Abstract

This study explores the influence of political risk on firms in the tourism industry. It addresses a research gap regarding the impact of political risk on firm-level performance and failure and uncovers the role of organizational slack in this relationship. Firm-level political risk is estimated from 2002 to 2019 financial data for firms across six tourism sectors in a developed economy, the United States. Such risk is found to be significantly associated with firm performance and business failure. From the perspectives of the resource-based view and the threat-rigidity hypothesis, the results support the moderating effects of absorbed and unabsorbed slack on links between risk, performance, and business failure. Given that the COVID-19 pandemic has highlighted the tourism industry’s vulnerability, this study will be of interest to tourism firms seeking to improve business sustainability and resilience.

Keywords

Introduction

Substantial research has found that firms try to avoid investing in areas exposed to significantly disadvantageous political factors (Demiralay and Kilincarslan 2019; Holburn and Zelner 2010). Adverse political action, such as governmental authorities’ discriminatory changes to legislation, regulations, and investment terms, increases the risk that firms’ ability to utilize their assets and generate returns may be constrained, thus eroding their performance (Butler and Joaquin 1998). The USA, which is the research context for this study, has been ranked the third most visited destination by international tourist arrivals (UNWTO 2019), demonstrating its important role in generating global tourism-related business. Recent events, such as the trade “war” between the United States and China, have raised concerns about the risks posed by the political system. This “war” has led to devaluation of China’s currency against the US dollar, making it more expensive for Chinese tourists to travel to the United States. Domestically, in a terrorist incident in El Paso, Texas, in August 2019, a gunman targeting Mexicans shot 22 dead and injured more than 20 (BBC News 2019a). Some governments have warned their citizens not to travel to the United States because of recent domestic terrorist incidents. In fact, in view of uncertainties arising from recent political events, American tourism firms may be facing more political risk than ever.

Political risks have a critical influence on many aspects of firms’ behaviors, including loss of employment and tourist income, and business failure. For example, Hong Kong, one of the most famous tourism destinations in the world, has been badly affected by protests and citywide strikes, and more than 200 flights were canceled on August 5, 2019, with a significant fall-off in bookings, particularly in Hong Kong’s hospitality and tourism sectors (BBC News 2019b). Tourism-related businesses are vulnerable to instability from political and economic forces (Sönmez, Apostolopoulos, and Tarlow 1999). Empirical evidence reveals that political risk has severe financial consequences for companies, including reducing corporate investment and increasing the costs of finance (Bradley, Pantzalis, and Yuan 2016; Julio and Yook 2012; Waisman, Ye, and Zhu 2015). Companies may cultivate connections with powerful politicians to manage political risk (Fisman 2001). Some have more bargaining power than others, depending on their size, ownership, and relationships with local government (Moon and Lado 2000). Acemoglu et al. (2016) find that companies are more likely to make political donations if returns on their companies’ shares are sensitive to political uncertainty, which explains why firms in the tourism sector are among the top contributors. Tourism companies have been actively managing political risk. Therefore, aggregate or sector-level measurements of political risk, which have been widely adopted in previous studies, may be not that precise to draw conclusions for the relationship between political risk and companies’ performance. Hassan et al. (2019) have developed a new measurement of firm-level political risk to investigate the impact of political risk on US listed firms. Their results indicate that most variation in political risk occurs at the corporate level rather than at the sector level or across the economy as a whole.

Previous studies (e.g., Madanoglu and Ozdemir 2018; Saha and Yap 2014; Yang and Cai 2016) have leveraged macropolitical and macroeconomic data to estimate variations in firm-level performance. For example, Saha and Yap’s (2014) study of 139 countries identifies the devastating impact of political instability and terrorism on tourism development. Existing literature on the impact of political risk and uncertainty on tourism focuses only on the national level. Regime types have been often used as an indicator of political risk, but according to Barry (2016), because service industries are generally more sensitive to such risk than extractive industries, firm-specific factors deserve greater research attention.

This study focuses on firm-level political risk and its potential impact on tourism firms, about which little is as yet known. Three perspectives motivate this study. First, from the resource-based view of the firm (Bonardi 2011), the impact of political risk on firm performance is likely to differ between firms, as their resources differ and they implement different business strategies in response to external shocks such as trade wars and pandemics. Second, since political instability negatively affects tourist arrivals and revenues (Saha and Yap 2014), tourism-related businesses may be more vulnerable to the resulting risks, which may have more profound effects than firm performance on business failure. Third, Voss, Sirdeshmukh, and Voss (2008) argue that absorbed and unabsorbed slack resources are important for firms’ product exploration and exploitation in the face of environmental threats. Existing tourism literature (e.g., Demiralay and Kilincarslan 2019; Liu and Pratt 2017; Saha and Yap 2014) emphasizes the negative impact of political risk on tourist arrivals, tourism income, and tourism industry development but fails to examine how individual tourism firms can ensure business sustainability and minimize negative impacts. Nohria and Gulati (1996) define slack as firms’ available resources beyond the level necessary to meet immediate business requirements. Therefore, this study investigates the role of organizational slack in mitigating the impact of political risk on tourism firms, as a moderator of the relationship between political risk and firm performance, and business failure.

This study contributes to three strands of literature. First, although the impact of political risk on tourism has been extensively investigated (Demiralay and Kilincarslan 2019; Liu and Pratt 2017; Saha and Yap 2014), little light has been shed on firm-level variations. Emerging examples in the business world illustrate that political risk is largely a firm-specific phenomenon (Darby et al. 2020; Gad et al. 2020; Hassan et al. 2019), requiring firm-level rather than macro-level research. This study is believed to be the first in the tourism domain to reveal the effect of firm-level political risk on business performance and failure. Second, this study provides important evidence on how organizational slack influences the link between political risk and performance. As the tourism industry has become more vulnerable during the COVID-19 pandemic, the role of organizational slack in dealing with external shocks has become even more important. The findings of this study will thus be beneficial to scholars, industry practitioners, and policy makers seeking to improve business sustainability and resilience in the tourism sector.

Literature Review

Impact of Political Risk on Tourism

Risk can be viewed as a combination of the possibility that an incident will happen, and its possible outcomes (Khattab, Anchor, and Davies 2007). Khattab, Anchor, and Davies (2007) identify that most firms engaging in international business face political, financial, cultural, and natural risks. Political risk strongly influences the performance of firms’ foreign investments, leading to reduced investment expenditure (Julio and Yook 2012). The term “political risk” is often used to describe a broad context covering both societal and legal risks (Khattab, Anchor, and Davies 2007). Political risks are classified as emanating from either the host government (including expropriation, currency inconvertibility, restrictions on taxes, imports, and exports), the host society (including terrorism, revolutions, and demonstrations), or interstate (including wars and economic sanctions). Political risk is recognized as having a significant influence on firms’ decisions, and in turn their performance. Strategic responses to political risk are determined by firms’ organizational capability to assess that risk and to manage the policy-making process. Organizational capabilities associated with managing political risk, referred to as “political capabilities” (Henisz and Zelner 2005; Holburn and Zelner 2010), refer to how firms deploy or utilize their political resources effectively to develop ties and coalitions, such as lobbying government officials to maintain or introduce appropriate policies. A firm’s political risk thus differs according to its political capability.

Unlike other types of business, tourism-related businesses and activities are discretionary in nature: no matter how attractive a destination and how cheap a trip or hotel, tourists will stop visiting if they perceive significant travel barriers such as visa restrictions, or insecurity arising from political uncertainty (Cothran and Cothran 1998). Therefore, the supply side of the tourism industry is highly susceptible to political dynamics, political risk, and maladministration (Saha and Yap 2014). Political risk may also arise from wars, terrorist acts, or intergovernmental tensions that interfere with peaceful international relations (Julio and Yook 2012). The tourism industry is extremely vulnerable to external factors such as political risk and health crises (Corbet et al. 2019; Kim and Marcouiller 2015; Ritchie and Jiang 2019). For example, the 9/11 attacks in 2001 had a huge economic impact on American inbound tourism. At the firm level, hotels and casinos—as two major forms of tourism investment—are particularly vulnerable to political risk owing to their massive fixed assets (Cothran and Cothran 1998; Jang and Tang 2009).

The complexity of tourist experiences, the discretionary nature of tourism spending, and the impossibility of storing unsold tickets and unoccupied hotel rooms make tourism firms highly vulnerable to unsystematic exogenous risks such as political crises (Williams and Baláž 2015). This is attributable to most firms’ lack of control over the travel experience, which is shaped by various external events (Williams and Baláž 2015). Tourism firms usually find it difficult to protect their service innovations from competitors, while external factors limit their ability to seek and secure resources (Saha and Yap 2014). It is essential for tourism companies to manage specific firm-level factors in the face of various risks. Lee and Jang (2007) assert that size and debt leverage are positively associated with systematic risk, while profitability and growth are negatively associated. Therefore, there is variation in how different tourism firms are influenced by risks, including political risk. Tourism firms with available resources and capabilities tend to seek ways to manage risks by acquiring and utilizing knowledge, diversifying, and acquiring resources (Williams and Baláž 2015).

Athari et al. (2020) indicate that tourism activities and the number of tourists increase significantly in countries with low levels of political risk. Therefore, policies to reduce political risk are effective in advancing the development of the tourism industry (Faber and Gaubert 2019). In the tourism literature, studies focus mainly on the relationship between terrorism and tourism (e.g., Demiralay and Kilincarslan 2019; Liu and Pratt 2017; Lanouar and Goaied 2019), and on the association between tourism demand and policy-related economic uncertainty (Köseoglu et al. 2013; Madanoglu and Ozdemir 2018). For example, Demiralay and Kilincarslan (2019) find that tourism firms’ stock returns are very sensitive to geopolitical risk, while Madanoglu and Ozdemir (2018) find that hotels’ operating performance is negatively associated with policy-related economic uncertainty, using measures such as average room rate, occupancy, and revenue per available room. Although the macro impact of political risk on tourism firms’ performance has been investigated, differences in the extent of political risk faced by individual firms have generally been neglected. It is more meaningful to examine the impact of political risk at the firm level, rather than merely considering the macro impact of political uncertainty, because although the whole tourism industry suffers from risks, some individual firms suffer more.

Firm-Level Political Risk and Firm Performance

Both macro and micro aspects of political risk have major negative effects on business. Macro factors have similar effects on all companies in a country or region, whereas micro factors affect specific industries or firms (Alon and Herbert 2009). For instance, macropolitical risks include potential changes to monetary policies that may influence a country or region’s currency and taxation, as well as trade policies (Alon et al. 2006). Micropolitical risk is much more relevant and specific to some sectors or firms than macropolitical risk, yet there is little literature on the extent of its impact (Alon and Herbert 2009).

Micropolitical risks do not affect all businesses. In the tourism sector, they are often associated with tourism-related policy changes, such as travel visa requirements, tourism taxes, and funding for national parks and historical sites (Alon et al. 2006). Micro- and macropolitical risks are not entirely separate, with common factors including the governmental, social, and economic environments (Alon et al. 2006). Micropolitical risk assessments are undertaken when adjusting macropolitical risk ratings (Alon and Herbert 2009). For example, Alon and Herbert’s (2009) risk assessment model includes economic-, social-, and government-related political influences emanating from both within and outside a country, as well as firm-related factors. As tourism practitioners tend to focus on changes that may particularly affect their own firms, the impact of micropolitical risks on tourism firms deserves more research attention. The impact of political risk must also be considered within the framework of firm-specific characteristics, as political risk varies across firms (Khattab, Anchor, and Davies 2007).

In the US market, firms’ differing political capabilities play a key role in firm performance. Firms’ ties with political leaders or parties may provide a critical competitive advantage. US firms create and fund political action committees (PACs) that campaign and raise funds for specific issues or candidates. PAC contributions may enhance firms’ performance by giving them access to key officials, enabling them to influence the legislative process for their own benefit (Brown 2016). Bonardi, Holburn, and Vanden Bergh (2006) find that having experience of dealing with government agencies positively affects firms’ returns. Firms widely recognize making donations to political campaigns and lobbying politicians as ways to manage political risk. Large firms may gain more than medium and small firms from swaying political decisions (Hassan et al. 2019).

Hassan et al.’s (2019) textual analysis of firms’ conference calls, capturing management’s views on firms’ exposure to political risks, reveals that increased firm-level political risk makes firms’ stock returns significantly more volatile, and leads to decreased capital expenditure and hiring. Affected firms may find it more difficult to maintain profits and performance. Although evidence remains scarce on the effect of firm-level political risks on tourism organizations, based on previous literature on micropolitical risk, firm-specific capabilities, and recent research findings on firm-level political risk from Hassan et al. (2019), we hypothesize that:

Hypothesis 1: Firm-level political risk is negatively associated with tourism firms’ performance.

Firm-Level Political Risk and Business Failure

Business failure has been explored in many developed and undeveloped economies (e.g., Mellahi and Wilkinson 2004). Park and Hancer (2012) define business failure as a situation in which a company’s financial reservoir fails to meet its payment obligations. Although bankruptcy clearly signals a firm’s demise, it presents only a partial picture of the failure (Mellahi and Wilkinson 2004). Altman’s (1968) model aims to predict organizational bankruptcy by measuring leading sources of business failure. Other indicators of business failure have since been identified, including negative profitability (D’Aveni 1989), withdrawal from international markets (Jackson, Mellahi, and Sparks 2005), and loss of market share (Mellahi, Jackson, and Sparks 2002). Mellahi and Wilkinson (2004) observe that technological, regulatory, economic, and demographic changes generally create waves of business failure. Governance failures are ascribed to institutional and political factors, which in turn induce business failure. Copious studies verify that various external factors may lead to business failure (Zhang, Amankwah-Amoah, and Beaverstock 2019). For example, Karabag (2019) identifies political risk and national technological policy changes as the main factors contributing to Turkish firms’ failure.

Two main streams of literature use either deterministic or voluntaristic theoretical frameworks to investigate factors influencing business failure (Zhang, Amankwah-Amoah, and Beaverstock 2019). From the deterministic perspective, external factors give rise to failures owing to managers’ limited control over their business environment (Karabag 2019). Institutional factors such as economic regimes and political risk are generally considered to be deterministic (Mellahi and Wilkinson 2004). Empirical studies have examined the effect of political instability on direct investment in foreign countries (Touny 2016) and tourism (Sivesan 2017), but few have investigated the effect of firm-level political risk on tourism-related business failures.

External turbulence such as political risk may cause changes to interest rates and sharp declines in real-estate values. Such crises place tourism firms at risk of business failure, given their capital-intensive and highly geared nature, as a large proportion of these firms’ capital expenditure is funded from long-term debt financing using property as collateral (Park and Hancer 2012). The tourism industry’s close ties with the economic climate expose it to financial distress. Its vulnerability to unsystematic exogenous risks (Saha and Yap 2014; Williams and Baláž 2015), such as natural and sociopolitical disasters, requires managers to assess and manage risk at the firm level. Tourism companies have differing abilities to obtain the required returns and cash flows to meet their obligations and avoid business failure under the force of exogenous political risk. The negative effects of political risk also differ, as they are absorbed by firm-specific capabilities (Park and Hancer 2012). Tourism companies must be able to hedge their debt-financing risks resulting from political risk in order to strengthen their financial position and avoid business failure. Hence, we propose the following hypothesis:

Hypothesis 2: Firm-level political risk is positively associated with the likelihood of firms’ business failure.

Moderating Effect of Organizational Slack

Cyert and March (1963) describe how organizations make decisions. An important implication of behavioral theory for business organizations is that firms with stronger financial performance have lower organizational downside risks, and that poor financial performance increases these risks. In this theory, the concept of “slack” is defined as bundles of potential or available resources that an organization can freely deploy to adapt to changes (Staber and Sydow 2002). Voss, Sirdeshmukh, and Voss (2008) define financial slack as financial resources in excess of those required for the organization to operate. Financial slack increases organizations’ resilience to external shocks, such as uncertainties regarding changes to economic policies (Rafailov 2017). It serves as a buffer against the external environment, and protects organizations from negative impacts on their performance (Rafailov 2017). Martinez and Artz (2006) argue that maintaining slack provides a resource cushion enabling managers to weather unexpected external changes.

Singh (1986) categorizes organizational slack into unabsorbed and absorbed slack. The former refers to available resources, such as uncommitted liquid assets, that can be freely used to meet current liabilities, while the latter relates to salaries, administrative costs, and other expenses (Wefald et al. 2010). Firms that maintain a good level of absorbed slack experience lower employee turnover, as staff are less likely to be required to work extra hours when a firm encounters changes to customer demand (Singh 1986). Xu et al. (2015) explain that absorbed slack includes generic resources that are usually employed for a specific purpose and are less easily redeployed, whereas unabsorbed slack, with a low level of absorption, includes resources that can be easily redeployed within the organization. Excess resources in unabsorbed slack are often used to help firms’ research and development, new market entry, and implementation of new strategies (Xu et al. 2015).

Argilés-Bosch et al. (2018) distinguish between absorbed and unabsorbed slack in terms of their resource constraints. Constrained resources contribute largely to absorbed slack. These include finished and manufactured products, which are constrained because of their limited discretionary usage, and other examples include machines and equipment (Argilés-Bosch et al. 2018). In tourism firms, some pre-booked tours and charter flights offer less discretion for resource redeployment, while financial resources such as cumulative earnings from previous operations, as a typical example of unabsorbed slack, can be readily redeployed to meet new demands (Tabesh, Vera, and Keller 2019).

From the resource-based view, an appropriate combination of organizational resources, in the form of financial, physical, political, human, organizational, or informational resources, should promote firm performance and efficiency (Zhang et al. 2018). Financial slack can be deployed for various uses (Mishina, Pollock, and Porac 2004). From the perspective of resource redeployment, executive operators need slack resources for expansion and innovation (Daniel et al. 2004). Unabsorbed slack, in the form of bundles of unconstrained resources, increases exploration and facilitates resource redeployment and synergies (Argilés-Bosch et al. 2018; Tabesh, Vera, and Keller 2019). Uncommitted resources within a firm’s unabsorbed slack can easily be redeployed and used more flexibly, with discretion for new strategies to adapt to external policy changes (Lee, Liu, and Yu 2021). Unabsorbed slack helps firms in turbulent business environments not only to tackle uncertainties, including political risk, but also to achieve goals under institutional pressures (Xu et al. 2015). With more unabsorbed slack, firms find it easier to allocate resources to mitigate the negative influences of political risk on their performance, and tend to suffer less from financial distress and bankruptcy (Hadlock and James 2002).

Absorbed slack may offset intermediate organizational risk (Wefald et al. 2010), providing a buffer to reduce coordination costs, improve economies of scope, and resolve resource conflicts. Xu et al. (2015) claim that absorbed slack may reduce costs and make resource allocation and utilization more efficient. From the perspective of the threat-rigidity hypothesis, in threatening situations, firms may be less likely to engage in high risk-taking behavior and more likely to take strong control, conserve resources, and focus on essential activities (Sarkar and Osiyevskyy 2018). Resources committed to specific tasks within a firm’s absorbed slack may serve as a buffer, because the less discretionary nature of organizational slack limits its function, forcing top management to concentrate solely on existing strategies and manage workflow operations (Lee, Liu, and Yu 2021). Teirlinck (2020) argue that absorbed slack may help firms to create long-term competitive advantage, for example through investment in technological development and education and training. The more absorbed resources a firm has, the more likely it will be to concentrate on implementing strategic activities (Lee, Liu, and Yu 2021).

In summary, from the resource-based view and in relation to the concept of resource deployment, unabsorbed slack with unconstrained resources can be redeployed for various uses to mitigate the impact of political risk on firm performance. From the perspective of the threat-rigidity hypothesis, absorbed slack with constrained resources may help firms to focus on essential activities, may have a buffering effect on normal business operations in a threatening environment, and may contribute to long-term competitive advantage. Based on this mechanism, both types of slack may moderate associations between firm-level political risk and firm performance, as well as organizational failure risk (measured by bankruptcy risk). Extant studies of the association between slack and firm performance are inconclusive (e.g., Daniel et al. 2004; Wefald et al. 2010; Xu et al. 2015). Few studies investigate slack as a moderator of the effects of political risk on firm performance and organizational failure. Based on these arguments, we therefore hypothesize that:

Hypothesis 3a: Absorbed and unabsorbed slack have moderating effects on the link between political risk and firm performance.

Hypothesis 3b: Absorbed and unabsorbed slack have moderating effects on the link between political risk and business failure.

Methodology

Sample and Data

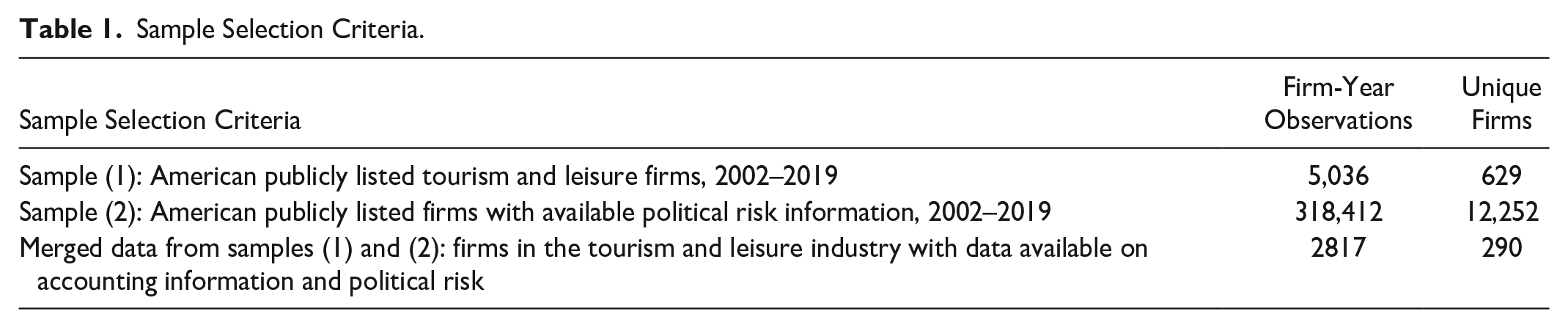

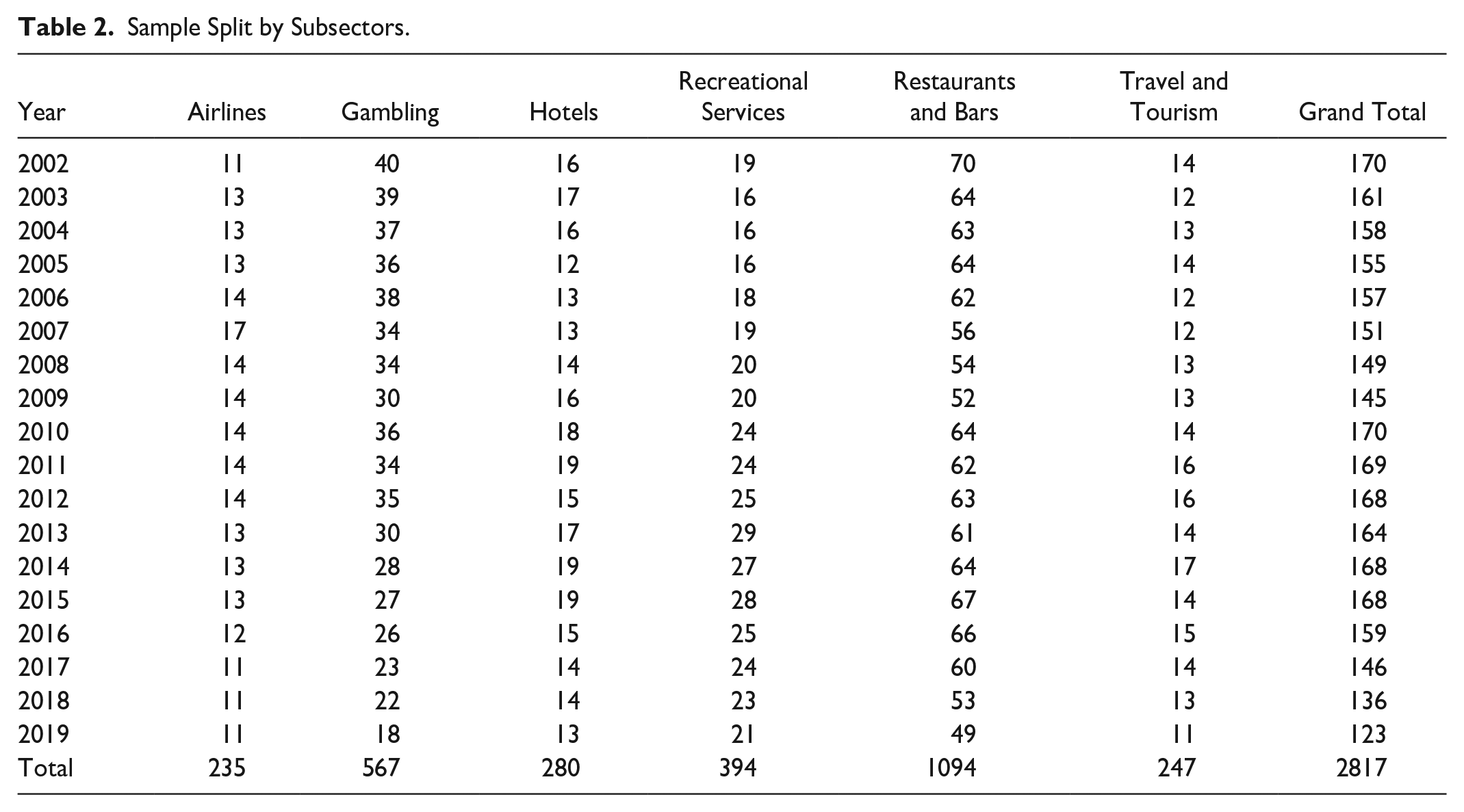

To examine the impact of firm-level political risk on American tourism firms’ performance, we included six subsectors in our sample to gain a broad picture of the tourism industry (see Table 2). Data were drawn from various sources. Accounting information, including financial performance measures, were obtained from the Bloomberg database, and Hassan et al.’s (2019) measure of firm-level political risk was retrieved from an online source (https://www.policyuncertainty.com/firm_pr.html). Table 1 presents the sample selection criteria.

Sample Selection Criteria.

Sample Split by Subsectors.

The primary sample included all publicly listed American firms in the tourism and leisure industry according to the Industry Classification Benchmark (ICB), from 2002 to 2019, resulting in 5,036 firm-year observations and 629 unique firms. In order to deal with survival bias, we allowed firms to exit and enter the US listed market. Merging the data on political risk resulted in an unbalanced panel data set of 2,817 firm-year observations, representing 290 unique tourism and leisure firms over 2002–2019. Our sample period ended at 2019 because this was the latest year for which political risk information was available. Table 2 provides information across the years of analysis on the distribution of firms for six subsectors of the tourism and leisure industry: travel and tourism, airlines, recreational and services, hotels, restaurants and bars, and gambling.

Dependent Variables

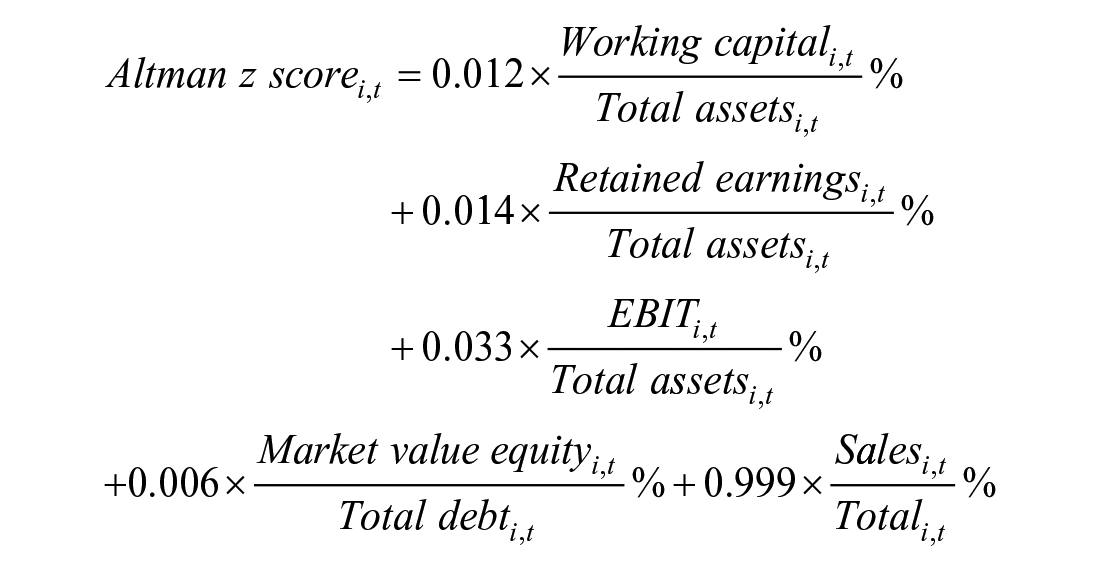

Both accounting- and market-based performance measures were employed as dependent variables in this study. Return on assets (ROA), a commonly used accounting ratio, has been widely applied in previous studies to measure tourism firms’ performance (e.g., Kang and Lee 2014; Zheng and Tsai 2019). Another frequently used accounting ratio is return on equity (ROE), which reflects a firm’s ability to gain from its employed capital (Moon and Sharma 2014). To increase the robustness of this research, we used Tobin’s Q as a proxy, calculated as the total market capitalization divided by the total book value of equity, which is a market-based performance measure also commonly used to measure tourism firms’ performance because it is closely associated with firms’ stock-related performance (Chen, Hou, and Lee 2012). In summary, three performance measures—Tobin’s Q, ROA, and ROE—were used in this study. Lastly, the Altman’s (1968) measure of bankruptcy risk was used in this study, applying a multiple discriminant model, the Altman z-score, to measure firms’ bankruptcy risk. The Altman z-score has been widely used to measure bankruptcy risk and was employed in this study as a dependent variable to measure organizational failure risk (Altman 1968; Altman et al. 2017). The Altman z-score model for publicly listed firms was applied:

Independent Variable

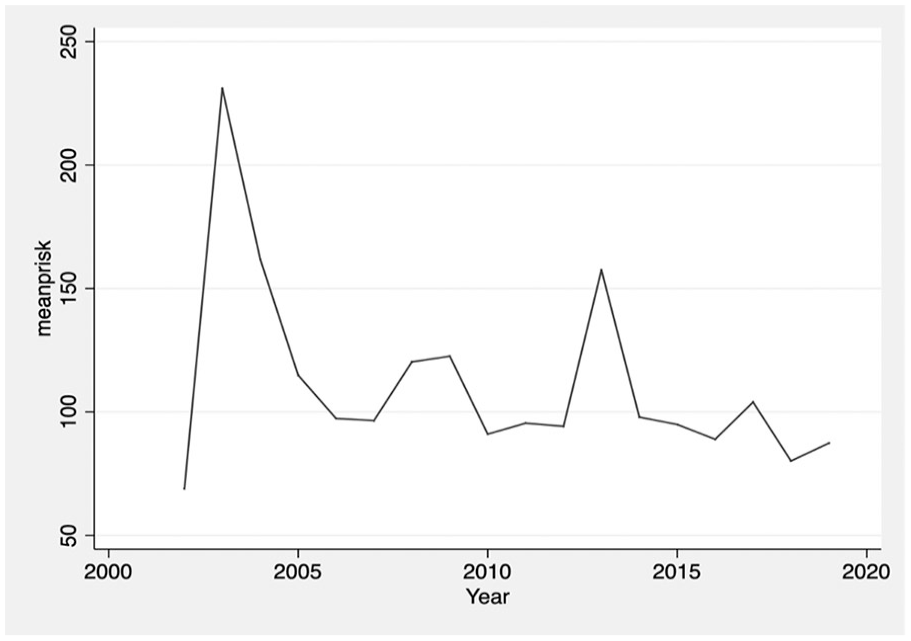

Firm-level political risk was the main independent variable used in this study. This is measured on a quarterly basis, capturing political topics disclosed in conference calls by firms’ management (Hassan et al. 2019). Figure 1 shows changes in the mean of firm-level political risk retrieved from Hassan et al. (2019) for the US tourism industry between 2002 and 2019. This presents a picture of important political events in the United States. For example, the line chart peaks in 2003 in response to the invasion of Iraq, with another peak around 2006 in response to the transatlantic aircraft plot. Thus, the mean political risk for the US tourism and leisure industry was expected to be high around such important political events.

The firm-level political risk of American tourism firms from 2002 to 2019.

Measure of Firm-Level Political Risk

This study adopted the firm-level political risk index developed by Hassan et al. (2019), who conducted a textual analysis based on transcripts of US listed firms’ quarterly earnings conference calls. This pioneering firm-level measure of political risk allows a firm’s political risk to be quantified at specific points in time, based on documented conversations in conference calls focusing primarily on general political risk. To discern language relating to nonpolitical and political matters, a pattern-based sequence-classification method was used (Hassan et al. 2019). As an overall measure of political risk exposure, a training library of political texts (including textbooks on American politics and political sections of US newspaper articles) and a training library of nonpolitical texts (articles from nonpolitical sections of US newspapers) were compiled to identify word combinations frequently used in the documentary evidence. To measure specific political risks, training libraries were developed from texts on eight political topics to identify word patterns often used to discuss particular political topics (Hassan et al. 2019).

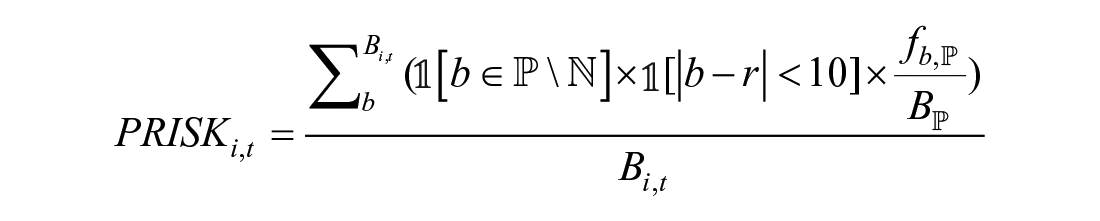

Firms’ overall risk was captured from data from conference calls dealing with risk and uncertainty issues (Hassan et al. 2019). Using the textual analysis method, Hassan et al. (2019) developed a set of measures to capture the specific effect of political risks encountered by individual firms. They measured firm-level political risk by disaggregating each firm i’s conference-call transcript in quarter t into a list of bigrams included in transcript b (Hassan et al. 2019). They counted the frequency of occurrences of bigrams reflecting a particular political issue in a group of 10 words with meanings similar to “risk” or “uncertainty,” and then divided this by the total frequency of bigrams (details for the process can be found via Appendix 3 in Hassan et al. 2019):

where

Data on political risk are reported quarterly. Based on Darby et al. (2020), we calculated annual average political risk indices based on all four quarters’ firm-level political risk indices from Hassan et al. (2019). These measures should be interpreted as indicative of the risk perceived by firm managers and participants in their conference calls (Hassan et al. 2019). Unlike previous studies (e.g., Baker, Bloom, and Davis 2016; Madanoglu and Ozdemir 2018) that have used an influential index of aggregate economic policy uncertainty through textual analysis of newspaper articles, Hassan et al.’s (2019) measure not only provides the first firm-level measure of political risk to allow a meaningful distinction between aggregate sector-level and firm-level exposure, but also allows flexible decomposition into topic-specific components (Darby et al. 2020).

We used two measures to assess the moderating role of organizational slack: unabsorbed slack and absorbed slack. Following previous studies (Singh 1986; Xu et al. 2015), unabsorbed slack was measured by the ratio of cash reserves to total assets, which indicates financial slack at a firm level. Absorbed slack was calculated as the ratio of general expenses to total sales, adapted from Wefald et al. (2010).

Control Variables

The analysis also involved several control variables that might impact firms’ financial performance. We controlled for the effects of firm size (SIZE), fixed assets ratio (FIX), leverage (LEV), growth in sales and assets (SG and AG), and liquidity ratio (LIQ). Firm size was measured by the logarithm of total assets (Kang and Lee 2014), and leverage was measured by total debt to total assets (Zheng and Tsai 2019). In tourism firms such as gambling firms, hotels, restaurants, and airlines, value is normally created from fixed assets. Therefore, the fixed-assets ratio was used, calculated as a firm’s fixed assets divided by total assets (Zheng and Tsai 2019). Lazăr (2016) claims that growth in sales and assets are determinants of firms’ performance and stock performance. Sales growth (SG) was calculated as sales at time t minus sales at time t – 1 divided by sales at time t – 1. Assets growth (AG) was calculated as assets at time t minus assets at time t – 1 divided by assets at time t – 1. The liquidity ratio (LIQ), measured as the ratio of current assets to current liabilities, is positively associated with firm performance (Adams and Buckle 2003). The lower a firm’s liquidity, the higher the risk of bankruptcy (Mihalovic 2016).

Model Estimations

Three key panel data estimation models are commonly applied: pooled ordinary least squares (OLS), fixed effects, and random effects (Asterriou and Hall 2016). First, to determine whether a fixed effects or random effects model would be the more appropriate estimation model for this study, a Hausman test was run. Second, an F test was conducted to determine whether the fixed effects model was more efficient than the pooled OLS model. Fixed effects models were predominantly selected based on the results of these tests. Fixed effects models are advantageous in eliminating bias that may lead to correlations between panel-level disturbance and independent variables. They allow unobserved variables to be associated with observed variables (Asterriou and Hall 2016), and remove the impact of time-invariant characteristics to enable assessment of the net effect of the predictors on the outcome variable (Asterriou and Hall 2016).

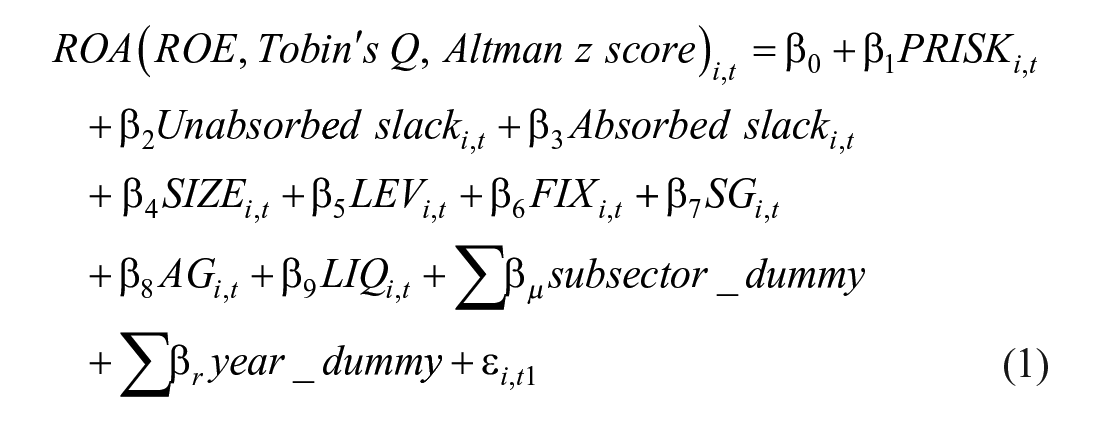

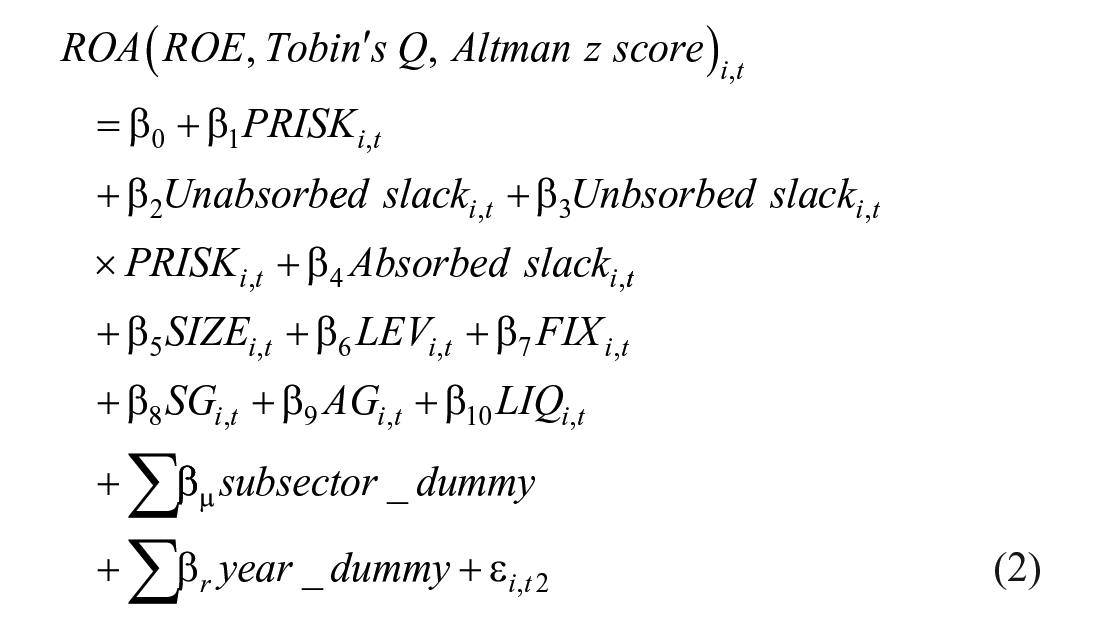

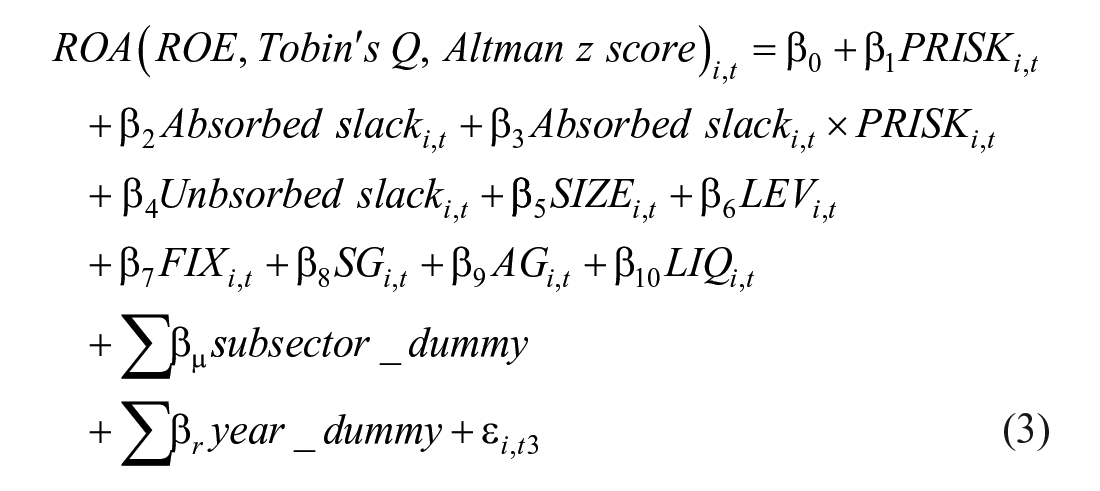

A “robust” regression method was used to mitigate any heteroscedasticity. Equation (1) tests the impact of firm-level political risk on firm performance measures and bankruptcy risk, which relate to hypotheses 1 and 2. Equations (2) and (3) test the moderating effects of absorbed and unabsorbed slack on relationships between firm-level political risk, firm performance, and business failure (measured by bankruptcy risk), which are associated with hypotheses 3a and 3b.

where ROA is computed as earnings before interest, taxes, depreciation, and amortization at time t divided by total assets at time t; ROE is earnings before interest, taxes, depreciation, and amortization at time t divided by total equities at time t; Tobin’s Q is a proxy calculated as total market capitalization divided by the total book value of equity at time t; Altman z-score is calculated as 0.012 × working capital/total assets (%) i,t + 0.014 × retained earnings/total assets (%) i,t + 0.033 × earnings before interest and tax/total assets (%) i,t + 0.006 × market value equity/total debt (%) i,t + 0.999 × sales/total assets (%) i,t (Altman 1968); PRISK is a firm-level political risk measure derived from textual analysis of firm-level conference call transcripts centered around political issues; Unabsorbed slack is cash at time t divided by total assets at time t; Absorbed slack is general and administrative expenses at time t divided by total sales at time t; SIZE is the natural logarithm of total assets at time t; FIX is fixed assets at time t divided by total assets at time t; LEV is total liabilities at time t divided by total assets at time t; SG and AG are growth in sales and growth in assets; and LIQ is the ratio of current assets at time t to current liabilities at time t. Two interaction terms were added to equations (2) and (3): Unabsorbed slack and PRISK, and Absorbed Slack and PRISK.

Results

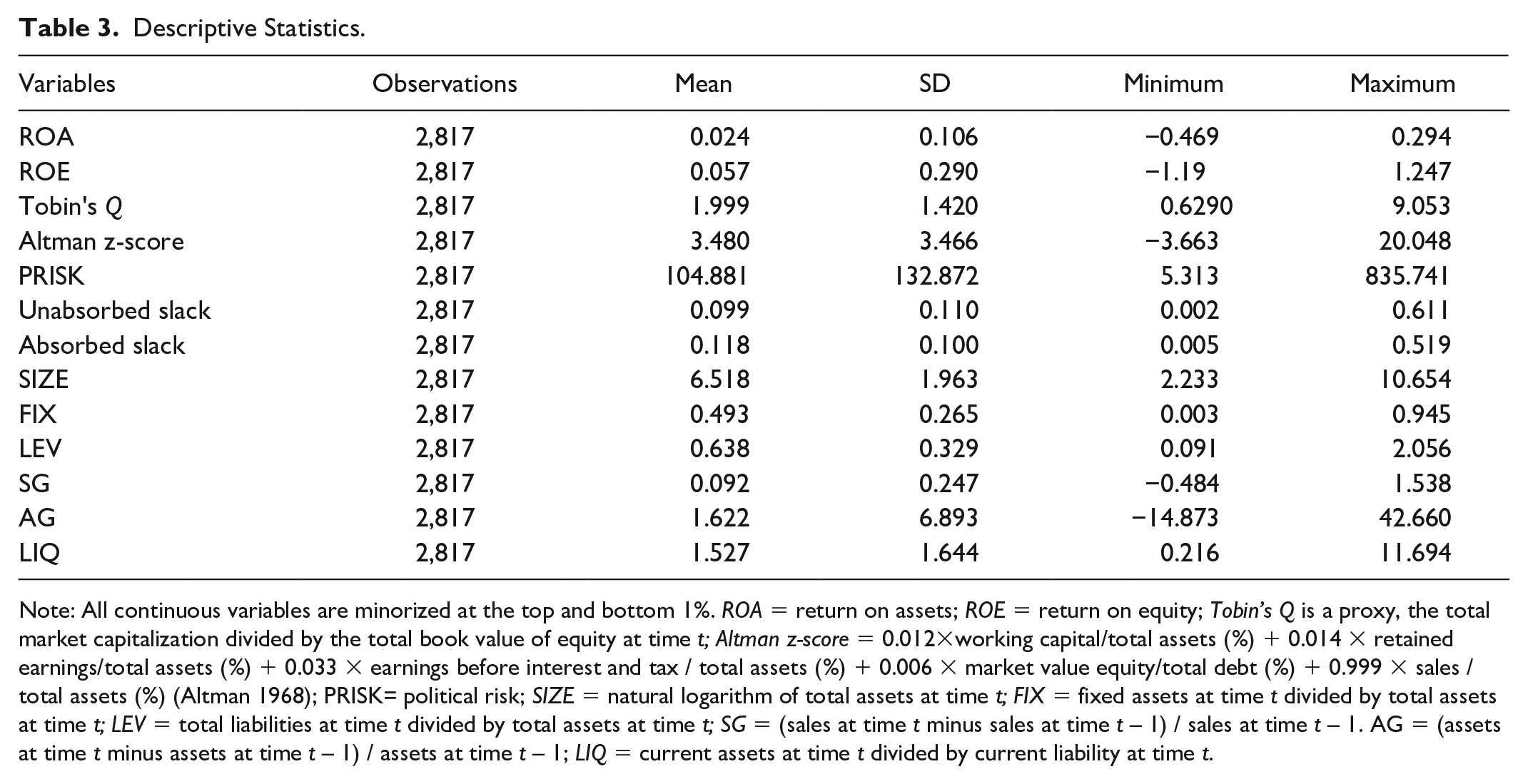

Descriptive Statistics

Descriptive statistics for the explanatory and control variables are shown in Table 3. The continuous variables were winsorized at the top and bottom 1%. The means of the sample are 0.024 for ROA, 0.057 for ROE, and 1.999 for Tobin’s Q, and the Altman z-score is 3.480. On average, the political risk score (PRISK) is 104.881, and the mean values of unabsorbed and absorbed slack are 0.099 and 0.118, respectively. The average logarithm of total assets (SIZE) is 6.518, and the value of 0.638 for LEV suggests that total liabilities average more than half of the total assets of the sample firms. The average fixed assets ratio (FIX) is 0.493, and the average growth rates for the sample firms’ sales and assets are 0.092 and 1.622, with an average liquidity ratioof 1.527.

Descriptive Statistics.

Note: All continuous variables are minorized at the top and bottom 1%. ROA = return on assets; ROE = return on equity; Tobin’s Q is a proxy, the total market capitalization divided by the total book value of equity at time t; Altman z-score = 0.012×working capital/total assets (%) + 0.014 × retained earnings/total assets (%) + 0.033 × earnings before interest and tax / total assets (%) + 0.006 × market value equity/total debt (%) + 0.999 × sales / total assets (%) (Altman 1968); PRISK= political risk; SIZE = natural logarithm of total assets at time t; FIX = fixed assets at time t divided by total assets at time t; LEV = total liabilities at time t divided by total assets at time t; SG = (sales at time t minus sales at time t – 1) / sales at time t – 1. AG = (assets at time t minus assets at time t – 1) / assets at time t – 1; LIQ = current assets at time t divided by current liability at time t.

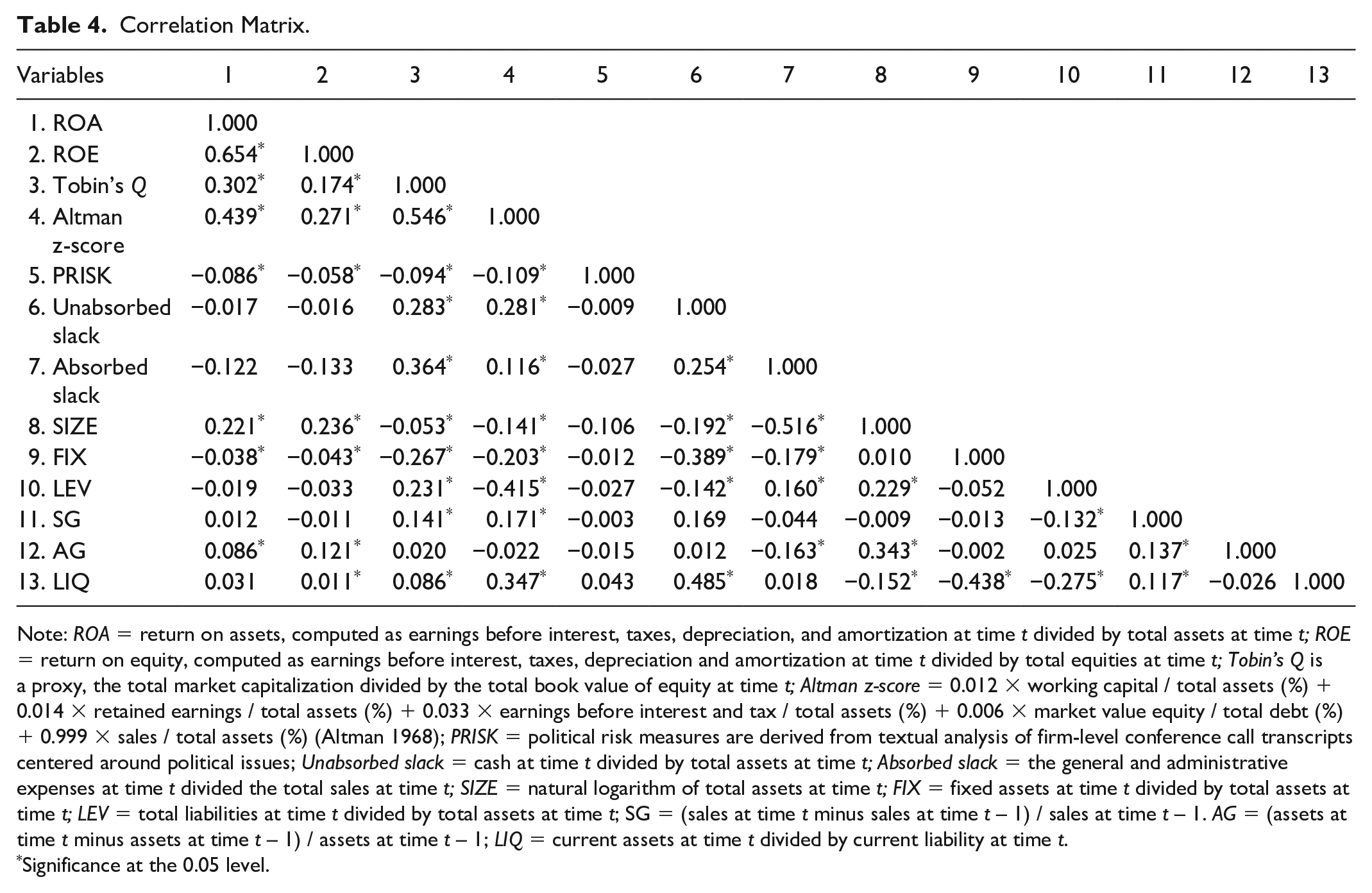

Pairwise correlation coefficients for the variables are shown in Table 4. We note no high bivariate correlations among the variables, indicating that multicollinearity is not an issue in our models. The correlation matrix suggests that firm-level political risk is negatively correlated with all three financial performance measures and the business failure risk measure (Altman z-score). No significant correlation is found between either unabsorbed or absorbed organizational slack, firm performance (ROA, ROE, Tobin’s Q), and the business failure risk measure (Altman z-score).

Correlation Matrix.

Note: ROA = return on assets, computed as earnings before interest, taxes, depreciation, and amortization at time t divided by total assets at time t; ROE = return on equity, computed as earnings before interest, taxes, depreciation and amortization at time t divided by total equities at time t; Tobin’s Q is a proxy, the total market capitalization divided by the total book value of equity at time t; Altman z-score = 0.012 × working capital / total assets (%) + 0.014 × retained earnings / total assets (%) + 0.033 × earnings before interest and tax / total assets (%) + 0.006 × market value equity / total debt (%) + 0.999 × sales / total assets (%) (Altman 1968); PRISK = political risk measures are derived from textual analysis of firm-level conference call transcripts centered around political issues; Unabsorbed slack = cash at time t divided by total assets at time t; Absorbed slack = the general and administrative expenses at time t divided the total sales at time t; SIZE = natural logarithm of total assets at time t; FIX = fixed assets at time t divided by total assets at time t; LEV = total liabilities at time t divided by total assets at time t; SG = (sales at time t minus sales at time t – 1) / sales at time t – 1. AG = (assets at time t minus assets at time t – 1) / assets at time t – 1; LIQ = current assets at time t divided by current liability at time t.

Significance at the 0.05 level.

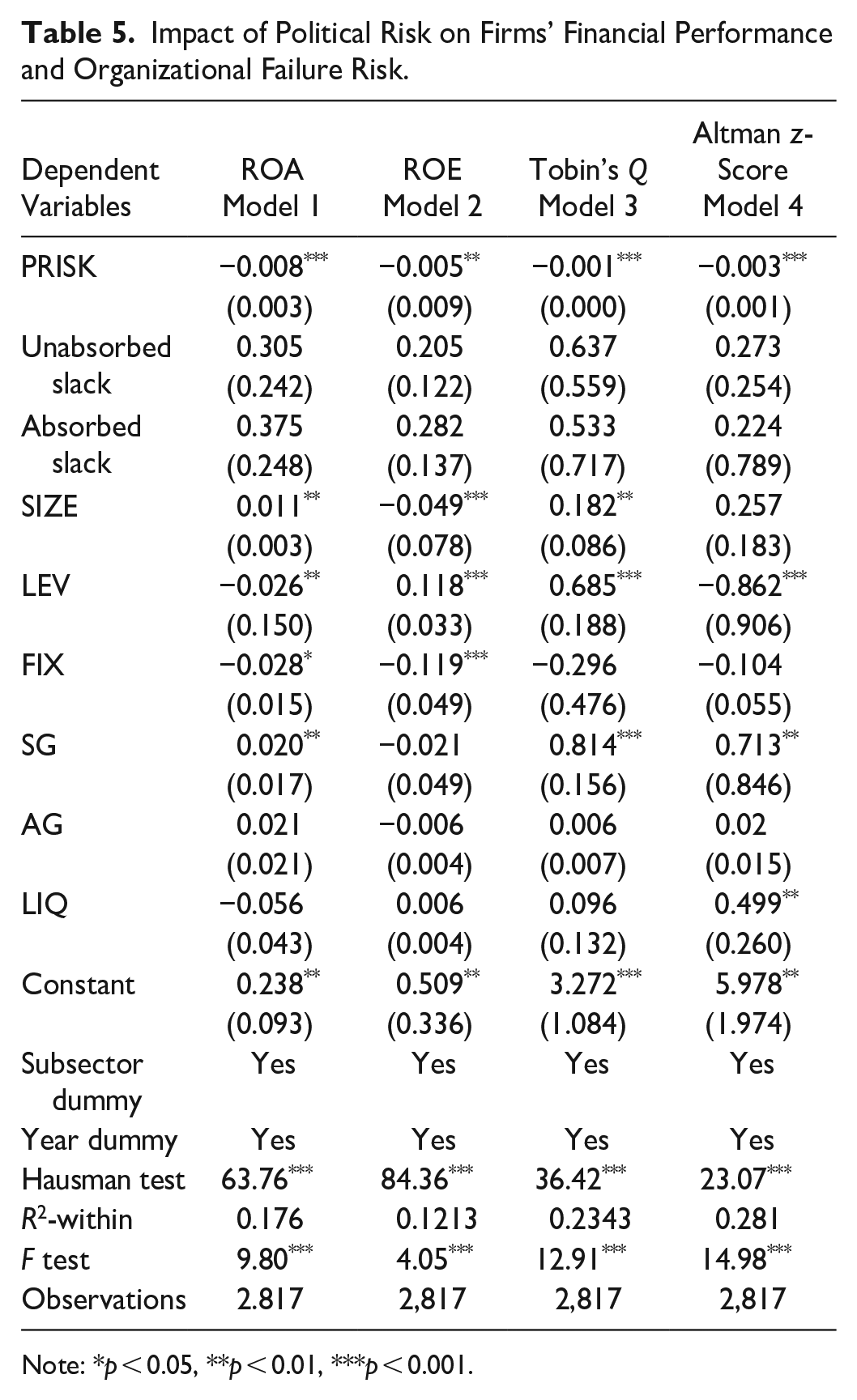

Impact of Firm-Level Political Risk on Firms’ Financial Performance

Table 5 reports the fixed effects panel regression analysis results for the effect of firm-level political risk on firms’ financial performance and business failure risk. The results of Hausman test (models 1–4) indicate the rejection of null hypothesis of the test, suggesting fixed effects estimation is consistent. Model 1 shows a significantly negative relationship between political risk (PRISK) and ROA (β = −0.008; p < 0.01), model 2 reveals a significantly negative relationship between firm-level political risk (PRISK) and ROE (β = −0.005; p < 0.05), model 3 presents a significantly negative relationship between political risk (PRISK) and Tobin’s Q (β = −0.001; p < 0.01), and model 4 indicates a negative and significant relationship between political risk (PRISK) and Altman z score (β = −0.003; p < 0.01). The coefficients of PRISK indicate that if political risk increases by one standard deviation, tourism firms experience reductions of 0.8% and 0.5% in ROA (with a standard error, SE, of 0.003) and ROE (SE 0.009) respectively, a 0.1% decrease in Tobin’s Q, and a 0.3% decrease in Altman z-score (SE 0.001). Overall, the empirical results indicate that firms facing greater political risk are more likely to experience negative financial performance, supporting hypothesis 1. A negative impact of firm-level political risk on the Altman z-score is also shown, indicating that greater firm-level political risk results in a lower Altman z-score, and thus an increased likelihood of bankruptcy.

Impact of Political Risk on Firms’ Financial Performance and Organizational Failure Risk.

Note: *p < 0.05, **p < 0.01, ***p < 0.001.

Moderating Effect of Organizational Slack

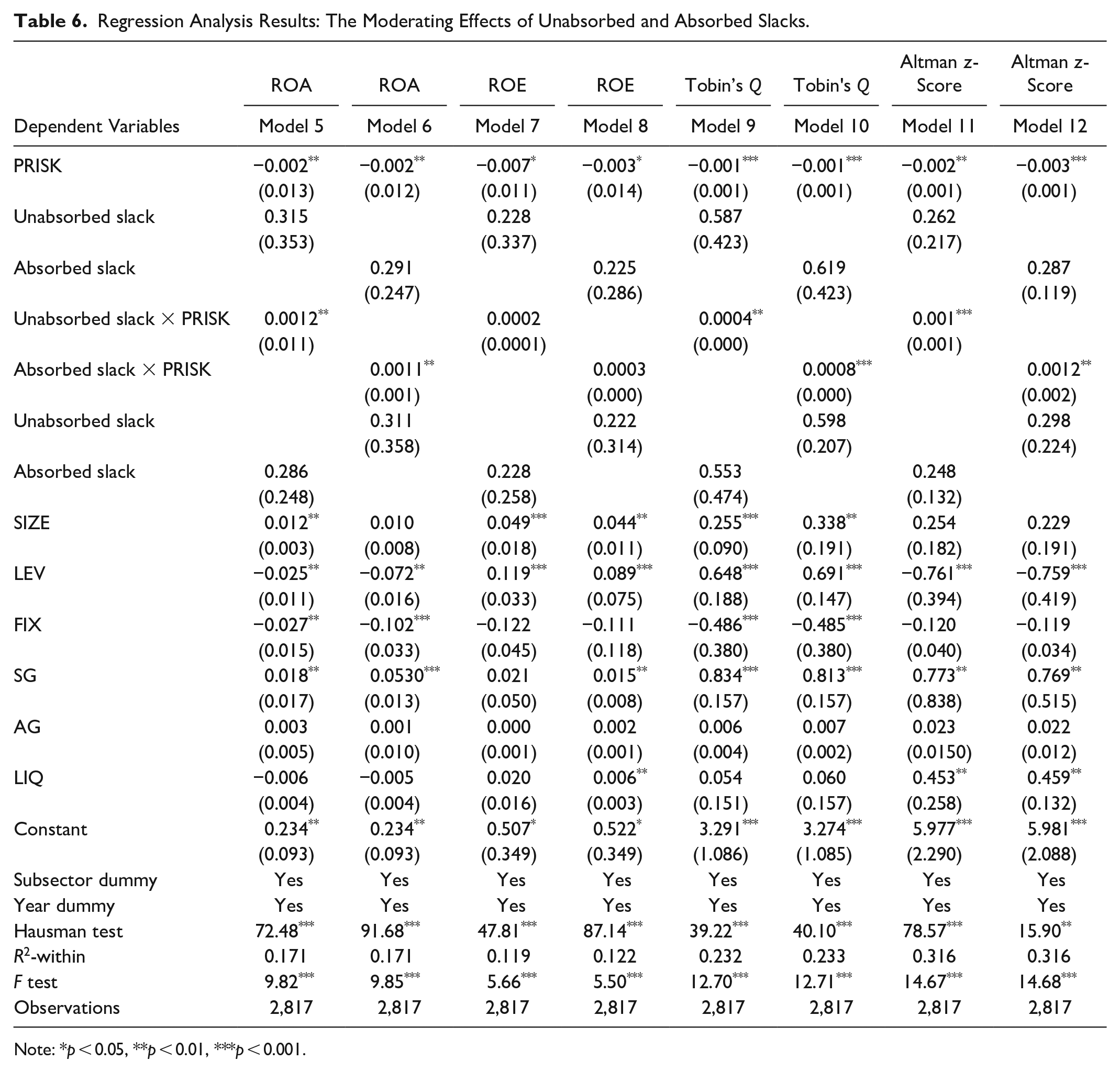

Table 6 presents the results of fixed effects panel regression analysis including the effects of the moderating variables (unabsorbed and absorbed slack) on relationships between firm-level political risk, firm performance, and the Altman z-score. The results of Hausman test (models 5–12) indicated the rejection of null hypothesis of the test, suggesting fixed effects estimation is consistent. In models 5 and 6, the previously identified negative relationship between firm-level political risk (PRISK) and ROA is moderated by unabsorbed and absorbed slack. Statistically significant interactions between Unabsorbed slack and PRISK (β = 0.0012; p < 0.05), and between Absorbed slack and PRISK (β = 0.0011; p < 0.05) in models 5 and 6 suggest that the negative relationship between firm-level political risk and ROA is weaker in incorporating with unabsorbed or absorbed slacks. The positive moderating effects of unabsorbed and absorbed slack on the negative relationship between PRISK and Tobin’s Q are supported in models 9 and 10. Statistically significant interactions between Unabsorbed slack and PRISK (β = 0.0004; p < 0.01), and Absorbed slack and PRISK (β = 0.0008; p < 0.01) in models 9 and 10 suggest that the negative relationship between firm-level political risk and Tobin’s Q is weaker in incorporating with unabsorbed or absorbed slacks. Significant coefficients for the interactions between Unabsorbed slack and PRISK (β = 0.001; p < 0.01), and Absorbed slack and PRISK (β = 0.0012; p < 0.05) are found in models 11 and 12, which implies that the negative relationship between firm-level political risk and the Altman z-score is weaker in firms with unabsorbed or absorbed slacks.

Regression Analysis Results: The Moderating Effects of Unabsorbed and Absorbed Slacks.

Note: *p < 0.05, **p < 0.01, ***p < 0.001.

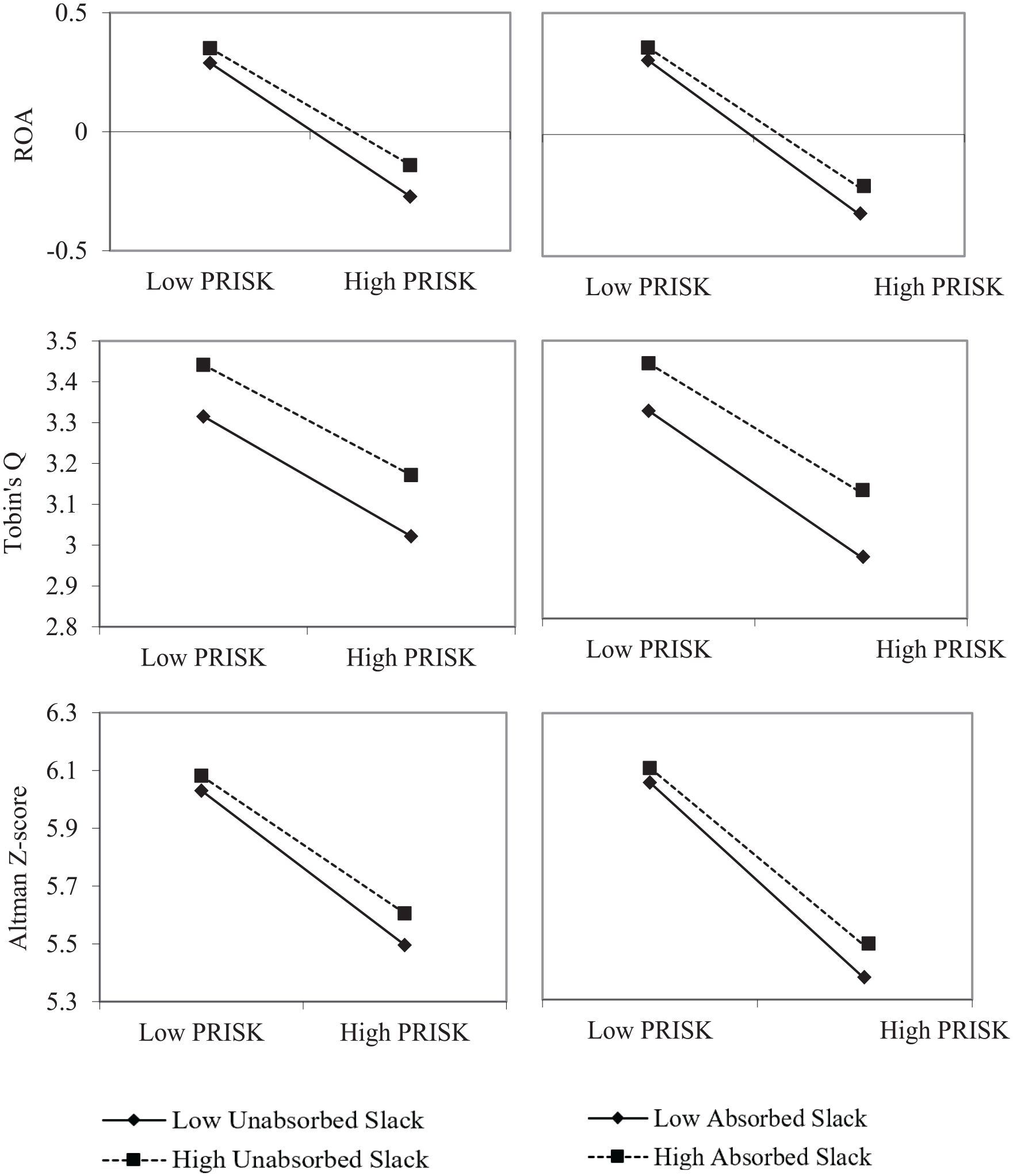

Supporting hypotheses 3a and 3b, Figure 2 visualizes the moderating effects of unabsorbed and absorbed slacks. These results suggest that higher levels of unabsorbed and absorbed slacks mitigate the negative impacts of firm-level political risk (PRISK) on ROA and Tobin’s Q. Figure 2 also shows that firms with higher levels of unabsorbed and absorbed slacks tend to perform better in terms of ROA and Tobin’s Q when suffering firm-level political risk. Firms with higher levels of unabsorbed and absorbed slacks also tend to be less affected by higher firm-level political risk because having a higher Altman z-score indicates a less likelihood to have a distress and trouble in maintaining a good financial health. In contrast, firms with lower levels of unabsorbed and absorbed slacks tend to have lower Altman z-scores under the higher firm-level political risk, indicating a higher likelihood to have a financial distress and heightened risk of bankruptcy and business failure.

The moderating effects of unabsorbed and absorbed slacks.

Discussion and Conclusions

This study examines the impact of firm-level political risk on American tourism firms’ financial performance and business failure risk, and provides empirical support for negative relationships between these factors. It also empirically tests the moderating effects of unabsorbed and absorbed organizational slacks.

The tourism industry is perceived to be greatly influenced by macro-environmental factors such as terrorism, economic conditions, and political uncertainty (Ritchie and Jiang 2019). The association between political risk and tourism has been widely studied from both national and international perspectives. Many studies have also examined the considerable effects of macro-level political risk. This study fills a gap in extant studies of the effect of political risk and uncertainty. Several studies have investigated developing economies, such as China (Yang and Cai 2016) and Tunisia (Lanouar and Goaied 2019), with a few studies (e.g., Chang and Zeng 2011; Madanoglu and Ozdemir 2018) in developed economies, but little research has been carried out on major developed economies such as the United States, where political choices may affect the global macro outlook. This study is significant in exploring the impact of political risk on American tourism firms’ financial performance. The negative impact of firm-level political risk on firms’ financial performance is strongly supported, which is in line with the large effect of macro-level political risk. Consistent with previous research (Julio and Yook 2012; Madanoglu and Ozdemir 2018), the results of this study show that political risk has a negative impact on firms in six subsectors of the American tourism industry.

From the perspective of organizational behavior, Argilés-Bosch et al. (2018) argue that absorbed and unabsorbed slack may help firms to deal with external shocks, including political risk and uncertainty. Our results confirm the positive moderating effects of absorbed and unabsorbed slack on the identified negative link between firm-level political risk and firm performance. With regard to reducing the negative impact of firm-level political risk on the Altman z-score, absorbed and unabsorbed slack may help firms be more cost-efficient and overcome financial distress, in turn lowering the likelihood of bankruptcy (Hadlock and James 2002). The results clearly demonstrate that firms with a higher levels of absorbed or unabsorbed slacks tend to be less affected under a higher firm-level political risk because having a higher the Altman z-score indicates a less likelihood to have a distress and trouble in maintaining a good financial health. In line with T. Lee, Liu, and Yu’s (2021) suggestion that the impact of political risk varies with differences in firms’ strategic resources and capabilities, this study confirms that both uncommitted and committed resources within firms’ unabsorbed and absorbed slacks are critical in mitigating the negative impact of firm-level political risk.

This is believed to be one of the first studies in the tourism context to focus on the impact of political risk from a firm-level perspective. It enriches the existing literature and sheds new light on the impact of firm-level political risk, business failure, and the moderating role of organizational slack in tourism. Applying the resource-based view of the firm and the concepts of resource deployment and organizational slack to the tourism business context also helps identify sources of competitive advantage and capabilities for dealing with risks in the tourism industry. Tourism-related businesses are much more vulnerable to external shocks than other types of business (Madanoglu and Ozdemir 2018; Tsionas and Assaf 2014), and this study provides empirical evidence that organizational slack has a buffering effect on tourism firms’ vulnerability to political risk. Tourism firms are vulnerable to risk relating to banking and financial policies, as the tourism industry is one of the biggest borrowers of capital and must take precautions against influential political events (Madanoglu and Ozdemir 2018; Tsionas and Assaf 2014).

The detailed insights of our findings for different performance measures reveal that the negative effect of firm-level political risk on tourism firms tends to be greater for accounting-based performance measures (ROE and ROA) than for market-based performance measures (Tobin’s Q). This implies that these firms’ senior management should not prioritize market-based performance measures, because these may be less sensitive to firm-level political risk. In other words, firm-level political risk may cause greater harm to firms’ free cash flows and profitability than to their market value, while potential financial distress will lead to increased borrowing during politically uncertain periods. Business failure risk deserves greater attention from senior management, who need to understand the roles of absorbed and unabsorbed slacks in dealing with external shocks, including political risk and uncertainty.

The results of this study suggest that the mitigating effects of unabsorbed and absorbed slacks on the negative impact of political risk on firm accounting performance. The influences of unabsorbed and absorbed slacks should encourage tourism firms’ management to utilize different types of resource appropriately in their firms to deal with political risk. As unabsorbed slack includes unconstrained or uncommitted resources within a firm, tourism firm managers should consider redeploying these resources and increasing their discretionary utilization to mitigate the negative impact of political risk. In addition to financial resources, which are a typical example of unconstrained resources, tourism firms should increasingly redeploy resources such as cash in marketable securities and short-term investments. Slack in customer relations has been identified as another type of unabsorbed slack (Voss, Sirdeshmukh, and Voss 2008), so focusing on committed customers who might provide tangible and foreseeable benefits might provide valuable support for firms in difficult times. Tourism firms in mass markets must value loyal customers and view them as an essential component in building unabsorbed slack.

Additionally, absorbed slack has a slightly stronger mitigating effect than unabsorbed slack on the negative impact of political risk on the Altman z-score (business failure risk). These findings suggest changes to senior management’s financial activities and decision making. As absorbed slack is associated with constrained or committed resources that can be redeployed, tourism firms should focus on required and essential activities to lower the possibility of business failure. Firms with higher levels of absorbed slack should concentrate on resource utilization for long-term business planning. In a threatening environment, absorbed slack allows firms to focus on restricting losses and cutting costs, because committed resources are less discretionary in nature. Therefore, it is essential for tourism firms to evaluate whether committed/constrained resources might contribute to long-term business planning. Although the data set for this study did not capture the impact of the COVID-19 pandemic on tourism businesses in the United States, the results still provide some valuable insights into how tourism firms might deal with external shocks, by enhancing unabsorbed and absorbed slacks through increased redeployment and discretionary utilization of resources, concentration on required and essential business activities, and restriction of losses by cutting back.

This study has some limitations. We acknowledge that firm-level measures may not fully capture all firm-level political risk, and research on such measures is still developing (e.g., Baker, Bloom, and Davis 2016; Hassan et al. 2019). Furthermore, owing to the limited availability of firm-level political data spanning the period 2002–2019, the results might be replicated using an updated data panel to study other business sectors. The results may have limited generalizability to private firms because of differences in their strategies for financial management and business planning. Future studies might examine the effect of firm-level political risk across different industries and countries, and other firm specific factors might also be investigated, such as the extent of business diversification and corporate governance. Since Hassan et al.’s (2019) new firm-level political risk index is publicly accessible, future research might also investigate how different types of corporate political activities are linked with actual political risk at a firm level, which in turn affects firm performance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.