Abstract

The rising earnings inequality in China has sparked a heated debate on the socioeconomic outcomes of market transformation. While a large body of literature has focussed on the temporal trend of wage inequality during the reform period, much less attention has been devoted to the structural causes of regional variations in sectoral wage differentials. Using a micro-data sample from the 2005 one percent population sample survey and multilevel methods, this article examines the geographic variability of wage differentials between economic sectors in urban China, with a particular focus on the combination effects of market expansion and state intervention. The results indicate that sectoral wage differentials vary substantially across regions, and that market expansion interacts with state intervention to reconfigure earnings outcomes. Specifically, prefectures located in the interior region tend to exhibit a large wage premium for the state sectors, while prefectures located in the coastal region tend to display a wage advantage of the foreign-invested sector. The wage gap between the state and non-state sectors is smaller in areas with diversified ownership; openness to foreign investment increases the relative wages of foreign-invested-sector employees; stringent government regulation of industries increases the wage gap between the state monopoly sector and the non-monopoly sector; and strong redistributive power increases the wage premium for the public service sector over other sectors. Our findings suggest the necessity to take into account contextually constituted and locally specific wage-setting mechanisms when studying China’s wage inequality.

Introduction

Earnings inequality in China has grown dramatically since the early 1990s when economic reforms were deepened (Li and Sicular, 2014; Poon and Shang, 2012; Xie and Zhou, 2014; Zhang and Bao, 2015). The rising earnings inequality in China has sparked a heated debate on theorising market transition from a socialist planned economy. For example, in his market transition theory, Nee (1989) argued that markets replace redistributive mechanisms in the distribution of resources during China’s economic reform and asserted that economic success is more closely related to human capital rather than political capital. Such theory has, however, drawn many criticisms. For example, some researchers attributed the increase in returns to human capital to economic development rather than to market transition (Hauser and Xie, 2005; Xie and Hannum, 1996), while other scholars argued that political power and positional power persisted in determining income in the course of economic transformation (Walder, 2002; Zhou, 2000).

Although a large body of research has examined earnings inequality in relation to economic transformation in China, our understanding of this issue is constrained by limitations in previous research. First, while a large body of literature has examined the wage gap between the state and non-state sectors (the effect of ownership segmentation) (to name a few, Chen et al., 2005; Démurger et al., 2012; Meng, 2012), very few scholars have tried to measure the wage premium for the monopoly sectors over the non-monopoly sectors (the effect of administrative monopoly). In fact, the state sector in China has been divided into two segments since the early 1990s: a state monopoly sector in which state-owned enterprises reap excessive profits through scale economies, price manipulation and administrative protection and a state non-monopoly sector in which state-owned enterprises make relatively low profits due to fierce market competition (Bian and Zhang, 2002). Therefore, a novel approach is needed to differentiate between monopoly and non-monopoly sectors in China.

Second, while most previous studies have focussed on the temporal trend of wage inequality during China’s reform, only a few studies have been undertaken to explain the causes of geographical variability of earnings inequality (Bian and Zhang, 2002; Hauser and Xie, 2005; Nee and Cao, 2005; Shu et al., 2007; Xie and Hannum, 1996). However, most of these studies have merely focussed on the process of market expansion, devoting insufficient attention to the concurring process of state transformation. The state’s regulation of the economy is geographically specific and socially embedded (Hu and Lin, 2011; Wei, 2007). Although some scholars have found substantial regional variations in the state’s regulation of industrial mix and land conveyance in China (He et al., 2007; Lin and Hu, 2011; Liu and Lin, 2014), little empirical research has been done to quantitatively measure how state transformation along with market expansion reconfigure employment outcomes within a particular region.

Third, most previous studies on wage inequality across sectors are primarily based on survey data collected at a limited number of sampled cities (Bian and Zhang, 2002; Nee and Cao, 2005). For example, Bian and Zhang (2002) and Nee and Cao (2005) capitalised on 1995 Chinese Household Income Project (CHIP) survey data, which were drawn from around 55 municipalities and counties located in 11 out of China’s 31 provinces. It is necessary to investigate this issue with a more geographically diverse database, because China’s labour markets differ substantially across regions (Hauser and Xie, 2005; Meng, 2012).

To fill these research gaps, the present article investigates the geographic variability in wage differentials among economic sectors in urban China, using a micro-data sample from the 2005 one percent population sample survey (hereafter, 2005 Survey) and multilevel models. It particularly focuses on how regional variations in market expansion and state intervention matter in shaping sectoral wage differentials across 320 prefecture-level units (hereafter, prefectures). It contributes to the existing literature in the following ways. First, different from previous research on wage differentials between the public and private sectors, this study provides a more nuanced and accurate account of wage inequality by considering simultaneously the effects of both ownership segmentation and administrative monopoly. Second, this study goes beyond earlier stratification studies that merely focus on the effect of market expansion. On the contrary, following Zhou’s (2000) ‘market-politics coevolution model’ and Bian and Zhang’s (2002) ‘market-state interaction view’, this study examines how market expansion interacts with state intervention to structure earnings outcomes in a spatially specific manner. Furthermore, this study covers 320 out of China’s 340 prefectures in 2005, therefore providing a more comprehensive and thorough picture of wage inequality across economic sectors.

The rest of this article is organised as follows. The next section reviews previous literature on the market transition debate in China. The section after that presents the research hypotheses of this study based on our understanding of the geographic variability of sectoral wage differentials. This is followed by a section introducing the data and models used in this study and visualising the spatial patterns of sectoral wage differentials in China. We then present the results of multilevel models on the mechanisms of the geographic variability of sectoral wage differentials, before summarising the main findings of the article and drawing attention to its more general significance.

Economic transformation and earnings inequality

Market transition theory is among the most famous but controversial theories on the impact of China’s market reforms on socioeconomic attainment (Nee, 1989). This theory asserts that market reform shifts the mode of distributing resources from a redistributive system to a market-oriented system, and such shift benefits direct producers rather than redistributors. This theory also suggests that the Chinese reform undermines the value of political capital and increases the importance of human capital in income determination. Market transition theory is supported by the following findings in post-reform China (Cao and Nee, 2000): first, returns to human capital have increased substantially over time; second, the advantage of redistributors possessing redistributive power has declined relative to that of economic actors possessing market power; third, new opportunities have emerged outside the state redistributive economy. Thus, socioeconomic transformation in China is argued to be accompanied by the rising importance of human capital and entrepreneurship, the expansion of private/hybrid sectors and the declining significance of redistributive power and political capital.

Market transition theory has triggered a lively debate about the socioeconomic impact of China’s economic transformation. Many researchers challenged the validity of the theory at theoretical and conceptual levels. In his ‘market-politics coevolution model’, Zhou (2000) argued that the expansion of the market was not a self-evolving process. Rather, both politics and markets coevolved in response to each other during China’s socioeconomic transformation. For one thing, economic activities in the marketplace are shaped by polities, as many economic entities expand with the help of and under the rule of political authorities in China. For another, the expansion of non-state sectors contributes to the increase in state revenue, which encourages government agencies to change their role from redistributors to regulators and adopt policies to promote market expansion (Zhou, 2000). Under such circumstances, it is not only the case that returns to education increase in the reform era, but also that returns to positional power and organisational hierarchy persist over time.

Using a ‘market-state interaction perspective’, Bian and Zhang (2002) treated Chinese economic transition as an interactive process of market growth and state transformation. They set out two features of the market-state interactive process: first, marketisation is ‘a multifaceted and historical process in which product, labour, and capital markets grow through different historical trajectories’; second, state transformation occurs along with marketisation, which is reflected in ‘the role transformation from a redistributive state to a regulative state, in the formation of a state monopoly sector and in the conversion of state properties to cadres’ control and income rights through an insider privatization’ (Bian and Zhang, 2002: 399). This market-state interactive process leads to the growth in earnings inequality in China by increasing economic returns to both positional power and human capital (Bian and Zhang, 2002).

In this study, we adopt Zhou’s (2000) ‘market-politics coevolution model’ and Bian and Zhang’s (2002) ‘market-state interaction perspective’ in the analysis of wage inequality in urban China, since both of these two theories reflect the reality of the Chinese labour market: market expansion is not necessarily accompanied by the retrenchment of the state, and market transformation benefits not only market-oriented sectors but also state monopoly sectors. Conceptually, we treat market expansion and state transformation as two interrelated and interactive processes; empirically, we measure the magnitude of market expansion and state intervention with two sets of indicators. Contrary to what is articulated in Nee’s (1989) market transition theory, the state evolves in response to and facilitates market expansion, and in return its role in market economies is reinforced due to a growing economy (Bian and Zhang, 2002; Zhou, 2000). Therefore, it is necessary to use more sophisticated and comprehensive measures to quantify the multifaceted process of market transformation.

Understanding the geographic variability of sectoral wage differentials

In this study, we focus on how the geographic variability of sectoral wage differentials is influenced by the multifaceted process of market transformation. Historical evidence shows that, between the early 1980s and the mid-1990s, market expansion is accompanied by a substantial increase in the relative wages of non-state-sector employees, as non-state companies are more profitable in the market and have more freedom to convert business profits into wages (Zhou, 2000). From a geographical perspective, the non-state economy is assumed to be more competitive and vital in areas with high degrees of marketisation and economic openness, because non-state enterprises enjoy more business opportunities and favorable institutional settings in these areas. This is exemplified by the fact that the non-state sector thrives in coastal China while growing relatively slowly in central and western China (Fan et al., 2010; Lin and Hu, 2011; Wei, 2004). As workers’ wages are closely linked to the profitability and competitiveness of their work units (Chen et al., 2011; Xie and Wu, 2008), we can suggest the following working hypothesis:

Hypothesis 1: The wages of non-state-sector employees relative to state-sector employees are higher in areas with a higher level of market expansion.

In response to the rapid expansion of the market, the state has substantially changed its administrative functions from ‘direct intervention’ (through centralised planning and party and government organs, etc.) to ‘indirect regulation and control’ (through central banks, taxation and market regulations, etc.) (Bian and Zhang, 2002; Naughton, 2006). Rather than imposing entire control over the economy, the state has allowed private and foreign investors to enter a selected set of industries such as commerce, service, construction and manufacturing while maintaining strict control over industries strategically vital to the national economy and security such as banking, petroleum, energy, railway transportation and telecommunication (Naughton, 2006). Consequently, China’s industries become divided into two sectors: a state monopoly sector with high entry barriers and low market competition and a non-monopoly sector with a diversified ownership and a large number of competitors. Some studies have shown that a substantial wage gap exists between the state monopoly sector and the non-monopoly sector, because state monopolistic enterprises make excessive profits through scale economies, price manipulation and generous supports from the banking system (Bian and Zhang, 2002; Yue et al., 2011).

The wage premium in the state monopoly sector is assumed to vary across different regional and institutional contexts. Some geographers have indicated that ownership transformation in China exhibits multiple forms and local trajectories, and that state-firm relationships are different in different places (Hu and Lin, 2011, 2013; Wei, 2004, 2007). For example, where local governments rely on large-scale state-owned enterprises within their jurisdictions to achieve their economic and political objectives, the state monopoly sector tends to receive more administrative protections, subsidies and privileges from the governments (Hu and Lin, 2011, 2013). Therefore, in these areas, the workers of the state monopoly sector are more likely to earn more than their counterparts in the non-monopoly sector. This is verified by Poon and Shang (2012)’s finding that the mining and energy industries in central and western provinces, which are dominated by state-owned enterprises, pay their workers higher wages than other industries. By contrast, where the state influences the local economy primarily through indirect means, the wage premium of state-monopoly-sector workers over non-monopoly-sector workers is supposed to be lower. This leads to our second working hypothesis:

Hypothesis 2: The wage premium in the state monopoly sector over non-monopoly sectors is higher in areas with a more stringent government regulation of industries.

Wage-setting mechanisms are assumed to differ between the public service sector and other economic sectors. For government civil servants and tenured employees of not-for-profit public service units (e.g. public school teachers), their wages are closely related to the fiscal capacity of local governments (Chan and Ma, 2011). Some scholars have indicated that, with the rise of extra-budgetary activities and the commercialisation of the public sector, workers’ earnings in for-profit public service units become increasingly dependent on their work units’ ability to generate revenues rather than on the allocation of budgetary funds (Wong, 2009; Xie and Wu, 2008). Nevertheless, in general, labour remuneration in the public service sector is more subject to redistribution in the form of government spending, while that in both monopoly and non-monopoly sectors is more determined by market mechanisms (Chan and Ma, 2011; Démurger et al., 2012). By the same token, the wage premium in the public service sector over other sectors is hypothesised to vary by the redistributive power of the government:

Hypothesis 3: The wage premium in the public service sector over other sectors is higher in areas with stronger redistributive power.

Data and methodology

Overview of the data

The data used in our analysis were extracted from the 2005 Survey. The 2005 Survey was carried out by the National Bureau of Statistics of China using a stratified, cluster and Probability Proportional to Size (PPS) sampling technique. The dataset of the 2005 Survey includes 2,585,481 observations. We only considered individuals aged 15–65 who lived in urban areas, who were engaged in non-agricultural occupations and who earned between CNY 1 and CNY 100 per hour through employment. We excluded employers and self-employed individuals from our sample, as their earnings determination mechanism might be different from that of employees (Parks, 2012). It should be noted that rural migrants who lived and worked in cities were considered in our analysis as well. We further restricted the sample to 320 out of 340 prefectures in China, excluding prefectures with a very small sample size.

Two indicators, the ownership type and the industrial sector of a wage earner’s work unit, were used to distinguish among sectors. With regard to the ownership type, the state sector and non-state sector were distinguished. While the state sector comprises government/party agencies, state-run public service units and state-owned enterprises (including enterprises in which the state holds the controlling share), the non-state sector includes collectively owned enterprises, domestic privately owned enterprises, individual/household enterprises, foreign-invested enterprises and other types of non-state-owned enterprises.

As for the industrial sector, the public service sector, the monopoly sector and the non-monopoly sector were identified. 1 The public service sector includes 15 two-digit industries in which the lion’s share of employment was provided by administrative and civil service institutions (xingzheng shiye danwei) that were established with the aim of providing public goods and services. 2 The monopoly sector refers to 17 two-digit industries in which the market is dominated by a small number of goods or service providers. These industries are characterised by a high concentration ratio, high barriers to entry, a lack of market competition and high monopoly profits. We primarily referred to Bian and Zhang (2002) and Yue et al. (2011)’s approaches to demarcate the monopoly sector. Three indicators drawn from 2004 China Economic Census Yearbook, the total number of legal entities (faren danwei), the average size of legal entities and the share of total assets owned by state-owned enterprises, were used to adjust the classification. 3 Our classification can be justified by an official document issued by the State Council, which demarcated the scope of monopoly industries (State Council, 2005). Lastly, the non-monopoly sector refers to 54 two-digit industries characterised by a large number of competitors, relatively low barriers to entry and a high share of non-state investment.

As a result, five economic sectors were identified based on the indicators of ownership type and industrial sector: the public service sector (the overlap between the state sector and the public service sector), the state monopoly sector (the overlap between the state sector and the monopoly sector), the state non-monopoly sector (the overlap between the state sector and the non-monopoly sector), the collective and domestic private sector (the overlap between the non-state sector and the non-monopoly sector) and the foreign-invested and other sector (the overlap between the non-state sector and the non-monopoly sector). We lumped together collectively owned and privately owned domestic enterprises, partly because many firms registered as collectively owned firms were de facto privately owned firms in the 2000s (Lin and Hu, 2011), and partly because our preliminary analytical results showed little difference between these two ownership sectors in wage determination. In addition, those who worked for non-state-run civil service institutions (e.g. private schools), non-state-owned enterprises in monopoly industries, social and religious organisations, international organisations and community committees were excluded from the analysis, because the number of employees working in these sectors is very small in China. The final sample includes 318,205 individuals from 320 prefectures of 31 provinces, among which 19.64 percent, 7.87 percent, 18.53 percent, 45.01 percent and 8.95 percent of individuals are employed in the public service sector, the state monopoly sector, the state non-monopoly sector, the collective and domestic private sector and the foreign-invested sector, respectively.

Mapping sectoral wage differentials in China

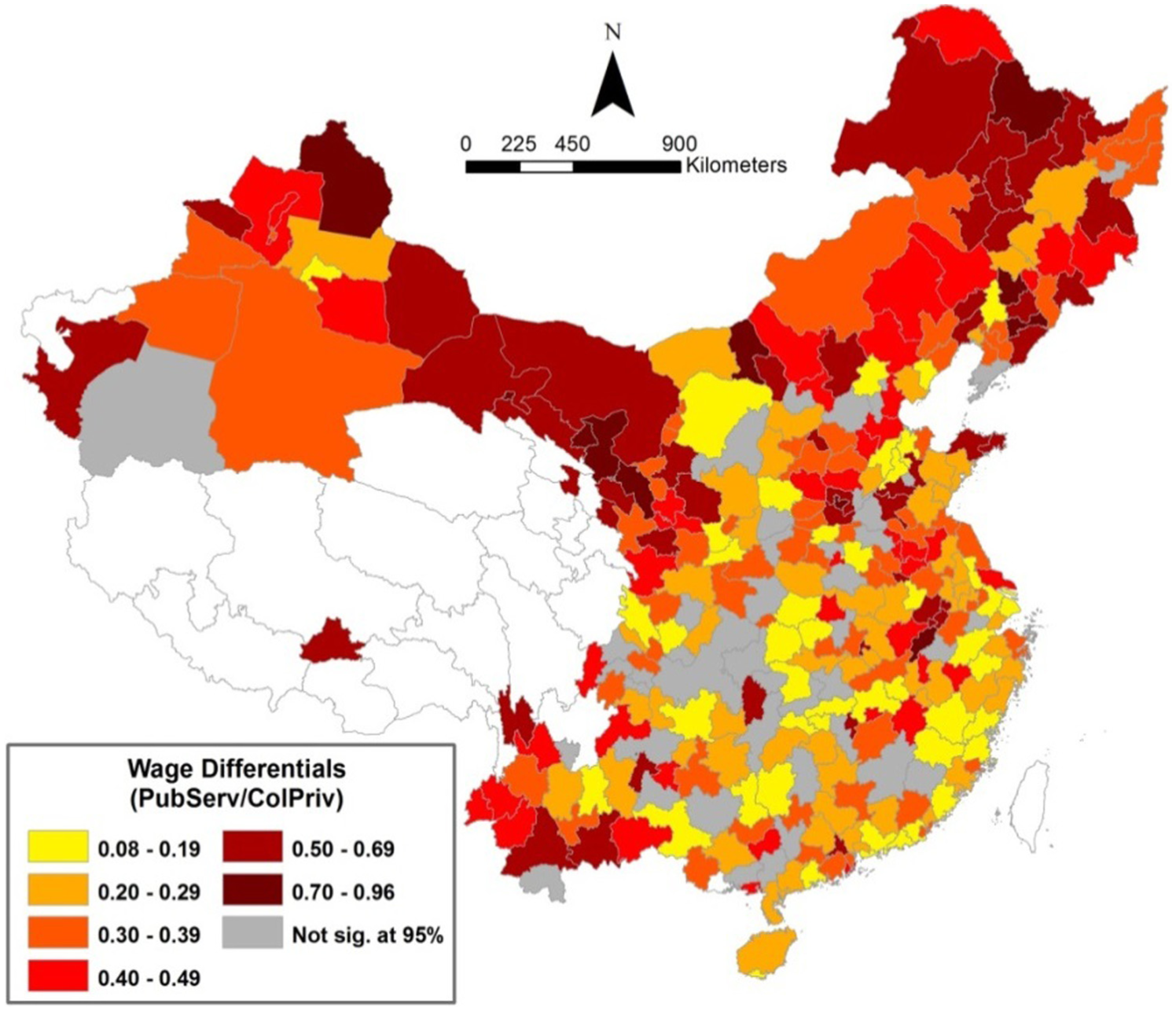

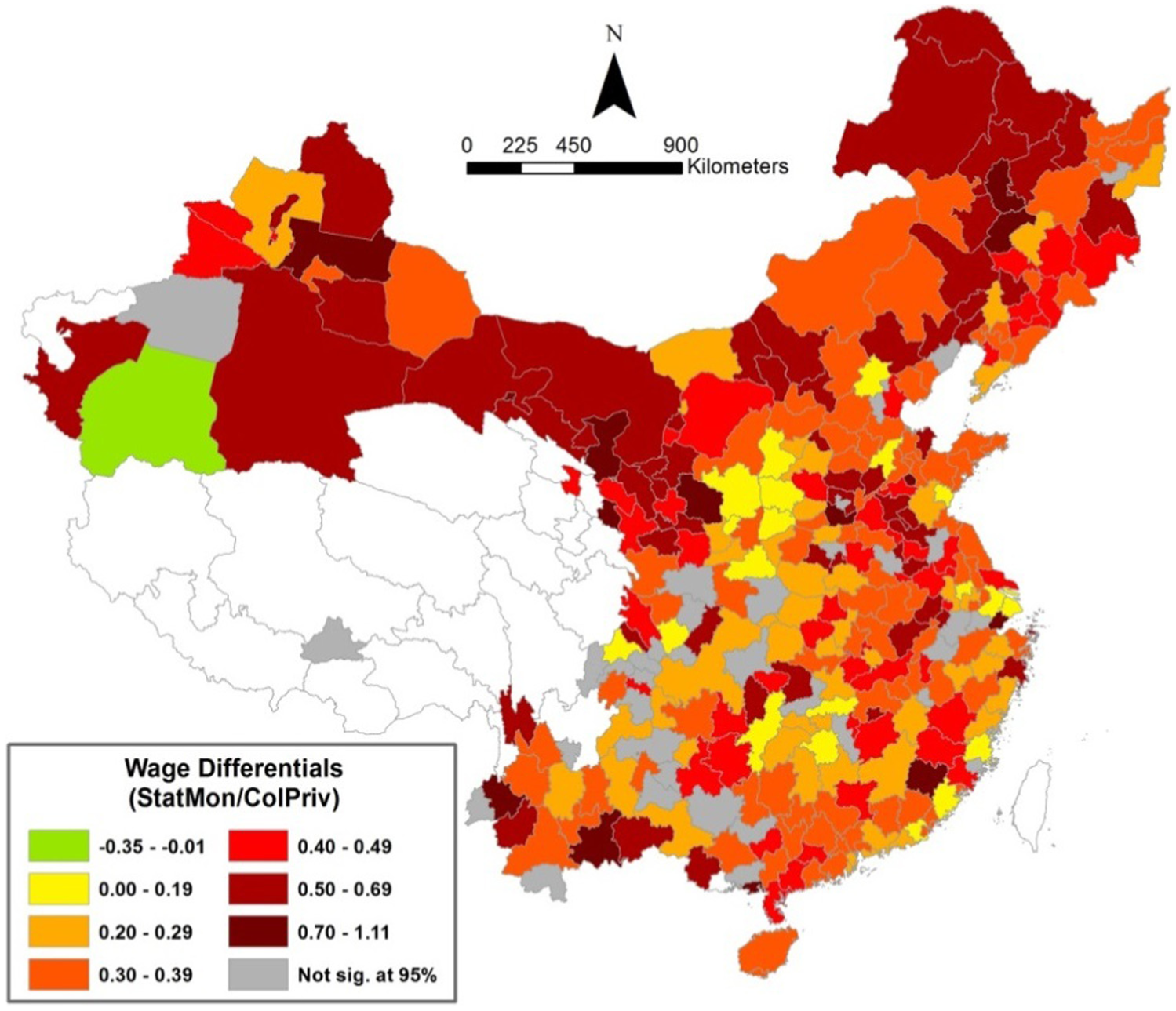

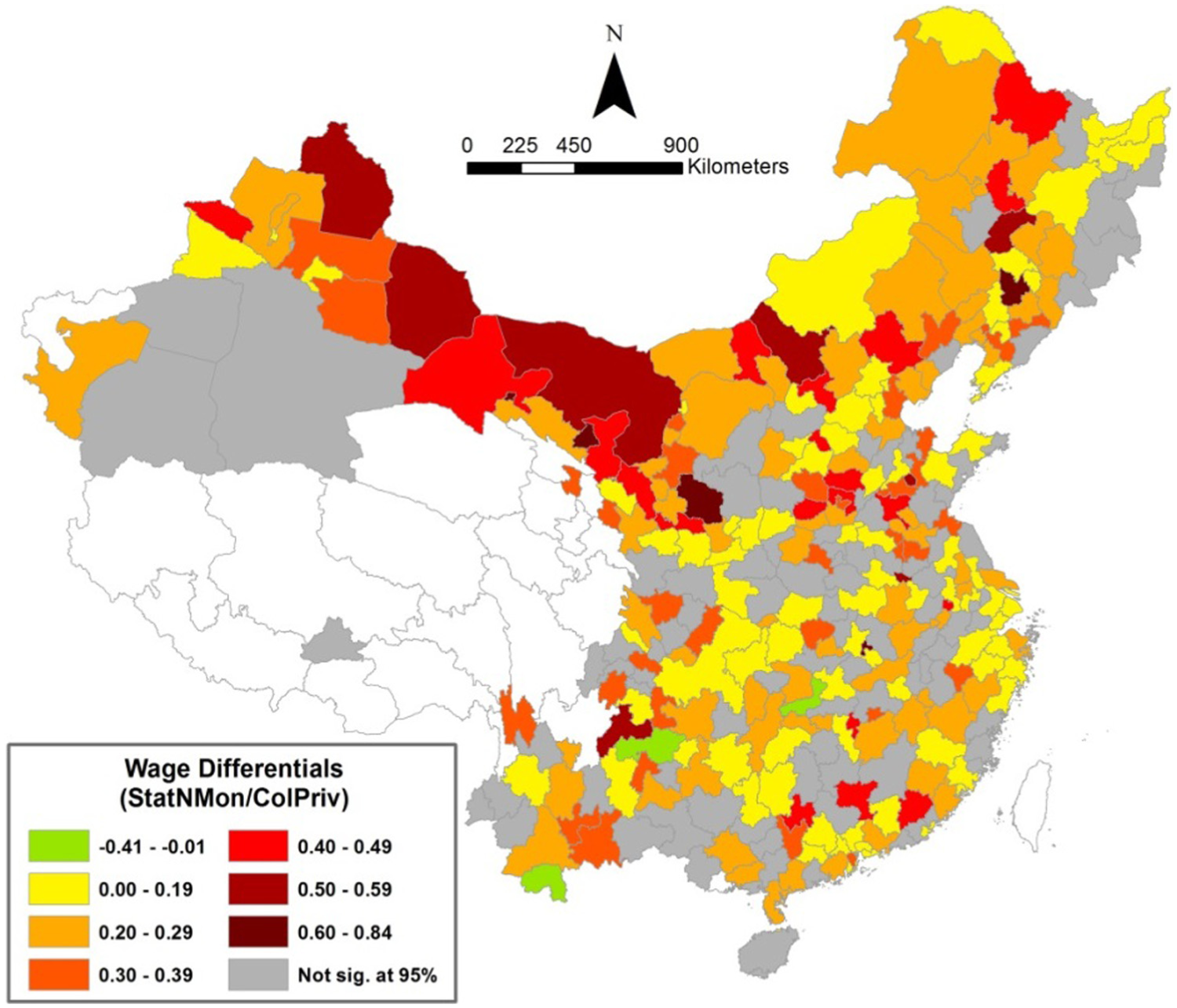

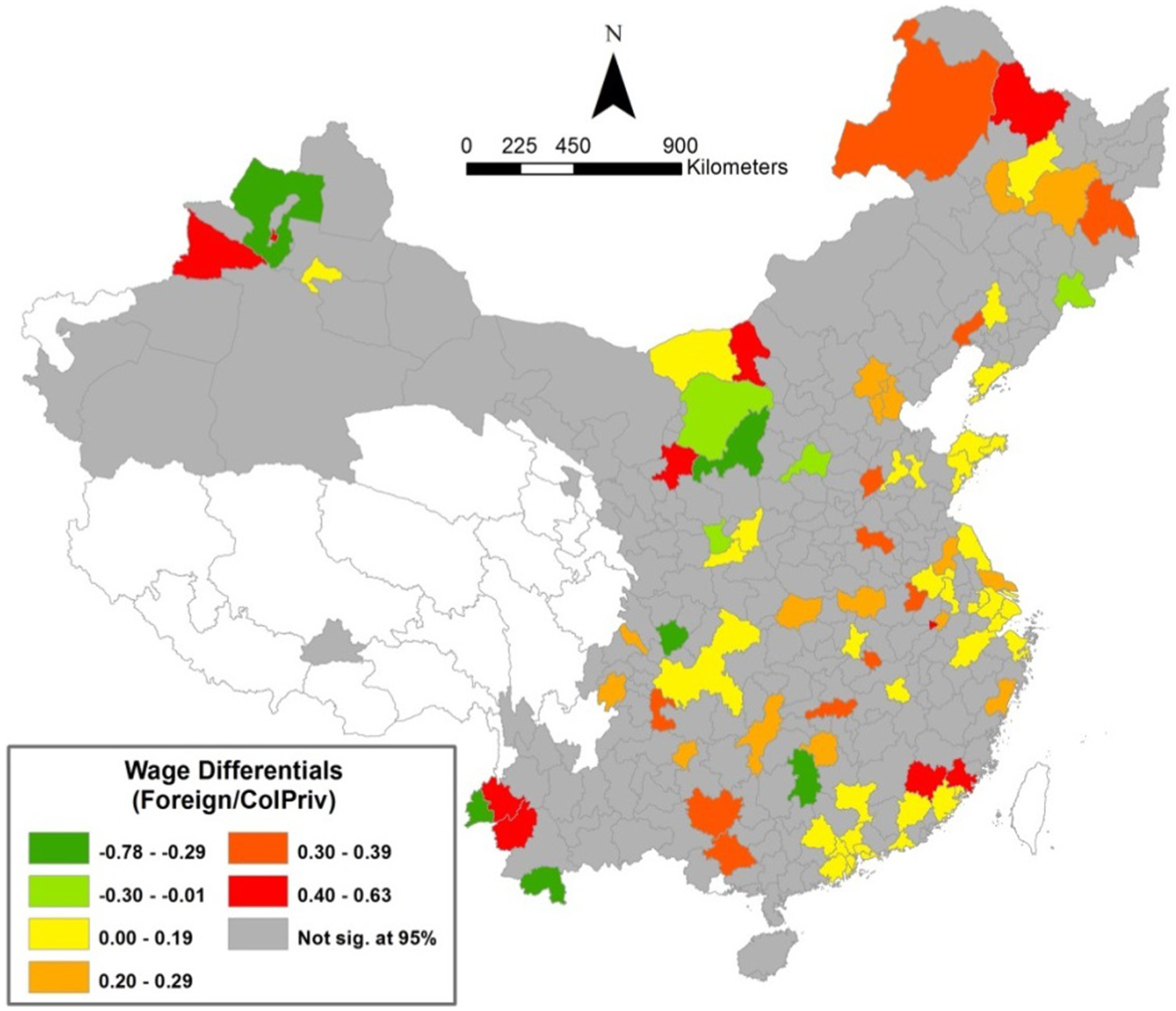

Figures 1–4 illustrate the inter-prefecture variability in the wage differentials between the collective and domestic private sector and each of the other four sectors. We assumed that, in the extreme case, different prefectures may have totally different wage-setting systems and, therefore, ran a single-level OLS regression separately for each of the 320 prefectures (Hauser and Xie, 2005). In these 320 regressions, the dependent variable is the hourly wage, including base wages, bonuses and subsidies, in logarithmic form, 4 and the independent variables include four sectoral dummies and other individual-level variables listed in the upper panel of Table 1. Based on the results from these 320 regressions, we mapped regression coefficients for four sectoral dummies throughout the country using the collective and domestic private sector as reference. A coefficient of 0.1 indicates that, on average, the employees of the public service sector (or other three sectors) earn approximately 10 percent more than their counterparts of the collective and domestic private sector in the same prefecture when all other individual-level variables are controlled.

Independent variables in the multilevel model.

Source: A, micro-data sample from 2005 Survey; B, China Statistical Yearbook for Regional Economy, 2002–2006 (for some prefectures, the missing values of some years were estimated through average treatment); C, Economic Census Yearbook 2004 for all provinces other than Anhui and Guangxi (data about these two provinces are aggregate provincial data from the China Economic Census Yearbook 2004).

Wage differentials between the public service sector (PubServ) and the collective and domestic private sector (ColPriv).

Wage differentials between the state monopoly sector (StatMon) and the collective and domestic private sector (ColPriv).

Wage differentials between the state non-monopoly sector (StatNMon) and the collective and domestic private sector (ColPriv).

Wage differentials between the foreign-invested sector (Foreign) and the collective and domestic private sector (ColPriv).

Figures 1–4 show the existence of significant regional heterogeneity in wage differentials between economic sectors. When all other individual-level variables are controlled, 276 and 284 prefectures show a statistically significant wage premium for the public service sector and the state monopoly sector, respectively. Although nearly all provinces display a wage premium for the public service sector and the state monopoly sector, only prefectures located in the interior region, especially Northeast China, Northwest China, Inner Mongolia and Yunnan, show a large wage premium for these two sectors. Among these prefectures are centres for petroleum extraction and processing (e.g. Daqing and Karamay), tobacco production (e.g. Yuxi) and the production of electric power (e.g. Huainan).

In contrast, 223 prefectures have a significant wage advantage for the state non-monopoly sector, and most prefectures with a large wage advantage for the state non-monopoly sect are scattered across the central and western regions. The economy of these cities is mostly undiversified and dependent on energy, mining and heavy industries as such coal mining and processing (e.g. Datong, Pingdingshan and Hebi), metal ore mining (e.g. Jinchang and Panzhihua), metallic manufacturing (e.g. Jiayuguan, Anshan and Handan) and machinery manufacturing (e.g. Baotou and Anshan). Only 83 prefectures exhibit a significant wage advantage for the foreign-invested sector. These are mostly located in coastal areas, especially the Pearl River Delta, Yangtze River Delta, Bohai Economic Rim and South Fujian. This is consistent with the fact that coastal areas are more likely than the rest of China to be home to foreign-invested enterprises (Chen et al., 2011). In addition, some large inland cities (e.g. Xi’an, Chongqing, Wuhan and Changsha) and some famous border cities (e.g. Mudanjiang and Hulun Buir) also show a significant wage advantage for the foreign-invested sector.

The multilevel modelling framework

We further employed the multilevel model to quantify the effects of individual and contextual factors on wage differentials between economic sectors (Goldstein, 2011; Parks, 2012; Wang, 2008). 5 Two-level models were used to estimate the wage differentials between the collective and domestic private sector and each of the other four sectors. The collective and domestic private sector was chosen as the reference category. In the model, 318,205 individuals at level 1 were nested within 320 prefectures at level 2. A level 1 equation is specified as follows:

where Yij is the logged hourly wage of individual i in prefecture j. X1ij, X2ij, X3ij and X4ij are sectoral dummies representing the public service sector, the state monopoly sector, the state non-monopoly sector and the foreign-invested sector, respectively, for individual i in prefecture j, and their corresponding coefficients (β1j, β2j, β3j, β4j) represent the wage differentials between the collective and domestic private sector and each of the other four sectors in prefecture j. The level 1 intercept (β0j) represents the average wage for the collective and domestic private sector in prefecture j. A vector of individual-level variables,

Our two-level models split spatial variation in the average wage for the collective and domestic private sector and inter-sectoral wage gaps into fixed and random components. For the fixed part, a vector of prefecture-level variables,

As for prefecture-level variables, two variables were used as a proxy for market expansion. The share of industrial output produced by the non-state sector (NSOUTP) was used to measure the degree of ownership diversity, and a high value of NSOUTP indicates a full market penetration in the scope of production activities (Fan et al., 2010). The ratio of foreign investment to GDP (FORINV) was employed to capture the degree of foreign openness, and a high value of FORINV denotes a high degree of globalisation and a high level of openness to foreign capital (Fan et al., 2010).

Two variables were used as a proxy for state intervention. The ratio of employment in monopoly industries to employment in non-monopoly industries (MONOP) was used as a proxy for the state control over industries, and a high value of MONOP means stringent state regulations (Bian and Zhang, 2002; Yue et al., 2011). The ratio of fiscal expenditure to GDP (FISCAL) was intended to measure the redistributive power of the state, and a high value of FISCAL denotes a strong government distribution power (Fan et al., 2010).

In addition, three controlled variables were included in the models. First, given that large-sized firms tend to pay higher wages than small-sized firms (Chen et al., 2011), we used the average size of enterprises (AVESIZE) to capture the effect of economies of scale. Second, given that capital-intensive firms tend to offer higher wages than labour-intensive firms (Chen et al., 2011), we used the regional level of fixed assets per employee (CAPINT) as a proxy for capital intensity. Third, we included a regional dummy (COAST) in the models to control for unobservable location-related factors (Chen et al., 2005; Démurger et al., 2012).

Results

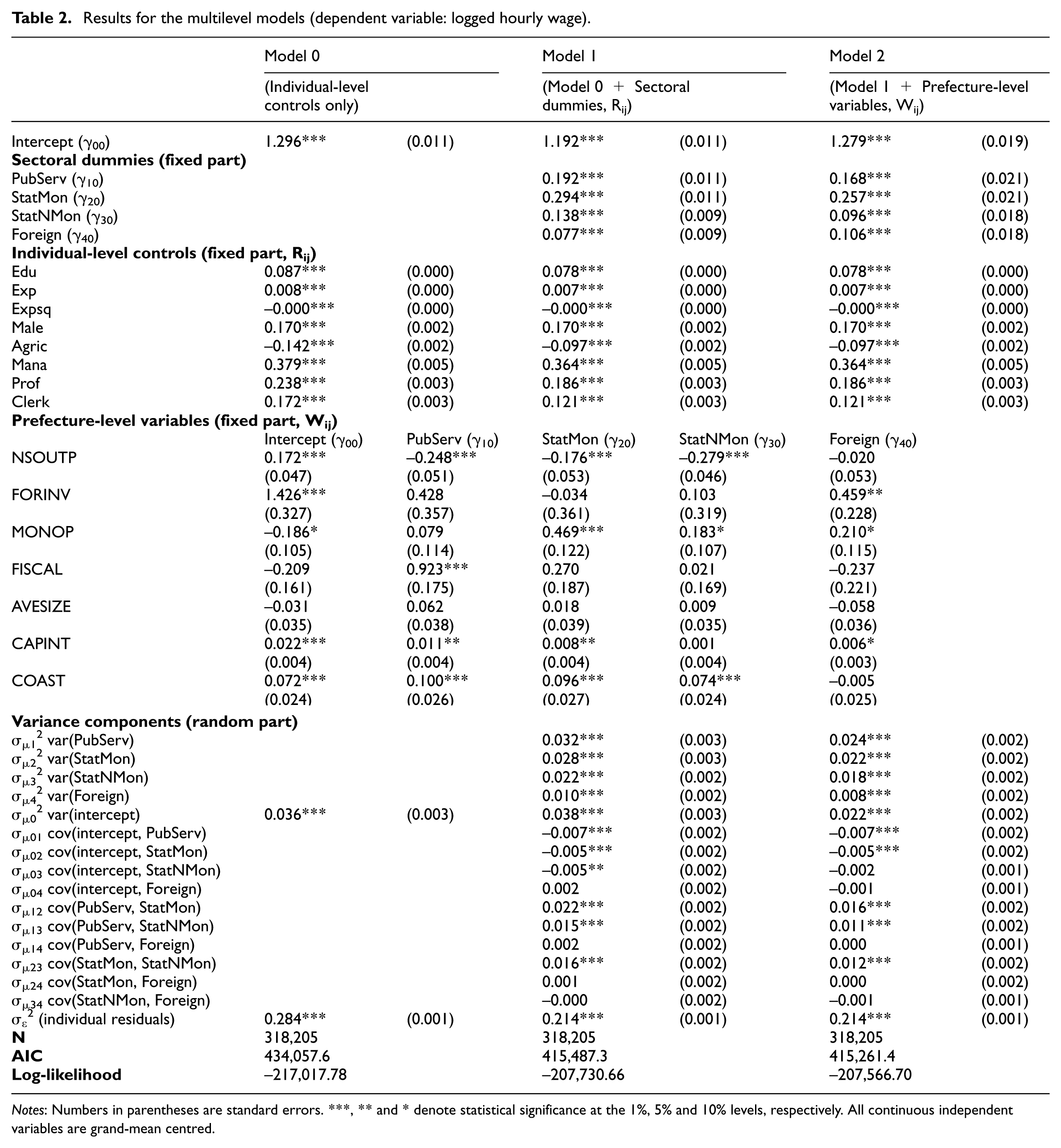

Table 2 presents the results for the multilevel models specified in equations 1–6. In terms of model adequacy, a likelihood ratio test and a comparison of the Akaike Information Criterion (AIC) between three models suggest that adding sectoral dummies and prefecture-level variables can significantly increase the explanatory power of the models. We firstly construct a model with individual-level variables other than four sectoral dummies (Model 0). All individual-level controlled variables are statistically significant and display expected signs. Given that the focus of this article is on how regional variations in market expansion and state intervention influence wage inequality across sectors, the coefficients of individual-level controls are not discussed any further in this article.

Results for the multilevel models (dependent variable: logged hourly wage).

Notes: Numbers in parentheses are standard errors. ***, ** and * denote statistical significance at the 1%, 5% and 10% levels, respectively. All continuous independent variables are grand-mean centred.

Model 1 includes not only individual-level controls but also four sectoral dummies. The coefficients of γ10, γ20, γ30 and γ40 represent the weighted grand mean of wage differentials between the collective and domestic private sector and each of other four sectors across 320 prefectures. On average, the average wages of the public service sector, the state monopoly sector, the state non-monopoly sector and the foreign-invested sector are about 19.2 percent, 29.4 percent, 13.8 percent and 7.7 percent, respectively, higher than that of the collective and domestic private sector.

Model 2 includes not only all individual-level variables but also prefecture-level variables. When prefecture-level variables are added to Model 1, the wage premium of state sectors decreases, and the wage premium of the foreign-invested sector increases. As shown in Model 2, the average wages of the public service sector, the state monopoly sector, the state non-monopoly sector and the foreign-invested sector are about 16.8 percent, 25.7 percent, 9.6 percent and 10.6 percent, respectively, higher than that of the collective and domestic private sector. This study particularly focuses on the coefficients for prefecture-level variables and their interaction terms with four sectoral dummies. The coefficients associated with NSOUTP and FORINV support our Hypothesis 1 that the relative wage of non-state-sector employees is higher in areas with a higher level of market growth. Specifically, a one-percent increase in the NSOUTP results in a decrease in the hourly wage for the public service sector, the state monopoly sector and the state non-monopoly sector by about 0.25 percent, 0.18 percent and 0.28 percent, respectively, relative to that for non-state sectors. 6 A one-unit increase in the FORINV results in an increase in the hourly wage for the foreign-invested sector by about 45.9 percent relative to that for other sectors. Overall, the diversity in ownership forms particularly affects the wage gap between the state and non-state sectors, while the openness to foreign investment particularly influences the wage differentials between the domestic-invested and foreign-invested sectors.

The coefficients related to MONOP confirm our Hypothesis 2 that a stringent regulation of the government on industries increases the wage premium in the state monopoly sector. Specifically, a one-unit increase in the MONOP causes an increase in the hourly wage for the state monopoly sector, the state non- monopoly sector and the foreign-invested sector by about 46.9 percent, 18.3 percent and 21.0 percent, respectively, relative to that for the collective and domestic private sector. This finding suggests that the wage gap between the state monopoly sector and the non-monopoly sector increases with more government regulation. The coefficients related to FISCAL support our Hypothesis 3 that the wage premium in the public service sector is higher in areas with stronger redistributive power. Specifically, a one-unit increase in the FISCAL results in an increase in the hourly wage for the public service sector by about 92.3 percent relative to that for other sectors.

As for the control variables related to general firm characteristics, the wage differentials between the collective and domestic private sector and other sectors are not influenced by the change in the average size of enterprises (AVESIZE). A one-unit increase in the degree of capital intensity of enterprises (CAPINT) results in an increase in the hourly wage for the public service sector, the state monopoly sector and the foreign-invested sector by 1.1 percent, 0.8 percent and 0.6 percent, respectively, relative to other sectors. In addition, prefectures located in coastal provinces (COAST) relative to those located in the central and western regions tend to display a higher hourly wage in the state sectors relative to the non-state sectors.

Discussion and conclusion

Using the 2005 Survey data and multilevel models, this article has examined the geographic variability of wage differentials between economic sectors in urban China. The results from single-level regressions for each of 320 prefectures have indicated that sectoral wage differentials vary substantially across regions. More specifically, prefectures located in the interior region tend to exhibit a large wage premium for the state sectors, while prefectures located in the coastal region tend to display a wage advantage for the foreign-invested sector. The results from multilevel models have shown that market expansion interacts with state intervention to reconfigure earnings outcomes: the wage gap between the state and non-state sectors is smaller in areas with diversified ownership; openness to foreign investment increases the relative wages for the foreign-invested sector; stringent government regulation of industries increases the wage gap between the state monopoly sector and the non-monopoly sectors; and strong redistributive power increases the wage premium for the public service sector over other sectors.

This article makes conceptual and empirical contributions to the study of wage inequality across economic sectors in urban China. Conceptually, it has incorporated both ownership segmentation and administrative monopoly into the framework of wage inequality across sectors, and empirically, it has proposed a new approach to classify Chinese economic sectors in recent years. Our findings have shown that employees in the state monopoly sector earn much higher than those in both state and non-state non-monopoly sectors, and that the wage premium for the state monopoly sector over non-monopoly sectors is determined primarily by government regulations on industries, when all other prefecture- and individual-level variables are controlled. Therefore, we attribute the rising earnings inequality in recent years partly to the combination effect of ownership segmentation and administrative monopoly. It should be noted that our wage data contain respondents’ earnings including wages, bonuses and subsidies, but hidden income and employee benefits may not be reported. This may cause an underestimate of income gaps between the state sector and the non-state sector, since workers in the state sector have more opportunities to reap hidden income and enjoy more favourable benefits than their counterparts in the non-state sector (Xie and Wu, 2008).

This study goes beyond the existing literature by examining the effect of market transformation on wage differentials between sectors within a multifaceted and multilevel framework. Rather than focusing exclusively on the role played by seemingly irresistible market penetration, we have viewed market expansion and state transformation as two separate but interrelated processes. The empirical evidence of this article has indicated that sectoral wage differentials in China are mediated by not only market expansion but also state intervention, and that these two forces contribute to regional variations in wage inequality in China. Our findings have not only supported Bian and Zhang’s (2002) assumption that China’s state has transformed its role from a redistributive state to a regulative state in response to the expansion of market, but have also quantitatively measured the extent to which both redistributive power (proxied by government spending) and regulatory power (proxied by the administrative protections of state monopolistic enterprises) influence earnings inequality.

Furthermore, our findings support the assumption made by some economic geographers that labour markets are spatially constituted and locally contingent, and that an individual’s employment outcome is not only determined by his/her personal attributes but also influenced by local labour market conditions (Parks, 2012; Peck, 1996). Little research has so far been done on delving into the impact of local conditions on labour market outcomes in the Chinese context, with a few exceptions such as Xu et al. (2006) and Chen (2011). Consequently, there is a great need to take into account contextually constituted and locally specific wage-setting mechanisms when studying China’s wage inequality.

Although our conclusion is based on survey data collected in 2005, the situation regarding to the wage premium of public and state monopoly sectors and heavy state involvement in economic affairs is still ongoing in the mid-2010s. First, strategic industries such as petroleum extraction, tobacco, State Grid and telecommunication were still firmly in the hand of the state, and in some capital-intensive industries such as coal mining and real estate which were once open to all private investors, state-owned enterprises strengthened their dominance in the market through acquisitions and mergers (as Wines (2010) put it, ‘the state sector advances, and the private sector retreats’). Second, state-owned enterprises benefitted more from the Chinese government’s stimulus package than their privately owned counterparts in recent years. For example, the Chinese government launched a large stimulus plan in 2008–2010 to combat the global financial crisis, yet this stimulus plan resulted in a surge of investment and bank loans in the state sector (Johansson and Feng, 2016). Third, the wage advantages of state monopoly sectors over private sectors remain apparent in the mid-2010s, as state-owned monopoly enterprises still reap excessive profits through scale economies, price manipulation and administrative protection. Therefore, research findings from this study are still valuable to the understanding of the more recent situation of Chinese labour markets.

It should be noted that this exploratory study merely focuses on the impact of market transformation, instead of a comprehensive set of contextual factors, on wage inequality in China. The next step of our research is to incorporate more macro-level structural factors such as industrial mix, labour force composition and macroeconomic policies into the analysis and to investigate the geographic variability of wage inequality by gender, class and the rural-urban divide. Another limitation of this study is that the estimation of our multilevel models might be biased by the presence of unobserved heterogeneity (i.e. variables related to individual characteristics that are unobserved but correlated with observed variables). For example, an individual’s possibility of entering the public and state monopoly sectors is likely to be influenced by his/her social capital and political capital, which are not observed due to the limitation of the data. Failing to address this problem will cause an upward bias in the coefficients of the public and state monopoly sectors. Future research on wage inequality in China is needed to address the issue of unobserved heterogeneity based on higher quality data and more advanced econometric techniques such as instrumental variables methods and Heckman correction for selection bias.

Footnotes

Acknowledgements

The authors would like to thank Jing Shen, Mingrui Shen and the anonymous referees for their valuable comments.

Funding

This work was supported by the National Natural Science Foundation of China (41501151, 41329001); the China Ministry of Education (11JJDZH006); the National Key Technology R&D Program (2012BAI32B07); and the Research Centre for Urban and Regional Development, Hong Kong Institute of Asia-Pacific Studies. This research is also supported by the Program for Professor of Special Appointment (Eastern Scholar) at Shanghai Institutions of Higher Learning.