Abstract

This study examines differences between non-standard (here: temporary employees and solo self-employed people) and standard workers (here: permanent employees) in financial hardship. It also examines whether these differences are conditional on the country context. To this aim, multilevel regression analysis was applied to European Social Survey data, covering 32 countries and the time period 2002–2018. The results show that temporary employees and the solo self-employed report more financial hardship compared to permanent employees, and that temporary employees experience more financial hardship than the solo self-employed. Both macroeconomic decline and higher levels of social protection generally enlarge the gap in financial hardship between non-standard and standard workers. Furthermore, solo self-employed persons are hit harder by macroeconomic adversity and they are not or less entitled to social benefits than temporary employees, reflected by smaller differences in financial hardship between these groups of non-standard workers. The findings are mostly in line with labor market dualization theories.

Introduction

Non-standard paid work has become commonplace as a result of globalization, the expansion of service industries and changing demographics of the labor force (Eurofound, 2018; Kalleberg, 2000). Any form of paid work that is not full-time, indefinite and for a single employer is widely considered non-standard (ILO, 2016). Although we acknowledge that non-standard work is an umbrella term that encompasses many forms of paid work, such as on-call work, part-time jobs and disguised employment, non-standard work will here refer to temporary employment and self-employment, as the purpose of this study is to compare employees on an open-ended contract (here standard workers) to those on a fixed-term contract and self-employed people with and without personnel (here non-standard workers) in terms of financial hardship. A permanent contract is still the most prevalent employment relationship in the European Union (EU), yet about 12% of all working individuals aged 15–64 years had a temporary contract and near 11% were self-employed in 2023 (Eurostat, 2023). Even under our narrow definition that excludes part-time employment, almost a quarter of the labor force has a non-standard employment arrangement.

An often-heard concern is that non-standard work is uncertain, unstable and insecure (Kalleberg and Vallas, 2018). Temporary contracts may offer greater flexibility and act as a stepping stone, providing opportunities to enter the labor market and gain human capital (Gash, 2008; Giesecke and Groß, 2003), yet a majority of temporary workers would prefer more security and an indefinite contract (ILO, 2016). Similarly, being your own boss provides autonomy and flexibility for some, while solo self-employment is an intermediate situation between employment and unemployment for others (Eurofound, 2017). Previous research showed that employees on a temporary contract generally report more income, job and employment insecurity than permanent employees (Burgoon and Dekker, 2010; Chung, 2019; Kiersztyn, 2018). Most evidence also points to negative wage effects of temporary employment, at least when compared to permanent employment (Latner and Saks, 2022). Moreover, temporary employees are less protected from dismissal and usually receive less social security benefits compared to permanent workers (Kalleberg, 2000).

The self-employed are often excluded from these studies because the insecurity they face would not result from their specific employment arrangement, but exclusively from market forces (Kiersztyn, 2018). As insecurity is seen as part of the game for self-employed workers, a comparison to employees is often left out (Conen and Schippers, 2019b). The group of self-employed persons is highly diverse though, ranging from genuine entrepreneurs employing staff to independent contractors, freelancers, on-call workers, platform workers and solo self-employed workers who have limited employment alternatives (Murgia et al., 2020) and were pushed into self-employment (Kautonen et al., 2010). Prior studies demonstrated that solo self-employed persons experience a lot of insecurity as well, which is not only due to labor market conditions, but also because of, for example, no or limited pension entitlements and a lack of health and disability insurance, which in part also applies to self-employed people with employees (Borghi et al., 2018; Conen and Schippers, 2019a; Murgia and Pulignano, 2021; Schulze Buschoff and Schmidt, 2009; Spasova et al., 2017). Labor market transformations and particularly the changing nature of self-employment have resulted in a grey area between dependent employment and self-employment (OECD, 2019). This raises the question to what extent the situation of in particular the solo self-employed is nowadays really so different from that of temporary workers. We will therefore make a distinction between solo self-employed workers and self-employed workers with personnel, which we label business owners.

The current study bridges the seemingly separate strands of literature on insecurity related to having a temporary contract and being solo self-employed by directly comparing these groups of non-standard workers and by comparing them to standard workers in terms of the extent to which these ‘individuals or households are unable to fulfil fundamental physiological and security needs while working’ (Conen and Schippers, 2019b: 5). Specifically, we look at financial hardship while working: that is, finding it difficult to cope on the household’s income, which is a meaningful indicator of insecurity and vulnerability for both employees and self-employed workers. 1 Using a subjective measurement of financial hardship largely remedies the issue that earnings from self-employment are known to be quite difficult to measure and compare to wages of employees. Furthermore, we focus on household income rather than individual income because the latter does not necessarily tell us if a person has difficulties making ends meet when a partner also contributes income to the household. Our approach enables us to study financial hardship among both non-standard and standard workers and to compare their situation.

Differences in financial hardship among and between these groups of workers are likely to depend on the economic and institutional context. Thus far, research has primarily concentrated on country differences in income, job and employment insecurity, highlighting that poor macroeconomic performance is positively, whereas a high level of social protection is negatively associated with financial hardship (Nelson, 2012; Van Oorschot and Chung, 2015; Visser et al., 2014; Whelan and Maître, 2013). Little is known, however, about the role of these characteristics in shaping differences in financial hardship among non-standard workers and between non-standard and standard workers. Studies on the conditions under which non-standard and standard employment arrangements relate to insecurity are scarce and tend to exclude the (solo) self-employed (e.g., Chung, 2019; Kiersztyn, 2018; Lübke and Erlinghagen, 2014). Yet, based on labor market dualization theories (Emmenegger et al., 2012; Lindbeck and Snower, 1989) and reference group theory (Whelan et al., 2001), it can be expected that macroeconomic adversity and the degree of social security in a country do not affect all workers equally. We argue that a worse performing economy disproportionally hits non-standard workers, especially the solo self-employed. Furthermore, we test competing hypotheses on the role of social protection, examining whether higher levels of social security in a country lead to smaller (especially non-standard workers are protected) or larger differences (especially standard workers are protected) in financial hardship between non-standard and standard workers. In doing so, this study contributes to our understanding of the extent to which the gap in financial hardship between temporary workers and solo self-employed people and between these two groups of non-standard workers and standard workers is conditional on macro-level features. We also explore empirically whether these dynamics differ for men and women.

In sum, this study addresses the following research question: To what extent are differences in financial hardship among non-standard workers and between non-standard and standard workers across Europe modified by macroeconomic decline and the level of social protection? By answering this question, we contribute to the literature in two main ways. First, we include a broader range of employment arrangements, focusing not only on dependent employment, but also on self-employment. This allows us to assess whether insecurity experienced by people who have a temporary contract is similar to that experienced by solo self-employed workers, as recent labor market developments suggest. It also results in a more comprehensive picture of the variability in financial hardship between workers in non-standard and standard work arrangements. Second, this study pays explicit attention to the question whether this variability is influenced by macroeconomic adversity and social protection. To the best of our knowledge, this is the first study that examines these cross-level interactions while including both employees and the self-employed. As such, this study tests implications from dualization theories and reference group theory and improves our understanding of the context dependency of the gap in financial hardship between non-standard and standard workers and between temporary employees and solo self-employed persons. We do so by using high-quality data from the European Social Survey (ESS), examining a larger number of countries (32) over a longer time span (2002–2018) than any previous study.

Theory and hypotheses

Financial hardship

Financial hardship here reflects the extent to which individuals find it difficult to live on their current household income. Earlier studies have used ‘all combinations of financial/economic and strain/stress/hardship’ (Blekesaune, 2013: 60) to refer to this concept. Both objective factors (e.g., actual income) and subjective aspects (e.g., income insecurity) may play a role in experiencing financial hardship. Note that income and financial hardship are correlated, but clearly distinct concepts (Whelan et al., 2001). Households with high income might still experience financial hardship because of, for example, high mortgage payments, alimony or children attending college. Vice versa, households with a low income do not necessarily experience difficulties in making ends meet if the expenses match the income situation. Financial hardship is thus not only influenced by actual income. It is also related to financial obligations, coping capacities and worries about future difficulties. Furthermore, Whelan and colleagues (2001) argue, based on reference group theory, that individuals’ subjective evaluation of financial hardship is largely shaped by a comparison to similar households.

Non-standard versus standard workers

According to labor market dualization and segmentation theories, the labor market consists of a primary and secondary segment, with jobs in the primary segment offering employment security (i.e., permanent contracts) and higher wages. Contrastingly, people who work in the secondary segment of the labor market are more expendable and earn less (Eichhorst and Marx, 2015; Emmenegger et al., 2012; Lindbeck and Snower, 1989; Piore, 1975). Non-standard workers are usually regarded as labor market outsiders who are employed in this secondary tier, in particular when temporary contracts are used by organizations to increase flexible staffing and respond to fluctuations in the business cycle. This also involves solo self-employed people, as a fairly new way through which organizations achieve flexible work arrangements is by firing and rehiring own-account workers (Natili and Negri, 2023). Such non-standard employment practices are usually not covered by traditional labor and social security laws (Eurofound, 2017). Both temporary workers and the solo self-employed thus face unstable employment and more frequent layoffs. They are also worse off in terms of training opportunities and career advancement prospects compared to standard workers. This limits non-standard workers’ accumulation of human capital and subsequently harms their employment opportunities and earnings potential (Giesecke, 2009; Horemans, 2017). Business owners are generally perceived to be labor market insiders (Conen and Schippers, 2019b). They probably started out in solo self-employment, yet are now relatively successful compared to the solo self-employed in the sense that they (can afford to) have employees. Although business owners are traditionally referred to as non-standard workers, it is plausible that the level of financial hardship experienced by business owners is closer to or even lower than that of standard workers.

Empirical evidence suggests that temporary workers suffer a wage penalty compared to permanent employees because they have less bargaining power and shorter tenure and because employers offer new employees lower wages while observing and evaluating their performance (ILO, 2016; Westhoff, 2022). Prior studies also showed that workers on a temporary contract and solo self-employed individuals face increased risks of in-work poverty due to their incomplete labor force attachment and a wage penalty (Crettaz, 2013; Halleröd et al., 2015). This objective disadvantaged financial position of these groups of workers should result in them reporting higher levels of financial hardship than standard workers. Additionally, non-standard workers experience more insecurity and are more worried about future prospects. In the case of temporary employees it could be that financial hardship is partly fueled by the knowledge that their contract will expire and future earnings are uncertain; for (solo) self-employed persons it could be the struggle to keep the business running, the acquisition process and the accompanying irregular income.

Furthermore, from a reference group perspective, some groups of non-standard workers are likely aware of their comparatively vulnerable position in the labor market. Research has shown that many employees on a temporary contract would prefer a permanent contract (ILO, 2016). This also holds true for some groups of solo self-employed workers, particularly those who are solo self-employed for involuntary reasons (Conen et al., 2016). The awareness of having a relatively disadvantaged position compared to standard workers is also expected to result in higher levels of reported financial hardship. Note that non-standard workers might have another reference group and compare themselves to unemployed people (Gebel, 2013), which in that case would mean they report lower levels of financial hardship compared to when permanent employees are the reference group. However, it can still be expected that, on average, non-standard workers experience more financial hardship than standard workers.

Making a comparison within the group of non-standard workers is more challenging, at least when it comes to the comparison between temporary workers and the solo self-employed. A recent study has indeed shown that solo self-employed people are very much similar to other groups of non-standard workers in terms of the employment and income insecurity they experience (Natili and Negri, 2023). This study found one relevant distinction, namely the access to social protection, with solo self-employed persons facing (even) higher barriers to social benefits compared to other non-standard workers, such as those on a temporary contract. This means that, all else being equal, the solo self-employed can be expected to experience more financial hardship than temporary workers.

The moderating role of the country context

One of the main contributions of this study is its focus on the interplay between the macro and micro level. We argue that it is important that variation in the gap in financial hardship between non-standard and standard workers and between temporary employees and solo self-employed people is understood in light of a country’s economic and institutional context. Here we examine macroeconomic decline and social protection. These country characteristics have previously been used to either explain cross-national variation in perceived employment and job insecurity or to determine whether non-standard workers react differently to these contextual circumstances in terms of employment and job insecurity (e.g., Chung, 2019; Kiersztyn, 2018; Lübke and Erlinghagen, 2014). We are unaware of any studies that focus on differences in financial hardship between non-standard and standard workers that include the self-employed and examine to what extent differences are conditional on the state of the economy and the level of social protection in the country where people work.

Starting with the economic situation in a country, when economic and labor market conditions deteriorate, the demand for products and services decreases. Especially for temporary employees and the solo self-employed it might then be more difficult to keep and find work. Labor market insider-outsider theory states that labor market outsiders, such as temporary workers and solo self-employed people, are in a relatively uncertain employment situation and most vulnerable to market forces (Kiersztyn, 2018; Lindbeck and Snower, 1989). When macroeconomic conditions become poorer, they will be the first to feel the economic implications for their work and financial situation. Insecurity caused by their employment arrangement becomes even more immediate and worries about future difficulties are likely to increase even further. Put differently, existing insecurities are reinforced by poor macroeconomic performance. Research by Mau and colleagues (2012), also based on ESS data, has similarly shown that only the less privileged occupational classes report higher levels of socio-economic insecurity when unemployment levels are higher. We expect this to be especially the case among solo self-employed people as their situation is even more dependent on the business cycle compared to temporary workers. Although people on a temporary contract also face a lot of insecurity, they at least have an employment arrangement that provides them an income for as long as it lasts. Thus, our expectations are as follows:

Hypothesis 1: The larger the macroeconomic decline, (a) the larger the difference in financial hardship between non-standard and standard workers and (b) the larger the difference between temporary workers and the solo self-employed.

Moving on to the level of social protection in a country, prior studies showed that average levels of financial hardship are lower in countries with higher social spending (Nelson, 2012; Visser et al., 2014). Even for people engaged in paid work, the presence of social safety nets, such as unemployment and disability benefits, may mean people feel protected and less insecure, resulting in them reporting less financial hardship than in countries where social protection is absent or less generous. It is likely, however, that not everyone benefits, or benefits equally. Given that the solo self-employed are typically responsible to take care of their own social insurance (Conen et al., 2016), the cushioning role of social security is expected to be most strongly felt by employees with a temporary contract because they have the most to gain from, for instance, unemployment benefits.

For some groups of non-standard workers, including the solo self-employed, it could be that they were unemployed in the past and now have a non-standard work arrangement because of that unemployment episode. If they previously received benefits to secure a decent living, they could take that into account when assessing how they feel about their current labor market position and income. A country’s social safety net may thus provide a sense of income security, especially for non-standard workers. Moreover, social protection encompasses more than income replacement. It may also involve cash transfers for housing, childcare or healthcare purposes, which are often conditional on income. As non-standard workers, on average, have lower income than standard workers (ILO, 2016), they are more likely to receive these other forms of governmental social assistance compared to standard workers. As a result, they will likely report comparatively less financial hardship in countries with higher social spending. This corresponds to what reference group theory predicts, as non-standard workers may feel that especially they benefit from welfare benefits or that they can fall back on social security if need be. In sum, our next hypothesis reads:

Hypothesis 2: The higher the level of social protection, the smaller the difference in financial hardship between non-standard and standard workers.

Based on labor market dualization theory and welfare dualism, a contrasting hypothesis on the role of social protection can be formulated. Rather than closing the gap in financial hardship between non-standard and standard workers, higher levels of social protection may enlarge this gap. Labor market insiders, that is, standard workers, have a lot of bargaining power and would disproportionally benefit from employment protection and welfare benefits. Social assistance partly came into existence through negotiation by labor unions for standard workers (Esping-Andersen, 1999; Flora and Heidenheimer, 1981), who to this day may benefit from social protection in terms of their experienced level of financial hardship. For example, in many countries, eligibility for unemployment benefits is linked to continuous employment and paying social security contributions. This partly restricts access to unemployment benefits to standard workers, likely leading to more trust in their financial situation. In contrast, labor market outsiders, such as temporary employees, do not experience these advantages. Being institutionally excluded then could even be called a socio-economic risk (Natili and Negri, 2023; Schwander and Häusermann, 2013). Note again that solo self-employed persons are usually excluded from national social protection schemes (Conen and Schippers, 2019b), so this means that when looking at the group of non-standard workers only, it can be expected that temporary workers are further removed from solo self-employed people in terms of reported financial hardship when there is an extensive social safety net in place. In a sense, temporary employees are to a lesser degree labor market outsiders as temporary contracts do provide more social security than solo self-employment. Hence, our final expectations are:

Hypothesis 3: The higher the level of social protection, (a) the larger the differences in financial hardship between non-standard and standard workers and (b) the larger the difference between temporary workers and the solo self-employed.

Data and measurements

European Social Survey

This study employs data from nine rounds of the European Social Survey (ESS), conducted biennially between 2002 and 2018. The survey data are collected through face-to-face CAPI interviews and the questionnaire has been administered in 38 countries to date. In each country the population consists of all persons aged 15 and over (no upper age limit) living in private households, regardless of their nationality, citizenship or language. Individuals are selected by random probability methods. A minimum target response rate of 70% has been specified, but achieving this target has proven to be difficult in many countries, with an average response rate across all countries and waves of 59.2% and response rates varying between 27.6% and 81.4%. More detailed information about the questionnaires, sampling procedures and data collection can be found on the website of the ESS: https://www.europeansocialsurvey.org.

Selection of cases

After merging the data from all nine rounds, Albania (N = 1,201), Kosovo (N = 1,295), Latvia (N = 2,898), Montenegro (N = 1,200), Romania (N = 2,146) and Serbia (N = 2,043) were first removed because of a (too) low number of (solo) self-employed people and/or lacking data on the country characteristics. Second, we selected people aged 18 to 59 years who are engaged in paid work for at least 12 hours a week. Limiting the age range ensures that we examine adults and makes it likely that we exclude workers who already receive some form of retirement income. This is important because they are plausibly a selective group in terms of work characteristics and experienced financial hardship. Third, the sample was restricted to persons who have established an independent household. We do not want to include employed children who still live in the parental home as the measure of financial hardship pertains to the household’s income. No direct measure was available, but as a workable solution we removed singles under the age of 25 who do not have children themselves and live with at least one parent in the household. Altogether, these case selections resulted in a sample size of 177,457 individuals, 221 country-wave combinations and 32 countries.

Multiple imputation of missing values

We used the fully conditional specification (FCS) approach in SPSS version 29, also called multivariate imputation by chained equations (MICE), to impute missing values on the individual-level variables (15 imputed datasets, 20 iterations). We included all individual-level variables (see Table 1) as predictors in the imputation model, along with country and ESS round dummy variables to take into account the hierarchical nature of the data. We also included three auxiliary variables, namely health, religiosity and size of city or village. A total of 28,669 respondents (16.2%) had at least one missing value. The missing data proportions ranged between 0.04% (gender) and 7.47% (working hours). 2

Dependent variable

The outcome variable in this study is financial hardship. Respondents were asked which of the descriptions on a showcard came closest to how they felt about their household’s income nowadays. The answer categories were ‘living comfortably on present income (0)’, ‘coping on present income (1)’, ‘finding it difficult on present income (2)’ and ‘finding it very difficult on present income (3)’. Previous studies have also relied on this measure to capture the subjective assessment of financial hardship (e.g., Conen and Schippers, 2019b; French and Vigne, 2019). We regard financial hardship as an interval variable because we are interested in whether people experience less or more financial hardship. We argue, for instance, that the step from living comfortably on present income to coping on present income is also relevant, as this step represents meaningful change in people’s lives. Thus, we are interested in analyzing the full range of our outcome variable. Having said that, we will also analyze a dichotomous measure of financial hardship, with categories 0 and 1 coded as 0 (80.8%) and categories 2 and 3 coded as 1 (19.2%), and compare the results of the linear and logistic regression models.

Independent variable

To construct the measure of employment arrangement, we used three variables in the ESS data: employment relation (employee or self-employed), employment contract (unlimited or limited duration) and the number of employees of a person. We combined these variables to construct a new variable consisting of four categories: permanent contract (employee and unlimited duration of contract), temporary contract (employee and limited duration of contract), solo self-employed (self-employed and no employees) and business owner (self-employed and at least one employee). Temporary employees and the solo self-employed are regarded as non-standard workers and permanent employees as standard workers. As discussed, business owners are traditionally classified as non-standard workers, but we argue that they are not in a comparable situation as temporary workers and the solo self-employed.

Moderating variables

The country context is hypothesized to moderate gaps in financial hardship between workers with different employment arrangements. Macroeconomic conditions and the level of social protection are measured, in each combination of country and year, by change in GDP per capita and social spending. Figures on GDP were obtained from the data website of the World Bank (data.worldbank.org). The growth rate in GDP was calculated by taking the percentage of increase or decrease in GDP comparing the year of the ESS wave and the previous year. This measure of economic activity resembles the popular definition of periods of expansion and contraction based on quarterly changes in GDP. As we cannot match quarterly changes to the country-year combinations, we use the yearly equivalent. Note that a higher score on this variable denotes macroeconomic growth instead of macroeconomic decline, so the regression coefficients regarding this indicator have to be interpreted the other way around. Expenditures on social protection, measured as percentage of GDP, were taken from the Government Finance Statistics (GFS) section on the data website of the International Monetary Fund (IMF) (data.imf.org). It includes not only unemployment benefits, and sickness and disability benefits, but for example also expenditures on housing, and family and children. As such, it is an indicator of the general level of social protection in a country-year.

Control variables

To reduce omitted variable bias and to tap into the expenses households have, we control – at the individual level – for unemployment in the last five years, occupation based on the International Standard Classification of Occupations (ISCO), working hours in the main job, educational level based on the International Standard Classification of Education (ISCED), biological sex (0 = male, 1 = female), age (as a proxy for the time spent in the labor market), migration background (i.e., respondent and/or both parents born abroad), partner’s employment status (categories for employed, non-employed and not having a partner; the latter group consisting of people who do not have a partner and people who do not live together with their partner), partner’s educational level (also ISCED) 3 and number of children living in the household.

Taking these controls into account makes the groups of non-standard workers to standard workers more similar, so that we are better capable of singling out what matters about their employment arrangement for financial hardship. 4 The partner variables seem especially important in that regard. Self-employed persons without personnel may have started their own small business because they could afford it. For instance, a partner who earns a stable, high income may have allowed them to monetize their talent or hobby. These self-employed individuals might have a low, insecure income, but they will not experience financial hardship. We partially take this into account by controlling for partner’s work status and education in the analysis, but based on this reasoning, temporary workers should report more financial hardship than the solo self-employed.

We also control for GDP per capita at power purchasing parity (PPP) and current prices, which was logged to reduce the influence of country-wave combinations with high GDP per capita, and the unemployment rate, derived from the statistical database of the United Nations Economic Commission for Europe (UNECE). Additionally, we take into account the absolute change in unemployment rate in two consecutive years. All country-level variables are mean-centered. Table 1 features descriptive statistics for the variables included in the analysis.

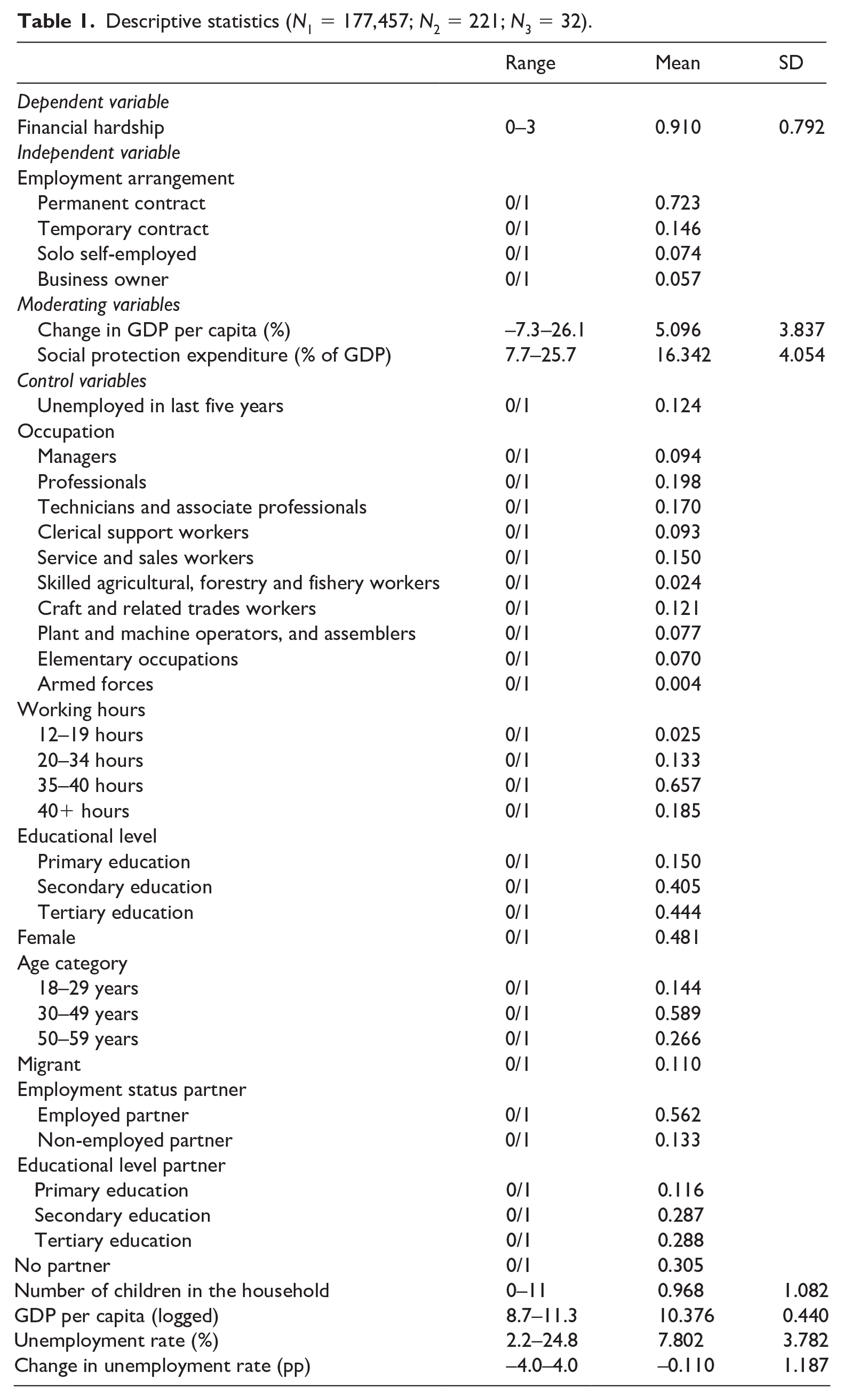

Descriptive statistics (N1 = 177,457; N2 = 221; N3 = 32).

Analysis

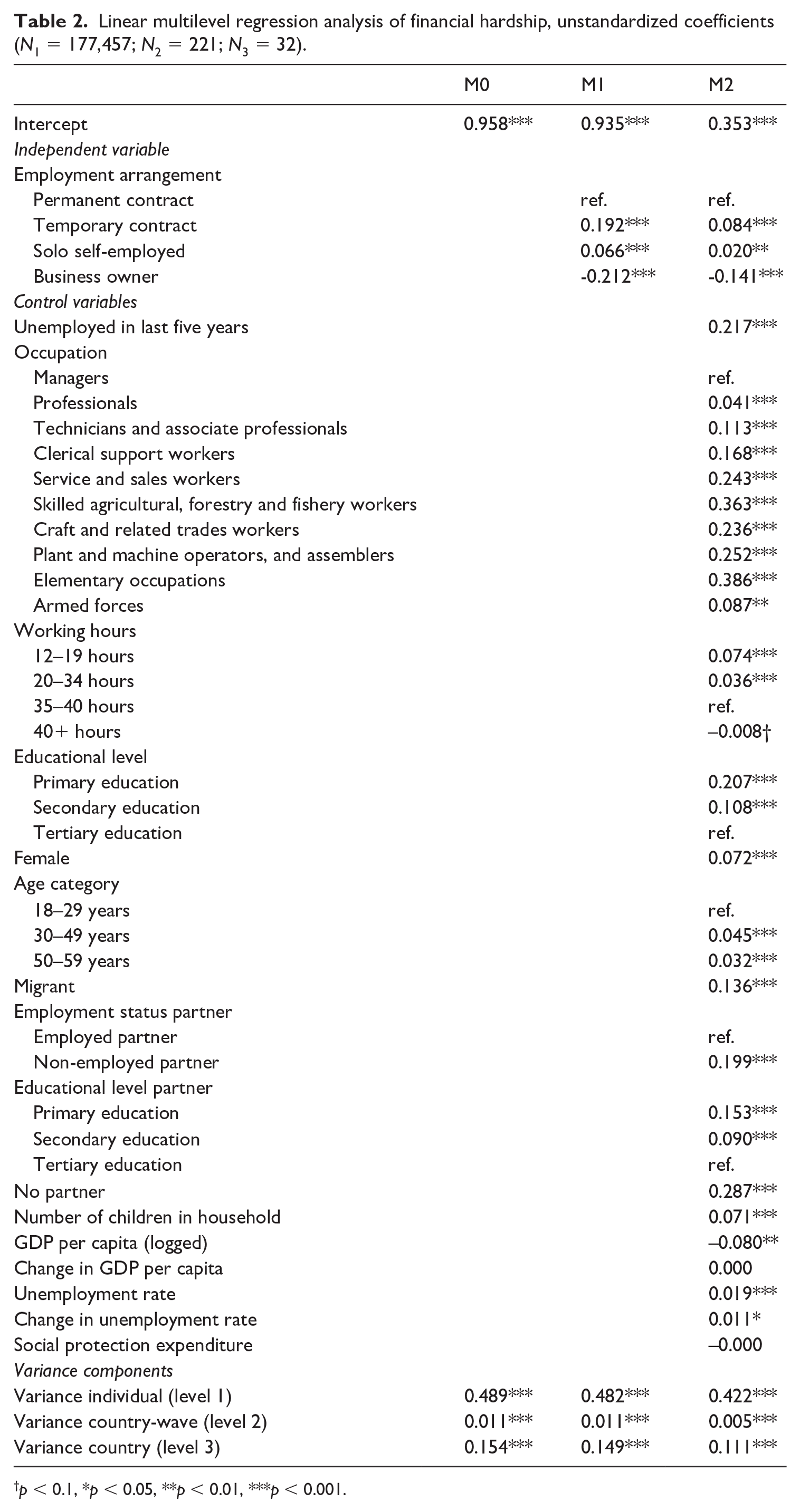

To test our hypotheses, we apply linear multilevel regression analysis (also called mixed or hierarchical models) on the multiple imputation dataset (m = 15), with respondents (level 1) nested within country-wave combinations (level 2) nested within countries (level 3). SPSS applies Rubin’s rules to obtain pooled regression coefficients and standard errors. We started with estimating a null model without predictors (see Model 0 in Table 2). Likelihood ratio tests show that all variance components are statistically significant (p < 0.001). The intraclass correlations amount to 1.7% (0.011/0.654) at level 2 (country-year) and 23.5% (0.154/0.654) at level 3 (country). In Model 1, we present the uncontrolled differences in financial hardship between non-standard and standard workers. We add the controls in Model 2. Permanent employees form the reference category in the models in Table 2. Models 3 and 4 in Table 3 test the cross-level interaction hypotheses. In these models, we included random coefficients for the dummy variables of employment arrangement (Heisig and Schaeffer, 2019). Permanent workers are the reference category in Models 3a and 4a, while temporary workers form the reference group in Models 3b and 4b. The final step of the analysis is to run these models separately for men and women to explore sex differences.

Linear multilevel regression analysis of financial hardship, unstandardized coefficients (N1 = 177,457; N2 = 221; N3 = 32).

p < 0.1, *p < 0.05, **p < 0.01, ***p < 0.001.

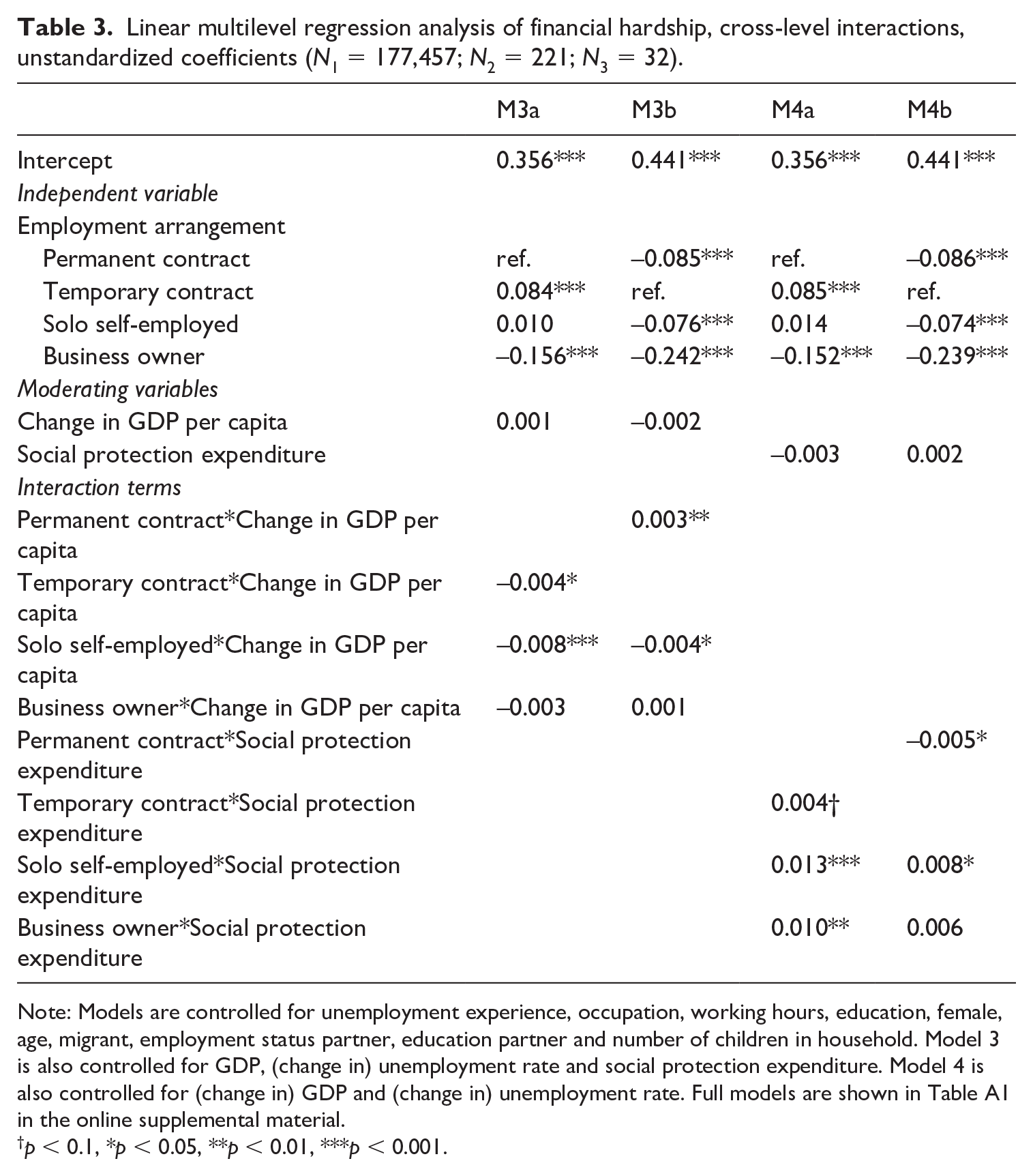

Linear multilevel regression analysis of financial hardship, cross-level interactions, unstandardized coefficients (N1 = 177,457; N2 = 221; N3 = 32).

Note: Models are controlled for unemployment experience, occupation, working hours, education, female, age, migrant, employment status partner, education partner and number of children in household. Model 3 is also controlled for GDP, (change in) unemployment rate and social protection expenditure. Model 4 is also controlled for (change in) GDP and (change in) unemployment rate. Full models are shown in Table A1 in the online supplemental material.

p < 0.1, *p < 0.05, **p < 0.01, ***p < 0.001.

In the online supplemental material (see Table A4 and Table A5), we show the results of the analysis of the dichotomized outcome variable. Binomial or logistic multilevel analysis was performed on a dataset in which the missing values were removed because SPSS does not support this type of analysis on a multiple imputation dataset. To check whether the removal of missing values was influential, we also ran the linear models on the dataset in which the missing values were deleted (see Table A2 and Table A3). Overall, these robustness checks strengthened our confidence in the main findings related to the hypotheses. Only the cross-level interaction between temporary contract and change in GDP per capita does not reach statistical significance in the binomial regression analysis, whereas it does in the linear models.

Results

Model 1 in Table 2 shows that, without any controls, temporary employees and the solo self-employed indeed report more financial hardship than people on a permanent contract, whereas business owners display lower levels of financial hardship compared to people who have a permanent contract. On average, temporary employees score about one-fifth of a scale point higher and business owners score roughly the same amount lower.

Adding all the control variables in Model 2 reduces these differences. Additional analyses (results not shown here) in which the control variables were added to Model 1 one by one demonstrate that mainly occupation and to a lesser extent recent unemployment and education are responsible for the reduced gaps, suggesting there is selection into employment arrangements. We actually want to control for these selection dynamics because it leads to a better (indirect) test of the proposed theoretical mechanisms. Still, we find differences between employment arrangements in financial hardship, over and above the controls. For example, people who have a temporary contract score 0.084 higher on the financial hardship scale from 0 to 3 than permanent employees, which corresponds to 10.6% of the standard deviation of financial hardship (0.792). This does not seem a big difference, but it is still theoretically meaningful.

We also re-ran Model 2 with temporary contract instead of permanent contract as the reference category. Findings show that the difference between having a temporary contract and being solo self-employed is statistically significant (p < 0.001), with those on a temporary contract experiencing more financial hardship than the solo self-employed. Although we did not formulate a formal hypothesis for this contrast, it was expected that, all else being equal, the solo self-employed would display higher levels of financial hardship than temporary workers. It turns out to be the other way around. We come back to this finding in the discussion.

We now turn to the cross-level interactions in Table 3. The results in Model 3a show that decreases in GDP enlarge the difference in financial hardship between those who have a temporary contract and those on a permanent contract (0.084+0.004), and between the solo self-employed and workers who have a permanent contract (0.010+0.008). The gap in financial hardship between business owners and permanent employees is not moderated by macroeconomic decline. In Model 3b the reference category is formed by temporary workers. The results from this model show that the stronger the GDP decline, the smaller the difference between temporary employees and solo self-employed persons in experienced financial hardship (–0.076+0.004).

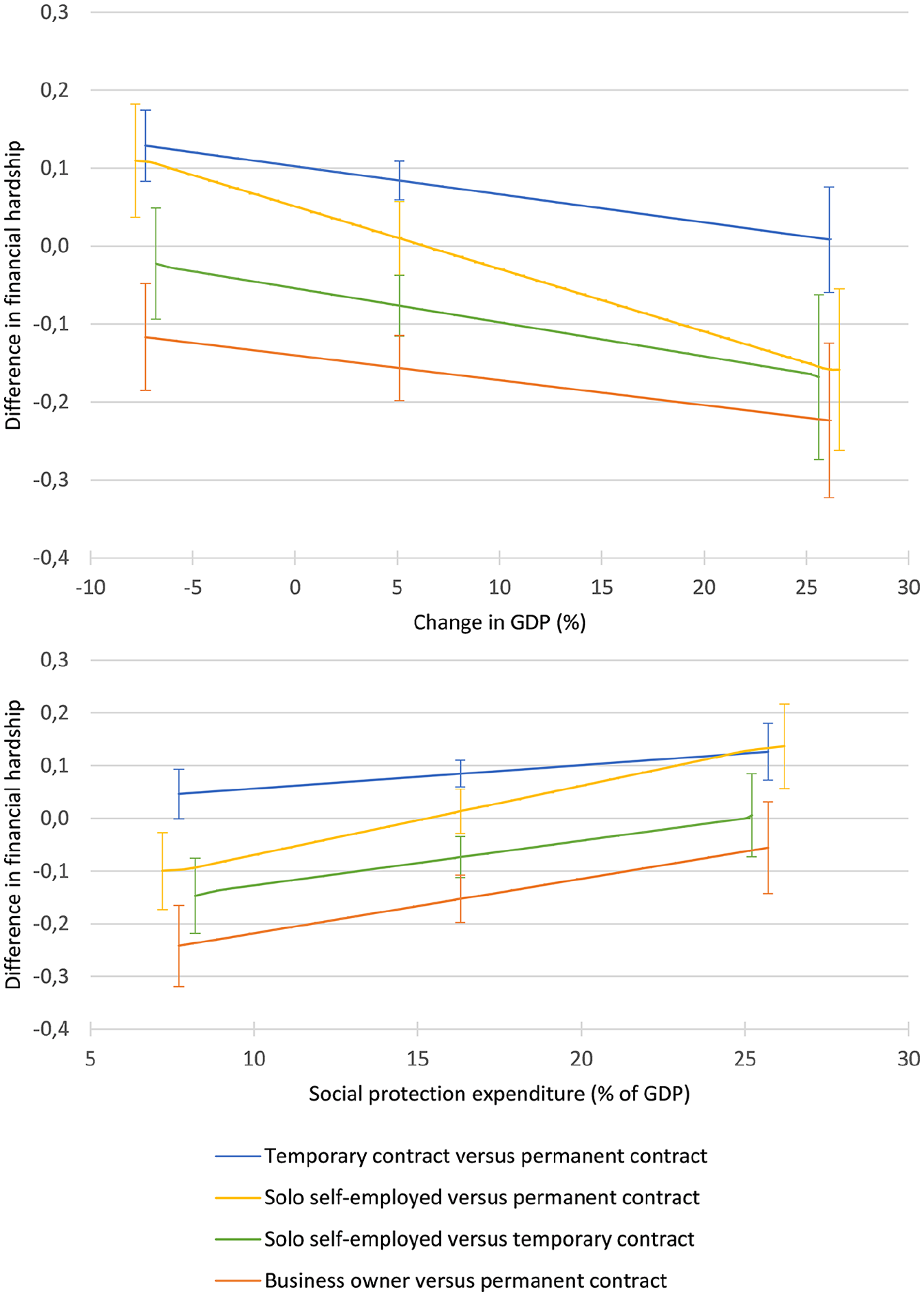

These interactions are visually represented in the upper part of Figure 1. It shows that when GDP is down by 7.3% (minimum value), workers with a temporary contract report more financial hardship than permanent employees, which holds across a large part of the range of change in GDP. Yet, people on a temporary contract and those who have a permanent contract experience similar levels of financial hardship when GDP grows by, for instance, 26.1% (maximum value). The solo self-employed report more financial hardship than permanent employees across the range of negative growth in GDP. There is no difference in financial hardship between these groups in country-wave combinations with or near the average growth gate in GDP of 5.1%, whereas solo self-employed persons experience less financial hardship than permanent workers in times of (strong) economic boom. Solo self-employed people and temporary workers report equal levels of financial hardship when GDP declines strongly, but the former group experiences less financial hardship than the latter if GDP is stable or increases. These results are in line with hypothesis 1a, but not entirely with hypothesis 1b. Although the solo self-employed indeed seem to suffer relatively more in times of economic hardship, they generally report lower levels of financial hardship than temporary employees. Overall, the effect sizes are quite modest, but it is noteworthy that some of the differences in financial hardship change from positive to negative across the range of GDP growth.

Differences between employment arrangements in estimated financial hardship at minimum, average and maximum value of country characteristics with 95% confidence intervals.

As can be seen in Model 4a, the higher the expenditures on social protection, the larger the difference in financial hardship between temporary employees (0.085+0.004, though marginally significant), the solo self-employed (0.014+0.013) and people who have a permanent contract. The gap in financial hardship between business owners and people on a permanent contract is smaller when social protection expenditure is higher (–0.152+0.010). Furthermore, the results in Model 4b show that the gap between solo self-employed persons and temporary employees is smaller when the level of social protection is higher (–0.074+0.008).

These findings are visualized in the bottom part of Figure 1. Here we can see that, regardless of the level of social protection, temporary workers experience more financial hardship than permanent employees. Compared to workers on a permanent contract, the solo self-employed display lower levels of financial hardship at the minimum value of social protection expenditure (7.7% of a country’s GDP), similar levels at the average value (16.3%) and higher levels at the maximum value (25.7%). Finally, solo self-employed persons report less financial hardship than temporary employees across most of the range of expenditures on social protection, although there is no difference between the two groups when social spending is highest. These results reject hypothesis 2 and support hypothesis 3a. Hypothesis 3b is only partially supported as, again, the solo self-employed generally report lower levels of financial hardship than temporary workers, but the latter group does seem to profit relatively more from social protection than the former group. Finally, it has to be said that also here the effect sizes do not seem that strong. It is especially interesting that relative gaps between non-standard and standard workers switch signs across the range of social spending.

Differences between men and women

As employment and the division of paid and unpaid labor between partners is highly gendered, it is likely that the consequences of having non-standard work for financial hardship are gendered as well, which is why we explore differences between men and women. Table A6 in the online supplemental material shows the descriptive statistics for men and women; Tables A7 and A8 show the estimates and significance levels of separate analyses for men and women. In general, it can be seen that the direction of the effects in these models is rather similar to the effects reported in the main models. Here we focus on some interesting differences in the findings with regard to our hypotheses.

The first noticeable difference is that among women there is no difference in financial hardship between solo self-employed women and those who have a permanent contract (see Model 2). This might be a selective group of solo self-employed women who are able to afford to have this employment arrangement, probably because there is a partner with sufficient income. Looking at the cross-level interactions and compared to the main analysis, we see that for men the results are reproduced. For women the interaction terms between temporary contract and GDP growth (Model 3) and social protection expenditure (Model 4) are not statistically significant. The analysis of the contrast between the solo self-employed and temporary workers likely runs into power issues as for both men and women the main effects and interactions are in the same direction, yet the interaction terms between being solo self-employed and the country characteristics do not reach statistical significance. We theoretically reflect on these exploratory findings in the discussion.

Conclusions and discussion

This study set out to compare non-standard workers to standard ones in terms of financial hardship. Across 32 European countries, the level of financial hardship turned out highest among temporary employees, then among solo self-employed persons, followed by permanent employees, and appeared to be lowest for business owners. Our first conclusion is therefore that non-standard workers, especially those in temporary employment and to a lesser degree the solo self-employed, indeed face higher risks of financial hardship compared to standard workers. Although the underlying theoretical mechanisms were not explicitly tested, our findings are in line with expectations based on labor market dualization theories (Emmenegger et al., 2012; Lindbeck and Snower, 1989), reference group theory (Whelan et al., 2001) and arguments related to the disadvantaged objective financial position of non-standard workers (here temporary workers and the solo self-employed), who also have to deal with more insecurity, for instance because their contract will expire and because they do not benefit from the same degree of protection against contract termination (Crettaz, 2013; Halleröd et al., 2015). Owning a business and having personnel is usually also regarded as a form of non-standard work (ILO, 2016), but they are at the same time considered to be labor market insiders who are comparatively successful (Conen and Schippers, 2019b). Furthermore, selection effects are shown to play a role as the likelihood to be in a non-standard work arrangement in part depends on people’s occupation, education and unemployment history. Although we adjusted for relevant confounders to the best of our ability, the fact that the solo self-employed experience less financial hardship than temporary employees could be because solo self-employed people are expected to have more agency in becoming solo self-employed compared to selection into temporary employment.

Our second conclusion is that the country context matters. This study has demonstrated that macroeconomic decline and the level of social security are not only important in explaining cross-country differences in general levels of financial hardship (Nelson, 2012; Visser et al., 2014), but also in determining the extent to which there are differences in financial hardship between non-standard and standard workers, and among non-standard workers. This was the first study to be able to show this for such a large number of countries and long time span, while also including the self-employed and, moreover, distinguishing solo self-employed people and business owners. The results showed that the gap in financial hardship between non-standard and standard workers is larger if a country’s economy is declining, suggesting that non-standard workers are more vulnerable to market forces and get hit the hardest because their employment situation is more uncertain (Kiersztyn, 2018). This applied most strongly to the solo self-employed as they report similar levels of financial hardship to temporary workers in times of economic bust. A somewhat unexpected finding was that solo self-employed people actually experience less financial hardship than workers on a permanent contract at high levels of economic growth. A potential explanation is that especially self-employed people without personnel benefit from periods of economic expansion during which consumers spend more and also find their way to the products and services of solo self-employed persons more often. This could increase their profits considerably while there is relatively little improvement in income for waged workers.

Our exploratory analysis of sex differences revealed that particularly men in temporary employment are vulnerable to macroeconomic adversity. It could be that men consider it traditionally their responsibility to provide for their family, making a secure and decent income more important for them. Macroeconomic decline might then especially be related to financial hardship among men who have a temporary contract and whose employment continuity and breadwinner role are thus uncertain.

Furthermore, the gap between solo self-employed individuals and those who have a permanent contract is not smaller, but larger if governments spend a larger share of GDP on social protection. There were some indications – in particular among men – that this holds true for the contrast between temporary and permanent workers as well. It seems that especially people who have an open-ended contract benefit from social protection, which is in line with labor market dualization theories. At the same time, we saw that temporary employees benefit more from higher levels of social protection in terms of how much financial hardship they experience compared to the solo self-employed, which is not that surprising as own-account workers generally have to take care of their own social insurance and because temporary workers are to some degree covered by social security policies.

Our exploratory analysis of sex differences also points towards the idea of labor market dualization, as in particular male permanent workers, who were historically overrepresented in the labor force and represented by labor unions, seem to benefit from social protection. This creates the paradoxical situation that the ones most in need of social safety nets are least eligible. All in all, our findings add to the growing body of research on the increasing labor market dualization between insiders and outsiders (Biegert, 2019; Emmenegger et al., 2012). Future studies should delve deeper into the precise role that social benefits play in narrowing or widening gaps in financial hardship between non-standard and standard workers, also paying attention to differences between men and women. Although theorizing and testing sex differences was not the core focus of this study, the exploratory results do warrant future research in this direction.

Even though the long time span and multi-country character of this study provided broad and new insights into the antecedents of financial hardship across Europe, some limitations should be kept in mind. First, data on employment histories could provide more insights into changes in work arrangements over time as well as selection into certain work arrangements and how this is related to financial hardship. It would be important to distinguish people with a high initial level of financial hardship selecting into temporary jobs from temporary workers who experience increased financial hardship as a result of their employment arrangement. It would be even more relevant, although challenging, to study whether these dynamics differ between countries and, if so, which country characteristics are able to explain this variation. Second, jobless people were not part of the analytical sample. This seems especially pressing when studying the role of macroeconomic decline, as it might be precisely non-standard workers who are let go and were thus not part of the analysis. Although we could not include the unemployed with the data at hand, the results are likely an underestimation because, relative to standard workers, non-standard workers drop out more in periods of economic recession and they therefore would experience more financial hardship. Third, to measure the work situation of the respondent’s partner, no distinction can be made between a partner being solo self-employed or a business owner as of ESS round 6. However, this likely is a relevant distinction to make for understanding household financial hardship. In designing future studies, it is therefore advised to gather detailed information about the partner’s work arrangement and/or income, preferably including multiple-item measurements of financial hardship and other insecurity measures as well. Finally, solo self-employed persons reported less financial hardship than temporary workers and somewhat more financial hardship than people who have a permanent contract. This hints at the possibility that solo self-employment is not that bad after all and that independent contractors are doing quite well, especially compared to temporary workers. Yet, to draw more valid conclusions, information about the precise nature of solo self-employment is needed in order to disentangle people who pursue their hobby as work and likely experience less financial hardship from, for instance, those who work in the gig economy and likely display higher levels of financial hardship.

The present study has added to the ever-growing body of research that indicates that non-standard workers are vulnerable to experience more income, job and employment insecurity than standard workers (Burgoon and Dekker, 2010; Chung, 2019; Kalleberg and Vallas, 2018; Kiersztyn, 2018; OECD, 2019). Being in a non-standard work arrangement has negative consequences for people’s ability to cope on their income. What is more, periods of economic contraction and high levels of social protection generally aggravate these negative consequences, demonstrating that the divide between non-standard workers and standard workers is larger under these circumstances. This study concludes that non-standard workers are a vulnerable part of the workforce and that the extent to which they are labor market outsiders and therefore vulnerable depends on the country context.

Supplemental Material

sj-pdf-1-eid-10.1177_0143831X241287649 – Supplemental material for Financial hardship while working: A comparison of standard and non-standard workers across Europe

Supplemental material, sj-pdf-1-eid-10.1177_0143831X241287649 for Financial hardship while working: A comparison of standard and non-standard workers across Europe by Mark Visser, Marleen Damman and Gerbert Kraaykamp in Economic and Industrial Democracy

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.