Abstract

Studies of employee ownership (EO) have repeatedly cautioned that selection effects may be in part responsible for the apparent effects of EO on employee attitudes. Favourable attitudes among employee owners may result from individuals with positive views towards EO selecting into the company or the EO plan. Using data from a US employee stock ownership plan (ESOP), this study investigates whether EO as a factor in employment choice influences psychological ownership and preferences for working in EO firms in the future. The findings reveal that joining the company due to EO has a substantial, independent effect on psychological ownership beyond the influence of plan participation. The article quantifies the magnitude of this selection effect. Additionally, joining for this reason strongly impacts preferences for future employment in employee-owned firms.

Keywords

Introduction

Four decades of research into employee ownership have shown positive, albeit often small, effects of employee ownership on company performance (O’Boyle et al., 2016) and on the attitudes of employee owners towards their firm, such as loyalty and commitment (Buchko, 1993; Kruse et al., 2010; McCarthy et al., 2010; Pendleton et al., 1998). But a persistent issue has been the potential role of selection effects in these findings (Kruse et al., 2010; Weltmann et al., 2015): better performing firms may be more likely to select into employee ownership, and more committed and/or better-quality employees may be attracted to employee-owned companies and to their employee ownership plans (Kim et al., 2025). Thus, reported results on outcomes may exaggerate the direct impact of employee ownership in causing changes in performance or attitudes. This issue also raises questions about the direction of causality: in the case of studies of employee attitudes, pre-existing attitudes might influence the decision to acquire stock (in stock purchase schemes) or to join an employee-owned company. Thus, we cannot be sure that the observed employee ownership plan is primarily responsible for the apparent effects of employee ownership. To deal with causality issues, it is desirable to use data from firms where the participation decision is exogenous to the employee. This is what we do in this article.

The question addressed in the article is whether, and to what extent, selection effects have any influence on observed attitudinal outcomes of employee ownership. There are two strands to the analysis. One, using psychological ownership as our primary measure of attitudinal outcomes, we examine how far feelings of ownership derive from participation in the employee stock ownership plan (ESOP) and features of work in the company, and how far it emanates from the importance of employee ownership as a factor in joining the company (the selection effect). Two, we investigate the extent to which preferences for working in employee-owned firms in future are an outcome of being in an EO plan, or prior favourable attitudes towards employee ownership.

The research is based on an employee survey in a US ESOP that has been 100% owned by its employees for over 20 years. In the US an ESOP is a tax-qualified retirement plan whereby full or partial ownership of the company is passed to a trust, with periodic stock allocations to the retirement accounts of eligible employees. The research focuses on those employees who have joined the firm recently, and it is notable for observing similar numbers of participants and non-participants (yet to become eligible). Our research differs from most ESOP research where all or nearly all employees are ESOP beneficiaries at the time of the research (e.g. Buchko, 1993; Carberry et al., 2025; Hallock et al., 2004). A critical feature of our analysis is that participation in the plan is determined by meeting eligibility requirements set by the company, not employee choice. Once employees meet these requirements they are enrolled in the ESOP plan. This feature allows for a better isolation of how participation in the ESOP affects employees’ attitudes and behaviours, without having to account for the potential bias that could arise if employees could decide whether they want to participate or not. Instead, the key issue is whether employees joined the firm because of employee ownership.

The key contribution is that the research investigates what EO researchers have long suspected – that selection effects matter when evaluating outcomes of employee ownership. In considering the relationship between selection and psychological ownership, we can add to psychological ownership theory. An early exposition of this theory suggested employee views prior to experiencing ownership are also important, arguing that psychological ownership theory should incorporate expectations of ownership (Pierce et al., 1991). Our study addresses this by investigating whether the importance of employee ownership as a factor in joining the firm influences psychological ownership. Indeed, we find that those with positive prior views of employee ownership have relatively high levels of psychological ownership even when they are not yet formal owners of the company.

A novelty of the article in relation to sorting theory is that it explicitly focuses on the role of attitudes and preferences towards employee ownership in the decision to work for the company. Hitherto the sorting literature has focused on the relationship between employee characteristics, such as human capital, and ownership or pay incentives (Cadsby et al., 2007; Kim et al., 2025), and has been silent on employee motives. Our approach means that we can be more certain that any selection or sorting effect reflects a conscious decision by employees. By examining the role of selection effects, we are able to determine the extent to which plan participation impacts employee attitudes, and a key contribution to the employee ownership literature is that we are able to quantify relative selection and plan effects. The implication is that the direct effect of plan membership may be smaller than has been found in studies where selection effects are not taken into account (cf. Gerhart and Fang, 2014; Weltmann et al., 2015).

A key practical insight is that the results suggest that managers of employee-owned firms would do well to try to attract recruits who have favourable views of employee ownership. They might do this by attention to company branding, and highlighting employee ownership in company recruitment material. This would enhance their potential to recruit employees who are a good match with the company. Being proud to be employee-owned could well pay off.

Overall, the research contributes to a deeper understanding of employee perspectives on employee ownership, sheds light on the selection effects at play, and highlights the value-added by working in an employee-owned firm. It not only informs academic discourse but also provides practical insights for organizations considering or operating under employee ownership structures.

Literature review

Research into employee ownership has been mainly concerned with its potential effects on company performance (Guedri and Hollandts, 2008; Kruse, 2002; O’Boyle et al., 2016). The model widely drawn upon in the literature, implicitly or otherwise, posits that making employees owners can lead to attitudinal change, and hence to behavioural change such as working harder or a reduced propensity to quit (Sengupta et al., 2007), thereby enhancing organizational performance (Pendleton et al., 1998). Accordingly, there is also quite a substantial literature on the effects of various forms of employee ownership on organizational commitment and psychological ownership (Buchko, 1993; Kruse et al., 2010; Long, 1982; McCarthy et al., 2010; McConville et al., 2016: Pendleton et al., 1998).

One of the key limitations of the employee attitudes literature, and indeed much of the performance literature also, concerns the role of selection effects (see Weltmann et al., 2015). If employee-owned firms attract workers for whom employee ownership is important, these workers may display higher levels of psychological ownership even prior to being enrolled in the employee ownership plan, indicating that evidence on attitudinal outcomes of plan membership may exaggerate the extent of attitudinal change arising from actual membership of the plan. Further, where the plan takes the form of an ‘opt-in’ stock acquisition plan, as in the case of stock purchase plans, those employees for whom employee ownership is important may be more likely to purchase shares. Hence the posited effects of employee ownership on employee attitudes such as psychological ownership may operate in the opposite direction to that proposed in the employee attitudes literature (the reverse causality problem). There is a need, therefore, for research on employee ownership and attitudes to consider the role of prior attitudes to ownership, and how far these may contribute to the apparent attitudinal outcomes of employee ownership.

Most research on selection effects has focused on the role of employee sorting in variable pay schemes such as piece work. This posits that positive performance outcomes of incentive pay may arise from its capacity to attract high quality labour as much as from existing employees to work harder (Gerhart and Fang, 2014). Incentive pay may also encourage those existing employees who are less able to respond to the incentives to exit the organization. The most well-known study of this is Lazear’s (2000) research into the introduction of incentive pay in an automotive windshield shop, where it was found that around a half of the increase in productivity was due to the exit of less productive employees and their replacement by more productive ones. Dohmen and Falk (2011) find that productivity differences between fixed and variable pay schemes is largely driven by sorting. The implication is that studies which do not incorporate the role of sorting effects are likely to overstate the direct effect of the pay incentives on work behaviour (Dohmen and Falk, 2011).

In the employee ownership literature, a recent study has examined the relationship between the quality of human capital and employment in firms with employee ownership, drawing on an MTurk-generated survey and secondary analysis of a large individual-level panel dataset (Kim et al., 2025). The authors find a positive relationship between human capital and employment in firms with employee ownership arrangements, though this relationship declines at higher levels of human capital. They also find that these employees receive higher levels of compensation, attributed to superior financial performance in firms with employee ownership, along with human capital quality, and that these employees exert greater work effort (measured by hours worked). Why employees with higher human capital are found in firms with employee ownership arrangements could not be investigated in the study due to the nature of the data.

At the firm level, companies that are already more productive may be more likely to select HR practices that are seen as enhancing productivity. Thus, observations of productivity after the practice has been introduced may exaggerate the effects of the practice. In the worst case it may ascribe causality in the wrong direction. The relevance of this selection effect is borne out by Kraft and Lang’s (2016) study of profit sharing, which finds that firms that introduce profit sharing are already more productive than a control group of non-profit sharers. They also find that profit sharing enhances productivity, and they are able to disentangle and quantify the selection and profit-sharing effects.

Most of the research on sorting has focused on the sorting of higher quality workers into companies with incentive pay schemes, where workers with superior abilities or skills will be able to achieve higher levels of output or devote more effort. Whilst this research observes the outcomes of worker preferences (the revealed preference), it does not observe preferences as such, for instance that workers with superior skills want to work in firms with incentive schemes and want to devote more effort. In the absence of this, it is not impossible that the observed associations between worker quality and presence of incentive pay are due to chance or a variety of unobserved contextual factors (e.g. a change in the composition of the relevant labour market). Our suggestion, therefore, is that we need to know more about worker motivations for joining firms to fully understand sorting effects. There is some recognition of worker attitudes in the sorting literature: both Cadsby et al. (2007) and Dohmen and Falk (2011) find that individual risk preferences affect the propensity for choosing a variable pay scheme. But a greater focus on the perceived desirability of a variable pay plan by employees who are making the sorting decision would assist understanding of how the sorting effect operates.

In this article we endeavour to do this by investigating the role of employees’ views of employee ownership as a factor in joining an employee-owned firm as a potential influence on their subsequent attitudes. We consider two instances of attitudinal effects that may be brought about by employee ownership, but which may be affected by this selection effect: one is psychological ownership (i.e. feelings of ownership of the company), the other is preferences for employee ownership in future employment. The key issue is the extent to which observed attitudes are the outcome of being in the employee ownership plan, or instead reflect prior positive attitudes towards employee ownership. Two research questions are addressed:

To what extent does EO plan membership and the importance of EO when joining the company influence psychological ownership, and what is the magnitude of the selection effect in this context?

To what extent do employees express a preference for working in an EO company in the future, and how far are these preferences influenced by a selection effect?

The first question relates to the possibility that those for whom employee ownership was a factor in joining the company may well display positive attitudes to the company that could overstate the impact of plan membership per se. The rational for this is that if prior preferences and attitudes towards employee ownership are not observed, we cannot be certain that observed levels of psychological ownership are the outcomes of changes in attitudes brought about by the employee ownership plan. It is feasible that high levels of psychological ownership might be experienced prior to formal participation in the employee ownership plan if employees are already favourably inclined towards employee ownership. In our study these employees are those who indicate that they joined the company because of employee ownership, and this group provides the basis of the selection effect.

Psychological ownership, as developed by Pierce et al. (1991), is a psychological state whereby actors feel a sense of ownership, viewed as possessiveness, of a material object or immaterial phenomena. It can arise from control or a sense of control of the object of ownership, a feeling of intimate knowledge of it, and an investment of self in it (Brown et al., 2014). It can be felt at job or organizational level (Pierce et al., 2004). It is viewed as a separate concept from organizational commitment, identification and internalization, and indeed as an antecedent of them (Van Dyne and Pierce, 2004). A recent meta-analysis has found that psychological ownership is a stronger predictor of in-work behaviours than these other organizational attitudes (Zhang et al., 2021).

Several papers have investigated the effects of employee ownership on psychological ownership as there is an obvious, though not automatic, connection between the two (Pierce et al., 1991). Pendleton et al. (1998) found that ‘feelings of ownership’ played a mediating role between employee ownership and various employee attitudes, such as commitment, in UK employee-owned bus companies. Similarly, Carberry et al. (2025) show that psychological ownership mediates the impact of high performance work practices in employee-owned firms on employee commitment and behaviour. Wagner et al. (2003) found that ownership beliefs, arising from participation in a 401 (k) plan, led to positive attitudes to the firm and ‘ownership behaviours’, though it is debatable whether ownership beliefs equate to psychological ownership. However, not all studies find a positive relationship: McConville et al. (2016) and Poutsma et al. (2015) found that participation in an employee share ownership plan was not associated with psychological ownership. However, both these studies focus on minority share ownership plans in investor-owned companies rather than majority employee ownership.

Given this, it is reasonable to expect that employees who join a company because of its EO status may already possess higher levels of psychological ownership. This suggests that the relationship between EO and psychological ownership may, in part, reflect the influence of EO on the joining decision itself. Thus, we propose the following hypothesis:

H1: Joining the company because of employee ownership positively affects psychological ownership.

The second outcome of employee ownership we examine is employees’ preference for working in an employee-owned company in future. To the best of our knowledge, this has not been investigated before, though some studies have examined employee preferences for stock ownership (Caramelli and Carberry, 2014; Kuvaas, 2003). Although a hypothetical indicator of future intentions, the number and proportion of employees who indicate that they would like to work for an employee-owned firm in future might be taken as a measure of the success of employee ownership in their firm. We therefore anticipate that plan membership, and the psychological ownership that might emanate from this, will influence future preferences for working in employee-owned companies. However, once again selection effects may be important, with those who joined the company because of employee ownership more likely to have positive preferences for future employment in employee ownership. Thus, this apparent outcome of the experience of employee ownership may instead reflect prior preferences for employee ownership rather than the experience of working in an employee-owned firm. As a result, a focus on future employment preferences can be an effective test of the role of selection effects.

Consequently, we posit the following hypothesis:

H2: Joining the company because of employee ownership positively affects preferences for working in employee-owned firms in the future.

Methodological considerations

Ideally, any study of selection effects in employee ownership will have either a ‘before and after’ dimension, as in the Lazear and experiment-based studies, or comprise a sample where there are similar numbers of participants and non-participants. Unfortunately, conducting ‘before and after’ studies is extremely difficult, usually because the transition to employee ownership can be fraught and time-consuming for those concerned whilst researchers only discover about the transition after the event (Long, 1982). To the best of our knowledge there are just three studies of this type over the last 40 years: Long’s (1982) study of an electronics firm before and at two points after a conversion to employee ownership; Dunn et al.’s (1991) study of a Save As You Earn share option/purchase plan before and after its introduction; and Keef’s (1998) study of New Zealand managers before and after the introduction of a share purchase scheme. None of these studies explicitly considered the role of selection effects on observed attitudinal ‘outcomes’, though Dunn et al. (1991) found that many who initially held favourable views on the share ownership scheme subsequently failed to join it.

An alternative method is to compare participants and non-participants but this can be challenging because all or most employees may be participants. Studies of ESOPs in particular often lack variation in plan membership amongst respondents with all or nearly all employees enrolled in the plan. For instance, nearly all of Buchko’s (1993) respondents were participants in the ESOP. In Hallock et al.’s (2004) study, the participation rate was lower but their study focuses only on those participating in the ESOP. A further issue is that any variations in ESOP contributions, necessary to consider variations in attitudinal ‘outcomes’ when all employees are in the plan, may derive from employee rather than employer choices to make additional contributions from salary (up to 5%, compared with the 1.5% contributed by the company). In summary, factors such as limited variation in membership, employees making additional voluntary contributions from their salary, and a focus solely on ESOP participants complicate the measurement of employee ownership’s direct effects on attitudes and behaviour.

If, however, we can examine cases of employee ownership where some employees are in a plan but a similar number are not, where the joining decision is not made by the employee, and where we can identify the role of employee ownership in influencing whether employees join the firm, we can make a more judicious evaluation of the role of employee ownership in influencing employee attitudes and preferences. This is what we do in this article. We examine employee attitudes in an ESOP where there are a substantial number of non-participants, where the company rather than the employee decides employee participation in the plan, and where we have data on the role of employee ownership in the decision to join the company.

Unlike most of the sorting and selection literature (e.g. Cadsby et al., 2007; Dohmen and Falk, 2011; Kim et al., 2025; Lazear, 2000), we do not need data on employee quality to test our hypotheses. This is because our focus is employee attitudes apparently arising from participation in the plan rather than individual or company performance. Also, employee ownership differs from variable pay schemes in that its primary purpose is not usually to bring about immediate and direct changes in work effort. It can be viewed as a ‘soft’, ‘weak’ or ‘low-powered’ incentive in contrast to the ‘high-powered’ nature of individual incentive pay schemes (Pendleton, 2006; Prendergast, 1999). Hence worker capacity to modify their behaviour does not need to be an integral part of the analysis. Since ESOP participation is primarily a benefit, with no direct link to desired levels of work performance, there is also less need to select out of the firm to avoid unwanted expenditure of effort.

Methods

The research site

The research site is an American retail company, founded in the 1930s, with 100% ownership by an ESOP since the turn of the century (the ESOP was first created in 1988). An employee share ownership plan (ESOP) is a form of employee ownership involving a retirement plan, regulated by the Employee Retirement Income Security Act 1974 and subsequent legislation. It involves an ESOP trust acquiring shares, often using loans secured against the future income of the company, and holding them in trust for employees until their retirement. When employees leave the company their shares can be sold, usually back to the trust, with employees receiving the proceeds. In privately held companies an ESOP is typically a succession device when owners want to exit. In 2021, 6322 companies in the United States had an ESOP, of which most were privately held companies, with over 10 million active participants (National Center for Employee Ownership [NCEO], 2024).

The company in our research is amongst the largest 50 ESOPs in the USA. It has just over 100 stores in four states, and around 5000 employees. The company was fully acquired by the ESOP trust in 2001, taking the form of a leveraged buy-out. Employees receive stock into their ESOP accounts with contributions from company profits over the years ranging from 3% to nearly 20% of salary (with the annual average being 11% for an employee with 20 years’ employment). US Form 5500 data show that there is currently around $110 million worth of assets in the ESOP, and around 2400 employees (i.e. around half of employees) with plan balances. The stock price has increased from around $20 in 2001 to over $1000 in 2022, with the result that an hourly-paid shop-worker with 20 years’ service will have 400,000–500,000 dollars of stock in their ESOP account.

To become enrolled in the ESOP, employees must meet three conditions: be over 21, have a year’s employment and work at least 1000 hours in this qualifying year. Employees are automatically enrolled at the next enrolment date after these conditions are satisfied (September and March). There is a six-year vesting schedule. Voting rights on key decisions are passed through to participating employees, with votes taking place recently on the various acquisitions made by the company.

According to the vice-president for HR, the level of employee turnover is lower than the norm for the retail sector. Much of the turnover arises from young employees who have taken on employment part-time during high school or college, leaving to go to university or otherwise embark on their careers. There is no evidence to suggest that turnover arises from employees wanting to select out of being enrolled in the ESOP. 1 Employee turnover, along with the company’s recent expansion, means that a substantial number of new employees join the company each year. There is therefore a sizeable group of employees who are yet to be participants in the ESOP plan at any one time, and this provides us with approximately equal groups of participants and non-participants. Interview data indicate that the company is well regarded locally as a good place to work, and the management of the company devotes considerable attention to staff welfare and maintaining a strong ‘family’ culture.

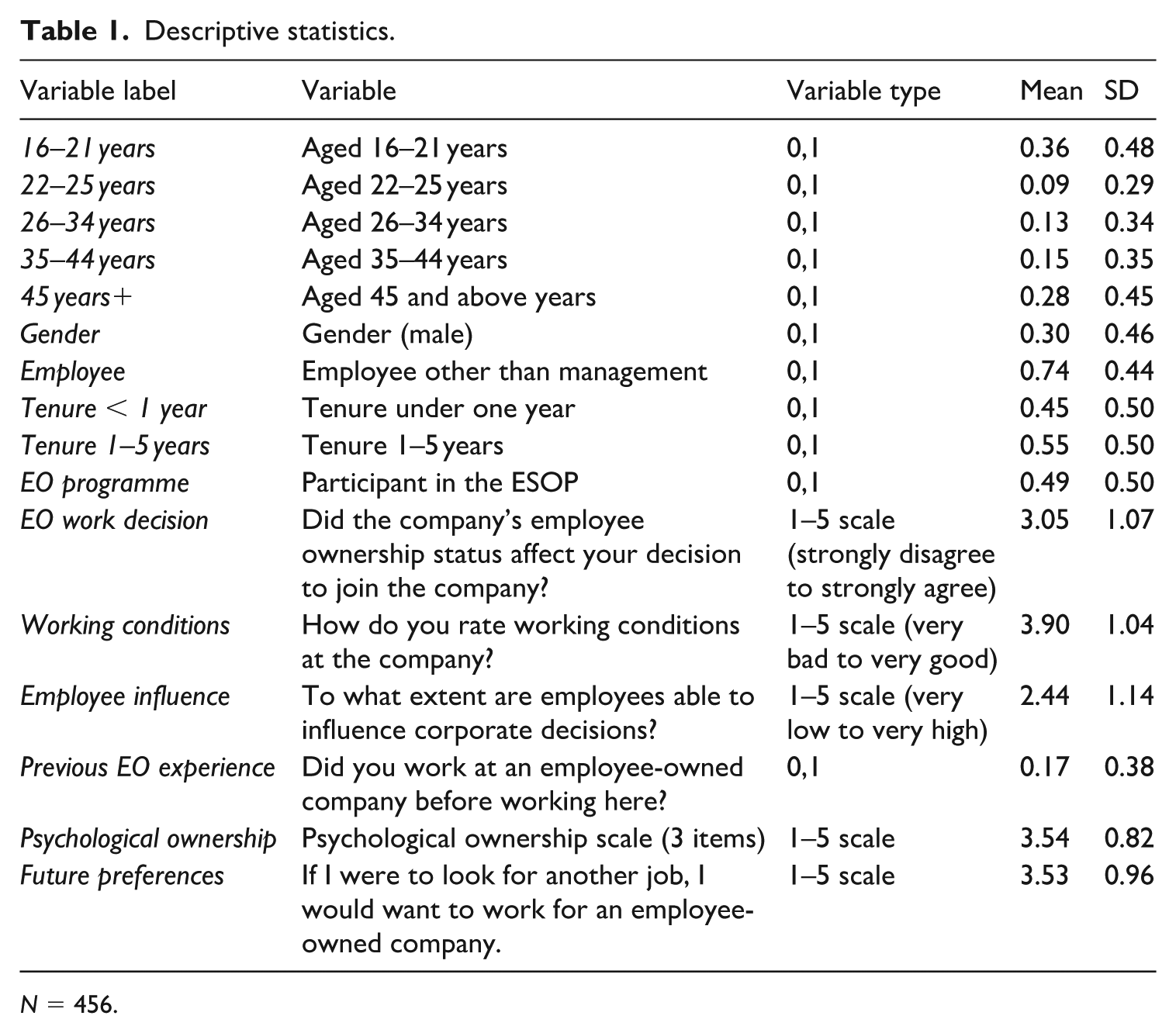

To collect data to address the research questions, an interview was conducted with the vice-president for human resources, along with an anonymized employee survey. The survey was distributed to all employees across company operations in four states in 2022. The VP instructed the branch managers to display a QR code for the questionnaire in each break room. To encourage responses, the team with the highest participation was promised a pizza party as a reward. As employee surveys are a common practice in the company, staff were already accustomed to this process. Just over 10% of the company’s employees responded to the survey, with 566 completed responses. The age structure of respondents mirrors the U-shaped workforce profile as a whole (as derived from interview data), with 36% of the sample aged 16–21 and 28% over 45; 70% of respondents are female, and 74% work on the ‘shop floor’.

Although employees of all ages and job tenures responded to the survey, the analysis is restricted to those who have been working for the firm for five years or less. This is because we ask employees to recall the importance of employee ownership in deciding whether to work for the company, and we need to restrict the potential for recall error (see Jacobs 2002; Ornstein et al., 1992; Schwenk, 1985). This reduces the sample size to 456 employees (we analyse the group of employees with more than five years of tenure in robustness tests). To minimize potential information loss due to missing data, multiple imputation was applied. This method replaces missing values with several plausible estimates while accounting for the uncertainty in the imputed values, ensuring that the analysis is based on a more complete dataset and produces more robust results (see Rubin, 2004). Although some variables exhibit missing values, this issue can be considered moderate. The overall extent of missing data ranges from 0% to 14.47% of the final sample, which is well within acceptable limits. Research shows that missing data rates of up to 20% can still yield valid and reliable results, provided appropriate methods, such as multiple imputation, are employed (see De Goeij, 2013; Dong and Peng, 2013). We also utilize listwise deletion in robustness tests.

Within the selected sample there are two tenure groups: those with under one year’s employment, and hence not yet eligible for the ESOP; and those with one to five years’ employment, and who are mainly (subject to the age and hours requirement) enrolled in the plan. Of the final working sample, 48% are plan participants – giving more of a balance between participants and non-participants than has been the case in earlier research.

Variables

To address the potential selection effect we use a five-point scale (strongly disagree to strongly agree) measure asking whether the company’s employee ownership status influenced the decision to join the (EO work decision).

The measure for psychological ownership, one of the two dependent variables, is derived from Van Dyne and Pierce (2004). They argue that psychological ownership is a unidimensional concept, and they measure this using four items. In our study, we use three items on a five-point scale: ‘I feel like an owner’, ‘I feel invested in (the company’s) success’ and ‘I feel responsible for daily operations at (the company)’. This selection captures core features of psychological ownership, as conceptualized by Van Dyne and Pierce (2004), Pierce et al. (2003) and Brown et al. (2014) covering feelings of possessiveness, self-investment and responsibility. An exploratory factor analysis (EFA) confirmed a one-factor solution, with substantial loadings for each variable ranging from 0.70 to 0.89. Internal consistency was acceptable (Cronbach’s α = 0.74).

A further five-point scale variable measures the preference for working in an employee-owned firm in future. This is the second dependent variable (Future preferences).

Plan participation is measured by a dummy variable, indicating whether they are in the plan or not (EO programme).

Evaluation of working conditions (Working conditions) is measured by a five-point scale, as is a variable relating to assessments of employee influence (Employee influence) on key decisions. Both are predicted to influence psychological ownership (Poutsma et al., 2015) and preference for working in employee ownership in future.

Previous experience of working in an employee-owned firm is included in models to test hypothesis 2 (Previous EO experience).

Dummy measures for age, tenure, gender and employment status (worker or manager) are included as controls.

Descriptive statistics are presented in Table 1.

Descriptive statistics.

N = 456.

A correlation matrix for these variables can be found in Appendix 1. Note that there are some fairly high correlations between some variables (where p > 0.2), but these do not give rise to problems with multicollinearity in the regression analysis. Appendix 2 provides further details of plan participation rates, tenure and gender by age groups.

Procedures

An integral feature of the analysis is that enrolment in the ESOP plan is exogenous to the employee but the opportunity for joining the plan may be a factor in joining the company.

We test hypothesis 1 by examining whether employees who joined the company because of employee ownership report higher levels of psychological ownership. We also consider whether being enrolled in the employee ownership plan plays a role. We then measure the magnitude of the possible selection effect, noting that there are various ways of conceptualizing and calculating this. The ANOVA comparison presents an overview of the different levels of psychological ownership amongst groups defined by both plan membership and the importance of employee ownership in joining the company. We then use an Blinder–Oaxaca decomposition to calculate the ‘unexplained’ differences between those for whom employee ownership was important in joining the firm and those for whom it was not, using this as a measure of the selection effect.

In the second part of the analysis, we shift focus to future preferences for working in an EO firm. A key consideration is whether the preference for future employment in an EO company is influenced by the decision to join the current firm because of employee ownership rather than arising from membership of the plan. We test hypothesis 2 by investigating how various factors, including psychological ownership and prior experience with EO companies, shape these future preferences.

Results

EO, selection and psychological ownership

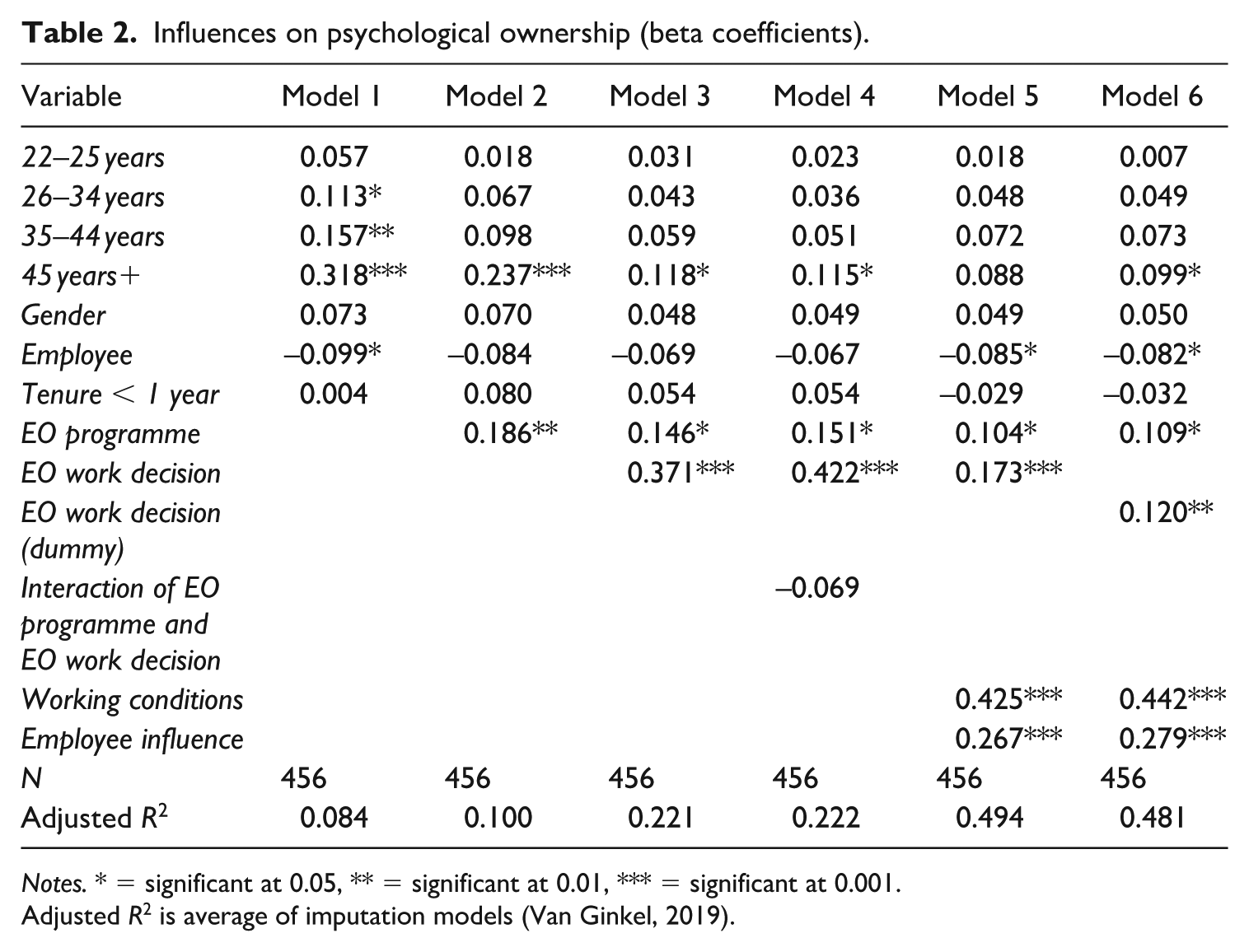

In Table 2 we report a series of regressions which show the influences on psychological ownership. The key independent variable is participation in the plan, whilst the selection effect is captured by the variable recording whether employee ownership influenced the decision to work in the company. An alternative dummy measure of this latter variable, where ‘strongly disagree’, ‘disagree’ and ‘neutral’ responses are considered to equate to EO being unimportant in joining the company, and ‘agree’ and ‘strongly agree’ are treated as EO being important, is used in the final model to facilitate direct quantitative comparison with plan membership. Gender, tenure, age and occupational level status are controlled for. 2 The expectation, based on theory and prior evidence (Pendleton et al., 1998; Pierce et al., 1991), is that participation in the plan will have a positive relationship with psychological ownership. For hypothesis 1 to be supported, the variable recording whether employee ownership influenced the decision to join the company must be positive and statistically significant.

Influences on psychological ownership (beta coefficients).

Notes. * = significant at 0.05, ** = significant at 0.01, *** = significant at 0.001.

Adjusted R2 is average of imputation models (Van Ginkel, 2019).

Table 2 provides six models for influences upon psychological ownership. Model 1 provides a baseline model comprising personal characteristics. It is notable here that the age dummies – except for the youngest age group – are significant, and that the beta coefficients increase with age. The employee dummy shows a negative effect, suggesting that managers exhibit slightly higher levels of psychological ownership. Model 2 adds enrolment in the ESOP programme, and the coefficient on this variable is fairly substantial and significant at p < 0.005. In this model, only the highest age group shows a statistically significant effect, indicating a reduced explanatory role of age once ESOP enrolment is controlled for.

Model 3 adds the variable for EO being an influence on joining the company. The coefficient for this variable is sizeable (significant at p < 0.001), whilst the size of some other beta coefficients reduces quite substantially. Meanwhile the adjusted R2 for this model shows substantial growth on that for Model 2. The coefficient for being in the ESOP reduces from 0.186 to 0.146. Even so, ESOP membership and joining the company because of its employee ownership may have distinct effects on psychological ownership. This interpretation is supported by the inclusion of an interaction between these two variables in Model 4 – here the coefficients of the constituent variables become larger, whilst the coefficient on the interaction term is negative and not significant, indicating that each variable is not moderating the other. Model 5 adds employee evaluation of working conditions at the company and perceived employee influence over decisions. As can be seen, these have sizeable effects on psychological ownership, and the model fit increases substantially. Finally, in Model 6 we replace the scale measure for selection with a dummy to permit direct comparisons with the effect of being in the ESOP. The beta coefficient for joining the company because of employee ownership is slightly higher than that for plan participation (0.120 vs 0.109), indicating the selection effect can be larger than the plan membership effect.

Overall, the key result is that the coefficients for the variable measuring the selection effect are significant throughout, indicating that hypothesis 1 is supported. Further, inclusion of the variable measuring the selection effect reduces the size of the plan membership coefficient.

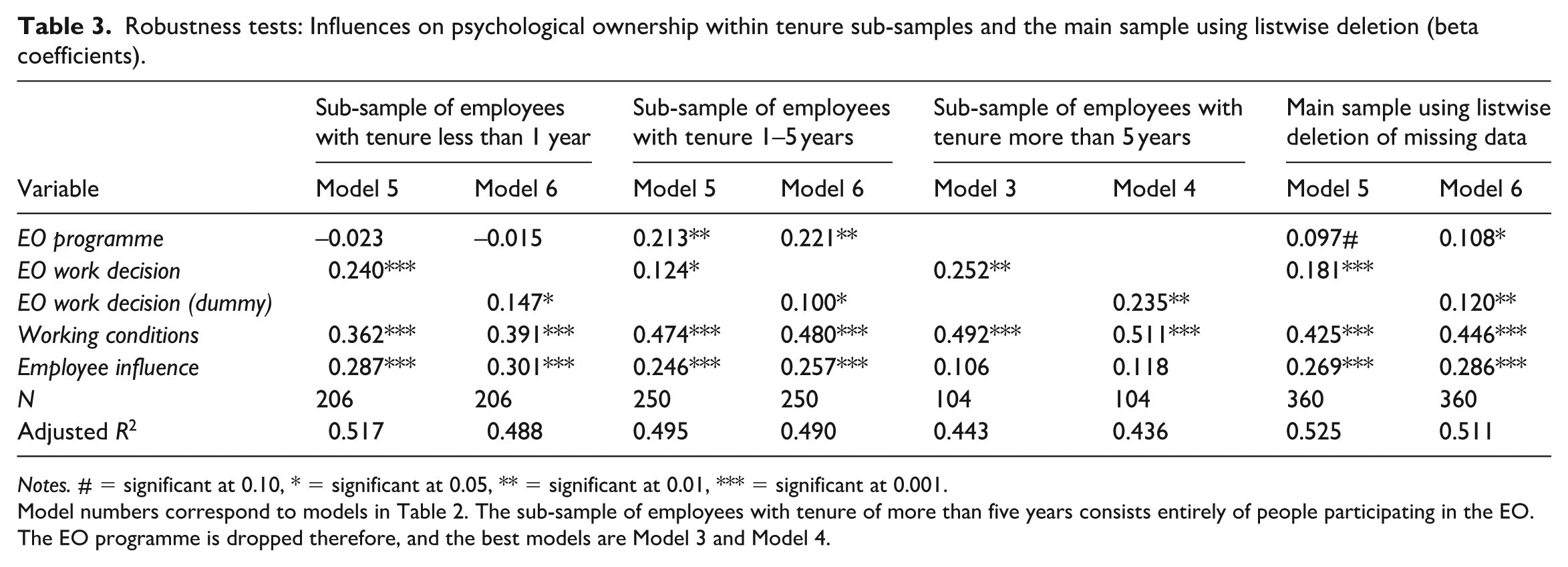

We check for multicollinearity in each model and find that variance inflation factors (VIF) are well below the commonly accepted threshold of 5 despite fairly high levels of correlation between some of the variables in the models (see Appendix 1). We also tested the robustness of our results by conducting the analysis with three sub-samples: one restricted to employees with less than one year of tenure, another restricted to employees with one to five years’ tenure and one for employees with more than five years’ tenure. A further robustness test was conducted with the sample using listwise deletion of missing data.

Table 3 summarizes the robustness test results for the key variables of interest using the models that exhibit the highest levels of adjusted R2 (detailed results can be found in Supplementary Materials). For the sub-sample of employees with one to five years’ tenure and in the sample using listwise deletion of missing variables, participation in the EO plan shows significant and positive effects on psychological ownership. By contrast, for employees with less than one year of tenure, this effect disappears. This is not surprising given that employees in this group are not yet eligible to join the plan. In the robustness test for employees with more than five years’ tenure, the EO programme variable is not included because all individuals in this group are already participants. Across all sub-samples, the selection effect remains statistically significant, and the selection variable coefficients are larger than those for the plan programme in three of the four sets of results. Working conditions and employee influence consistently remain strong predictors of psychological ownership. An exception is found in the group with more than five years’ tenure, where employee influence loses significance.

Robustness tests: Influences on psychological ownership within tenure sub-samples and the main sample using listwise deletion (beta coefficients).

Notes. # = significant at 0.10, * = significant at 0.05, ** = significant at 0.01, *** = significant at 0.001.

Model numbers correspond to models in Table 2. The sub-sample of employees with tenure of more than five years consists entirely of people participating in the EO. The EO programme is dropped therefore, and the best models are Model 3 and Model 4.

Levels of psychological ownership and selection effects: Further analysis

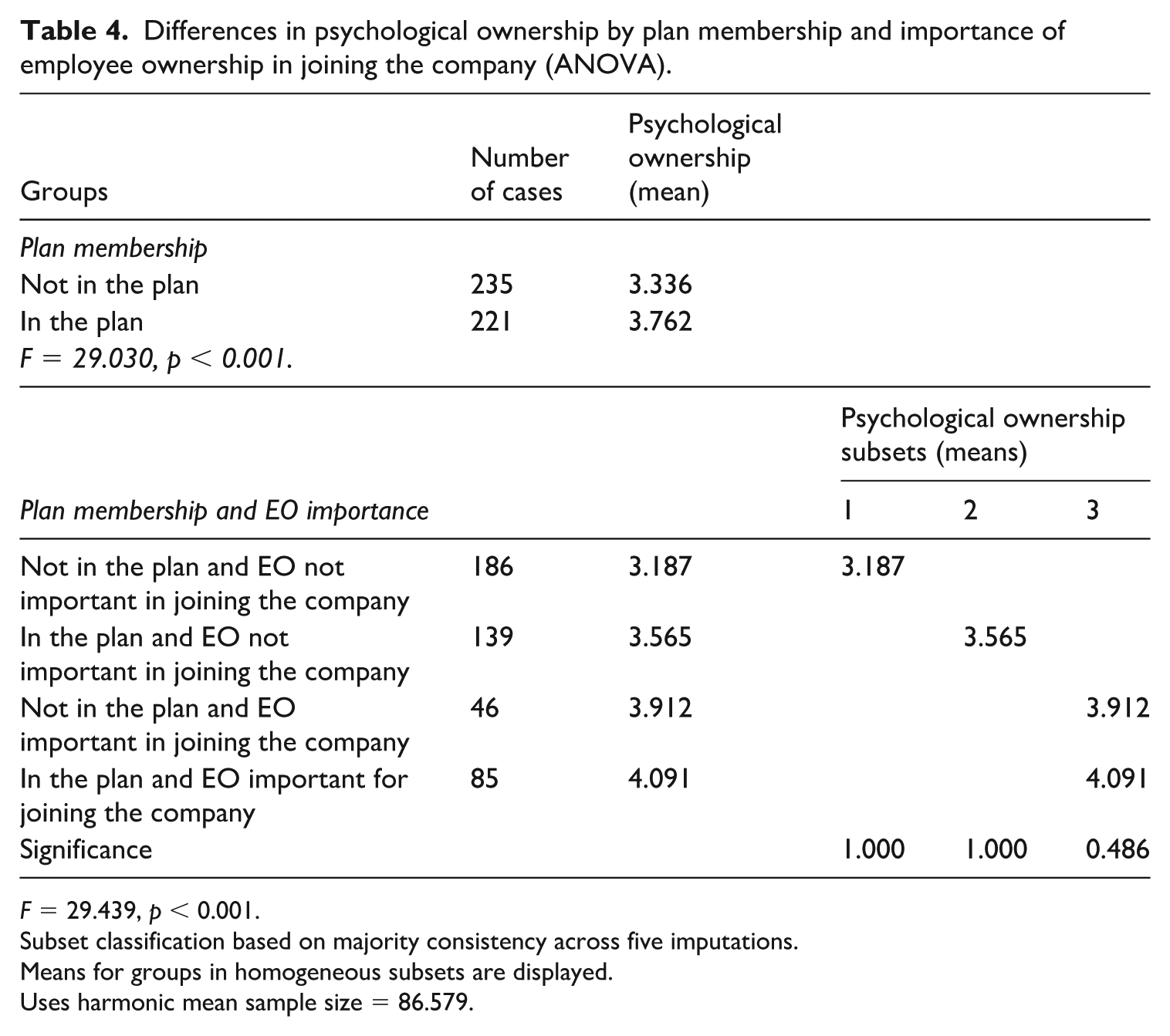

To illustrate the impacts of being in the plan and selection effects, we compare the mean levels of psychological ownership between four groups determined by whether employees are in the ESOP and whether EO was important for them in joining the company (the selection variable). This further highlights the potential importance of selection effects relating to the choice to join an employee-owned company.

Comparing the level of psychological ownership between those not in the plan and those in it, as is customary in studies of the effects of employee ownership (see McConville et al., 2016; Pendleton et al., 1998; Weltmann et al., 2015), Table 4 shows a sizeable and significant difference (3.336 vs 3.762 on a 1–5 scale, F = 29.030, p < 0.001). This indicates that those in the ESOP have higher feelings of psychological ownership.

Differences in psychological ownership by plan membership and importance of employee ownership in joining the company (ANOVA).

F = 29.439, p < 0.001.

Subset classification based on majority consistency across five imputations.

Means for groups in homogeneous subsets are displayed.

Uses harmonic mean sample size = 86.579.

The ANOVA comparison further shows the relevance of selection effects in interpreting the effect of employee ownership on psychological ownership, and there are several ways these can be considered. Comparing those in the plan for whom employee ownership was important in joining the company with plan members for whom it was not shows a difference in psychological ownership of 4.091 vs 3.565, a gap of 0.526 scale points, significant at p < 0.001 in a Scheffé test.

Those for whom EO was important in joining the company have much higher levels of psychological ownership whether they are in the plan or not. Those not in the plan for whom EO was important have a psychological ownership score of 3.912 compared with 3.187 amongst those not in the plan for whom EO was unimportant (significant at p < 0.001 in a Scheffé test) and 3.565 for those in the plan for whom EO was unimportant (significant at p < 0.1 in a Scheffé test). The effect of joining the plan is much smaller for those for whom EO is already important, with a gap of 4.091 vs 3.912 between those in the plan and those who are not. This difference is not statistically significant.

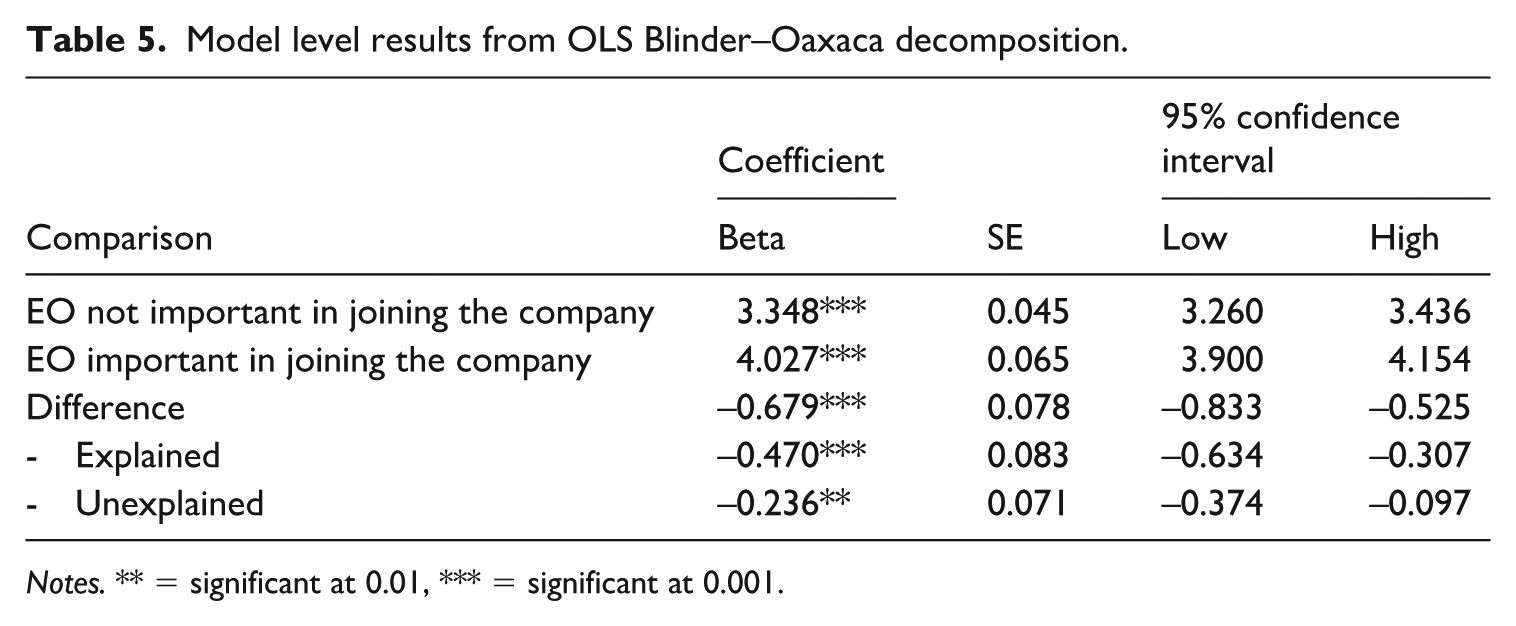

We further conduct an OLS Blinder–Oaxaca decomposition to better understand the difference in psychological ownership between those who consider employee ownership important and those who do not. This method is typically used to compare labour-market outcomes of two groups by analysing differences in means and coefficients (Blinder, 1973; Oaxaca, 1973). It decomposes the overall difference in the dependent variable between the groups into two components: one attributed to differences in observable characteristics (e.g. levels of coefficients) and an unexplained component, often used as a measure of discrimination (Jann, 2008). In our analysis, the unexplained component represents the selection effect, capturing the difference in psychological ownership between those who prioritized EO when joining the company and those who did not beyond that which can be attributed to observable differences (i.e. the other variables in the model). The results are summarized in Table 5, with Appendix 3 providing more detailed results.

Model level results from OLS Blinder–Oaxaca decomposition.

Notes. ** = significant at 0.01, *** = significant at 0.001.

Table 5 shows that individuals who consider EO an important factor in joining their company have higher psychological ownership than those who do not. Specifically, the average score for psychological ownership for people who view EO as important is 4.027 compared with 3.348 for those who do not, resulting in a difference of 0.679. This difference is significant at p < 0.001. The explained component accounts for –0.470 (significant at p < 0.001) indicating that part of the disparity can be attributed to observed factors that differ between the two groups.

The selection effect can be calculated by comparing the unexplained effect (0.236) to the overall difference. By doing so we find that about 34.7% of the difference in psychological ownership between those who consider EO to be important and those who do not cannot be explained by the observed characteristics included in the model. In other words, about a third of the difference in psychological ownership is influenced by this selection effect.

Preferences for future employment in employee-owned companies

An indicator of the effects of employee ownership is whether employees would want to work for another employee-owned firm in future. We ask employees whether they would want to work for another EO firm if they were looking for another job: 42% indicated agreement (‘agree’ or ‘strongly agree’) that they would. However, the role of selection effects must be considered when analysing these preferences: over half (54%) of these employees indicated that they joined the company because it was employee-owned. It is possible that these employees may prefer to work for an employee-owned company in future irrespective of their participation in the current plan. If we do not measure the selection effect, this preference might be erroneously attributed to the effects of working in an employee-owned company.

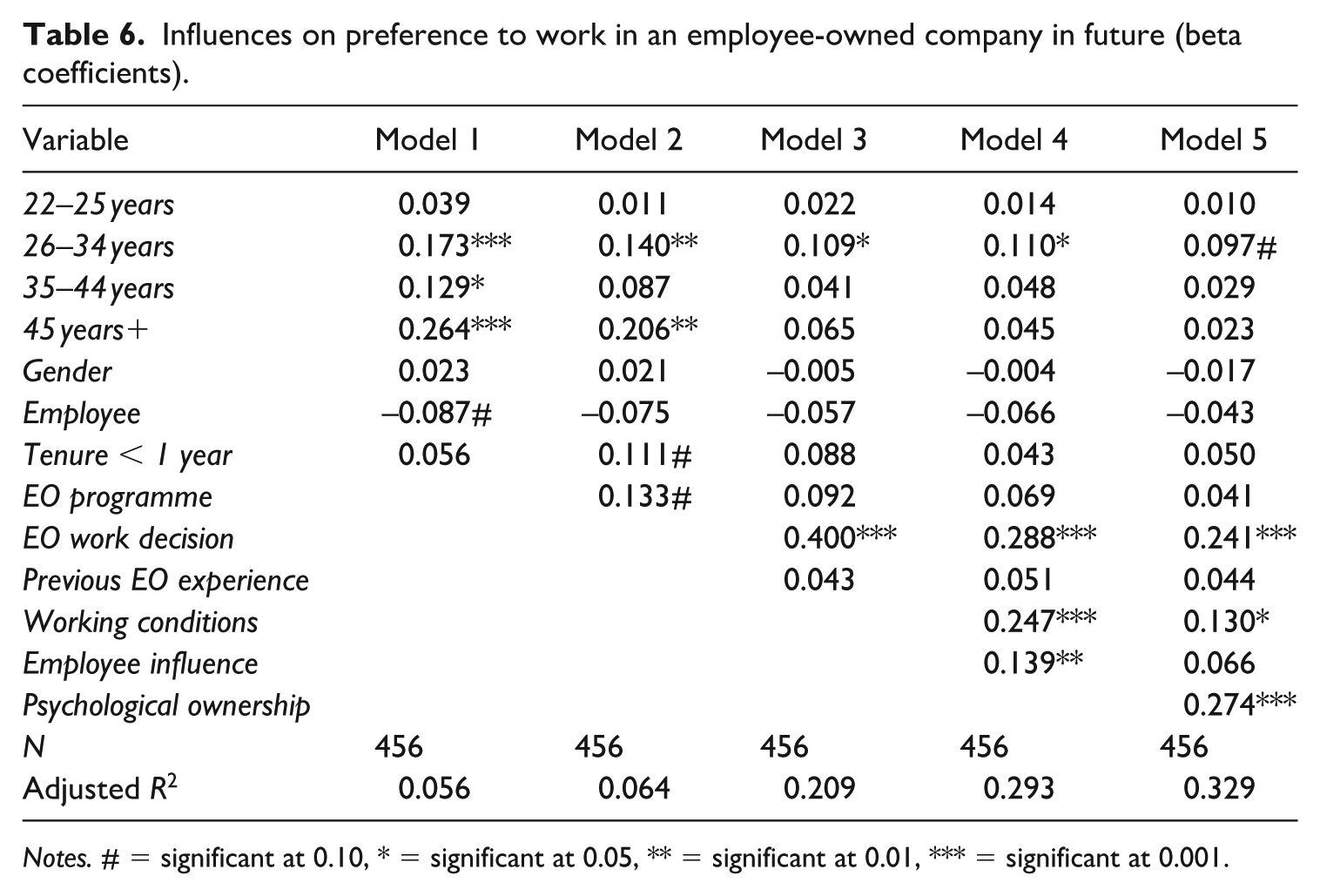

To test hypothesis 2, we conduct a set of regression analyses that include all variables from the previous regressions and the addition of previous experience at an EO company and psychological ownership as independent variables. See Table 6 for results.

Influences on preference to work in an employee-owned company in future (beta coefficients).

Notes. # = significant at 0.10, * = significant at 0.05, ** = significant at 0.01, *** = significant at 0.001.

Model 1 is a baseline model that includes demographic variables such as age, gender, employee status and tenure. Three of the four age groups (26–34, 35–44 and 45+) show a significant preference (at p < 0.05) for working in EO companies. With the introduction of the EO programme variable in Model 2, ESOP participants show a higher preference for working in EO companies in the future (0.133, significant at p < 0.10). Two of the age variables remain significant, though the coefficients are reduced somewhat. Being employed in the company for less than one year reveals a positive effect (0.111, at p < 0.10). The model’s explanatory power improves slightly (adjusted R2 = 0.064).

Model 3 adds the key selection variable relating to selecting employment with the company due to EO. This variable has a strong positive effect (0.400, at p < 0.001), indicating that individuals who chose to work for the company due to EO are significantly more likely to prefer working in these environments in the future. Previous EO experience does not show a significant relationship, and participation in the EO programme loses significance. Moreover, just one of the demographic characteristics exhibits a statistically significant effect. The adjusted R2 rises to 0.209.

In Model 4, working conditions and employee influence are introduced. Both factors show strong positive effects (0.247 and 0.139 respectively), indicating that better working conditions and greater employee empowerment enhance future preferences for EO companies. The coefficient on the selection variable (EO programme) is reduced somewhat but remains sizeable (0.288, at p < 0.001). Model fit improves further with an adjusted R2 of 0.285.

Finally, Model 5 reaches the highest explanatory power (adjusted R2 = 0.329). It introduces psychological ownership, which has a large positive effect (0.274, p < 0.001). This suggests that individuals who feel a stronger sense of ownership are more likely to prefer working in EO companies in future. While working conditions remain significant, their effect is less pronounced, and employee influence loses significance. As in previous models, the decision to join the company due to EO continues to have a strong impact on future EO preferences.

The coefficient on the variable measuring the selection effect is significant throughout, indicating that hypothesis 2 is supported. Indeed, the analysis demonstrates that on the whole the most significant factor influencing preferences for working in employee-owned companies in future is the selection effect (the beta coefficient for psychological ownership is somewhat larger in the final model). Factors such as working conditions contribute to shaping these preferences, but the decision to engage with an EO company remains paramount.

Discussion

Contributions

Overall, our results on the relationship between employee ownership and psychological ownership are consistent with other studies of employee ownership: plan membership is associated on average with higher levels of psychological ownership. However, delving down into the results, we also find higher levels of psychological ownership amongst those who are not yet in the plan but to whom employee ownership appears to be important, as indicated by the influence of employee ownership on their decision to join the firm. This group records higher levels of psychological ownership than those in the plan but for whom employee ownership seems to be of less importance.

Overall, selection effects, in terms of certain employees being attracted to the firm because of employee ownership, appear to be important. The regression results suggest that the selection effect has a larger effect than that of plan membership on psychological ownership. The decomposition analysis indicates that 34.7% of the difference in psychological ownership between individuals who viewed EO as important when they joined the firm and those who did not can be attributed to the selection effect.

In terms of contribution to the literature, our results confirm what has long been suspected – that selection effects can be an important contributor to the apparent employee-level effects of an employee ownership programme (cf. Weltmann et al., 2015). The magnitude of plan effect is reduced once selection effects are taken into account. Those studies that find a substantial effect of plan membership on employee attitudes, such as McCarthy et al. (2010), might find that this is reduced if prior views are incorporated. Equally, our results find that employee ownership nevertheless has an effect on employee attitudes even after the selection effect is controlled for.

An important finding from our study is that employee ownership does not initially appeal to everyone, and we should not expect the effects of employee ownership to be viewed as uniformly positive. Only a minority of relatively new employees indicate that employee ownership was an important factor in their decision to join the firm (29% of the sample), despite a much larger number knowing that the company was employee owned (65%). Nevertheless, 53% of those in the plan indicate that they would seek to work in an employee-owned firm in future, compared with 35% of those not yet in the plan (chi-square statistic significant at p < 0.002). There are a few who disagree with the statement that they would prefer to work in an EO firm in future (4% of those in the plan, 10% of those not in it), with the remainder being agnostic. Unsurprisingly there is an age dimension to this – the youngest age group, members of which are not yet in the plan, are least likely to indicate a preference to work in an EO firm in future, whilst the oldest age group is the most likely.

In considering the relationship between selection and psychological ownership, we are able to add to psychological ownership theory. This theory has focused on the feelings that individuals (and groups) have about objects that they feel they possess. An early exploration identified various features of employee ownership that can contribute to psychological ownership (Pierce et al., 1991). Their model suggested that employee views prior to experiencing ownership can also be important, and argues that psychological ownership theory should incorporate expectations of ownership. Our study adds to this by finding that the importance of employee ownership as a factor in joining the firm has a strong influence on levels of psychological ownership. Indeed, we find that those with positive prior views of employee ownership have relatively high levels of psychological ownership even when they are not yet formal owners of the company. More generally, the research is supportive of those perspectives that emphasize that prior preferences and expectations are important in influencing evaluations and reactions to employee ownership (Klein and Hall, 1988).

Although our study is cross-sectional, it does provide some indication of how the current experience of employee ownership fits with past experience and forward-looking, albeit hypothetical, preferences for the future. It therefore enables a more dynamic interpretation of the effects of employee ownership. Ideally, future studies will adopt a longitudinal design so these considerations can be explored with greater validity and reliability.

Implications for practice

Although the study is geared towards issues arising in the academic literature regarding employee sorting, our findings nonetheless have a set of practical implications for those managing employee-owned companies. The first is that provision of an employee ownership plan, such as an ESOP, does have positive effects on psychological ownership even though the effects of plan participation are smaller than when selection effects are not considered. Thus, companies can benefit in terms of employees’ sense of ownership by moving to employee ownership. Second, to ensure a good match between new employees and the firm, those involved in recruitment and selection could delve more into prospective employees’ views of employee ownership during the selection process. Third, companies might publicize their employee ownership status so as to attract potential employee recruits who are more favourably inclined towards employee ownership.

Limitations

Although the article provides illuminating insights on the role of selection into ESOPs, there are some limitations that need to be highlighted. Perhaps the most important is that the information on the role of employee ownership as a factor in joining the company could be subject to recall bias (Golden, 1992; Schwenk, 1985). Respondents may see their past decisions through ‘rose-tinted spectacles’, possibly because they have come to like employee ownership since being employed by the firm, or their recollections could just be wrong. We have tried to limit the potential for this by restricting the sample to those who have been employed for five years or less, on the basis that the more recent the decision the less likely recollections are to be biased. We investigated this further by comparing the mean scores on this variable for those with under one year’s tenure (who are also not yet in the ESOP) with those with tenure from one to five years, finding no significant differences between them in an independent samples t-test. A further feature which suggests that biases are not substantial is that the coefficients for this variable and for psychological ownership function largely independently of each other.

Another limitation of our study lies in the use of a hypothetical question when asking respondents whether they would consider working for another employee-owned firm if they were seeking a new job. While this question does not directly measure EO satisfaction in the traditional sense, it serves as a valuable proxy for understanding perceptions and evaluations of EO. As research has shown, hypothetical questions can be a valuable tool for exploring respondents’ attitudes when aiming to infer potential future behaviours or preferences (Hargittai et al., 2020; Keusch et al., 2019). Given the typically high turnover rates in the retail sector (Booth and Hamer, 2007), this hypothetical question is particularly relevant as it reflects a realistic scenario that employees may actively think about.

Unlike many studies of employee attitudes in ESOPs and other employee-owned organizations (e.g. Buchko, 1993; Gamble et al., 2002), we are not able to consider the financial benefits of participation in the plan and how this might influence psychological ownership. We do not have comprehensive information on the size of plan allocations to individuals once they are enrolled in the plan, or on plan balances. We cannot impute these from Form 5500 information because our tenure measure is a categorical one, meaning that we cannot precisely allocate annual allocations. However, as our sample is limited to those in the early years of ESOP membership, we do not anticipate substantial variations in plan balances. Nor are plan balances likely to be substantial given the limited time in the plan. Hence, we anticipate that variations in the financial benefit of ESOP membership have a limited effect on employee attitudes.

Our models include subjective evaluations of working conditions and employee influence as independent variables, and it might be argued that they could be used as alternative dependent variables. Whilst this could be illuminating, we have chosen not to do this so as to keep a focus on psychological ownership and to maintain some comparability with previous studies of employee ownership outcomes. We are also mindful that previous research has demonstrated that subjective perceptions of the work environment shape employee attitudes and behaviours, and finds that subjective work-related context factors are robust predictors of attitudinal outcomes such as commitment (Ahakwa et al., 2021; Zhenjing et al., 2022). Our results indicate that including working conditions as an independent variable substantially increases the models’ R2.

We are not able to observe employees who have sorted out of the plan by leaving their employment. Employees sorting out of the variable pay scheme is an important component of Lazear’s results. Whilst worker capacity to devote extra effort does not appear to be an issue for us, given our research design and objectives, it is possible that employees who do not like ESOPs select out of the firm before they become eligible to participate. We cannot rule this out due to data limitations, but we nevertheless believe this is not important for several reasons. One, the long-standing and well-known nature of the ESOP suggests that employees who dislike ESOPs would not have become employed in the first place; two, interview data indicate that most of the employee turnover arises from college students working part-time then leaving to pursue university courses or embark on their full-time careers.

Finally, whilst our study is an attempt to deal with some of the limitations arising from the use of single period cross-sectional surveys, it does itself take this form. This reflects the practical difficulties of securing access to conduct ‘before and after’ studies of employee ownership conversions. Ideally, future studies would take a multi-period form, perhaps obtaining information at the point individuals join the company prior to a later survey of them, but this may not be easy to achieve.

Conclusions

Our study confirms that selection effects significantly impact psychological ownership and future employment preferences. It enhances psychological ownership theory by showing that pre-existing views on employee ownership influence psychological ownership, even before employees formally become owners. Employees who join a company because of employee ownership tend to display higher psychological ownership and stronger preferences to work in employee-owned firms in the future. This demonstrates that selection effects not only affect psychological ownership but also directly shape future employment preferences, highlighting the importance of considering these effects in employee ownership research.

Despite the prominence of these selection effects, the study also confirms that participation in an employee ownership plan does impact employee attitudes. However, the key implication is that the direct effect of plan membership may be smaller than previous studies have suggested, especially when selection effects are accounted for. By quantifying the magnitude of these selection effects, the study offers a deeper understanding of their significance.

The practical implication of this study is that managers of employee-owned companies should prioritize attracting recruits who already have positive views of EO. This can be achieved through strategic branding and emphasizing the employee ownership model in recruitment materials. Additionally, understanding the role of selection effects can help organizations better assess the true impact of EO on employee attitudes and behaviours, enabling more informed decision-making in recruitment and retention strategies.

Supplemental Material

sj-docx-1-eid-10.1177_0143831X251389047 – Supplemental material for Employee ownership and attitudes: The role of selection effects

Supplemental material, sj-docx-1-eid-10.1177_0143831X251389047 for Employee ownership and attitudes: The role of selection effects by Rebecca Fichtel, Andrew Pendleton, Thomas Steger, Nadia Faltermeier, Juliane Fink and Carmen Sitz in Economic and Industrial Democracy

Footnotes

Appendices

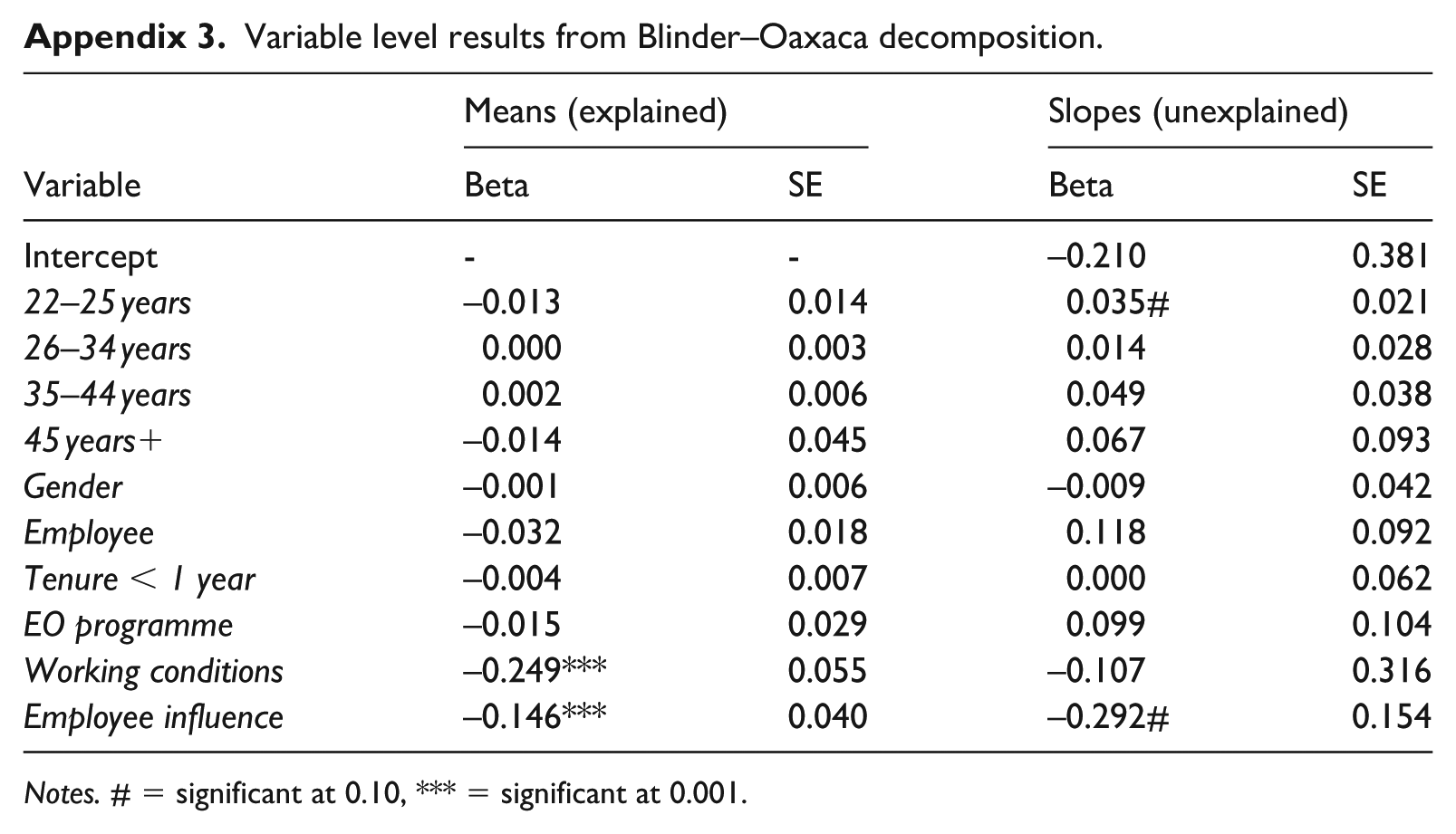

Variable level results from Blinder–Oaxaca decomposition.

| Variable | Means (explained) | Slopes (unexplained) | ||

|---|---|---|---|---|

| Beta | SE | Beta | SE | |

| Intercept | - | - | –0.210 | 0.381 |

| 22–25 years | –0.013 | 0.014 | 0.035# | 0.021 |

| 26–34 years | 0.000 | 0.003 | 0.014 | 0.028 |

| 35–44 years | 0.002 | 0.006 | 0.049 | 0.038 |

| 45 years+ | –0.014 | 0.045 | 0.067 | 0.093 |

| Gender | –0.001 | 0.006 | –0.009 | 0.042 |

| Employee | –0.032 | 0.018 | 0.118 | 0.092 |

| Tenure < 1 year | –0.004 | 0.007 | 0.000 | 0.062 |

| EO programme | –0.015 | 0.029 | 0.099 | 0.104 |

| Working conditions | –0.249*** | 0.055 | –0.107 | 0.316 |

| Employee influence | –0.146*** | 0.040 | –0.292# | 0.154 |

Notes. # = significant at 0.10, *** = significant at 0.001.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.