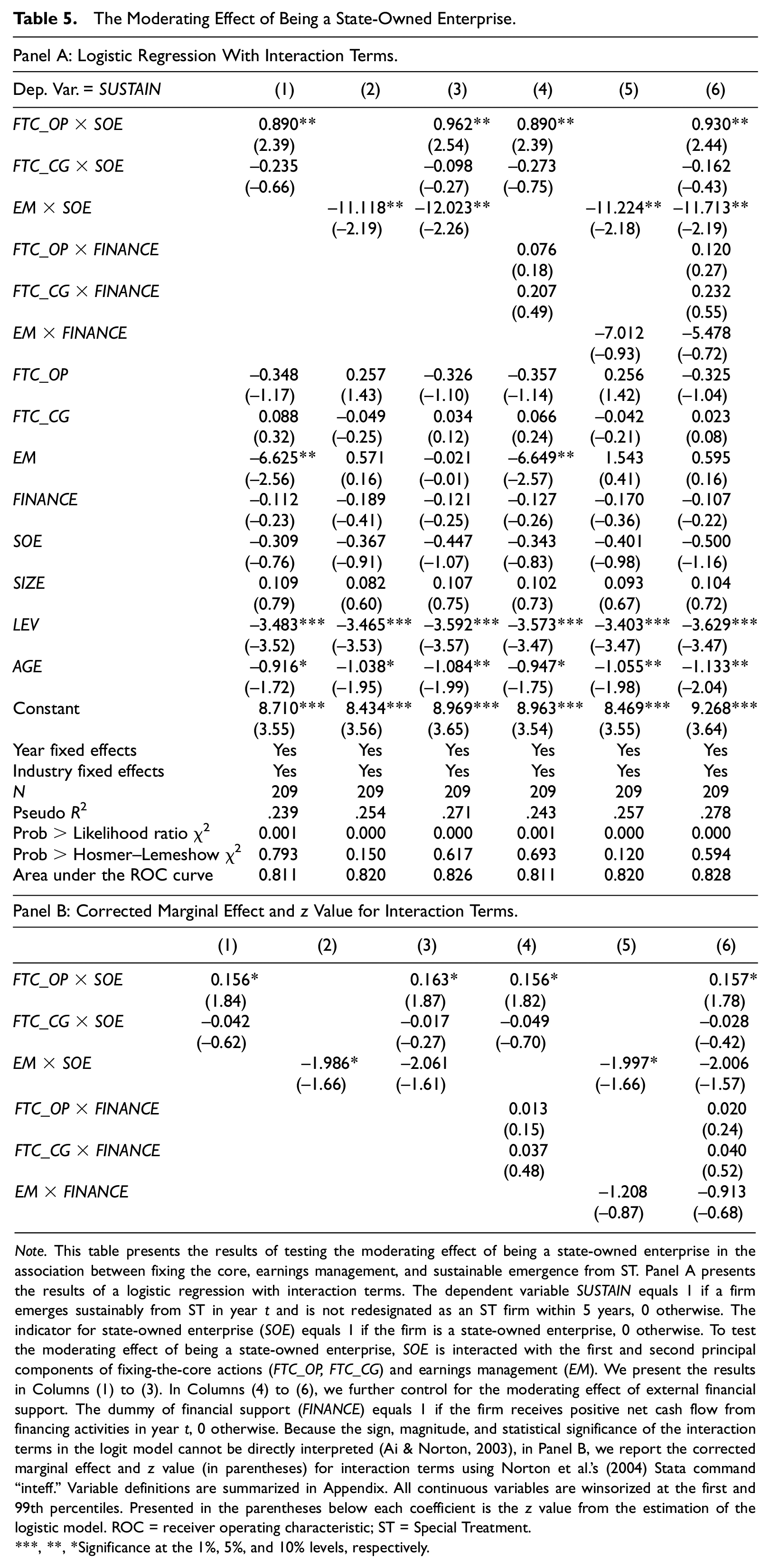

Test of H3: The Moderating Effect of Being an SOE

In this section, we examine how being an SOE moderates the relation between fixing the core, earnings management, and sustainable emergence. First, we focus on testing H3a in which we argue that support from the government facilitates firms fixing the core of their business. We expect the positive association between fixing the core and sustainable emergence to be greater for SOEs. To test this hypothesis, the dummy variable of SOE is interacted with the first and second principal components of fixing-the-core actions (FTC_OP, FTC_CG). We include these interaction terms in our baseline model to rerun the regression and focus on the coefficients on the interaction terms. Table 5, Panel A, Column (1) presents the regression results. Because the sign, magnitude, and statistical significance of the interaction terms in the logit model cannot be directly interpreted (Ai & Norton, 2003), in Panel B, we report the corrected marginal effects and z values for the interaction terms using Norton et al.’s (2004) Stata command “inteff.” Therefore, we rely on the results in Panel B as the basis of our inferences.

The Moderating Effect of Being a State-Owned Enterprise.

Note. This table presents the results of testing the moderating effect of being a state-owned enterprise in the association between fixing the core, earnings management, and sustainable emergence from ST. Panel A presents the results of a logistic regression with interaction terms. The dependent variable SUSTAIN equals 1 if a firm emerges sustainably from ST in year t and is not redesignated as an ST firm within 5 years, 0 otherwise. The indicator for state-owned enterprise (SOE) equals 1 if the firm is a state-owned enterprise, 0 otherwise. To test the moderating effect of being a state-owned enterprise, SOE is interacted with the first and second principal components of fixing-the-core actions (FTC_OP, FTC_CG) and earnings management (EM). We present the results in Columns (1) to (3). In Columns (4) to (6), we further control for the moderating effect of external financial support. The dummy of financial support (FINANCE) equals 1 if the firm receives positive net cash flow from financing activities in year t, 0 otherwise. Because the sign, magnitude, and statistical significance of the interaction terms in the logit model cannot be directly interpreted (Ai & Norton, 2003), in Panel B, we report the corrected marginal effect and z value (in parentheses) for interaction terms using Norton et al.’s (2004) Stata command “inteff.” Variable definitions are summarized in Appendix. All continuous variables are winsorized at the first and 99th percentiles. Presented in the parentheses below each coefficient is the z value from the estimation of the logistic model. ROC = receiver operating characteristic; ST = Special Treatment.

, **, *Significance at the 1%, 5%, and 10% levels, respectively.

Consistent with our prediction, in Panel B Column (1), we find that the interaction effect between FTC_OP and SOE is significant at the 10% level (z value = 1.84). In terms of economic significance, the corrected marginal effect on the interaction term FTC_OP

Next, we test H3b in which we argue that due to SOEs’ significant incentives and opportunities for earnings management, any abnormal positive earnings they report, compared with non-SOEs, are more likely to be due to earnings management. Hence, we predict that the negative association between earnings management and sustainable emergence is greater for SOEs. To test this hypothesis, earnings management (EM) is interacted with the dummy variable of SOE and we focus on this interaction term in Column (2) of Table 5 Panels A and B. Consistent with our hypothesis, we find that the interaction effect between EM and SOE is significant at the 10% level (z value = −1.66). In terms of economic magnitude, the corrected marginal effect on the interaction term EM × SOE is −1.986. That is, if EM increases by one standard deviation (= 0.080), the probability of an SOE’s sustainable emergence is 15.89% (= 1.986 × 0.080) lower than that of a non-SOE. The main effect of EM becomes insignificant in Column (2), suggesting that the negative effect of earnings management concentrates in SOEs.

In Table 5 Columns (3) to (6), we present additional results to provide further insights. In Column (3), we include all the interaction terms between SOE and fixing-the-core actions (FTC_OP, FTC_CG) and earnings management (EM). Results from Column (3) are generally consistent with the first two columns. In Columns (4) to (6), we further control for the moderating effect of financial support from various stakeholders. 14 The dummy for financial support (FINANCE) equals 1 if the firm receives positive net cash flow from financing activities in year t, 0 otherwise. That is, we control for the interaction terms between FINANCE and the first and second principal components of fixing-the-core actions (FTC_OP, FTC_CG) as well as for earnings management (EM). Again, we continue to find that the positive (negative) relation between fixing-the-core actions (earnings management) and sustainable emergence is pronounced only for SOEs. We also find positive (negative) coefficients on the interaction terms between FINANCE and fixing-the-core actions (earnings management). These regression coefficients have the expected signs, but they are not statistically significant at the conventional significance levels. These results highlight the inherent distinctiveness of being an SOE and simply receiving explicit financial support: In addition to funding support, SOEs enjoy other forms of benefits such as positive signaling and business connections (Sun et al., 2002).

Additional Analyses

In the Online Supplemental Material, we conduct several additional analyses. In section 4.1, we explore the complementary/substitution effects between fixing the core and earnings management and we find no supporting evidence. In section 4.2, we examine alternative outcomes of fixing the core and earnings management. We find supporting evidence that fixing the core benefits firms’ ongoing operation and future performance, while earnings management harms firm value. In section 4.3, we examine whether firms experiencing a 1-year loss would take similar actions to avoid the ST designation in the first place. We find that both fixing the core and earnings management are positively associated with the likelihood of avoiding ST.

Conclusion

What enables a distressed firm to emerge sustainably is an important question. In this article, we consider two key actions that firms can take when trying to emerge from distress, namely fixing the core and earnings management. We find that the more effort put into fixing the core to improve operating efficiency prior to emergence from ST, the higher the likelihood that the firm will emerge sustainably. In contrast, firms engaged in accruals-based upward earnings management have a lower probability of sustainable emergence, consistent with accruals reversal creating downward pressure on future earnings. We also find that the positive (negative) effects of fixing the core (earnings management) on sustainable emergence concentrate in SOEs, highlighting the important role of government support in the context of corporate turnaround.

Our study offers useful insights to both academics and practitioners about actions that affect a distressed firm’s long-term survival. Nevertheless, a few caveats need to be considered. First, our study is based on a small sample of distressed firms. As a result, the lack of statistical significance for some results might be due to a lack of statistical power rather than the absence of an economic effect. Second, our study uses a unique setting, the ST system in China. In this setting, firms have obvious incentives to engage in earnings management because of the clearly stipulated earnings-based guidelines for removing the ST designation. Hence, our results might not be generalizable to other countries. Finally, recent years have seen significant changes in China’s regulatory environment. As a result, the strategy that firms adopt to emerge from the ST system may have changed over time.

Supplemental Material

sj-docx-1-jaf-10.1177_0148558X211051169 – Supplemental material for Fixing the Core, Earnings Management, and Sustainable Emergence From Financial Distress: Evidence From China’s Special Treatment System

Supplemental material, sj-docx-1-jaf-10.1177_0148558X211051169 for Fixing the Core, Earnings Management, and Sustainable Emergence From Financial Distress: Evidence From China’s Special Treatment System by Jiao Jing, Kenneth Leung, Jeffrey Ng and Janus Jian Zhang in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

Variable Definitions.

| Variable | Definition |

|---|---|

| Fixing-the-core variables | |

| INC_OP_EFF | Equal to 1 if the firm improves its operating efficiency by cutting the ratio of selling, general, and administrative expenses to annual sales in year t, 0 otherwise. This is the first indicator of fixing the core. |

| INC_MK_SHR | Equal to 1 if the firm increases market share in year t, defined as the percentage of annual sales to industry revenues, 0 otherwise. This is the second indicator of fixing the core. |

| CHG_CEO | Equal to 1 if the firm changes its CEO in year t, 0 otherwise. This is the third indicator of fixing the core. |

| CHG_BD | Equal to 1 if the firm changes the board of directors by adding new directors and/or removing existing directors in year t, 0 otherwise. This is the fourth indicator of fixing the core. |

| Other variables | |

| SUSTAIN | Equal to 1 if a firm emerges sustainably from ST (due to two consecutive years’ losses) in year t and it is not redesignated as an ST within 5 years, 0 otherwise. |

| FTC_OP | The component scores generated from a principal component analysis (PCA) using only variables that have a reasonable association with the underlying construct of operating improvement. Specifically, we perform an initial PCA to estimate the underlying construct(s) among the four fixing-the-core actions. We identify two components with eigenvalues greater than 1. The first (second) component has the highest loadings for INC_OP_EFF and INC_MK_SHR (CHG_CEO and CHG_BD). To reduce noise, we follow Bratten et al. (2019) and perform PCA again to estimate the first component scores using only INC_OP_EFF and INC_MK_SHR. |

| FTC_CG | The component scores generated from a PCA using only variables that have a reasonable association with the underlying construct of corporate governance improvement. Specifically, we perform an initial PCA to estimate the underlying construct(s) among the four fixing-the-core actions. We identify two components with eigenvalues greater than 1. The first (second) component has the highest loadings for INC_OP_EFF and INC_MK_SHR (CHG_CEO and CHG_BD). To reduce noise, we follow Bratten et al. (2019) and perform PCA again to estimate the second component scores using only CHG_CEO and CHG_BD. |

| EM | Discretionary accruals obtained from the modified Jones (1991) model controlling for the return on assets, where the model estimation is a cross-sectional regression with observations in each industry-year of the Chinese stock market. |

| FINANCE | Equal to 1 if the firm’s net cash flow from financing activities is positive in year t, 0 otherwise. |

| SOE | Equal to 1 if the firm is a state-owned enterprise, 0 otherwise. |

| SIZE | Firm size, defined as the natural log of total sales in year t. |

| LEV | Leverage ratio in year t, defined as total liability divided by total assets. |

| AGE | Natural log of the number of years starting from the firm’s IPO year. |

ST = Special Treatment.

Acknowledgements

We thank Christophe Van Linden, Fatima Shuwaikh, Nancy Su, Qingmei Xue, Zili Zhuang, and participants of the 2017 Accounting Horizons Special Forum Conference, the 2019 Financial Market and Corporate Governance Conference, the 2019 Journal of International Accounting Research Conference, the 2019 Journal of Accounting, Auditing and Finance Conference, and seminar participants at the Hong Kong Polytechnic University for helpful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge financial support from the Hong Kong Polytechnic University, Hong Kong Baptist University, and Jinan University. Jiao Jing gratefully acknowledges financial support from the National Natural Science Foundation of China under Grant No. 72002081.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.