Abstract

The relationship between finance and the environment has attracted increasing attention in energy and sustainability research. While financial development is often considered a driver of economic growth, it also entails environmental consequences, particularly through increased energy use and carbon emissions. This study investigates how financial innovation and financial development influence environmental sustainability in the E7 economies (2000–2021), with a specific focus on the moderating role of regulatory quality. Using panel data and random-effects generalized least squares (RE-GLS) estimations, the results show that financial innovation contributes to emission reduction and supports sustainability objectives, particularly when complemented by strong regulatory quality. In contrast, financial development and trade expansion are found to intensify carbon emissions, underscoring the persistence of environmentally harmful financing patterns. The inclusion of supplementary governance indicators, such as voice and accountability, confirms the robustness of the findings. Overall, the study demonstrates that regulatory quality plays a pivotal role in shaping whether financial systems act as environmental enhancers or detractors. These findings provide actionable insights for policymakers and stakeholders in emerging economies, highlighting the need to strengthen governance frameworks and align financial systems with long-term sustainability and emission-reduction goals.

Keywords

Introduction

The rapid expansion of financial systems has long been regarded as a cornerstone of economic growth, particularly in emerging economies. However, growing empirical evidence suggests that financial expansion can also intensify environmental pressures through increased energy consumption, industrial activity, and carbon emissions (Gyamfi et al., 2022; Samour et al., 2022; Udemba and Tosun, 2022). The rapid expansion of financial systems has long been regarded as a cornerstone of economic growth, particularly in emerging economies. However, growing empirical evidence suggests that financial expansion can also intensify environmental pressures through increased energy consumption, industrial activity, and carbon emissions (Hu et al., 2021; Wen et al., 2022). As countries strive to balance growth with climate commitments under the Paris Agreement, understanding whether finance acts as an environmental enabler or detractor has become a central policy concern (Ali et al., 2023).

Recent research has increasingly distinguished between financial development (FD) and financial innovation (FI) when assessing environmental outcomes. While FD reflects the overall depth and scale of financial markets, FI captures the evolution of new instruments, technologies, and mechanisms that may facilitate cleaner production and sustainable investment (Nuta et al., 2025; Siddik et al., 2025). However, empirical findings remain mixed. Several studies report that FD exacerbates carbon emissions by accelerating fossil-fuel-based industrialization and energy demand, whereas FI, particularly when aligned with green finance principles, can support emission reduction by improving capital allocation efficiency and enabling low-carbon technologies. This divergence highlights the need to examine these financial dimensions jointly rather than treating finance as a homogeneous construct. An increasingly important yet underexplored factor in this relationship is regulatory quality (RQ). Strong regulatory frameworks can shape the direction of financial flows by enforcing environmental standards, reducing market failures, and limiting opportunistic behavior such as greenwashing (Bos and Gupta, 2019). In contrast, weak governance may allow financial expansion to reinforce carbon-intensive growth patterns.

Although prior studies acknowledge the importance of institutions, empirical evidence on how RQ moderates the effects of FD and FI on carbon emissions remains limited, particularly in emerging economies. This gap is especially relevant for the E7 economies (Brazil, China, India, Indonesia, Mexico, Russia, and Turkey). These countries account for a substantial share of global energy demand and carbon emissions, while simultaneously experiencing rapid financial sector expansion and uneven regulatory capacity (Hussain et al., 2021; Rauf et al., 2023). Unlike developed economies, E7 countries face the dual challenge of sustaining economic growth and managing rising environmental risks (Abaidoo and Agyapong, 2022). Real-world policy debates such as green credit guidelines in China, sustainable finance roadmaps in India, and regulatory reforms in Turkey illustrate the urgency of understanding whether financial systems, under varying governance conditions, can support environmentally sustainable pathways. Against this background, the present study investigates the nexus between FI, FD, and environmental sustainability, with RQ as a moderating factor, using panel data for E7 economies over the period 2000–2021. Likewise, the robustness of baseline outcomes is re-examined by including an additional governance indicator (voice and accountability) to further ensure the analysis's sensitivity. Specifically, the study addresses the following research questions:

Does FI contribute to reducing carbon emissions in emerging economies? Does FD, in its conventional form, intensify environmental degradation? How does RQ condition the environmental impacts of FI and FD? What policy insights can be derived for aligning financial systems with sustainability objectives in high-growth economies?

This study makes several novel contributions. First, it conceptually and empirically disentangles financial innovation from financial development, demonstrating that these dimensions exert fundamentally different environmental effects. Second, it explicitly models regulatory quality as a moderator, offering new evidence on how governance determines whether finance supports or undermines environmental sustainability. Third, by focusing on the E7 economies, the study provides policy-relevant insights for energy-intensive emerging markets, where institutional capacity varies widely, and environmental risks are most acute. Overall, the findings contribute to the energy-finance-environment literature by showing that financial systems do not inherently promote sustainability; rather, their environmental impact depends critically on the quality of regulation guiding financial activity. These insights offer practical implications for policymakers seeking to design governance frameworks that steer financial innovation toward sustainable energy transitions while constraining the environmental costs of unchecked financial development.

Section “Literature review” concisely summarizes relevant literature studies. Section “Methodology” is dedicated to the analysis of statistics and the application of techniques. Section “Results” offers valuable insights into results based on the employed approaches. The study is concluded in Section “Discussion”, where policy proposals are provided.

Literature review

The relationship between financial systems and environmental sustainability has become a central theme in energy and environmental economics, particularly as countries confront the dual challenge of economic expansion and carbon mitigation (Rajpurohit and Sharma, 2021). Early strands of the literature treated finance as a growth-enhancing mechanism with largely indirect environmental consequences (Ntow-Gyamfi et al., 2020; Zhang et al., 2021). However, more recent studies have demonstrated that financial systems exert a direct and often heterogeneous influence on energy consumption patterns and CO2-EM, depending on their structure, depth, and governance environment (Baloch et al., 2021; Umar and Safi, 2023). A substantial body of empirical research finds that FD measured through credit expansion, stock market capitalization, or banking depth tends to intensify CO2-EM in emerging economies (Bekun et al., 2019; Gokmenoglu and Sadeghieh, 2019; Gyamfi et al., 2022; Samour et al., 2022). This effect is primarily attributed to increased industrial activity, fossil-fuel-based energy demand, and relaxed financing constraints for pollution-intensive sectors. Studies focusing on developing and emerging economies consistently report that financial deepening accelerates energy consumption and emissions when environmental regulations are weak or poorly enforced (Huo et al., 2023; Kamal et al., 2021). These findings suggest that financial development, in its conventional form, often reinforces unsustainable growth trajectories rather than facilitating energy transitions.

In contrast, a growing literature distinguishes FI as a qualitatively different mechanism _ENREF_63 (Aslan et al., 2024; Naseem et al., 2023). FI encompasses new instruments, technologies, and financing models such as green bonds, sustainability-linked loans, and fintech-based solutions that can improve capital allocation efficiency and reduce the cost of clean energy investments (Martinez et al., 2022; Rehman and Islam, 2023). Empirical evidence increasingly shows that FI supports emission reduction by enabling renewable energy deployment, improving firm-level energy efficiency, and fostering environmentally responsible investment behavior (Andrew et al., 2024; Ullah et al., 2023). Nevertheless, these positive effects are not universal, indicating that innovation alone does not guarantee sustainability gains.

One key explanation for these mixed findings lies in institutional and RQ. Institutional theory posits that regulatory frameworks shape market behavior by constraining opportunism, reducing uncertainty, and aligning private incentives with public objectives (Fakher and Ahmed, 2023). Empirical studies provide strong evidence that governance quality conditions the environmental impact of financial systems (Udeagha and Breitenbach, 2023). In economies with robust regulatory institutions, FI is more likely to be channeled toward low-carbon activities, while FD becomes less environmentally damaging (Cai and Wei, 2023; Chen et al., 2023)_ENREF_48_ENREF_48. Conversely, weak regulatory environments allow financial expansion to amplify emissions through unchecked industrial growth and energy-intensive investments (Barnett, 2003). Despite this recognition, the moderating role of RQ remains insufficiently explored, particularly in the context of emerging economies. Most existing studies examine the direct effects of finance or institutions on emissions, but few explicitly model how RQ interacts with different dimensions of finance, namely financial innovation and financial development, to shape environmental outcomes. This omission limits our understanding of why similar levels of financial expansion produce divergent environmental consequences across countries.

The relevance of this gap is especially pronounced for the E7 economies, which are characterized by rapid financial expansion, rising energy demand, and heterogeneous regulatory capacities. While some E7 countries have introduced sustainable finance initiatives and environmental regulations, enforcement remains uneven, and financial resources often continue to flow toward carbon-intensive sectors. Existing studies focusing on developed economies offer limited guidance for these contexts, where institutional constraints and energy structures differ markedly. Taken together, the literature suggests three critical insights. First, FD and FI exert distinct and sometimes opposing effects on environmental sustainability. Second, RQ plays a decisive role in shaping whether finance supports or undermines emission reduction objectives. Third, there remains a lack of integrated empirical evidence that jointly examines these relationships in high-growth, energy-intensive emerging economies. Addressing these gaps, the present study develops a unified framework to analyze how financial innovation and financial development influence carbon emissions under varying levels of regulatory quality in the E7 economies.

Methodology

Data and variable specifications

Variable description.

Environmental sustainability is proxied by CO₂ emissions, reflecting the environmental pressure associated with energy consumption and industrial activity. Although emissions do not capture all dimensions of sustainability, they remain the most widely used indicator in energy-environment research and are particularly relevant for energy-intensive emerging economies. The key explanatory variables are financial innovation (FI) and financial development (FD). FI is a multidimensional concept; data limitations across emerging economies necessitate the use of proxies that capture systemic financial evolution. In this study, broad money (% of GDP) is employed as a proxy for financial innovation following a stream of empirical literature that associates monetary deepening with the diffusion of new financial instruments, payment mechanisms, and financial intermediation technologies in developing economies. Although broad money primarily reflects liquidity, its expansion in emerging markets often coincides with the adoption of digital banking, mobile payments, and non-traditional financial services, which collectively embody financial innovation. Thus, in contexts where direct measures of fintech penetration or financial patents are unavailable or inconsistent, broad money provides a pragmatic and widely accepted approximation of innovation-driven financial expansion.

Alternative indicators of FI such as fintech adoption indices, digital payment volumes, or patent counts in financial technologies were considered. However, these indicators suffer from limited time coverage, inconsistent reporting, and a lack of cross-country comparability for the E7 economies over the study period. Given the long temporal span of the analysis (2000–2021) and the need for uniform measurement across countries, broad money remains the most suitable proxy for capturing economy-wide financial innovation dynamics in a macro-panel setting. While FD captures the overall depth and scale of financial markets, which may expand credit availability and industrial output but also intensify fossil-fuel-based energy use. Regulatory quality (RQ) is incorporated as both an independent and moderating variable. It reflects the ability of governments to formulate and implement sound policies, enforce regulations, and promote market discipline factors that are central to aligning financial activity with environmental objectives. Additionally, to ensure comparability and mitigate scale-related distortions, all continuous variables are transformed into their natural logarithmic form, except for governance indicators, which are standardized indices. Logarithmic transformation reduces skewness, stabilizes variance, and allows estimated coefficients to be interpreted as elasticities, a standard practice in macro-panel energy and finance studies.

Econometric specifications

The present article employed the subsequent regression model to investigate the impact of various factors on CO2-EM in certain nations. The simulation's fundamental structure is as follows:

Equation 1 includes the explained, explanatory, and control factors of the research, but it does not incorporate the moderating variable. Subsequently, Equation 2 incorporates the RQ variable to investigate its role as a moderator on CO2-EM.

In Equations 1 and 2,

Econometric methods

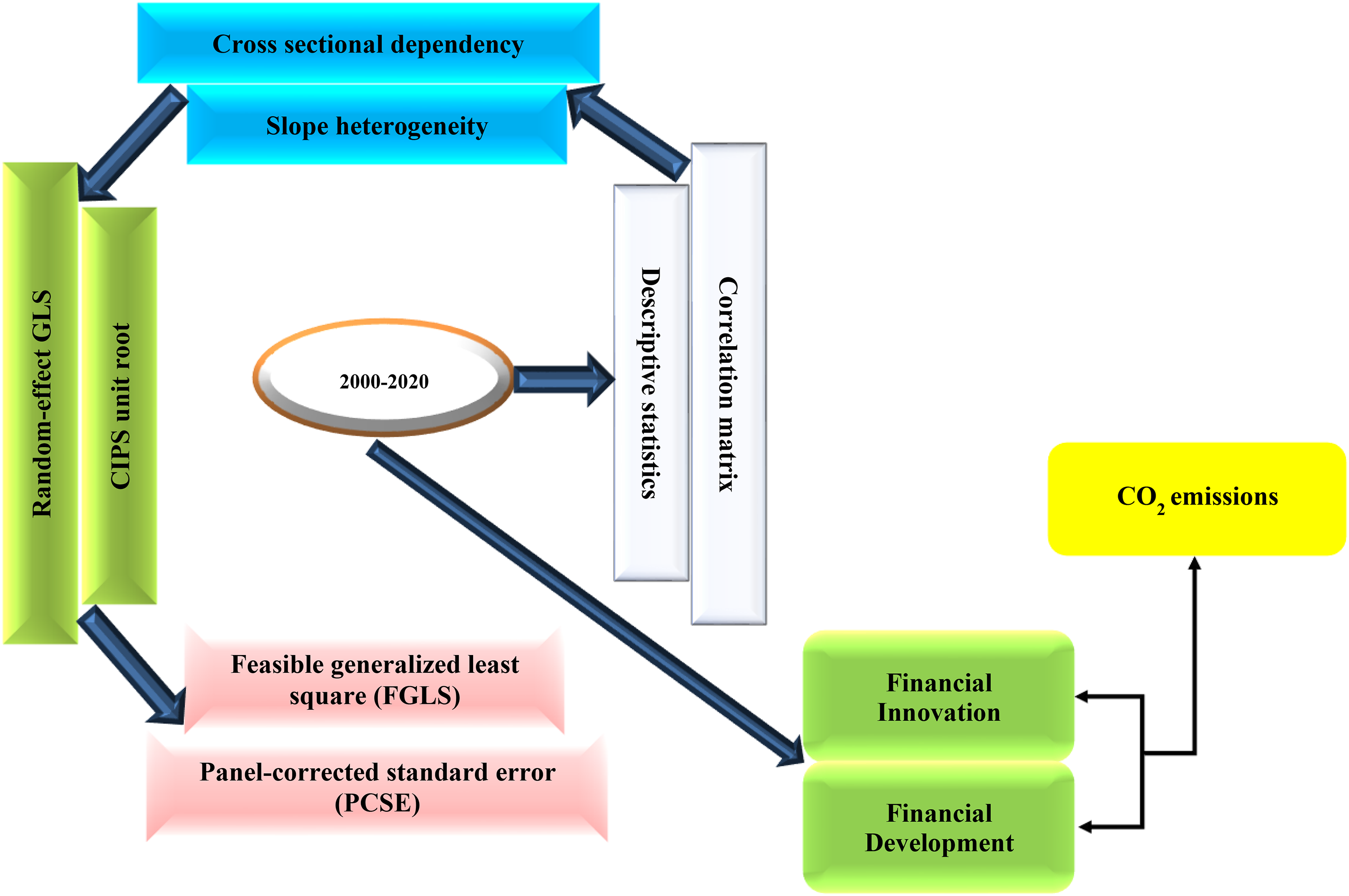

The econometric methodologies employed to carry out the analysis are mentioned in this section, with the initial phase involving preliminary investigation via summary statistics and a correlation test. This stage also entails “cross-sectional dependence (CSD), panel unit root, slope heterogeneity (SLH), and CIPS unit root tests.” The study examined CSD using Pesaran (2015) technique since CSD was identified as a fundamental issue in the analysis of panel data. Given the high level of global interconnectivity in today's globe, the unpredictable actions of one nation in reaction to a certain variable can have significant and widespread effects on other countries. For instance, trade agreements and intercultural and economic convergence may contribute to regional economic development. Therefore, it is crucial to assess CSD, as neglecting it will possibly result in significant econometric consequences. Likewise, the SLH test is employed to ascertain the statistical significance of the disparities between the slopes of two or more regression lines. Hence, this study utilized the Pesaran and Yamagata (2008) SLH test to investigate the differences across models for E7 nations. The equations for both mentioned tests are as follows:

where

Furthermore, it is acknowledged that RE-GLS assumes that unobserved country-specific effects are uncorrelated with the regressors. Given the macroeconomic nature of the data, this assumption may not fully hold. To address this concern, several steps are taken. First, CSD and SLH tests are conducted to ensure the suitability of panel estimators in the presence of interconnected economies. Second, fixed-effects estimations are employed as robustness checks to verify the stability of coefficient signs and significance. Third, feasible generalized least square (FGLS) and panel-corrected standard error (PCSE) estimators are used to account for heteroskedasticity, autocorrelation, and cross-sectional dependence. The consistency of results across these alternative estimators strengthens confidence in the RE-GLS findings. While dynamic panel techniques such as system GMM are often used to address endogeneity, their application requires large cross-sectional dimensions and strong instruments. Given the relatively small number of countries and the risk of weak instrumentation, RE-GLS complemented by robustness checks is considered more appropriate for the present analysis. Figure 1 visualized the econometric analysis framework of the study, and the recommended general specification of RE-GLS is as follows:

Econometric analysis framework.

Results

Descriptive statistics and correlation analysis

Descriptive statistics are employed to comprehend the features of the sample before conducting the main estimations (Table 2). The mean CO2 is 4.295, and the standard deviation (SD) is 3.288. India reported a minimum CO2 value of 0.884 in the dataset, alongside Brazil and Indonesia. Although E7 economies lessened their emission level during the last few decades because of technological expansions, CO2 per capita continues to be high contrasted with other world areas. The maximum CO2 value (11.885) was accredited to Russia in 2011, and other leading countries, such as China and Turkey, were accredited for emission releases. It underscores substantial energy utilization and the pattern of manufacturing being outsourced to foreign nations.

Summary statistics.

Moreover, the FI unveils mean and SD values of 4.047 and 0.650. Countries like Indonesia and Mexico demonstrate rather reduced FI, with Russia having the minimum value of 0 in 2000 because of their relatively small magnitude. It can result from the nation's insufficient financial capacity or the absence of the structures required for FI adoption to be widely implemented. Conversely, China reported the highest FI value of 5.356 in 2020, while other E7 countries also demonstrated higher FI levels later in the sample period due to the modern structure. These countries usually have pro-FI government laws that further promote the use of FI tools in various industries, creating an atmosphere favorable to technical advancement, effectiveness, and competitiveness.

FND shows mean and SD values of −0.811 and 0.220, respectively. All countries in the panel constantly reveal negative FD, implying various prospective challenges in the region. The financial infrastructure in E7 countries, including banking systems, capital markets, and regulatory frameworks, may be underdeveloped or inefficient. It can lead to issues such as a lack of transparency, poor governance, and inadequate investor protection. Furthermore, income inequality and wealth distribution disparities affect access to monetary services and opportunities for economic advancement. Also, limited access to technology and digital infrastructure can impede FD in E7 countries, particularly in expanding digital financial services and promoting financial innovation. Indonesia reported a minimum value of −1.308 in 2003, while China reached a maximum FD of −0.394 in 2020.

Likewise, the RQ average is −0.106, and the SD is 0.293, signifying varied intensities of regulations in selected economies. Notably, four nations in the panel, including China, India, Indonesia, and Russia, frequently show negative RQ values, which suggests probable administration issues in the environmental regulations. Indonesia had a minimum value of −0.866 in 2003. In contrast, countries like Brazil, Mexico, and Turkey occasionally had negative RQ scores, which might be related to economic changes. Turkey achieved a maximum value of RQ 0.463 in 2013, showcasing exceptional legislative and regulatory success indicative of a solid regulatory system, governance stability, generosity, and a favorable legal climate.

In addition, the average stated GDP is 1.349 with SD 0.816, revealing the economic vigor of E7 economies, constituting almost 35% of the global economy, and showing 5.2% growth between 2010 and 2020. Strong technological infrastructure, experienced personnel, steady political situations, and capital access lead to higher GDP in these nations. These countries also feature well-developed financial markets, efficient regulatory systems, and high levels of innovation and productivity. Brazil, Russia, and Turkey exhibited negative GDP values once during the study period, with a minimum value reported at −1.641 for Russia in 2016. Moreover, the reported mean and SD of PTNT are 2.231 and 0.308, while India stated a minimum value of 0.959 in 2001. Lesser PTNT values occur due to variations in patent counts across countries and industries, with many patents having limited societal value. The skewed distribution of patents and differences in patent regulations make cross-country comparisons challenging, and changes in patent laws complicate trend analysis over time. Nonetheless, each nation in the selected panel shows a favorable tendency, with the max PTNT value of 2.747 illustrating regional technical advancements.

TRE average is 3.818, and SD is 0.302; Brazil and Mexico report minimum and maximum values of 3.096 and 4.389, respectively. E7 countries have observed substantial growth in trade and investment in recent years due to their expanding economies and increasing global integration. These economies actively trade with developed and developing nations, seeking to leverage their competitive advantages in various industries. They have become major players in international trade, exporting a wide range of goods and services such as manufactured products, agricultural commodities, natural resources, and technology-related services.

The correlation results in Table 3 indicate that the data have no coefficient over 0.6, which reveals that the likelihood of encountering multicollinearity issues is reduced; hence, we can proceed with estimating the panel regression. Further, the findings specify a positive association between FND, PTNT, and TRE and a negative correlation between FI, RQ, and GDP with CO2-EM.

Correlation matrix.

CSD analysis

Table 4 displays the CSD outputs to confirm its presence in the panel. Breusch-Pagan, Pesaran Scaled, Bias-corrected scaled LM, and Pesaran CD tests are employed to show strong evidence of CSD in the panel, with a significance threshold of 1%, except for variables RQ and TRE in column 4. CSD outcomes reveal that we reject the H0, suggesting its presence in the panel. Except for column 4, CSD is validated by the p-values of RQ and TRE for all parameters in all other columns. This interdependence can be viewed in several ways. For instance, the results suggest that pollution is cross-border, and E7 nations have comparable associated problems. Therefore, any remedial measures implemented in a particular region would affect the adjacent countries.

CSD analysis.

Note: 10%*, 5%**, and 1%*** significance level.

SLH test

SLH test results are shown in Table 5. Determining whether the slope coefficients exhibit heterogeneity or homogeneity and which estimation technique should be preferred is essential. The output reveals that SLH coefficients exhibit heterogeneity since the p-values imply significance at the 1% level.

Testing for slope heterogeneity.

Note: 10%*, 5%**, and 1%*** significance level.

CIPS unit root analysis

Since the diagnostic test indicated the existence of CSD in the data, the study proceeds to perform panel unit root tests using the Pesaran CIPS method to assess the level of stationarity of the variables. The results in Table 6 show the null hypothesis (H0) rejection at a significance level of 1%. It leads to the conclusion that all variables are stationary in their first difference form (1) and will not provide spurious outcomes. Collectively, the diagnostic test results justify the selected estimation strategy. Evidence of cross-sectional dependence and slope heterogeneity confirms the interconnected nature of E7 economies and supports the use of panel estimators robust to such features. The absence of severe multicollinearity, as indicated by correlation diagnostics, suggests that coefficient estimates are stable and interpretable. While potential endogeneity concerns cannot be entirely ruled out in macro-panel settings, the consistency of results across RE-GLS, FGLS, and PCSE estimators mitigates concerns of model-driven bias and strengthens confidence in the empirical findings.

CIPS unit root.

Note: 10%*, 5%**, and 1%*** significance level.

Key regression findings

This study investigates how FI and FND affect CO2-EM in E7 countries. Four models are used under panel RE-GLS regression, and the findings are presented in Table 7. Model 1 performed a regression analysis on CO2-EM using all the research variables. The individual moderation effects of (FI × RQ) and (FND × RQ) are explored in Models 2 and 3, respectively. Similarly, their collective moderation assessment was conducted in Model 4. The utilization of R2 and Wald chi2 tests assesses the models’ fitness. The regression estimates reveal a statistically significant and negative association between FI and CO₂-EM across all model specifications at the 1% level. Specifically, a 1% increase in FI is associated with reductions in CO₂ emissions ranging from 1.737% to 4.067%, depending on the model. These results indicate that innovation-driven financial expansion contributes to emission mitigation in E7 economies.

RE-GLS regression results.

Note: M indicates Model; Standard errors in parentheses; * p < 0.1, ** p < 0.05, *** p < 0.01.

In contrast, FND exhibits a positive and statistically significant relationship with CO₂-EM in all estimated models. The magnitude of the coefficients suggests that scale-driven financial expansion intensifies emission levels, reflecting increased economic activity and energy demand in the absence of adequate environmental safeguards. The coefficient of RQ is consistently negative and significant at the 1% level, indicating that improvements in governance effectiveness are associated with substantial reductions in CO₂-EM. The variation in coefficient magnitudes across models reflects heterogeneity in regulatory enforcement and institutional capacity among E7 countries. Regarding moderation effects, the interaction term FI × RQ exhibits a negative and significant coefficient, implying that stronger RQ enhances the emission-reducing impact of financial innovation. Similarly, the interaction term FND × RQ also shows a negative association with emissions, suggesting that effective regulation can mitigate the environmentally adverse effects of financial development. In the full interaction model, both moderation effects remain robust, with the magnitude of the FND × RQ interaction exceeding that of FI × RQ.

Among control variables, trade openness (TRE) exerts a positive and statistically significant effect on emissions across most model specifications, indicating that trade-related economic expansion remains energy-intensive in E7 economies. Population growth shows limited significance, while GDP per capita does not exhibit a statistically robust relationship with emissions. Beyond statistical significance, the magnitude of estimated coefficients offers meaningful policy insights. For instance, a 1% increase in FI is associated with a measurable reduction in carbon emissions, suggesting that innovation-led financial expansion contributes to cleaner production processes. Conversely, the positive elasticity of emissions with respect to FD indicates that scale-driven financial expansion intensifies energy consumption when not adequately regulated. These magnitudes highlight that RQ plays a decisive role in determining whether financial growth translates into environmental gains or costs. The graphical representation of the interaction effects is presented in Figure 2.

Graphical illustration of the moderating effects of RQ on FI-CO2 and FND–CO2.

Beyond statistical significance, the magnitude of estimated coefficients offers meaningful policy insights. For instance, a 1% increase in FI is associated with a measurable reduction in carbon emissions, suggesting that innovation-led financial expansion contributes to cleaner production processes. Conversely, the positive elasticity of emissions with respect to FD indicates that scale-driven financial expansion intensifies energy consumption when not adequately regulated. These magnitudes highlight that RQ plays a decisive role in determining whether financial growth translates into environmental gains or costs.

Robustness results

Table 8 reports robustness analysis under FGLS and PCSE methods, using RQ as a moderator. The findings validated the benchmark results and suggest its robustness and consistency. FI and FND coefficients consistently maintain a negative and positive significance, respectively, across different models. Also, the moderations of RQ and control indicators further strengthen the primary findings.

Robustness check with RQ.

Note: Standard errors in parentheses; + p < 0.2, * p < 0.1, ** p < 0.05, *** p < 0.01.

To further validate the robustness, we replace RQ with voice and accountability (VA) as independent variables using the same methods. The regression findings in Table 9 indicate that VA substantially and negatively affects CO2-EM in all models, like RQ. Simultaneously, the indications and importance of nearly all the outcomes align with the regression results of RE-GLS (Table 7), demonstrating the persistence of our study. Moreover, the moderation findings for (FI × VA) and (FND × VA) similarly demonstrate the same link but with marginally higher coefficient values. The robustness checks confirm the stability of the estimated relationships across alternative estimators. Building on these validated findings, the following section discusses their theoretical implications and policy relevance.

Robustness check with voice and accountability (VA).

Note: M indicates Model; Standard errors in parentheses; + p < 0.2, * p < 0.1, ** p < 0.05, *** p < 0.01.

Discussion

The findings of this study provide strong empirical support for theoretical perspectives that emphasize the role of financial systems and institutional quality in shaping environmental outcomes. From an institutional economics standpoint, financial mechanisms influence emissions through both scale effects, which tend to increase environmental pressure, and efficiency effects, which can facilitate cleaner production and energy transitions. The positive relationship between FND and CO2-EM confirms the dominance of scale effects in E7 economies, where financial deepening often accelerates industrial expansion and energy consumption. This result aligns with earlier evidence from emerging economies, which suggests that credit expansion frequently finances carbon-intensive sectors in the absence of stringent environmental oversight (Lv and Li, 2021; Muazu and Vo, 2021). The finding also explains why FND, despite its growth benefits, has not yet translated into environmental improvements in high-growth developing regions.

In contrast, the emission-reducing effect of FI highlights the importance of efficiency-enhancing financial channels. FI appears to support cleaner production by reallocating capital toward low-carbon technologies, renewable energy projects, and environmentally responsible firms. This result corroborates recent studies emphasizing the role of innovative financial instruments in facilitating sustainable investment and energy efficiency (Manzoor and Zheng, 2021; Naseem et al., 2023). The divergence between FND and FI underscores the necessity of distinguishing between quantitative financial expansion and qualitative financial transformation. A key contribution of this study lies in demonstrating the moderating role of RQ. The negative and significant interaction effects confirm that governance frameworks condition the environmental consequences of financial activity. Strong RQ amplifies the emission-reducing impact of FI while simultaneously dampening the adverse environmental effects of FND. This finding extends prior research that treated governance as a direct determinant of emissions by revealing its interactive role in shaping finance-environment linkages.

The heterogeneous moderation effects observed across models further suggest that regulatory institutions in E7 economies differ substantially in enforcement capacity and policy effectiveness. Where RQ is high, financial systems are more likely to channel resources toward environmentally sustainable activities. Conversely, weak governance allows financial expansion to reinforce carbon-intensive growth patterns. These insights are particularly relevant for emerging economies pursuing rapid economic development alongside climate commitments. Overall, the results suggest that financial systems alone cannot deliver environmental sustainability. Instead, regulatory quality acts as the critical transmission mechanism through which financial innovation and development influence emissions. This interaction-based evidence provides a more nuanced understanding of why similar financial trajectories produce divergent environmental outcomes across countries.

Conclusion

Key empirical conclusions

This study examined the interplay between financial innovation, financial development, regulatory quality, and carbon emissions in E7 economies over the period 2000–2021. The empirical evidence reveals three key findings. First, financial innovation consistently reduces carbon emissions, indicating that innovation-led financial mechanisms contribute to cleaner production and energy-efficient investments. Second, financial development increases emissions, reflecting scale-driven economic expansion that remains reliant on carbon-intensive activities. Third, regulatory quality plays a decisive moderating role by amplifying the environmental benefits of financial innovation while mitigating the emission-enhancing effects of financial development. These results underscore that financial systems influence environmental outcomes not in isolation, but through their interaction with governance quality.

Policy implications for E7 economies

The findings yield clear and actionable policy implications for E7 economies. Strengthening regulatory quality emerges as a critical lever for aligning financial expansion with environmental objectives. Governments should enhance regulatory enforcement mechanisms, integrate environmental standards into financial supervision, and promote transparency through mandatory carbon disclosure frameworks. For financial innovation to translate into sustained emission reductions, policymakers should incentivize green financial instruments such as green bonds, sustainability-linked lending, and climate-aligned fintech platforms. In contrast, the emission-enhancing effects of financial development suggest the need for regulatory safeguards that discourage credit allocation toward carbon-intensive sectors. Country-specific policies—such as differentiated capital requirements for high-emission industries or targeted subsidies for clean energy finance—can help ensure that financial growth supports climate commitments rather than undermining them.

Contributions to literature

This study contributes to the literature in several important ways. First, it empirically distinguishes between financial innovation and financial development, demonstrating that these dimensions exert fundamentally different environmental effects. Second, it advances the finance–environment literature by explicitly modeling regulatory quality as a moderating mechanism, rather than treating governance as a purely direct determinant. Third, by focusing on E7 economies, the study provides evidence from high-growth, energy-intensive contexts that remain underrepresented in existing research. The consistency of findings across multiple estimators further strengthens the robustness and credibility of the results.

Limitations and future research

Despite its contributions, this study has limitations. The analysis relies on macro-level proxies, such as broad money for financial innovation, which may not fully capture firm-level technological advancements. Data constraints also limit the inclusion of alternative governance indicators and sector-specific emissions. Future research could employ micro-level datasets, incorporate direct measures of fintech adoption or green finance penetration, and explore non-linear or threshold effects of regulatory quality. Extending the analysis to comparative regional settings or dynamic policy shocks would further enrich the understanding of finance–environment interactions.

Footnotes

Ethical approval

The authors all agree to ethical approval and understand its related rules and content.

Consent for publication

All authors provide their consent for publication of this manuscript and related content.

Author contributions

Yihan Lu: validation, visualization, resources, and writing—review and editing; Snovia Naseem: conceptualization, methodology, formal analysis, investigation, and writing—original draft; Umair Kashif: conceptualization, formal analysis, investigation, resources, writing—original draft, and writing—review and editing.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability

The datasets generated during and/or analyzed during the current study are available from the corresponding author on reasonable request.