Abstract

In China, the absence of a strict referral system leads to overcrowding in tertiary hospitals and underutilization of primary care, challenging the implementation of a tiered diagnosis and treatment system. This study investigates how differential health insurance reimbursement rates can be leveraged to guide patient flow. We developed an agent-based simulation model, calibrated with real-world data on hypertensive inpatients from Beijing (2015-2017). The model simulated patient healthcare-seeking choices under various reimbursement scenarios for primary, secondary, and tertiary hospitals. Adjusting reimbursement rates significantly redirected patient flow and altered medical insurance fund expenditure. Increasing the reimbursement rate for primary hospitals proved particularly effective in channeling patients toward them. We identified an optimal balance—maximizing the proportion of hypertensive inpatients seeking care at primary hospitals (achieving 36.41%, compared to an observed baseline of 16.39%) while controlling total fund expenditure—when reimbursement rates were set at 95% for primary, 85% for secondary, and 70% for tertiary hospitals. Differential health insurance reimbursement serves as a potent policy lever to steer patient flow within a tiered healthcare system. The agent-based modeling approach provides a valuable tool for policymakers to simulate and identify optimal reimbursement strategies, thereby promoting efficient healthcare delivery and sustainable fund management.

Introduction

Hierarchical Diagnosis and Treatment and Medical Insurance Payment

A defining feature of China’s healthcare landscape is the considerable freedom patients enjoy in choosing their healthcare providers. The absence of a strict mandatory referral system allows patients to directly access tertiary hospitals, bypassing primary care facilities. This autonomy, however, presents a double-edged sword: while empowering individual choice, it has resulted in severe overcrowding at top-tier hospitals and chronic underutilization of primary care institutions. Consequently, establishing and promoting an effective hierarchical diagnosis and treatment system has become a cornerstone of China’s ongoing healthcare reform, with its success largely hinging on the effective implementation of this tiered structure.

Recognizing this challenge, the State Council General Office issued the “Guidance on Promoting the Construction of Hierarchical Diagnosis and Treatment” in 2015. This policy proposed establishing a tiered system by starting with common and chronic diseases, aiming to guide patient flow through differentiated medical insurance payment policies across different levels of medical institutions. 1 To further cultivate a rational medical treatment order, the National 14th Five-Year Plan emphasized the implementation of differentiated medical insurance payment and pricing policies. 2 As an economic lever to modify residents’ healthcare-seeking behavior, medical insurance payment policy design plays a pivotal role in advancing hierarchical diagnosis and treatment in China.3,4

Subsequent policy documents, including the 2017 “Guiding Opinions on Further Deepening the Reform of the Basic Medical Insurance Payment Method” 5 and the 2020 “Opinions on Deepening the Reform of Medical Insurance System,” 6 have called for more sophisticated management and a manageable, efficient payment mechanism. These developments impose stricter requirements on China’s medical insurance payment system reform. A central and challenging issue remains: how can medical insurance payment reforms effectively incentivize hierarchical diagnosis and treatment?

Medical Insurance Policies and Patient Choice of Medical Care

The unique characteristics of medical services distinguish patient demand and utilization behavior from that of ordinary goods. 7 The study of healthcare demand behavior originated from utility theory, analyzing the maximization of utility function under income constraints. Grossman’s health human capital model and the inclusion of health insurance factors by Newhouse and Phelps’ are classic frameworks for analyzing factors influencing medical demand. 8 Andersen further proposed that factors influencing medical demand include propensity characteristics, enabling resources, and need, providing a robust analytical framework for understanding patients’ healthcare choices. 9 This model has been revised over the years, offering a basis for explaining the influence of various factors on healthcare choices and their interactions.

Among the numerous factors influencing residents’ healthcare behavior, key determinants include gender, income, age, and distance.10 -13 Crucially, effective medical insurance policies can facilitate patient access to care.14 -16 When the out-of-pocket payment decreases, the consumption of medical services increases significantly, 17 a trend supported by empirical data from Taiwan. 18

While it is well-established that medical insurance stimulates residents’ healthcare demand, a more nuanced question arises: does medical insurance policy specifically affect residents’ demand behavior for different levels of care?

Residents’ choice of medical institutions is fundamental to the hierarchical diagnosis and treatment system. Some studies have found that medical insurance policies can influence patient hospital choice by increasing the cost disparity between hospitals of different levels. 19 Research from China indicates that reimbursement rates adjusting for different levels affect communitywide care choices. 20 Another Chinese study suggested that varying reimbursement rates influence the decision to seek treatment, with increases for primary hospitals boosting their patient share. 21

Differential reimbursement rates create a tiered structure of out-of-pocket costs for patients. When seeking care for a comparable condition, the financial burden is significantly lower at primary hospitals compared to tertiary ones due to the higher reimbursement rate.17,18,21 This cost disparity serves as a powerful economic incentive, making the policy-preferred option—visiting primary hospitals—also the most financially rational choice for patients, thereby channeling patient flow in a way that supports hierarchical diagnosis.

Globally, adjustments to medical insurance policies have been used to influence healthcare utilization. In the United States, commercial insurers have implemented “gatekeeper” systems through differentiated reimbursement packages. 22 In France, patients can choose whether to participate in a social insurance-based “gatekeeper” system, with the government providing different reimbursement rates for different visit types. 23 Australia use different reimbursement rates for general practitioners and specialists to guide patient flow.

Agent-Based Modeling

Medical insurance policy creation and implementation are highly uncertain and complex processes involving various stakeholders, including patients, physicians, and hospitals. Traditional qualitative and quantitative research methods possess inherent limitations in capturing this complexity. In contrast, simulation methods, being experimental, process-oriented, and future-focused, offer a fresh perspective on health policy research and have recently gained prominence.

Agent-based modeling and simulation (ABMS) is a computational microsimulation technique that involves modeling a system’s individuals(agents) and developing the system’s overall behavior through their interactions.

In 2017, The Lancet published an expert review calling for a complexity modeling approaches to address global public health challenges, highlighting the important role of ABMS. 24 Currently, ABMS is widely used in public health to model infectious disease epidemics,25 -27 chronic diseases,28,29 health behaviors,30 -32 healthcare delivery,33,34 and health economics. 35

Several studies have explored the impact of insurance policies on patients’ healthcare choices using ABMS, including the influence of costs, 36 comparisons of outpatient reimbursement options, 37 the effects of accountable care organizations, 38 and the impact of widening cost gaps between hospital levels. 19 Integrating the ABMS into medical insurance policy analysis can help identify impact patterns, forecast the macro and micro effects of potential policy adjustments, and thus facilitate more scientific, and effective policy formulation.

A study by Tan et al used ABMS to adjust reimbursement rate for different hospital levels separately and found the impact of differential medical insurance reimbursement on inpatient chronic disease residents to be limited. 39 This suggests that isolated adjustments to the reimbursement rate for a single hospital level have a limited effect on guiding patient distribution. Thus, a significant and underexplored research gap exists in determining how to systematically and combinatorially adjust rates across multiple hospital levels to identify the optimal “reimbursement combination” that best balances patient flow with medical insurance fund control.

This study selected hypertensive inpatients as the research population for the following reasons: First, hypertension is a common chronic condition and a key focus within the tiered diagnosis and treatment policy. Second, its disease severity has clear classification standards (ICD-10), facilitating the precise characterization of patient heterogeneity within the model. Finally, the relevant data possesses good accessibility, providing a reliable foundation for model construction and validation.

Compared to previous studies, this research introduces key innovations in both model design and research focus. While the ABMS studies19,20 concentrated on the impact of cost disparities or a single type of insurance, and Tan 39 was confined to adjusting the reimbursement rates of hospital levels in isolation, this study aims to synchronously and coordinately adjust the medical insurance reimbursement rates for primary, secondary, and tertiary hospitals. It dynamically observes changes in patient flow and medical insurance funds under this complex scenario that more closely mirrors real-world policy, with the goal of identifying synergistic effects and optimal policy configurations that cannot be detected through single-policy adjustments.

Based on the above rationale, this study aims to construct a real-world data-based ABMS model to simulate the healthcare-seeking behavior of hypertensive inpatients and its impact on medical insurance fund expenditure under different medical insurance reimbursement rate combinations. We propose the following core hypothesis: Synchronously adjusting the medical insurance reimbursement rates across multiple hospital levels can effectively guide patient flow, and there exists an optimal reimbursement rate combination that maximizes the proportion of patients seeking care at primary hospitals while simultaneously ensuring the controllability and balance of medical insurance fund expenditure. The results of this study are intended to provide a quantitative decision-making basis for the refined reform of medical insurance payment methods.

Materials and Methods

Study Design and Data Sources

This was an agent-based simulation study utilizing real-world data from Beijing, China, covering the period from 2015 to 2017. The study population consisted of hypertensive inpatients enrolled in the Beijing urban residents’ basic medical insurance, screened according to the following criteria: ① coverage under the aforementioned insurance, ② inpatients status in primary, secondary, or tertiary hospitals in Beijing, ③ age over 35 years.

The simulation was initialized with 2165 agent residents, a number that represents a 1:10,000 scale-down of the actual Beijing resident population during the 2015 to 2017 period. A total of 65 hospitals were included based on the 2015 to 2017 Beijing Health and Family Planning Development Statistics Bulletin, comprising 40 primary, 17 secondary, and 8 tertiary hospitals.

Basic demographic data for Beijing residents were sourced from the Beijing Municipal Bureau of Statistics. The Information Center of the Beijing Municipal Health Commission provided retrospective, anonymized, individual-level discharge records for hypertensive inpatients from Level II and above hospitals in Beijing. Patient records with a primary diagnosis of hypertension (ICD-10 codes: I10xx02, I10xx03, I10xx04, I10xx05) were screened to extract information on admissions, total costs, out-of-pocket costs, and admissions by region and age. Data for primary care institutions were supplemented from 3 district-level social management centers and several community health service centers in Beijing.

This study was reported in accordance with the Consolidated Health Economic Evaluation Reporting Standards (CHEERS) guideline. 40

Modeling Approach and Justification

Unlike traditional econometric methods that often identify average effects from historical data, ABMS is particularly suited for modeling complex, dynamic systems involving heterogeneous individuals. Its advantage lies in capturing individual heterogeneity, simulating interactions between agents (eg, patients, hospitals), and conducting counterfactual policy experiments to observe emergent system-level outcomes, such as shifts in patient flow and insurance fund expenditure under novel reimbursement combinations.41 -43

Study Assumptions

The following assumptions were made, informed by the ABMS literature and the practical context of patient visits.

These assumptions are interconnected and serve to define the scope and focus of our model. The stability of the study population (H1) and the specific insurance coverage (H2) together establish a well-defined cohort for examining policy effects. Focusing solely on inpatient care (H3) while assuming full insurance coverage (H4) allows us to isolate the role of reimbursement rates in patients’ decision-making. The standardized classification of hypertension severity (H5) introduces meaningful variation among patients, enabling us to examine how disease severity might influence choices when faced with different reimbursement rates. While these choices necessarily simplify the real-world context, they provide a coherent foundation for examining our core research question regarding how combinations of reimbursement rates might affect patient flow.

Model Design

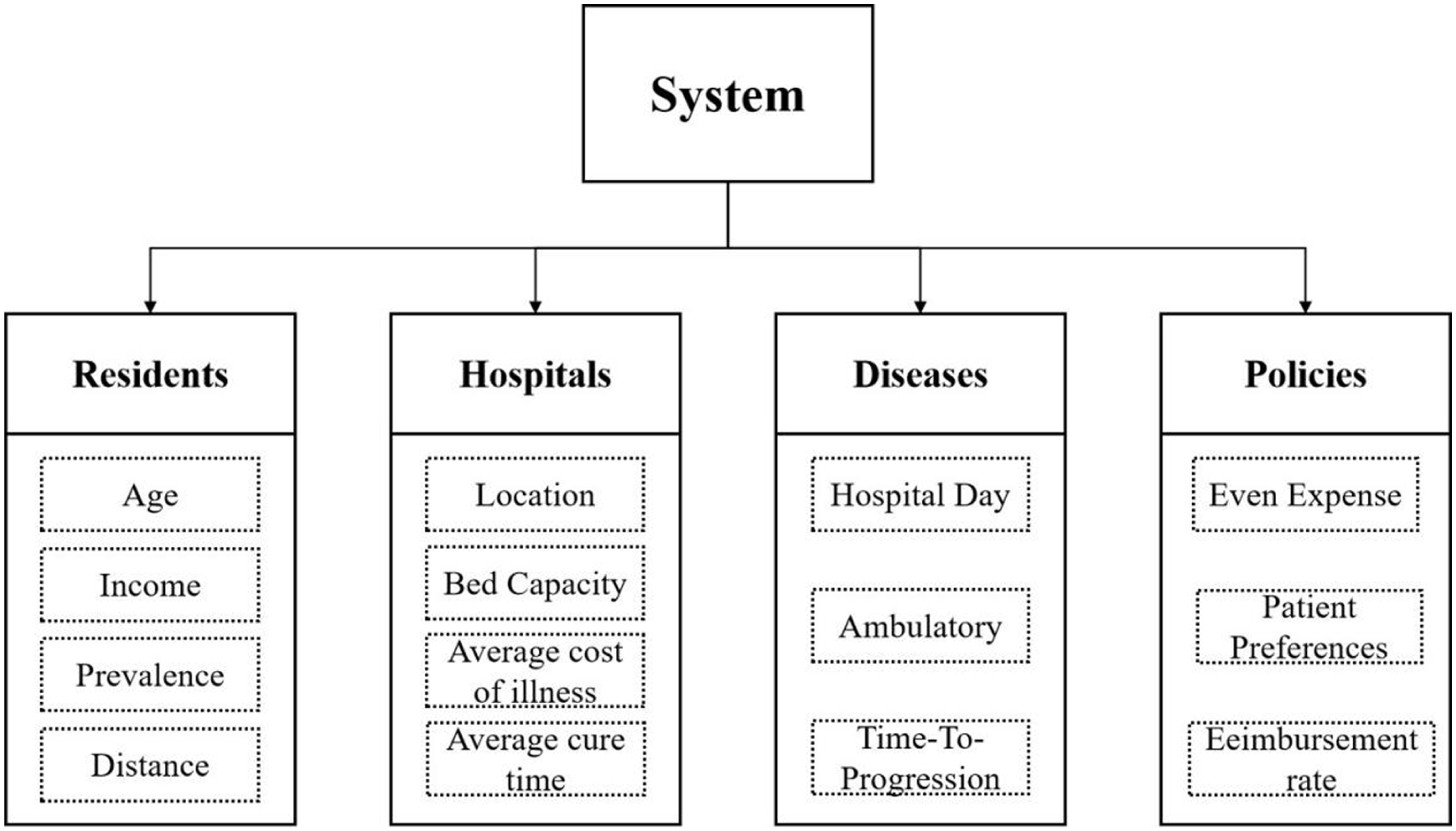

The simulation system integrated 4 interconnected sub-models: patients, hospitals, diseases, and policies (Figure 1). The patient and hospital models were parametrized using empirical data, while the disease and policy models were constructed based on established literature and clinical guidelines.44,45

Schematic of the system design, including the following 4 models: patients, hospitals, diseases, and policies.

The core agent decision-making process is illustrated in Figure 2. A key behavioral mechanism is the distance tolerance coefficient (K), which modulates a patient’s sensitivity to travel distance based on disease severity. This design is grounded in the empirically observed tendency that patients with more severe conditions prioritize clinical capability over proximity.46 -49 Consequently, in our model, K increases with hypertension severity (Level 1: K = 1; Level 2: K = 2; Level 3: K = 3), effectively expanding the acceptable travel range for more severe cases.

Model structure representing the general flow of patients in the simulation. *Dcost: The average cost of medical care for hypertension.

Hospital choice was modeled using a preference index (PI), quantified as a decreasing function of the out-of-pocket cost ratio between high-level (X) and low-level (Y) hospitals:

where

The model was implemented using AnyLogic.

Statistical Analysis

The data analysis in this study encompassed both descriptive statistics and model validation metrics. Descriptive statistics were used to summarize the characteristics of the patient population and hospital resources. For model validation, the primary statistical measures were the Relative Error (RE) and Root Mean Square Error (RMSE), calculated to quantify the discrepancy between simulated outputs and observed real-world data.

The formulas for these calculations are as follows:

Here,

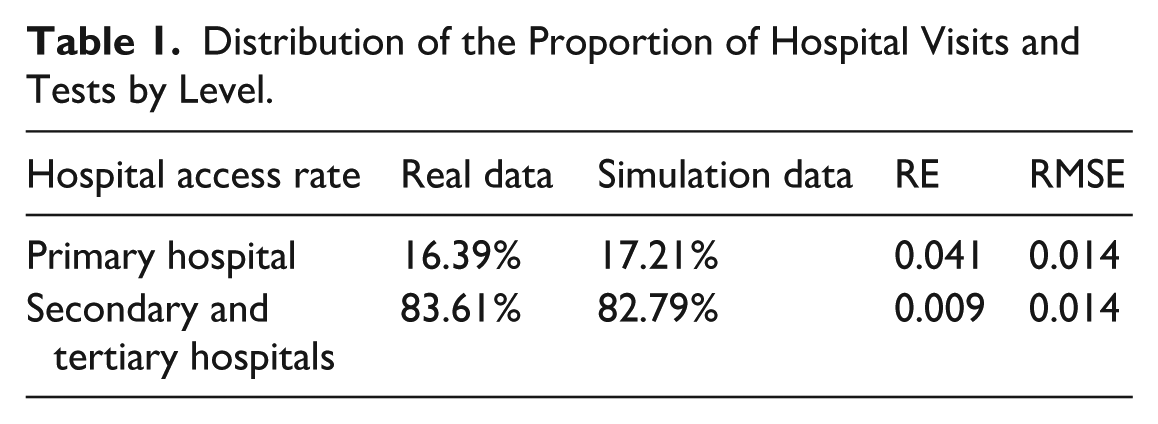

As shown in Table 1, all validation metrics fell within these acceptable ranges, confirming the model’s predictive accuracy.

Distribution of the Proportion of Hospital Visits and Tests by Level.

Results

Overview of Key Findings

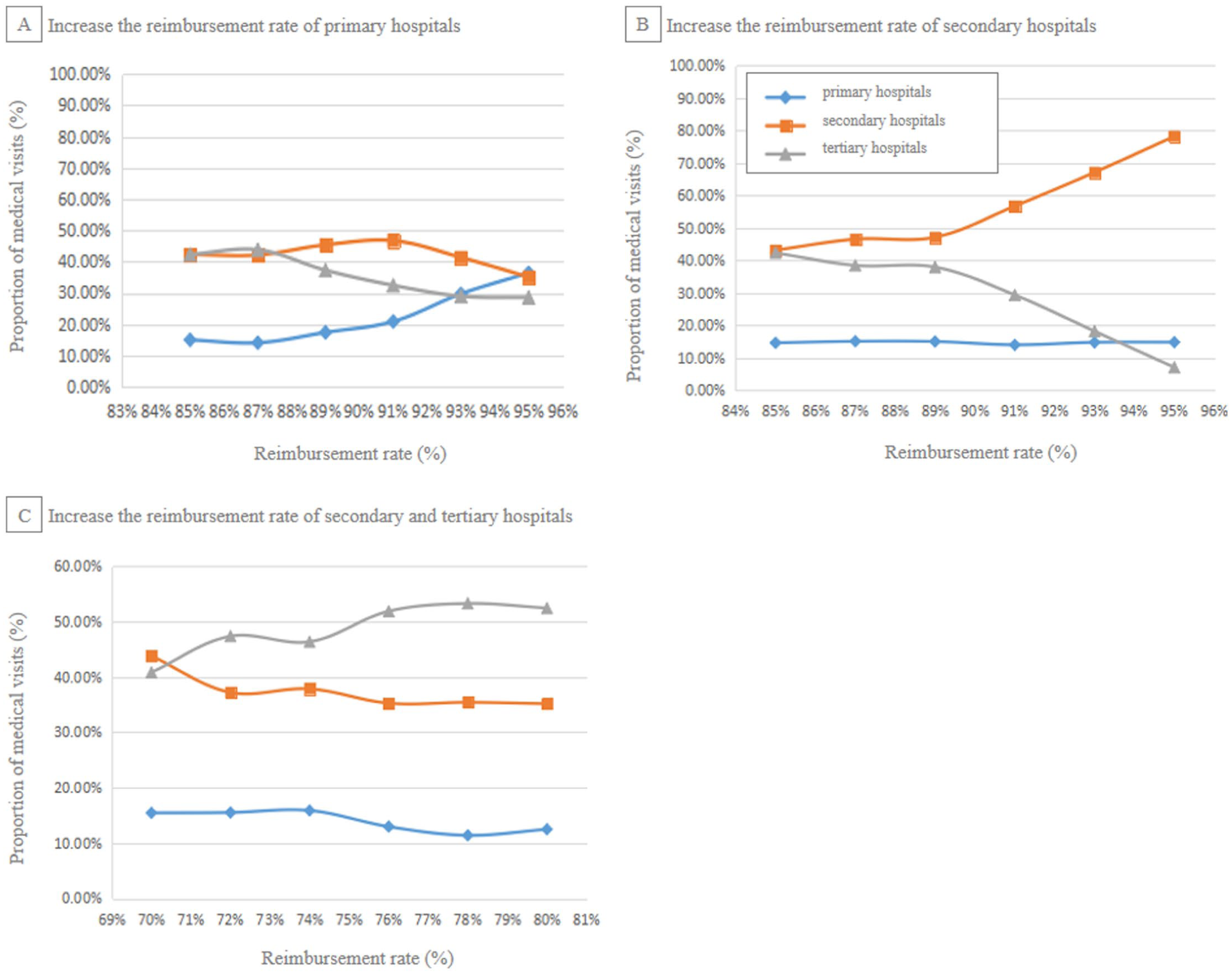

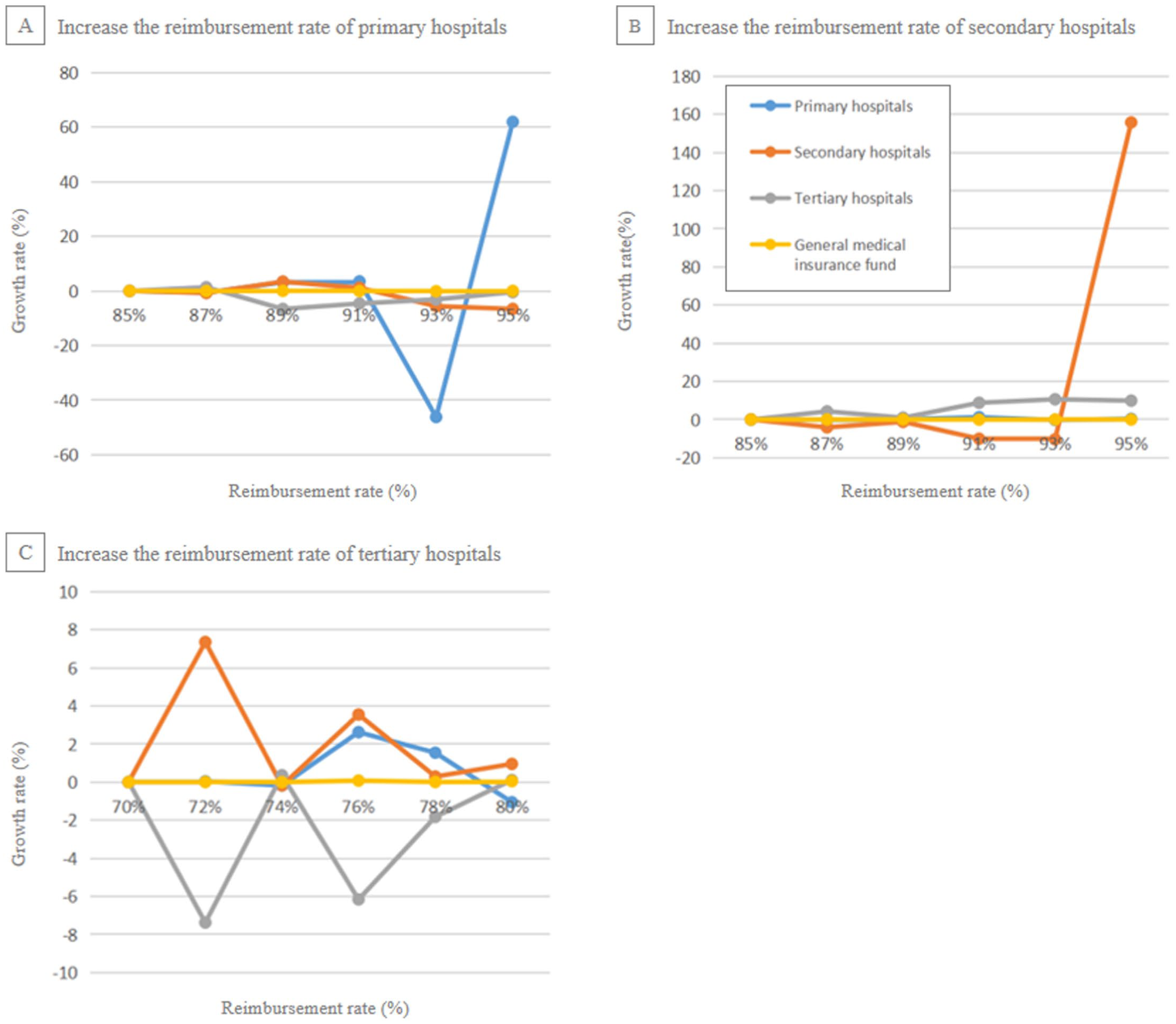

We conducted a total of 126 simulation runs, organized into 7 experimental sets. Each set involved adjusting reimbursement rates and was run 6 times with incremental 2% changes. To minimize the impact of random factors, the “random seed” option was selected under the “randomness” setting. Each specific alteration was tested 3 times, and the final outcome for a simulation experiment was determined by averaging these 3 results. Figures 3 and 5 illustrate changes in patients’ healthcare choices after adjusting reimbursement rates for different hospital levels separately or simultaneously, while Figures 4 and 6 show corresponding changes in the growth rate of medical insurance fund expenditure at each hospital level.

Changes to patient access options brought about by adjusting reimbursement rates for different levels of hospitals.

Changes in the growth of the medical insurance fund brought by adjusting reimbursement rates for different levels of hospitals.

Changes to patient access options brought by adjusting reimbursement rates for different levels of hospitals.

Changes in the growth of the medical insurance fund brought about by adjusting reimbursement rates for different levels of hospitals. *Q1 through Q6 correspond to the reimbursement rates after each 2% increase, with Q1 being the initial rate of 85% for primary and secondary hospitals and 70% for tertiary hospitals.

Our simulation experiments demonstrated that synchronously adjusting medical insurance reimbursement rates across hospital tiers effectively redirected patient flow and altered the distribution of medical insurance fund expenditure. The most significant steering effect was achieved by increasing the reimbursement rate for primary hospitals, which consistently channeled a greater proportion of hypertensive inpatients toward primary care. An optimal balance—maximizing primary hospital utilization while maintaining control over total fund growth—was identified when reimbursement rates were set at 95% for primary, 85% for secondary, and 70% for tertiary hospitals.

The results in Figure 3 demonstrate that increasing the reimbursement rate for primary hospitals is the most potent single policy lever for redirecting patients from tertiary to primary care. For policymakers, this suggests that investing financial incentives at the grassroots level is a more direct and effective strategy to relieve overcrowding in top-tier hospitals than disincentivizing tertiary care alone.

Figure 4 highlights a critical financial insight: steering patient flow toward lower-cost primary and secondary hospitals is key to ensuring the financial sustainability of the medical insurance fund. This demonstrates that the policy goal of hierarchical diagnosis is not only about patient distribution but also an essential mechanism for long-term cost control.

The synergistic effect observed in Figure 5 underscores the importance of combinatorial policy design. Adjusting reimbursement rates at multiple levels simultaneously (eg, raising primary while lowering tertiary) creates a powerful dynamic that is more effective than any single adjustment. Policymakers should therefore consider systemic reimbursement packages rather than isolated rate changes.

As shown in Figure 6, the fiscal impact on the insurance fund varies significantly depending on the combination of reimbursement rates. This allows policymakers to calibrate and fine-tune multi-level policies, finding a balance that achieves the desired patient redistribution without placing undue stress on the fund.

Patient Flow in Response to Single-Level Reimbursement Adjustments

Adjusting the reimbursement rate for each hospital level individually revealed distinct patterns in patient steering.

As the reimbursement rate for primary hospitals increased, the proportion of patients choosing them rose steadily. This confirms that financial incentives are a potent tool for making primary care more attractive to patients. Increasing the reimbursement for secondary hospitals caused a dramatic shift, attracting patients primarily from tertiary hospitals rather than primary ones. This suggests that secondary hospitals serve as a viable and preferred alternative to tertiary facilities when the financial incentive is favorable. An increase in tertiary hospital reimbursement rates resulted in only a minor uptick in their patient share, but significantly increased the financial burden on the insurance fund, indicating poor cost-effectiveness.

The Synergistic Effect of Multi-Level Reimbursement Adjustments

Simultaneous adjustments revealed synergistic effects that were not apparent from single-level experiments. For instance, concurrently increasing primary reimbursement while decreasing tertiary reimbursement (eg, Primary: 95%, Tertiary: 70%) produced a strong effect, efficiently shifting patients from tertiary to primary care. In contrast, adjusting only secondary and tertiary rates together merely redistributed patients between these 2 levels without effectively promoting primary care utilization.

Identification of an Optimal Reimbursement Combination

Through 126 simulation experiments, we identified several reimbursement combinations that improved patient distribution. The most optimal combination, which achieved the highest flow to primary hospitals while ensuring sustainable fund expenditure, is presented in Table 2.

Optimal Reimbursement Combinations for Steering Hypertensive Inpatients.

The optimal combination (Experiment 1) showing that a high reimbursement rate of 95% for primary hospitals, coupled with a descending rate for higher-level hospitals, successfully directs over 36% of inpatients to primary care—more than double the baseline rate of 16.39%.

Dynamics of the Medical Insurance Fund

The redistribution of patients had a direct impact on the medical insurance fund. Scenarios that increased the patient share at primary and secondary hospitals, which have lower average costs, helped alleviate the growth pressure on the fund. Conversely, policies that increased the patient share at tertiary hospitals accelerated fund expenditure. The optimal combination (95%, 85%, 70%) not only improved patient flow but also contributed to a more sustainable financial trajectory for the insurance fund.

Discussion

The agent-based simulation model developed in this study effectively captured the dynamics of patient flow and medical insurance fund expenditure across hospital levels under varying reimbursement rates, aligning with findings from prior research in China indicating that reimbursement rates significantly influence medical demand behavior. 51 The most significant finding is that an optimal configuration exists (95% for primary, 85% for secondary, and 70% for tertiary hospitals), which successfully balances the dual objectives of guiding patients to primary care and ensuring the sustainability of the medical insurance fund. Consistent with the literature, increasing the reimbursement rates generally increased patients volume and visits at the respective hospital level. 52 Although chronic disease patients often prefer high-level hospitals, cost remains a factor in their decision-making process.53,54 The implementation of differentiated reimbursement rate demonstrates a positive impact, with an appropriate differential proving more effective. To harness the benefits of medical insurance adjustments, a differentiated reimbursement policy based on disease type, offering higher rates for chronic diseases treated in primary hospitals, could effectively alleviate patient’ financial burdens.

Our simulation results confirm that differential reimbursement rates significantly impact medical insurance fund flows. A critical observation is that when rates were adjusted for multiple hospital levels simultaneously, trends in average costs and patient out-of-pocket expenses were not always aligned. This implies that while a hierarchical system might meet access needs, it does not automatically guarantee lower overall medical costs. Although increasing the proportion of patients visiting primary and secondary hospitals can reduce individual out-of-pocket expenses, it may simultaneously strain the medical insurance fund if not carefully calibrated. Therefore, the effect of any single medical insurance policy is limited in motivating fully rational patient care-seeking. 55 Achieving hierarchical diagnosis and treatment requires synergistic efforts integrating medical insurance, medical service delivery, and pharmaceutical policies.

Currently, medical insurance reimbursement rates in Beijing are relatively high, shifting focus toward addressing systemic weaknesses, such as the quality of primary care and medication availability. When designing a hierarchical system, it is crucial to consider the interests and establish coordination mechanisms across insurance, care delivery, and pharmaceuticals to genuinely guide patients toward primary healthcare. Indeed, insurance policy adjustments represent just 1 lever for promoting hierarchical diagnosis and treatment.

Improving the service capacity of primary hospitals is fundamental to change residents’ medical care choices. Previous studies consistently identify hospital quality as a top selection criteria for patients,56 -58 which explains the default preference for high-level hospitals. As economies develop and incomes rise, health consciousness increases, leading individuals to seek better medical technology, often perceived as concentrated in higher-level facilities. From an institutional perspective, hospitals at different tiers have distinct functions and resource endowments; high-level hospitals possess more abundant resources and advanced technologies, better meeting the complex needs of chronic diseases patients.

Several studies from China suggest that implementing family doctor contract services and establishing medical alliance can improve patient perceptions of primary care quality and help address quality deficits.59 -62 Therefore, for primary hospitals to enhance their service capacity, they must actively leverage favorable policies like family doctor contracts and medical alliances. 45 Providing technical and expert support from higher-level hospitals to primary hospitals within the same region can raise standards. Simultaneously, the participation of higher-level hospital specialists in family doctor contract service can improve service quality and build resident trust. This improves the patient’s access environment, encouraging voluntary choice of primary hospitals and fostering a more rational care-seeking pattern. In this regard, China’s National Health Commission proposed supportive mechanisms for primary hospitals in 2023, such as mobile medical services and specialist secondments. 63 Future efforts could effectively enhance primary care quality by deploying medical resources through mobile services and specialist stations.

Strengths and Limitations

The simulation approach used in this study bridges, to a certain extent, the gap between traditional qualitative and quantitative research methods. Our model accounts for the heterogeneity and complexity of patients’ healthcare choice behavior, enabling better simulation and prediction of the impacts of medical insurance policy adjustments on both patient choices and fund expenditures.

Several limitations of this study should be considered. First, the model was designed and calibrated specifically for hypertensive inpatients in Beijing; thus, the exact optimal reimbursement rates may not be directly transferable to other regions with different economic levels, medical resource distributions, or patient preferences. Second, the model considered only inpatient behavior, excluding the potentially influential role of outpatient visits and referrals. Third, we focused on a single chronic disease; the steering effect of reimbursement rates might differ for acute conditions or diseases with different clinical pathways. Fourth, given the agent-based simulation methodology employed—distinct from empirical studies relying on random sampling—no traditional a priori sample size estimation or power analysis was conducted.

Despite these limitations, the ABMS framework itself is highly adaptable. The model can be recalibrated and extended to other contexts by incorporating new regional data, adjusting core parameters (eg, distance tolerance, cost structures), and introducing different disease modules. Future research could apply this framework to other chronic diseases or integrate outpatient behavior to provide a more comprehensive tool for health policy design.

Conclusions

Leveraging real-world data, this research establishes a simulation framework to demonstrate that the systematic, combinatorial adjustment of reimbursement rates across hospital tiers is a potent mechanism for optimizing healthcare delivery. The findings confirm that such coordinated policy levers can simultaneously redirect patient flow toward primary care and ensure the financial sustainability of the medical insurance fund. The identified optimal rates offer concrete guidance for chronic disease payment reform, while the adaptable modeling framework provides a generalizable tool for forecasting policy impacts in diverse contexts. Prospective model enhancements, including the integration of parameters for health literacy and drug policies, promise to further increase its analytical robustness and utility for evidence-based health policy design.

Supplemental Material

sj-pdf-1-inq-10.1177_00469580261422679 – Supplemental material for Channeling Patient Flow in China: An Agent-Based Model of Insurance Reimbursement and Hierarchical Care

Supplemental material, sj-pdf-1-inq-10.1177_00469580261422679 for Channeling Patient Flow in China: An Agent-Based Model of Insurance Reimbursement and Hierarchical Care by Ning Zhao, Jia Yang, Mei Gu, Jin Li, Danhui Li, Wensheng Ju and Moning Guo in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Footnotes

Acknowledgements

List of Abbreviation

AMBS: Agent-based modeling and simulation

Ethical Considerations

The studies involving human participants are reviewed and approved by the Ethics Committee of Capital Medical University (NO.Z2020SY117).

Consent to Participate

Verbal informed consent was obtained from all participants. All methods were performed in accordance with the relevant guidelines and regulations.

Author Contributions

NZ and JY contributed to conception and design of the study, and contributed to the manuscript revision. WJ and MnG collected data and organized the database. NZ wrote the first draft of the manuscript. MG, DL and JL performed the statistical analysis. All authors contributed to reading the manuscript and approved the submitted version.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the National Natural Science Foundation of China (Grant Nos. 71603175 and 72274129).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The original contributions presented in the study are included in the article material, the data for this study are part of the overall project and so are not publicly available. Access to the datasets of this study can be directed to the corresponding authors.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.