Abstract

Echoing the recent revival of elite studies, we ask how financialization shapes the composition of contemporary elites and how organizational mechanisms transform its characteristics in terms of class, gender and race. We ask whether the bureaucratization of finance contributed to a ‘purge’ of particularisms. Or to the contrary, whether class, race and gender have become more salient criteria of elite selection with the emergence of neo-patrimonial organizational forms? Using Orbis data on legal forms of financial firms, and original sociodemographic data on founders and managers in key firms, we show that neo-patrimonial organizational forms based on trust networks are spreading within finance. Moreover, we demonstrate the impact of organizational forms on elite reproduction along gender, race and class lines. White men with upper-class background are over-represented in neo-patrimonial firms – mostly found in the hedge fund and private equity industry − compared to bureaucratic firms mostly found in banking. We suggest that financialization is not a modernization process but a recombination of bureaucracy and neo-patrimonial logics.

Introduction

Financialization, the ‘increasing importance of finance, financial markets, and financial institutions to the workings of the economy’ (Davis & Kim, 2015, p. 203), is a major trend since the 1980s (Krippner, 2005; Van der Zwan, 2014). Especially in liberal market economies such as the United States and the United Kingdom, financialization contributes significantly to the rise of inequalities and shapes the nature of contemporary elites (Piketty, 2014; Roberts & Kwon, 2017; Savage & Williams, 2008). In this article we echo the recent revival of elite studies and investigate the transformation of elites through the lenses of class, gender and race (Cousin et al., 2018; Glucksberg, 2018; Khan, 2012; Savage, 2014, 2015; Young et al., 2021). Our specific contribution is to connect recent literature on elites with analyses of organizational mechanisms, to show how the latter shift boundaries of elite composition (Acker, 2006; Neely, 2022).

We examine two organization-related theses about how financializaton affects elites. First, we investigate whether business elites become more meritocratic by a supposed dynamic of modernization and organizational renewal of finance (Morrison & Wilhelm, 2007). In this perspective, bureaucracies are supposed to ‘purge particularism’ as they ‘operate on the basis of formal rationality, with formalized procedures for the selection of employees, . . . as opposed to particularistic tendencies based on personal loyalties and/or ascribed characteristics’ (Stainback et al., 2010, p. 230). As a result, trust relationships based on class, gender or race would lose their influence and analytical skills and competencies would become more important (Savage, 2015; Savage & Williams, 2008). A second strand of literature, opposed to this, posits that in the same financial sector, such particularistic tendencies – selection and promotion based on gender, race or social background – have remained important or were even reviving over the last decades (Neely, 2022; Rivera, 2016; Soener & Nau, 2019). These authors state that in the hypermodern financial sectors ‘patrimonial’ tendencies have survived or have even become more important in the last decades.

We study the contribution of organizational forms to elite reproduction and link this focus to classical questions of a sociological approach to elites (Savage, 2015; Zald & Lounsbury, 2010). We are interested in how the composition of the US-American financial elite is reproduced in terms of race, gender and class – we do not examine reproduction as the relationship between (elite) parents and their offspring. Building on recent contributions in economic sociology (Lin & Neely, 2020; Soener & Nau, 2019), we develop and test a ‘neo-patrimonial’ hypothesis according to which the rise of ‘hybrid organizational forms’ favors the reproduction of elites along gender, class and race lines. By ‘hybrid organizations’ we understand mainly limited liability companies (LLCs) and limited partnerships (LLPs). These organizations’ ‘legal-organizational structure combines benefits of corporate status like limited liability without burdens like full public disclosures, rigid governance structure and double taxation, making them something of a “hybrid business”’ (Soener & Nau, 2019, p. 401). Whereas bureaucracy’s impersonal rules should have a mitigating effect on class, gender or race related reproduction, the trust network of patrimonial organizations should amplify it.

We evidence this argument in three steps. First, we hypothesize that hybrid organizational forms have become increasingly important in specific segments of the finance industry (private equity and hedge funds) but not in others (asset management, banking). Second, we posit that the founders of these neo-patrimonial firms are disproportionally sourced from traditional elite groups (upper-class white men). These groups have the resources (in terms of wealth, social status and networks) both to found new financial firms and to make them successful. Third, we argue that even in 2018, financial elites who are men, white and upper class tend to get preferentially selected in hybrid organizational firms compared to public firms. We posit that the reason is that these hybrid organizational forms favor a particular organizational inequality regime based on trust networks.

Our analyses draw on firm-level Orbis data to locate LLCs and LLPs within the financial industry, and on a stratified sample of 806 individuals, who in 2018 occupied top positions in the 40 largest organizations in key segments of the US financial field. Overall, our results confirm that hybrid firms are dominant and increasing in hedge funds and private equity. Moreover, ‘upper-class white men’ are over-represented among founders and top managers within hybrid organizations, holding constant their educational backgrounds and social networks. We conclude that neo-patrimonialism, as a form of organizational mechanism, leads to higher rates of elite reproduction than bureaucracy.

This article is organized as follows. First, we review the recent literature on elites and how it reconnects with theories of class, gender and race. We then develop an analytical framework to explain differential rates of elite reproduction in the US financial elite. After a presentation of our data and methods, we show the results and discuss their theoretical implications for the links between organizational forms and the classed, gendered and racial characteristics of elites.

Theoretical background

Elite research and organizational mechanisms

In 2014 Thomas Piketty published his book Capital in the 21st Century. In it, based on historical data series, he shows that capitalism, without the intervention of counterbalancing forces, inevitably increases the inequality of wealth – as the return on capital is almost always bigger than economic growth. In sociology, Piketty’s work on wealth distribution was a crucial catalyst for a mutual rediscovery between research on elites and class analysis (Savage, 2104, 2019).

On the one hand, Piketty has put very wealthy elite groups again in the spotlight of social science research. The evidence on the growing inequalities to which these elite groups contributed let sociologists rediscover the divide between the middle classes and the upper classes – which, particularly in the UK, has been long overshadowed by a focus on the conflict between working and middle classes. This initiated many studies which investigated elites explicitly or put a special emphasis on the higher echelons of the class structure (Korsnes et al., 2017; Kuusela, 2018; see also Cousin et al., 2018; Khan, 2012). On the other hand, Piketty’s book also led to calls to study inequalities and the groups at the very top through a sociological lens (Savage, 2014). In this view, elites became a group with a specific economic position (not just a political group with influence as in Weber’s account) that can be conceptualized with class theory. What is more, Piketty’s emphasis on family and intergenerational transmission also inspired research on the role of family, women and gender in the formation and persistence of elite groups (Bessière & Gollac, 2023; Glucksberg, 2018; Higgins, 2022; Keister et al., 2022). Finally, Piketty’s second book, Capital and Ideology (2020), focused on comparative questions and the colonial relationships and thereby initiated research on elites and race (Young et al., 2021).

In this contribution, we seek to connect this debate to the literature on organization and apply it to one of the dominant industries of contemporary capitalism – finance. We seek to show how organizational mechanisms contribute to the formation of elite groups (Palmer & Barber, 2001; Stearns & Allan, 1996; Tomaskovic-Devey & Avent-Holt, 2019; Zald & Lounsbury, 2010) and argue that – even in supposedly hyper-rational finance – organizations are never ‘neutral’. Organizations are crucial sites of class (Palmer & Barber, 2001), gender (Acker, 2006) and race (Ray, 2019) related group formation and production of inequalities. Acker (1990), for instance, showed that organizations not only produce gender segregation, but also income and status inequality, cultural images of gender and specific gender identities. Similarly, Ray’s theory of ‘racialized organizations’ (2019) argues that organizations ‘enhance or diminish the agency of racial groups’, ‘legitimate the unequal distribution of resources’ and transform whiteness into a credential (Ray, 2019, p. 26). These theoretical insights are reflected in numerous empirical studies assessing the influence of organizational features on discrimination practices and managerial diversity (Bielby, 2012; Reskin & McBrier, 2000; Stainback et al., 2010). Even though we do not adopt here an explicitly intersectional perspective, we think that the potency of racial, class related or gender related attributes can be reinforced by their interrelation (Crenshaw, 1989).

Financial intermediaries as the new financial elite

Why is it relevant to study elite reproduction in the context of finance? The financialization of the economy has profoundly transformed the field of economic relations in the US in the 1980s and 1990s. The idea at the heart of financialization is that firms should first and foremost maximize their shareholder value (Lazonick & O’Sullivan, 2000). This helped a new group of firms, the so-called ‘financial intermediaries’, to gain central power positions in capitalism. These firms – asset management firms, private equity firms, investment banks or hedge funds – increasingly reallocated streams of money between large institutional investors (such as pension funds, insurers or sovereign wealth funds) and corporations so that they became the most important corporate shareholders. The individuals at the helm of these financial firms – founders, owners, partners and top-managers – can be considered as the most powerful contemporary elites, for three reasons (Moran & Flaherty, 2023): First, these individuals are among those reaping the highest compensations, not only in form of salaries or bonuses, but also through dividends or participation in the profits made through investments (Ajdacic, 2022). Second, these individuals occupy crucial relational positions within ‘financialized networks of accumulation’ (Moran & Flaherty, 2023, p. 1165) and, as leaders of institutional investors, shape the strategic decisions of the companies they control (Davis, 2009; Fligstein, 1990). Third, these individuals are politically powerful and able to ‘activate and shape institutional and regulatory systems to their advantage’ (Moran & Flaherty, 2023, p. 1167). But the rise of the financial intermediaries transformed the financial field also in another way: some of them were only recently founded, relatively small and organized in new organizational forms – different from the bureaucratic structures of the large, traditional banks. We might distinguish four types of financial intermediaries.

Historically at the heart of the financial field, the core business of investment banks has been fee-based consultancy serving mergers and acquisitions (due diligence, risk analysis, deal structuring, etc.). In addition, investment banks originate and distribute financial products (bonds, securities, derivatives) and trade on the financial markets, either on their own account or as brokers for institutional clients. Since the early 1970s, a dynamic of rationalization and bureaucratization has accompanied the strategic shift of these firms from corporate finance to the trading of financial securities, an activity often complex and more and more automated. Mirroring industrial firms, all major investment banks abandoned their status as partnerships and became public firms during this period; after the repeal of the Glass–Steagall Act in 1999 (which at its introduction in 1933 separated commercial and investment banking), some of them even merged with large commercial banks. Traditional investment banking (based on community and trust) was being replaced by strategies increasingly based on scientific skills, meritocratic promotion mechanisms and bureaucratic principles (Morrison & Wilhelm, 2007).

Arguably asset management firms are the most important players in the world of contemporary finance (Davis, 2009; Fichtner et al., 2017). Even though some of these firms were founded in the 1930s, it is only since the reform of the US pension scheme in 1978 that their assets have grown substantially. These firms, often organized as bureaucratic corporations, ‘passively’ manage large portfolios of securities. They elicit cash from a large (mostly institutional) audience and invest it in shares, bonds and other types of financial instruments. Recently, index funds and exchange-traded funds have formed the core classes of investment funds.

Private equity firms first emerged in the 1960s, but their rise to prominence parallels the emergence of a market of corporate control and the (hostile) takeover movement in the USA in the 1980s – a central moment in the financialization of US economy. In the ‘leveraged buyout (LBO)’ business model, private equity firms seize control of targets and use the cash flow or (stripped) assets of the portfolio firm to secure and then repay the borrowed money, which typically represents 80% of the acquiring vehicle. Active investors, they use ‘operational’ and ‘financial engineering’ strategies to increase the share price of the targeted companies. In contrast to banks, even larger private equity firms such as Carlyle or KKR, are relatively small and often organized in hybrid organizational forms.

Hedge funds are a relatively heterogeneous group of investment funds, often actively managed, which promise high investment returns. Initially, hedge funds used to ‘hedge’ risks with specific investment techniques independent of any economic cycles. Since the early 2000s, they have become popular investment vehicles utilizing a large variety of strategies – from trading to debt restructuring – to avoid regulatory controls. Compared to other investment institutions, hedge funds are relatively small firms.

Even though the financial crisis of 2008 and the regulatory reaction in form of the Dodd–Frank Act in 2010, a general overhaul of US financial regulation, might have transformed the relative weight of these financial intermediaries, the system as a whole and the roles and positions of its elites remained surprisingly stable. While asset managers became ever more dominant since 2008 (Fichtner et al., 2017), hedge funds have (temporarily) lost in importance. Most investment banks, such as Merrill Lynch or JP Morgan, were forced to merge with larger commercial banks (and thus became more powerful).

Neo-patrimonialism and elite reproduction in finance

The classed, gendered and racialized nature of organizations are backed by observations of financial firms (Crompton & Le Feuvre, 1992; Ho, 2009; Souleles, 2019). Neely (2018), studying the hedge fund industry, speaks of ‘patrimonialism’ to make sense of the practices leading to white and male dominance in this sector. She defines it as authority based on the principles of ‘trust, loyalty and tradition’ (Neely, 2018, p. 366). The idea of striving or reviving patrimonialism is seducing but stands in contrast to theories and historical reviews of the US banking sector. Morrison and Wilhelm (2007) show that the period from 1960 to 2000 corresponds to a phase of profound modernization and bureaucratization of the US (investment)-banking sector, based on technological innovation, new organizational forms and more meritocratic selection of employees and managers. Since the 1980s, measures of ‘diversity management’ were introduced in many bureaucratic firms, such as banks, in an attempt to reduce ascriptive inequalities and simultaneously enhance productivity (Ashley, 2022). Bacharach and Mundell (2000) argue that the period since 1975 marks the triumph of an ‘ethnically diverse’ elite obsessed by financial performance. While ethnic diversity doubtlessly increased, it probably did not to the extent suggested by these authors (Zweigenhaft & Domhoff, 2018).

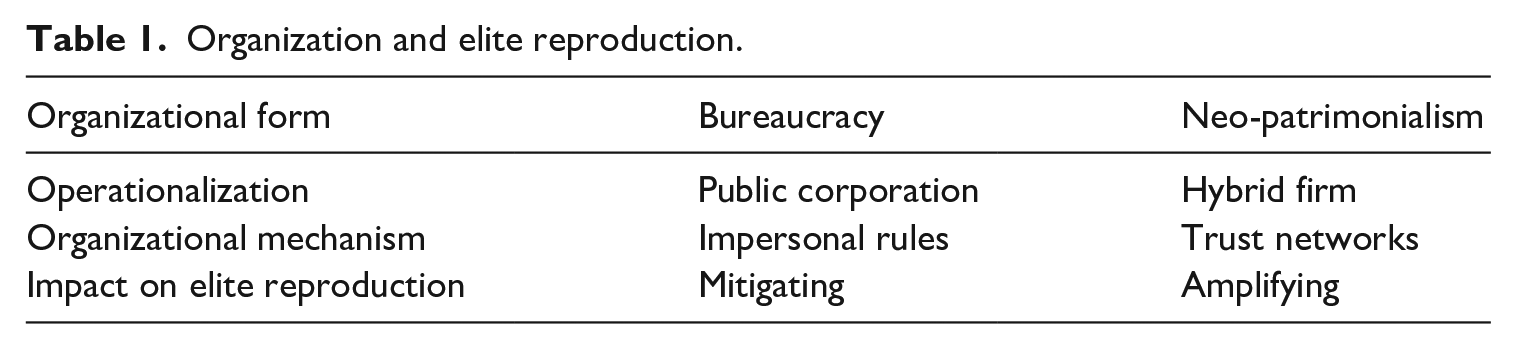

Even though the mentioned qualitative studies of finance are enlightening, we might wonder whether patrimonialism prevails more in some organizations than in others, and if this variation can help us understand how patrimonialism leads to inequality outcomes. In other words, beyond the practices these authors describe in specific financial sub-industries, what is the link between patrimonialism and elite formation? For us, a crucial link is organizational form. We thus propose to reframe, operationalize and test their propositions by contrasting patrimonialism with bureaucracy. We conceptualize bureaucracy and patrimonialism as competing organizational forms, whereby public firms are the operationalization of bureaucracy and hybrid firms the operationalization of patrimonialism (Soener & Nau 2019) (see Table 1).

Organization and elite reproduction.

Public corporations are good indicators of bureaucracy because they are the epitome of the ‘modern corporation’ (Berle & Means, 1991; Chandler, 1977). By contrast, partnerships are good indicators of patrimonialism because these organizational forms often rest on a familial basis and preexisted the rise of the modern corporation. Hybrid firms (LLPs and LLCs) are good indicators of neo-patrimonialism because they blend features of corporations with that of traditional partnerships (Soener & Nau, 2019).

These organizational forms entail different mechanisms of elite reproduction, which impact the social composition of these groups. In a bureaucratic organization, high formalization, high openness of positions and high environmental accountability generate inequality through impersonal rules. Impersonal rules are therefore the main organizational mechanism of elite reproduction in bureaucratic organizations. On the other hand, in patrimonial organizations, low formalization, less openness and low external accountability generate inequality from trust networks. In these organizations, there is usually no elaborated division of labor, individuals are often coopted in leadership positions, and the organizations’ goals are defined as private or even family related. Here the main mechanisms of elite reproduction are loyalty and trust. In line with Weber, we believe that impersonal rules, characteristic of bureaucracy, do not eliminate, but mitigate elite reproduction based on ascription, whereas trust networks amplify such elite reproduction and therefore lead to higher levels of inequality.

The neo-patrimonial hypotheses

In this section we show how the nexus between the type of organization and elite composition is created through firm founding and the recruitment and promotion criteria of firms.

The rise of hybrid firms

Historically, hedge funds and private equity firms were born out of a desire of specific banking elites to make more money through carried interest schemes and reduced tax rates allowed by partnership and hybrid legal status (Godechot, 2008; Neely, 2022). In addition, activities in the hedge fund and private equity sectors are marked by greater market uncertainty, which favors close cooperation in trusted environments and collaborations with socially similar partners (Neely, 2018). Their business models are based on trustful connections with clients and collaborators. To obtain ‘private information’ and to raise capital from their investors and source operations for LBOs and other acquisitions, financiers need to establish close, trusting relationships with economic elites of other sectors (Eaton, 2022).

Hypothesis 1: Within finance, hybrid organizational forms are growing and are dominant in hedge funds and private equity, but are less prevalent in investment banking and asset management.

The privilege of the founders

Trust networks are particularly important in the founding phase of new (financial) firms. Seed capital is by definition risky because the entrepreneur or future enterprise has not yet a track record of performance (Neely, 2022). In the initial phase of a firm, trust, or the belief that another party to a transaction will not take advantage of one’s vulnerability, is key (Cook & Gerbasi, 2006). Trust based on beliefs about collective traits tends to be particularly strong because the social attributes of individual humans provide stable reference points (Zucker, 1986). There is evidence that social similarity in terms of attributes such as gender, race and class has a positive effect on trust – whiteness or maleness becomes a credential (Neely, 2018; Ray, 2019; Simpson et al., 2007). We therefore expect that during the founding period of the private equity and hedge fund industries, those with traditional elite attributes – white men with upper-class background – have had better chances to found firms that would have become successful.

Hypothesis 2: Firm founders in the financial sector are more likely to be white men with upper-class background than other financial elites.

Trust-based recruitment

After the founding years of a firm, the importance of trust networks becomes more ambiguous. On the one hand, organizational growth implies structural inertia and possible entrenchment of a power group. On the other hand, the importance of trust networks may gradually decrease over time, as ‘charisma’ of founders is routinized through procedures for leadership succession (Weber, 2019). We argue that the relative weight of such effects varies with the organizational form. We know that informality produces higher amounts of gender or race related inequality (Acker, 1990). We thus expect that while trust networks remain important in partnerships and hybrid organizations, its centrality decreases in more bureaucratic organizational forms.

Hypothesis 3: In 2018 hybrid organizations have a higher likelihood of having white men, or people with upper-class background, at their helm compared to public corporations.

Data and methods

To respond to our first hypothesis about the spread of hybrid organizational forms we rely on firm-level data from Orbis. To test our second and third hypotheses on the nexus between organization and its directing personnel, we use a database on the 40 most important US financial firms, their top managers in 2018 and their founders (between 1975 and 2006).

Organizational forms

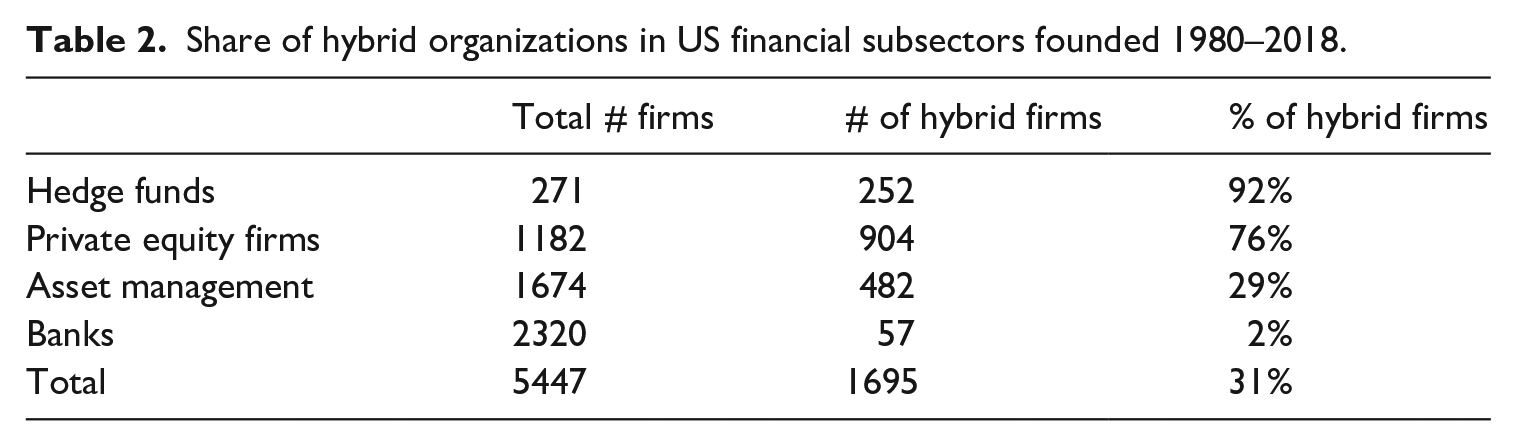

In a first step we focus on the organizational forms in the different subsectors of finance. While the data of the Internal Revenue Service are encompassing and historically very precise, they do not permit finer distinctions between financial subsectors (Soener & Nau, 2019). We therefore rely on the Orbis database and have recoded their variables on organizational forms and precise subsectors. We exported all active companies in the US with information on the incorporation date in the NACE Rev2 category 64 (financial service activities – export date: 15/08/20) and category 66 (activities auxiliary to financial services – export date: 21/08/20). The Orbis category ‘financial company’ is a catch-all for various types of financial entities; therefore, we rechecked this category manually, to identify hedge funds which were wrongly classified in the ‘financial company’ category. Based on the Orbis variable ‘type of entity’ we created four subsectors: private equity firm, hedge fund, bank and asset management. The asset management subsector corresponds to the subcategory SIC 672 and the subcategory NACE Rev 6420 within the Orbis category ‘mutual and pension fund/nominee/trust/trustee’. The banking subsector corresponds to the Orbis type of entity ‘banks’ and the variable sectors ‘Banking, Insurance & Financial Services’. We categorized the ‘national legal form’ into a binary variable (hybrid firm vs. corporate). Hybrid firms include ‘Limited liability companies/corporations’, ‘Sole proprietorship’ and all types of partnerships. Missing entries on the legal status for banking entities in Orbis were completed with the Factiva database. The initial downloaded dataset comprised 39,554 US financial firms. After homogenizing the entities by ID and name, restricting the sample to the period 1980–2018, the sample included 5981 entities with 8.9% missing values for legal form. The final sample contains 5447 firms (for details see Table 2).

Share of hybrid organizations in US financial subsectors founded 1980–2018.

Founders and top managers in 2018

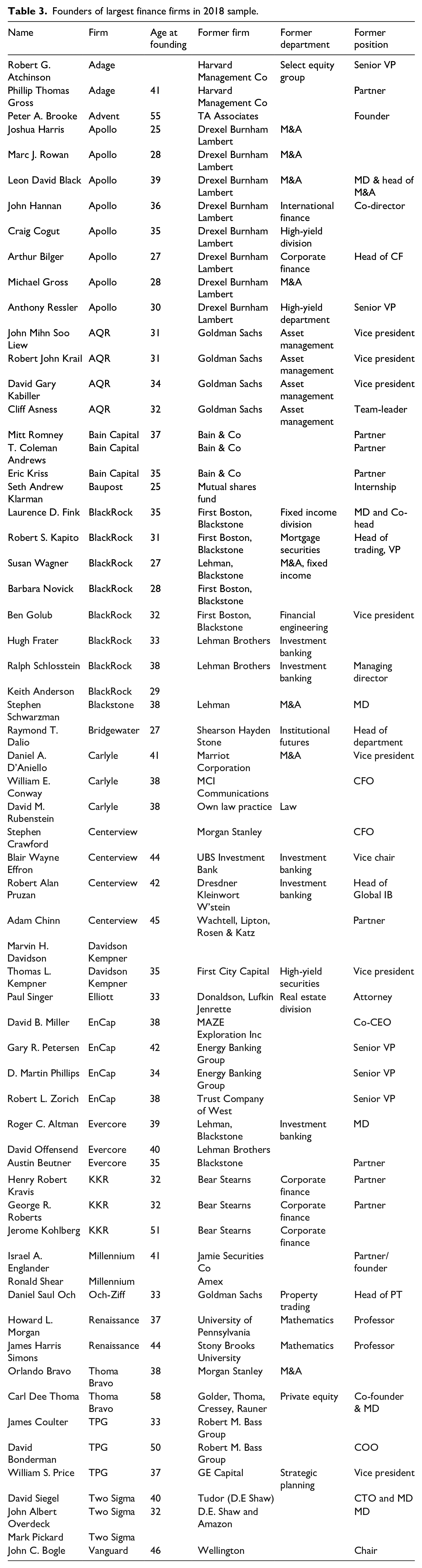

According to the ‘positional approach’ of elite sociology, elites are best studied by examining the actors occupying the most influential positions within the most powerful institutions in a given field (Hoffmann-Lange, 2018). Therefore, to study the social characteristics of the financial elites in different sectors and types of organizations, we rely on a sample of founders, directors and managers of the 10 largest US firms in the sectors of hedge funds, private equity, investment banks and asset managers in 2018 (Appendix A). We consider these to be the most relevant financial intermediaries and have decided to exclude venture capital (as a potential further important industry of financial intermediation), because it is closely linked to a specific industry (tech and biotech). Moreover, as many firms are active in two or more of these sectors, we have categorized the firms according to their main activity. We study both individuals who founded these firms between 1975 and 2006, and their 2018 top management cohort. For each firm we selected approximately 20 individual board members and top executives, including the founders listed in Table 3. The number of selected individuals by firm varies from 3 to 28. This number depends on the size of the board and the top-management teams – and also on the information we were able to collect on these individuals. We then collected information on these individuals based on Capital IQ, Boardex and Orbis (i.e. [commercial] financial information and analytics databases which include high quality information on the members of the boards and executive management teams of the globally most important firms). These sources are augmented by information found in the ‘directories’ module of Nexis Uni, in annual reports, in the press and on the internet. Our final sample is composed of 806 founders, directors and managers of the 40 biggest investment banks, asset management firms, private equity firms and hedge funds. Note that this positional method has certain limitations, notably concerning the cut-off criteria for the number of firms, the distinction between powerful and non-powerful positions and the weighting of specific sectors or position in the elite sample (Hoffmann-Lange, 2018).

Founders of largest finance firms in 2018 sample.

Variables

The independent variables are three social attributes: gender, race and social class. For race, we searched for pictures of the individual online and categorized the person using US Census categories (White, Middle Eastern, Black, Asian, Indian, Native). See Hermanowicz and Clayton (2020) or Brint et al. (2020) for a similar and recent coding scheme. The underlying assumption of this coding is that race is a categorization system enforced by social institutions on individuals, and that the main distinction in the US is between ‘white’ and ‘non-white’. Whenever there was a doubt, we did not code anything. The social class variable is whether the individual has a degree from an Ivy League university (either at undergraduate or graduate level). While these elite universities have become more diverse in terms of religious affiliation, race, gender and geographical origin, they continue to draw students from the most privileged class background (Karabel, 2005, pp. 536–557). Therefore, we assume that attendance of an Ivy League university is an indicator of upper-class origin (Domhoff, 1967; Karabel, 2005; Rivera, 2016) – even though also students from working-class background attend Ivy League universities. The Ivy League universities include Brown University, Columbia University, Cornell University, Dartmouth College, Harvard University, University of Pennsylvania, Princeton University and Yale University. Even though other definitions of elite university have been suggested recently (Bühlmann et al., 2022; Rivera, 2016), we argue that Ivy League universities do better capture the old and venerable nature of the privileged classes we try to identify here.

We know that women are less likely to be represented among PhDs, as well as in business and natural sciences (Bradley, 2000). We therefore include variables such as having an MBA, a PhD and a business or science degree as control variables. To code these degrees, we manually constructed a dictionary of terms and categories. We considered a degree in ‘Economics’ to be business related. Categories can overlap and in effect 9% of our sample have both a business related and science related degree. If no degree was mentioned, we considered that the individual did not have a degree.

The other control variable is social networks: minorities tend not to reach the top of organizations or societies due to their relative lack of connections and absence of membership in elite social networks. Based on information from Boardex, we control for whether the individual offers any such ‘non-professional’ activities. We categorized affiliations in 13 types and 30 subtypes by a combination of automatic (string matching) and manual allocation. As examples, the Council on Foreign Relations and the World Economic Forum are coded as ‘policy-planning network’; the Partnership for New York City, or the Robin Hood Foundation, are classified as ‘philanthropic organization’. If no information on such activities was mentioned, we considered that this person did not belong to any other organization.

The dependent variables are (1) whether the individual is a founder of one of the 40 organizations and (2) whether s/he belongs to a ‘hybrid’ organizational form or a public organizational form. We define a ‘hybrid’ form based on the analysis of legal form of US businesses by Soener and Nau (2019). We consider all LPs, LLPs, LLCs, private firms and holding companies as ‘hybrid’. Public companies and subsidiaries are defined as ‘public firms’ (Appendix A).

Analytical strategy

To examine hypothesis H1, we run a descriptive analysis of the yearly share of hybrid firms according to the subsector and present it in a line graph ranging from 1980 to 2023.

Hypothesis H2, on the privilege of founders, is analyzed by a series of logistic regressions in which we compare those who are founders (DV = 1) to those who are non-founders (DV = 0). As independent variables, gender, race and class (measured by Ivy League attendance) are used. As the influence of these variables might be confounded by level and domain of education (which is particularly gendered) as well as membership in elite social networks, we introduce other variables as controls. We present three models: Model 1 without controls, Model 2 with only educational controls and Model 3 with both educational and network-based controls.

Hypothesis H3 is examined with logistic regressions. Here the organizational form is the dependent variables: DV = 1 if the individual is a hybrid firm leader and DV = 0 if the individual is a leader of a public firm. The independent variables – gender, race and class – are used in the same way as for H2, with three models successively introducing educational and network-based control variables.

Results

The rise of hybrid firms within finance

Soener and Nau (2019) show that, generally, the financial sector relies substantially on hybrid organizational forms such as LPs, LLCs or LLPs. With our first hypothesis (H1) we add to this research by positing that there are decisive differences within the financial sector: hedge funds and private equity firms rely heavily on hybrid organizations; other subsectors such as banking and asset management, much less.

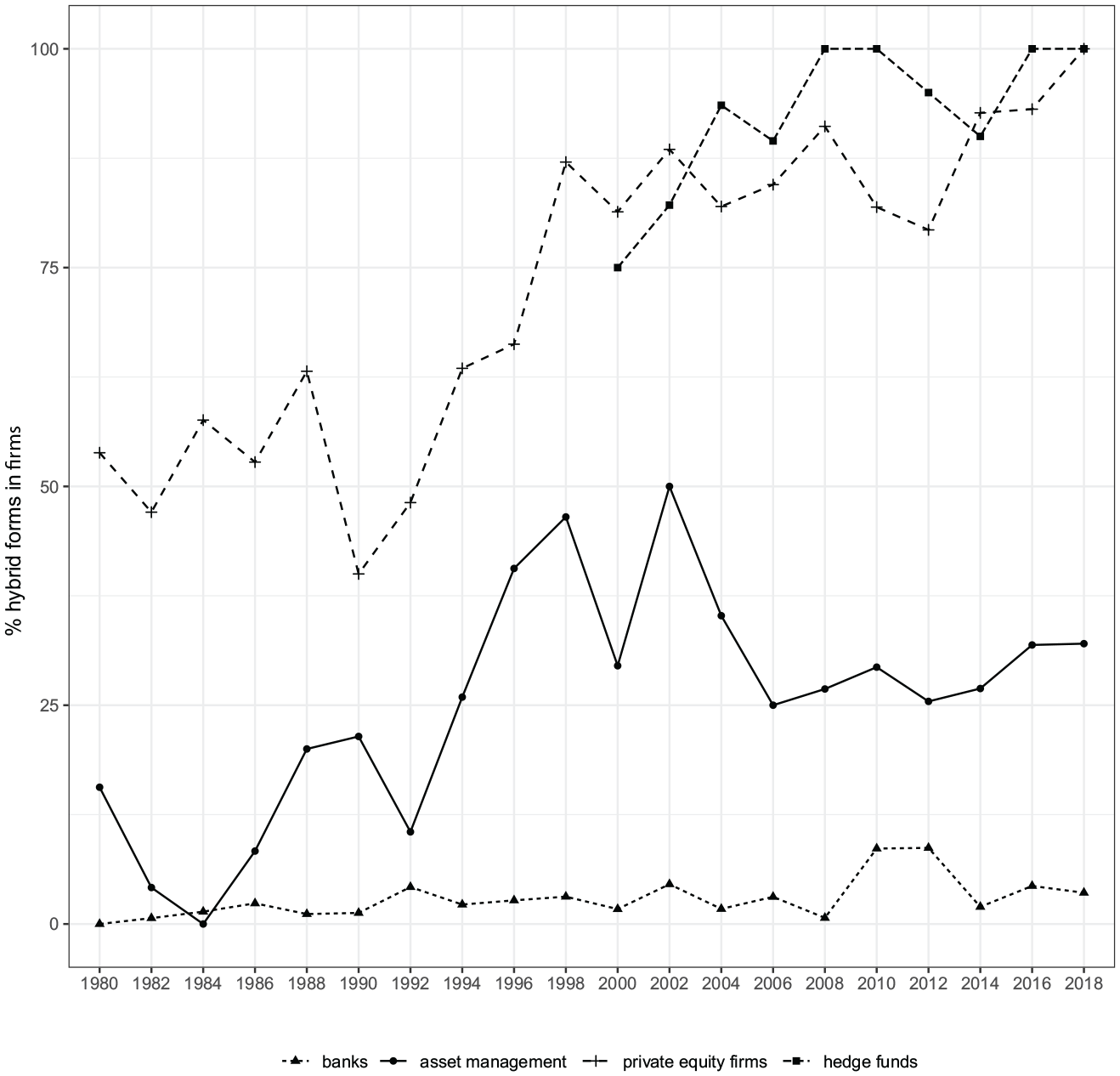

Our results show that whereas among entities founded between 1980 and 2018 only a small minority of 2% of banks are organized as a hybrid form, and around 29% of asset management firms are structured as hybrid entities, 92% of hedge funds and 76% of private equity firms are organized so (Figure 1).

Share of hybrid firms among subsector incorporations (1980–2018).

Historical analysis shows that the proportion of hybrid organizations among hedge funds, private equity and asset management firms rose steeply from about 1990. Only in the banking sector do we fail to observe such an increase in hybrid forms. This means that next to hedge and private equity funds, asset management has become more hybrid in recent decades, albeit capped at a lower level than hedge funds and private equity.

Overall, these results confirm our hypothesis that in terms of organizational forms there are major differences within finance. Both ‘modern’ bureaucracies and neo-patrimonial forms coexist in the current financial sector: although hedge funds and private equity have become increasingly dominated by hybrid organizational forms, asset management firms and particularly banks have remained organized as public firms.

The privilege of the founders

Our second hypothesis (H2) states that founders of new firms in the financial field are more likely to be white, men and with high social status compared to the average top managers of these firms. If we restrict the sample to those firms founded since 1975 and still among the 10 most important in their sector in 2018, we find only two asset management firms and two investment banks. In contrast, almost all the hedge funds and private equity firms that dominate in 2018 were founded between 1975 and 2001 (Appendix A). Not all, but most, of these firms are hybrid organizations (or at least were so when founded).

We have identified 63 founders of all the top financial firms created between 1975 and 2006 and compared them with the top management of financial firms in 2018.

Notice that most founders have worked in large (investment) banks before starting their own business. It is notable that the founder teams often worked together, for the same bank, even in the same departments within a bank (Godechot, 2008). This means that neo-patrimonial elements such as trust, a common work culture, a common habitus, loyalty and social similarities are of fundamental importance to the founding of these financial firms.

Even though our data give little insight into the motivations of these founders to quit modern bureaucratic banks, extant literature often provides anecdote about tensions and conflicts: we know for example that there were ‘rising tensions’ between the three founders of KKR and Bear Stearns, or that there was a conflict between Larry Fink and First Boston.

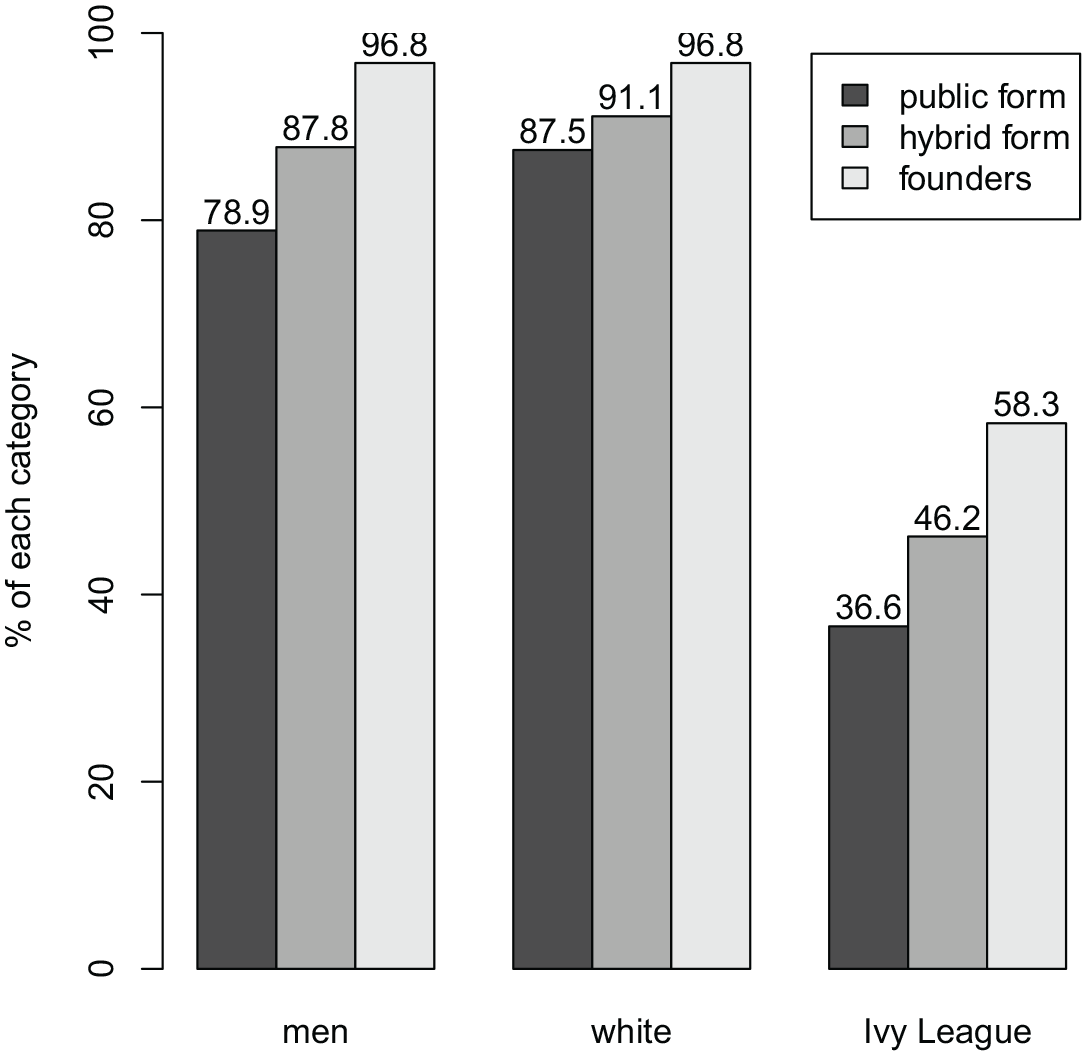

As expected from our hypothesis, founders form a very specific cohort possessing the characteristics of the powerful in a very concentrated way (Useem & Karabel, 1986). Ninety-seven percent of financial firm founders are white men. Almost 60% of founders have an Ivy League degree, compared with 46% (hybrid) and only 37% (public firms) of other cohorts in our sample (Figure 2).

Share of men, white and Ivy League graduates in the sample.

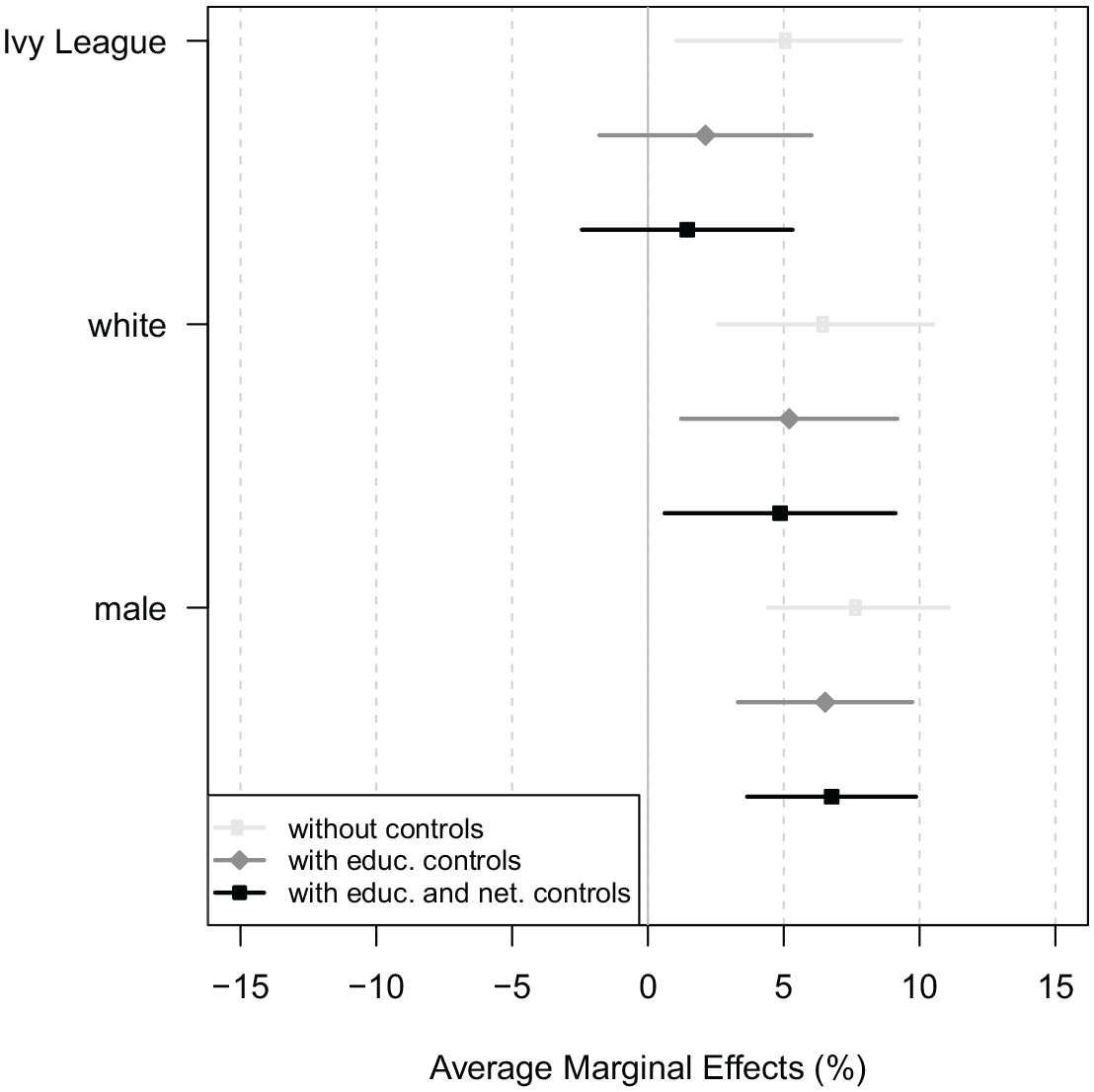

Figure 3 presents a coefficient plot of a set of logistic regression models displayed in Appendix B. Coefficients are expressed as average marginal effects (Mood, 2010). In non-linear models, the average marginal effect (AME) is the average change in probability when x increases by one unit. Multiplied by 100 it indicates the increase or decrease of chances in percentage points. For instance, an AME of 0.11 for the chance as an Ivy League alumni to be a founder of a financial firm, means that the chances are 11% higher than those of non-Ivy League alumni to found such a firm.

Probability of men, whites and Ivy League graduates to be a founder.

Model 1 (in light gray) tests hypothesis H2 without controls, Model 2 (in grey) with educational controls and Model 3 (in black) with both educational and social network controls. Model 1 shows that being a man, white and with an Ivy League degree is indeed associated with being a founder compared to a non-founder. Models 2 and 3 show that two of these results hold when adding education and social network variables. Men and whites have a 7% and 5% higher (respectively) chance of being a founder in the complete Model 3. The Ivy League variable becomes non-significant when we add controls. Nevertheless, the overall evidence indicates that founders are a more privileged group than other financial elites in 2018.

Recruitment and promotion based on trust

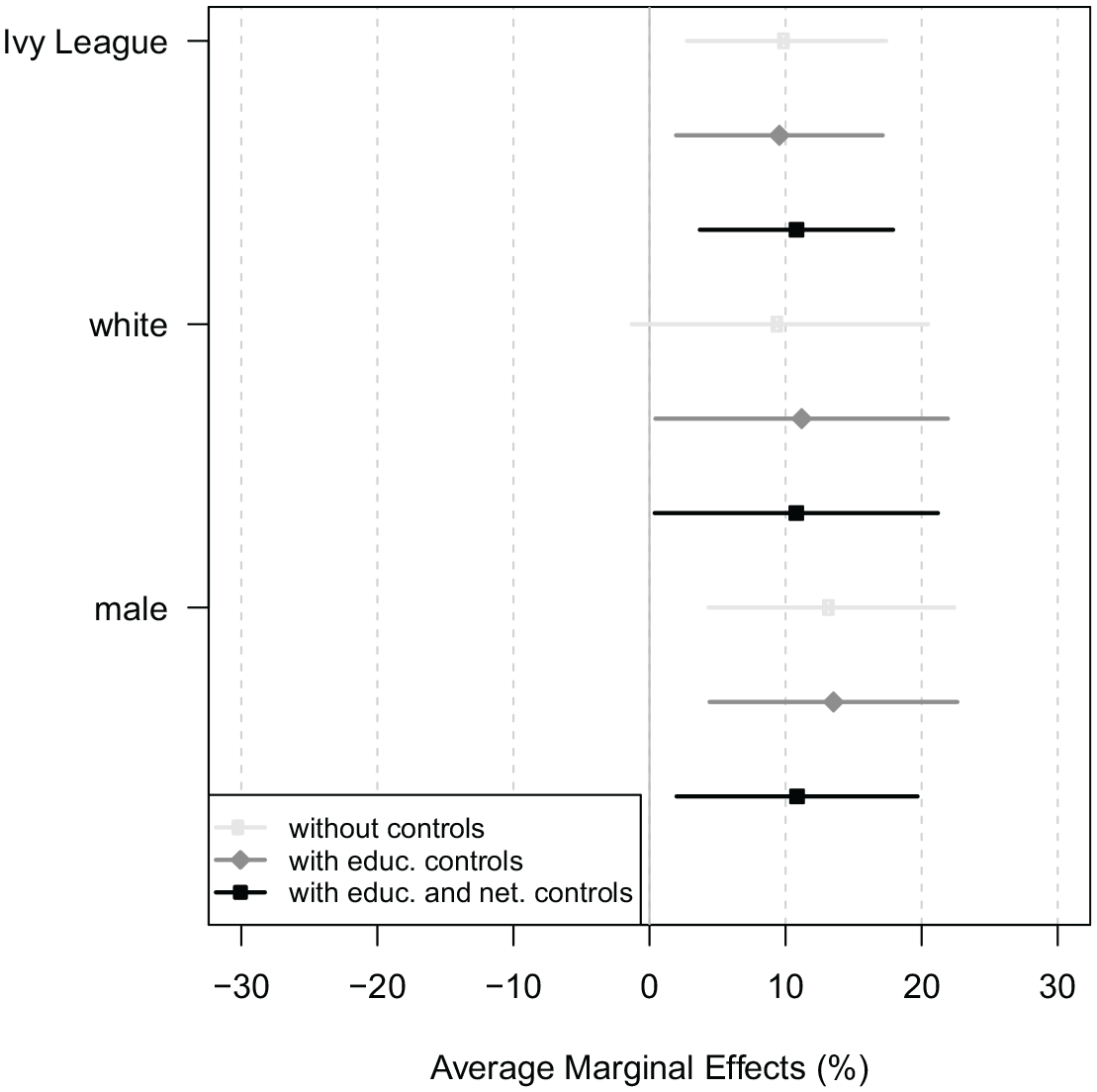

Our third hypothesis posits that hybrid financial firms have a higher likelihood of having men, whites and people with a higher social status at their helm than public corporations. Figure 2 shows the proportion of men, whites and graduates of Ivy League universities in public and hybrid firms next to founders. We observe that men consist of 88% of hybrid firm leaders and 78% of public firm leaders, a statistically significant difference. Also, whites compose a greater proportion of hybrid firm leadership (91%) than public firm leadership (87%). We also observe that Ivy League graduates are in higher proportion in hybrid firm leadership compared to public firm leadership. The results of the logistic regressions are shown in Figure 4 (see Appendix C).

Probability of being a man, white and Ivy League in hybrid organizations.

Model 1 (in light gray) tests H3 without controls, Model 2 (in grey) with education controls and Model 3 (in black) both with educational and social network controls. According to the first model, managers who are men, white and hold an Ivy League degree have a higher likelihood to be selected into the leadership of a hybrid firm compared to a public firm. The race attribute is weaker and not statistically significant at p < 0.10. But these results hold (or are reinforced) when adding education and social network variables: the coefficients stay high, and the race variable becomes significant at the 5% level. Men, whites and Ivy League graduates have an 11% higher chance of belonging to the leadership of a hybrid firm compared to public firms in Model 3. These results endorse our hypothesis H3. Individuals in hybrid organizations seem to be promoted according to trust networks favoring high status white men.

Discussion

Our findings show that hybrid forms of organization have increased in hedge funds and private equity, yet remain less important in asset management and insignificant in investment banking. As a consequence, hybrid organizational forms contribute to a polarization of the finance industry – cleaving it into bureaucratic and neo-patrimonial poles. We have demonstrated that founders have been significantly more white, men and from an upper-class background. We argue that these characteristics are then perpetuated and reinforced by recruiting and promoting mechanisms based on trust and loyalty, typical of patrimonialism and distinct from processes in bureaucratic firms.

On a very general level, our results confirm research on elite diversity (Zweigenhaft & Domhoff, 2018): diversity has increased, but the change is very modest. Women and non-whites make up around 10% of the financial elite as we define it. This means that the order of magnitude is similar to Zweigenhaft and Domhoff’s findings on corporate CEOs and board members.

Our results show, more specifically, how the characteristics of elites and organizational structures interact to produce specific forms and levels of inequality (Acker, 1990). In line with authors such as Stearns and Allan (1996) we think that during historical transitions specific groups of actors tend to exploit the situation with organizationally innovative strategies. Since the early 1970s many investment banks have undergone an organizational transformation, from traditional partnerships to public firms. They have become larger, more transparent and a little more meritocratic (Morrison & Wilhelm, 2007). This bureaucratization reduced opportunities for entrepreneurship and money making. Even though these firms promised generous bonuses, they could not offer the same benefits as did the founding of a new firm. This is why certain elite members opted out of these mega-finance corporations and founded hybrid firms – structures better suited to satisfy their thirst for recognition and entitlements (Godechot, 2008; Stearns & Allan, 1996).

In line with Palmer and Barber (2001), we think that the social attributes of elites – such as class, gender or race – are not irrelevant for organizational behavior. One of the reasons these founders opted for smaller, more informal hybrid firms was the elective affinity between their functioning and the trust-based mechanisms of hedge funds and private equity (Eaton, 2022; Neely, 2022). As future clients would trust more in socially similar founders of investment firms, this has potentially advantaged white founders – their whiteness functions as a credential (Ray, 2019). This mechanism is also at play for gender, as men are potentially perceived as more credible and trustworthy by other men. Neely (2018, pp. 369–370) argues that ‘prospective investors are more likely to invest in a founder’s startup when the person is perceived to have strong social ties and access to capital’. For both African Americans and women, it is arguably more difficult to attract investments and to found a successful finance boutique (Bielby, 2012). Ivy League attendance can also be a sign of trustworthiness. Many financial startups were founded by people from the same university or from the same workplace, such that elite alumni networks are important channels of economic opportunities (Eaton, 2022).

Our results suggest that organizational forms contribute to the reproduction and stabilization of socially selective elites (Acker, 1990; Ray, 2019). Trust networks remain important in hybrid firms and contribute to the reproduction of white men elite from top universities. In hybrid firms, the dominant group seems more closed than in bureaucratic firms. Since hybrid firms are less regulated by the state and the investment community, they are less accountable to legal and societal norms. Indeed, this lack of regulation may be one of the reasons to found such firms. Inversely, the literature shows that organizational formalization is less conducive to ascriptive inequality (Anderson & Tomaskovic-Devey, 1995) and typical functional features of bureaucracy can enhance diversity.

Conclusion

In the last decade, the influential work of Piketty (2014, 2020) on income and wealth distribution has put elites back on the agenda. Sociology has taken up this challenge, intensified its studies of the upper zones of the social space and investigated how class, gender and race shape elite formation and reproduction (Glucksberg, 2021; Kuusela, 2018; Savage, 2014; Young et al., 2021). In this contribution, we studied how financialization transforms elite composition and added organizational mechanisms to the equation to ask whether organizations mitigate or reinforce inequalities in terms of class, gender and race. In this perspective we studied the constitution of a new financial elite that rose to economic power with the financialization of the US economy: the founders, directors and managers of top financial firms in investment banking, asset management, private equity and hedge funds. We developed an analytical framework linking organization and elite theories, and addressing the issue of ascriptive inequality (Neely, 2018; Soener & Nau, 2019). We hypothesized that neo-patrimonialism – an organizational form competing with bureaucracy – would lead to higher share of ‘elite white men’ because of the greater importance of trust networks for elite reproduction in these settings.

To verify this proposition, we conceived a new, granular analysis of the rise of hybrid organizations in the US, investigated the profile of the founders of these firms and examined the social characteristics of top-management teams of the 40 most relevant US finance firms in 2018. Using logistic regression modeling we demonstrate that founders, directors and top managers of LPs, LLCs and LLPs – disproportionately represented in hedge funds and private equity – are indeed significantly more male, white and upper class compared to their peers in public firms.

Our first contribution relates to the integration of recent elite sociology with theories of organization (Neely, 2022; Ray, 2019). It is important to consider not only elites’ organizational positions, but their broader social attributes to understand their strategies and organizational behavior (Palmer & Barber, 2001; Stearns & Allan, 1996). We demonstrate that there is an interaction between the organizational form and elite reproduction in financial elites: hybrid firms tend to favor traditional elites, while public firms seem to diminish their top tier representation. We suggest that a social mechanism – the relative importance of trust networks – as well as the historical process can explain this fact: the rise of hybrid firms in some financial subsectors since the 1970s. Overall, this shows that class and elite reproduction is not limited to family-based transmission of cultural or symbolic resources, but is completed and potentially reinforced by organizational mechanisms all along the life course.

Our second contribution concerns the relationships between financialization and inequality (Savage & Williams, 2008). Observers continue to argue that contemporary Wall Street merely recruits the ‘best and the brightest’, and as a result, the financial sector would become vigorously meritocratic and blind to gender, race or class. Others show that gender and race, for instance, remain important contemporary barriers to accessing top positions in finance (Ho, 2009; Neely, 2018). Our contribution shows that both arguments can be right: finance may be both open and closed to outsiders, depending on the type of organizations in which individuals evolve. Bureaucracy tends to inhibit such practices, whereas recruitment based on informal networks enhances it (Dobbin et al., 2015; Reskin & McBrier, 2000). Our results indeed show that ‘elite white men’ are over-represented in hybrid organizations that are collegial and opaque to public scrutiny.

Footnotes

Appendices

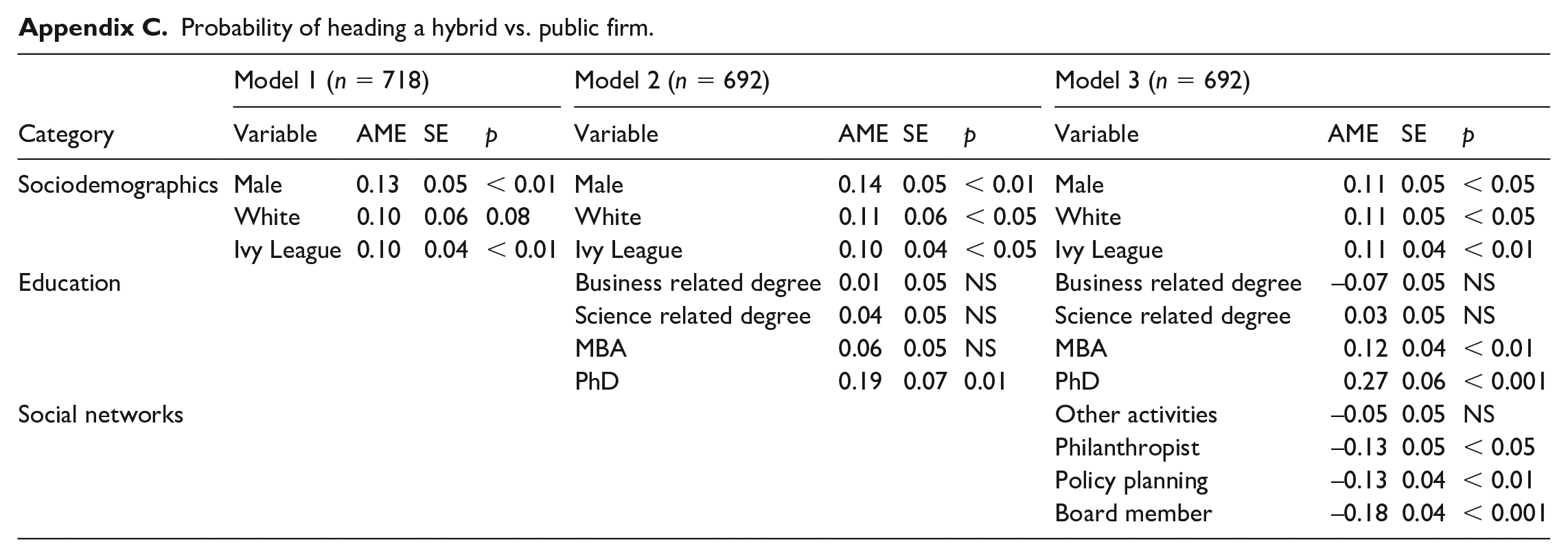

Probability of heading a hybrid vs. public firm.

| Model 1 (n = 718) | Model 2 (n = 692) | Model 3 (n = 692) | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Category | Variable | AME | SE | p | Variable | AME | SE | p | Variable | AME | SE | p |

| Sociodemographics | Male | 0.13 | 0.05 | < 0.01 | Male | 0.14 | 0.05 | < 0.01 | Male | 0.11 | 0.05 | < 0.05 |

| White | 0.10 | 0.06 | 0.08 | White | 0.11 | 0.06 | < 0.05 | White | 0.11 | 0.05 | < 0.05 | |

| Ivy League | 0.10 | 0.04 | < 0.01 | Ivy League | 0.10 | 0.04 | < 0.05 | Ivy League | 0.11 | 0.04 | < 0.01 | |

| Education | Business related degree | 0.01 | 0.05 | NS | Business related degree | −0.07 | 0.05 | NS | ||||

| Science related degree | 0.04 | 0.05 | NS | Science related degree | 0.03 | 0.05 | NS | |||||

| MBA | 0.06 | 0.05 | NS | MBA | 0.12 | 0.04 | < 0.01 | |||||

| PhD | 0.19 | 0.07 | 0.01 | PhD | 0.27 | 0.06 | < 0.001 | |||||

| Social networks | Other activities | −0.05 | 0.05 | NS | ||||||||

| Philanthropist | −0.13 | 0.05 | < 0.05 | |||||||||

| Policy planning | −0.13 | 0.04 | < 0.01 | |||||||||

| Board member | −0.18 | 0.04 | < 0.001 | |||||||||

Acknowledgements

We would like to thank the three anonymous reviewers and the editors of The Sociological Review for their constructive and useful comments. We also gratefully acknowledge François Schoenberger, Paul Lagneau-Ymonet, Nicolas Sommet, Neil Fligstein, Megan Tobias Neely and Kevin Young for their valuable insights and feedback on earlier drafts of this article. Any remaining errors are solely our responsibility.

Funding

The authors disclosed receipt of the following financial support for the research, authorship and/or publication of this article: Swiss National Science Foundation, Grant n°178817, The Rise of the Financial Elite – Access, Integration and Spread of Power.