Abstract

To stay within the safe boundaries of global warming, the world now has 30 years to decarbonize its economy. This represents a very significant challenge for tourism as a growth system. Much attention has been paid to different tourism subsectors such as aviation, accommodation, and activities to reduce emissions, mostly on the basis of (future) technology. However, the Paris Agreement demands immediate action and significant year-on-year progress on a zero-carbon trajectory. This article discusses destination management under the new low-carbon imperative. It analyses challenges, including economic viability and resilience, that have also gained importance in light of the COVID-19 pandemic, and explores opportunities for better profitability on the basis of a leakage/spending value dichotomy proposition. The final section highlights the foremost role that destination managers must play in building prosperous and resilient low-carbon tourism destination systems and discusses the key insights for destination managers.

Introduction

The global tourism system has to fully decarbonize over the coming 30 years, in line with other economic sectors, if global goals of stabilizing climate change are to be met (IPCC 2018). This will require a medium- to long-term systemwide transition commitment on the part of governments to move to a low-carbon economy (Stern, 2007; Higham, Ellis, and Maclaurin 2019). Simultaneously, given the climate emergency, it is important that in the short term, tourism destination managers seek ways to gain all available efficiencies to immediately ramp down tourism carbon emissions (Scott, Hall, and Gössling 2019). New destination management models are required to move to a tourism paradigm that accounts for the carbon footprint of tourism revenue. It is generally acknowledged that several tourism subsectors, specifically transportation, face great difficulties in reducing emissions for interrelated reasons of rapid growth, their energy intensity, and high cost of technology change (Larsson et al. 2019; Peeters et al. 2016). Yet, tourism stakeholders have ignored this emerging problem over decades and pursued volume growth strategies with little or no attention being paid to the implications for climate change (Scott, Hall, and Gössling 2016). Such strategies have created vulnerabilities, including environmental externalities that now must be accounted for (Peeters et al. 2018). They also imply very significant “carbon risks” as a result of upcoming mitigation policies (Scott et al. 2016) and exacerbate climate change outcomes, including the loss of climate assets, ecosystems, and cultural heritage, and damage to tourism and transport infrastructure (Scott, Hall, and Gössling 2019). Associated risks, such as aviation’s potential to act as a vector in the distribution of pathogens, have also become more tangible with the COVID-19 pandemic (Gössling, Scott, and Hall 2020).

At a first glance, it appears that many developments in the global tourism system have predicted a high-emissions, low-value dilemma. For instance, there is much evidence that tourism follows a volume growth logic (UNWTO 2019) that is not uncommon and in fact underpins the global economy in its entirety (Schmelzer 2015), yet ill-suited to be maintained under any decarbonization scenario (Hall 2009). Given the high carbon footprint of tourism (Lenzen et al. 2018) and its dynamic development (Gössling and Peeters 2015), growth in tourism is, inevitably, associated with increasing carbon emissions. Notably, on the transport side, this growth is fueled by deregulation and subsidies, creating overcapacity in the system, while in accommodation, an oligopolistic platform economy fosters competition through direct price comparison and the rapid introduction of new accommodation capacity through peer-to-peer business models (Zervas, Proserpio, and Byers 2017). Evidence suggests that these developments are behind the observed global decline in average length of stay in many destinations, requiring destination managers to attract growing tourist arrivals to maintain bed night numbers (Gössling et al. 2018). The evolution of the global tourism model is consequently becoming increasingly reliant on transportation to maintain its economic contributions, at an ever-growing carbon cost.

In this situation, new tourism models have to be found that can significantly reduce the sector’s emissions while maintaining its income and employment benefit. This will require a rethinking of tourism as a development strategy (Sharpley and Telfer 2015; Schilcher 2007; Scott, Hall, and Gössling 2019) as well as the introduction of new management approaches to achieve decarbonization aligned with low-carbon trajectories as outlined in the Paris Agreement (UNFCCC 2019). Meeting global decarbonization goals will require changes in business strategies to maintain and increase the economic value created by tourism (Oklevik et al. 2019). It will also require a fundamentally different role for transportation, specifically air travel (Lyle 2018). Vulnerabilities in the system, be they related to climate change or pandemics (among other things), highlight the need to critically assess destination resilience (Scott, Hall, and Gössling 2019). To discuss the implications and opportunities for tourism, a destination focus is best suited, as it brings together very different actors and stakeholders in tourism, while contributing to larger-scale, systemic mitigation. To this end, the article conceptualizes the constituent elements of a high-value, low-carbon, and economically resilient destination model.

Against this background, the goal of this article is to discuss the meaning and implications of the low-carbon imperative for destinations. Specifically, we seek to explore how the tourism system can be decarbonized without jeopardizing employment and income, while reducing risks related to mitigation (e.g., carbon taxes), exposure to external threats (e.g., weather extremes), and even black swan events (e.g., pandemics). The article’s structure is as follows: It first discusses the current state of the tourism system, the importance of profitability, the emergence of the platform economy, and other structural changes that have progressively increased system vulnerability over time. It goes on to deliberate on the growth model characterizing global tourism and then addresses the need for an alternative destination model under the low-carbon imperative. Here we confront and discuss the urgent need to prioritize decarbonization in combination with value generation and support of resilience structures. This “destination tripartite” (high value–low carbon–resilient), which encapsulates a shift in destination management approaches from volume to value perspectives, is discussed in the last section. The article concludes with a summary of insights and implications for destinations.

Tourism: A Race to the Bottom?

Tourism has experienced a decade of unprecedented growth, fueled to a large extent by changes in income and travel opportunities in Asia (UNWTO 2019). China in particular has had a key role in this growth, with travel demand growing at around 10% per year, and the country receiving 23% of global aircraft deliveries in 2018 (Aviation Week 2019). Even elsewhere, arrivals have continued to increase, however, and the UNWTO (2019, p. 3) highlighted 2018 as the “9th consecutive year of sustained growth,” reaching 1.4 billion international tourist arrivals as a result of strong economic growth. Notably, while tourist arrivals increased by 5% in 2018, international air traffic, measured in revenue passenger kilometers, grew by 6% (ICAO 2018).

While tourism growth has provided new economic opportunities, two recent events may serve as a reminder of the price pressure that has built up in the system, and its lack of resilience to external shocks. The first is the demise of tour operator Thomas Cook in October 2019. As the BBC (2019) reports, a reason for Thomas Cook’s collapse was the unusually warm summer in 2018, as the heatwave was “blamed for falling bookings” in the UK. This is reminiscent of the northern summer 2003 heatwave, a prolonged period of temperatures exceeding 40°C in central Europe and probably the hottest period in Europe since AD 1500. The 2003 heatwave was found to be likely attributable to climate change (Stott, Stone, and Allen 2004) and had an effect similar to the 2018 heatwave, in that many people decided to stay at home in the following year. However, contrary to expectations by travelers, the summer in 2004 was unusually cold and rainy, causing a rush on last-minute bookings to “warm” destinations (Gössling and Hall 2005). The two analogue summers of 2003 and 2018 illustrate how climate change may increasingly affect travel behavior in the future, with potentially significant implications for the tourism industry. Even more problematic for destination resilience are black swan events, that is, unforeseeable developments with extreme consequences. Toward the end of January 2020, a few hundred cases of Corona (COVID-19) infections had been recorded, almost all of them in China’s Wuhan region (Johns Hopkins University 2020). By mid-March 2020, the virus had spread to 155 countries and regions, reaching 175,000 cases (March 16, 2020), forcing entire countries into shut-down. Tourism subsectors including aviation and cruises were hit particularly hard, with grim short-term prospects for most destinations (Gössling, Scott, and Hall 2020).

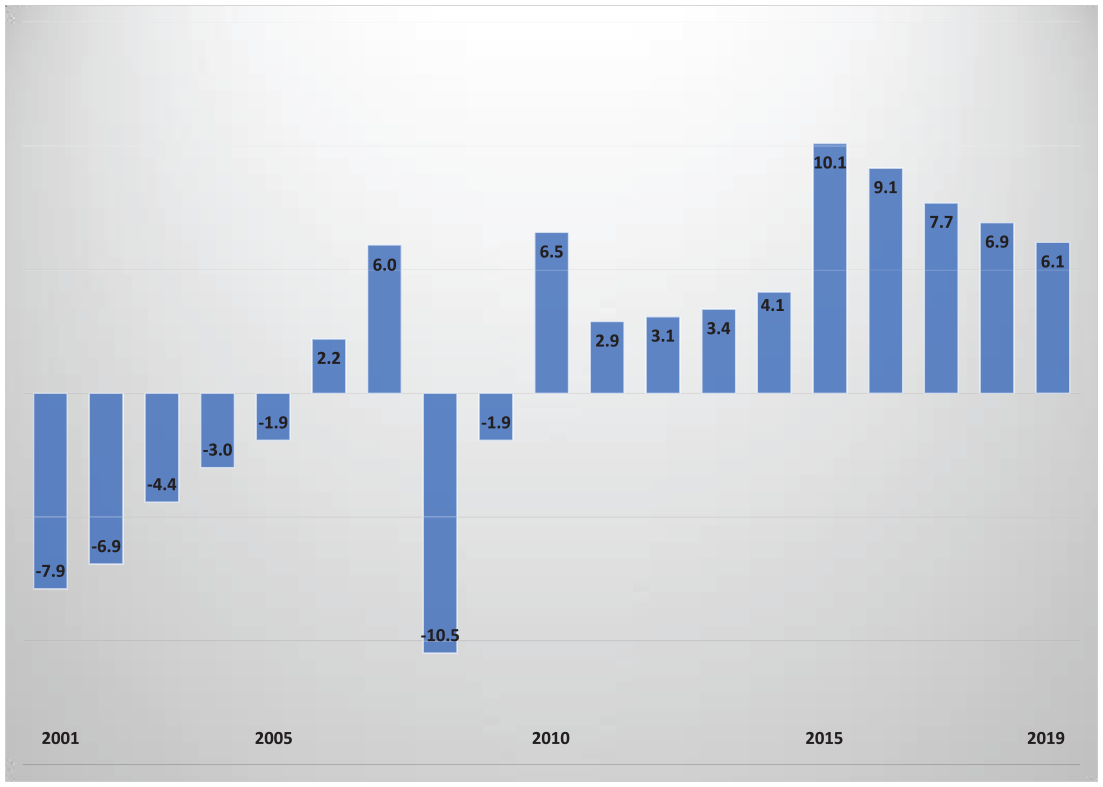

This is perhaps specifically relevant if seen in comparison to the small and sometimes declining profits in tourism subsectors such as aviation. The world’s airlines’ profits have been small since 1947 (Adler and Gellman 2012), and airlines generated a profit in only one out of two years in the period 1988-2003 (Doganis 2005). The 2007 financial crisis implied massive losses to airlines (Adler and Gellman 2012), with a net loss per departing passenger of US$10.5 in 2008 (IATA 2009). More recently, airlines have remained profitable, though margins have declined in recent years. The International Air Transport Association (IATA 2017, 2019) reports an average net profit per departing passenger of US$2.9 to US$10.1 in the years 2010–2018, with profits declining from US$10.1 in 2015 to US$6.1 in 2019 (Figure 1). As a result of the COVID-19 pandemic, the year 2020 will in all likelihood again incur very significant losses to aviation. Profitable years also need to be seen in light of subsidies afforded to the sector, which may amount to hundreds of billions of US dollars since the inception of commercial aviation under the Convention on International Civil Aviation 1947 (The Chicago Convention) (Gössling, Fichert, and Forsyth 2017). As a result, global aviation may never have generated a profit.

Global average net profit per departing passenger, US dollars.

Another challenge for tourism and destination profitability is the rise of the platform economy, which is characterized by its domination through a limited number of global players, competition based on direct price comparison, and the concentration of profit flows. These are developments with potentially limited positive effects regarding the Sustainable Development Goals (Gössling and Hall 2019). As an example, the emergence of AirBnB, founded in 2008, added significant bed capacity to destinations: the platform claims to have hosted 500 million guests in more than 7 million listings by November 2019 (AirBnB 2019), and its implications for residential housing, neighborhood structures, and a range of associated issues, such as safety and tax evasion, are discussed in a growing number of articles and reports (Ayouba et al. 2019; Peeters et al. 2018; Wachsmuth and Weisler 2018; Zervas, Proserpio, and Byers 2017).

An important outcome of these changes from an economic perspective is that businesses in destinations—often representing microbusinesses—forward significant shares of their turnover to a more limited number of “venture laborers” (Neff 2012). Room reservations (e.g., Booking, AirBnB), transport (e.g., Momondo, Uber, Lyft, Lime), or reservations of activities (e.g., TripAdvisor) are usually characterized by monopolistic structures and ownership in the United States. These processes of economic extraction go along with changes in travel communication, and control over business reputation. Social media platforms such as Facebook or Instagram shape the social norms of travel and tourism consumption, while users of Google rate and recommend businesses (e.g., Germann Molz 2012; Giglio et al. 2019; Hasnat and Hasan 2018). This implies opportunities for some businesses and represents a risk for others, specifically because these processes are difficult to control. The need to improve profitability and resilience, and to simultaneously reduce emissions, may be hampered by the structures of the platform economy.

The transformation of destinations toward a low-carbon model is also made more difficult by the expansion and low cost of air travel. Air transport is now the major transport mode in international tourism, which has shifted transportation—and tourism as a whole—toward greater carbon intensity (Gössling and Peeters 2015). For example, in Europe, the market share of low-cost carriers (LCC) was 5% in 2001, and 26% in 2011 (UNWTO 2012), causing a significant decline in the cost of air travel. According to IATA (2019), 2018 global air fares plummeted by 60% compared with 1998. This pushed the share of international tourist arrivals by air from 43.7% in 1998 to 57% in 2018 (UNWTO 2000, 2018). However, lower fares also meant that tourists could go on holiday more often, traveling greater distances and for shorter periods. This is evident in the global decline in average length of stay. Analysis of UNWTO data for 32 destinations with close to half a billion international tourist arrivals in 2015 revealed that length of stay had fallen by almost 15% since 1995, from 5.4 to 4.6 nights (Gössling et al. 2019).

Notably, the largest percentage decline was found in mature tourism economies, including France, Portugal, Netherlands, and Greece (Gössling et al. 2019). Austria saw an almost linear decline in length of stay by 27.5%, “losing” an average of close to 1.5 million guest nights per year as a result of changes in length of stay. By implication, it is necessary for destinations to attract growing tourist arrivals to maintain guest night numbers that, all other things being equal, increases demand for additional transport infrastructure (Gössling et al. 2019). Apart from the overall growth in tourist numbers, change in length of stay is thus also a factor in the expansion of airports throughout the world, along with the hub system adopted by most airlines (Finance and Trade Watch 2016). As transport accounts for most of the carbon footprint of tourist trips, and the vast majority of the carbon footprint of long-haul tourism, this affects the sector’s carbon intensity negatively (Gössling 2010).

At the same time, there appears to be an increase in specifically carbon-intense forms of tourism. The most carbon-intensive forms of tourism and tourist transportation tend to be the fastest growing (Hopkins and Higham 2016). The cruise sector is an example of these development trajectories. For tourists, cruises involve travel to and from ports of embarkation and disembarkation, almost always by air, before and after the very carbon-intense cruise passage itself (Howitt et al. 2010). The cruise system also means that staff are flown to the ship from all over the world, as the working environment in international waters makes it possible to hire from low-income countries (Klein and Roberts 2003). Cruises are planned in a way that involves particularly spectacular journeys. For example, MSC World Cruises (2019), offers a 117-night around the world cruise, including visits to 23 countries in 2020. This journey offering to dock in close to a quarter of all countries in the world is only exceeded in terms of the consumption of destinations by the company’s 2021 offer: a 119-night world cruise with ports of call and short-duration shore excursions in 31 countries (Figure 2). This example illustrates how growth in the global cruise industry increases the carbon intensity of tourism. Notably, these developments are subsidized in complex financing structures: cruise ship construction may be based on export credits, bank loans, private placement notes, and publicly traded notes (Kizielewicz 2017). The debt amassed by cruise corporations can be significant. Carnival Corporation & plc, for example had a total debt exceeding US$9 billion in 2014, and Kizielewicz (2017) indirectly points at the problem of overcapacity in the sector, forcing cruise operators to lower ticket prices while being under increasing pressure to reduce emissions and pollution.

Screenshot depicting route of MSC’s 2021 world cruise.

This discussion shows that tourism, a sector already more carbon-intense than other economic sectors (Lenzen et al. 2018), continues to increase its energy intensity while rapidly growing in tourist numbers. Carbon risks arise out of this combined development pathway, as tourism will be affected by changes in the cost of fuel, as well as taxes, duties, or other fees imposed on carbon (Scott et al. 2016). For example, the cost of the European Trading Scheme for airlines—a mechanism aimed at reducing emissions in the European Union—is €800 million per year, while the benefit of the global jet fuel tax exemption has been put at €27 billion in the EU alone (T&E 2019). Addressing these contradictions would significantly increase the cost of air travel. Aviation may also be forced to introduce quota feed-ins of alternative fuels (Larsson et al. 2019). The expectation is that tourism will be confronted with the internalization of its climate change cost, which is problematic in a situation of small profit margins.

Compounding these vulnerabilities, it is well established that tourism will be affected by climate change (Scott, Hall, and Gössling 2019). Climate change risks include the degradation or loss of natural assets such as reef systems, and damage to tourism infrastructure, for instance, as a result of “coastal squeeze,” as rising oceans erode beaches (Schleupner 2008). Impacts can also comprise operational aspects, such as the availability and cost of food, energy or labor, and the wider domestic and international market structures and their demand implications. In addition, Scott, Hall, and Gössling (2019) also observe that the capacity of destinations to adapt to climate change and to balance other climate change risks is often low. This represents a triple challenge for destinations to transform their tourism systems. Systemic changes and low profitability have to be balanced with decarbonization needs, while reinforcing the destination’s overall resilience in a global economy that is likely characterized by growing instability (see World Bank Group 2019; Espiner, Orchiston, and Higham 2017). The shut-down of many countries during the Corona-virus crisis in 2020, and its impacts on employment, stock exchanges, or structures of provision, is a worst-case example of vulnerabilities arising out of and affecting the global tourism system (Gössling, Scott, and Hall 2020).

Framing the Low-Carbon Tourism Economy

Tourism performance is usually measured in terms of “growth,” represented by key performance indicators including international tourist arrival numbers or expenditure. The UNWTO (2019), for example, relies solely on these indicators when it measures the sector’s performance, with growth implicitly being understood as progress. Similarly, the raison d’être for the World Travel and Tourism Council is to rigorously measure the economic contributions of tourism, globally and nationally, as a tool to inform government policy. Yet, as outlined by Schmelzer (2015, p. 263), there is a “quasi-religious adoration of growth by economists and policy makers” that routinely ignores the social and ecological costs of growth. This includes resource exploitation and emissions of harmful substances, though economic growth is also a reason for vast inequalities in wealth, assets, and power, as well as economic instability as a result of debt or unemployment (Harvey 2011). Although this has been frequently highlighted in the academic literature (Constanza et al. 2014; Macekura 2015; Piketty 2015), it is rare to see any critique of the growth model on the part of the world’s supranational organizations, particularly in relation to the social and environmental costs of tourism. The United Nation’s former Secretary General Ban Ki-Moon’s address to the World Economic Forum in 2011 stands out as a lone voice in its message: For most of the last century, economic growth was fueled by what seemed to be a certain truth: the abundance of natural resources. We mined our way to growth. We burned our way to prosperity. We believed in consumption without consequences. Those days are gone. . . . Over time, that model is a recipe for national disaster. It is a global suicide pact. (Ki-Moon 2011)

From a more generic point of view, volume-based “growth” is problematic because it is, as a concept, inadequate to capture whether an economic activity creates social welfare benefits. For a company, profitability should be more relevant than turnover, while for society, value as expressed in terms of employment and fair income distribution should have greater relevance than GDP growth (Harvey 2014). Yet, there is much evidence that for businesses and policymakers, growth is an imperative in itself (Schmelzer 2015). The challenges arising out of this perspective for destination managers are twofold: First, under scenarios of decarbonization, more attention will have to be paid to social welfare, that is, tourism’s profitability and wealth distribution in the regional economy. Second, the need to immediately reduce emissions from absolute levels will require significant changes in tourism models, including the phasing out of specific forms of high-carbon tourism regardless of industry promises of future technical solutions.

Given the challenge of reducing emissions to zero within 30 years (IPCC 2018), a related question is how destination managers can move forward to advance the carbon imperative. General insights may be derived from the transition literature (Rotmans, Van Asselt, and Kemp 2001), which is of specific relevance in light of the need to transform economies toward a new steady-state equilibrium that generates employment and income benefits in the longer-term future (Hall 2010). Much attention has been paid to transitions, which require exogenous pressure, the weakening of the existing system, and an alternative, usually defined as a niche innovation (Geels et al. 2017). Current developments in tourism would suggest that there is a weakening of the system in many destinations, as reflected in overtourism phenomena and the risks implied in tour operator vulnerabilities (Peeters et al. 2018; Milano, Cheer, and Novelli 2019). What is lacking, at this point, is an alternative trajectory for developing destination economies, along with change in policy paradigms (Hall 2011). This new pathway has to be economically attractive, because regime change may otherwise only result out of a crisis.

A wide range of publications have sought to address revenue generation processes in destinations, though not with a view to reduce overall tourism (e.g., Becken and Simmons, 2008; Dwyer, Forsyth, and Dwyer 2010). A concept linking value more directly to emissions is that of eco-efficiencies. These have been calculated for a range of destinations, including the Seychelles, France, Amsterdam, or Rocky Mountains National Park, showing that per unit of value (here: one Euro), emissions ranged between 0.1 and 16.1 kg CO2 (Gössling, Scott, and Hall 2005). In a more recent article, Lenzen et al. (2018) calculated tourism eco-efficiencies on the basis of Input/Output analysis, estimating that at around 1 kg CO2-equivalent (CO2-e) per US dollar of final demand, tourism is more carbon-intense than global manufacturing at 0.8 kg CO2-e per US dollar, construction at 0.7 kg CO2-e per US dollar, or the world economy average of 0.75 kg CO2-e per US dollar. With projections that the global economy will more than double its GDP to 2050 (e.g., PWC 2019), the challenge of decarbonization is evident: per unit of financial value, emissions have to decline even more radically. By linear interpolation, this means that by 2030, eco-efficiencies in tourism would have to improve to about 0.4 kg CO2-e per US dollar. 1 As various authors have outlined, any such challenge can only be met by a combined focus on immaterialization, dematerialization, and decarbonization (Tapio et al. 2007).

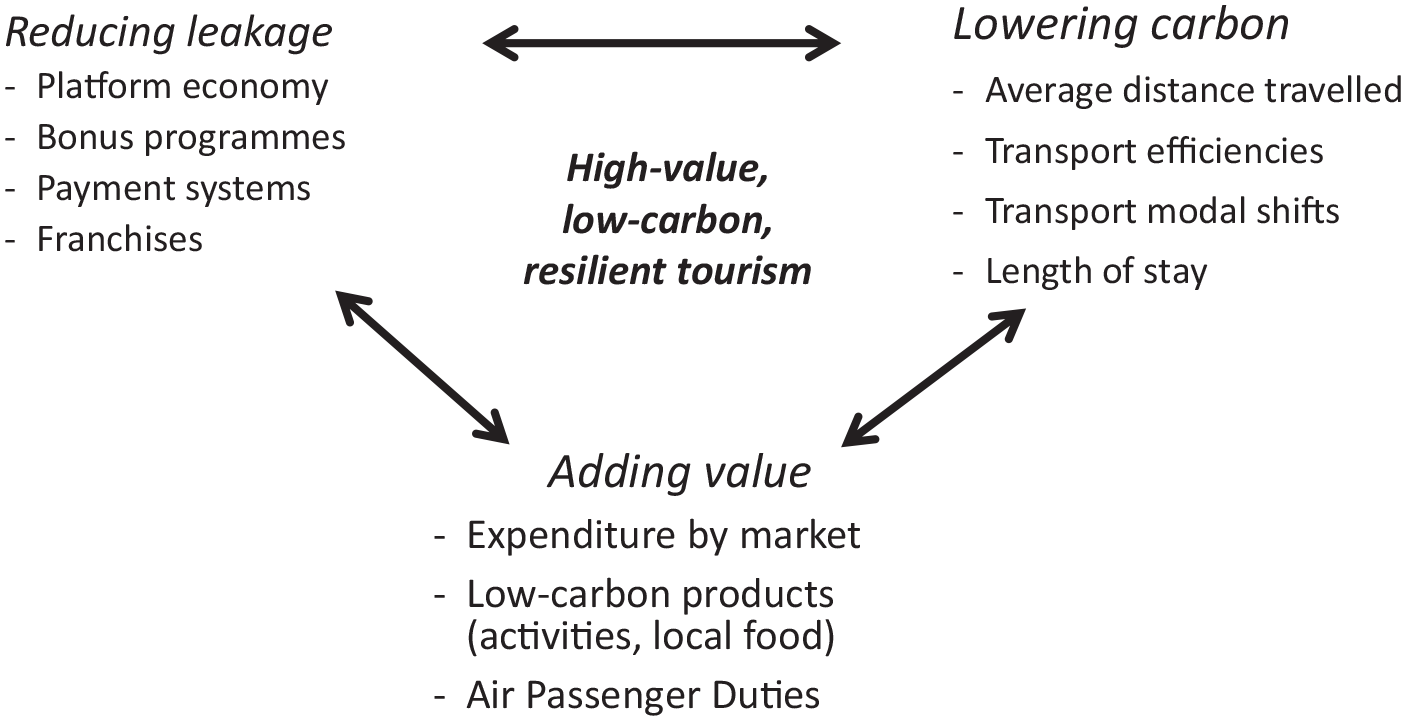

These insights provide the framework for a new destination management model under the low-carbon imperative. Earlier studies have pointed at two principal strategies to increase destination performance by maximizing profit, that is, to increase visitor numbers or to reduce cost (Scott and Breakey 2007). Yet, as preceding sections have discussed, the decarbonization imperative makes it necessary to stabilize or reduce tourist arrivals. This is only feasible if the (welfare) value that can be derived from tourism increases, or if economic leakage (rather than cost) is reduced. Stability in markets is another aspect of a resilient tourism economy. Together, these objectives form a high value–low carbon–resilient tourism destination management tripartite (Figure 3), as a blueprint for more robust, profitable destination models. The fundamental objective of the tripartite is to work toward the overall goal of reducing tourist emissions per unit of tourism value created.

The destination tripartite—low carbon, added value, and reduced leakage.

A key question for destination managers is how objectives of decarbonization, value creation, and reducing leakage can be practically achieved. The following sections present and critically consider a number of key strategies arising from Figure 3 (above). Because this does not represent an exhaustive review of the sorts of strategic directions arising from Figure 3, it should also inspire further research into the means by which destinations may most effectively reduce leakage, lower carbon, and add value.

Lowering Carbon

Opportunities for destinations to reduce tourism carbon emissions through management have been addressed in various publications to date (Gössling, Scott, and Hall 2015, 2018; Gössling et al. 2016; Oklevik et al. 2019). As air travel is the most relevant contributor to emissions, reducing the share of air transport is critical (Peeters et al. 2016). The gravity model indicates that international trade is dominated by import and export markets that offer the advantage of proximity (Anderson 2011). The gravity model clearly applies to aviation emissions, given the inescapable link between distance and tourist aviation emissions (Smith and Rodger 2009). Marketing to proximity source markets and, equally, demarketing long-haul markets, is an immediate step that can be taken to lower the carbon footprint of tourist arrivals (Gössling, Scott, and Hall 2015). Given that outbound air travel needs to be accounted for in the destination carbon inventory (Lenzen et al. 2018), marketing to domestic tourists, so often neglected under the established growth model, will serve the same interests in lowering aggregate tourism carbon emissions. In some countries, there already is a growing focus on domestic tourism markets (e.g., Roth-Cohen and Lahav 2019), a trend that by necessity has been entrenched by the COVID-19 pandemic and the widespread closing of international borders between tourism-generating regions and destinations (Gössling, Scott, and Hall 2020).

Developing closer markets is a related longstanding recommendation for destination managers (Gössling, Scott, and Hall 2015). Becken (2008) argued that dwindling oil resources would lead to a growing cost of energy, requiring tourism managers and business owners to consider the carbon intensity of their products. While “peak oil” did never become an economic argument for reducing emissions, as the cost of oil remained low, some countries have recently moved toward the introduction of carbon taxes, as global economic media have warned (Forbes 2019). Other countries, including the United Kingdom, have already introduced significant air passenger duties. Thus, even though the scale of carbon taxes remains as yet insignificant (Markham et al. 2018), it is possible that national approaches to address aviation’s emissions will become relevant in the future. Addressing the market mix and transport mode shares is thus important both in terms of reducing emissions and creating more robust destination models.

Given the failures of supranational organizations to resolve the problems of aviation and maritime transport emissions (Smith and Rodger 2009; Higham, Ellis, and Maclaurin 2019), most notably the International Civil Aviation Organization’s (ICAO’s) CORSIA proposition (Lyle 2018), it is inevitable that tourist destinations will need to demonstrate leadership on the tourism decarbonization imperative. The regulation of air travel is possible at the subglobal level, which offers opportunities for destinations to demonstrate strong climate leadership (Sandler 2004). It is conceivable that forward-thinking destination managers may drive carbon action in the interests of long-term competitive advantage. Higham, Ellis, and Maclaurin (2019, p. 543) note that destinations that “adopt air transport carbon charges that return to the maintenance and enhancement of their tourism sectors will enjoy immediate short-run advantages over their competitors in the sector, as they will be replacing marginal and relatively invisible price advantages under the old regime with highly visible and marketable low-carbon advantages under the new one.” Such initiatives on the part of early adopters are likely to drive a wider shift toward the high-value, low-carbon, and economically resilient destination model. There is increasing evidence in mature tourism markets that such concerns are becoming important in tourist decision making, specifically as there is much evidence of social norm change in the wake of flight shame debates (Gössling, Humpe and Bausch 2020).

A range of aviation climate-policy mechanisms are available to destinations (Larsson et al. 2019). It is noteworthy that under the Chicago Convention 1947, nation-states are required to negotiate and maintain Air Service Agreements (ASAs) with all foreign countries with which they share international aviation arrangements: typically, ASAs formalize arrangements relating to the nine “freedoms of the air” (Duval 2013). Forward-thinking destinations could extend ASA negotiations to strategically incorporate environmental standards in an attempt to ensure that all airlines operating to and from a particular destination meet minimum emissions standards, in alignment with the destination’s stated year-on-year zero-carbon trajectory targets. Such a system would reward “less unsustainable airlines,” punish airlines that lack a demonstrated sustainability commitment, and provide the highly visible and marketable low-carbon advantages that will be available under the new destination management regime (Higham, Ellis, and Maclaurin 2019). It would also encourage all airlines to advance the urgent carbon emissions agenda rather than continue to compete only on the basis of price (Markham et al. 2018).

As indicated, another way forward is to consider the market mix. One study concluded, for a sample of 11 countries, that the average amount of greenhouse gas emissions caused by one international tourist arrival varied between 370 kg CO2 in Spain and 1830 kg CO2 in New Zealand (Gössling, Scott, and Hall 2015). The study also found that in countries where the market mix changed, emissions would decrease or increase. As an example, average emissions per tourist in the Seychelles declined from 1580 kg CO2 in 1995 to 1450 kg CO2 in 2010 as a result of growing visitor numbers from closer markets. In comparison, average emissions per tourist in the United States, China, Turkey, or South Africa increased because of more arrivals from more distant markets. In the United States, this meant growth in average per tourist emissions from 1020 kg CO2 in 1995 to 1570 kg CO2 in 2010 (Gössling, Scott, and Hall 2015).

Developing markets with a view to distance is thus of considerable importance in addressing emissions, specifically where such changes involve a lower share of air travel (Smith and Rodger 2009). As destinations regularly market themselves overseas, there are many opportunities to consciously revise marketing campaigns with strategic outcomes to the fore. Destinations may ultimately choose to demarket long-haul, high-carbon markets. Similarly, long-haul destinations may find it strategically beneficial to collaborate rather than compete, in an attempt to ensure that tourists who do continue to travel long haul extend their total length of stay. Given that regional visitors are least likely to be burdened by high transport emissions per tourist (Gössling, Scott, and Hall 2015), and the need to account for the emissions of outbound tourists in national carbon inventories (Lenzen et al. 2018), is also likely that destinations will increasingly see the strategic wisdom in marketing to domestic tourists.

Changing average length of stay is an associated mechanism of reducing emissions, while simultaneously reducing air transport capacity needs. Austria is an example that illustrates this point. As outlined, the country’s average length of stay declined by about 1.4% per year over the past two decades (Gössling, Scott, and Hall 2018). In a scenario where the country had instead managed to increase length of stay by the same percentage, the number of bed nights had grown by 15 million in a decade, without any associated need to expand transport capacity. Notably, in many countries there appears to be an interest in staying longer, though often this is hampered by barriers such as the packages offered, or low-cost carriers reducing the cost of transport (Oklevik et al. 2019). Under the circumstances, an increase in transportation cost is likely to be a factor in efforts to reverse the long-standing downward trajectory in tourist length of stay. The high carbon costs of regional transport at the destination signals the need for modal shifts and the development of low-carbon transport corridors on high tourist transit routes to further mitigate tourist transportation emissions (Hopkins and Higham 2016), while perhaps offering the additional benefit of extended length of stay (Gössling, Scott, and Hall 2019).

Adding Value

Much research has sought to identify markets that are more profitable (Legoherel 1998; Pizam and Reichel 1979; Weaver and Oppermann 2000), usually with a focus on differences in market segments. Profitable markets may not only be characterized by higher spending per person; they can also involve favorable price perceptions and open holiday budgets, have an interest in staying in a different season, or spending more time in the country (Gössling et al. 2016). Research does suggest that various of these parameters can be developed, and that expenditure can increase where additional opportunities for spending—in the form of activities, or local food—can be offered. For instance, Oklevik et al. (2019) found, in a study of international visitors to Norway, that the interest to participate in activities varies between nationalities, and that there is a substantial gap between intended and actual participation in activities. Findings suggest that destinations can strategically increase spending by considering such forms of “frustrated” spending.

A rarely discussed aspect of adding value is the introduction of air passenger duties or departure taxes, for instance, in the form of an air passenger duty. This would seem specifically relevant for countries that have seen significant growth rates in the tourism system, or a decline in the average length of stay. A higher cost of air travel is likely to stimulate interest to stay longer, with evidence that even a very significant air passenger duty will only affect growth rates modestly (Markham et al. 2018; Seetaram, Song, and Page 2014). An air passenger duty can thus have direct and indirect economic benefits, as it helps reducing growth rates that are excessive, or because it increases length of stay. An example for a country that may profit from an APD is Iceland, where international tourist arrival growth by air has varied between 17.8% and 39.5% per year in the period 2010-2017 (Statistics Iceland 2020), leading to rising emissions (Sharp, Grundius, and Heinonen 2016) and local concerns over economic resilience (Helgadóttir et al. 2019). As an air passenger duty can be implemented at a very low administrative cost, it can make a direct and highly significant economic contribution to the national economy.

Reducing Leakage

An aspect that is rarely discussed by destination managers is economic leakage, in the form of provisions, bonuses, or fees paid to third entities involved in a destination. Economic leakage received much attention starting in the 1970s in the context of tourism as a development strategy (e.g., Hills and Lundgren 1977; Jafari 1974). It may be time for destinations to reconsider these issues. For instance, in some destinations, entire tourist areas consist of franchises owned by foreign corporations, with obligations for the franchise taker to pay for brand membership, branded (and often globally sourced) foodstuffs, or branded packaging. An easy way to retain money in the local economy is to prioritize local, individual retail initiatives in destinations. Local economic benefits will be particularly large where purchases are made locally as well, for instance foodstuffs from regional farmers by cafés and restaurants (Hall, Mitchell, and Sharples 2004).

Through the platform economy, the share of financial resources leaving national economies has grown enormously: It is known, for example, that hotels advertising through the largest reservations platform Booking.com will have to pay fees ranging between 12% and 20% of the price charged (Gössling et al. 2016). Hotels may voluntarily increase this share in exchange for a high listing position. The question is whether destinations are better off developing their own national platforms and banning the large platforms entirely. According to Turkish newspaper Hürriyet Daily News (2018), Booking.com was at least temporarily banned from operating in Turkey, and similar restrictions were sought by The Association of Turkish Travel Agencies for AirBnB and other platforms. Where this is legally feasible, destinations with unique features have no reason to pay commissions to global platforms, specifically since this also implies a loss of control over destination image and business reputation (Gössling and Hall 2019). While reservations have key strategic relevance for destinations, the platform economy also has oligopolistic tendencies in a range of other areas, such as transportation (Uber) or consumer items (Amazon) that destinations may wish to address as they imply leakage.

Another important example for leakage in the tourism system are bonus and payment systems. These are outside destination control, but can be mentioned here as issues related to losses to destinations. The most prominent example of bonus systems are frequent-flyer programs that reward high-mobility patterns with additional free mobility or other benefits, such as upgrades or onboard purchases (Ostrowski, O’Brien, and Gordon 1993). Not only do such systems reduce profitability, they also increase transport demand (free travel, discounts) or transport energy intensities (free upgrades) (Mowlana and Smith 1993), while “justifying” overcapacity in the system (Gössling, Fichert, and Forsyth 2017). As airlines will be reluctant to abandon loyalty schemes, it is up to destinations to limit bonus programs. As bemoaned by the Financial Times (2019), Norway taxes bonus points gained through business travel, and the country even banned frequent flier schemes from 2002 to 2013. There is thus legal precedent for restrictions, as also recently recommended by the UK Committee on Climate Change (CCC 2019) to address the high-frequency, short-duration model of air travel practiced by the so-called high emitters, that is, the 15% of travelers who account for a disproportionate share (upward of 70%) of air travel consumed by British nationals in a given year.

Finally, global tourism is entangled in global finance structures, as discussed for cruise ships (Kizielewicz 2017). Even more important are digital payment systems needed to facilitate financial transactions. For customers, credit cards are an easy way of making payment. Some credit cards even pay earnings on transactions that customers can redeem on specific purchases, suggesting to customers that credit cards generate benefits rather than a cost. Yet, for many businesses, the cost of credit card transactions is significant (Börestam and Schmiedel 2012; Verdier 2011). More recently, a wide range of smartphone-based payment systems has come into existence, while cyber currencies have been discussed as options to reduce the cost of transactions: Bitcoin, for example, is apparently already accepted by some large platforms (Önder and Treiblmaier 2018). While these developments highlight the need to discuss associated issues such as tax evasion, money laundering, and payment for illicit products and services, they are also an expression of the high cost of monetary transactions, and many businesses search for alternatives. As Önder and Treiblmaier (2018, p. 2) affirm, “small tour operators need to be part of a Global Distribution System in order to be competitive and must therefore comply with the stipulated rules and accept the mandated fees.” They also suggest that for this reason, blockchain-based travel platforms will eliminate intermediaries.

Discussion and Conclusions

The global economy must fully decarbonize over the coming 30 years (IPCC 2018). Tourism is inescapably implicated in this imperative given that the tourism system is a significant contributor to global carbon emissions (Lenzen et al. 2018). Yet while other economic sectors have advanced a carbon mitigation commitment, the tourism response to the climate emergency has been both belated and ineffective (Scott et al. 2016). To date, the efforts of global organizations such as the UNWTO and WTTC, and initiatives such as the UN Sustainable Development Goals and ICAO CORSIA scheme have offered little more than publicly palatable and politically agreeable rhetoric while global tourism emissions continue to increase ahead of the steep arrivals growth curve (Lyle 2018). The prevailing failure is epitomized by the continuing inability of the ICAO to achieve a meaningful resolution to continuing high annual growth in international aviation emissions (Higham, Ellis, and Maclaurin 2019). Carbon emissions per dollar tourism GDP continue to increase rather than decrease (Lenzen et al. 2018). Given the failure of global action on tourism carbon mitigation, it is clearly apparent that the immediate response must come from the subglobal (destination) level of climate leadership and action.

Destinations consequently have a key role to play in reducing emissions, as they comprise clusters of tourism stakeholders who can work toward decarbonization while meeting secondary goals of increasing profitability and resilience. Given the observed instability in the global tourism system and its tendency to become more vulnerable (Scott, Hall, and Gössling 2019), there is a need for destinations to understand interdependent risks of low profitability, carbon intensity, and climate change, all of which demand fundamental changes in volume-growth destination management approaches that seek to constantly increase tourist arrivals. The new low-carbon imperative makes it necessary to prioritize value over volume, and to rethink the mechanisms for value generation (Oklevik et al. 2019; Scott, Hall, and Gössling 2019). Much evidence suggests that destinations have not proactively sought to explore existing opportunities to reduce leakage and to increase the value of tourism systems, and the major obstacle to destination management under the low-carbon imperative may be the mindset of destination planners.

The challenge for destinations is to support processes that will help tourism to develop along a net zero emission trajectory to 2050. Destinations can support these processes directly, through the market mix they seek to attract, with closer markets being favorable to distant ones, while fostering discrete markets that use more rather than less sustainable transport modes to both travel to and from the destination, and in transport preferences and decision making at the destination (Hopkins and Higham 2016). Destination managers must focus on the mechanisms available through the involvement of a range of tourism system players to increase tourist length of stay (Gössling, Scott, and Hall 2018). Clearly, length of stay is implicated in such things as annual leave provisions, transport capacities, services and costs, tour packages, accommodation pricing mechanisms, and destination services and activities, among other things. They can also address growth indirectly, through the implementation of carbon-based air passenger duties. The processes leading to change rely on destination managers offering leadership and collaborating with policy makers and businesses in implementing the frameworks for such destination models, and fostering the interests of businesses to translate these into profitability.

Clearly, the risks for tourism economies associated with energy-intense volume growth models are becoming increasingly acute (Scott, Hall, and Gössling 2019). Thus, it is necessary to analyze the destination management challenges arising from a low-carbon proposition, which center on continuing economic viability while driving down tourist emissions. In taking up the challenge, this article contributes a conceptualization of a destination management model under the low-carbon imperative. Our conceptual model is underpinned by a destination management tripartite: lowering carbon emissions, adding value per tourist arrival, and reducing economic leakage, to move destination management approaches from a volume to a value imperative.

This destination management tripartite offers the opportunity to explore avenues to reduce tourism carbon emissions for greater profitability on the basis of a leakage/spending value dichotomy proposition. Our discussions do not represent an exhaustive review of the strategic directions arising from a new climate-conscious destination management paradigm. It does provide a planning framework for forward-thinking national/local governments and national/regional tourism organizations, whether they be inspired by vanguard action and leadership in tourism carbon mitigation or simply engaged with destination risk mitigation. Our conceptual contribution should encourage further research and dialogue into the opportunities available to destinations to effectively reduce leakage and add value while pursuing reduced tourism carbon emissions and enhanced system resilience. This could for instance include research into business carbon intensities and the need to introduce new performance indicators, such as the ratio of profits to emissions. Research on leakage should investigate the implications of the platform economy for destination models. Destination resilience and its foundations are another aspect deserving greater academic attention, in which a specific focus may have to be on the avoidance of future pandemics. Most importantly, however, the low-carbon imperative should inspire destination managers to take up and offer leadership, and to fundamentally reinvent tourism destination management systems in accordance with the urgent net-zero carbon 2050 objective (IPCC 2018).

Footnotes

Acknowledgements

The authors acknowledge the Otago Business School (University of Otago) and the organisers of the Tourism Policy School (March 8–9, 2019), Queenstown (New Zealand). The discussions that took place throughout this event richly informed the planning and writing of this article.

Author’s note

Stefan Gössling is also affiliated with Service Management and Service Studies, Lund University, Helsingborg, Sweden and School of Business and Economics, Linnaeus University, Sweden.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.