Abstract

‘Vertical urbanisation’, a new form of housing densification, has accelerated in the 21st century and now dominates the skylines of many global cities. Tall residential buildings are more complex than lower-rise multi-occupied buildings due to their sophisticated infrastructures and technologies, co-dependent spatial relationships, mixed uses and density of occupation. They are also more legally complex, especially when individual units are sold using legal forms such as condominium, strata title or leasehold (multi-owned properties) rather than remaining in single ownership with apartments being rented out. This means that property rights in residential towers are distributed among multiple parties, forming an intricate web of legal relationships of different and often conflicting interests. This article demonstrates that an understanding of the various ways in which law operates at all stages of high-rise development and management can make an important contribution to urban theory. However, there has been little theoretical or empirical research into the roles of law(s) in shaping these physical and social spaces. Using primarily English developments for illustration, we show how different laws (in this case, the laws of England and Wales) interact with housing financialisation at various scales, from the global to the home, to shape the production, materialisation, safety and maintenance of residential towers and their surrounding neighbourhoods, as well as the lived experiences of residents and their neighbours. Our grounded analytical approach provides a framework for future empirical research investigating residential towers, in England and elsewhere, that will contribute new understandings to urban development and theory.

Introduction

‘Vertical urbanisation’, which increasingly includes residential accommodation, dominates the skylines of many global cities (Harris, 2015). During the 21st century this rapid acceleration of high-rise towers has been ‘fuelled by … population growth and stimulated by market-friendly policies that promote urban densification’ (White and Punter, 2023: 5), and ‘bolstered by new building technologies and massive injections of overseas capital’ (Atkinson, 2019: 2). These high-rise buildings, frequently built by private developers and marketed as prestigious apartments for wealthy owners, transform their surrounding neighbourhoods (for better or worse) and are often seen as markers of a city’s prosperity (Filiz, 2023).

Urban scholars have researched this phenomenon through different disciplinary perspectives, variously concerned with geographical theory (Graham, 2018), urban form (White and Punter, 2023), the insertion of another layer of local government (Harris and Patterson, 2024), liveability and residents’ experiences (Gifford, 2007), the crisis of verticality and its failure (Laing Ebbensgaard et al., 2024) or particular geographies (see, e.g. Nethercote, 2019 regarding Melbourne; White and Punter, 2023 regarding Toronto) and sub-markets, with special interest in the ‘prime’ and ‘super-prime’ global trends which attract investment from transnational elites. This article responds to the recent call for further ‘interdisciplinary interrogation and rethinking’ on urban verticality (Laing Ebbensgaard et al., 2024: 629) by illustrating how law, intertwined with financialisation, operates at different scales and in various ways to produce and shape the life of residential towers. An examination of the ‘violent effects of power verticals’ highlights the power asymmetries associated with vertical urbanisation (Laing Ebbensgaard et al., 2024: 619); this article does not aim to set out or explain the law in detail but rather highlights how power is exercised through law intertwined with financialisation.

We take a broad conception of law as a social construct that includes its role within, while also shaping, society (see Blandy et al., 2006; Lippert and Steckle, 2016). It encompasses both the formal and informal ways in which property and property relationships ‘are located in time and space and in lived experiences’ (Blandy et al., 2018: 113). Different forms of law interact rather than existing in isolation. The concept of interlegality, meaning ‘different legal spaces superimposed, interpenetrated’ in a dynamic process (de Sousa Santos, 1987: 297), illustrates how separate forms of law all affect the life of one high-rise building or development. Law operates at different scales, from the global to the home, and has different dimensions. Formal laws operate alongside the informal laws of wider networks of social and commercial norms and organisational practices. Law affects the material form of high-rise buildings and their surroundings, as well as governing relationships between owners, residents, neighbourhoods and cities. Without recognition of law’s role(s) and operation, policy makers struggle to respond to urgent contemporary challenges such as building safety, sustainable cities and achieving net zero.

The consequences of inadequate laws and regulatory systems can be seen in recent catastrophic events involving tall towers across the world: the emergency evacuation of Opal Tower in Sydney after cracks developed in a load-bearing concrete panel, the collapse of Champlain Towers in Miami and the fire that engulfed Grenfell Tower in London. Seeking explanations for these events, our approach provides a frame for analysing the roles of law(s) and of financialisation in shaping high-rise residential buildings, both materially and socially.

This article builds on a body of socio-legal scholarship exploring multi-owned residential property. An emerging interest is the relationship between multi-owned sites, urban democracy and service delivery; Pieterse (2024), for example, suggests that in the South African context multi-owned sites should be reconceived to more specifically acknowledge and support their public functions. Attention has also been drawn to how shared residential sites operate as a form of private government (see, e.g. Lippert and Treffers, 2021). A focus on the ‘inner ordering of condo inhabitants and spaces’ (Lippert and Steckle, 2016: 133) allows analysis of key institutional processes associated with the life cycles of residential towers. This includes revealing the power and activities of the professional agents associated with them, referred to by Lippert and Steckle as juridification (law firms), financialisation (real estate agents) and commodification (property management companies). Lippert and Steckle (2016: 146) argue that acknowledging the roles of these processes and agents provides the potential for a bridge between the ‘penchant in urban geography for focussing on development and the preference in socio-legal studies for centring on “inner” private urban governance’.

We agree that it is important to recognise the key role of institutional processes and actors, and these are accommodated in our analytical frame. Additionally, we look holistically at the multilayered role(s) of law(s) in high-rise residential housing, extending beyond private urban governance to the life cycle of high-rise residential buildings, from the planning and design stages through construction to first occupation and the inner ordering thereafter.

Height adds complexity to the material, legal and social issues. High-rise buildings differ from other multi-owned properties in terms of their financing, scale, design, built form, legal complexity and spatial use. Garfunkel’s comparative study of high-rise condominiums in four cities (Tel Aviv, Paris, Sydney and Tarragona) identifies particular governance challenges stemming from the complexity of tall buildings: they require enhanced maintenance expertise and increased resources to deal with their more sophisticated infrastructure and technologies, usually requiring a specialist property manager to be engaged; there is often ongoing involvement from developers and other actors such as property managers and real estate agents; service charges are significantly higher; and there are frequently diminished social relationships and internal tensions between residents, as well as problematic interactions with surrounding urban society (Garfunkel, 2017). Height also magnifies the challenges arising from living ‘cheek by jowl’ as the individual units are spatially embedded in ‘a previously unimaginable density and proximity’ (Harris, 2021: 33).

Law is crucial to understanding how residential towers are planned and built, and how life is experienced by residents and neighbours. Our analytical framework recognises the different forms of law – planning, property, contractual and regulatory laws, plus other informal laws and practices – that collectively influence the height, shape, design, maintenance and governance of towers. As law is always contextual and geographically specific (Imrie and Thomas, 1997) there are wide differences in national and local laws between and within jurisdictions. Our approach therefore requires that particular attention is given to place (physical location). In this article, the place we focus on is England and the relevant law is that of England and Wales, but the analytical framework can be applied more generally.

In England, apartments in residential towers are sold on a long leasehold basis (time-limited ownership for e.g. 99 or 999 years). As the Law Commission (2020) notes, ‘the landlord and leaseholder have opposing financial interests – generally speaking, any financial gain for the landlord will be at the expense of the leaseholder, and vice versa’ (para 1.33). A freeholder, either an individual or more likely a corporate legal entity, owns title to the building and the development as a whole, including the shared parts of the building. The leaseholders own title to their apartment with rights of access to the common parts. The leasehold system of England and Wales contrasts with the condominium framework used in many other jurisdictions (Easthope, 2019: 21ff). We use the term ‘condominium’ here as an umbrella term to refer to those legal systems that provide for individual unit ownership within a building that is co-owned and governed collectively by the unit holders. It includes condominium itself (differently configured in, e.g. the United States of America, Canada, Israel, Italy); copropriété (France); sectional title (South Africa) and strata title (Australia).

Scales, financialisation and law

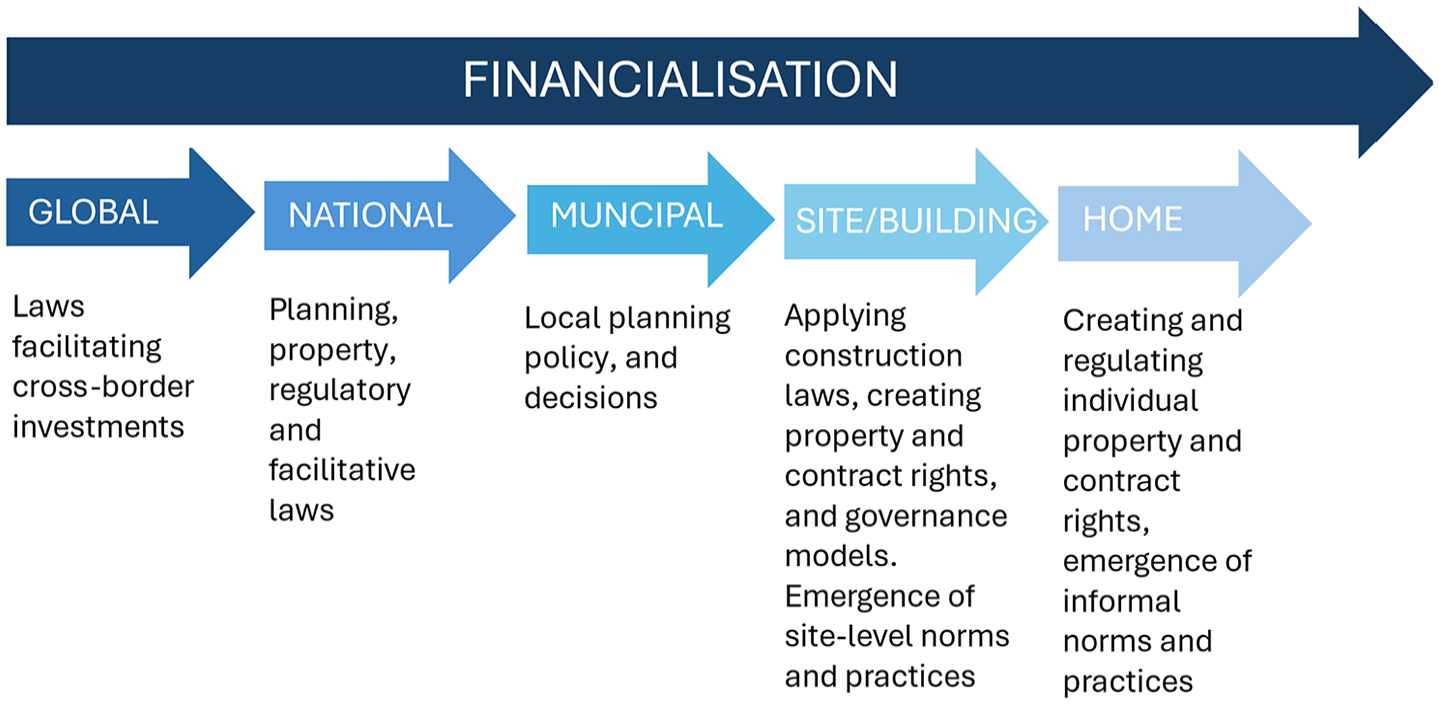

Figure 1 represents our analytical framework as a diagram, showing the five scales at which the interactions of financialisation, formal and informal laws must be understood. The financialisation of housing has been summarised as the ‘increasing dominance of financial actors, markets, practices, measurements and narratives at various scales’ (Aalbers, 2016: 2). Although there is insufficient space here to discuss the extensive literature on housing financialisation, this article explores how law is deeply intertwined with financialisation at different scales. Figure 1 provides a visual overview of this complex relationship. Financialisation is a key socio-economic driver of the increase in residential towers, and reaches into each of the scales shown in Figure 1. As will be seen, law and financialisation are not separate processes; financialisation shapes the law, which in turn facilitates financialisation (see e.g. Harris, 2011).

The analytical framework of scale, law and financialisation – examples.

Taylor’s (1982) foundational work on scale helps to illustrate how financialisation and law intertwined co-produce high-rise residential buildings, from early financing, design, planning and building, to their ongoing presence as urban spaces, investment outlets and homes. Although scale is not a clear, neat concept, the idea of different interlocking scales teases out the complex ways in which economic processes, laws and practices coalesce to create and sustain each specific residential tower, as well as its effects on the wider neighbourhood and city (Valverde, 2009: 143).

Taylor’s goal was to provide a materialist framework to organise political geography. For this purpose he identified three scales (global, national and urban/local). Our framework, designed to illustrate the multiple levels at which financialisation and laws impact on residential high-rise buildings, identifies five scales. Our starting point is the global, recognising, as Taylor did, the significant role that global capital plays. At this level, financialisation is the dominant player and law operates through international standards and codes that regulate and facilitate cross-border investments. The national level captures overarching nation-state laws, such as planning, property and regulatory laws as well as the facilitative laws (see Blandy and Wang, 2013) that work together with private law-making at the site and home levels through the ‘technologies of law’ and ‘organisational practices’ (Bright and Weatherall, 2017: 205). This multilayering of laws affecting residential towers requires that Taylor’s urban/local level is further differentiated to include: the municipal (the scale at which local government decisions are made); the site/building (the scale of construction, property rights creation, and governance); and, following Marston (2000), the individual home or household (the scale of everyday lives).

Following a brief note on methodology, the article reviews what is known about tall residential buildings in England. It then examines how financialisation and law(s) intertwine at various scales, contributing to the production and materialisation of the initial form and later life of tall residential buildings and their immediate surroundings. The final section emphasises how the absence of empirical data about the ownership and governance of tall buildings in England hinders the development of effective policies to promote thriving individuals and communities. This absence is particularly acute at the scales of site/building and home where there is no data in relation to legal, governance and management arrangements used and how the arrangements impact on, for example, maintenance, costs and quality of life. Our socio-legal framework provides the basis for new research agendas.

A note on methodology

This article is primarily theoretical, building on and synthesising pre-existing research from a range of academic disciplines. As there is little empirical work that is directly relevant to support and illustrate this proposed framework for understanding tall residential buildings, particularly in the English context, we draw on an eclectic range of sources including media reports, policy papers and developers’ websites to ground our analysis. We also refer to the facts (not the law) provided in an English law report to illustrate how power is both exercised and resisted by freeholders and leaseholders. In terms of legal methodology, our analysis is from the perspective of ‘law in action’ rather than legal formalism (‘the law in books’); that is, we aim to present a realistic account about what actors and decision-makers do and how they behave.

Tall residential buildings in England

There is no universally accepted definition of ‘tall building’, although 50 m (or 14 storeys) has been suggested as the threshold for a tall building (Council on Tall Buildings and Urban Habitat, 2021). In England a building at least 18 m high (or seven storeys) attracts extra regulation focussed on safety issues (Building Act 1984, section 120D, added by Building Safety Act 2022 section 31). In Greater London, the Spatial Development Strategy (known as the London Plan 2021) states that a tall building should be locally defined; definitions adopted by local London boroughs range between 25 and 30 m (8–10 storeys; NLA, 2023: 14–15). Rather than a rigid definition, therefore, we adopt Nethercote’s (2018: 680) approach that a building is tall if it has ‘a significant vertical dimension’.

Although the skyline of England’s largest cities is undergoing a vertical transformation driven by private high-rise residential development, very little is known about the buildings themselves. Not even basic data are available, such as how many tall towers there are, the number of storeys each has, or whether the buildings are standalone or part of a larger complex of mixed height, mixed use buildings. Tall towers are not homogenous. Architectural form can range ‘from sublime “starchitect”-designed skyscrapers to generic tower blocks’ (Nethercote, 2018: 658). Most privately built English residential towers provide apartments for market sale but there are increasing numbers of ‘build to rent’ towers which are intended for rental housing (not sale) with the investor retaining ownership of the building and providing services. Indeed, recent data show a decline in high-rise residential properties for sale in London, with a growth in build-to-rent schemes of 20–25 storeys (NLA, 2023: 11). Planning rules typically require that privately built apartments must include a proportion of ‘affordable housing’, for sale or rent, for those whose needs are not met by the market (MHCLG, 2023: paras 64–66).

The high-rise trend is most pronounced in London and Manchester but is also accelerating in other large cities such as Birmingham and Leeds. Over the decade to 2020 an average of 20 tall (20 storey plus) buildings were completed in London each year with over 580 towers in the pipeline, thus contributing significantly to the number of new homes (NLA, 2022: 6). In Manchester, which boasts the five tallest buildings in the UK outside London, 3400 apartments in residential towers gained planning permission in the first four months of 2022 (Timan, 2022).

These high-rise developments are seldom exclusively residential. They may contain commercial and retail units, sports facilities, lifestyle amenities and hospitality venues, each with different letting and governance arrangements. Deansgate Square in Manchester city centre provides a typical example. It was completed in 2021, providing over 1500 homes in four 40–67 storey towers (SimpsonHaugh, n.d.). Residents have exclusive access to a tennis court, swimming pool, cinema, gym, studios and basement car park, while the ‘public realm’ (in fact, privately owned space) around the towers includes cafés and restaurants, leisure facilities and pedestrian walkways next to the River Medlock. This development, like many others, shapes its immediate neighbourhood.

Financialisation and law(s) intertwined

In this section we discuss ways in which law(s) and financialisation combine to influence the urban environment, through the planning and construction stages, the ongoing management and maintenance of tall towers and the lived experiences of residents.

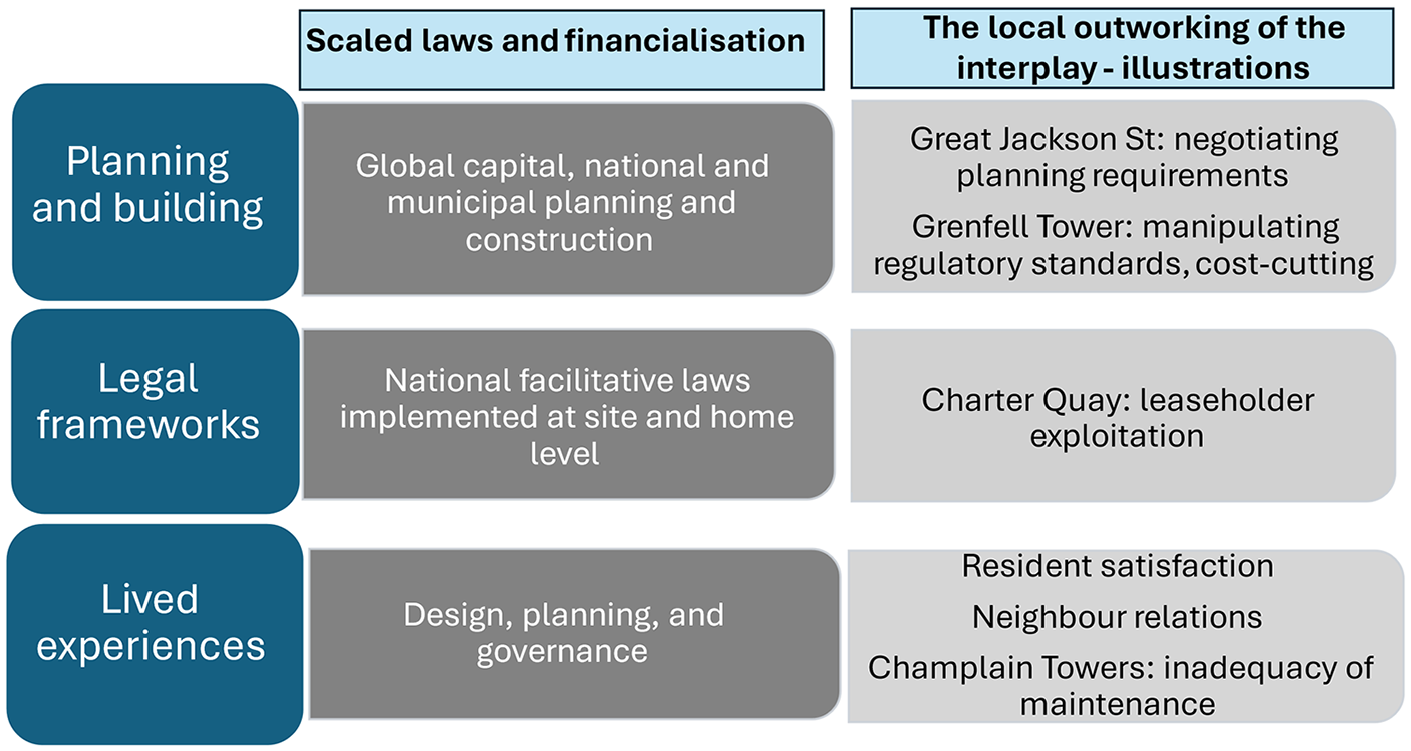

Figure 2 refers to examples used in the following text to illustrate the impact of this symbiotic relationship at the local level. As with law, the process of financialisation operates at various scales, impacting both production and consumption (Aalbers, 2016: 2). We are interested in how financialisation interacts with law, a relationship largely ignored in urban theory.

The effect of law and financialisation at the local level.

Planning and building residential towers

As shown in Figure 1, the planning, financing and construction of residential towers is shaped by the interconnection of law and financialisation at global, national and municipal scales. Skyscraper developments usually involve significant capital mobilisation at the global scale. Projects are often financed from afar and supported by institutional investors without the involvement of local actors (Nethercote, 2018: 667). The UN Special Rapporteur expresses concern that in this now globalised model, developers and owners have ‘no engagement with or accountability to the communities in which their “assets” are located’ (UN General Assembly, 2017: 10). For developers, towers offer economies of scale; extending buildings upwards allows more residential units to be built and sold.

Planning law implements policies developed at national and local scales, reflecting political ideologies (Taylor, 1982), as well as decisions made at the municipal level. In combination with financialisation, planning law determines where a tower can be built, its height, its relationship to adjacent buildings, and its external aesthetic. Planning policies are often pressed into the service of financialisation, with developers exploiting the pressure on local authorities to encourage investment and achieve city regeneration. For example, local-scale London planning policies include regulatory schemes favouring high-rise buildings despite planners’ misgivings (Laing Ebbensgaard et al., 2024)

Non-resident neighbours have little opportunity to influence planning decisions but may find their environment completely changed by the addition of one or more towers (Roast, 2024; Sheehan, 2024). Further, although urban environments are strongly determinative of health and wellbeing, planning law takes little direct account of a tower’s impact on such issues. Vertical development may, for example, impact on non-resident neighbours causing material harm through loss of daylight, sunlight and outlook (Laing Ebbensgaard, 2024). Indeed, a recent English study found that the legal density and complexity of planning law enable ‘large property developers and other powerful private actors … [to use] … the law to promote projects that generate the most profits, to the detriment of health and well-being of residents’ (Montel, 2023: 317).

As Figure 2 indicates, developers have become adept at ‘selling’ their projects as an enhancement of the immediate environment and of the cityscape (Laing Ebbensgaard, 2024), often including the creation of the public, quasi-public and private spaces around tower developments. For example, the 2007 Development Framework for the Great Jackson Street area in Manchester designated it ‘a new, vibrant City Centre neighbourhood’; tellingly, ‘as a symbol of the regeneration of the area, sites for tall buildings were identified’ (Deloitte Real Estate, 2018: 7), and subsequently built. The 2018 Update document displays more concern for the public realm in the area, including landscaping, pedestrian connectivity and a mix of leisure facilities and commercial outlets for non-residents, designed to inject animation and activity at street level. This suggests that planning law and financialisation, represented at this scale by the interests of property developers and investors, intertwine and become aligned over time.

Affordable housing targets are a notable source of tension between planning law and financialisation; developers and planning authorities negotiate around reducing initial numbers, or making alternative provisions elsewhere. For example, at Great Jackson Street, Manchester, five towers ranging from 47 to 71 storeys providing 2388 apartments are planned, but none would be affordable housing (Whelan, 2024). The landowner, Renaker, offered to contribute £90,000 towards affordable housing elsewhere in the city. Having initially described this as an ‘insult’, councillors were persuaded by planning officers to accept as Renaker will also contribute £1.5m to a new school and invest £10 million in public realm improvements (Jessel, 2022). Developers thus use their strong negotiating position to shape towers and the surrounding urban spaces (Blandy and Wang, 2013), entrenching socio-economic divides in the city through the planning process.

The construction and form of towers is also impacted by regulatory laws, ‘broadly defined as attempts to control, order or influence the behaviour of others’ (Black, 2002: 1), that take effect through national legislation and statutory instruments, with impact at the local level. Regulatory law thus affects the form of the built environment, for example through building regulations that specify construction standards (The Building Regulations 2010). Tall residential buildings should, of course, be constructed and maintained to be safe places. But high regulatory standards are often in tension with financialisation. In 2017 a devastating fire at Grenfell Tower in London, England, caused the loss of 72 lives. The 24-storey tower was built in the 1970s to provide council housing. The core component of the original construction was concrete, but during 2015 and 2016 the tower underwent a major refurbishment which included combustible insulation and cladding being added to the external walls. The occupier make-up had changed by then to become a mix of long leaseholders (owner-occupiers), council tenants and tenants of private landlords. The tragedy led to the exposure of multiple failings in relation to construction products, build design and quality and regulatory standards, and has caused a major crisis in building safety in high-rise buildings throughout the United Kingdom (Grenfell Tower Inquiry, 2024).

The Phase 2 report from the Grenfell Tower Inquiry illustrates the fraught relationship between financialisation and regulatory law, and its consequences. The UK government missed opportunities to amend regulatory documents to prohibit the use of combustible products on high-rise buildings; product suppliers engaged in deliberate strategies to manipulate tests, misrepresent test data and mislead the market; pressure from commercial interests within the building control inspection process meant that the system was not effectively serving the public interest; and cost reduction (often referred to as ‘value engineering’) in the refurbishment project drove the choice of the particular combustible cladding system (ACM, aluminium composite material) which was found to be the principal cause of the rapid fire spread (Grenfell Tower Inquiry, 2024).

This fraught law–financialisation relationship can also be seen in other design issues. There is, for example, an evident risk to life if residents need to evacuate to escape from fire. The consequence of a tall building having only a staircase was seen in Grenfell Tower: firefighters had to share the sole (smoked-filled) staircase with evacuating residents, with devastating outcomes. Notwithstanding the life-safety risks, regulatory laws have permitted the construction of towers with only one staircase, thereby enabling developers to maximise the marketable internal spaces (see, e.g. Booth, 2022). Regulations are changing to mandate second staircases in new English buildings above 18 m from 30 September 2026, but developers will still play the system. For example, the plans accompanying an extant planning application by a joint venture between a housing association and private developer have been tweaked to avoid the new second staircase rule by reducing the height of ground floor commercial units by 30 cm so that the overall height will be 17.7 m (Rogers, 2025).

English regulatory law has been shaken up by the Grenfell Tower fire. However, it is unclear how effectively the new building safety regime being implemented pursuant to the Building Safety Act 2022 can address the complexity of tall residential leasehold towers.

Setting up the legal framework for residential towers

Private law-making powers play a key role in constituting residential towers, alongside governmental law or regulation. National laws provide the toolbox from which parties can select how to structure the local property and contract rules that apply to the site, building and home. The legal scholar Hart refers to these types of law as ‘power-conferring’; they ‘provide individuals with facilities for realising their wishes … to create structures … of rights and duties’ (Hart, 1961: 27, emphasis in original). He also notes an important constraint, that the facilitative laws ‘detail the manner and form in which the power is to be exercised’.

In England, facilitative law in the form of property law permits units sold in residential towers to be set up either as long leaseholds or (following the Commonhold and Leasehold Reform Act 2002) as commonhold units. Leasehold has become deeply unpopular amongst flat owners, particularly because of the opportunities for landlords to profit at leaseholders’ expense (as illustrated later). The commonhold system of owning and managing apartments is akin to the condominium system. However, ‘fewer than 20 commonholds are currently in existence … there is insufficient incentive, financial or otherwise, for those involved in building homes and commercial property to move away from leasehold which, from their perspective, is considered to work well’ (Hopkins and Mellor, 2019: 327). Developers and mortgage providers continue to select leasehold, favoured by financialisation processes, but options may soon be restricted as the UK government has pledged to introduce a draft Commonhold Bill in late 2025, aiming to make commonhold the default tenure for new apartments.

Bright and Weatherall’s (2017: 205) ‘building governance’ framework explains how the ‘governance tools’ (the lease and associated documents) enable, shape and constitute the physical form of the block of apartments and affect the social relations within it. It is the professional actors (developers, managing agents, and lawyers) who select how ‘technologies of law’, such as the lease (Riles, 2005), are used in site development. These actors therefore control the ‘juridical field’ (Bourdieu, 1987), manipulating the ‘critical legal events’ involved in the process of setting up, selling and managing such developments to their advantage (Blandy et al., 2006; White and Punter, 2023: 104–107). It is the freeholder/developer, and their lawyers, who mould the property and contractual rights derived from facilitative law to structure site-specific property and management arrangements: the length of the lease; the particular contractual distribution of rights and responsibilities; the delineation of which spaces are privately used, which are shared and which are public; and the mechanisms for governance and management, including the provision of service charges, and so on. The outcome is a complex legal matrix.

In many towers there will be additional legal entities (‘intermediate landlords’) holding sub-leases between the freeholder and the individual unit owners, for example a housing association which has a long lease from the freeholder and in turn sells (or lets) individual apartments at affordable rates. Unlike the statutory legal requirements which mandatorily regulate aspects of condominium properties there is no standard template for the wording or content of residential long leases in England. Nor are there standard form agreements for the commercial, retail and leisure spaces within these buildings which will have different tenure and governance arrangements to the apartments. Indeed, a feature of English law is that each development will have a different legal matrix with individually formalised property and contractual arrangements. This complexity is also present in other jurisdictions in relation to arrangements beyond the condominium form itself, for example, in relation to air space parcels (see Harris, 2025; Teys, 2024). This emphasises the need for empirical research to analyse how laws play out in practice.

The leasehold system provides many opportunities for profit-making (financialisation) in residential towers. Most leases will allocate the right to manage the building to the freeholder (or an intermediate landlord). The developer-freeholder can choose whether to retain the freehold as, perhaps, both investor and manager; to sell it and disappear from the scene; or (we suspect unusually for tall blocks) to transfer it to a company in which each apartment owner has a share. Freehold sales have provided attractive investment opportunities. Until July 2022, leases often specified that ground rents would double at 10-year intervals. This provided a reliable income stream and explains why many freeholds have been bought by pension funds, ground rent companies or offshore trusts. Recent legislation (The Leasehold Reform (Ground Rent) Act 2022, section 3) has prohibited the use of ground rents at more than a notional amount for new leases, but many other opportunities remain for ongoing income generation by landlords. Developers may sell the opportunity to manage the site to a property manager or embed a subsidiary company as the management company of the site in perpetuity as a means of providing further revenues.

Financialisation does not take a standard form across different jurisdictions; laws enable money to be raised and to flow by whatever routes are most advantageous. In England the leasehold system provides the potential for freeholders to exploit leaseholders and although there is regulation of service charges it can be difficult for leaseholders to challenge them. The kind of issues that may arise can be seen at a mixed-use site, known as Charter Quay, in Kingston-upon-Thames, London. Leaseholders at this development complained to the First Tier Tribunal (Property Chamber) about high service charges and poor service quality. The law report illustrates how the professional actors controlled the juridical field to their advantage: the freeholder, management company, intercom provider, etc. were all effectively part of the Tschenguiz family empire of companies and the Tribunal described this intricate corporate structure as descending in a ‘quasi-biblical fashion’ from one British Virgin Island company (Charter Quay Ltd v D Winsor and others, 2011: para 13). Contracts relating to management of the site were agreed between these related or subsidiary companies without any provision for scrutiny by the leaseholders, providing the freeholder with many opportunities for profit. The Tribunal found the resulting arrangements to be ‘extremely onerous’ to the leaseholders (Charter Quay Ltd v D Winsor and others, 2011: paras 23, 36 and 88), and decided the management fees and insurance commission should be reduced by as much as 75% in one year. Although the Charter Quay leaseholders were unusual in their cohesiveness and persistence in challenging service charges before a Tribunal, accusations of freeholders ‘ripping-off’ leaseholders are not rare, as is clear from numerous media reports and reported Tribunal decisions.

In addition to the formal structuring through facilitative law and the technologies of law, property relationships are lived relationships, socially constructed and connected through organisational practices and everyday understandings (Blandy et al., 2018). Thus, the property and contractual rights distributed by leases, management contracts, and so on between the freeholder, intermediate landlords, the individual unit-owners, renters, mortgagees, and tenants are overlaid by social arrangements which make the reality of the lived relationships between rights-holders socially complex. A richer understanding of towers requires an awareness of how the community of owners, users and managers engage in decision-making, practical management and use the space (Bright and Weatherall, 2017: 206; Nethercote, 2022).

Residents’ lived experience of towers

The lived experience of those living in and near towers will be influenced by the interplay of financialisation and laws playing out at the various scales discussed above. The ‘feel of the place’ will be affected by how many units are owner-occupied, empty, or occupied under short-term rental arrangements from buy to let landlords, as well as by the social mix (determined by affordable housing targets). The financialisation of housing means that many units are bought as investments, either as ‘buy to let’ or as ‘buy to leave’. Some of these investors will be from overseas, and ‘buy to leave’ flats have been described as a ‘specific asset class, a “safe deposit box” for transnational wealth elites’ (Fernandez et al., 2016: 2444). They are particularly common at the high-end of the market, creating what Soules (2021) refers to as ‘zombie urbanism’ or ‘necrotecture’ (Atkinson, 2019), with a deadening effect on the social vitality of social spaces and the city.

Developers can maximise profits by gaming the system to reduce social mix, either through negotiating on affordable housing targets, as seen above in the Great Jackson Street development, or by excluding the affordable housing from certain parts of the development and by denying certain tenure groups access to some facilities. Divisions are heightened by the use of separate entrances (‘poor doors’) for social tenants (Osborne, 2014) although, in London, recent guidance for housing design says that poor doors are ‘unacceptable’ (Mayor of London, 2023). Segregation can have significant impacts on the critical challenges of, and within, tall urban environments, considerably beyond their visual impact. At One Tower Bridge, London, marketed as ‘a prestigious development offering a five-star living experience’ (Berkeley Group, 2016), affordable housing is confined to a separate block with no access to the communal gardens. Although this means the tenants do not pay service charges for pool or garden maintenance, they also have no allocated play space and tenants have received notices that allowing children to play in the corridors is ‘a breach of tenancy agreements’ (Grant, 2022). Indeed, children may be unwelcome in apartment blocks; a study from Australia illustrates how social norms intersect with (formal) regulation and design to make families with children feel out of place (Kerr et al., 2025). This combination of profit-seeking, architectural design and private law-making creates social segregation rather than inclusion.

The ‘volumetric neighbours’ (Nethercote, 2022) in residential towers, whether owners or tenants, have highly variable levels of satisfaction with their homes. There can be positive features of verticality; for example, views can be intensely meaningful to residents in creating special homes (Baxter, 2017). Residents’ experiences are influenced by personal demographics, such as socio-economic status, stage of life cycle, gender and their degree of choice in moving to the high-rise (Appold et al., 2006; Gifford, 2007), as well as by physical features such as the building’s location, design, density and the extent of facilities and common spaces. These latter factors, as we have seen, are influenced by both financialisation and law, operating together at interconnected scales.

Nethercote’s (2022) large-scale empirical study into densely occupied high-rise ‘investor grade’ residential buildings in Melbourne and Perth showed that Australian high-rise residents held simultaneous but conflicting ideas of ‘home as belonging’ and ‘home as dominion’ (p. 19). Encountering other residents in the hallways, lifts and shared facilities can enhance feelings of belonging, ‘offering opportunity for friendships, social contact, safety in numbers and comfort for lonely and vulnerable elderly and disabled residents’ (Leshinsky, 2021: 117). Resident-led initiatives can create sociable norms of ‘live and let live’, as found by research into ethnically mixed new high-rise buildings in Israel (Arviv and Eizenberg, 2021). Advertisements for expensive high-rise buildings may, however, emphasise the idea of dominion, supporting the powerful idea of property as exclusive, ‘a space to insulate buyers from forms of social connection’ (Atkinson, 2019: 7). Such design seeks to disentangle ‘individual units’ from ‘the messy unpredictability of collective life’ (Soules, 2021: 18, 137), emphasising ideas of individuality, central to neoliberal housing financialisation.

The governance and management arrangements for buildings are major determinants of satisfaction levels, but are often overlooked. Unique selling points, such as the much-publicised Sky Pool which ‘stretches between the roof tops’ (Gregory, 2021) at London’s Embassy Gardens development, attract ultra-wealthy investors and buyers/residents (Embassy Gardens, n.d.). However, such facilities add significantly to the complexities and costs of management and maintenance. At a more mundane level, but central to the day to day lived experiences of residents, constant care is needed to maintain the building, for example, when a lightbulb in the entrance hall needs replacing and management needs to step in. In condominium-based systems a forum for collective decision-making by unit owners makes key decisions, but this apparent autonomy, important for resident satisfaction, is often constrained by developers having tied in management of the building to property managers closely connected with their development company (Blandy et al., 2010; White and Punter, 2023: 104–107). In addition, international condominium research shows that tensions are likely between owners and renters, between residents and property managers, and between residents and condominium board members, and that these frictions increase as buildings age (see, e.g. Easthope and Randolph, 2021; Webb and Webber, 2017). Further complexity is added to governance because differential management arrangements apply to units occupied by different tenure and user groups, affecting the lived experiences of residents (Harris, 2019).

In England, the leasehold system adds an additional layer of tension as governance is controlled by the freeholder while the leaseholders, although paying for services, are excluded from participation in decision-making (Hammond and Marriage, 2021). The absence of voice and autonomy causes significant discontent (see survey by Brady Solicitors, 2016) and can lead to leaseholders suffering further from the profiteering practices of freeholders and connected managers, as illustrated by the Charter Quay litigation discussed earlier (Charter Quay Ltd v D Winsor and others, 2011).

Financialisation and inadequate regulation causes problems not only at the construction stage of high-rise buildings, but also with their ongoing management and maintenance. For example, whilst the exact cause of the collapse of Champlain Towers in Florida remains unknown, it has raised concerns that condominium laws are ill-designed to ensure that ageing blocks are properly maintained and managed (see, e.g. Florida Bar RPPTL Condominium Law and Policy Life Safety Advisory Task Force, 2021). This disaster occurred despite its condo board knowing that urgent repairs were needed (McKenzie, forthcoming), illustrating the difficulties in getting unit owners to agree on expenditure. This highlights the need for mandated periodic inspections by relevant independent professionals and for adequate reserve funds, accompanied by effective organisational practices. In England, neither inspections nor reserve funds are required. Post-Grenfell, thousands of blocks have been found to be unsafe and the remediation costs are eye-watering, typically several million pounds per block (Bright, 2023). Similar sums will be involved to ensure that tall towers remain safe as they age, but there are serious, and unaddressed, questions about how the necessary level of finance can be raised. As Bright argues, law (particularly regulatory and property law) must adjust, and be adaptable, to provide for the resilience of towers against the process of ageing and the challenges of climate change (Bright, 2023).

Using scale to analyse the interplay of law and financialisation

Residential towers are an important feature of today’s urban landscapes across the world, transforming skylines, neighbourhoods and cities. They provide homes for millions and financial assets for investors. Yet much of the existing research into vertical housing fails to consider the roles which law plays in the production and life of residential towers.

This article argues that it is therefore essential to analyse the various types of laws that, together with financialisation, co-produce and sustain residential towers. The framework used builds on the geographical scholarship of scale and suggests five scales at which to examine this intertwined relationship. At the global scale, financialisation drives many aspects of the development and architecture of residential towers. In most jurisdictions, facilitative law was changed to establish the legal form of condominium before residential towers could be built, sold, and occupied (Harris, 2011). English lawyers simply adopted the already available lease form and there is a particular need for research into English residential towers to take account of English legal processes. The ineffective and piecemeal response to the post-Grenfell building safety crisis in England has exposed the lack of basic data on buildings’ height and fabric, together with organisational data about who the ‘owner’ is, how buildings are looked after and how to identify the ‘responsible person’ for ensuring the building is safe.

National planning policies and law, together with regulatory law, are key to the design and construction stages for residential towers. Municipal planning consent processes, in combination with financialisation and facilitative law, affect the physical form, the interplay of public and private spaces, the mix of residential, commercial, retail and leisure spaces, and the mix between social and private housing. At the site/building and home scales, routine management and longer-term maintenance and renewal planning for residential towers are complex tasks, governed by a combination of regulatory law, the lease as a technology of law and operational practices, all intertwined with the forces of financialisation. Our analytical lens shows that property relationships are not fixed in time, but are dynamic, context-specific and socially complex ‘to accommodate changing patterns and understandings of spatial use, new rights-holders, relationship needs, economic realities, opportunities, technical innovations and so on’ (Blandy et al., 2018).

Detailed empirical studies using mixed methods, including doctrinal legal and documentary analysis, are needed to understand the coalescence of financialisation and law(s) in creating particular sites of residential towers. At the site/building level such research will reveal the variety of, and interrelationship between, various property rights, and the structuring of governance arrangements. At the scale of the home, further research is needed into residents’ lived experiences, ‘pursuing ethnographic detail to open up the variety of experiences, imaginaries and practices of a vertical urban life’ (Harris, 2015: 609).

Application of our analytical frame will enable international comparisons to be made, and will provide more robust foundations for the development of policy on high-rise residential buildings, taking into account their multi-faceted complexity and their impact on regions, cities, neighbourhoods and those living in and around the towers.

Footnotes

Acknowledgements

This paper has benefitted from multiple workshop conversations, particularly at the Oñati International Institute for the Sociology of Law in 2022 and at Southampton University in 2023. We are very grateful to the organisers and contributors, with special thanks to Professor Helen Carr and Professor Douglas Harris.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.