Abstract

There is often a gap between what managers perceive they do in terms of fairness (managers’ justice enactment perceptions) and how fairly employees feel treated by their supervisor (employees’ organizational justice perceptions). This study investigates three managerial actions as potential predictors of congruence in managers’ justice enactment and employees’ justice perceptions. Using individual pay setting as context, the authors hypothesize that goal clarity, continuous feedback, and supervisory credibility predict congruence in justice perceptions (distributive, procedural, interpersonal, and informational justice). Analyses are based on 124 pay-setting managers with their employees from an industrial company in Sweden. Results reveal that goal clarity, continuous feedback, and supervisor credibility reduce the mean-value difference in justice perceptions between managers and employees. This study broadens the organizational justice literature by contributing with a new way of simultaneously studying justice enactment and justice perceptions to further knowledge on how to facilitate and improve fairness in organizations.

Keywords

Most often, leaders believe they are fair, and deem fairness principles as mere common sense . . . Thus, we explain that it is necessary but not sufficient to be fair; in addition, it is necessary for them as leaders to be seen as fair. (Skarlicki and Latham, 2005: 505)

Introduction

Employees’ justice perceptions are positively associated with organizational commitment, organizational citizenship behaviors, and task performance (Colquitt et al., 2013; Rupp et al., 2014). Justice perceptions are subjective evaluations of the fairness of outcome allocations (distributive justice), processes resulting in outcome allocations (procedural justice), the treatment and quality of explanations employees receive from superiors (interpersonal and informational justice) (Colquitt, 2001). Only recently has the literature started to also consider justice enactment, or managers’ adherence to justice rules and principles (Graso et al., 2019; Scott et al., 2014). Rooted in social exchange theory, perceived and enacted justice refer to the same phenomenon, but from different perspectives (Huang et al., 2017). ‘One of the most obvious antecedents of employee justice perceptions [is] . . . a supervisor’s actual adherence to, or violation of, justice rules’ (Zapata et al., 2013: 4). Empirically, the association between managers’ justice enactment and employees’ justice perceptions varies from non-significant to moderately high (e.g., Huang et al., 2017; Koopman et al., 2019; Malmrud et al., 2020).

We believe this is a puzzle essential for the justice literature at large. While some may claim that it is the employees’ justice perceptions that matter, this line of thought would render justice enactment, or what managers think they do in terms of justice, futile. Also, in their review on justice enactment, Graso et al. (2019) argued that ‘workplace injustice shows little sign of abating, despite the fact that the criteria that promote perceptions of fairness at work have been well-established and that both practitioner-oriented and academic literature exhort the importance of fair workplace practices’ (p. 1). Recognizing that both aspects – what employees perceive their manager does and what managers perceive they do – are subjective evaluations, though from different perspectives, may provide insights on how to improve justice and fairness at workplaces. One of these avenues is to focus on which managerial actions, as perceived by employees, can facilitate congruence in justice. Here, we use the term congruence in justice to refer to an agreement in perceptions between managers’ justice enactment and employees’ justice perceptions.

This article attempts to make the following contributions. Based on the perceptional nature of justice perceptions, managers and employees may have different perceptions. Indeed, the motivated cognitions perspective (Barclay et al., 2017) elucidates that both recipient (i.e., employee) and actor (i.e., manager) of justice have different motives and goals, which can lead to differing views. Thus, we contribute to the organizational justice literature by investigating predictors that can facilitate congruence. Using individual pay setting as the context, we hypothesize that employees’ perceptions of goal clarity, continuous feedback, and supervisor credibility relate to congruence in all four justice dimensions. Generally, the different justice dimensions are highly correlated, but conceptually, they symbolize different aspects of, for instance, the pay-setting process. Arguably, distributive justice is a relevant aspect of performance-based pay-setting discussions, but, at least in part, due to budgetary constraints also the justice dimension managers have the most difficulty achieving. As stated by Scott et al. (2009), managers’ scope is limited regarding distributive but also procedural justice but less restricted for interpersonal and informational justice as concerns annual pay increases. But as managers act as organizational representatives, employees are often not aware of the restrictions in latitude that managers face. Thus, we study if the prediction of congruence is similar for different justice dimensions.

Secondly, this article contributes to the compensation literature and specifically merit pay (i.e., annual pay increases based on employee performance), in which issues of justice and fairness are seen as paramount for achieving the goals of performance appraisals and compensation efforts (Fulmer et al., 2023). Previous research has pointed out fairness-related challenges in the pay-setting context (Maaniemi, 2013) and shown that congruence in justice perceptions between managers and employees is associated with more positive work attitudes and behaviors among employees (Malmrud et al., 2020). Despite the relevance of justice for pay setting and performance appraisal, the role of fairness is less often investigated in relation to pay setting; for instance, a recent review of the performance management literature (Pulakos et al., 2019) only mentions fairness and justice in passing. Thus, it is of great practical interest to study what managerial actions can help managers and employees to agree in their justice perceptions.

Lastly, we attempt to contribute to the literature on congruence as an outcome, a topic that is generally scarce in any field of organizational behavior and psychology. One of the reasons for this lack of studies has to do with the methodological difficulties to predict congruence (Bednall and Zhang, 2020). In this article, we use a recently published strategy to analyze predictors of congruence and, through this, add to the limited literature of congruence-as-outcome (Bednall and Zhang, 2020).

Congruence in organizational behavior and psychology research

Congruence is also referred to as ‘self–other agreement’ or ‘agreement’ and is defined as the ‘the fit, match, similarity, or agreement between two constructs’ (Edwards, 2009: 34). Within the organizational behavior literature, studies on congruence are more common among topics of leadership (Markham et al., 2015; Sosik, 2001), leader–member exchange (Sin et al., 2009), and person–organization fit research (Ostroff et al., 2005), but there are studies on social support (Bashshur et al., 2011) and psychological contract (Lambert, 2011; Tekleab and Taylor, 2003). These studies indicate that congruence between managers and employees has positive consequences for various outcomes, like effectiveness, commitment, and performance (Fleenor et al., 2010; Sosik, 2001; Tekleab and Taylor, 2003).

Although many scholars have highlighted the relevance of studying both managers’ and employees’ or teams’ perceptions, the literature on congruence is generally sparse. Moreover, past studies have focused on congruence-as-predictor but almost no studies exist that examine congruence-as-outcome. One of the reasons for this sparsity has to do with the methodological challenges in analyzing congruence per se as well as analyzing congruence-as-outcome. Fleenor et al. (2010) noted that ‘the inconsistent operationalizations of SOA [self–other agreement] constitute a major stumbling block to drawing broad conclusions about the causes and consequences of SOA’ (p. 1006). For congruence-as-predictor, polynomial regression analysis with response surface analysis is a frequent approach (Edwards, 1994).

However, for studying congruence-as-outcome, there is no unified view on the strategy to use: ‘Research examining congruence as a dependent variable has been far less common, which may in part be because of limitations of the current approaches in conceptualizing and operationalizing difference’ (Bednall and Zhang, 2020: 1013). The early approaches of studying congruence were related to varieties of difference scores, which have been widely criticized since Edwards’ (1995) study. Edwards (1995) proposed multivariate regression analyses to study the congruence-as-outcome variable, while Cheung (2007) put forward a different approach, which Edwards (2009), in turn, criticized. A new approach was published recently (Bednall and Zhang, 2020) that supposedly overcomes issues of previous strategies. Thus, in the present study, we follow the approach suggested by Bednall and Zhang (2020).

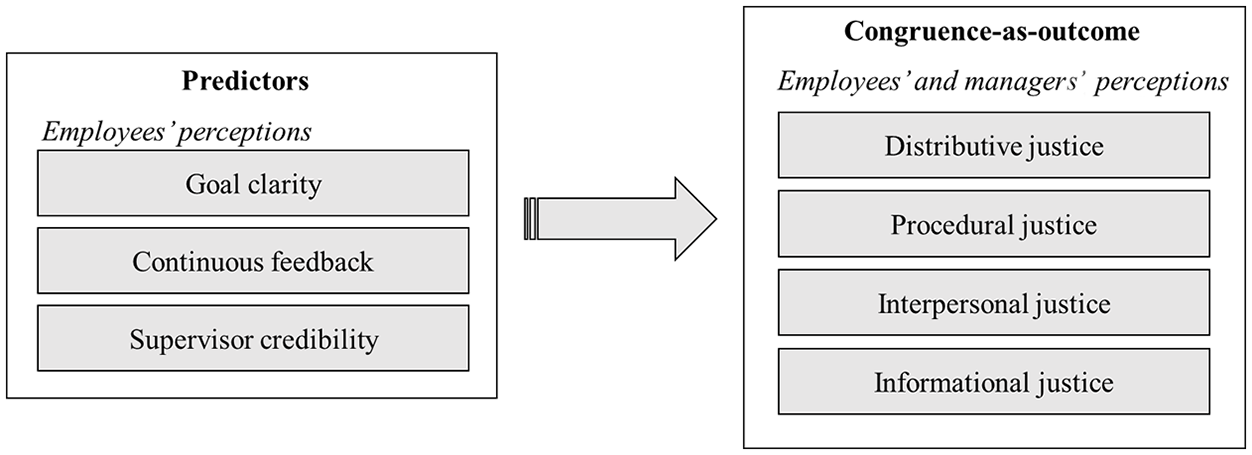

As a consequence of the few available studies on antecedents of congruence per se, specifically concerning organizational justice, as well as the various operationalizations of congruence and different analytical strategies used to predict congruence, it is difficult to generalize from existing studies. Therefore, we derive possible antecedents in light of the context of the study, namely, pay setting. Figure 1 shows the theoretical model.

Theoretical model.

Organizational justice in the pay-setting context

One of the most complex HR practices managers need to perform is to implement fair performance appraisals and pay-setting discussions with their employees (Maaniemi, 2013). This is particularly true for individualized pay-setting systems where annual pay increases are based on employees’ performance in the preceding year, that is, merit pay (Fulmer et al., 2023). Merit pay focuses on annual pay increases, based on skills, responsibilities, and qualities in job performance, and differs from other types of pay-for-performance models, such as bonuses and the whole salary being based on what has been accomplished (i.e., variable pay) (Gerhart and Fang, 2014). This type of pay-setting model is common in Sweden (Stern, 2023) as well as the Nordic countries (Maaniemi, 2013).

The assumption is that fair pay setting results in decisions that are accepted by employees and, in turn, lead to higher work motivation and productivity. Indeed, it has been found that congruence between managers and employees in regard to higher levels of pay justice is associated with more positive work-related attitudes and behaviors among employees (Malmrud et al., 2020). Fairness in pay setting involves that managers judge performance adequately, allocate salary increases or bonuses consistently, and explain decisions and procedures in a respectful way (Andersson-Stråberg et al., 2007). It is not uncommon to see differing views between manager and employee when it comes to pay setting. Managers are considered as ‘givers’ of information whereas employees are ‘receivers’. While managers are more focused on fulfilling the requirements of the pay-setting system, employees focus more on the quality of the decision and process (Fulmer et al., 2023; Maaniemi, 2013). Thus, it seems beneficial to look at both sides of justice (enactment and perceptions) within the pay-setting context.

Based on interviews with both managers and employees within the Finnish pay-setting context (which has large similarities to the system in Sweden, which is the context of the study), several challenges have been identified that hinder justice perceptions (Maaniemi, 2013). The first set of challenges lies within the realm of the content and context of pay setting. Employees and managers both complained that they lacked understanding of the scale to judge performance, criticizing that performance was difficult to assess objectively. Moreover, employees problematized that managers lacked the ability to correctly evaluate their performance because they did not have the time, experience, knowledge, or opportunity to do so. Managers also perceived a lack of time to monitor their employees’ performance, a lack of expertise and ability to judge performance as well as a high number of employees as hindering factors. Both employees and managers also criticized that budgetary constraints and the small amount of money to be distributed among subordinates resulted in no substantial monetary consequences of good performance. Several of these challenges generalize to other pay-setting contexts and countries as well. In a recent review, Fulmer et al. (2023) problematized several practical issues that are very related: that current compensation strategies cannot differentiate well for high performers, that budget limitations hinder fair rewards or meaningful income change as well as information asymmetry between actors and receivers.

Derivation of hypotheses

Pay setting, or salary revision work, is a continuous process with several phases that generally takes place throughout the whole year (Pulakos et al., 2019). This yearly process typically starts with a so-called developmental discussion where the goals for the coming year are set, usually at the individual level. Then the idea is that the pay-setting manager should provide continuous feedback on the employee’s behavior and job performance in relation to the set goals throughout the whole period. At the end of the process, the pay-setting manager assesses employees’ job performance taking into consideration the goals that were set. After this evaluation of performance in relation to the goals, the pay-setting discussion takes place and finally the size of the salary increase for each employee is determined (Pulakos et al., 2019). Thus, managers need to clearly communicate what goals an employee has for the upcoming year (goal clarity), provide continuous feedback to let the employee know whether they meet the expectations (continuous feedback), and to be credible in assessing the employee’s performance (supervisor credibility).

Goal clarity

Goals guide individuals’ attention and effort and serve as a type of self-management mechanism to monitor, evaluate, and adjust one’s own behavior (Locke and Latham, 2006). Goal clarity reflects an employee’s perception of ‘the extent to which the individual’s work goals and responsibilities are clearly communicated’ (Sawyer, 1992: 130). If employees perceive the goals set for their next year as clear, then they know what is expected of them and also better understand on which grounds their performance is assessed at the end of that year. In the justice literature, Folger et al. (1992) suggested that it would be unfair to blame or punish employees for not meeting performance standards if those standards were not clearly communicated and understood. In line with that, past research has found that goal clarity is associated with pay-related justice perceptions (Andersson-Stråberg et al., 2007) and pay satisfaction (Williams et al., 2006).

One of the managers’ tasks during pay setting is to set goals for the next year (Latham and Ernst, 2006; Maaniemi, 2013), usually together with the employee. If the manager is clear in communicating goals and expectations of performance for the next year, it not only provides clarity for employees but also provides clarity of what managers expect from employees. Managers setting goals together with their employees need to have an exchange about what performance can look like, how it can be measured and achieved, and what expectations are reasonable. In other words, goal clarity increases the likelihood that both managers and employees have a similar understanding of what the employee is expected to do in their work.

Hypothesis 1: Goal clarity is positively associated with justice congruence between managers and employees.

Continuous feedback

Several theoretical models suggest that feedback is an important resource for employees because it helps them know the results of their work (Hackman and Oldham, 1976; Locke and Latham, 2006). Continuous feedback should counteract some of the challenges between perceptions of employees and managers mentioned by Maaniemi (2013). Specifically, receiving feedback from the manager on a regular basis should help employees understand the perspective of the manager, getting a better idea of what is expected of them, which is associated with employees’ perceptions of pay equity (Andersson-Stråberg et al., 2005). It has been suggested that employees’ fairness perceptions are affected by how constructive the feedback they get is perceived (Alder and Ambrose, 2005). At the same time, there is a substantial positive association between perceived feedback constructiveness and feedback frequency (Kuvaas et al., 2017). Thus, continuous feedback is likely viewed as more constructive, which, in turn, affects justice perceptions positively.

Furthermore, through continuous feedback employees will gain a better understanding of what they need to do to improve their performance. As a result, employees may be less surprised by the performance evaluation they get during pay setting (Pichler et al., 2020). Such communication about employees’ performance has been associated with higher levels of fairness in relation to pay setting among employees (Scott, 2018) and might tune employees’ and managers’ perceptions and increase congruence in pay-setting justice. At the same time, when managers give feedback continuously (and not just at the annual pay-setting discussion), the likelihood increases that managers have a better sense of what employees do, what challenges they encounter, and how they perform on an average basis. Moreover, managers who give regular feedback and discuss the performance of their employees will likely get a better understanding of the subject field of the employee, and hence gain more knowledge of the work of the employee.

One of the identified challenges in adhering to justice rules for managers is limited information (Ambrose and Schminke, 2009). This may include that managers do not adequately take into consideration the specific needs and competences of employees. For instance, an employee who gets a challenging work task from their manager may view this as proof of their value whereas another may view it as an unfair extra burden (see Sherf et al., 2021). In circumstances like these, continuous feedback from the manager may help, as managers and employees are more likely to communicate on a regular basis, which gives managers a chance to understand employees’ needs and employees a chance to understand the motives behind managerial actions.

Hypothesis 2: Continuous feedback from the manager is positively associated with justice congruence between managers and employees.

Supervisor credibility

In the pay-setting literature, supervisor credibility has also been referred to as supervisors’ knowledge or source expertise and has been suggested to be a key factor for successful pay setting (Kingsley Westerman et al., 2015; Pulakos et al., 2019). In response to one of the challenges in pay setting identified by Maaniemi (2013), we predict that supervisor credibility should help congruence in justice. Employees who believe that their manager has the competence to judge their performance and understand their work and subject matter, are more likely to accept managers’ decisions, and may thus view decisions and interactions as fair. Likewise, when managers experience that their employees believe in their competence, they may also be more confident in their interactions with employees, give employees more room to voice their opinions, and explain their thinking and decision-making to a larger extent. Thus, supervisor credibility is expected to positively influence justice perceptions and justice enactment. Empirically, performance evaluations are considered as fair when supervisors are familiar with the performance of the employee being evaluated (Fulk et al., 1985; Landy et al., 1978). Similarly, feedback reactions are more positive when feedback is provided by credible sources, and by experienced and competent raters (Kingsley Westerman et al., 2015; Kinicki et al., 2004).

In the justice literature, source credibility has also been considered. It has been suggested that the perceived accuracy of feedback positively affects justice perceptions (Alder and Ambrose, 2005). For instance, it has been argued (Folger et al., 1992) that performance appraisals can only be accurate when appraisers have the knowledge and skill to judge performance. Empirically, studies have found that employees have higher justice perceptions when managers base their performance appraisals on accurate evidence (Greenberg, 1987) and when they believe their managers have knowledge of their performance (Stanton, 2000).

Hypothesis 3: Supervisor credibility is positively associated with justice congruence between managers and employees.

Methods

Study context and procedure

This study was conducted in Sweden, a country where individualized pay setting has increased in recent decades (Bender and Elliott, 2018; Stern, 2023). In Sweden, annual pay raises are typically regulated by collective bargaining agreements as negotiated by employer organizations and labor unions, and these agreements set the norm on how much pay can increase every year, which has on average been between 2 and 4% in recent years (Swedish National Mediation Office, 2020, 2023). The pay of around two-thirds of all workers is determined to some extent by individualized pay setting (Swedish National Mediation Office, 2023). Some collective agreements involve a standard pay increase (in percentage or an actual amount) whereas other agreements are numberless and leave it to the employer/manager to determine any potential increases (pay decreases are not allowed). In most of the collective agreements, such pay agreements stipulate that the annual pay increase should be based upon responsibilities and qualities of work performance based on specific pay-setting criteria (Ulfsdotter Eriksson et al., 2021). The individual pay-setting manager has the authority and mandate to distribute pay among their subordinates, and these decisions are based on performance. Typically, therefore, individual managers need to make decisions regarding annual pay increases based on specific pay criteria and performance assessments based on stipulations in the collective agreements and the organization’s specific pay processes (Malmrud et al., 2023).

The data for the present study stem from an industrial company with mainly high-skilled jobs operating in several geographical areas in Sweden with a numberless collective agreement, which means that there were no guaranteed pay increases or no pre-determined ‘pot’ (i.e., percentage of money to be distributed among the employees). Pay-setting managers were responsible for deciding on the amount of pay raise for each of their subordinates based on market salaries, competence, performance, and responsibilities. Employees had the option to appeal against decisions by the pay-setting manager, in which case human resources and the local unions take over negotiations.

Data collection was conducted in 2016, right after the annual pay raises had been established that year. The company informed staff about the data collection through the intranet. Managers and employees received an invitation email from the research team, clarifying the purpose of the project, data treatment, that participation was fully voluntary, and including a personalized link to a web survey. Up to four reminders were sent. The project has been approved by the Regional Ethics Committee in Stockholm (Ref. No. 2015/1733-31/5).

Participants

Out of the company’s 348 pay-setting managers, 213 participated in the study (61% response rate). A non-response analysis based on company records revealed that there was no difference between the managers who replied to the survey and those that did not reply regarding age (t[df=346]=1.25, p=.212), tenure (t[df=604]=0.60, p=.546), or gender (χ2[df=1]=0.03, p=.861). Out of the 2,793 non-managerial, white-collar employees, 1,191 participated in the study (43% response rate). A non-response analysis based on company records revealed that there was no difference between employees who replied to the survey and those that did not reply regarding age (t[df=2614]=1.74, p=.081), tenure (t[df=2791]=−0.76, p=.449), or gender (χ2[df=1]=0.41, p=.521).

Using company records, managers and employees were matched. In total, 566 employees, who replied to the survey and were not classified as multivariate outliers, could be matched with their manager, who also replied to the survey and were not classified as multivariate outliers. A group comparison between those employees that could be matched and those that could not be matched with a manager revealed that employees who could be matched had longer tenure (t[df=1188]=2.42, p=.016) and had supervisors who rated themselves higher on justice enactment (t[df=161]=2.23, p=.027, M=4.10 vs. M=3.97). There were no significant differences regarding age, gender, or justice perceptions.

For the 566 employees, 34% were women and 66% were men, with an average age of 45 years (SD=11), and the average tenure was 10 years (SD=9). For the 155 pay-setting managers, the mean age was 48 years (SD=9), 27% were women and 73% men, they had worked as manager at the company for an average of 5 years (SD=5), and had an average of 9 subordinates (range 1–24, SD=5). Each of the 155 managers had at least one subordinate who responded to the survey, n=124 had at least two subordinates who provided data, n=99 had three subordinates, n=70 had four subordinates, and n=1 manager had 12 subordinates providing data.

Aggregation analysis

The present study’s data contained 155 managers and 566 employees. Managers filled out the questions about justice enactment towards their employees in general, and not to specific employees. Therefore, we decided to aggregate employees’ data per manager. Previous studies have used multilevel studies to accommodate the nested data (Kopperud et al., 2014). Analytical techniques for congruence-as-outcome using multilevel analyses have however not been developed to the best of our knowledge. Other studies with a similar data structure have aggregated subordinates’ data (Mosson et al., 2018; Nielsen et al., 2022; Sosik, 2001).

In order to justify aggregation of employees’ data per manager, agreement and reliability in the ratings of employees from the same manager were assessed (Bliese, 2000). The rwg(J)uniform index assesses within-group agreement of whether employees provide similar values, with values above .71 indicating strong agreement between raters (here: employees of a specific manager) (LeBreton and Senter, 2007). The intra-class coefficient ICC(1) provides an estimate of the extent to which employees’ ratings can be attributed to group membership (of having the same manager). The ICC(1,k) gives an indication on how reliably the mean ratings (across employees) distinguish between different managers. The suggested cutoff values for ICC(1) are above .05 and for ICC(1,k) values above .70 (Bliese, 2000; LeBreton and Senter, 2007). Due to the large differences in the number of employees that provided data per manager (ranging from 1 to 12), we only selected the n=124 managers with at least two employees providing data. Further, we estimated the ICC(1) and the ICC(1,k) for five employees per manager (for a similar procedure, see Mosson et al., 2018). We calculated the different indices for the four justice dimensions (see Table in the Supplemental Materials). All values were above the traditionally recommended cutoff values, suggesting that aggregation could be justified. We also tested agreement and reliability across employees for the predictors, and also these results suggested that the predictors could be aggregated across employees. Thus, for further analyses, data based on n=124 managers and aggregated scores for subordinates per manager were used.

Measures

Justice perceptions

Employees’ justice perceptions were measured with the scale by Colquitt (2001), translated into Swedish and adapted to match the context of pay (Andersson-Stråberg et al., 2007). The response scale ranged from 1 (to a very small extent) to 5 (to a very large extent). Distributive justice was measured with four items, an example item being: ‘To what extent does your pay reflect the effort and dedication you have put into your work?’ Internal consistency (Cronbach’s alpha) was .93. Procedural justice was measured with six items (e.g., ‘To what extent have you been able to express your views and feelings on pay-setting issues?’), with α=.86. Interpersonal justice was measured with four items, an example item being: ‘To what extent has your boss treated you with respect in relation to pay setting?’ (α=.86). Informational justice was measured with five items (e.g., ‘To what extent has your boss explained the pay-setting process clearly and thoroughly?’), with α=.88.

Justice enactment

Managers’ perceptions of justice enactment were assessed with the same scale (and response format) as for justice perceptions, but adapted to mimic the actor perspective. All items started with ‘As supervisor, to what extent do you think that . . .’. An example item for distributive justice enactment was ‘. . . your employees’ pay reflects the effort and dedication they have put into their work?’ (α=.80). An example item for procedural justice enactment was ‘. . . your employees have been able to express their views and feelings on pay-setting issues?’ (α=.77). Interpersonal justice enactment was composed of four items, which resulted in α=.65, with an example item being: ‘. . . you have treated your employees in a polite manner in relation to pay-setting?’ Informational justice enactment was measured with five items (α=.81), with an example item: ‘. . . you have clearly and thoroughly explained the pay-setting process?’

Goal clarity

Goal clarity was assessed with three items based on Rizzo et al. (1970) and Caplan (1972). The three items were: ‘It is clear what is expected of me on my job’, ‘The goals and objectives of my work are clearly expressed’, and ‘I find my work objectives to be vague and unclear (reversed)’. The response scale went from 1 (strongly disagree) to 5 (strongly agree), with α=.78.

Continuous feedback

Feedback was assessed with four items based on Hackman and Oldham (1975). The response scale went from 1 (strongly disagree) to 5 (strongly agree). The items were: ‘My manager generally lets me know how satisfied he/she is with my work effort’, ‘My manager generally lets me know if I am carrying out my work satisfactorily or not’, ‘I receive continual feedback on my work performance from my supervisor’, and ‘Performance feedback from my supervisor is usually received in direct connection with carrying out the work’. Cronbach’s alpha was .91.

Supervisor credibility

Two items were used to measure supervisor credibility, based on the one-item measure by Landy et al. (1978). The two items were: ‘Do you think your pay-setting supervisor is knowledgeable about your work performance?’ with a response scale ranging from 1 (to a very small extent) and 5 (to a very large extent) and ‘Do you have confidence in your supervisor’s ability to judge your work performance?’ with an answer scale ranging from 1 (a very large degree of confidence) to 5 (a very small degree of confidence). The latter item was recoded, such that higher values indicate higher credibility. The correlation between the two items was .73 (p<.001), α=.84.

Analysis

We followed the directional and nondirectional difference (DNDD) approach as suggested by Bednall and Zhang (2020). Congruence is conceptualized as two orthogonal components, Y1 (managers’ justice enactment) and Y2 (employees’ justice perceptions), that can be described by directional and nondirectional differences between them. Directional difference is ‘a systematic positive or negative difference in the levels of two sets of matched observations’ where this difference is operationalized as ‘the arithmetic difference between the conditional expected (predicted) values of Y1 and Y2’ (p. 1016). Nondirectional difference is the remaining inequality between Y1 and Y2 after the directional difference has been taken into consideration. Bednall and Zhang (2020) split the nondirectional difference into two sources of variability. Shared variability ‘refers to fluctuations occurring in both Y1 and Y2, meaning that they follow a similar pattern. For example, if the two raters discuss their scores, their ratings may show a similar (positive) pattern even if one person provides systematically higher ratings than the other. Alternatively, if the first rater intends to oppose the other rater’s judgments, their ratings may show a mirror opposite pattern’ (p. 1017). Unique variability refers to variability that only exists either in Y1 or Y2.

Bednall and Zhang (2020) propose that differences can be predicted from antecedents. For instance, when the directional difference is negatively influenced by a predictor X, this means that the mean-level difference between managers’ justice enactment and employees’ justice perceptions is reduced when levels of predictor X are higher. That is, a negative directional difference indicates the predictor X reduces incongruence, and instead, facilitates congruence. Specifically, managers’ justice enactment and employees’ justice perceptions were regressed onto each predictor separately (i.e., goal clarity, continuous feedback, supervisor credibility). The significance of the directional difference was assessed by computing the coefficient for the effect of predictor X on Y1 (justice enactment) minus the coefficient for the effect of predictor X on Y2 (justice perceptions). In the case of significant directional difference, a graphic illustration was used to help interpretation. This is called Step 1. While the DNDD approach also allows to test whether shared variability (Step 2) and unique variability (Step 3) can be affected by antecedents, for hypothesis testing, we examined the significance of the directional differences in Step 1 as we were interested in whether the predictors affect the directional difference between managers’ justice enactment and employees’ justice perceptions. For the sake of completeness, we show the results of Step 2 and Step 3. Given the high correlations between study variables, the analyses follow three separate steps, that were all conducted for the predictors and the justice dimensions separately. Analysis was performed in Mplus (Muthén and Muthén, 1998–2017).

Results

Descriptive statistics

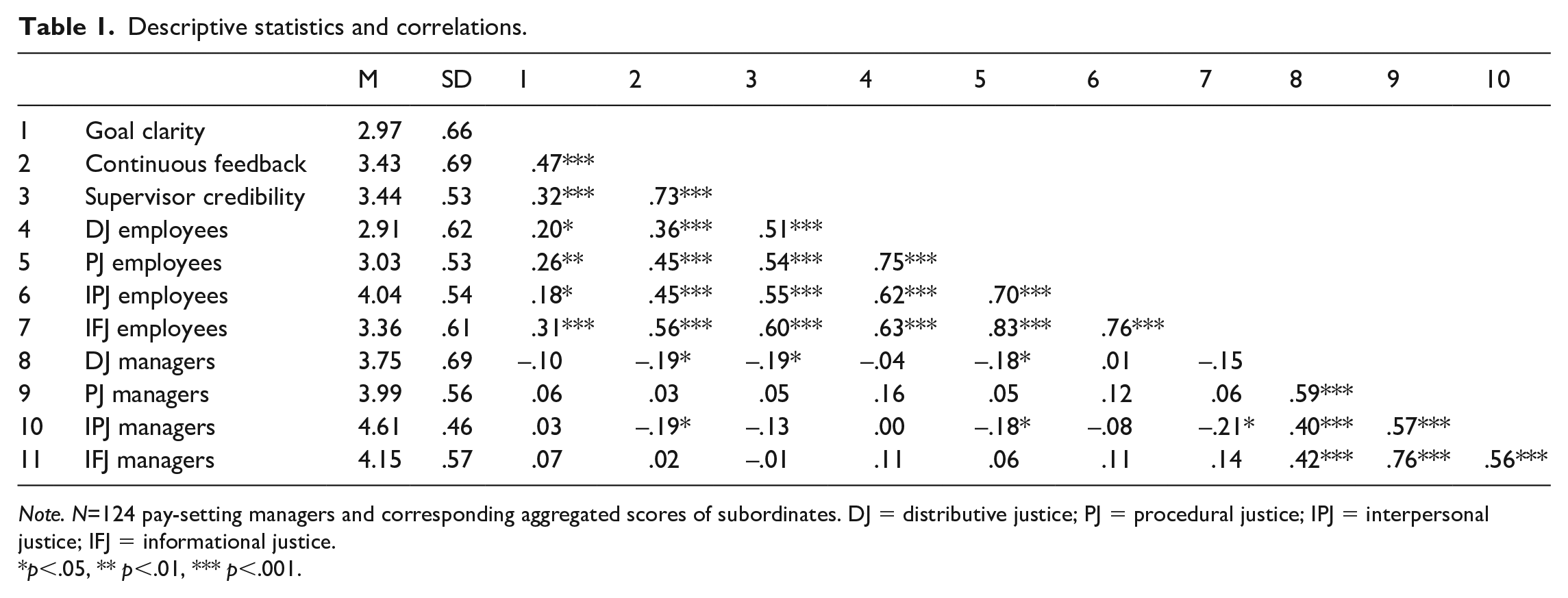

Table 1 shows the descriptive statistics and correlations of the study variables. The three predictors correlated substantially with one another, with the lowest correlation (r=.32, p<.001) between goal clarity and supervisor credibility and the highest correlation (r=.73, p<.001) between continuous feedback and supervisor credibility. Given these intercorrelations between predictors, we view that our strategy to test each predictor separately is justified. Similarly, employees’ justice perceptions were also highly correlated with one another, with correlations ranging between r=.62 and r=.83 (p<.001). Interestingly, the correlations between justice enactment dimensions were lower, ranging from r=.40 to r=.76 (p<.001). Surprisingly, correlations between employees’ (aggregated) justice perceptions and managers’ justice enactment ranged between negative and zero. Distributive and interpersonal justice perceptions were not significantly correlated with any justice enactment dimension. Lastly, continuous feedback was negatively associated with distributive and interpersonal justice enactment as was supervisor credibility with distributive justice enactment (all: r=–.19, p<.05). Although not as expected, we do not regard these correlations as an artifact. Subsequent congruence analysis will elucidate these relationships.

Descriptive statistics and correlations.

Note. N=124 pay-setting managers and corresponding aggregated scores of subordinates. DJ = distributive justice; PJ = procedural justice; IPJ = interpersonal justice; IFJ = informational justice.

p<.05, ** p<.01, *** p<.001.

Apart from the correlations, the table also shows that managers and employees had differences in their mean values, with managers having, on average, higher mean values in justice enactment than employees had in their justice perceptions. All differences were significant (p<.001), with the biggest mean-level difference in procedural justice and the lowest mean-level difference in interpersonal justice.

Hypothesis testing

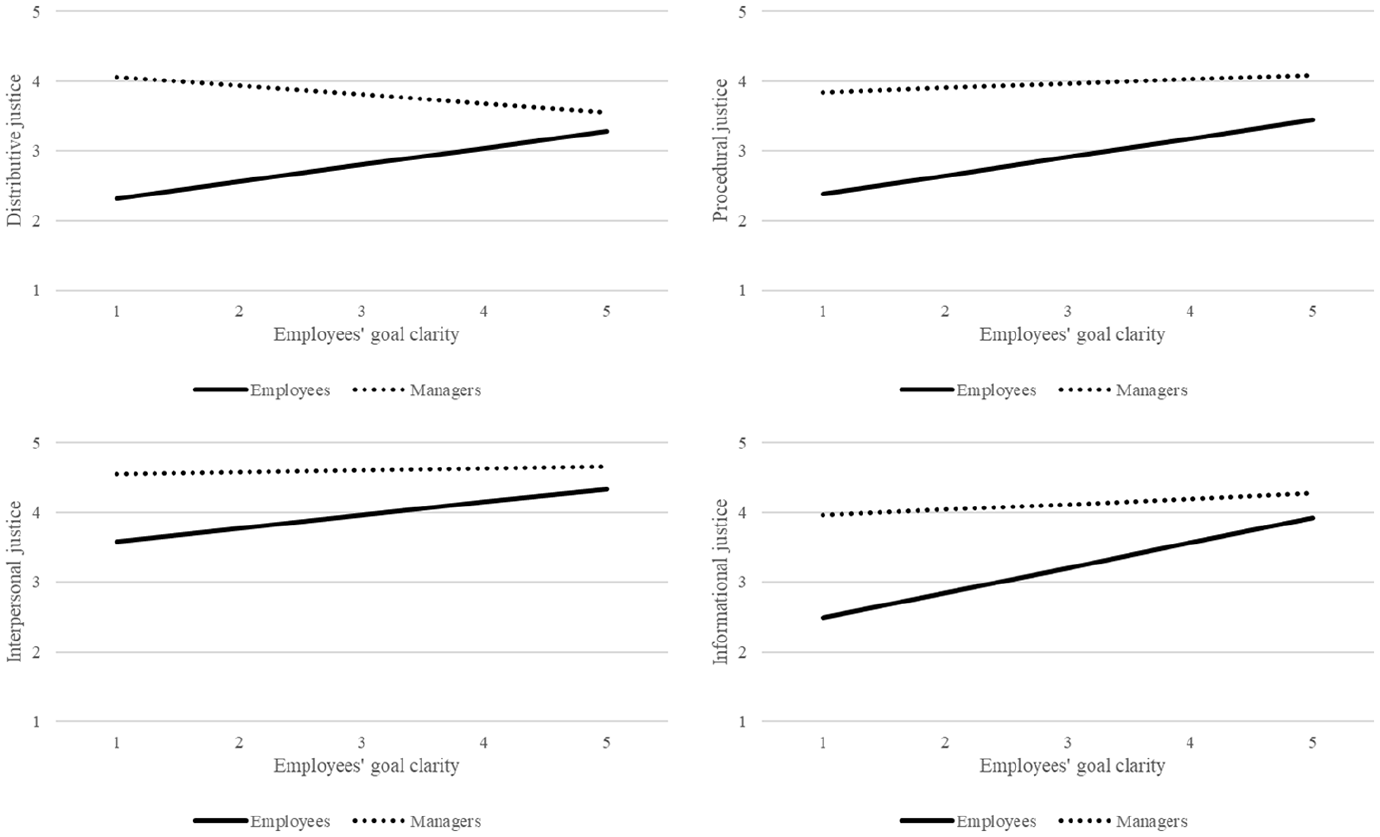

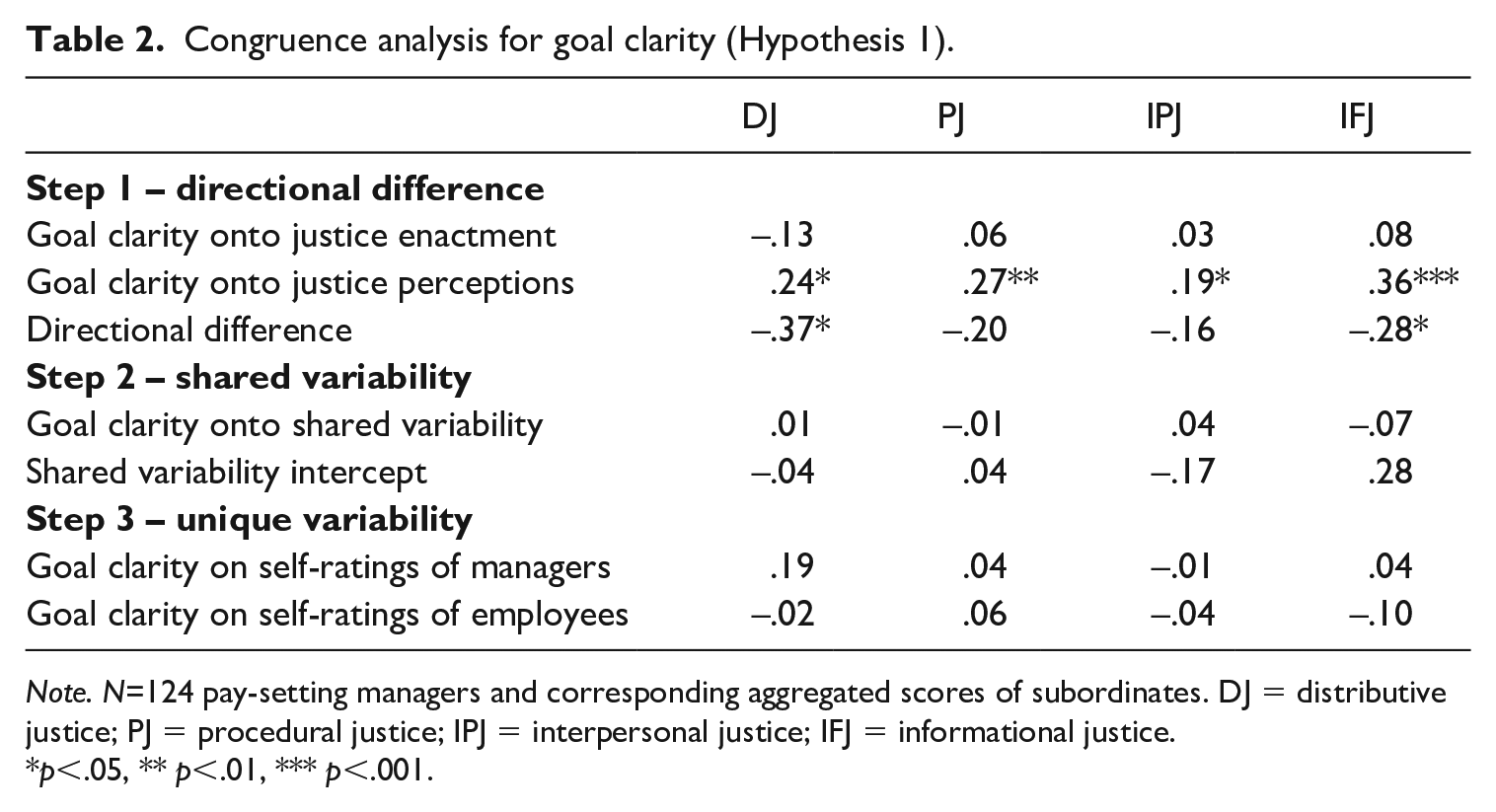

Hypothesis 1 stated that goal clarity is positively associated with congruence in managers’ and employees’ justice perceptions. Table 2 provides the coefficients from the congruence analysis for goal clarity. Employees’ perceived goal clarity was positively associated with all four dimensions of employee justice perceptions, but not significantly associated with any of the justice enactment dimensions. The directional difference (Step 1), reflecting the effect of goal clarity on the mean-level difference between managers’ justice enactment and employees’ justice perceptions, was significant for distributive and informational justice but not for procedural and interpersonal justice. Importantly, the directional differences were negative, indicating that with higher goal clarity, the directional differences reduced, thus positively associating with congruence between managers and employees. Figure 2 visualizes these results graphically. It can be seen that with increasing levels of goal clarity, the mean-level difference in distributive and informational justice between managers and employees was smaller. Thus, Hypothesis 1 was supported for distributive and informational justice but not supported for procedural and interpersonal justice.

Figures detailing results for Step 1 for goal clarity on justice congruence.

Congruence analysis for goal clarity (Hypothesis 1).

Note. N=124 pay-setting managers and corresponding aggregated scores of subordinates. DJ = distributive justice; PJ = procedural justice; IPJ = interpersonal justice; IFJ = informational justice.

p<.05, ** p<.01, *** p<.001.

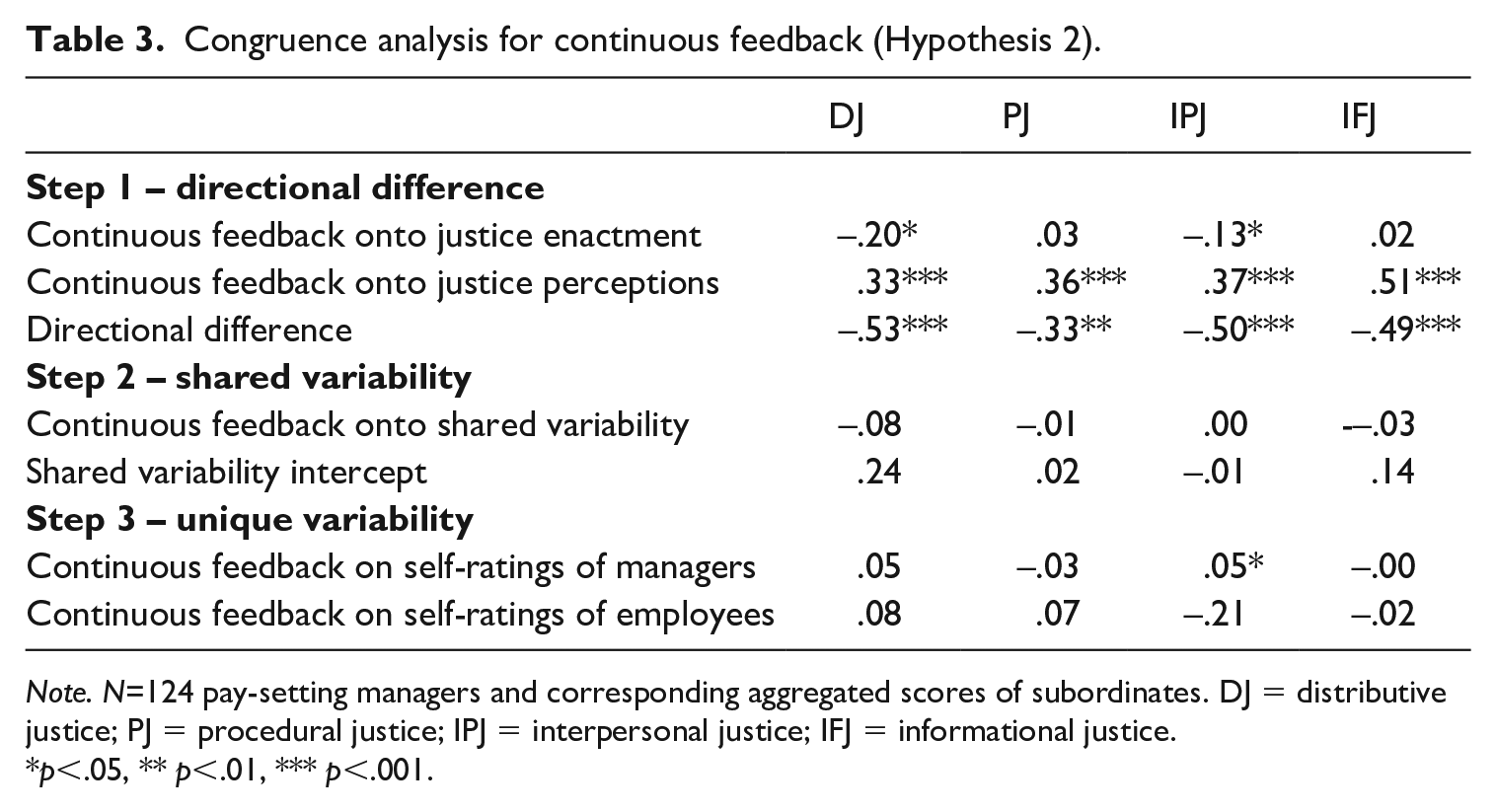

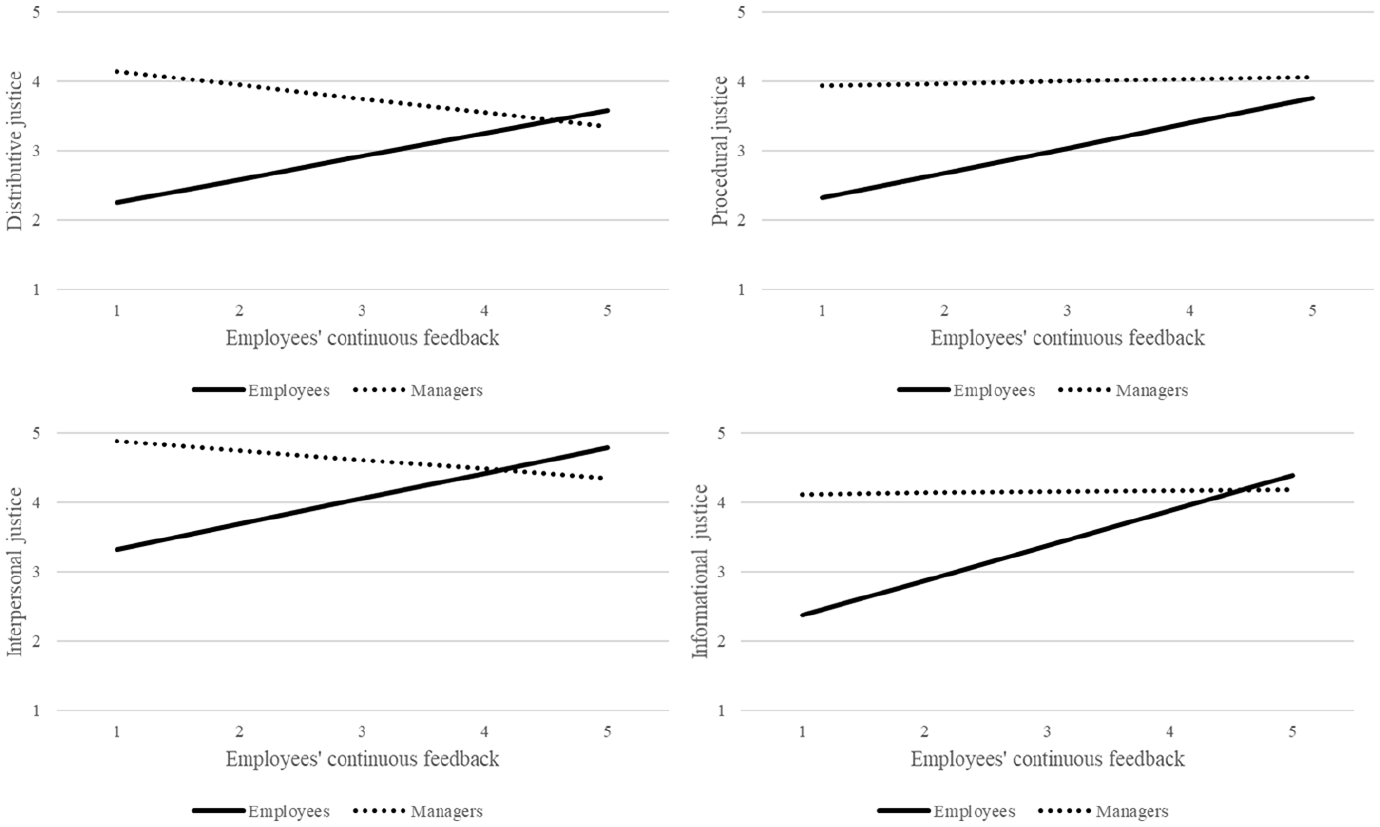

Hypothesis 2 stated that continuous feedback has a positive association with congruence between managers’ and employees’ justice perceptions. Table 3 provides the coefficients from the congruence analysis for continuous feedback. Continuous feedback was positively associated with all four dimensions of employees’ justice perceptions, but negatively associated with distributive and interpersonal justice enactment, and unrelated to procedural and informational justice enactment. The directional difference (Step 1) was significant for all four justice dimensions. Again, the directional differences were negative, indicating that with higher continuous feedback, the mean-level differences between managers and employees were reduced, positively associating with congruence between managers and employees. Figure 3 displays these results graphically. Thus, Hypothesis 2 was supported.

Congruence analysis for continuous feedback (Hypothesis 2).

Note. N=124 pay-setting managers and corresponding aggregated scores of subordinates. DJ = distributive justice; PJ = procedural justice; IPJ = interpersonal justice; IFJ = informational justice.

p<.05, ** p<.01, *** p<.001.

Figures detailing results for Step 1 for continuous feedback on justice congruence.

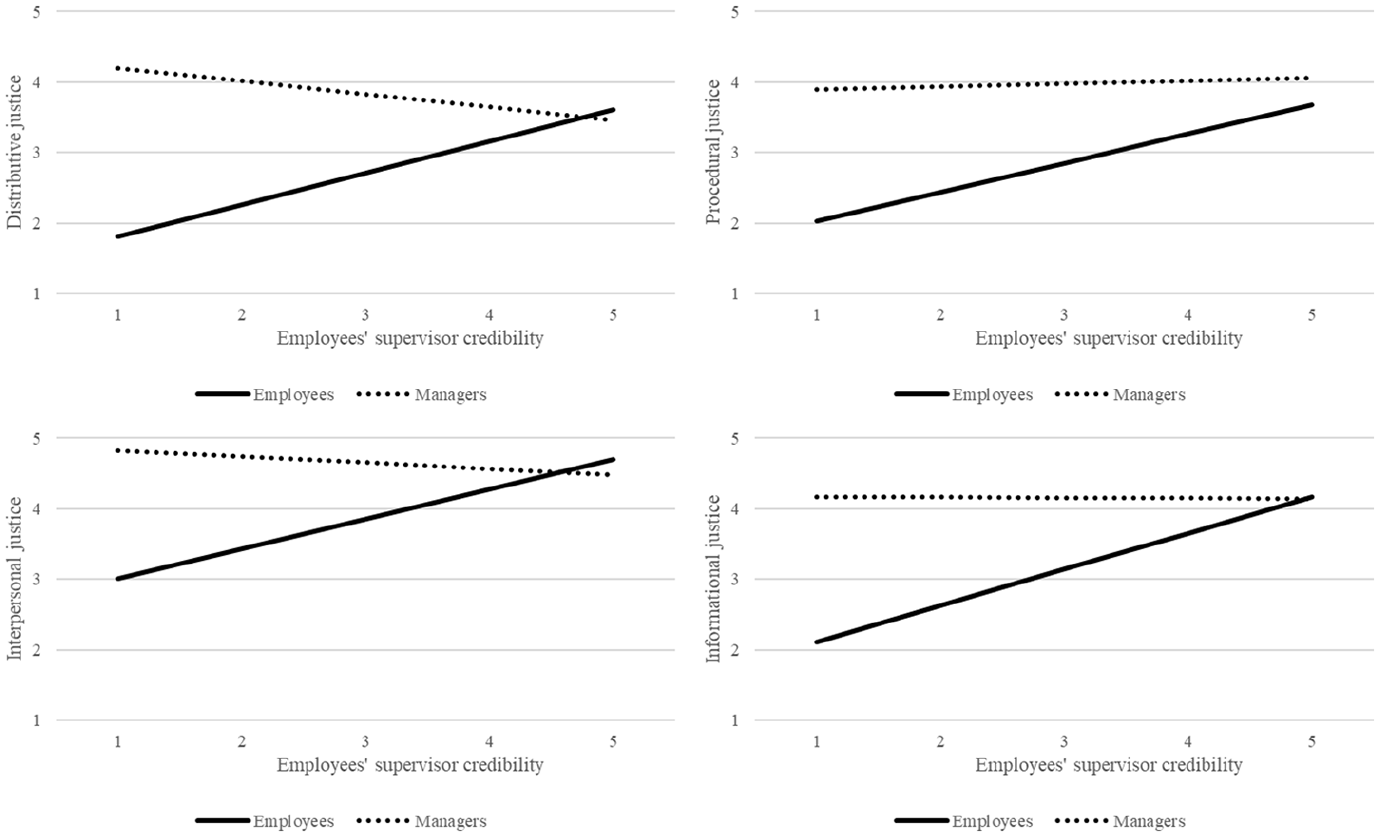

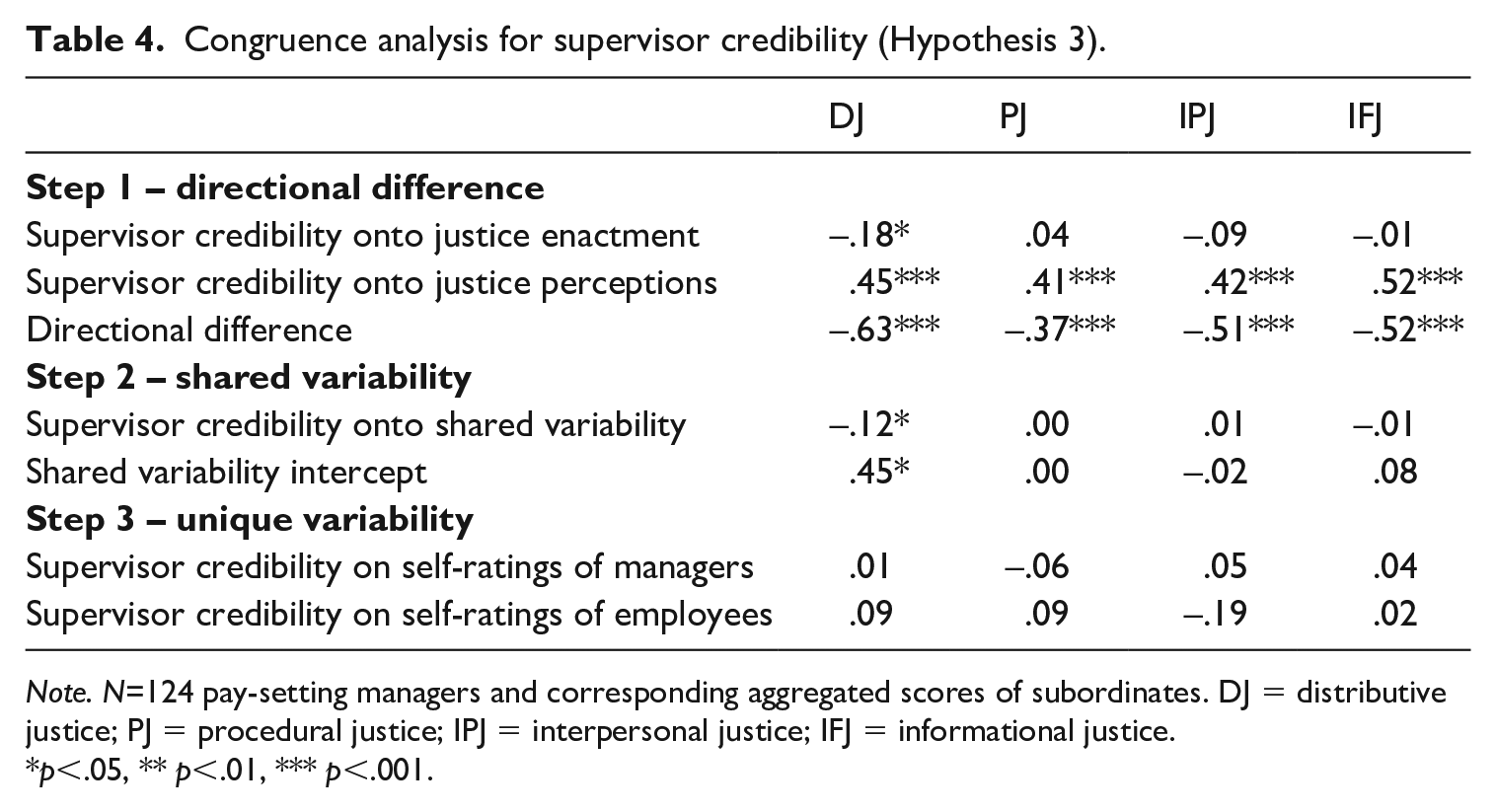

Hypothesis 3 stated that supervisor credibility associates positively with congruence in managers’ and employees’ justice perceptions. Table 4 provides the coefficients from the congruence analysis for supervisor credibility and Figure 4 displays these results graphically. Supervisor credibility was positively related to all four dimensions of justice perceptions. Supervisor credibility was negatively associated with distributive justice enactment, but not with the other dimensions of justice enactment. The directional difference (Step 1) was significantly negative for all four justice dimensions, indicating that the mean-level difference between managers’ justice enactment and employees’ justice perceptions was smaller with higher levels of supervisor credibility. Thus, Hypothesis 3 was supported in that higher supervisor credibility associates positively with congruence.

Figures detailing results for Step 1 for supervisor credibility on justice congruence.

Congruence analysis for supervisor credibility (Hypothesis 3).

Note. N=124 pay-setting managers and corresponding aggregated scores of subordinates. DJ = distributive justice; PJ = procedural justice; IPJ = interpersonal justice; IFJ = informational justice.

p<.05, ** p<.01, *** p<.001.

Discussion

This aim of the study was to predict congruence between managers’ justice enactment and employees’ justice perceptions. The pay-setting context was deemed useful for understanding how employees and managers may create agreement in justice perceptions. Drawing upon the pay-setting literature, three predictors of justice congruence were derived: goal clarity, continuous feedback, and supervisor credibility. We followed a recently published method, the DNDD approach by Bednall and Zhang (2020), to predict congruence in justice. In the following, we discuss the results, highlight implications, methodological consideration as well as future research potentials.

Theoretical discussion

Decades of research on organizational justice have shown that employees’ justice perceptions are important for a variety of outcomes (Colquitt et al., 2013; Rupp et al., 2014). The relatively recent research focus into how managers view their justice actions has added to the complexity of the subjective nature of organizational justice (Graso et al., 2019; Scott et al., 2009). However, regarding the joint consideration of both managers’ justice enactment and employees’ justice perceptions much is to be learnt (Huang et al., 2017; Koopman et al., 2019). The empirical gap between what managers think they do and what employees perceive their manager does is both theoretically interesting and practically relevant, especially when it comes to how congruence may be predicted.

Relying on the pay-setting literature, we developed arguments that having clear goals, getting continuous feedback, and dealing with a credible supervisor, as perceived by employees, would increase the likelihood that managers and employees see eye to eye when it comes to assessing justice dimensions. The results indeed showed that these three managerial actions were consistently negatively associated with the mean-level difference between managers’ justice enactment and employees’ justice perceptions (with two exceptions for goal clarity: procedural and interpersonal justice). This indicates that the predictors were positively associated with congruence between employees and managers. As far as mean-level differences in justice perceptions are concerned, goal clarity, continuous feedback, and supervisor credibility seem to help gain congruence in justice perceptions.

Another aim of the study was to explore whether results would be similar for different justice dimensions. The findings suggest that there are differences between justice perceptions. Although the figures for the mean-level differences looked relatively similar, the size of the directional effects indicate the tendency of stronger effects for distributive justice. This result may be explained by the fact that distributive justice is particularly relevant during pay-setting procedures. Another explanation may be related to managers’ latitude. It has been suggested that managers have less discretion over distributive justice aspects relative to other justice dimensions (Scott et al., 2009). That is, it may be that managers allow themselves to more self-critical when it comes to distributive justice than with the other justice dimensions. The motivated cognitions perspective of justice (Barclay et al., 2017) suggests that managers want to view themselves as fair and justify their actions to themselves in order to keep positive self-esteem about themselves. The pay-setting context is limiting to managers as has been noted by others. Maaniemi (2013) described in her interview study that managers find that the difference in pay increases that is possible to distribute to employees does not equate well to the efforts and performance differences between employees. Similarly, Fulmer et al. (2023) noted that a common problem with merit pay is a constrained amount of salary increase available to distribute by managers, such that maximum payments limit managers to compensate high-performing employees adequately. It could be that managers are more self-critical when it comes to distributive justice, also because they can partly attribute their actions to the context of pay setting.

There were several unexpected findings as well. The three studied predictors had either no relationship or a negative relationship with managers’ justice enactment. Continuous feedback and supervisor credibility were negatively associated with distributive justice enactment, and continuous feedback had a negative association with interpersonal justice enactment. Recommendations given to managers for pay setting and performance management include setting clear goals and expectations, providing regular feedback as well as coaching, helping and course-correcting employee performance (Pulakos et al., 2019). We expected that managers who adhere to these recommendations would perceive themselves as more fair and not less. There can be several explanations for these surprising findings. One is that we asked employees about managerial actions and not managers. It may be that employees perceived they received continuous feedback whereas managers did not think they provided it. Another explanation may be that because of regular and continuous feedback, managers are unhappy with what they can offer to their employees in terms of pay raises. Managers who engage in regular feedback and can judge their employees’ performance well may feel limited by the context of how large a pay increase they can give to employees. They may also understand that employees expect a great deal from pay-setting discussions, and thus may feel uncomfortable in their role as superior distributing pay and making performance appraisals.

Methodological considerations

There are several strengths and limitations of the study we want to comment on. One strength of this paper is that it contributes to the limited literature on congruence-as-outcome. Here, we followed a new methodological approach and applied it to congruence in justice during pay setting. While polynomial regression with surface response analysis (Edwards, 1994) has developed to be the most common method to study the consequences of congruence, there is no unified view on which method is best to use for predicting congruence. At least three methods have been proposed (Bednall and Zhang, 2020; Cheung, 2007; Edwards, 1995) and only a few studies have been published on predicting congruence. This uncertainty of which method is best to use in congruence research limits scholars in answering research questions about not only whether congruence has positive or negative effects, but also in understanding how perceptual gaps can be reduced. While we followed the procedure by Bednall and Zhang (2020), the use of a new method is thus also a limitation of this study.

Another strength of the present paper is that two sources of data were used: managers’ justice enactment and employees’ justice perceptions. Managers were asked to rate their justice enactment in relation to all of the performed pay setting with their subordinates. That is, managers were asked to make a joint assessment of their justice enactment despite potential differences towards different subordinates. We decided on this approach for two reasons. One reason was that we expected managers to merge their perceptions about their behavior towards different employees into one assessment. Secondly, the company we worked with for the data collection could not guarantee that managers would fill out a survey about justice enactment after every pay-setting discussion with each employee. Thus, likely, managers would have filled out all surveys after all of the pay-setting discussions were completed and thus may have merged their perceptions across employees anyhow. The company was weary about overburdening their managers, as some managers had many subordinates and as the phase of the pay-setting discussions is a very busy time for pay-setting managers. We could have also selected only one employee per manager, after the data collection was completed, but we decided against this because managers did fill out the questionnaire about justice enactment in relation to all of their employees. Another limitation is that data were cross-sectional. It would have been ideal to be able to ask employees about goal clarity, continuous feedback, and supervisor credibility before their pay-setting discussion. We may instead assume that the pay-setting process and outcome affected their survey responses regarding managerial actions.

Moreover, generalizability is limited as the study was conducted in one organization and in one country with a particular pay-setting system. However, the organization where data were collected worked hard with their pay-setting system and procedures and trained all supervisors in the pay-setting system. While this particular study concerned one specific organization focusing on a particular type of pay-for-performance (i.e., merit pay) in a country where merit pay is common (Ulfsdotter Eriksson et al., 2021), an open question is whether cultural aspects also impact on the extent to which specific predictors relate to congruence. It may be that managers in low power-distance cultures like Sweden have to exert more effort to justify decisions for employees and involve them in their decision-making process (cf. Shao et al., 2013). This dynamic may also affect which predictors are relevant to investigate for justice congruence. Although we studied three relevant managerial actions anchored in the pay-setting literature, it would be interesting to consider these even in more detail. For instance, one could study goal difficulty as well as the type and frequency of feedback. Furthermore, it may also be relevant to investigate managers’ and employees’ attitudes towards the pay-setting system and performance appraisal process. For justice congruence in other contexts, other predictors should be explored as well. The search for aspects that close the perceptual gap between what managers think they do and what employees perceive their managers to do seems indeed paramount. Despite these outlined limitations, as the first paper on predicting congruence in organizational justice, we thus believe our study makes strong contributions to theory and practice.

Practical implications

Perceptions of fairness and justice in pay setting are central in order to attain future performance, commitment, and motivation (Fulmer et al., 2023). Here, it is not enough that employees themselves perceive the pay setting as fair – instead with this study, we add to the notion that managers’ perceptions of their own actions also matter. Indeed, a prior study has shown that congruence between employees and managers can lead to even better work consequences of employees than when just considering employees’ perceptions (Malmrud et al., 2020). Based on this, the present study is a first step to understanding how such congruence in justice perceptions between managers and employees can be achieved in the pay-setting context, where fairness is particularly impactful. One important implication relates to the striking mean-level differences between managers’ justice enactment and employees’ justice perceptions. Although it is well-known that pay setting is a particularly sensitive HR task and thus differing views between management and employees can be expected, the size of mean-level differences emphasizes just how different the perceptions of employees and managers are. These perceptions need to be investigated further to understand to what extent these perceptions during the pay-setting discussion are based on prior expectations or anticipations, or on actual behavior of employees and managers during the meeting. Another important result is that congruence was almost always achieved when managers indicated less justice enactment perceptions, i.e., downward slope. This may mean that managers are less prone to make judgmental errors about their own behaviors, but it may also mean that managers need to think they are not doing a good job to be seen as fair. Experimental studies might be suited to test these explanations.

As there are no prior studies or much theory about predictors of congruence, we have selected three important components from pay setting: setting goals, giving feedback, and credibility of the manager. Results show that with higher levels of goal clarity, continuous feedback, and supervisor credibility, the mean-level gap between managers’ justice enactment and employees’ justice perceptions is reduced. The results that continuous feedback and supervisor credibility (and partly goal clarity) were able to associate with more congruence are encouraging. Employees’ justice perceptions were highest when they perceived high scores of goal clarity, continuous feedback, and supervisor credibility. Thus, these three managerial actions can be recommended to create justice perceptions in the pay-setting context but maybe even beyond this context. Making goals more explicit, creating points of contact between managers and employees through continuous feedback and understanding the work and effort of employees might be strategies that help create more than ‘just’ justice congruence during pay-setting. Another implication is that it will not be enough if a manager is well-versed in justice behaviors during the pay setting to be perceived as fair by their employees. Instead, managers’ behaviors during the entire year leading up to an annual pay-setting discussion are relevant for creating justice congruence. At the same time, even though many managers may not enjoy performance appraisals and pay discussions (Malmrud et al., 2023), the effects of justice behaviors extend beyond these meetings.

Conclusions

Despite decades of research on organizational justice perceptions, there is (at least) one puzzle piece that has not been getting attention and has important ramifications for theory and practice. This piece concerns the empirical gap between managers’ justice enactment and employees’ justice perceptions. Many studies have emphasized that if managers just adhere to a specific set of justice rules, employees feel fairly treated at work. In the past two decades, a short period of time within this academic literature, researchers have begun to study justice rule adherence (or justice enactment), putting the spotlight on the fact that managers have their individual motives, skills, or opportunities to be ‘just’. Few articles have measured both employees’ and managers’ experiences of justice – and the few that have did found this empirical gap. The relevance of this gap is this: even though managers think they are adhering to justice rules, employees may view their managers’ adherence to said justice rules very differently. This gap puts some doubt on the practical relevance of the justice rules or on trainings in justice and instead opens up for attempts to solve this puzzle. In this study, we attempted to start solving the gap, by looking at managerial actions that can predict congruence in justice between managers and their employees. In this study, we find that goal clarity, continuous feedback, and supervisor credibility can reduce the mean-level difference in employees’ and managers’ justice perceptions. Results are encouraging and indicate that it is possible to identify actions that can enhance justice congruence. We therefore encourage others to continue with this important work.

Supplemental Material

sj-pdf-1-eid-10.1177_0143831X241261311 – Supplemental material for What makes employees and managers see eye to eye concerning organizational justice? Predicting congruence in the Swedish pay-setting context

Supplemental material, sj-pdf-1-eid-10.1177_0143831X241261311 for What makes employees and managers see eye to eye concerning organizational justice? Predicting congruence in the Swedish pay-setting context by Constanze Eib, Johnny Hellgren, Helena Falkenberg and Magnus Sverke in Economic and Industrial Democracy

Footnotes

Author contributions

CE had the idea, analyzed the data, and wrote the first draft. All authors discussed the idea and structure of the paper. HF, JH, and MS collected the data. MS received the grant that enabled the data collection. All authors read the final draft of the manuscript.

Data transparency

The data are not publicly available due to legal restrictions that guarantee the privacy of research participants. Overall statistics (means, correlations, without demographics) are available on request from the corresponding author [CE].

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The present study is based on data from the project ‘Legitimacy in Pay-setting: A Psychological Perspective on Work-related Pay-setting and Employee-related Pay-setting’, financed by a grant to Magnus Sverke from the Confederation of Swedish Enterprise (no. 313002).

Supplemental material

Supplemental material for this article is available online.

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.