Abstract

This study examines the drivers of the steady decline in South Africa’s private sector labour share between 1971 and 2019. The focus on South Africa is instructive as its distributional contestation is bounded in a matrix of racial conflict. Crucial reforms on trade, finance and welfare were undertaken since 1994, but the study finds little evidence that the extension of the franchise promoted egalitarianism, since white economic elites invested in de facto political power. This study employs an Unrestricted Error Correction Model to estimate the drivers of the private sector labour share, and the findings suggest that globalisation, financialisation and public spending have decreased the labour share, while the effects of education have been positive but insufficient to halt the decline.

Introduction

South Africa has the highest income inequality in the world – the income share of its top 10% (more than 60% of national income) exceeds its peers in the USA, Brazil and India – and is even higher than the Middle East region (Assouad et al., 2018). A number of studies have documented this extreme level of income inequality, albeit using different data sources, time periods and dimensions of inequality – principally top incomes and wage inequality (Alvaredo and Atkinson, 2010; Hundenborn et al., 2019; Leibbrandt et al., 2000, 2012; Mosomi and Wittenberg, 2020; Wittenberg, 2017a, 2017b). However, fewer studies have focused on functional income distribution, with Kaseeram and Mahadea (2015) and Burger (2015) as notable exceptions; however, they focus on the post-1994 period and use fewer explanatory variables.

In this article, we estimate the drivers of South Africa’s functional income inequality from 1971 to 2019 – the longest period covered in such a study on South Africa so far. Our interest is focused on documenting and explaining the dynamics of the private sector wage share due to the combination of high-income inequality and anaemic growth in South Africa (Makgetla, 2004), which presents important lessons for other racially divided societies, with a long history of legally entrenched racial hierarchies, like Brazil or the Southern USA. Moreover, our focus on the labour share allows us to capture not only the degree of the employer–employee distributional conflict but also the extent of racial exploitation over a longer period as compared to previous studies. Conflict over wage negotiation and the resulting wage share is a commonly used measure of cost competitiveness, and this study empirically identifies the political and economic institutions that underpin its dynamics.

The absence of sufficiently long time series data on the racial distribution of income restricts our study to the labour share. However, we draw the reader’s attention to three key facts: (a) black South Africans account for 74% of the employed in 2017, as compared to 11% for white South Africans (Mosomi and Wittenberg, 2020); (b) black South Africans earn 25% of white South African wage income in 2017 (Mosomi and Wittenberg, 2020); (c) employers and top management are primarily white South Africans (Alvaredo and Atkinson, 2010; Nattrass and Seekings, 2001). Though there is no one-to-one mapping of these facts to the evolution of the private sector wage share, we expect black South Africans to be disproportionately affected by changes in the labour share. Ergo, the latter can be interpreted as indirect evidence of the evolution of the racial distribution of income.

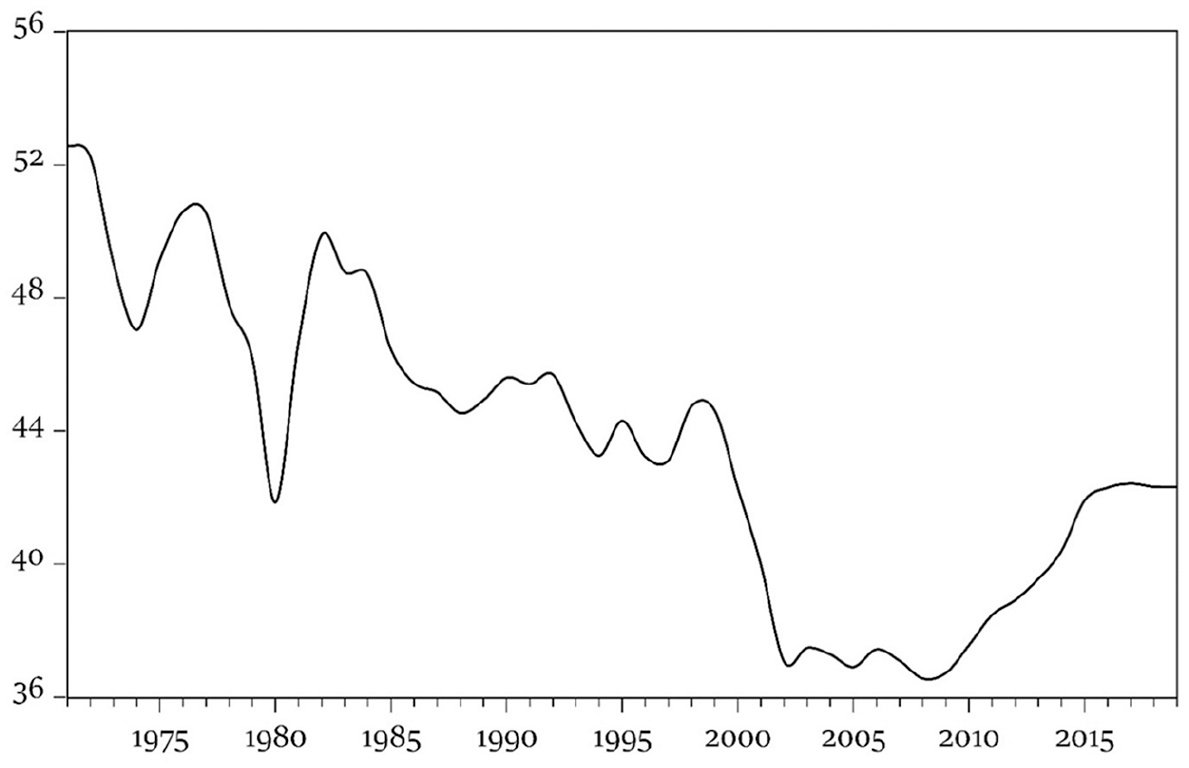

For the period under consideration, we observe a steady decline in the wage share from 1971, with substantial decreases in 1980 and the late 1990s to early 2000s. However, the secular decline stabilised between 2002 and 2009, and has since trended upwards. It is interesting that for the majority of the period, including the post-1994 democratisation period, the labour share has trended downwards. What are the factors that explain the observed patterns? This is the motivating question for this study. The empirical literature on the drivers of wage shares in advanced economies concludes that deunionisation, withdrawal of the welfare state, globalisation and financialisation have all contributed to rising functional income inequality since the 1980s (Alvarez, 2015; Bengtsson, 2014; Dünhaupt, 2017; Flaherty and Ó Riain, 2020; Gouzoulis, 2021; Kristal, 2010; Lin and Tomaskovic-Devey, 2013; Stockhammer, 2017; Wood, 2017). Similar conclusions are drawn for the handful of studies that investigate the cases in emerging economies, which, however, focus on a limited number of explanatory factors (Guschanski and Onaran, 2017; Ibarra and Ros, 2019; Jayadev and Narayan, 2020; Onaran, 2009).

In this study, our methodological approach is two-fold. First, we provide historical and institutional analyses on how industrial relations, social welfare, globalisation and finance influence the balance of power between employees and employers. Second, we employ an Unrestricted Error Correction Model to estimate the drivers of the private sector labour share. We find strong evidence that the Finance, Insurance and Real Estate (FIRE) sectors, Foreign Direct Investment (FDI) inflows, mortgage debt, public consumption and trade openness decrease the private sector wage share. Further, educational attainment, measured by the Human Capital Index, and industrial action increase the private sector wage share.

Our results provide two main interesting insights on the inequality debate. First, our negative result for public consumption is atypical in the literature, even for the few studies on developing countries. Based on our historical analysis, this puzzle may be explained by discriminatory public welfare under apartheid, and fiscal austerity in democratic South Africa (Hunter et al., 2003). It follows that the nexus between public welfare and distribution may be undermined in multi-racial societies due to discrimination and political economy considerations, e.g. minority economic elites. Second, we find strong positive effects for education, but this is almost completely negated with similarly strong negative effects from the size of the FIRE sectors and mortgage indebtedness. Griffith-Jones and Karwowski (2015) and Karwowski (2015, 2018) document the growth of the FIRE economy as a direct consequence of policies adopted after the end of apartheid. Given that white South Africans own a larger share of capital (Alvaredo and Atkinson, 2010; Assouad et al., 2018), this finding shows how social mobility policies can be neutralised, if initial capital ownership is highly concentrated. This result is strong evidence against the argument that income inequality can be reduced from the bottom up, at least in multi-racial societies.

The rest of the article is structured as follows. The next section presents the literature review. The third section discusses the political economy of income distribution in South Africa since the early 1970s. The fourth outlines our empirical strategy and data. The fifth reports our findings, and the sixth section concludes.

Determinants of income inequality: Theory and evidence

The extant literature on the determinants of the functional distribution of income stresses the roles of labour market institutions, the welfare state, trade and financial globalisation, and financialisation. Given the complex and ever-evolving nature of power relations in a society, different theories underline the importance of different channels that influence the employer–employee balance of power (Gouzoulis, 2021; Köhler et al., 2019; Stockhammer, 2017). The remainder of this section reviews these channels that co-determine the private sector functional distribution of income.

Labour militancy, power resources and segregation

The degree of labour market regulation and the state of employment relations have been identified as key determinants of income inequality by the Power Resources Theory (PRT) pioneered by Stephens (1979) and Korpi (1983). The lower the employment/underemployment rate and the wider the coverage of centralised bargaining, the more powerful workers become in wage negotiation. Indeed, numerous studies report empirical evidence that unionisation, centralised bargaining coordination and strike activity lead to higher labour shares and less wage dispersion (Bengtsson, 2014; Cowling and Molho, 1982; Dell’Aringa and Pagani, 2007; Devicienti et al., 2019; Gouzoulis, 2021; Hancke, 2012; Kristal, 2010; Leslie and Pu, 1996; Pontusson, 2013).

Yet, the relationship between labour market coordination and inequalities is substantially less straightforward in societies where bargaining coverage varies due to race and gender discrimination. In societies where racism is widespread, unions might primarily represent different ethnicities and races, thereby, they may undermine working class cohesion. It follows total union density can be an inappropriate measure of labour power for racially divided societies, and collective struggles over income distribution are more accurately measured by total strike activity and participation. Even in case studies like South Africa, a country with a rich trade union history and many ‘racially mixed’ unions, legislation imposed by apartheid restricted the rights of black unionised workers (Bhorat et al., 2015). Thus, even in this case, industrial action can be a better measure of workers’ collective power.

Public spending and welfare retrenchment

Beyond labour militancy and employment relations, PRT also emphasises the role of public welfare expenditures for bargaining outcomes. Increased welfare spending (including unemployment benefits) decreases the discrepancy between the average wage and the income of the unemployed, therefore employees feel safer to demand higher wages. An additional channel relates to the point that public expenditure increases demand and employment growth, thereby enhancing wage demands through weaker labour market competition.

Thus, a widely accepted assertion of the income distribution literature is that economies with extensive welfare states tend to be more egalitarian, while the steep rise in income inequality during the last four decades is largely associated with welfare state retrenchment (Esping-Andersen and Myles, 2009). Indeed, econometric studies on income distribution show that declining unionisation and strike activity, as well as wage bargaining decentralisation, have contributed to decreasing wage shares and rising earning dispersion (e.g. Bengtsson, 2014; Cowling and Molho, 1982; Dell’Aringa and Pagani, 2007; Devicienti et al., 2019; Gouzoulis, 2021; Kristal, 2010, 2013; Pontusson, 2013).

Trade openness, capital mobility and the factors of production

The debates within political economy on whether trade globalisation and capital mobility benefit the abundant or the scarce factor of production date back to Stolper and Samuelson (1941). They posit that globalisation tends to increase wages in developing economies since labour is the abundant factor of production. In contrast, Gereffi et al. (2005) argue that the globalisation of commodity chains encourages relocation to low-wage countries, which disproportionately benefits the most mobile factor of production, i.e. capital (Rodrik, 1997). According to this view, the intensified labour market competition induces a ‘global race to the bottom’ between workers of advanced and developing countries, who accept lower wages to attract investment.

Overall, there is strong evidence that trade openness, FDI flows and financial globalisation have decreased labour’s income share in advanced as well as developing economies. The ILO (2008) and IMF (2017) provide evidence that foreign assets and liabilities have contributed to the rise of functional income inequality. Also, Harrison (2002), Jayadev (2007), Onaran (2009), Stockhammer (2017) and Gouzoulis and Constantine (2021) report panel and time series evidence that trade and capital account openness and FDI have decreased the labour shares of both advanced and emerging economies. Finally, Böckerman and Maliranta (2012) empirically demonstrate that Finland’s export share causes intra-industry restructuring that decreases its labour share.

Financial dependency and the employer–employee balance of power

In early work, Greenwood and Jovanovic (1990) posit a non-linear relationship between financial development and income distribution. They argue that the richest social groups have disproportionate access to credit during the early stages of financial development, which engenders income inequality. However, beyond some threshold level of financial development, access for the poor increases and lowers income inequality. But Claessens and Perotti (2007) note that vested interests in unequal societies can impose barriers and undermine equal access to credit. Strikingly, even when the poor households become financialised, they usually accumulate debt rather than investment income to keep up with the Joneses and/or counterbalance inadequate public welfare.

Evidence shows that household indebtedness and the associated fear of default make employees more likely to accept lower wages and avoid union participation (Froud et al., 2002; Gouzoulis, 2021; Grady and Simms, 2019; Langley, 2007; Wood, 2017). Financial development also promotes firm-level debt, and job losses and wage cuts are common strategies to protect corporate balance sheets (Froud et al., 2000; Lazonick and O’Sullivan, 2000; Thompson, 2003). Furthermore, the increase in non-financial corporations’ financial profits (Krippner, 2005; Tomaskovic-Devey and Lin, 2011) makes growth less dependent on labour and, consequently, lowers labour shares (Alvarez, 2015; Lin and Tomaskovic-Devey, 2013). Overall, increases in inequalities due to financialisation tend to be larger in economies with weaker labour market institutions (Argitis and Dafermos, 2013; Gouzoulis, 2021; Wood, 2017).

Industrialisation, skill upgrading and long-run inequality

The seminal studies of Lewis (1954, 1955) and Kuznets (1955) theorise and map the inequality–industrialisation–growth nexus. Lewis (1955) identifies differentials in saving rates and productive expenditures as the key mechanisms behind inequality. In pre-capitalist agricultural societies, the main source of income for the wealthy social groups is land rents, which do not require significant investment spending. In industrialised economies, a larger share of profits is related to industrial investment, which requires expenditures on raw materials, innovation and labour costs. Therefore, the rise of new high-wage sectors during industrialisation creates a divided economy, with the agricultural sector paying lower wages. As the economy gradually develops and becomes industrialised, labour moves toward the high-productivity, high-wage sectors, thus, inequality declines.

Contrariwise, Acemoglu and Robinson (2002) claim that the co-occurrence of rising growth and declining inequality before the early 1980s was the outcome of radical pro-labour reforms, rather than the result of the trickle-down effects of industrialisation. Moreover, recent long-run evidence shows that the Lewis/Kuznets curve is inverted in many advanced and developing economies (Piketty, 2014, 2020). Indeed, industrialisation may not necessarily induce a smooth skill upgrading and workforce movement to high-wage sectors in racially divided societies. As argued in the next section, South Africa is a good example where this process has been far from smooth. Relevant anti-Kuznets evidence is presented by Jayadev and Narayan (2020), who show that privatisation, technology, concentration and informalisation induced a steep decline in India’s wage shares since 1983. In contrast, Ibarra and Ros (2019) attribute the decline in Mexico’s labour share between 1990 and 2015 to the first phase of a Kuznets cycle.

The political economy of South Africa’s income distribution

The election victory of the National Party (NP) in 1948 is considered the starting point of apartheid, which refers to institutionalised racism against black South Africans. Though the apartheid regime lasted from 1948 to 1994, it went through different phases due to internal struggles and international pressures.

The rise and fall of apartheid are identified under three periods (Posel, 2011): (1) The 1950s, where black South Africans could live in cities as long as their work was necessary for the white urban citizens. Black South Africans who already lived in cities were allowed to stay, but a clear separation between white and black neighbourhoods was established through buffer zones. (2) The 1960s, the peak of apartheid, when the state displaced a ‘surplus’ black African population of about 3.5 million people to segregated, self-governing homelands. Due to the distinct political authority in the new homelands, the central government was not responsible for the welfare and education of displaced black South Africans. (3) The 1970s–1994 era, when economic conditions, protests and rebellions induced a ‘reformist’ turn, as compared to the earlier phases.

Given that the majority of the working class population in the country has been historically black South Africans and the majority of employers white South Africans, a key question that emerges is how the employment relationship in South Africa evolved since the early decline of the apartheid regime. As noted earlier, existing studies on functional income distribution in South Africa cover only the post-1994 period and explore a limited number of explanatory factors that do not cover the full extent of institutional restructuring that took place since the early 1970s (Burger, 2015; Kaseeram and Mahadea, 2015). Given the review of relevant literature, overviewing important determinants of the employer–employee conflict related to globalisation, capital flows, housing and finance is a major omission.

Figure 1 reports the evolution of the private sector wage share in South Africa from 1971 to 2019. Following Stockhammer (2017), the private sector wage share is defined as the ratio of ‘Compensation of employees to GDP at factor cost’. 1 The data are sourced from the South African Central Reserve Bank (SARB), and exclude self-employment income and fringe benefits. However, we are not concerned with under-estimating the private sector wage share for two reasons. First, the peak ratio of social benefits to compensation of employees is only 0.89% according to SARB. Second, while data on self-employment income are only available after 1995, black South Africans had few opportunities for self-employment during apartheid and the size of the self-employed remains relatively small even after 1994 (Bargain and Kwenda, 2011; Seekings, 2007).

Private sector wage share (% GDP), 1971–2019.

Further, our focus on the private sector wage share, as opposed to the total or public sector wage share, allows us to evaluate the intensity of the traditional capital–labour conflict. Conceptually, centring on the private sector wage share is important given that functional income distribution theories generally focus on interactions and negotiations between private employers and employees, since the nature of employment relations in the government sector tends to be very different. Also, the use of the private sector wage share enables this study to test the hypothesis that the extent of government welfare affects employer–employee wage bargaining. Since we employ government consumption as a proxy measure for public welfare, this work avoids endogeneity issues by excluding the public sector wage bill. 2 Additionally, the promise of democracy and the end of apartheid is that both functional and racial income inequality would decrease in the private sector. This work allows us to evaluate whether this promise was kept. Moreover, for the period under consideration, the South African economy had experienced significant changes in its political institutions and production structure, and undergone extensive reforms relating to trade, finance and labour relations targeted at the private sector. A fundamental objective of this work is to appraise the distributional credentials of these reforms. The rest of this section discusses the political and economic institutions in South Africa, and how they relate to the post-1970 trend of functional income inequality.

Segregation and industrial relations under apartheid: 1970–1990

South Africa grew rapidly from 1960 to the early 1970s, mainly due to the FDI inflows and the exchange controls that prevented capital flight, which boosted manufacturing production through giant conglomerates. Consequently, this led to employment growth for black South Africans (Lodge, 2011). The FDI-induced economic pressures incentivised the state to direct industry towards areas closer to the homelands, which brought some limited prosperity in these areas in terms of improved educational attainment and some black workers being employed in relatively more skilled roles, such as teachers, managers or civil servants (Lodge, 2011). ‘Limited prosperity’ describes the relative poverty reduction due to the trickle-down effects of industrialisation, which came with rising income inequality, high overall unemployment and limited social security. Notwithstanding the misreported social statistics by official authorities (Alenda-Demoutiez and Mügge, 2020), the rise of inequalities for black workers during this period is widely acknowledged (Griep et al., 2014; Seekings and Nattrass, 2005: Ch. 5).

This emerging reality created new demands for more political rights (Seekings and Nattrass, 2005: 105) and led to the formation of black trade unions (Godfrey et al., 2007). Initially, many unions were led by leaders of the African National Congress (ANC) and maintained a top-down structure in terms of decision-making power. However, Buhlungu (2009) contends that they gradually became more inclusive with democratically elected union leaders. Independent black trade unions organised strikes over wages in 1973, which led to the Bantu Laws Amendment Act of 1973 that assigned some limited rights to black workers but ultimately disempowered their unions (Budeli, 2012). Yet, despite their largely progressive role, it is worth highlighting that not all unions were strictly ‘workerist’ per se or ‘politically coordinated’ in all cases.

The ensuing industrial conflict combined with international pressures coerced the government to establish the Wiehahn Commission, and its 1979 report suggested that employees should be granted full rights to association independent of race, religion or gender, and argued for the establishment of an Industrial Court (Lichtenstein, 2019). The apartheid state accepted most proposals and removed the racial elements of the Bantu Act, which allowed the creation of several new fully autonomous trade unions in the early 1980s. The new industrial relations model allowed black workers to institutionalise their broader anti-apartheid struggle (Finnemore and Van der Merwe, 1992). Furthermore, the social security system steadily expanded to the black population, reducing benefits and pensions inequalities. Indicatively, the real increase in the pensions of black South Africans between 1970 and 1993 was 7.3%, but major inequalities persisted since black pensioners kept receiving significantly less than white pensioners as a share of the average wage (Van der Berg, 1997).

Several social uprisings led by black workers and students occurred during this early phase of the anti-apartheid struggle. The two more important revolts were the 1976–77 student-led uprising in Soweto and the 1984–86 popular rebellion (Murray, 1989). In the context of the latter revolt, a major national institution emerged in 1985: the Congress of South African Trade Unions (COSATU), the successor of the Federation of South African Trade Unions (FOSATU) which was established five years earlier. The ‘Social Movement Unionism’ model of COSATU allowed it to play an important role in the industrial terrain, but also in the fight for the end of apartheid (Budeli, 2012; Hirschsohn, 1998). Notwithstanding continued attacks against union leaders between 1988 and 1990, the intensified struggle led to the unbanning of the South African Communist Party (SACP) and the ANC, which together with COSATU formed the Tripartite Alliance after the release of Nelson Mandela from prison in 1990. In addition, during the same period, the Pan African Congress (PAC) was also unbanned.

South Africa in transition: Globalisation, finance and inequality

The racial conflict episodes of the 1988–90 period and the intensified international sanctions of the 1980s triggered the fall of apartheid. Negotiations between the NP and the ANC took place between 1990 and 1992, which resulted in an agreement for the first free elections in 1994 when Mandela was elected the first post-apartheid president of South Africa.

Despite its radical agenda during the late apartheid and early transition years, the ANC quickly adopted a moderate stance against business leaders and softened its views on nationalisation and regulation of key industries (Nattrass, 1994). 3 Given the ANC’s newly adopted market-oriented approach, it sought to reconcile capital–labour–state relations through the 1996 Growth Employment and Redistribution (GEAR) macroeconomic strategy. The GEAR plan aimed to boost private investment and employment through fiscal austerity and the liberalisation of the labour market (Streak, 2004). The policy intervention included negative real interest rate policies and tax breaks for firms, but employers responded by increasing capital intensity and the employment of the better-trained workforce. Inevitably, the latter was smaller due to the under-provision of education for black South Africans (Moll, 1996; Nattrass, 2014), and higher capital intensity decreased their wages. Consequently, since 1994, the total unemployment rate in the country has been increasing steadily reaching almost 30 and 40% according to the strict and the expanded definitions, respectively (Alenda-Demoutiez and Mügge, 2020).

Regarding wage coordination, the establishment of an employer–employee negotiation framework and associations of business owners achieved the establishment of basic labour market institutions, which initiated the democratisation of the workplace. This allowed some coordination between employers and employees in the country. On the one hand, certain trade unions acknowledged the wage–employment–profitability trade-off and accepted productivity-related bonuses at the expense of basic wages (Nattrass, 1995). On the other hand, unions rejected the possibility of stopping mass strikes and regional wage setting (Nattrass, 1997). However, these reforms have not fully succeeded in addressing racial divisions of the past, hence cooperation between white and black business owners, as well as between employers and employees remains dysfunctional (Bischoff et al., 2021). Also, it is worth noting that despite the fact that the number of trade unions both in the private and the public sectors grew substantially after 1994, their membership dynamics follow distinct trajectories (Bhorat et al., 2015): union members in the public sector increased from 835,795 in 1997 to 1,393,189 in 2013, and the union density of the sector grew from 55.2% to 69.2%. Contrariwise, in the private sector, union membership between 1997 and 2013 increased only by approximately 50,000 persons, while private sector union density shrunk from 35.6 to 24.4% during the same period.

Limited privatisations were also used by the state as a means of partially restoring historical injustices. More specifically, the unbundling of white-owned private corporations and the privatisation of certain assets of the apartheid state favoured the emergence of a small black business elite, while a limited group of black professionals enjoyed promotions due to affirmative action policies (Adams et al., 1997). However, these black empowerment policies within the private and the public sectors reached only a minority of politically affiliated insiders, with the majority of black employees remaining poor and excluded (Andreasson, 2006; Hartshorn and Sil, 2019; Michie, 2020; Nattrass, 2014; World Bank, 2018). Interestingly, Habib and Padayachee (2000) challenge the de facto deracialising character of these privatisations, since the new black businesses are financed by foreign and white South Africans. Despite the fact that social grants provision has expanded to almost 50% of the population (Waidler and Devereux, 2019), these phenomena of exclusion and poor public service delivery, especially in the former black homelands, have often triggered violent local protests with some support by trade unionists (Alexander, 2010; Alexander and Pfaffe, 2014).

Beyond policies related to the domestic market, the ANC had undertaken extensive trade and capital account liberalisation. For example, foreign exchange controls were removed in the mid-1990s and led to significant investment volatility due to fluctuations in FDI and portfolio capital flows. Moreover, the end of international sanctions after apartheid accelerated trade integration and capital inflows. These capital and investment inflows induced an asset price boom, which exposed South Africa to international financial fragility (Isaacs and Kaltenbrunner, 2018). In contrast to what the state expected, openness did not have a positive impact on employment but led to higher unemployment especially in the manufacturing sectors (Jenkins, 2008). The continuing rise in unemployment since 1994 has been particularly harmful to black South Africans, who experienced dramatically higher rates due to the long-lasting effects of apartheid (Alenda-Demoutiez and Mügge, 2020). Indian and coloured South Africans also suffer from higher unemployment rates compared to white South Africans, whilst unemployment rates are remarkably higher for women across all racial categories (Alenda-Demoutiez and Mügge, 2020).

Several studies argue that white South African business leaders have unsuccessfully lobbied for financial liberalisation since the late 1970s (Davies et al., 1985; Habib and Padayachee, 2000). However, it is after the 1990s that the South African financial development model attempted to increase competition in the financial sector and break up large commercial banks and non-banking financial institutions, but ultimately this process rather exacerbated concentration. This transformation led to two key structural changes within the non-financial sectors of the economy. First, since the 1990s, non-financial corporations (NFCs) started investing heavily in risky financial assets rather than innovation and productive activities (Andreoni et al., 2021). Second, since the mid-1990s, South Africa experienced a massive credit-fuelled residential housing bubble, which remains dramatically larger compared to most emerging economies and very close to the trend of the Anglo-Saxon economies (Griffith-Jones and Karwowski, 2015; Karwowski and Stockhammer, 2017). Crucially, the two processes are interconnected since NFCs’ financial investment includes foreign capital inflows to purchase property assets (Karwowski, 2018). The housing bubble has since collapsed (2007–8) leading to a decline in mortgage indebtedness.

All things considered, the trajectory of the private sector labour share reflects the economic and political changes over the period under consideration (see Figure 1). The early secular decline in the wage share appears to be consistent with the turbulent years associated with intense industrial and armed conflict. In contrast, the relative stability of the early democratisation years can potentially explain the temporary stabilisation of the private sector wage share, and the globalisation and financialisation shocks are prima facie explanations of the steep decline that followed. The increase of the labour share between 2009 and 2015 may correspond to the decrease in mortgage debt and to the construction and tourism boom associated with the 2010 FIFA World Cup that took place in South Africa. We test these hypotheses in the Findings section.

Research methodology and data sources

Empirical design and econometric approach

Building on the political economy analysis of the South African power relations and the theoretical postulates presented in the previous sections, we proceed to the econometric analysis of the determinants of functional income inequality in South Africa between 1973 and 2018. The baseline econometric specification is as follows:

where:

PWS is the private sector wage share (see Figure 1). We use the private sector wage share to minimise endogeneity biases that arise due to the use of government consumption, in the absence of welfare spending series.

LM is labour militancy proxied by the number of strikes and lockouts (total economy), which is expected to exhibit positive effects on the wage share, depicting primarily the growth of the black trade union movement.

PUB is public spending measured by government consumption (share of GDP). Given the history of discriminatory public welfare expenditures in South Africa and narrow welfare reforms in the post-democratisation period, we do not expect government consumption to increase the private sector wage share as in the standard literature.

GLOB is trade globalisation proxied by trade openness (imports plus exports as a share of GDP), which is the most common proxy used in the literature. Given the discussion in the previous section, we expect a negative coefficient.

FIN is financialisation proxied by the size of the finance, insurance and real estate (FIRE) sector (gross value added as a share of GDP). Given the extent of financialisation in the country and the weak labour market institutions, we expect FIRE to increase inequality.

HUM is human capital development proxied by the Human Capital Index (based on average years of schooling and assumed rates of return to education), which is expected to positively affect labour.

DEM is a time dummy variable that controls for the post-apartheid period (1994–2018). Since democratisation empowers a larger number of people and is related to inclusiveness (Scheve and Stasavage, 2009), we expect a positive coefficient.

REVOLT is a time dummy variable that controls for the 1976–77 ‘Soweto uprising’ and the 1984–86 popular rebellion led by black students and trade unionists (see Murray, 1989). 4 Since the majority of the working class population in South Africa is black, we expect positive effects on the wage share.

Given the single-equation design of our study, we use the Unrestricted Error Correction Model (UECM) (Davidson et al., 1978; Sargan, 1964), which is widely used in empirical wage share studies (Bengtsson, 2014; Flaherty and Ó Riain, 2020; Gouzoulis, 2021; Gouzoulis and Constantine, 2021; Kristal, 2010). This approach largely addresses the usual serial correlation issues, especially in the context of macro-level and small sample size studies. 5 The UECM includes both the long-run (level) and the short-run (first-differenced) coefficients of the independent variables as follows:

where the vector

There are two preconditions for the use of the UECM: (1) all variables must be stationary at either levels or first differences; (2) the dependent and independent variables must have a cointegrating long-run relationship. As reported in the Appendix, all variables that we use are either I(0) or I(1). Moreover, after estimating the stationary regression between the dependent variable and the explanatory variables, we find that its residuals are stationary, which constitutes evidence of a cointegrating relationship. Therefore, both requirements are satisfied.

Alternative specifications and robustness checks

Beyond the explanatory variables of the baseline equation, we experiment with several additional variables to evaluate alternative channels that influence functional income inequality and the robustness/sensitivity of the baseline findings.

In specification (2), we replace Trade Openness and the FIRE Sector with FDI Inflows (Net; share of GDP) to evaluate whether attempts to attract foreign capital increased inequality. In specification (3), we replace Trade Openness with Exports Diversification (Overall [Theil] Index) to explore how the structural transformation of the economy affects the labour share. We do not include both indicators in the same specification since export diversification is expected to increase exports and affect overall trade openness. In specification (4), we replace Trade Openness with the Nominal Exchange Rate (Local currency unit per US$) to assess how the abolition of exchange controls after apartheid affected income distribution. In specification (5), we replace FIRE Sector with the Mortgage Debt Ratio (Total mortgage advances of households and non-profit institutions serving households [NPISHs] over the disposable household income) to explore whether the post-1990s debt-fuelled housing bubble decreased the wage share as in many advanced liberal market economies. In specifications (6) and (7), we replace the FIRE Sector with Financial Development (Index) and the Chinn–Ito Index (Capital account openness) respectively, as alternative proxies for domestic and international financial liberalisation. In specification (8), we replace the Human Capital Index with the Unemployment Rate to examine if the remarkably high unemployment rate in the country increased inequality. While the two variables measure different channels, we do not include them in the same specifications as education influences employment opportunities (Cairó and Cajner, 2018). Despite data reliability having improved due to efforts to deracialise and normalise labour statistics since 1999, some caution is advised in interpreting any results related to unemployment (Alenda-Demoutiez, 2020).

In specification (9), we replace the Human Capital Index with the Capital–Labour Ratio (Average) to account for changes in relative factor endowments. In specifications (10) and (11), we replace the Human Capital Index with Industry (Value-added) and Urbanisation (Share of total population), respectively, to assess the potential distributional consequences of industrialisation and urbanisation following Lewis (1954). In these specifications, we drop human capital development given the nexus among skill attainment, capital intensity and industrialisation (Allais, 2020). The same holds for urbanisation (Bertinelli and Zou, 2008), especially in the context of South Africa’s rural–urban divide in welfare provision. In specification (12), we replace Strike Activity with Redundancy Pay (Legally mandated redundancy compensation [time dummy]) as a proxy for labour market social safety nets that decrease inequalities. In specification (13), we add the WBL Index (Women Business and the Law Index Score [scale 1–100]) as a proxy for gender equality in the business sector. In specification (14), we add Remittances (Received; share of GDP) to examine whether payments received from abroad increase or decrease inequality. In specification (15), we add the IPCG Tax (Taxes on income, profits and capital gains; share of revenue) to evaluate whether income taxation has been pro-labour. Finally, in specification (16), we add Natural Resources Rents (Share of GDP) to examine the potential distributional effects of mineral reserve exploitation.

Data sources

The series for Public Consumption, Trade Openness, FDI Inflows, Nominal Exchange Rate, Industry, Urbanisation, Remittances, WBL Index, IPCG Tax and Natural Resources Rents are sourced from the World Bank Indicators. The proxy for Strike Activity comes from the ILO database, whilst Exports Diversification, Financial Development and Unemployment Rate are sourced from the IMF. Redundancy Pay comes from Armour et al. (2016), whereas the data source for the FIRE Sector, Mortgage Debt Ratio and Capital–Labour Ratio is the SARB database. Finally, the Human Capital Index and the Chinn–Ito Index were obtained from Feenstra et al. (2015) and Chinn and Ito (2006), respectively. The final dataset covers the period 1971–2019 and the data were obtained on 11 November 2020. Further descriptive statistics are reported in the Appendix.

Results and discussion

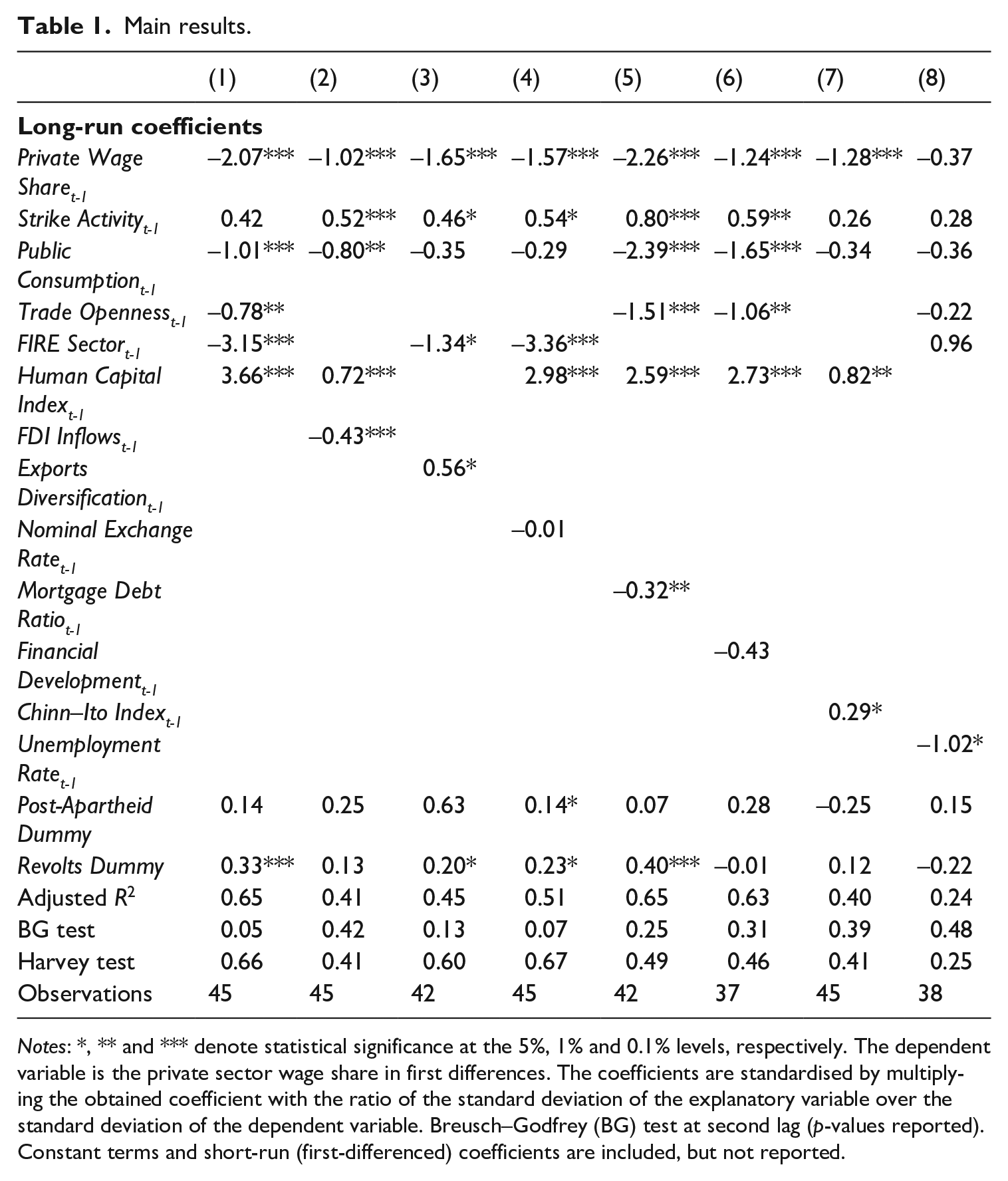

Table 1 reports the main econometric findings. In specification (1), the FIRE Sector, Human Capital Index and Trade Openness have the expected signs and are statistically significant at the 1% or 0.1% levels. Public Consumption exhibits a negative impact on the private labour share and is statistically significant at the 0.1% level. In specification (2), Strike Activity, Human Capital Index and FDI Inflows have the expected signs and are statistically significant at the 0.1% level. The sign of Public Consumption remains similar to the baseline result and statistically significant at the 1% level. In specification (3), Exports Diversification has the anticipated positive effect on the private sector wage share, while Strike Activity and FIRE Sector keep their expected signs. All three coefficients are statistically significant at the 5% level. Adding the Nominal Exchange Rate in specification (4) does not affect the long-run signs of Strike Activity, FIRE Sector and Human Capital Index in terms of signs, magnitude and statistical significance. Yet, the new variable does not exhibit a significant impact on the labour share.

Main results.

Notes: *, ** and *** denote statistical significance at the 5%, 1% and 0.1% levels, respectively. The dependent variable is the private sector wage share in first differences. The coefficients are standardised by multiplying the obtained coefficient with the ratio of the standard deviation of the explanatory variable over the standard deviation of the dependent variable. Breusch–Godfrey (BG) test at second lag (p-values reported). Constant terms and short-run (first-differenced) coefficients are included, but not reported.

In specifications (5) and (6), where we test the effects of alternative finance indicators, the remaining long-run coefficients are unchanged as compared to the baseline specification. The Mortgage Debt Ratio decreases the private sector wage share, with its long-run coefficient statistically significant at the 1% level, whilst Financial Development has the expected negative effect but is statistically insignificant. Further, in specification (7), we find that the Chinn–Ito Index exerts a positive impact and is statistically significant at the 5% level. The remaining coefficients do not change signs, but only Human Capital Index is statistically significant at the 1% level. In specification (8), including Unemployment Rate affects the statistical significance of other control factors. Unemployment itself is found to decrease the private sector labour share and is statistically significant at the 1% level. However, this finding must be viewed with some caution, given the long-standing issues with the calculation of this indicator in South Africa (Alenda-Demoutiez and Mügge, 2020).

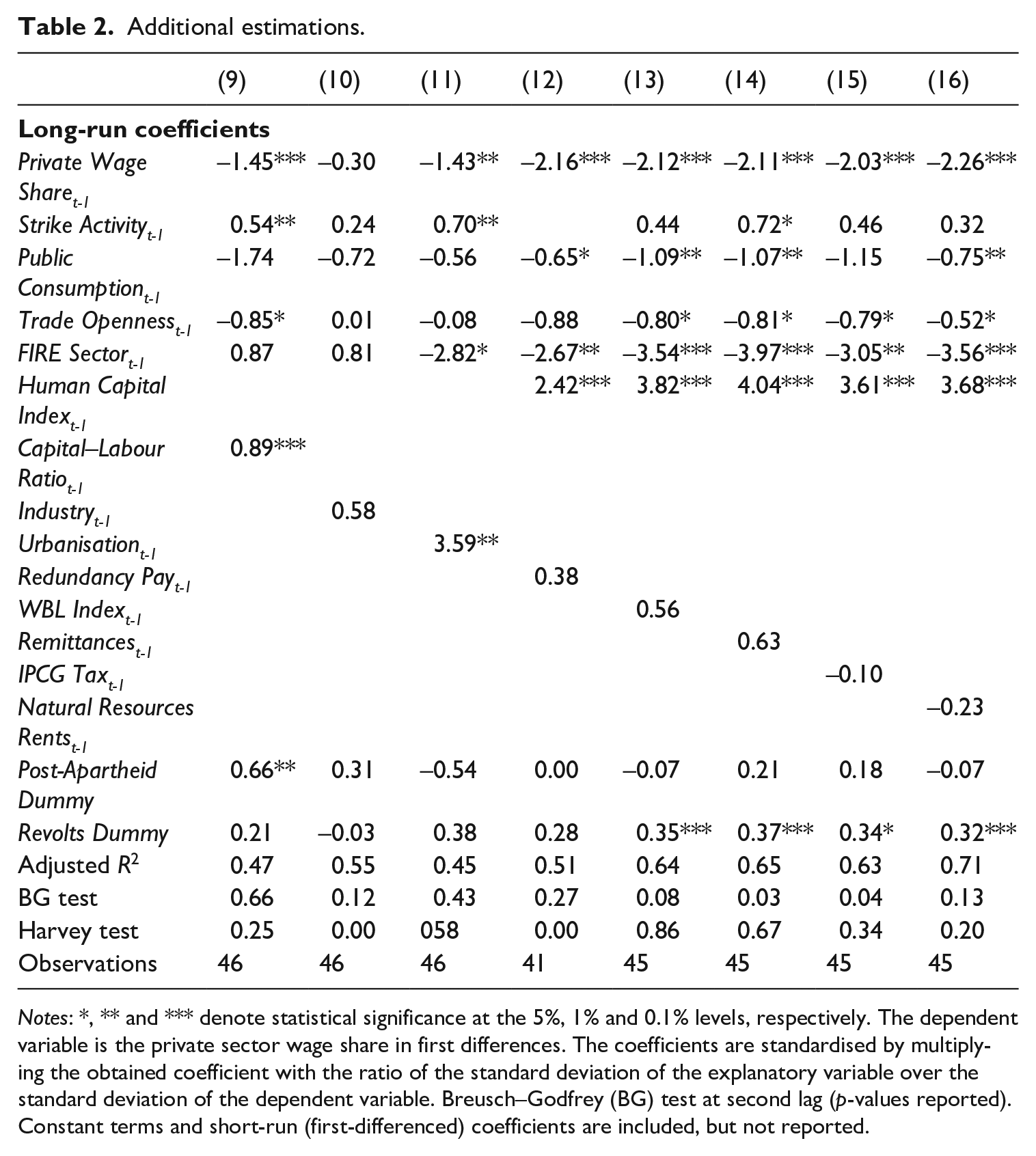

Table 2 reports the additional econometric findings. In specifications (9) and (10), replacing Human Capital Index with Capital–Labour Ratio and Industry, respectively, does not affect the signs of Strike Activity, Trade Openness and Public Consumption as compared to the baseline findings. Yet, only the former two coefficients are statistically significant at the 1% and 5% levels, respectively. Capital–Labour Ratio exhibits a positive and statistically significant effect (0.1% level) on the private sector labour share, whereas the sign of Industry is also positive but statistically insignificant. In specification (12), where we replace Strike Activity with Redundancy Pay, the remaining long-run coefficients are similar to the baseline results in terms of sign and statistical significance, except for Trade Openness that becomes statistically non-significant. Redundancy Pay has the expected positive long-run impact but it is not statistically significant. Finally, in specifications (13) to (16), the long-run coefficients remain unchanged as compared to the baseline model. Trade Openness, FIRE Sector and Human Capital Index are statistically significant at the 1% or 0.1% levels in all four specifications. Public Consumption and Strike Activity are statistically significant in equations (13), (14) and (16), and in (14), respectively. All additional control variables in these specifications exhibit the expected effects but are statistically insignificant.

Additional estimations.

Notes: *, ** and *** denote statistical significance at the 5%, 1% and 0.1% levels, respectively. The dependent variable is the private sector wage share in first differences. The coefficients are standardised by multiplying the obtained coefficient with the ratio of the standard deviation of the explanatory variable over the standard deviation of the dependent variable. Breusch–Godfrey (BG) test at second lag (p-values reported). Constant terms and short-run (first-differenced) coefficients are included, but not reported.

Regarding post-estimations diagnostics, according to the Breusch–Godfrey and Harvey tests, only two out of 16 equations face some serial correlation or heteroscedasticity issues. Also, Variance Inflation Factors analysis indicates no multicollinearity problems in our specifications. These tests underline the statistical robustness of our econometrics results. All things considered, our quantitative findings provide robust evidence that globalisation and financialisation have decreased the South African private sector wage share since 1970, whilst human capital development has exhibited positive effects on it. Labour militancy and public spending are found to play important but relatively limited roles.

Conclusion

This study finds strong evidence that trade globalisation, financialisation (mortgage debt, FDI inflows and the FIRE sectors) and public consumption lower the South African private sector wage share since 1971. Crucial reforms on trade, finance and welfare were undertaken after the democratisation period of 1994, but we find little evidence that the extension of the franchise increased the labour share. Human capital development, union strike activity and periodic revolts against apartheid lower functional income inequality, but their impact has been insufficient compared to the effects of globalisation and financialisation.

These results are instructive on several fronts. South African democracy is not redistributive – this is a striking finding given the implicit political promise of the African National Congress. While we do not explicitly investigate the racial distribution of the private sector wage share, we expect black South Africans to be disproportionately affected by a contraction in the labour share, as they represent approximately two-thirds of the employed. It follows that more research is needed on the political empowerment of minorities or majorities (in the South African case), and the reduction of extreme inequalities across races.

Unlike the standard result in relatively homogeneous societies, public consumption lowers the South African labour wage share. In post-apartheid South Africa, the ‘Growth Employment and Redistribution Macroeconomic Strategy’ was underpinned by fiscal austerity (Streak, 2004). Indeed, public welfare coverage expanded in democratic South Africa, but the key dimensions of the welfare state that matter for wage bargaining were absent. This demonstrates how the unfortunate coincidence of a non-redistributive democratic transition and certain economic reforms, e.g. fiscal austerity, conspired to increase functional income inequality. It follows that policymakers must be cognisant of timing and the prevailing global policy winds when they undertake deep structural reforms.

Overall, the positive effects of schooling, strike activity and revolts were insufficient to overcome the adverse effects of trade globalisation, financialisation and public consumption on the private sector wage share. This shows that schooling and industrial actions are equalisers, but not enough when a society is racially divided in terms of capital ownership and unionisation, and/or when policy betrays political promises.

Footnotes

Appendix

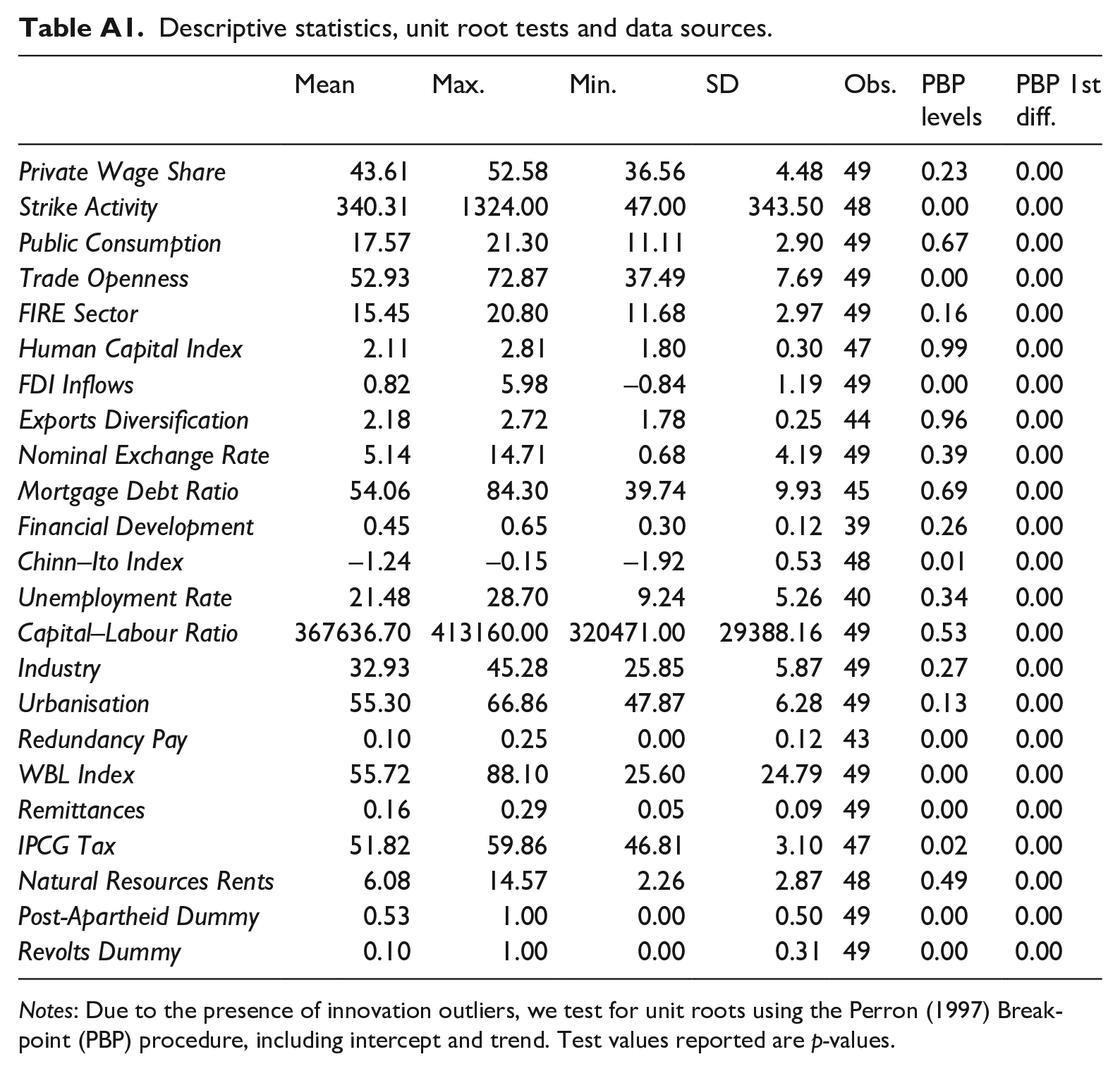

Descriptive statistics, unit root tests and data sources.

| Mean | Max. | Min. | SD | Obs. | PBP levels | PBP 1st diff. | |

|---|---|---|---|---|---|---|---|

| Private Wage Share | 43.61 | 52.58 | 36.56 | 4.48 | 49 | 0.23 | 0.00 |

| Strike Activity | 340.31 | 1324.00 | 47.00 | 343.50 | 48 | 0.00 | 0.00 |

| Public Consumption | 17.57 | 21.30 | 11.11 | 2.90 | 49 | 0.67 | 0.00 |

| Trade Openness | 52.93 | 72.87 | 37.49 | 7.69 | 49 | 0.00 | 0.00 |

| FIRE Sector | 15.45 | 20.80 | 11.68 | 2.97 | 49 | 0.16 | 0.00 |

| Human Capital Index | 2.11 | 2.81 | 1.80 | 0.30 | 47 | 0.99 | 0.00 |

| FDI Inflows | 0.82 | 5.98 | –0.84 | 1.19 | 49 | 0.00 | 0.00 |

| Exports Diversification | 2.18 | 2.72 | 1.78 | 0.25 | 44 | 0.96 | 0.00 |

| Nominal Exchange Rate | 5.14 | 14.71 | 0.68 | 4.19 | 49 | 0.39 | 0.00 |

| Mortgage Debt Ratio | 54.06 | 84.30 | 39.74 | 9.93 | 45 | 0.69 | 0.00 |

| Financial Development | 0.45 | 0.65 | 0.30 | 0.12 | 39 | 0.26 | 0.00 |

| Chinn–Ito Index | –1.24 | –0.15 | –1.92 | 0.53 | 48 | 0.01 | 0.00 |

| Unemployment Rate | 21.48 | 28.70 | 9.24 | 5.26 | 40 | 0.34 | 0.00 |

| Capital–Labour Ratio | 367636.70 | 413160.00 | 320471.00 | 29388.16 | 49 | 0.53 | 0.00 |

| Industry | 32.93 | 45.28 | 25.85 | 5.87 | 49 | 0.27 | 0.00 |

| Urbanisation | 55.30 | 66.86 | 47.87 | 6.28 | 49 | 0.13 | 0.00 |

| Redundancy Pay | 0.10 | 0.25 | 0.00 | 0.12 | 43 | 0.00 | 0.00 |

| WBL Index | 55.72 | 88.10 | 25.60 | 24.79 | 49 | 0.00 | 0.00 |

| Remittances | 0.16 | 0.29 | 0.05 | 0.09 | 49 | 0.00 | 0.00 |

| IPCG Tax | 51.82 | 59.86 | 46.81 | 3.10 | 47 | 0.02 | 0.00 |

| Natural Resources Rents | 6.08 | 14.57 | 2.26 | 2.87 | 48 | 0.49 | 0.00 |

| Post-Apartheid Dummy | 0.53 | 1.00 | 0.00 | 0.50 | 49 | 0.00 | 0.00 |

| Revolts Dummy | 0.10 | 1.00 | 0.00 | 0.31 | 49 | 0.00 | 0.00 |

Notes: Due to the presence of innovation outliers, we test for unit roots using the Perron (1997) Breakpoint (PBP) procedure, including intercept and trend. Test values reported are p-values.

Acknowledgements

We are grateful to Antonio Andreoni and participants of the BUIRA Conference 2021 ‘The Past, Present and Future of Industrial Relations and the Politics of Work’ for their feedback on earlier versions. We would also like to thank an anonymous referee for their constructive suggestions.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.