Research in corporate financial reporting identifies two important roles of accounting accruals. First, accruals smooth fluctuations in operating cash flows. Second, accruals allow recognition of losses in an asymmetric timely manner. While these two roles imply different relations between individual accrual components and operating cash flow news, prior research often focuses on the properties of aggregate accruals. We investigate the role of individual accrual components and identify asymmetry in the relation of investment with operating cash flow news as a confounding factor. We show that this investment factor operates through depreciation and amortization accruals, which typically account for the bulk of aggregate accruals. Overall, our article demonstrates the importance of adopting a granular approach to identifying the different roles of individual accrual components.

Accruals are a central feature of financial reporting. Separating accounting from the mere counting of cash, accruals align cash flows and the underlying economic activities generating the cash flows. Prior research distinguishes between two different roles of accruals. First, accruals smooth news about operating cash flows via offsetting variation in non-cash working capital items, such as inventories, accounts receivable, and accounts payable (e.g., Dechow, 1994). Second, accruals allow recognition of bad news about operating cash flows on a timelier basis than good news (e.g., Basu, 1997). In practice, the most fundamental manifestations of asymmetric timely loss recognition, or conditional conservatism, are lower-of-cost-or-market accounting for inventories (FASB: ASC 330), goodwill impairments (FASB: ASC 350), and long-term asset write-downs (FASB: ASC 360).

While smoothing and asymmetric timeliness imply different relations between individual accrual components and operating cash flow news, prior research often focuses on aggregate accruals measured as accounting earnings minus operating cash flows. For example, Ball and Shivakumar (2006) search for an asymmetric relation between aggregate accruals and operating cash flows to identify conditional conservatism. More recently, Bushman et al. (2016) search for a negative relation between aggregate accruals and operating cash flows to study how the smoothing role of accruals has evolved over time. The objective of our article is to develop and implement a granular approach to identifying the roles of individual accrual components.

We decompose aggregate accruals () as the sum of conditionally conservative accruals (), short-term accruals (), and depreciation and amortization accruals (). In this decomposition, measures the subset of accruals through which conditional conservatism is applied in practice. STACC measures short-term accruals excluding the current portion of conditionally conservative accruals such as inventory write-downs. The component measures depreciation and amortization accruals as reported on the statement of cash flows excluding the noncurrent portion of conditionally conservative accruals such as long-term asset write-downs. We then use this decomposition to identify the roles of individual accrual components.

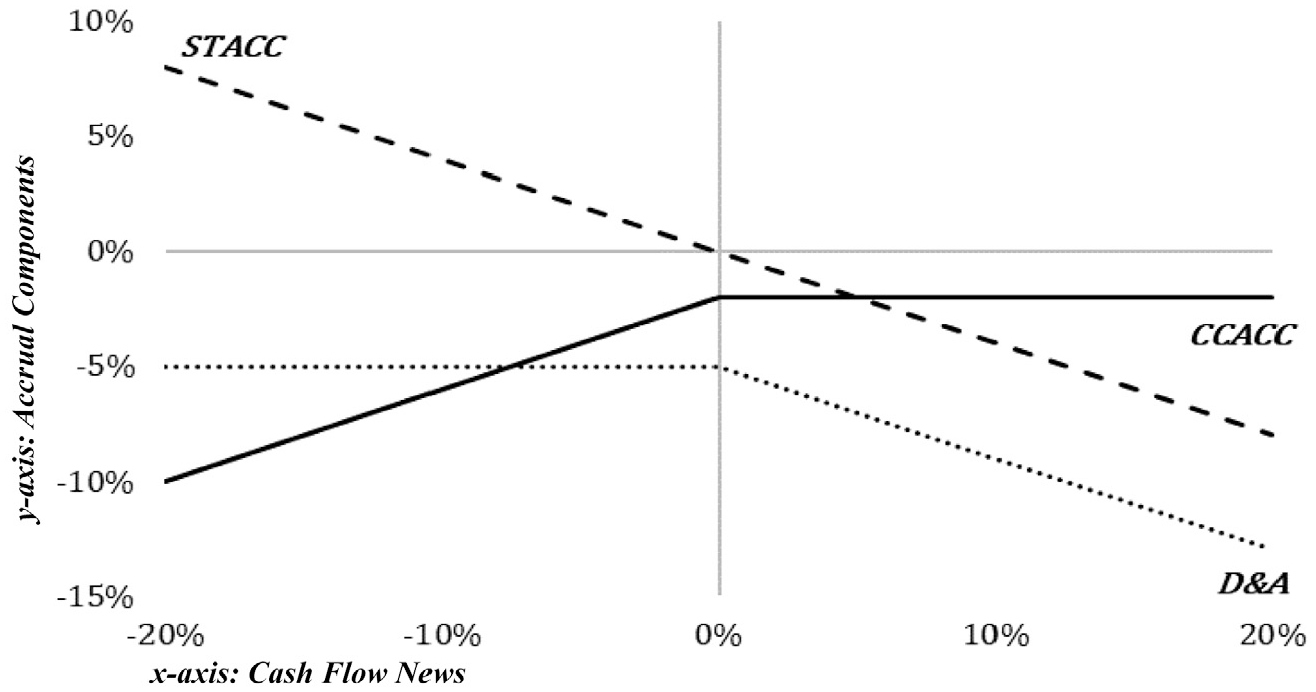

Figure 1 illustrates the predicted relations of the individual accrual components with operating cash flow news across good and bad news partitions. Under conditional conservatism, while firms are required to immediately recognize expected future losses as they become known, they recognize expected future gains only in the subsequent periods in which they are realized. Consequently, a key implication of conditional conservatism is asymmetry in the relation of with operating cash flow news. Specifically, we predict that while the component of aggregate accruals will be positively related to operating cash flow news when news is bad, it will be unrelated to operating cash flow news when news is good. Turning to the component of aggregate accruals, it is widely agreed that short-term accruals smooth fluctuations in operating cash flows to produce a less volatile measure of earnings (e.g., Dechow, 1994; Dechow et al., 1998). Smoothing implies that the component of aggregate accruals and operating cash flow news will be negatively and symmetrically related across good and bad news partitions.

Illustration of predicted relations.

With respect to the component of aggregate accruals, we expect an overall negative relation between accruals and operating cash flow news. Furthermore, we predict that the relation between accruals and operating cash flow news will be asymmetric across good and bad news. These predictions are based on three related observations. First, the relation between accruals and operating cash flow news is likely to mirror the relation between investing cash flows and operating cash flow news, since accruals reflect the intertemporal allocation of current and past capital expenditures. Second, a large number of corporate finance studies show that capital expenditures increase with internally generated funds. Third, we argue that capital expenditures should be more sensitive to operating cash flow news when news is good than when news is bad. The last argument follows from the idea of asymmetric adjustment costs; that is, the marginal adjustment cost is higher for capital stock decreases than for capital stock increases (e.g., Abel & Eberly, 1994, 1996; Arrow, 1968; Hall, 2001).1

We test our predictions for a sample of U.S. firms post-1989; the first year with comprehensive coverage of statement of cash flow data. We measure conditionally conservative accruals, , as negative special items. We measure short-term accruals, as the change in accounts receivable, plus the change in inventory, minus the change in accounts payable and accrued liabilities, minus the change in accrued income taxes, plus the net change in other current. We measure depreciation and amortization accruals, as reported on the statement of cash flows.

Our findings on the relation of with operating cash flow news are consistent with asymmetric timely loss recognition. The coefficient estimates from piecewise-linear regressions of on positive and negative operating cash flow news imply that the accounting system records cents of conditionally conservative accruals per dollar of bad news and effectively zero cents of such accruals per dollar of good news. Consistent with the smoothing role of short-term accruals, we find a negative and symmetric relation between and operating cash flow news. The coefficient estimates from linear regressions of on operating cash flow news imply that per dollar of operating cash flow news, the accounting system records cents of short-term accruals of the opposite sign. The piecewise-linear regression results show that the relation between and operating cash flow news is symmetric across good and bad news; the incremental sensitivity of to bad news is not significantly different from zero.

With respect to the relation of investing cash flows with operating cash flow news, our linear regression results are consistent with long-standing evidence in corporate finance that capital expenditures increase with internally generated funds. Consistent with our prediction, we find that the relation between capital expenditures and operating cash flow news is asymmetric across good and bad news partitions. Specifically, the piecewise-linear regression results show that firms invest nearly 33 cents per dollar of positive operating cash flow news and effectively zero cents per dollar of negative news. Although asymmetry in the relation of investing cash flows with operating cash flow news cannot be attributed to conditional conservatism, it is relevant for understanding asymmetry in aggregate accruals. This is because investment is linked to the accrual generating process through accruals, which typically account for the bulk of aggregate accruals.

Indeed, we find that the relation of accruals with operating cash flow news mirrors that of investing cash flows. Starting with the linear regression results, we find an overall negative relation between accruals and operating cash flow news. Importantly, our piecewise-linear regression results show that the conditional relations of accruals with operating cash flow news are asymmetric across news partitions. The good news coefficient is , which implies that accruals increase in absolute magnitude with operating cash flow news when news is good, and the incremental bad news coefficient is , which implies that accruals are relatively insensitive to operating cash flow news when news is bad. We stress that this evidence of asymmetry in accruals cannot be attributed to asymmetric timely loss recognition. In fact, as illustrated in Figure 1, the relation of accruals with operating cash flow news is opposite of what one would expect if accruals were subject to conditional conservatism. If accruals were subject to asymmetric timely loss recognition, one would expect a positive relation between accruals and operating cash flow news for bad news, and no association for good news. In contrast, our results show that the relation between accruals and operating cash flow news is flat for bad news and negative for good news.2

The above findings highlight a major pitfall in inferring conditional conservatism from the properties of aggregate accruals. Starting with Ball and Shivakumar (2006), a number of studies document that the piecewise-linear regression of aggregate accruals on operating cash flows yields a positive incremental coefficient on bad news. This incremental bad news coefficient, also known as the asymmetric timeliness (AT) coefficient, is typically attributed to conditional conservatism. Consistent with prior research, we find that the AT coefficient from the piecewise-linear regression of aggregate accruals on operating cash flow news is . Different from prior research, however, we argue that the AT coefficient for aggregate accruals is an upwardly biased measure of the degree of conditional conservatism because it commingles asymmetry in , which is indeed attributable to conditional conservatism, with asymmetry in accruals, which is unrelated to conditional conservatism. In fact, we find that asymmetry in accruals accounts for nearly of evidence of asymmetric timeliness in aggregate accruals.

Similarly, a number of prior studies (e.g., Bushman et al., 2016) have used the estimated negative slope coefficient from the linear regression of aggregate accruals on operating cash flows as a measure of smoothing. We argue that such an approach to infer smoothing is generally biased, since its reliance on aggregate accruals comingles properties of different components of accruals. In particular, the slope coefficient from the linear regression of aggregate accruals on operating cash flow news commingles the negative relation of with operating cash flow news, which is indeed related to the smoothing role of short-term accruals, with two opposing effects that are unrelated to smoothing. The first effect is the overall positive relation between and operating cash flow news due to timely loss recognition. The second effect is the overall negative relation between accruals and operating cash flow news. While these two forces will tend to offset each other, there is no reason to expect that they will do so perfectly in empirical settings.

Overall, our article underscores the importance of adopting a granular approach for identifying the different roles of individual accrual components. This granular approach has broad implications for research on time-series and cross-sectional variation in the different roles of accruals. Admittedly, our empirical measures of accrual components are subject to measurement error. For example, we measure conditionally conservative accruals as negative special items. Special items include not only short-term and long-term accruals through which asymmetric timely loss recognition is applied in practice, but also other unusual and nonrecurring items. It is also possible that our measure of short-term accruals includes some conditionally conservative accruals. Notwithstanding these measurement challenges, our granular approach of zeroing in on individual accrual components offers a substantial improvement over the standard practice of using aggregate accruals when identifying the different roles of accruals.

This article proceeds as follows. Section “Framework and Predictions” lays out a framework to decompose aggregate accruals and develops our empirical predictions on the relations of individual accrual components and operating cash flow news. Section “Empirical results” describes the data and presents our empirical results. Section “Conclusion” concludes.

Framework and Predictions

Decomposition of Aggregate Accruals

We define aggregate accruals () from the statement of cash flows as earnings minus operating cash flows . That is,

Variants of this aggregate accruals measure have been widely used in research on smoothing and asymmetric timeliness. By virtue of accounting identities, aggregate accruals can be written as follows:

In the above equation, denotes conditionally conservative accruals through which asymmetric timely loss recognition is applied in practice; that is, inventory write-downs, long-term asset impairments, and goodwill impairments. denotes short-term operating accruals excluding the current portion of conditionally conservative accruals, such as inventory write-downs. denotes depreciation and amortization accruals excluding the long-term portion of conditionally conservative accruals, such as goodwill impairments and long-term asset write-downs. We provide a formal derivation of Equation 1 in the Online Supplement (Appendix 1).3

The smoothing and asymmetric timeliness (AT) roles of accruals imply different relations between individual accrual components and operating cash flow news. However, research on the roles of accruals typically focuses on the relation between aggregate accruals and operating cash flow news. We argue that the focus on aggregate accruals can lead to biased estimates of both smoothing and asymmetric timeliness.

Relation of Conditionally Conservative Accruals With Cash Flow News

Before considering the AT role of accruals, it is instructive to examine how accruals would vary with cash flow news if both unrealized gains and losses were symmetrically recognized (e.g., fair value accounting). Under such symmetric accounting system, any favorable (unfavorable) change in expectations of future cash flows would be recorded as an unrealized gain (loss) in current period earnings. Given that current period cash flow news is positively related to changes in expectations of future cash flows, timely recognition of unrealized gains and losses would introduce a positive relation between accruals and cash flow news. Under conditional conservatism, expected future losses are immediately recognized as they become known, but expected future gains are recognized in the subsequent periods when they are realized. As current period cash flow news is positively related to changes in expectations of future cash flows, conditional conservatism would imply an overall positive relation between conditionally conservative accruals and cash flow news. In terms of the following linear regression model (we omit firm subscripts for simplicity),

timely loss recognition implies a positive slope coefficient .

Consider now a piecewise linear regression of on cash flow news:

where is an indicator variable for negative cash flow news. While the coefficient captures the sensitivity of to good news, the coefficient measures the incremental sensitivity of to bad news. Asymmetric timely loss recognition implies that conditionally conservative accruals do not vary with good news but are positively related to bad news. In Figure 1, this asymmetric relation is illustrated by the solid line that slopes upward for bad news and is flat for good news. We summarize this discussion as follows.

Prediction 1

Conditional conservatism in accrual accounting implies that

i. the coefficient from the linear model is positive (), and

ii. the good news coefficient from the piecewise-linear model is zero (), while the incremental bad news coefficient is positive ().

Relation of Short-Term Accruals With Cash Flow News

To understand the smoothing role of short-term accruals, suppose there is a negative shock to a firm’s current operating cash flows. Specifically, suppose one of the firm’s customers, who was expected to pay in the current period, is unable to do so until the next period. While current earnings would remain unaffected by such a negative shock, the firm would report a higher level of positive short-term accruals (i.e., accounts receivables) in the current period. On the other hand, if there was a positive shock to the firm’s current operating cash flows because the firm had to unexpectedly defer payment of certain salaries to the next period, the firm would have to record additional negative short-term accruals in the form of accrued wages. These examples illustrate that a key implication of the smoothing role of accrual accounting is that short-term accruals and operating cash flow news are negatively related. We therefore predict a negative slope coefficient in the following linear regression model:

Moreover, since our measure of short-term accruals excludes any asset write-downs, we predict a negative and symmetric relation between and operating cash flow news. To make this precise, consider the following piecewise linear regression of on :

where is an indicator variable for negative news. A symmetrically negative relation between short-term accruals and operating cash flow news implies that the good news slope coefficient is negative, while the incremental bad news slope coefficient is zero. In Figure 1, this symmetric relation between and operating cash flow news is illustrated by the dashed line that slopes downward across the bad and good news regions. We summarize this discussion as follows.

Prediction 2

Smoothing in accrual accounting implies that

i. the coefficient from the linear model is negative (), and

ii. the good news coefficient from the piecewise-linear model is negative (), while the incremental bad news coefficient is zero ().

Relation of Depreciation and Amortization Accruals With Cash Flow News

Dating back to Fazzari et al. (1988), a long line of research in corporate finance finds that capital expenditures increase with internally generated funds. Prior research offers two non-mutually exclusive explanations for the investment-cash flow sensitivity (e.g., Lewellen & Lewellen, 2016). First, internally generated funds may be cheaper than externally raised funds in the presence of financing constraints. Alternatively, more positive news about operating cash flows may simply proxy for more profitable investment opportunities. Regardless of whether the investment-cash flow sensitivity reflects financing frictions or investment opportunities, it is widely accepted that there is an overall positive relation between capital expenditures and operating cash flows.

Consider the following linear regression model:

where the dependent variable is either investing cash flows or accruals. Since higher capital expenditures imply more negative investing cash flows (), we predict an overall negative relation between and news about operating cash flows; that is, . And, since accruals reflect the intertemporal allocation of current and past capital expenditures, we predict that the relation of accruals with operating cash flow news parallels that of with operating cash flow news; that is, .

While prior research in corporate finance typically estimates a linear relation between investment and operating cash flows, we argue that investment is likely to be more sensitive to positive cash flow news and less sensitive to negative cash flow news. Our argument follows from the idea that the marginal adjustment cost for capital stock reductions is expected to be higher than for capital stock increases. The idea of asymmetric adjustment costs goes back to Arrow’s (1968) seminal work on investment irreversibility and subsequent work on costly investment reversibility due to transaction costs and the firm-specific nature of investments (e.g., Abel & Eberly, 1994, 1996; Hall, 2001).4 With asymmetric adjustment costs, we predict that investing cash flows and accruals are more sensitive to positive cash flow news and less sensitive to negative cash flow news.

To make these predictions precise, consider the following piecewise-linear regression model:

where is an indicator variable for negative operating cash flow news. The dependent variable is either investing cash flows or accruals. We predict that the relation of investing cash flows and accruals with operating cash flow news is negative when news is good; that is, and . We also predict that the relation of investing cash flows and accruals with operating cash flow news is less negative when news is bad, so that the incremental bad news coefficient is positive; that is, and . We summarize this discussion as follows:

i. the coefficient from the linear model is negative (), and

ii. the good news coefficient from the piecewise-linear model is negative (), while the incremental bad news coefficient is positive ().

We note that a positive incremental bad news coefficient in piecewise-linear regressions of the form in Equation is often interpreted as evidence of conditional conservatism in the dependent variable. In contrast, we argue that the incremental bad news coefficient in Equation 7 will be positive even though investing cash flows and accruals play no role in asymmetric timely loss recognition. In Figure 1, the asymmetric relation between accruals and operating cash flow news is illustrated as the dotted line that is flat in the bad news region and slopes downward in the good news region.

A comparison of asymmetry in accruals with asymmetry in the component of aggregate accruals highlights that even though both asymmetries imply a positive incremental bad news coefficient, the underlying conditional relations are completely opposite of each other. While the relation between accruals and operating cash flow news is flat for bad news and negative for good news, the relation between and operating cash flow news is positive for bad news and flat for good news. Put differently, even though the incremental bad news coefficient is positive for accruals, the underlying conditional relations are opposite from what is expected under conditional conservatism. This observation highlights a major pitfall in focusing exclusively on asymmetric coefficient estimates from piecewise-linear regressions without considering the underlying conditional relations.

Relation of Aggregate Accruals With Cash Flow News

In contrast to our granular approach, prior studies on smoothing and conditional conservatism have relied on aggregate accruals. Consider Ball and Shivakumar’s (2006) piecewise-linear regression model of aggregate accruals () on operating cash flow news:

where is an indicator variable for negative operating cash flow news. Conditional conservatism implies that accruals will be more sensitive to negative operating cash flow news so that the incremental bad news coefficient is positive; that is, . The coefficient, also known as asymmetric timeliness (AT) coefficient, is often used as a measure of the degree of conditional conservatism in accrual accounting. However, we argue that the coefficient is likely to be an upwardly biased measure of the degree of conditional conservatism because it commingles asymmetric timely loss recognition with asymmetry in D&A accruals.

From the decomposition of in Equation 1, it follows that can be written as the sum of the incremental bad news coefficients for the individual components,

While short-term accruals are expected to be symmetrically related to operating cash flow news; that is , D&A accruals are expected to vary with operating cash flow news in an asymmetric fashion; that is, . Given that accruals play no role in asymmetric timely loss recognition, asymmetry in the relation of with operating cash flow news is predicted to be a source of upward bias in AT estimates from model ; that is,

The good news coefficient in model can be written as the sum of the good news coefficients for the individual components,

While conditionally conservative accruals are expected to be unrelated to positive cash flow news; that is , accruals are expected to be negatively related to positive cash flow news; that is . Given that accruals play no role in smoothing fluctuations in operating cash flows, the good news coefficient for aggregate accruals is an overstated measure of smoothing; that is,

Consider next Bushman et al. (2016), who estimate variations of the following linear regression model to examine the smoothing role of accruals:

Bushman et al. (2016) predict a negative slope coefficient on operating cash flow news, that is, , and interpret the estimated coefficient as a measure of smoothing. However, we argue that is likely to be a biased measure of smoothing; that is,

To see this, note that Since and operating cash flow news are expected to be positively related; that is, , the estimated value of will be less negative due to the presence of in aggregate accruals. On the other hand, accruals and operating cash flow news are expected to be negatively related; that is, , which implies that the estimated value of will be more negative due to the presence of in aggregate accruals. While it is possible that these two forces offset each other, this is unlikely to be true in all empirical settings.

Empirical Results

Sample Construction and Variable Definitions

Following the framework developed in section “Framework and predictions,” we express aggregate accruals () as the sum of conditionally conservative accruals (), short-term accruals (), depreciation and amortization accruals (), and other accruals ().

We measure as negative special items. Special items include short-term and long-term accruals through which conditional conservatism is applied in practice, such as inventory write-downs, goodwill impairments, and long-term asset write-downs, along with other unusual and nonrecurring items. We set nonnegative values of special items to zero because conditionally conservative accruals can be either zero or negative. To ensure consistency with the measurement of operating cash flows from continuing operations, we adjust special items for extraordinary items and discontinued operations .5

We measure from the statement of cash flows as the change in accounts receivable, plus the change in inventory, minus the change in accounts payable and accrued liabilities, minus the change in accrued income taxes, plus the net change in other current assets . Our measure of excludes the current portion of conditionally conservative accruals (e.g., inventory write-downs). This is because Compustat reclassifies special items under funds from operations-other () on the statement of cash flows.

We measure as reported on the statement of cash flows (). accruals represent non-cash charges for obsolescence and wear-and-tear on property, allocation of the current portion of capitalized expenditures, and depletion charges, and exclude long-term asset write-downs. By definition, when bad news trigger the recognition of long-term asset write-downs, such write-downs will flow through the component rather than the component of aggregate accruals. We measure from the statement of cash flows as the sum of deferred income tax expense, plus equity in net loss/earnings, plus the sale of PP&E and investments gain/loss.6

We measure investing cash flows () from the statement of cash flows as net cash flows from investing activities. By definition, represents net cash received or paid for all transactions classified as investing activities on the statement of cash flows. We measure operating cash flows from continuing operations () as net cash flows from operating activities minus the cash portion of extraordinary items and discontinued operations.

Our empirical measures of accrual components are admittedly subject to measurement error. For example, our measure is unlikely to capture all write-downs (e.g., Johnson et al., 2011). Due to measurement error in , our measure of is unlikely to be completely free from conditionally conservative accruals. While there is no perfect way to deal with measurement error, our granular approach of zeroing in on individual accrual components offers a substantial improvement over simply using aggregate accruals when identifying the roles of accruals in corporate financial reporting.

We measure news about operating cash flows () as the regression residuals from a first-order autoregressive model of estimated by industry and year . Following Ball and Shivakumar (2006), we define industries using two-digit SIC codes and require a minimum of ten observations for each industry-year. We observe that is mostly auto-correlated at one-year lag. Therefore, our results are not sensitive when we expand the prediction model to include higher-order lags of .7

We note that Ball and Shivakumar (2006) consider the year-over-year change and the industry-adjusted level of as alternative measures of cash flow news. When compared to the year-over-year change in operating cash flows, we argue that offers a more realistic measure of news because does not follow a random walk. Whereas a random-walk process would imply a persistence coefficient of one, the persistence coefficient of in our sample is in fact . When compared to the industry-adjusted level of operating cash flows, we argue that offers a more comprehensive measure of news. This is because industry-adjusted disregards gains and losses from industry-wide shocks, while incorporates industry-wide shocks as news. Ball and Shivakumar (2006) also consider stock returns as another measure of economic news. However, stock returns are right skewed and subject to confounding sources of cross-sectional variation (e.g., Dutta & Patatoukas, 2017).8

We obtain accounting data for U.S. non-financial firms from Compustat (Fundamentals Annual). We scale the accounting data by the beginning-of-year total assets. To mitigate small-scale effects, we exclude observations with beginning-of-year total assets below MN. To mitigate the effect of outliers, we trim observations in the top and bottom one percentile of each annual cross-section for each variable. Following Ball and Shivakumar (2006), we exclude firm-year observations in which acquisitions occurred because business combinations are a key source of accruals that do not articulate across the balance sheet and the statement of cash flows (e.g., Hribar & Collins, 2002).

Our sample includes 85,654 firm-year observations from 1989 to 2017. Our sample starts in 1989 because this is the first year with comprehensive coverage of statement of cash flow data after the promulgation of SFAS No. 95. Our sample ends in 2017 because this is the most recent year with available data from Compustat. Online Supplement Appendix 2 provides the variable definitions along with the corresponding Compustat data item mnemonics.

Descriptive Statistics

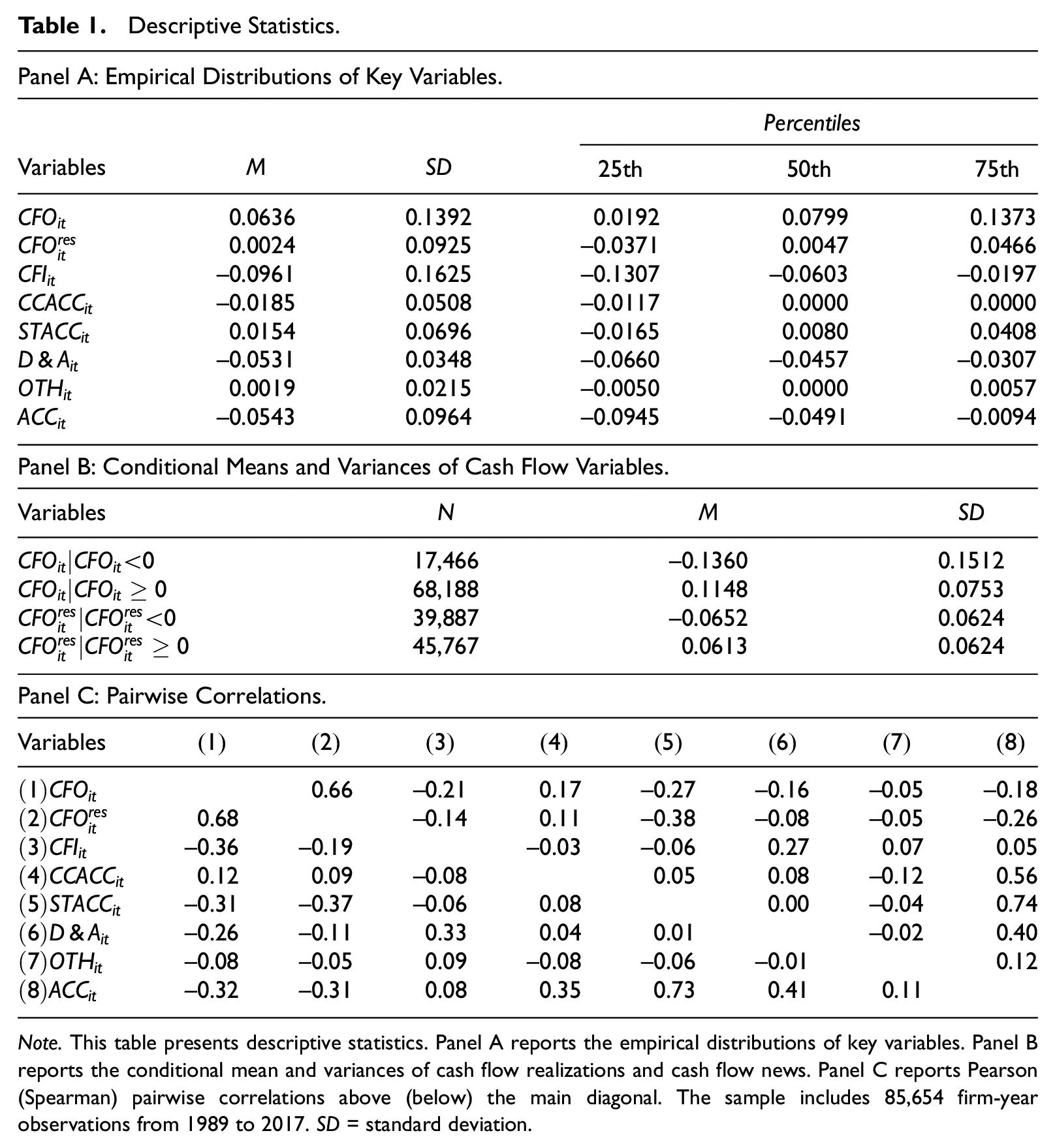

Table 1, Panel A, reports the distributions of key variables. We express all variables as a percentage of the beginning-of-year total assets. For the average firm, operating cash flow is and investing cash flow is . Turning to the individual accrual components for the average firm, conditionally conservative accruals () is , short-term accruals () is , depreciation and amortization accruals () is , other accruals is , and aggregate accruals () is . Clearly, for the average firm accruals account for the bulk of aggregate accruals.

Descriptive Statistics.

Panel A: Empirical Distributions of Key Variables.

Variables

0.0636

0.1392

0.0192

0.0799

0.1373

0.0024

0.0925

−0.0371

0.0047

0.0466

−0.0961

0.1625

−0.1307

−0.0603

−0.0197

−0.0185

0.0508

−0.0117

0.0000

0.0000

0.0154

0.0696

−0.0165

0.0080

0.0408

−0.0531

0.0348

−0.0660

−0.0457

−0.0307

0.0019

0.0215

−0.0050

0.0000

0.0057

−0.0543

0.0964

−0.0945

−0.0491

−0.0094

Panel B: Conditional Means and Variances of Cash Flow Variables.

Variables

17,466

−0.1360

0.1512

68,188

0.1148

0.0753

39,887

−0.0652

0.0624

45,767

0.0613

0.0624

Panel C: Pairwise Correlations.

Variables

0.66

−0.21

0.17

−0.27

−0.16

−0.05

−0.18

0.68

−0.14

0.11

−0.38

−0.08

−0.05

−0.26

−0.36

−0.19

−0.03

−0.06

0.27

0.07

0.05

0.12

0.09

−0.08

0.05

0.08

−0.12

0.56

−0.31

−0.37

−0.06

0.08

0.00

−0.04

0.74

−0.26

−0.11

0.33

0.04

0.01

−0.02

0.40

−0.08

−0.05

0.09

−0.08

−0.06

−0.01

0.12

−0.32

−0.31

0.08

0.35

0.73

0.41

0.11

Note. This table presents descriptive statistics. Panel A reports the empirical distributions of key variables. Panel B reports the conditional mean and variances of cash flow realizations and cash flow news. Panel C reports Pearson (Spearman) pairwise correlations above (below) the main diagonal. The sample includes 85,654 firm-year observations from 1989 to 2017. SD = standard deviation.

Table 1, Panel B, reports the conditional means and variances of cash flow realizations () and cash flow news (). While the distribution of is asymmetric around zero with the standard deviation of losses being more than twice as large as the standard deviation of gains, the distribution of is symmetric around zero with the standard deviation of bad news being comparable to the standard deviation of good news. By virtue of OLS regression properties, the incremental coefficient on negative values of from a piecewise-linear regression of on will be affected by the spread in the conditional variances of positive and negative values of .9 It follows that asymmetry in the distribution of cash flow realizations introduces a confounding source of asymmetry. Symmetry in the conditional variances of cash flow news is, thus, a desirable property when searching for smoothing and asymmetric timeliness in the relation of accruals with cash flow news across good/bad news partitions.

Turning to the pairwise correlations, Table 1, Panel C, reports a positive correlation between and , which is consistent with timely loss recognition, and a negative correlation between and , which is consistent with smoothing in accrual accounting. The negative correlation between and is consistent with long-standing evidence in corporate finance of a positive link between corporate investment and internally generated funds. The positive correlation between and is consistent with prior evidence that higher corporate investment is associated with more negative accruals (e.g., Lewellen & Resutek, 2016). The negative correlation between and is consistent with prior evidence on the relation of aggregate accruals with alternative measures of cash flow news (e.g., Ball & Shivakumar, 2006).10

Relation of Conditionally Conservative Accruals With Cash Flow News

First, we examine the relation of conditionally conservative accruals () with operating cash flow news (). We estimate the model specifications using pooled cross-sectional OLS regressions. The models include industry fixed effects based on two-digit SIC codes and year fixed effects to control for industry-specific and aggregate time-varying factors. We base statistical inferences on standard errors clustered by firm and year to address time-series and cross-sectional residual dependence.

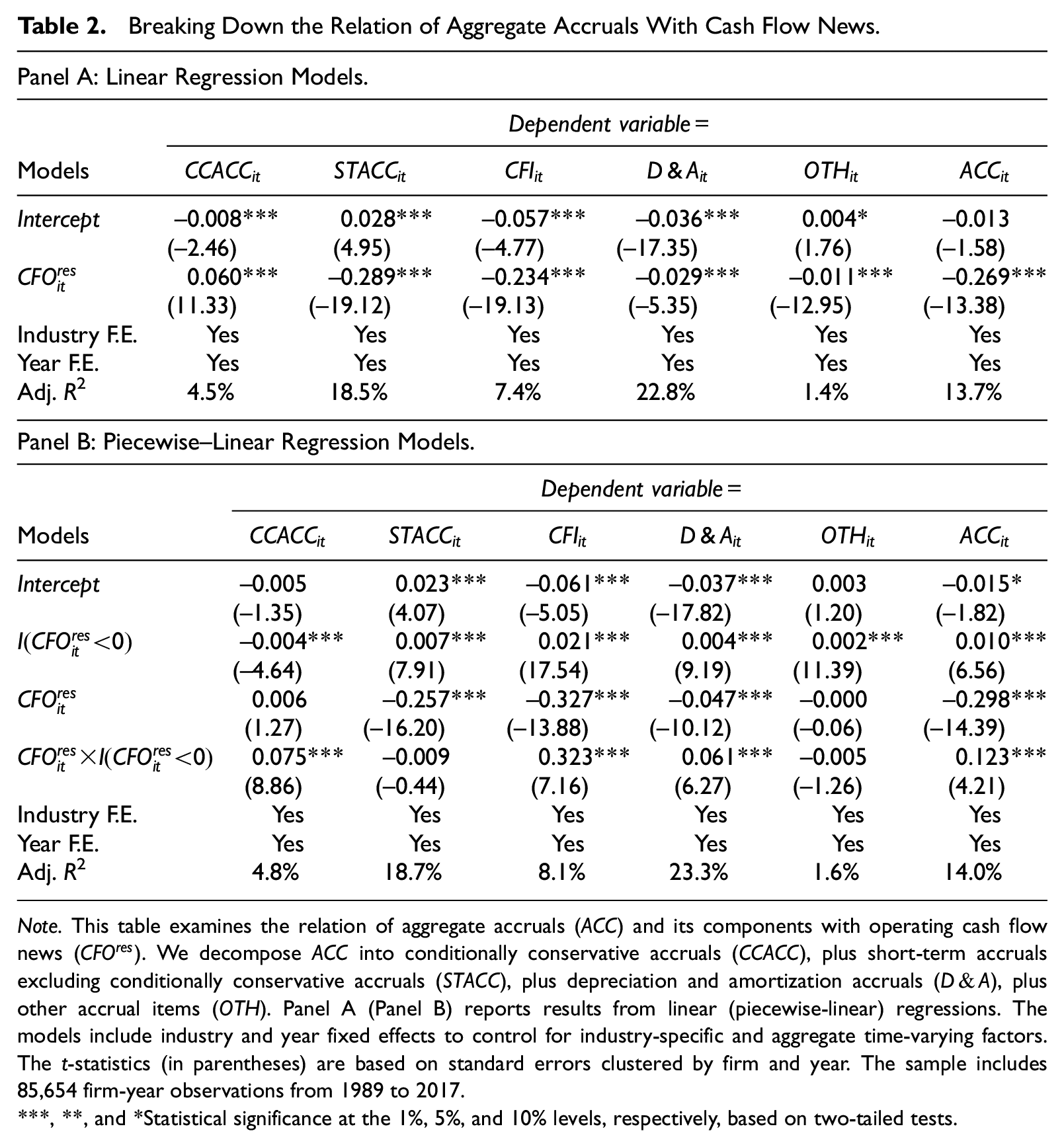

Column 1 of Table 2 reports regression results based on linear and piecewise-linear models of on . The results are consistent with Prediction 1. Starting with the linear regression results, we obtain a significantly positive slope coefficient on , which is consistent with an overall positive association between and operating cash flow news. Turning to the piecewise-linear regression results, we find evidence consistent with two key implications of asymmetric timeliness. First, the coefficient on positive operating cash flow news is indistinguishable from zero, which implies that is unrelated to good news. Second, the incremental coefficient on negative cash flow news is significantly positive, which implies that is asymmetrically related to bad news. In combination, the piecewise-linear slope coefficients imply that the accounting system records cents of conditionally conservative accruals per dollar of negative cash flow news, and effectively zero cents of such accruals per dollar of positive cash flow news. With respect to the good news coefficient for , the confidence interval around the point estimate of is to . It follows that at a high level of confidence the good news coefficient is reliably small.

Breaking Down the Relation of Aggregate Accruals With Cash Flow News.

Note. This table examines the relation of aggregate accruals () and its components with operating cash flow news (). We decompose into conditionally conservative accruals (), plus short-term accruals excluding conditionally conservative accruals (), plus depreciation and amortization accruals (), plus other accrual items (). Panel A (Panel B) reports results from linear (piecewise-linear) regressions. The models include industry and year fixed effects to control for industry-specific and aggregate time-varying factors. The t-statistics (in parentheses) are based on standard errors clustered by firm and year. The sample includes 85,654 firm-year observations from 1989 to 2017.

, **, and *Statistical significance at the 1%, 5%, and 10% levels, respectively, based on two-tailed tests.

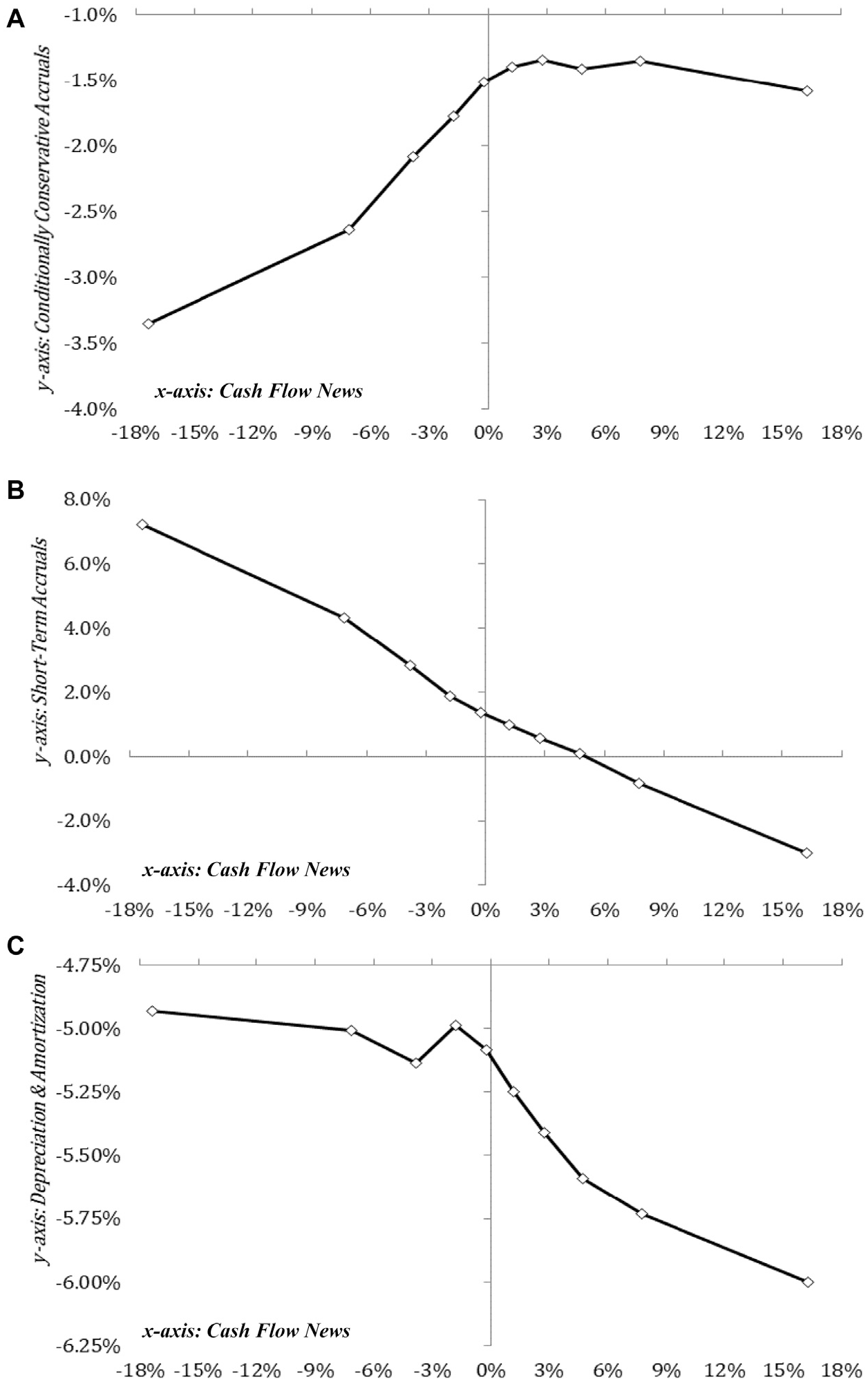

Figure 2, Panel A, presents the plot of on across decile portfolios formed annually based on . The portfolio analysis yields evidence consistent with the regression analysis. Focusing on the good news portfolios, the relation of with is relatively flat, which is consistent with the zero good news coefficient estimate. Turning to the bad news portfolios, the relation of with is positive, which indicates that firms with more negative cash flow news report more negative conditionally conservative accruals. Given the difference in the conditional relations of with across news partitions, it follows that the incremental slope on negative news is positive, which is consistent with the significantly positive AT regression coefficient estimate. The figure also shows that the “kink” in the relation of with is located at zero cash flow news, which is consistent with proper model specification for the piecewise-linear regression of on .

Relation of accrual components with cash flow news. Panel (A) relation of conditionally conservative accruals with cash flow news. Panel (B) relation of short-term accruals with cash flow news. Panel (C) relation of depreciation and amortization accruals with cash flow news.

As an additional test, we search for asymmetry in the relation of with cash flows news across randomized good news and bad news partitions. For each iteration, we randomly assign half of our sample as good news and the other half as bad news. We then search for asymmetry in the relation of conditionally conservative accruals with cash flow news across the randomized partitions. Construct validity would imply no evidence of asymmetry in the relation of conditionally conservative accruals with cash flow news across randomized partitions. Consistent with this notion of construct validity, we do not find evidence of asymmetry in the relation of with cash flow news across randomized news partitions. Across iterations, the mean value of the AT coefficient is with a standard deviation of .

Relation of Short-Term Accruals With Cash Flow News

Recall that we measure from the statement of cash flows as the change in accounts receivable, plus the change in inventory, minus the change in accounts payable and accrued liabilities, minus the change in accrued income taxes, plus the net change in other current assets. We note that excludes the current portion of conditionally conservative accruals (e.g., inventory write-downs) and allows us to zero in on the smoothing role of accrual accounting in alleviating fluctuations in operating cash flows. Column 2 of Table 2 reports regression results based on linear and piecewise-linear models of on cash flow news (). The results are consistent with Prediction 2.

Starting with the linear regression results, the significantly negative coefficient on is consistent with the role of short-term accruals in smoothing fluctuations in operating cash flows. The magnitude of the coefficient implies that per dollar of operating cash flow news, the accounting system records cents of short-term accruals of the opposite sign. As we explain in section “Framework and Predictions,” the smoothing role of short-term accruals implies a symmetrically negative relation between and cash flow news across good and bad news partitions. Consistent with this implication, the piecewise-linear regression results show that the overall negative association between and operating cash flow news is symmetrically negative for good and bad news. In fact, the incremental bad news coefficient is not significantly different from zero. With respect to the incremental bad news coefficient for , the confidence interval around the point estimate of is to . Thus, the good and bad news coefficients are not significantly different from each other at a high level of confidence.

Figure 2, Panel B, presents the plot of on across decile portfolios formed annually based on . The portfolio analysis yields evidence consistent with the regression analysis. It shows that firms with more positive news about operating cash flows record more negative short-term accruals. Turning to the bad news portfolios, we find consistent evidence of a symmetrically negative relation between short-term accruals and operating cash flow news and no evidence of nonlinearity at zero news.

Relation of Depreciation and Amortization Accruals With Cash Flow News

Column 3 of Table 2 reports results based on linear and piecewise-linear regressions of investing cash flows on operating cash flow news. Prior to interpreting our results, recall that higher capital expenditures imply more negative investing cash flows. Starting with the linear regression results, we find evidence of an overall negative association between investing cash flows and operating cash flow news. The coefficient on implies that firms invest cents per dollar of operating cash flow news. This finding is consistent with long-standing evidence in corporate finance of a positive link between capital expenditures and internally generated funds.

Turning to the piecewise-linear regression results, we find asymmetry in the relation of investing cash flows with operating cash flow news. Consistent with firms facing higher costs in adjusting capital stocks downward than upward, the piecewise-linear regression results imply that capital expenditures increase with good news and are less responsive to bad news. In fact, we find that capital expenditures are virtually insensitive to bad news. The good news coefficient is , the incremental coefficient on bad news is , and, therefore, the bad news coefficient is close to zero. Put differently, the estimates imply that firms invest nearly 33 cents per dollar of positive operating cash flow news, while they invest zero cents per dollar of negative operating cash flow news.

Although asymmetry in the relation of investing cash flows with operating cash flow news cannot be attributed to conditional conservatism, it is relevant for understanding asymmetry in the relation of aggregate accruals with operating cash flow news. This is because investment is linked to the accrual generating process through accruals, which typically account for the bulk of aggregate accruals (see Table 1).11

Column 4 of Table 2 sheds light on the relation of accruals with operating cash flow news. The linear regression results document an overall negative association between accruals and operating cash flow news that cannot be attributed to the smoothing role of accruals in ameliorating fluctuations in operating cash flows. Turning to the piecewise-linear regression results, we find asymmetry in the relation of accruals with operating cash flow news mirroring evidence of asymmetry in investing cash flows. The good news coefficient is , the incremental coefficient on bad news is and, therefore, the bad news coefficient is . Stated otherwise, while accruals increase in absolute magnitude with good news, they are relatively insensitive to bad news. Therefore, the AT coefficient for accruals is positive.

Figure 2, Panel C, presents the plot of accruals on across decile portfolios formed annually based on . The portfolio analysis yields evidence consistent with the piecewise-linear regressions. Focusing on the good news portfolios, we find that firms with more positive news about operating cash flows record more negative accruals. For the bad news portfolios, the relation between accruals and negative operating cash flow news is relatively flat. The figure also shows that the kink in the relation of accruals with is located at zero news.

Since the recognition of depreciation and amortization plays no role in asymmetric timely loss recognition, our evidence of asymmetry in the relation of accruals with operating cash flow news cannot be attributed to conditional conservatism. Importantly, the conditional relations between accruals and operating cash flow news are opposite of what would be expected under conditional conservatism. While the relation between accruals and operating cash flow news is flat for bad news and negative for good news, the relation between and operating cash flow news is positive for bad news and flat for good news.

Taken together, the results are consistent with Prediction 3. One general implication is that the incremental coefficient on bad news cannot be interpreted in isolation from the underlying conditional relations.12

Implications for Prior Research Using Aggregate Accruals

Column 5 of Table 2 focuses on the relation of aggregate accruals () with operating cash flow news (). Starting with the linear regression results, we observe an overall negative relation between and . The coefficient estimate implies that per dollar of operating cash flow news the accounting system records cents of aggregate accruals of the opposite sign. Recall that . The cash flow news slope coefficients for , , , and are , , , and , respectively. The breakdown confirms that when estimating the degree of smoothing in aggregate accruals, the component is a source of downward bias since , while the component is a source of upward bias since . Our results show that provides a downward biased estimate of smoothing (i.e., because the two opposing effects do not completely offset each other.

Turning to the piecewise-linear regression results, our findings confirm prior evidence of asymmetry in the relation of aggregate accruals with operating cash flow news. The good news coefficient is , the incremental coefficient on bad news is , and, therefore, the bad news coefficient is . With respect to the incremental coefficients on bad news, we note that . The piecewise-linear regression results show that the AT coefficients for , , , and are , , , and , respectively. While and do not have a significant impact on the asymmetric relation of aggregate accruals with cash flow news, asymmetry in the relation of with cash flow news accounts for nearly of asymmetry in the relation of aggregate accruals with cash flow news (divide by ). When compared to the AT coefficient for , the AT coefficient for overstates the degree of asymmetric timeliness in accrual accounting; that is, .

With respect to the good news coefficient for , we note that . The piecewise-linear regression results show that the good news coefficients for , , , and are , , , and , respectively. While the good news coefficients for and are not significantly different from zero, the significantly negative good news coefficient for accounts for nearly of the overall good news coefficient for aggregate accruals (divide by ). Given that accruals play no role in smoothing operating cash flow fluctuations, it follows that the good news coefficient for aggregate accruals is an overstated measure of smoothing; that is, .

Starting with Ball and Shivakumar (2006), prior research typically attributes asymmetry in the relation of aggregate accruals with operating cash flow news to conditional conservatism. However, our evidence shows that the AT coefficient for aggregate accruals is upwardly biased because it commingles the asymmetric timeliness role of conditionally conservative accruals with asymmetry in the relation between accruals and operating cash flow news. While asymmetry in accruals does not reflect asymmetric timely loss recognition, the incremental bad news coefficient for accounts for nearly of the AT coefficient for aggregate accruals. Taken together, our evidence shows that focusing on aggregate accruals can lead to biased estimates of both smoothing and conditional conservatism.13

Additional Analyses

Has the smoothing role of accruals disappeared?

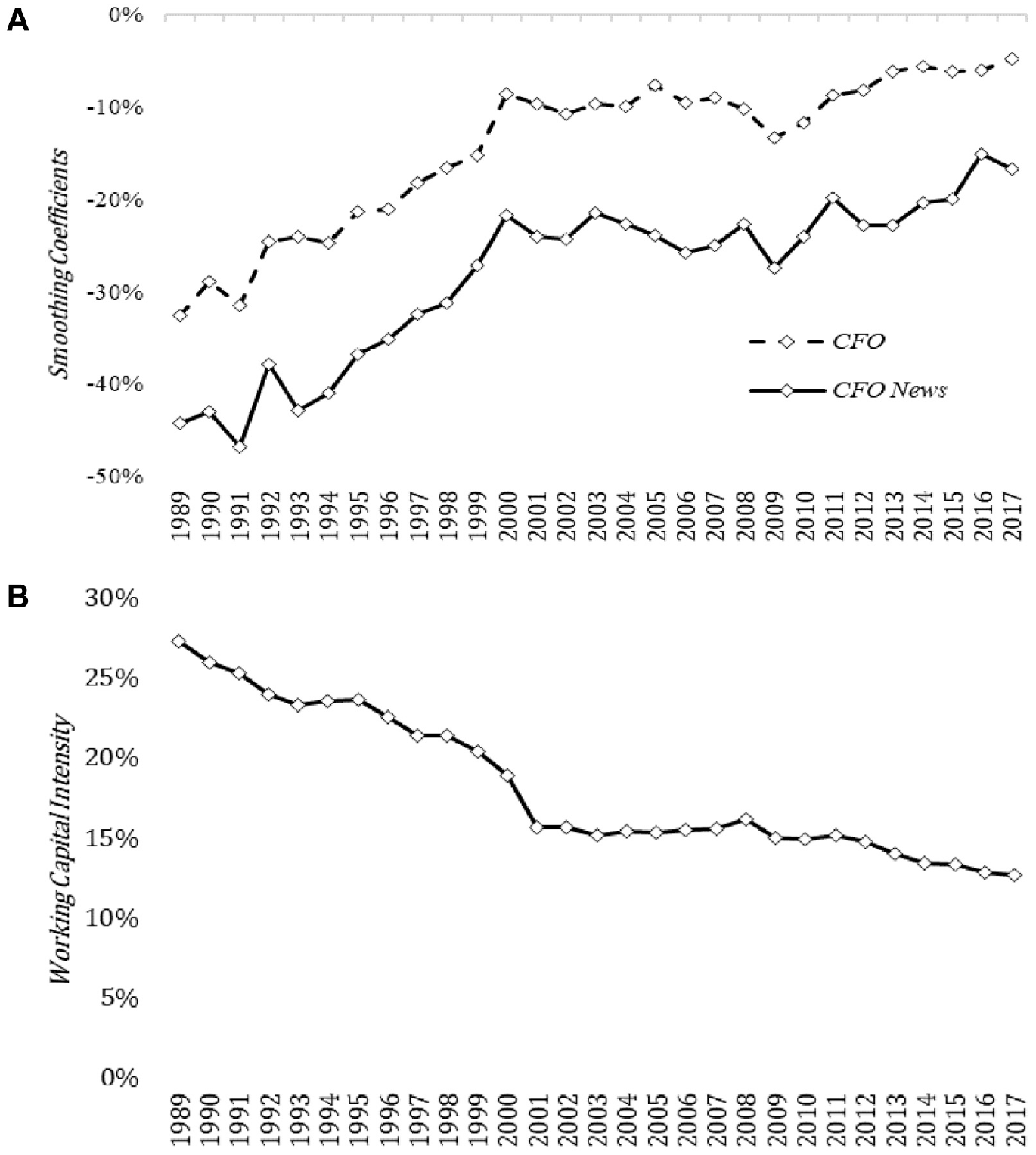

Next, we provide evidence that our approach to identifying the different roles of accruals has broader important implications for research on time-series and cross-sectional variation in smoothing and asymmetric timeliness. Figure 3, Panel A, reports the estimated slope coefficients from annual cross-sectional regressions of (a) short-term accruals on operating cash flow realizations (dashed line) and (b) short-term accruals on operating cash flow news (solid line). The annual coefficients show that the estimated degree of smoothing in is consistently more negative for operating cash flow news rather than operating cash flow realizations. While both series exhibit a declining trend, the relation of with operating cash flow realizations indicates that the smoothing role of short-term accruals has largely disappeared in recent years. In contrast, the relation of with operating cash flow news indicates that the smoothing role of short-term accruals has remained significant throughout the period from 1989 to 2017.

Has the smoothing role of accruals disappeared? Panel (A) the changing landscape of smoothing. Panel (B) the changing landscape of working capital intensity.

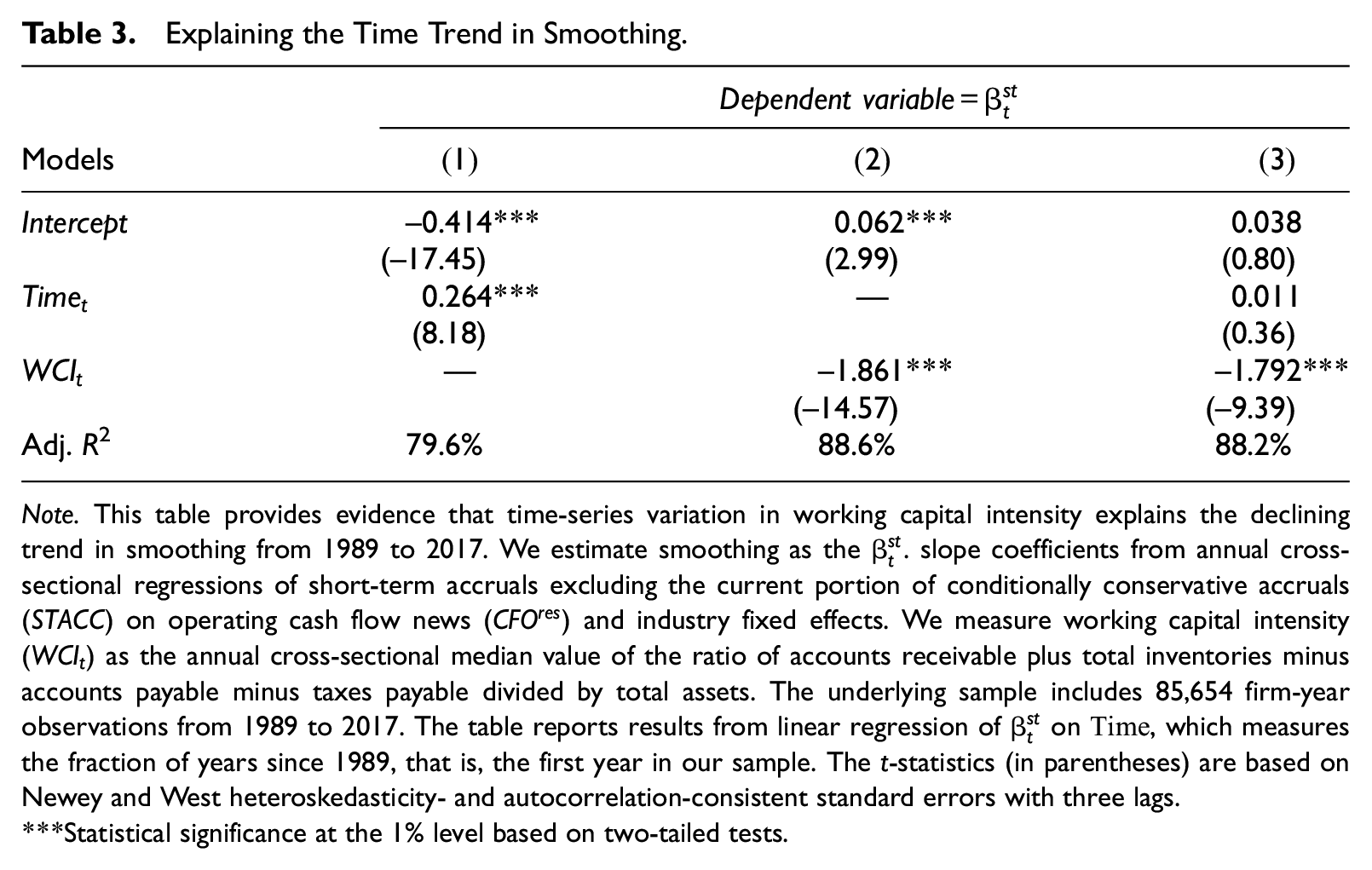

Figure 3, Panel B, presents evidence that the declining trend in the smoothing role of matches a corresponding trend in working capital intensity (). Over our sample period, has declined by more than half from 28% in 1989 to 13% in 2017. This declining trend in is consistent with the increasing prominence of intangible-intensive firms (e.g., Srivastava, 2014). Evidence that the degree of smoothing in decreases with is also consistent with predictions from models of the short-term accrual process (e.g., Dechow et al., 1998; Frankel & Sun, 2018). Within the context of these models, smoothing is expected to decrease with the level of since lower working capital intensity implies shorter operating cash cycles. Consistent with this prediction, Table 3 reports results from time-trend regressions and shows that time-series variation in the level of explains almost entirely the declining time trend in the degree of smoothing. Moving from the simple to the multiple regression results, the time-trend coefficient drops by 96% from 0.264 to 0.011.

Note. This table provides evidence that time-series variation in working capital intensity explains the declining trend in smoothing from 1989 to 2017. We estimate smoothing as the . slope coefficients from annual cross-sectional regressions of short-term accruals excluding the current portion of conditionally conservative accruals () on operating cash flow news () and industry fixed effects. We measure working capital intensity () as the annual cross-sectional median value of the ratio of accounts receivable plus total inventories minus accounts payable minus taxes payable divided by total assets. The underlying sample includes 85,654 firm-year observations from 1989 to 2017. The table reports results from linear regression of on , which measures the fraction of years since 1989, that is, the first year in our sample. The t-statistics (in parentheses) are based on Newey and West heteroskedasticity- and autocorrelation-consistent standard errors with three lags.

Statistical significance at the 1% level based on two-tailed tests.

Overall, the evidence shows that the degree of smoothing in has remained significant every year post-1989 and that the declining trend in smoothing is closely related to a corresponding trend in working capital intensity. One key implication of our evidence is that research on time-series variation in the smoothing role of accruals should zero in on the mapping of operating cash flow news into short-term accruals (excluding the current portion of conditionally conservative accruals), while accounting for changes in working capital intensity over time.

Are small firms more conditionally conservative?

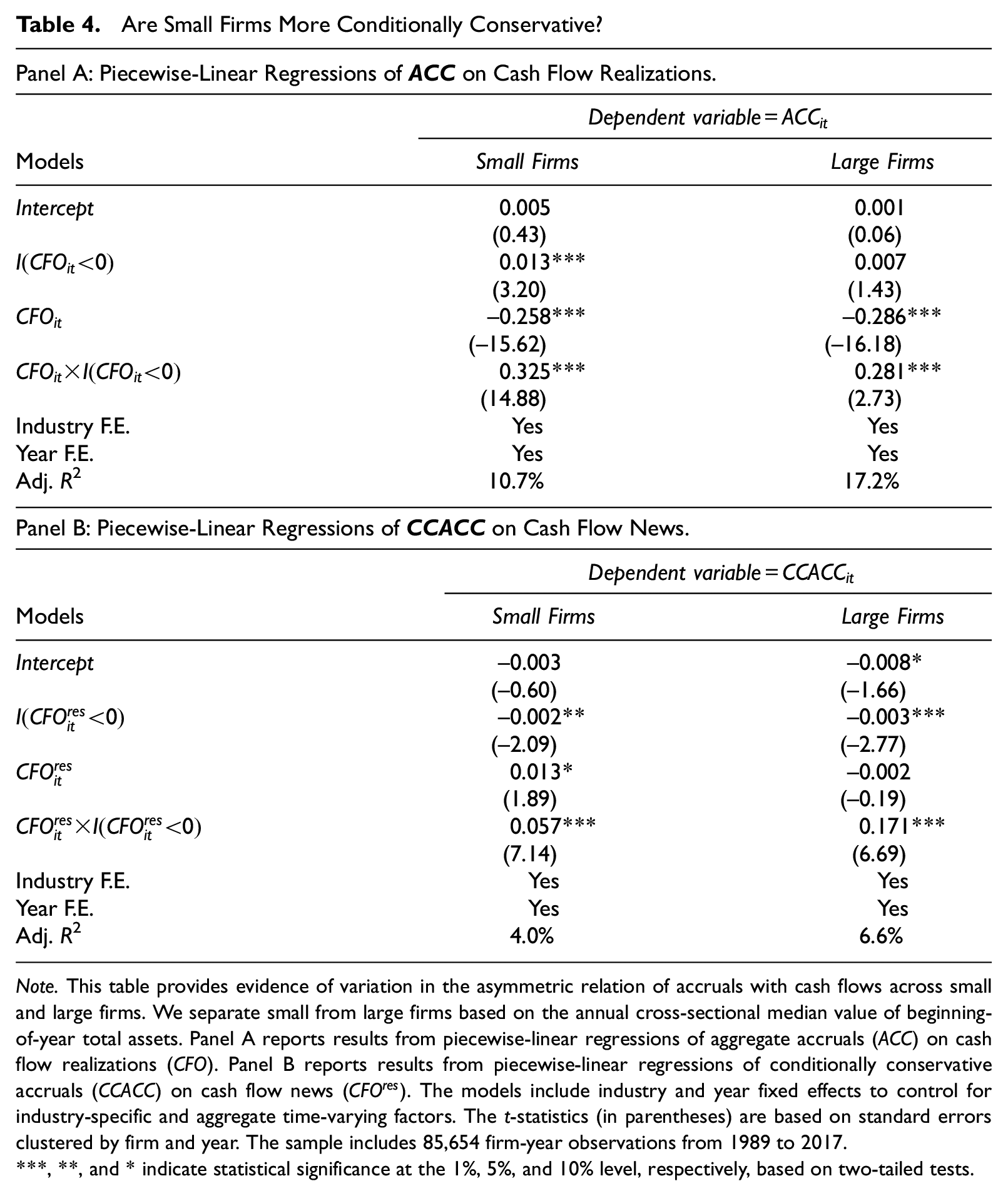

Next, we search for evidence of cross-sectional variation in AT coefficient estimates and provide evidence that our granular approach has the potential to yield different inferences about variation in the degree of asymmetric timeliness across firms. While there is a plethora of partitioning variables, we consider size as one of the most salient firm characteristics. We separate small from large firms based on the annual cross-sectional median value of beginning-of-year total assets. Table 4 reports results from piecewise-linear regressions estimated separately across partitions of small and large firms.

Are Small Firms More Conditionally Conservative?

Panel A: Piecewise-Linear Regressions of on Cash Flow Realizations.

Models

0.005(0.43)

0.001(0.06)

0.013***(3.20)

0.007(1.43)

−0.258***(−15.62)

−0.286***(−16.18)

0.325***(14.88)

0.281***(2.73)

Industry F.E.

Yes

Yes

Year F.E.

Yes

Yes

Adj. R2

10.7%

17.2%

Panel B: Piecewise-Linear Regressions of on Cash Flow News.

Note. This table provides evidence of variation in the asymmetric relation of accruals with cash flows across small and large firms. We separate small from large firms based on the annual cross-sectional median value of beginning-of-year total assets. Panel A reports results from piecewise-linear regressions of aggregate accruals () on cash flow realizations (). Panel B reports results from piecewise-linear regressions of conditionally conservative accruals () on cash flow news (). The models include industry and year fixed effects to control for industry-specific and aggregate time-varying factors. The t-statistics (in parentheses) are based on standard errors clustered by firm and year. The sample includes 85,654 firm-year observations from 1989 to 2017.

, **, and * indicate statistical significance at the 1%, 5%, and 10% level, respectively, based on two-tailed tests.

Table 4, Panel A, shows that the relation between aggregate accruals and cash flow realizations is more asymmetric for small firms. Table 4, Panel B, shows that the relation between accruals and cash flow news is significantly more asymmetric for large firms relative to small firms when we zero in on conditionally conservative accruals rather than aggregate accruals. The AT coefficient increases by a factor of three from 0.057 for small firms to 0.171 for large firms and the AT coefficient spread is significantly different from zero ( statistic of 41.00). Our evidence of a positive association between firm size and the degree of asymmetric timeliness is consistent with arguments that larger firms may be more conservative due to increased litigation demand for timely bad news recognition (e.g., Khan & Watts, 2009), and greater exposure to public scrutiny and political costs (e.g., Givoly et al., 2007; Watts & Zimmerman, 1986).

Cash flow news versus cash flow realizations

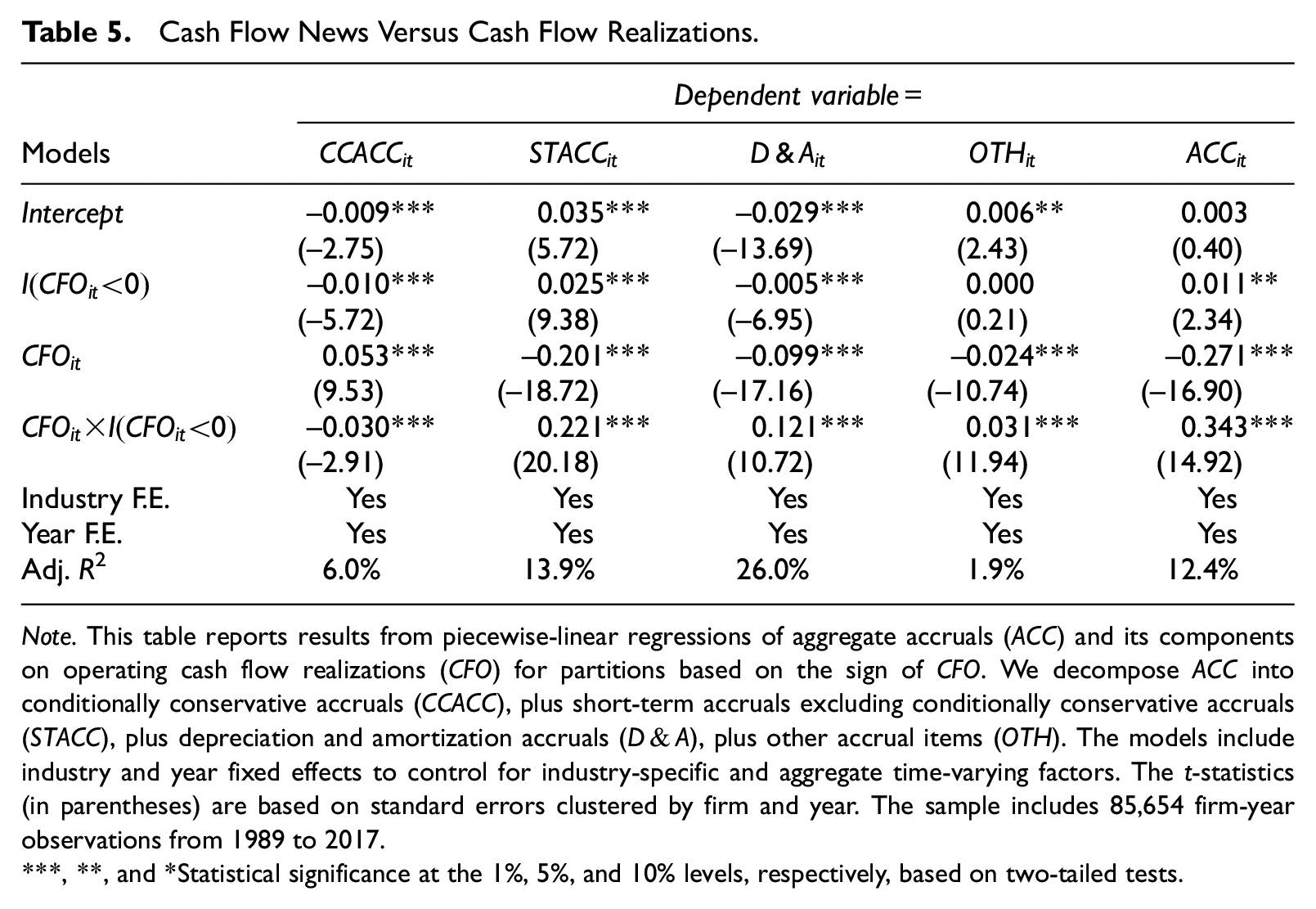

Our approach to identifying smoothing and asymmetric timeliness focuses on the relation of individual accrual components with operating cash flow news. Different from our granular approach, prior studies have focused on the relation of aggregate accruals (rather than individual accrual components) with operating cash flow realizations (rather than operating cash flow news). Since accrual recognition is typically triggered by news, we argue that understanding the mapping between individual accrual components and operating cash flow news offers a more direct and productive approach to identifying the different roles of accruals. In contrast, operating cash flow realizations blend cash flow expectations with cash flow surprises, thereby, offering a poor measure of cash flow news. Indeed, 37% of observations with positive operating cash flow realizations have negative operating cash flow news in our sample.

To illustrate how blending cash flow news with cash flow expectations can distort inferences about asymmetric timeliness, Table 5 reports results from piecewise-linear regressions of accrual components on operating cash flow realizations. While the positive AT coefficient for aggregate accruals is consistent with asymmetric timely loss recognition, we observe that this evidence of asymmetry in the relation of aggregate accruals with operating cash flow realizations is entirely due to accrual components other than conditionally conservative accruals. In fact, we find that the incremental bad news coefficient for is significantly negative , which is inconsistent with the fact that must reflect conditional conservatism. Furthermore, the positive incremental bad news coefficient for indicates spurious evidence of asymmetric timeliness since our measure of short-term accruals excludes the current portion of conditionally conservative accruals. As before, the positive incremental bad news coefficient for cannot be attributed to asymmetric timeliness because the recognition of accruals is not subject to asymmetric timeliness.

Note. This table reports results from piecewise-linear regressions of aggregate accruals () and its components on operating cash flow realizations () for partitions based on the sign of . We decompose into conditionally conservative accruals (), plus short-term accruals excluding conditionally conservative accruals (), plus depreciation and amortization accruals (), plus other accrual items (). The models include industry and year fixed effects to control for industry-specific and aggregate time-varying factors. The t-statistics (in parentheses) are based on standard errors clustered by firm and year. The sample includes 85,654 firm-year observations from 1989 to 2017.

, **, and *Statistical significance at the 1%, 5%, and 10% levels, respectively, based on two-tailed tests.

Determinants of expected accruals

Following Larson et al. (2018), we further expand the right-hand-side of the piecewise-linear regression model of accrual components on operating cash flow news with a vector of previously identified determinants of expected accruals. The vector includes employee growth, the beginning-of-year net capital intensity, the interaction of employee growth with net capital intensity, as well as a piecewise-linear transformation of the market-to-lagged book ratio. We report these results in Table A1 of the Online Supplement. The evidence shows that our inferences are not sensitive to controlling for previously identified determinants of expected accruals. With respect to , we continue to find that the good news coefficient is indistinguishable from zero while the incremental bad news coefficient is significantly positive. With respect to , we continue to find a symmetrically negative relation between short-term accruals and operating cash flow news. With respect to accruals, we continue to find significant evidence of asymmetric timeliness that cannot be attributed to conditional conservatism. We caution, however, that the vector of determinants is unlikely to perfectly measure firm-specific expected accruals.

Conclusion

Understanding the roles of accruals is one of the primary goals of accounting research. In this article, we investigate the role of individual accrual components and identify asymmetry in the relation of investment with operating cash flow news as a confounding factor. We show that this investment factor operates through depreciation and amortization accruals, which typically account for the bulk of aggregate accruals. Overall, our article demonstrates the importance of adopting a granular approach to identifying the different roles of individual accrual components. More generally, this approach illustrates that researchers can gain valuable insights by intersecting seemingly unrelated lines of research across disciplines. In this article, we gain new insights about the accrual process by intersecting research in accounting on accrual properties with research in corporate finance on investment-cash flow sensitivity.

Supplemental Material

sj-pdf-1-jaf-10.1177_0148558X211035224 – Supplemental material for Identifying the Roles of Accounting Accruals in Corporate Financial Reporting

Supplemental material, sj-pdf-1-jaf-10.1177_0148558X211035224 for Identifying the Roles of Accounting Accruals in Corporate Financial Reporting by Sunil Dutta, Panos N. Patatoukas and Annika Yu Wang in Journal of Accounting, Auditing & Finance

Footnotes

Acknowledgements

We thank Samuel Davidson (AAA discussant), Omri Even-Tov, Rich Frankel, Jacquelyn Gillette, Thomas Hemmer, James Potepa, Richard Sloan, Jake Thomas, Jenny Zha Giedt, the PhD students at Berkeley Haas and Yale University, and seminar participants at the Australian National University, Rice University, the University of Houston, U.C. San Diego, Yale University, and the 2019 AAA Annual Meeting for helpful comments and discussions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge financial support from the Center for Financial Research and Management at Berkeley Haas.

ORCID iD

Panos N. Patatoukas

Supplemental Material

Supplemental material for this article is available online.

Notes

References

1.

AbelA.EberlyJ. (1994). A unified model of investment under uncertainty. American Economic Review, 84(5), 1369–1384.

2.

AbelA.EberlyJ. (1996). Optimal investment with costly reversibility. Review of Economic Studies, 63(4), 581–593.

3.

AllayannisG.MozumdarA. (2004). The impact of negative cash flow and influential observations on investment-cash flow sensitivity estimates. Journal of Banking and Finance, 28(5), 901–930.

4.

AndersonM. C.BankerR. D.JanakiramanS. N. (2003). Are selling, general, and administrative costs sticky?Journal of Accounting Research, 41(1), 47–63.

5.

ArrowK. (1968). Optimal capital policy with irreversible investment. In WolfeJ. (Ed.), Value, capital and growth, papers in honour of Sir John Hicks (pp. 1–19). Aldine Publishing.

6.

BallR.ShivakumarL. (2006). The role of accruals in asymmetrically timely gain and loss recognition. Journal of Accounting Research, 44(2), 207–242.

7.

BankerR. D.BasuS.ByzalovD. (2017). Implications of impairment decisions and assets’ cash-flow horizons for conservatism research. The Accounting Review, 92(2), 41–67.

8.

BankerR. D.BasuS.ByzalovD.ChenJ. (2016). The confounding effect of cost stickiness on conservatism estimates. Journal of Accounting and Economics, 61(1), 203–220.

9.

BarthM. E.ClinchG.IsraeliD. (2016). What do accruals tell us about future cash flows?Review of Accounting Studies, 21(3), 768–807.

10.

BarthM. E.CramD. P.NelsonK. K. (2001). Accruals and the prediction of future cash flows. The Accounting Review, 76(1), 27–58.

11.

BasuS. (1997). The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics, 24(1), 3–37.

BushmanR.LermanA.ZhangF. (2016). The changing landscape of accrual accounting. Journal of Accounting Research, 54(1), 41–78.

14.

DechowP. (1994). Accounting earnings and cash flows as measures of firm performance: The role of accounting accruals. Journal of Accounting and Economics, 18(1), 3–42.

15.

DechowP.GeW. (2006). The persistence of earnings and cash flows and the role of special items: Implications for the accrual anomaly. Review of Accounting Studies, 11(2–3), 253–296.

16.

DechowP.KothariS. P.WattsR. (1998). The relation between earnings and cash flows. Journal of Accounting and Economics, 25(2), 133–168.

17.

DietrichJ. R.MullerK. A.RiedlE. J. (2007). Asymmetric timeliness tests of accounting conservatism. Review of Accounting Studies, 12(1), 95–124.

18.

DuttaS.PatatoukasP. N. (2017). Identifying conditional conservatism in financial accounting data: Theory and evidence. The Accounting Review, 92(4), 191–216.

19.

FazzariS.HubbardG.PetersenB. (1988). Financing constraints and corporate investment. Brookings Papers on Economic Activity, 1988(1), 141–206.

20.

FrankelR. M.SunY. (2018). Predicting accruals based on cash-flow properties. The Accounting Review, 93(5), 165–186.

21.

GiglerF. B.HemmerT. (2001). Conservatism, optimal disclosure policy, and the timeliness of financial reports. The Accounting Review, 76(4), 471–493.

22.

GivolyD.HaynC.NatarajanA. (2007). Measuring reporting conservatism. The Accounting Review, 82(1), 65–106.

23.

HallR. (2001). The stock market and capital accumulation. American Economic Review, 91(5), 1185–1202.

24.

HribarP.CollinsD. (2002). Errors in estimating accruals: Implications for empirical research. Journal of Accounting Research, 40(1), 105–134.

25.

JohnsonP. M.LopezT. J.SanchezJ. M. (2011). Special items: A descriptive analysis. Accounting Horizons, 25(3), 511–536.

26.

KeatingA. S.ZimmermanJ. L. (1999). Depreciation-policy changes: Tax, earnings management, and investment opportunity incentives. Journal of Accounting and Economics, 28(3), 359–389.

27.

KhanM.WattsR. (2009). Estimation and empirical properties of a firm-year measure of accounting conservatism. Journal of Accounting and Economics, 48(2), 132–150.

28.

LarsonC.SloanR.Zha GiedtJ. (2018). Defining, measuring and modeling accruals: A guide for researchers. Review of Accounting Studies, 23(3), 827–871.

29.

LaurionH.PatatoukasP. N. (2016). From micro to macro: Does conditional conservatism aggregate up in the national income and product accounts?Journal of Financial Reporting, 1(2), 21–45.

30.

LewellenJ.LewellenK. (2016). Investment and cash flow: New evidence. Journal of Financial and Quantitative Analysis, 51(4), 1135–1164.

31.

LewellenJ.ResutekR. J. (2016). The predictive power of investment and accruals. Review of Accounting Studies, 21(4), 1046–1080.

32.

PapadakisG. (2007). Investment dynamics and the timeliness properties of accounting numbers [Doctoral dissertation]. Massachusetts Institute of Technology.

33.

PatatoukasP. N.ThomasJ. K. (2011). More evidence of bias in differential timeliness estimates of conditional conservatism. The Accounting Review, 86(5), 1765–1793.

34.

PatatoukasP. N.ThomasJ. K. (2016). Placebo tests of conditional conservatism. The Accounting Review, 91(2), 625–648.

35.

SrivastavaA. (2014). Why have measures of earnings quality changed over time?Journal of Accounting and Economics, 57(2–3), 196–217.

36.

SteinJ. C. (2003). Agency, information and corporate investment. In ConstantinidesG. M.HarrisM.StulzR. M. (Eds.), Handbook of the economics of finance (pp. 111–165). Elsevier.

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.