Abstract

This article introduces the notion of the ‘gentrification regime’, which we believe is better able to capture the diversity of gentrification trajectories than the more macro-level notions of gentrification ‘waves’ or ‘stages’. We define a ‘gentrification regime’ as a specific set of relations between producers and consumers of housing made possible by a particular policy and financial context. Empirically, this article tracks the shift from a gentrification regime in which social upscaling is linked to increases in ownership to one that foregrounds the development of the private rental sector. To evidence this shift, we use the full set of property transactions linked to the production and the sale of apartments in the city of Dudelange in Luxembourg between 1970 and 2019 to reconstruct the trajectories of residential projects. We observe the replacement of local developers, responsible for a construction boom in the early 1990s, by national-level developers focusing on locally supported flagship projects targeting investor demand, itself stimulated by national fiscal policies. We witness an investor interest for both new and existing housing, signalling an increased pressure on the housing market, which seems to lead to an incipient (cross-border) exclusionary displacement. The article thus shows that national-level fiscal policy, and not only the deregulation of the private rental sector, can create value gaps that trigger a shift to buy-to-let gentrification. The notion of ‘gentrification regime’ is thus shown to provide a new way to understand the locally and temporally specific processes underlying the diversity of gentrification dynamics we see today.

Introduction

While gentrification involves changes in both the users and the owners of place, the former has usually been foregrounded – such as in Clark’s (2005: 263) definition of gentrification that sees it as a ‘change in the population of land-users’. Recent work has shown the extent to which producers of housing are central actors in the appearance and intensification of gentrification (Nethercote, 2020; Paccoud et al., 2022). Any attempt to theoretically or conceptually capture the variety of gentrification processes must therefore emphasise the relationship between the users and owners of place, and thus the interconnections between consumers and producers of housing. The ways in which gentrification is led by or responds to changes in public policies and financial technologies is also well documented (Aalbers, 2020; Lees and Ley, 2008).

In this article, our starting point is that processes of socio-spatial change are always locally and temporally specific: while the ‘waves’ or ‘stages’ models of gentrification hold explanatory value, they have problems with non-linear processes and sudden changes related to locally specific policies or financial instruments. To capture the diversity of gentrification trajectories, we propose the concept of ‘gentrification regime’. A gentrification regime describes the way in which producers and consumers of housing solidify their interactions around a particular type of gentrified property, a solidification made possible by a defined set of policies and financial instruments.

We use this notion to track the shift from a gentrification regime in which social upscaling is linked to increases in ownership to one that foregrounds the development of the private rental sector. To do this, we draw on the case of Luxembourg, where, faced with a structural deficit of supply in relation to growing demand for housing as the country’s economy grew increasingly tied to its financial centre, policy support started to specifically target rental investors at the turn of the 20th century (Mezaroş and Paccoud, 2024). Instead of increasing supply, as was hoped for, large-scale developers redirected a large proportion of new housing to fulfil new investor demand. In the case of Luxembourg, where public actors are not significant landowners, this shift in regime points to the particular role of developers, who can take the lead in effecting housing market change in response to the policy environment. The shift to a gentrification regime in which housing production internalises incentives for rental investors puts pressure on private sector tenants, but also on owner-occupiers who face increasing competition in local housing markets.

To investigate the way in which this new gentrification regime took hold on the ground, we draw on the full set of property transactions linked to the production and the sale of apartments in the city of Dudelange between 1970 and 2019. We draw on these records to reconstruct the trajectories of residential projects in the city, including land acquisition and assembly, navigation of the planning process and the sales of the apartments (including first and repeat sales). This data shows that local property actors render concrete the possibilities opened up by national-level fiscal policy changes, and in the process spread gentrification dynamics even to small, post-industrial towns.

In what follows, we broadly ground the notion of ‘gentrification regime’ in the literature, taking as its starting point the three types of actors that Smith (1979) identified as involved in neighbourhood gentrification. These three types of developers – the professional, the occupier and the landlord – can stand for three broad gentrification regimes that have mutated according to changes in public policy and financial technologies. In the empirical analysis and discussion, we provide a detailed account of the way in which a landlord developer regime has taken hold in Dudelange over the last 20 years. We first demonstrate this by analysing production-side logics, then turn to how they have impacted housing consumers, including through an exploratory analysis of the trajectories of those who sold their property in Dudelange in recent times.

Gentrification regimes

The occupier, professional and landlord developer gentrification regimes

It is fruitful to return to Smith’s (1979) landmark study of gentrification in Philadelphia, as it lays out the central components of gentrification research: housing producers, housing consumers, public policy and financial technologies. Indeed, he was the first to document the fact that ‘gentrification may be initiated in a given neighborhood by several different actors in the land and housing market’ (Smith, 1979: 545). His study also highlighted that gentrification is initiated by ‘some form of collective social action at the neighborhood level’ (Smith, 1979: 545). Smith mentions the state (urban rehabilitation) and financial institutions (redlining) as drivers of this collective social action.

In this article, taking inspiration from the concept of urban regime, we propose the notion of a ‘gentrification regime’ to bring together these different elements and to facilitate the identification of particular constellations of actors, policies and financial instruments that push gentrification forward in particular contexts. While we borrow the term regime, we do not suggest here that there is always and necessarily the same level of shared decision making as in the cases described in Stone (1989). Some gentrification regimes might include local political actors, while others might be pushed forward only by national-level fiscal policies: the degree of shared and collaborative agency – as well as the political scale at which this agency operates – thus needs to be ascertained empirically.

We have identified three types of gentrification regimes, each tied to one of the three ‘gentrifiers’ that Smith identified: ‘(a) professional developers who purchase property, redevelop it, and resell for profit; (b) occupier developers who buy and redevelop property and inhabit it after completion; (c) landlord developers who rent it to tenants after rehabilitation’ (Smith, 1979: 546).

The ‘occupier developer’ is usually associated with the beginnings of gentrification, in which owner-occupiers invest ‘sweat equity’ into properties in relatively disadvantaged areas. This gentrification regime can, however, be thought more broadly as any configuration in which gentrification is pushed forward by those who are at the same time owners and users of place. This includes, amongst others, marginal gentrifiers (Rose, 1984), rural gentrifiers (Phillips, 1993), and super-gentrifiers (Lees, 2003), as well as owner-occupiers turned investor-activists in an era of financialised homeownership (Cook and Ruming, 2021).

The category of ‘professional developer’ can stand for a gentrification regime in which the process of upscaling is pushed forward by more than one owner of place. In such a gentrification regime, the owner-occupier is still the final owner and user of place but is no longer involved in the production of the housing unit through which social upscaling is made possible. Examples of this regime include new-build gentrification (Davidson and Lees, 2010, 2005), state-led redevelopment (Shin, 2009) and transnational gentrification (Sigler and Wachsmuth, 2016), as long as the gentrified properties produced are destined for owner-occupation.

The ‘landlord developer’ represents a third gentrification regime in which the final owner is no longer the user of place, with this position taken up by individuals who might be the visible face of gentrification but who as renters are not deriving economic benefits from the social upscaling they contribute to. This type of gentrification can occur through a number of different channels: investors purchasing a housing unit to renovate and put up for rent, new-build housing that is purchased as a rental investment and urban regeneration that transfers units from the social to the private rented sector (Paccoud, 2017). It is linked to the development of build-to-rent models (Nethercote, 2020), developers marketing their supply to buy-to-let investors (Pollard, 2023), housing as a site of investment for the super-rich (Fernandez et al., 2016) or overseas investors (Ho and Atkinson, 2018) and the facilitation of short-term rentals (Cocola-Gant and Gago, 2021).

While Smith (1979) uses the term ‘developer’ for the three types of gentrifiers he proposes, the focus here is thus on the relation between the owners (producers) and users (consumers) of place. This makes it possible to move from an actor-centric typology of gentrification to one that foregrounds the type of gentrified property produced and who it is targeted to. For example, developer-led gentrification could fall in either the ‘professional developer’ or ‘landlord developer’ regime depending on whether the units produced are destined for owner-occupiers or investors. In both cases, the producer is the same type of actor, but the final user of place is different – it is thus two different types of gentrified properties that are created, with their own logics and capacities to spread gentrification.

All three of these gentrification regimes rely on particular public policies. The state is thus ever present in setting the framework conditions for the operation of a particular regime of gentrification, even before gentrification becomes the explicit content of public policy (Lees and Ley, 2008). The three gentrification regimes described here can loosely be attached to public policies subsidising owner-occupation (‘occupier developer’), facilitating property development (‘professional developer’) and incentivising property investment (‘landlord developer’), though these can exist concurrently.

These gentrification regimes also draw on distinct sources of finance, and their diversification thus intersects with the rise of financialisation (Aalbers, 2019). For example, Wyly and Hammel (1999) locate the impetus for a new wave of ‘occupier developer’ gentrification in financial innovations linked to mortgage markets. In the case of the ‘professional developer’, Sanfelici and Halbert (2016) point to the newfound ability of developers to draw on financial markets as a crucial driver of the fragmented pattern of Brazilian housing production. Inflections of the ‘landlord developer’ regime can be seen in the work of Fields and Uffer (2016), who show how large financial actors became involved in the ownership of housing, as well as in the Canadian context where August and Walks (2018) and Crosby (2020) study how financialised landlords draw on specific investment tools to accelerate gentrification processes.

Conceptualising changes in gentrification regimes

The fact that gentrification can change over time is well documented, both across countries and within particular cities and neighbourhoods (Kadi and Matznetter, 2022; Verlaan and Albers, 2022). While ‘stage’ models of gentrification have focused on changes in the profile of gentrifiers in an area over time (Kerstein, 1990), the ‘wave’ model looks at the impact of changes at the level of broad systems (economic cycles, global urban governance, globalisation, financialisation, etc.) on local socio-spatial change (Aalbers, 2019; Hackworth and Smith, 2001). The notion of the ‘gentrification regime’ that we introduce here provides a complementary perspective: it focuses on changes in the type of gentrified property around which property interests coalesce. While ‘wave’ and ‘stage’ models of gentrification tend to follow a certain sequence and to universalise particular economic or political trends, the notion of a ‘gentrification regime’ has the flexibility to capture non-linear processes and sudden changes related to locally specific policies or financial instruments.

More generally, it is possible to distinguish two ways in which change can occur at the level of gentrification regimes: changes within regimes ((de)-intensification, (de)-acceleration) and changes between regimes (qualitative shift). The theories of the rent gap (Smith, 1979) and the value gap (Hamnett and Randolph, 1984) are helpful here in conceptualising change over and beyond the initial occurrence of gentrification. The rent gap alerts us to the possible intensification of gentrification processes: as the rent gap expands in a particular location, an intensification of the operation of a particular gentrification regime can occur. Super-gentrification, as coined by Lees (2003), can, for example, be seen as the intensification of the ‘occupier developer’ regime, even if in some specific cases the purchase could be motivated by strategies such as ‘buy to leave’ (Glucksberg, 2016). Similarly, the shift from ‘classical’ rental tenancies to short-term renting (Cocola-Gant and Gago, 2021) intensifies the ‘landlord developer’ regime by accelerating tenant turnover compared to buy-to-let gentrification (Paccoud, 2017).

In turn, the value gap posits the potential for endless qualitative shifts between tenures as their relative ability to push forward gentrification ebbs and flows (Hamnett and Randolph, 1984). Policy decisions that modify the economic returns on one tenure type compared to another can thus cause a qualitative shift in the type of gentrification regime operating in a given context. In the UK, the introduction of the buy-to-let mortgage and the deregulation of the private rental sector led to a shift from the ‘occupier developer’ to the ‘landlord developer’ regime (Paccoud, 2017). As will be shown later, this shift can also be caused by the development of tax advantages for property investors, as already hinted at in the Australian case (Weller and van Hulten, 2012). Similarly, the redirection of property developers from production for owner-occupation to production for property investment represents a qualitative shift in a gentrification regime. This is notable, for example, in the differences between classic new-build gentrification (Davidson and Lees, 2005) and new forms of build-to-rent (Nethercote, 2020).

Given the importance of policy changes in explaining shifts between gentrification regimes (and to a lesser extent the intensification of gentrification within a particular regime), it is important to reflect on the mechanisms through which such decisions are taken. The ‘transition from public policies ambivalently engaging gentrification to the process now becoming a significant tool of public policy’ (Lees and Ley, 2008: 2380) is well documented. The way in which public policies have either spurred or slowed gentrification processes has recently been encapsulated in the notion of the commodification gap (Bernt, 2022). Taking a very long-term perspective, Kadi and Matznetter (2022) point to changes in rent regulations as important inflection points in Vienna’s gentrification trajectory. However, less has been written on the political economy of such policy decisions, and especially on the influence of private sector actors in structuring the policy field. The real estate development sector has, for example, been shown to shape the regulatory systems surrounding land use (Leffers and Wekerle, 2020; Waldron, 2019).

A final consideration in relation to changes in gentrification regimes concerns geography, and gentrification’s ability to spread. At the urban-regional level, much of the discussion has centred on whether gentrification could extend beyond the central core and the architectural cachet that attracted the first gentrifiers. Studies have since documented social upscaling in a number of environments once seen as impervious to gentrification, such as rural areas (Phillips, 1993), brownfield sites (Davidson and Lees, 2005), social (public) housing estates (Reades et al., 2023) and areas with a significant minority population (Paccoud et al., 2022; Walks and August, 2008). Insofar as gentrification regimes depend on particular assemblages of actors, policies and financial technologies, they provide a means to conceptualise extensions of existing gentrification dynamics, which usually involve changes in one of these dimensions – such as the shift from owners to tenants as the main vehicle of gentrification in deprived areas (Paccoud, 2017). We now turn to our case study to show how the notion of a gentrification regime makes visible how national-level fiscal policy change can enable local property actors to import gentrification into a post-industrial location.

Luxembourg: A policy-driven gentrification regime change

Luxembourg (660,809 inhabitants in 2023) is a small landlocked country in Western Europe bordering Belgium, France and Germany (Figure 1). Its economy has been profoundly transformed since the 1970s: in 2022, financial activities accounted for 25.2% of Luxembourg’s Gross Value Added (GVA), a significant increase from 3.1% in 1970, while the iron, steel and metal processing industry contributed a mere 1% of GVA, down from 28.7% in 1970 (STATEC, 1990, 2023). Between 1975 and 2022, a growing gap between a relatively constant number of new housing units produced yearly and high economic and population growth has caused an 8.7-fold increase in real house prices (Observatoire de l’Habitat [ODH], 2023b).

Luxembourg, Esch-sur-Alzette and Dudelange.

As argued elsewhere, this gap is to some extent artificially created in a context of a highly concentrated landownership and property development structure (Paccoud et al., 2022). Residential land is mainly in private hands and is owned by a small number of families and local property developers: 0.5% of the resident population owns 50% of the residential land, and five local developers own half the residential land owned by companies (ODH, 2021). This control over land supply makes it possible to throttle housing production through land hoarding (by private individuals) and land banking (by developers) – in the absence of an inheritance tax on transfers to direct heirs and very light-touch property taxation (Paccoud et al., 2022).

Since the early 2000s, Luxembourg policy makers have used fiscal policy to try to speed up the production of housing. The idea was that stimulating housing demand through tax subsidies would indirectly encourage the construction of new units. While this fiscal framework was first designed to enable as many residents to become homeowners as possible, it was progressively expanded to buy-to-let investors from 1991 onwards (Mezaroş and Paccoud, 2024). Tax advantages, and particularly the possibility of deducting a percentage of acquisition costs from income tax declarations, stimulated domestic investor demand for housing but did not lead to any noticeable increase in the amount of housing built. Between 2015 and 2022, investors acquired between a third and a half of all new off-plan apartments, heightening the competition for housing with other buyers able to draw on inexpensive credit, and thus propelling a further round of house price growth.

The development of fiscal subsidies targeted towards investors can be seen as a qualitative shift in the type of gentrification regime occurring in Luxembourg, from a professional to a landlord developer regime. While a shift of this type has been documented in the UK following the introduction of the buy-to-let mortgage and the deregulation of the private rental sector (Paccoud, 2017), the development of tax advantages in Luxembourg for investors seems to create the same type of value gap between purchasing as an owner-occupier or as an investor. This makes it possible for professional developers to increasingly draw on pre-financing from sales to property investors to fund new construction projects, thus subtracting an important percentage of planned units from would-be owner-occupiers. The spatial consequences of this closure of the value gap also show similarities with the case of the UK, where buy-to-let investors seem to have targeted places in which high-income individuals do not want to live as owner-occupiers (Paccoud et al., 2021). In Luxembourg, 28% of the off-plan apartments purchased by property investors between 2015 and 2021 were in the south of the country, where the steel industry once concentrated. The south of Luxembourg is now a post-industrial landscape under pressure from the ripple effects of competition for housing in and around the capital city, a consequence of ‘spatially displaced demand’ (Hamnett, 2009). This indicates that a policy-driven shift to a landlord developer regime could, as in the case of the UK, enable the spread of gentrification to more ‘difficult’ locations.

To show how the landlord developer regime has taken hold on the ground, we analyse detailed information on the owners of property over the last 50 years in the southern city of Dudelange. A small rural settlement until the end of the 1870s, it then experienced massive population inflows with the opening of one of the country’s largest steel plants. Since its deindustrialisation from the 1970s onwards, Dudelange has become a residential suburb of the capital, and is now faced with the same rapid increases in house prices in recent decades, overlaid on the same landownership structure: a small group of residential landowners have played a central role in the city’s development over the last 70 years (Paccoud, 2020).

Methodology

The article draws on land registry archives providing detailed information on all property transactions in the city of Dudelange, with a particular focus on the transactions involved in the construction and sale of apartments. We focus on apartments (52% of Dudelange’s housing stock) as we consider them as stepping stones in housing trajectories and because the information in the notarial deeds is more detailed than for houses. We have information on the acquisition and assembly of the land required for the construction, as well as the first apartment sale by the developer of the project and all subsequent transactions involving these apartments. These transactions are extracts of the notarial document officialising the sale, and include information on the buyers and sellers involved, including their place and date of birth, declared occupation and address at the moment of purchase, as well as details about the transaction (type, price and location of the property transacted).

The occupations were manually coded, and we particularly focused on upper-class occupations, those classified as ‘managers’, ‘professionals’ and ‘technicians and associate professionals’ in the International Standard Classification of Occupations (ISCO). We distinguished between single buyers – those purchasing on their own, regardless of their marital status – and couple buyers for whom the spouse (or someone living at the same address) is included in the deed, regardless of the way in which ownership is split between them. Excluded from the analysis were individuals between whom the relationship could not be determined or was of another nature (e.g. family or business) or where the property was acquired by more than two buyers.

To complement the information drawn from the notarial deeds, we also analysed building permits. This includes the date at which a building application was submitted to the municipal administration and the date at which it was accepted, as well as some information on the application (location, number of units foreseen). By combining this with the property transactions, we were able to date the major moments in the life of a new residential project. The Dudelange municipal administration has also provided extracts of their population register, which we were able to cross-reference with property registers. Additionally, we used information from the Luxembourg Business Registers to group companies owned by the same shareholders into broader conglomerates. Finally, informal discussions took place with individuals at Dudelange City Hall involved in planning and policy decisions, at the Land Registry in charge of land measurements in Dudelange, as well as with local stakeholders with extensive knowledge of real estate actors in the city to truth-check our findings.

The shift to a landlord developer regime in Dudelange and its consequences

Housing producers: From local to national-level developers

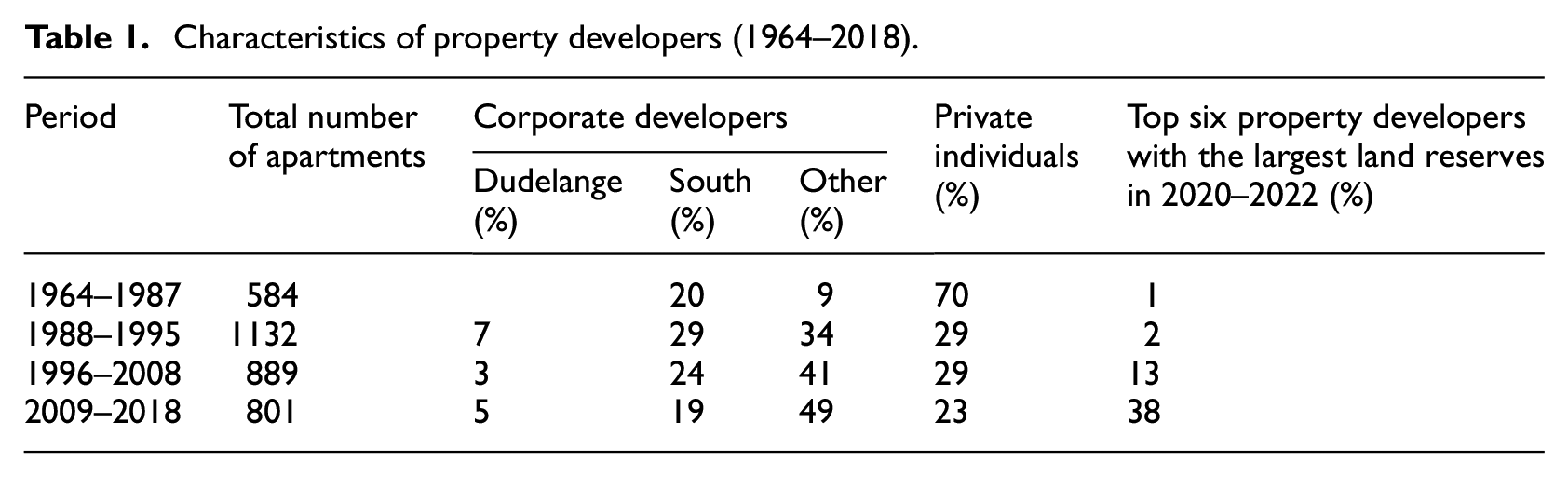

This section traces the way in which the landlord developer regime was imported into Dudelange by national-scale property developers in the early 2000s. To understand this process, it is necessary to start with the massive development of new apartment buildings that took place in the city between 1988 and 1995. During that period, 1132 apartments were built, close to twice as many as between 1964 and 1987 (see Table 1). This construction boom occurred at the same time as a similar increase in new-build activity in the nearby city of Esch-sur-Alzette, and 15 years after a similar spike in new construction in the capital. Both Dudelange (1981) and Esch-sur-Alzette (1976) had recently been connected to the capital city via new highways, and this offered an opportunity for developers to attract to these southern cities the aspiring homeowners who were starting to be priced out of Luxembourg City. In Dudelange, this was made possible by historically lax building regulations, which contained theoretically allowable densities far above what had been constructed in the city in the preceding decades (and contained a number of loopholes, such as the ability to build multifamily housing in gardens or car parks at the centre of fully urbanised blocks). As shown in Table 1, the construction boom involved a professionalisation of property development, as the share of apartments built by private individuals fell from 70% to 29% of all apartments.

Characteristics of property developers (1964–2018).

This period of intensive building in the south of the country occurred off the back of very rapid property price increases in Luxembourg, where real house prices almost doubled between 1985 and 1992. It had three characteristics:

Developers acquired land in Dudelange during the construction boom cheaply: for the 35 largest projects built in the period, the purchase of the land accounted for an average of 8.5% of the total sales price of the flats. In 15 of those projects, the price paid for the land was recouped with the sale of a single apartment, and in 11 others by the sale of two apartments. This seems to be because land sales occurred in a period of uncertainty concerning Dudelange’s economic situation following the closure of its steel factory, a driver of the city’s economy since its opening a century earlier.

To capitalise on increasing prices, local developers in Dudelange built very quickly: the first sale of an apartment occurred on average 324 days after the land purchase in the 35 largest projects during the construction boom (totalling 569 apartments), with just under half (17 out of 35) completing this process in less than 200 days. This involved applying for and receiving a building permit, marketing the property, identifying a buyer and completing all sale-related administrative steps (including the official signing of the deed in front of a notary).

To maximise the number of units built in that period, developers seem to have drawn heavily on loans from financial institutions. In 1990 and 1991, 17% of all residential loans in Luxembourg went to property developers, the highest since the beginning of the data in 1976, at a time in which interest rates were very high (8.25% in 1990 and 1991). For comparison, this proportion is around 9% on average between 2012 and 2022, in a context of significantly lower interest rates.

This building activity came to a halt as the impacts of the global recession in the early 1990s hit Luxembourg. With large loans to repay and construction projects slowing down – in Dudelange, the building code was tightened in 19921 as the city was unable to keep up with the public equipment and infrastructure needed for the rapidly increasing population – many of the largest developers active in Dudelange during the construction boom went bankrupt in the late 1990s and early 2000s.

The return of house price growth in the early 2000s, which coincided with the strengthening of fiscal incentives for property investors, thus took place as the property development sector was reconfiguring. As shown in Table 1, the percentage of flats in Dudelange built by local developers (including those from other areas in the south of the country) has steadily decreased over time. This is due to a growing interest in Dudelange from large developers operating at the national level. In Luxembourg, the last 20 years have seen a process of concentration in the property development sector linked to the difficult access to residential land. While this access has always been difficult, rapidly increasing house prices in the last decades have reinforced longstanding mechanisms of intra-familial land transfers (Schifano and Paccoud, 2024). Over the years, five property developers have managed to accumulate significant residential land reserves: Arend & Fischbach (founded in 1989), Giorgetti (1898), Tracol (2006), Promobe (1991) and Stugalux (1973). Together, these five developers owned 37.3% of all residential land in company hands in Luxembourg in 2020–2022 (ODH, 2023a), at an estimated value of close to €2.5 billion. These five developers are Luxembourg based, with only one foreign developer – Thomas & Piron – able to acquire significant land reserves since its arrival in the Luxembourg market in 1990.

As shown in Table 1, these six large developers produced 38% of the flats in Dudelange in the last period, especially through the development of large flagship projects supported by the municipality. Emblematic of these flagship projects is the largest residential development completed in the city in the last decade, made possible by a joint venture between one of the five largest developers in the country and a local ‘land promoter’ (Shepherd et al., 2024) active in the city since the early 1990s. The project, whose planning was led by the municipality, incorporated land acquisitions made earlier by the local land promoter and was made possible by the sale of municipally owned land.

The construction boom orchestrated by smaller, local developers thus seems to have put Dudelange on the map for national-level developers who brought to the city a different housing production model through large flagship projects supported by the municipal administration. The share of residential bank lending going to developers dropped after the construction boom, and has averaged 8% since 1996. This source of funding seems to have been replaced by pre-financing from sales to property investors. As per information obtained by crossing property registers with Dudelange population registers, in the largest 15 apartment buildings constructed in Dudelange since 2010, only 129 out of the 282 units are currently occupied by their owner (45.7% 2 ). This contrasts with an overall homeownership rate of 73% in Dudelange (as per the 2011 population census). This signals the extent to which this recent production is targeted towards property investors in Luxembourg, a tendency also found in France (Pollard, 2023). Property developer reliance on investors is clearly brought to light in an interview with the CEO of Giorgetti, one of the largest developers in the country. This is his reaction to measures introduced recently to limit tax advantages for investors: ‘The state has erred in complicating property investments. If these are less attractive, there will be fewer investors. And if there are fewer investors, there are fewer new housing units’. 3

Schematically, the construction boom can thus be seen as a reinjection of capital into deindustrialising Dudelange (to close a rent gap created by its proximity to the nascent financial centre), while the shift to a landlord developer regime under the impetus of national-level developers signals an attempt to close the value gap through sales to fiscally stimulated property investors. While the construction boom happened without much municipal interference, the shift to the landlord developer regime was facilitated by flagship projects supported by the city. As will be shown in the next section, this shift to a landlord developer regime has brought about an important upscaling of new apartment buyers in Dudelange, with knock-on effects on the flats built during the construction boom.

Housing consumers: Professionalisation, property investment and cross-border displacement

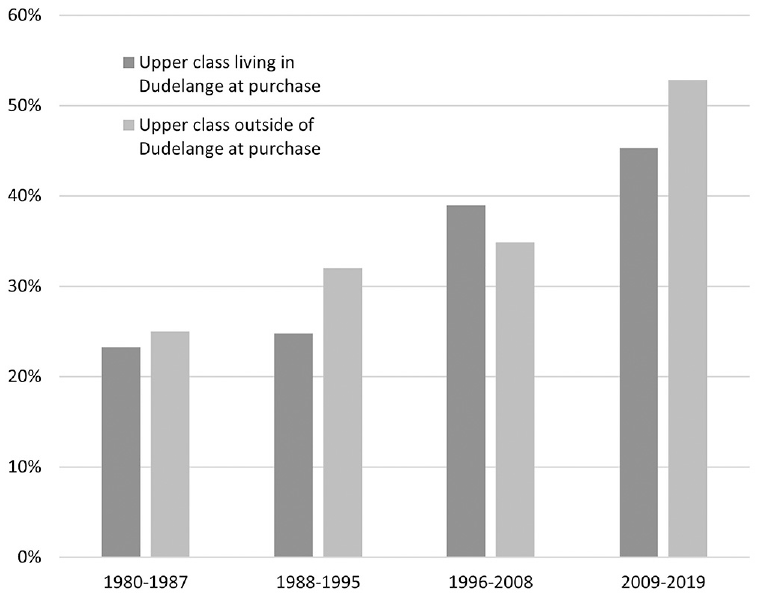

As an echo to the frenetic activity of small-scale developers in Dudelange, the construction boom put Dudelange on the map of aspiring homeowners across Luxembourg: in the 1980–1987 period, the share of buyers indicating a residential address in Dudelange stood at 67.1%, a share that fell to 54.9% during the construction boom (1988–1995) and that has remained just above 50% since then. The upsurge in buyers living in the capital city is particularly remarkable: while they made up 7.3% of buyers in Dudelange in the 1980–1987 period, this share doubles to 14.3% during the construction boom. Figure 2 shows that the construction boom (1988–1995) also seems to have made Dudelange attractive to a larger number of outside buyers with upper-class occupations. In the subsequent periods, there is a generalised upscaling of buyers of newly built flats: most pronounced after the construction boom for buyers living in Dudelange (with those with upper-class occupation increasing from 25% to 39% between the second and third periods), and more recently for buyers living elsewhere at the moment of purchase (from 35% to 53% between the third and fourth periods).

Place of residence of upper-class apartment buyers at time of purchase.

By placing Dudelange on the map, the construction boom created a demand at the national level for newly built apartments in the city. Given the limits placed on the number of new units by the 1992 building code, this created a growing competition for housing in the city that spilled over into existing apartments: while 29% of all apartment buyers in Dudelange in the 1990s were upper class, from the 2000s onwards the upper class represent 40% of the buyers of flats built during the construction boom. The continued professionalisation of buyers of newly built flats over the last two decades has thus put pressure on the existing stock, and notably on the ageing apartments of the construction boom period that are still in high demand in the context of reduced building activity in the city.

As fiscal incentives for property investors were scaled up from 2002 onwards, demand for apartments in Dudelange further increased. Multiple-property owners (individuals who owned more than one property in Luxembourg at the moment of the analysis) are today important owners of apartments in the city, both of new and of older properties. They make up 53% of the owners of apartments in residences with more than 10 flats newly built between 2012 and 2018 (Mezaroş and Paccoud, 2024), and 42% of the current owners of apartments built during the construction boom. The timing and motivations of investors in newly built flats have been documented in Mezaroş and Paccoud (2024)– these are individuals over the age of 45 born in Luxembourg, with mainly upper-class professions (55% of those for whom a profession is available in the notarial deeds). Here we focus on the characteristics of multiple-property owners in older buildings. These rely on another set of tax advantages, which allow the deduction of a wide range of acquisition and running costs from their tax declarations. This includes interest payments, local taxes, costs linked to building management and upkeep, as well as insurance – all of this on top of the possible deduction of 2% of acquisition costs.

There are currently 185 multiple-property owners with at least one apartment built during the construction boom in Dudelange. Collectively, they own 78 houses, 514 apartments, 41 buildable land plots and 245 hectares of land across Luxembourg. Among these 185 multiple-property owners, 115 purchased one or more construction boom-era apartments after 1995, a sign that these flats were specifically targeted as investments. 4 The vast majority of these investors were over 45 years of age (94 out of 115), and close to half over 60 years of age (56 out of 115). Among those with a profession recorded in the notarial deeds (106 out of 115), 52% have upper-class occupations. There were slightly more purchases since 2009 (63) than there were between the construction boom and 2008 (52), showing a sustained interest from property investors for ageing apartments in Dudelange. This explains the increasing professionalisation of apartment buyers in the city, who are competing against investors – both in new and existing buildings – with significant housing portfolios.

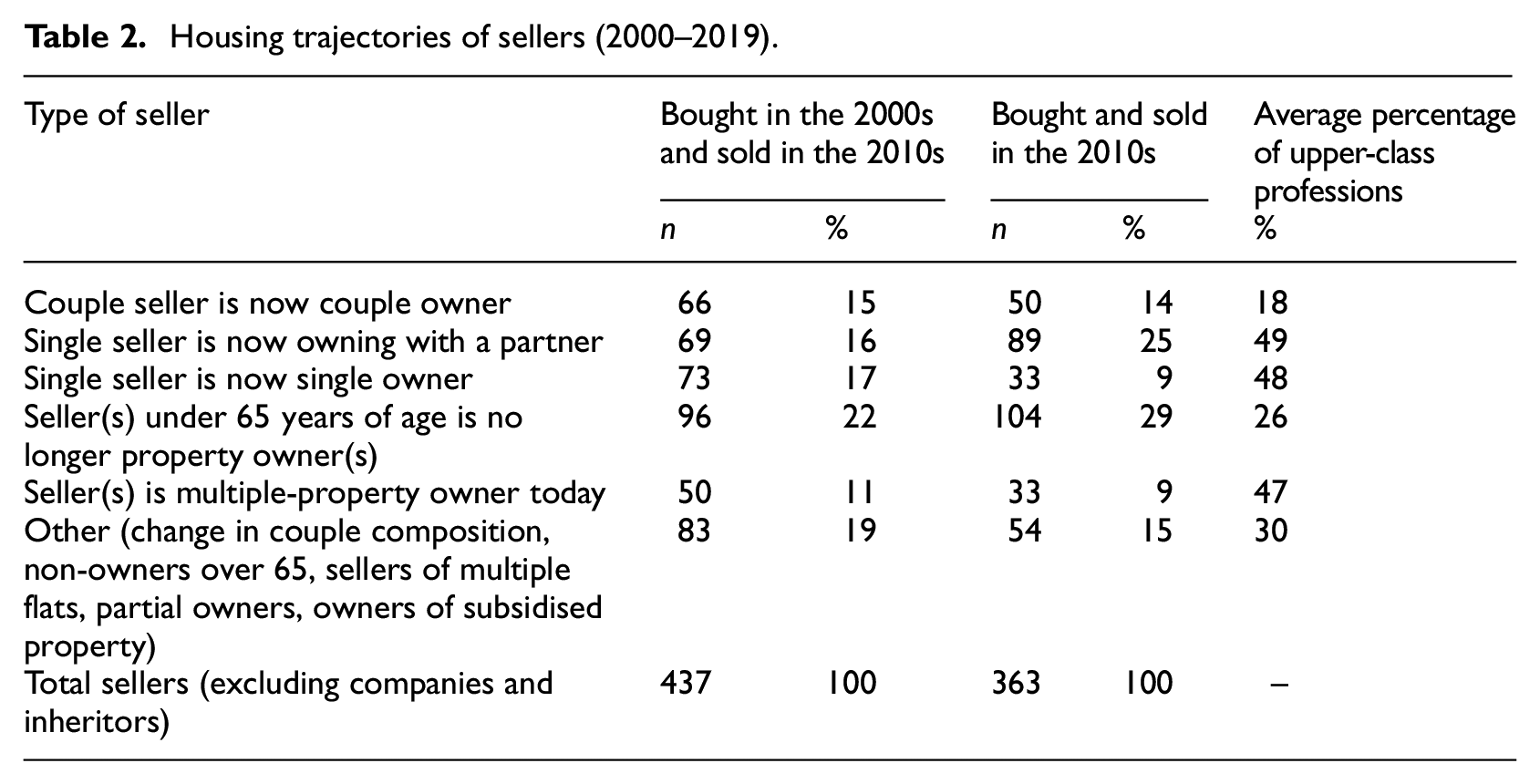

The increased competition on the Dudelange housing market in the last two decades seems to have impacted the residential trajectories of apartment owners in the city. Table 2 shows the current property situation in Luxembourg of households who sold their Dudelange apartments in the 2010s. We distinguish between two cohorts – those who bought their apartment in the 2000s and those who bought it in the 2010s – to account for the impacts of the deepening of the landlord developer regime between these two periods.

Housing trajectories of sellers (2000–2019).

The results indicate important disparities between households in their ability to remain property owners in Luxembourg after selling their Dudelange property: 22% of those who bought their Dudelange apartment in the 2000s no longer own any property in Luxembourg today, a figure that increases to 29% for those who bought their flat in the 2010s. 5 The vast majority of those who still own property in Luxembourg (and who are not multiple-property owners today) have remained close to Dudelange: 61% of the sellers who currently own property in Luxembourg own a house in the southern region and 20% an apartment in the southern region. Only 3% of them are now owners of a house or apartment in the municipalities surrounding the capital city. In the landlord developer gentrification regime currently operating in Dudelange, those who do not have upper-class professions are increasingly facing constrained residential careers, and there is little evidence that they are able to act as savvy investors (Cook and Ruming, 2021).

The figures also show that couple formation appears to be an increasingly important component of upward residential trajectories in Luxembourg. The number of those who now own as a couple, after being either single or couple sellers, increased from 31% to 39% between the two time periods. Moreover, sellers who purchased their first Dudelange apartment by themselves are much more likely to still be property owners in Luxembourg today if their next purchase was with a partner. Indeed, while there is roughly the same share of single owners who bought in the 2000s who are currently owning alone (17%) or with a spouse (16%), among those who bought more recently single sellers who purchased with a partner (25%) largely outnumber those who bought their next flat alone (9%). The occupations of the individuals in Table 2 also show that, for both cohorts of buyers, the percentage of the upper class among those who are owners today is lower for those who were couple sellers (18%) as compared to those who were single sellers (48%/49%). This seems to suggest that buying and selling as a couple has been a way for those without upper-class professions to remain homeowners in Dudelange. This effect seems to be weakening, however, as shown by data not included in Table 2: among those sellers under 65 years of age who are no longer property owners in Luxembourg, the share of couple owners has increased from 35% to 53% from the first cohort of buyers to the second. These results show that the Luxembourg housing market has become more difficult to navigate over the course of the last two decades, especially for those who remain single buyers but also increasingly for couples.

While the evidence here does not make it possible to know where the currently property-less went, their characteristics point to a possible displacement over the border into neighbouring France, Germany or Belgium, where housing is more affordable. Indeed, among the 200 Dudelange apartment owners under 65 years of age who sold and are no longer owners of property in Luxembourg, 51% were born in Luxembourg (mostly in the Southern region), 31% in Portugal (the origin country of the largest migrant group in Luxembourg), 8% in areas close to the Luxembourg border and only 12% in other places. Only 26% of them have upper-class occupations (Table 2). These characteristics match those of the so-called ‘atypical cross-border workers’ visible in administrative datasets: cross-border workers who have nationalities other than those of the three countries surrounding Luxembourg (France, Germany and Belgium) – that is, people who keep their job in Luxembourg once they move to a neighbouring country. Their number has rapidly increased: they made up 18.1% of all cross-border workers in 2022, as compared to 8.7% in 2012. In 2022, this included 13,700 Luxembourg nationals and 10,300 Portuguese nationals. For those who are alone or who cannot afford prices in the south of Luxembourg, crossing the border is a way to buy the same property for half the price while keeping their employment in the country, a phenomenon that can be conceptualised as a form of exclusionary (cross-border) displacement.

Discussion and conclusions

In this article, we propose the concept of a ‘gentrification regime’ as a way to understand the locally and temporally specific unfolding of socio-spatial change. This concept foregrounds the process through which producers and consumers of housing solidify their interactions around a specific type of gentrified property, and how this depends on, and responds to, changes in policies and financial instruments. We believe this notion is better able to capture the diversity of gentrification trajectories than the more macro-level models of gentrification ‘waves’ or ‘stages’. To show how this concept can operate in practice, we provide evidence that gentrification in Dudelange was set in motion as a by-product of the shift to a landlord developer regime at the national level. In the 1990s, local developers drew on debt financing and relatively easy access to land to build more, and more quickly, than in any other period of the city’s history. The construction boom put Dudelange on the map of those priced out of the capital. The economic downturn and the tightening of building regulations reconfigured the property development landscape, with national-level developers progressively replacing bankrupted local developers. Through municipally supported flagship projects, these national developers have brought to Dudelange a new gentrification regime centred on investor demand, itself stimulated by national fiscal policies. The sale of new flats predominantly to investors has gone hand in hand with investor interest in older buildings, including those built during the construction boom. The competition for housing between owner-occupiers and investors has created a generalised professionalisation of apartment buyers in the city. In such a regime, increasing housing supply does not mechanically dampen gentrification: the attraction of property investors to formerly divested areas upsets the social balance and puts exclusionary pressure on those unable to keep up.

This article thus shows that national-level fiscal policy can have concrete impacts on local housing markets by spreading gentrification dynamics to new areas. This is particularly visible in Luxembourg given the generosity of tax deductions for investors in both new and existing units, but it is likely to contribute to shifts in the landlord developer regime elsewhere. The value gap that underlies the shift from an occupier or professional developer regime to a landlord developer regime can thus have multiple origins: the deregulation of the private rental sector, fiscal policy incentivising (private individual) property investors and perhaps particular incentive structures favouring institutional investors. The identification of value gaps linked to the development of private renting in its multiple forms can thus serve to bring together disparate threads in the gentrification literature, such as work focusing on buy-to-let gentrification, the various instantiations of build-to-rent and gentrification linked to the accelerated temporality of renting. Given the importance of locally supported flagship projects for the spread of the landlord gentrification regime in Dudelange, the potentially mediating role of local planning mechanisms and city-level decision making is important to keep in mind: local decisions could potentially inhibit or exacerbate the gentrification potential of national-level policy change. While our focus here has been on the shift in both the type of producer and the type of consumer of housing in Dudelange following national fiscal policy changes, the notion of a gentrification regime offers the flexibility to study – for local socio-spatial change – the type of collaborative and shared agency at the heart of Stone’s urban regime.

The consequences of the landlord developer gentrification regime for tenants have been well documented elsewhere. Here, we provide evidence that this gentrification regime also affects the prospects of those who own their main residence. In Dudelange, very few apartment owners were able to exit the southern region once they had sold their apartment in the city. We also find that a significant proportion of former apartment owners in the city no longer own any property in the country today. It is possible that some of these have crossed the border to acquire more living space, although our interpretations are limited by the lack of information on their residential trajectory outside of Luxembourg. We frame this potential phenomenon, which seems to affect apartment owners without upper-class professions, as the (cross-border) exclusionary displacement of property owners, a group whose experience of gentrification is seldom discussed. This could explain the rise of atypical cross-border workers – those who keep their employment in Luxembourg once they leave for a neighbouring country. Despite not being ‘forced’ to move, voluntary departure can be considered to be (exclusionary) displacement if the in-movers have wealthier profiles (Davidson and Lees, 2010; Lees, 1996). While the reasons behind selling and moving out of an area may depend on individual circumstances, the inability to remain a homeowner when trying to purchase larger housing (Phillips et al., 2020) or in the context of council estate renewal (Cooper et al., 2020) points to a similar dynamic. This phenomenon complicates the purported link between owning property and stability and wealth: in the array of real estate actors such as landowners, developers or investors, those who own only the home they live in are nearer the bottom of the pyramid than the top.

Future research should thus widen the scope of gentrification, and displacement in particular, to all those suffering from the effects of property wealth inequalities, including owner-occupiers. More work is also needed on the ways in which Luxembourg impacts the housing markets of neighbouring countries, such as through the cross-border displacement of those who leave the country to buy property in France, Germany or Belgium that in turn makes housing more expensive for current residents in these border areas. It is possible to frame this as gentrification operating at the national level, with those unable to keep up with property prices spilling over into neighbouring countries and further spreading gentrification in the areas across the border. From the perspective of receiving places, this can be seen as another instantiation of transnational gentrification, except that the gentrifiers come from just across the border rather than from more distant places. This process might be better captured by the term ‘cross-border gentrification’.

Footnotes

Acknowledgements

We would like to thank the editor and the three anonymous reviewers for their insightful feedback throughout the publication process. Additionally, we would like to express our appreciation to the Administration du Cadastre et de la Topographie for its continuous support since the beginning of this project, and to Tiago Ferreira Flores and Karolina Zieba-Kulawik for their research assistance.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Luxembourg National Research Fund, project numbers: C18/SC/12690935/TER_INEQ/Paccoud (Territorial inequality: A study of the local mechanisms implicated in long run changes in property wealth concentration) and AFR 14538172 (GentriLux – Gentrification in Luxembourg: Linking social changes to property wealth inequalities).