Abstract

Recent literature highlights the importance of providing citizens public sector accounting education to help them become public finance literate. This study performs a questionnaire-based survey to a convenient sample of citizens to collect their perspective on the topic. The results indicate an average familiarity of the respondents with key public finance concepts, with male respondents appearing more familiar. The respondents place more importance in being able to monitor and assess the state’s financial performance and condition rather than that of the local government. In practice, when making voting decisions during municipal elections they focus less on financial information, compared to when it comes to state elections, mainly due to difficulties in accessing the municipalities’ financial information. The respondents are further supportive of receiving public sector accounting education as they believe it could help them monitor the local and state government’s financial condition and performance, take more rational election decisions and more actively participate to public matters. They perceive that such an education should take place from high-school and not earlier, and they find useful this educational process to continue via online and on-site seminars. Finally, they make recommendations on the specific content (learning objectives) of public sector accounting education at the different educational levels (school, high-school, municipal seminars, and online seminars).

Keywords

Introduction

Citizens are in need of financial and non-financial information related to the state and local government to make informed public-related decisions (Brusca and Montesinos, 2006; Cohen and Karatzimas, 2015). Public sector accounting standard setting boards perceive citizens as one of the most important groups of users (GASB, 1987; CICA, 2009; AASB, 2009; IPSASB, 2013) and there is an ongoing debate on identifying their main information needs that should be satisfied (Brusca and Montesinos, 2006; Van Helden and Reichard, 2019; Kang et al., 2022).

In this realm governments try to be more accountable to citizens with the provision of relevant information (Monfardini, 2010). Some jurisdictions have further employed popular financial reports to provide a more easily understood information experience to non-accounting savvy citizens (Yusuf et al., 2013). Nevertheless, even if these citizen information needs are satisfied through the adequate provision of information, it is not certain that citizens can actually make use of this information, since the average citizen is illiterate in public finance issues (Karatzimas, 2020). One wonders whether the provision of relevant knowledge through specific education on public finance could help the average citizen make use of this information. Recent literature (Allen, 2013; Karatzimas 2020, 2021) has highlighted the importance of the provision of such education to citizens to create public finance (or government accounting) literate 1 citizens. In particular, government accounting literacy refers to citizens possessing the appropriate level of public sector accounting knowledge and understanding that could help them reach a state of being able to evaluate and monitor public administrations and inform their public-related decisions (Karatzimas, 2020). As such it differs from the concept of financial literacy, but appears complementary to the context of tax literacy (Nichita et al., 2019; De Clercq, 2021).

Scope of this study is to record citizens’ perceptions on the usefulness of public finance information and on the possibility of receiving relevant education. For the purposes of the study a questionnaire-based survey to a convenient sample of citizens is performed. The originally developed questionnaire starts by evaluating the respondents’ rate of familiarity with key public sector accounting/public finance concepts (e.g. public debt; accountability; budget) to introduce the participants of the study to the conceptual boundaries of the topic, and to actually evaluate their familiarity with key concepts. Then a set of questions addresses the importance of being able to monitor and assess local and state government financial performance and condition, the impact from receiving PSA education to citizens’ public-related decision-making, as well as the role, context and content of such education in different educational levels. The interest of the study lies in the fact that it is –to the best of our knowledge-the first questionnaire-based survey that holistically approaches citizens’ perception on the important issue of public finance literacy, starting from familiarity level to conclude with learning objectives’ suggestions. So far the topic has been addressed either theoretically (e.g. Karatzimas, 2020, 2021) or with the provision of educational insights (Allen, 2013), but it deserves further investigation as it touches upon issues of outmost importance that range from increased democratic participation to improved public value generation.

The results indicate average familiarity with key public finance concepts, with male respondents appearing more familiar. The sample finds it more important to be able to monitor and assess the state’s financial performance and condition rather than the local governments’. When making voting decisions during municipal elections they focus less on financial information, compared to when it comes to state elections. Difficulties in assessing the municipalities’ financial information as well as ideological reasons being the most important reasons why. The respondents further find that receiving public sector accounting education (PSAE) could help them monitor the local and state government’s financial progress and financial performance, take more rational election decisions and more actively participate to public matters. Furthermore they perceive that such an education should take place from high school and not earlier, and they find useful this educational process to continue via online and on-site seminars. Finally, they make recommendations on the specific content (learning objectives) of public sector accounting education at the different educational levels (school, high school, municipal seminars, and online seminars).

The paper proceeds as follows: the following Section provides a review of the relevant literature. Section 3 presents the methodological approach and Sec. 4 the results from the responses analysis. Finally Sec. 5 concludes with a discussion and concluding remarks.

Literature review

Citizens have a central role in democracies and their relationship with governments should be of outmost importance (Kymlicka and Norman, 1994; Barton, 2011). In this context, citizens require timely information from central and local governments -and other public entities-to constantly inform their decision-making (Vanhommerig and Karré, 2014). In practice though, this is not always the case (Denhardt and Denhardt, 2009; Citrin and Stoker, 2018). To rebuilt trust between these governments and citizens accountability measures have been established (Beshi and Kaur, 2020; Gordon, 2000). In this realm financial reporting of public entities is considered a basic means of being accountable to citizens (Patton, 1992; Mack and Ryan, 2006), and citizens are officially considered important users of financial information for decision-making purposes (GASB, 1987; CICA, 2009; AASB, 2009; IPSASB, 2013). A lot of discussion however has been dedicated to the actual use of this information by citizens, due to the difficulties faced in understanding it by the–usually not accounting expert-average citizen (Cohen et al., 2017). Moreover, difficulties in having access to this information have been recorded (Jordan et al., 2016). Public trust could be eroded if state and local government financial information is not readily consumable by citizens, given the importance of this information for citizens (Waymire et al., 2015). Popular financial reports have been proposed as a way to tackle this problem, but then the presented information could be subjective and biased (Cohen and Karatzimas, 2015). Moreover, the average citizen could still face difficulties in understanding all the information as long as they remain illiterate on such issues (Karatzimas, 2020).

Another proposed approach is to educate citizens in public finance and accounting issues to make them capable of understanding this information. Relevant literature (Thomas, 1990; Allen, 2013; Jordan et al., 2016; Karatzimas, 2020, 2021) suggests that some accounting education to citizens could enable citizens’ engagement in decision-making and governance. Over and above, the concept of government accounting or public finance literacy promotes an education plan the introduces public finance courses to citizens at as early as primary school level to create a new citizen culture/mentality that would make them able to understand, monitor and evaluate local and central government finance issues which are directly linked to citizens’ well-being (Karatzimas, 2020). Allen (2013) considers informed citizens to be in a better position to demand changes that would improve a nation’s financial position, and calls for the public’s education on issues such as national debt and government spending. In the same realm, Karatzimas (2020) argues that the provision of a targeted public sector accounting education to citizens could have beneficial effects in citizens’ willingness to actively engage and participate in public matters, as for instance elections, referendums and participatory budgeting. It has been further argued that as such literacy could inspire active engagement this could also prove beneficial to co-design initiatives that could ultimately lead to public value generation (Karatzimas, 2021).

The concept of citizens’ government accounting literacy has not been explored so far from the perspective of citizens. In this paper, through a questionnaire-based survey, the actual preferences and perspective of a sample of citizens in the above topics is analyzed. Moreover, the different point of view of citizens due to different age, status and familiarity with accounting is explored.

Methodological approach

This study uses a questionnaire based survey to collect citizens’ perceptions on government accounting literacy. The survey took place in Greece, and uses a convenient sample to get a wider inclusion of citizens of a different age, educational level, occupation, etc. Convenient sampling is ideal when the target population is defined in terms of a very broad category (Alvi, 2016). The questionnaire has been administered online. Eventually 260 citizens participated in the survey.

Overall there are three research questions the study tries to answer: RQ1: Do citizens find public finance information useful? RQ2: Do citizens use public finance information when making voting decisions? RQ3: How do citizens perceive the possibility of receiving public finance education at different contexts?

To move on with the questionnaire at first the respondents had to rate their level of familiarity with specific key accounting terms and concepts, that introduced them to the topic.

Although the survey is intended for wider applicability, since it is firstly applied in Greece it would be useful to briefly provide some information of the country’s context which could partially explain some of the respondents’ answers. 2 Greece is a European Union member-state hardly hit by the international financial crisis of 2008 that led the country to the financial assistance of ‘the Troika’ (i.e. the European Commission, the International Monetary Fund and the European Central Bank). Due to the country’s dire financial condition, that was worsened by the –at that time-political instability, Greece had to sign three succeeding memoranda of understanding (MoU) with the international lenders the first being signed in 2010 (Cohen and Karatzimas, 2022). These MoUs were accompanied by conditionality terms related to specific reforms in both the public and private sector; the financial assistance was provided upon the satisfaction of these conditions. During this period there were notable reforms for the public sector financial management like the introduction of the Medium-Term Fiscal Strategy and the accounting framework for the General Government (Cohen and Karatzimas, 2022). Although the Greek government became more transparent, there have not been any changes in reporting for citizens. Eventually, in 2018 the country completed its obligations and returned to normality. This questionnaire survey took place during the second year of the COVID-19 pandemic. Moreover, it is important to note that local governments in Greece do not publish a popular financial report, neither is participatory budgeting widely promoted.

The sample

From the 260 respondents, 132 (50.8%) are female and 128 (49.2%) male. The age of the respondents varies, with the majority (N = 95; 36.5%) being between 18-25 years old, 71 (27.3%) between 36-45 years old, 35 (13.5%) between 26–35 and 46–55, 18 respondents (6.9%) between 56–65, and 6 (2.3%) over 66 years old.113 (43.5%) of the respondents are HEI students, 59 (22.7%) are public servants, 48 (18.5%) private sector employees, 18 (6.9%) self-occupied, 15 (5.8%) academics and 7 (2.7%) retired. As regards the education level, 97 respondents (36.2%) have a bachelor’s degree from a HEI, 94 (36.2%) have a master, 43 (16.5%) are high school graduates and 26 (10%) hold a PhD. Finally, 182 (70%) of the respondents consider themselves familiar with accounting, while 78 (30%) do not, and 92 (35.4%) are also familiar with public sector accounting while 168 (64.6%) are not.

Results

Familiarity with, perceived importance and use of public finance information

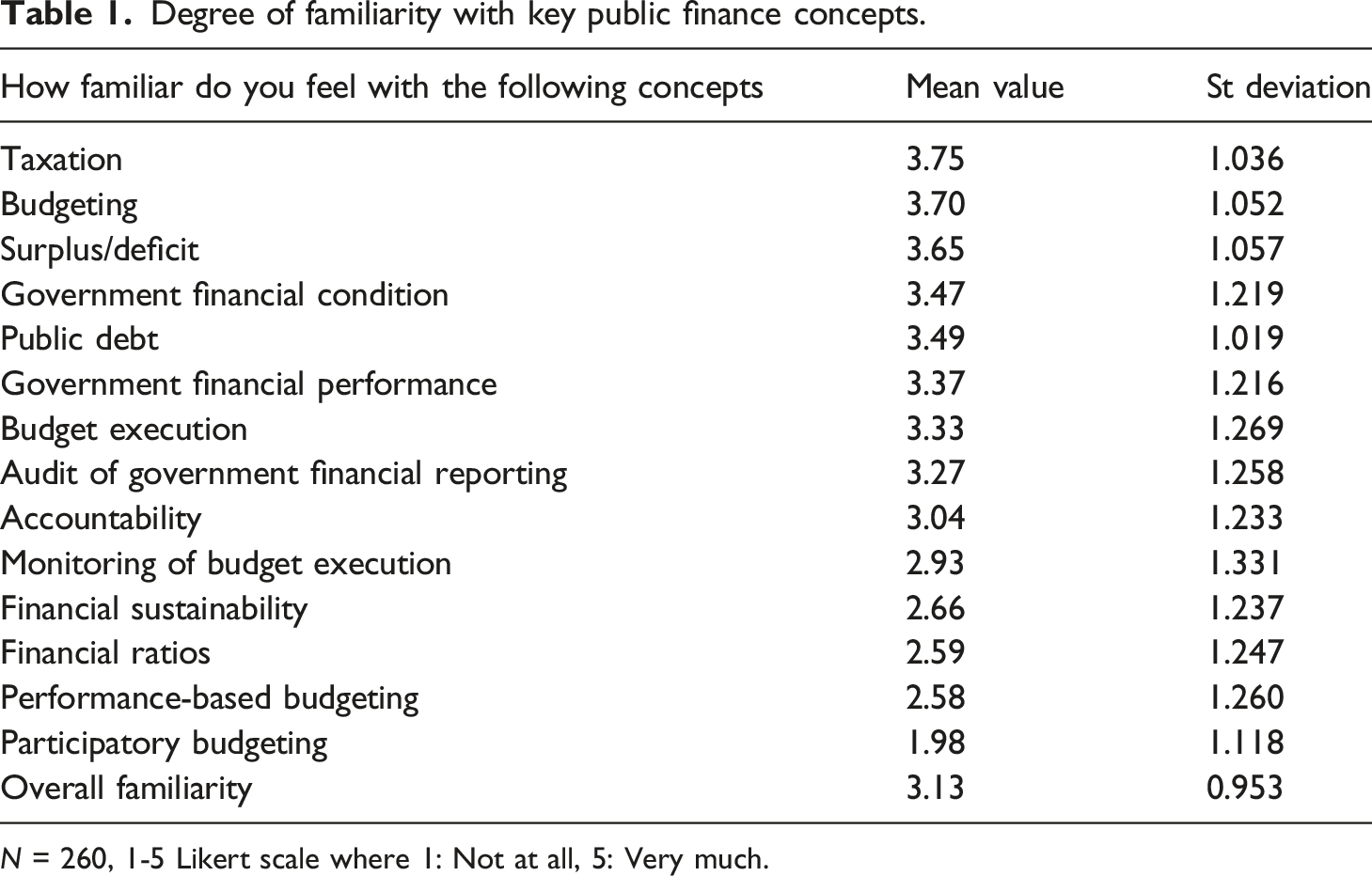

Degree of familiarity with key public finance concepts.

N = 260, 1-5 Likert scale where 1: Not at all, 5: Very much.

It appears that the relevant concepts where respondents feel to an extent familiar include taxation, budgeting, surplus/deficit, public debt, financial condition and performance, while they do not appear familiar with participatory budgeting, performance-based budgeting, financial sustainability and financial ratios. By combining the above items into one variable to evaluate the overall familiarity level of the sample, the mean value is 3.13 (st. deviation: 0.953) indicating an average familiarity with public finance concepts that statistically significantly differs from the average value of 3 (t-test p-value = 0.000).

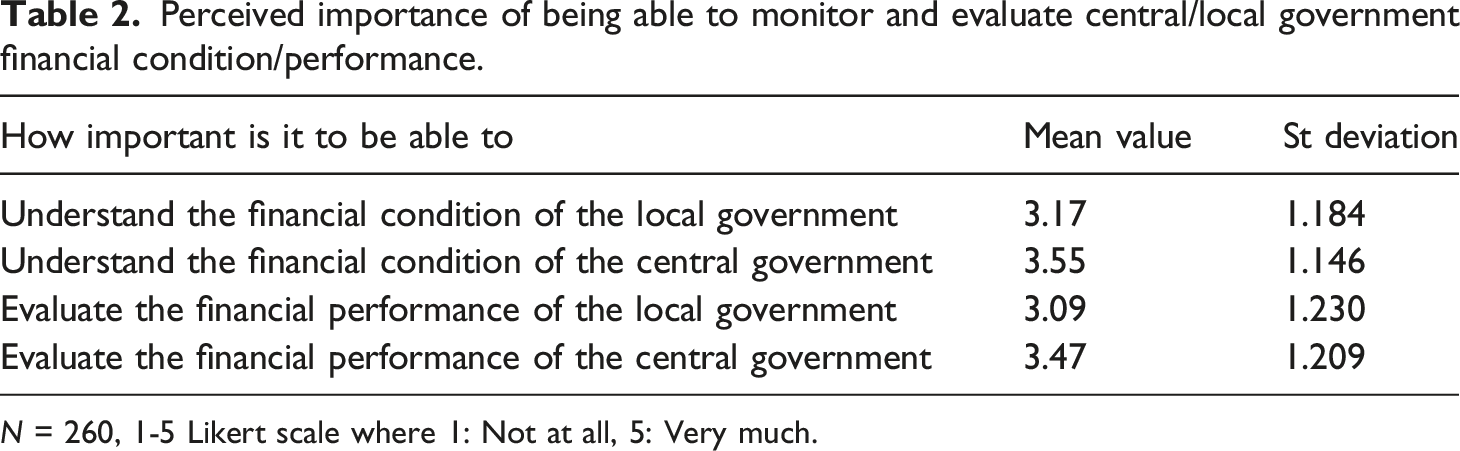

Perceived importance of being able to monitor and evaluate central/local government financial condition/performance.

N = 260, 1-5 Likert scale where 1: Not at all, 5: Very much.

The overall familiarity variable appears significantly correlated (pearson chi-square p-values: 0.000) with the perceived significance of being able to understand the financial condition of both central and local government as well as of being able to evaluate their performance. This indicates that the more familiar with public finance concepts the more important the above aspects are perceived.

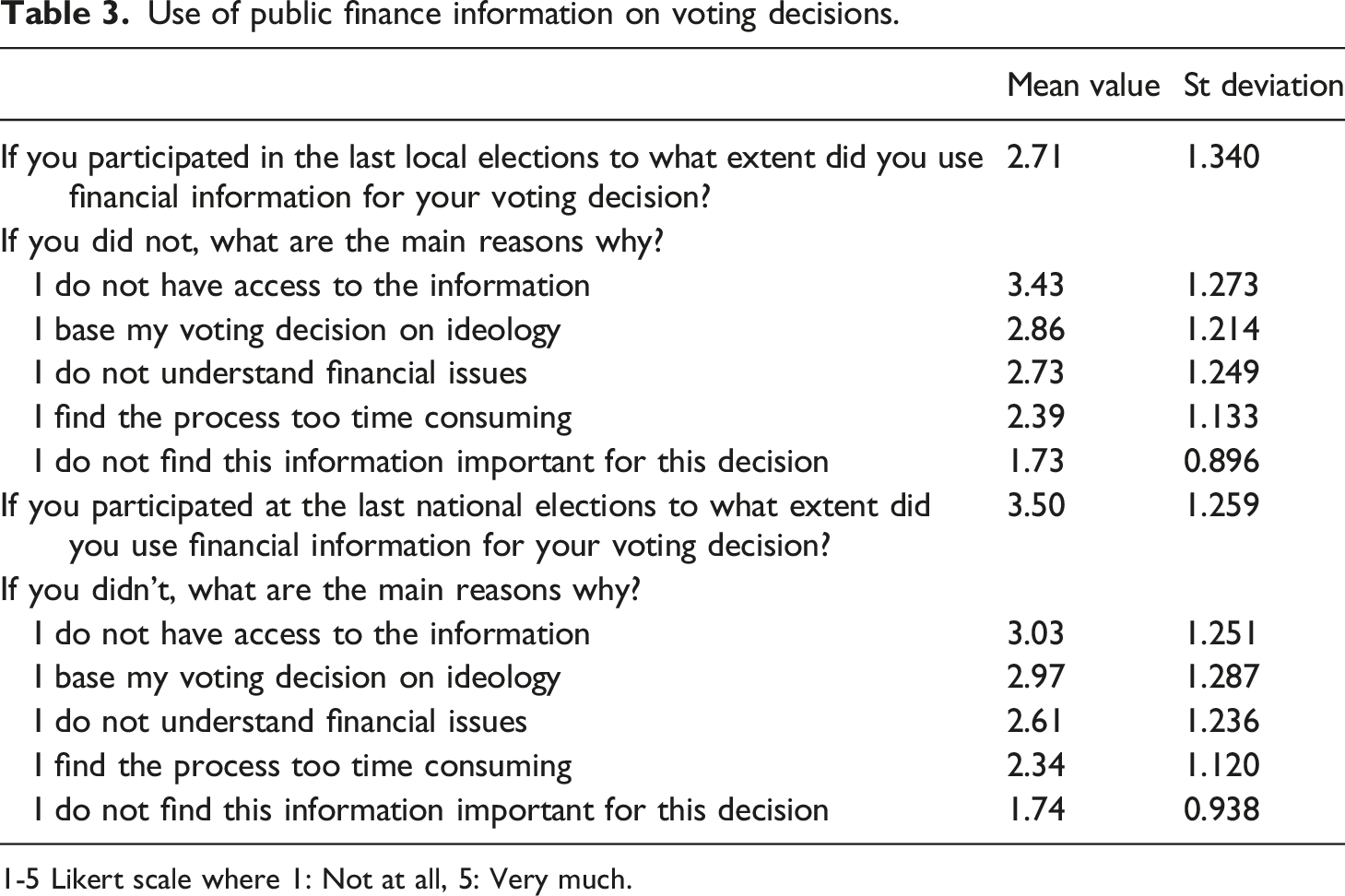

Use of public finance information on voting decisions.

1-5 Likert scale where 1: Not at all, 5: Very much.

Interestingly, the respondents do not use financial information when deciding on the local elections vote, but they consult such information when it comes to national elections (mean values 2.71 and 3.50 respectively). On both cases the most important reason why they do not use financial information refers to the difficulties in having access to it, which is more evident in the case of local elections.

Perceived importance of public finance education

Perceived importance of public finance education.

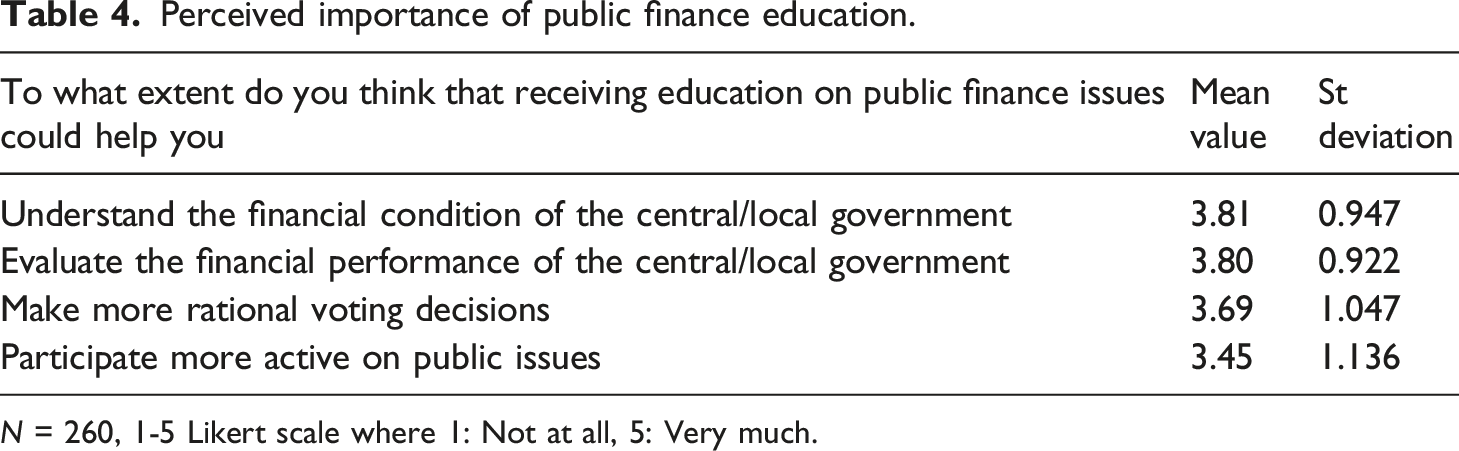

N = 260, 1-5 Likert scale where 1: Not at all, 5: Very much.

The respondents consider that PSA education could help them understand the central/local government financial condition and performance (mean value 3.81 and 3.80 respectively), and to make more rational voting decisions (mean value: 3.69) and to a lesser extent to engage more actively on public issues (mean value: 3.45). The overall familiarity variable is significantly correlated to the three first aspects (p-values: 0.000, 0.000 and 0.010 respectively) but not with the aspect of more active participation. It appears that the more familiar with public finance concepts the more important they perceive the outcome from receiving such education.

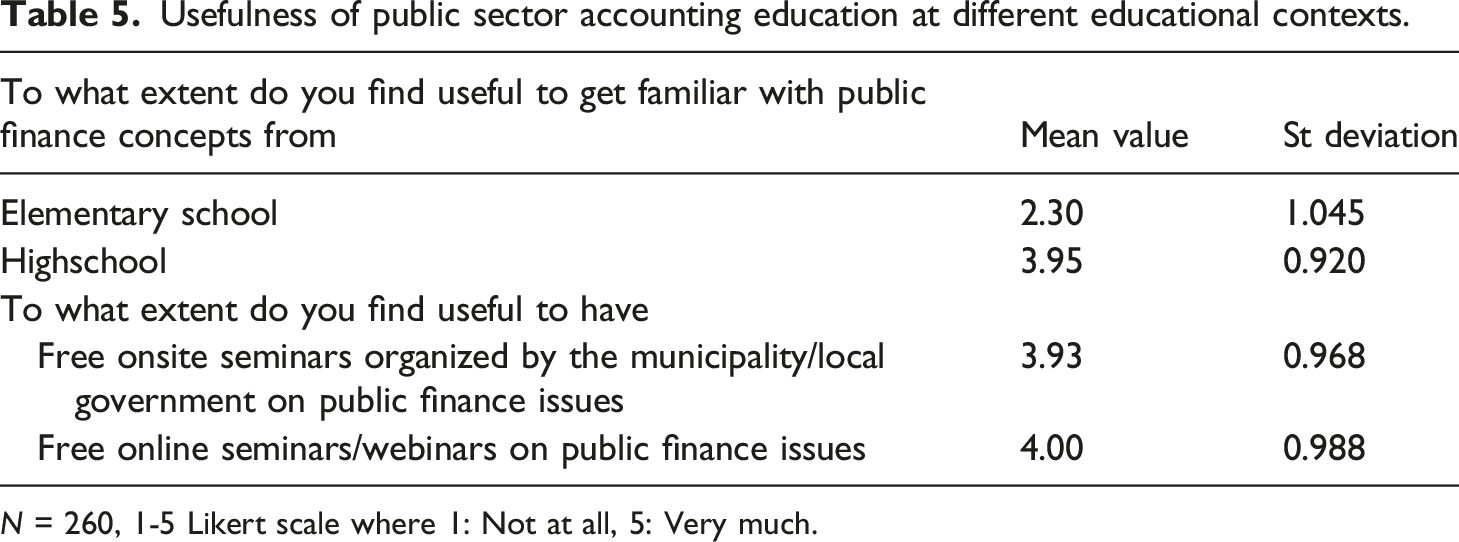

Usefulness of public sector accounting education at different educational contexts.

N = 260, 1-5 Likert scale where 1: Not at all, 5: Very much.

Finally, if public finance seminars were provided at school the slight majority (N: 134; 51.5%) prefers this to take place as part of an existing course (e.g. on financial literacy or on civic education), while the rest (N: 126; 48.5%) would prefer it to be an independent course.

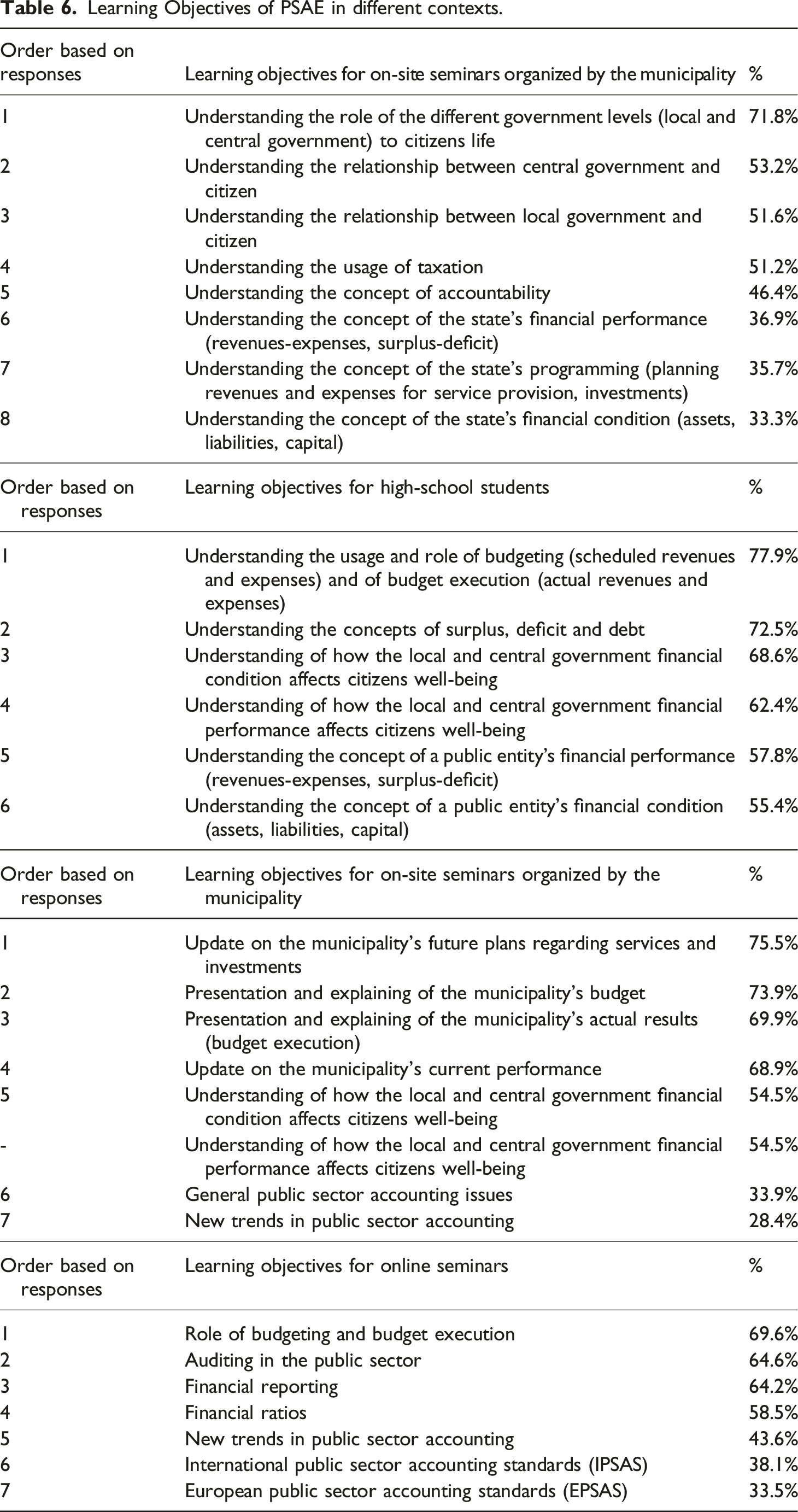

Learning objectives of a PSA educational program

Learning Objectives of PSAE in different contexts.

As regards the learning objectives of a PSA course at elementary school this is basically limited to “Understanding the role of different government levels to a citizen’s life” (71.8%), and to a lesser extent to “Understanding the relationship between central and local government and citizen” (53.2 and 51.6% respectively). This stance agrees with their strong opinion that such education should start from high-school, and not as early as elementary school.

When it comes to the high-school level, the preferred learning objectives widen, including “Understanding the usage and role of budgeting (scheduled revenues and expenses) and of budget execution (actual revenues and expenses)” (77.9%), “Understanding the concepts of surplus, deficit and debt” (72.5%), and “Understanding of how the local and central government financial condition and financial performance affect citizens well-being” (68.6 and 62.4% respectively).

As regards the option of having seminars organized by local governments, the sample prefers them to cover topics such as “The municipality’s future plans on services and investments”, “Presentation and explanation of the municipality’s budget forecast and actual execution”, and “The municipality’s current performance” rather than topics that include general public sector accounting issues and new trends. Finally, in the case of receiving on-line seminars the interest mainly revolved around the role of budgeting and budget execution, auditing in the public sector and financial reporting and ratios, rather than on new trends, International or European public sector accounting standards (IPSAS or EPSAS).

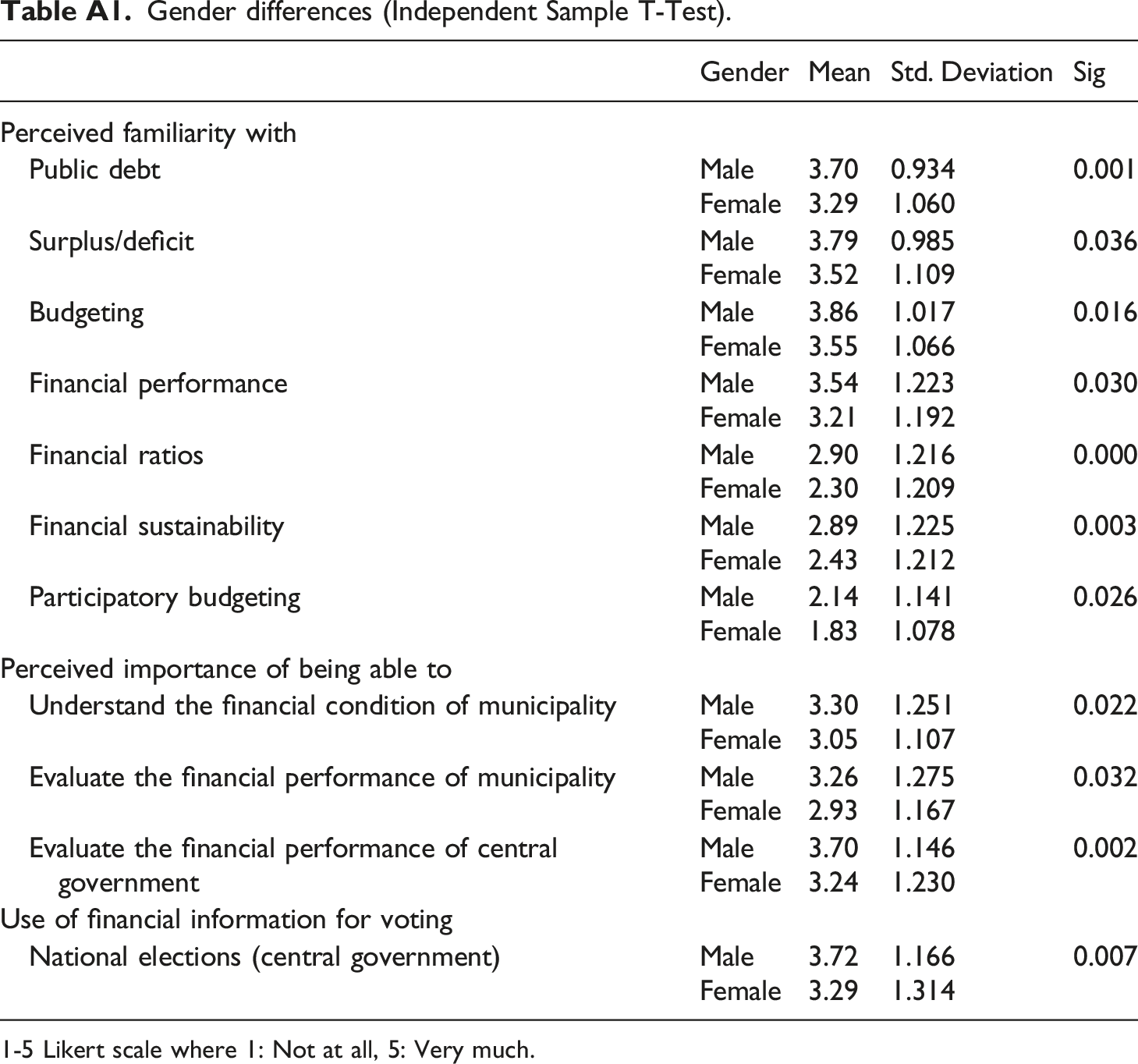

Gender effect

Gender differences (Independent Sample T-Test).

1-5 Likert scale where 1: Not at all, 5: Very much.

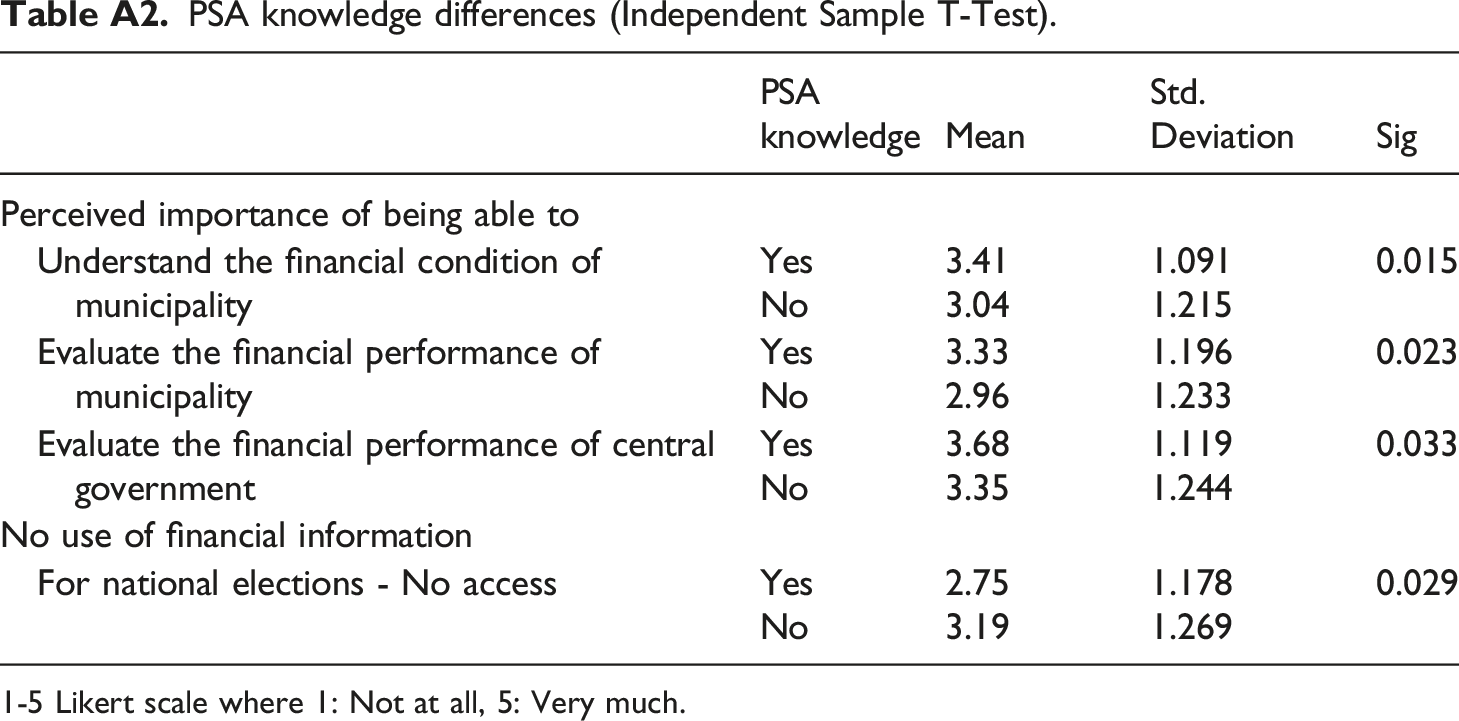

Accounting knowledge effect

By using independent sample t-tests further comparisons were performed between participants with and without (a) general accounting knowledge and (b) public sector accounting knowledge.

PSA knowledge differences (Independent Sample T-Test).

1-5 Likert scale where 1: Not at all, 5: Very much.

Age and status effect

Performing One-Way Anova T-test just a few differences appear, more notably regarding the familiarity with public finance concepts (budget execution, financial sustainability) between younger respondents (age 18–25 years old) and respondents between 46–55 years old, with the latter appearing more familiar (Results not tabulated).

As regards status (Results not tabulated), various differences appear when it comes to overall familiarity between academics and (a) students (sig. 0.002), (b) private sector employees (sig. 0.000) and (c) public sector employees (sig. 0.045). Moreover, important differences turned out between public servants and students regarding their perspective on the possible positive effect of public sector accounting education on making rational voting decisions (sig. 0.032) and more actively participating on common issues (sig. 0.044), with public servants appearing less optimistic compared to students. Finally, academics and public servants appear more in favor of having such courses available from elementary school compared to retired respondents (sig. 0.007and 0.046 respectively). The above results are confirmed by the non-parametric Kruskal–Wallis test.

Educational level effect

By running One-Way ANOVA test to check for any differences due to the different educational levels of the participants to the survey (Results not tabulated), it appears that masters and PhD graduates are more familiar to the concepts compared to high school graduates (p-values = 0.001 and 0.000 respectively), and PhD graduates are more familiar compared to HEI graduates (p-value = 0.008). It is important to note here, that people coming from different educational levels appear to share the same more or less perceptions on citizens’ government accounting literacy.

Discussion and conclusion

This paper is a first attempt to capture citizens’ perspective on various public finance/accounting education aspects. The topic is important as it is closely linked to issues such as active participation and engagement, and public value creation (Allen, 2013; Karatzimas, 2021). The sample was conveniently selected to include citizens with different characteristics and thus achieve a more inclusive outcome. The analysis of the responses indicates an average familiarity of citizens with key public finance issues, with male respondents appearing to some extent more familiar than female respondents. The respondents perceive the ability to understand and evaluate the financial condition and performance at the central government level as a more important skill, compared to the local government level. The same stance is followed when it comes to the use of financial information during election periods, as this is more evident for national elections. Apparently, the respondents perceive more important the use of financial information for the central rather than the local government. Difficulties in accessing the relevant information as well as voting based on ideology appear as the most important reasons why financial information is not used. The problem of limited access (Jordan et al., 2016) as well as the impact of ideology (Lau, 2003) has already been recorded in literature.

The respondents are supportive of the potential outcome from being educated in public sector accounting, as this could help them become able to understand and evaluate financial condition and performance of public entities, and furthermore to make use of it in voting decisions, having thus a more rational stance during elections. They are further supportive of having such education from high-school, but not earlier, and to continue getting updated or further educated through seminars either online or onsite. In the case of elementary schools the results do not agree with what has been proposed in literature that supports an as early as possibly introduction of such concepts to young citizens (Karatzimas, 2020), as is the case of financial literacy programs (OECD, 2005). As regards the preferred learning objectives for high-school PSA education these include the understanding of (1) the usage and role of budget forecasts and the budget execution, (2) the concepts of surplus, deficit and debt, (3) how local and central government financial condition affects citizens well-being, (4) the concept of a public entity’s financial performance (revenues-expenses, surplus-deficit), and (5) the concept of a public entity’s financial condition (assets, liabilities, capital). Finally, when it comes to the possibility of free seminars to citizens, this is positively viewed, but their preferences seem to exclude topics such as new trends in public sector accounting, IPSAS or EPSAS. Contrarily, the preferences are oriented towards more practical and current issues such as the budgeting process of the municipality, its current performance and future plans (on-site seminars) and the understanding of financial reporting, budgeting and auditing in the public sector (online webinars). This stance probably shows a more narrow interest on local government finance and could also indicate the need of citizens to focus on learning first the ‘basics’ of PSA before moving to more complicated aspects.

It is further encouraging that citizens understand the possible beneficial outcomes from such education not only in understanding financial condition and evaluating performance but also in triggering a more rational decision-making based on financial figures and in more actively engaging. This comes in line with theoretical approaches on how public accounting education can affect citizens’ comprehension of public finance issues (Allen, 2013; Dubauskas, 2016) and improve interest in public matters (Allen, 2013; Karatzimas, 2020). Investing in educating citizens could therefore prove priceless for active engagement and potential co-development initiatives (Karatzimas, 2021). Especially, if apart from such an education plan, local/central governments were more decisive in providing adequate information through popular financial reports or online dashboards and citizens’ guide on the budget 3 . These practices are not really used in Greece, but their use could prove beneficial for a more efficient information experience for citizens (Yusef et al., 2013; Blazey et al., 2022). Furthermore, participatory budgeting could be more meaningful when citizens have an understanding of basic public finance (Karatzimas, 2020).

What is further important to note, is that citizens of different age seem to agree on the importance of this education, and this is also evidenced on the perceptions of citizens with a different status. On the other hand the less familiarity recorded by female respondents’ raises certain concerns and should therefore be further investigated. In a study by Park et al. (1994; p. 349) it turned out that although the genders performed equally well in accounting, male participants appeared to be more confident, assertive, and self-sufficient compared to female participants on the survey. This has been recently confirmed by Haustein et al. (2021). This could explain the difference in familiarity recorded in the present study. From a different standpoint, Greece ranks among the worst performers in the 2022 European Gender Equality Index (EIGE, 2022), with significant gender inequalities in employment and education. Female citizens in Greece appear to be less financial literate compared to male citizens (Philippas and Avdoulas, 2020). Τhe sample could be further expanded to increase the number of participants and thus get a clearer picture. This expansion could also include citizens from other countries to explore also the impact of culture on citizens’ perspective on government accounting literacy.

Footnotes

Acknowledgements

The author would like to thank the participants of the 16th CIGAR Workshop held in Cottbus, Germany, and in particular Jens Heiling, Tobias Polzer and Sandra Cohen for their fruitful comments and suggestions on an earlier version of the paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.