Abstract

Organisations in many countries operate employee stock purchase plans. Research has focused on employees’ current employee stock ownership (ESO) enrolment decision but, as plans are often ongoing forms of compensation, employees will likely have made the decision before. Drawing on the theory of habit, we investigate whether experience of enrolment decisions influences the current enrolment choice. We also consider how decision experience affects the decision-making process. Using employee-level data from two Australian companies, we find that the more an employee has made a particular choice in response to repeated company invitations, the more they are likely to repeat it. We also find that employees with prior experience of ESO enrolment decisions make a quicker decision whether to join or not. Those making the decision for the first time take longer and are more reliant on advice from others. The findings show that understanding share plan participation requires a temporal consideration of employee behaviour.

Introduction

Many large organisations around the world operate plans to enable employees to purchase company stock. Examples include s.423 employee stock purchase plans in the USA, the Share Incentive Plan in the UK and ‘salary sacrifice’ plans in Australia. These plans are usually aimed at creating an identity of interest between employees and company, thereby encouraging employee retention (Hennig et al., 2023), greater work motivation and performance (Nyberg et al., 2018), and ultimately superior corporate performance (Kim and Han, 2019; O’Boyle et al., 2016). At a societal level, they may help to counter inequalities of wealth (Dudley and Rouen, 2021). The benefit to employees derives from access to dividends and capital gains from stock price increases, assisted by a range of benefits including share matches, discounts, ‘lookback’ features and favourable tax concessions (which also minimise downside risk). Babenko and Sen (2014) observe that enrolment in these plans is a ‘no-brainer’, with employees recommended to borrow on a credit card if liquidity constraints otherwise inhibit enrolment.

The employee stock ownership (ESO) literature has examined influences on the employee decision whether to enrol or not, highlighting the role of demographic influences (Pendleton, 2010), attitudinal orientations to share plans (Caramelli and Carberry, 2014; Paterson and Welbourne, 2020), financial knowledge and literacy (Ouimet and Tate, 2020) and the role of social norms and peer pressure (Bryson and Freeman, 2019; Oehmichen et al., 2018; Ouimet and Tate, 2020). Much of the ESO participation literature, especially that written from a finance perspective, assumes that employee decisions follow a boundedly rational process of collection and analysis of available financial information, with the apparent irrationality of not enrolling attributed to transaction costs arising from lack of knowledge and limited financial literacy (Babenko and Sen, 2014; Bryson and Freeman, 2019). The implication is that employees will become more likely to enrol in ESO plans as their understanding of them increases with repeat exposure to share plan invitations.

Evidence from the pensions and savings literatures questions whether employees make financial decisions in this way. These show that financial contribution and asset allocation decisions are subject to biases and heuristics, often leading to sub-optimal outcomes (Benartzi, 2001; Benartzi and Thaler, 2001; Thaler and Sunstein, 2009). One potential heuristic is doing what has been done before, especially if this has had favourable outcomes, without reviewing preferences or considering new information. The literature on habit and routines in social psychology and health highlights the role of experience of decisions in influencing current and future decisions on the same matter (Ouellette and Wood, 1998). Where behaviour/decisions are repeated on multiple occasions, cognitive processing can become automatic and can be performed quickly in parallel with other activities and allocation of minimal attention (Ouellette and Wood, 1998).

In less frequent decision-making contexts, such as an annual invitation to join a share plan, the decision is less automatic and ‘unthinking’, but experience in making the decision can influence the decision-making process, with reduced processing activity (relative to the first time the decision is made). When faced with repeat decisions, people will tend to make the same decision quickly, with reduced information search and processing of relevant information (Verplanken et al., 1997). Research in financial behaviour shows that savings ‘habits’ play an important role in encouraging regular saving, with the strength of habit becoming stronger over time. Building on these results, it is plausible that many employees will make the decision whether to join based on what they did in previous ESO invitations.

The article examines two key issues: (a) the influence of previous enrolment experience on a current decision to enrol in an ESO plan and (b) the influence of decision experience on the way that this decision is made. Extant research highlights the role of ESO knowledge rather than experience of making ESO decisions. In this view, as knowledge of share plans, and the financial benefits attached to them, percolates through organisations, possibly through peer-assisted social learning, employees should become more willing to enrol (Babenko and Sen, 2014; Degeorge et al., 2004; Ouimet and Tate, 2020). The alternative view, which guides our analysis, is that employees can become ‘stuck in their ways’, consistent with the theory of habit (Hodgson, 1997). If they have not enrolled in the past, they will likely not enrol now. Equally, if they have enrolled in the past, they will probably enrol again.

We evaluate the role of ESO experience using employee survey data from two organisations in Australia with stock ownership plans. The two organisations operate in different industries, and have different types of workforces, but share very similar ESO plan designs due to common regulatory frameworks. They have also operated ESO plans for a similar length of time, with organisational inertia meaning that plans change very little, if at all, from year to year. This research design means that we can determine whether employees behave in similar ways across different industries, consistent with our predictions regarding the role of experience and habit. The stability of share plan characteristics also provides a supportive context for the development of habitual employee behaviour.

Our study contributes to the ESO literature in three ways. First, we highlight the role of ESO experience as an influence on ESO enrolment decisions The focus of research to date has been on a current ESO participation decision, often guided by an interest in the demographic and financial characteristics of (non) participants. However, ESO plans are usually a continuing component of an organisation’s compensation offerings (Stebe et al., 2022), meaning that most employees are likely to have made the ESO participation decision previously. We extend the ESO literature by investigating the effect of past ESO experiences on a current ESO participation decision. Second, we shift the focus away the ‘rational investment model’ of financial decision-making which implies that enhanced knowledge of financial instruments over time will lead to better decision-making, and argue that repeat exposure to share plan offers is likely to lead to an increased propensity to enrol by lowering the transaction costs arising from lack of ESO knowledge (Babenko and Sen, 2014). We look at a current decision in the context of what employees decided in the past and identify a path dependency in their decision-making. Third, we provide new insights on how employees make their enrolment decision. We find that most employees make a very quick decision, and we distinguish between ‘quick joiners’ (employees who make a quick decision to enrol) and ‘quick decliners’ (employees who make a quick decision not to enrol). While the same factors influence the speed of their decision-making, they operate in different directions.

Determinants of ESO participation

The literature on the determinants of participation in stock ownership plans has overlooked the role of experience in making the enrolment decision. Instead, it has mainly focused on identifying demographic or attitudinal correlates of the current enrolment decision (Brown et al., 2008). The most common approach posits that certain types of people are more or less likely to enrol. These studies identify demographic correlates of enrolment such as age, gender and income (e.g. Pendleton, 2010). Of particular note is the effect of income on the probability of enrolment (Degeorge et al., 2004; Engelhardt and Madrian, 2004; Pendleton, 2010) and on the size of contributions conditional on enrolment (Degeorge et al., 2004; Pendleton, 2010). Informed by the life cycle savings hypothesis (Modigliano and Ando, 1957), consumption smoothing is predicted to be associated with low enrolment among young people, rising through middle age, and declining as the retirement horizon looms into view.

Employee attitudes towards stock ownership and the company have also been used to explain enrolment and non-enrolment, often drawing on Klein’s (1987) three models of employee satisfaction with ESOPs: intrinsic, instrumental and extrinsic. Pendleton (2010) found that instrumental (desire for involvement) and extrinsic (desire for financial return) views of share plans were both associated with the decision to enrol in a share plan. Other researchers also report that employee concerns to secure financial returns from participation in an ESO plan is predictive of plan participation (French, 1987; Jackson and Morgan, 2011; McConville et al., 2016). Researchers have found that positive views of the company, especially organisational commitment (Caramelli and Carberry, 2014) and identity (Paterson and Welbourne, 2020; Pendleton, 2010), influence the enrolment decision or a preference for employer shares, though some studies have found that these attitudes have little effect (Dunn et al., 1991).

Standard rational optimising models in finance, tempered by the transaction costs of enrolment, have been used to investigate the ESO enrolment decision (Babenko and Sen, 2014; Ouimet and Tate, 2020). ESO enrolment provides economic benefits, and an assumption is that all employees should enrol in the plan even if they face liquidity constraints. Non-enrolment is explained by transaction costs such as lack of knowledge about stock ownership along with low levels of financial literacy. The implication is that enrolment rates should increase as knowledge and understanding of ESO is enhanced by repeated company offerings. There has been very little empirical investigation of this: the one study investigating this finds that experience of previous ESO offers has a negative rather than a positive effect on the probability of joining the ESO plan, though financial expertise, proxied by employment in a job requiring financial knowledge, is positively related to enrolment (Rapp and Aubert, 2011).

Researchers have investigated the role of peer effects, with enrolment rates found to be higher where a higher proportion of peers have joined the plan (Bryson and Freeman, 2019; Oehmichen et al., 2018; Ouimet and Tate, 2020). Drawing on earlier findings on retirement savings (Duflo and Saez, 2002) and theoretical work by Kandel and Lazear (1992), these studies attribute peer effects to social learning (Ouimet and Tate, 2020), peer pressure (Bryson and Freeman, 2019) and social norms (Duflo and Saez, 2002).

While providing useful insights into ESO participation, researchers have evaluated participation decisions in isolation from previous ESO experiences. They do not consider whether employees are enrolling in a plan for the first time or are continuing their previous patterns of ESO participation. This omission is important because, as an ongoing element of a compensation plan, it is likely that many employees will have made an ESO enrolment decision previously (Stebe et al., 2022). Their current ESO decision to enrol (or not) seems likely to be affected by what they have done previously.

Multiple repeat behaviour in a stable context may be viewed as a ‘habit’. Where behaviour/decisions are repeated on multiple occasions, cognitive processing can become automatic and can be performed quickly in parallel with other activities and require minimal attention (Ouellette and Wood, 1998). Past behaviour is a significant predictor of future behaviour, independent of attitudes, intentions, norms and control (Ouellette and Wood, 1998). There is empirical support for the importance of habitual decision-making across many disciplines. Evidence from psychology, consumer marketing and health shows that previous behaviour is a significant predictor of current and future behaviour (Kidwell and Jewell, 2008; Lindbladh and Lyttkens, 2002; Ouellette and Wood, 1998). Studies of financial decision-making have also found that experience is an important influence on current decisions (Kidwell and Jewell, 2008; Loibl et al., 2011). There is also a long tradition in sociology highlighting the importance of habit (Camic, 1986), with recent theoretical discussions viewing habit as a form of subjective rationality (Esser, 1990).

In less frequent decision-making contexts, such as an annual invitation to join a share plan, the decision is less automatic and ‘unthinking’, but experience in making the decision can influence the intent to decide as well as the decision process itself, with reduced processing activity (relative to the first time the decision is made). Research in financial behaviour shows that savings ‘habits’ play an important role in encouraging regular saving, with the strength of habit becoming stronger over time (Loibl et al., 2011).

Regular invitations to enrol in repeat offerings of a stock purchase plan are amenable to decision-making based on previous decisions. For most employees, their current ESO plan will not be the first they have been invited to join: in our sample just 5% are ‘first-timers’ (first time enrolling in an ESO). In Australia, companies with all-employee subscription-based share plans issue annual invitations to enrol in the plan (for a year), with information about the forthcoming plan typically sent to employees by email towards the end of the preceding financial year. This information sets out the procedure for enrolling in the plan, and how payments to the plan will be taken. This information changes very little from year to year. More bespoke information, such as the economic prospects for the company and its share price over the coming year, is not provided in these communications. Nor is information tailored to the individual’s financial and tax circumstances, with the generic nature of the company-provided materials being due to concerns about legal infringements concerning the provision of financial advice (Benartzi, 2001; Liang and Weisbenner, 2002). Independently sourced information about the prospects for the company and its share price can be difficult for an employee to interpret, so experience may be used as a substitute for information search and cognitive processing. Given substantial evidence that individuals respond in the same way over repeat decisions, and that decision experience influences current decision-making, we predict that similar processes will be at work with stock plan decision-making. We therefore propose the following hypothesis

H1: Experience in making a decision to enrol increases the probability of enrolling in the current plan.

Experience of making the same decision may influence the current decision-making process, and at the expense of a full consideration of relevant current information. Where the current decision to be made is identical or very similar to a previous decision, decision-makers may assume that the same conditions apply as in the previous situation (Aarts et al., 1998; Verplanken et al., 1997). Aarts et al. (1998) show that where a decision or behaviour is repeated there is often greater use of heuristics, less cognitive processing and decreased information search. Verplanken et al. (1997) show that those who have experience of deciding in a certain way are more likely to focus any information search on the habitual choice than on alternative choices (see Kidwell and Jewell, 2008 for discussion). The similarity between the current and previous decisions may also mean that individuals do not re-visit their preferences (Samuelson and Zeckhauser, 1988). It seems likely therefore that the more experience an employee has in making a particular decision, the more likely the current decision will be made quickly, with previous decision choices repeated. This will tend to exclude any reconsideration of preferences or benefits arising from alternative decision outcomes. This reasoning gives rise to following hypothesis:

H2: The greater the amount of experience in making the stock plan enrolment decision, the quicker the enrolment decision will be made.

Methods

Survey approach

To test these hypotheses, two companies in Australia were chosen for data collection. They were selected to provide variation in industry context and workforce characteristics, and thus to facilitate evaluation of the generalisability of the predicted employee behaviour. Company A was formed in the late 1970s and has been listed on the Australian Securities Exchange for 30 years. It is a market leader in financial management, registry and governance services for companies. The workforce is predominantly office-based and much of the work involves the design and operation of information processing systems. The company has offices in all the mainland Australian capital cities. It also has operations in 21 other countries, but these employees are not included in the research. Company B traces its origins back to the late nineteenth century. At the time of the research, it was an integrated fuels manufacturer, distributor and retailer, with a varied workforce ranging from highly skilled chemical engineers through to retail staff. It was a market leader in its sector in Australia and was listed on the Australian Stock Exchange. After the research was completed, it was acquired by an American multinational. The two companies therefore provide a variety of workforce types under the same ESO plan (due to government regulation of ESO in Australia).

Each company operates an annual ‘salary sacrifice’ plan, whereby employees can purchase up to $AU 5000 ($5500 in Company A, where the extra $500 is covered by a separate tax-exempt plan) of company shares per annum from their pre-tax salary. This type of scheme is long-standing in Australia though the $5000 cap dates from just under 10 years before the research was conducted. Employees can defer the tax payable until the earliest of either the end of the holding period (usually three years), termination of employment or 15 years (seven years for shares acquired before 2015) since the shares were acquired. 1 To secure these tax benefits, the plan must be open to at least three-quarters of Australian employees. This plan can be less advantageous to employees than in other jurisdictions because the tax liability can arise when the shares are released to the employee from the holding period rather than when the shares are disposed of.

All eligible employees (those employed for a minimum eligibility period) are sent an invitation in the middle of May to enrol in the plan for the forthcoming financial year commencing in July. The average amount subscribed by our respondents was $2479 (Company A = $2718; Company B = $1782). The companies have been offering ESO plans for similar lengths of time: Company A for 17 years, Company B for 13 years. Experience is more likely to be a determinant of subsequent decisions when there is a stable context (Ouellette and Wood, 1998), so we calculated the share price volatility for both companies. In the year leading up to the offer, the annual share price volatility (measured as the standard deviation relative to the average price over the year) for Company A was 8.75% and for Company B 5.4%. This was somewhat lower than volatility in the market during this and preceding years (see https://tradingeconomics.com/australia/stock-price-volatility-wb-data.html). At the same time, the stock price of each company increased from the start of the preceding year to the time of the offer: 20 and 5% respectively.

To investigate the role of individual characteristics, attitudes and histories of stock plan participation, an employee survey was chosen as the most appropriate research instrument. We surveyed employees in September, around three months after the decision period closed to seek information on the decision they had just made. This timing was chosen so that the decision was fresh in the minds of potential respondents, and hence decision recall should be reliable (Holtom et al., 2022; Spector, 2019). Cross-sectional designs such as ours can be particularly appropriate when they are focused on a particular event that has recently taken place (Spector, 2019). In the survey we asked a range of questions concerning the enrolment decision, how it was made, previous enrolment (non-enrolment) in share plans, and assessments of the share plan and the company.

The survey was administered in collaboration with the company administering the share plans in each company. A link to the Qualtrics survey was sent to share plan managers in the companies, via the plan administrator. Consistent with good survey design (Holtom et al., 2022), we had no direct contact with any personnel in the participant organisations. There were no guaranteed financial rewards for completing the survey, but respondents were invited to submit their details separately (to preserve anonymity of responses) to a prize draw.

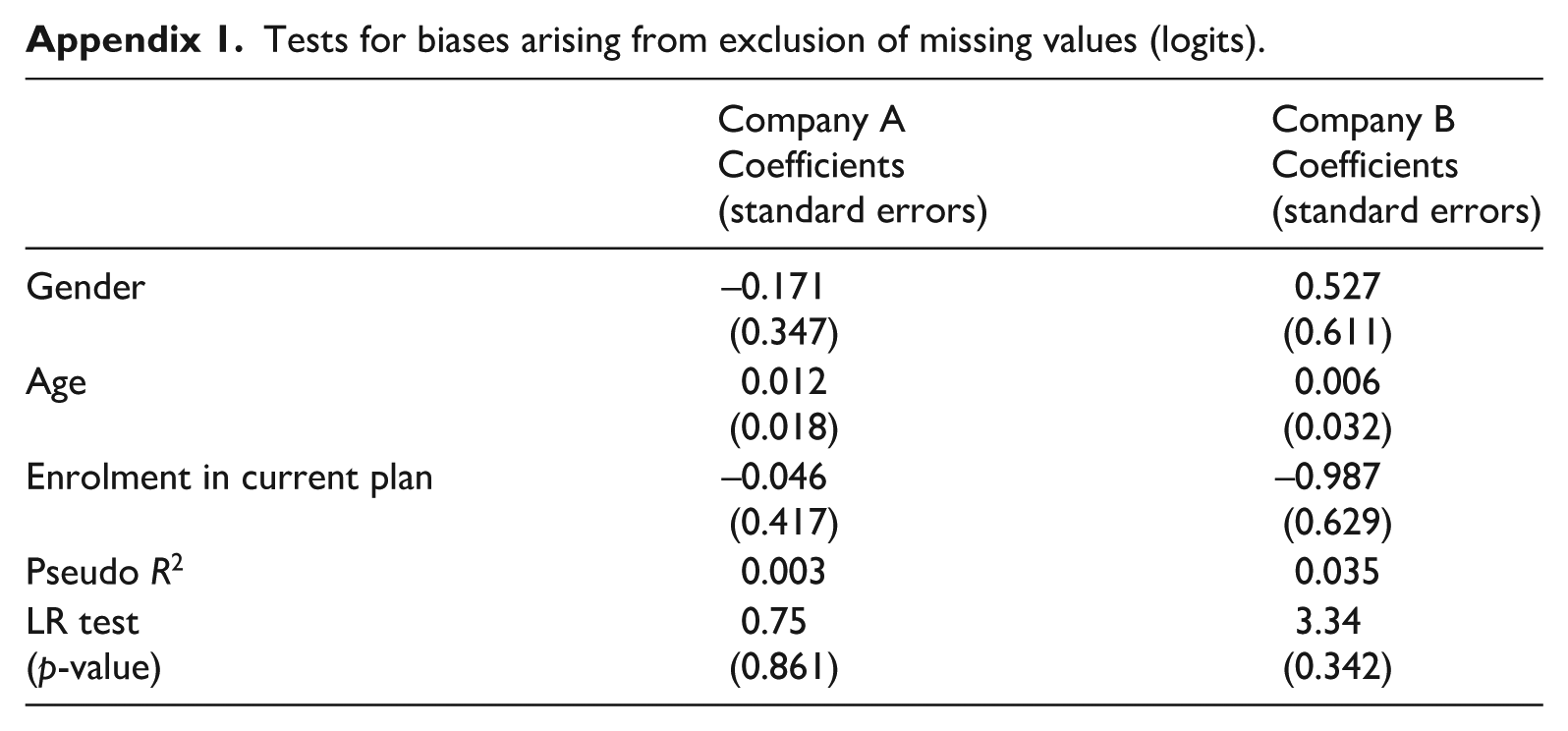

The survey was sent to 1458 employees in Company A (its entire Australian workforce) and to 978 employees based on the East Coast of Australia in Company B (around one-fifth of its total workforce). We received 753 completed survey questionnaires (500 for Company A, 253 for Company B), an overall response rate of 31%. Fifty incomplete surveys were removed as key information was missing, leaving 462 surveys for Company A and 241 for Company B. We tested for response biases that might arise from exclusion of cases with missing values (Goodman & Blum, 1996) by comparing the characteristics of people who provided some information on their response to the current share offer with those who provided full details of their share history for each company. The dependent variable was based on those who provided details on their full share history (coded 1) and those where information was missing (coded 0), while the independent variables comprised demographic characteristics (gender and age) and current plan enrolment. None of the independent variables differed significantly between the two groups, and the chi-square test of differences between each company model and a null model was not significant at p < 0.05 (see Appendix 1). An MCAR (Missing Completely At Random) test using the same variables suggested that missing values were randomly distributed (at p < 0.05) (Li, 2013; Little, 1988).

The ESO participation rate recorded in the survey was 79% in Company A and 56% in Company B. This was slightly higher than the actual participation rates recorded in the companies (67% in Company A, 50% in Company B). We compared respondent characteristics with those provided for all employees by the companies and, finding no significant differences, judged that these differences were unlikely to introduce substantial biases to the analysis.

Measures

Dependent variables

Two dependent variables are used in the analysis. Enrol records whether the employee joined the plan at the current invitation (1 = joined, 0 = not joined) to test H1. Decision speed records the time reported by respondents to make their (non) participation decision (to test H2). To generate Decision speed respondents were presented with several ordered categories ranging from ‘immediately’ to ‘longer than a month’ (see Appendix 2). We recoded responses to capture an employee’s immediate response to the plan invitation: 1 for immediate decision, 0 otherwise. Combining time taken to decide with Enrol generated four categories of respondents: quick yes (‘quick joiners’); quick no (‘quick decliners’); slow yes; slow no (‘slow deciders’). The two slow deciders groups were merged because the quick joiners and quick decliners are of primary interest.

Independent variables

We generated three measures of experience. First, ESO experience records the number of times the respondent has decided to enrol in the plan in the past (prior to the current decision). The number of times an employee has decided is a measure of the strength of a habit (Ouelette and Wood, 1998). Second, ESO last year records whether respondents enrolled in the plan last year (1 = yes, 0 otherwise). We include this measure of experience to capture the influence of a recent previous ESO participation as Katona and Harris (1978) suggest that recent experiences can be more influential than more distant experiences. Third, Decision ratio builds on ESO experience so that multiple decisions not to enrol in the plan become symmetrical to multiple decisions to enrol (rather than remaining at zero). These capture repeat decisions not to enrol as well as repeat enrolment decisions. After creating the ratio, 0.5 is subtracted from the value so that a preponderance of decisions not to enrol turns the variable negative. The resulting number is then multiplied by the number of times the decision has been made to capture the extent of experience. To test H1 we use ESO experience and ESO last year while we use Decision ratio to test H2.

Control variables

As noted earlier, researchers have identified the personal and financial characteristics of (non) participants. We therefore control for Gender, Age and Ends meet. We include gender as women often have lower rates of participation in the stock market (van Rooij et al., 2011; 1 for males, 0 otherwise). Age is important as participation in savings and share plans tends to rise with age though it is often found to fall close to retirement (Babenko and Sen, 2014; Degeorge et al., 2004; Pendleton, 2010). We use a continuous measure based on years. Ends meet controls for disposable income and liquidity constraints (Aubert and Rapp, 2010) by asking respondents ‘Overall, how difficult or easy do you find it to make ends meet in your household?’ Responses ranged from 1 ‘very difficult’ to 5 ‘very easy’ (Alessie et al., 2006). There are risks associated with ESO participation (Kruse et al., 2022). We control for Risk preference using a measure derived from the German Socio-Economic Panel which assesses the willingness of respondents to take or avoid risks (‘Are you generally a person who is fully prepared to take risks or do you try to avoid taking risks?’) using a slider scale from 0 (not at all willing to take risks) to 100 (very willing to take risks) (see Dohmen et al., 2011). To control the perceived risk associated with company shares (Stock risk) we asked, ‘How risky do you think it is to hold shares in the company in which you are employed?’ Participants could indicate between not at all risky (0%) up to exceptionally risky (100%).

Investing in an ESO is complex, so we include a measure of Financial ability. This is a four-item scale assessing self-perceived capability and confidence in managing financial matters, adapted from items in the Financial Self-Efficacy Scale (Lown, 2011). A representative item is ‘I am confident of my ability to make financial investment decisions’ with respondents being asked to rate their agreement on a 1–5 scale (alpha = 0.87). Knowledge of ESO measures respondents’ self-assessed knowledge of the features of stock plans because a lack of knowledge is a barrier to enrolment (Babenko and Sen, 2014). Six questions measure various aspects of ESO knowledge, each with the stem ‘How aware are you of’ followed by features of the ESO such as ‘how much can be paid into the share plan’, ‘how to sell shares’ etc. (alpha = 0.90). Stock attitude is a three-item measure capturing attitudes to stock ownership plans derived from Klein (1987). A representative item is ‘The share scheme is a great way to increase your income and wealth’ (alpha = 0.89).

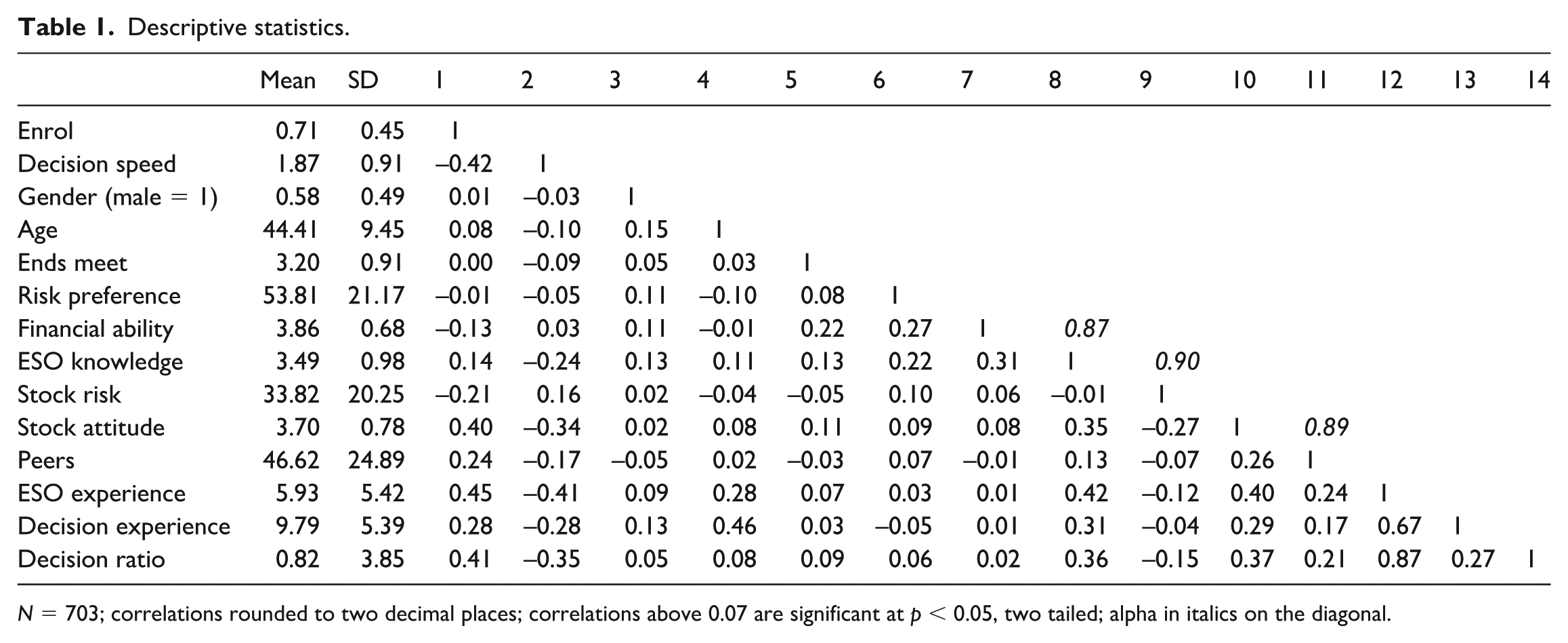

Peers can influence stock plan participation (Bryson and Freeman, 2019; Oehmichen et al., 2018; Ouimet and Tate, 2020), while social learning theory suggests that peer behaviour may also affect the approach to decision-making and the development of habitual behaviour (Bandura, 1977. We assess the effect of Peers based on a measure derived from Bryson and Freeman (2019) ‘What percentage of employees in your work unit do you think are participating in the share plan this year?’ It ranges from 0% to 100%. Means, standard deviations and correlations for study variables are provided in Table 1.

Descriptive statistics.

N = 703; correlations rounded to two decimal places; correlations above 0.07 are significant at p < 0.05, two tailed; alpha in italics on the diagonal.

Results

Determinants of ESO enrolment

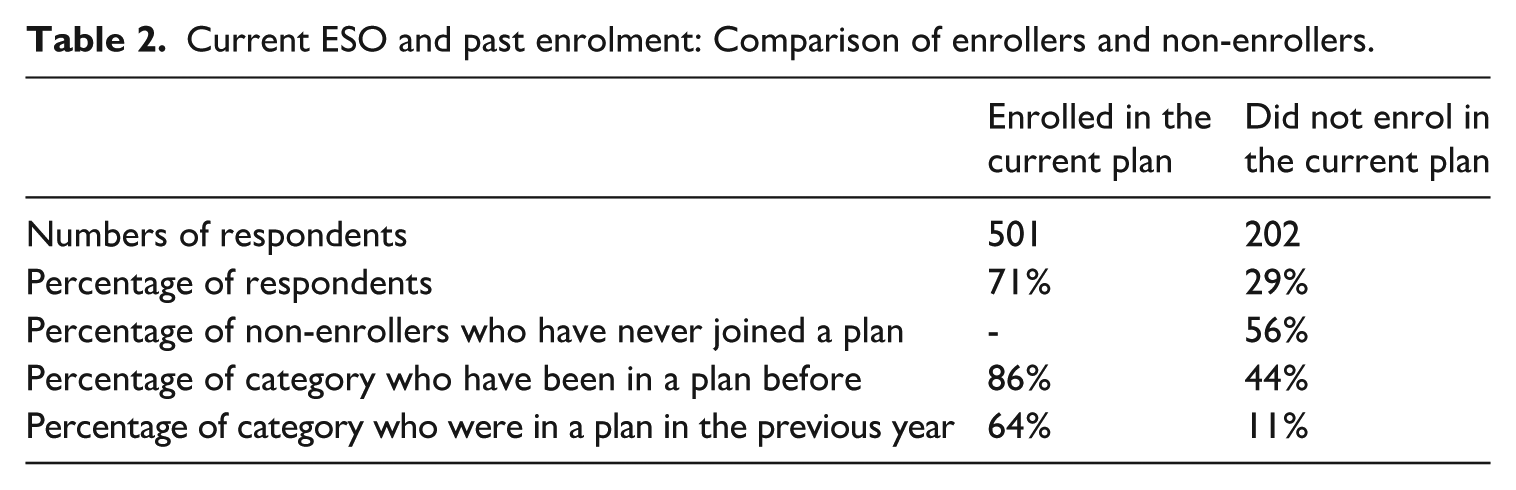

Table 2 provides data on the decision to enrol into the current offer and its relationship to the experience of previous stock plan enrolment: 71% of respondents enrolled in the current plan, of whom 86% have joined a plan before. Of the current enrollers, 64% had also enrolled in the plan last year. Turning to the non-enrollers, 56% have never joined a plan; 11% had, however, joined the plan last year. While there is some evidence of switching activity, a substantial proportion of respondents in the current year did what they had done in previous years.

Current ESO and past enrolment: Comparison of enrollers and non-enrollers.

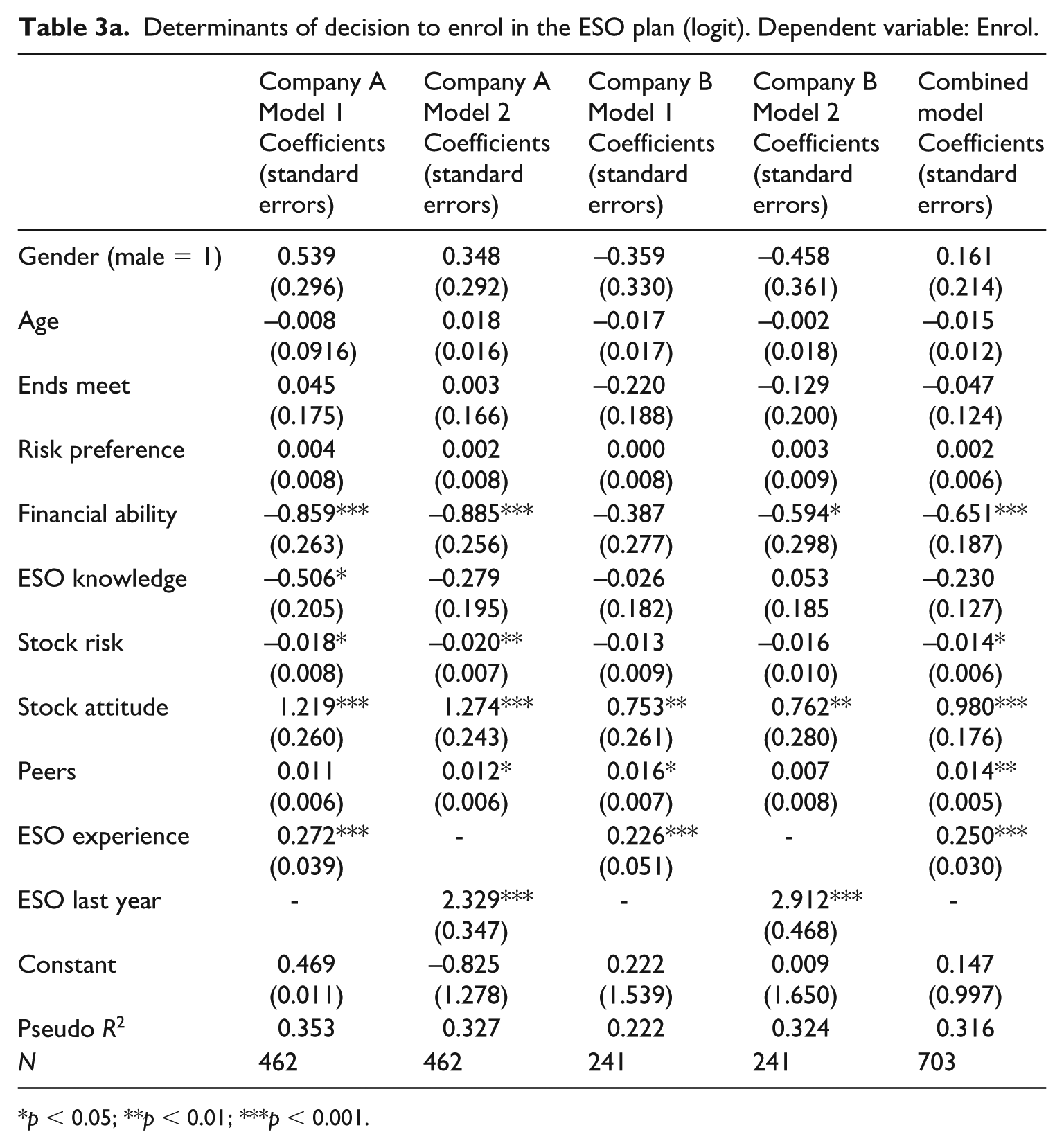

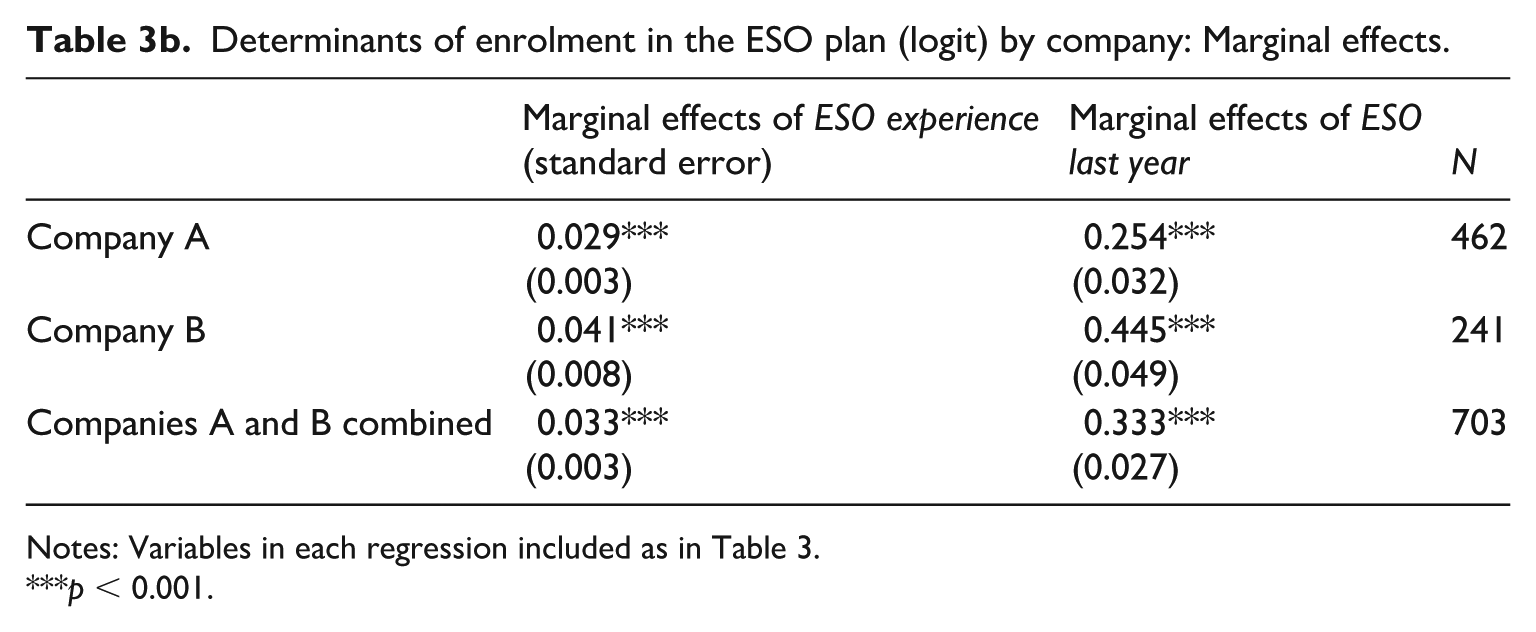

To test Hypothesis 1 (greater experience of being in the ESO plan in the past will affect the probability of joining the plan in the current year), we undertake a series of binomial logits with Enrol as the dependent variable. Table 3a presents separate models for the two companies, along with a combined model, using ESO experience as the independent variable. In an alternate model for each company, we substitute ESO last year as a measure of recent experience. Table 3b provides the marginal effects for these variables.

Determinants of decision to enrol in the ESO plan (logit). Dependent variable: Enrol.

p < 0.05; **p < 0.01; ***p < 0.001.

Determinants of enrolment in the ESO plan (logit) by company: Marginal effects.

Notes: Variables in each regression included as in Table 3.

p < 0.001.

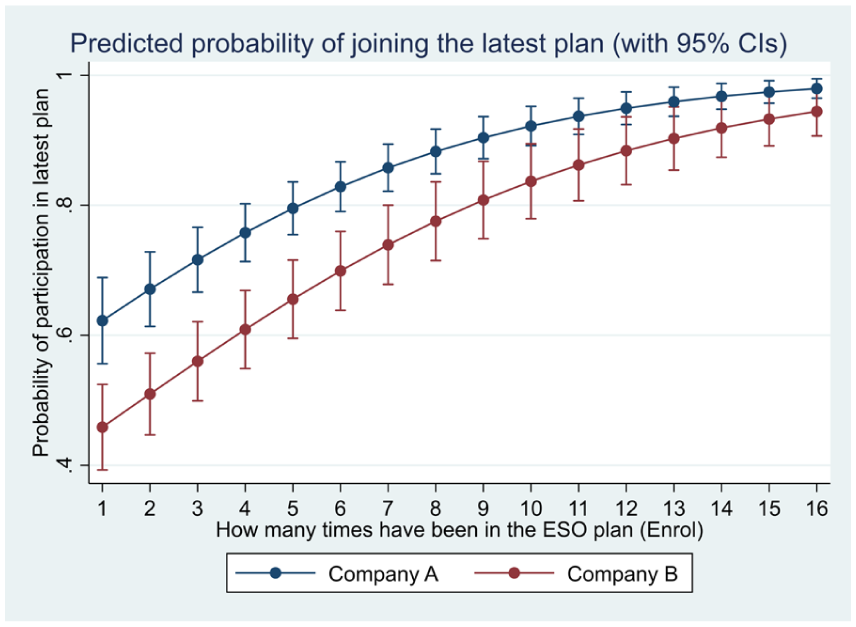

We find that ESO experience and ESO last year are significant at p < 0.001 in all models, with marginal effects ranging from 0.029 to 0.041 for ESO experience (a one unit change in ESO experience increases the probability of current enrolment by up to 4.1%) and from 0.254 to 0.445 for ESO last year (a one unit change in ESO last year increases the probability of current enrolment by up to 44.5%). Note that the difference between these two sets of marginal effects reflects measurement differences between the two variables: ESO last year is a 0,1 variable whereas ESO experience is continuous. Likelihood ratio tests comparing models for Companies A and B without the ESO experience variable and models including it show chi-square results of 70.58 and 24.23 respectively, both significant at p = 0.000. These results indicate that previous experience of being in ESO schemes has a similar positive effect between the two companies, irrespective of the measure of experiences. VIF figures (not shown) do not exceed 1.57, with most under 1.3, indicating that multicollinearity is not a problem with the models. Figure 1 (using ESO experience) shows how previous experience of being in ESO schemes increases the probability of joining the current scheme. These results thus support Hypothesis 1, with similar effects across two companies in different sectors.

Predicted probability of deciding to enrol in the plan based on previous experience (by company).

Regarding previous explanations of ESO participation, it is notable that the demographic variables are insignificant in all models, 2 and that financial ability has a negative rather than positive effect on the probability of joining the plan (significant in most models). In contrast to previous studies, liquidity constraints (Ends meet) have insignificant effects in all models (see Degeorge et al., 2004; Engelhardt and Madrian, 2004; Pendleton, 2010). (Knowledge of ESO is significant at p < 0.05 or better in Company A, Model 1, it becomes insignificant in all other models, indicating that there is little difference in knowledge of ESO between enrollers and non-enrollers once other factors are controlled for; cf. Rapp and Aubert, 2011.) Favourable attitudes to ESO as a financial instrument have a positive relationship with the probability of joining the current plan, as predicted by the literature (French, 1987; Jackson and Morgan, 2011; McConville et al., 2016). Peer effects also have a positive, albeit small, effect on the probability of joining in some models (Bryson and Freeman, 2019; Oehmichen et al., 2018; Ouimet and Tate, 2020).

These findings notwithstanding, the overriding finding from these models is the importance of previous ESO experience as an influence on joining an ESO plan. Hypothesis 1 is clearly supported: experience counts.

Speed of ESO decision-making

Most respondents make the decision whether to enrol in the ESO plan very quickly. As shown in Appendix 2, over half of respondents say that they made the decision whether to enrol or not ‘immediately’, with a further 14% indicating that they made the decision on the same day as receiving the invitation. This is more marked for enrollers than non-enrollers, with 68% of the former (52% of non-enrollers) indicating that they made an immediate decision. This speed of financial decision-making contrasts with the view that people should carefully deliberate and evaluate important financial decisions (Harrison, 2005).

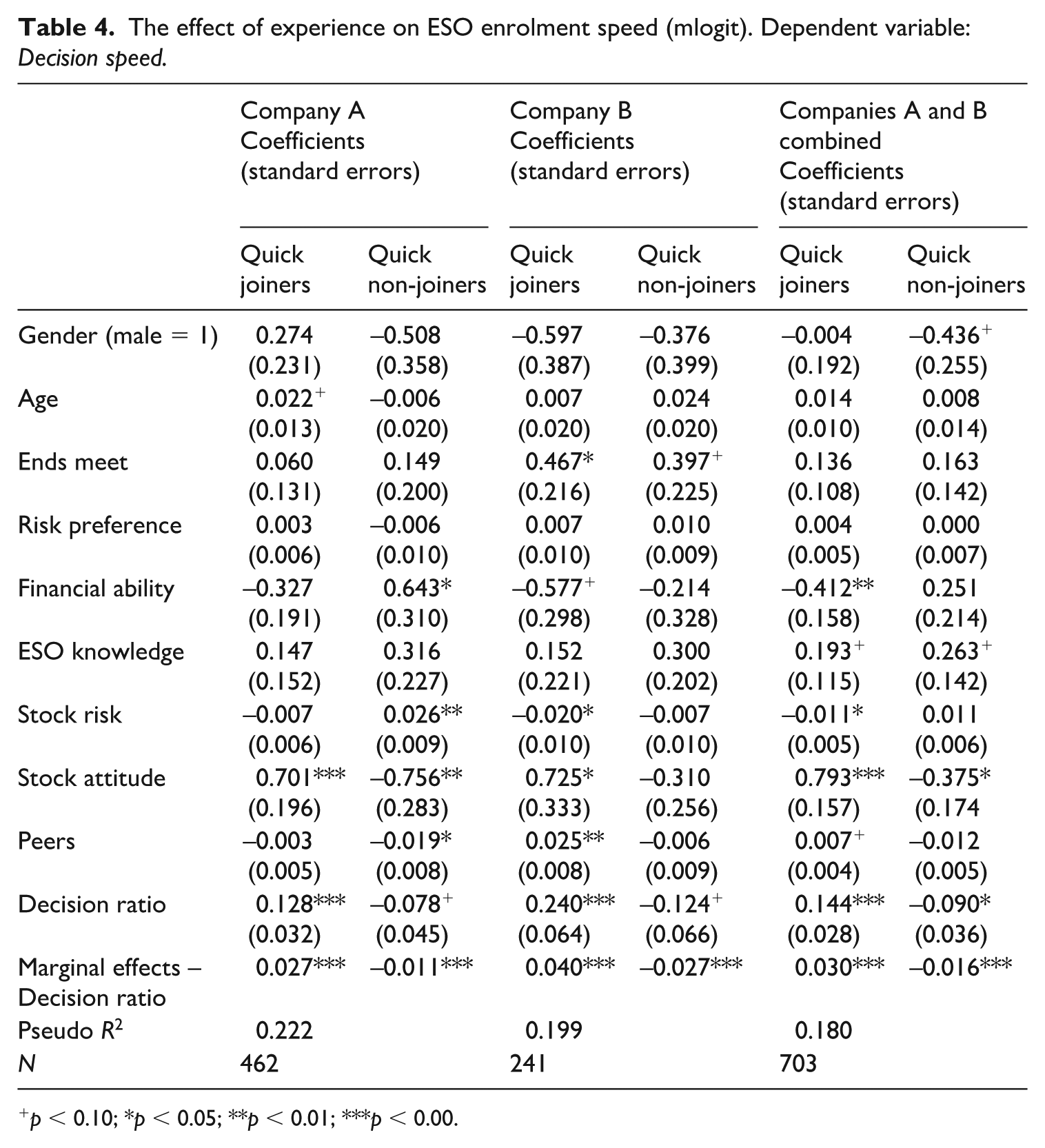

Turning to Hypothesis 2, we posited that experience of being in ESO plans will lead to quick decisions to join the current plan, while experience of declining to enrol in ESO plans will lead to a quick decision not to enrol in the current plan. We test the hypothesis by running multinominal logits where the dependent variable is Decision speed. The observed categories of the dependent variable are an immediate decision to enrol (‘quick joiners’), an immediate decision not to enrol (‘quick decliners’), with a slow decision serving as the base category. We use Decision ratio as the independent variable to give equal weight to enrolment and non-enrolment experiences. If experience functions as predicted, we anticipate a positive relationship with quick joiners and a negative relationship with quick decliners. As before, we compare the two companies, and it is anticipated that findings will be similar between them given the similarity and duration of their ESO plans. Table 4 presents results.

The effect of experience on ESO enrolment speed (mlogit). Dependent variable: Decision speed.

p < 0.10; *p < 0.05; **p < 0.01; ***p < 0.00.

The coefficients on Decision ratio are as hypothesised: positive for quick joiners and negative for quick decliners, for both companies. In each case, the coefficients and levels of significance are greater for ‘quick joiners’ than ‘quick decliners’, though all are significant at p < 0.10 or better. The reported marginal effects indicate average effect size with an instantaneous change increasing the probability of a quick join by 2–4%, while a negative change increases the probability of a quick decline by 1–2.7%. Hypothesis 2 is therefore supported. Experience leads to a quick decision, with the decision outcome influenced by the nature of the experience.

Post hoc analyses

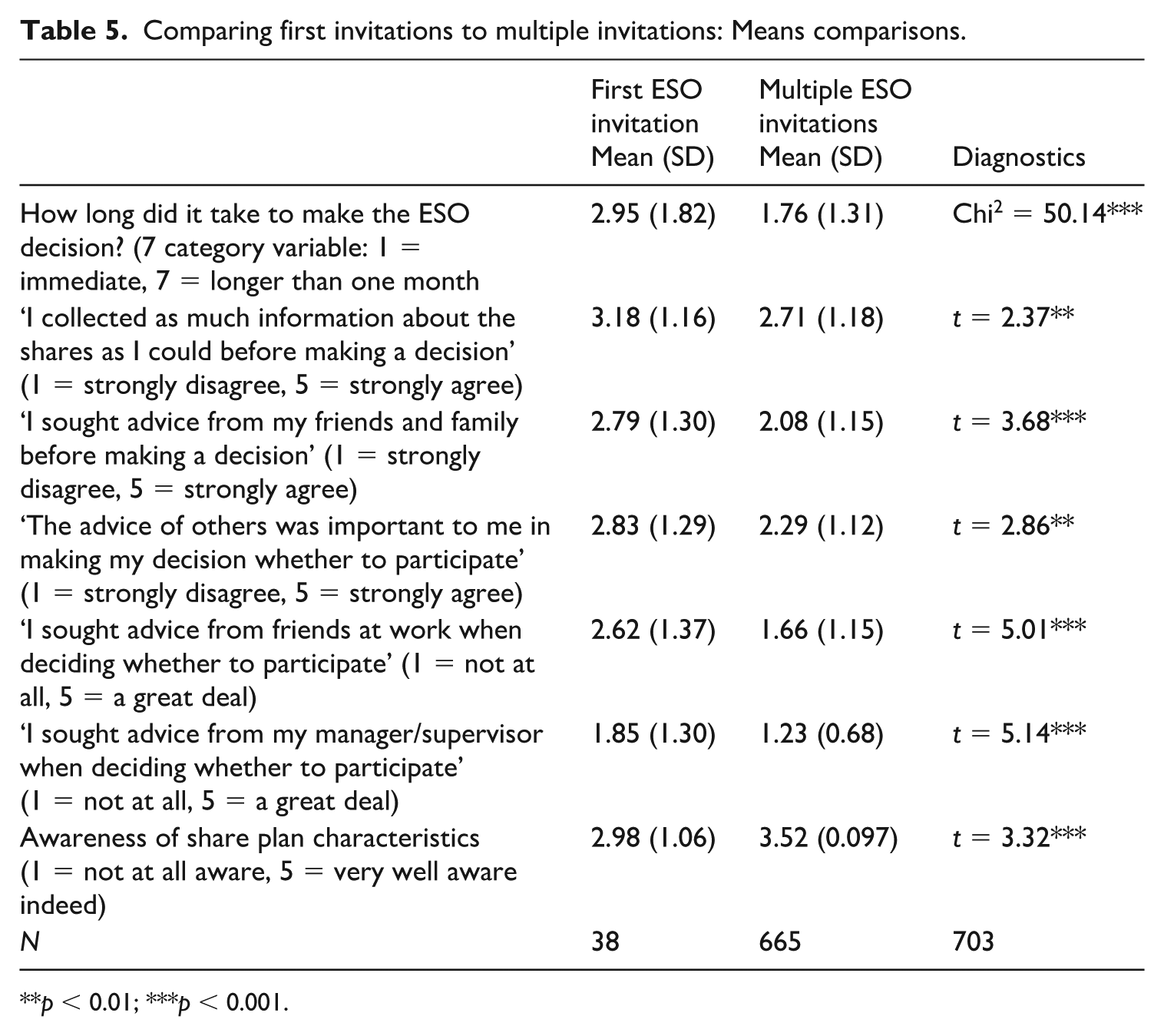

Our findings provide support for the role of habit when employees are making an ESO enrolment decision: they repeat past decisions when making a current decision, irrespective of the measure of experience. Further, experience of making the enrolment (or non-enrolment) decision is associated with much quicker decision-making. As an additional test, we compared the decisions of employees with and without any experience of the ESO decision. Consistent with the theory of habit (Ouellette and Wood, 1998), employees without experience are more likely to engage in conscious decision-making rather than take the more automatic approaches of employees who rely on experience when deciding. In our data set, we have 38 employees who were being invited to participate in an ESO for the first time (received their first share plan invitation just prior to our data collection). In Table 5 we compare the mean (categories in one instance) of first and multiple invitation employees across various aspects of making the share plan decision. We find that employees receiving their first ESO invitation took longer to make their decision, sought and relied on advice from others, and felt less aware of the share plan characteristics. While the sample size is small, the results are consistent with the predictions from the theory of habit and provide some additional support for our findings. ‘First-timers’ make their decisions differently from their more experienced colleagues.

Comparing first invitations to multiple invitations: Means comparisons.

p < 0.01; ***p < 0.001.

Summary and discussion

Our article examines the role of experience of previous enrolment in a stock plan on a current decision whether to enrol in a company stock purchase plan. The results demonstrate path dependency in the decision made by employees: most do what they have done before, and a significant predictor of enrolling (or not enrolling) is what has been done before. This is the case across our two organisations, with similar plans though operating in different industries. The role of experience in influencing the current decision is consistent with the theory of habit. Our respondents make the same decision and quickly (most respondents make their decision ‘immediately’), indicating little attempt to re-evaluate preferences or consider the efficacy of the stock plan in meeting those preferences. Further, as noted by the theory of habit (Ouellette and Wood, 1998) favourable attitudes to the stock plan grow with the number of occasions that employees have enrolled in the plan. In combination, our results demonstrate the value of evaluating current ESO participation decisions in the context of past decisions.

Theoretical implications

Compensation systems are used by organisations to influence employee attitudes and behaviour and subsequently organisational performance. These organisational benefits are more likely the higher the number of employees in the plan (Pendleton and Robinson, 2010). However, unlike other forms of compensation, employees have a choice about enrolling in an ESO, and hence it is important to understand how employees make not only the first but also subsequent enrolment decisions. Conceptually, researchers have relied on standard investment models of decision-making. Our findings, consistent with habit, suggest that many employees are more likely to make their current enrolment decision based on what they did previously, highlighting the potential importance of non-rational elements in ESO decision-making. Our results are consistent with and supportive of previous work on other aspects of financial decision-making (e.g. on 401k plan behaviour) that highlights the role of biases and heuristics in financial decisions (Benartzi, 2001; Benartzi and Thaler, 2001; Thaler and Sunstein, 2009).

Our findings suggest a need to reconceptualise ESO enrolment. Researchers typically conceptualise ESO enrolment as a one-time event, then often comparing the attitudes and behaviours of shareholders and non-shareholders to evaluate the impact of ESO on a range of individual and organisational outcomes (e.g. McCarthy et al., 2010; Nyberg et al., 2018). Our study highlights the need for a broader definition and measurement of ESO enrolment beyond current enrolment status to include previous decisions. Taking a more comprehensive definition of ESO enrolment has the potential to challenge some of our existing understanding of the organisational impacts of ESO. For example, the effect of plan enrolment on a ‘first-timer’ may be very different from that on a repeat enroller and hence on the organisational outcomes. Our findings therefore provide strong support for incorporating a temporal dimension into theories of employee participation in share ownership plans.

Policy and practice implications

Organisations seek the maximise the participation rates in a share plan (Stebe et al., 2022), but our findings suggest that participation rates in ESO plans may not change much over time due to the role of habit in ESO decision-making. By identifying the factors that contribute to consistent responses to share invitations over time we provide practitioners with insights into potential interventions. Finance practitioners may gain an improved capacity to predict the take-up, costs and resourcing (stock issues or stock purchases) of employee equity plans. Those in charge of ESO plan communications can gain a better appreciation of how employees will respond to stock plan invitations and communications. Many companies seek to maximise plan enrolment with information that appeals to rational decision-making by, for example, providing information about the ESO plan, how to purchase shares and the potential financial returns. But our results indicate that employees with previous experience of share scheme invitations tend to make these decisions quickly and decide in line with what they have done previously. There may be a limit to the influence that companies have on employee decision-making. The implication of our findings is that the typical communications strategy used by companies – invitations followed up by reminders – misidentifies typical patterns of employee behaviour. The reminders are too late: the decision may have already been made. Potential interventions may include communication activity prior to an ESO invitation. Organisations may have more success in achieving higher enrolment rates by more sustained communications activity prior to the invitation to encourage employees to re-visit their preferences. There are two potential challenges with this approach. First, companies need to be careful not to violate legal constraints on the provision of financial advice (Pendleton and Robinson, 2021). Company ESO communications might be seen to function as ‘implicit investment advice’ (Liang and Weisbenner, 2002). Second, habit may mean that employees will discount such initiatives. Once an employee has adopted a certain way of doing things, they may well tend to continue to invoke that way even if their circumstances have changed (Jarzabkowski and Kaplan, 2015).

The theory of habit suggests that employees repeat the same decisions when the context is stable (Ouellette and Wood, 1998), so creating some instability might be effective in changing decision-making patterns. Substantial changes to plan communications content or delivery, or to plan design (within the limits allowed by the regulatory framework), might break the habits of those who are accustomed to declining to participate. But equally there is the danger that those in the habit of enrolling at each invitation might find change challenging, leading to lower levels of ESO participation.

Strengths and limitations

There are two key strengths of our research. First, it was focused on a discrete event (opportunity to enrol in a share scheme) that occurred just before the survey was administered, with the survey questions focusing on what employees had done in response to this event. Second, we incorporated a time dimension into our study by asking respondents for retrospective information – previous offers to enrol in a share plan. This provides an opportunity to compare the ESO histories of our respondents and identify the path dependency of a current enrolment decision. Spector (2019) notes that cross-sectional designs are particularly appropriate when they are focused on a particular event that has already taken place and strengthened when they incorporate past experiences that help explain current decisions.

However, several limitations of our study need to be acknowledged. First, although we found that many employees took the ESO decision very quickly with minimal information collection and review, we do not know whether they had considered their preferences prior to the company invitation. Second, we use subjective measures of ESO knowledge and financial ability, but objective measures may well be preferable given that people often over-state their financial knowledge (Aran and Murciano-Goroff, 2025). Nevertheless, it is noteworthy that enrollers consistently recorded lower financial ability than non-enrollers.

Third, we focussed on the decision to enrol or not enrol and the speed of decision rather than the magnitude of the contributions to the ESO. It is plausible, however, that decisions may be slower and more considered when the financial commitment is larger. We experimented with a contribution to income ratio measure, finding insignificant effects in Company A and significant results (at p < 0.05) in Company B. A smaller sample size makes these results suggestive rather than conclusive.

Fourth, we collected our data during a period of rising stock prices, so employees may have repeated previous decisions in expectation of share price increases. Falling stock prices may lead employees to re-visit their preferences and to change their decision. In the event of an adverse market shock, where employees suffer significant losses (real or ‘paper’) on their employer stock, employees may be shocked into breaking their share plan habit and reverting to a more deliberative approach to decision-making with future share offers.

Future research

Drawing on the limitations noted above, future researchers might usefully investigate the quality of past experiences so that we can get a better understanding of the role and nature of experience. We might anticipate employees with a positive ESO experience enrol each time shares are offered – rewarded decisions are repeated. Further, these employees may hold a positive view of the organisation as an outcome of positive experiences and as a justification for their ongoing decision, and it will be worthwhile investigating the relationship between habit and attitudes to the company such as organisational commitment. Employees with a negative experience are unlikely to enrol again in a share plan. Our findings are consistent with these possibilities but suggest the need for additional research into the formation of habits in relation to the enrolment decision.

Future analysis of switchers could assist in understanding how (and how many) positive and negative ESO experiences influence the ESO decision of an employee. Their movement in and out of a scheme is potentially consistent with rational investment perspectives of the ESO decision – they evaluate the costs and benefits of enrolment each time shares are offered and decide based on their assessment. Relatedly, the greater the number of ESO experiences, the higher the likely level of financial contributions an employee has made. Each subsequent offer increases an employee’s level of financial contribution but also potential risk. It is also possible that decision-making is more deliberative, and less habit-driven, when contributions are larger or represent a substantial increase on previous contributions. We see opportunities to advance research into the role of experience in ESO decision-making by incorporating the total level of financial contributions, relative to income, to the ESO.

We are yet to understand how habits in relation to ESO might change over time. Habits can reflect an employee’s reluctance to change but the ESO enrolment decision can involve costs. During our data collection stock prices were rising so employees may have relied on past decisions when making their enrolment decision. Future researchers might investigate the employee enrolment decision in the context of volatile share prices or challenges to corporate reputations (Kruse et al., 2022), especially during the share invitation period. The potential for greater losses may create an incentive for the enrollers to re-evaluate their approach to the ESO decision, making it worthwhile to investigate employees’ stock plan decision-making in the wake of a market shock.

We find that peer effects can be important in both quick join and quick decline decisions. Future research could investigate further the role of peers in this decision-making and the role they play in the formation of ESO decision-making habits. Such research might explore whether some peers are particularly influential: we might investigate the position of these individuals in the organisational hierarchy and in social networks.

Conclusion

Researchers have demonstrated that employee share ownership can generate benefits for organisations, such as reduced employee turnover (Hennig et al., 2023), but typically overlook how employees make the decision whether to enrol into a plan. While ESO offers, like many financial products, provide sufficient time to undertake a careful and rational assessment, we find that that many employees make the ESO enrolment decision quickly based on what they have done before. These results might be disturbing to critics of ESO: those who choose to enrol quickly and based on experience may well be intensifying the dangers of concentrating their wealth and human capital. They also provide challenges to companies since entrenched habits of non-participation among some employees mean that it is difficult to raise ESO participation rates, especially as corporate approaches to share plan communications and invitations also seem to be ‘set in their ways’.

Footnotes

Appendices

Tests for biases arising from exclusion of missing values (logits).

| Company A |

Company B |

|

|---|---|---|

| Gender | –0.171 (0.347) |

0.527 (0.611) |

| Age | 0.012 (0.018) |

0.006 (0.032) |

| Enrolment in current plan | –0.046 (0.417) |

–0.987 (0.629) |

| Pseudo R2 | 0.003 | 0.035 |

| LR test (p-value) |

0.75 (0.861) |

3.34 (0.342) |

Acknowledgements

Previous versions of the article were presented at the EIASM Reward Management Conference, the Rutgers-Oxford Employee Ownership Research Conference and the Future of Equity: Silicon Valley Employee Ownership Symposium. We are grateful to participants for their comments on the article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.