Abstract

We empirically analyse the impact of human capital and housing supply on urban growth in the US and China. Integrating the heterogeneity of housing supply helps determine how a positive human capital shock translates into more population, higher house prices, or higher wages. To causally estimate this effect, we use a rich urban-level data set, choose our controls using the post-double-selection methodology, and instrument human capital with the per capita number of historical educational institutions. We find that human capital positively impacts urban population, house price and wage growth. While an elastic housing supply reinforces the impact on urban growth, it reduces house price growth and wage growth. Our results infer that human capital increases productivity in both countries and acts as an amenity only in the US.

Introduction

In 2018, 86% of the US and 59% of the Chinese population lived in urban areas. Between 2008 and 2018, urban areas in the US and China grew an average of 8.9% and 12.8%, exceeding average population growth by 1.8 and 5.1 percentage points, respectively. 1 In both countries, the size and pace of growth have varied widely across urban areas. Our sample’s standard deviation in urban population growth between 2008 and 2018 was 7.9% for the 385 US metro areas and 15.4% for the 309 Chinese cities.

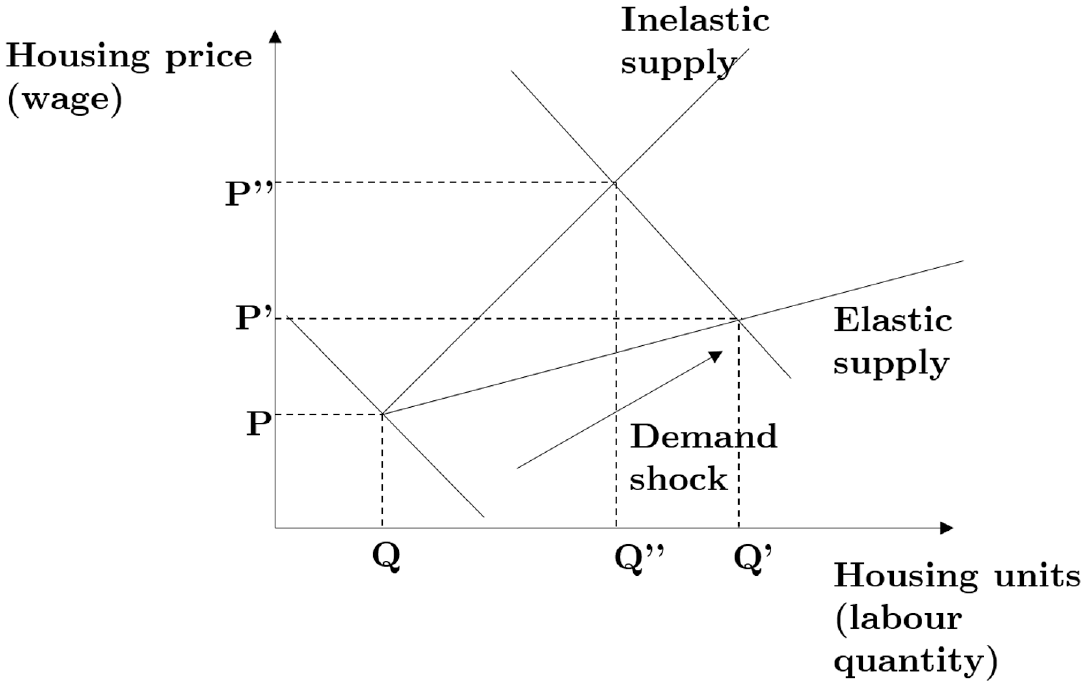

Human capital, which acts as a demand-side force, is a central determinant of urbanisation and economic growth (Gennaioli et al., 2014; Storper and Scott, 2009). 2 Starting from the Romer–Lucas model, which regards knowledge as the source of increasing returns to scale, urban economists broadly agree on the benefits of human capital accumulation in urban growth and labour migration. However, the impact of human capital on urban growth crucially depends on the housing supply elasticity, that is, the housing supply slope. Ganong and Shoag (2017) and Carlino and Saiz (2019) document the importance of housing supply in mediating the impact of demand shocks on city growth. The housing supply elasticity helps determine the extent to which increases in human capital will create bigger cities or higher-paid workers and higher house prices (Glaeser et al., 2006). As depicted in Figure 1, in areas with elastic housing supply, a positive demand shock caused by human capital leads to more housing units and only a limited increase in home prices. The new housing supply hinders a large increase in labour demand and, thus, wage growth, as an elastic housing supply leads to an elastic labour supply. In other words, in areas with elastic housing supply, the positive demand shock leads to the construction of more housing, a larger labour force, and, thus, moderate wage growth. In contrast, in areas of low housing supply, the positive demand shock has a limited impact on new housing construction and the urban population. Human capital gets capitalised into higher home prices, hindering urban growth. The effect on wages depends on the connection between human capital and population growth. Suppose human capital leads to population growth by encouraging increased local productivity, as Glaeser et al. (1995) suggested. In that case, wages rise because firms become more productive and have to compensate workers for rising house prices. As shown by Gaubert (2018), excessive housing costs and the inelastic housing supply inflate wages in large cities. However, human capital can also act as an amenity (Glaeser et al., 2001; Shapiro, 2006). Suppose more-educated populations spur the growth of consumption amenities and/or their political influence leads to desirable outcomes such as reductions in crime and pollution. In that case, more-educated populations experience more rapid growth in life quality. Since wages are determined by labour demand, increasing amenities exert little effect on nominal wages. Since house prices rise, real wages decline.

Housing supply and demand.

Integrating the heterogeneity of housing supply and controlling for other urban growth determinants, we empirically analyse and compare the impact of human capital on urban growth, house prices and wages in the US and China. Comparing the largest developed and developing countries shows the importance of urban growth determinants for countries with different social–political systems at different urbanisation stages.

To causally estimate the impact of human capital interacted with housing supply elasticities on urban growth, house prices and wages, we choose our controls – from more than 50 variables on human capital, transportation, economic output and amenities – using the post-double-selection (PDS) methodology of Belloni et al. (2014) and instrument human capital with the per capita number of educational institutions in the US in 1940 and 1948 in China. Selecting the confounding factors with PDS – a Lasso-type technique – reduces the omitted variable problem, thus improving the robustness of causal inference. Furthermore, using the per capita number of established educational institutions as an instrument reduces the omitted variable and reverse causality problems and helps dispel the fear that this problem reflects recent events. To look at the short, medium and long-run effects of human capital, we look at two, five and ten-year periods. We find that human capital, measured as the share of the population with a college degree, significantly increases population growth, house price growth and wage growth in the US and China in the short to long run. The direct impact of human capital on urban growth is larger in the US than in China. Urban areas with a more elastic housing supply experience a stronger effect of human capital on urban population growth in both countries and a weaker impact on house price growth and wage growth. This infers that human capital acts as a productivity booster in the US and China but also as an amenity in the US. Interestingly, the housing supply elasticity has a relatively more pronounced impact in China. This may reflect China’s stringent land quota system and acute affordability crisis.

Our paper bridges two strands of the literature. The first strand focuses on human capital as a determinant of urban growth. Lucas (1988) and Simon and Nardinelli (2002) show that the stock of human capital in an urban area influences its economic performance, affecting the attractiveness of an urban area. Urban areas with a more highly skilled population also experience faster growth in quality of life, spurred by the improved consumption amenities demanded by this proficient cohort (Shapiro, 2006). The human capital significance has increased and is the key engine of city growth (Sunley et al., 2020). The high-skilled population also tends to congregate together. People learn from one another within communities and acquire expertise through interactions, resulting in spatial clusters of employment and creative activities (Acs et al., 2018; Feldman, 1994; Glaeser, 1999; Glaeser and Shapiro, 2003; Sonn and Storper, 2008). Moretti (2004) corroborates that the supply of college graduates has substantial spillover effects on less-educated groups. From the viewpoint of the consumer city (Glaeser et al., 2001), accomplished neighbours are an attractive consumption amenity. There are also low barriers to entry and little potential cultural friction for cohorts with high human capital (Florida, 2002). Moreover, cities are growing by adapting to new technologies, where human capital serves as a tool for a city to deal with reinvention (Glaeser and Saiz, 2004). This is especially true when cities face adverse productivity shocks from either declining trade opportunities or unpleasant weather, which hinders immigration. As Shapiro (2006) points out, urban areas with more educated and skilled residents shift more rapidly from a manufacturing-intensive industrial structure to a more advanced industrial composition than cities with less human capital. Broxterman and Yezer (2021) show that the association between college share and city growth in the US is concave rather than monotonic. Urban growth, driven by economic fundamentals or elastic housing supply, mainly involves agglomerating skilled workers with high wages in urban areas (Autor, 2019).

The second strand of the literature focuses on the economic implications of housing supply. Glaeser and Gyourko (2018) document that the implicit tax on development created by housing regulations is higher in many areas than any reasonable negative externalities associated with new construction. Inelastic housing supply leads to higher house prices (Cosman et al., 2018; Hilber and Vermeulen, 2016), spatial misallocation of labour (Hsieh and Moretti, 2019) and lower migration response of households (Diamond, 2017). Moreover, housing shortages limit migration into cities generating social inequalities and inhibiting urban growth (Rodríguez-Pose and Storper, 2020). Thus, housing supply plays a crucial role in urban growth (Glaeser et al., 2006).

Our contribution to the literature is threefold. First, we empirically estimate how human capital impacts urban growth, house prices and wages, considering the heterogeneity of housing supply. Specifically, we show to what extent human capital translates into urban growth, more expensive housing, or higher wages. Second, we build rich city-level datasets for the US and China encompassing housing supply elasticities and variables on human capital, transportation, economic output and amenities. Third, this analysis compares the largest developed economy with the largest developing one, thus shedding light on the different urbanisation stages and social–political systems.

The remainder of the paper is structured as follows. The second section derives the hypotheses. The third section presents the city-level data on human capital, transportation, output and amenities and provides descriptive statistics. The fourth section explains our empirical identification strategy. The fifth section discusses the results. The final section concludes.

Hypotheses

Given that the housing supply elasticity only affects how a shock translates into larger population, higher house prices, or higher wages, we interact the housing supply elasticity with human capital (Duranton and Puga, 2014). Specifically, we formulate the following questions with hypotheses:

How does human capital impact urban population growth, house prices and wages?

H1: Higher human capital positively affects population growth, housing price growth and wage growth.

To what extent does this impact depend on the housing supply elasticity?

H2: The impact of human capital on population growth, housing price growth and wage growth is reduced in areas with more elastic housing supply.

What are the differences between urban growth dynamics in the US versus China?

H3: Due to China’s political system, stringent land quotas, and acute affordability crisis, the moderating effect of housing supply on the relationship between human capital and urban growth is relatively more pronounced in China than in the US. However, China’s top-down land quota allocation system allows city leaders to directly control how much land a city can convert from a rural area to an urban area and the floor-to-area ratio regulation that also affects housing supply elasticity.

To test these hypotheses, we build a rich urban-level data set encompassing housing supply elasticities and more than 50 variables on human capital, transportation, economic output and amenities for both countries. This rich urban-level dataset allows us to control for other determinants when analysing how the housing supply elasticities affect human capital’s effect on urban growth, house prices and wages.

Data and descriptive statistics

To construct our data set, we combine various data sources. Our data set covers the period 2008–2018. Online Supplemental Table A.3 provides an overview of the variables used in our empirical analyses.

Dependent variables

Urban growth

We use population growth to measure urban growth. In the US, we use the Metropolitan Statistical Area (MSA) population reported by the United States Census Bureau’s annual American Community Survey (ACS). Annual data are benchmarked to the decennial Census and represent the total population residing in each MSA.

To produce comparable results to US urban growth, we use ‘cities’ as the geographic unit for China, including both provincial-level (such as Beijing) and prefecture-level cities (such as Nanjing in Jiangsu province). Chinese cities comprise several clusters of urban areas and surrounding rural territories. 3 The principal source of the city-level population data is the Chinese Population Census in 2000 and 2010, the 1% population sampling surveys in 2005 and 2015, and the Provincial Statistical Yearbook (2008–2018). 4 Note that the population we use to calculate urban growth is the total number of residents living and working in a city rather than the residents with the local hukou (household registration system). Since local governments restrain the hukou registration, the two population measures differ significantly for large cities and cities with many migrants. For instance, the number of Beijing residents in 2018 was approximately 21.54 million, while the Beijing hukou population was only about 13.59 million. Many Chinese urbanites do not have local hukou, but these migrant workers are still an essential source of the labour force and the engine of city growth. 5

House prices

We utilise the Federal Housing Finance Agency’s (FHFA) All-Transactions Home Price Index to measure housing price growth in the US. The FHFA index is a weighted repeat-sales index that measures the average change in repeat sales or refinancing of the same single-family property. For China, we collect the housing data from the Chinese Real Estate Index System (CREIS), which records real estate development and housing transaction. 6 This database documents housing transactions and real estate development data in China from government information and is widely used in previous studies on the housing market in China (Somerville et al., 2020; Tsai and Chiang, 2019).

Wages

As a proxy for wages, we obtain individual income data from the Bureau of Economic Analysis (BEA) for US MSAs and average wage data from the China City Statistical Yearbook (2008–2018) for Chinese cities. 7

Human capital

In line with the literature on spatial sorting of human capital (Behrens et al., 2014; Eeckhout et al., 2014), we acknowledge the importance of a city’s human capital for its attractiveness. This is especially true for highly-educated workers. Therefore, to measure human capital across urban areas, we use data on educational attainment, that is, the share of residents over 25 years old with a bachelor’s degree or higher by location of residence. For the US, the Census Bureau collects these data annually through the ACS. Similarly, we obtain the data on educational attainment from the Chinese Census and China City Statistical Yearbook.

To deal with the possible issue of endogeneity due to labour sorting or omitted variables in estimating the impact of human capital on urban growth, we follow Glaeser and Saiz (2004) and Chauvin et al. (2017) and instrument human capital using the per capita number of historical educational institutions. For the US, we use the number of colleges per capita operating in 1940. On the one hand, colleges or universities in an urban area tend to raise education there (Moretti, 2004). On the other hand, this variable has the advantage of being predetermined and not a function of recent events, which might attract the population to a metropolitan area (Glaeser and Saiz, 2004). For China, we use the per capita number of colleges in 1948 (Chauvin et al., 2017). Because the colleges were established by the Republic of China (1912–1949), the presence of a college before the foundation of New China is unlikely to be correlated with the local labour market and housing market conditions in the 2000s.

Housing supply elasticities

To estimate how housing supply elasticities affect human capital’s impact on urban growth, we collect housing supply data for US MSAs from Saiz (2010). Comparatively, we obtain housing supply elasticity data for Chinese cities from Henderson et al. (Forthcoming). 8

Control variables

We chose our controls using the post-double-selection (PDS) methodology of Belloni et al. (2014) from several variables encompassing both countries’ transportation, economic output, amenities and political intervention. See Online Supplemental Appendix A.1 for a detailed description of the control variables.

Empirical framework

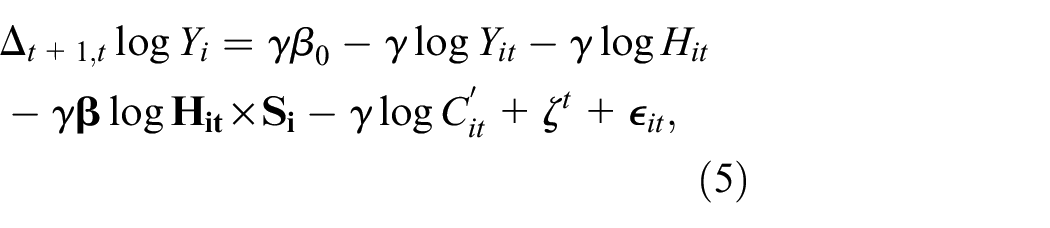

To estimate the effect of human capital on urban growth, house prices and wages, we start with the following simple ‘changes on changes’ urban growth regression based on Duranton and Puga (2014):

where

According to the spatial equilibrium condition,

Combining equations (2) and (3) leads to the following ‘changes on levels’ regression:

Since we focus on human capital and the heterogeneity of housing supply as urban growth drivers, we estimate the following equation:

where

Undoubtedly, this regression comes with some problems. One possibility is that some omitted productivity variable disproportionately attracts educated people to an urban area and increases house prices and wages. To address this possibility that changes in urban growth, house prices and wages result from a spurious correlation between human capital – that is, the share of people with a college education – and other urban characteristics, we control for a wide range of confounding factors. More specifically, we chose our controls using the post-double-selection (PDS) methodology of Belloni et al. (2014), which employs Lasso-type techniques to appropriately select controls and thus improve the robustness of causal inference. In equation (5), we control for the following urban area-period-specific characteristics that are correlated with changes in human capital and urban growth outcomes. First, we control for various transport infrastructure measures because, since at least the monocentric city model, we know that transport infrastructure plays a crucial role in urban growth. Second, we control for labour market characteristics, like industry concentration and unemployment. Third, to consider the economic fortunes of urban areas, we control for urban area GDP. Fourth, we control for several amenities, like temperature, that make an urban area more attractive. Fifth, we include region dummies. Finally, to control for time trends, we include period fixed effects.

10

Note that we refrain from using urban area fixed effects. If human capital follows successful urban areas, the correlation between changes in human capital and the error term

Another issue is reverse causation. Glaeser and Saiz (2004) documented that reverse causation from urban growth to education is only prevalent in some declining MSAs. Since 80.68% and 78.49% of US and Chinese cities in our sample, respectively, are growing, this may not account for much of the relevant effect. To alleviate these problems, we use per capita historical colleges as an instrument for human capital. This reduces the omitted variable and reverse causality problem, although it does not fully address that unobserved human capital may be correlated with measured human capital. Nevertheless, the historical instrumental variable helps dispel the fear that this problem reflects recent events. Moreover, to avoid the endogeneity of current definitions of growth, we use the most recent MSA (2010) and Chinese city (2015) boundaries.

Results

US results

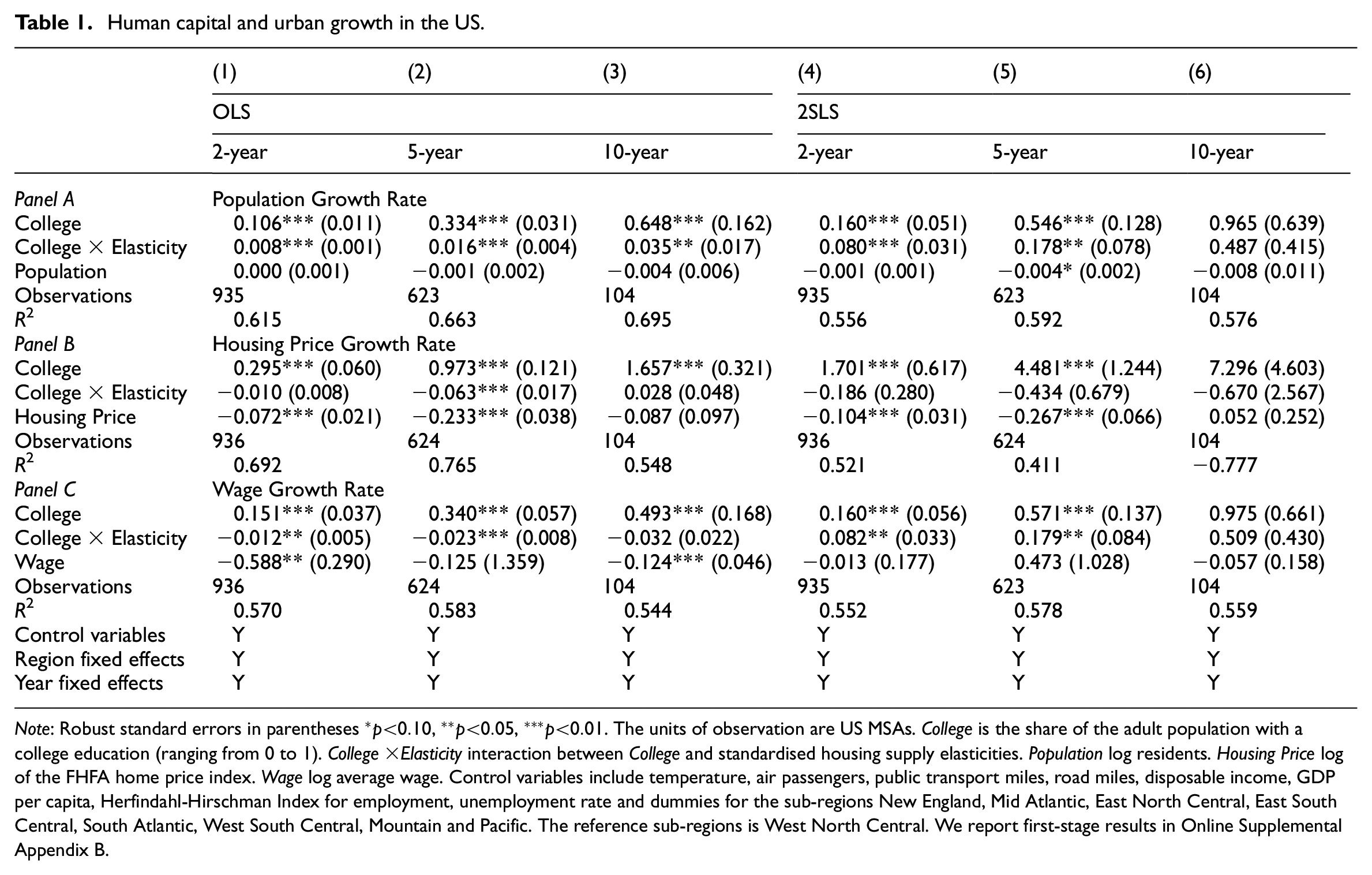

Table 1 shows the US results for equation (5) for the different periods. The first three columns present the Ordinary Least Squares regression (OLS) results, while the last three present the Two-Stage Least Squares (2SLS) results. Columns (1)−(3) of Panel A show that a 10% increase in the share of the population with a college degree leads to a 1.1, 3.3 and 6.5 percentage points increase in population growth in the next two, five and ten years, respectively. This effect is statistically and economically meaningful. Furthermore, the interaction term coefficients between human capital and housing supply elasticity show that a one-standard-deviation increase in housing supply elasticity (more elastic housing supply) boosts urban population growth, on average, by 0.2, 0.4 and 1 percentage points in the next two, five and ten years. Columns (4)−(6) present the second-stage regression results using the number of colleges in 1940 per capita as an instrument. The direct impact of human capital on population growth is slightly larger than in the OLS estimates, although the ten-year estimates are insignificant. However, the interaction term estimates are approximately ten times larger than the OLS ones. This shows that the OLS results suffer from a downward bias. In line with Hypothesis 1 and 2, the OLS and 2SLS results evidence the positive impact of human capital on urban growth and that this impact crucially depends on the housing supply elasticity.

Human capital and urban growth in the US.

Note: Robust standard errors in parentheses

Panel B of Table 1 reports our estimates for the impact of human capital on housing prices for US MSAs. The results in columns (1)−(3) show that a 10% increase in the share of population with a college degree leads to a 3.0, 9.7 and 16.6 percentage point increase in housing price growth in the next two, five and ten years. In the short to medium run, the negative interaction term coefficients between human capital and housing supply elasticity confirm that more elastic urban areas exhibit smaller housing price increases when facing a positive shock in human capital. A one-standard-deviation increase in housing supply elasticity leads, on average, to a 0.3 and 1.7 percentage points decrease in housing price growth in two years and five years, although only the 5-years interaction term is statistically significant. This confirms our Hypothesis 1 and 2. The interaction terms become positive but are not statistically different from zero in the long run. The 2SLS results in columns (4)−(6) show a much larger impact of human capital and housing supply on house price growth. The interaction terms stay negative but become insignificant. 11

Panel C of Table 1 presents the effects of human capital on wages in the US. Our estimates in columns (1)−(3) show that a 10% increase in the college share increases wage growth by 1.5, 3.4 and 4.9 percentage points in the next two, five and ten years. A one-standard-deviation increase in housing supply elasticity attenuates this effect by 0.3 and 0.6 percentage points for the two-year and five-year future growth, although the interaction term is not significant for the 10-year results. The negative interaction terms favour the hypothesis that human capital leads to higher productivity instead of acting as an amenity. Columns (4)−(6) show the 2SLS results. The estimates of the direct impact of human capital on wage growth increase slightly compared to the OLS estimates. Interestingly, the interaction terms become positive, indicating that inelastic places experience less wage growth. This is only possible if human capital also acts as an amenity. An increasing portion of highly-educated people in an inelastic housing supply environment leads to no change in nominal wages and an increase in house prices. This result echoes the finding in Glaeser et al. (2001) and Fu and Gabriel (2012) that talented individuals sort themselves into places with high human capital.

Our results are in line with Glaeser and Saiz (2004), Moretti (2004) and Chauvin et al. (2017), although the magnitude of our effects is smaller because they look at more extended periods.

China results

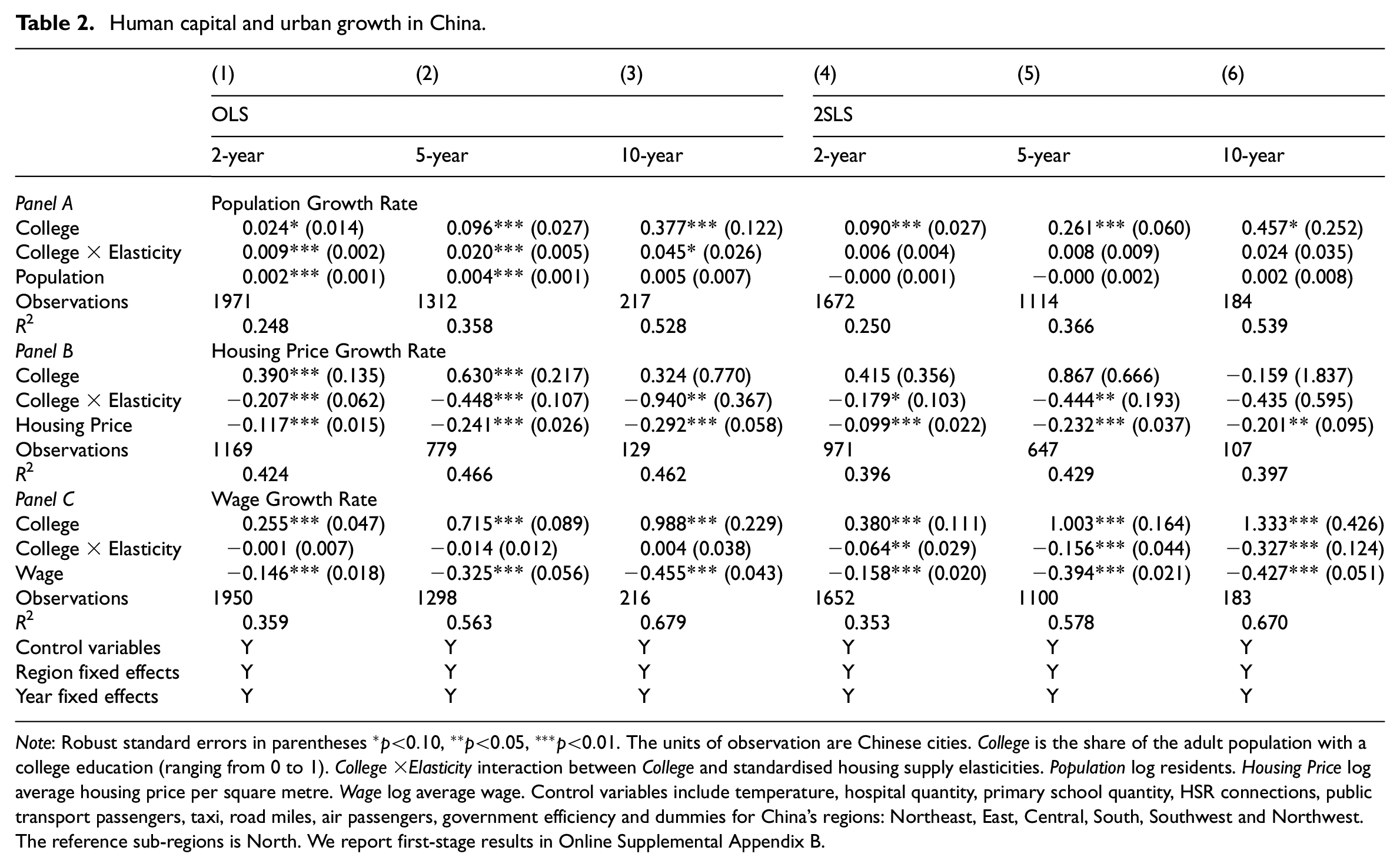

Table 2 shows the Chinese results for equation (5) for the different periods. Columns (1)−(3) of Panel A show that a 10% increase in the share of the population with a college degree leads to a 0.2, 1 and 3.8 percentage points increase in population growth in the next two, five and ten years. Confirming Hypothesis 1 and 2, the interaction term coefficients between human capital and housing supply elasticity show that a one-standard-deviation increase in housing supply elasticity will augment the human capital impact on urban growth, on average, by around 0.1 percentage points in two years to 0.4 percentage points in ten years. Columns (4)−(6) present the second-stage 2SLS results using the number of educational institutions in 1948 as an instrument. Like the US, the direct impact of human capital on urban growth is larger in the 2SLS estimates compared to the OLS ones. The interaction terms remain positive but become slightly smaller and insignificant. Note that the magnitude of the direct impact is smaller than for the US. One possible explanation is that human capital has a more negligible effect on a manufacturing economy than on a knowledge economy. According to the World Bank, the share of the economic output of China’s manufacturing and service sector was around 28% and 53% in 2018, respectively, while it was 11% and 77% in the US (World Bank, 2018a, 2018b). Compared to the US, the moderating effect of housing supply elasticities is relatively more prominent in China. 12 Since 2006, housing prices in Chinese cities have grown much faster than income, causing housing affordability issues (Shen, 2012). Thus, the housing supply elasticity is increasingly important in explaining migration patterns and population growth. This result also corroborates the findings of Niu et al. (2021) that population inflows in response to positive labour demand shocks are more substantial in cities with more elastic housing supplies. Moreover, the different political systems, institutions and growth mechanisms also help drive these results.

Human capital and urban growth in China.

Note: Robust standard errors in parentheses

Panel B of Table 2 presents our estimates for China’s human capital housing prices relationship. The results in columns (1)−(3) show that a 10% increase in human capital causes housing prices growth to increase by 3.9 and 6.3 percentage points in the next two and five years. The ten-year estimate is also positive but is statistically insignificant. The most natural explanation is that migration in China was initially even more restricted and, thus, the cities were far from equilibrium (Chauvin et al., 2017). Interestingly, the interaction terms are negative, increasing over time and highly significant. A one-standard-deviation increase in housing supply elasticity is, on average, associated with 1.7, 3.8 and 7.9 percentage point decreases in housing price growth rate in the next two, five and ten years. Columns (4)−(6) of Panel B report the 2SLS results for housing price growth. The main effect of human capital on housing price growth remains similar, except for the ten-year estimate, but are statistically insignificant. However, the interaction terms are consistent with the OLS results and indicate that cities with a more elastic housing supply experience smaller housing price growth. These results are in line with Hypothesis 1 and 2.

Panel C of Table 2 shows the impact of human capital on wages in China. As can be seen in columns (1)−(3), a 10% rise in college share of adults increases wage growth by 2.6, 7.2 and 10 percentage points in the next two, five and ten years. These human capital effects are smaller than those reported by Chauvin et al. (2017), who find that a 10% increase in the share of adults with college degrees is associated with an over 60% increase in earnings over 30 years (starting from 1980). This is probably because they look at a more extended period, and the human capital externalities have been decreasing over time. The interaction terms are negative but not statistically significant. Columns (4)−(6) of Panel C show the 2SLS results. The main effect of human capital on wage growth is slightly larger than the OLS estimates. The interaction terms between human capital and housing supply elasticity become statistically significant and indicate that a one-standard-deviation increase in the elasticity leads, on average, to a 0.5, 1.3 and 2.7 percentage point decline in wage growth rate for the next two, five and ten years. These results infer that while human capital leads to higher productivity, the corresponding growth will be relatively modest in elastic housing markets.

Comparison between the US and China

In the US, urbanisation occurred over a long period starting with the Industrial Revolution in the late-18th century. In 1820, less than 10% of the American population lived in urban areas, whereas over 80% percent do so today. 13 In contrast, China has experienced unprecedented urbanisation since the reform and opening policy initiation in 1978. Whereas in 1978, less than 20% of the Chinese population lived in urban areas, more than 60% do so today. 14 Comparing the largest developed and developing countries shows the importance of urban growth determinants for countries with different social–political systems at different urbanisation stages.

Our results show that the direct impact of human capital on urban growth is larger in the US than in China. These results align with the literature showing that the more developed a country, the more human capital matters (Chauvin et al., 2017). 15 Confirming Hypothesis 3, the interaction term between human capital and housing supply elasticity, which amplifies the effect on urban growth, is relatively larger in China. The impact of human capital on housing prices is larger in the US in the medium to long run but similar to China in the short run. This shows how this effect is becoming more critical in China in recent years. The interaction term which attenuates the impact on house prices has a larger magnitude in China. Finally, the impact on wages is slightly larger in China. In the US, human capital seems to increase local productivity and act as an amenity, while it only increases local productivity in China.

Another critical difference is that both countries have very distinctive political systems directly affecting urban growth. The US is a federal constitutional democratic republic, while China is a communist country governed by one political party. These differences substantially affect the housing markets. Whereas land is mostly privately owned and supplied in the US, China has a duo-land ownership system. China divides land ownership into state ownership (urban areas owned by the city government) and collective ownership (rural areas owned by rural villages). Thus, city leaders in China have a strong incentive to convert farmland in the city’s periphery rural area by paying farmers a compensation fee to lease it out as urban land. Anyone who wants to acquire the land-use right for profit must pay a land lease fee to the city government. This source of revenue has become significant for many local governments (Zheng and Kahn, 2013). Moreover, China’s central and provincial governments cap the five-year or ten-year maximum net increase in new construction land for each city, and this land quota system strongly constrains urban land supply. Regardless, China’s top-down land quota allocation system allows city leaders to directly control how much land a city can convert from a rural area to an urban area and the floor-to-area ratio regulation that also affects housing supply elasticity.

Despite the difference in political systems, since China is in an earlier urbanisation stage than the US, the US determinants serve as precursors for China. Our results suggest that human capital will become increasingly important in driving urban growth in developed and developing countries. Thus, countries and cities should continue to invest in human capital while ensuring an elastic housing supply.

Conclusion

This paper empirically analyses and compares the impact of human capital and housing supply on population growth, housing prices and wages in the US and China. To estimate this impact causally, we use PDS methodology to choose a rich set of controls and instrument human capital with the per capita number of historical educational institutions. We find that an increase in the share of the population with a college degree leads to a rise in population growth, housing price growth and wage growth. Urban areas with a more elastic housing supply experience even stronger population growth but attenuated house price growth and wage growth. These results infer that human capital increases productivity and, in the US, also acts as an amenity.

Admittedly, the political, institutional, economic and social differences between the US and China limit both countries’ direct comparability. Nevertheless, the US results may serve as a precursor for China. Our results hold essential lessons for policymakers. To foster urban growth, policymakers should invest in higher education and ensure an elastic housing supply. Our results align with the ‘housing as opportunity’ policy discussion. This discussion states that restrictive regulations in metropolitan areas hinder the expansion of the housing supply and dampen migration into prosperous regions (Ganong and Shoag, 2017; Glaeser and Gottlieb, 2008; Hsieh and Moretti, 2019). In China, many young individuals reside in rental units in the most regulated areas, such as Beijing and Shanghai. Thus, they would be worse off if housing prices kept increasing. Conversely, older homeowners will benefit from increased housing equity. In other words, the gains in housing wealth due to stringent housing supply are unevenly distributed. Older homeowners are receiving most of the gains, while the younger and possibly higher-educated become poorer in real terms. Combined with the recent talent war across Chinese cities, coordinated housing and talent policies could amplify the advantages of housing supply stimulation policies. The situation is similar in the US. Glaeser and Gyourko (2018) show that the limited housing supply growth has facilitated an intergenerational wealth transfer favouring older generations.

Both the US and China would benefit economically from reducing housing supply barriers to bolster urban economies. However, it is essential to acknowledge that less restrictive housing supply and migration to the metropolitan area are not without cost and consequences (Rodríguez-Pose and Storper, 2020). The deregulation of the housing supply can lead to inter-regional inequality, urban sprawl, congestion, etc. Thus, the government must consider these costs besides housing prices when enacting housing policies. Ultimately, the challenge lies in fostering urban growth through synergistic human capital and housing supply strategies without exacerbating socio-spatial inequality.

Supplemental Material

sj-docx-1-usj-10.1177_00420980231182074 – Supplemental material for The impact of human capital and housing supply on urban growth

Supplemental material, sj-docx-1-usj-10.1177_00420980231182074 for The impact of human capital and housing supply on urban growth by Simon C Büchler, Dongxiao Niu, Anne K Thompson and Siqi Zheng in Urban Studies

Footnotes

Acknowledgements

We are grateful to Maximilian von Ehrlich, David Geltner, the editor Chris Leishman, Albert Saiz, Zhengzhen Tan, Bill Wheaton, and two anonymous referees for very helpful advice and suggestions. We benefited from numerous comments by the participants of the AREUEA Singapore 2021, the MIT Sustainable Urbanization Lab (SUL) 2021 seminar, and the MIT Price Dynamics Seminar 2021. We thank the authors of Zheng et al. (2017) for generously sharing the data on industrial parks in China.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.