Abstract

In addressing one of the least-researched areas in tourism—the formation of product strategies—this study focuses on the homogeneous package tour phenomenon. It draws on Industrial Organization theory to explore the impact of relationships between industry subgroups on the development of such products. With a specific focus on Chinese package tours to the UK, tour itineraries were firstly mapped to provide a visualization of relative homogeneity. Then, by examining the resource traits of participating firms, two subgroups in the industry were distinguished: tour operators (including wholesalers and retailers) and travel agencies (including Online Travel Agencies). It was found that the determination of product homogeneity involves a combination of the dependent relationship between tour operators; a more independent relationship between travel agencies; and the nature of the interdependence between the two. Strong bargaining power on the part of suppliers and weaker customer power further strengthened product homogeneity.

Introduction

Having an effective product strategy is a key determinant of a firm’s survival and performance. However, how such strategies are developed remains one of the least-researched areas in tourism (Aladag et al., 2020; Harrington et al., 2014). This is despite the enormous influence that firms such as tour operators and travel agencies wield over the purchasing decisions of tourists that flow from such strategies, with consequential impacts on destinations. Package tour products to foreign destinations are particularly sought after by groups that experience language and logistical barriers, notably in the case of Chinese tourists. It has been observed that product homogeneity is commonplace in markets where such barriers are prevalent (Ji et al., 2022). The applicable package tours are intensive consumers of the common pool of resources allocated to destinations, by conveying large tourist numbers to a small set of attractions worldwide, thereby disrupting destination ecosystems. This study seeks to explain the homogeneity prevalent in such larger-scale package tour products. The standardization question is also applicable to predictions about the future of long-haul international travel, following the full restoration of leisure travel after Covid-19.

A range of factors drawn from Industrial Organization (IO) theory might be expected to explain the greater product homogeneity amongst tour packages. Such factors would include the vertical integration of the tour operator with travel suppliers (i.e., airlines and hotels) (Klemm & Parkinson, 2000); the oligopolistic structure of the tour industry (Davies & Downward, 2007); and the normally high consumer demand for outbound travel (Porter, 1989), combined with low repeat visitation and inadequate destination knowledge (Chen et al., 2013). However, a potentially overlooked factor is that the relevant “industry” comprises a number of different clusters or subgroups of companies, with often differing systematic traits (Caves & Porter, 1977; Delgado et al., 2010). The nature of the inter- and intra-subgroup relationships which result may therefore play a part in the development of homogeneous products (Bain, 1968; Delgado et al., 2010). Furthermore, there is a continuing lack of clarity about how such relationships have been shaped by classic industry elements such as the relative bargaining power of suppliers and customers.

The present study applies the theory of subgroup relationships and key industry influencers to investigate the formation of homogeneous package tour products. It addresses the extent to which travel itineraries are homogeneous; how subgroup relationships are conducive to product homogeneity (including intra- and inter-subgroups); and how other classic industry players (i.e., suppliers, customers, entry barriers, and product substitutes) have affected such relationships, whether positively or negatively.

The specific research focus is the extent and nature of Chinese package tours to the UK. It was reported that China generated 128 million outbound tourists before the Covid-19 outbreak and had become the world’s largest market (UNWTO, 2018). A unique feature is the market’s reliance on package tours, which accounted for over 80% of China outbound travel (Hong Kong and Macau are excluded) (Zhang et al., 2011). Although China is only the UK’s 13th largest inbound tourist market by visitation, it is the country’s second biggest long-haul market in both tourist numbers and expenditures ($2.4billion). Its potential has been recognized by Visit Britain (the UK’s Destination Marketing Organization) even during Covid-19. It is forecast that the Chinese travel market will recover to 2019 levels by 2026 (VisitBritain, 2020). However, the repeated appearance of negative newspaper stories in the UK about the impacts of homogenous Chinese package tours is a continuing concern.

This research is the first to bring in the study of subgroup relationships and strategy formation to tourism. While scholarly conceptual publications in tourism drawing from IO started to appear from about 2012 (Aladag et al., 2020), performance assessment was the exclusive focus (e.g., Davies & Downward, 2007). Although the Resource-Based view of the firm (RBV) (Barney, 1991) appears to be a more popular approach, the current authors are surprised by the neglect of an IO perspective, since a firm’s competitiveness derives from the macro, industry-level nexus, as well as from deploying unique resources and capabilities (Tavitiyaman et al., 2011). This study pioneers a further innovative approach by considering the impact of classic industry influencers on subgroup relations. We believe that findings specific to tour operators can address a significant gap in understanding the formation of package tour products, with particular relevance to Chinese tour operators. Practical implications of the research are also explored for the recovery of long-haul travel post-Covid-19.

Literature Review

Product Homogeneity

Strategy encompasses two broad areas according to Bain (1968): the pricing policies of firms and the interaction, cross-adaptation and coordination process of policies adopted by competing sellers. The former involves the objectives pursued and methods employed in determining price and output; policies of product improvement or variation over time; and sales promotion policy (Bain, 1968). The latter includes the possible collusion which might arise when price setting and the level of pricing interdependence when anticipating a rival’s reaction (Bain, 1968). Porter (1989) further developed Bain’s notion of “product variation” by specifying three product strategies: cost leadership, differentiation, and focus.

Product homogeneity is an outcome of adopting a cost leadership strategy that is designed to reduce production and development costs, gain higher profit margin, and increase market share (Sitanggang & Absah, 2019). Companies deploying a cost leadership strategy can obtain enhanced competitive advantage and customer satisfaction as a consequence of continuous growth (Mortazavi et al., 2017). On the other hand, Banker et al. (2014) argue that companies have better opportunities to maintain their performance sustainably through a differentiation strategy. It has been suggested that companies providing unique products or services enjoy fewer perceived substitutes, larger profit margins and higher levels of customer loyalty (Panwar & Khan, 2020). However, Banker et al. (2014) warn that differentiation is less stable and riskier. Alternatively, by concentrating company resources on a niche market, a focus strategy allows companies to provide professional products and services, develop stronger customer relationships, and enhance brand reputation (Akintokunbo, 2018). All three product strategies have been associated with significant corporate innovation including of processes, products, and administration (Fathali, 2016).

Industry Subgroups and Relationships

An industry consists of various subgroupings of firms (Porter, 1979). Each subgroup is distinct, while the firms within each subgroup tend to resemble one another. Such structural differences can be attributed to distinctive resources and capabilities (Barney et al., 2001), and occur along dimensions that extend beyond size (Porter, 1979). These may include differential adoption of information technology, branding and organization structure (e.g., Tavitiyaman et al., 2011). Such subgroups do not generally enjoy equal market shares. In tourism and hospitality—particularly in the case of tour operating—it is commonly agreed that the industry is polarized, or oligopolistic, and is characterized by imperfect competition (Klemm & Parkinson, 2001). So-called “mega chain” tour operators comprise the oligopoly subgroup; vast numbers of small, independent operators make up the remaining market (Davies & Downward, 2001). Each subgroup is differentiated in terms of product strategy, in that chain operators use low-cost strategies, whilst small operators often deploy differentiation strategies (Carey et al., 1997). Chain operators earn a low margin of about 5% (Curtin & Busby, 1999; Klemm & Parkinson, 2001; Tapper, 2001), albeit on significant sales volume. By contrast, small operators can earn twice as much—though on a much smaller volume of sales (Carey et al., 1997). These group distinctions align with Bain (1968)’s oligopolistic structure hypothesis that consists of an oligopolistic core and a competitive fringe of small sellers. The former features a small number of sellers supplying significant market share. The latter, ranging from few to relatively many, supplies so small a fraction of the market that their own price and output will not noticeably affect the welfare of other sellers in the industry.

The relationships between the two subgroups provide a general reference point for product strategy formation. It is generally postulated that there is greater mutual dependence within a subgroup than between subgroups (Porter, 1979). However, Bain (1968) in contrast hypothesized a more “contained” relationship between the two subgroups, in which many small sellers in the industry capitalize on whatever joint profit maximizing or other policies that are pursued by sellers in the oligopolistic core. They enhance their market share by charging prices that are lower by the amount that most profits them. The oligopolistic sellers consequently have to set pricing policies that will contain the smaller sellers or, at any rate, avoid a rapidly increasing market share. However, the impact of this small fringe is restricted by competitive disadvantages relative to larger firms—most frequently in the form of higher production costs or of products adjudged as inferior by consumers. Larger sellers may be able to establish prices well above their own costs, though below the maximum level. The configuration of these subgroup relationships can determine industry competitiveness, as well as its product outputs and overall profitability (Caves & Ghemawat, 1992; Mazzeo, 2002).

The relationships within subgroups also impact on the formation of product strategies. Within the oligopolistic core, firms recognize their mutual interdependence and tend to agree, either expressly or tacitly, to joint profit-maximizing policies and are somewhat deterred from independent profit making and antagonistic actions by the threat of retaliation (Bain, 1968). Such cooperative relationships can enhance their market shares, maximize industry price, and sustain product profiles. Davies and Downward (2007)’s study of UK tour operators, found that pricing is more attributable to a firm’s own sales volume and profit margin, and less on competitor prices, thereby maintaining stability and goodwill within the sector. The strength of the cooperative relationship depends on fulfilling the following conditions, namely that: (a) sellers are sufficiently scant and have large enough market shares to recognize their mutual interdependence; (b) market share at any common price is equal; (c) their cost conditions are identical; and that (d) a price or output change by any seller will be known about immediately and draw an instantaneous response from rivals. On the contrary, within the competitive fringe of small sellers, firms are independent and prone to pursuing independent price and product policies to maximize their advantage.

The relationship between subgroups can remain stable according to Caves and Porter’s (1977) concept of mobility barriers. Mobility barriers deter new entrants from entering a subgroup or switching between subgroups because the barriers support existing firms and provide significant advantages over new entrants. The advantage can be established on the basis of product differentiation, absolute cost and scale economies (Bain, 1968); capital requirement, access to distribution channels and government policy (Porter, 1989). Studying the consumer and industrial goods markets, Karakaya and Stahl (1989) found that the most important entry barrier was cost advantage.

Subgroups in the Chinese Outbound Tour Service Industry

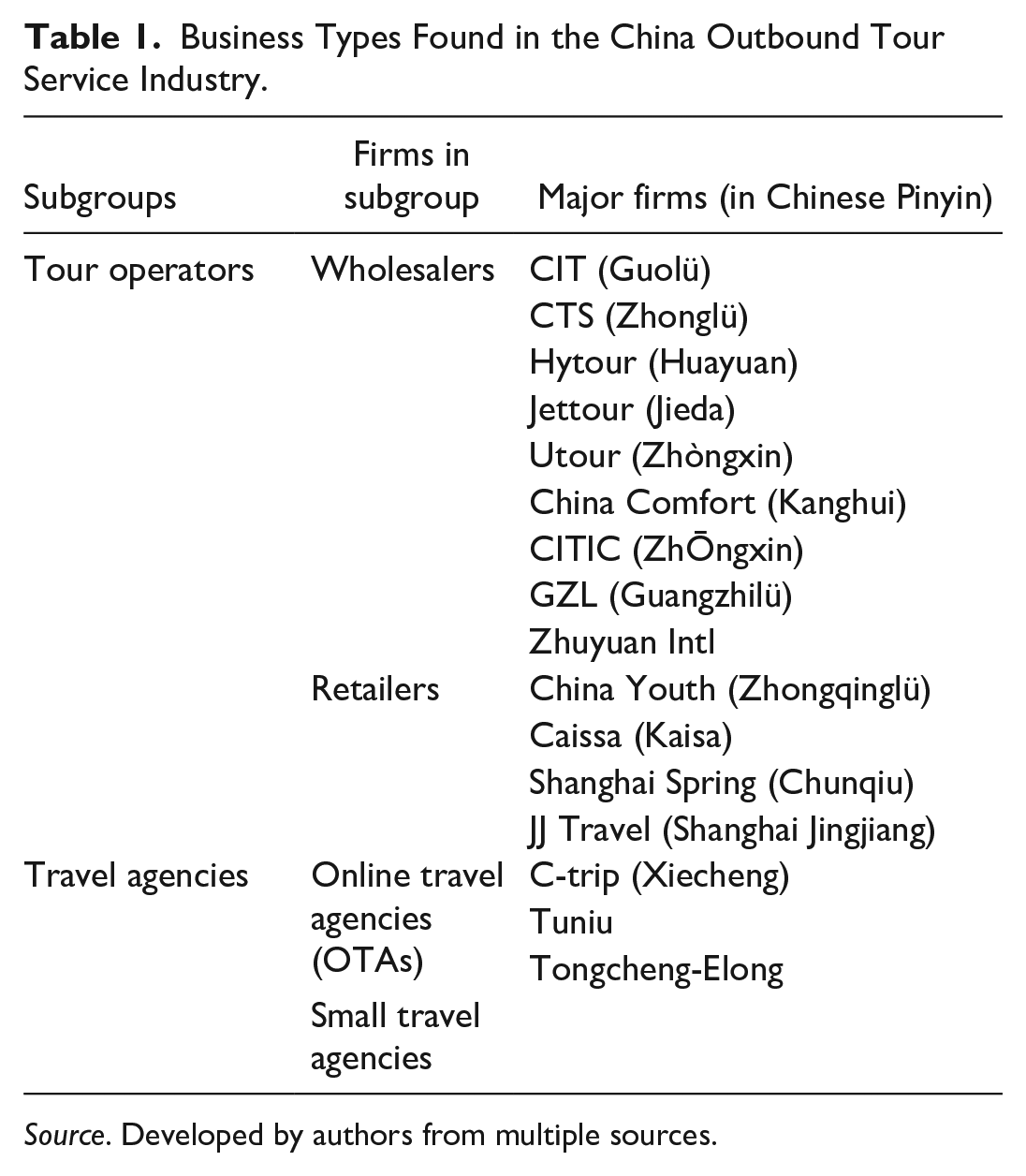

As defined in the UNWTO Tourism Satellite Account (TSA), “tour operators” are businesses that combine two or more travel services (e.g., transport, accommodation, meals, and sightseeing) and sell them indirectly through travel agencies, or directly to end consumers, as a complete package tour product. However, particular characteristics are evident in the case of the Chinese tour service industry. There were 40,682 registered travel operators and agencies in China in 2020 (Bank of China Securities, 2021), of which around 3,700 were licensed to operate outbound tours (GF Securities, 2017). China outbound tourism is viewed as lucrative, creating revenue of ¥168.4 billion (about $26,622 billion) and accounting for 44.93% of total sales (GF Securities, 2017). 85% of the outbound tours are to Asian countries and 5% are destined for Europe. The Chinese industry diverges from the UNWTO definition by comprising four types of operation: (1) wholesalers, (2) retailers, (3) small travel agencies, and (4) online travel agencies (OTAs) (Tebon Securities, 2019) (see Table 1).

Business Types Found in the China Outbound Tour Service Industry.

Source. Developed by authors from multiple sources.

The first two types share a common capacity to develop tours. Wholesalers are few in number and were originally established as government departments. Benefiting from historical advantages, they have enjoyed ready access to travel suppliers such as airlines and hotels (which were originally state-owned). Their major business has been to design and wholesale their products to other types of tour operations. In recent decades, they started to operate their own “high-street” agencies, and to reach out to consumers. However, the wholesale trade still accounts for most of their business. In 2017, for example, 65% of total sales by the biggest wholesaler—Utour—derived from the wholesale trade (TravelDaily, 2017). Retailers comprise the second type of business and had a high street presence from the start. They sell to consumers as well as wholesale their products. However, the distinction between wholesalers and retailers is increasingly blurred (Bank of China Securities, 2021).

A feature common to both small travel agencies and OTAs is their distribution of products developed by the first two types (i.e., wholesalers and retailers). Though some small and online travel agencies develop their own international package tours, these are limited in scale and predominantly for private and customized tours (TravelDaily, 2013, 2017). Small travel agencies focus on providing package tours and secure advantage by offering face-to-face advice. It is worth stressing that, despite studies highlighting the threat from OTAs to tour operators, OTAs have a continuing focus on selling overseas leisure components such as flight tickets, hotel bookings and/or attraction admissions.

It is widely believed that the current industry structure of Chinese tour operators is mildly concentrated, with only 35% of sales made by wholesalers and retailers (Tebon Securities, 2019). However, these firms control the resources to develop package tours. Given the research aim of examining package tour product strategies, the four types are categorized into two subgroups: one with tour products and one with no such products, termed “tour operators” and “travel agencies” respectively (see Table 1).

The Impact of Suppliers, Consumers, and Substitute Products on Strategy Formation

According to Porter’s (1981) Five Forces model, strategy formation is influenced by multiple forces, notably suppliers, customers and the threat of substitute products. The following discussion considers the impacts of Porter’s thinking on package tour strategies.

Suppliers can exert power over sellers by either raising prices or by reducing the quality of purchased goods (Porter, 1981), hence increasing the product cost. In the tourism business, travel suppliers constitute the essential components, namely transportation, accommodation, and attraction ticketing. The capacity of hotels, flight scheduling, and frequency of flights determines the quality and breadth of product options. Furthermore, the perishability of these services necessitate quick sale to maximize revenue (Guilding & Ji, 2022). Consequently, suppliers seeking to sell their services must maintain long-term relationships with tour operators, particularly those with excellent sales records (Kanani & Buvik, 2018). On the other hand, as supplier prices determine the overall cost of a package tour, tour operators should also maintain a close relationship with suppliers in order to secure discounts (Klemm & Parkinson, 2001). This close-knit association provides substantial advantages to both parties and forms a significant barrier to mobility between subgroups. Therefore, it is hypothesized that the number of suppliers and their ties with tour operators are significant in maintaining relationships between subgroups.

Customers can develop preferences for competing products over others on the basis of quality or design, product/service knowledge, product/service reputation and value, and promotion (Bain, 1968). When customers have strong preferences, they can demand product innovations, higher quality or more service, pushing down prices, and playing competitors off against each other at the cost of industry profits (Porter, 1989). However, Chinese consumers are inexperienced in international travel, have limited access to independent travel advice (Jørgensen et al., 2018), and are constrained by language barriers (Jin & Sparks, 2017). They therefore seek out travel agency offerings (Chen et al., 2013), unconcerned about the prospects of tour homogeneity. Furthermore, strong demand for Chinese outbound travel has given firms an incentive to use an undifferentiated product strategy (Mazzeo, 2002).

Products with high potential for substitutes can experience a price ceiling as a result of low switching costs, hence reducing profit (Porter, 2008). Conversely, product differentiation can enable profits to grow (Bain, 1968). Furthermore, although product differentiation can create entry barriers, a concentrated market does not necessarily stimulate greater product variation. These may be limited due to scarce natural resources or patent controls (Bain, 1968). It is nonetheless generally agreed that the competitive relationship tends to be stronger in high substitute scenarios and less so in differentiated ones (Mazzeo, 2002). Consequently, product substitutes can affect firm relationships within subgroups where homogenous products are sold.

Summary: Theoretical Framework

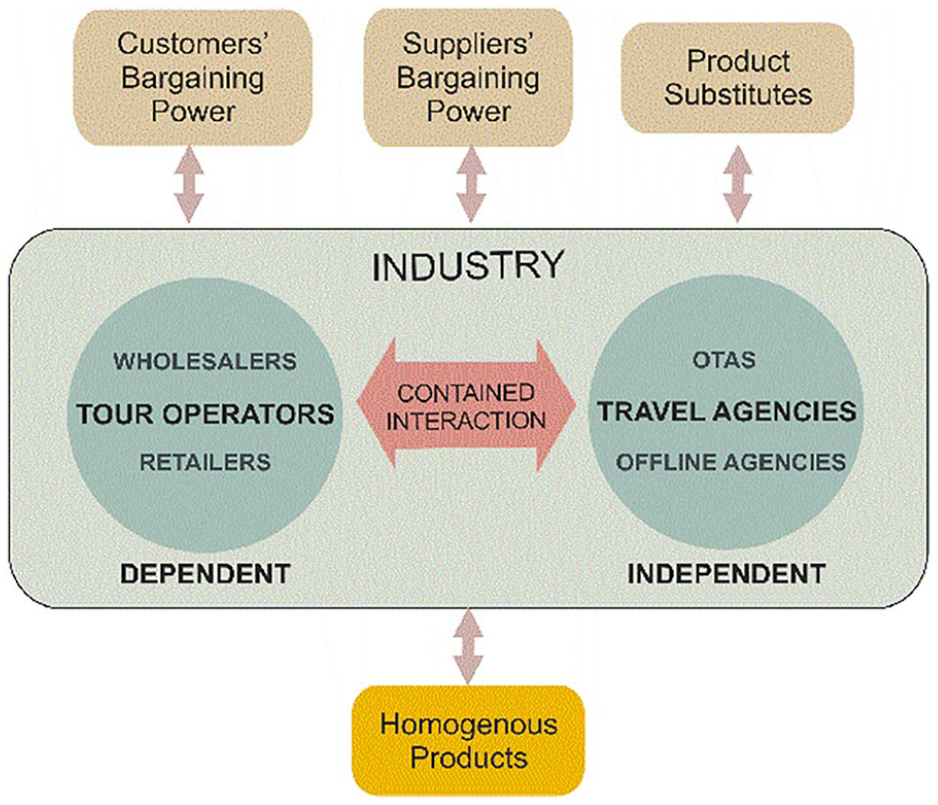

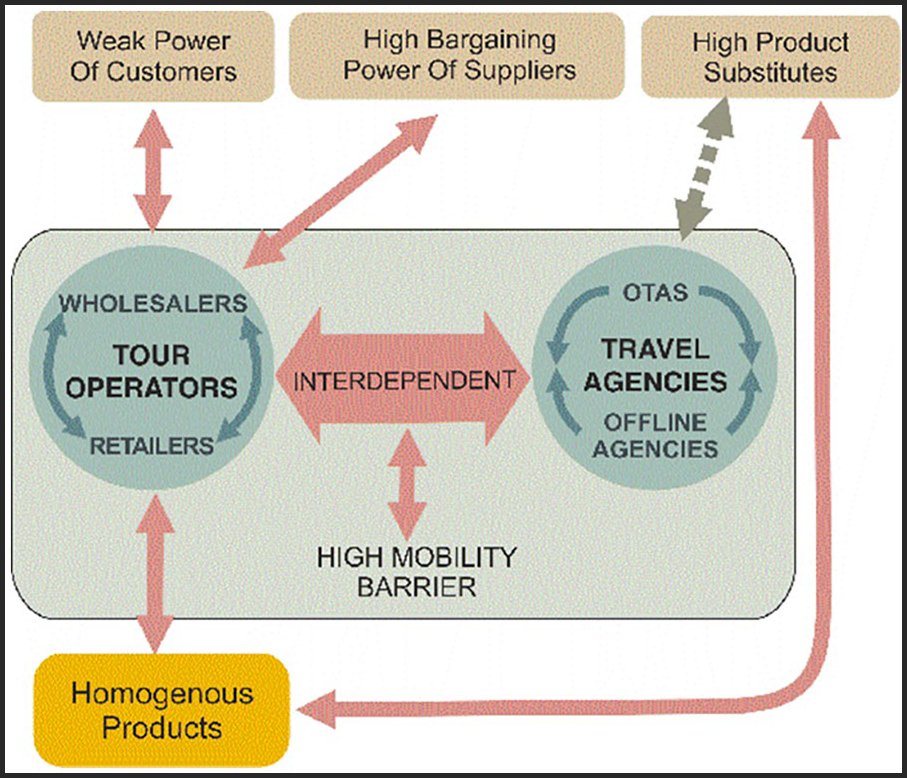

Our proposed framework (Figure 1) consolidates insights drawn from the literature and explains how homogeneity in Chinese package tours derives from subgroup relationships (i.e., tour operators versus travel agencies), as well as from major industry players (i.e., consumers, suppliers and substitute products). A “dependent” relationship is proposed between wholesalers and retailers within the tour operator subgroup, which promotes greater product homogeneity. Amongst the travel agency subgroup, it is proposed that a highly “independent” relationship exists between OTAs and small agencies. It is suggested that the relationship between both subgroups is “contained..” Lastly it is suggested that industry players can work to either weaken or strengthen these proposed relationships.

Theoretical framework.

Mixed Methods

The study adopted a mixed-methods approach, involving secondary and primary data, including interviews, to generate a visualization of product homogeneity. The authors extracted secondary data from the websites of Chinese tour operators that make reference to UK group tour packages. This visualization provides a foundation for exploring the ways in which homogeneity has occurred.

Secondary Data Collection

Systematic data collection was undertaken to ensure that the sample was fully representative of Chinese group tour packages into the UK. The China Tourism Academy definition was adopted, including a tour operator’s market share, competitive advantage, operational performance, business strategy, and financial position (CTA, 2019). The top 13 tour operators were selected, comprising 85.5% of package tours to the UK (GF Securities, 2017). Tour itineraries from China to the UK were extracted from the firms’ websites (Supplemental Appendix 1) during the period 8th to 18th July 2019, the peak booking season to the UK. To avoid sampling errors that could be associated with the concentrated period of data collection, interviewees were asked to confirm that no other itineraries were available outside this period.

Primary Data Collection

Our research approach aligned with Charmaz’s (2006) constructivist grounded theory. Charmaz’s development of grounded theory adopts the middle ground between positivism and postmodernism; it assumes the “relativism of multiple social realities, recognizes the mutual creation of knowledge by the viewer and the viewed, and aims toward interpretive understanding of subject’s meanings” (Charmaz, 2006, p. 250). This position posits that neither data nor theories are “discovered” but are instead constructed jointly by researchers and participants through interactions and emerging analyses.

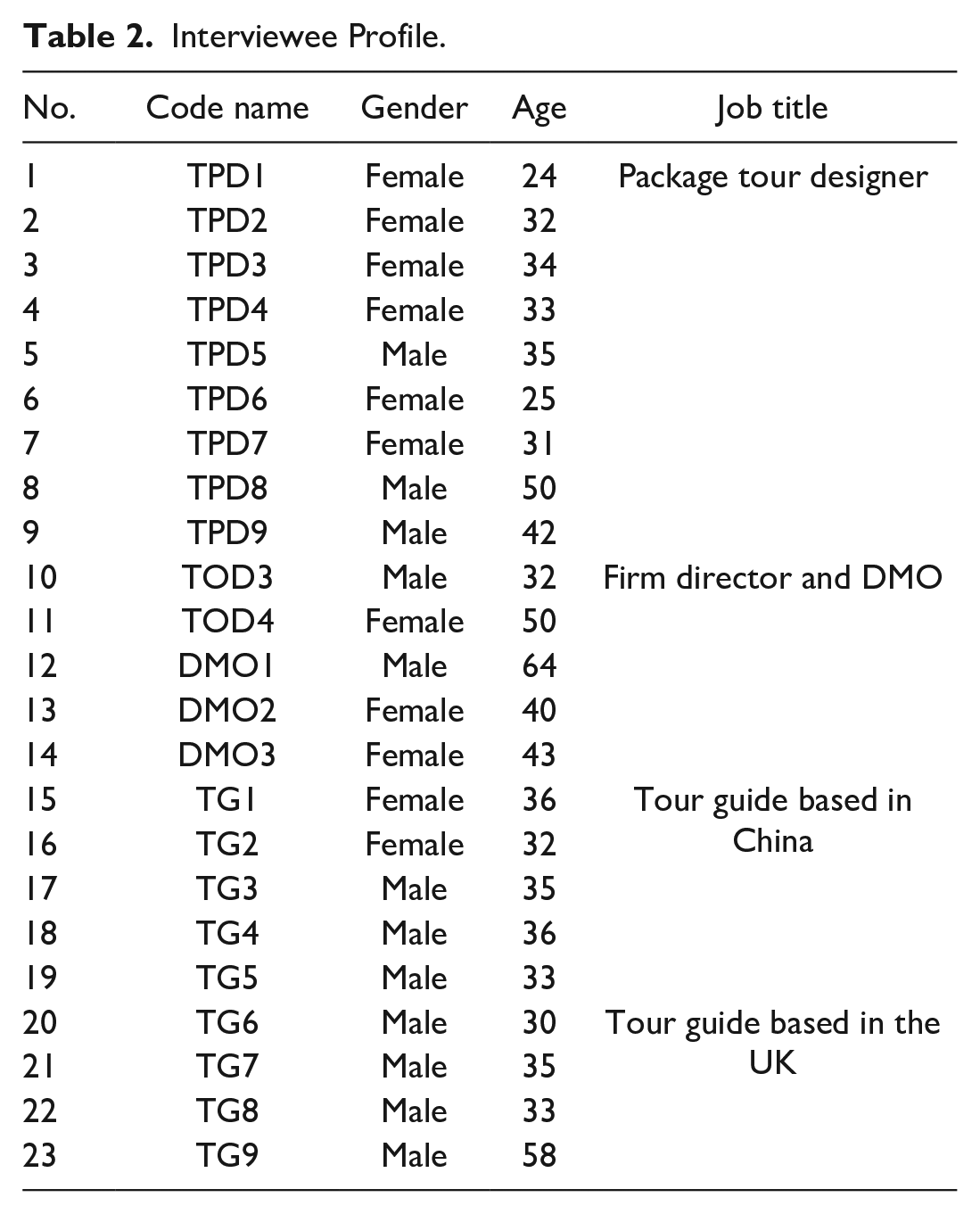

Interviewees were selected according to the following criteria (Patton, 2015): (1) package tour designers, chosen for their knowledge of operating constraints and of the uniqueness of their own products and those of competitors; (2) high level officials at DMOs or senior managers in tour operators, chosen to provide an overview of the macro structure of the outbound travel industry and insights into subgroups, negotiation and relationships with suppliers, and a clearer vision of product development; and (3) tour guides because they would understand any similarities between tours and would tend to receive immediate feedback from consumers about their travel experiences. Collectively the interviews were chosen to provide details of the nature of and relationships between the various industry players outlined in the research framework. A total of 23 interviews were conducted (Table 2).

Interviewee Profile.

Snowball sampling was used to recruit participants since it enabled interviewing of familiar and trusted individuals, thereby increasing participation (Hennink et al., 2020). Qualified participants were initially identified from the lead author’s social network, including her graduate alumni who worked in tour operators or travel agencies in China. Interview data were collected between December 2019 and October 2020, following research ethics approval by the lead author’s institution and participation consent from interviewees. Semi-structured in-depth interviews were conducted virtually on WeChat and followed an interview guide. Each interview was conducted in Chinese and lasted from 60 to 90 minutes.

Secondary Data Analysis

The study applied Line Density and Hotspot analysis to determine package tour itinerary product features (i.e., differentiated, homogeneous/standardized, or focused).

Primary Data Analysis

Interview records were transcribed by a specialist third-party firm. While constructivist grounded theory empowers interview respondents, the ultimate power to interpret the interviewee accounts resides with the researchers. Reflecting on the attendant risks (Finlay & Gough, 2003), the first two authors undertook independent coding of the first two transcripts, then shared and compared the codes, discussing any discrepancies until reaching agreement. A codebook with description of the codes (see Supplemental Appendix 2) was developed incrementally to ensure consistency and the same codes were applied to all transcripts.

The authors started with initial (or “opening”) coding which was applied line by line and paragraph by paragraph, based on research questions. These initial codes were treated as provisional and open to modification and refinement to improve their fit with the data. This process involved revising existing codes, and constructing new, more elaborate codes by merging or combining identical codes, through constant back-and-forth comparison between codes and codes, as well as codes and data. As a result, focused (or “selective”) codes were generated. These were more representative and conceptual than the initial codes (Charmaz, 2006). With the focused codes, researchers were able to devise tentative conceptual categories, thereby giving them conceptual definitions and enabling them to assess interrelationships. When progressing to the final stage—theoretical coding—the researchers followed the guidance of “abduction” and analyzed how focused codes might relate to each other in order to formulate hypotheses and eventually a theory (Thornberg & Charmaz, 2014). Supplemental Appendix 3 presents examples of the coding procedure using NVivo.

The researchers engaged in memo writing as they were collecting and analyzing data, noting ideas about codes and their relationships. All interviews were initially transcribed into and analyzed in Chinese to retain accuracy and any rich data that might be lost in translation prior to the confirmation of key findings—at which point translation into English was performed. The accuracy of the translations was checked by the authors with proficiency in both Chinese and English.

Major Findings and Discussion

The typical tour group size was between 25 and 40 tourists. The average length of itinerary was 11.7 days, including 2 days spent flying. The itineraries were all-inclusive and cost approximately ¥20,840 (about $3,105) including return air fare, accommodation, meals, and admission to attractions. In this section, we discuss: (1) the nature of the applicable package tour product development strategy (differentiation, lost-cost/standardized, or focused); and (2) how such a product strategy has been formulated. Finally, we provide a high-level summary of product strategy formation.

Product Homogeneity

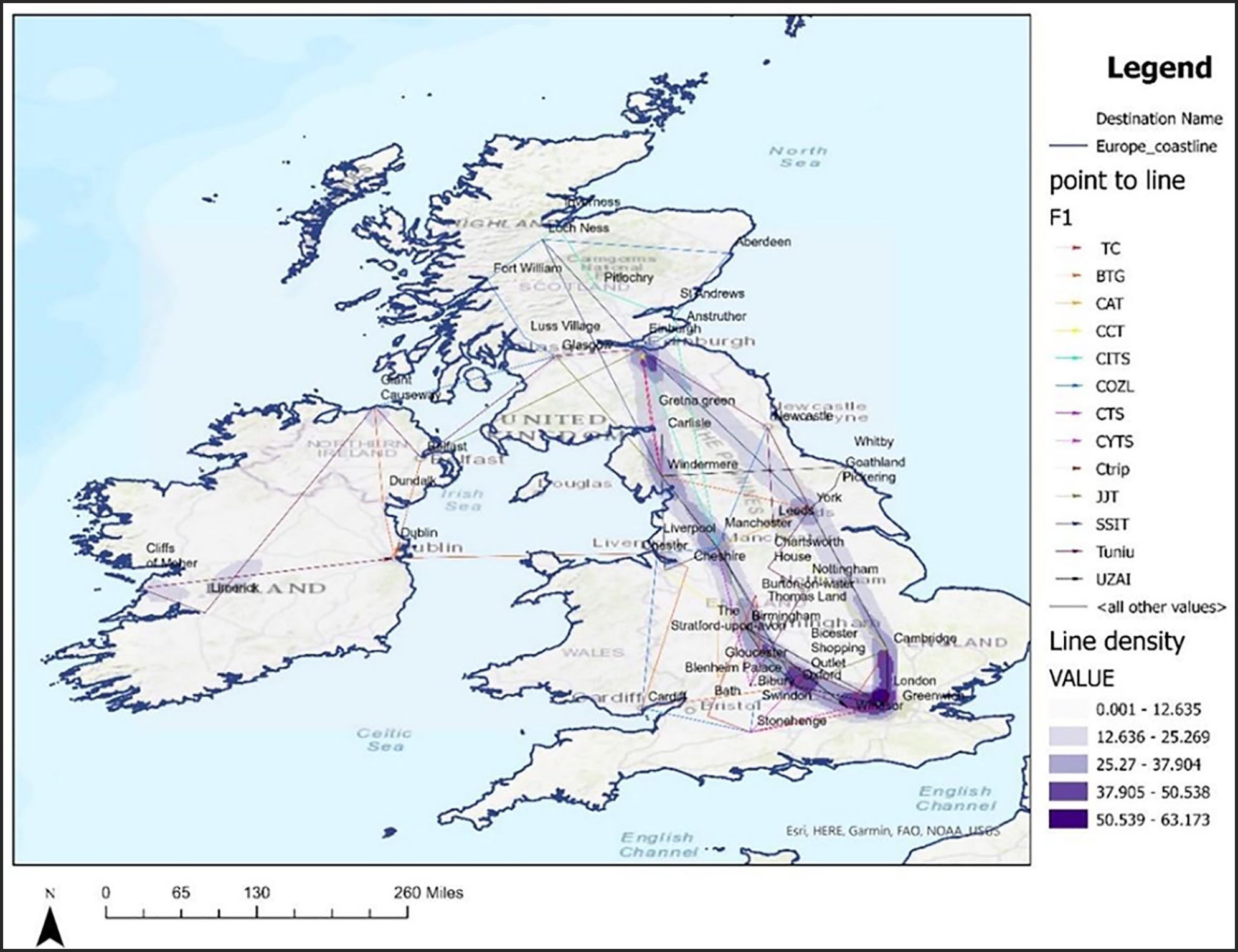

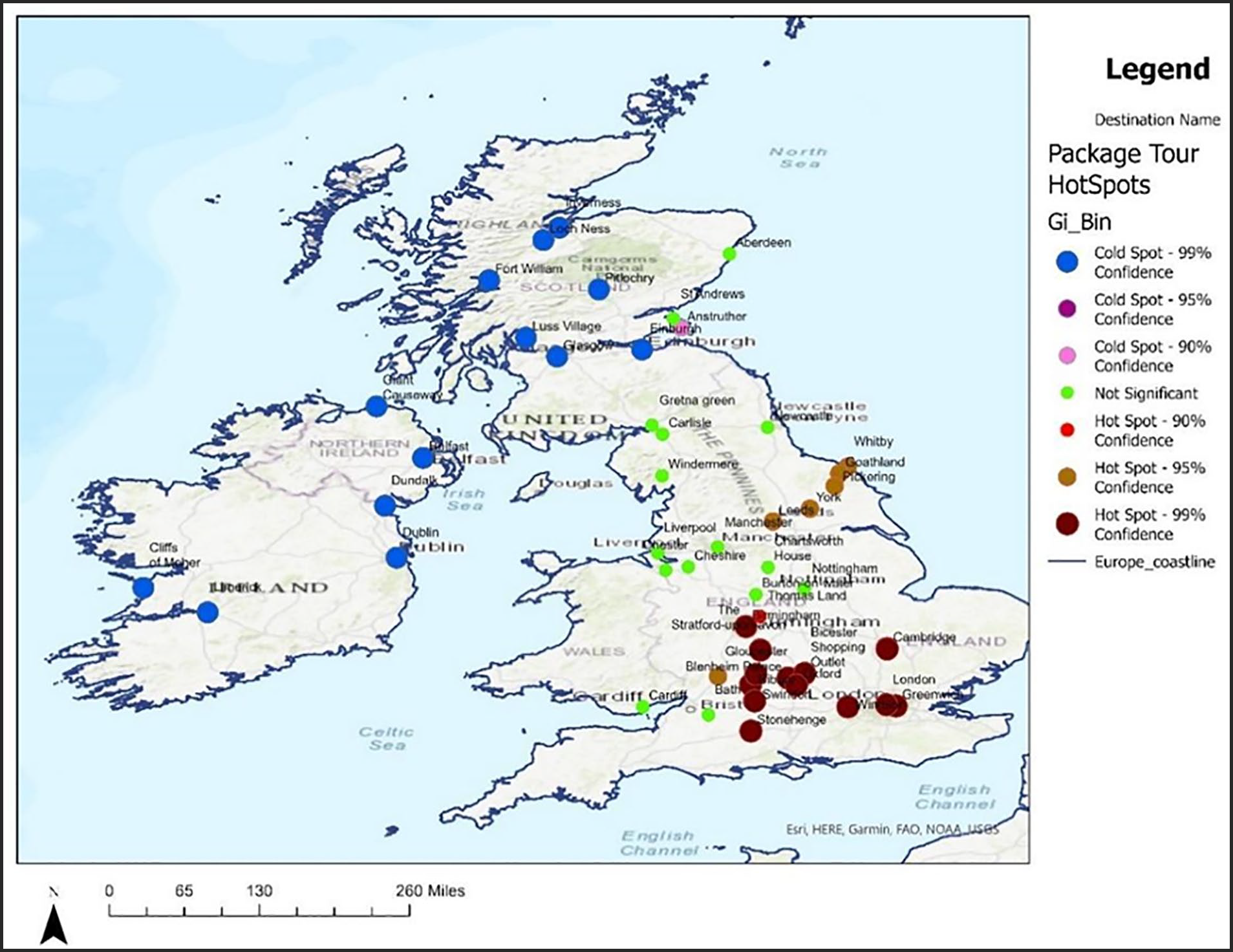

To examine the features of the tour itineraries, line density and hotspots analysis were deployed because they provide an effective visualization of the distribution of points of interest (Yuill, 1971). Our line density analysis (Figure 2) shows a high concentration of routes, in a broadly oval shape, covering Edinburgh, the Midlands, southeast England and London. Other parts of the UK are hardly visited, notably Wales and the west of England. Two main route types are identified: “close circle” and “open linear” (the classification is based on whether the same airport is used for landing and departure). The close circle pattern is separated into anticlockwise and clockwise patterns. The linear pattern can then be divided into domestic and international itineraries, depending on whether Ireland is included. In the close circle pattern, the itineraries cover many of the same destinations such as: London, Oxford, Cambridge, Windsor, Manchester, York, and Edinburgh. Belfast and Dublin are the main destinations in the linear pattern. Overall, the patterns show high convergence, with the clockwise closed route being the most commonly operated itinerary (n = 7), followed by domestic linear (n = 4), and the least being anti-clockwise closed and international linear (n = 1). It is evident that all routes have high levels of concentrated convergence, with some scattered diversity in Scotland and Ireland. The hotspot analysis (Figure 3) identifies hot, cold and insignificant points of interest. Hotspot cities are concentrated in London, Oxford, Cambridge, Birmingham, Stratford-upon-Avon, Bourton-on-Water. The places of interest to Chinese package tours differ from those favored by Australian and American package tourists (VisitBritain, 2020). Interested readers may refer to Ji et al. (2022) for more detailed analysis.

Line density analysis.

Hotspots analysis.

The Formulation of Product Homogeneity

Subgroup relationships

Our first finding is that relationships between two subgroups—tour operators and travel agencies—are interdependent rather than contained. Tour operators recognize that profit relies on volume of sales—“a tour cannot depart if the number of tourists in it is small – that means losing profit” (DMO2). There is additional pressure on tour operators to sell tours quickly because tours and airfares are perishable. They must use travel agency networks as well as their own distribution system. “The tour operators need as many travel agencies as possible to distribute their products to reduce their operation risks” (TOD3). What strengthens this relationship is that travel agencies have no products and must obtain them from tour operators. However, the tour operators are selective in giving away products. Only less mature products of moderate-high risk are made available. Some firms permit travel agencies to market in their own ways or even to set their own prices. Meanwhile, the more mature and promising products are sold through the tour operators’ own high-street offices, thereby enabling them to secure higher profit margins.

Secondly, there is fierce competition between OTAs and small travel agencies within the travel agency subgroup, as observed by interviewee TOD3 “Price wars exist among travel agencies - they need to attract customers with similar products.” This confirms the impact of high substitutability in starting price wars (Bain, 1968; Marshall & Parra, 2019; Porter, 2008). As a consequence, both types of firm seek to differentiate their products. One strategy is to choose the products from the tour operators that provide opportunities to “add their own character” (TG3). Although most OTAs and some small agencies offer customized tours, they are still relatively underdeveloped (TravelDaily, 2017). The current advantage of OTAs still involves their providing “one-stop price comparison” and “online payment” (TPD7) which appeals to younger tourists (Talwar et al., 2020). However, the small agencies remain secure because tourists have to sign paper contracts to complete a package tour purchase, which can be only done in an office setting. Tourists typically use OTAs to compare prices and then visit a travel agency to find the best deal, sign the contract and pay (TPD7). Consequently, increased competition has pushed OTAs to grow their high-street offices, notably in second- and third-tier Chinese cities; at the same time, offline agencies were adopting an “offline-to-online” strategy to increase their online presence (TravelDaily, 2017).

Thirdly, within the tour operator subgroup, the relationship between wholesalers and retailers is confirmed as generally harmonious and dependent, tending to be most cooperative when launching new, or jointly developing less mature routes. An interviewee (TOD4) remarked “When we promote new products and where the demand is uncertain, we have to collaborate with other tour operators to minimize risks. The price competition among tour operators is moderate.” There is wide scholarly support for such rational relationships between monopoly/oligopoly firms. For example, Davies and Downward (2007) identified that the pricing strategies of UK tour operators were based more on juggling between their own sales volume and profit factors, instead of benchmarking against competitors’ prices or market conditions. It has been important for maintaining stability and goodwill within the sector (Davies & Downward, 2007), confirming the motivation of avoiding retaliative action from rivals (Bain, 1968). Indeed, as stated by interviewee TOD4, “Big tour operators [wholesalers and retailers] care about their brand images in the public eye so they like to set fixed and consistent prices on their products.” Although retailers also sell wholesalers’ products, wholesalers are more standardized and compete on sales volume, while retailers are relatively specialized and have a stronger brand image (TPD8). Relationships between wholesalers and retailers are generally cooperative.

As a result, both subgroups prefer standardized products because they are “convenient” and “transferrable” and because “[the] same routes enable different travel agencies to bring together their respective customers and regroup them at the airport. As tours become bigger, running costs are reduced bringing lower prices for the consumers, so this benefits both consumers and the businesses” (TOD4). Such interdependence enables tour operators to take advantage of travel agencies, growing their market share quickly and realizing economies of scale, leaving the small tour agencies with no grounds to compete and further widening the barriers to mobility between subgroups.

High mobility barriers between subgroups

There are high entry barriers between subgroups. They are created by the availability of resources to develop products. The first type of resource is the possession of strong cash flows. Airlines and hotels demand advance payments (“capital”), which constitute the most essential elements of a package tour. As one interviewee (TOD4) suggested: “Cash is the most critical resource as it secures destination, airline and hotel resources”. Insufficient capital has handicapped small travel agencies in developing products. The second resource type involves long-term successful cooperation with major tour suppliers through a network, including those in international destinations. The network is established and secured by a tour operator’s record of consistent sales. Consistency gives confidence to suppliers and also provides tour operators with “the privilege to hoard seats and sometimes those on newly opened air routes” (TOD4). By contrast, because travel agencies lack network access they cannot develop new itineraries, let alone replicate existing ones.

Brand image (or “reputation”) is the third identified resource. The OTAs and small agencies are regarded as less reputable, particularly “risky and unreliable” due to lacking a physical presence (TOD7). By comparison, tour operators are perceived as more “reliable to fulfill the contract,” “resourceful”, and as having a “professional attitude”, “high service standards” and as being “more experienced to deal with emergencies abroad” (TG1 and TG6). This confirms Chen et al. (2013)’s findings on how tour operator reputation and brand image can affect Chinese consumers’ purchasing decisions. The last resource type involves destination knowledge (so-called “specialized knowledge”). It is observed that “Most staff of travel agencies might never have visited the UK. They lack the specialized knowledge to develop tourism products” (TOD3).

The study findings confirm the presence of most types of resource that general tourism firms demand (Mandal et al., 2016). The impact of a strong network with other tourism suppliers evidently secures competitive advantage (Çakmak et al., 2018; Denicolai et al., 2010; Duarte Alonso, 2017). A further contribution of this research is the re-classifying of capital as an inimitable resource and as the most significant source of competitive advantage.

Finally, tour operators enforce sales agreements on travel agencies to ensure product sales and minimize agency costs. They also dedicate a department to monitoring performance. Such agreements not only stipulate tour package price, commissions and incentives but also the customer service standards for travel agencies. One interviewee (TOD4) stated that “The main duty of travel agencies is to follow our standards, sell our tour packages and communicate with customers. If their selling performance is good, we give additional commissions, or award them with a free trip aboard. They can also use this travel experience to persuade consumers.” In addition, tour operators also develop product brochures for agency use. Through such means, they standardize marketing discourse and ensure a consistent information flow from tour operator to travel agency. As stated by interviewee TOD3, “Their knowledge [travel agencies] about an itinerary is totally passed down from tour operators.”

As possessors of the resources, tour operators are able to engage in itinerary design. Travel agencies have none of their own products and generate business from distributing existing products to end consumers. As was stated by Interviewee TOD3: “Nearly 80% of UK tourism products are from several, countable, major tour operators. They control resources, design itineraries and set the [service] standards. It is inevitable that travel agencies have to sell tour operators’ products, because they do not have airline resources and product design ability.”

Impacts of substitutable products, customers and suppliers on product homogeneity

The interdependent relationship between subgroups generates highly substitutable products. This, nonetheless, gives travel agencies an unexpected advantage because they can switch to whichever firm offers better commissions. In light of this, “. . . tour operators need to offer attractive commissions to attract the travel agencies because they are likely to choose the best deals” (TOD3). Travel agencies can also be selective amongst homogeneous package tours and even “resist standardized itineraries offered so we [the tour operators] have to adjust our products a little bit to differentiate ourselves” (TOD4). In other words, a plethora of substitute products gives bargaining power to travel agencies. They can both secure profits and potentially challenge the stable inter-subgroup relationship, thereby making some demands on tour operators to diversify their products. The threat of substitution complicates the relationship between firms. On the one hand, an elevated level of substitutes brings sales volume and economies of scale (Bain, 1968), and enables tourists “to compare products easily and . . . increase price transparency” (TG1). On the other hand, it risks disrupting inter-subgroup relationships and stimulates product innovation.

It has been established that customer bargaining power is weak because of inadequate destination knowledge. Customers rely on tour operators to inform their travel plans (Jin & Sparks, 2017). The “bandwagon” effect associated with Chinese culture further promotes tour uniformity. The bandwagon involves a tendency to seek a sense of belonging or security by buying products identical to a customer’s reference group (Mainolfi, 2020). As was remarked by interviewee TG6 “the Chinese believe the more people choose, the better the purchase decision.” Therefore, “it is much easier to sell a package tour of 30 persons than a package tour of 15 because the bigger group infers popularity and quality” (TPD1). Furthermore, “if they haven’t visited iconic destinations, such as the British Museum, Cambridge and Oxford, they would feel like they haven’t been to the UK” (TOD4). Customers feel capable of differentiating between seemingly similar products, though not on the basis of destination knowledge but rather a firm’s reputation and brand image and on the product service aspect, notably hotel rankings and the quality of meal inclusions. “Chinese tourists tend to be very careful. They want to minimize the costs, traveling risks and maximize the experience” (TG1). In response to this concern, tour product variation is based mainly on service standards.

Suppliers, and particularly airlines and hotels, have considerable power over tour operators because their prices determine package tour costs and profits. To secure a discount and to minimize costs, tour operators maintain the relationship through strong sales records. As mentioned by interviewee TPD6, “The relationship with the airlines depends on sales performance – good records ensure long-term relationship.” Tour operators felt the pressure of materializing pre-bookings, as was noted by interviewee TOD4: “We spend as much as ¥5,000,000 annually ($761,730) in booking air fares. Because we sell more seats, we maintain successful cooperation with airlines. That gives us the priority to the future bookings not only in the existing routes but also the new ones.”

Toward a Theory of Industry Structure and Product Homogeneity

Figure 4 presents the major theoretical contribution of this study. It explains the formation of homogeneous products from the perspective of subgroup relationships and impacts created by the industry players. Product homogeneity is a consequence of varied relationships within and across subgroups, along with the bargaining power of consumers and suppliers and the level of product substitutes. Though the current research confirms prior conclusions about external network resources (Abrate et al., 2020), it has been established that these are mostly owned by wholesalers of the tour organizing business, indicative that they have exclusive control over subsequent operational and dynamic capabilities. Furthermore, with the classification of the tour organizing industry into wholesalers and retailers, buyer-supplier relationships should be categorized accordingly (e.g., Pan et al., 2007).

Product strategy formation of package tours.

The dependent relationship between wholesalers and retailers in the tour operator group and the independent relationship in the travel agency group support Bain’s original hypotheses (1968). This relationship also resembles the UK product strategy setting in that pricing (and products) should not seek to outcompete rivals (Davies & Downward, 2007), but rather maintain stability and goodwill within the sector. The dependent relationships between wholesalers and retailers dis-incentivize product variations, thereby perpetuating existing market shares. On the other hand, fierce competition between OTAs and small travel agencies in the tour agency group is a result of selling similar, substitutable products. This accidentally encourages the subgroup to add their own personality into the products handed over to them, thereby challenging product homogeneity.

Contrary to prior understanding, the inter-subgroup relationship is identified as “interdependent” instead of “contained” (Bain, 1968). This interdependent relationship resembles Das and Teng’s (2000) notion of the unilateral contract-based alliance that is formed to share “property-based” resources such as capital and distribution channels. Furthermore, cooperation tends to be established when both firms occupy a vulnerable strategic position or else need resources (Czakon & Czernek-Marszałek, 2021; Eisenhardt & Schoonhoven, 1996). It is worth noting that such interdependent relationships depend on the extent to which both subgroups possess complementary resources. Indeed, what a firm possesses not only determines its competitive advantage but also its reaction to other firms and strategies (Das & Teng, 2000). Firms in the tour operator subgroup possess important resources enabling them to develop products, and set industry prices, hence determining profit. Though the competitive tour agency subgroup has none of these resources, firms sell their products through their own distribution networks. Furthermore, this interdependent relationship is secured by contracts. On the one hand, such contracts grant access to each other’s resources: for the travel agent to access the product and for the tour operator to access wider distribution channels. On the other hand, the contracts also ensure that consistent marketing discourse flows from tour operators to travel agencies and then onto customers. The interdependent relationship perpetuates standardized products, increases mobility barriers, and enhances competition in the tour agency subgroup.

Other forces exert either enhancing or weakening effects, or otherwise moderate the interdependent relationship. The concentrated nature of tourism suppliers and how they coordinate to form package tours offers little opportunity for diversification and perpetuates a homogeneous product profile. A pipeline of research and development has long been regarded as the key resource to product innovation (e.g., Li & Atuahene-Gima, 2001). Innovative package tours are derived from the components including transport, accommodation, attraction ticketing, and destination knowledge, which pull together all the resources. However, there is widespread horizontal integration in the airline industry (Klemm & Parkinson, 2000), which constrains choice in organizing tours, due to flight scheduling and frequency issues, price, and the selection of landing/departing cities. Ji et al.’s (2022) study of Chinese package tours to the UK demonstrated how flight landing and departure cities have determined travel sequencing and geographic coverage. Furthermore, the choice of accommodation for large tours is based on capacity and price, whilst capacity constraints have already filtered out many options. Attractions are considered only after these focal points have been fixed (Jin & Sparks, 2017). Options for product diversity are reduced layer by layer. Lastly, possibilities for product diversification are further constrained by the vertical integration that characterizes tourism businesses (TUI is a notable example).

Furthermore, although customers represent a potentially potent force that drives product innovation (Porter, 1989), Bain (1968) has noted that they need to be “savvy..” The present study has confirmed that Chinese consumers are inexperienced in international travel and have minimal product knowledge. This is partly due to the limited accessibility of independent information (Jørgensen et al., 2018) as well as to language barriers which impede their understanding of official destination promotions (Jin & Sparks, 2017). While travel agencies are their main sources of information, they cannot decide on the basis of product features but depend on the reputation of tour operators (Chen et al., 2013; Heung & Chu, 2000). This study has also observed that consumers respond to the bandwagon effect, preferring to tour the same attractions as their peers. It is interesting to note that this feature of Chinese tourists contrasts with more mature European tourism markets such as Switzerland where business survival depends on providing specialized products (Dolnicar & Laesser, 2007). Lastly, the demand for international travel is strong; consequently, tour operators are dis-incentivized to promote different products (Mazzeo, 2002).

It is worth noting that the availability of high-level substitutes gives travel agencies bargaining power because they can choose the tour operators that offer the best commission and/or differentiation opportunities. Hence, high availability of substitutes challenges the interdependent relationship, and limits profit maximization for big firms, thereby confirming Bain (1968)’s hypothesis. It is also worth observing the development of effective resistance. In particular, OTAs have aggressively increased their physical presence and have broadened their market base through merging/acquiring small-medium travel agencies (TravelDaily, 2017). As their capital has grown significantly, this may ultimately allow them to access the key resources. However, the timescale of any impact on product homogeneity is unclear. Finally, the above theory suggests a closed, self-enhancing system perpetuating homogeneous package tours, with some resistance coming from the competitive tour agency subgroup.

Conclusion

The various strategies of tourism businesses have been significantly under-researched, particularly in the case of product strategy and the relationships between industry subgroupings. Using the example of Chinese package tours to the UK, this study firstly applied GIS data to visualize package tour itineraries and to demonstrate product homogeneity. In subsequent interviews, we sought to understand how such homogeneity had developed. A framework was subsequently proposed that utilizes the relationships between and across subgroups—as well as other well-known industry players—to explain the formation of homogeneous package tours. This forms a major theoretical contribution of the present research (detailed in Section 4.3).

The practical implications of our findings reflect the consequences of this strategy for excessive tourism, given that many destinations suffered from this pre-Covid-19. One reason was that these packages were so similar, sending tourists to the same attractions and at the same time. While it has commonly been suggested that this reflects the popularity of these attractions, the current study points to a lack of product variation and the static structure of the tour service industry within the tourists’ home country, as well as a contributory role by the closely tied relationships between firms. This also means that if and when international package tours are resumed post-Covid-19 with no change in industry relationships toward product diversity, product homogeneity will likely persist, thereby affecting destinations in the same way as was the case pre-Covid-19.

While this study has highlighted the challenges associated with product diversification, it does identify opportunities for DMOs. Firstly, the spatial patterns and travel corridors of existing behaviors reveal immediate opportunities to add adjacent attractions and cities to existing itineraries. UK DMOs can also develop brand new itineraries for sale by Chinese tour operators. Secondly, Chinese tour operators are the main points of contact for intervention by DMOs in product redesign, including wholesalers and retailers. Thirdly, as the market structure is fairly stable, adding incentives or travel vouchers could encourage the inclusion of new attractions.

Caution is needed when interpreting our study findings. Since the research focused exclusively on Chinese package tours to the UK, the efficacy of the proposed theory merits testing in other tourist source countries. The present research has focused on one of many product offerings, namely package tours to the UK. It is worth investigating whether the theories generated from the UK context are replicable in other international destinations. Nonetheless the findings of the present research that are specific to tour operators have filled a significant gap in our understanding of the formation of product strategies in this industry.

Supplemental Material

sj-docx-1-jtr-10.1177_00472875221141881 – Supplemental material for Why Have Package Tour Itineraries Been Homogeneous? Insight From Industry Subgroup Relations

Supplemental material, sj-docx-1-jtr-10.1177_00472875221141881 for Why Have Package Tour Itineraries Been Homogeneous? Insight From Industry Subgroup Relations by Mingjie Ji, Christine Y.H. Zeng, Brian King and Jonathan Reynolds in Journal of Travel Research

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors received research funding from British Academy’s partnership with the Department for Business, Energy and Industrial Strategy and Sino-British Fellowship Trust [No.SRG1819\190033].]

Supplemental Material

Supplemental material for this article is available online.

Author Biographies

Mingjie Ji was an auditor at PricewaterhouseCoopers prior to her academic career. Her research includes tourism company strategies, tourism impacts and consumer behavior. Her co-authored textbook with Dr. Chris Guilding Accounting Essentials for Hospitality Managers (4th edition) is well received.

Dr. Christine Y.H. Zeng’s research interests include ethical decision-making, hospitality innovation, social sustainability and cross-cultural studies.

Dr. Brian King is well-known for his research on hospitality leadership, destination marketing, tourism impacts, and Chinese outbound tourism.

Dr. Jonathan Reynolds research interests include retail firms’ strategy, supply chain management, electronic commerce and omni-channel retailing, innovation and entrepreneurship in retailing, retail productivity and skills, and the role of place in marketing and retailing.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.