Abstract

While housing has been a central object of financialisation, questions regarding how multi-scalar states shape the financialisation of housing remain under-researched. I address this knowledge gap through a case study of the financialisation of affordable housing in Toronto. By analysing pertinent policy documents, I examine the roles and relationship of the federal, provincial and local states in the financialisation of affordable housing. Two findings are highlighted. (1) Although policies from all levels of government show traits of financialisation – in terms of both the connection between social policy and financial markets, and financialised ideologies prevailing in policy discourses, the extent and pattern of the manifestation of financialisation are distinct. This research thus calls for a nuanced understanding of the state’s role in the financialisation of housing from a multi-scalar perspective. (2) Affordable housing policies usually do not give an explicit definition of ‘affordable’. By scrutinising the policy specifications, I found that the target group is mainly moderate-income, rather than low-income, households. It will be increasingly difficult for low-income households to meet their housing needs.

Introduction

Housing has become a key object of financialisation (Aalbers, 2017b). As evidenced by the proliferation of empirical studies on the financialisation of housing, states at both the national scale and the local scale play a key role in this process (e.g. Aalbers et al., 2017; Fields and Uffer, 2016; Walks, 2014). While many studies have analysed the role of either the national state or the local state, few have systematically explored the roles of states at different scales. Existing understanding on this topic is limited to the national state creating the overall situation of marketisation, privatisation and deregulation to favour financialisation at the local scale (e.g. Aalbers et al., 2017; Fields and Uffer, 2016). However, literature on multi-scalar governance suggests that governance processes are organised and regulated in a complex manner by institutions at multiple scales (e.g. Brenner, 2004; Jessop, 2006). Existing understanding on the roles of multi-scalar states in the financialisation of housing is oversimplified.

To address this knowledge gap, this article adopts a multi-scalar governance perspective on studying the financialisation of affordable housing in Toronto. Here, I consciously use ‘affordable housing’ instead of ‘social/public housing’. Social housing generally means subsidised housing provided for low-income households. It was a typical form of housing welfare for low-income households under the Keynesian welfare state. Under the neoliberal restructuring of the welfare state from the 1980s, housing policies became increasingly market orientated. State subsidies for social housing have been diminishing. Instead, housing services for households unable to secure market units are increasingly provided in variegated forms, such as housing allowances, housing tax credit and construction subsidies, in substitution of the traditional social housing (e.g. Orlebeke, 2000; Wallace, 1995). In recent policy documents tackling housing unaffordability in advanced capitalist states, the term ‘affordable housing’ is frequently used instead of ‘social/public housing’ (e.g. Hulchanski, 1995; Whitehead, 1991). This loosely refers to housing that has been made ‘affordable’ through variegated forms of state support. The exact meanings of ‘affordable’ depend on the specific policy programmes. I will examine them in the later policy analysis.

In Canada, the provision of social housing used to be the federal government’s responsibility. In the 1960s–1970s, the federal government built significant numbers of social housing units. However, under the neoliberal restructuring of the welfare state, the federal government ceased to build new social housing units in the early 1980s, ended subsidies abruptly in 1993 and ‘downloaded’ Beresford et al. (2014) the responsibilities to the provinces in the mid-1990s. The provincial governments, in most cases, further downloaded the burden from federal downloading to municipalities in the late 1990s and early 2000s (see Suttor, 2016, for a comprehensive review of Canada’s social housing policy history). But the downloading of responsibilities has not come with the provision of equal funding and resources (Hackworth and Moriah, 2006). Moreover, the federal government’s retreat from providing social housing has been concomitant with a state-led mortgage securitisation. Fuelled by a massive growth of mortgage-backed securities since the early 2000s, Canadian cities have experienced a debt-driven housing market boom and a rapid rise in housing prices (Walks and Clifford, 2015). This situation is particularly evident in large urban centres, where the (re)concentration of capital and people has further pushed up housing demand. The rise in housing demand and prices, coupled with a growing income polarisation (see Hulchanski, 2007, among others), has resulted in a housing unaffordability crisis.

Toronto, Canada’s largest urban centre and a leading global city, has become one of the world’s most unaffordable cities to live in (Wetzstein, 2017). From 2005 to 2018, the average residential price in the Toronto region increased about 150% (Canadian Real Estate Association, 2019). Toronto residents would need over 66% of their income to cover their housing expenses (e.g. mortgage repayment or rental fee; RBC Economic Research, 2019). Under such a housing market situation, it is difficult for low-income households to meet their housing needs through pure market means. Also, the city’s social housing waiting list has become intolerably long. From 2006 to 2015, the number of active households on Toronto’s Rent-Geared-to-Income (RGI) waiting list almost doubled, increasing from 47,930 to 82,414 (ONPHA, 2016: 27). The average waiting time reached 8.4 years in 2015 (ONPHA, 2016: 32). The rapid deterioration of housing affordability and the shortage of social housing units have meant that pressure has been put on governments to provide more affordable housing units (ACORN Canada, 2018; CBC News, 2018). The three levels of government have designed a variety of market-orientated policy programmes, using both financialised and non-financialised policy instruments to address the housing unaffordability problem. The pressing political pressures and the complexity of neoliberal housing governance have triggered intensified actions and interactions between multi-scalar states on this problem.

This article examines the federal, provincial and municipal states’ roles and relationship in the governance of affordable housing in Toronto through the lens of financialisation. This lens plays a relevant explanatory role because of the centrality of housing in financialisation (Aalbers, 2017b) and ‘the demonstrable importance of finance to contemporary social life on all manner of axes’ (Christophers, 2015: 185). The research method is policy document analysis. Drawing upon the analysis, the article seeks to understand how and to what extent affordable housing has become a new frontier for financialisation, and what this phenomenon implies for the restructuring of multi-scalar governance and the welfare state. Building on this empirical case study, the article expects to enhance our understanding of the state’s role in the financialisation of housing from a multi-scalar governance perspective.

This article is organised as follows. The next section elaborates on how to use financialisation as an analytical lens and builds a conceptual framework for policy analysis. The third section examines policy documents around affordable housing from each of the three levels of government. The fourth section summarises the findings and elucidates multi-scalar states’ roles in the financialisation of affordable housing. The concluding section moves one step further to discuss the broader implications of multi-scalar governance and welfare state restructuring, as well as the limitation of the research and potential directions for future research.

Conceptual framework

The burgeoning literature on financialisation in the past two decades has raised dozens of understandings of this concept. Van der Zwan (2014) classifies contemporary scholarship on financialisation into three strands: financialisation as a new regime of accumulation; the financialisation of the modern corporation, featuring the ascendancy of the shareholder value orientation; and the financialisation of everyday life. Aalbers (2017a) identifies as many as 10 themes to encompass the existing literature. Christophers (2015) even warns that the concept of financialisation has been overstretched and has become excessively fragmented and vague, pushing it to the limits of reasonable analytic mutations.

Likewise, existing studies on the financialisation of housing have developed variegated understandings of the concept (Aalbers, 2017b). Earlier studies capture it narrowly as the proactive extension of residential mortgage loans (e.g. Gotham, 2009; Wainwright, 2009; Walks and Clifford, 2015). Later studies diverge from the one-fold mortgage extensions to variegated forms, such as financial investors’ upgrading of rental housing for profit extraction (Fields and Uffer, 2016), the utilisation of social housing as a collateral to raise credit for speculation (Aalbers et al., 2017) and the use of capital collected from financial activities for housing production (Romainville, 2017). In general, existing uses of financialisation in understanding the contemporary housing phenomenon mainly focus on concrete financialised behaviours. But such usages are ill-suited for the particular context of this research. As this research adopts a multi-scalar governance perspective, the analytical framework must enable comparing policies from multi-scalar governments. As governments at different scales have their own sets of duties, their concrete policy actions around affordable housing are qualitatively different. It makes little sense to compare the concrete policy actions. Instead, a higher level of abstraction is necessary to build the analytical framework.

Inspired by both political-economic and cultural-economic understandings of financialisation in the existing literature, which I will explain in detail below, I examine both the political-economic and cultural-economic manifestations of financialisation in policy documents. I assume that governmental policy documents may both (1) prescribe pro-financial market interventions, and (2) imply financialised rationales, values and ideologies. Thereby, I analyse the policy documents with two questions in mind. (1) What are the relationships between policies around the funding of affordable housing and financial markets? (2) To what extent and how does financialised representation manifest in policy rationales and policy discourses? The rest of this section clarifies some conceptual issues related to these two strands of analysis.

The relationship between social policy and financial markets

The relationship between social policy and markets in general has been a central debate in comparative welfare state studies. There are two conventional hypotheses on this relationship: substitution and complementarity. The normative framework of comparative welfare state research defines social policy in mature capitalist economies by its contribution to de-commodifying labour (e.g. Esping-Andersen, 1990; Korpi, 1983): social policy ‘permits people to make their living standards independent of pure market forces’ (Esping-Andersen, 1990: 3) to some extent. This definition derives from an understanding of the origin of welfare states as a political response to the counter-movement to the Great Transformation depicted by Polanyi (1944; Esping-Andersen, 1990). The rise of a market society instigates a counter-movement of protecting the society from the market, which then becomes an important driver of the consolidation of the welfare state. Reflecting such structures of class power, the telos of social policies is interpreted as ‘de-commodifying labour’– resisting the self-regulating market, correcting the access to and distribution of goods and services and compensating for undesirable market outcomes. However, another strand of scholarship criticises the de-commodification orientation for its ignorance of the productive forces of social policy and welfare. Contrary to the assumption that social policy compensates and crowds out markets, it reveals that social policy can create and underpin the market as well (e.g. Estevez-Abe et al., 2001; Holliday, 2000).

The Global Financial Crisis (GFC) and its aftermath have raised questions regarding the relationship between social policy and financial markets (Schelkle, 2012b). Using a quantitative method, Gerba and Schelkle (2013) systematically explore this question in six OECD countries. They find that the relationship could be complementary, substitutive or uncertain, but this finding is unable to explain the difference in the extent of the social impact of GFC. Hence, a qualitative perspective that moves beyond the dichotomy between complementary and substitutive is necessary to make sense of the social policy–financial markets relationship. Schelkle (2012b) takes up this question. Agreeing upon the notion that social policy can both compensate and create markets, she views social policy as constitutive for financial markets and examines the ideas on which this constitutive role is built: whether social policy moulds financial markets for social welfare purposes, or emulates market mechanisms to expand the reach of financial markets. Such a distinction matters because it has implications regarding which stakeholders become advantaged and the degree to which the concerns of the disadvantaged obtain political representation (Schelkle, 2012b). The importance of this distinction has been verified by empirical studies. Schelkle (2012a) compares homeownership finance in the United States, the United Kingdom and France to examine why household indebtedness and foreclosure after the housing bubble burst were much worse in the United States. Her study shows that the United States stands out for singularly aggressive market-making policies, which helped to expand financial markets for social policy purposes, but are complemented by few market-compensation policies to compensate for adverse market outcomes (as in the United Kingdom) or market-correcting policies to regulate the market and prevent undesirable outcomes (as in France). Such a different configuration of social policy between the US and European countries has also been observed in areas other than housing, such as in the pensions (Mabbett, 2012) and credit markets (Trumbull, 2012). The differences are rooted in state actors’ ideational differences about instrumentalising financial markets for social welfare purposes: whether the state views financial markets only confidently as a socially beneficial means to promote welfare for all, or also cautiously as a threat to welfare and social solidarity.

Inspired by these studies, in my analysis of affordable housing policies in Toronto, I firstly examine to what extent policies from each of the three levels of government instrumentalise financial markets to fund affordable housing. But how much a state instrumentalises financial markets does not suffice to indicate the state’s ideational stance towards this action. A nuanced interpretation of the role of the state necessitates discourse analyses of the policy documents to detect the ideational stance of the state. Thus I refer to cultural studies of financialisation for insights into discourse analyses of financialisation, as explained in what follows.

Financialisation as rationale, values and ideology, and its representation in social policies

Scholarship of the financialisation and the everyday school, mainly stemming from sociology and cultural studies of finance, has broadly extended the boundary of financialisation from within the financial sector and cooperation to the entire political-economic domains and everyday life (e.g. Aitken, 2007; Langley, 2006; Martin, 2002). It has significantly pushed the scope of financialisation from the material conditions of finance – such as financial activities, visible rules and formal procedures – to a cognitive sphere – the representation of financialisation through symbols, discourses and imaginations. Sociology and cultural studies of finance underline the ways in which financialisation influences behaviour by providing the cognitive script that human beings rely on unconsciously in everyday situations.

This body of scholarly work has identified the hegemonic role of derivatives in the financial system, and its socio-cultural implications. Derivatives, as the name suggests, are ‘a financial contract whose value is derived from something else’ (Norfield, 2012: 105). Their value is tied to the value of other assets through risk contracts on the future changes of those assets. The hegemonic role of derivatives lies in that they constitute an integral part of the financial system, that they motor the whole system and that they themselves make up an enormous market (Arnoldi, 2004). The performance of derivatives necessitates financial ways of calculating to render possible future risks for trade. The calculation process involves deconstructing things into a set of quantifiable attributes, calculating the probabilistic future changes of these attributes and interpreting these quantified attributes through the lens of risk (Bryan and Rafferty, 2014). The ascendancy of finance compels human beings to enact such financial ways of calculating frequently and repeatedly. By doing so, ‘a derivative logic’ (Bryan and Rafferty, 2014) is increasingly being implanted into the memory structures of humans, built into habit and applied to everyday behaviour.

The logic of derivatives is penetrating into political culture and social policies. The state has become an institution that emulates the mechanism of the financial system. Unbundling service delivery and funding, contracting out risks to the private sector and the voluntary sector and downloading risks and responsibilities to individuals have become the state’s policy rationales (Bryan and Rafferty, 2014). A notable and widely used example is that of social impact/benefit bonds. The rate of return on these bonds is dependent on the extent to which the project achieves its aim of improved social outcomes in terms of public sector savings. Moreover, the logic of derivatives is shaping governmentality. In order for the financial market to continuously render possible future risks and keep expanding without developing another financial crisis, the state needs to, on one hand, aid ordinary people in engaging in financial activities and taking risks, and, on the other hand, ensure that they fulfil their responsibilities of meeting their contractual payments. In policy discourses, such purposes disguise themselves as the promulgation of financial literacy (Finlayson, 2009), the instigation of calculative engagement and risk-taking and the emphasis on individual responsibility as a moral code (Langley, 2006; Martin, 2002).

In summary, financialised representations in policy documents manifest as follows. In terms of policy rationale, policies imply financial ways of calculating, such as risk trading and value extracting. In terms of policy discourse, the language of policies propagandises using financial markets to solve social problems, such as aiding people to engage in financial activities and preaching individual responsibilities as a moral code. I will be attentive to these points in the later policy analysis.

The federal, provincial and municipal governments’ affordable housing policies

Canada’s system of government consists of two constitutionally recognised levels of government (federal and provincial) and a third level (local government) that is empowered by the provinces. While the federal and province governments have near equal status, municipalities do not have much autonomy and often become ‘creatures of provinces’ (Keil, 2002: 578). The constitution has not specified which level of government is responsible for housing governance. Instead, as housing is intimately related to many other public sectors such as finance, social welfare programmes and land use planning, all three levels of government are intricately involved in housing governance.

In Toronto, all three levels of government have responded to the soaring need for affordable housing. The policy system around affordable housing has been piecemeal, spanning a bewildering patchwork of legacy programmes, temporarily-based programmes and intertwined policies from multiple governmental sectors (e.g. housing; finance; health; and the environment and climate change), using a wide range of policy instruments. The first problem of research design is how to select policies for analysis. I set up two guidelines. First, I only analyse the realm of policies around the provision of additional affordable housing units, while excluding policies around the repair, renovation and management of existing units. Providing more affordable housing units is a pressing issue in Toronto. It has become the focus of recent affordable housing policies. Also, the capital cost for adding new housing units is generally much higher than that for maintaining existing ones. An estimated cost to create a new housing unit is CA$150,000 on average across Canada (Federation of Canadian Municipalities, 2016: 13). In Toronto, the cost is even higher. Hence, I assume that policies around adding more affordable housing units are at the frontier of the financialisation of affordable housing policies. Second, I primarily focus on policies targeting general households with affordable housing needs, and do not scrutinise policies targeting specific groups of vulnerable people, such as the homeless, survivors of domestic violence and persons with disabilities. These groups are minorities who have special needs besides housing needs, which are usually addressed with special concerns by social policy.

Bearing these in mind, I use both content analysis and discourse analysis to scrutinise the affordable housing policies of each of the three levels of government. Broadly, the analysis is guided by two sets of questions. (1) What policy instruments are used to provide additional affordable housing units? To what extent do these policies directly utilise financial markets, rather than instruments which are not directly related to financial markets such as taxpayer funded investments and subsidies, and land use and planning tools? (2) In what ways are financialised rationales, values and ideologies manifested (or not) in policy discourses? What do these financialised representations imply for each of the three states’ ideational stances towards the utilisation of financial markets for affordable housing purposes?

The federal government

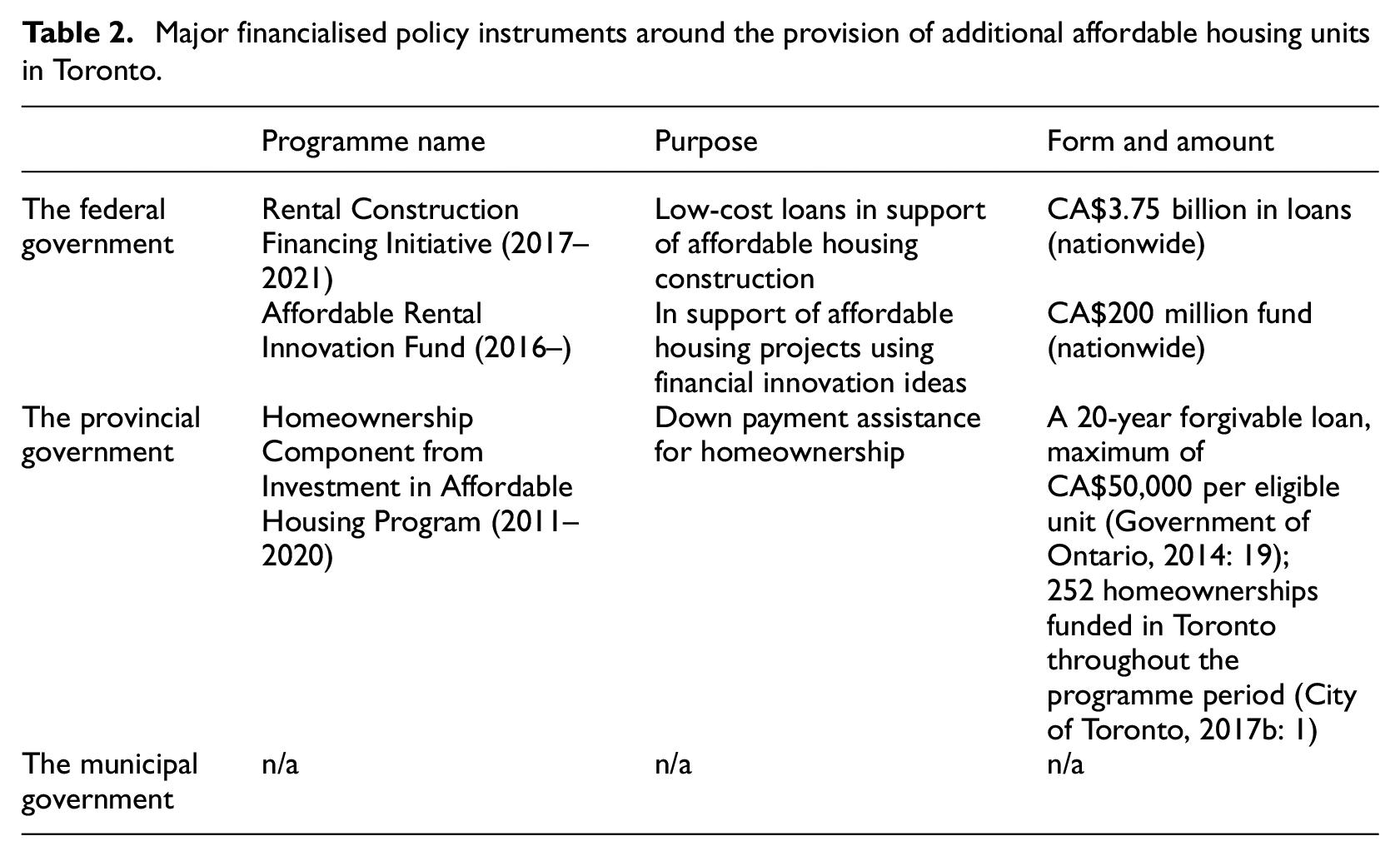

The federal government is involved in building new affordable housing units through jointly funded programmes with provincial governments and its own programmes, both of which are managed by Canada Mortgage and Housing Corporation (CMHC), a state-owned Crown cooperation and the national housing agency. As the joint programme Investment in Affordable Housing Program (IAH) is mainly designed and operated by each provincial government, I will discuss it in the next sub-section on the provincial government’s policies. Here I only examine the programmes designed and operated solely by CMHC. In 2016, CMHC started the Affordable Rental Innovation Fund (ARI) with CA$200 million. The fund was for ‘unique ideas that will revolutionise the sector moving forward’ (CMHC, 2016). ‘Revolutionise’ decidedly implies financial revolutionising, as it highlights ‘the design and use of customised financing models … to … lower the costs and risks associated with housing projects’ (CMHC, 2016). Financial innovation is conceived of as a panacea to overcome the tensions between risk and cost in funding affordable housing. Novel funding schemes such as equity capital investments, minority ownership models and dividend payments are raised as examples (CMHC, 2016). These funding schemes are more speculative than traditional debt-financing, as they enable the borrower to benefit from the appreciating value of property.

Another initiative for increasing the number of affordable housing units is the Rental Construction Financing Initiative (RCF). This initiative has a total of CA$3.75 billion in available loans, and is open from 2017 to 2021 (CMHC, 2017a). It furnishes municipalities, the private sector and not-for-profit organisations with low-cost loans to construct affordable housing. One of the affordability requirements is to have ‘at least 20% of units at or below 30% of the median income for the area’ (CMHC, 2017a; emphasis added). This implies that it is median-income, rather than low-income, households that are targeted. Moreover, the loan offers a generous 10-year term, a fixed interest rate and up to a 50-year amortisation period to cover up to 100% of the cost for residential space. It even devises more risky and aggressive lending schemes such as step-payment and second loan programmes to overextend the loans. The loan offers ‘interest only payments financed by the loan during construction through to occupancy permit’, and ‘principal and interest payments are due after 12 months of stabilized effective gross income’ (CMHC, 2017a). The federal state thus actively creates markets for financial capitals through governmental guarantees to socialise credit risk.

The recent trend of policies on affordable housing in Canada sees responsibilities being downloaded to the lower level of governments, whereas the federal government’s role is confined to offering modest funding. CMHC’s direct engagement in managing affordable housing programmes seems to be against this broader trend. A possible way to resolve this contradiction is to interpret the federal state’s purpose as expediting the use of financial innovations to solve the housing unaffordability problem, so as to delegate this task to financial markets and completely get rid of subsidising affordable housing in the long term. This interpretation is confirmed by two additional pieces of evidences. In 2017, CMHC started a post-secondary student contest, with CA$10,000 to be awarded to up to 10 submissions of ideas on ‘financing models that lower the costs and risks associated with rental housing projects innovation’ (CMHC, 2017c). CMHC also commits to offering ‘tools and financial assistance to help you create affordable housing without long-term federal subsidies’ (CMHC, 2018; emphasis added).

The National Housing Strategy (NHS) released in November 2017 also confirmed this policy trend. The NHS set up a CA$15.9 billion National Housing Co-Investment Fund to build new affordable housing and to repair existing housing, of which CA$11.2 billion is low interest loans and CA$4.7 billion is financial contributions (Government of Canada, 2017: 10). The aforementioned two CMHC programmes will also be integrated into this fund. As the ARI is a five-year programme with CA$2 billion in capital funding and the RCF is a four-year programme with CA$2.5 billion in loans, considering that the NHS is a 10-year plan and assuming ARI and RCF will continue as before with the same average annual funding amount during the NHS’s implementation period, the NHS commits to a new spending of only CA$0.7 billion capital funding but CA$4.95 billion in loans for affordable housing construction and repair.

The provincial government

With bilateral agreements with CMHC, the province cost matches federal investments and takes care of the design of the IAH (2011–2020) and the delivery to municipalities. The IAH includes an affordable rental component and a homeownership component to provide more affordable housing units. The rental component funds up to 75% of the total capital cost per unit or CA$150,000 per unit, whichever is less, for affordable rental housing construction (Government of Ontario, 2014: 12). ‘Affordable’ is defined as rents at or below 80% of the CMHC Average Market Rent (AMR). The City of Toronto does not implement this scheme, probably because the maximum per-unit funding is inadequate to attract developers, considering the much higher construction cost in Toronto than in other cities. Projects with low rents are difficult to get financed, as lower rents mean that money available for mortgage payments per month is also less. Most of the time, without public subsidies, projects with rents at or below 100% AMR cannot secure mortgage finance (Pomeroy, 2018). The homeownership component aims to assist low- to moderate-income households to purchase affordable homes by providing down payment assistance in the form of a forgivable loan, which is forgiven after a minimum of 20 years. The province shares the appreciated value of the home, which is payable when the home is sold. Thus, the homeownership scheme is a proactive market-making policy that uses public funding to bring people at the margins of homeownership and mortgages into the finance markets.

Financialised rationale and the logic of derivatives are visible in the province’s policy discourses. The province published the Updated Long-Term Affordable Housing Strategy (AHS) in March 2016. In this document, the province promises ‘modernizing our social housing system’ (Government of Ontario, 2016: 22). The rhetoric of ‘modernizing’ implies that the old system is obsolete and justifies the need to build a new system. The province declares that the new system will be ‘people-centered, partnership-based, locally driven, and fiscally responsible’ (Government of Ontario, 2016: 22). These neoliberal justifications euphemise the downloading of responsibilities and risks to municipalities and individuals, rather than facilitating the provision of customised housing services, as the following analysis shows.

The Rent-Geared-to-Income Program is a state corrective to housing markets which compensates for the difference between politically defined affordable rent (usually 30% of household income) and market rent. The waiting list for this programme in Toronto has been incredibly long due to the housing market boom. The AHS proposes a new housing allowance scheme – the Portable Housing Benefit Framework (PHB) – which allows tenants to find a unit on the private rental market but still receive subsidies. However, it only covers the gap between an affordable rent, defined as 30% of household income, and 80% of the average rent of the local housing market (Government of Ontario, 2017). Tenants will have to pay more if they are unable to secure rental units priced at 80% of average market rates, which is highly likely in places with tight rental housing markets like Toronto, in which the vacancy rate is only 1.1% (CMHC, 2017b). The transition to PHB shows an individualisation of responsibility for risk-taking. The province points out that the RGI system can ‘discourage tenants from becoming more economically self-sufficient’ (Government of Ontario, 2016: 19), while the new programme is politically sold as ‘equitable’ and ‘client-centered’ (Government of Ontario, 2017: 3). Such policy discourses promulgate individual responsibility as a moral code to legitimate the new system.

The province also has non-financialised policy instruments for affordable housing purposes, such as legislation on second units and inclusionary zoning (Government of Ontario, 2016: 16). The province proposes to require municipalities to ‘provide development charge exemptions for second units in new homes, and amend the Building Code Standards to reduce unnecessary costs to building second units’ (Government of Ontario, 2016: 16). Legislation permitting municipalities to adopt inclusionary zoning was released in April 2018. It empowers municipalities to require developers to build a proportion of affordable housing in residential developments. Both of these initiatives show a downloading of responsibilities and risks to municipalities, as neither has funding attached to it. It is hard to see how these initiatives can alleviate the affordable housing problem. For example, it has been over a year since the legislation on inclusionary zoning was enacted, but the city is still preparing a way to implement it and no concrete actions have been taken.

The municipal government

The City of Toronto is mainly an implementer of the province’s housing policies, such as the aforementioned IAH’s homeownership component and the housing allowance programme. But it has also taken its own initiatives to facilitate affordable housing construction within its limited jurisdictional and fiscal capacity. The city released the Open Door Affordable Housing Program (Open Door) in 2016. This programme has two components – a homeownership scheme derived from the province’s IAH homeownership component, and the affordable rental housing scheme designed by the city itself. The rental housing scheme offers fee exemptions and property tax relief in exchange for at least 20% of affordable housing units provided for a minimum of 25 years in construction projects (City of Toronto, 2017a: 6). Besides offering fee exemptions and tax relief, the city even provides capital funding out of its own general funds. The amount of this fund is CA$10 million for the year of 2018 (City of Toronto, 2018: 8). But the city attaches disincentives to it: ‘applicants … must be aware that those applicants requiring no funding or smaller amounts of funding will be more comparative… and more likely to be approved’ (City of Toronto, 2018: 8), probably due to its fiscal constraints. In addition, the city utilises its control on planning approval to offer fast-track approval incentives for developers who contribute affordable housing units (City of Toronto, 2017a: 2). Overall, the city itself does not directly rely on financial markets to fund affordable housing.

There is little financialised ideology in the discourses of the city’s policy documents. The city neither preaches risk-taking or individual responsibility nor advocates utilising financial tools to resolve social problems. I found an interesting difference between the city’s and the province’s policy discourses. Similar to the province, the city proposes to make surplus land public for affordable housing construction. The language in the city’s policy document is ‘unlocking opportunities… on private, public and non-profit land for affordable housing’ (City of Toronto, 2017a: 2; emphasis added). In contrast, the province’s language is that, ‘the province is leveraging the value of this land to develop new rental and affordable housing units for individuals and families in Toronto’ (Ontario Ministry of Housing, 2017; emphasis added). ‘Leveraging the value’ is a term frequently used in the realm of corporate finance. This is indicative of a financialised discourse in the province’s policy language. Also, the province’s policy discourse stresses who it is for –‘individuals and families’– thereby constructing a benevolent role for itself. In contrast, the city’s policy discourse is much less financialised.

Summary of findings

The roles of the federal, provincial and municipal states

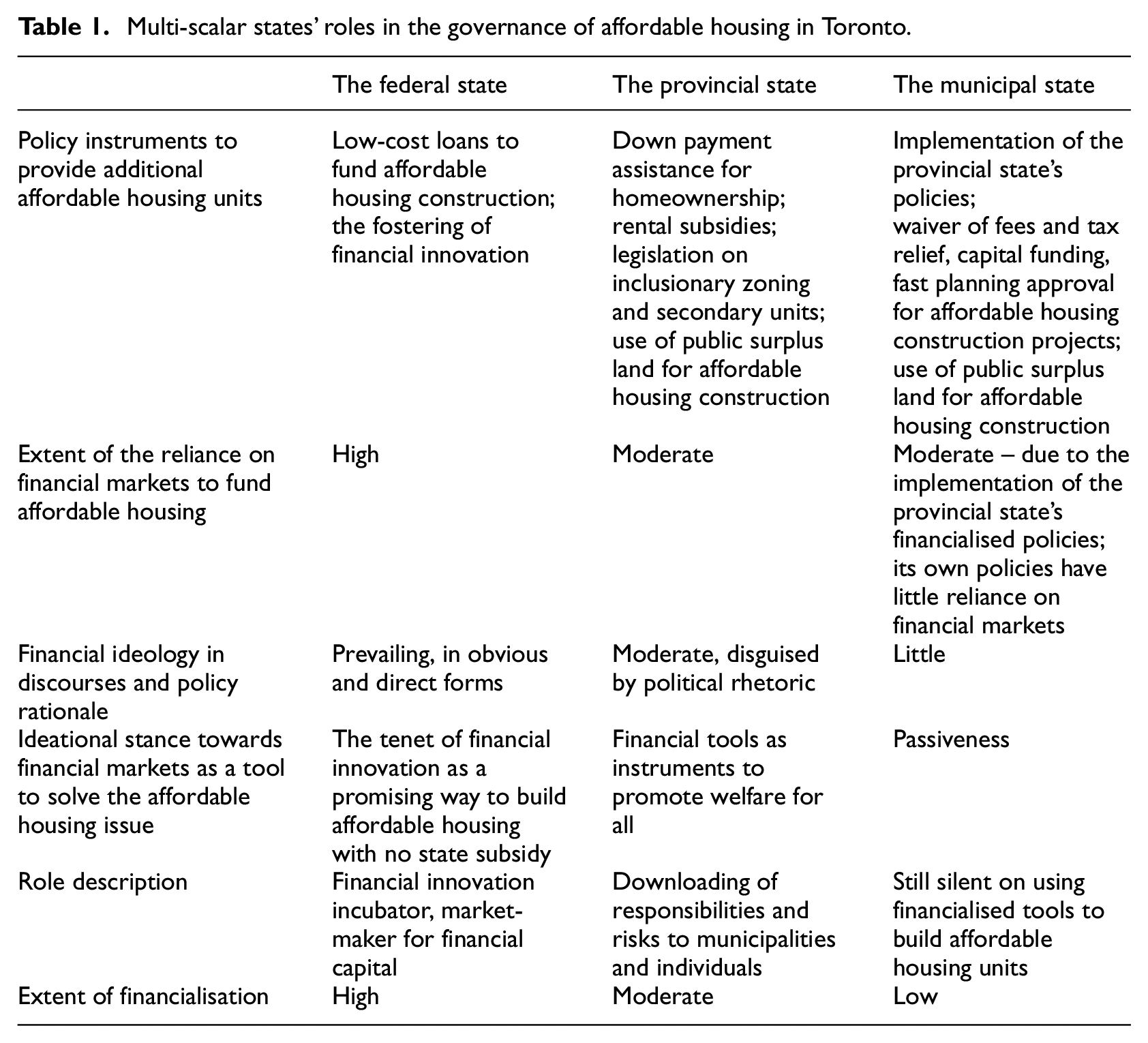

As evidenced by the empirical accounts presented above, the three levels of government expect to depend upon financial markets to fund the provision of new affordable housing units to distinctive extents. The federal state adopts proactive, market-creating policies (e.g. debt-financing, equity-funding) through a variety of financial innovations to manage and socialise risk. The provincial government uses financialised funding methods (e.g. down payment assistance) juxtaposed with non-financialised incentives (e.g. construction subsidies, rental subsidies, land use planning tools). The municipal government funds affordable housing from its own revenue, which does not directly rely on financial markets (Tables 1 and 2).

Multi-scalar states’ roles in the governance of affordable housing in Toronto.

Major financialised policy instruments around the provision of additional affordable housing units in Toronto.

The three levels of government also differ greatly in terms of the representation of financialisation in policy rationales and policy discourses. The federal government’s policy documents show arresting financialised ideologies, as evidenced by repeated emphases on financial innovation and the belief in the power of financial innovation to fund affordable housing construction without any state subsidies. At the provincial government level, financialised ideologies are mainly manifested as the downloading of risks and emphasis on individual responsibilities. The representation of financialisation is disguised by political rhetoric and mingled with neoliberal ideologies. In the municipal government’s policy documents, few financialised discourses are identified (Table 1).

The city stands out for its non-financialised affordable housing policies. Instead of further downloading risks to individuals, it keeps trying to upload responsibilities to the provincial and federal governments. The city criticises the provincial and federal governments, urges them to take more responsibility and ask for more funding from them. For example, while the province emphasises municipalities’ role in providing funding –‘we … would propose reforms to allow Service Managers to use other forms of appropriate, municipally-funded housing assistance’ (Government of Ontario, 2016: 22; emphasis added) – the city asserts the province’s responsibilities and declares itself to have only ‘an intermediary role’: ‘the key to meeting the housing needs of the many thousands of households with serious affordability problems is providing more provincially-funded rent supplements’ (City of Toronto, 2009: 18; emphasis added). Officers from the city have been speaking at public occasions to urge the federal and provincial governments to take a greater role and provide more funding to tackle the affordable housing problem.

Nonetheless, it would be misleading to assume that the city is fully aligned with low-income households and principles of social equity. There is no sign that the city has considered a radical approach to raising its own tax revenue to fund affordable housing. Such a radical approach would not be unprecedented in the city’s history – in the 1940s, with the federal and provincial governments’ indifference to social housing, the city, pushed by local reformers, affirmed low-income households’ housing rights and approved subsidies from its own funding to build social housing (Bacher, 1993: 10). Now the city stresses the economic benefits of affordable housing. As the Housing Opportunities Toronto Plan (2010–2020) declares, ‘Toronto is a major driver of Canada’s economy, and affordable housing is a key factor in the City’s economic success. It helps to create jobs and to attract and retain skilled key workers and business investment’ (City of Toronto, 2009: 4). The city’s concern is with urban competitiveness in the globalisation era. While this article is not able to forecast whether the city’s affordable housing policies will move to a financialised direction in the future, for the present, financial power has not yet gained sufficient representation at the local state level to shift the objective of the local state’s affordable housing policy from stimulating economic growth to creating markets for financial capital.

Financialisation and the changing nature of affordable housing policies

A point particularly worthy of attention is the deterioration and inconsistency of the meaning of affordable housing. While the standard definition of affordable housing is that it ‘costs less than 30% of before-tax household income’ (CMHC, 2013: 6–17), all three levels of government have substantially lowered this criterion. The definitions they use include: ‘80% of median market rents’ (Government of Canada, 2017: 12), ‘at or below 80% of the CMHC AMR’ (Government of Ontario, 2014) and ‘at or below Toronto’s AMR’ (City of Toronto, 2017a: 5). These criteria are close to 30% of the income of a middle-class household, but not of a low-income household. In 2015, the median one-person household income in the Toronto Census Metropolitan Area was CA$39,560 (Statistics Canada, 2017). The average one-bedroom AMR was CA$1067 (CMHC, 2015: 35), which is 32.4% of the median one-person household income. Furthermore, a clear definition of affordable housing is commonly absent from affordable housing policies, including the federal government’s National Housing Strategy (2017) and Ontario’s Long-Term Affordable Housing Strategy Update (2016). Politicians speak publicly on affordable housing without explaining what exactly it means. It seems that only in specific programmes is a definition of affordable housing spelled out, as without this the programme could not be operated in practice. This is indicative of a hidden amendment of the meaning of affordable housing. Affordable housing, which conjures an image of state-subsidised housing for low-income households, no longer targets low-income households but targets middle-income households.

The hidden amendment of the target of affordable housing policies, concomitant with the financialisation of affordable housing, indicates that the state is trying to incorporate moderate-income households that are on the margins of homeownership into finance markets. After the financialisation of owner-occupied housing through state-led mortgage securitisation (Walks and Clifford, 2015), the state is expanding the reach of financial markets to affordable housing. Affordable housing, which used to be sheltered from the volatility of financial markets, as it used to be heavily regulated and subsidised by the state, has become a new frontier for financial capital.

Conclusion

This research has examined multi-scalar states’ roles in the financialisation of housing through a case study of Toronto’s affordable housing policies. While existing literature suggests that the national state creates the overall situation of marketisation, privatisation and deregulation to favour the financialisation of housing at the local scale, this research demonstrates the need for a subtle examination of the roles of multi-scalar states in the financialisation of housing. In the case of Toronto, multi-scalar states utilise financial markets to fund affordable housing in distinctive ways. The federal state has become a financial incubator for radically utilising social policies to create markets for financial capital and overtly propagandise financialised ideologies. The provincial state adopts both financialised and non-financialised policy instruments. Financialised ideologies in policy discourses are visible, but disguised by political rhetoric. The local state is the least financialised. It neither directly relies on financial markets to fund affordable housing nor shows any financialised ideologies. Nevertheless, under constitutional and fiscal constraints, the local state is forced to follow federal and provincial policies to embrace financial markets to tackle the affordable housing problem.

This finding suggests a governance restructuring under financialisation. In large Canadian cities, the rising demand for affordable housing is mainly prompted by the federal state’s mortgage securitisation policies (Walks and Clifford, 2015), but the impacts are borne locally, as political pressures around the housing question arise first at the local level (Harris, 1995). Without equal fiscal resources, the local state has been pushed into an impossible situation in addressing the housing unaffordability problem. The financialisation of affordable housing is mainly pursued by the federal state. Although the local state has obtained more jurisdiction under this neoliberalisation, it has little choice but to accept and implement the federal and provincial governments’ financialised affordable housing policies. The local state is compelled to transfer social responsibilities to the rule of financial markets. The governance of affordable housing in Toronto has not experienced a deregulation, but a financialised neoliberal reregulation. This exemplifies ‘the second face of neoliberalisation’ as a process of reregulation as de-politicisation (Major, 2012: 541). Regulatory activities are moving to insular institutions dominated by federal and province finance officials and private financial institutions. While the local state’s autonomy has been further undermined, the federal and provincial states remain powerful. Finance has become a decentralised form of power that reshuffles the relationships between multi-scalar states.

The changing nature of affordable housing policies has generated insights on the restructuring of the welfare state under financialisation. The Toronto case exemplifies not simply the neoliberal retrenchment of the welfare state and the residualisation of social housing, but an uneven restructuring of ‘affordable housing’ as a component of the welfare state. On one hand, considerable emphasis has been placed on vulnerable groups of people such as victims of domestic violence and the homeless (Government of Ontario, 2014) to de-commodify and compensate for undesirable housing market outcomes. On the other hand, the welfare state creates the market for financial capital by incorporating the middle classes who are at the margins of homeownership into financial markets under the name of social policies. But general low-income households, who are neither as lucrative to housing finance markets as the middle class nor the most vulnerable group in society, have been marginalised by housing welfare. Through its financialised restructuring, the welfare state is as much in the business of creating financial markets as it is of helping the most vulnerable social groups.

Housing scholars have widely agreed on the special position of housing in the welfare state, with considerable debate on its standing as either a cornerstone or a wobbly pillar of the welfare state (Harloe, 2008; Malpass, 2008; Torgersen, 1987). This study reveals two characteristics of housing that enable the state to proceed with the financialised restructuring of the welfare state. Unlike other major domains of the welfare state, such as pensions, schooling and health, there is no clear standard of housing in state welfare. The ambiguity in housing welfare makes the hidden deterioration of the meaning of affordable housing possible without causing much political backlash. Also, since there is no conformity as to who should receive housing welfare, the state has been able to shift the recipients of affordable housing welfare from general low-income people to the most vulnerable social groups and the moderate-income class. These findings can potentially inform the theorisation of the relationship between housing, welfarism and financialisation.

Due to data constraints and the analytical scope and framework of this research, the policy analysis remains at a relatively general level. Also, policy analyses can only tell us what the states intended to do, not what they actually did. These are the major limitations of this research. Nevertheless, the research has provided an overall assessment of the current status of the financialisation of affordable housing in Toronto. The findings can inform future studies exploring this phenomenon at a more fine-grained level. Future studies may examine detailed capital investments and returns through the channel of affordable housing, specifications set in governmental affordable housing programmes and the implementations of those programmes.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article. Funding support for open access publishing was provided by the University of Toronto’s, Graduate Department of Geography & Planning Open Access Publication Fee Support Fund.