Abstract

Using data from the 2013 American Community Survey, we found that 24.3 million people (about 1 in 4) who were either eligible for Medicaid/Children’s Health Inusrance Program (CHIP) or appeared likely to shop for Qualified Health Plan (QHP) lacked residential high-speed Internet. Specifically, 28.6% or 18.9 million people eligible for Medicaid/CHIP and 17.1% or 5.5 million people who appeared likely to shop for a QHP did not have high-speed Internet in the home. For both the Medicaid/CHIP eligible and those likely to shop for a QHP, the proportion of people living in households without Internet varied substantially by race, geography, and other socio-demographic characteristics.

Keywords

Introduction

A key feature of the Affordable Care Act (ACA) is the establishment of online Marketplaces that make it easier to apply for and enroll in health insurance. The online Marketplaces facilitate eligibility determination for Medicaid/Children’s Health Insurance Program (CHIP) and for tax credits that subsidize private insurance. They also provide a central location to compare and shop for Qualified Health Plans (QHPs). During the 2015 open enrollment period, the Marketplaces had 35.2 million Web visitors compared with 16.8 million telephone contacts. 1

The online Marketplaces appear to have been successful at attracting visitors, but people without Internet in the home face additional application burdens that could dissuade application and enrollment. The “digital divide” has narrowed in recent years, but there are still gaps in residential Internet that could cause barriers to health plan enrollment under the ACA.2,3 Only one previous study, to our knowledge, has examined Internet availability among populations targeted by the online Marketplaces. 4 That study, a 2013 survey sponsored by the Kaiser Family Foundation (KFF), found that 19% of uninsured adults below 139% of poverty and 14% of uninsured adults between 139% and 400% of poverty could not easily access the Internet from home or another location, compared with 98% of those with income above 400% of the Federal Poverty Level (FPL).

The KFF study suggested that a substantial share of adults who could likely benefit from an online Marketplace lacked easy access to the Internet. However, the study had limitations. The survey excluded children even though children are an important population served by the online Marketplaces. Children could have different levels of Internet availability given that they tend to live in poorer households compared with childless adults. 5 Compared with large federal surveys, the KFF study had a moderately sized sample (n = 8762). Furthermore, 50% of their sample was concentrated in California, Missouri, and Texas. The authors were unable to examine how Internet access varied across different demographic groups. Identifying groups that are at more or less risk of lacking Internet is important for tailoring ACA outreach to specific consumer groups.

This article expands on the KFF study using new data from recently added questions on the American Community Survey (ACS). Using these data, we estimate the number (and percentage) of people who lack residential high-speed Internet, within populations that otherwise appear likely to benefit from an online Marketplace. For those who do report residential Internet, we estimate the share that relies exclusively on a mobile connection. Not only do those who rely solely on mobile connections tend to have less stable access to the Internet due to data limits and service interruptions, 6 but applying for and choosing a plan from a mobile devise (when a Marketplace is mobile compatible) might pose unique challenges as well. For example, whereas 35% of all HealthCare.gov visits were from a mobile device, only 15% of consumers who signed up for coverage during the second enrollment period did so through a mobile device. 7 This suggests that consumers may find mobile enrollment difficult. Finally, we leverage the large sample size of the ACS (n = 3 132 795 million individuals) to examine how Internet availability varies across subgroups, before and after adjusting for covariates. Our results inform ongoing outreach activities and speak to how recent proposals to subsidize Internet access could have important implications for health policy initiatives.

Methods

Data come from the 2013 ACS—a household survey conducted annually by the US Census Bureau. In 2013, the Census Bureau added new questions that assessed the presence and type of residential Internet service (eg, dial-up, cable, mobile). 2 We used these new data to identify people who did not have high-speed Internet in the home. We focused on high-speed Internet because the constraints imposed by dial-up service are often prohibitive.

We identified two distinct groups of non-elderly individuals (aged 0-64) deemed most likely to benefit from the online Marketplaces: those enrolled or otherwise eligible for Medicaid and those who appeared likely to shop for a QHP. Both groups were defined using information on health insurance coverage held on the day of interview and annual family income. Family income was obtained by summing personal income within health insurance units—a collection of related individuals who could be covered under the same private health insurance plan (ie, a nuclear family).

The first group was composed of non-elderly people who were either currently enrolled in Medicaid/CHIP or appeared eligible because they were uninsured and had family incomes below 2014 state specific Medicaid/CHIP income thresholds. 8 The income thresholds varied by state and by categorical eligibility type. The eligibility types included children, pregnant women (identified in the ACS as women that gave birth in the last year), parents, and childless adults.

The second group we considered included people who appeared likely to shop for a QHP (called “potential Marketplace participants” in the tables below). We defined this group as people who had incomes above state-specific Medicaid/CHIP income thresholds or 100% of poverty, whichever was higher, and were either uninsured or insured through the individual market. We excluded the population below 100% of FPL (people not eligible for Medicaid because they lived in a state that had not expanded Medicaid) because QHPs are likely unaffordable for this group and they are not eligible for financial assistance. Finally, we also considered a higher socioeconomic status group—people who had employer-sponsored insurance and family incomes above 400% of poverty. This group was used as a reference group.

In each of these groups, we estimated the number and percentage of people who lived in a household without high-speed Internet, overall and for selected socio-demographic groups. Our choice of groups was informed by previous research examining the digital divide. 1,2 Specifically, racial minorities, the less educated, those living in rural areas, and other traditionally vulnerable groups tend to be less likely to have Internet in the home compared with their counterparts. One of the most important predictors we examine is family income relative to the federal poverty guidelines (FPG). Each group has different income distributions by definition so we use different poverty levels depending on the group. For the Medicaid/CHIP group, we use 0% to 49%, 50% to 99%, 100% to 138%, and 139%+ FPG. For the potential Marketplace participants, we use 100% to 199%, 200% to 299%, 300% to 399%, and 400%+ FPG. For simplicity, we label the categories low, moderate-low, moderate-high, and high for each group.

We report both unadjusted and adjusted rates (ie, predicted probabilities scaled to the percent scale) that were obtained from logistic regression. Standard errors and statistical tests were adjusted for the complex sample design of the ACS. 9 We defined statistical significance using a critical value of 0.05. Like all survey data, ACS estimates are subject to non-sampling error. However, the new Internet estimates track closely with other sources, including widely used data from the Pew Internet Project. 10

Results

Overall we found that among all those who could potentially benefit from access to an online Marketplace (“potential Marketplace users”), 24.3 million or 24.8% lacked residential Internet (Figure 1). More than 1 in 4 non-elderly people (18.8 million) who were either currently enrolled or otherwise appeared eligible for Medicaid/CHIP lacked high-speed Internet in the home. An additional 5.5 million potential Marketplace participants lacked residential Internet (17.1%). Comparatively, having high-speed residential Internet was nearly universal for high–socioeconomic status individuals with employer-sponsored health insurance.

Percentage of non-elderly individuals who live in a household without high-speed Internet, by health insurance eligibility group.

We found that roughly 10% of Internet users who were Medicaid eligible and 8% of Internet users who were likely to participate in a Marketplace depended solely on a mobile connection (data not shown). Comparatively, only 4.7% of Internet users in the high–socioeconomic status group were mobile users only.

By definition, the Medicaid/CHIP eligible and potential Marketplace participants differ according to income. In Table 1, we explore other population characteristics for each sample. Nearly half of the individuals currently enrolled or potentially eligible for Medicaid/CHIP are children, and over half are also living in households where the householder is working part-time or not working at all. Meanwhile, potential Marketplace participants were more likely to be older individuals (35-64 years of age), and they were more likely to live in households with only adult residents and to live in a household where the householder had at least some college education and was working full-time.

Population Characteristics by the Health Insurance Eligibility Group.

Source. 2013 American Community Survey.

Note. Eligibility groups are defined in the text. Overall, we estimated 32.2 million potential Marketplace participants and 69.9 million enrolled or potentially eligible for Medicaid/CHIP. See the text for poverty levels and their definitions. SE represents standard errors that account for the sample design. AIAN = American Indian/Alaska Native; NHOPI = Native Hawaiian/Other Pacific Islander.

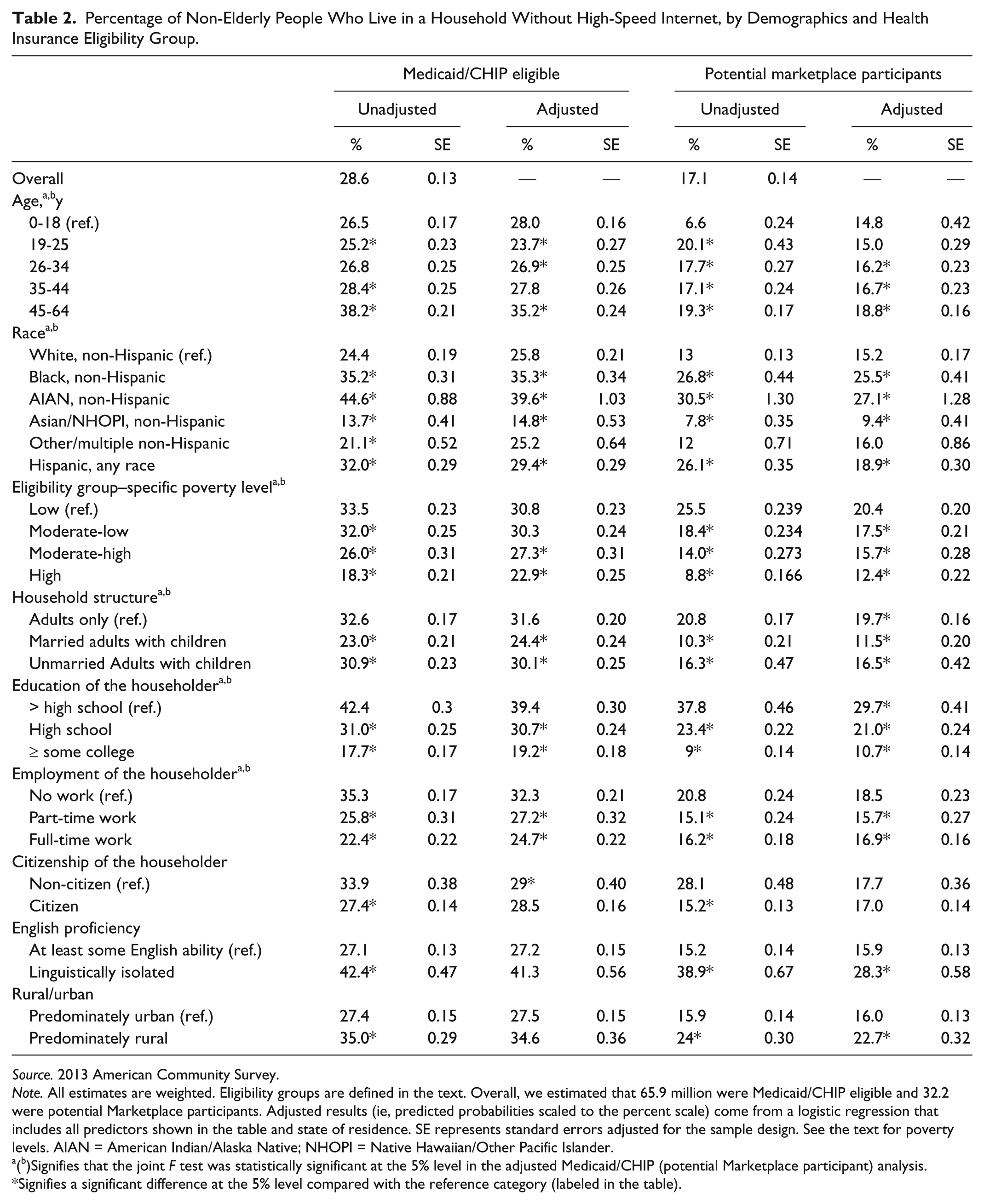

In Table 2, we show what socio-demographic groups were more and less likely to lack high-speed residential Internet. We present unadjusted and adjusted rates (ie, predicted probabilities scaled to the percent scale) that were obtained from logistic regressions that controlled for the predictors shown in Tables 1 and 2, in addition to a full set of state of residence dummies. Controlling for both rural/urban and state of residence helps to account for the fact that the supply of Internet connections varies across geography. We omit the coefficients on sate of residence to simplify presentation and because the independent contribution of each state to the predicted rate is not our main focus.

Percentage of Non-Elderly People Who Live in a Household Without High-Speed Internet, by Demographics and Health Insurance Eligibility Group.

Source. 2013 American Community Survey.

Note. All estimates are weighted. Eligibility groups are defined in the text. Overall, we estimated that 65.9 million were Medicaid/CHIP eligible and 32.2 were potential Marketplace participants. Adjusted results (ie, predicted probabilities scaled to the percent scale) come from a logistic regression that includes all predictors shown in the table and state of residence. SE represents standard errors adjusted for the sample design. See the text for poverty levels. AIAN = American Indian/Alaska Native; NHOPI = Native Hawaiian/Other Pacific Islander.

(b)Signifies that the joint F test was statistically significant at the 5% level in the adjusted Medicaid/CHIP (potential Marketplace participant) analysis.

Signifies a significant difference at the 5% level compared with the reference category (labeled in the table).

As shown in the first set of columns in Table 2, older individuals (aged 45-64) who were eligible or enrolled in Medicaid/CHIP were more likely to lack residential Internet compared with younger individuals, but the relationship between age and the presence of residential Internet was not linear. For example, there was not much variation by age for those under 45, but then there was a substantial increase for the 45- to 64-year-olds and this relationship remained after adjustment.

Non-Hispanic American Indian/Alaska Natives (AIANs) were 1.8 times more likely to lack residential Internet compared with non-Hispanic whites (44.6% vs 24.4%; P ≤ .05). Non-Hispanic Asians, however, were significantly less likely to lack residential Internet, compared with Non-Hispanic whites. After adjusting for covariates, there remained substantial racial disparities in residential Internet in the Medicaid/CHIP population, particularly for Non-Hispanic blacks, non-Hispanic AIANs and Hispanics. The presence of high-speed Internet in the home also varied substantially and significantly by household structure, education, employment, language ability, and rural status. Differences by citizenship did not persist after adjustment. Even in this relatively low-income group, family income was predictive of home Internet. The lowest income group (below 50% of FPL)was 8 percentage points more likely to lack residential internet compared to the highest income group (above 138% of poverty).

The second set of columns in Table 2 considers the population that appeared likely to shop for a QHP. Although the overall share that lacked residential Internet was lower for the QHP population compared with the Medicaid eligible population, both groups had similar demographic patterns. For example, Non-Hispanic blacks, AIANs, and Hispanics were significantly more likely to lack Internet compared with Non-Hispanic whites. Just over 10% of those with at least some college experience lacked residential Internet compared with 29.9% of those with less than a high school education (P ≤ .05). There were also statistically significant differences by household structure, education, employment, language ability, and rural status.

As in the Medicaid/CHIP eligible group, family income was an important predictor. After adjusting for covariates, just over 20% of potential Marketplace participants with relatively low incomes (100%-200% of poverty) lacked residential high-speed Internet compared with 12.4% of potential participants with incomes over 400% of FPL.

Discussion

We found that 24.3 million people who could benefit from an online Marketplace lacked access to high-speed Internet in the home. This included 28.6% of those currently enrolled or eligible for Medicaid/CHIP and 17.1% of potential Marketplace participants. Within the health insurance eligibility groups targeted by the online Marketplaces, we found variability in who had high-speed Internet in the home. African Americans, Hispanics, American Indian/Alaska Natives, those with poor English ability, and those living in rural areas were at particularly high risk of lacking residential Internet. These differences remained even after controlling for income and for potential differences in supply across geography (as captured by our rural/urban and state of residence variables). Our study had limitations. Our data were based on self-reports, and though the ACS has been shown to produce health insurance and income estimates that are of equal quality as other surveys,11,12 the quality of the new Internet questions has not been as rigorously evaluated. We also did not have individual data on health insurance enrollment facilitated by the Marketplaces so were unable to directly test the hypothesis that having residential Internet increases the probability of signing up for coverage. That remains an important area for future research. As future years of the ACS become available, it may be possible to examine if the ACA increased insurance coverage in Internet-connected households to a different degree than non-connected households. However, such work will need to overcome the fact that a household’s Internet status could be correlated with unobserved factors that also help determine insurance coverage. Simply comparing connected and non-connected households may not represent the causal impact of the Internet.

Millions of people have gained coverage since the opening of the online Marketplaces in January of 2014, but millions of others have yet to sign up.13-15 Those interested in obtaining coverage may utilize other application channels (eg, phone) or may seek out the Internet away from home. However, enrolling the remaining eligible will partially depend on minimizing the non-financial costs of application. Residential Internet might be the easiest option for many consumers. Stigma associated with calling or visiting a “social-service” office, travel time, and inconvenient office hours are 3 barriers that residential access to online Marketplaces could help to alleviate. Our results suggest that a suite of new initiatives to subsidize Internet for rural populations, public housing residents, and other low-income populations may play an important role in the ACA. 1 However, ensuring universal access to high-speed residential Internet should not be viewed as a panacea. The groups that we identified as being the most at risk of lacking high-speed Internet (ie, older, low-income, less educated, linguistically isolated, and racial/ethnic populations) are likely to experience multiple barriers to enrollment, including financial and time cost, misinformation, and distrust. Navigators and application assisters will continue to play important roles in both informing consumers about the benefits of coverage and educating them about appropriate health plans given family circumstances.

Finally, though our interest centered on health insurance enrollment under the ACA, the Internet clearly plays a much broader role in population health. The Web is quickly becoming an irreplaceable health resource that is essential for managing personal health records, learning about disease symptoms, and comparing provider quality.16,17 Our results highlight the idea that efforts to achieve health equity should include minimizing disparities in residential Internet access.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported, in part, by a grant from the Robert Wood Johnson Foundation to the State Health Access Data Assistance Center.