Abstract

As the world is paying increasing attention to carbon reduction, this paper uses Chinese commercial banks’ green credit and applies the DEA-Malmquist index method to construct an evaluation index system based on the panel data of the top 10 Chinese banks regarding green credit from 2015 to 2021. The results of the study show that: (1) the overall total factor productivity of the banking industry in mainland China from 2015 to 2021 is greater than 1 and shows a fluctuating upward trend except for 2015, with the mean value greater than 1 indicating a steady increase in the green credit operating efficiency of the banking industry; (2) Further analysis shows that the average value of the technical efficiency change index is greater than the average value of the technological progress index, which can be understood as the important reason for the rising operational performance of green credit business in the banking industry, and technological progress also provides a supporting role for the rising operational performance; (3) the average value of the scale efficiency change index from 2015 to 2021 is less than 1, and from 2017 onwards the value starts to be less than 1 and declining, it can be concluded that scale efficiency hinders the increase of technical efficiency index. (4) The magnitude of change in total factor productivity and the influencing factors of the 10 banks are all related to technical efficiency, indicating that the improvement of technical efficiency is the dominant factor in the improvement of green credit operational efficiency; (5) the pure technical efficiency of all 10 banks keeps increasing while the scale efficiency is decreasing, indicating that pure technical efficiency is the key factor in the improvement of banks’ technical progress index, while scale efficiency inhibits the further improvement of technical progress index. The increase in the technical progress index has been inhibited by scale efficiency.

Keywords

Introduction

In recent years, under the impact of the New Crown epidemic, our economy has faced unprecedented havoc and various financial businesses have been hit hard, with banking businesses being hard hit. The low-carbon economy has emerged against the backdrop of a worldwide drive to reduce carbon emissions. As green finance is vital to our “double carbon” goals, banks are now the most important institution in the practice of green finance, not only as a fundamental part of our financial system, but also as an essential part of our lives. Nowadays, the impact of the epidemic has had a huge impact on the credit side of the banking sector. Therefore, how to improve the performance of banks’ green credit operations in the context of carbon reduction has become a key concern in China. Therefore, the objective of this paper is to investigate the impact of the green credit performance of the commercial banking sector under the new epidemic and during the non-epidemic period. The research method used is the DEA-Malmquist index method, and by comparing the data from these two states, the credit capacity of banks, and the aspects and impacts of the impact.

The Data Envelopment Approach (DEA) was developed by Charnes et al. (1978) in his study of the relative efficiency between multiple service units providing homogeneous services. The Mattingley Publishing Co (2020) used the non-parametric model Malmquist- DEA approach to compare the efficiency of the state-owned Life Insurance Cooperative of India Limited (LIC) with that of selected private sector insurers in India for the period 2008–09 to 2017–18 through technical efficiency, pure technical efficiency, scale efficiency, and total factor productivity. The efficiency of private sector insurance companies was analysed; Odeck (2006). To enable a more accurate assessment of regional projects to reduce road fatalities, the DEA-Malmquist index method was used to analyse road safety performance; Xin Zhang and other scholars used a structural equation modelling (SEM) approach to determine the impact of green banking activities on green financing and bank environmental performance, and further research explored the impact of the main theories and management policies, suggesting his limitations and future research directions; Wang Liang (2014) studied the operational efficiency of listed commercial banks in China based on data envelopment analysis; Huang Coronation and Du Yafei (2014) used the data envelopment method to empirically study the efficiency of commercial banks in China; James Bryan Jessica Clempner Simon Low (2020) examined the role of retail banks in combating the new coronavirus outbreak in the context of the far-reaching impact that the new coronavirus (COVID-19) has already had on people's lives and the global economy, suggesting the need not only to implement immediate tactical responses and government support measures, but also to develop more refined COVID-19 response credit policies; Yang Zifeng and Bai Jiping (2021) proposed optimising the credit structure for the development of green credit in Jinzhong City to achieve their own sustainable development in a low-carbon context; Wang Binying (2022) questioned whether green credit would enhance the business performance of commercial banks based on listed banks in low-carbon pilot cities and obtained accurate answers; Fan Yibin and Wang Weifang (2011) analysed (2011) the current situation and problems of green credit business development of commercial banks in China under the low-carbon economy and put forward suggestions for improving green credit business of commercial banks; Wang Xianju (2012) studied the policy environment and difficulties of commercial banks in implementing green credit in a low-carbon context and explored effective ways to implement it. Taslima Julia and Salina Kassim (2020) study green banking to understand its characteristics and objectives and propose directions for sustainable development; Faridah Djellal and Faïz Gallouj (2016) conduct this work to study the extent to which services and service innovation contribute to sustainable development, concluding that service innovation for sustainable development: a path to greening through service innovation; Antunes et al. (2022) uses a data envelopment analysis model to assess efficiency in China over the period 2012–18 and concludes, among other things, that bank size has a positive impact on the development of non-traditional banking.

In summary, various scholars at home and abroad have conducted more research on green credit in commercial banks under the epidemic, but there are still many shortcomings, due to the relative lack of literature examining the top 10 banks in mainland China as a whole and the relatively small amount of literature analysing panel data. Therefore, this paper will take the top 10 banks in mainland China as the object of study. Applying the DEA-Malmquist index method, an evaluation index system is constructed based on the panel data of the top 10 banks in China from 2015 to 2021 to analyse and evaluate the green credit performance of commercial banks in the hope of improving service innovation, technological progress and creating a green financial environment.

Model construction

In order to scientifically study the impact of green credit on banks’ business performance, this paper applies the DEA-Malmquist index model to dynamically analyse the relevant indicators of 10 banks for the period 2015–21.

In DEA, the unit or organisation being evaluated is referred to as a decision-making unit (DMU for short.) DEA uses linear programming to construct a data envelope curve by selecting multiple input and output data for a decision-making unit with the best input and output as the production frontier. Valid points are located on the frontier and are assigned an efficiency value of 1. Invalid points are located outside the frontier and are assigned a relative efficiency value index greater than 0 but less than 1.

DEA-Malmquist index model

The traditional DEA model can only measure the static relative efficiency of different decision units at the same time, while the DEA-Malmquist index model is a dynamic efficiency analysis of the data of each decision unit in different periods. In this paper, the DEA-Malmquist index model is chosen to make the results of the run more accurate and the analysis more convincing. The Malmquist index is calculated using the distance function (E) and is mathematically represented as follows.

Selection of indicator system

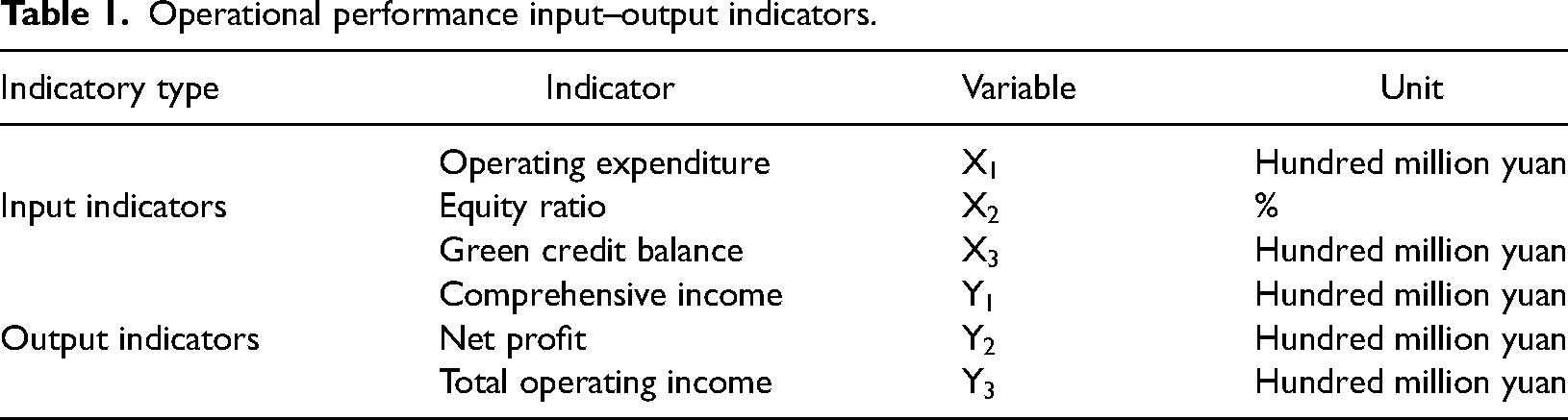

The performance assessment of commercial banks’ green credit operations in the context of epidemic prevention and carbon reduction studied in this paper is divided into two aspects: input indicators and output indicators. The input indicators are mainly the financial indicators and green credit indicators of the banks, where the financial indicators include the operating expenditure and equity ratio of the banks. When studying the factors influencing the comprehensive efficiency of Chinese commercial banks, Chi et al. (2006) and others chose operating expenditure as one of the input indicators, taking into account the profitability of banks. Meanwhile, this paper considers the analysis in terms of the impact of green credit on the operating performance of Chinese commercial banks with reference to the study by Li Yacong and Zhang Ruibin scholars (2022). Zhao Qing scholars (2010) mentioned that the equity ratio indicator can affect the operating performance of banks in terms of their long-term solvency. The output indicators in this paper are consolidated earnings, net profit and gross operating income, and the impact of the epidemic and banks’ green credit is considered to analyse banks’ operating performance in terms of their profitability. Based on the above considerations, we have established the indicator system as shown in Table 1.

Empirical analysis

Malmquist index and decomposition of green credit operating efficiency in the banking industry by year

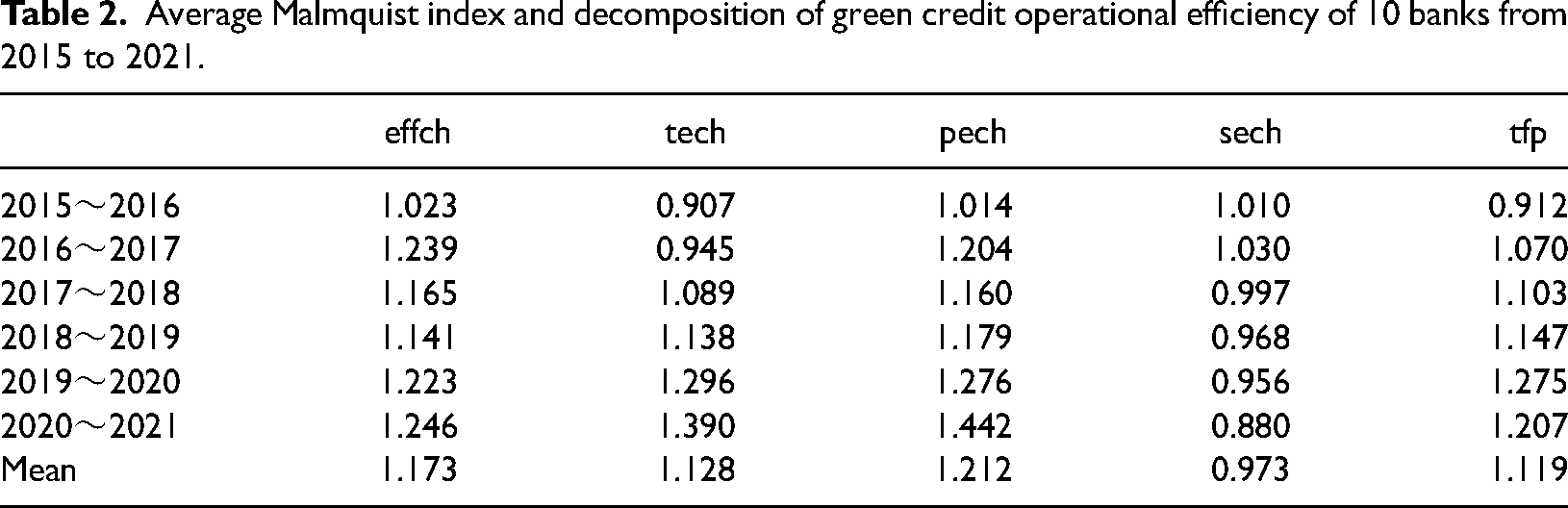

Malmquist can dynamically reflect the changes of green credit operating performance in the banking industry, and the Malmquist index is applied to decompose the green credit operating performance productivity of 10 banks in the banking industry from 2015 to 2021, and the results of the analysis are shown in Table 2.

Operational performance input–output indicators.

Average Malmquist index and decomposition of green credit operational efficiency of 10 banks from 2015 to 2021.

As can be seen from Table 2: In terms of overall efficiency changes, the average value of total factor productivity (tfp) of the banking industry as a whole from 2015 to 2021 is 1.119, that is, an average growth rate of 11.9%, and the average value of the total factor productivity index is greater than 1 in every 2 years from 2016 onwards, indicating that the efficiency of green credit operations in the banking industry has been in a stable upward phase in the past 5 years. Comparing the tfp of the banking industry from 2015 to 2019 with that from 2020 to 2021, it can be found that the total factor index of green operation in the banking industry increases rather than decreases under the influence of the epidemic, which means that the investment in green credit business in the banking industry does not decrease with the epidemic, but increases continuously in technology, management and resources in response to the development trend of carbon finance in recent years, which has led to the improvement of green credit operation efficiency in recent years. (1) The Malmquist index is further decomposed into efficiency index of technological change (effch) and technological progress index (tech), which shows that the mean value of the index of technological efficiency change is 1.173, with an average annual increase of 17.3%, while the mean value of the index of technological progress is 1.128, with an average annual increase of 12.8%, which can be understood that the improvement of technical efficiency is the key to the continuous improvement of the operational performance of green credit business in the banking industry, while the technological progress of the banking industry as a whole is not the dominant factor, although it is a catalyst for banks to develop green credit business in the context of the epidemic and carbon reduction finance. The technical change efficiency index and technical progress index values for 2020–21 reach their peak values compared with previous years, which shows that the overall efficiency of green credit business in the banking industry is not affected by the epidemic. The technical efficiency and technical progress efficiency of the banking industry are good, indicating that the structure of the banking industry's green credit business has been continuously adjusted and innovated during this period, and the organiaational management investment has been followed up, which is good overall. (2) Then it decomposes the technical progress change index into pure technical efficiency change index (pech) and scale efficiency change index (sech). The average value of pure technical efficiency change index is 1.212, and the average annual increase of pure technical efficiency is 21.2%, which indicates that the performance level of green credit business in the banking industry is improving continuously. During 2015–21, the banking industry will continue to improve green credit products and systems, and pure technical efficiency will continue to improve. The value of pure technical efficiency change index is always greater than 1, and this index reaches the maximum value in 2020–2021, which shows that under the epidemic, the management and technical development of green credit business of banks are not affected, and they are still in the stage of continuous climbing, which is the root cause of the overall operational performance improvement; the average value of scale efficiency change index is 0.973, and the average annual decrease in scale efficiency is 2.7%, and the value has been less than 1 and decreasing since 2017, and it is also observed that the scale efficiency value in 2020–21 has decreased by 7.6% compared with the value in 2019–20, which is too large, which shows that the change in scale efficiency hinders the improvement of technical efficiency index, and this hindrance is especially obvious after the epidemic. However, this does not mean that the banking industry needs to reduce the scale of green credit business, but more importantly, to optimise the resource allocation of green credit business so as to achieve the optimal performance of green credit operations.

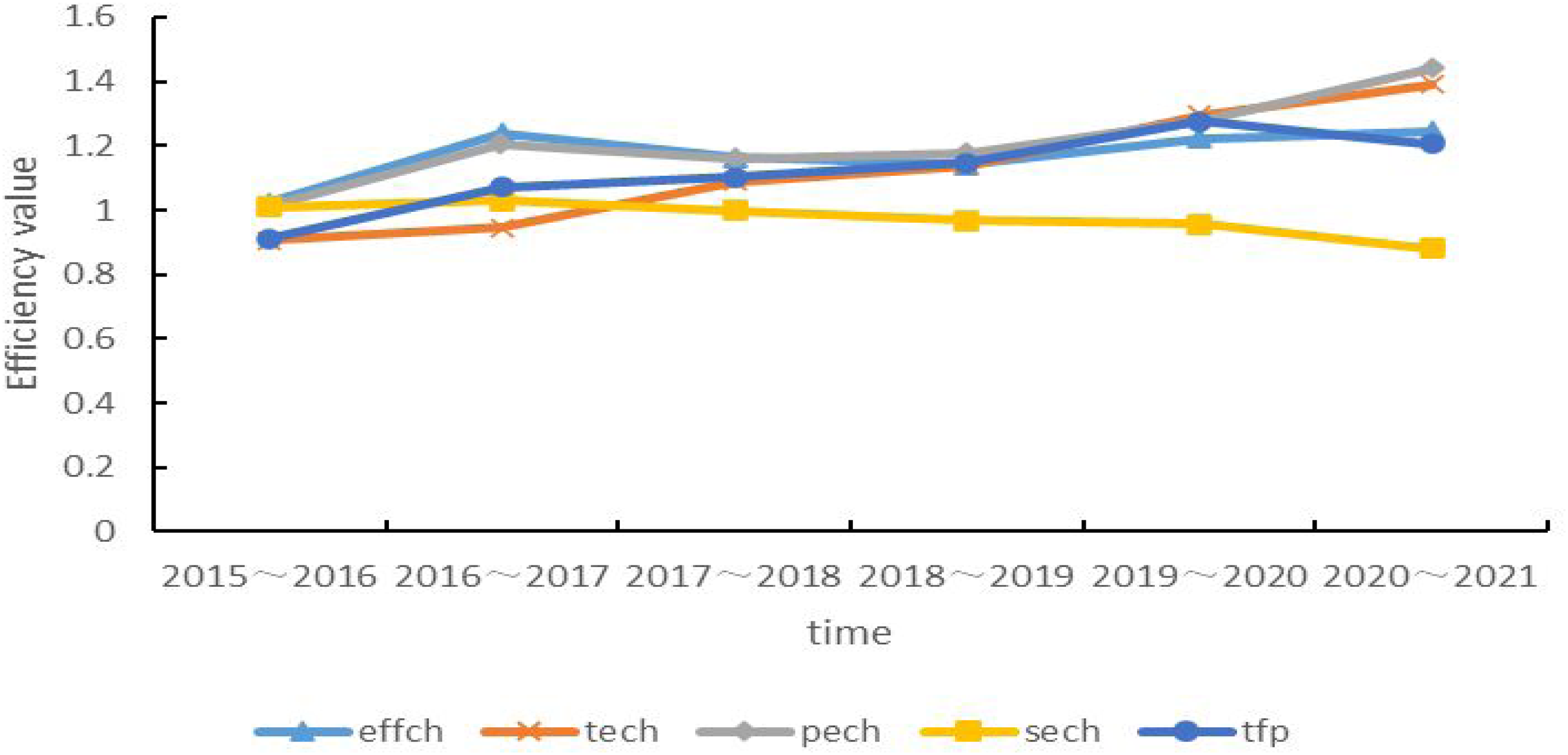

The Malmquist index of green credit operation efficiency in the banking industry and the time dynamic curve of the decomposition are plotted on the basis of Table 3, and the changes of each index can be observed more clearly, as shown in Figure 1. From 2015 to 2020, the average value of total factor productivity of the 10 banks is on an upward trend. From 2020 to 2021, although there is a decline, the overall situation is stable. It can also be seen that although the development of green credit operation in China's banking industry is in the stage of continuous growth, the growth rate has been slow and maintained at a stable level of continuous development. Although the epidemic has slowed down the speed of green credit operation efficiency improvement in the banking industry, it has not affected its continuous improvement; the change index of technical efficiency of 10 banks reached the highest value in 2016 to 2017 and the lowest value in 2017 to 2018, after which it gradually climbed with each year. This fluctuating upward trend of technical efficiency values reflects the continuous rise of organisational and management efficiency of green credit business in the banking industry; the technical progress index of 10 banks increased year by year from 2015 to 2021, which indicates that the production frontier surface of green credit business in the banking industry is moving forward and the level of technical development is constantly improving; the scale efficiency of 10 banks decreased year by year from 2015 to 2021, and decline expands from 2020 to 2021, while the pure technical efficiency values show a fluctuating upward trend. Combining the trends of the pure technical efficiency values and scale efficiency values, it can be concluded that the operation and management efficiency of the green credit business in the banking industry is constantly improving, which is an important reason contributing to the improvement of the overall operation performance. However, the resource allocation efficiency becomes an obstacle and the emergence of the epidemic aggravates the difficulties in resource allocation and generates resource losses.

Trend of changes in the five major efficiency values of the 10 banks from 2015 to 2021.

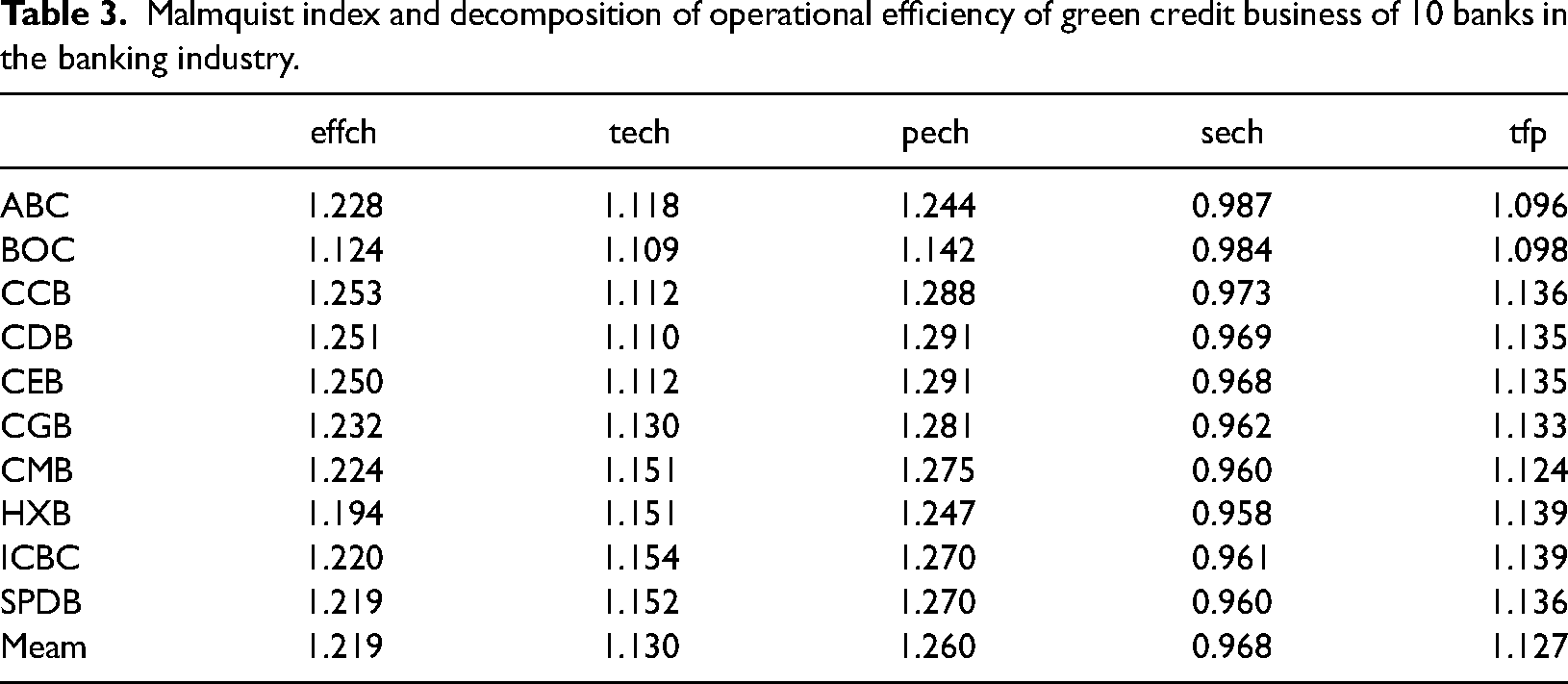

Malmquist index and decomposition of operational efficiency of green credit business of 10 banks in the banking industry.

Malmquist index and decomposition of green credit operation efficiency of banks in the banking industry

As shown in Table 3, the total factor productivity of all 10 banks is greater than 1 during 2015–2021, which indicates that the green credit operating performance of these 10 banks is increasing. Among them, two banks, HBX and ICBC, have the highest total factor productivity values, which indicates that their green credit operating productivity has increased the most, with an increase of 13.9% over the seven-year period, followed by two banks, CCB and SPDB, both with an increase of 13.6%. In contrast, BOC and ABC banks have lower green credit operating productivity with only 9.8% and 9.6% respectively.

Further decomposition from the Malmquist index is as follows: the change index of technical efficiency and the change index of technical progress of these 10 banks are both greater than one, and the increase of technical efficiency of each bank is significantly greater than the increase of technical progress, which is consistent with the overall annual Malmquist index decomposition results, and both indicate that the improvement of technical efficiency is still the dominant factor in the improvement of green credit operating efficiency. It also shows that these 10 banks are following the development of carbon finance and actively promoting the innovative development of green credit business. The technical efficiency value of HXB is smaller than the average value, so the improvement of its green credit operation performance can start from technical efficiency and strive to reach the average level; while for ABC, CCB, CDB, and CEB, the four banks whose technical progress index values do not reach the average value, they should focus on technical progress and consider increasing the introduction of talents to improve their overall performance; Aamong them, BOC's technical efficiency index and technical progress index both do not reach the average level, so both technical progress and technical efficiency improvement are helpful for their overall performance improvement; From the view of decomposing tech into pech and sech, the pech of all 10 banks is greater than 1, while sech is less than 1, which means that the pure technical efficiency of each bank is increasing, while the scale efficiency is decreasing, which means that the pure technical efficiency is the key factor for the improvement of technical progress index, while the scale efficiency inhibits the further improvement of technical progress index, and the resource allocation of each bank needs to be optimised.

In summary, the changes in green credit operating efficiency of the 10 representative banks are consistent with the overall direction, technical efficiency is the key factor for the improvement of green credit operating performance in the banking industry, and the epidemic background does not affect the sustainable development of green credit business in the banking industry. The phenomenon that the scale efficiency does not exceed 1 either from the sub-year or the sub-bank also indicates that the unreasonable resource allocation is the main reason that hinders the further improvement of the performance, and in the future, each bank can reasonably formulate the system and refine the management from the perspective of optimising the resource allocation.

Conclusion

This paper conducted an empirical study on the green credit operation efficiency performance of 10 banks in mainland China and obtained the following conclusions: (1) The total factor productivity of the banking industry in mainland China from 2015 to 2021 was greater than 1 overall except for 2015 and showed a fluctuating upward trend, with the mean value greater than 1 indicating that the green credit operation efficiency of the banking industry has steadily improved and the overall efficiency of the green credit operation of the banking industry has not been a significant impact of the epidemic. (2) Further analysis revealed that the mean value of the technical efficiency change index was greater than the mean value of the technical progress index, which can be interpreted as an important reason for the rising performance of green credit operations in the banking industry, while technical progress also provided a supporting role for the rising performance of operations. (3) The average value of the scale efficiency change index from 2015 to 2021 is less than 1, and it is less than 1 from 2017 and continues to decline, which shows that scale efficiency hinders the rise of the technical efficiency index, and this hindrance is magnified when the epidemic occurs. Banks should pay more attention to optimising the allocation of resources for green credit business, to improve green credit business performance. (4) The magnitude of change in total factor productivity and the influencing factors of the 10 banks are all related to technical efficiency, indicating that the improvement of technical efficiency is the dominant factor in the improvement of green credit business efficiency. (5) The pure technical efficiency of all 10 banks is increasing while scale efficiency is decreasing, indicating that pure technical efficiency is a key factor in the improvement of banks’ technical progress index, while scale efficiency inhibits further improvement of the technical progress index. At the same time, as the epidemic exacerbated the difficulty of allocating resources to green credit operations in the banking sector, banks should focus on overcoming the risks faced by the epidemic, such as shutdown control and lagging, while realising the key role of resource allocation in improving overall operational performance. Technological efficiency is the most important reason for the rise in operational performance of green credit business in the banking sector, and it is clear from the study that in the context of the epidemic and carbon reduction had little impact on green credit business in the banking sector. Of course, under certain conditions, technological progress also provides a boost to the rise in operational performance. Secondly, economies of scale hindered the improvement of technical efficiency indicators and the misallocation of resources was the main reason for the further improvement of performance. In summary, the improvement of technical efficiency is the leading factor in the improvement of green credit operational efficiency.

Green credit, as one of the important products of green finance in China, is also receiving more and more attention from financial institutions and investment entities. It is characterised by the innovation of financial products, the enthusiasm of market input and the sustainability of social benefits. And commercial banks, as the main body of reasonable allocation of funds, have become the leaders and main force in the current development of green financial credit. In the process of developing green credit, commercial banks have to take on more social responsibility than developing traditional credit. Therefore banks should focus on improving the technical efficiency of banks as a way to enhance the efficiency of their green credit operations.

At present, energy security is a widespread concern worldwide, and energy security cannot be separated from the long-term development of transitional finance such as green finance, and the issue of allocation optimisation found in the study is the key to the long-term development of green finance. We should start from policy formulation at the macro level and organisational management at the micro level to do a good job of allocating green financial resources in the financial market in the banking sector to provide some security for energy.

Supplemental Material

sj-pdf-1-eea-10.1177_01445987231162994 - Supplemental material for Green credit operation performance evaluation of commercial banks in the context of epidemic and carbon reduction

Supplemental material, sj-pdf-1-eea-10.1177_01445987231162994 for Green credit operation performance evaluation of commercial banks in the context of epidemic and carbon reduction by Wentsao Pan, Zhonghuan Wu, Wenxuan Shen, Chan Wen, Ziqi Li, Xiuli Liao and Menglei Wu in Energy Exploration & Exploitation

Supplemental Material

sj-pdf-2-eea-10.1177_01445987231162994 - Supplemental material for Green credit operation performance evaluation of commercial banks in the context of epidemic and carbon reduction

Supplemental material, sj-pdf-2-eea-10.1177_01445987231162994 for Green credit operation performance evaluation of commercial banks in the context of epidemic and carbon reduction by Wentsao Pan, Zhonghuan Wu, Wenxuan Shen, Chan Wen, Ziqi Li, Xiuli Liao and Menglei Wu in Energy Exploration & Exploitation

Footnotes

Acknowledgements

This research was funded by the Hunan Philosophy and Social Science Foundation Project no. 20YBA121.

Author contributions

The authors confirm their contribution to the paper as follows: W-TP: conception of the study framework and methodological design. ZHW: data collection. WXS: analysis and interpretation of results. CW: writing research methods and analysis of data. ZQL: data organisation. MLW: writing the introduction. XLW: reference search. All authors: the final version of the manuscript.

Data availability

The original contributions presented in the study are included in the article or supplementary material, further inquiries can be directed to the corresponding author/s.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical approval

Written approval for the publication of this paper was obtained from the Hunan University of Science and Engineering and all authors.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Hunan Philosophy and Social Science Foundation Project, (grant number 20YBA121).

Supplemental material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.