Abstract

This paper measures the macroeconomic influence of recent political crisis, protest and uprisings in Africa with the generalized synthetic control method and evaluates the role played by natural resource dependence on the modulation of the nexus. We find that political crisis, protests and uprisings have a significant and negative nexus with economic growth while the nexus is positive with investment and price level. For economic growth, the deviation of the actual series from the counterfactual is negative, instantaneous, persistent and highly significant; indicating non-negligible costs of the shock. Indeed, dependence on natural resources amplifies the negative influence of political crisis, protests and uprisings on GDP. Finally, the more the treated country depends on natural resources, the more it becomes resilient to the investment losses caused by political crisis.

Introduction

There are two main scholarly and policy tendencies that motivate the focus of the present study, notably: (i) the criticality of political crisis in Africa's economic development and (ii) gaps in the extant political crisis literature. These two perspectives are engaged in turn below.

Consistent with contemporary literature (Asongu et al., 2021), a fundamental threat to Africa's economic development in the recent decades has been political instability. This narrative is better articulated by Asongu and Nwachukwu (2016a) who substantiate the perspective with insights from notable case studies of political strife and crisis: Angola (from 1975 through 2002); Chad (from 2005 through 2010); recently South Sudan and the Western region of Cameroon as well as the long standing crisis in the Democratic Republic of Congo; Liberia (from 1999 to 2003); the Central African Republic (from 1996 through 2003; reignited between 2004 through 2007; 2012 to the present day); Burundi (1993 through 2005); Sierra Leone (1991 through 2002); Somalia with recurrent crises since the 1990s; Sudan with the Darfur crisis and Côte d’Ivoire (2002 to 2007 and 2010 to 2011). According to the attendant literature, the spades of political unrests and civil wars have engendered substantial economic liabilities that fundamentally influence countries’ ability to engage in a number of economic activities and projects.

Building on the above, during the last ten years, Africa has been characterized by a long series of anti-government protests, uprisings and revolutions. The most famous of which is the Arab Spring. The Arab Spring is a wave of protests and uprisings that began in Tunisia and Egypt in 2010 and 2011. This wave of protests spread to some other countries in Africa and the Middle East. According to the literature on economic losses, crises such as civil wars are very important (Costalli et al., 2014; World Bank, 2003). Other studies have tried to depict the determinants of crises of which, the most treated are civil wars. For example, Anyanwu (2002) investigated whether civil wars in Africa have economic and political determinants.

Second, the extant contemporary literature on political crisis in Africa has largely focused on inter alia: the relevance of political crisis on trade (Asongu et al., 2021); the importance of party systems in economic development (Pelizzo & Nwokora, 2016, 2018); externalities of political instability from tax structure (Dalyop, 2020) and income inequality (Oualy, 2021); regional intervention in boosting democracy and the importance of political crisis in the nexus (Ateku, 2020); politico-economic effects of predicting natural resource income (Frynas & Buur, 2020); nexuses between political instability, foreign investment and economic growth (Williams, 2017) and the effect of political instability on economic growth (Okafor, 2017). The closest studies in the literature to the present study are Williams (2017) and Okafor (2017). The present study departs from the underlying papers by measuring the macroeconomic influence of protests, uprisings, political crisis in Africa by means of the Generalized Synthetic Control (GSC) method and by extension, assesses the incidence played by dependence in natural resources in the investigated nexus.

There is a large body of literature on the relationship between civil war and economic growth. “Civil war” and “revolution” refer to two situations of conflict and internal unrest in a given country. Although we note some similarities between these two concepts, there are key differences that prevent us from employing the terms interchangeably. Firstly, civil wars are by definition violent. In fact, most scholars adhere to a total of at least 1,000 battle deaths to declare an internal conflict as a “civil war” while revolution or political conflict can be non-violent (for example Gandhi's peaceful demonstrations) (Asongu et al., 2020a, 2020b, 2020c). To the best of our knowledge, the highlighted existing works are based on the impact of civil war on economies. In a different light, we focus our analysis on recent political conflicts and revolutions in Africa. The choice can be justified by the fact that with the structural changes in African countries (e.g. from spillover effects of Arab spring and recent political transitions), it is relevant to understand the macroeconomic influence of recent political conflicts in Africa.

In the light of the above, the objective of our paper is to evaluate the macroeconomic influence of the recent crisis in Africa. Firstly, instead of civil war or classical crisis, the paper is interested in recent political crises mainly dominated by revolutions, protests and uprising. Secondly, in comparison to previous works which used Synthetic Control (SC), we employ the recent generalized extension labeled GSC . Thirdly, we go beyond the existing literature by evaluating the role played by natural resource dependence in modulating the influence of the crisis within the macro-economy.

The remainder of the paper is organized as follows. The theoretical underpinnings are engaged in Section 2 while Section 3 presents the data as well as identifies the candidate countries and their counterfactuals. Section 4 covers the methodology while Section 5 discusses the results. Section 6 evaluates the role played by natural resources on the average treatment influence on the treated while Section 7 concludes with implications and future research directions.

Theoretical Underpinnings: Economic Growth and Political Conflicts

Consistent with Asongu et al. (2021), it is relevant to clarify the nexus between economic growth and political conflicts. Such theoretical insights are in accordance with Olson’s (1963) Rise and Decline of Nations (RADON) in the perspective that, there are some elements of political stability that are favorable for economic growth and other dimensions of political instability that can facilitate economic growth. Therefore, the problem statement of this study on the nexus between political crises and economic growth is directly linked to the theoretical underpinnings surrounding Olson’s (1963) RADON.

According to the attendant theoretical literature (Huntington, 1968; Olson, 1963), political systems that are destabilizing (i.e. political crisis), can be linked to economic growth such that political instability or crisis is not necessarily linked to negative macroeconomic outcomes in terms of economic prosperity. This theoretical underpinning has been recently confirmed by Asongu et al. (2021) within the remit of trade openness. Moreover, as also substantiated by Hussain (2014), there are some types of political stabilities that are associated with negative macroeconomic outcomes and in the same vein, some types of political instabilities that are linked to positive macroeconomic outcomes.

Beyond the relevance of Olson's RADON engaged in the preceding paragraphs, the theoretical fundamentals on the linkage between political crisis and economic growth are in line with the corresponding literature on linkages between development outcomes and political systems (Asongu et al., 2021; McGuire & Olson, 1996; Zureiqat, 2005). Consistent with the attendant literature, the relationships build on three main types of political organizations, namely: anarchy, dictatorship and democracy. It is worthwhile to emphasis that these three types of political organizations are in line with the notion of political stability that is employed in this study given that political stability is conceived and measured in terms of the likelihood that a government can be overthrown or destabilized by violence and mechanisms that are not constitutional, involving terrorism and domestic violence. In other words, it is understood by contemporary literature (Asongu & Nwachukwu, 2016b, 2017; Tchamyou, 2021) as the election and replacement of political leaders. Accordingly, the approach via which political leaders are brought into office by means of political elections can engender the identified three principal types of political organizations. For instance, “roving bandits” is typical of bandits who determine the laws of society and such anarchy is not characterized by governments that are interested in providing public goods and services, not least, because within the remit of such anarchies, a few elite leverage on armies to increase their wealth instead of using public funds for more productive societal engagements (Zureiqat, 2005). It follows that when such a political organization is prevalent, economic growth is anticipated to be low.

With respect to McGuire and Olson (1996), autocracy aims to primarily monopolize theft in profit of “stationary bandits”. Accordingly, in the light of the perspective that governing entails stakes as to the manner in which society produces, it may be apparent that some amount of public services and goods are provided by autocratic leaders who are constrained to do so in exchange for some taxes. The obvious ramification is that the society is left with some incentives of production which can enhance economic growth beyond considerations from an anarchy-oriented political organization. In essence, while the personal income of autocrats is likely to increase given that they considerably extort rents from citizens through taxation, compared to anarchists; these autocrats enable citizens to have relatively better average standards of living.

Consistent with McGuire and Olson (1996), the third strand or democracies is linked to relatively more public commodities compared to other dimensions of political organizations. Additionally, this type of political organization has been established to be associated with enhanced political stability (Asongu & Nwachukwu, 2016c). Moreover, economic growth is linked to better democratic standards of political organization relative to anarchies and autocracies. In the light of the narrative, better public commodities are provided by governments because citizens are most likely prepared to pay taxes in exchange for enhanced delivery of public commodities.

The linkages between the discussed forms of political organizations and political stability can be understood in the perspective that the attendant political organizations are connected with some level of political stability which is linked with incentives for economic activities that engender economic growth. As documented in Asongu et al. (2021), the theoretical nexus between stability/instability and economic prosperity is provided by Olson (1963). With respect to the study, as much as political stability is positively linked to economic growth, political instability can also be positively connected with economic prosperity. These linkages have been substantiated by subsequent literature, notably by Alesina et al. (1996) and De Haan and Siermann (1996) who have broadly confirmed the same arguments on the nexus between political stability/instability and macroeconomic ramifications.

Putting the above into greater perspective, Asongu and Nnanna (2019) and Alesina et al. (1996) have maintained that political stability is linked to certainty about economic policies and consequently, avail avenues of more incentives for economic agents to consider engaging in investments that can boost economic activities and by extension, economic growth. The underlying position is also because investors have been established to give more priority in macroeconomic environments that are stable (Kelsey & le Roux, 2017, 2018) in order to avoid opportunities for capital flight and maintain a positive economic outlook. The perspective of De Haan and Siermann (1996) is in accordance with the narrative in the previous paragraph, not least, because such opportunities are connected with greater availability of capital and labor supplies, which are naturally, linked to more economic growth avenues.

Data Presentation and Identification of Candidate Countries and Their Counterfactuals

This section presents the data used in the study and identifies the selected countries and their counterfactuals.

Data Presentation

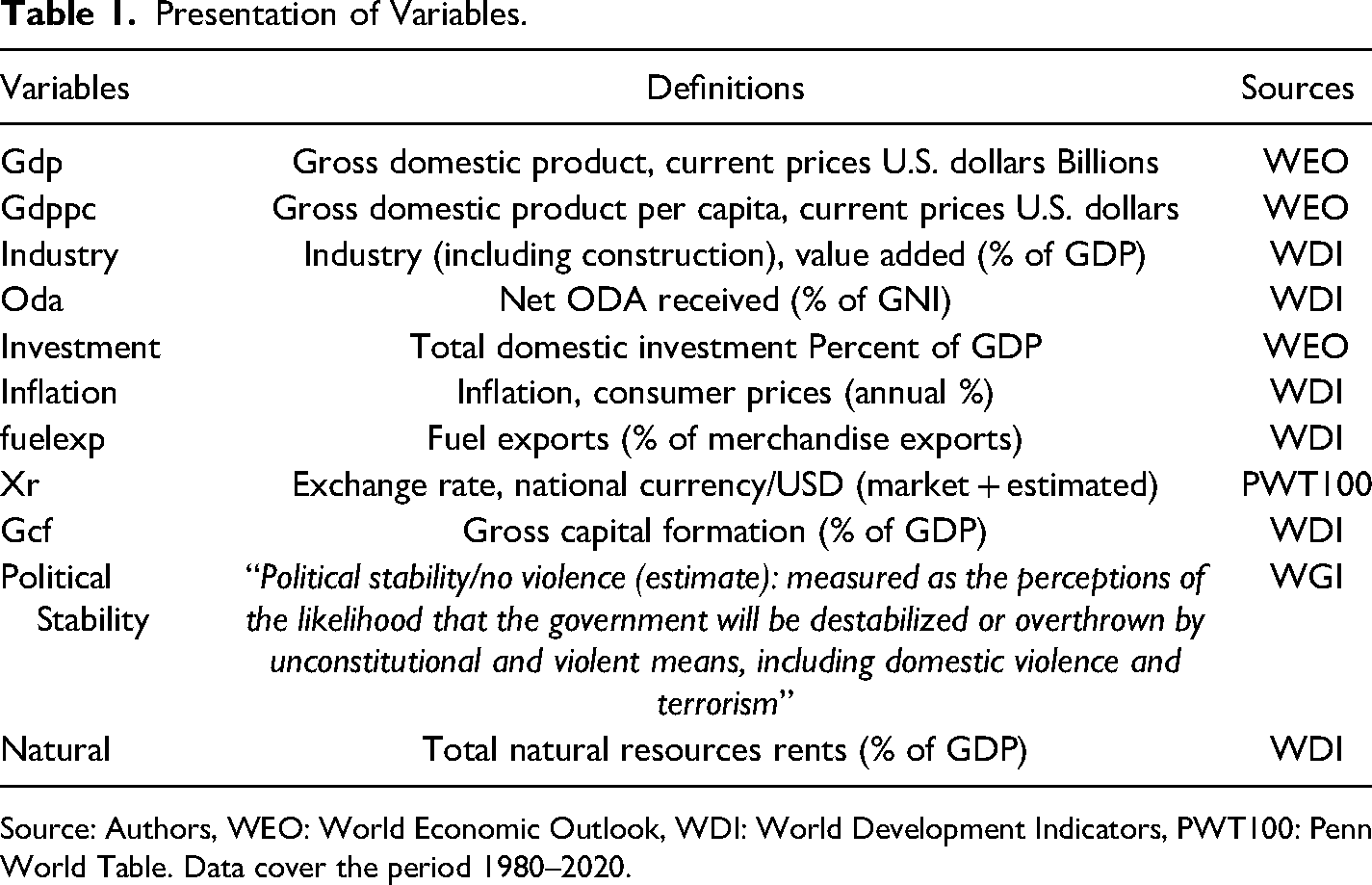

The variables are presented in Table 1. The data cover the 1980–2020 periods, both for the treated and the control groups. The selection is based on macroeconomic growth theory on applications of the synthetic control method (Abadie & Gardeazabal, 2003; Colonescu, 2017, inter alia). We have 3 predictors of the outcome variable (GDP, investment and inflation) to assess nexuses from the shock.

Presentation of Variables.

Source: Authors, WEO: World Economic Outlook, WDI: World Development Indicators, PWT100: Penn World Table. Data cover the period 1980–2020.

The Identification of Candidate Countries and Their Counterfactuals

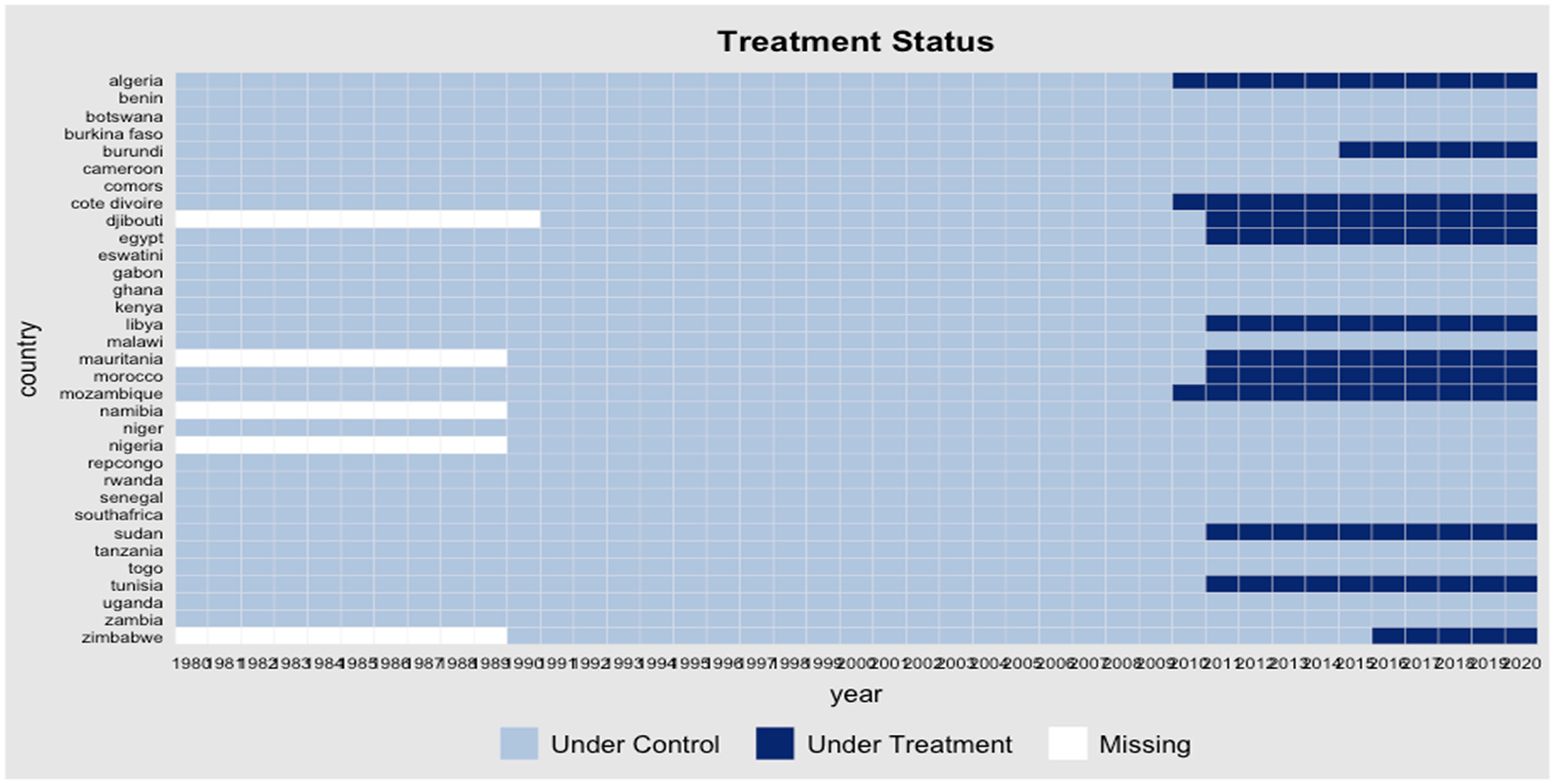

To have a response of whether political crisis has a significant nexus at the macroeconomic level, the definition of the treatment and treatment period is required. The first step in the empirical section is the definition of the treatment. In conformity with the program evaluation methods, we define the treatment as the event or the intervention to which units are exposed or not. Thus, in our study, the term “treated country” and “control country” will represent respectively, countries exposed to events and countries which are not exposed. Accordingly, an event or intervention is a political shock such as revolutions, protests and uprisings that have occurred in Africa since the 2000s. Table 1 provides the selected countries used for the study. The treated countries are those that have experienced a political crisis or protest and uprisings lasting more than one year and where the crisis has reached a certain level of intensity. The selection is also subject to data availability. In order to apply a synthetic counterfactual method, it is essential to have a control group. In order to do this, we use African countries which are not exposed to a severe uprising or protest. Note that the notion of similarity is essential at the step of choosing a control group. We identify a set of African countries having similar conjunctural and structural characteristics before the date of the events. Table 1 provides the selected countries.

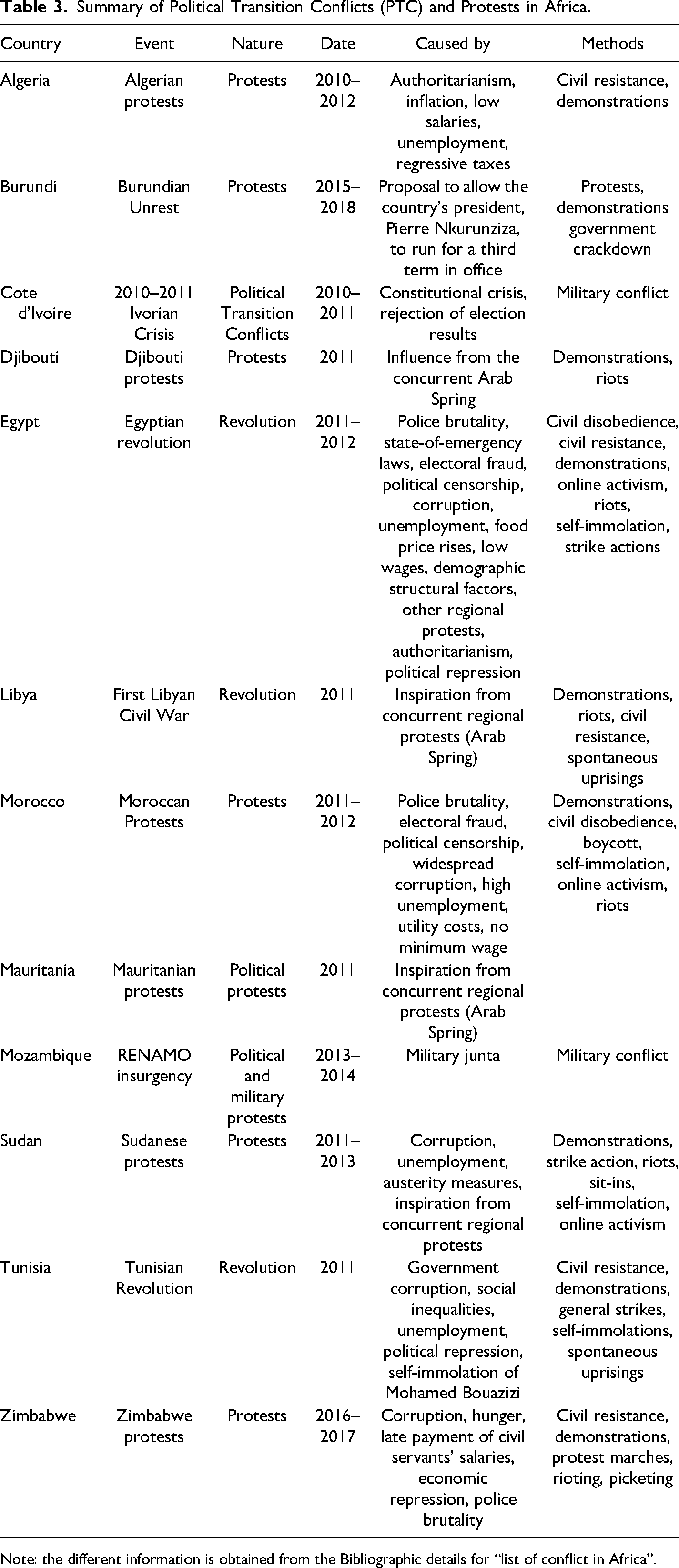

Table 2 and Graph 1 provide a panoramic view of the different episodes of political crises in Africa in recent years. The shocks are widely dominated by the Arab Spring. We note 3 revolutions (Egypt, Libya and Tunisia), 5 protests and uprisings (Algeria, Burundi, Morocco, Sudan and Zimbabwe) and 1 political crisis transition (Cote d’Ivoire). As it is shown in Graph 1, of the 12 treated countries, 10 corresponding incidents characterizing the treated countries took place either in 2010 or 2011 (Figure 1 and 2 and Table 3).

Political transition crisis and protests in Africa. Source: authors.

Evolution of the average treatment

Selected Countries for the Sample.

Source: authors.

Summary of Political Transition Conflicts (PTC) and Protests in Africa.

Note: the different information is obtained from the Bibliographic details for “list of conflict in Africa”.

Methodology

In this section, we present the Synthetic Control model and its generalized version used to evaluate the macroeconomic costs of recent political crisis in African countries.

A Motivating Model: The Synthetic Control Model (SC)

The econometric models on the nexus between conflicts and economic outcomes have some shortcomings among which, is the problem of endogeneity. Among these problems, we can cite reverse causality where an explanatory variable depends on the value of the dependent variable. In our case, the endogenous nature of the event stems from reverse causality because it is possible that the economic environment (price, unemployment, low wages, corruption, inter alia.) can cause political transition conflicts, revolutions or protests. In this paper, we suggest a model that controls for both omitted variables and reverse causality. For example, in the empirical finance literature, some techniques are suggested on how to handle reverse causality, notably: (i) the propensity score method (Forbes et al., 2015), (ii) Instrumental variables (Giordani et al., 2017), and (iii) Vector autoregression (VAR) model (Gregorio et al., 2000). However, these approaches are still potentially subject to the problem of omitted variables and mis-specification biases. The main advantage of the synthetic control method is to address the endogeneity problem in the assessment of the events on economic activity as well as contribute towards mitigating reverse causality issue. The synthetic control approach addresses the endogeneity problem by constructing a counterfactual outcome that represents what a country would have experienced had the political conflicts and protests events not occurred (Abadie et al., 2010; Abadie & Gardeazabal, 2003). For example, to assess the influence that the Arab Spring in Tunisia had on prices, a counterfactual to prices in Tunisia can be constructed; a construction that consists of several countries that never experienced these events and that jointly approximate the evolution of prices in Tunisia's prior to the change.

The Synthetic Control (SC) is a method for program evaluation impact developed by Abadie and Gardeazabal (2003) and extended by Abadie et al. (2010). Thereafter, it has been widely used in macroeconomic literature. Some notable studies that have employed the technique include: Cavallo et al. (2013) who have investigated the impact of natural disasters on economic growth; Abadie et al. (2010) who have assessed the effect of Germany's Reunification on West Germany's GDP; Campos et al. (2014) who have investigated the benefits of membership within the European enlargement and El-Shagi et al. (2016) who have examined real effective exchange rate misalignment in Euro area. The SC method is also a useful tool to assess the macroeconomic impact of crisis such as civil wars. To put this in perspective, the seminal paper of SC is applied on the economic costs of conflicts with the case study of the Basque country (Abadie & Gardeazabal, 2003). Costalli et al. (2014) measure the economic consequences of civil wars in a sample of 20 countries, while Colonescu (2017) proposes an empirical study on the effects of adopting a common currency (i.e. the euro) on a country's GDP, inflation and debt by trying to answer the following question: “what would a country's GDP have been if the country did not join the euro area, while the other countries did?”.

Thus, to estimate the significant influence, this chosen method makes it possible to define the counterfactual (i.e. the result that would have been obtained for a group of treated if the intervention had not taken place). It is for this reason that the following question is answered in the present study: what would an African country's GDP (or investment or price level) have been if the country did not endure the crisis?

Following Colonescu (2017), there are 4 stages required to construct a SC: i) the selection of the control group, ii) the construction of the counterfactual, iii) the prediction of the evolution of the outcome variable in the post-treatment period and finally, iv) the observation of the gap between the treated country and the counterfactual.

Now let us describe the technical framework of the SC methodology established by Abadie et al. (2010). Suppose there are

Let

The observed outcome for unit j at the period t is given as:

The Generalized Synthetic Control Model (GSCM)

According to Abadie (2021), SCs have become widely used in empirical research in economics and social science. With respect to the author, this is probably explained by their interpretability and transparent nature. However, there are some limitations of the method as has been apparent in the recent waves of extension. Hence, it is worthwhile to mention the GSC model proposed by Xu (2017). According to Xu (2017), the GSC improves the SC in efficiency and interpretability into several ways. Firstly, it generalizes the SC method to cases of multiple treated units and/or variable treatment periods. Secondly, the GSC provides uncertainty estimates such as standard error and confidence intervals with a possibility of parametric bootstrap procedures. Thirdly, in order to reduce the risks of overfitting, GSC can provide the correct number of factors with the cross-validating perspective. We present the GSC model in the framework presented by Xu (2017).

Let

Where

Now let

For each unit the data generator process becomes:

Where

The control and the treated units are subscripted from

Now, the average treatment influence on the treated (ATT) at time t (when

Empirical Results and Discussion

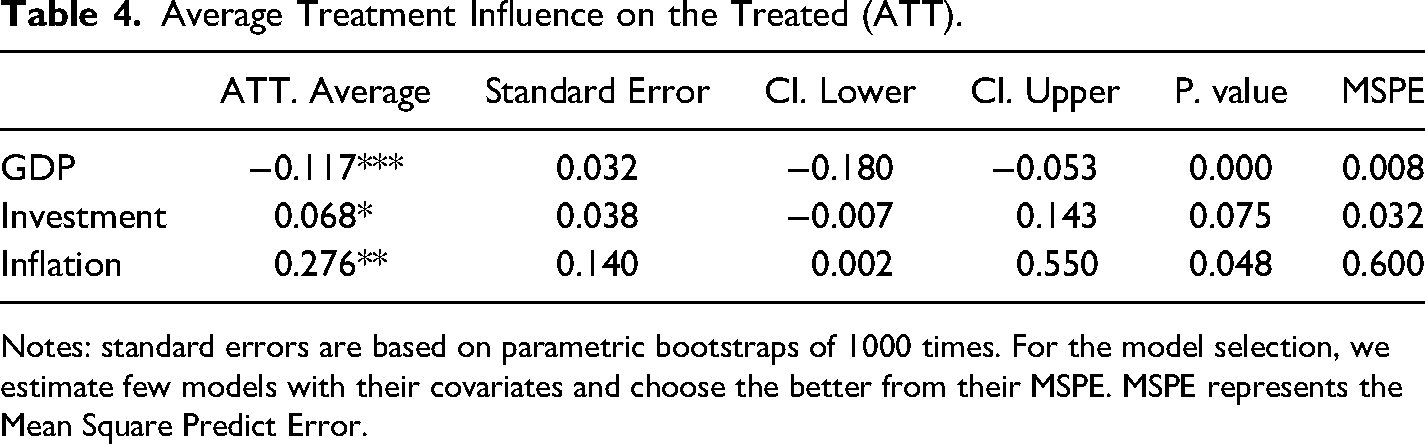

The average treatment influence on treated (ATT) is reported in Table 4. For the model selection, we refer to the cross-validation procedure before the estimation of the influence. We choose the factor that minimizes the MSPE. The results show that the ATT is significant at 1%, 5% and 10% for GDP, inflation and investment, respectively. These results imply that political crisis and protests significantly influence the selected macroeconomic variables in Africa. The nexus is negative for GDP but positive for investment and inflation. The negative coefficient associated to GDP indicates that if the crisis had not occurred, economic growth would be at a higher level compared to the counterfactual. More precisely, if the crisis had not occurred, the GDP level would have been 11.67% higher than its actual level and the price level would have been 27% lower than its actual level. Surprisingly, we note that the investment exceeds the counterfactual amount by 6% on average.

Average Treatment Influence on the Treated (ATT).

Notes: standard errors are based on parametric bootstraps of 1000 times. For the model selection, we estimate few models with their covariates and choose the better from their MSPE. MSPE represents the Mean Square Predict Error.

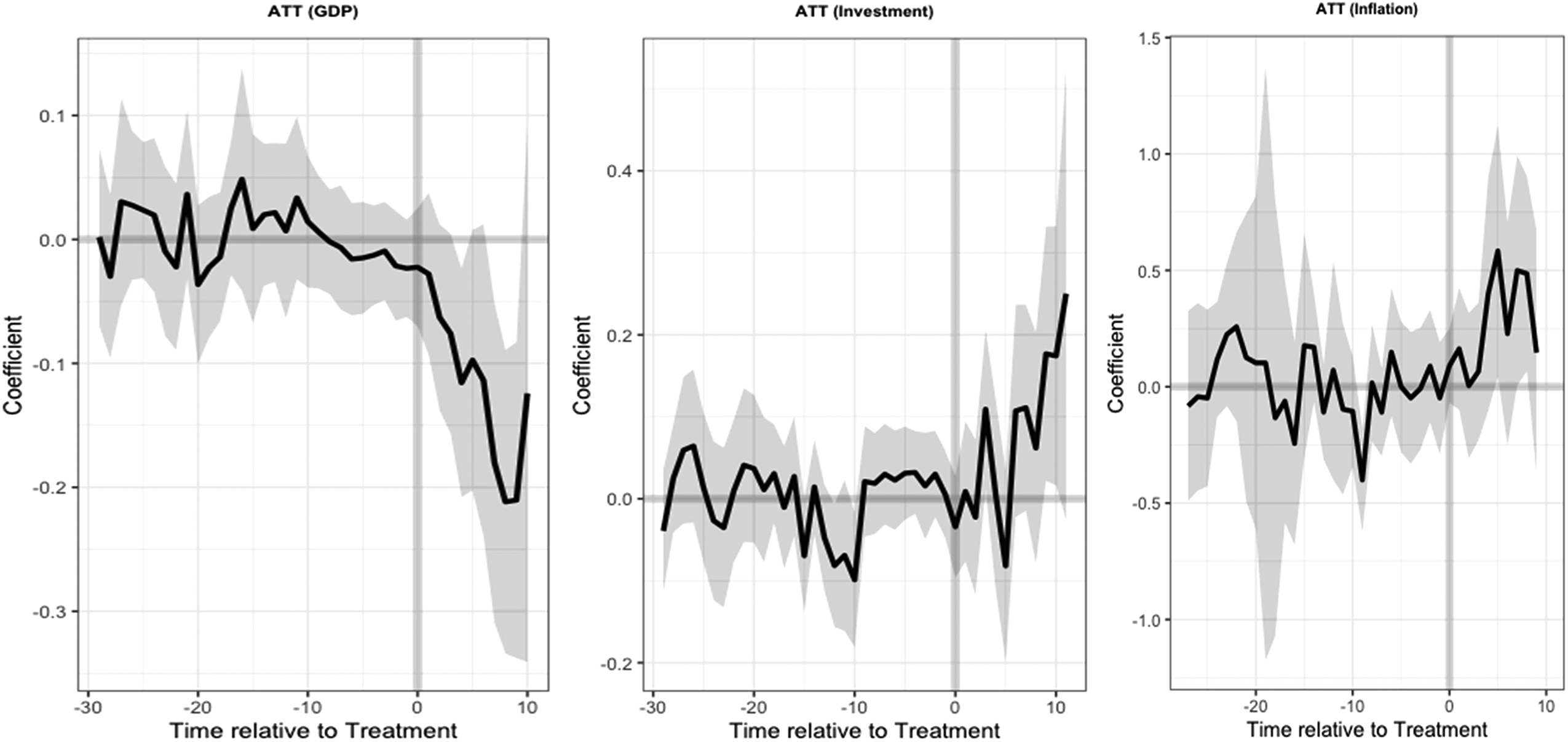

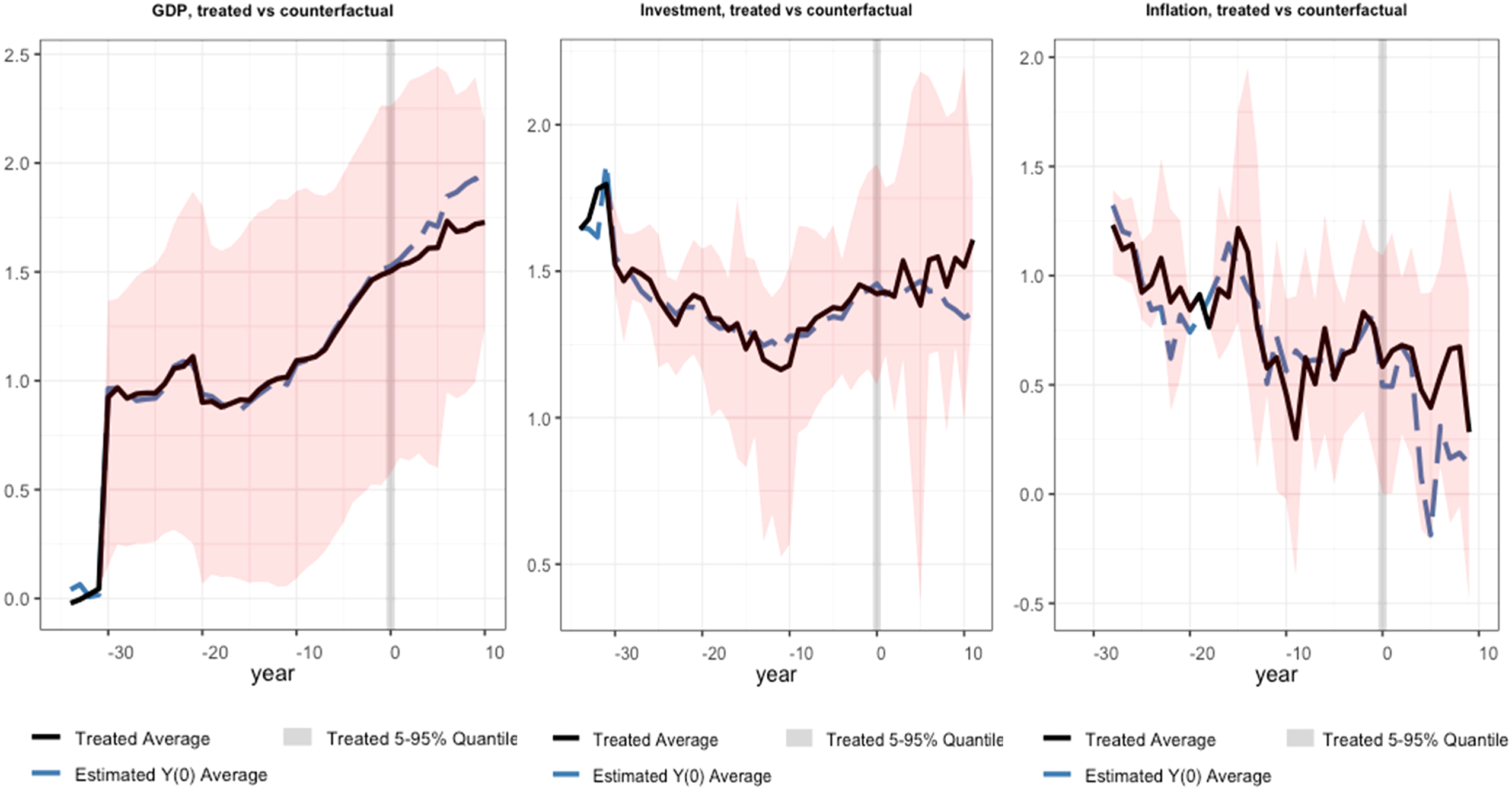

The results of the ATT over time are displayed in Figure 3. The vertical line represents the date of the political crisis or the protest and uprising. For the GDP, we note instantaneous and persistent decreasing deviation between the actual and the counterfactual over time (−3% (first period), −11% (fourth period) and −21% (ninth period)). This result confirms the literature on the economic costs of crisis (Anyanwu, 2002; Costalli et al., 2014). Regarding the investment, on average, during the first periods after the shock, the ATT is very low (between 0.8% and 0.5% for the first and the fourth period). However, we note a significant increase of the nexus from the sixth year after the crisis. The ATT goes from 11% (seventh period) to 25% (eleventh period). This result could be explained by the fact that after the crisis, the affected countries tend to increase their investment especially for economic recovery. Finally, we note that after the political crisis, the actual price levels are higher than those of the counterfactual. For example, one year after the shock, the price levels are 16.3% higher than the synthetic control. The ATT reached the maximum during the fifth period (58%). Beyond this year, we noticed a persistent decrease over time.

Variable trends, treated country versus counterfactual.

For a better view of the nexus, we can refer to Figure 3. It shows the actual trends of GDP, investment and inflation and their counterfactuals. For each variable, the treated is compared to its counterfactual. For GDP, the crisis has a substantial and persistent influence. From the date of the event, the GDP of the countries where the crisis occurred is under the counterfactual. The deviation between the actual GDP and the counterfactual is continuously widening. This result indicates non-negligible costs of the crisis on economic growth. Regarding investment, we note a relatively strong co-movement between the actual values and the counterfactual during the five first periods. This result implies that the crisis does not have an instantaneous influence on investment. However, from the sixth year, the gap widened continuously. Finally, the actual inflation exceeds the synthetic control especially after the fourth period. The gap reaches its higher magnitude from the fifth year.

Overall, political crisis, protests and uprisings have significant nexuses with the macro-economic indicator and the nexus appears to change over time from the date of the shock. For growth, the deviation of the actual series from the counterfactual is negative, instantaneous, persistent and highly significant; indicating non-negligible costs of the shock. This result could also indicate that political crisis, protests and uprisings could have permanent and sustained nexuses and therefore change the growth path in the long run. For investment, we find that, political crisis tends to boost investment but only from the sixth period; after a while the price level of the treated countries exceeds that of the counterfactual drastically some years after the event.

Natural Resource's Role on the Treatment Influence on Treated (ATT)

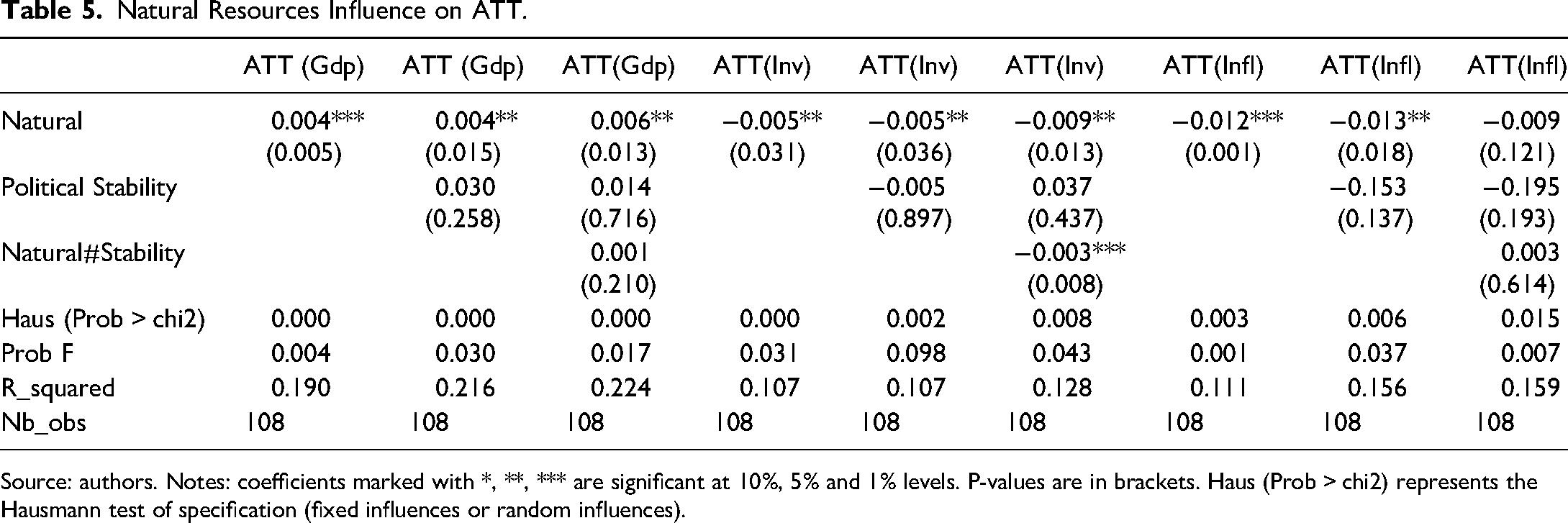

In this section, we want to analyse the role played by the natural resources in the paths of the ATT. More precisely, we examine the determinants of political crisis on economic growth and focus our analysis on natural resources and governance. This choice can be justified by the fact that our treated countries depend significantly on natural resources such as many African economies. Our idea is based on the Dutch disease theory and its mechanisms (Badeep et al., 2017; Bhattacharyya & Hodler, 2010), inter alia.

For this purpose, we use our ATT represented by the gap between the actual indicator and its counterfactual obtained with the GSC previously. We select natural resources rents (% GDP) and the stability to depict the role played by governance to modulate the relationship. Moreover, we integrate its interaction with political stability.

The results are presented in Table 5. The Hausman test shows that the panel with fixed influences better represents the data generator process. Regarding the ATT on GDP, the results indicate that only natural resources significantly and positively influence the gap between actual growth and the synthetic control. The positive nexus indicates that the dependance on natural resources amplifies the negative influence of political crisis and uprisings on economic growth. Indeed, neither the stability nor the interaction variable is significant. This result implies that governance cannot modulate this negative nexus. Further, natural resources negatively influence the ATT on investment. Thus, the more the treated country depends on natural resources, the more it becomes resilient to investment losses caused by the political crisis. Since the interaction with political stability is significant at 1% level and negative, this resilience is reinforced by a higher level of governance. Finally, regarding the price level, it is apparent that natural resources are significant only with the regression without the interaction. Its negative sign implies that it mitigates the influence of the crisis on inflation.

Natural Resources Influence on ATT.

Source: authors. Notes: coefficients marked with *, **, *** are significant at 10%, 5% and 1% levels. P-values are in brackets. Haus (Prob > chi2) represents the Hausmann test of specification (fixed influences or random influences).

Conclusion and Policy Implications

In this paper, we have investigated the macroeconomic influence of the recent political crisis, protests and uprisings in Africa. In the first part of the article, we have employed a recent extension of the Synthetic Counterfactual labeled GSC on three macroeconomic variables namely: GDP, investment and inflation. In the second part, we have used the estimated difference between the actual macroeconomic variable and their counterfactual (ATT) to assess the role played by natural resources on the crisis’ negative influence on economic development.

The results can be summarized as follows. In the first exercise, the GSC shows that political crisis, protests and uprising have significant influences on macroeconomic indicators. Indeed, the nexuses change over time from the date of the shock. For growth, the deviation of the actual series from the counterfactual is negative, instantaneous, persistent and highly significant; indicating non-negligible costs of the shock. This result demonstrates that political crisis, protests and uprisings could have permanent and sustained nexuses and therefore change the growth path in the long run. For investment, we find that, political crisis tends to boost it but only from the sixth period, while the price level of the treated countries drastically exceeds that of the counterfactual some years after the event.

In the second exercise, it appears from the regressions that for the ATT on GDP, only natural resources significantly influence the gap between actual growth and the synthetic control. The positive nexus indicates that dependance on natural resources amplifies the negative influence of political crisis and uprisings on economic growth. Further, natural resources negatively influence the ATT on investment. Thus, the more the treated country depends on natural resources, the more it becomes resilient to the investment losses caused by political crisis.

Firstly, given that natural resource dependance amplifies the economic losses from political crisis, African countries should find strategies to diversify their economies away from dependance on natural resources. Secondly while natural resource dependance is favorable for investment in the period after the crisis, a substantial part of the resources should be oriented towards funding economic reconstruction and providing appropriate responses to political crises.

The findings of this study could be improved in different ways. A first way is to reconsider the problem statement using microeconomic data because some insights from event studies may not be captured with macroeconomic data. Hence, surveys within the remit of primary data could provide more qualitative insights in understanding the investigated nexus. A second way is to assess the role of other macroeconomic variables such as human capital, infrastructure and governance in mitigating economic losses accruing from political conflicts, crises and strife. It is therefore worthwhile for future studies to evaluate the mechanisms (political change/political rent-seeking/economic redistribution) by which political shock is transmitted in the economy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.