Abstract

The purpose of this article is to establish a framework with its related measures for the development of a balanced scorecard (BSC) for auditing firms. A BSC was developed providing the detailed measures for performance evaluation comprising five key elements: learning and growth, clients, internal business processes, financials, and audit-related perspectives of corporate ethics. A survey was undertaken along with descriptive statistics and confirmatory factor analysis in four auditing firms, to assess the external auditors’ opinions for the proposed BSC measures. The results suggest that the development and use of the proposed BSC measures will enhance audit firms’ performance. Audit firms would have a better understanding of the various drivers of performance and strategies thereby creating a competitive advantage. The results are valuable to not only audit firms but also auditing oversight boards who could direct the design of their monitoring process by understanding performance systems in different size audit firms.

Keywords

Introduction

Auditing standards provide guidelines for audit quality with little attention given to how audit firms should be managed. For example, the International Standard on Auditing (ISA) 220 highlights the importance of elements related to the internal processes and the human resource management of employees without incorporating a more integrated performance measurement system in an ever-dynamic environment. Auditing firms require a system by which its performance rather than only the quality of their outputs (i.e., audit opinion) can be measured. This system may be composed of (a) supervision, (b) internal reviews, (c) external reviews, and (d) performance and benchmarking. While more emphasis was given to external peer reviews and internal reviews by quality control partners, performance and benchmarking started to gain more attention in recent years (Albright et al., 2015; Ditillo et al., 2016; Hoque, 2014; Kaplan & Norton, 2001; Kunz et al., 2016; Neely et al., 2002; Sayed, 2013). Such performance measurement systems should include important elements of performance, such as customer satisfaction, growth, and financial viability of conducting the audit (Hoque, 2014; Kaplan, 1984; Kaplan and Norton, 1992, 1996a, 1996b). Albertsen and Lueg (2014, p. 431) found that only 30 out of 117 empirical studies have a research design that is sufficiently comprehensive to capture a full balanced scorecard (BSC). This view was also shared by Kaplan and Norton (1996a, 1996b): “(the) extent (of) research lacks valid constructs for the BSC and focuses too much on planning (ex-ante) with the BSC and not sufficiently on evaluation and control (ex-post).”

Thus, there is a need for additional research into the BSC design and implementation in various types of organizations including professional services. Moreover, Hoque (2014) reviewed 181 research studies covering 20 years of BSC design and application where none of these studies provided a detailed framework of BSCs in audit firms. Audit firms should be examined for possibly adopting a more holistic and integrated performance measurement approach such as the BSC. As the BSC is a flexible measurement tool (Kaplan & Norton, 1996a), whereas auditing is a more regulated profession, this study is undertaken to assess how auditing firms can benefit from a BSC. The current research develops a BSC framework, along with its related measures, for auditing firms.

Professional services have unique characteristics associated with professional knowledge considered the core source for their service success as it represents both the input and output in their production process. Moreover, professional services rely on other firms’ output as their intermediate input for the provision of such services (Sayed, 2013). This is considered a significant difference between professional and manufacturing organizations, where the latter is viewed as a consumer product. Thus, the different role between both organizations requires diverse means to assess their service outputs (Ditillo et al., 2016). By adopting an exploratory two-stage empirical approach, this article, using expert auditors’ opinions, proposes and validates a BSC approach to integrate the objectives and measures of a measurement system for auditing firms. A BSC would enable audit partners and managers to have access to view the audit firm’s performance in various areas simultaneously. Thus, the current research has three objectives: (a) to establish a framework for BSC perspectives in audit firms; (b) to empirically validate the scales of these perspectives including the measures identified for the developed BSC; and (c) to assess auditors’ opinions of the developed BSC effect on the performance of audit firms.

This article has several contributions to the auditing and performance evaluation literature. First, it critically reviews the literature related to the nature and type of performance measurement systems used in professional services and whether any of them follow a BSC or similar models. Second, it addresses an issue of practical relevance in the implementation of a BSC in audit firms as advocated by Baldvinsdottir et al. (2010), who argued that over the past few years there has been a decline in accounting research for the logical and normative analyses of practice. The research provides a scientific analysis as well as real case studies of appropriate performance indicators of a BSC or a similar system in professional auditing firms, by adding a fifth perspective, corporate ethics to Kaplan and Norton’s (1996a, 1996b) four perspectives. This perspective is unique for audit firms as the type of service provided is mainly based on ethics, integrity, and honesty. Third, the research follows the trend in the literature to analyze the importance of nonfinancial measures in performance evaluation compared with financial measures identifying those considered for professional services such as auditing. Fourth, the research investigates how the use of the proposed BSC framework would enhance the performance of audit firms compared with traditional performance systems based on auditors’ opinions.

The remainder of this article is structured as follows: The “Performance Measurement and a BSC in Professional Services” section reviews the literature and develops the research questions (RQs) and hypotheses. The “Research Method” section discusses the research methodology followed by the results. The “Auditors’ Perceptions of the BSC—Findings and Discussion” section provides descriptive statistics and confirmatory factor analysis (CFA) for the results of the survey of the auditors’ opinions about the proposed BSC, and finally, conclusions, limitations, and recommendations for future research are presented.

Performance Measurement and a BSC in Professional Services

The importance of performance measurement has been widely discussed in the accounting literature (Ditillo et al., 2016; Neely, 2005; Neely et al., 2002; Paranjape et al., 2006; Taticchi et al., 2010). Lynch and Cross (1991) state that performance measurement is “the single most powerful tool to ensure success of business strategies” (pp. 20–23). Other studies highlighted such importance confirming the need for organizations to develop and successfully implement performance measurement systems using financial and nonfinancial measures (i.e., customer satisfaction, internal process and interactive learning process) and communicating such measures to all levels of management (Albertsen & Lueg, 2014; Sayed, 2013; Sousa & Aspinwall, 2010; Yazdifar & Tsamenyi, 2005).

Traditionally, firms only measured performance financially, either through profits or other related measures (Kaplan & Norton, 2001). However, firms need to have a balance between both financial and nonfinancial indicators to link performance measures to strategy and build competitive advantage (Albright et al., 2015; Kaplan & Norton, 1992). Numerous frameworks have been developed to address such balance including: Performance Pyramids and Hierarchies (McNair et al., 1990), Results and Determination Framework (Fitzgerald & Brig all, 1991), the Balanced Scorecard (Kaplan and Norton, 1992, 1996a, 1996b, 2001), the Intangible Asset Scorecard (Sveily, 1997), Integrated Performance Management Systems (Bititci et al., 1997), and Performance Prisms (Neely et al., 2002).

Although extensive research has been undertaken for performance measurement in the manufacturing sector (Abdallah & Alnamri, 2015; Albertsen & Lueg, 2014; Kopecka, 2015), nevertheless differences remain within the service sectors, which prohibit a smooth transfer of concepts and the need for tailored research studies (Sayed, 2013). Moreover, professional services such as auditing require high contact time with clients who may need customized services. In such services, the focus is on the process rather than the output and is based on personnel who must be competent, qualified, and knowledgeable. Users may rely on financial statements of businesses only if independence, objectivity, and skills of auditors with related audit quality can be achieved (Ditillo et al., 2016). These objectives should be simultaneously achieved while controlling the costs related to audit tasks and maintaining professional standards (Sweeney & McGarry, 2011). The diversified features of performance measurement of service industries result in the need for additional research in developing measures to assess performance within these types of services including professional services (Hegazy & Tawfik, 2015).

Based on the above discussion highlighting the importance of a BSC in service industries, two RQs can be formed within the audit services. Auditors are charged with the responsibility of attesting the fair presentation of their clients’ financial statements and play a critical role in the economy. Numerous standards are issued to ensure they fulfill that role efficiently, but interestingly, auditing standards do not give much attention to how audit firms measure and assess their very own performance. They are concerned with what the firm develops rather than how it develops its own performance measurement. Extensive research concentrated on auditing firms’ development to maintain and enhance the quality of their outputs with less research directed to their inputs and internal management. This creates a research gap. Furthermore, studying how a BSC may result in improvements to auditing firms’ performance measurement and their related management systems could prove beneficial not only to the auditing profession but to all those concerned with its effectiveness including oversight boards. Consequently, a BSC design raises two important RQs and hypotheses for auditing firms:

Sweeney and McGarry (2011) indicated the importance of informal controls in audit firms. This is due to the peculiarities of the audit sector characterized with restricted direct supervision in the field, high levels of uncertainty, the essential role of trust, and the complexity of measuring audit quality. Formal and informal communications are used within the structure of any audit firm. Informal provision of performance evaluation information is frequently preferred, aimed toward more formal processes, due to time pressures and the importance of subjective performance judgments (Ditillo et al., 2016). Human capital and their behavior perspectives are important for the audit profession. Auditors experience, efforts, and training as well as the relationship between audit partners and their subordinates should be captured and the efficiency and effectiveness under which the audit is performed, assessed. Time budget pressures exist for audit tasks as a limited number of hours is allocated to certain audit engagements. Finally, partners’ intuition, hunch, and expertise are major components of any control and performance measurement system in audit firms. This is reflected in an auditor’s “sixth sense,” which includes asking the right questions during the audits, recruiting the best applicants, and finding a balance between trust and monitoring of subordinates (Pierce & Sweeney, 2005).

Moreover, the development of a set of measures for a proposed BSC for auditing firms would be achieved based on studying and analyzing BSC concepts and their application in other service industries. Usual key performance indicators that could be included in the BSC of a service or another industry may not be suitable for the auditing profession. For example, auditors cannot satisfy their customers’ needs with a tailored product because auditors have to provide their opinion about the fair presentation of their clients’ financial statements irrespective of whether clients are “satisfied” with it or not. Furthermore, providing “new products” to customers may not be allowed for certain customers (i.e., providing some corporate finance services to listed companies) as per auditing standards and oversight boards’ requirements. Consequently, the research aspires at developing a BSC for measuring the performance of auditing firms after considering the requirements of auditing standards and the needs of such professional firms. Empirical examining such proposed BSC is necessary to discover its practicality and whether it will enhance the performance of the audit. Thus, applying a BSC can increase practitioners’ satisfaction with performance evaluation in an audit firm. All the above issues have led to the development of the following hypotheses:

Research Method

Case Study Analysis

The current research is descriptive and exploratory. It is descriptive by describing what performance measures are used in some Egyptian auditing firms and exploratory by exploring whether the use of BSC would be practically feasible and would enhance audit performance, given the regulatory environment governing the audit services and their outputs (Saunders et al., 2007). The research study identified the phenomena under study “Balanced scorecard proposed measures” and investigated its application within the audit environment. Yin (2003) highlights that a case study copes with technically unique situations in which there will be several issues of interest more than data could point to. Using a case study proved a worthwhile vehicle for exploring and gaining an in-depth analysis of performance systems across the two studied audit firms. The research was conducted using both semi and unstructured interviews at various stages of the research. An interview with the principal partner of the Big 4 firm was undertaken to get his opinion to refine and adapt the literature for the development of a BSC to audit firms. The questions asked were developed from issues arising in the literature and refined based on insights from the pilot testing performed. The development of the BSC for audit firms was equally constructed from both the previous literature and the investigations held in the mid-size audit firm. Unstructured interviews with the quality control manager, the partner(s), and other employees of the medium size firm were undertaken to evaluate the practicality of the proposed BSC. Empirically, the researchers also observed how the audit partner measures the performance of his subordinates and how the employees fill and hand in their work. This process continued for 2 weeks at the medium size audit firm.

Data Collection, Sample, and Questionnaire Design

After the proposed BSC for an audit firm was developed, the researchers prepared a questionnaire to assess the appropriateness of the proposed BSC measures for audit firms. The results were then statistically tested to assess the expected effect of the proposed BSC on the audit performance. The questionnaire helped collect the auditors’ (with different years of experience) perceptions about the proposed BSC and its likely effect on the performance of the audit. The questionnaire was based on the 5-point Likert-type scale rating. It was pilot tested by presenting its content to four audit partners in four different auditing firms (two from the Big 4 and two from audit firms with international affiliation) and four professors of auditing and management accounting at two reputable Business Schools. A total of 220 questionnaires were distributed. Completed responses of 169 questionnaires were collected from audit firms within a period of 8 weeks. The questionnaires covered five distinct subareas of the proposed BSC: learning and growth, internal business process, financial perspective, client, and corporate ethics perspectives. To measure the performance of the audit considering the five BSC perspectives, the questionnaire included at the end of each perspective a statement to assess the relationship between the application of the proposed measures in each perspective and the expected effect on the performance of the audit firm. The following sections will present the findings related to the development of a BSC for audit firms and the results of the research hypotheses testing.

A BSC Development Framework for Auditing Firms

Hegazy and Tawfik (2015), using case studies in auditing firms, discussed the challenges facing firms in developing their performance evaluation systems. They indicated that the auditing firms’ websites and brochures handed to clients provide the background knowledge for researchers to understand the nature, structure, and activities of these professional firms. Furthermore, analyzing internal documents was useful in understanding and describing the performance measurement systems adopted in auditing firms. Hegazy and Tawfik (2015) showed that despite the Big 4 audit quality control possessing full awareness of the BSC concept, the BSC per say is not yet implemented. The partner in such firm stated, “each element in the BSC is individually measured owing to its importance.” He indicated the importance of people, knowledge, and clients as the major assets of an audit firm. He confirmed that people use knowledge to serve clients who provide the financials and reputation that stimulates growth. Despite the quality control manager of the medium size audit firm confirming the importance of a BSC, nevertheless in terms of practicality he notes that a “BSC is not applicable to all firms as some measures would not be adequately measured, if any, by medium or small sized firms lacking sound information systems to record and measure various elements” (see Sousa & Aspinwall, 2010, for similar observations).

There are five elements which may be included in a BSC for auditing firms: learning and growth, internal business process, customers, financials, and corporate ethics. The first important component is learning and growth. The characteristics of such perspective include the assessment of the qualifications and experience of the employees in auditing firms. Sophisticated and detailed procedures are implemented to ensure employees perform as expected, are knowledgeable, and are presentable. Furthermore, it values the quality of its output necessitating the preparation of working papers for every engagement. Qualification of professionals is measured in terms of international certificates received, average years of audit experience, and calculating the percentages of qualified professionals relative to the less qualified ones. At the same time, measuring employees’ competence may rely on factors such as awareness of the job’s tasks, work quality, speed of concluding work, following plans, continuously updating working papers, trustworthiness, behavior, self-motivation, attendance, punctuality, and appearance. Each factor is weighted, and a score calculated. Ditillo et al. (2016) indicated that an auditor with the best qualification is the one who can fulfill his or her work in 8 h. This should be compared against a budget criterion. Partners, however, are assessed through their commercial attitude reflected in the customer acquisition process. Their performance documented in performance reports are compared with their peers within the audit firm resulting in a stimulating internal competition. Auditors are also evaluated after every engagement where they provide a full report on all tasks performed, the duration consumed, and the expenses incurred. This is fully reviewed by their supervisors and quality control manager to assess the auditor’s performance. Employees or managers nominated for promotion are assessed based on characteristics such as leadership, communication skills, and qualifications.

Moreover, employees should be given targets and appraised using the number of activities to be performed monthly rather than on the hours worked. “Employees who hand in their work in shorter time are better than those staying hours just to report them on their time sheets” (Hegazy & Tawfik, 2015). Salaries and statuses are prorated upward in reflection to any qualifications received, especially international ones. Furthermore, compensation is only based on individual work (Eccles, 1991; Neely, 2005). Outstanding employees are motivated to become partners through special salary increases, moral support, and words of appreciation by their peers. Also, speedy promotion can be achieved once employees earn their professional certificates. Training is also considered a vital element and there is a strict policy of requiring a minimum of annual training hours. This is coupled with a system called “dialogue” which is used as a record between management and staff. This records everything such as the level of satisfaction, any problems, or complaints, and is given a score. Whistleblowing techniques (Near & Miceli, 1995) encourage employees to anonymously report any quality concerns. Continuous feedback is provided by managers and partners about the quality control achieved and the participation of the employees in achieving such level. Other measures could be used to evaluate employees’ satisfaction, which include employees’ turnover, and the ability of the Certified Public Accountant (CPA) to recruit qualified and motivated graduates.

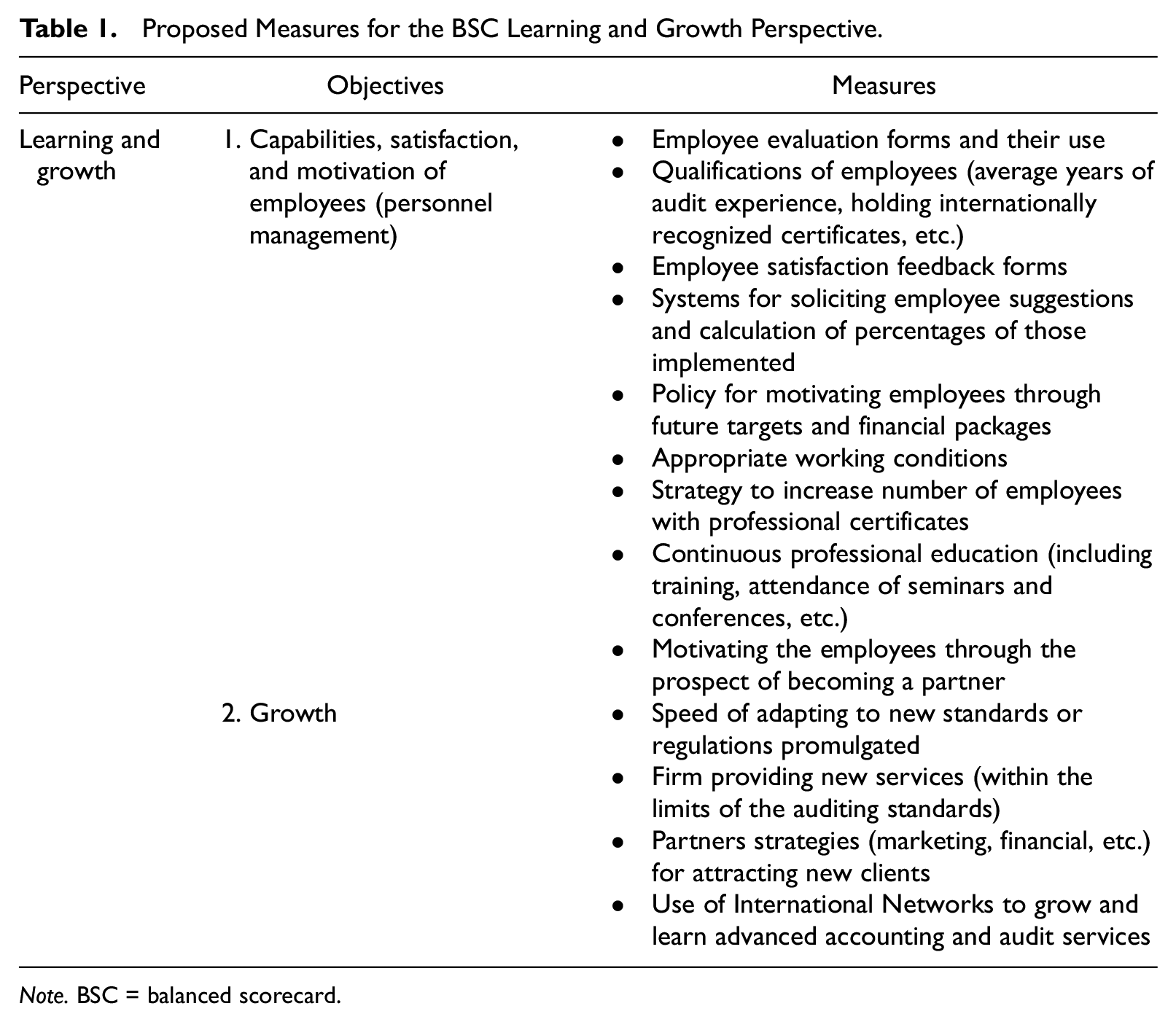

Growth measures may include the number of customers or total revenues received. These figures are compared with budgets and previous year results identifying any problems affecting the firm’s growth. This may include staff/partners’ problems and cases of suing. In addition, it measures its ranking with respect to other audit firms operating in the market using the internationally agreed upon measure “total billings” received by international CPA firms. Furthermore, the time to develop new products is critical to the growth of firms (Kaplan & Norton, 1996a). Most of the CPA firms adopt a principle to serve all clients starting from the existence of an investment opportunity until the end of a company’s life. Moreover, CPA firms ensure any innovated services offered conform to independence standards, because the provision of some services to audit clients such as bookkeeping is prohibited, whereas others are allowed subject to an audit committee’s approval (see Arens et al., 2013; Gary & Manson, 2007). Table 1 illustrates the suggested objectives and measures for the learning and growth aspect based on the above analysis.

Proposed Measures for the BSC Learning and Growth Perspective.

Note. BSC = balanced scorecard.

The second component of the proposed BSC is the “Internal Business Process,” which audit firms measure through the effective and efficient delivery of a high-quality audit with an appropriate report. This is assessed while referring to the detailed documented working papers which describe every single step of the audit in both manual and electronic formats (see also Ditillo et al., 2016). Multilayered and strict quality control procedures should be in place to monitor the adherence to the work agenda by every employee (soft and hard). The firm should also ensure continuously recording, updating, and reviewing (by the in-charge partner) the working papers. In addition, all listed companies audited must have their working papers reviewed by a partner not involved at any stage of the audit to ensure the audit report is fully supported by the working papers. More and above, an internal quality control department must ensure that all audit files are in place and all required signatures are present. In addition, annual quality control visits from the headquarters of the affiliated firms further assures a high-quality control is maintained.

The Recruitment process must run in the most efficient way. As a first step, mainly based on quantitative measures such as high school and university grades, the human resource department should select the most qualified and promising candidates. During the second step, interviews are conducted with the preselected candidates by a committee of one or more partners and managers (Ditillo et al., 2016). The questions expected should focus on the knowledge of international accounting and auditing standards and the ability of candidates to communicate within the team and with the client’s personnel and management “Social competence.” A selected mentor should also be provided for every recruit to act as a guide. At the same time, the recruitment process must be linked with how efficient the audit work is, “Efficiency is the ability to perform a high-quality audit at low cost” as indicated by the partner of a Big 4 (Hegazy & Tawfik, 2015). A strategy plan should also be developed for every engagement and a budget prepared (as suggested by Fitzgerald & Brig all, 1991). The estimated hours needed for an audit engagement are multiplied by a chargeable rate applicable to every auditor on the team, reaching budgeted revenues necessary to cover costs. The actual times and revenues received are then benchmarked against this to compute the “recovery rate” and evaluate the delivery on time.

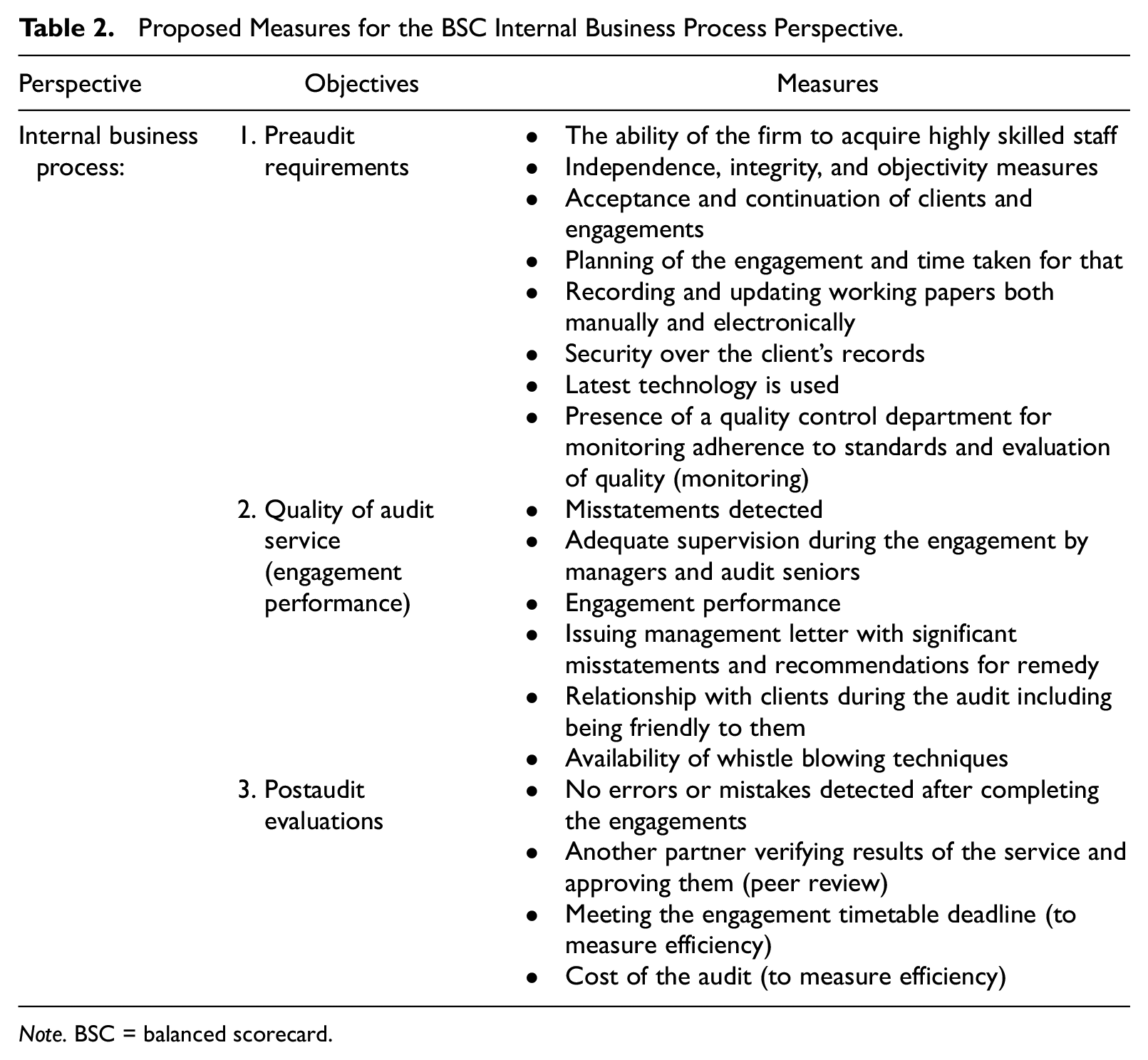

Moreover, auditing firms should set up sophisticated information systems containing the company’s files and records, highly secured customers’ databases, and a cataloged (hard and soft copy) library holding up to date information on auditing standards, regulations, laws, and references. In addition, state-of-the-art electronic auditing tools such as computer-assisted auditing tools (CAATs) should be implemented (Gary & Manson, 2007). As independence is priceless for audit firms, a firm must have strict measures for circumventing any breaches through an independence declaration form signed by every auditor as well as having strict supervisory measures during work. Clients are informally assessed based on risk, previous year’s reports, personnel’s comment, and cost–benefit analysis by executive partners. Engagement performance is measured through both internal and international quality reviewers. This is achieved with reference to working papers, and several checklists to ensure standards and plans were followed, all documents are present and sample sizes are appropriate. An official management letter printed on the firm’s letterhead should be addressed to each client after each engagement expressing all recommendations identified and adding value to their clients’ business. Table 2 presents the proposed objectives and measures for the internal business process aspect.

Proposed Measures for the BSC Internal Business Process Perspective.

Note. BSC = balanced scorecard.

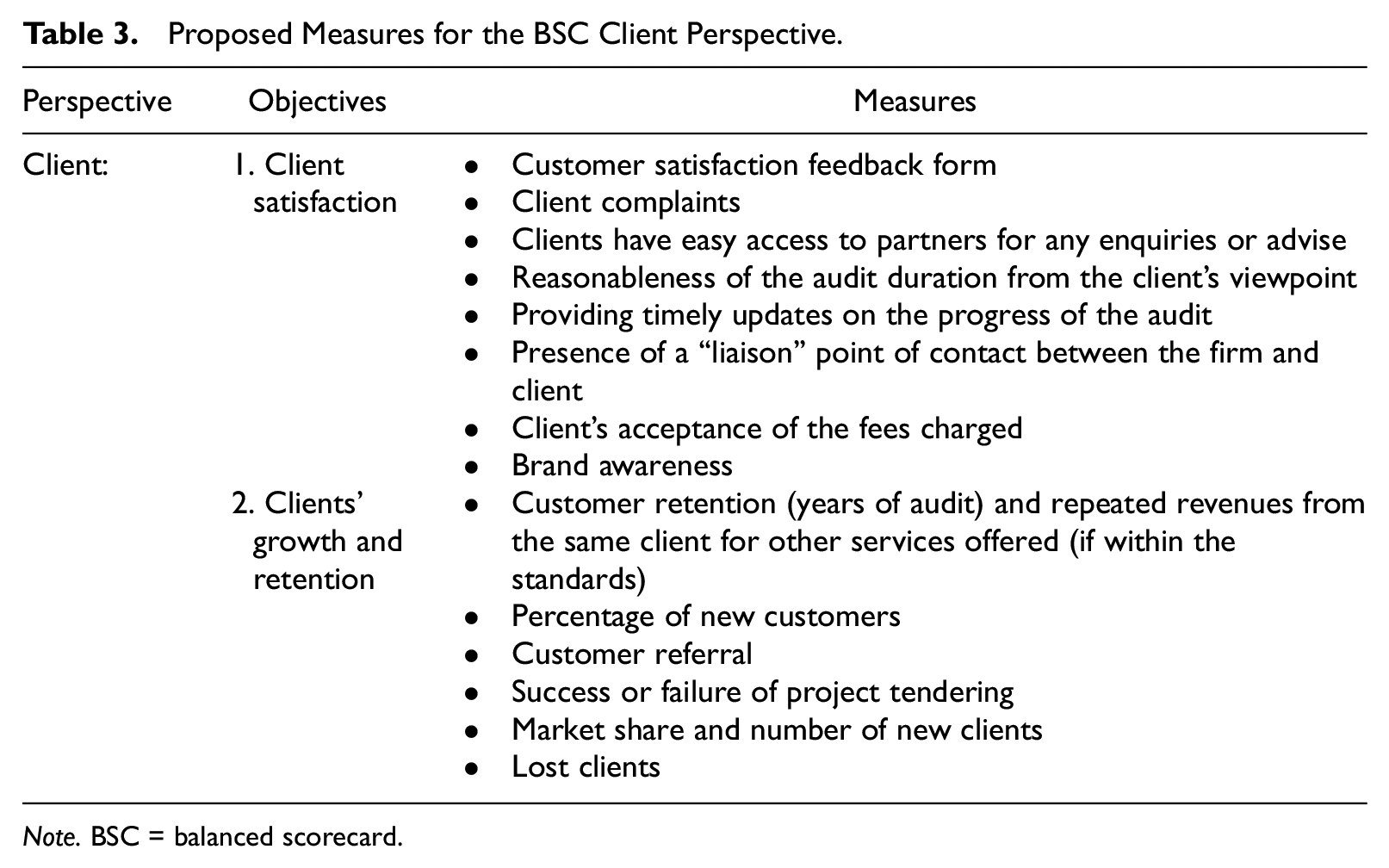

Furthermore, the customers’ assessment and relationship form the third component of the BSC. Formal and written procedures for reaching and measuring customers’ satisfaction include sending customers’ satisfaction questionnaires to the top management of the client requesting a response directly to the firm’s principal partner without the knowledge of the in-charge audit partner. This assessment will measure the client’s satisfaction on areas such as the reasonableness of the audit duration, the value added by the service, and the behavior of the on-site personnel. In addition, clients should be provided with a list of numbers to contact for any queries. The firm initially sets the fees and periodically requests higher fees, which if approved is interpreted as an appreciation of the audit firms’ efforts. Another approach may be based on direct calls made by the managing partner to a list of clients arranging for a meeting to discuss the client’s satisfaction. This is mainly used with those clients too busy to fill in questionnaires. Finally, outsourcing is applied using specialized institutes. Some researchers view brand awareness as a success indicator (Kaplan & Norton, 1996a) particularly relevant to the case of a Big 4 firm. Similarly, high fees charged may not be an indication of success, but a reflection of the efforts exerted in conjunction with the client size. Table 3 highlights the component of the customers’ assessment.

Proposed Measures for the BSC Client Perspective.

Note. BSC = balanced scorecard.

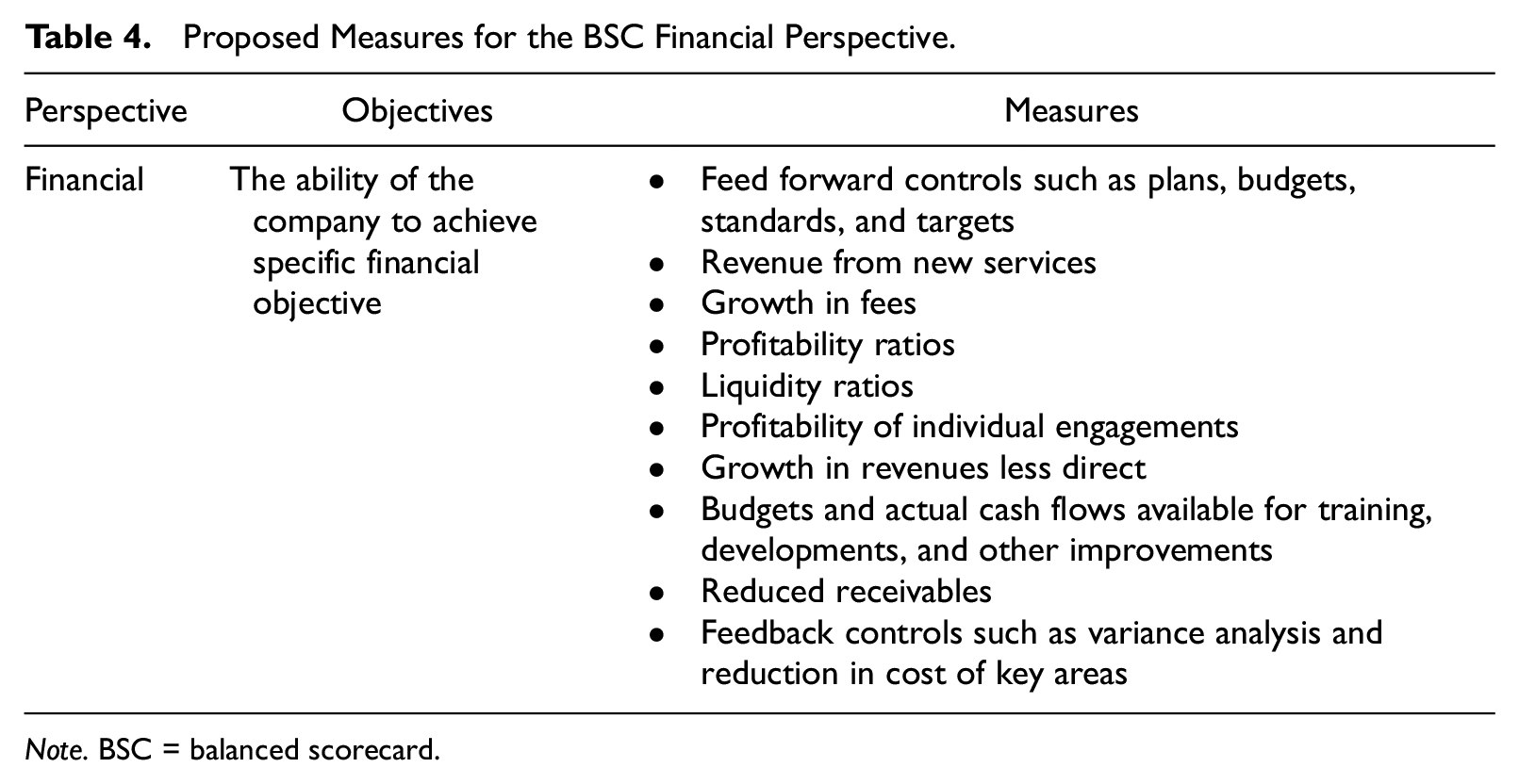

On a further note, the fourth component “financials” can be measured by each audit firm through its sophisticated information system. An audit firm should measure operating profit for every audit team as revenues less direct costs (see Ditillo et al., 2016). Operating profit for every executive in charge of a cluster of audit teams as well as profits per senior partner should be calculated. Overheads and the partners’ remuneration are then deducted attaining the firm’s profit. Such process is repeated quarterly until reaching year end profits, which is compared with budgets and last year’s figures for identifying any significant unfavorable variances leading to an audit firms’ performance evaluation. As Hegazy and Tawfik (2015) indicated, a list of total revenues received from each client, decompose total revenues into its constituents from audit, tax, review and consultancy services and compare those with last year to determine growth, revenue from each service is matched against its expenses including applicable taxes to calculate its profits and again compare it with last year and a monthly statement of all expenses is prepared.

With respect to the practicality of the proposed elements, budgets are planned for recruitments, developments, training, salaries, and other expenditures each year. Ditillo et al. (2016) indicated that the budgeting function usually starts at the manager level within an audit firm. Feedback controls are achieved by comparing actual figures to the budgets or to last year’s results. Expected revenue per engagement and “recovery rates” are also calculated. Revenues from new services are analyzed and revenues from ordinary services broken down by category and lines of business. Moreover, the cost per auditor is calculated using a time sheet filled by every auditor, which is multiplied by an applicable hourly rate to reach the cost per audit team. Table 4 illustrates the objectives and measures of the financials aspect for the proposed BSC.

Proposed Measures for the BSC Financial Perspective.

Note. BSC = balanced scorecard.

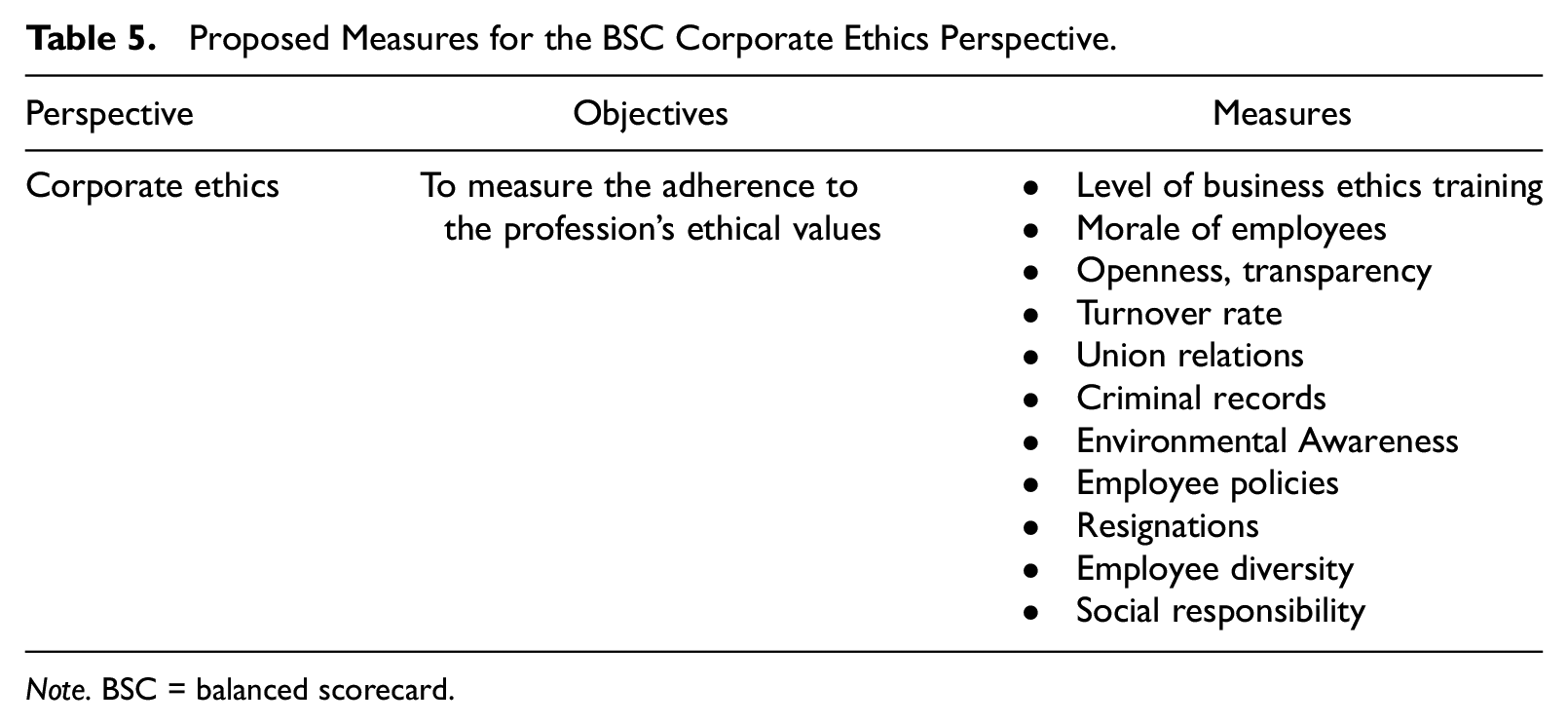

Finally, the Corporate Ethics aspect forms the fifth component of the proposed BSC. This additional perspective from Kaplan and Norton’s original BSC follows other research studies such as by Parida et al. (2003) and Parida (2007) who added a perspective for health, safety, and environment for maintenance performance. Also, Francioli (2014) and Kang et al. (2015) had a fifth perspective in their BSC for strategic linkages and sustainability in the case of hotels. Due to the range of auditing services and recent corporate collapses, attention has been drawn to ethical standards accepted within the accounting and auditing profession (Jackling et al., 2007). Auditing firms aim to be a productive member of the community through employing several techniques and adhering to corporate ethics. Some of these firms not only audit several not for profit organizations, that aim to provide services to the public, such as cancer research and heart diseases, for free but also provide donations in both monetary and in-kind forms. Auditing firms regularly pay taxes on time, create jobs, recruit annually, and basically provide value-added services to the economy and financial community, through their high-quality audits. Table 5 presents the integrated ideas related to the corporate ethics element, measuring the firm’s performance in relation to the society and/or community (Tsamenyi et al., 2010).

Proposed Measures for the BSC Corporate Ethics Perspective.

Note. BSC = balanced scorecard.

Auditors’ Perceptions of the BSC—Findings and Discussion

This section examines auditors’ perceptions regarding the proposed BSC for auditing firms and its possible impact on the performance of the audit work. It also provides evidence related to the two RQs and hypotheses through a questionnaire. Respondents were required to rank the five perspectives using an increasing numeric scale.

Descriptive Statistical Analysis

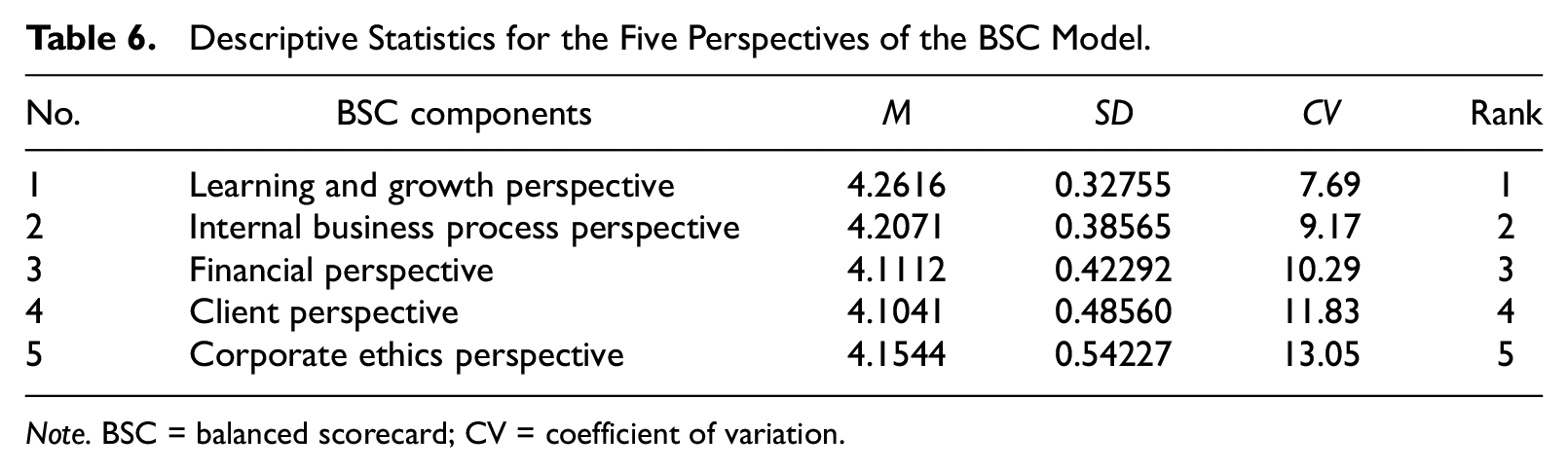

Table 6 shows the significance of the five components of the proposed BSC from the auditors’ perspectives, with a mean that is greater than 4. It also provides a rank for the five dimensions of the proposed model where auditors ranked the learning and growth perspective highest, followed by internal business process and financial perspective, then client perspective, and finally corporate ethics perspective. The analysis also provided a rank for the different measures (variables) within each perspective according to coefficient of variation (CV) percentage. The lower the value of the coefficient of variation, the more precise the estimate, and vice versa.

Descriptive Statistics for the Five Perspectives of the BSC Model.

Note. BSC = balanced scorecard; CV = coefficient of variation.

More detailed analysis of the measures forming each of the components of the proposed BSC is presented in the following sections.

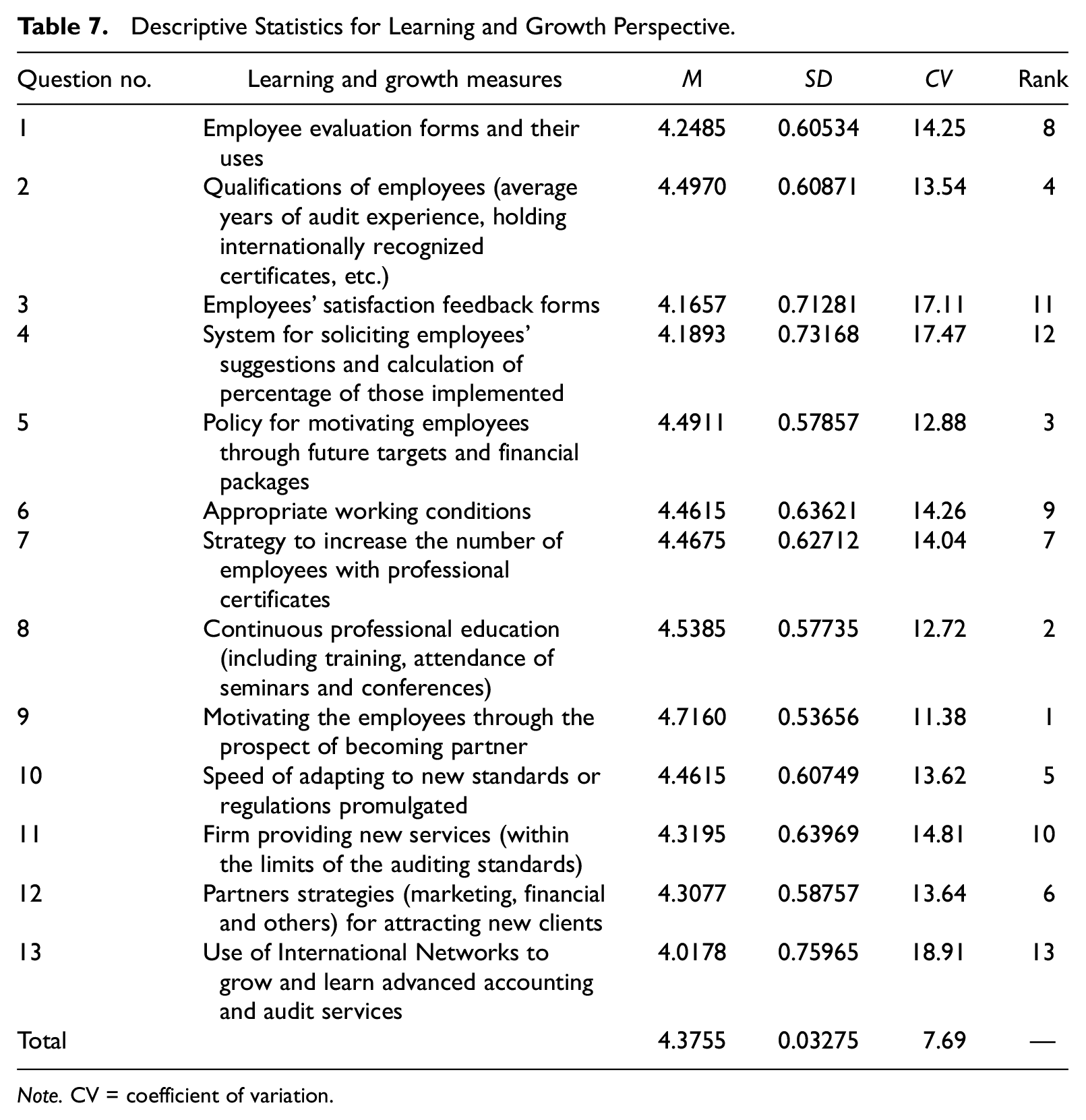

Learning and growth

According to the descriptive statistics in Table 7, the most three homogeneous variables are: Motivating the employees through the prospect of becoming a partner, continuous professional education (CPE), and the policy for motivating employees through future targets and financial packages. These results show that motivating the audit firm’s employees form the most important measure for any business success whether in an industrial, service, or not-for-profit organization

Descriptive Statistics for Learning and Growth Perspective.

Note. CV = coefficient of variation.

However, the most three heterogeneous variables of the learning and growth perspective are: Employee satisfaction feedback forms, systems for soliciting employee suggestions and percentage calculations of those implemented, and the use of International Networks to grow and learn advanced accounting and audit services. It seems that most respondents, mainly auditors and seniors, are not interested in these measures as they may not have access to such information. Also, auditors are reluctant to put significant weight on the above measures to minimize the risk of a possible sudden decrease in their remunerations and incentives in situations, where systems for soliciting employees’ suggestions and then calculating the percentage of those implemented, are not achieved.

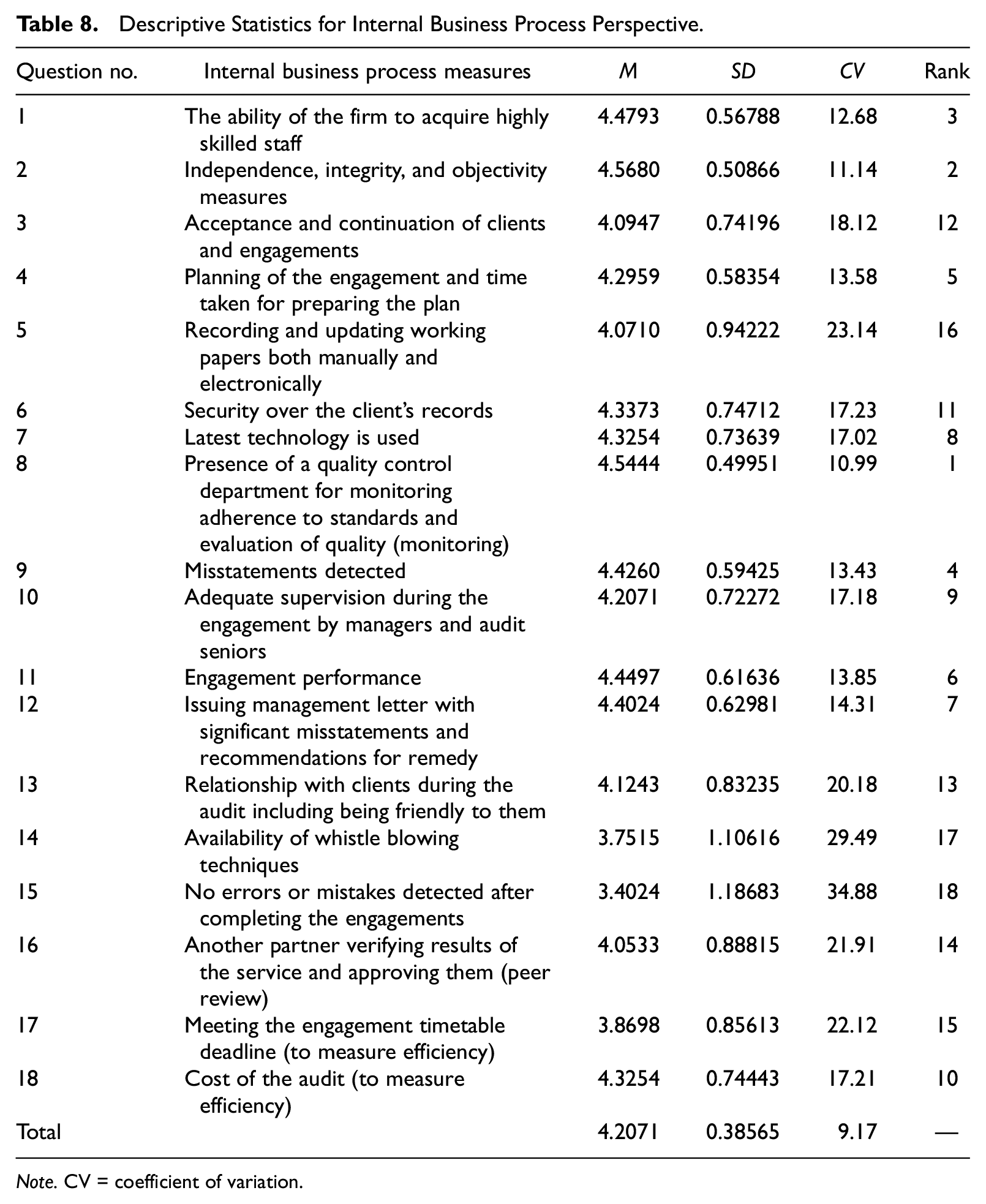

Internal business process

According to the descriptive statistics presented in Table 8, the most three homogeneous variables include: The presence of a quality control department for monitoring adherence to standards and evaluation of quality (monitoring); independence, integrity, and objectivity measures; and the ability of the firm to acquire highly skilled staff. These results confirm the trend in the accounting and auditing literature, within academia and practitioners about the importance of quality control in providing auditing services, as well as the ethical behavior of auditors at all levels in every audit firm. The qualifications, experience, and continuous training of the audit staff in a professional firm are considered vital elements in the internal business process of any BSC.

Descriptive Statistics for Internal Business Process Perspective.

Note. CV = coefficient of variation.

However, the most three heterogeneous variables found are: The errors or mistakes detected after completing engagements, availability of whistleblowing techniques, and recording and updating working papers both manually and electronically. The results show the unawareness of the respondents for the need to have a good follow-up process after the completion of the audit to ensure its proper documentation and the review of the results achieved. As to the whistleblowing tool, the Egyptian culture is lacking the notion of transparency and full disclosure as respondents still believe that it is an unethical behavior if one complained about a deficiency or unethical conduct made by one of his colleagues.

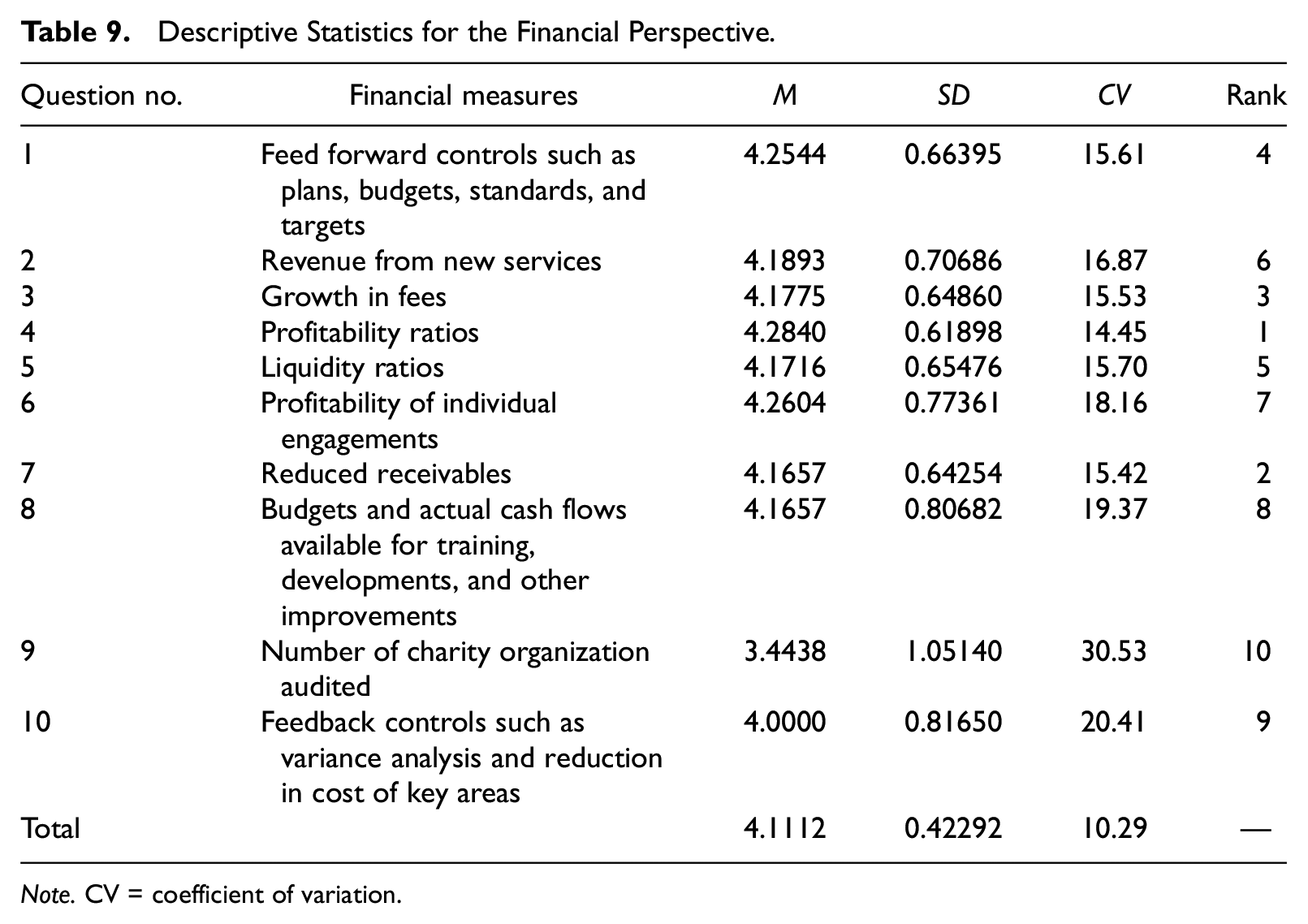

Financial perspective

Table 9 illustrates that the most three homogeneous variables found are: profitability ratios, reduced receivables, and growth in fees. These results follow the measures required for a successful business, with profitability and liquidity seen as the most significant financial measures. Audit firms need a continuous flow of cash represented in their audit and other service fees to develop the firms’ internal processes including IT audit, backup databases, CPE for its staff, better-automated information, and filling systems.

Descriptive Statistics for the Financial Perspective.

Note. CV = coefficient of variation.

However, the most three heterogeneous variables are: the number of charity organizations audited; feedback controls such as variance analysis and reduction in cost of key areas, budgets and actual cash flows available for training; and developments and improvements. A possible interpretation of the results is that respondents believe that the number of charities audited, and the payment of taxes and cash flows are a by-product of audit firms, which are mainly concerned with making adequate profits and secure liquidity.

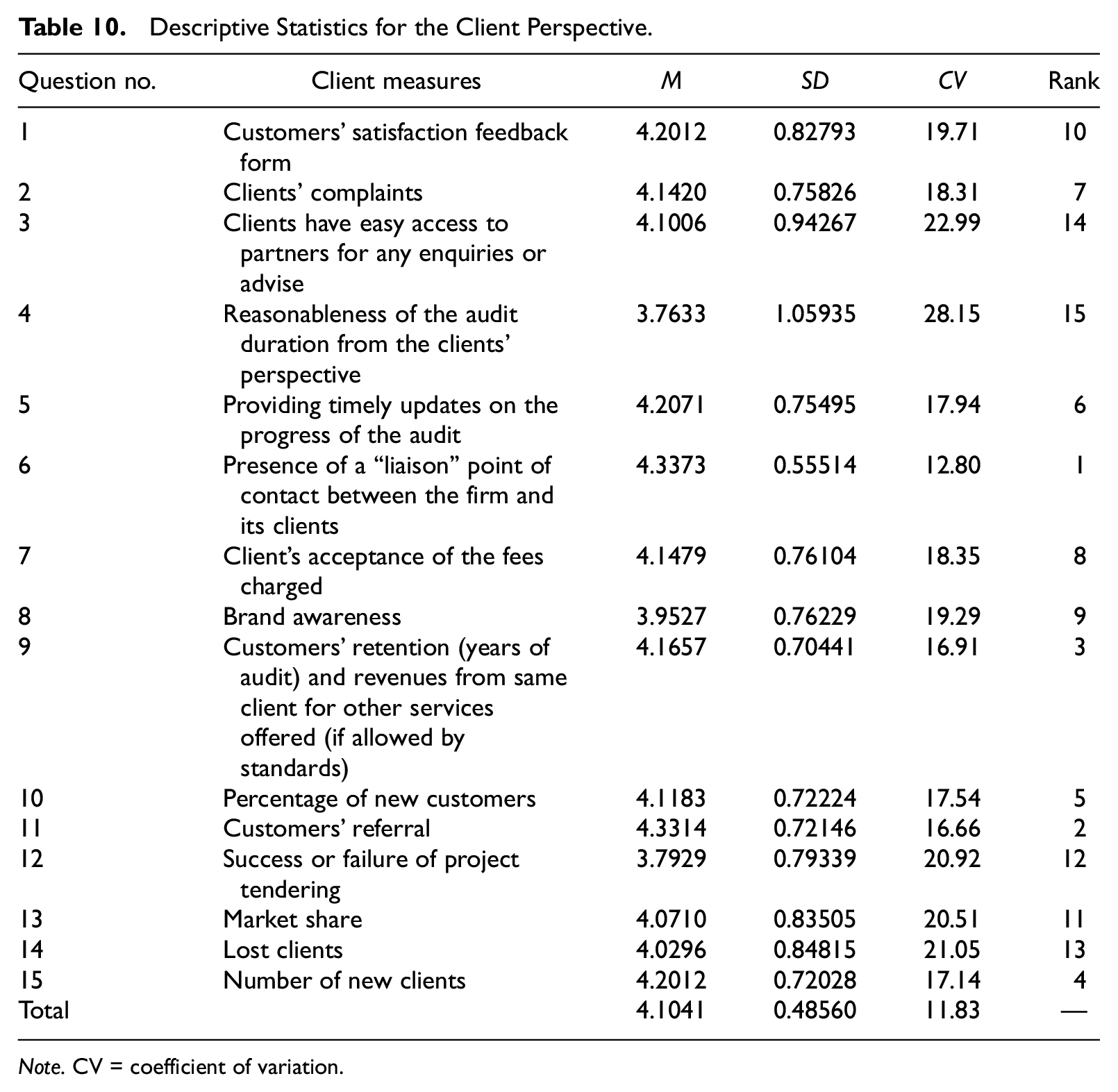

Client perspective

The results in Table 10 illustrate the most three homogeneous variables: Presence of a “liaison” point of contact between the firm and the client, customer referral and customer retention, and revenues from the same client for other services offered. Partners can identify deficiencies in the provision of the audit services by listening to management’s complaints and responding with corrective actions. Customers’ referrals include acquiring clients through words of mouth “good reputation,” marketing, and other media campaigns. The retention of a client would require great efforts by partners in charge such as providing high-quality services, allocating qualified and experienced staff, providing quick responses to clients’ inquiries, and tendering fair fees for audit engagements.

Descriptive Statistics for the Client Perspective.

Note. CV = coefficient of variation.

However, the most three heterogeneous variables are: the reasonableness of the audit duration from the clients’ perspective, clients having easy access to partners for any inquiries or advice, and lost clients. Again, the respondents assessed the measures of the client’s perspective from their own interest and benefits. They ignored the importance of some of the above measures which are considered essential for the retention of existing clients and acquiring new clients.

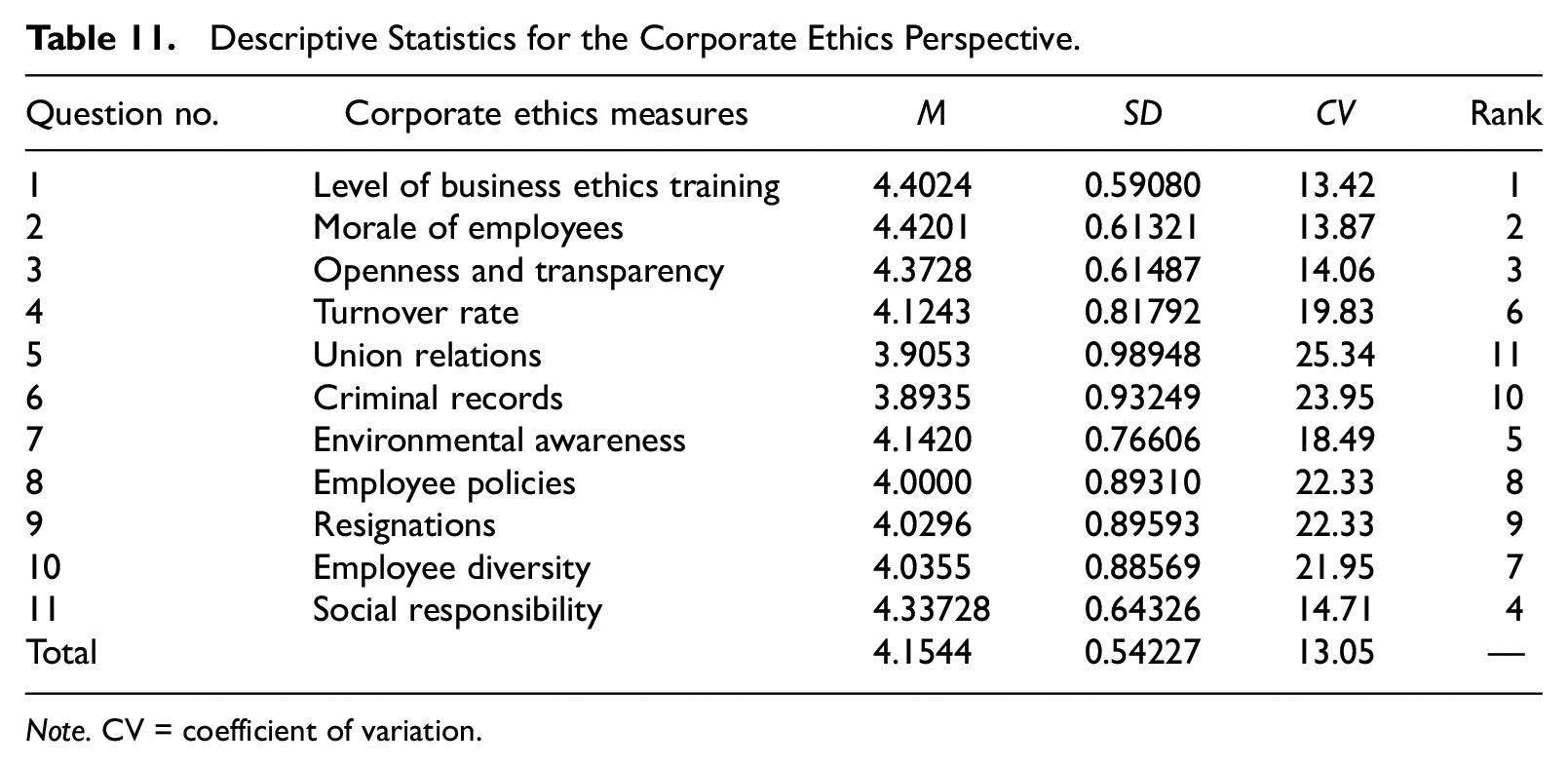

Corporate ethics

Table 11 shows that the most three homogeneous variables are: the level of business ethics training, morale of employees and openness, and transparency. Such findings show the awareness of the partners, seniors, and auditors of the importance of ethical training for all members of an audit firm, as well as the need for complete transparency and openness in the presentation of the audit results to internal and external parties. The dishonesty in the provision of the audit services may affect the employees’ morale and make them disinterested in putting efforts and time in performing their audit responsibilities. This might be due to the uncertainty in the employees’ beliefs that their findings would not be presented to shareholders and those responsible for governance.

Descriptive Statistics for the Corporate Ethics Perspective.

Note. CV = coefficient of variation.

However, the most three heterogeneous variables found are: union relations, criminal records, and employee policies or resignations. The Egyptian culture, as an example of an emerging economy, remains different to that in developed countries in terms of acknowledging the importance of union relations and their ability to apply organized strikes to seek the interests of business employees (Samaha & Hegazy, 2010). This element is viewed by respondents as not significantly affecting the corporate ethics perspective. At the same time, criminal records are considered not acceptable by respondents, hence it is rare to find an employee in an audit firm with any current or previous criminal record. Maintaining integrity and honesty in the audit remains crucial.

To sum up, the results of the descriptive statistical analysis provide evidence in support of the first hypothesis indicating that the proposed BSC is a viable technique to be used in auditing firms if the five perspectives are used to measure the performance of the audit tasks. Finally, the respondents’ answers’ means are found to be over 4 while the analysis also provided a rank for the different measures (variables) within each perspective.

Pearson Correlation and CFA

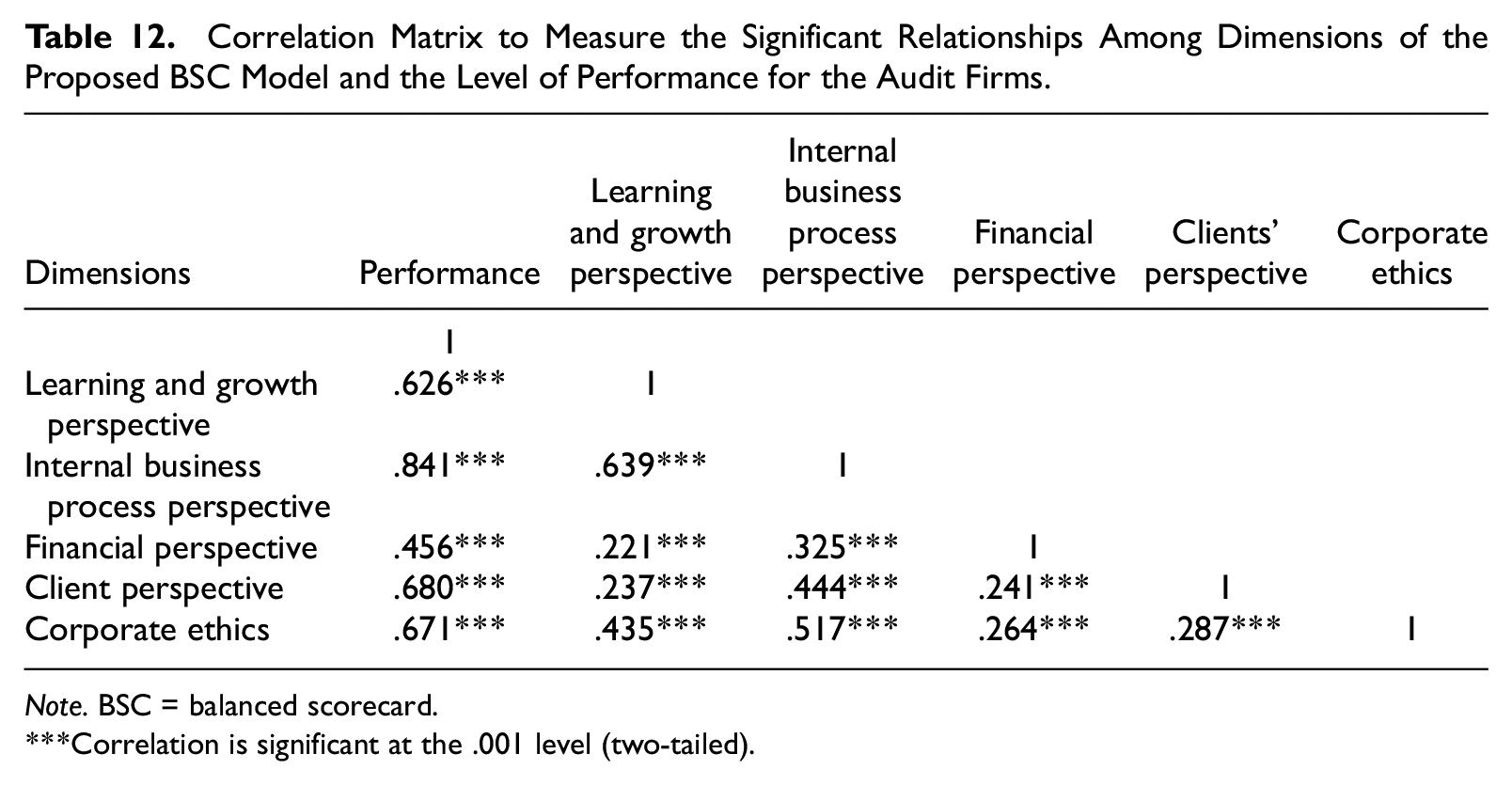

To test the most significant dimensions of the proposed BSC model that affect the level of performance for auditing firms, the researchers used the following two statistical techniques: The Pearson correlation matrix to assess the significant relationships among dimensions of the BSC model and the level of performance for the auditing firms, and the CFA technique to explore the most significant dimensions of the BSC model that affect such performance.

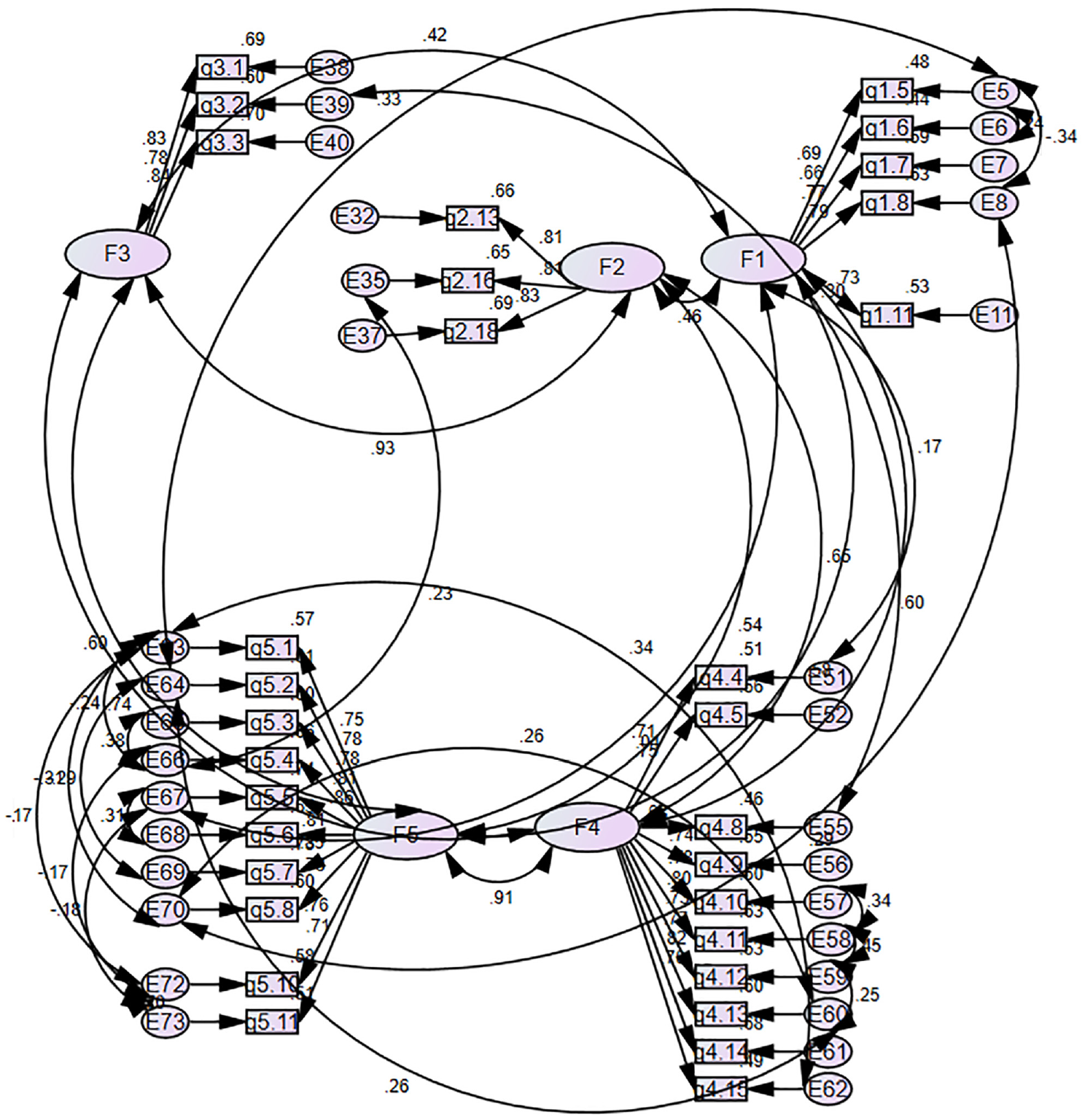

According to the correlation matrix results shown in Table 12, there is a significant positive linear relationship among the dimensions of the BSC model and the level of performance of auditing firms at a significant less than .001 level. At the same time, the CFA was first conducted to test how well the measured variables represent the constructs. When the CFA results are combined with construct validity tests, it can provide a better understanding of the quality of their measures. The model fit is assessed in terms of alternative indices and is satisfactory if comparative fit index (CFI) > 0.90, goodness-of-fit index (GFI) > 0.90, and root mean square residual approximation (RMSEA) < 0.10 (Hair et al., 2010). The researchers conducted both initial CFA and final CFA with the fit measured variables representing the constructs as follows.

Correlation Matrix to Measure the Significant Relationships Among Dimensions of the Proposed BSC Model and the Level of Performance for the Audit Firms.

Note. BSC = balanced scorecard.

Correlation is significant at the .001 level (two-tailed).

CFA for Research Constructs

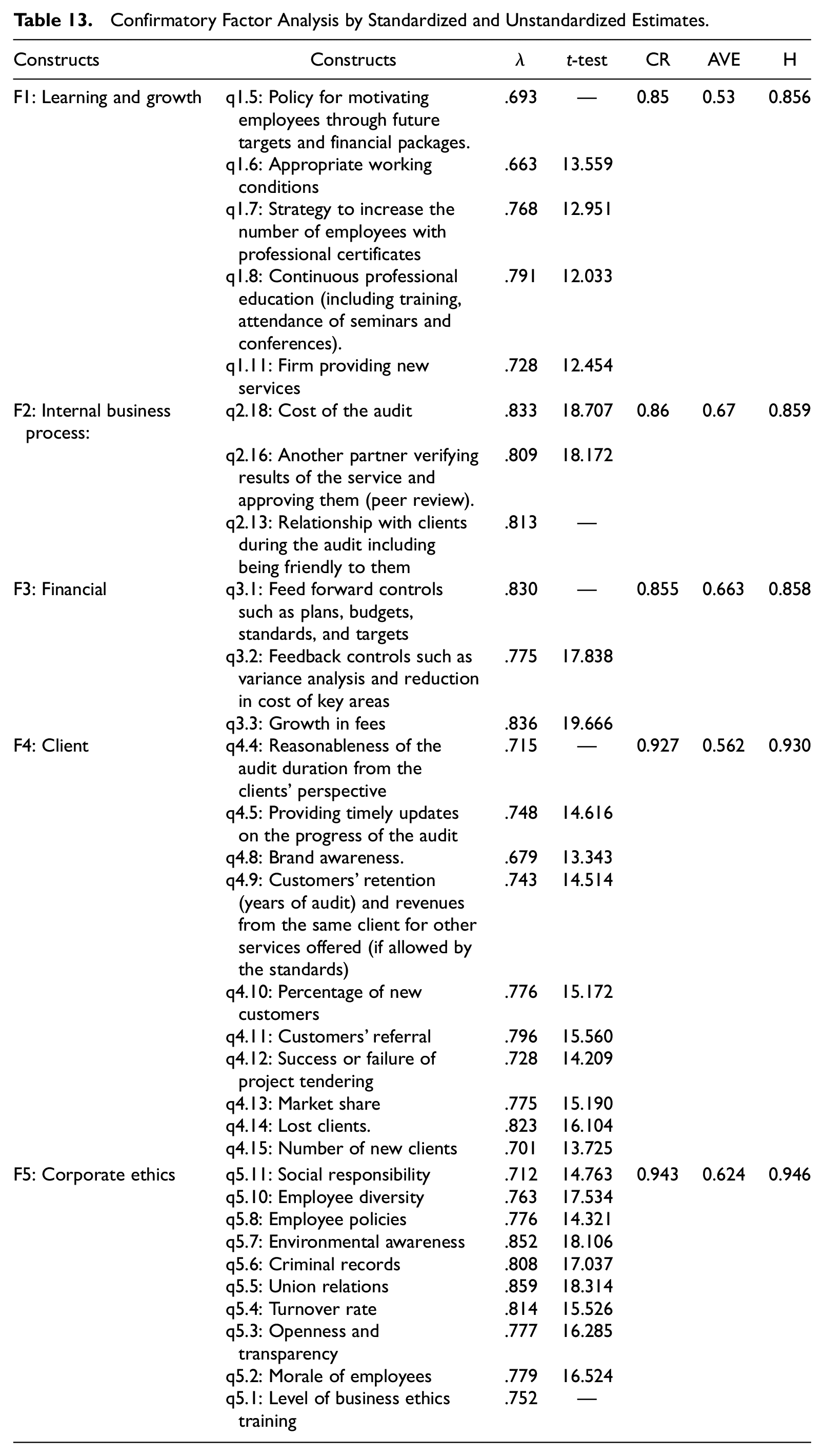

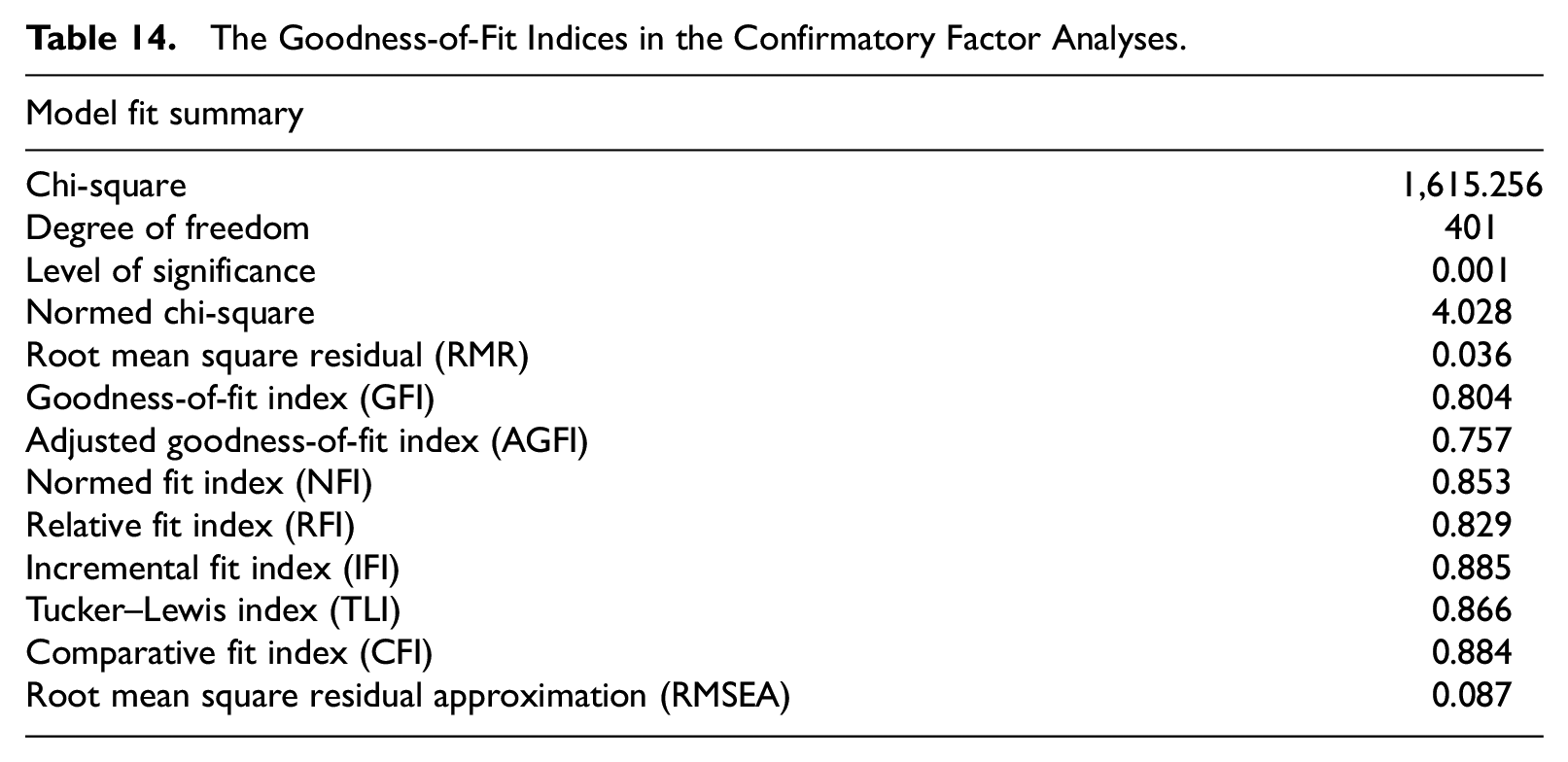

The CFA was used to test how well the constructs are represented by the variables. The main strength of the factor analysis is that it enables the researchers to assess the importance of the variables in the proposed model and indicates the most important variables within each construct. When the results of the CFA are to be combined with both discriminant and validity tests, the researchers can get a better understanding of the quality of model measures. The construct validity is the extent to which the constructs are measured by the set of measured items. The model fit is measured in terms of 10 indices: normed chi-square with cut-off values less than 5, GFI, adjusted goodness-of-fit index (AGFI), normed fit index (NFI), relative fit index (RFI), incremental fit index (IFI), Tucker–Lewis index (TLI), CFI, RMSEA, root mean square residual (RMR). The average variance extracted with cut-off values greater than .5, and the square root of the AVE of each construct should be much larger than the correlation coefficient of the specific construct with any of the other constructs (Fornell & Larcker, 1981). A model is considered satisfactory if CFI > 0.95, GFI > 0.90, and RMSEA < 0.10 (Hair et al., 2010). The researcher conducted the final CFA with the fit measured variables representing the constructs for 10 antecedents.

Based on the findings shown in Figure 1 and Table 13, the researchers conclude the following: First, all standardized regression weights (factor loading) are greater than 0.50, which means that all measured variables, are statistically significant, that is, the measured variables represent the constructs. Second, the t-tests for all measured variables is significant at a level of significance less than .001, showing the importance of the observed variables in measuring the impact of constructs on the performance of the audit firms. Because of squared multiple correlations (i.e., average variance extracted for the variables), all the variables that have less than .50 were excluded from the model constructs. The Composite Reliability (CR) values are greater than 0.70 which indicates that the variables did converge at some point (Hair et al., 2010). Average Variance Extracted (AVE) of all the constructs of the proposed model; Learning and growth perspective, Internal business process perspective, Financial perspective, Clients’ perspective, and Corporate Ethics turned out to be larger than the cut-off values (0.50). Because of these results, the average variance extracted for all latent constructs is 0.6098, and this indicates that the latent variables had a high convergent validity (Fornell & Larcker, 1981; Hair et al., 2014).

The initial confirmatory factor analysis for a measurement model.

Confirmatory Factor Analysis by Standardized and Unstandardized Estimates.

Referring to Tables 7 to 11, which included the main measures proposed by the researchers for each construct of the model, however, it can be noted from Table 13 that the measures approved by the CFA are the most homogeneous measures for each of the perspectives resulting in the highest consistency in enhancing the performance of the auditing firms (second hypothesis). The other variables had been excluded by the analysis because their existence impairs the overall performance of the auditing firms and can affect the collective effect of the other variables. The first hypothesis had been verified through selection of the valid measures within each of the perspectives, which had been compared with the previous measures used in other service companies. Their differences support the results of hypothesis 1. Recently, it has been proposed to use the Heterotrait–monotrait ratio of the correlations (HTMT) approach to assess discriminant validity (Henseler et al., 2015). Table 13 shows that the HTMT ratio is less than 0.90, which means the latent variables had a high discriminant validity.

Measuring the Goodness of Fit of the (CFA) Model

From Table 14, the study confirms the following results: First, all the goodness-of-fit tests of the model showed significant results (i.e., most indicators at acceptable limits or near to cut-off values, and then the possibility of matching the actual form of the model estimated). Second, the values of RMR and RMSEA are less than 0.08, which indicates a close fit of the model in relation to the degrees of freedom. Third, the mean variance extracted for all latent constructs is .6098, that is, there is adequate convergent validity. Fourth, the average variance extracted for the constructs of learning and growth perspective, internal business process, financial perspective, client perspective, and corporate ethics are .53, .67, .663, .562, and .624, respectively. This indicates that there is a highly internal consistency based on the average inter-item correlation. AVEs of all scales turned out to be more than the cut-off values. Overall, the evidence of a good model fit, reliability, and convergent validity indicates that the measurements within the model are valid with a level of significance .001. The values of the CFA provide support for the viability of the model to be used in the auditing firms.

The Goodness-of-Fit Indices in the Confirmatory Factor Analyses.

As to the effect of the above analysis on the research hypotheses, the results provide partial support for H1 related to the components of the BSC for auditing firms. This was evidenced in the results of the descriptive statistics through the consensus of the respondents on the measures proposed by the researchers for the BSC. Also, the use of the correlation matrix (Pearson correlation) indicated the significant relationships among the various perspectives with their related measures and the level of the performance of auditing firms. The CFA added a new dimension to the results where it identified the impact of each of the measures within the BSC’s each perspective and eliminated the least significant measures. Finally, as to H2, the results indicated that the variables representing the BSC measures explain (59.66%) from total variation of dependent variables; the performance of the auditing firms and the rest due to either the random error in the regression model or other independent variables were excluded from the regression model.

Conclusion

This article developed and empirically examined a BSC for audit firms. The development of the BSC was based on the review of the literature for similar BSCs in service industries and interviews made in two audit firms and with academics from reputable universities in Egypt. A survey was conducted to evaluate the perspectives and measures included in the BSC. The validation process indicates that the learning and growth perspective is the most critical perspective with the client and the internal process ranked as the next most critical. The respondents indicated that the least critical perspective is the financial perspective.

Several findings emerged from this research study. First, the results show that auditors place more emphasis on qualitative measures such as learning and growth, including motivation and continuous professional education and internal business processes, such as the presence of a quality control department and the ability to acquire skilled staff, rather than the financial measures in assessing their firms’ performance. Second, regulations and the requirements for compliance with auditing standards place pressure on partners and employees to satisfy those standards first before they start considering their customers’ satisfaction and financials. However, most of the respondents to the study’s questionnaire confirmed the importance of the use of nonfinancial measures in the proposed BSC. Third, the study shows that audit firms wish to design and implement detailed structures including procedures and policies to assess their performance including customers’ satisfaction, employees’ motivation, corporate ethics, and their financial achievements. Checklists, questionnaires, and direct communication are considered the most important tools used to assess the performance. Fourth, the analysis of the auditors’ perceptions of the BSC for audit firms confirms the importance of employees’ motivations through fair remuneration, appropriate promotion, and continued professional education. Employees were not interested to acquire information about the growth in the firm’s revenues and profitability, but were more concerned about how to achieve the quality of their audit work and get compensated for such performance. The findings are broadly consistent with those presented by other researchers who have attempted to analyze the diverse range of interrelated factors associated with performance evaluation (Lee et al., 2001).

There is strong evidence that the success of business organizations, particularly service organizations, is still in a developmental phase. Future research may develop an overall index to capture the contribution of each measure to overall performance. Also, a BSC requires considerable amount of time and money for an effective implementation, therefore firms should assess the objectives and measures of applying a BSC considering the available resources and budgets before gradually introducing required modifications to their performance measurement systems. Moreover, reasons for the auditing profession’s heavy reliance on nonfinancial rather than financial measures as suggested by the literature and the current research, should be more thoroughly investigated perhaps by undertaking comparable studies within different industries in various economies. Finally, as the validation of the BSC model was made in two audit firms based on a case study, a wider application of the model should be undertaken within a larger sample of audit firms.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.