Abstract

The goal of the Abia State Health Insurance Agency (ABSHIA) has been to increase coverage since its implementation. However, the sustainability of the scheme is crucial to continue providing affordable healthcare in the State. This study aimed to identify and compare factors that influence the sustainability of ABSHIA in rural-urban areas of Abia State. The study used a mixed-method cross-sectional design that involved collecting data through a questionnaire on enrollment, satisfaction, and willingness to renew membership. Key informant interviews and focus group discussions were also conducted to obtain qualitative data from healthcare providers and ward development committees. The collected data were analyzed using appropriate statistical tests. The results showed a higher enrollment in rural areas compared to urban areas, with no significant difference in satisfaction and willingness to renew membership between the 2 locations. The study also identified factors that positively influenced willingness to renew membership, but it was found that traveling a distance of 15 min or more decreased willingness to renew membership in urban Abia. Furthermore, poor health status was found to have a low influence on willingness to renew membership in rural Abia. Among other barriers to renewal, poor quality of care and, nonpayment of health workers’ capitation was identified as significant factors. It is crucial to prioritize the sustainability of ABSHIA to achieve the sustainable development goal of health for all in the State.

Three question-and-answer

In countries with a significant gap between rural and urban areas, various factors play a critical role in determining the sustainability of any health insurance scheme. To achieve universal health coverage and ensure the long-term viability of these schemes, it is essential to analyze these factors separately for both settings.

This research contributes to the field of public health by promoting sustainable social health insurance (ABSHIA) that considers the specific needs of both rural and urban populations. This can lead to improved health outcomes and a more equitable healthcare system for all citizens of Abia State.

The study has shown that the theory on user behavior and insurance adoption holds in the context of Abia State. It has identified critical areas for improvement within the healthcare system of the State. Lastly, this research provides valuable evidence to guide policy decisions around health insurance in Abia State.

Introduction

The World Health Assembly has been urging countries to prioritize the implementation of universal health coverage, which is a top issue on the sustainable development goals (SDGs) and global development agenda.1,2 Universal health coverage is a practical way of providing affordable access to promotive, preventive, curative, and rehabilitative services for all, which reduces the reliance on direct out-of-pocket payments. Out-of-pocket payments often create significant financial barriers to accessing healthcare, impoverishing lives, particularly in developing and underdeveloped countries.1,3

The Nigerian government introduced the National Health Insurance Scheme (NHIS) in response to the call for universal health coverage. This scheme is designed to reduce out-of-pocket payments and expand healthcare access, reducing health inequalities. The NHIS operates by pooling funds through contributions made by individuals or groups, which are then used to purchase covered services from healthcare providers on behalf of scheme members. The various mechanisms for pooling funds in the NHIS include social health insurance, community-based health insurance, medical savings accounts, and voluntary health insurance.2,4

After years of inadequate access to healthcare, frequent shortages of essential drugs and vaccines, uneven distribution of healthcare professionals, the proliferation of substandard health facilities, and the decline of hospitals into mere consulting clinics, the National Health Act was finally signed into law in 2014. This legislation aimed to establish a comprehensive framework for regulating, developing, and managing the health system in Nigeria. 5 Under the Act, the National Health Insurance Scheme is responsible for providing health coverage through the Basic Health Care Provision Fund (BHCPF). This fund is financed by an annual grant of not less than 1% of the consolidated revenue fund from the federal government, as well as other sources of funding such as grants from international donors and innovative sources. However, for States to receive funding, they must first establish primary healthcare development agencies and State health insurance agencies, among other requirements. 6

In 2019, the government of Abia State launched a social health insurance program known as the Abia State Health Insurance Agency (ABSHIA) to provide health insurance for about 200 000 residents. 7 The program provides a basic minimum package of health services at primary and secondary health facilities. The services offered include basic laboratory investigations, immunization services, basic surgical procedures, treatment of common diseases such as malaria, diarrheal and ENT infections, HIV, management of non-communicable diseases like hypertension and diabetes, maternal, newborn and child health care, eye care and emergency care, dental care, public health education and promotion, and in-patient admissions for a maximum of 10 days per year. The focus for the first 5 years of implementation is to enhance population coverage rather than benefit package expansion. 8 However, to achieve this goal, it is crucial to improve the quality of care provided, as this directly affects client satisfaction and the sustainability of the program.

The sustainability of a health insurance scheme refers to its ability to continue operating over time. Various indicators can be used to measure sustainability, such as satisfaction/acceptability, renewal/ownership, early engagement of stakeholders, funding, improved resources, institutionalization of activities and innovation. 9 Studies conducted in Ghana, Ethiopia, and Nepal have shown that determinants of sustainability in health insurance schemes include the quality of services, the cost of premiums, long waiting periods for administrative processing of membership cards, lack of confidence in the scheme, travel costs to health facilities, the conduct of health workers, and lack of institutional cooperation between service providers and regulating bodies.10 -13

It has been 4 years since the ABSHIA implementation in Abia State. Therefore, it is important to identify factors associated with the sustainability of the health insurance scheme in both rural and urban Abia State. This will help guide the government in achieving high coverage and sustaining the health insurance scheme in the State.

Materials and Methods

Study Area

This study was conducted in Abia State, Nigeria, which was established in 1991. The State is located in the southeastern region of Nigeria and covers an area of 5834 km 2 , which is approximately 5.8% of Nigeria’s total land area. Abia State shares boundaries with Anambra, Enugu and Ebonyi to the north and northeast, Imo to the west, Cross River and Akwa Ibom to the east, and Rivers to the south. The southern part of the State is a low-lying tropical rainforest with some oil palm brush. The population of Abia State is about 4.1 million, and the majority of the people are Igbo Christians. The State has a governor and 17 local government areas with 292 wards Abia State has an abundance of educational institutions, including over 800 primary schools, 160 secondary schools, 1 teacher-training college and 5 technical colleges. Abia State University at Uturu and the Abia State Polytechnic at Aba are 2 of the most prominent institutions. The main occupations in Abia State are trading, farming, and civil service employment. Health services in Abia State are provided at 3 levels of care: primary, secondary, and tertiary. There are 2 tertiary hospitals and 15 general hospitals across the 17 local government areas. There are also 687 public primary health care centers distributed across political wards. Collaborations exist between the government, private sector, and health partners in service delivery. The State Ministry of Health and its line agencies regulate and coordinate health activities in the State. Abia State has established its own Health Insurance Scheme, which is governed by the Abia State Health Insurance Agency (ABSHIA) to improve financial access to health for citizens. Enrollment began with the informal sector, where a mandatory amount of N15,600 ($40) per head per year and N56,800 ($146) per family per year.

Study Design

The study utilized a cross-sectional analytical design that involved both quantitative and qualitative data collection methods. This design was deemed the most suitable for the project since information was gathered from various groups of subjects at a single point in time. For the quantitative arm of the study, the data was collected using a semi-structured interviewer-administered questionnaire, while for the qualitative arm, an interview guide of key informant interviews and focus group discussion was used. The study was conducted for 6 months, from April to October, after receiving approval. The study included all insured and uninsured household heads or their representatives who had lived in the area for at least 1 year (Figure 1). However, household heads or representatives who were absent during the interview and households that declined to participate in the study were excluded.

Study Participants

The study participants were household heads or representatives aged 18 years or older in the urban and rural Local Government Areas of Abia State. A household is defined as a group of people who eat from the same pot while the household head is the person responsible for leadership and financial decisions within the household. For the qualitative arm, Key informant interviews were conducted with the Executive director of ABSHIA, the Chairman House Committee on Health, a Health care provider, a Representative of the third party administrator (TPA), a Representative of ABSHIA and a community stakeholder. Four (4) Focused group discussions (2 per study location amongst the insured and uninsured household members) were also conducted. The purpose of the qualitative method of data collection was to gain detailed insights from key stakeholders of the health insurance scheme on the established policies and implementation processes with challenges faced. In addition, information on barriers and facilitators elicited would be compared with the quantitative arm of the study whilst triangulating information from both qualitative methods.

Sample Size Determination and Sampling Technique

The sample size is determined using the formula for comparing 2 independent groups.

Where

Assuming a design/clustering effect of 2 the sample size =

Also accounting for a possibly maximum non-response rate of 10% from each study area,

Where q is the adjustment factor and F is the estimate of the non-response rate.

The total required sample size N for the study is 854, approximately 860 households that is, 430 per study site.

A multistage sampling technique for selecting the households in the urban and rural study areas.

Data Collection Procedures

Four research assistants who are at least graduates with experience in administering survey instruments; good communication skills and proficiency in English and Pidgin English languages were recruited. The training took place in ABSHIA, Umuahia, Abia State and consisted of a review of the survey instruments question by question with clarifications on gray areas. During the training, the research assistants rehearsed the use of the tools to improve their expertise in the administration of the instruments and good enough speed in its delivery. Training of the assistants was followed by a pre-test using Kobo toolbox software for data collection. The pre-test helped to further validate the survey instrument—addressing areas of ambiguities and errors as well as estimation of time requirement for administering the tools.

Focus group discussions for household members and in-depth interviews with key stakeholders using an interview guide were used to collect qualitative data in this study. A total of 4 FGDs was carried out in the health facilities in the study areas—2 per study area, categorized based on their insurance status among 8 to 10 consenting participants and selected purposively based on the inclusion criteria. The principal investigator moderated the sessions which took 45 min to an hour, assisted by an experienced note-taker who took notes on paper in addition to recording the discussion with a digital voice recorder after obtaining permission from the participants. An observer noted the non-verbal expressions of participants. The sessions were conducted on a round table for proper eye contact and engagement of all participants. The criteria for selecting the participant was the ability to communicate in Pidgin English and the local language Igbo. Mapping was done to purposively select key stakeholders for interviews. Using an interview guide, the discussion lasted for 45 min.

Data Analysis

Data was collected using the Kobo toolbox, which is an open-source mobile data collection platform. There was provision for multiple mobile data connectivity options to ensure all data collected are transmitted to the central server at the end of each day’s work to ensure they are quality assured in a timely fashion. The team supervisors provided on-the-spot monitoring and quality control of data during data collection, data cleaning and data assessment. This was emphasized during the training of the research assistants and their supervisors. Analysis of quantitative data was done using SPSS version 25.0. Categorical variables were summarized using frequencies to present the proportions of such variables as occupational status; marital status; educational status; ethnicity; and sex. Quantitative variables like age and income were summarized using means and standard deviations. Inferential statistics using the Chi-square test and binary logistic regression were used to examine associations between explanatory variables and the outcome variables. The level of significance was set at P < .05.

Qualitative Data

The research team conducted interviews and obtained data from the participants, which was then coded by 2 data coders separately. The team then compared and appraised the interpretations to ensure coherence. The initial coding involved identifying emerging themes and subthemes in addition to the pre-determined themes based on the study objectives. The thematic framework was applied to all transcripts by assigning codes to relevant phrases, sentences, and paragraphs from the interviews, which allowed patterns to be observed in the data as well as the context in which they were occurring. The segment of the coded data was combined, and final mapping and interpretation were done. The final results were triangulated to identify corroborating or contradicting information and comparisons made with the study’s quantitative arm.

Results

Description of the Study Population From the Quantitative Study

As shown in Table 1, the mean age of participants in urban Abia State was 43.16 + 11.17 years, which was significantly higher (P < .05) than the mean age of participants in rural areas, which was 40.61 + 13.07 years. The proportion of study participants in different age groups varied significantly between rural and urban areas of Abia State. Additionally, there was a significant difference (P < .05) in the proportion of study participants by sex, marital status, educational status, occupation, and estimated household income per month when both study locations were compared. Those in rural Abia (N62044 + 27154.26) had a significantly higher (P < .05) monthly income than those in urban Abia (N403396 + 32246.82).

Characteristics of Study Participants.

significant difference at p < 0.05

Enrollment Status of Participants Into ABSHIA in the Quantitative Study

Enrollment into ABSHIA was significantly higher in rural Abia (27.3%) than in urban Abia State (18.2%) (Figure 2).

Enrollment status of rural (A) and urban (B) study participants into ABSHIA.

Study Participants’ Satisfaction of the Benefit Package of ABSHIA in the Quantitative Study

Out of the respondents who enrolled on ABSHIA in rural (n = 122) and urban Abia (n = 82), 116 (95.1%) and 78 (95.1%) respectively were satisfied with the benefits package of the scheme. There was no significant difference (χ 2 = 0.001, P = .990) in the satisfaction level when rural and urban study participants were compared (Figure 3).

Satisfaction of ABSHIA benefit package of rural and urban study participants.

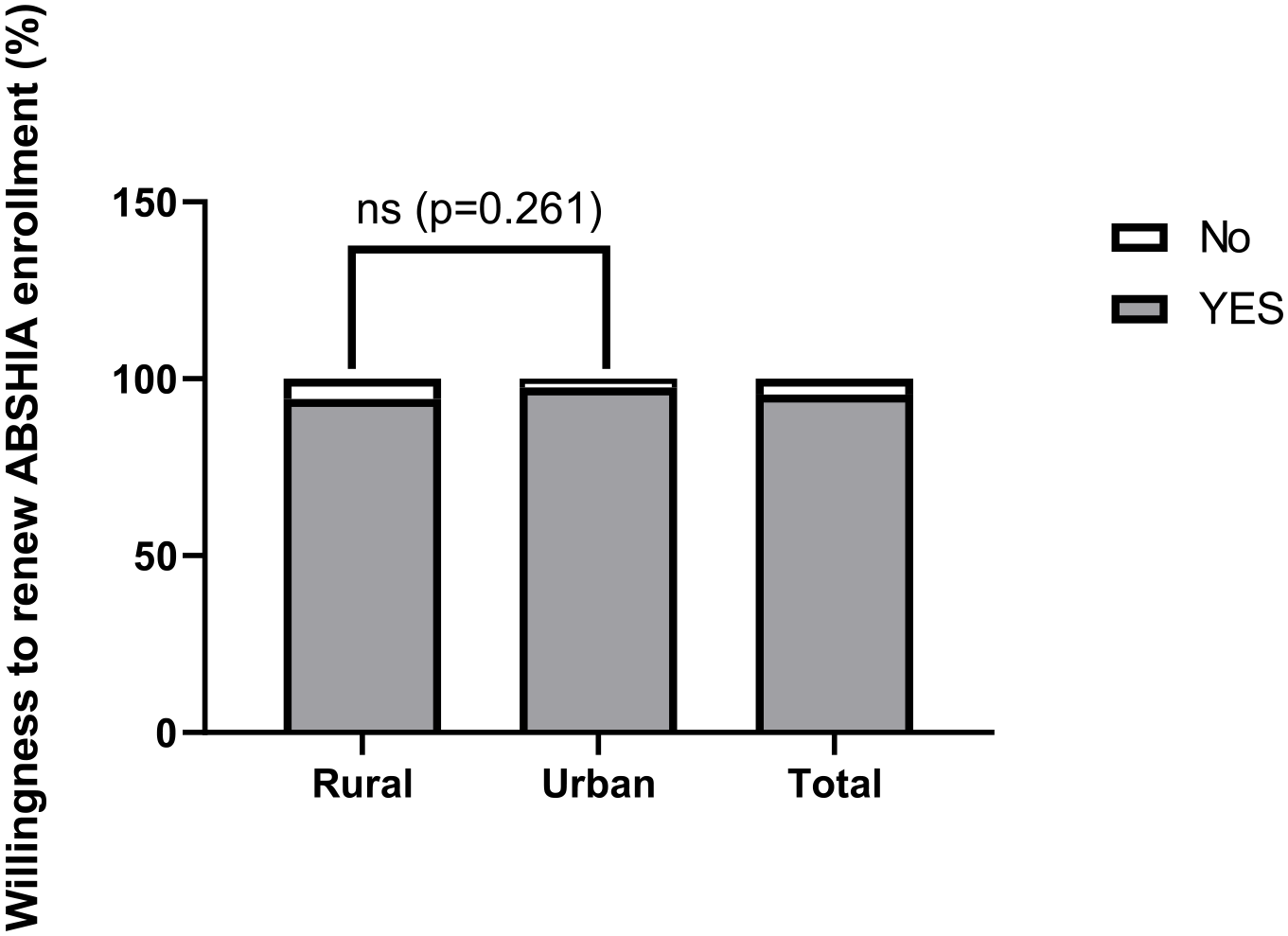

Willingness to Renew Enrolment Into ABSHIA in the Quantitative Study

Similarly, it was found that the majority of the respondents who enrolled in ABSHIA in both rural and urban Abia were willing to renew their membership. However, a small percentage of rural Abia respondents (5.7%, n = 7) and urban Abia respondents (2.4%, n = 2) were unwilling to renew their membership. When rural and urban study participants were compared, there was no significant difference (χ2 = 0.001, P = 0.261) in the willingness to renew ABSHIA enrollment (Figure 4).

Willingness to renew ABSHIA enrollment among study participants.

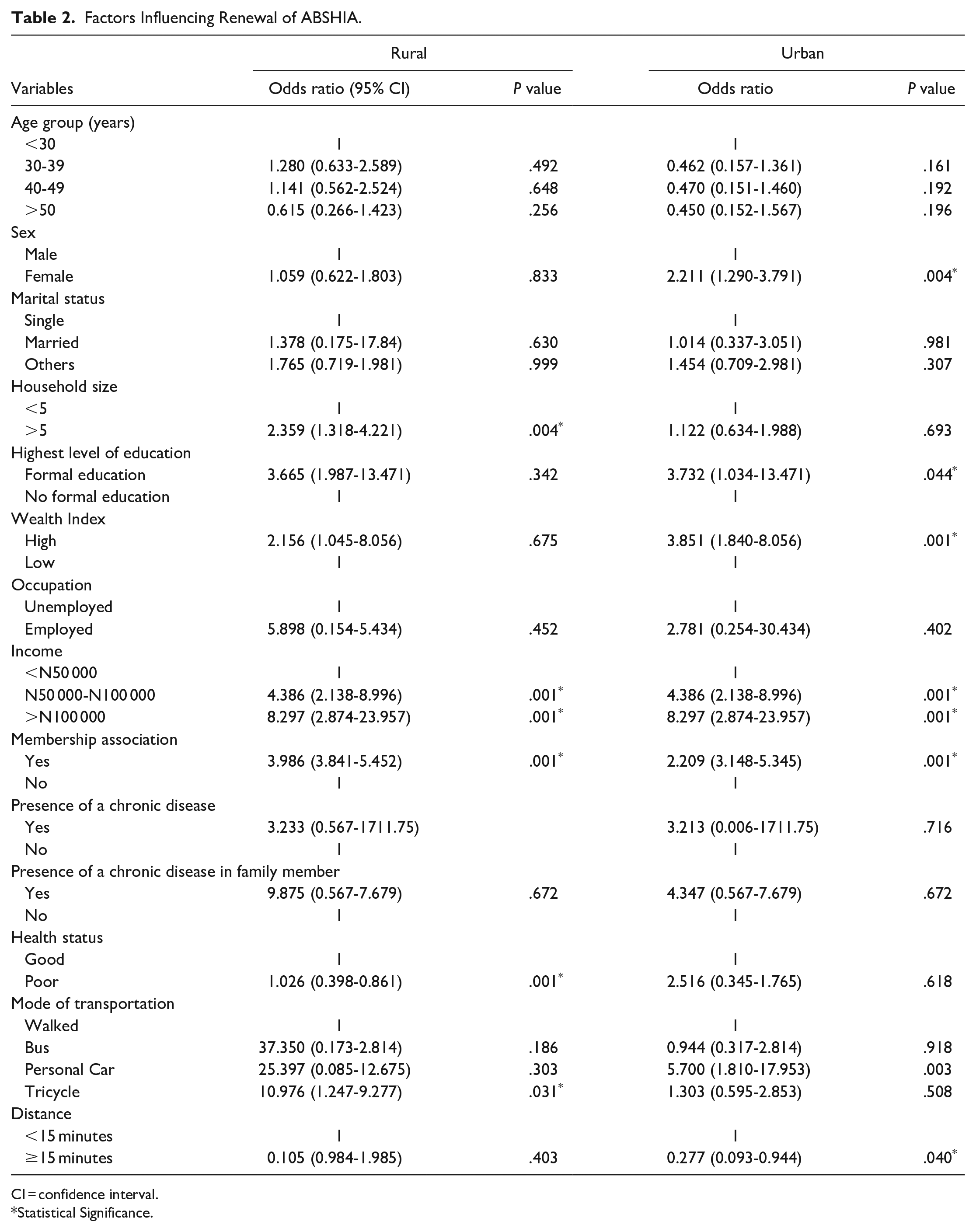

Factors in the Quantitative Study Influencing Willingness to Renew Membership of ABSHIA in Rural and Urban Abia State

The logistic regression conducted revealed that in urban Abia, females (OR: 2.211; 95% CI: 1.290-3.791), individuals with formal education (OR: 3.723; 95% CI: 1.034-13.471), high wealth index (OR: 3.851; 95% CI: 3851; 95%: 1.034-13.471), earning between N50 000 and N100 000 (OR: 4.386; 95% CI: 2.138-8.996) or more (OR: 8297; 95%: 2.874-23.957) and those who are members of an association (OR: 2.209; 95% CI: 3.148-5.345) are more likely to renew their membership of ABSHIA. However, those who have to travel more than 15 min (OR: 0.277; 95% CI: 0.093-0.944) to reach a health facility are less likely to renew their membership. On the other hand, in rural Abia, the study found that participants with a household size of more than 5 (OR: 2.359; 95% CI: 1.318-4.221), earning between N50 000 and N100 000 (OR: 4.386; 95% CI: 2.138-8.996) or more (OR: 8297; 95%: 2.874-23.957), members of an association (OR: 3.986; 95% CI: 3.841-5.452) and those who can access health facilities through tricycles (OR: 10.976; 95% CI: 1.247-9.277) are more likely to renew their membership of ABSHIA. Conversely, participants with poor health status (OR: 1.026; 95% CI: 0.398-0.861) are less likely to renew their membership.

Factors Influencing Renewal of ABSHIA.

CI = confidence interval.

Statistical Significance.

Factors Influencing the Sustainability of ABSHIA in the Qualitative Study

Membership Renewal

Many people who enrolled in the program did not want to renew their membership because they were not satisfied with the quality of services provided. One member stated that they wanted quality care at a low cost, but they were disappointed with the program’s poor services. Another person who was interviewed reported that some families had enrolled and were planning to mobilize members of their community if the program succeeded. One respondent was of the opinion that the cost of premium should be subsidized to aid renewal. Furthermore, another respondent noted that 34 members were sponsored by a reputable community member with the hope of increasing the number to 100 or more, but no renewals or increase in enrollment has occurred due to dissatisfaction.

“I did not enjoy ABSHIA and I am not willing to renew.”(FGD Urban Enrolee)

“A man enrolled 34 members in his community and hoping to increase it to 100 and more, but I haven’t seen the man renew the enrolment. . ..this is really sad.”(KII, ABSHIA rep)

Community Involvement

Many of the participants in the discussion emphasized the importance of involving the entire community in the scheme. They suggested that this would not only provide security, but also increase awareness and allow for feedback on the effectiveness of the scheme. Some participants recommended that the board members should include traditional chiefs, women leaders, police officers, youth leaders, healthcare workers, local government chairmen, pastors, teachers, market women representatives, and other trusted members of the community. Others suggested that payments should be made directly to the health facility in the community to prevent misuse of funds. Additionally, many respondents believed that the scheme should be mandatory for all members of the community, as it would greatly benefit them.

“The community management should work together, cooperate and secure what is here and support the scheme in whatever way they can.” (KII WDC)

“. . ..by giving feed-back report on how the place is run so that it will make the government to continue to help the community in return.” (KII WDC )

“Manpower, provide security and cleanliness to keep the environment clean.”(Rural FGD non-enrolees)

It should be for those already in power, but people who are trustworthy. You train them on it because I feel there may be some people who are experienced and know what to do but the opportunity is not given.”(FGD Rural non-enrolee)

“For it to work, it has to be compulsory.”(FGD Urban enrolee)

Government

Most of the respondents emphasized the importance of government support for the scheme, as their individual contributions may be small. Additionally, some respondents suggested that the government should provide health care centers with necessary resources such as drugs, equipment, and competent staff, and ensure prompt payment of salaries to prevent frequent strikes. Many respondents also believed that the government should effectively use mass media to raise awareness in both urban and rural areas, in order to increase participation. It was also suggested that a monitoring and evaluation system should be implemented to ensure the success of the scheme.

“Funds. The government need to fund the programme. If you say community alone, the community cannot do this because if you check, most of them are surviving on menial money they get everyday which is not even enough for their feeding.”(KII WDC)

Providing drugs and giving us more equipment. . .. . …if we come here and we see that there are changes, we will know that government is trying.”(KII, HCW)

“They should include more doctors and nurses to treat people. . …proper remuneration of health workers, so they can work well.”(FGD enrolee urban)

Lack of Engagement With Health Care Providers

Many of the enrollees were rejected by healthcare providers (HCPs) due to a lack of communication between ABSHIA and the HCPs. Some respondents noted that HCPs were not properly informed about pricing and benefits. The benefit package did not accurately reflect the current reality. For example, the cost of a Cesarean section was significantly lower than the standard price, which discouraged HCPs from providing services. This issue was compounded by delays in payment of capitation for primary healthcare services and reimbursement of fees for service by ABSHIA for the limited number of enrollees in the scheme. Enrollees were being denied services that they had paid for through their premiums.

“The few times CS was done, it took time for ABSHIA to reimburse me. This has made me turndown enrolees when I know ABSHIA won’t pay me. There’s so much delay in claims of payment. How do I run the clinic without money. . .. . .the claim process is cumbersome!” (KII HCP)

“I waited for 3 months before I received my capitation. This isn’t right!”(KII HCP)

Most of the HCP felt that the pricing of services was also very low. Comparison made with NHIS was not ideal because of the disparity in the number of enrolees, where ABSHIA had very few enrolees when compared to NHIS.

“The NHIS has more enrolees and can afford to set CS at N120,000 because the capitation for primary care can cover. ABSHIA has very few enrolees and cannot put the pricing on the same level. This has affected the scheme.”(KII HCP)

The whole claim process has been very cumbersome as expressed by some respondents. The electronic process set for this process has been unsuccessful leading to prolonged delays of claims and frustration in the delivery of quality services. One of the respondent reported that pre-authorization codes take a long time to be issued, especially when cases requiring urgent intervention present in the facility.

“When a patient comes with swelling and you want to do a procedure, it can take up to 2 days before you get a code to treat. Sometimes, you go ahead to treat hoping to get paid, but ABSHIA will go back and forth with you as to why you carried out a procedure before getting a code. You may not even be paid at the end of the day. This is so discouraging. They need learn from other HMOs how it is done electronically and seamlessly” (KII HCP)

Discussion

Summary of findings from the study reveal that, despite higher enrollment in ABSHIA in rural Abia, satisfaction with the benefit package and willingness to renew membership were similar in both rural and urban areas. Factors such as being a female, formal education, high wealth index, earning N50 000 and more, and membership in an association had a significant influence on willingness to renew membership in urban Abia. However, distance to a health facility had a low influence on willingness to renew membership in urban Abia. In rural Abia, household size of greater than and equal to 5, earning N50 000 and more, membership in an association, and access to transportation using tricycle to reach a health facility had a high influence on renewal of membership. Poor health status had a low influence on willingness to renew ABSHIA membership in rural Abia. Other factors that influence the sustainability of ABSHIA in the state include poor quality of service, lack of community involvement resulting in low awareness levels, unclean health facilities, and no feedback on the effectiveness of the scheme in the community. Additionally, the unsubsidized cost of the premium package due to lack of government intervention, poor supply of drugs and equipment in health facilities, low remuneration of healthcare workers, and rejection of enrollees by healthcare providers due to delays in claiming their capitation, leading to owed payments, and the high cost of certain benefits in the premium package, such as cesarean sections, and delay in obtaining preauthorization codes before receiving treatment also contribute to the challenges faced by ABSHIA.

The study found a significant difference in the proportion of individuals who participated in the quantitative research between rural and urban areas in Abia State. This suggests that the population of study participants who consented to participate in the different variables analyzed are not similar in both locations. For instance, more males were sampled in rural Abia while more females were sampled in urban Abia State.

The lack of significant difference in satisfaction and willingness to renew membership between rural and urban enrollees suggests that the benefit package of ABSHIA is the same in both locations, ensuring equity in healthcare in the State. This finding is similar to the reports on urban-rural differences in satisfaction with primary healthcare conducted in Ghana and that on rural-urban differences in health system performance among older Chinese adults, where no difference in satisfaction was observed between rural and urban dwellers.16,17 Contrary to our finding, another study conducted in Scotland reported higher satisfaction in rural locations compared to urban and suburban residents. 18

In urban Abia, being a female influenced the willingness to renew membership of ABSHIA in this study. This could be attributed to the fact that females use healthcare services frequently due to reproductive health issues and pregnancy. The cost of childbirth and cesarean sections is likely high in private hospitals, so females in urban areas would prefer to renew their membership in the scheme because these services are subsidized. This result is in agreement with a report on factors influencing the non-renewal of health insurance in the Ashanti region of Ghana, which showed that females are more likely to renew their membership. 19 However, the lack of a significant association between being a female and willingness to renew membership in rural Abia contradicts the generalization that women in rural areas are more likely to renew their subscription to health insurance than their urban counterparts, as reported. 20

Furthermore, in urban Abia, having a formal education significantly influenced the willingness to renew membership. This influence was particularly felt in urban Abia due to the lower population with higher education compared to rural Abia. This suggests that individuals with higher educational attainment are more likely to make timely decisions and renew their subscriptions due to their better understanding of the benefit package and operating principles of ABSHIA, in contrast to those without formal education. This finding is consistent with those of other authors who have reported that higher educational attainment has a significant impact on the renewal of membership in health insurance schemes.19,21,22

The high wealth index in urban Abia appears to have a significant influence on the willingness of individuals to renew their membership. This could be attributed to the fact that a higher wealth index makes the cost of the scheme package more affordable. Additionally, a higher wealth index provides a level of financial protection, allowing study participants in this location to allocate funds for their health. This finding is consistent with a study conducted in Nepal, which found that household wealth status was a significant predictor of health insurance enrollment and renewal. 23 However, a study in the Oromia Region of Ethiopia reported that individuals with lower or middle levels of wealth were more likely to renew their membership. 21

The distance of 15 min or more required to travel to renew membership of ABSHIA in urban Abia had a low influence on willingness to renew. This could be attributed to the fact that instead of spending on transportation, residents with a high wealth index in urban Abia would rather make out-of-pocket payments at private hospitals, chemists, and non-accredited health facilities close to them. A systematic review of barriers to renewing health insurance membership has shown that the time spent traveling to a health facility is a major obstacle. 22 On the contrary, a study on reasons for dropouts from a community-based health insurance scheme in Ethiopia revealed that those who travel a long distance to a health facility appreciate the quality of healthcare and are less likely to drop out of the scheme. 24

In rural Abia, one of the main factors that influences membership renewal is having a household size of 5 or more people. The sociodemographic profile of rural Abia reveals that the majority of residents are government workers who rely on a monthly income and may have to spend more out-of-pocket. As a result, they are more likely to renew their ABSHIA subscription. This finding is consistent with a study conducted in Ethiopia, which found that households with less than 5 people were less likely to renew their health insurance subscriptions. 21 However, another study showed that people with large household sizes may struggle to renew their membership due to varying premium costs based on family size, leading some to drop out of the scheme. 22

Furthermore, the use of a tricycle as a means of transportation to reach a health facility greatly influenced the willingness to renew membership in rural Abia. Tricycles are a cost-effective and efficient mode of transportation in rural areas. 25 This is especially important in rural Abia, where many government workers rely on their salaries and a cheap means of transportation is a determining factor in their decision to renew their membership.

In rural Abia, poor health status has a negative impact on the likelihood of renewing membership. This could be due to the low quality of service received during previous visits and hospitalizations at ABSHIA accredited health facilities. This finding is consistent with a study on a community-based insurance scheme, which found that individuals who had been hospitalized due to poor health were less likely to renew their membership. 26 Another possible explanation for this trend could be the unsubsidized premium package of the scheme. Many respondents have expressed dissatisfaction with the lack of government intervention. Additionally, the long wait times for preauthorization codes at accredited health centers may also contribute to the lower renewal rates among those with poor health status. These individuals may not have the physical endurance to wait for extended periods of time for treatment.

High income and membership in an association were found to have a significant impact on the willingness to renew membership in both rural and urban areas of Abia. This is likely due to the fact that a higher income allows for greater affordability of the renewal package for the scheme. This finding is consistent with a previous study conducted in Ethiopia, which also found that individuals with higher incomes were more likely to renew their health insurance. 19 Additionally, the influence of membership can be attributed to the role of socialization in disseminating information.

During the Key Informant Interviews (KII) with healthcare providers and ward development chairpersons, several barriers were identified. These barriers include poor quality of service, unavailability of prescribed drugs, long waiting periods for insurance claims to be processed, unclean health facility environments, nonpayment of health workers’ capitation, and negative attitudes of health workers toward scheme enrollees. These barriers have been reported in published studies as reasons for non-renewal of health insurance scheme membership.10,19,21,22,27

Conclusion

This study has found that the design of ABSHIA promotes equity in the delivery of healthcare services in the State. However, to sustain the success of the scheme, several challenges must be addressed, including low awareness of the scheme, poor quality of healthcare delivery, inadequate social infrastructure, and weak administrative and systemic processes such as capitation payment. Therefore, an in-depth qualitative study is recommended to adequately understand and address the sustainability challenges of ABSHIA.

Limitations of the Study

The study was conducted shortly before a change in governance making it difficult to reach out to most key stakeholders. However, those who were interviewed gave sufficient and useful information regarding ABSHIA. Another limitation is the use of representatives of household heads aged 18 years or older. This is because some households were unwilling to participate in the study but sent their oldest child. Representatives in the age group are not knowledgeable about the day-to-day proceedings of the agency as the principal household heads. Further, these representatives are just members of the scheme as a result, data collected from them might not be a true reflection of the head of the household who holds the insurance scheme’s principal membership. Especially when measuring perception/attitude variables like satisfaction, and willingness to renew membership.

Footnotes

Acknowledgements

We are grateful for the work and support of ABSHIA team, the research assistants and the TPAs for the technical assistance and support. We would like to thank the stakeholders in the communities, the Primary Health Care personnel and members of the community for their cooperation.

Author Contribution Statements

Dr. Ukweh Ikechukwu: developed the proposal and data collection tool and read the manuscript

Dr. Ukweh Ofonime: Provided funding for the research

Dr. Iya-Benson-Conducted analysis using SPPSS

Dr. Ewelike is the executive secretary of Imo State insurance that provided man power that did data collection.

Dr. Oku O. Afiong supervised the study

Iziga-Eruchalu C. wrote and edited the manuscript

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

Ethical approval for the study was obtained from the Cross River State Health Research Ethics Committee, with ethical approval number CRSMOH/HRP/REC/2023/474.