Abstract

Remittances have been characterized as resilient flows of capital that provide financial relief to migrant households and emerging economies during downturns, crises and other periods of hardship. This article examines patterns of remittance transfer to Sri Lanka between January 2020 and December 2022, drawing on Central Bank statistics and online remittance surveys with migrant workers to test prominent assumptions about the drivers of remittance behavior. Findings indicate little evidence to support explanatory factors linked to the resilience hypothesis, instead pointing to the likelihood that fluctuations in official remittance figures reflect shifts between formal and informal remittance channels.

Introduction

As 2020 drew to a close, Sri Lanka’s remittance economy appeared defiantly buoyant. Contrary to severe forecasts of declining global and regional remittance flows as the COVID-19 pandemic unfolded (Ratha et al., 2020a, 2020b), foreign income transfers to Sri Lanka remained strong: Breaking monthly records in December and ending the year with an annual increase over the previous year (CBSL, 2023). This outcome was achieved despite significant reductions to the size of Sri Lanka’s migrant workforce—resulting from job losses, repatriation flights, and a halt on recruitment and new departures—seemingly confirming one of the longstanding assumptions about remittances: That they are “resilient” or even “countercyclical” inflows of developmental capital (Gammeltoft, 2003; Kim et al., 2022; Page and Plaza, 2006; Sirkeci et al., 2012). Indeed, that remittance flows typically remain stable or increase to provide relief during crises has become a common argument in support of the so-called “migration-development nexus” (Faist and Fauser, 2011).

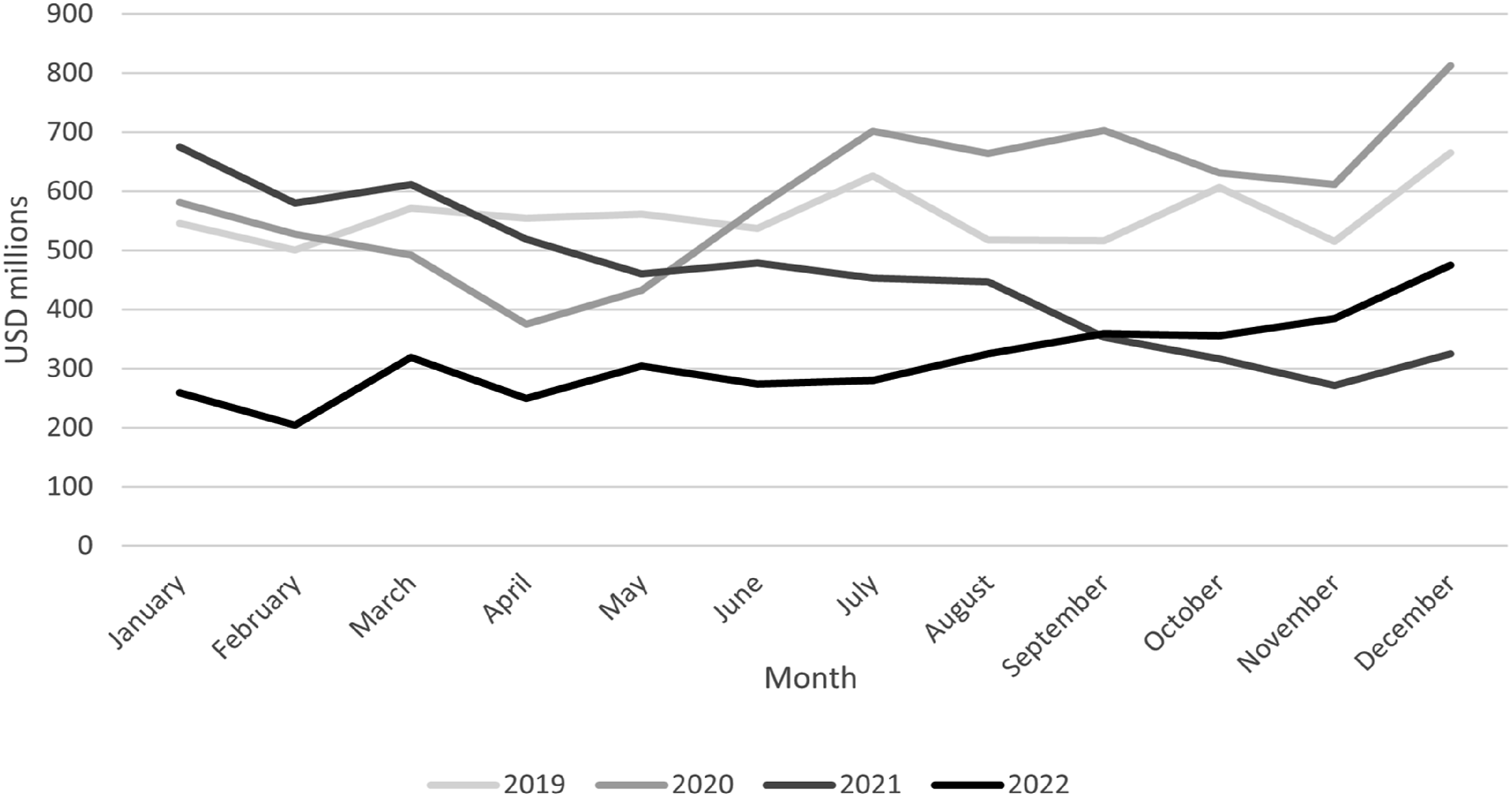

Yet, only five months after the record highs of December 2020, remittances to Sri Lanka began to collapse (see Figure 1). Monthly transfers began slumping in May 2021; by December, they were less than half of what was recorded the year prior. The implications of this precipitous collapse were not limited to the millions of migrant households that depend on foreign income transfers for their day-to-day survival. For decades, migrant workers’ aggregate income transfers have been the largest individual component of Sri Lanka’s current account balance (CBSL, 2023). Alongside lost tourism receipts throughout the pandemic (Karunarathne et al., 2021), declining remittances eroded Sri Lanka’s foreign exchange reserves, threatening the viability of a longstanding “soft peg” that defended the rupee to keep significant (and maturing) external debt obligations in check. In March 2022, with remittances continuing to stagnate and foreign exchange reserves all but depleted, the Central Bank of Sri Lanka (CBSL) was forced to float the rupee—triggering massive currency depreciation and straining external debt repayments. In May 2022, Sri Lanka defaulted on its foreign obligations for the first time, plunging the country into an economic crisis. Monthly remittance transfers to Sri Lanka in USD millions (2019 to 2022).

The macroeconomic shifts that transpired in Sri Lanka between 2020 and 2022 are hard to explain according to the conventional wisdom of “triple-win” migration. Since the mid-1990s, when migrant income transfers began outpacing Official Development Assistance (ODA) and Foreign Direct Investment (FDI) as the largest capital inflows for emerging economies, a pronouncedly “optimistic” appraisal of the developmental potential of remittances has emerged as a policy consensus (De Haas, 2012; Gamlen, 2014). The main thrust of the re-enlivened case for a migration-development nexus was that (temporary) labor migration could yield mutually beneficial outcomes for countries of destination and countries of origin, as well as migrant workers and their families. Despite the contentious nature of this prognosis (Chi, 2008; Ness, 2023; Withers, 2019), the bourgeoning growth of global remittances bolstered the notion that countries of origin benefit from the accumulation of foreign exchange earnings, while migrant households gain the opportunity to increase and diversify their income streams to mitigate risk and facilitate investments (World Bank, 2006). A less scrutinized claim is that these remittance flows are also resilient or counter-cyclical: That they remain stable or increase during all manner of crises and other times of hardship, whether at national or household scales.

Sirkeci et al. (2012: 30) summarize this position in the introduction to their edited volume on the resilience of remittances during the Global Financial Crisis (GFC): Remittances remain one of the less volatile sources of foreign exchange earnings for developing countries. The literature has indicated for some time that migrant remittances tend to be stable or even countercyclical in response to economic hardship—be it a financial crisis, natural disaster, or political conflict—in a remittance-recipient country.

Between these two very different crises are a number of inadequately explained interactions between Sri Lanka’s remittance economy and its real economy. Minimally, the crux of irresolution relates to the question of why remittances increased throughout 2020 (when the crippling effects of the pandemic were in full effect) and only began decreasing in mid-2021 (when many of the restrictions on foreign employment had begun easing). More significant, however, is the implication the scenario poses for the supposed resilience of remittance flows in the context of the migration-development debate. In attempting to disentangle patterns of remittance transfer into Sri Lanka between January 2020 and December 2022, I draw on CBSL data and an online remittance survey with migrant workers (n = 53) to suggest there is weak empirical support for remittance “resilience” in 2020 or a corresponding “collapse” in 2021. Instead, I propose that the principal explanation for fluctuations in recorded income transfers were shifts between formal and informal remittance channels. During the early stages of the pandemic, when lockdown measures inhibited informal remittance networks, migrant workers likely sent a greater share of income via formal channels—thus appearing to increase aggregate remittance inflows. Conversely, as various other factors placed strain on Sri Lanka’s increasingly untenable currency peg, available evidence suggests that many migrant workers switched to informal remittance channels offering better exchange rates, consequently eroding official remittance receipts and hastening the onset of a financial crisis. This observation, in turn, sustains a broader criticism of the conceptualization of remittances as resilient. Not only are crises varied in their characteristics and irreducible to simplistic relationships, but with formal remittances forming a significant share of foreign exchange receipts for emerging economies, sudden shifts to informal channels can pose a serious threat to macroeconomic stability.

Of course, Sri Lanka’s economic crisis had many other short-term triggers. Major strains emerged at the confluence of economic mismanagement (e.g., excessive borrowing, populist tax concessions, expansionary monetary policy, fertilizer bans and endemic corruption) and external pressures (e.g., predatory lending, declining tourism, the pandemic and the war in Ukraine). A full discussion of these issues is beyond the scope of this article, but also beside the point of the contribution: Which is to demonstrate that these factors are set against, and embedded within, a longer-term strategy of “migration instead of development” that—for Sri Lanka—appears to be a source of vulnerability rather than resilience.

Background: The dimensions of Sri Lanka’s remittance economy

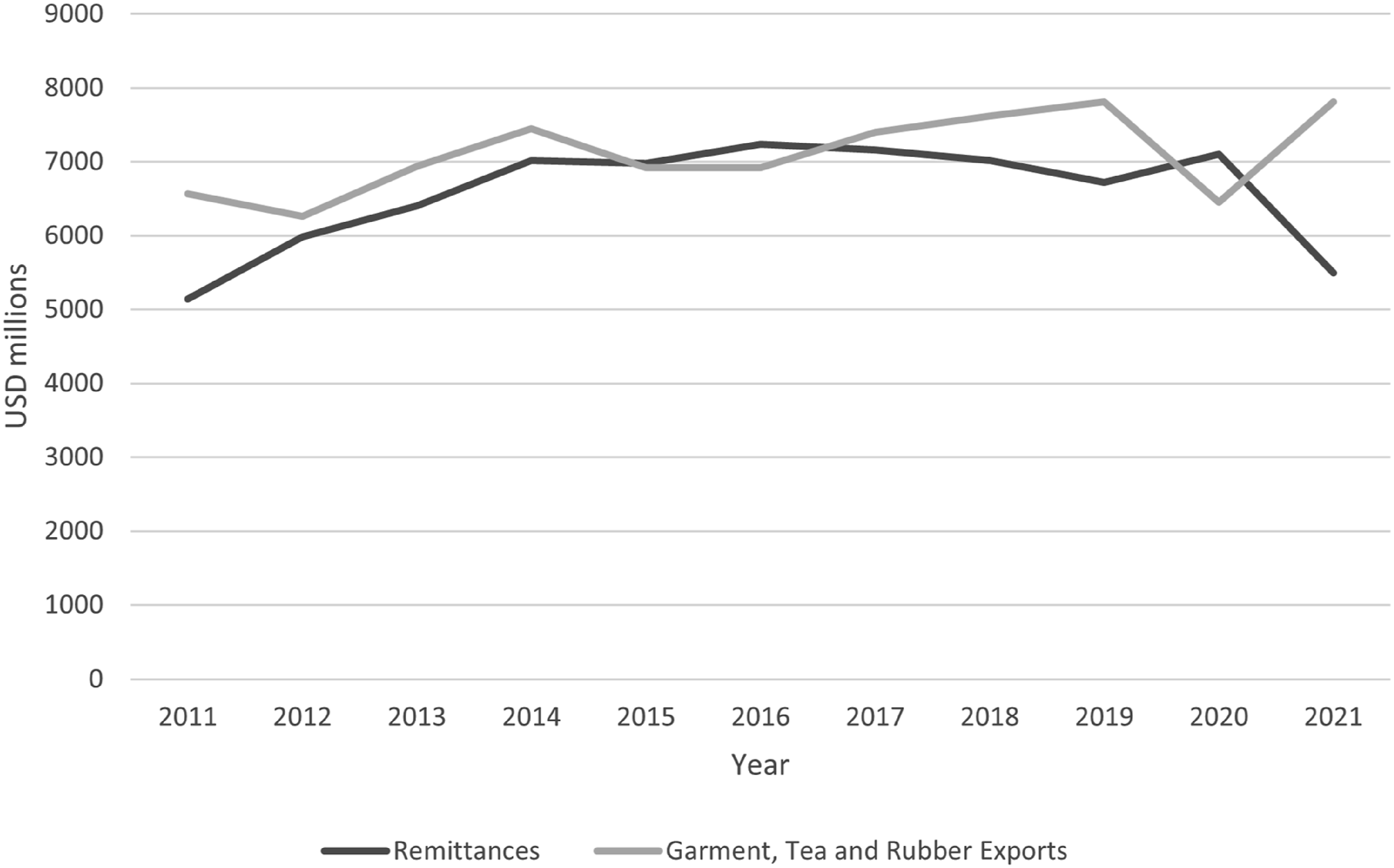

Sri Lanka recorded USD 6.7 billion in migrant workers’ personal income transfers in 2019—equivalent to 7.8 percent of gross domestic product (GDP) and 56 percent of export earnings for the same year (CBSL, 2023). Foreign exchange earnings from remittances also exceeded tourism receipts by USD 2.6 billion in 2018 even at the height of Sri Lanka’s tourism boon (CBSL, 2023). Likewise, remittances have kept pace with the combined earnings from the top three export industries (i.e., garments, tea and rubber) over the past decade (see Figure 2). Remittances versus garment, tea and rubber exports (2007 to 2021).

Approximately half of these remittances (51.5 percent) in 2019 (SLBFE, 2022a) were reported to have originated from migrant workers employed in West Asia, 1 who accounted for more than 87 percent of registered departures in 2019 and comprised the vast majority of Sri Lanka’s migrant workforce (SLBFE, 2022b). The latest statistics indicated there were a total of 1.9 million Sri Lankans employed in West Asia as of 2010, a figure equivalent to approximately 25 percent of the local workforce (SLBFE, 2012). The vast majority of these workers are employed in low-wage occupations classified as “low-skilled,” “semi-skilled,” “clerical,” “skilled” and “middle-level” by the Sri Lanka Bureau of Foreign Employment (SLBFE). However, the small share of higher-paid “professional” workers increased sharply from 1.8 to 4.9 percent five years before 2020 (SLBFE, 2022a). While women have historically accounted for a majority of departures, owing to the preponderance of employment opportunities for domestic workers, recent restrictions on the migration of women below particular ages and with young children have caused a reversal of this trend (Weeraratne, 2016). In 2019, women represented 39.8 percent of registered departures (SLBFE, 2022a). However, other women may have pursued irregular migration pathways to circumvent restrictions imposed by the (now annulled) Family Background Report (Arambepola, 2023; Joseph et al., 2022; Weeraratne, 2016).

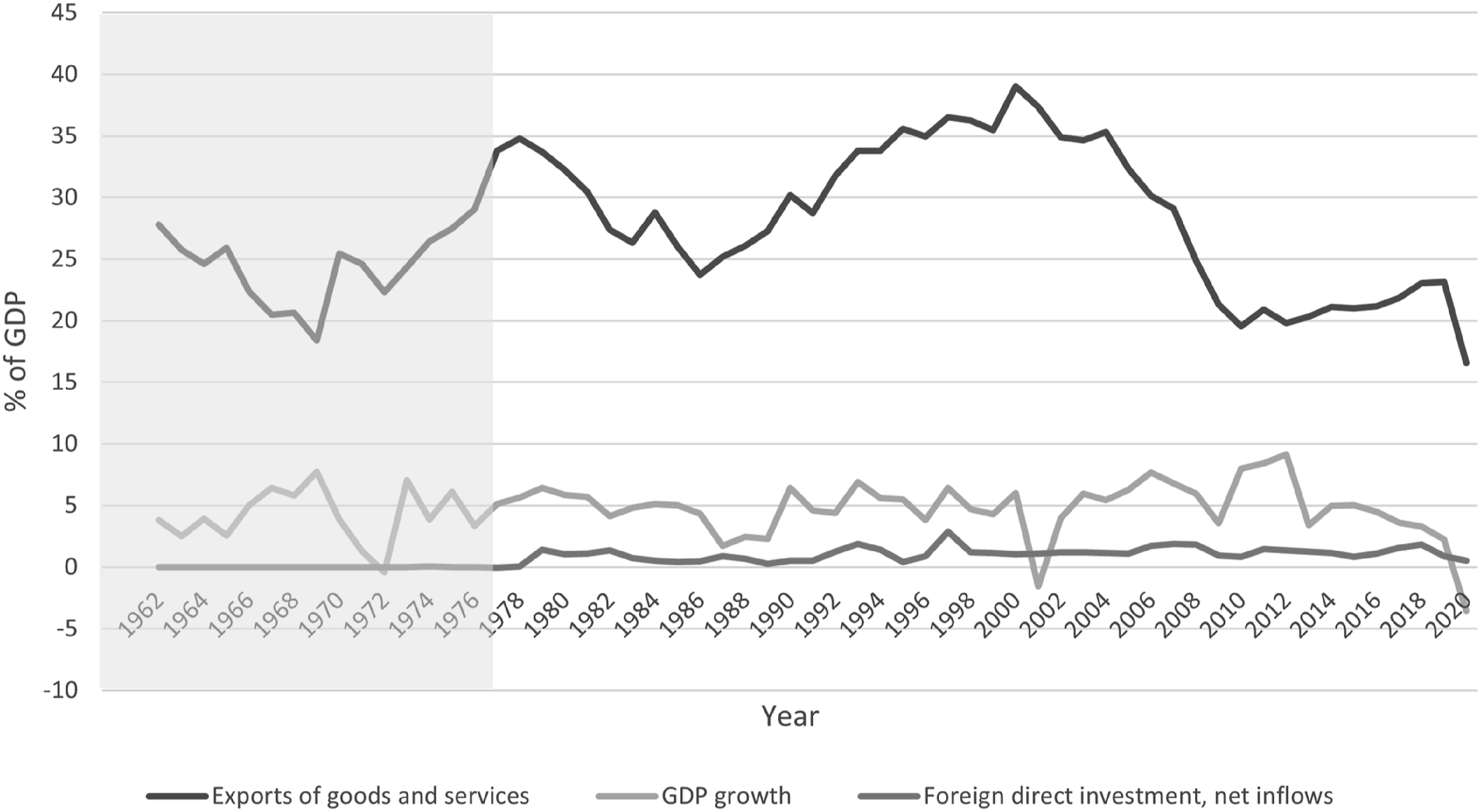

Like other major countries in South Asia, Sri Lanka began promoting temporary labor migration to meet burgeoning demand for low-wage labor within Gulf Cooperation Council (GCC) countries following the 1973 oil boom (Humphrey, 1991; Jain and Oommen, 2016). However, Sri Lanka was a relative latecomer to the Gulf labor market, having operated as a centrally-planned “closed economy” for much of the 1960s and 1970s (Kelegama, 2006). It was not until the 1977 election of the Jayawardene government that emigration policies were deregulated in step with a broader suite of liberalization reforms across the economy (Gamburd, 2000). Having famously declared, “Let the robber barons come!,” Jayewardene dismantled import controls, floated the currency, deregulated the banking system and reversed attempts to decentralize industry in favor of export processing zones for garment manufacturing (Kelegama, 2006). While limited FDI did arrive, GDP and export growth did not (see Figure 3). The garment sector gradually created a new stream of low value-added export revenue, but not enough to offset burgeoning imports or the economic repercussions of civil war (Kelegama, 2006). As of 2020, Sri Lanka’s export profile remains dominated by primary and low value-added goods with poor terms of trade (CBSL, 2023). GDP growth, exports and FDI (1962 to 2020).

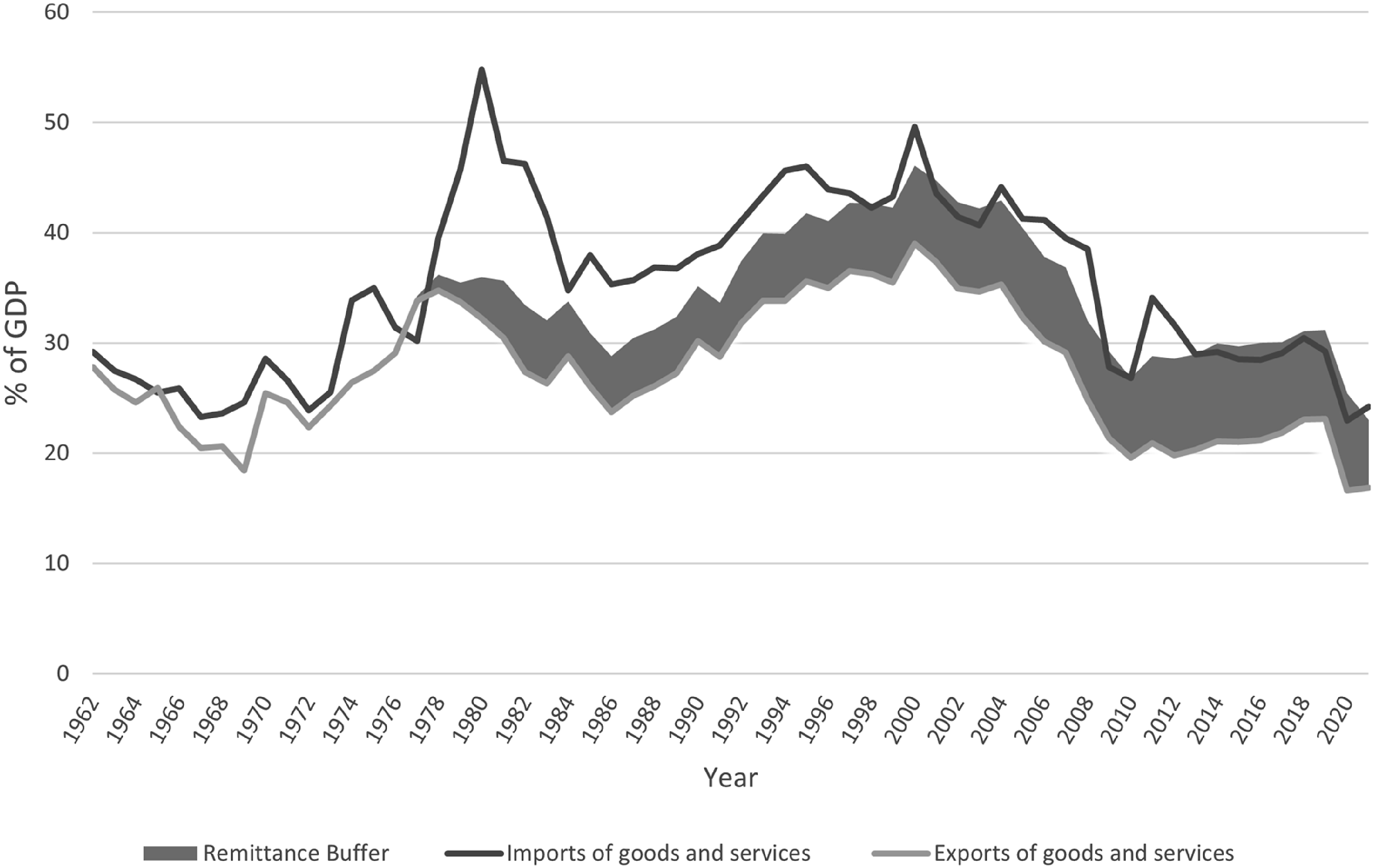

1977 marked the beginnings of Sri Lanka’s remittance economy, with low-wage migrant workers generating personal income transfers that provided a new avenue of foreign exchange earnings to cushion against the widening trade deficit of the “open economy” period (Withers, 2019). As I have argued elsewhere (Withers, 2019; Withers et al., 2022), temporary labor migration has since become a path-dependent feature of Sri Lanka’s economy. A persistent “remittance buffer”—conceived as the GDP value of remittances relative to the trade deficit (see Figure 4)—has, until recently, enabled the CBSL to periodically manage a soft peg to the United States (US) dollar. Defending the rupee in this manner has allowed Sri Lanka to finance imports and repay external debt obligations, providing relative macroeconomic stability underpinned by the export of unemployment and import of remittances. Yet, Sri Lanka’s economy also serves as a textbook case of “migration instead of development,” whereby migration has had a negligible (Barajas et al., 2009) or negative (Chami et al., 2018) effect on local processes of capital formation typically associated with economic development (Lewis, 1954). As several studies have observed, significant remittance inflows can result in a “Dutch disease” effect and cause currency appreciation that stymies the growth of export industries (Lartey et al., 2012; Roy and Dixon, 2016). A corollary of this lack of local industries in Sri Lanka is that household remittance expenditure—long known to be primarily directed toward everyday consumption, consumer durables and housing (De Silva et al., 1993)—generates multiplier effects that can stimulate imports and exert additional pressure on the exchange rate regime (Withers, 2019). Continued migration and growing remittances are required to sustain such a macroeconomic balancing act. Imports, exports and remittances (1962 to 2021).

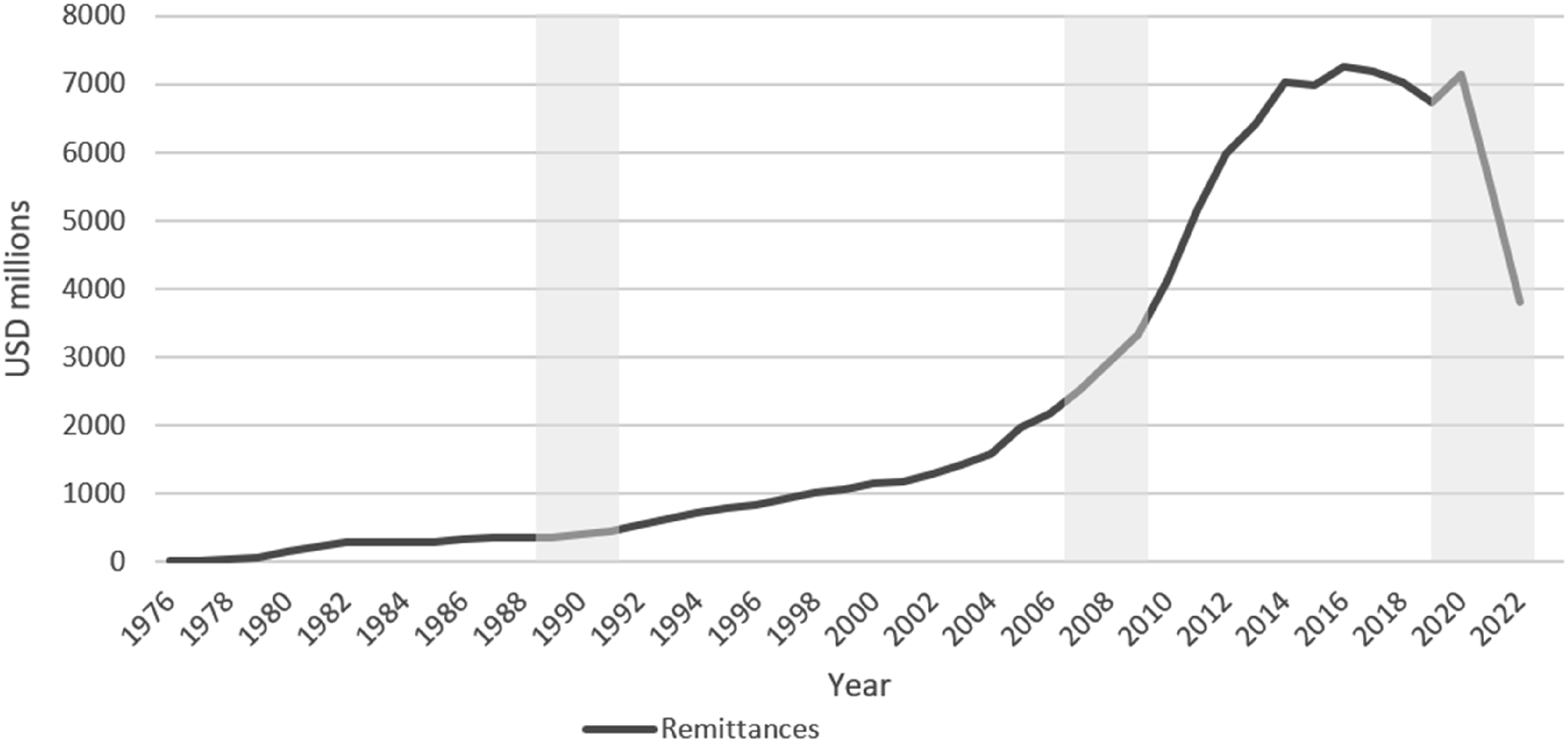

Crises and shocks that affect patterns of migration and remittance are thus key considerations for Sri Lanka’s macroeconomy. The international literature addressing the resilience of remittance flows has largely discussed “crises” affecting countries of origin. For example, natural disasters or economic downturns might prompt migrants to remit additional income to help their families and communities at home (Sirkeci et al., 2012). Empirical studies have been fairly unequivocal in suggesting that remittances have countercyclical characteristics under such circumstances (Frankel, 2009; Kapur, 2004; Yang, 2008), acting as an “automatic stabilizer” that can complement a fixed or tightly managed exchange rate regime by compensating for some of the monetary policy autonomy otherwise forgone by a currency peg (Singer, 2010). However, “crises” take on various forms, including exogenous shocks that disproportionally affect countries of destination or are global in their proportions. Prior to the COVID-19 pandemic, Sri Lanka’s remittance economy experienced two such shocks: The Gulf War (Humphrey, 1991) and the GFC (Rajan and Narayana, 2012). However, in neither case did remittances meaningfully decline (see Figure 5). While mass repatriations following Iraq’s invasion of Kuwait in 1990 significantly reduced the stock of Sri Lanka’s migrant workforce, this disruption was temporary and followed by a redoubling of recruitment as the cessation of conflict in 1991 brought renewed military and infrastructural investment (Addleton, 1991; Wickramasekara, 1993). Meanwhile, the strong demand for oil insulated the GCC countries from the worst of the GFC, resulting in a milder downturn and a quicker return to growth. Less than three percent of Sri Lankan migrants lost their jobs, the overall departures of migrants actually increased between 2007 and 2009, and remittance flows were largely unaffected (Rajan and Narayana, 2012). Remittances (1976 to 2022).

In short, there were circumstantial factors associated with the GCC countries that explain the stability of remittance transfers to Sri Lanka during previous regional and global crises. By contrast, the disruptions posed by the COVID-19 pandemic were altogether more pervasive and more persistent, eventually placing unprecedented strain on Sri Lanka’s managed exchange rate regime with dwindling reserves available for expansionary domestic policies, for financing imports amid a widening trade deficit and for the repayment of international loans (Tennekoon, 2022). However, the seemingly counter-intuitive timing of the “rise and fall” of Sri Lanka’s remittance receipts throughout the pandemic confounds the conventional explanations of remittance resilience and instead points to a fundamental vulnerability for developing countries that are reliant on remittances to defend an otherwise untenable currency peg.

Analysis: COVID-19 and the destabilization of Sri Lanka’s remittance economy

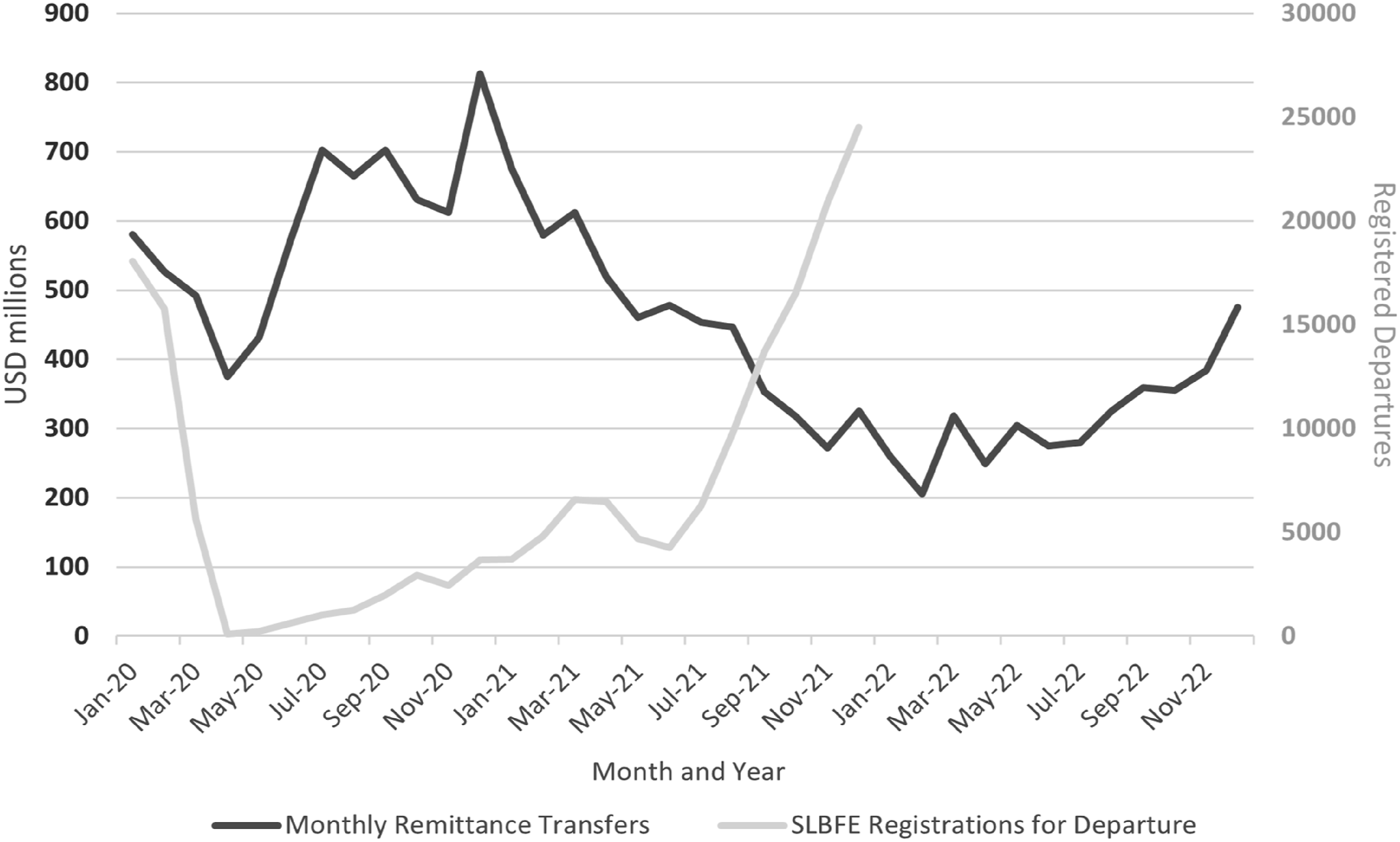

At its outset, the COVID-19 pandemic seemed likely to destabilize Sri Lanka’s remittance economy. The GCC countries where most Sri Lankan migrant workers were employed were quick to implement border closures and lockdown measures. New migrant departures came to a standstill, contracts were suspended and jobs were lost; by May 2020, thousands of workers began returning on repatriation flights (Weeraratne, 2021a). In short, the effective stock of migrant workers in the Gulf, the most significant determinant of bilateral remittance flows (Kim et al., 2022), was greatly reduced. World Bank economists foreshadowed this eventuality, cautioning in April 2020 that South Asia would experience a 22.1 percent decline in remittance transfers (Ratha et al., 2020a). Yet Sri Lanka, and many other migration-dependent economies of the Global South, continued to record significant remittance inflows. By October 2020, the World Bank revised its regional estimate for South Asia to a far more moderate 3.6 percent reduction (Ratha et al., 2020b); by the year-end, Sri Lanka had defied this expectation, posting an annual increase in remittances despite a clear reduction in migrant departures (see Figure 6). Migrant departures versus remittance transfers (2020 to 2022).

Based on migrant income transfers recorded in 2020, remittances seemed resilient in responding to the crisis. World Bank economists embraced this view in the aforementioned October 2020 report (Ratha et al., 2020b) and again, more emphatically, in the May 2021 edition of the Migration and Development Brief—the title of which was “Resilience: COVID-19 Crisis Through a Migration Lens” (Ratha et al., 2021). Meanwhile, an International Monetary Fund (IMF) working paper published shortly after provided an early analysis of global remittance flows in 2020 and likewise concluded that such flows had “defied the odds” and confirmed their role as an “automatic stabilizer” (Kpodar et al., 2021: 24). At global and regional levels, this verdict is hard to dispute: While remittance flows to low- and middle-income countries contracted by 0.8 percent in 2020, they increased to 10.2 percent in 2021 and continued to grow by an estimated 4.9 percent in 2022 (Ratha et al., 2022). However, this was not the case in Sri Lanka, where remittance flows began to falter throughout 2021—despite increasing migrant departures 2 (see Figure 6) alongside the intensification of local needs arising from escalating COVID-19 cases (WHO, n.d.) and deepening economic problems (Weerakoon, 2021a, 2021b) over the same period. According to the most vocal proponents of the resilient remittance hypothesis, these are exactly the kinds of circumstances that should spur a countercyclical increase in the transfer of “dollars wrapped with care” (Ratha, 2014).

What, then, best explains the fluctuations seen in Sri Lanka’s remittance economy between January 2020 and December 2022? Before interrogating the two anomalous phases—that is, the increase of remittances as migrant stock diminished in 2020, and the decline of remittances as migrant stock rebounded in 2021 and 2022—it is worth revisiting the arguments supporting the idea of remittance resilience. Sirkeci et al. (2012) summarize below six key factors observed during and after the GFC: 1. Migration patterns that span multiple countries and regions of destination diversify sources of remittances and hedge against location-specific shocks, increasing their resilience. 2. Remittances are strongly related to migrant stock (i.e., the total number of established migrants) and are not overly susceptible to disruptions to migrant flow (i.e., recent departures and arrivals). 3. Migrant populations can be averse to returning home, even when faced with job losses, and find means of remaining and working in countries of destination—even on an irregular basis. 4. Migrant populations often absorb income shocks during crises, reducing their own consumption in order to maximize remittances. 5. If migrant populations do return home, they tend to bring savings with them, which are recorded as remittances in cases where this entails formal income transfers from non-residents to residents. 6. Currency depreciation in remittance-receiving countries can produce a “sale” effect on remittance behavior. The cost of goods, services and assets in the home country become significantly cheaper for migrants earning foreign currency and thus attract greater inflow.

Several of the factors described above were nominally applicable to Sri Lanka between 2020 and 2022. Sri Lanka has diverse migration patterns within and beyond the GCC countries (factor 1), representing a significant “migrant stock” beyond those whose mobility was disrupted by the pandemic (factor 2) (UN, 2020). While a significant number of workers were repatriated in 2020, the great majority remained abroad (factor 3) and continued to send remittances (factor 4) (Weeraratne, 2021a). However, noting that low-wage migration to the Gulf has been characterized as “survival migration” in which workers regularly remit the majority of their pay (Eversole and Shaw, 2010), it is unlikely that there was any significant increase in formal remittance resulting from the savings of repatriated workers (factor 5). Sri Lanka maintained a stable currency peg throughout 2020 and when depreciation did eventually occur in early 2022, it was not accompanied by a surge in remittances, as CBSL data reveals (factor 6).

The rise: May 2020 to April 2021

The Government of Sri Lanka responded promptly to the pandemic, having assembled a National Action Committee for COVID-19 on 26 January 2020, a day before the country’s first confirmed case was reported (Amaratunga et al., 2020). Travel restrictions and quarantine measures were implemented from 28 January, with stringent social distancing and curfew policies following shortly thereafter: While the authoritarian nature of the response attracted criticism, the efficacy of these measures in containing the initial outbreak has also been praised (Amaratunga et al., 2020). Infection rates remained relatively low throughout 2020. Although the underlying social and economic preparedness was lacking, the government implemented broad cash transfer schemes to support the welfare of poorer households (Kidd et al., 2020). With the unilateral closure of international borders on 22 March, and parallel restrictions in major countries of destination for Sri Lankan migrant workers, migration flows also stopped except for the government-chartered repatriation flights for workers who had lost employment abroad (Weeraratne, 2021a). The loss of income and jobs for migrant workers in the GCC countries during the pandemic was widespread: The equivalent of 11 million full-time jobs were lost across the region in the first half of 2020 (ILO, 2020), affecting hundreds of thousands of South Asian workers in the first few months of the pandemic (Tazyeen et al., 2022). The combined effect of these domestic and international settings was a reduction in the stock of migrant workers in the Gulf while Sri Lanka weathered a comparatively “mild” public health crisis. Despite reduced capacity to transfer more income from abroad, and without an acute need to send more income home, monthly remittances to Sri Lanka only declined in March and April before making a swift recovery and increasing to record-breaking levels by the year-end (CBSL, 2023).

Some explanatory factors outlined by Sirkeci et al. (2012) may be relevant but are not corroborated by available data. Sri Lanka’s extensive migration ties to wealthy Global North countries, where social protection measures shielded many workers from lost income, could imply a shift in the origin of remittances from low-wage temporary migrant workers in GCC countries to more “altruistic” transfers from established diaspora groups (Weeraratne, 2020). However, this scenario is not supported by recent SLBFE (2022a) statistics, which report only a marginal increase in the share of remittances from Europe (0.2 percent) and North America (0.1 percent), alongside a slight decrease from Australia and New Zealand (0.1 percent combined). Similarly, a focus on cumulative migrant “stock” rather than “flows” might partly explain the resilience of remittances in the face of declining departures, but less so in relation to migrant workers in GCC countries, where local labor laws mandate short-term contracts that necessitate the frequent circulation of workers between home and host countries.

In lieu of adequate explanations, Sri Lankan policy experts have suggested a range of additional factors specific to the particularity of the COVID-19 crisis that might better explain the unexpectedly buoyant remittance economy (Weeraratne, 2021a). One consideration, borne out of survey data collected by Weeraratne (2021b), is that the lockdown measures in GCC countries disrupted “physical” remittance methods (e.g., sending money by visiting remittance transfer services)—causing a backlog of unsent remittances in March and April, resulting in additional transfers throughout May and June. However, Weeraratne (2021b) indicates that this does not explain the increase in remittances throughout the year and instead suggests other possible factors. These include an increase in transfers from less frequent remitters outside the GCC countries (again, not supported by SLBFE data), “bumper” remittances from existing savings and termination pay-outs, or the movement of remittances from informal channels that depend on in-person transactions—as with the Undiyal or Hawala systems 3 —into more accessible formal channels, like online banking (Weeraratne, 2021a).

The idea that public health measures imposed during the early stages of the pandemic inhibited in-person transactions and caused remittances to move from informal to formal channels is a particularly plausible explanation. Official remittance data only reflects the formal component of income transfers, such as those sent through bank transfers or remittance transfer services like Western Union and Moneygram. It has long been known that there are substantial informal remittance flows operating in parallel with most major formal remittance channels (Sirkeci et al., 2012), though there have been persistent problems in quantifying the volume of so-called “shadow remittances” sent via Undiyal-type transactions, in-kind or carried in-person (Kpodar et al., 2021). The standard practice in economic modeling approaches is to “rely on errors and omissions in the balance of payments to gauge a shift of informal remittances to formal channels” (Kpodar et al., 2021: 19), but this approach has been notoriously unreliable (El Qorchi et al., 2003). In search of a better proxy measure, Kpodar et al. (2021) took advantage of fluctuations in passenger air traffic during the pandemic to test the hypothesis that the ratio of formal to informal remittances increases when physical travel (i.e., a single medium of informal remittance) is disrupted. They found a positive association across 52 countries, reporting that “a complete shutdown of passenger air traffic […] would lead to an increase in formal remittance inflows by about 10 percentage points within the first two months” (Kpodar et al., 2021: 19) and caution that in this event, “remittance flows do not necessarily increase; rather the flows are better captured in official statistics” (Kpodar et al., 2021: 20). Given that disruptions to air traffic are most likely to affect in-person and in-kind transfers, rather than Undiyal-type transactions that might also have been affected by physical distancing measures, the reported effect was likely a conservative estimate.

The fall: May 2021 to December 2022

More confusing is the sudden decline in remittance transfers to Sri Lanka that began in May 2021. Total remittances fell by 22.7 percent year-on-year in 2021 and a further 30.9 percent in 2022, culminating in the lowest annual figures since the end of the Sri Lankan Civil War in 2009 (CBSL, 2023). Thus, the factors discussed by Sirkeci et al. (2012) provide little explanatory value in this context. Remittances steadily and persistently declined at a time when migrant departures were rising alongside intensifying local needs amid spiking COVID-19 cases (WHO, n.d.) and food shortages (Weerakoon, 2021b).

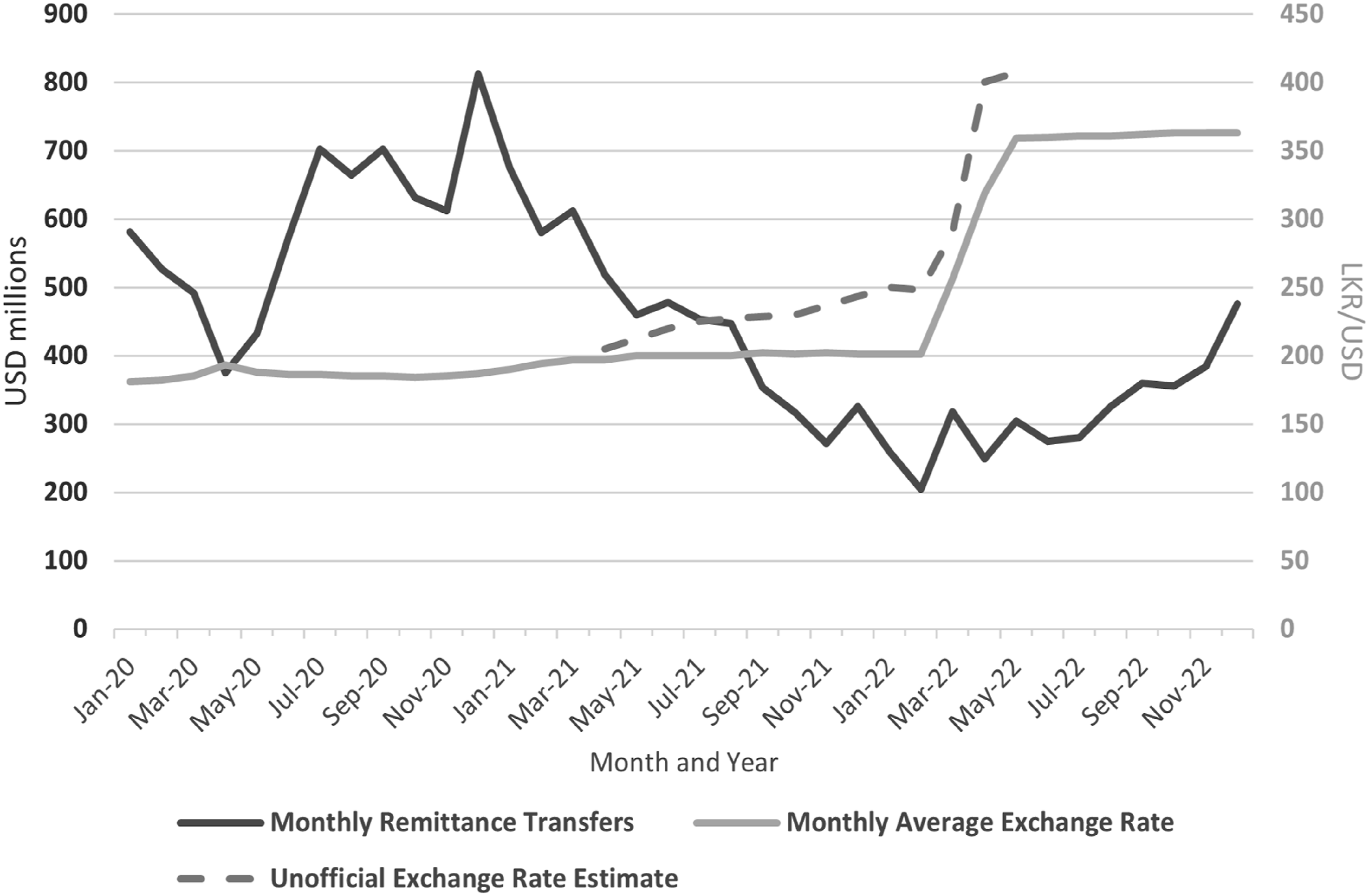

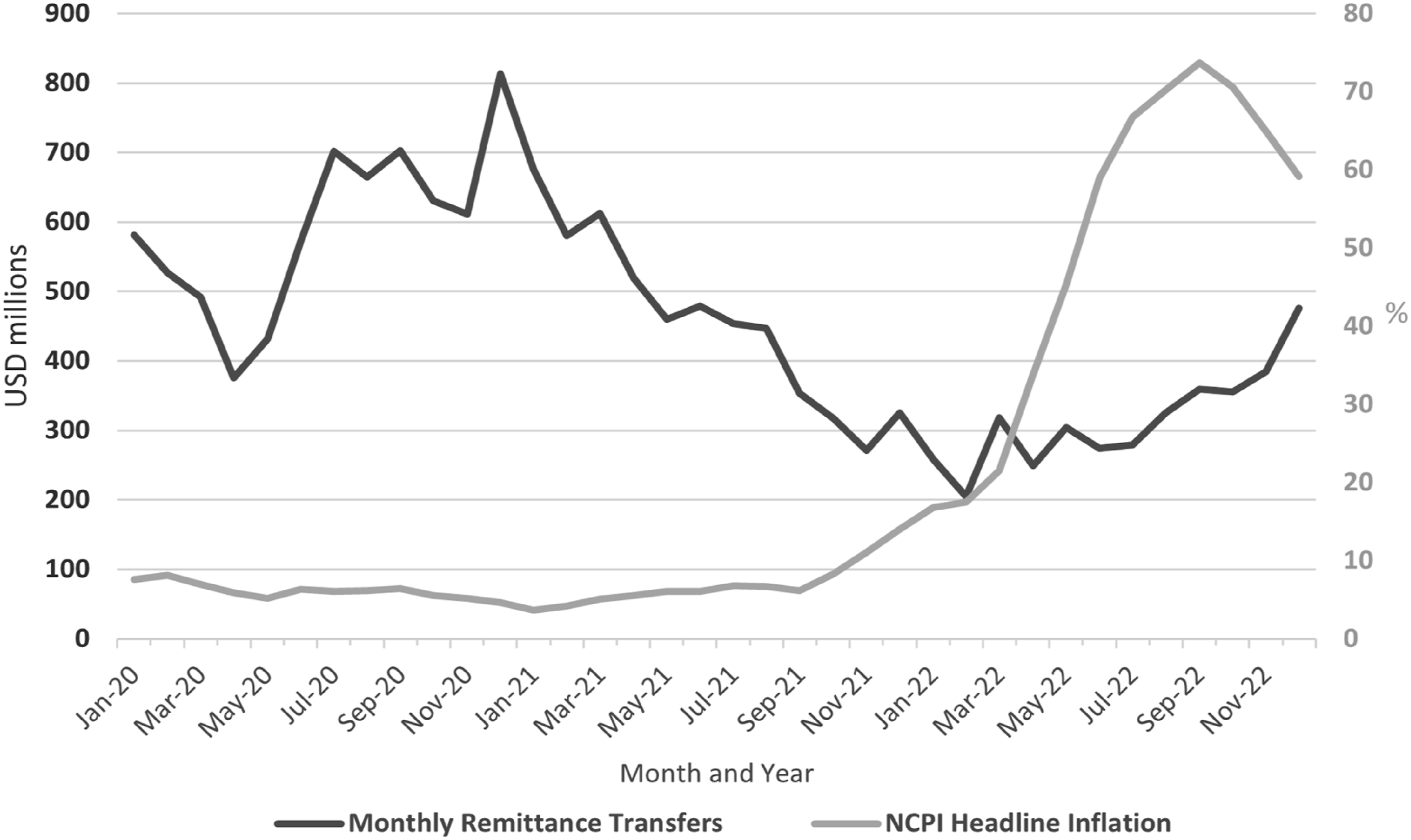

With foreign exchange reserves dwindling, the exchange rate was finally allowed to float in March 2022, triggering massive currency depreciation—but without a corresponding injection of remittances from migrant workers seeking to capitalize on “sale” pricing (Sirkeci et al., 2012). Instead, remittances continued to falter as the exchange rate depreciated (see Figure 7). Though remittances are more often discussed as a cause of inflation (Roy and Dixon, 2016), it has also been suggested that the financial hardships associated with rising inflation can be a trigger for increased remittances (Sirkeci et al., 2012): Sri Lanka had runaway inflation by the end of 2021, but this appears to have had no discernible impact on remittances either (see Figure 8). Again, local analysts looked for other explanations to explain the trend, and again the role of the informal remittance economy came to the fore (Weeraratne, 2021b). Notably, while the official Sri Lankan rupee (LKR) or USD exchange rate was maintained at a relatively stable peg throughout 2021 and the start of 2022, the diminished availability of USD prevented exchange from occurring at these rates in practice—prompting a decoupling between official and “gray” or “black” market exchange rates (Weeraratne, 2021b). Remittance transfers versus exchange rate (2020 to 2022). Remittances transfers versus inflation rate (2020 to 2022).

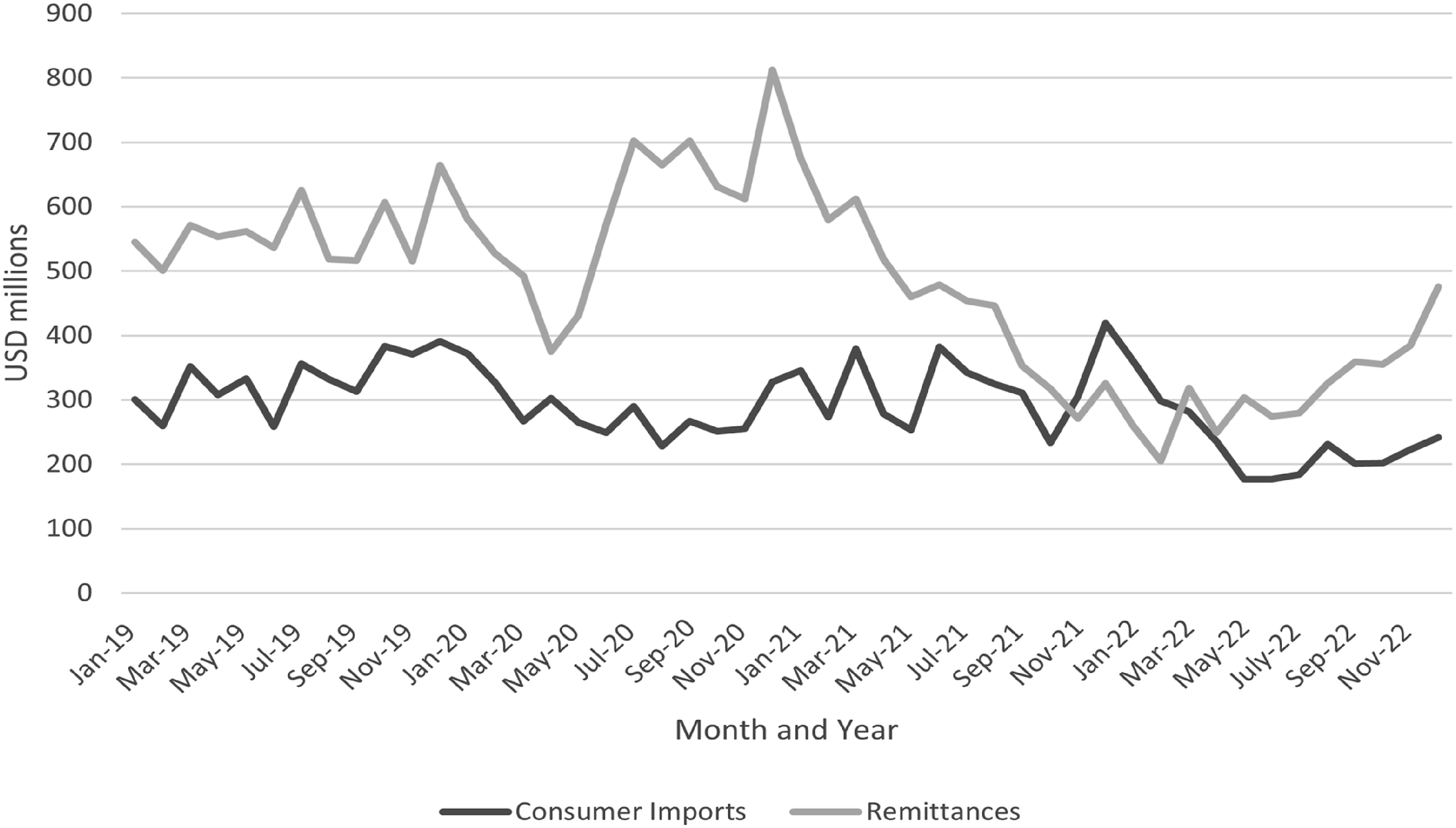

Using kerb market rates reported in various Sri Lankan media outlets between April 2021 and May 2022 (Economy Next, 2021a, 2021b, 2021c, 2022; Jayasinghe, 2021a, 2021b; Weeraratne, 2021b; Wijewardena, 2022) allows for estimates of the unofficial exchange rate that prevailed throughout that period (see Figure 7). Apparently, in the context of dwindling supplies of USD, de facto currency depreciation began much earlier than official exchange rates would indicate. Furthermore, it was reported that unauthorized money exchanges were offering the most attractive rates for remitting migrant workers which, coupled with confusion generated by the CBSL’s introduction of several mandatory conversion policies intended to capture foreign currency, may have prompted a general shift toward informal remittance channels (Weeraratne, 2021b). Ajith Nivard Cabraal, then Governor of the Central Bank, was explicit in attributing declining remittances to the presumed growth in informal cash transfers via the Undiyal system (Jayasinghe, 2021a). This possibility is supported by the observation that it was only after the rupee was floated in March 2022—effectively mitigating the discrepancy between official and unofficial exchange rates—that remittances slowly began to recover (see Figure 7). Likewise, consumer goods imports, which are strongly linked to household remittance expenditure (Phillips, 2009), remained relatively stable as recorded personal income transfers began declining in 2021, suggesting the presence of informal remittance flows to sustain this consumption (see Figure 9). It is only after the exchange rate floated and imports became costlier that consumer goods imports meaningfully declined. Just as the supposed increase in remittances during 2020 might best be explained by the “formalization” of remittance flows, so too might the apparent decline in remittances during 2021 and 2022 be explained by a subsequent phase of “informalization” during the beginnings of the foreign exchange market (forex) crisis. Remittance transfers versus consumer goods imports (2019 to 2022).

Online survey findings

A short online survey was used to explore the possibility that remittance transfers shifted between formal and informal channels during Sri Lanka’s protracted crisis, and to examine other characteristics relating to remittance decisions over that period. The survey was limited to high-skilled migrant workers of Sri Lankan origin who were primarily located within a GCC country between 2020 and 2022. A research assistant based in Qatar distributed the survey via email and social media channels over a three-week period in February 2023, resulting in 53 valid responses from workers located in Qatar, Dubai, Oman and the UAE (incomplete responses and those not satisfying sampling criteria were omitted from analysis). The survey was limited to closed-ended questions relating to workers’ location, occupation and patterns of remittance; no identifying or sensitive information was collected, in adherence with the Qatar Institutional Review Board’s guidelines for low-risk research.

Confining the sample to workers in GCC countries reflects the enduring significance of the region as a source of remittances to Sri Lanka (SLBFE, 2022a), while the inclusion criteria relating to highly-skilled workers was a practical concession to administering an online survey (i.e., by targeting workers with a higher likelihood of computer ownership and financial literacy). Nonetheless, this group of workers accounted for only 6.9 percent of registered migrant departures in 2021 (SLBFE, 2022b) and represented a distinct minority of Sri Lankan temporary migrant workers in the Gulf. Their remittance decisions were likely to differ from lower-waged migrant workers. Thus, the survey findings were only indicative of this particular sub-population. Despite these limitations, the absence of reliable data pertaining to informal remittance channels makes the survey a valuable instrument for gauging the factors that explain broader patterns in remittance behavior.

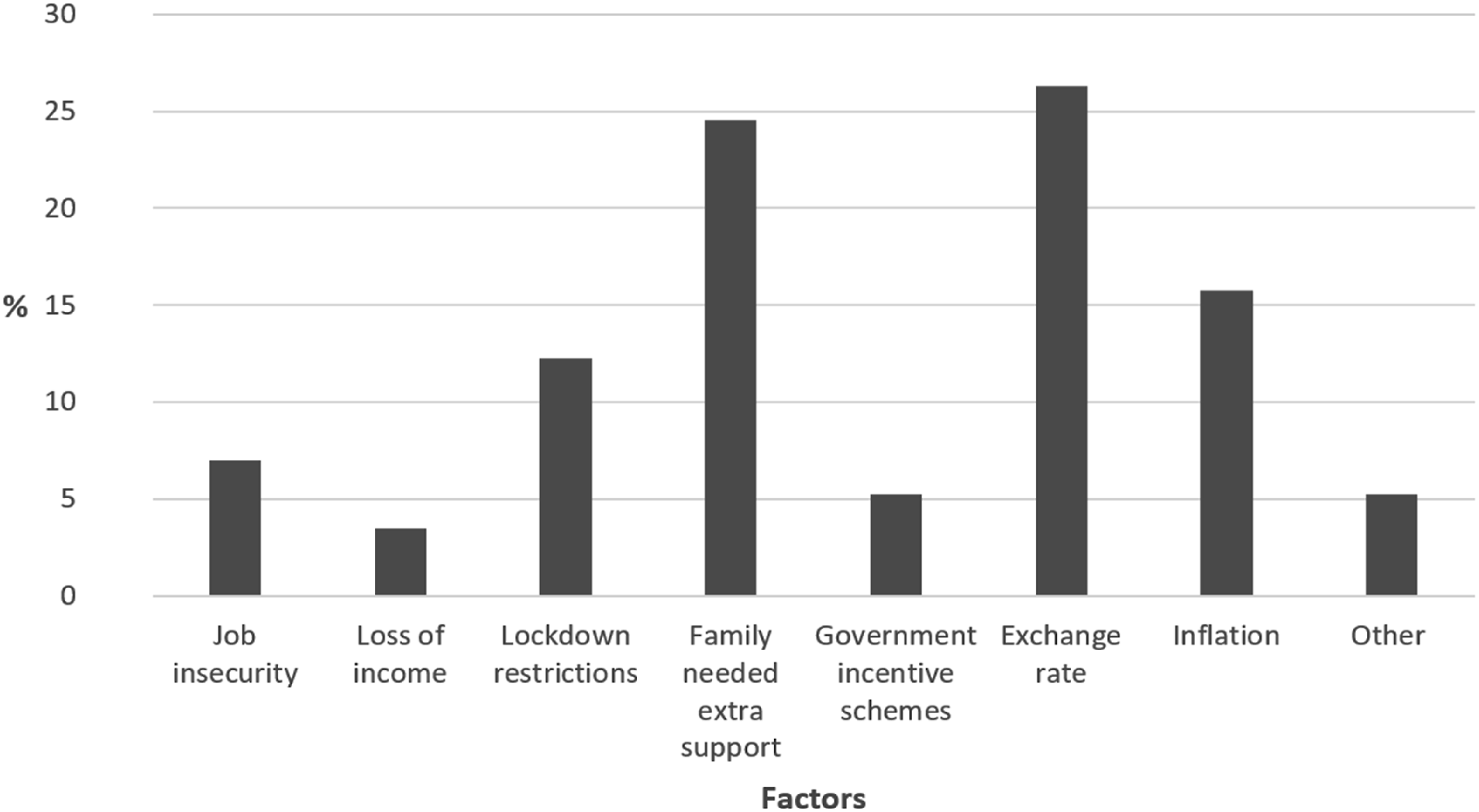

Findings revealed that 86.7 percent of respondents sent remittances to Sri Lanka between 2020 and 2022. The amount and frequency of these income transfers varied for 77.8 percent of the cases. Half of the respondents (50 percent) reported sending less, about a quarter (27.5 percent) reported sending the same, while some (12.5 percent) were unsure and a few (10 percent) reported sending more than they did prior to the COVID-19 pandemic. When asked what factors influenced decisions or ability to remit during this period (see Figure 10), considerations relating to the exchange rate (26.3 percent) emerged as the most frequent explanation—ahead of additional support for family (24.6 percent) and inflation (15.8 percent). Factors influencing decision or ability to remit (2020 to 2022).

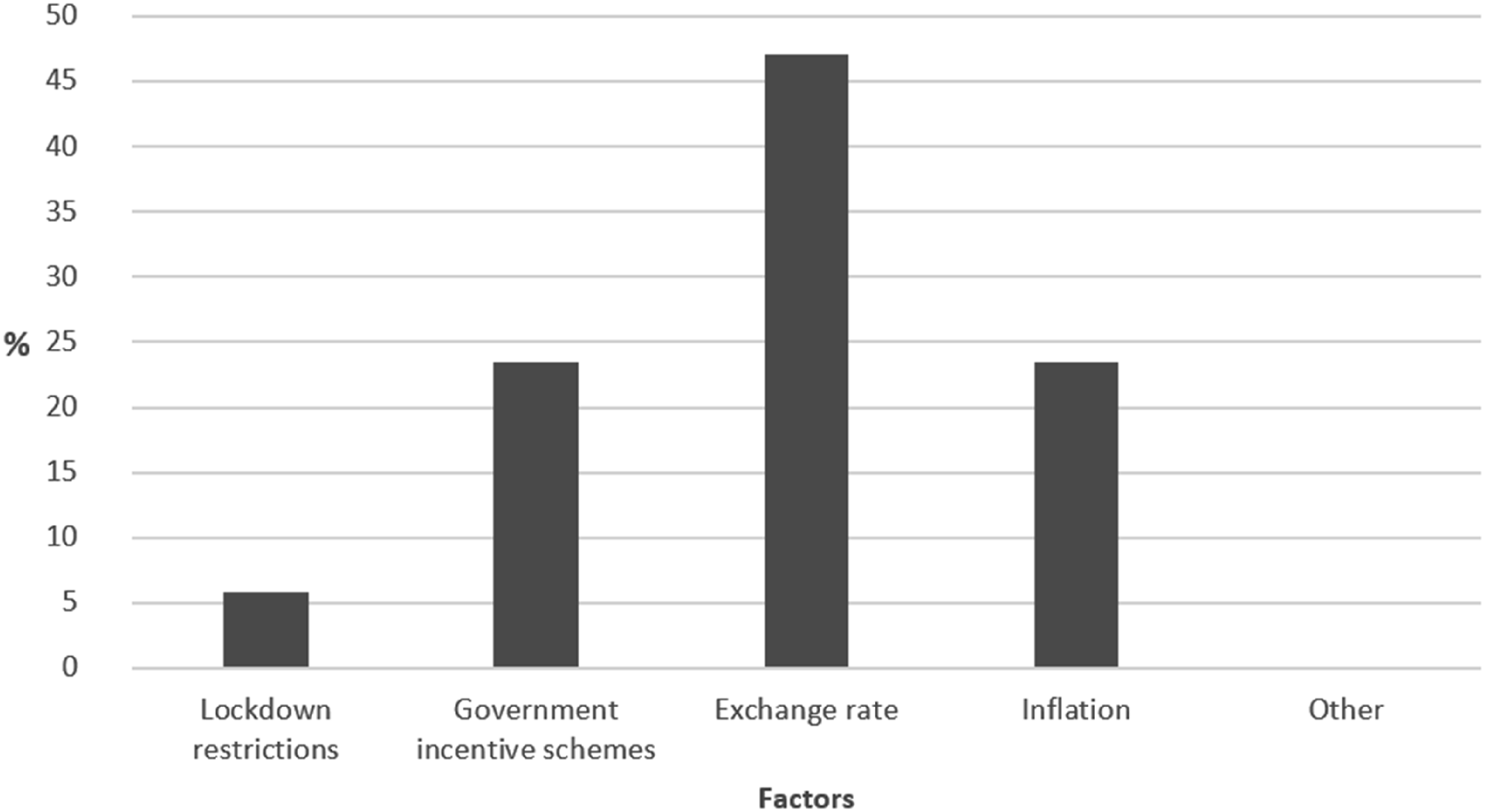

Queried about whether they switched between formal and informal remittance channels, the majority of the respondents (79 percent) reported that they only used formal remittance channels, while the remainder (18.6 percent) reported changing between formal and informal methods or only using informal remittance methods (2.3 percent). Those who switched between remittance channels were prompted to identify factors that shaped that decision (see Figure 11), with the exchange rate again emerging as the dominant factor (47 percent). Factors influencing decisions to switch between formal and informal remittances (2020 to 2022).

While far from conclusive given the limitations of the survey, these findings do offer some clues about remittance patterns among highly-skilled Sri Lankan temporary migrant workers in the Gulf—namely, the overall reduction in remittances between 2020 and 2022, the prominence of exchange rate variation as a factor influencing decisions to remit, and a notable degree of switching between formal and informal channels of remittances. These findings support the idea that personal income transfers declined while Sri Lanka faced crises, contrary to the resilience narrative. Moreover, the results highlighted how complicated interactions between formal and informal elements of the economy defied any simplistic assumptions about the stabilizing effect of remittances.

Further research addressing the remittance characteristics of lower-waged migrant workers during the COVID-19 pandemic would greatly extend these cursory insights. The need is particularly pressing because highly-skilled migrants, like those who responded to the survey, were likely from wealthier households and earned higher wages—perhaps allowing for a broader range of financial decision-making relative to the constraints endured by low-income migrant households that often straddle the poverty line (Ekanayake and Amirthalingam, 2023). Indeed, anecdotal evidence reported in Sri Lanka media suggests that low-wage migrant workers were those most likely to use Undiyal services as the forex crisis matured, both to maximize exchange rates and to bypass Sri Lanka’s increasingly bureaucratic attempts to attract formal remittances (Thomas, 2022).

Concluding discussion: The myth of “resilient” remittances

The prognoses of “triple win” migration suggest that extensive integration with foreign labor markets and substantial remittance flows should be a source of macroeconomic stability during crises. Sri Lanka’s experience during the COVID-19 pandemic and subsequent forex crisis suggested otherwise. Remittances decreased steadily as Sri Lanka’s economic problems worsened, contrary to the depiction of remittances as resilient or countercyclical capital inflows that respond positively to “financial crisis, natural disaster, or political conflict” (Sirkeci et al., 2012: 2). A closer inspection of recently published CBSL data reveals that general sources of resilience identified during the GFC offered little explanation for the fluctuations in Sri Lanka’s remittance inflows. Instead, by demonstrating a strong correlation with the decoupling of official and unofficial exchange rates, available data supported the possibility that changes in net remittance volume were secondary to the informalization of income transfers in response to Sri Lanka’s untenable currency peg. Online survey data with highly-skilled migrant workers based in the Gulf between 2020 and 2022 further supported the hypothesis that better exchange rates prompted some to switch from formal to informal remittance channels. These findings were limited by the availability of migration and remittance data in Sri Lanka—including updated estimates of total migrant stock, the lack of country-disaggregated remittance figures, a lingering dearth of studies examining worker and household remittance behavior, and the difficulty of disentangling the many confounding factors that contributed to the eventual economic crisis. The important function of differing exchange rate regimes within remittance-dependent economies is regrettably beyond the scope of this analysis, but a promising topic for future research. Notwithstanding these considerations, the apparent decline in remittances was certainly fundamental to the crisis given their hitherto central role in maintaining Sri Lanka’s macroeconomic stability.

Sri Lanka’s experience during the COVID-19 pandemic may be exceptional in some respects, but offers a stark reminder that there is no empirical consensus to assert that remittances are fundamentally imbued with resilient or countercyclical properties. Despite the frequency with which this claim is made by World Bank economists (Page and Plaza, 2006; Ratha et al., 2008; Ratha et al., 2021; Sirkeci et al., 2012), there is little consensus among econometric studies testing the cyclicality of remittances during downturns. While recent economic modeling suggests that bilateral remittance flows to developing countries across Asia between 2008 and 2018 were generally countercyclical, these findings varied significantly by sub-region: Being “acyclical” or “procyclical” in 40 percent of cases in South Asia, 45 percent of cases in East Asia and in 55 percent of cases across the Pacific (Kim et al., 2022). While some earlier studies concluded that migrant income transfers were countercyclical (Chami et al., 2009; Frankel, 2009), other studies—including panel analyses of 100 countries from 1975 to 2002 (Giuliano and Ruiz-Arranz, 2009) and 116 countries from 1970 to 2007 (Cooray and Mallick, 2013)—found remittances decreased during periods of volatility in home countries. Although the resilience narrative appears to have gained standing in the aftermath of the GFC, when the focus shifted to the stability of (increasingly sizeable) remittance flows during systemic global economic shocks, the evidence is again patchy. Several studies have shown that remittances were less volatile than other capital flows during the GFC (Ratha et al., 2008) and, in regions like South Asia, increased substantially (Rajan and Narayana, 2012). Nonetheless, other regions reported significant declines in remittances during the crisis (Danzer and Ivaschenko, 2010), suggesting that large remittance channels can transmit exogenous shocks to receiving economies (Abdih et al., 2012) and heighten exposure to risk (Barajas et al., 2010). The potential for remittances to rapidly shift between formal and informal channels in response to exchange rates and other situational factors further complicates the collective ambivalence of these studies.

These findings have a bearing on the migration-development debate more broadly. Migration-development “optimists” frequently refer to the under-reporting of remittances due to the volume of informal transfers that elude capture within official statistics (Sirkeci et al., 2012), but appear to have given little consideration to how these “shadow remittances” might affect the presumed resilience of remittance economies during periods of crisis. Of course, insofar as remittances continue flowing to households in need, they offer continuing financial support to those experiencing hardship. From the perspective of families attempting to meet their immediate needs under duress, it matters little whether these remittances arrive via formal or informal means, so long as these continue flowing. However, when the same remittances shift out of formal channels and into informal ones, the implications for remittance-dependent countries can be significant, particularly under a managed exchange rate regime. In such circumstances, a relative decline in formal remittances manifests as the loss of foreign exchange earnings while import-stimulating patterns of consumption persist, placing additional strain on a currency peg. In Sri Lanka’s case, the steady erosion of formal remittances in 2021 and 2022 exposed an extremely fragile macroeconomic balance, whereby the incomes of temporary migrant workers played a structural role in maintaining a soft currency peg at the heart of a debt-driven “migration instead of development” model that hinged upon the implicit assumption of continuous returns from temporary labor migration. Not only did remittances fail to automatically stabilize the economy as the forex crisis worsened, their informalization seemingly hastened its collapse.

Footnotes

Acknowledgments

The author would like to acknowledge the generous feedback of Jessie Liu, as well as the valuable comments and suggestions of two anonymous reviewers, in preparing this article. Further acknowledgment is due to Anoji Ekanayake and Nishadi Liyanage for their time and input.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.