Abstract

This paper analyzes a survey of individual microentrepreneurs’ (MEI) access to credit for business, broken down by their color or race in two Brazilian cities: Rio de Janeiro and Salvador. The central hypothesis of this study was that color or race is a significant predictor for credit rationing in both cities. However, the most crucial variables to explain the difference in credit approval were primarily related to credit risk operation—adverse selection, moral hazard, and collateral—as expressed by predictor: loan size and credit restriction (inversely correlated to odds of credit approval). The city of the loan operation had a robust explanatory power, with credit more accessible in Rio de Janeiro than in Salvador. Evidence of racial discrimination in the credit markets for business affected not all Afro-Brazilian MEI but blacks compared with white and brown MEI. Lenders could treat potential borrowers based on a pigmentocratic pattern, with this issue appearing more clearly in Rio de Janeiro. Further inquiries in this realm are recommended, preferably with a larger sample and a survey covering all Brazilian domestic territory.

Credit Rationing and Discrimination

Asymmetric Information Theory can rationalize the idea that micro, small, and middle businesses’ access to credit for business is subjected to more rigorous scrutiny. This is because their loan contract costs are proportionally higher than for more prominent companies due to relatively minor amounts, dispersion, and absence of audited financial statements (Ang, 1991; Chakravarty & Xiang, 2008; Park & Coleman, 2009; Stiglitz & Weiss, 1981). Theoretical and empirical evidence shows that this problem becomes more difficult when examining micro-entrepreneurs, mainly if they are poor or women or belong to historically discriminated groups (Armendariz & Morduch, 2005; Avery et al., 1998; Bester, 1987; Dymski, 2005; Labie et al., 2011; Yunus, 2007).

The economics of discrimination literature suggests that market functioning is commonly embedded in attitudes such as distaste or statistical profiling. Therefore, beyond observable characteristics, the decision-making process can be influenced by ascribed individual features such as gender, ethnicity, and race (Arrow, 1972a, 1972b, 1998; Becker, 1995; Phelps, 1972). The literature also shows that those attitudes regularly target the finance industry, biasing the lender's loan application decision-making process against historically discriminated groups.

In the United States, the database most often employed to inquire about small business access to loans is the Small Business Credit Survey (SBCF; formerly the National Survey of Small Business Finance) by the Federal Reserve Banks. Focusing on racial and ethnic asymmetry, in 2021, 13% of non-Hispanic African American owners and 20% of Hispanic owners held credit, contrasted with 31% of non-Hispanic Asian and non-Hispanic White owners (United States Federal Reserve System, 2021, p. 23).

Based on previous versions of the SBCF, several papers have employed logistic regression to assess the net racial discrimination effect on credit application outcomes. Although these contributions commonly did not find odds asymmetries for loan applications and interest rates, they did not fail to reject the null hypothesis that African American entrepreneurs face a higher likelihood of credit application denials, regardless of their credit history and other observable personal and enterprise characteristics (Blanchard et al., 2008; Blanchflower et al., 1998; Brown et al., 2011; Cavalluzzo & Cavalluzzo, 1998; Cavalluzzo & Wolken, 2002; Coleman, 2002; Mitchell & Pearce, 2011; Park & Coleman, 2009).

The absence of statistics disaggreegated by race or correlated categories prevents further information about racial inequalities in finance in most parts of the world. Nevertheless, this does not mean its absence. Raturi and Swamy (1999) studied Zimbabwe's financial market, identifying higher odds of credit rationing for black entrepreneurs. They concluded that the black disadvantages in credit approval rates were due to the proportionally higher number of applications compared to white applicants. In India, based on the All-India Debt and Investment Survey, taken at the beginning of the 2000s, Kumar (2013) found that privileged castes accessed the available funds more easily in the locally managed credit cooperatives, a reality that does not usually occur in commercial banks subject to anti-discriminatory national laws.

Most studies on credit access inequality in Latin America and the Caribbean have focused on gender or firm size (Bebczuk, 2004; Hochschild, 1979; Zambaldi et al., 2011), as exemplified by studies carried out in Argentina (Bebczuk, 2004), Brazil (Agier & Szafarz, 2011, 2013; Neri, 2008), Chile (Medel, 2017), Colombia (Méndez, 2017), Ecuador (Pearlman, 2014), and Peru (Buvinic & Berger, 1990). In several contributions, both variables have shared the same concern: gender and micro and small entrepreneurship. This research agenda was triggered by disseminating microfinance strategies to fight poverty in Bangladesh, led by Muhamad Yunnus and the notorious Greeman Bank (Deere & Catanzarite, 2017; Neri, 2008; Yunus, 2007). However, few works have dealt with the problem of racial inequality in the credit market for businesses in that region.

Deere and Catanzarite (2017) investigated the credit market in Ecuador, fitting into their model race and ethnicity alongside other independent variables. They found higher odds for Afro-Ecuatorians of asset debt than the other ethnic or racial contingents. However, according to the authors, “given the relatively small presence [of this category] in the sample, this association may not be valid” (Deere & Catanzarite, 2017, p. 122).

Thus far, to the best of our knowledge, only Storey (2004) has considered racial discrimination in credit for business in Latin America and the Caribbean, focusing on Trinidad and Tobago's First National Baseline Survey. Mirroring the reality in the United States, Afro-Trinidians’ odds of credit denial were 25% higher than Indo-Trinidians and mixed-race people. In this sense, our survey is the first to focus on Brazil, bearing as its central concern the credit access by race groups in that country.

Brazilian Bank Industry and Micro-Individual Entrepreneurs

Contrary to the United States, Brazil does not rely on many national and representative databases containing information about small businesses’ access to credit to support their undertakings. So far, the most comprehensive is the 2003 Urban Formal Economy (ECINF), accomplished by the Brazilian Statistic Office (IBGE), representing 10.3 million self-employed employers with up to five workers resident in urban zones from all over Brazil. This survey shows that 2.3% of self-employed blacks and browns and 3% of whites received bank loans (Rossetto, 2006). However, unlike the Small Business Credit Survey, this source did not find a variable for the result of entrepreneurs’ applications.

In Brazil, micro and small entrepreneurship usually entangle with informality, implying millions of workers, self-employed, and small entrepreneurs laboring without social security benefits and payment of fiscal duties (Oliveira, 1980; Saboia, 1985; Souza, 1999). At the end of the 2000s, among 14.9 million small businesses, only 4.5 million were formally registered (Dallari, 2009), not contributing to facilitating their access to bank credit, as viewed above. The Brazilian Federal Reserve calculated that at the beginning of the 2010s, for the same amount of loan for working capital higher than 30 days, the micro business paid an average interest rate of almost 50%, a ratio of 2:82 compared to credit operations for large corporations (Banco Central do Brasil, 2011, pp. 67, Graph 4.22).

In 2008, the Brazilian government passed legislation to address the high informality rate of economic undertakings by creating individual microentrepreneurs (MEI; microempreendedor individual in Portuguese). This legal instrument envisioned reducing the bureaucratic cost to a business's start-up, moreover guaranteeing differential fiscal treatment for entrepreneurs who hire no more than one employee, earn a yearly revenue of up to BRL 60,000 (now BRL 81,000, around USD 15,000), and neither belong to nor are co-owners of other firms. MEI also must pay a fixed monthly amount to taxes and the national social security institute (International Labor Organization [ILO], 2014, p. 8; Schwingel & Rizza, 2013).

Empirical evidence also shows that the MEI legislation encouraged microentrepreneurs to seek loans. In 2013, around one in five MEI reported that one of the main difficulties in running their businesses was “getting credit/borrowed money” (SEBRAE, 2013, pp. 45, Graph 6.11). Nevertheless, while in 2012, 10.3% of MEI sought credit, one year after, this percentage has increased to a little more than one in five (SEBRAE, 2013, pp. 38, Graph 32, 2017, p. 51). SEBRAE provides regular “credit/financing orientation” for micro, small, and middle entrepreneurs, and since 2015, a variable about the necessity of that support has been integrated into the MEI profile questionnaire. In that year, the expectation for that consultancy was a little below 10%, but in 2017, this expectation was shared by more than half sample (SEBRAE, 2016, p. 66, Graph 42; SEBRAE, 2017, p. 70). This means that in envisioning reducing the level of informality, MEI legislation directly or indirectly addressed the problem of credit access.

Methods

The Survey

The “Afro-Brazilian Access to Business Credit Research Project” project focused on the credit access conditions of MEI from two Brazilian cities: Rio de Janeiro (capital of Rio de Janeiro State, in the Southwest Region) and Salvador (capital of Bahia State, in the Northwest Region). This study, whose Principal Investigator is the author of this paper, received financial support from the Inter-American Development Bank (IADB) in partnership with the Laboratory for Ethnic and Racial Equity (LAESER), a research center on race inequality placed at the time of the survey in the Federal University of Rio de Janeiro (UFRJ). The survey is registered at IRB ID: STUDY00002919, The University of Texas at Austin, Office of Research Support and Compliance Institutional Review Board.

The questionnaire targeted the credit access conditions of a sample of 1,024 MEI in Rio de Janeiro (518) and Salvador (506). Through an agreement with SEBRAE state headquarters, we obtained a list of entrepreneurs registered in 2012 as MEI in the Receita Federal (the Brazilian Internal Revenue Service; IRS) for those places. This allowed us to draw our sample design stratified in each city by nine principal economic branches as defined by the National Classification of Economic Activities (CNAE). 1

The Brazilian city with the most MEI is São Paulo (at the end of 2020, about 1,06 million), but the survey covered Rio de Janeiro and Salvador due to logistical conditions. This does not mean the absence of importance of either place for Afro-entrepreneurship. Rio de Janeiro and Salvador are of particular interest in studies on Brazilian race relations, considering their cultural, political, and historical importance (Azevedo, 1955; Lopes, 2011; Pinto, 1953). Furthermore, these are the second and third largest cities whose individuals self-identify as black and brown (the Brazilian Statistic Office terminology to refer to Afro-Brazilians) 2 and MEI residents: around 644 thousand in Rio de Janeiro, and 233.4 thousand, in Salvador. 3

Measures

The dependent variable of our logistic regression was credit approval. It was a binary variable in which the dummy was the MEI whose solicited amount was wholly released (1) and those whose application was totally or partially rejected (0). Keeton's approach frames this definition for credit rationing typologies: type I, when applicants receive just part of the total amount requested, and type II, when the banks reject the application outright or partially (Bellier et al., 2012; Keeton, 1979; Steijvers & Voordeckers, 2009). The principal hypothesis of this paper was the statistical significance of the racial difference in rates of credit approval for businesses in Rio de Janeiro and Salvador.

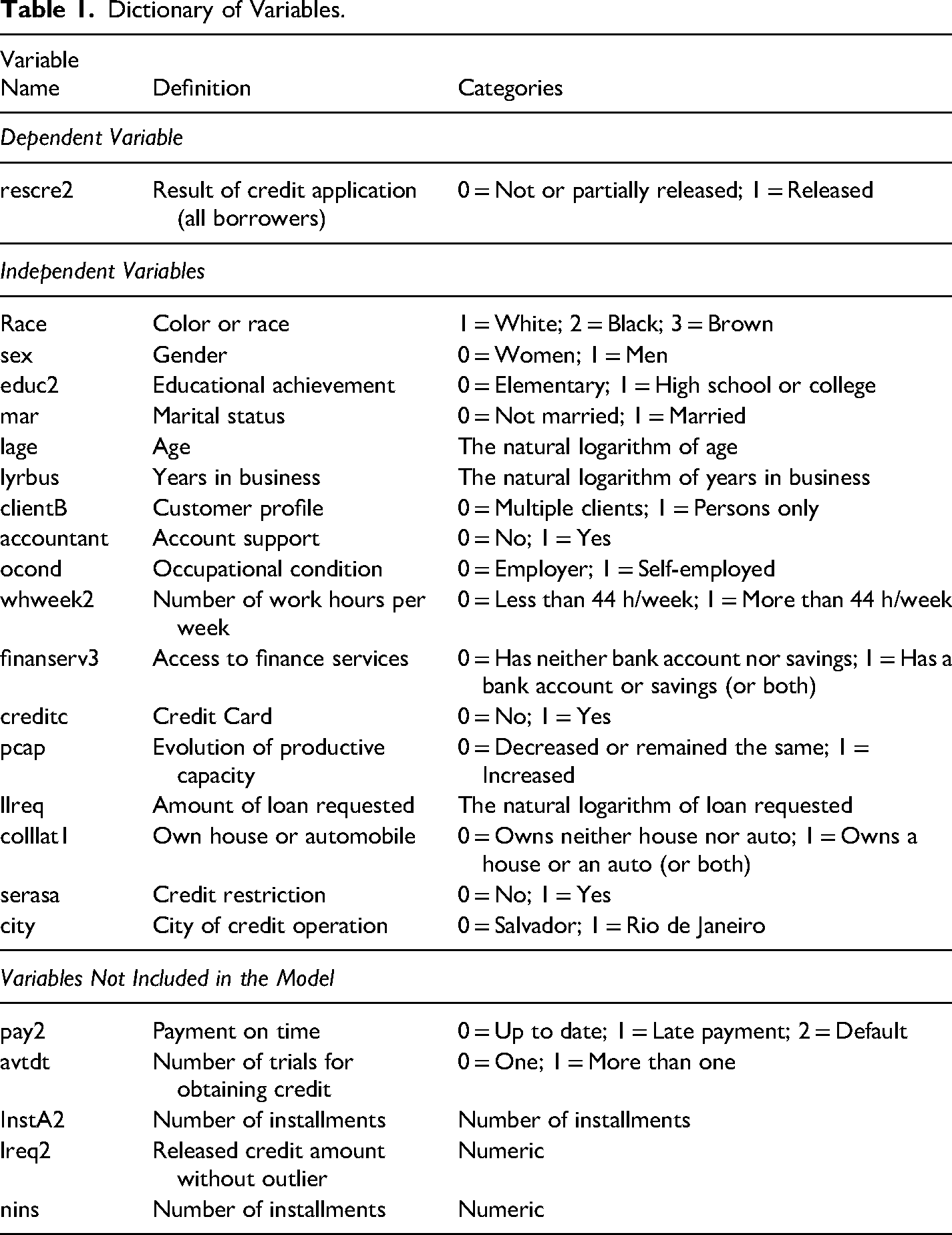

Dictionary of Variables.

Four sets of predictors shaped both models for credit rationing. The first was the bivariate of credit approval being race as the independent predictor. The literature shows that personal and business finances overlap in micro, small, and middle businesses (Avery et al., 1998; Voordeckers & Steijvers, 2006). Thus, the second group of variables represented the MEI color or race (white, black, or brown), gender (male or female, without the inclusion of non-binary gender), education (elementary or high school or college), age (natural logarithm), marital status (married or not married), previous bank relationships through bank and savings account (yes or no), credit card (yes or no), time in the business (natural logarithm), work hours per week (more or less than 44 h per week) 4 , requested amount (natural logarithm), clients (person only or other customers), occupational condition (self-employed or employer of one employee), and accountant support (yes or no).

The third set of covariants added to the model the requested amount, a covariant, which expressed the contract risk due to adverse selection. The fourth model included two other variables related to moral hazard: collateral (have a house or car or neither) and credit restriction or nome sujo (bad credit) in Portuguese (yes or no). An additional predictor city was included in the last logistic regression, referring to the place of either the businesses’ operation or the loan contract. Finally, we ran two complementary models broken down by the city of the credit operation (Rio de Janeiro or Salvador) to assess the model behavior in both places.

Statistical Analysis

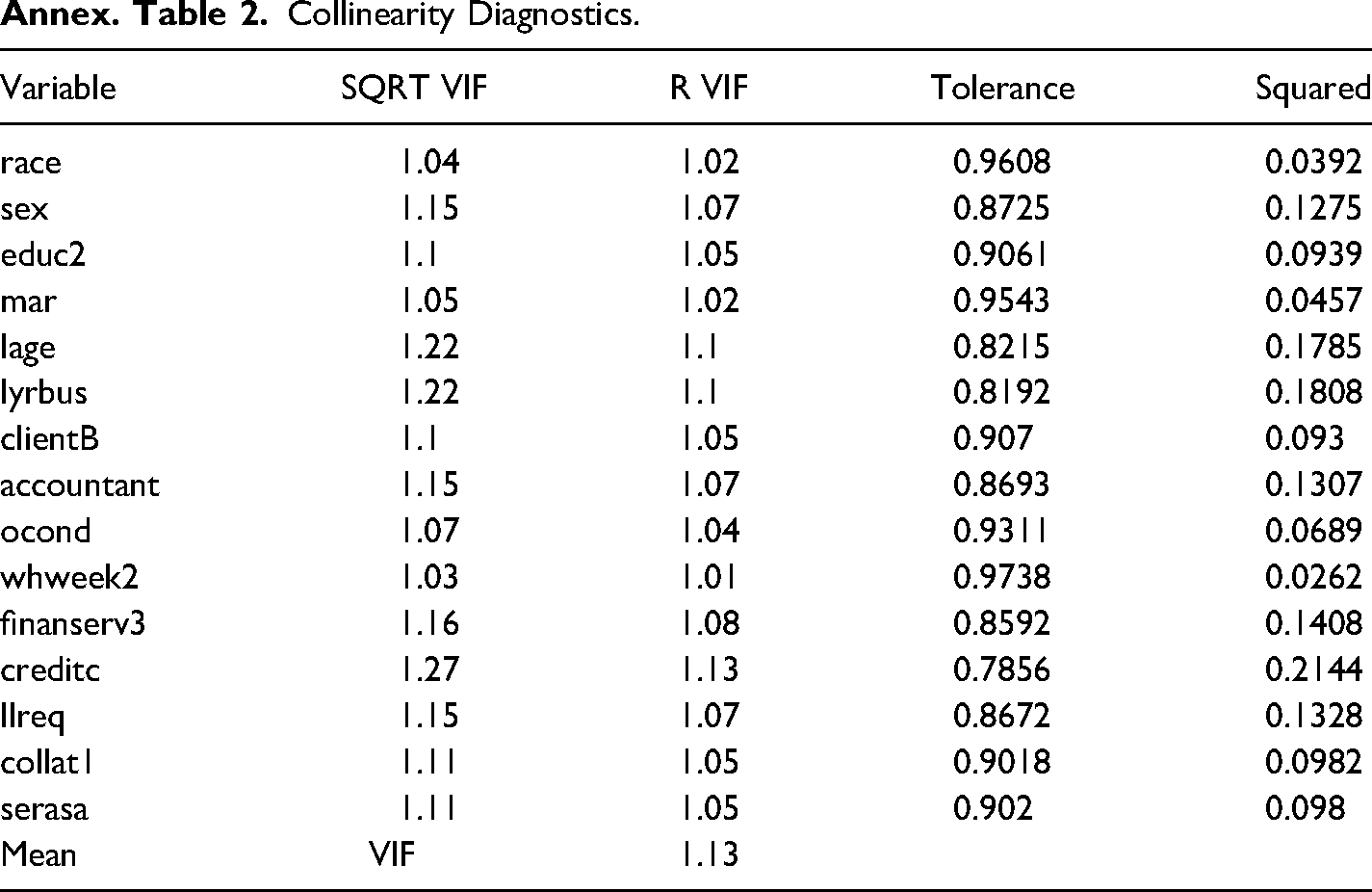

The analytical sample included 260 white, black, and brown MEI and their first application for credit between April and June 2013. We calculated descriptive statistics and estimated logistic regressions, comparing credit rationing by race in Rio de Janeiro and Salvador, considering their respective MEI populations. Listwise deletion was employed to address the missing data, and all final logistic regressions evaluated 215 cases (Menard, 2010). We considered two-tailed p-values of <0.05 statistically significant but also approaching predictors whose p-values were almost significant at <0.1. All statistical analyses considered the complex survey design and were conducted using Stata/MP v17.0 survey data commands (svy). The variance inflation factor (VIF) for loan rejection was 1.13, indicating a low likelihood of collinearity for either model (Annex, Tables 1 and 2).

Results

Descriptive Statistics

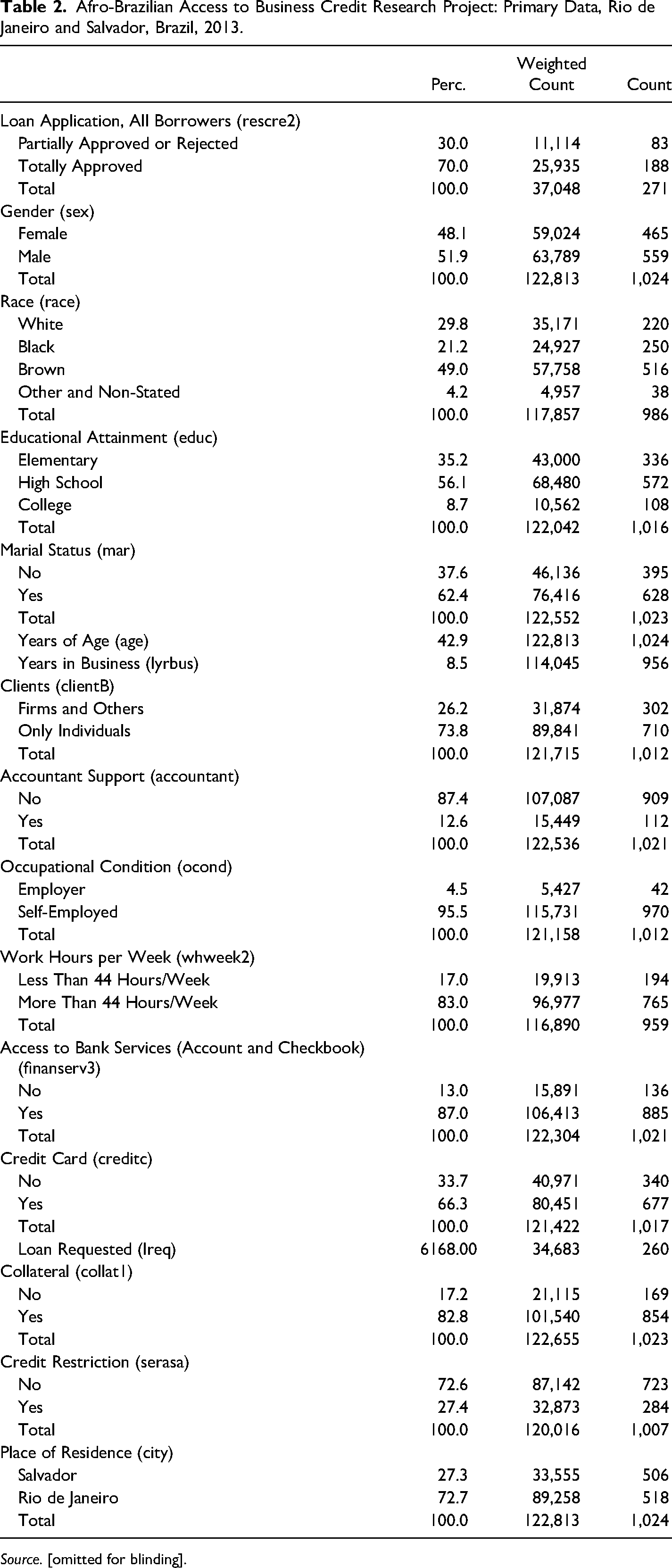

In our sample, 30% applied for credit. Of these, around three-quarters had their contracts approved, and one-quarter were fully or partially rejected. Over the dataset, 9% of MEI had their proposals rejected. Discouraged borrowers represented almost 20% of the sample, meaning that the ratio of discouragement to rationing was around two, mirroring a tendency also observed in other studies on credit discouragement (Cavalluzzo & Wolken, 2002; Jappelli, 1990; Mama & Ewoudou, 2010) (Table 2).

Afro-Brazilian Access to Business Credit Research Project: Primary Data, Rio de Janeiro and Salvador, Brazil, 2013.

Source. [omitted for blinding].

In the weighted sample, most of the entrepreneurs lived in Rio de Janeiro. The gender distribution was almost even. The majority were brown (49%), followed by white (30%) and black (21%). Due to their small number, those of Asian, Indigenous, or non-stated race (4.2%) are not included in this paper. The interviewees were mostly married, had collateral (house or car) to offer for credit contracts, had bank accounts or savings, had credit cards, served persons only, and worked more than 44 h per week. Relatively few declared that they had accountant support or were one-employee bosses. The interviewees’ average age was almost 43 years. They had run their businesses for around 8.5 years, and almost 30% had credit restrictions (nome sujo) (Table 2).

MEI Demographic, Socioeconomic, and Entrepreneurial Characteristics, Rio de Janeiro and Salvador, Brazil, 2013.

Standard errors in parentheses.

*p < .05, **p < .01, ***p < .001.

Source. [omitted for blinding].

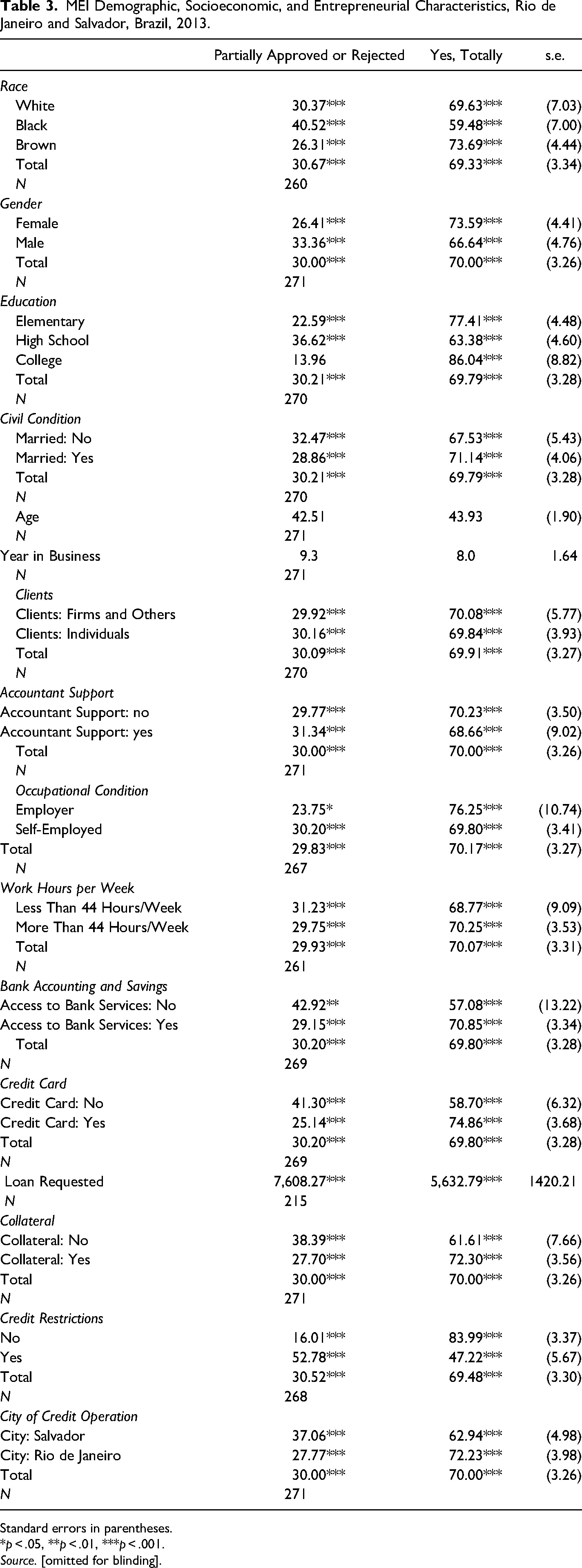

More of the wholly approved credit borrowers lived in Rio de Janeiro than in Salvador. Counterintuitively, in our sample, female entrepreneurs presented a higher percentage of credit approval (74%) than men (67%). Borrowers with higher education diplomas, followed by those with elementary-level education, had higher approval rates than those with high school certificates. MEI who were married, with guarantees to offer (house or car), with a credit card, served persons only, used an accountant service, were employers and worked more than 44 h per week were more likely to have full credit released (Table 3).

As expected, MEI with nome sujo had a lower rate of credit approval. Again counterintuitively, in our sample, owning a bank account or savings did not correspond to a higher rate of obtaining a loan contract. Older borrowers had higher odds of having their credit application approved. However, years in business did not mean better chances to obtain a loan contract (Table 3).

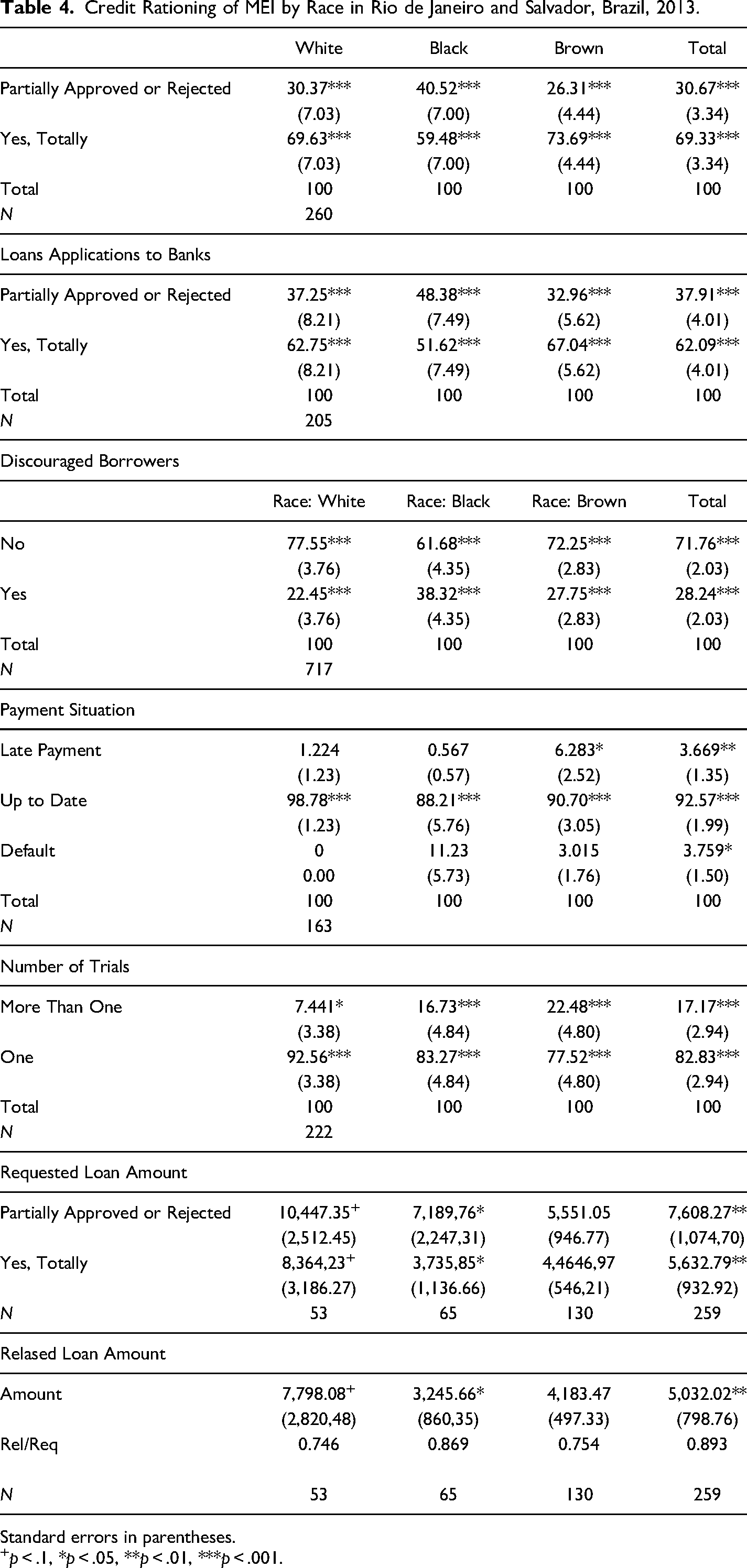

The descriptive statistics allowed the hypothesis that black and brown MEI had a general disadvantage in credit access compared to white MEI. Although their credit solicited–credit released ratio was lower than for black and brown MEI, white MEI had a higher rate of requested and released loans. Brown and black MEI were the most affected by problems of late settlement and credit restrictions and had a greater proportion of entrepreneurs needing to try more than once to obtain business loans (Table 4).

Credit Rationing of MEI by Race in Rio de Janeiro and Salvador, Brazil, 2013.

Standard errors in parentheses.

p < .1, *p < .05, **p < .01, ***p < .001.

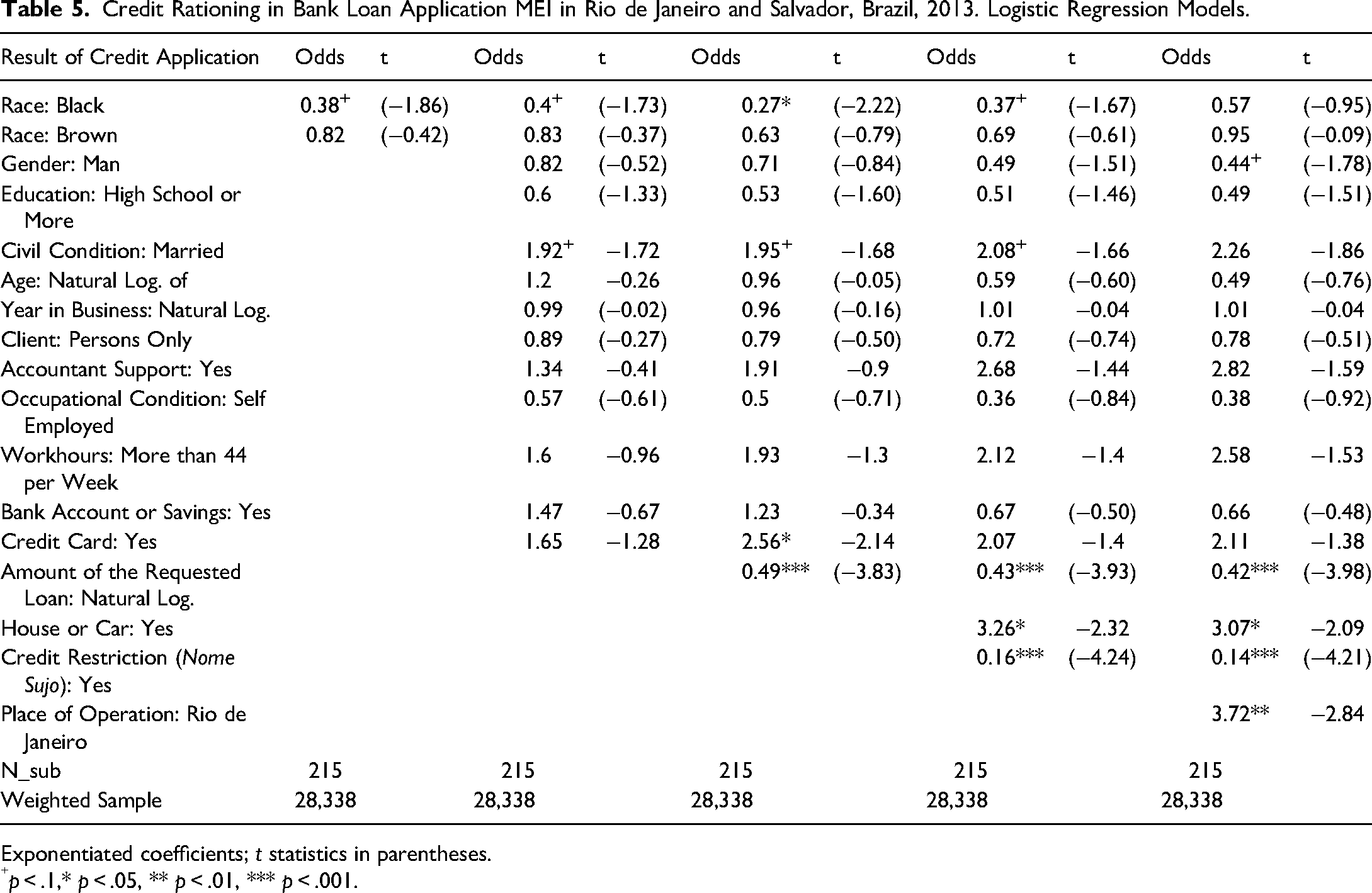

Credit Rationing in Bank Loan Application MEI in Rio de Janeiro and Salvador, Brazil, 2013. Logistic Regression Models.

Exponentiated coefficients; t statistics in parentheses.

p < .1,* p < .05, ** p < .01, *** p < .001.

The Model

The bivariate logistic regression for credit rationing combining Rio de Janeiro and Salvador showed that MEI blacks were about 62% less likely to get approval for credit applications than MEI whites (p = .064). The MEI brown odds ratio to obtain credit was 82% of MEI whites; nevertheless, this statistic was not statistically significant. The second model incorporated MEI demographic and financial variables. In this logistic regression, considering white as the omitted category, black was 60% less likely to get credit contracts. Conversely, the married odds ratio of obtaining credit was more likely by 92% (p = .085 for both latter predictors) (Table 5).

The third logistic regression considers adverse selection on the basis of the requested loan amount. As expected, this variable was negatively correlated with credit approval, meaning higher requests were almost half less likely to obtain contracts from banks (p < .001). In this logistic regression, MEI with credit cards odds ratio of obtaining approved loans was 2.6 times greater (p < .05). As in the second model, the married MEI odds ratio was 94% higher than MEI living under other civil conditions (p < .1). In this logistic regression, blacks were 73% less likely to obtain loan contracts than whites (p < .05) (Table 5).

The fourth model examined covariants referred to as moral hazards. This logistic regression output showed that bidding on a guarantee (house or car) correlated positively to full loan approval, more than tripling the borrower's odds ratio of getting a credit contract (p < .05). Conversely, nome sujo MEI was almost 85% less likely to get their application for credit approved (p < .001). As in the third logistic regression, the chances of obtaining a loan contract were also associated negatively with the credit application amount. Loans applications of higher amounts were about 57% less likely to obtain a loan contract (p < .001). Thus, based on this model, mirroring the literature, both adverse selection and moral hazard seem to be the essential predictors determining the odds of MEI obtaining a credit contract. In this logistic regression, the black category was around 60% less likely to get loans (p < .1) (Table 5).

Finally, we ran a fifth logistic regression incorporating the city. This model considers adverse selection and moral hazard's explanatory power to explain credit rationing dynamics. Higher loan requests are less likely in almost 60% to be well-succeeded in their application for credit (p < .001). Credit restriction (nome sujo) was also less likely in almost 90% to obtain credit (p < .001). Conversely, offering collateral more than triplicated the potential borrower's odds ratio of obtaining a loan contract (p = .01). Moreover, Rio de Janeiro's MEI was a fourfold greater likelihood o obtaining loan contracts than Salvador`s residents (Table 5).

The black category lost statistical significance in explaining credit rationing in this last model, although the coefficient is again negative. On the other hand, men were 56% less likely to obtain credit than women (p < .1) (Table 5).

We ran two complementary models for Rio de Janeiro and Salvador separately. Simplifying the analysis, we discuss the logistic regression with all covariates plus a predictor for adverse selection (loan requested amount) and moral hazard (collateral and credit restriction). These additional exercises helped deepen the behavior of this set of predictors in each place, notwithstanding the split of the sample size in each city and their corresponding reduction, leading us to see this information with some caution.

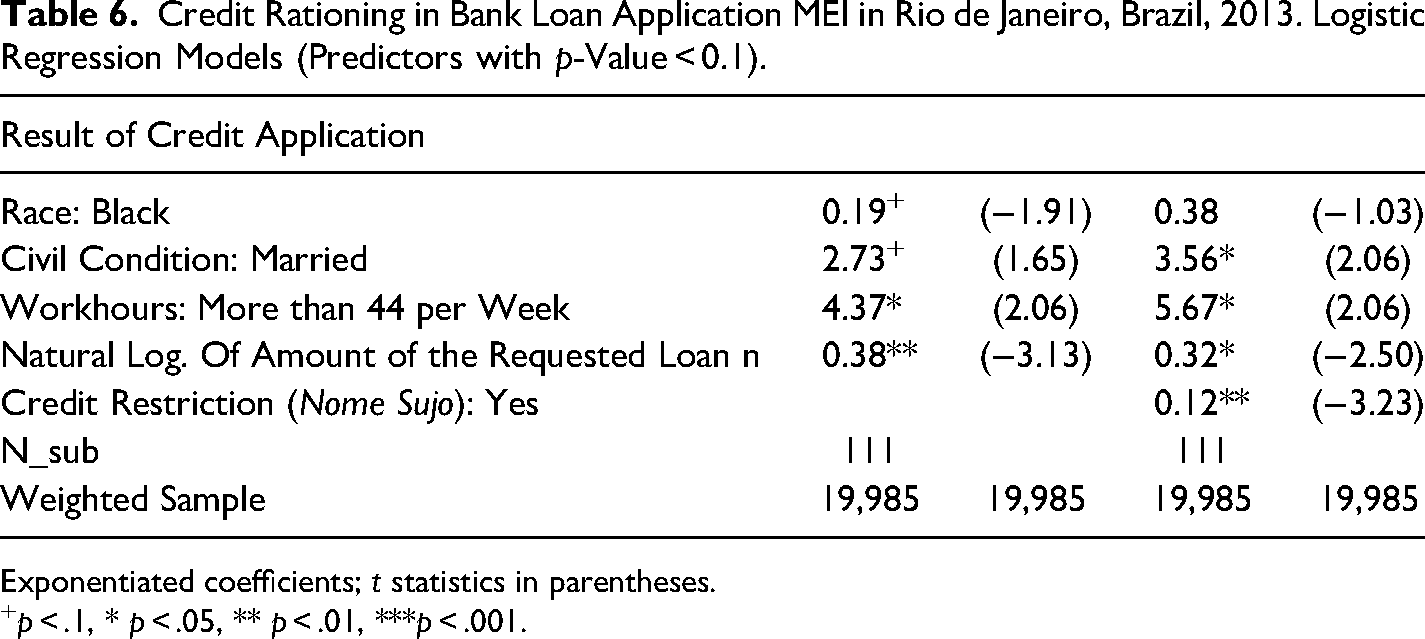

In Rio de Janeiro, the first logistic model examined shows that the most significant loan requests amount was associated negatively with contract release, being less likely to obtain credit by 62% (p < .001). The odds ratio of work hours per week (more than 44 h a week) was more than four times more likely to get a credit contract (p < .05). Being married correlated positively with full credit release, with an odds ratio of 2.72 times greater (p < .1). Conversely, the black MEI odds ratio of obtaining credit was 19% of the white MEI (p = .057). Nome sujo MEI's odds ratio was only 12% of the MEI in the alternative position (p < .001), and higher requests for loans were almost 70% less likely to obtain credit (p < .01). In this latter model, collateral and being black lost their overall explanatory power. However, being married (odds ratio 3.56 greater) and working more than 44 h per week (odds ratio 5.7 greater) were associated positively with a higher likelihood of loan approval (p < .05 for both covariants) (Table 6).

Credit Rationing in Bank Loan Application MEI in Rio de Janeiro, Brazil, 2013. Logistic Regression Models (Predictors with p-Value < 0.1).

Exponentiated coefficients; t statistics in parentheses.

p < .1, * p < .05, ** p < .01, ***p < .001.

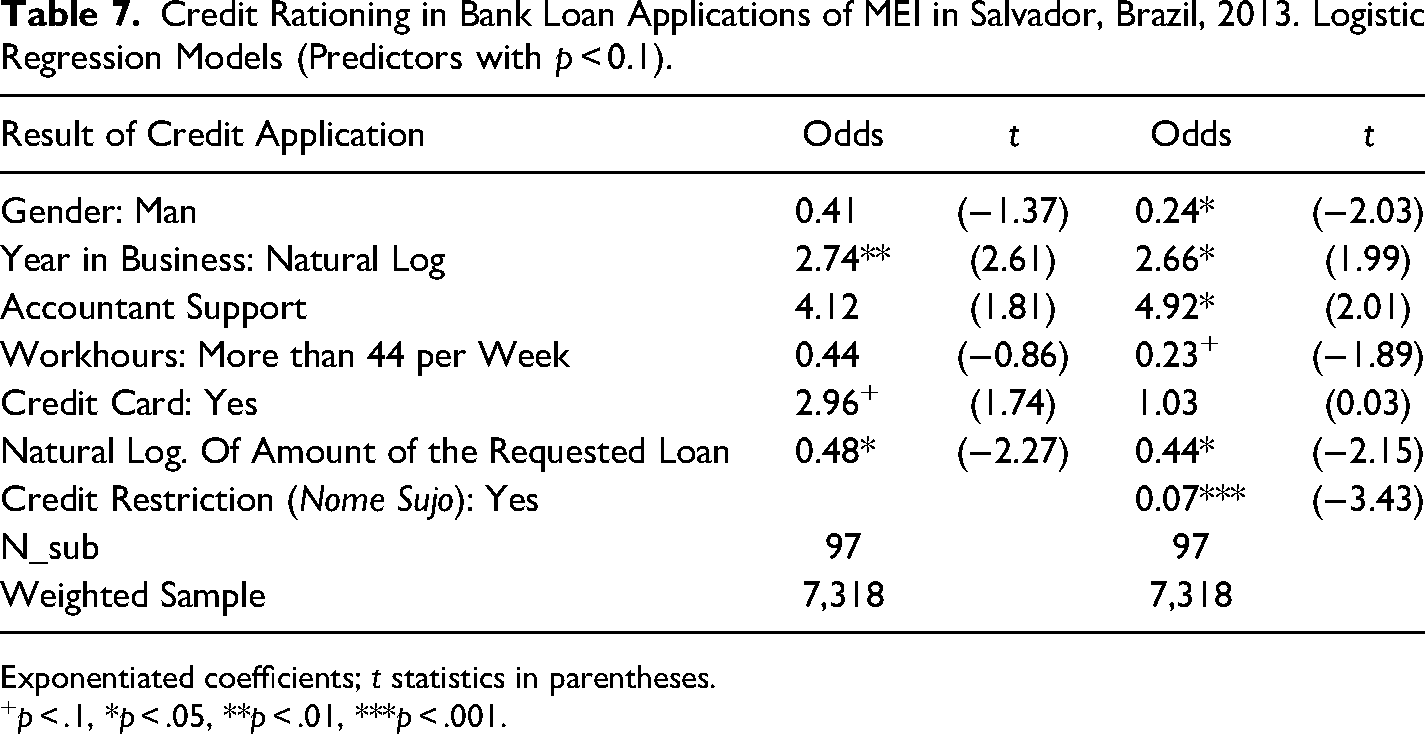

Credit Rationing in Bank Loan Applications of MEI in Salvador, Brazil, 2013. Logistic Regression Models (Predictors with p < 0.1).

Exponentiated coefficients; t statistics in parentheses.

p < .1, *p < .05, **p < .01, ***p < .001.

The analysis of the Salvador model partially mirrors some Rio de Janeiro behaviors. In the logistic regression with all variables plus the loan requested amount, this latter predictor was almost 50% less likely to obtain their credit contract proposal approved (p < .05). In this model, the odds ratio of the year in business for credit approval was more than 2.5 times greater (p < .01). Accountant support and credit card possession were the covariants whose odds ratio was 311% and 196% higher to obtain a loan contract (p < .1). The logistic regression in Salvador, including the moral hazard predictors (credit restrictions and collateral), showed that nome sujo MEI was more than 90% less likely to get their credit contract approved (p < .001). However, the predictor collateral lost its explanatory power. The higher loan requested amounts were less likely in about 67% to get credit (p < .05). As in the previous model, the predictor years in business (in about 165%) and accounting support (almost five times) had a greater odds ratio of credit approval (p < .05). In this latter logistic regression, men were 74% less likely to obtain a loan contract (p < .05). Also counterintuitively, MEI with longer working hours per week (more than 44 h per week) had less likelihood of credit approval (p < .1) (Table 6).

Discussion

Although information access is pivotal in all kinds of markets, in the financial industry it depends upon collateral assets that are not always easily screened. Banks evaluate potential borrowers based on moral hazard and adverse selection, which implies analyzing credit history, collateral, resource destination, or business plan. However, under information asymmetry, these instruments often drive banks to ration credit for potential good borrowers. Those lenders’ behavior is verified not only in more solid economies but in emergent markets too, naturally, including Brazil (Azam et al., 2001; Baltensperger & Devinney, 1985; Bellier et al., 2012; Diagne, 1999; Drakos & Giannakopoulos, 2011; Keeton, 1979; Mama & Ewoudou, 2010; Stiglitz & Weiss, 1981; Zambaldi et al., 2011).

Therefore, the literature on credit rationing dissects a universal phenomenon that is supposed to be met worldwide. Accordingly, this paper reasserts the credit rationing theory scholarship, which synthetically highlights that banks avoid risky credit operations due to their higher chances of default and financial losses. The loan requested amount (adverse selection), collateral, credit restriction (moral hazard), and place of business operation were the predictors with more explanatory power to determine credit rationing in the Brazilian cities of Rio de Janeiro and Salvador.

Framed on 1993, 1998, and 2003 Survey of Small Business Finance databases, Chakravarty and Xiang (2008, p. 801) noted that ceteris paribus, “the probability of being approved for a loan decreases with the amount of loan requested,” and Kirschenmann (2016, p. 69) acknowledged that alongside moral hazard, loan size “deal[s] with adverse selection.” Therefore, our logistic regressions’ output invariably showed a negative correlation between the solicited amount and credit approval.

Berger and Udell (1990) reported that around 70% of all commercial and industrial lending contracts in the United States were framed on collateral pledges. Analyzing the Belgian bank system, Voordeckers and Steijvers (2006) found that family firms had higher odds of gaining more collateral. In Brazil, such enterprises have also featured low survivance chances and managerial issues (Pinheiro & Moura, 2001; Tasic, 2005; Zambaldi et al., 2011). In their survey on small and medium enterprises’ business credit access in that country, Zambaldi et al. (2011, p. 313) noted that “liquid collateral credit products seem to fit with the small business segment, reducing risk.”

Steijvers and Voordeckers (2009, p. 942) note the necessity of distinguishing personal and business collateral. However, a limitation of our survey is that many firms’ assets were missing, which is why we took only the personal physical guarantees (house and car). Notwithstanding, our parameter estimates suggest that collateral has some explanatory power to determine credit approval rates.

The nonpayment of previous debt leads people and businesses in Brazil to have loans underwriting standards negatively recorded. After being reported by their lenders or sellers, three leading private institutions (Society for the Credit Protections—SPC, Boa Vista SPC, and Serasa-Experian) keep those default borrowers’ CPF (the Brazilian version of Social Security Number) in a national dataset. These borrowers’ register is “negative,” or, as it is popularly termed in Brazil, these people have their registers harmed or become nome sujo—bad credit, as usually said in the United States.

In 2022, the number of Brazilians with their name in the SPC/Boa Vista/Serasa records reached almost 67 million. Close to our survey in 2013, this was around 57 million (Confederação Nacional de Dirigentes Lojistas (CNDL) & Serviço de Proteção ao Crédito (SPC Brasil, 2015). The nome sujo condition does not legally prevent a borrower from gaining credit. They may still borrow from relatives, friends, moneylenders, non-banking financing companies, microcredit institutions, or even banks, magazines, and stores. Nevertheless, nome sujo borrowers have their chances of obtaining loans greatly diminished. Until the beginning of the 2010s, when our survey took place, Brazil did not have a positive register for potential borrowers, meaning the inexistence of a credit score for good borrowers (Pinheiro & Moura, 2001; Zambaldi et al., 2011). Although this situation has shifted, the negative record (nome sujo) is Brazil's primary source of information on borrowers’ moral hazard thus far. 5 Accordingly, in all logistic regressions, the odds ratio of credit approval for nome sujo MEI was invariably less than their competitor, not facing the same reality.

However, international scholarship also regularly indicates other covariants beyond the predictors more directly reported to the lenders’ microeconomic behavior. The place of residence, for instance, is also commonly referred to in the literature as a crucial predictor for distinct odds of credit approval (Berkovec et al., 1998; Blanchflower et al., 1998; Cavalluzzo & Cavalluzzo, 1998; Jappelli, 1990). Rio de Janeiro's credit approval odds for MEI were fourfold higher than in Salvador. The socioeconomic peculiarities between these sites might be a possible reason for understanding the difference. In 2013, Rio de Janeiro's gross domestic product was around five times greater than Salvador's, with 4.3 times as many bank agencies. In Rio de Janeiro, the Hershman–Herfindahl Index (HHI) was 0.18 for the number of agencies and 0.23 for the volume of credit operation, whereas, in Salvador, it was lower: 0.16 and 0.20, respectively. 6 Ahead, we will comment on how these data might also help us understand the behavior of race as a predictor.

Rostamkalaei et al. (2020, p. 182) note that credit card ownership is “associated with a decrease in the likelihood of fearing rejection.” Indeed, in our logistic regressions, although imperfectly, credit card ownership was the predictor that best showed the importance of client–customer relationship time to reduce informational opacity for lenders. Only outside a nome sujo condition can borrowers have a credit card. In case of default, this service is suspended almost immediately. Thus, for the banks, having a credit card in Brazil is a fair proxy for low moral risks. However, in our model, this predictor's explanatory value was reduced when the variables of credit restriction and collateral were included in the models.

On the other hand, our survey asked about possessing a bank account and savings, but it did not explain the odds of credit approval whatsoever. A credible explanation is that even nome sujo borrowers can have both, although with more limited services (no credit access or checkbooks). Unfortunately, in this paper, information such as the bank account time, the availability of a bank manager for customized financial support, the number of bank relationships, and pre-approved lines of credit became omitted variables. Perhaps due to this, financial services did not explain the odds of credit approval.

The literature also shows that married borrowers have greater chances of gaining credit (Jappelli, 1990; Mama & Ewoudou, 2010), and our survey partially bears out those findings. Storey (2004) noted that a business’ durability is a possible indicator employed by banks to assess business soundness. This means that the predictor “time in the business” mixes enterprise survival and the business owner's experience (Han et al., 2009). On the other hand, the MEI legislation predicts that an accountant should prepare a yearly accounting balance, although, in our dataset, only 11% reported having done so. Since the issue is straightforwardly related to business information opacity (Drakos & Giannakopoulos, 2011), this support helps to amplify MEI's odds of obtaining a loan contract. Our logistic regression outputs confirm both trends, even though why these variables’ statistical significance was observed in Salvador only is unclear.

According to Brazilian legislation, 44 work hours per week is the maximum. Again referring to Storey (2004), this predictor could refer to levels of business engagement, theoretically increasing the odds of MEI receiving a loan contract. However, the logistic regressions for Rio de Janeiro and Salvador displayed inverted coefficient signals for that predictor, preventing us from reaching a definitive conclusion in this sense.

Beyond the asymmetrical information theory, this paper dialogues with another theoretical outlook: the economics of discrimination. A neat microeconomic logic could explain the reason for credit contract rejection: risk credit operations carry a danger of financial losses and are thus avoidable by lenders. However, asking which groups are more vulnerable to adverse selection and moral hazard will never be in vain. One of the principal literature concerns is whether, due to screening errors, potential good borrowers are prevented from credit access to support their businesses. The question is to verify whether these mistakes are embedded with sociocultural peculiarities, making minority good borrowers particularly vulnerable to becoming chronically credit-rationed. Historically discriminated groups are led to occupy specific stances across the social layer, territory, and spaces. So, are the reasons for these contingents’ lower rate of credit access these structural variables? Nevertheless, what is the explanation when, even after statistical controls, minority businesspersons still have lower odds of credit approval? However, in this regard, only partially our paper reasserts the main findings of the international literature on this subject.

In two of our models, the logistic regressions’ coefficient correlated positively with being a woman and having higher odds of credit approval. This finding is counterintuitive and does not bear out the studies in this field. For instance, Sexton and Bowman-Upton (1990, p. 31) noted the female businessperson's disadvantage due to stereotypes regarding their supposed poor entrepreneurial ability and being “rated as more emotional,” and Orhan (2001) bears out this framework. Nevertheless, the gender difference in favor of women noticed in Salvador may give clues about what happened.

The literature on credit discouragement often reports that female small business owners are subjected to what Agier and Szafarz (2013) defined as the “glass ceiling effect” for loan applications. This means that anticipating some banks’ unwillingness to release higher-value loans, women limit their value contract proposals (Gama et al., 2017; Treichel & Scott, 2006). Even though in Rio de Janeiro, the solicited credit amount by gender was almost the same, in our dataset, the average loan requested by MEI women from Salvador was 38% of that of men. Therefore, a possible reason for the inverted coefficient in Salvador could be associated with a perverse silver lining of the “glass ceiling effect.”

The axis of this paper is the influence of race over the likelihood of credit approval. The question is if these decisions can also be influenced by negative attitudes against entrepreneurs associated with historically discriminated groups. Regardless of their entrepreneurial characteristics, they would be more exposed to negative selective screenings. Nevertheless, this discussion needs to comprehend some aspects related to race relations in Brazil.

The black and brown categories correspond to the official classification of the Brazilian statistic office for Afro-Brazilians, which is different from the United States, where all African Americans, regardless of skin color or shades, are grouped into a unique category.

Considering that the logistic regressions ran with the complete dataset, out of five models, in four logistic regressions, we observed that black MEI was less likely to get credit contracts than those for white and brown MEI. Nevertheless, the disadvantage of brown MEI compared to white ones in their quest for credit, verified in the descriptive statistics, was never statistically significant. Most Brazilian demographic surveys show that, even after statistical control, black and brown socioeconomic data converge in indicators such as income, occupation, poverty, and education (Gonzales & Hasenbalg, 1982; Hasenbalg, 1979; Oliveira et al., 1981; Paixão & Rossetto, 2020; Silva, 1980; Soares, 2000). However, not all studies on racial inequality in Brazil see black and brown socioeconomic conditions converge, contrarily being affected by a pigmentocratic pattern (Silva & Paixão, 2014; Telles, 2014; Telles & Flores, 2013). This hypothesis has been verified in most of our logistic regressions.

On the other hand, the variable of race lost statistical significance in the logistic regression examining the variable of the city. Decomposing the model for both cities in one (which assessed the sum of demographic and entrepreneurial predictors, plus the loan requested amount), the predictor race was near statistical significance in Rio de Janeiro but not Salvador. Therefore, paradoxically, borrowers generally had higher chances of obtaining credit in Rio de Janeiro, but the black MEI did not.

We tried to reproduce the interactive effect between race and bank concentration accomplished by Cavalluzzo and Cavalluzzo (1998) and Cavalluzzo and Wolken (2002), which employed the HHI to test the classic Becker's (1995) hypothesis that less competitive markets are more exposed to racial discrimination. 7 Partially confirming those findings, tellingly, Rio de Janeiro, where the HHI was higher than in Salvador, was where blacks had lower odds of obtaining credit than did other groups. However, our simulation was based just on two cities, and the model incorporating the HHI did not adjust well. Nevertheless, although the logistic regressions did not permit any conclusion in this sense, black MEI had lower credit access odds in Rio de Janeiro, paradoxically, where access to financial services and bank concentration was higher.

Implications for Public Policy: Race Relations and Development

In 2012, the Secretary for Strategic Affairs (SAE), directly subordinated to Brazil's president's cabinet, defined the monetary lines to classify the social classes 8 . Notwithstanding several criticisms of the SAE's methodology (Pochmann, 2012, 2014), more than nine in ten interviewees could be regarded as belonging to the upper class in our database. This proportion matches the SEBRAE national survey on MEI socioeconomic profile (92.3%; SEBRAE, 2016, p. 30, Table 7). Given the legal and regulatory system for business in Brazil, the counterintuitive information of an upper-class entrepreneur working in informal conditions can be understood. The World Bank estimated that in 2014, out of 189 countries, Brazil ranked a modest 116th in the “rankings on the ease of doing business” (Weltbank, 2013). The high bureaucratic transaction costs cut across all social layers, including the better-off. In the end, at least until 2013, the MEI benefitted wealthy informal entrepreneurs more than poorer ones.

This study thus mismatches with the survey by Agier and Szafarz (2011, 2013) in poor Rio de Janeiro areas and almost all studies in Latin America and the Caribbean targeting credit access for business. Moreover, these papers did not incorporate the racial component, exclusively centered on gender relations and economically vulnerable groups. Zambaldi et al. (2011) and Chakravarty and Xiang (2008) were concerned with credit access problems for small businesses in Brazil (the latter alongside nine other emergent countries), meaning that they targeted a best-positioned world compared to those in our study. In summary, the studied group of this survey, MEI, occupies an intermediate position: above those regarded as poor and below small entrepreneurs with amassed conditions to set up a more structured business under a better financial and legal entrepreneurial stance.

Therefore, never setting aside its possible implications for public policies, as the third theoretical field debated in this paper, the current contribution relates to how racial equality policies related to not the relief of poverty but strategies for economic development. MEI are better-off informal microentrepreneurs with tremendous potential for contributing to the domestic economic development model framed on social and racial equity. Although this research agenda seems consolidated in the United States (Brimmer, 2014; Walker, 2009), it is still in its infancy in Brazil.

Conclusion

This paper is among the first to apply the asymmetric information theory in Brazil's credit for business to focus on race relations. A major limitation of our analysis is that our study covered just two Brazilian cities, which may not represent the entire country or other regions regardless of their importance for the country or domestic race relations. Nevertheless, the logistic regressions run in this paper indicate a possible avenue for future research covering a sample of more than two cities.

The literature on credit access shows that small businesses, women, African Americans, and minority groups are subjected to higher rates of credit denial. However, although the findings for smaller businesses and female entrepreneurs obey a universal pattern concerning ethnic and racial groups, most surveys have examined the United States. Whether the rational behavior determining loan contracts is universal, incorporating alternative realities and examining institutional and sociocultural peculiarities, such as banking regulations and race relations patterns, may contribute to verifying whether racial discrimination in the credit market for business follows the prevailing American standard.

Nonetheless, our finds do not permit a definitive and robust conclusion about the statistical significance of the predictor race over the odds of obtaining credit. The most crucial variables to explain credit approval differences were related to credit risk operation. However, indications of racial discrimination in the credit market for business have been verified, affecting not all Afro-Brazilian MEI but blacks. As the main finding, we highlighted the indications of a pigmentocratic pattern in the Rio de Janeiro and Salvador financial system, making credit access for business among black MEI less likely than white and brown ones, even after statistic control. This finding is an original contribution to the international literature on racial discrimination in the credit market for business and dialogues with the characteristics of the Brazilian model of race relations more referred to individual features such as tone of skin color and hair than people's origin.

On the other hand, instead of surveying all entrepreneurs, our survey dealt with those with particular characteristics: MEI. . Our logistic regressions incorporated predictors of social class (education) and firms’ entrepreneurial conditions (client profile and occupational condition, and if self-employed and employer), but none had explanatory power. This was not by chance. MEI socioeconomic conditions are confined by the contours of the legislation, which defines the limits for gross receipts and the number of occupied employees.

Thus, the socioeconomic asymmetries within the MEI category are expected to be lower than in other studies focused on racial inequality in Brazil or compared with most surveys on this subject accomplished in the United States, comprehending a vast gamut of businesses’ size. In this sense, the logistic models’ racial disparities verification should surprise us, not its absence.

Notwithstanding, considering the issue this paper touches on social justice issues and the racial equity development model, further inquiries are recommended, preferably with national representation and a more robust sample. 9

Footnotes

Collinearity Diagnostics.

| Variable | SQRT VIF | R VIF | Tolerance | Squared |

|---|---|---|---|---|

| race | 1.04 | 1.02 | 0.9608 | 0.0392 |

| sex | 1.15 | 1.07 | 0.8725 | 0.1275 |

| educ2 | 1.1 | 1.05 | 0.9061 | 0.0939 |

| mar | 1.05 | 1.02 | 0.9543 | 0.0457 |

| lage | 1.22 | 1.1 | 0.8215 | 0.1785 |

| lyrbus | 1.22 | 1.1 | 0.8192 | 0.1808 |

| clientB | 1.1 | 1.05 | 0.907 | 0.093 |

| accountant | 1.15 | 1.07 | 0.8693 | 0.1307 |

| ocond | 1.07 | 1.04 | 0.9311 | 0.0689 |

| whweek2 | 1.03 | 1.01 | 0.9738 | 0.0262 |

| finanserv3 | 1.16 | 1.08 | 0.8592 | 0.1408 |

| creditc | 1.27 | 1.13 | 0.7856 | 0.2144 |

| llreq | 1.15 | 1.07 | 0.8672 | 0.1328 |

| collat1 | 1.11 | 1.05 | 0.9018 | 0.0982 |

| serasa | 1.11 | 1.05 | 0.902 | 0.098 |

| Mean | VIF | 1.13 |

Acknowledgments

The author acknowledges Mark Wenner, Eduardo Sierra Gonzalez, Judith Morrison, Luana Ozemela, and Rachel Scarpari from the Inter-American Development Bank (IABD) for regularly supporting this survey. Mario Theodoro and Geovani Harvey provided comments on previous versions of this study. The survey questionnaire had the contribution of Ricardo F. Mello, Ruth Soriano Mello, Elizete Ignácio, and Anderson Oriente. Alinne Veiga proceeded with the sample design. Marco Aurélio Oliveira de Alcântara and Giseuda do Carmo Ananias de Alcântara coordinated the survey application. In Salvador, the study counted on the partnership of Bahia State University, and the author is pleased to Wilson Mattos, Claudia Rocha, and Kau Firmina. The author also acknowledges Irene Rossetto for her critical comments on a previous version of this manuscript. At the Univesity of Texas at Austin, the author is also pleased to Art Markman, Bruce Kellison, and Kevin Thomas. Acknowledging is also necessary to thank the Brazilian team of the Laboratory for Ethnic and Racial Equity (LAESER). This paper is dedicated to Luiza Bairros’ memory.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research including publication of this article: The Afro-Brazilian Access to Business Credit Research Project was supported by the Inter-American Development Bank [ATN/OC-11894-BR] with the administrative intermediation of José Bonifácio Foundation (FUJB) of the Federal University of Rio de Janeiro. Secondarily, this research also counted on support from the Brazilian Office of Ford Foundation (Grant n. 10801406-0), UT Austin IC2 Institute, and the UT Austin Institute for Urban Policy and Research Analysis (IUPRA).