Abstract

This article uses three cities in the same Canadian province (Ontario): Toronto, Ottawa and Waterloo, to examine how regions compete in high-technology markets. We find that regions use civic capital to leverage new, technological windows of opportunity, but they do so in very different ways. Tracing Toronto’s evolution from a marketing hub for foreign multinationals into a centre for entrepreneurship, we illustrate how weak ties and cross-sectoral buzz created a ‘super connector’, scaling high-technology firms in a wide variety of areas. In Ottawa, task-specific cooperation in R&D, education and specialised infrastructure enabled the region to overcome the disadvantages of its small size as a ‘specialist’ in a single, capital-intensive niche, telecommunications equipment. Finally, entrepreneurs in Waterloo eschewed task-specific cooperation for peer-to-peer mentoring. By diffusing generic knowledge about how to circumvent the liabilities of smallness, mentoring networks enabled this ‘scrapper’ city to support smaller start-ups in a broad range of niches.

The digital transformation is frequently depicted as a threat to latecomers and laggards. Firm-level economies of scale in the accumulation of intellectual property and data as well as regional agglomeration effects have created a winner-takes-all economy, divided between superstar cities on the one hand and left-behind places on the other (Kemeny and Storper, 2020; Zukin, 2021). And yet, despite these formidable obstacles, several historically low- and medium-technology regions have successfully navigated these disruptive developments, repositioning themselves within new digital markets. Focusing on Canada as a least-likely case of high-technology competition, we apply the concept of ‘civic capital’ (Nelles and Wolfe, 2022) to an examination of longitudinal and cross-regional variation between Toronto, Ottawa and Waterloo to illustrate how communities can use these ties to respond to technological disruption and exploit new opportunities.

Significantly, we expand on previous applications of the concept of civic capital to argue that it can support high-technology entrepreneurship in three different ways: facilitating cross-sectoral cooperation; constructing specialised, strategic goods; or diffusing general knowledge within decentralised mentoring networks. In Toronto, civic capital connected high-technology entrepreneurs to a variety of deep, globally competitive sectors, particularly financial services, creating a ‘sector connector’ with a diverse and growing community of successful start-ups and scale-ups. Without the advantages of a global city, Ottawa and Waterloo followed a niche-based path, but did so in very different ways. Ottawa relied on the construction of task-specific collective institutions and programmes to support its position as a ‘specialist’, upgrading its position in telecommunications equipment and moving into adjacent software-related fields. Waterloo, a ‘scrapper’, used mentoring networks to support small- and medium-sized enterprises across a wide variety of industrial sectors. Collectively, the analysis suggests that smaller urban regions can enter high-technology markets in different ways, each with distinct trade-offs.

Civic capital and high-technology competition

The shift to cloud computing, data analytics, mobile computing and artificial intelligence in the 2000s created new opportunities for urban regions with robust capabilities in software development. Yet not all urban regions, even those with excellent universities, navigated these shifts successfully. The app revolution which powered the growth of Toronto’s ICT sector (Denney et al., 2021) disrupted Waterloo and Ottawa, triggering the collapse of Waterloo’s largest technology firm, Research in Motion (now Blackberry), and exposing Ottawa’s vulnerabilities as a hardware-focused innovation centre in a software-dominated world (Ornston and Camargo, 2022).

A growing literature attributes the varying capacity of urban regions to respond to these opportunities and challenges to the presence of civic capital (Nelles and Wolfe, 2022; Safford, 2009; Storper et al., 2015). Civic capital offers a more nuanced approach to some of the broader concepts found in the literature, particularly quality of government, institutions and place leadership, usefully bridging gaps in both institution-centric and social capital approaches (Beer et al., 2019; Farole et al., 2011). Civic capital, as defined in the recent literature, is comprised of formal or informal networks between individuals and associations, grounded in a specific region or locality that sustains a common vision for the community. Civic capital is generated through a range of organisations, whose members collaborate to develop new relationships and establish common goals for the economic development of the urban region (Nelles and Wolfe, 2022: 8).

It is thus a constructive explanatory variable for analysing collaboration at the urban scale – including the degree of political willingness to cooperate based on a shared identity, set of goals or expectations. The concept provides a novel way to theorise collective action dilemmas and their resolution through collaborative processes. Civic capital is grounded in the analysis of ‘governance’ arrangements at the urban level – but provides an actor-centric perspective that focuses on the role of agency by civic actors and associations in promoting new patterns of economic development at the regional and local level (Beer et al., 2019). This article builds on these recent contributions to the literature by arguing that civic capital can take different forms in different urban contexts and perform several different functions.

The relationship between civic capital and high-technology competition has received particular attention in larger metropolitan regions. With deep capital pools and labour markets as well as a large stable of complementary, supporting industries, their diversity facilitates innovation, whether through serendipitous street-level interactions or broader patterns of cross-sectoral ‘buzz’ (Storper and Venables, 2004; Zukin, 2021). This diversity, however, can lead to fragmentation (Fritsch, 2003), as evidenced by the disappointing performance of cities with low levels of civic capital such as Los Angeles (Storper et al., 2015). And as Safford cogently argues, cities with certain kinds of networks may fail to generate the requisite levels of civic capital to support economic adjustment to external shocks (Safford, 2009). By contrast, high levels of civic capital enable certain big cities to exploit sectoral diversity. For example, civic capital enabled entrepreneurs in Silicon Valley to combine engineering, the arts, biology and finance in ways that their counterparts in Los Angeles could not (Storper et al., 2015: 177).

Smaller cities cannot expect to leverage this type of cross-sectoral buzz, prompting many to associate high-technology markets with larger, metropolitan areas (Caragliu et al., 2016; Duranton and Puga, 2000). Despite these disadvantages, a number of smaller cities such as Aalborg, Denmark and Salo, Finland have entered cutting-edge high-technology markets. We argue that they have done so by using civic capital in a different way, relying on task-specific, inter-firm cooperation to develop and diffuse deep knowledge within regional supply chains and collaborate in the construction of specialised public goods, including R&D consortia, training programmes, technological standards and other infrastructure (Dalum et al., 2005; Farole et al., 2011; Sabel, 1993). More commonly associated with mature industrial cities and regions (Todtling and Trippl, 2004), we argue that this ‘organizationally thick and specialized’ model (Trippl et al., 2018: 69) can also facilitate entry into high-technology markets.

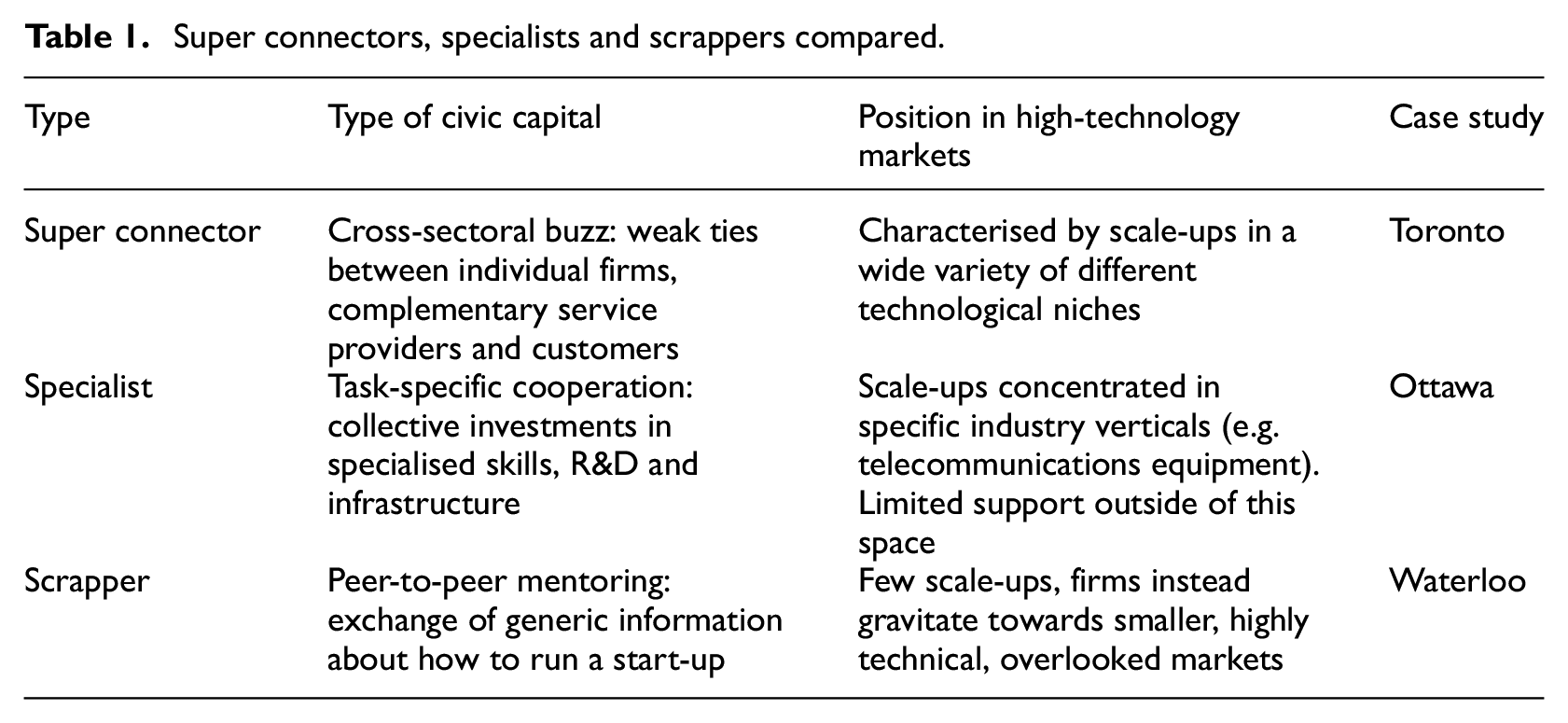

While this common distinction between large ‘diversified’ cities and smaller ‘specialists’ (Duranton and Puga, 2000) illustrates how civic capital can play different roles at different scales, it does not explain how smaller cities such as Cambridge in the UK (Garnsey and Heffernan, 2005) or Waterloo in Canada carved out competitive positions in high-technology markets without specialising in a particular industry. We argue that this reflects a different pattern of collective action, characterised neither by cross-sectoral buzz nor by task-specific cooperation but rather by the diffusion of generic knowledge within mentoring networks. While general, this form of civic capital can be useful for smaller regions, alerting entrepreneurs to unexpected opportunities in high-technology markets and helping them to navigate the unique challenges associated with capital scarcity, thin labour markets and the relative dearth of complementary industries (Ornston, 2021). Instead of specialising in a single sector, the most successful firms, whether guided by mentoring networks or by trial and error, are more likely to settle into small, overlooked niches in a wide variety of different areas. The sheer volume of independent niches, connected only by mentoring networks, can render ‘scrapper’ cities highly resilient. In contrast to larger ‘sector connectors’ and ‘specialists’, however, this diversified approach makes it harder to scale specific industries and firms (see Table 1).

Super connectors, specialists and scrappers compared.

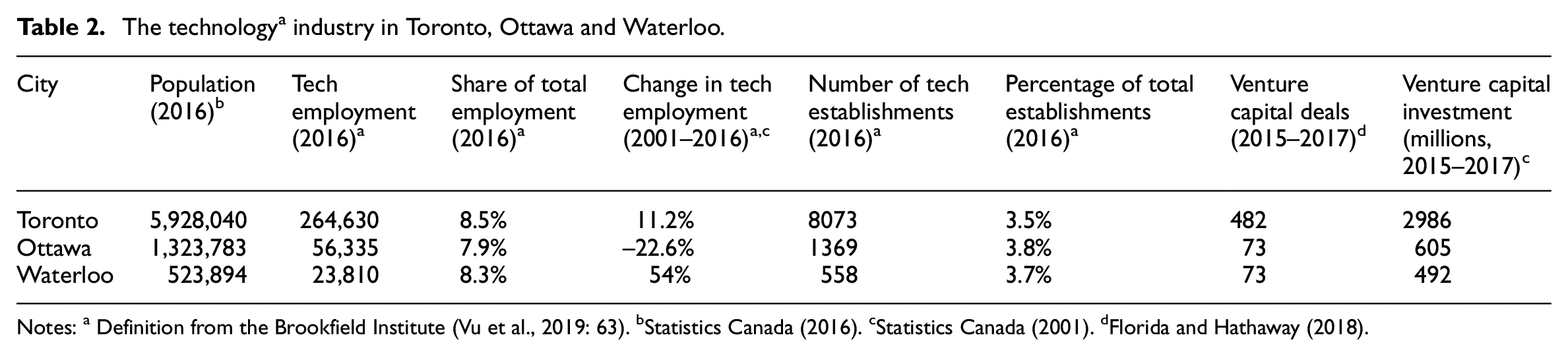

To investigate these claims, the article compares three Canadian cities, Toronto, Ottawa and Waterloo, all located in the same province, Ontario. The focus on Canada is deliberate as its laissez-faire national and provincial policies enable us to better disentangle the impact of civic capital relative to national- or provincial-level dynamics, while its status as a latecomer to high-technology markets (excepting Ottawa) increases longitudinal variation relative to long-established US tech clusters such as Boston or Silicon Valley. 1 High-technology entrepreneurship was a new development in Waterloo in the 1980s (Nelles et al., 2005), and the even more recent proliferation of start-ups in Toronto marked a break from its historic position as a sales and marketing site for multinational technology firms (Denney et al., 2021). In Ottawa, which historically benefitted from being co-located with several critical federal laboratories, we use the breakdown of associational governance to illustrate what happens when civic capital declines. Table 2 provides some summary statistics on the technology sector in these three cities.

The technology a industry in Toronto, Ottawa and Waterloo.

Notes: a Definition from the Brookfield Institute (Vu et al., 2019: 63). b Statistics Canada (2016). c Statistics Canada (2001). d Florida and Hathaway (2018).

To assess the role of civic capital, the article draws on 211 semi-structured interviews with policymakers (n = 24), industry observers (n = 15) and industry representatives (n = 172) in Toronto (T, n = 104), Ottawa (O, n = 56) and Waterloo (W, n = 51) from 2016 and 2022, the majority of which were conducted before 2020. Interview subjects, which extend from former founders from the 1970s to contemporary entrepreneurs to maximise longitudinal variation, were selected using secondary literature, newspaper reports and websites as well as subsequent snowball sampling. 2 We used responses to a sequence of open-ended and non-leading questions about regional strengths and weaknesses to investigate the level and type of civic capital. Specifically, we employed a qualitative analysis of the 211 interviews above to identify the history and activities of the key collaborative organisations in each city, as well as a thematic analysis to probe the degree to which the presence (or absence) of cross-sectoral interactions, specialised infrastructure and peer-to-peer mentoring supported or inhibited high-technology competition. 3 To address selection bias, all of the interview data presented in this article were triangulated with peer-reviewed academic literature, journalistic publications and organisational websites.

Toronto: Using civic capital to create cross-sectoral buzz

Toronto’s economy is the largest in Canada and it used civic capital to build the most diverse technology sector considered here. One analysis observed that ‘the Toronto region has become the country’s preeminent metropolis, its dominant economic engine as well as innovation milieu, as well as its principal gateway to the rest of the world’ (Bourne et al., 2011: 236). The leading sectors in Toronto’s economy are concentrated in the knowledge- and design-intensive sectors around business and financial services, some core manufacturing sectors, including automotive and computers, the biopharmaceutical and biotechnology sectors, as well as the cultural, creative and design-intensive sectors. Since the mid-2000s, Toronto has ranked as one of the largest technology clusters in North America, after the San Francisco Bay Area and New York (Bramwell and Wolfe, 2016).

Toronto’s status as a global hub for high-technology entrepreneurship is predicated on a dense pool of talented and highly skilled labour (Denney et al., 2021), including the city’s status as a magnet for inward migration, absorbing almost 40% of all immigrants to Canada and with foreign-born residents accounting for more than 50% of the region’s population (Statistics Canada, 2016). Our interviewees consistently pointed to the depth of talent in the region as one of its strongest assets (e.g. interviews T1, T2, T3 and T4; see also Denney et al., 2021). For decades, however, the high-technology enterprises best positioned to capitalise on these assets were multinational subsidiaries in information and telecommunications hardware rather than domestic start-ups (Britton, 2004; Creutzberg, 2006). These investments transformed Toronto into one of the three major geographic concentrations of ICT firms in the province of Ontario (Wolfe, 2002). The bulk of employment in Toronto’s ICT firms prior to 2000 was thus based in the subsidiaries of foreign, primarily US, MNEs (Denney et al., 2021).

There were important exceptions, such as locally owned Delrina and Workbrain, that paved the way for the next generation of successful entrepreneurs (Yunusov, 2017), but pre-2000 Toronto provides an excellent example of how the greatest barrier to high-technology entrepreneurship in large, urban agglomerations is ‘fragmentation’ (Fritsch, 2003). A Waterloo-based interviewee, after commenting approvingly about the depth of talent in Toronto, noted, ‘In Toronto you see segregated communities. You don’t see mixtures. For us to say we’re in Kitchener, not Waterloo, we don’t do that. But they make those geographic distinctions in Toronto’ (interview W1). A few short-lived attempts to create Toronto technology cluster organisations prior to 2000 either failed or were absorbed into larger national organisations and lost their capacity to represent the local cluster (interview T5). For older entrepreneurs, the well-documented absence of an entrepreneurial start-up culture (Lucas et al., 2009) did not preclude development, but certainly constituted a challenge (interview T6): ‘When I was starting my company, there was nothing. I was on my own. There was nobody to turn to. I knew no other entrepreneurs; I was making all the mistakes on my own’ (interview T3).

Consistent with the development of other high-technology clusters (Feldman et al., 2005), the emergence of a local high-technology industry was associated with the entrepreneur-led development of social connections through both formal and informal collaborative networks and organisations (interview T7; Denney et al., 2021). In addition to a profusion of incubators, accelerators and other intermediaries, Toronto has benefitted from boundary-spanning organisations, beginning with BarCamp meet-ups organised by entrepreneur David Crow as a catalyst in the self-organisation of Toronto’s technology community between 2005 and 2015. These efforts resulted in the creation of a ‘positive feedback loop and reward cycle for people that would come out of the basements and the small offices, share what they were working on, and get to know each other … it was revolutionary’ (Yunusov, 2017). In 2014, local entrepreneurs Alex Norman and Jason Goldlist founded TechToronto, a networking organisation which runs monthly meet-ups of over 500 people (during which its Twitter hashtag #TechTO trends nationally) (interview T7). It has grown to 8500 members and has drawn sponsorship from larger private-sector firms and local government (RBC, 2016). Interviewees cited TechToronto as emblematic of a larger ‘tech community in Toronto [that] has flourished over the last six or seven years’ (interview T8). In the words of the former entrepreneur above: What’s changed in the last 15 years, is this incredible support network has popped up … There is so much more here than there was even 10 years ago. It’s changed the trajectory of entrepreneurship just based on the supports that exists [and] the community that exists around that, I think if I were doing it now, I would not be the only entrepreneur that I knew. I would have another CEO to reach out to and talk to … So that’s the biggest [change]. (interview T3)

TechToronto does not support or even broker the kinds of specialised infrastructure which characterise its Ottawa equivalents, Invest Ottawa and the Kanata North Business Investment Area. Nor does it support the extensive and structured mentoring that underpins Waterloo, although its meet-ups certainly foster individual-level interactions. Rather, TechToronto is distinctive in its ability to link technology firms to complementary services, most notably investment, as well as local, advanced demand through the development of industry-specific meetings corresponding to existing local verticals such as FinTechTO, HealthTechTO and SalesTO. 4 This emphasis on cross-sectoral bridge-building extends to local ‘regional innovation centers’ (interviews W1, W2, T9, T10, T11 and T12; Bramwell et al., 2019). For example, the MaRS (Medical and Related Sciences) Discovery District excelled at connecting entrepreneurs to investors and advanced users in verticals such as financial services and medicine, but it struggled to develop a strong culture of peer-to-peer mentoring (Cicci et al., 2023).

Collectively, this cross-sectoral buzz has transformed the local landscape, fostering the emergence of new high-technology clusters such as fintech (Denney et al., 2021). The number of technology exits increased from fewer than 25 per year from 1995 to 2006 to over 125 per year in 2016–2018 (Denney et al., 2021: 203). While tech valuations continue to lag behind US technology clusters, the biggest challenge relative to Ottawa and Waterloo appears to be one of fragmentation, with some entrepreneurs finding the ecosystem hard to navigate (interviews W2, T13, T14, T15 and T16). 5 For those who can access the support networks above, however, the opportunities are substantial, offering an unparalleled depth of expertise in an exceptionally wide array of industries. This is evident in interviews not only with long-time Torontonians, but also with transplants, who were drawn to the region either to escape the narrow sectoral focus of Ottawa (interviews O1 and O2) or to leverage Toronto’s deep talent pool (interviews T2 and T4). The development of strong associational linkages that support civic capital has reinforced Toronto’s enviable position of combining scale and scope. Ottawa and Waterloo, as smaller communities, did not enjoy these benefits, but this did not preclude them from entering high-technology markets.

Ottawa: Using task-specific cooperation to achieve high-technology specialisation

During the second half of the 20th century, Ottawa was the exception that proved the rule of Canadian underperformance in high-technology markets, using civic capital to achieve scale in specific fields, most notably telecommunications equipment. During this period, the federal research laboratories in the region worked closely with local firms, most notably defence contractors, by funding private research, allowing lab access and spinning out firms. This collaborative environment, with strengths in telecommunications, attracted Northern Electric (Nortel) to move its research arm, subsequently Bell-Northern Research (BNR) after a merger with Bell Canada’s research facilities, to the Ottawa suburb of Kanata in 1962. By the 1970s, this laboratory had supplanted federal research labs as the key regional anchor. In addition to attracting thousands of researchers to Ottawa (Harrison et al., 2004: 1062), BNR served as a hub for dense, task-specific, inter-firm cooperation, with few parallels in Toronto or Waterloo.

For example, BNR partnered with local subcontractors, beginning with the establishment of a semiconductor manufacturing subsidiary, Microsystems International Ltd (MIL), in 1969. MIL would prove short-lived, but its employees would go on to launch more than 20 start-ups, including Calian, Mitel and MOSAID Technologies (Harrison et al., 2004). Nortel and Mitel were the two largest private-sector founders of the Canadian Microelectronics Corporation (CMC) in 1984, which conducted research on integrated chip design, trained engineering students in semiconductor design and diffused knowledge to the broader industry (Niosi and Bergeron, 1995: 54–55). The deep reservoir of civic capital in the region was institutionalised in the Ottawa-Carleton Research Institute (OCRI) in 1983. 6 Unlike the Atlas Group and Communitech in Waterloo, mentoring was not an area of focus (Spigel, 2017), perhaps in part due to the frictionless flow of information within the tight-knit telecommunications industry. OCRI’s initial title and subsequent rebranding as the Ottawa Center for Research and Innovation reflect the organisation’s laser-like focus on task-specific cooperation in research and human capital. OCRI, which boasted over 600 members by 2000, developed physical infrastructure such as a focused ion beam facility and also secured provincial support to expand specialised university engineering programmes and research (Julie, 2016; Niosi and Bergeron, 1995: 55).

Sector-specific cooperation in research, training and regional supply chains enabled Ottawa to do what few other Canadian cities could in the 20th century – carve out a competitive position in high-technology markets at a time when they were dominated by capital-intensive hardware industries with high barriers to entry. By the turn of the millennium, high-technology employment had surpassed federal employment for the first time in the city’s history (Harrison et al., 2004: 1048), the region ranked first in Canada in measures of technology employment and it led the country in venture capital investment (Florida and King, 2015). Ottawa, however, was very much a ‘telecom town’ (interview O3). Five of the region’s largest six firms by employment and six of the top 10 by revenue were in the telecommunications sector (PricewaterhouseCoopers, 1998). A software entrepreneur who left the city for Toronto commented: ‘Celtic House, like the big Ottawa guys, all they did was infrastructure … I wasted so much time talking to those guys. But all our founders did. And the angel groups were the same’ (interview O1).

As a result, the region proved vulnerable to the downturn in telecommunications markets at the turn of the millennium. Nortel reduced its headcount by two-thirds between 2001 and 2009 before declaring bankruptcy, while suppliers and spinouts were even harder hit (Spigel, 2011: 15). In contrast to Waterloo (Ornston and Camargo, 2022), anchor decline caused high-technology employment to shrink by 20.3% between 2001 and 2006 before hitting a new low in 2011 (Statistics Canada, 2001, 2006, 2011). Sectoral specialisation was exacerbated by the absence of Waterloo-style peer-to-peer mentoring (interviews O4, O5 and O6). Aspiring entrepreneurs in the 2000s were either forced to rely on industry veterans in telecommunications equipment or directed to a centralised question-and-answer service at OCRI which covered restaurants alongside software firms (Spigel, 2017: 301). As a result, and in contrast to Waterloo, several non-telecommunication-based entrepreneurs described how OCRI’s inaccessibility led them to either bootstrap their own development (interviews O5, O7 and O8) or leave the city (interviews O1 and O2).

Any effort to reallocate resources from Nortel was undermined by a crisis of associational governance (Ornston and Camargo, 2022). OCRI’s mandate became muddled when it merged with a local economic development agency in 2000. Increasing political interference resulted in the organisation ‘trying to be everything to everyone’ (interview O7), with the result that mayoral candidate Jim Watson actively campaigned against the organisation with comments like, ‘How many of you know what OCRI stands for, let alone what it does?’ (Kovessy, 2010). Nonetheless, it is unclear whether private leadership could have fared better, as the organisation haemorrhaged event and fee revenue and lost the ‘800-pound gorilla’ which gave OCRI its clout and focus (Julie, 2016: 17).

The eventual revitalisation of the Ottawa technology sector coincided with the reconstruction of its civic capital. Here, we observe two parallel but distinct processes of path creation. First, the Kanata North Business Investment Area recaptured OCRI’s tighter sectoral focus (Julie, 2016). This new form of civic capital, supported by a restructured and rebranded Invest Ottawa, has supported several new initiatives. Competing MNEs, Cisco, Juniper Networks and Nokia, have collaborated on the Center of Excellence for Next Generation Networks (CENGN), while ENCQOR, a 5G wireless testbed anchored by CGI, Ciena, Ericsson, IBM and Thales, followed shortly thereafter. In addition to tethering foreign firms in Ottawa, these projects created openings for smaller Canadian-owned firms to enter the telecommunications equipment value chain by contributing to software-defined networks or layering new applications on top of them (Haley et al., 2017).

These new applications reflect the region’s ability to apply its deep expertise at the interface of communications hardware and software to adjacent areas such as cybersecurity, the Internet of Things and autonomous vehicles (Haley et al., 2017). For example, when Waterloo’s flagship firm, RIM (renamed BlackBerry), pivoted to automotive software, it built its centre of gravity on its subsidiary in Ottawa, QNX. This reorientation was supported by dedicated infrastructure reminiscent of the specialised, private–public and inter-firm investments which characterised the Ottawa region in the past. For example, BlackBerry, alongside Ericsson, Nokia and Invest Ottawa, have contributed to the construction of Area XO, a test track for autonomous vehicles (Gorachinova and Wolfe, 2023).

The most dramatic move towards diversification, however, revolved not around the reconstruction of civic networks and incremental diversification in suburban Kanata, but rather around the independent, collaborative efforts of a new generation of software firms situated in downtown Ottawa (Spigel, 2017: 118). These downtown software entrepreneurs responded to OCRI’s deficiencies in the 2000s by establishing their own organisation, Fresh Founders (Ornston and Camargo, 2022). E-commerce giant Shopify’s role as an anchor within this community is less direct than was Nortel’s and the diverse network associated with Fresh Founders resembles Waterloo’s looser web of peer-to-peer mentoring relationships (see below). But Shopify executives have been more engaged than their counterparts at RIM in mentoring, launching incubators and making angel investments. This has created favourable conditions for entrepreneurs in and adjacent to e-commerce, but it may narrow the community’s focus. One entrepreneur, who found a more receptive audience in Toronto, remarked: [Ottawa] is very sector limited. We’re talking software, e-commerce, these things. So, there are people there [but] it depends on your company, right? I think for some companies, this is a fantastic place. [Names companies] had a great time, they were working with Shopify. They have an e-commerce security service that was perfect for them. That was amazing … [Names advisor, a Shopify employee] got bored very quickly of what we were doing, which was unfortunate. (Interview O2)

Ottawa’s ability to specialise and compete at scale in more than one high-technology sector indicates that the region’s capabilities are not limited to telecommunications equipment manufacturing and that specialists can outgrow dependence on a single industry. But Ottawa’s new bipolar structure still stands in contrast to Waterloo, which, despite its smaller size, has assumed a more diversified position in high-technology markets.

Waterloo: Peer-to-peer mentoring and scrappy start-ups

Unlike Toronto, the Waterloo region has long boasted a high level of civic capital, both at the industrial level and across the community (Leibovitz, 2003). The region’s inhabitants have been linked by a dense patchwork of churches, clubs, musical societies and other organisations since the late 19th century (Nelles et al., 2005: 233), as well as a culture of collaboration, most commonly expressed through references to Mennonite ‘barn raising’ (Bathelt and Spigel, 2019; Ornston, 2021). Historically, this deep reservoir of civic capital was applied to traditional industries (Munro and Bathelt, 2014: 221). This remained true even following the establishment of the University of Waterloo, as tech-oriented graduates migrated to US multinationals such as Microsoft (Ornston, 2021). One interviewee characterised 1990s Waterloo as: Essentially a Mennonite farming community. [We] had a wonderfully vibrant farming community and somewhat long-in-the-tooth textile and automotive assembly areas, as well as a fledging mathematics and actuarial area because of the insurance companies. And that was Waterloo. (Interview W3)

The entrepreneurial ecosystem which exists in Waterloo today can be traced back to the University of Waterloo professor Wes Graham, whose entrepreneurial activities inspired dozens of faculty spinoffs within a tight-knit academic community (Wolfe, 2009: 205). These informal interactions were organised into regularly scheduled meetings during the 1990s. At a standard event, a rotating host would present a 5–10-minute story followed by discussion and collective problem-solving (interview W4). In 1998, this ‘Atlas Group’ was institutionalised as Communitech, an official industry association with a president, permanent staff and 120 members (Pender, 2017). Although initially inspired by a visit to Ottawa and OCRI (interview W3), Communitech never pursued pre-competitive research consortia or sector-specific investments in human capital (Leibovitz, 2003). In the words of a Communitech veteran and long-time industry observer, ‘Just about the best thing we did at Communitech was move the focus away from [commercialization] towards expertise, EIRs [entrepreneurs in residence], mentors, and things like that’ (Will, 2017). 7 This absence of specialised public goods was mirrored by limited collaboration in innovation. In contrast to Ottawa’s dense local supply chains, Waterloo tech enterprises have looked abroad for partners (Bramwell et al., 2008: 106–107; Munro and Bathelt, 2014: 230). For example, local anchor RIM worked almost exclusively with external sub-contractors and frequently feuded with local actors (Howitt, 2019; Ornston and Camargo, 2022).

Unlike Toronto, cross-sectoral collaboration is also limited (Bathelt et al., 2011: 474–475). Although Communitech attempted to build bridges by constructing innovation labs around large firms in traditional industries, collaboration was rare, even among tech start-ups which were directly adjacent to local industries (interviews W1, W4, W5 and W6). The initiative has since been shuttered. A Toronto-based investor may have been particularly harsh in characterising Waterloo as ‘a wasteland for scale-up talent’ (interview T18), but many locals expressed similar concerns (interviews W5, W7, W8 and W9). For example, one tech employee said, ‘If you want venture capital, you’re going to Boston, Toronto or Silicon Valley. There isn’t this venture capital presence in Waterloo’ (interview W10). This deficiency prompted Communitech and other business leaders to promote the Toronto–Waterloo Innovation Corridor brand to link its tech economy more tightly to that of its larger neighbour (Wachsmuth and Kilfoil, 2021).

Why then do locals consistently speak of ‘barn raising’ (Bathelt and Spigel, 2019; Ornston, 2021) in the absence of task-specific cooperation or cross-sectoral buzz? In contrast to Ottawa and Toronto (Spigel, 2013), where this was identified as a weakness, industry representatives consistently point to mentoring networks as a regional asset and one of Communitech’s key strengths (see Ornston, 2021). Mentoring can be found in other regions, most notably through individual entrepreneurs in residence. Their individual, often sector-delimited experience, however, does not approximate the decentralised body of knowledge embodied in the dense, decentralised peer-to-peer relationships which underpin Communitech and the Waterloo community more generally (Spigel, 2017). As one interviewee explained: [Waterloo is] not quite as fragmented as it is in Toronto. It’s easy to get lost in the noise with all the big things happening in the big city … The support and assistance that exists for entrepreneurship isn’t just found locally with an incubator, it’s found throughout the community. (Interview W11)

These mentoring networks were especially valuable for a smaller region such as Waterloo for two reasons. First, senior–junior and peer-to-peer mentoring networks increased the supply of entrepreneurs by redefining what was possible in the context of a historically low- to medium-technology region (Ornston, 2021). For example, mentors assisted through the ‘validation of the ideas’ (interview W12) and by providing ‘role models’ (interview W7). Second, mentoring networks delivered general advice about how to operate a firm. As a former executive described it: One of the first things I did [when I moved here] was to join a peer-to-peer group at Communitech … The thing that struck me was the way the community was open and willing to share with each other … How do I do SRED tax credits? Who is the best person to go to? What should my option plan look like? (Interview W13)

This generic advice, drawn from a decentralised network of peers, rather than a single veteran entrepreneur, was particularly important for firms who could not draw on the resources of a large metropolitan area like Toronto or use well-established verticals as a shortcut to specialised knowledge and global markets like their counterparts in Ottawa. Mentoring networks taught Waterloo founders how to deviate from the big-city, Silicon Valley-style playbook by connecting proteges to international service providers (Bathelt et al., 2011: 482), as well as instructing them how to secure risk capital from Toronto and other cities (interviews W3 and W11), import human capital from outside the city (interview W1), co-locate closer to international customers (interview W4), construct dual office structures (interview W1) and manage remote workers (interview W9).

Among other strategies, mentors encouraged their peers and proteges to capitalise on the region’s engineering knowledge base by targeting technically demanding niches with lower capital and marketing requirements (interview W9). One advisor remarked, ‘I’m always telling students if you can find a business-to-business niche, you’re far better off than trying the big consumer plays because they take incredible resources’ (interview W11). As a result, and unlike Ottawa and Toronto, the most successful Waterloo-based scale-ups have thrived in obscure, technical, less capital-intensive, often slower-growing business-to-business or business-to-government niches overlooked by larger players (Howitt, 2019: 240). This ‘scrappy’, niche-based strategy results in a diverse sectoral profile, spanning from hardware to med tech as well as myriad, industry-specific software applications, connected by mentoring networks rather than well-developed industry linkages or specialised infrastructure.

There is an opportunity cost to a scrapper-based strategy. While Waterloo-based interviewees generally painted a positive picture of the region (Ornston, 2021), several locals acknowledged external critiques (interviews T18 and T19) that the region has struggled to scale new enterprises since a spate of initial public offerings in the 1990s (interviews W4, W7, W10 and W17). The emphasis on peer-to-peer networking and the diffusion of generic, non-specialised knowledge exacerbated these weaknesses. One scale-up employee remarked: When you’re starting, some of those early, high-level tips [are useful]. But we’re in the business of [identifies niche] right now … That’s pretty specific. So, then you start looking and saying, ‘Do I start relating more to someone because they’re in proximity to me? Is proximity a valuable asset?’. (Interview W17)

That being said, ‘scrapping’ has resulted in a surprisingly resilient pathway into high-technology markets, resulting in sustained employment gains and insulating the region from disruptive shocks (Ornston and Camargo, 2022). In one study, it ranked second to Silicon Valley in per adjusted start-up activity (Compass, 2015). As one industry representative concluded, however, it has followed a distinctly less glamorous pathway to high-technology markets: ‘Waterloo solves hard, boring problems. Valuable problems, obviously. Business-to-business is pretty good … But let’s face it, it’s not sexy’ (interview W18).

Conclusion: Civic capital and economic change

This comparative analysis of Ottawa, Toronto and Waterloo makes three theoretical contributions to the literature on regional development. First, we use longitudinal variation to illustrate how the institutionalisation of civic capital facilitates the transformation of high-technology clusters (Nelles and Wolfe, 2022; Safford, 2009; Storper et al., 2015). Civic capital, in the form of the Atlas Group and Communitech, turned Waterloo from a feeder of engineering talent to US technology firms into an entrepreneurial hub, while its collapse in Ottawa impeded the region’s response to disruptive economic shocks. Even Toronto, despite its formidable advantages, failed to capitalise on cross-sectoral buzz until the establishment of bridging organisations such as TechTO.

At the same time, cross-regional analysis qualifies broad, universalising accounts (Denney et al., 2021; Nelles and Wolfe, 2022; Storper et al., 2015) by suggesting that cities, and intermediaries which inhabit them (Cicci et al., 2023; Madaleno et al., 2022), use civic capital in very different ways. Toronto, a large city, cultivated loose ties between entrepreneurs, human capital, complementary service providers and advanced users, underscoring the importance of ‘cross-sectoral buzz’ in large, diversified cities, which can scale start-ups in a wide variety of different sectors (Storper and Venables, 2004; Zukin, 2021). This distinctive pattern of cooperation and specialisation does not generalise to our smaller cases.

The literature on smaller urban areas argues that smaller regions use stronger ties to generate Marshallian externalities and specialise (Caragliu et al., 2016; Todtling and Trippl, 2004; Trippl et al., 2018). Our case studies, however, challenge this literature on two fronts. First, and in contrast to the literature on social capital more generally (Gargiulo and Benassi, 1999; Grabher, 1993), we find that strong ties do not have to relegate (smaller) regions to mature, slow-moving industries. Ottawa relied on institutionally demanding, task-specific cooperation to enter new high-technology markets, constructing specialised infrastructure, first in telecommunications and optics, and then next-generation software-defined networks and the Internet of Things. While this pattern of task-specific cooperation and specialisation can be crisis-prone, we should not overlook its potential dynamism.

Second, we question the popular dichotomy between diversified cities and specialised, smaller regions (Caragliu et al., 2016; Duranton and Puga, 2000; Todtling and Trippl, 2004) by suggesting that the latter can support a wider array of innovative strategies (Herstad, 2018). Waterloo relied on a looser pattern of cooperation to compete in a wide variety of high-technology niches, albeit in a way that did not reflect big-city ‘Jacobian externalities’ or ‘cross-sectoral buzz’ (Storper and Venables, 2004). Instead, the diffusion of generic knowledge within dense, peer-to-peer mentoring networks helped firms to assume a foothold within a wide variety of small, highly technical niches. We believe this novel and understudied archetype, the ‘scrapper’, could shed light on smaller cities such as Cambridge (Garnsey and Heffernan, 2005) which succeed without a clear pattern of industrial specialisation. This alternative form of ‘niching’ (Kristensen and Levinsen, 1983), based not on sectoral specialisation but rather on diversification into small, unrelated markets, deserves more research, especially in light of the fragmentation of traditional, Marshallian industrial districts (De Marchi and Grandinetti, 2014).

Going forward, future research could focus on the causes and consequences of these different forms of civic capital. A detailed exploration of their origins is beyond the scope of this article but has been explored in other studies (Creutzberg, 2006; Nelles et al., 2005). Toronto’s status as a large, highly diverse metropole clearly militated against denser ties, but size does not explain why larger Ottawa specialised, whereas smaller Waterloo was characterised by looser connections and a more diversified profile. The fact that task-specific cooperation in Ottawa outlasted shifts in government intervention and a pivot from telecommunications equipment (Nortel) to e-commerce (Shopify) makes it hard to attribute differences in civic capital to the local government or sectoral specialisation. Nor is the role of a local anchor decisive. RIM, which employed a larger share of the local labour force in Waterloo, never sought to support task-specific cooperation (Ornston and Camargo, 2022), suggesting space for change agency in shaping civic capital (Beer et al., 2019).

The longer-term evolution of specialists and scrappers also deserves our attention, as Ottawa and Waterloo appear to be outgrowing their initial constraints, even as they rely on traditional patterns of cooperation. Ottawa is using task-specific cooperation to layer new specialisations on top of previous ones, creating a more diverse, multi-pillar economy, whereas peer-to-peer networking in Waterloo has eased barriers to scale by connecting the region to progressively larger pools of extra-regional capital, talent and customers. These developments are encouraging, suggesting that both specialisation and scrapping are viable long-term strategies. Unlike their larger counterparts, however, there are no shortcuts to scale for smaller regions. In the short to medium term, second-tier cities face important trade-offs in their efforts to promote local high-technology entrepreneurship.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors wish to acknowledge the generous financial support of the Social Sciences and Humanities Research Council of Canada through the Partnership Grant Program #895-2013-1008 and the Insight Grant #435-2020-0581, the research assistance of Alessandra Cicci, Brendan Haley, Todd Julie, Lisa Huh and Rebecca Byrne, as well as helpful feedback from Neil Bradford, Allison Bramwell, Dan Breznitz, Shiri Breznitz, Matthew Keller, Ben Spigel, Tara Vinodrai and three anonymous reviewers. Responsibility for any errors or omissions rests with the authors