Abstract

The ability to access the state as a taxpaying citizen is important for the purposes of building trust and reciprocity, voicing grievances and disseminating knowledge, and strengthening tax compliance and transparency. Based on original empirical data, this paper elaborates a theoretical argument of how state-citizen encounters in the case of taxation are conditioned by five interacting factors. Drawing on interviews with tax officials and taxpayers in Windhoek, Namibia, this paper shows that these five factors are weakly present and negatively reinforce each other, thereby providing insights into the Namibian tax system and everyday state-citizen tax encounters in developing countries.

Introduction

For the taxpaying citizen, being able to approach and access the state is significant for a number of reasons. It is an important indicator of governmental performance, accountability, and legitimacy (see e.g., Fjeldstad et al., 2012; Levi, 1988; Levi et al., 2009; Putnam et al., 1992; Rothstein, 2011; Speer, 2012). It enables space for building mutual trust and reciprocity, voicing grievances, disseminating knowledge, and exchanging ideas (Evans, 1996; Fjeldstad, 2004; Kitschelt, 2000; McCulloch et al., 2021; Van de Walle & Bouckaert, 2003). In young democracies and post-conflict societies, such space can be integral to strengthening state-society relationships and sustainable state-building processes (Andrews, 2013; Brinkerhoff & Brinkerhoff, 2015), but also lead to corruption and coercive government (Orock & Mbuagbo, 2012).

This article offers a case study of state-citizens encounters in Namibia to shed light on everyday taxation practices. We focus on taxation, specifically public channels of access in which citizens as taxpayers are able to encounter the state in the form of its tax authorities. Such channels of access often contribute to the wider institutionalization of a society and socialization into a robust tax culture; this setting can be conducive to improved tax compliance, augmented transparency and trust, and a stronger mutual understanding of the challenges involved in maintaining a system of taxation, both in the Global North (Rothstein & Stolle, 2003; Steinmo, 2018) and the Global South (Bräutigam et al., 2008; Broms, 2015; Moore et al., 2018). These encounters play an important role in constructing images of the state among citizens (Johansson, 2020; Kruks-Wisner, 2018; Lund, 2016), and influence perceptions of whether taxation is coercive and or it contributes to the common good. For instance, getting a fair assessment of one’s tax appeal, or experiencing bureaucratic arbitrariness and discrimination based on one’s gender, religion, or ethnic belonging may shape both citizenship practices and ideals (Kitschelt, 2000).

The main aim of this article is to understand everyday experiences of taxation in Namibia, through the eyes of both taxpayers as well as tax officials. On the basis of this case study, with its explicit micro-level perspective, this article seeks to shine light on two interrelated questions: 1) What public channels of access formally exist with regards to taxation in the country?; and 2) What are the awareness, perception, and usage of these channels among taxpayers? As one of Africa’s youngest democratic states, critical state-building processes are still ongoing in Namibia. Tax-paying culture is still being institutionalized, although tax compliance is relatively high. The Namibian context can help further our understanding of the conditions and outcomes of encounters between the state and its citizens in their capacity as taxpayers, as the country has a relatively developed tax administration while still facing many of the same challenges found across Sub-Saharan Africa. The central focus of this article is to understand tax encounters not only in their own right but also as they shape state-citizen encounters more broadly (see also Bräutigam et al., 2008; Lund, 2006, p. 695f, 2016; Makovicky & Smith, 2020; Prichard, 2015; Soss, 1999).

This article thus contributes to knowledge and understanding of two related issues, one theoretical and one empirical. First, theoretically it engages with the factors of state-citizen encounters which may help construct a robust tax culture. In order to materialize, these encounters require a supply of public channels of access: actual forums where state officials and citizens can meet and interact, and which are accessible and reasonably well-known. Regarding demand, there has to be some underlying interest in approaching the state, awareness of the channels’ existence, and a sense of perceived efficacy. These factors simultaneously interact and may reinforce each other in ways leading to different outcomes, ultimately producing situations either of institutionalized, recurring encounters of citizen inaction and limited engagement, or something in between. Together, these factors make up the analytical framework of this article.

Theoretically, the article builds on and contributes to a rich body of scholarship examining grassroots encounters between state officials and citizens in impoverished regions of the world (see e.g., Auyero, 2012; Bak Foged, 2019; Corbridge et al., 2005; Gough et al., 2004; Krishna, 2011; Kruks-Wisner, 2011, 2018; MacLean, 2011; Mathur, 2015). Previous work has chiefly focused on poor citizens attempting to gain access to the bureaucratic arm of the state in order to secure social welfare services to which they are entitled (including related grievances and complaints), however there is a dearth of studies looking at the same questions in the micro-level context of taxation (see discussion below, however). While taxation involves a different kind of transaction (extracting a monetary resource from citizens, rather than offering goods or services), there are similarities and the present analytical framework is partially underpinned by the literature on social welfare provision (in particular Kruks-Wisner, 2018). The article’s original framework was developed in an inductive way, in dialogue with the data collected for the article. This framework enabled us to systematize and understand the everyday experiences in our data, leading to new insights into how taxpayers and tax officials describe, experience, and reflect on their interactions with each other.

Secondly, the empirical contribution of the article is an account of tax authority-taxpayer encounters in Namibia by mapping out the public channels of access that exist, as well as their meaning and place in the lives of ordinary Namibian citizens. The wider literature on taxation in Sub-Saharan Africa often lacks any micro-level perspective. For instance, much attention has been paid to matters of tax design and reform, including the organization of tax administrations (see e.g., Ahlerup et al., 2015; Fjeldstad & Moore, 2009; Moore et al., 2018), and also the wider relationship between taxation and state building efforts, including democratization and public accountability (see e.g., Broms, 2015; Bräutigam et al., 2008; Herb, 2005; Majumdar et al., 2007; Prichard, 2015). In contrast, the micro-level perspective of individual taxpayers have been largely side-lined, partially because they are hard to research (see however Söderström, 2022; Gatt & Owen, 2018; Johansson, 2020; Juul, 2006).

This is a significant shortcoming as accounts of what happens on the ground may reveal critical insights into the nature and quality of a country’s tax system. There has been increasing recognition of that taxes are part and parcel of the everyday lives of citizens around the world (Boll, 2012; Oats, 2012; Shove et al., 2012). Oats, for instance, argues that too little attention has been paid to how “tax rules and regulations are put into practice” (Boll, 2012, p. 57; Oats, 2012, p. 5). Indeed, despite calls to view and research taxes as a social practice very few studies actually employ an interpretive or ethnographic approach (see however Bierschenk & Olivier de Sardan, 2019; Cirolia, 2020; Gatt & Owen, 2018, p. 1198; Goodfellow & Owen, 2020; Johansson, 2020). As such, this article contributes to this growing work on taxation as social practice, and how it is manifested in Namibia.

The next section elaborates the analytical framework and outlines the conditions of state-society encounters, adapted to the context of taxation and tax authorities. The section on research design contextualizes taxation in Namibia and outlines the fieldwork conducted in the capital Windhoek in late 2018 and early 2019, where interviews were held with officers of the tax authority and with formally employed taxpayers. The analysis shows how each of the factors are weakly present, as there is a low supply of public channels of access and a weak demand for them. The lack of both supply and demand negatively reinforces each other, and ultimately generate few instances where state-citizen encounters around taxation help to build trust, mutual understanding and generate legitimacy for the taxation system in Namibia. Lastly, the concluding section offers a discussion of the findings. This article uses the framework to understand citizen inaction and the relative absence of claim-making on the state, and also to explore how citizens employ different strategies to obtain goods or services from the state. Moreover, empirically, we show how the lack of trust on both sides, and the diverging experiences and ideas of encounters with the other, contribute to this negative reinforcement.

The Supply of and Demand for Public Channels of Access

Based on our research, we argue that state-citizen encounters are conditioned, and made possible by a number of key factors, or circumstances, and here we present this framework.

The Supply of Public Channels of Access

Regarding terminology, we use the term public channels of access to refer to spaces where encounters may occur. These are “public,” as by definition the spaces should be open to all taxpaying citizens and not differentiate between or discriminate against any groups or individuals, although in reality discrimination exists in numerous developing contexts (Gough et al., 2004). Information about the channels also needs to be produced and disseminated by the state, in order for them to function as intended (see e.g., Auyero, 2012; Gupta, 2012). We refer to channels rather than spaces, as in principle the encounters we are analyzing may involve a temporal process in several connected steps, and not necessarily be limited to just physical spaces. Moreover, when these are physical encounters they are not necessarily located in government buildings; indeed many (and sometimes the only) state-citizen encounters in developing regions occur when officials travel to rural areas (Gupta, 2012; Tendler, 1997).

Last and perhaps most important, the term access implies that there is a receiving agent within the public channel; here a tax officer who can attend to a citizen’s claims and queries. By definition, there needs to be a counterpart, a representative of the state, in order to speak of state-citizen encounters. Nonetheless, while this makes intuitive sense, the literature on social welfare provision in developing countries relates cases in which channels are quite literally inaccessible, as government offices and meeting halls are permanently closed or void of any receiving public official (see e.g., Gupta, 2012, pp. 26–29; Hull, 2012, pp. 134–137; Mathur, 2015, pp. 3–6). Nonetheless, access is far from a binary variable, and sometimes access is constrained for certain groups, conditioned by political ties, or is simply inadequate, due to understaffing or a lack of training (Allard, 2009; Gough et al., 2004; Kruks-Wisner, 2018).

In principle, public channels of access may be both formal or informal (MacLean, 2010), and may also be provided by state or citizen/society actors. The latter could include interest groups and social movements, unions, newspapers, and increasingly social media (Heller, 2013). This article focuses on channels of access that are formal and provided by the state. This is for two reasons. First, unlike all various forms of social welfare provision, taxation is almost solely a function of the state and tax administration and collection is almost exclusively initiated and carried out by state actors (see however Lust & Rakner, 2018). Second, direct official encounters with state representatives are likely to have a greater impact on citizens’ images and perceptions of the state than contact mediated through informal bodies or the media (Kitschelt, 2000). Nonetheless, we recognize that different kinds of informal brokers play an important intermediary role in helping poor citizens access the state in the developing world (Pellerin & Söderström, Unpublished; Krishna, 2011; MacLean, 2010). However, these informal interactions have already received attention (e.g. Jibao et al., 2017; Meagher, 2018; Prud’homme, 1992), therefore we focus on formal taxation encounters.

In sum, two factors condition the supply-side of state-citizen encounters: the existence of public channels of access, and the knowledge about these channels disseminated by the state.

The Demand for Public Channels of Access

Supply on its own, however, is not enough. The mere existence of public channels of access, even if they are robustly and equitably designed, says little about their potential to foster a tax culture, increase tax compliance, build trust in the tax system, and so forth (Bräutigam et al., 2008; Moore et al., 2018). Inspired by Kruks-Wisner’s (2018) theoretical model of what conditions active citizenship, based on an investigation of state claim-making and social welfare services in rural India, this article therefore argues that three additional ingredients, or factors, are essential to understand state-citizen encounters. These are: a need to seek out the state; awareness and perceived efficacy of, and trust in, the channels of access. If any of these is absent, the supply of public channels of access is not be matched by a demand, or use of them.

First, a citizen needs a reason, some motivating condition (a need or a want), to access the state. In the case of social welfare provision this is straightforward as a citizen stands to gain a material good or service, whereas in terms of taxation, the material advantage is less apparent. Yet, it is necessary to submit tax returns, for example, in order to comply with the tax laws and possibly obtain a refund. Or, if a taxpayer feels aggrieved by a certain decision it is in their interest to access the state in order to appeal a decision or seek a remedy. Still, the decision to approach the tax authorities may not be triggered by an explicit event (like an unfair decision); it could be driven by a need for information on one’s own tax balances, how tax regulations affect one’s business, or simply to voice concerns about the tax system more broadly.

Even if citizens have an interest in seeking out the tax authorities, nothing will happen unless they are aware about which public channels of access are available and what rights they have as taxpayers. This awareness may be produced directly by the state (as mentioned previously) and through different public information campaigns, but also through the education system, the media (both print and social), or simply by word-of-mouth (Heller, 2013, pp. 6–7; Lieberman et al., 2014). Moreover, awareness relates not only to knowledge of channels of access, but also to procedural and technical know-how about what steps to take when encountering the state (Kruks-Wisner, 2018, pp. 39–41). Many interventions and channels of access that aim to increase public participation and deliberation end up leading to overly technical and complicated processes that actually impede participation, in part because they are perceived as cumbersome, scary, or boring (Corbridge et al., 2005, pp. 121–124; Speer, 2012). Awareness is also socially produced by citizens; even if they hear about a channel of access from a state-initiated source, their perceptions and understanding will be mediated by stories and attitudes of neighbors, colleagues, and family-members, alongside their own past experiences of the channel (Corbridge et al., 2005, pp. 8–9). In order to capture this social production of knowledge we need an interpretive and everyday perspective on tax encounters.

Even if citizens have a reason to approach the tax authorities and know where and how to do so, they still also need to believe it is worth the effort and resources. They must have faith that their case will be attended to, and ultimately lead to some form of change. This amounts to external political efficacy; a conviction that individual or collective efforts can lead to change in the behavior of political agents and authorities (Craig et al., 1990). Efficacy may derive from the prevalent discourse about a certain public agency or past personal experiences of it (Kruks-Wisner, 2018, pp. 37–39; MacLean, 2011). It should be noted that perceptions of public service performance (including channels of access) may both hamper action from citizens, as well as trigger increased efforts to access the state for better services (Chong et al., 2015; Kruks-Wisner, 2018, pp. 38–39). In sum, in addition to the two factors on the supply-side, the demand-side of state-citizen encounters is conditioned by three factors: the interest or need of citizens to approach the state, their awareness and knowledge of how to do so, and a sense of this being worthwhile.

A Mutually Reinforcing Effect

The supply and demand of public channels of access are not independent of each other, but rather simultaneously and mutually reinforcing. If public channels of access are provided and are widely announced, awareness of these may spread and citizens may find it worthwhile to engage with them when needed, increasing the demand. Conversely, a high demand among citizens for more information and knowledge, and for formal platforms on which to engage the state, may spur the state to increase channels of access. However, the reinforcement effect may also be negative. A low supply—few or poorly functioning channels of access—may curb citizens’ willingness and perceived ability to meet the state even if they need to, keeping public awareness at low or deteriorating levels. From the state’s perspective, a lack of visible grassroot demands for public channels of access might reduce incentives to provide any.

This article uses these five factors of state-citizen encounters as a framework to analyze taxpayers’ experiences with the tax authorities in Namibia. We first map the supply of public channels of access, and then examine the demand for these channels, thereby also illuminating the wider social practice of being a taxpayer in Namibia, in particular how meetings with the tax man are experienced and what factors encourage or hinder such meetings.

Research Design and Data Collection

Taxation in Namibia is highly centralized and carried out by the Inland Revenue Department (IR), a branch of the Ministry of Finance (MoF). 1 At the time of fieldwork in late 2018 the IR was in the process of being transformed into the Namibian Revenue Agency (NAMRA). This was to be a semi-autonomous body modelled on its South African equivalent in which the formulation of tax policy is separated from the tax collection and citizen-engagement functions. The transition would also computerize and digitalize large parts of the tax system in an effort to boost transparency and decrease the manual processing and reporting system (Interviews 1, 2, 3, and 7). However, at the time of our fieldwork, the tax authority was in practice a direct extension of the Ministry of Finance, with little autonomy and situated in the same building and offices as the Ministry of Finance. Indeed, taxpayer respondents indicated that they saw little distinction between the two, with some referring to the IR as the MoF building.

The IR collects a range of taxes, including income tax, corporate tax, property tax, VAT, and export customs (Interviews 1, 2, and 3), any of which may lead to encounters in public channels of access. This article focuses on formal income taxpayers, and their perceptions and experiences of meeting with the tax authorities. These are citizens who are formally employed, publicly or privately, and pay taxes through their employer as follows: after registering as a taxpayer, each individual receives a tax card which is submitted to the employer, who deducts a certain amount of tax from the individual’s monthly salary and transfers this to the IR. Thus, tax payments largely occur without much contact with the tax authorities, in contrast filing your tax return does involve more interaction (as will be discussed further in the analysis). Income tax follows a progressive rate, exempting incomes under NAD 40,000, with a cap of 37% for incomes over 750,000 NAD (Interviews 1, 4, and 7). 2 Citizen-state interactions related to the pay as you earn policy, such as taxes on formal income, are particularly interesting in that they are routinized, yet likely to involve the least conflictual bargaining and room for maneuver on either side. The extent to which these routinized tax payments and instances of contact with the tax authorities are seen as legitimate or accessible enough, will impact voluntary tax compliance as well as the pool of individuals who pay income tax. VAT and income tax are both difficult to evade for the formally employed citizen, and the threshold to appeal a case with the tax authorities may be higher (Namibia has high compliance, see e.g., Aiko & Logan, 2014, p. 10). Yet these taxes are central to the larger political conversation around taxes in the country, and as such they are core aspects of the fiscal contract with the state (Söderström, 2022; a pilot overview of letters to the editor in the major newspaper in Namibia also suggests this). As such, lack of confidence and problems with access around such taxes is worrisome in relation to building an accountable and democratic taxpaying culture. This article therefore focuses on taxes that are central to the ordinary citizen (as opposed to corporate tax, property tax, and export customs, specialized taxes which apply to fewer citizens) in order to analyze taxation and state-citizen encounters in its most commonly occurring form.

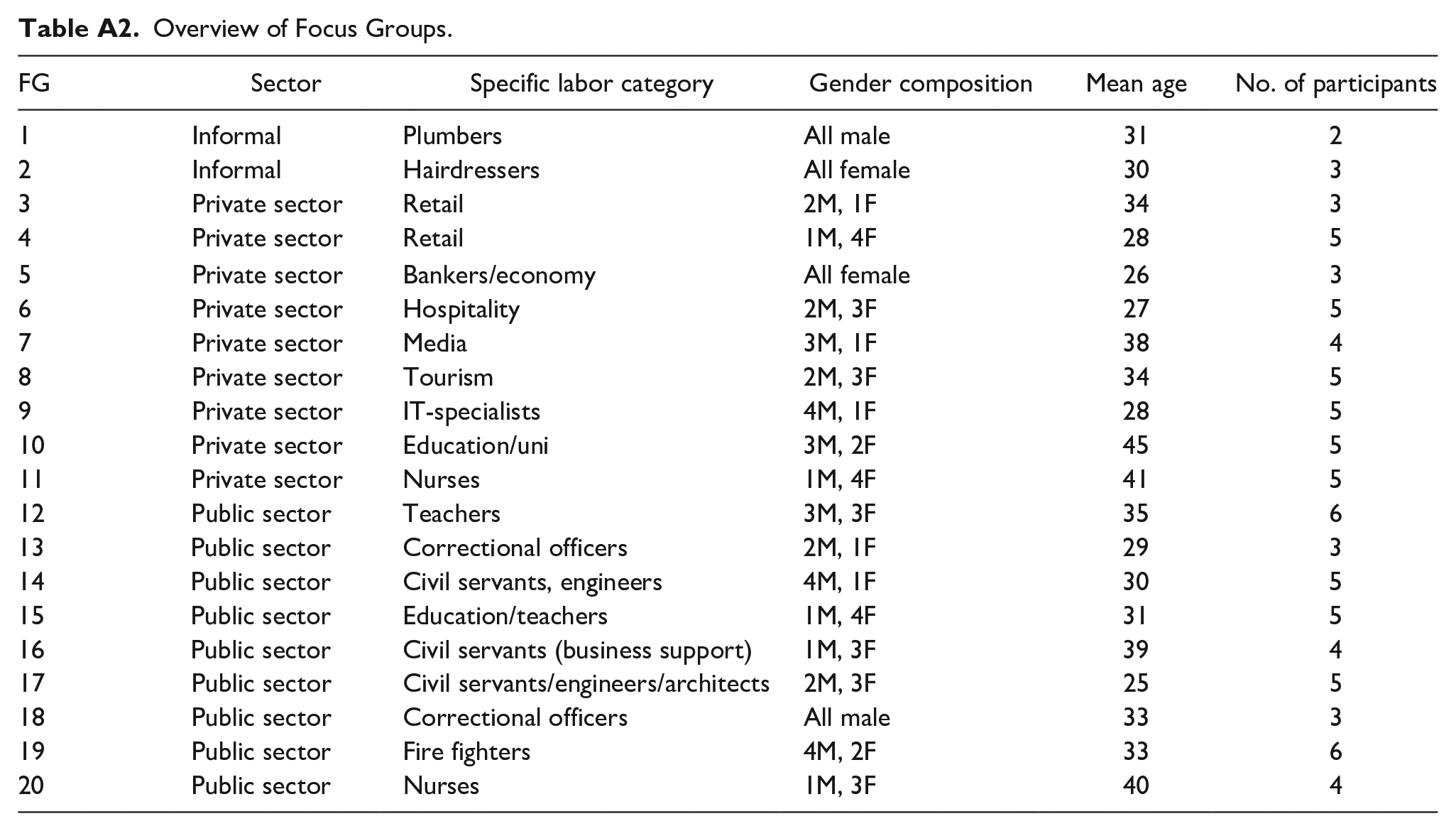

Fieldwork for this article was carried in Windhoek between November 2018 and February 2019. In order to gain information and insights into factors driving state-citizen encounters in public channels of access, in-depth interviews were held with 21 individuals within two different categories of respondents, namely tax officers and citizens (see Table A1 in Appendix). On-site observations were conducted in the spaces open to the public at the IR offices, for an hour or two each day over 1 week including participant observations at the IR office. In addition, 20 different focus groups (FG) were conducted with two to six participants in each, with a total of 86 participants, see Table A2 in Appendix. Regarding collection and analysis of data, the project took an inductive approach, following interpretive traditions in ethnographic research. The initial interview guides were therefore relatively open, seeking general insights into how taxpayers and officials describe, experience, and reflect on their interactions with each other. The initial aim was to elicit how taxpayers encounter the tax authorities, and to capture citizens’ experiences of these meetings in their own words and interpretations. Thus, the framework and factors presented in the previous section were arrived at after collecting the data. We moved from the everyday experiences and dynamics to the specific factors while processing the data, following an iterative process to make sense of the data, connect these with the theory, and develop the framework (Parkinson, 2022, p. 429; see also Schatz, 2009; Simmons et al., 2018; Soss, 2018). For us this meant that we re-read transcripts and mapped various themes to see how the tax experiences could be clustered, as well as returning to the literature to further refine the framework. As the factors were not formulated prior to the interviews, we could not ask respondents to compare or rank them in any way. Thus we could not engage in traditional member checking as a way to validate our findings, however, as we moved between interviews, observations, and focus group discussions, we used these various channels to both substantiate and question preliminary findings (see Angen, 2000 for a discussion of validity/validation within interpretive research). Indeed, focus groups in themselves also allow for this kind of internal scrutiny of respondents’ statements (Söderström, 2011). We do recognize, however, that our interpretation of the data is both temporally and contextually situated; this prompted both discussions between the authors of the article, but also with research assistants, even if such discussions can never be fully concluded.

The first category of interviewees included nine tax officers, all located at the headquarters of the IR in Windhoek. They worked in various sub-branches and offices and part of their job description is holding meetings with taxpayers, at least in theory. Due to the relatively small staff size of the IR and for reasons of anonymity, details cannot be provided on respondents’ exact locations within the department. Tax officers were selected following the criteria that a large part of their job description relates to meeting with taxpayers, and approached with help from a local research assistant and an informant at the IR. The interviews focused on the tax officers’ general work tasks, how they interact with taxpayers, and their perceptions of these meetings. Information was gathered about all channels in which tax officials and taxpayers might meet and how the IR communicates information about these. All interviews were held in offices at the IR. They were all conducted in English, and recorded except for one officer who declined to be recorded. Information from the interviews was also used to corroborate and triangulate statements and information derived from official documents and media reporting.

The second category of respondents consisted of twelve taxpaying citizens residing in Windhoek, including seven public employees and five from the private sector. All respondents were formal payers of income tax and they were found and approached with the help of local research assistants. Respondents were selected to reflect a variety of professions from both the public and private sector, who had all been formal income taxpayers for a few years. All interviews were held in English and recorded, lasting between 25 and 65 minutes. Interviews were organized either at the offices of a local research organization, or at the workplace of the respondent. These interviews focused on the demand-side factors: respondents’ possible reasons for approaching the IR, their awareness and perceived efficacy of this, and where applicable, their past experiences of meetings with tax authorities. The aim was to gather information about subjective experiences and opinions as regards public channels of access to the tax authorities. Respondents frequently did not understand questions at first, as taxation is a little discussed topic in Namibian society, and so things were often rephrased or clarified (see analysis).

In addition to the in-depth interviews, focus group data was collected from 86 respondents, most of whom were formally employed in either the private or public sector, and recruited via their workplaces. Again, discussions centered on formal income tax, although other forms of taxation were also discussed. The focus group interviews covered a much wider range of topics than the individual interviews, exploring both respondents’ direct experiences of taxation, but also how taxes are dealt with politically and how respondents understand the logic behind the tax regime. All focus groups were carried out in English and recorded. All groups were carried out in Windhoek where participants’ access to state services was relatively similar across the groups. There were also differences across and within groups in the sample reflecting the variation of these background characteristics in the population as a whole. In particular, the sample had a gender and age balance, reflecting the (young) population of Namibia, with respondents of a variety of ethnicities, and a mix of those formally working in the private and public sectors. While the sample was not representative, this variety at least maximizes the potential of the groups to cover a range of perspectives likely to be present in the urban population as a whole.

Public Channels of Access within Taxation in Namibia

The analysis is structured in five subsections, each exploring one of the factors of the supply and demand for public channels of access within taxation in Namibia. Once all the interviews were compiled, we looked for common themes, and in an iterative fashion we developed the analytical framework presented above. We illustrate the analysis with quotations representative of participants’ views (rare diverse views are noted in the text). We first turn to the supply side.

Supply Side: The Limited Supply of Public Channels of Access

The first factor relates to the supply of public channels of access, which in the context of taxation in Namibia can best be described as limited or weak, and spatially restricted to the actual office buildings of the IR in Windhoek and six additional sub-offices around the country.

The first and most significant entry-point to the IR is through a sub-branch known as the Customer Care Center, through which almost all errands and matters pass (Interviews 7 and 9). The Center has been in place since the early 2000s, and in practice it is just a rather large waiting room on the ground floor of the IR building in the downtown area of Windhoek (with a population of about 400,000). The room contains several rows of metal benches and a number of glass-framed counters along one side of the room. At first sight, the space appears quite unassuming, with little of interest besides a few posters issued by the Ministry of Finance stating the importance of paying taxes for the future prosperity of the country, as well as a metal rack holding different informational pamphlets explaining the rights, regulations, and provisions in different areas of the Namibian tax code. For instance, the rights and obligations of citizens are laid out in a short pamphlet titled the Taxpayer Charter, which is available online as well as in printed form at the IR offices throughout the country. Unlike the classic imagery of bureaucracy as seen, for instance in the work of Auyero who described social welfare offices’ waiting rooms in Buenos Aires full of bureaucratic arbitrariness and negligence intermixed with extremely long periods of waiting (Auyero, 2012), the center in Windhoek appears a relatively ordered and fast-paced space.

It is staffed by approximately 12 to 15 customer care officers divided into two smaller divisions. The first group deals with the submission of tax returns while the second is supposed to function as a mouthpiece for public information and for answering enquiries from citizens (Interview 7). The submission of tax returns is a process that all formal payers of income tax have to go through, at least in theory. It typically occurs at the end of June, 4 months after the end of the tax year which runs from 1 March to 28 February, though submission deadlines vary for different types of companies and customs returns, hence submissions occur throughout the year (Interviews 1 and 7). Tax returns can be submitted by post or courier, but the vast majority of formal income tax payers prefer to go to the Center in person (Interviews 1, 2, 4, and 10). Once there, the taxpayers are required to make sure that they receive a copy of the tax return form, which carries the official IR stamp on it. The importance of this procedure was emphasized, as the ability to object and appeal a tax decision (described below) hinges on the possession of stamped copies, and that lost ones are a recurring problem (Interviews 7 and 8; this procedure was widely acknowledged by the focus groups too). The planned digitalization of the tax system is thought to remedy this problem, yet it should be noted that vast numbers of Namibians do not have access to computer facilities (Interviews 9 and 10). The week or two preceding the tax return deadline are extremely busy with long lines outside the building as the tax returns are manually photocopied and stamped, and initial assessments offered to citizens. On most other days, however, including the periods observed briefly for this study, citizens seemingly have to wait less than 10 minutes before getting to see a tax officer.

The second group of customer care officers handles more general queries and questions and their services are available to citizens throughout the year. The most frequent queries relate to an individual’s personal tax balance; whether there is any outstanding amount to be paid, whether they are owed a tax refund, or how to report personal or corporate incomes. Others come in to obtain what is known as a Certificate of Good Standing, an official document needed for applying for some jobs, registering businesses, buying property, and submitting tenders to the government. While some citizens come of their own accord, the majority reportedly turn up and pose questions when they have been contacted by the IR. An automated system is used to generate either an email or a text message, or a printed letter in some cases, which is sent to taxpayers when something is out of order in their tax returns, or if there is an outstanding balance to be paid or received (Interviews 4 and 7).

We also probed the tax officers beyond the day-to-day running of the Center to inquire about their perceptions of taxpayer awareness and understanding and about how the tax system works more generally on the basis of their encounters. Their responses predominantly reflected the perception that citizens have limited awareness, and that it falls to the IR to educate them when they actually show up at the office building. One officer explained: “some of them do understand if they receive the SMS, some of them cannot read. So, in many cases the smart ones, if they receive a SMS, they will come to our offices. . .and then they will ask what does this mean?” (Interview 1). Similarly, another tax officer noted “my experience when I come in consultation with taxpayers is the lack of education in terms of the law and that is something that I’ve seen across all different categories of taxpayers” (Interview 9). When describing their interaction with taxpayers, another officer noted “most of them are positive, you will get one or two who will be a little bit aggressive or negative or so but we try our utmost best to keep the taxpayer calm and to explain to them exactly what happened. . .” (Interview 7). This suggests that officers believe that their clients are typically unhappy about general tax policies rather than with specific decisions (Interview 7).

One senior officer, who had spent almost two decades at the IR, lamented the public’s lack of a basic understanding of what taxation means and how to do it in practice. The officer suggested this is one of the main obstacles the IR faces on a daily basis when meeting citizens, and that it has improved little over the years (Interview 10). The officer acknowledged that the lack of information among the general public is often conflated with dishonesty or deliberate tax cheating. The majority of conflict or disputes between the two sides derives from misunderstandings and limited technical know-how, an opinion shared by most other officers too (Interviews 1, 2, 3, 5, 7, and 9). 3

While the Center is the first and most important channel of access, to a large extent serving as an informational unit, it is not the only one. In cases where the Center cannot answer an individual’s queries, or where they lack the mandate to take action, individuals are directed onward within the IR. In most cases this is simply to another division or a more senior officer, who then deals with the matter (Interview 7). Since the IR is small in terms of on-site staff, with a rather small sized tax-paying population in Namibia, it is not hard for an industrious citizen to gain an appointment with a division director or the commissioner (the second highest officer in command), although they might have to wait a few days (Interview 1). From this perspective, the channel of access, the IR itself, is multi-sited and, at least in principle, offers a procedure for citizens to obtain information, express grievances, and pursue tax matters.

There are three additional channels where taxpayers may encounter the tax authorities: auditing, debt collection and recovery, and appeals and objections. The first two apply to both individual taxpayers and companies of different kinds, yet in recent years these divisions have directed most, if not all, of their efforts toward companies rather than individual citizens, and as such are largely outside the scope of this article (Interviews 1, 2, 3, and 4). Slightly more common is the objection and appeal procedure; a mechanism provided in the Taxpayer Charter and in the tax legislation of the country. If a taxpayer feels they were treated unfairly with regards to a tax decision they have the option of first objecting, within 90 days and in writing, entitling them to a meeting with someone in the legal division of the IR. Should the objection be rejected, they may then lodge an appeal with the Tax Tribunal, and if this is also rejected, they may appeal to the High Court. Two officers mentioned that individuals will decide to object a few times a year, but this rarely develops into a tribunal or court case, due to the very long time periods involved. As court cases can drag on for years, most give up after having objected and met with the legal division, and either pay the outstanding balances, or simply ignore the decision that aggrieved them in the first place (Interviews 4, 9, and 10).

Supply-Side: Efforts to Foster Public Awareness

The second factor driving state-citizen encounters is state-led campaigns and efforts to foster public awareness and information, in this case about taxpayers’ rights, ways to approach the tax authorities, and information about the importance of taxation more generally. According to the tax officials, all three issues are addressed during one single event known as the Taxpayer Education Day. 4 It has been held for the past 4 years toward the end of June when the tax return submission date is near. The official aim of the event is encouraging voluntary compliance, providing technical information, explaining how tax returns work and how different forms are filled out, in addition to the wider goal of sensitizing and informing the general public about taxation and its importance. On this day, the IR sets up stalls at shopping malls, markets, and bus stations around the country and also goes on the radio to talk about taxation (Interviews 3, 5, 6, 7, 9, and 10). In interviews, officers praised the day as a clever innovation, as a pure service to the public, and an opportunity to meet with the tax authorities. One person explained: “that’s why we are having that day, to give a taxpayer time to come sit with you, anything they want, the person wants to know, we will communicate with them, any inquiries the person wants to do, we will do that” (Interview 7).

Yet not all officers were optimistic about the Taxpayer Education Day. One talked at length about the fact that people only show up if they actually have an urgent matter that needs resolving, and that “most material we distribute just ends up in dustbins or all over the place” (Interview 10). Another stated that the event falls short of its goal to actually educate people or sensitize them on taxation, claiming that it is pointless to have one single day per year for this purpose when taxation is rarely discussed in public at other times (see also Söderström, 2022). They saw it as overly technical as it focuses solely on tax return forms and not the wider phenomenon (Interviews 3, 4, 9, and 10). One officer was also disappointed with their ability to reach out to the informal sector: “The one I want to come on that particular day is a guy having a business around the street corner” (Interview 9). Another officer criticized the target groups for this outreach: “It [tax education] should be starting in primary school, or secondary school, not once per year, because they are getting one brochure, looking at it and then leaving it and then one more year of no education, so they lack any idea of why tax collection is important” (Interview 6). Focus group respondents also supported tax education in schools.

Probing for additional ways public awareness is raised by the IR or Ministry of Finance yielded few suggestions. Most officers stated that taxation is occasionally discussed in the newspapers, or on the radio, but only in relation to specific (often scandalous) events or court cases, and not to the idea of taxation itself or how to interact with the IR (Interviews 2, 3, 5, 6, 7, 9, and 10). In sum, the Customer Care Center at the IR buildings and the national Taxpayer Education Day appear to be the main and seemingly only ways to raise awareness.

Last, several IR officers highlighted two issues in their work which they believe constrains their ability to offer good services to taxpayers and improve relationships. The first is the manual processing of almost all taxation matters. Although all IR-offices are equipped with computers, the vast majority of incoming tax errands (for individuals and companies alike) are paper-based. This requires a considerable amount of time to enter data onto the computer, leading to mistakes and complicating meetings with taxpayers as documents are often missing (Interviews 3, 5, 7, 9, and 10). As such, there were high expectations on the new digitalized system, then expected to be implemented during 2019. The second issue that officers felt limited their efficacy is a reported lack of enough staff in absolute figures, and a lack of qualified staff with sufficient training and capacity (Interviews 1, 2, 3, 5, 7, and 9). Officers singled this out as a detrimental factor in their ability to not only serve taxpayers, but also carry out basic functions such as tax collection and auditing. For example:

we are there to recover tax, but we are not doing it any more, we are doing other divisions’ work [detailed examples]. We are not actually doing what we are supposed to do. We don’t do judgements any more, we don’t do summonses any more, we don’t do anything (Interview 2).

Overall, we see that both factors conditioning the supply of state-citizen encounters are rather limited. The number of channels to access the tax authorities are limited, and the efforts to raise awareness by the state are limited.

Demand-Side: Limited Perceived Needs of Approaching the IR

Next, our focus shifts to the perspectives of the taxpaying citizens, and the demand-side. For analytical clarity these three factors are addressed separately, although the three demand side factors were spoken of interchangeably as they in practice overlap.

The first demand-side factor is the question of perceived needs. One of the central questions during interviews with taxpayers aimed to map out the possible reasons they would have to approach the IR, for instance going to the Customer Care Center, writing or phoning an official, or attending the Taxpayer Education Day. In brief, the common answer was that there are very few reasons to do so, apart from going on the day when their tax returns have to be submitted in June. In contrast, tax officials tended to stress citizens pent-up need to engage more with the tax administration. As the respondents were all formally employed, taxes are deducted by their employers before the salaries are paid out, and as such they only need to fill out limited details on the tax return form. In practice, this is a self-assessment of what they have earned and paid in taxes, and for most the form comes pre-printed when they receive it from their HR-department (Interviews 8, 13–17, 19, and 21). The focus group discussions also revealed that most people get help with their tax returns either from their employers, or from family and friends. The IR is only seen as a third option, even though the forms are perceived as complicated. The often categorical negative responses, also shine some light on the limited wider knowledge of taxation, as illustrated by one taxpayer: “every now and then we would receive a notice that tax returns are due on the 31st [. . .] then you know, people will queue at the offices, otherwise I don’t think that there is any other form of relationship between the citizens and the authorities” (Interview 13). Other interviewees said that submission day was “the only time I actually meet with the taxman” (Interview 14), or that “besides that there is no communication between us and them” (Interview 19). One focus group participant, avoided contact altogether for 4 years despite the fact that: “they normally keep on sending me SMS: ‘submit your things’” (male 1, FG 18). Overall, this underlines the different perceived needs of having contact with the IR among taxpayers in contrast with the tax officials.

Only 3 out of 12 respondents recalled having interacted with the IR beyond submitting tax returns, and then only in order to obtain a Certificate of Good Standing, enquiring about a text message they had received from the IR, or settling an outstanding balance (Interviews 8, 15, and 17). Illustrative of the broader pattern, respondents were also unable to recall any clear case where a family member, colleague, or neighbor had reason to meet with the IR for something other than tax returns. Yet they alluded to the perceived hassle of doing so, citing reasons such as lengthy waiting times, difficulties of finding parking, and most commonly, a lack of awareness. Similarly, very few of the focus group respondents noted any interaction outside submission day; here, too it was a question of smaller appeals or trying to question the need to submit returns at all (for a deceased relative or due to a study break).

Demand-Side: Limited Awareness of Public Channels of Access

A second key demand-side factor in state-citizen encounters is knowing how to approach the state, which procedures to follow, and what type of resources are needed to do so. As previously outlined, taxpayer respondents were familiar with the Customer Care Center at the IR, and the process for handing in tax return forms. Yet, when questions were asked in interviews and focus groups to gauge the respondents’ awareness and knowledge beyond those meetings, there was a greater variety of answers, which indicated an overall limited awareness.

Some questions were of a hypothetical nature, enquiring what respondents would do if they felt aggrieved by a tax decision, needed assistance on some tax-related matter, or simply more information on what taxation is all about; that is what public channels of access they were familiar with besides submitting tax returns. Here, responses were mixed, and interestingly, not directly associated with a respondent’s profession or level of education. Some stated that they would go straight to the Center at the IR (Interviews 13, 14, 18, and 20). Others said they would first enquire with family or colleagues and only go to the IR as a last resort, again stating that it is perceived as a “hassle” (Interviews 12, 17, and 21). Similarly, most in the focus groups had limited ideas of additional ways to access the IR (FG 1–2, 4–11, 16–18, 20). For instance, one person noted “I don’t even visit their office to start off with. . .The ministry of finance, I don’t, I know it’s somewhere based there in town but I haven’t visited them, normally I just, we just fill in [the tax return form] and give it to our driver, so there’s no relationship, not at all” (Interview 16). Some also admitted that they had little sense of what the IR could offer in terms of citizen-services (Interviews 8, 15, and 16). One person was helped by a neighbor who works at the IR, but wondered how others cope: “I think it’s just overwhelming, especially for people who aren’t educated. I’m educated and I struggle” (Interview 17).

As the Tax Education Day was much discussed by the tax officers, care was taken to also enquire about this with taxpayers. Overall, responses indicated a clear lack of awareness: only a few respondents had heard of the day and knew what it was about (Interview 20, FG 5) (see also similar findings about the lack of knowledge of the tax system in other Sub-Saharan countries in Mascagni & Santoro, 2018, p. 6). Several individuals said this was the first time they had ever heard the event mentioned.

Data from the focus groups demonstrate that most respondents were also rarely familiar with the brochures and pamphlets produced by the tax authorities (FG 7, 10, 14, and 18). One woman had gone looking for information, to check if her boss was deducting her tax correctly: “Why did I download it [laughs]? [. . .] something was just weird about [my] tax, so I had to educate myself and I got this information” (female 3, FG 5). On seeing the brochures for the first time, many expressed a clear satisfaction, but also wondered why they had not seen them before. For instance, “As for this [taxpayer charter] I just feel deprived of information” (female 1, FG 11), or “now that I am looking at all these brochures, it actually feels nice to see because oh this is informing me, wow this is good, know I am informed, now I know” (female 2, FG 5). This sparked conversations about how the IR could ensure that these brochures actually reach people, such as handing them out together with the tax return forms. Simply providing access to them at the Customer Care Center was perceived as insufficient.

The focus groups conducted in 2019, showed more awareness of the impending reform and creation of NAMRA (FG 4–9, 11, 13, 17, and 20). While some respondents hoped for a more user friendly and more accessible system, where documents do not get lost, others were worried about computer literacy and access. A few had already had problematic encounters with the online interface, citing lack of user friendliness and system errors.

The interviews also explored the broader discourse in order to further our understanding of general awareness of public channels of access. Questions included: how is taxation discussed amongst the respondents’ family and friends? What do respondents know about taxation from newspapers or the radio? Here, responses varied from almost never having heard of taxation to a comparatively strong theoretical understanding, but with the common view that taxes and taxation are quite seldom discussed in public or private. One man stated that “. . .until today, I have never heard of taxation [. . .]. I only came to know it when I started working and from there I did not know much” (Interview 15). When asked where they would go for information about taxes, another respondent revealed that his participation in this research project was the first time he had reflected on taxation at all: “you rarely hear people discuss things, matters like this, because they don’t know anything” (Interview 8).

Demand Side: Low Perceived Efficacy of Public Channels of Access

The last demand-side factor in state-citizen encounters is the perceived efficacy of seeking out a public channel of access and engaging the state within it: do people believe this is worth the time and effort, and can efforts lead to some desired outcome or change? In several interviews this issue was approached through somewhat hypothetical questions as the respondents made clear that they had very little experience of encountering the IR. They were asked, for example, if they believed the tax authorities are fulfilling their mandate of serving the public (with tax services), whether it was talked about as a well-functioning organization, and if they felt it could be improved to the benefit of the individual taxpayer, themselves included. Here, respondents in both interviews and focus groups expressed a wide range of ideas and opinions. The majority were quite skeptical as to the performance of not only the IR, but also the Ministry of Finance and Government of Namibia more broadly, often hinting at corruption and the inefficient use of government funds. One respondent described the futility of approaching the tax authority: “sometimes their staff members are not that friendly, don’t show that eagerness to help, it’s as if ‘how can you not know this’, like they kind of blast you for ignorance so you probably feel more comfortable asking someone that you know [about tax matters]” (Interview 13). Or as noted by a woman in one focus group: “It’s a process of come back tomorrow” (female 3, FG 9). Overall, there was a sense that channels were not available (the right person for their case was not in place, not answering the phones, long waiting times, too few offices etc.) (FG 5, 11, 13, and 16), that there is a lack of capacity and competence (FG 4, 5, 7, 10, 11, and 20), and that when you meet with them they are often perceived as lacking both time and patience to help (FG 4, 5, 16, 19). In part, this experience mirrors the tax officials’ sense of being understaffed. In addition, some respondents also expressed distrust of the authority’s intentions, and a feeling that tax officers are biased and vindictive (FG 4, 6–8, 12, and 14). For instance, if you are unfriendly to the tax officer they are likely to punish you: “when you are rude to him he’ll just tell you it’s not there and the you’ll have outstanding tax returns for years and then when you [retire] the Government takes everything” (male 1, FG 6). One man was concerned about the NAMRA reform:

they cannot find me on the system because they are busy upgrading somewhere, somehow? So what will happen now, suddenly I will owe money to them, I think it’s a scam to me, how can you not warn the Namibian citizens that we are going on to a new system [. . .] I think there will be a trick in a way that is waiting for us some way, somehow (male 1, FG 4).

Some compared the IR with other actors, both private companies and other public agencies, and stressed the lower quality of service and treatment they received from the IR (FG 7 and 16). Overall, there was a sense it was useless and a waste of time to approach the authorities on the question of tax: “Really we really don’t have any way, anyone to go to, not even to the politicians to complain to because they don’t listen, they don’t care” (Interview 8). These accounts also had an undertone of distrust.

Two additional issues merit brief mention concerning the weak utilization of channels of access, and the low perceived efficacy of public channels of access. First, taxpayer respondents spoke of a widespread lack of engaging or challenging authorities in Namibia. They suggested that many Namibians prefer not to complain to the authorities or draw attention to themselves by organizing protests and strikes or filing petitions, which some claimed reflected the widely revered status of the dominant political party, SWAPO. Criticizing the government was seen as criticism of SWAPO, and indirectly, the Namibian independence. For instance: “They [the government] know people are still going to vote for them and they’re still going to continue with their old nonsense of doing nothing cause people are not complaining, or we are complaining but we are not going forth to show them that we are not happy” (Interview 16). Another noted “Generally civil society in Namibia is weak, we are not the kind of people who hold officials accountable. . .people have complained and there have been articles in the papers, but there is no militancy in us” (Interview 13). Respondents argued that the general reluctance to openly criticize or challenge the government and its agencies also impacts attitudes to taxation. It lowered the incentives to educate oneself about tax, or to make efforts to access state channels to pursue a claim or lodge an appeal. On the contrary, respondents stated that for tax—as with other issues—they simply choose to “bear the brunt” and muddle through. Here we see how ideas about the state in general shape taxation encounters, as well as how ideas around taxation shape ideas about the state in general.

Second, respondents opted for newspapers, or social media, when they want to voice concerns or grievances about taxation, or bring to light an unfair tax decision. For example: “people tend to do the most common thing which would be social media, they go on there and vent their frustrations. I don’t know how many people would actually go on down to the IR building and actually air their frustrations there” (Interview 14). Similarly, another respondent said: “They’ll complain on Facebook and they’ll send SMS to the newspaper but they don’t take action” (Interview 17). These spaces are not public channels of access, but rather a public platform where citizens can exert voice, only indirectly targeted at the government or the tax authorities.

Overall, the demand side in the case of these Namibian taxpayers show evidence of a limited perceived need to approach the IR, as well as a limited awareness of public channels of access, and these channels are also deemed to be inefficient, while taxpayers highlight other alternative channels outside the state to influence taxation as more efficient.

Concluding Discussion

This article sought to shine light on two related questions: what public channels of access formally exist with regards to taxation in the country and what is the awareness, perception, and usage of these channels among taxpayers? This was studied in the context of Namibia, drawing on interviews with tax officials and taxpayers in Windhoek alongside observations at the Inland Revenue Department. While our sample of respondents was limited, they included a range of different experiences, and their responses highlighted how interactions between tax officials and taxpayers can enable either a deepening of democratic statebuilding, or more coercive and corrupt state-citizen relationships. Based on a process of induction, we arrived at the following five factors governing these interactions: 1) supply of public channels of access; 2) state-efforts to publicly promote these; 3) perceived need for approaching the tax authorities; 4) awareness of the existence of public channels of access and knowledge of how to access them; and 5) sense of perceived efficacy. This article has demonstrated the limited occurrence and strength of these five factors of state-citizen encounters with respect to taxation in Namibia, a country with both a low supply of public channels of access and a weak demand for these. Rather than amplifying one another, each of these elements negatively reinforces each other, with few indications of anything changing in the near future in Namibia. For instance, lack of trust on both sides feeds into this encounter on both sides. It was clear that tax officials and tax payers had highly varying experiences and ideas of the encounters with each other, which likely contributes to the weakly present factors of both supply and demand. The perceptions within each group of the other reinforced their limited will or desire to increase the frequency and quality of encounters. As a whole, this offers an original micro-level and empirically grounded perspective on this issue and critical insights into the nature and quality of Namibia’s tax system.

Another contribution of our article is the original framework, which can also be used to understand citizen inaction and the relative absence of claim-making on the state, and not only how citizens follow a variety of strategies to obtain goods or services from the state (active citizenship). This framework is thus useful to discuss and contextualize the opposite of engaged interactions between state and citizen, namely the lack of engagement and encounters. Encounters with different state agencies or meetings for different purposes cannot be wholly separated, they reinforce and mediate each other. The ways in which people interact (or not) with the state in one area colors the modality and understanding of these relations in other areas.

Ultimately, the relative absence of taxation as a social practice, and the lack of benign cycles of state-citizen interactions provide little evidence of movement toward the coproduction of mutual trust, understanding and tax knowledge in the case of Namibia. The question is if the state-citizen relationship that is visible in relation to taxation, also permeates state-citizen relations in general in Namibia. It may be that the lack of engagement in this area of society reflects a lack of engagement in other areas, and the degree to which the state is seen as accessible with respect to taxes shapes how the state is seen as accessible in other areas. In the context of taxation authority reform, it is therefore crucial to also consider how such reforms in turn interact with citizen practices and understandings. Given the ongoing reform and transformation of the Inland Revenue Department into the Namibian Revenue Agency (NAMRA), it will be important to monitor how these practices and perceptions change or remain the same. Simply reducing personal interactions with tax authorities is not enough to make the most of such reforms. Rather any developments also need to take into account all factors in how access to tax authorities are conditioned and understood.

Footnotes

Appendix

Overview of Focus Groups.

| FG | Sector | Specific labor category | Gender composition | Mean age | No. of participants |

|---|---|---|---|---|---|

| 1 | Informal | Plumbers | All male | 31 | 2 |

| 2 | Informal | Hairdressers | All female | 30 | 3 |

| 3 | Private sector | Retail | 2M, 1F | 34 | 3 |

| 4 | Private sector | Retail | 1M, 4F | 28 | 5 |

| 5 | Private sector | Bankers/economy | All female | 26 | 3 |

| 6 | Private sector | Hospitality | 2M, 3F | 27 | 5 |

| 7 | Private sector | Media | 3M, 1F | 38 | 4 |

| 8 | Private sector | Tourism | 2M, 3F | 34 | 5 |

| 9 | Private sector | IT-specialists | 4M, 1F | 28 | 5 |

| 10 | Private sector | Education/uni | 3M, 2F | 45 | 5 |

| 11 | Private sector | Nurses | 1M, 4F | 41 | 5 |

| 12 | Public sector | Teachers | 3M, 3F | 35 | 6 |

| 13 | Public sector | Correctional officers | 2M, 1F | 29 | 3 |

| 14 | Public sector | Civil servants, engineers | 4M, 1F | 30 | 5 |

| 15 | Public sector | Education/teachers | 1M, 4F | 31 | 5 |

| 16 | Public sector | Civil servants (business support) | 1M, 3F | 39 | 4 |

| 17 | Public sector | Civil servants/engineers/architects | 2M, 3F | 25 | 5 |

| 18 | Public sector | Correctional officers | All male | 33 | 3 |

| 19 | Public sector | Fire fighters | 4M, 2F | 33 | 6 |

| 20 | Public sector | Nurses | 1M, 3F | 40 | 4 |

Acknowledgements

The data collection for this article was conducted with the help of several research assistants (Johannes Shekeni, Ndapunikwa Fikameni, and Martha Nangolo) and with the cooperation of the Institute for Public Policy Research (IPPR) in Namibia. Five of the focus groups were conducted by Lise Rakner. The two authors contributed to the article in different ways. The authors are grateful for constructive reviewer comments and feedback from Joanna Britton.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The work for this article was funded by the Swedish Research Council (grant number 2016-05607).