Abstract

Since the introduction of the euro, German growth has been primarily based on exports. Signs of an exhaustion of Germany's export-led growth model were already evident before the energy crisis of 2022–23, which hit the country hard. German elites could have capitalized on the shock to rebalance their growth strategy. But the opposite happened: the government's adjustment strategy has aimed at doubling down on export-led growth and protecting the core export industries. This article investigates the politics of Germany's economic policymaking in hard times. We show that the government's economic policy responses were driven largely by an export sector growth coalition led by cross-class alliances in the chemical, metalworking, and engineering sectors. In contrast to previous corporatist decision-making, which aimed to include broader societal concerns in peak-level concertation, German corporatism has undergone a functional transformation toward the predominance of export sector distributive coalitions. This article's findings contribute to the emerging literature on the politics of growth models in comparative political economy.

Comparative political economy (CPE) identifies Germany as the paradigmatic case of an export-led growth model, 1 defined as a macroeconomic configuration in which foreign rather than domestic demand serves as the economy's key growth driver. 2 Export-led growth models are dependent on conditions that cannot be readily controlled by domestic actors. These include open markets in a liberal trade regime, sustained foreign demand for domestic exports, and an advantageous real effective exchange rate vis-à-vis trading partners.

In the two decades since the introduction of the euro, these conditions have been favorable for the German economy. During this time, domestic sectors grew moderately at best (and even contracted at times), but sustained growth of net exports pulled the economy out of the long crisis persisting since the mid-1990s. In the aftermath of the 2008 global financial crisis, Germany enjoyed a period of moderate economic growth and declining unemployment, even coupled with real wage growth and a partial rebalancing of the previous decade's wage moderation. 3 However timid, this trajectory was interrupted by the outbreak of the Covid-19 pandemic. 4

Europe's 2022–23 energy crisis was accompanied by a severe inflation shock, which has hit Germany particularly hard, for several reasons. First, Germany's export-led growth model thrives on a large and resilient manufacturing sector, centered on the chemical, metalworking, and engineering industries—highly energy-intensive sectors. The cutting off of Russian gas exports to Europe thus affected the very core of Germany's manufacturing production, with the risk of bringing it to a halt. Second, Germany's energy shock was acute because, contrary to other European countries, it had increasingly relied on Russian gas and was therefore suddenly confronted with the need to substitute a large proportion of its energy imports at higher prices. 5 Third, with price inflation on the rise, and a cost-of-living crisis in the making, 6 fears emerged of a possible resurgence of class conflict, with unions’ more assertive wage claims threatening to engender a price-wage spiral and undermine Germany's international cost competitiveness. Concomitantly, the disruption of European energy markets has evolved in tandem with rising protectionism and geopolitical rivalries in the new multipolar order, 7 laying bare the extreme vulnerability of Germany's unbalanced export-led growth model. During 2023, Germany experienced an economic recession, and the economy continued to stagnate in 2024. 8

All things considered, one could in theory have expected the German government to seize the energy crisis to rebalance the export-led growth model, thereby reducing the country's foreign vulnerabilities. But Germany's adjustment to the energy crisis is a tale of doubling down, in which Germany's economic elites—once known for their ordoliberal penchant 9 —have brought new interventionist policy tools to bear on the unchanged aim of protecting and strengthening the export-led growth model, with high fiscal costs for the state and society.

In fact, soon after entering office in late 2021, the “traffic light” coalition government was confronted with the severity of the energy and inflation crises. 10 The government promptly engaged in national concertation with cross-class representatives from the chemical, metalworking, and engineering sectors, convening various high-profile concertation meetings at the Chancellery and subsequently forming a “gas price commission” to enact energy price caps. 11 The concerted adjustment strategy was aimed unequivocally at protecting Germany's core manufacturing industries and intensifying the export-oriented growth strategy via three strategic pillars. First, the government has generously subsidized increases in energy bills to contain firms’ energy input costs. Second, Chancellor Olaf Scholz has actively promoted wage restraint in sectoral collective agreements, with the government subsidizing firm-level inflation bonuses by exempting them from taxes and social security contributions. Third, the government and the gas price commission have secured extensive state aid for domestic firms under the European Commission's Temporary Crisis Frameworks.

Why and how does Germany persistently pursue an export-oriented growth strategy, even under adverse exogenous and macroeconomic conditions and the evident vulnerabilities associated with such an unbalanced growth model? In this article, we combine the concept of growth coalitions with the study of Germany's “semi-corporatist” system of interest representation to inquire into the political underpinnings of Germany's export-led growth model. 12 Economic adjustment in hard times constitutes fertile soil for studying the politics of growth models because it is during crisis times that economic elites’ beliefs, preferences, and conflicts of interest become particularly visible and social conflict intensifies over the determination of national economic policymaking. 13 Indeed, our analysis indicates that Germany's export-oriented adjustment strategy was determined largely by a clear-cut and identifiable growth coalition composed of cross-class actors from Germany's core export sector industries, namely, chemical, metalworking, and engineering. Such an export sector growth coalition enjoyed preferential access to the federal decision-making arena and became predominant in shaping the country's response to the energy crisis.

The capacity to shape and determine the government's economic policy stems from these sectoral social actors’ greater economic weight in the growth model, their stronger organizational capacity for sectoral interest representation, and their greater embeddedness in federal political circles via personal connections and ties through the supervisory boards of Germany's largest industrial firms. By contrast, lacking these elements, weaker sectoral representatives from other major economic sectors—such as construction, private services, and the public sector—were largely marginalized, along with their economic preferences. The export sector growth coalition eventually succeeded in framing its particularistic interests as Germany's collective interests and was able to appropriate large fiscal resources, for example, via direct energy subsidies to the industrial sector. As a result, Germany's adjustment strategy has heightened distributional conflicts between the manufacturing export sectors and the domestic sheltered sectors, with the former clearly emerging as a major beneficiary of the German government's new-found economic activism.

These findings contribute to CPE scholarship on the study of the energy crisis and the return of inflation, as well as burgeoning debates on the politics of growth models. 14 First, the article offers an empirical and systematic analysis of Germany's economic adjustment to the energy and inflation crisis. Second, by investigating the political economy of Germany's economic policy in hard times, it traces the process of interest intermediation “in action.” The study of the political determinants of Germany's export-oriented growth strategy during a major critical juncture reveals the specific political underpinnings of Germany's export-led growth model.

The article unfolds as follows. We discuss the vulnerabilities and exhaustion signs of Germany's growth model. We then introduce the analytical concept of growth coalitions and link it to the characteristics of Germany's sectoral corporatism. Subsequently, we establish the political dominance of representatives in the chemical, metalworking, and engineering industries and analyze empirically Germany's adjustment strategy to the energy crisis, uncovering the central role played by the export sector growth coalition in the definition of national economic policymaking. The conclusion discusses the article's findings with regard to the functional transformation of Germany's neocorporatist system of interest intermediation.

Germany's Export-Led Growth Model Under Stress

The growth model approach is part of a broader set of the CPE literature that studies the cross-national variation of modern models of capitalism. 15 At the center of interest are the drivers of macroeconomic demand. While wage-led growth predominantly defined European countries’ growth models during the Fordist period, various growth drivers have gained prominence in the post-Fordist era. In this respect, Germany stands out as an economic model in which, over the past two decades, growth was based largely on net exports, that is, on growing foreign demand for Germany's manufacturing exports. This is an unusual development for a big country with a large domestic sector. 16 During this phase, subdued wage growth, 17 low public and corporate investment, 18 and recurrent budget surpluses (during 2012–19) contributed to the compression of domestic demand. Correspondingly, Germany exhibited relatively low inflation, the depreciation of its real effective exchange rate, and chronic current account surpluses, 19 all of this in a context of liberalizing labor market and welfare state reforms. 20

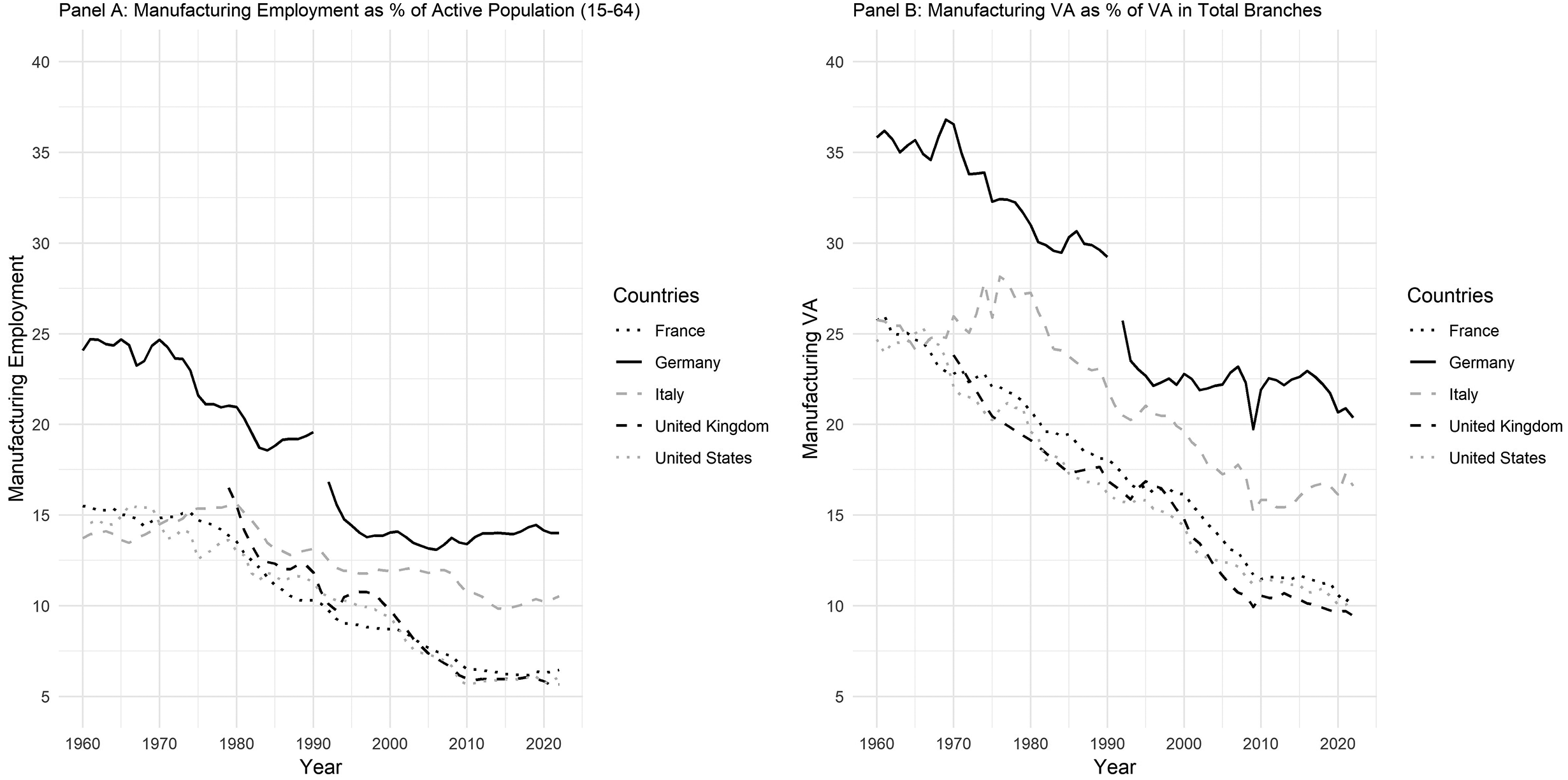

Germany's export-led growth model has developed hand in hand with a resilient manufacturing specialization. Historically, at least since the 1960s, Germany's manufacturing sector has been larger than those in the other major advanced economies. This contrasts sharply with the country's comparatively small construction and high-end services sector and an undersized public sector. 21 What is particularly striking, however, is that since the late 1990s Germany has decoupled from the secular trend of deindustrialization. 22 Its industrial export surpluses were large enough to stabilize the manufacturing sector, both in employment (Figure 1, panel A) and value-added terms (Figure 1, panel B). With an export-oriented growth strategy, Germany has in turn contributed to the deindustrialization of its trading partners, 23 a fact that regularly causes international conflicts within Europe and beyond. 24

Share of manufacturing employment as a percentage of the active population (panel A) and manufacturing value added as a percentage of the total economy (panel B), Germany compared with other major economies (1960–2022).

Retrospectively, Germany's export-oriented growth strategy seems to have benefited from the cumulation of particular structural and international conditions. In the recent past, however, it has become increasingly unclear whether Germany's export-led growth model can be successfully reproduced in the future. For that to occur, in fact, the extent of foreign demand channeled into Germany would have to expand even further. Several developments in the international political economy and new structural trends, however, indicate that this is not a realistic scenario.

First, the transformation of the German economy into an unbalanced export-led growth model during the 1990s and 2000s coincided with a phase of hyperglobalization. With international trade expanding on a global scale, Germany was able to secure steadily growing market shares. Since the 2008 global financial crisis, however, the expansion of international trade has slowed down, and global trade has partly receded into regional trade within competing economic blocs. 25 Moreover, since the mid-2010s, the trade policy landscape has undergone significant transformations. With economic protectionism on the rise, risks of trade disruptions are mounting and a liberal trade regime is no longer a given. Germany's industrial companies, for example, have openly voiced their fears of an escalating trade war with China over the European Union's decision to impose tariffs on Chinese imported electric cars. 26 As a result, doubts have emerged as to whether Germany is—and will remain—able to increase its export share in world markets to the extent necessary to sustain its export-oriented growth strategy.

Second, and relatedly, globalization has entered a new phase regarding the division of labor within international production networks. The late years of the hyperglobalization era were characterized by the emergence of global value chains with far-reaching vertical and international fragmentation of production. This resulted in deflation of the prices of goods flowing into German industrial production as intermediate products, 27 especially into Germany's large manufacturing hubs in the automobile industry, chemicals, and pharmaceuticals. 28 Under the headings of derisking, reshoring, and friend-shoring, the Covid-19 pandemic and new geopolitical rivalries have fostered a restructuring of global value chains and international trade patterns, 29 with increasing risks and vulnerabilities, especially for countries overreliant on foreign demand.

Third, Germany's export-oriented growth strategy was, among other things, premised on cost competitiveness and a heavy reliance on foreign energy imports for its energy-intensive industrial sector. In the past, Germany had sustained the former via a competitive undervaluation of its real exchange rate and obtained the latter from Russia. 30 The Ukraine war, which led to an energy crisis and inflation shock, eroded both foundational conditions underpinning Germany's growth strategy. Apropos the former, the supply-side shock risked spilling over to the labor market, engendering industrial conflict and a price-wage spiral across the economy, undermining Germany's international competitiveness. Regarding the latter, after the European Union's sanctions in response to its invasion of Ukraine, Russia retaliated by significantly reducing gas exports to Europe. Germany, heavily reliant on Russian fossil fuels—especially gas—was particularly vulnerable to the energy shock and was therefore disproportionately affected. 31

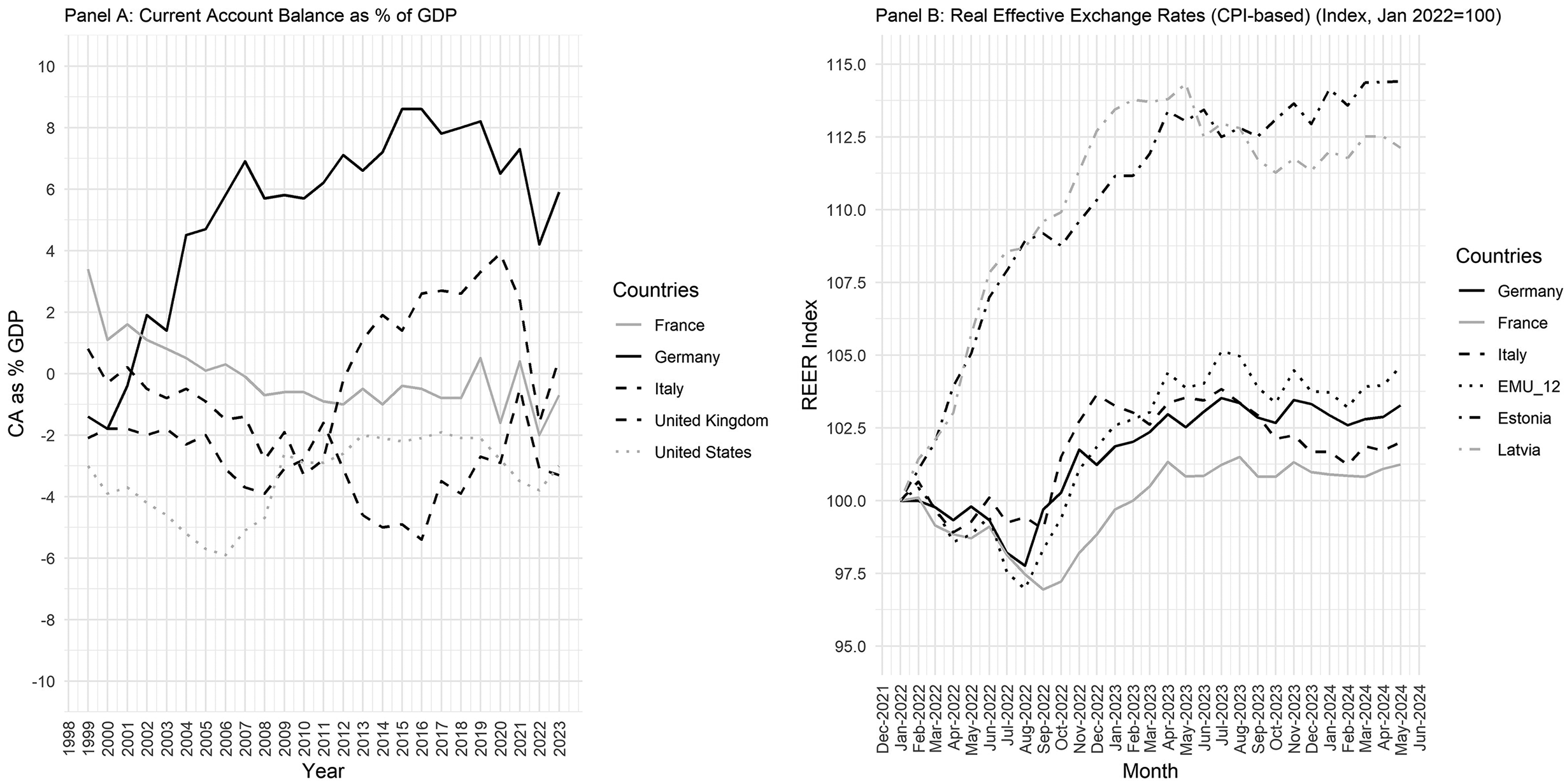

Thus, the energy crisis shook Germany's manufacturing powerhouse to the very core, with the current account surplus dropping by around 3 percent in 2022 (Figure 2, panel A). However, Russia’s disruption merely precipitated a growing awareness of Germany's energy problem—one that the country would have confronted regardless of the energy shock. A study of the future development of energy costs in Germany in fact shows that, because of the comparatively high production costs for renewable energy, Germany will experience substantial energy cost disadvantages in the mid- to long term. 32 This will have a negative impact on the production of energy-intensive raw materials, such as crude steel, aluminum, and basic chemicals, such as ammonia, which are core processes in many of the industrial value chains that characterize Germany's economy. These primary products would have to be imported in future. Although this is not problematic in itself, it raises questions about Germany's future capacity to generate economic growth via growing net exports in the industrial sector.

Current account balance as a percentage of GDP in selected countries (panel A) and real effective exchange rates based on the consumer price index (panel B).

As a result, the case for a rebalancing of the German growth model via strengthened domestic demand has never been as pronounced as it has been over the recent years. The economic turmoil caused by the energy crisis, coupled with mounting protectionism in international trade, have laid bare the vulnerabilities of Germany's export-led model. Thus, at least in theory, one may have expected this critical juncture to serve as a catalyst for change in Germany's export-oriented growth strategy. In practice, however, the contrary has occurred: both the narrative around the energy crisis and the adjustment strategy that followed have underscored the need to further protect and strengthen Germany's industrial prowess and the export-led growth model, at high fiscal cost and by means of proactive state intervention.

Indeed, the public was presented with the narrative of an imminent, eruptive, full-fledged deindustrialization, and the threat of an ongoing collapse of Germany's industrial base. 33 This and similar frames proved to be highly effective in steering the debate on adjustment strategies toward one-sided protection of the industrial sector. The narrative on the collapse of German industry has not materialized, however, as several indicators make clear. First, a marked decline in industrial production within some of the most energy-intensive parts of the chemical and metal industry certainly occurred. 34 But these were offset by relative stability in the mechanical engineering sector. 35 Second, when looking at manufacturing in 2021–23 from a value-added perspective, no deindustrialization of the German economy is discernible. 36 Third, with almost 46 million employees, the German economy recorded an all-time employment peak in 2023, despite the shock. Never before had the Germany economy recorded employment levels so high. 37 Fourth, after a decline in 2022, in 2023 the German current account surplus jumped back to 6 percent (Figure 2, panel A), the level at which trade surpluses are considered excessive under the European Macroeconomic Imbalance Procedure. 38

All in all, little speaks in favor of a collapse of the German industry. But it is unlikely that the fairly resilient German export industry can continue to act as the decisive German growth engine, as it did in the past. The contextual factors necessary for that are no longer present. The world economy's ongoing transformations suggest the need for a rebalancing of Germany's growth strategy with an eye to bolstering domestic demand and reduce domestic dependencies on foreign demand and intermediate inputs. During the recent energy crisis, however, the government's adjustment strategy consisted of doubling down and further protecting and promoting the industrial export sector. This strategy, we will show, was supported by a precise and identifiable growth coalition, consisting of a cross-class alliance of organized interests from the chemical, metalworking, and engineering sectors.

Sectoral Growth Coalitions in a Semicorporatist Setting

Why and how does the German government persistently pursue an export-oriented growth strategy, even under adverse exogenous and macroeconomic conditions and the evident vulnerabilities associated with an unbalanced export-led growth model? What are the political underpinnings of such economic policy choices? In this section, we provide an analytical lens for the study of interest intermediation in the design and implementation of growth strategies. 39 We argue that, in the German case, the analytical concept of growth coalitions should be combined with insights from the literature on sectoral corporatism, which highlights the role of sectoral “distributive coalitions” whereby particularistic, sectoral logics can creep into macro-corporatist settings.

Recent scholarship on the growth model approach has aimed particularly at studying the politics of growth, trying to shed light on the power bases of such macroeconomic constellations. 40 This literature builds on the premise that governments’ economic policy choices are informed by sectoral growth coalitions representative of both capital and labor's organized interests. Thus, employers’ organizations, trade unions, and firms representing given economic sectors will lobby political decision makers to have their particularistic policy preferences translated into collectively binding public policy decisions. Building on Peter Gourevitch's work, the growth model literature speaks of producer groups to characterize the network of actors directly involved in the production process. 41 The concept of sectoral growth coalitions includes further societal actors and political representatives who operate in support of the economic interests of the respective sector. These growth coalitions become predominant when the sector in question is among the leading sectors—or key engines of growth—in the growth model, and when they coalesce around an ideational construct that conceives the functioning of the whole economy as premised on the economic interests of certain key sectors. These coalitions, the literature suggests, are organized around “a set of propositions about how the economy works and what the overarching goals of government policy should be.” 42

Intersectoral conflicts of interest across economic sectors lie at the center of the new literature on the politics of growth models, building on older CPE debates. 43 Indeed, established political economy literature has shown that the economic interests of socioeconomic actors can diverge substantially, for example based on whether they operate within sheltered or export-oriented sectors. 44 Economic policies, which benefit domestic sectors such as construction, the public sector, or the low-end services, can be detrimental to the export-oriented industrial sector, and vice versa. Conflicts of interest emerge, first and foremost, on the parameters of macroeconomic policy: the export sector is particularly sensitive to exchange rates (and their degrees of stability), but is less sensitive to interest rates, while the opposite holds true for the construction sector. The public sector needs a solid tax base to thrive, and private services are dependent on anticyclical fiscal policymaking, while the export sector is cost-averse and therefore also tax-averse.

How sectoral interests are represented within policymaking processes depends on the properties and associational patterns of employers’ and workers’ interest organizations, and on the institutional environment that embeds them. In other words, producer coalitions perform differently depending on the national system of interest representation. Here, the overlap with the established literature on neocorporatism becomes apparent. 45 A large scholarship has investigated the effects of neocorporatist institutions on economic outcomes, such as price inflation and/or (un)employment, 46 or on societal outcomes, such as the quiescence of labor movements. 47 In countries with centralized wage-setting systems, peak-level, encompassing organizations are said to anticipate the inflation spillovers of their high wage demands and moderate their claims with a view to preserving employment levels. Thus, centralized wage-setting systems would guarantee lower unemployment levels with price stability, 48 an outcome described as a public good benefiting all societal actors in the political economy. 49

Many of the findings underpinning the neocorporatist scholarship derive from comparative analyses of inflation management during the 1973 and 1979 oil shocks. 50 Researchers concluded that encompassing organizations granted with a state-protected representational monopoly would not only transmit their preferences to the political arena but also instruct and discipline their members into accepting policy outcomes that are feasible, as well as compatible with the common good. By so doing, such encompassing organizations turn predatory particularistic preferences into socially acceptable collective outcomes and thus exercise a socio-economic regulatory function different from both price-based market mechanisms and state-mandated hierarchies. This governance mode was famously termed “private interest government” by Wolfgang Streeck and Philippe Schmitter. 51

But not all collective actions pursued by cross-class coalitions are corporatist in the strict sense. Mancur Olson famously argued that powerful organizations would instead behave as “distributional coalitions.” Such coalitions operate to extract rents from government policy by internalizing gains and distributing benefits to their members—in the form of club goods—while externalizing the costs of collective action to the collectivity. Over time, Olson predicted, the predominance of distributional coalitions would lead to institutional sclerosis and economic decline. 52 In a debate that followed his seminal book on “the rise and decline of nations,” Olson argued that even encompassing organizations would ultimately behave like rent seekers in the long run, because they consist of competing sectoral suborganizations with particularistic interests. 53

Considering Germany's sectoral organization of the political economy, there are good reasons to connect the concept of growth coalitions to the organizational properties of interest representation as established by the neocorporatism literature. In fact, there is a fine line between corporatism as stable involvement of encompassing organizations in politics (in the form of concertation), 54 and the inclusion of sectoral, non-encompassing organizations that behave as distributional coalitions in the policymaking process. We maintain that Germany's peculiar institutional setting, centered on neocorporatism intermediation with the predominance of powerful sectoral associations, underpins Germany's growth strategy aimed at promoting and protecting the manufacturing export sector, even at the expense of other domestic sectors.

Indeed, Germany has traditionally been “semi-corporatist.” 55 Stable concertation exists in certain policy areas, for example, in the administration of the social insurance funds and in the regulation of vocational training. In contrast, concertation at the top level has remained an exception. The focus of associational power is on the sectoral level. German trade unions and employers’ associations are neither centralized nor highly encompassing. Within their sectors, however, such organizations continue to have a representation monopoly.

Despite structural stability, interest intermediation in Germany has undergone a functional transformation, the results of which are closer to an Olsonian setting than to a neocorporatist one. This functional change has taken place gradually, over several decades, and has culminated in a particular logic of interest representation that politically favors well-connected industrial stakeholders in the export sector. The mode we describe in this article is therefore different from neocorporatist decision-making. It is not a process of social concertation with capital and labor. Rather it depicts the workings of a narrow coalition of cross-class sectoral actors that determine their particularistic economic interests and pursue joint strategies to have their preferences turned into collectively binding public policy. The moment of exchange across classes occurs at the beginning of the political process, not at the end, when tripartite actors meet. When the government is addressed, sectoral interests have already prevailed, and sectoral concerns trump class interests. This, we argue, is the core of the interest-based political foundation of the German industrial export model.

The response to the energy crisis in 2022–23 clearly points to an observable and fundamental shift from corporatism as private interest government, with a regulatory function oriented to and compatible with the common good, to a distributional coalition of particularistic manufacturing interests. In the past, under Fordism, when economies were predominantly industrialized, neocorporatist intermediation centered on the manufacturing sector was not necessarily a problem. Within today's economies populated by large service sectors, however, the scenario looks completely different: manufacturing-based interests are no longer representative of the economy at large. In imposing their particular sectoral interests on public policy, manufacturing coalitions unavoidably impose increasing costs on society as a whole. As Colin Crouch presciently put it in 2006, “If socio-economic change erodes the encompassing character of an organizational system, it will cease to operate in a neo-corporatist way.” 56

Thus, our analysis emphasizes the contrast between neocorporatist policymaking premised on encompassing organizations and neocorporatist decision-making involving, as in Germany, distributional coalitions that pursue narrow sectoral interests. What we will describe empirically resembles rent-seeking behavior in a semicorporatist setting aimed at preventing Germany's deindustrialization at almost any societal cost. In so doing, we combine an emphasis on sectoral actors’ agency with the study of enabling institutions within the system of interest representation.

The Representation of Sectoral Interests in Germany

We analyze the foundations of Germany's growth coalition in three steps. We begin by establishing the economic importance of given sectors—the chemical, metalworking, and engineering sectors—as key engines of growth within the German political economy. We proceed by analyzing the various organizational capacities of sectoral organized interests, showing how the chemical, metalworking, and engineering sectors enjoy a much more cohesive membership base and greater associational and representational capacity. Lastly, we delineate the institutional linkages and personal relationships that grant actors within these key sectors privileged access to the decision-making arena. The subsequent section will analyze how the export sector growth coalition made its way into federal economic policymaking during the energy crisis, resulting in the determination of the export-oriented adjustment strategy observable in Germany.

The Economic Weight of Germany's Sectoral Interests

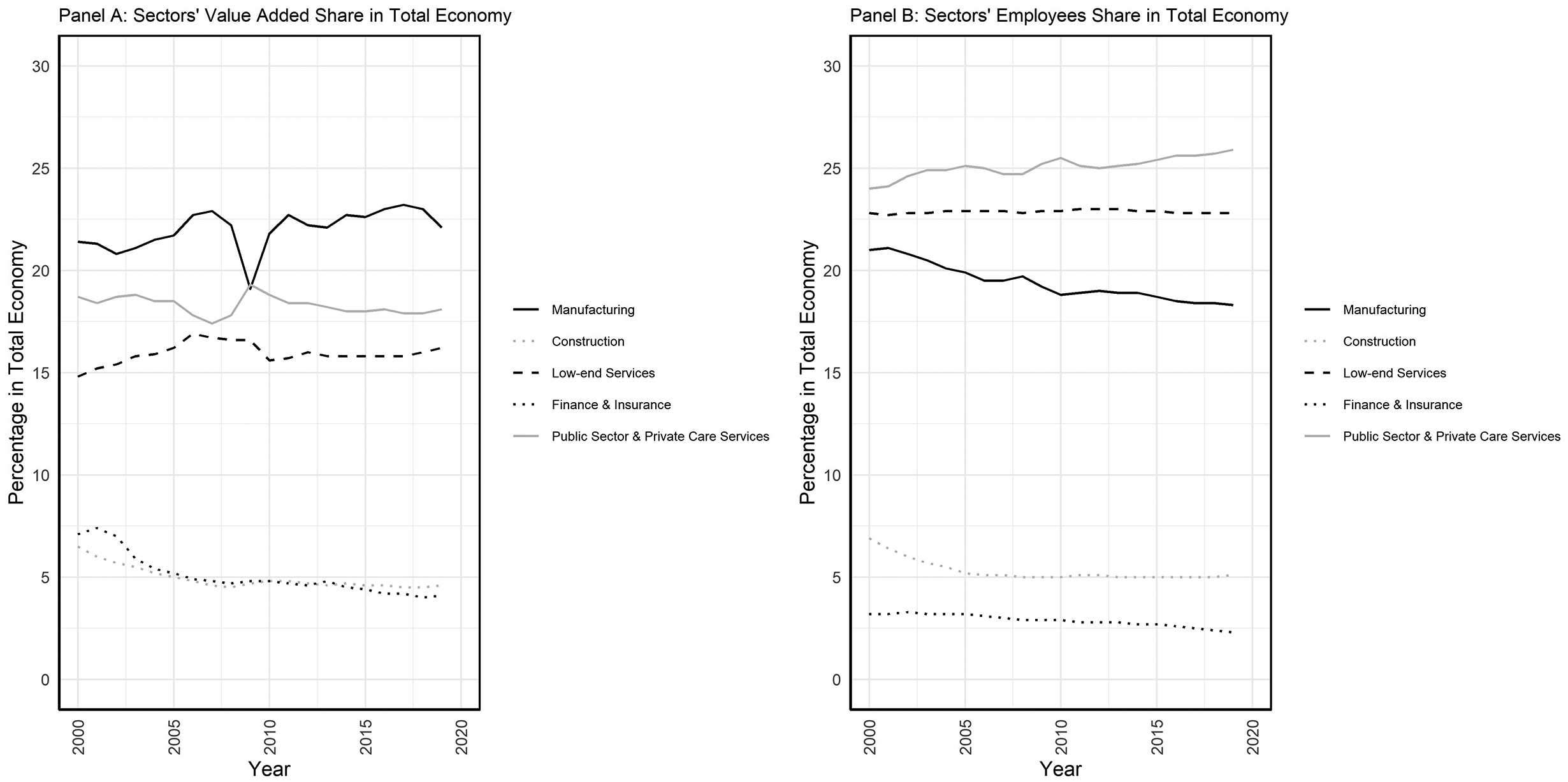

As mentioned, the manufacturing sector openly enjoys a privileged role in Germany's export-led growth model, given its relevance in both value-added and employment generation. Figure 3 shows how the manufacturing export sector accounts for above 20 percent of total value added and for more than 16 percent of total employment in the German economy. By international comparison, the financial and construction sectors are comparatively small in Germany. The other sectors in the German economy which could act as counterweights to the manufacturing sector are the low-end services and the public sector. However, as discussed in the next section, the latter sectors are either internally heterogeneous and divided or organizationally weak in Germany.

Share of sectoral value added (VA) and employment in the economy as a whole of the different major economic sectors, Germany.

In Germany, the manufacturing sector is the central component of the country's longstanding export orientation—a full-fledged “export mystique,” as it has been aptly described. 57 Manufacturing is predominant in the political economy, and the government openly recognizes that manufacturing must enjoy privileged access and disproportionate weight in the determination of Germany's growth strategy. This is the consensus view across the political establishment, including the Green Party, as epitomized by the Green Party's Economy Minister Robert Habeck in the foreword of the 2023 industrial policy strategy: “Germany has a long tradition based on strong manufacturing. I want it to remain that way.” 58 Within the manufacturing sector, a predominant role is played by Germany's two largest industries: the metalworking sector—comprising metal and electrical engineering industries with 25,600 companies and 3.9 million employees 59 —and the chemical and pharmaceutical sectors, with 1,700 companies and around 585,000 employees. 60

The Organizational Capacity of the Various Sectoral Interests

The associational capacity of unions and employers in Germany rests almost entirely on sectoral organizations. The peak organizations of trade unions (DGB) and employers (BDA) have limited influence compared with the sectoral organizations. 61 However, while the industry organizations representing business and workers’ interests within the manufacturing sector are clearly delineated, in public and private services they are internally heterogeneous, highly fragmented, and rather weak.

In the manufacturing sector, the strongest organizations are to be found in the metalworking and engineering industry, and the chemical and pharmaceutical industry. IG Metall and Gesamtmetall represent, respectively, workers and employers in the former; 62 in the latter, Industriegewerkschaft Bergbau Chemie Energie (IG BCE) and the Bundesarbeitgeberverband Chemie (BAVC) are the main organizations representing labor and capital. The organizational density of employers’ organizations has been declining over the past twenty years, but it remains more robust than trade union membership. 63 The metal sector's employers’ organization Gesamtmetall has tried to counteract membership decline by offering membership without collective bargaining participation (“OT membership”). In the chemical sector (which is smaller but more cohesive), the employers’ organization BAVC has developed several joint initiatives with the trade unions to strengthen sectoral social partnership. 64

Overall, while organizations in the metalworking and chemical industries have remained strong and well organized, the organizational capacity of associations in private and public services has become weaker. 65 Private services and the public sector are generally large economic sectors (Figure 2) and could in theory act as political counterweights to the metalworking, engineering, and chemical sectors in determining Germany's growth strategy. These sectors’ disorganization and fragmentation of interests prevents them from becoming embedded in federal policymaking circles, however.

The German public sector, in contrast to the Nordic countries but also France, is relatively small, 66 making the sector less relevant in political economy terms. 67 But most importantly, power is dispersed and public sector interest representation is highly fragmented, both on the public employers and the unions’ side. 68 On the employers’ side, state power in Germany is distributed across three layers of the federal state: the federal level (Bund), the States (Länder) and the municipalities (Gemeinden). As Peter Katzenstein noted long ago, these three tiers are “semi-sovereign” state powers in that they cannot exercise power over each other and are forced to negotiate reciprocally and coordinate on most matters of policy. 69 However, conflicts of interest persist vertically across state tiers and, at the level of the Länder, horizontally between richer and poorer states.

To take the example of public sector wage policy, until the late 1990s, the three public employers for the federal level (led by the Interior Ministry), the Länder level (organized by the Tarifgemeinschaft deutscher Länder [TdL]) and municipalities (by the Vereinigung der kommunalen Arbeitgeberverbände [VkA]), negotiated collectively in a national bargaining coalition (Tarifgemeinschaft) led by the federal Ministry of the Interior. This coalition collapsed in the early 2000s because of the fiscal crisis of the German Länder, which forcefully pushed through public sector wage restraint. The whole system of wage-setting underwent a process of organized decentralization, with the states negotiating independently of the federal and municipal levels. Similar problems of coordination have occurred for the civil servants (Beamte) for whom, since the 2006 constitutional reform, the states now have the legal authority to set wage policies and employment conditions by Land decree.

There is similar fragmentation on the trade unions’ side, where the former major public sector trade union, the Gewerkschaft Öffentliche Dienste und Verkehr (ÖTV), eventually merged with other unions representing private sector services to form a conglomerate union, Ver.di (Vereinigte Dienstleistungsgewerkschaft), resulting in a chaotic landscape, fragmented sector-specific interests and poor capacity for interest representation. 70 Ver.di is the second largest trade union in terms of members but has remained politically the weakest, even though it is based in Berlin and is closely affected by government spending. It has been held back by difficult organizational developments since the very beginning, and two decades after its creation, Ver.di seems never to have developed its own organizational culture. 71 Collective bargaining in the service sector varies enormously across various subsectors, which are extremely fragmented. In particular, the retail sector, restaurants, and hospitality but also the information and communications technology sector not only have low coverage rates, but also a multitude of different industry and employers’ organizations competing over representation of firms. 72 In business-related services, manufacturing trade unions compete with service sector unions over recognition, which further weakens their position.

The Political Embedding of Sectoral Interests

Industrial social partners in both camps are embedded within the political system and linked to the decision-making arena through interpersonal linkages, some of which are bolstered particularly via ad hoc federal commissions and the German system of firm-level codetermination. In what follows, we will focus on the political representation of trade unions for two reasons. First, labor representation generally has a position of structural weakness in the political economy. 73 Second, differences in the German unions’ approaches to political representation contribute to the entrenchment of the producer groups in the manufacturing sector.

The chemical union IG BCE has for a long time been the trade union with the best connections to parliament and the government. 74 Its predecessor, the chemical workers union IG Chemie, was led by Hermann Rappe, a conservative Social Democrat who was also a member of parliament between 1972 and 1998. He was one of the last union leaders who was a member of parliament while remaining a union leader—in the past, this was the key interface between trade unions and the political realm. IG Chemie has over time focused on cultivating a sectoral social partnership rooted in a strong aversion to strike action. 75 All of the current IG BCE board members are members of the Social Democratic Party (SPD), 76 and the IG BCE is highly active on various government platforms. Its chairman, Michael Vassiliadis, is a member of numerous committees ranging from the “Council on Sustainable Development,” the ethics committee “Secure Energy” (2011), the committee on “Growth, Structural Change and Employment” (2018–19), the National Council on Hydrogen, and the “High-Level Expert Group on the Chemical Strategy for Sustainability.” Not least, he was a highly influential member of the committee that regulated the phase-out of coal mining in Germany. 77 Because of its tight representation in political circles, the IG BCE has historically been able to punch above its weight given the relatively small sector it represents.

In contrast, IG Metall's political approach is more volatile. 78 IG Metall has always been a more ideological and left-wing trade union. Activists of the student movement joined IG Metall to stir up political opposition outside parliament during the 1970s. IG Metall has recruited many more left-wing academics to become full-time trade union officials. It also always had a faction leaning on the left of the SPD, even though most chairmen were SPD members. Currently, in mid-2024, only two of the five board members are SPD members, one is a member of Die Linke, and two are not party members. 79 Nevertheless, IG Metall representation vis-à-vis parliament and the government has strategically hired parliamentarians to anchor itself politically—a strategy that is alien to Ver.di. 80 IG Metall has a more distant but also more exclusive relationship with federal politics. The labor market reforms in 2003 (Agenda 2010 and the Hartz reforms) increased the political conflicts within the union, with some trade union officials supporting the expansion of Die Linke to west Germany.

Yet, IG Metall has always assumed that national politics would be open for them because of the importance of the car industry. In fact, then-Chancellor Merkel had several rounds of car industry meetings before and after the financial crisis to back the industry financially but also to discuss their concerns over emissions and illegal practices. For IG Metall, political power followed industrial power in firms and formal representation was not of high importance. However, IG Metall was the leading force for setting up the Alliance for the “Future of Industry.” The Alliance for the “Future of Industry” (Bündnis Zukunft der Industrie) was launched in 2014 by IG Metall's then chairman Detlef Wetzel. 81 Its purpose was to improve conditions facing German manufacturing industries in light of increasing economic and structural problems, such as the financial crisis, demographic decline, and climate change. The alliance focused initially on boosting Industrie 4.0 skills and training policy, but also on the design of tax exemptions for R&D and industry standards. 82 The most recent consultations held by Economy Minister Robert Habeck revolved around a cap on energy prices for energy-intensive firms. 83

Ver.di, in contrast, is a pluralist political union as leading union officials are affiliated with all three parties of the center-left: SPD, Greens, and Die Linke. Former chairman Frank Bsirske is a member of the Green Party and was elected to parliament after stepping down from his chairmanship in 2021. 84 Among the nine board members of Ver.di in 2023, four are members of the SPD, one of the Green Party, and the remaining four are not party members. 85

A major channel of influence through which unions are linked to national politics in Germany is workers’ (and trade union) representation on the supervisory boards of large German firms. To have trade union representation in firms reinforces unions' influence, but it also ties the unions' broader policies to individual corporations’ needs and interests. The position of union leaders in company supervisory boards is important as they provide the unions with useful information about firms’ performance and specific insights into the sector's major needs and challenges. Not least, trade union representatives at the company level—within works councils—use supervisory board meetings as a channel to tighten their position vis-à-vis the union leadership in collective bargaining but also, more generally, when it comes to formulating unions’ political viewpoints.

The policy priorities of the chemical, metalworking, and engineering unions are thus shaped fundamentally by the tight cross-class cooperation between corporations’ managers and union representatives within firms’ supervisory boards. In both IG BCE and IG Metall, the union leadership finds it difficult to override the preferences of the big firms’ works councils. The two leading firms in the chemical industry are BASF and Bayer, while the large car producers dominate the metal sector, together with Siemens and Bosch. Jörg Hofmann, IG Metall chairman until 2023, was a member of the supervisory board of Volkswagen and Bosch and previously of Mahle, Trumpf, and Mercedes. 86 His successor, Christiane Benner, is a member of BMW and Continental's supervisory boards. 87 The vice chairman of IG Metall, Jürgen Kerner, holds six supervisory board seats, including Siemens, MAN, Airbus, and ThyssenKrupp. 88 IG BCE chairman Michael Vassiliadis is a member of the supervisory boards of RAG AG (coal), BASF SE (chemical), Henkel GmbH&Co KG (chemical), and Steag GmbH (coal).

Ver.di is represented in big firms (primarily banks, insurance companies, postal services, Lufthansa and airports), too, but only in the former public sector firms does it have sufficient members to exert industrial pressure. The current chairman of Ver.di, Frank Werneke, does not hold a seat on supervisory boards. He held one at Deutsche Bank in 2021 but did not stand for reelection in 2023. 89 The representation of Ver.di at Deutsche Bank is weak and rests on the union's membership in Postbank, which is owned by Deutsche Bank. The nine-member board of Ver.di holds seats in Post AG, Lufthansa, AXA, E.ON, Sana Kliniken, Metro AG, RWE and Connex, 90 while board members of IG Metall and IG BCE have each between two and six seats on supervisory boards. This is indicative of the weak union presence in large firms in the service and logistics sectors.

There is a strong contrast in Germany between the depth and the breadth of export sector actors’ involvement in various national policy networks and that of actors from the public and private services. Moreover, representatives from the export sector enjoy much closer political connections and greater economic power by virtue of their representation in Germany's corporate giants. Manufacturing trade unions have various political connections, hire civil servants with political experience, enjoy closer ties to large firms through supervisory board representation, and serve on government committees to a far greater extent than service sector unions. Furthermore, while organized interests in the manufacturing sector organize relatively coherent policy priorities in the political realm and exploit the strategic positioning of key officials in federal policy networks, organizations in the public and service sectors are far less strategic and poorly cohesive internally. As the recent case of economic adjustment to the energy crisis reveals, these organizational and structural differences between the export sector and the rest of the economy mean that the export sector's systemic involvement in key national policy networks actively contributes to define German economic policymaking.

Germany's Adjustment Strategy to the 2022–23 Energy Crisis

Merely months into its tenure, the “traffic light” coalition government in Germany was confronted by severe economic challenges posed by Russia's invasion of Ukraine and the subsequent sharp rise in energy prices. To formulate the core pillars of a comprehensive adjustment strategy to shield the export sector, the government engaged cross-class representatives of the chemical, metalworking, and engineering sectors, convening several high-profile concertation meetings at the Chancellery. This export-oriented growth coalition pursued an adjustment strategy aimed at ensuring export sector firms’ capacity to contain the rise in input costs and maintain international cost competitiveness. The concerted adjustment strategy revolved around three strategic pillars: subsidizing increases in energy bills to contain firms’ energy input costs; promoting wage restraint in sectoral collective agreements to contain labor costs; and securing extensive state aid for domestic firms under the European Commission's Temporary Crisis Frameworks.

The High-Level Meetings of the “Concerted Action Group” and the “Gas Price Commission”

In July 2022, Social Democratic Chancellor Scholz summoned a so-called “concerted action group” due to meet in the federal government's Chancellery in Berlin to devise Germany's adjustment strategy to the energy crisis. Chaired by the chancellor, the network included prominent figures such as Economy Minister Robert Habeck (Greens), Finance Minister Christian Lindner (Liberal Democrats [FDP]), the Bundesbank president, a member from the Economic Experts Council, Rainer Dulger, president of the Confederation of German Employers’ organizations (BDA), and Yasmin Fahimi, president of the German Trade Union Confederation (DGB). The high-level group's second meeting took place in September 2022. In consultation with the participants of the concerted action group, the government also agreed to establish an “Expert Commission on Gas and Heat” (later dubbed the “gas price commission”), tasked with assessing the possibility of introducing energy price brakes. The Commission was chaired by economist Veronika Grimm; Michael Vassiliadis, chairman of the chemical sector union IG BCE; and Siegfried Russwurm, president of the Federation of German Industries (Bundesverband der Deutschen Industrie [BDI]).

The concerted action group's explicit aim was to “work together to overcome historical challenges, mitigate the effects of lost income and avert the risk of an inflation spiral.” 91 By involving the social partners in federal-level social concertation, the chancellor reportedly insisted that “the only way we as a country can overcome this crisis is if we join forces and agree on solutions together.” However, "together" here refers to an adjustment strategy devised primarily through the involvement of cross-class representatives from the country's core industrial sectors. These sectors were represented by relatively homogenous, powerful organizations and policy actors deeply embedded within federal decision-making circles. This can be shown by the composition of the concertation groups.

First, the concerted action group was spearheaded by representatives who emanated from the metalworking, engineering, and chemical sectors, and who were the clear drivers behind the determination of Germany's adjustment strategy. Rainer Dulger, president of the Confederation of German Employers’ Associations (BDA), holds a PhD in engineering and led the metalworking employers’ organization Gesamtmetall before rising to the BDA's leadership. DGB president Yasmin Fahimi is a chemist who served as the trade union secretary at IG BCE from 2000 to 2013 and sits on the supervisory board of the biotech, pharma, and chemical giant Bayer.

Second, the Expert Commission on Gas and Heat was composed of twenty-one members, including six economists, seven representatives of energy firms or businesses, and various other civil society organizations, such as the Tenants’ Association, welfare organizations, and environmental groups. However, the commission was chaired by economist Veronika Grimm, trade union leader Michael Vassiliadis, and industry representative Sigfried Russwurm. Michael Vassiliadis has been chairman of the chemical sector union IG BCE since 2009 and holds positions on the supervisory boards of some of Germany's largest corporations, such as chemical sector giants BASF and Henkel. As it happens, Vassiliadis is also the spouse of DGB president Yasmin Fahimi, herself a former IG BCE trade union official. Chairperson Sigfried Russwurm—an honorary professor in mechatronics—serves as president of the BDI and chairs the supervisory boards of some of Germany's leading metalworking companies, such as ThyssenKrupp and various Siemens subsidiaries. Thus, the composition of the Expert Commission on Gas and Heat further reflects the dominance and influence of representatives from the chemical, metalworking, and engineering industries in shaping Germany's policy responses to the energy crisis.

Views were divided within the Expert Commission on Gas and Heat over the merits of a cap for gas prices. Most of the economists in the commission favored not imposing a price cap and leaving it to the government to compensate consumers up to a fixed amount. 92 Such a solution would have protected lower incomes most, but would have penalized large industrial companies, who are large energy consumers. The co-chairs Michael Vassiliadis and Sigfried Russwurm orchestrated overnight meetings, pushing the various members of the commission to compromise in favor of the regulation of gas prices, which would have particularly benefited large gas consumers. The solution was eventually voted on in the commission to resolve the disagreements between economists, consumers and industry. 93 As one member of the commission pointed out, it was the powerful Michael Vassiliadis who kept the members on course. 94 The government was not represented in the commission, 95 which was ultimately responsible for a bail-out package of up to €200 billion and even for setting gas prices for industry at a lower rate than the gas prices paid by consumers.

In all, what is perhaps most indicative of the power imbalances between the industrial and service sectors’ representatives within federal concertation meetings is that Frank Werneke—leader of Ver.di and a commission member—was marginalized and had to formally issue a dissenting vote in the commission's interim report criticizing the agreement as socially unbalanced and particularly unfair toward poorer households. 96

Subsidizing Firms’ Energy Bills to Reduce Energy Input Costs

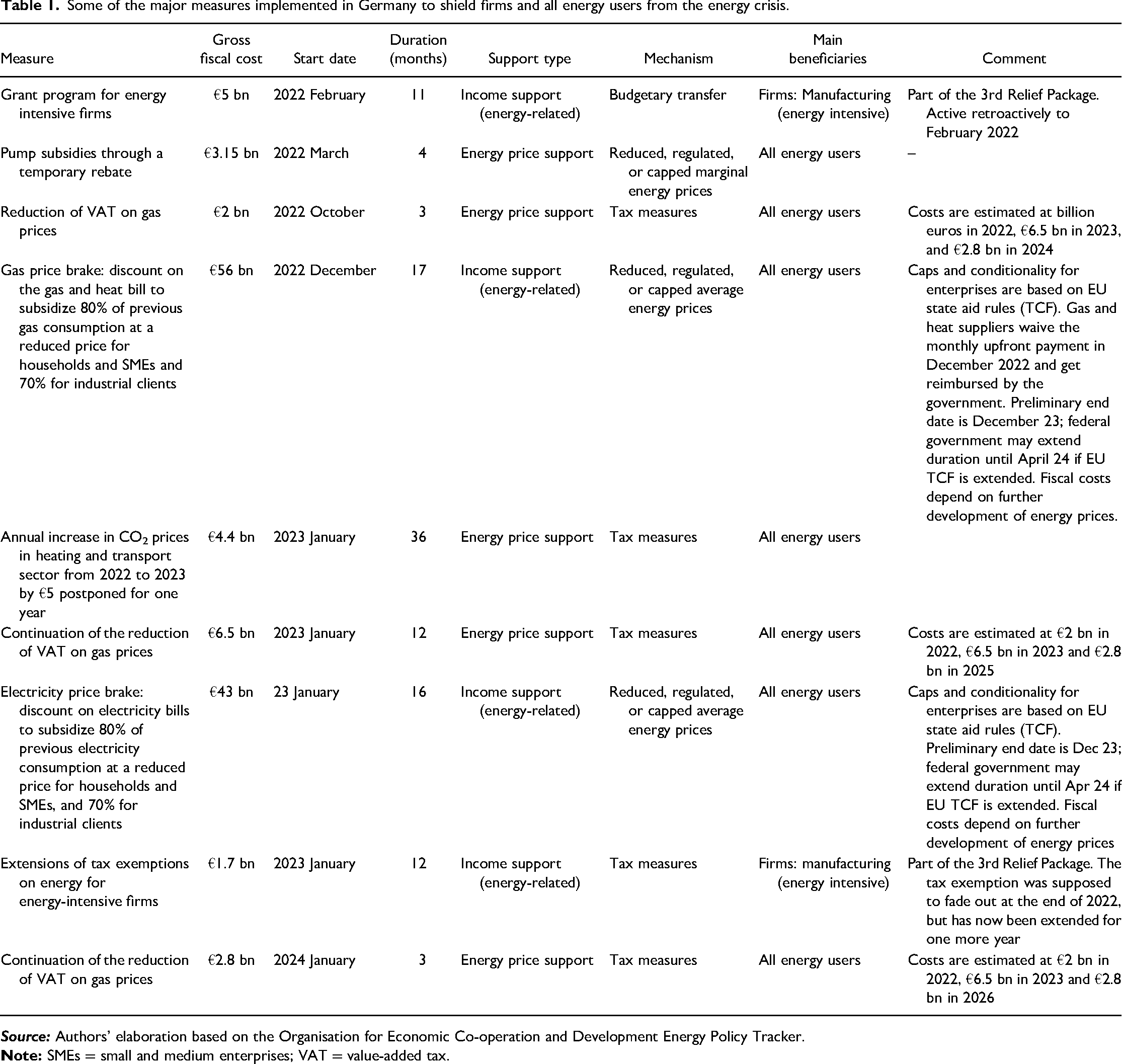

To support German firms, the government enacted various types of policies (see Table 1 for an overview), ranging from budgetary transfers to tax reductions on energy prices, and—belatedly if compared to France and Spain—brakes on electricity and gas prices. The government intervened by directly enacting measures targeted at smaller and medium-sized large industrial firms, or through broader measures benefiting all energy users and thus, indirectly, German firms.

Some of the major measures implemented in Germany to shield firms and all energy users from the energy crisis.

The most controversial measure was a subsidy for electricity prices faced by energy intensive companies. While both gas and electricity prices returned to prewar levels before Russia's invasion of Ukraine, electricity prices had increased substantially even before the energy crisis. 97 Therefore, the energy intensive industries continued to lobby for—and obtained—electricity subsidies but only for the manufacturing sector. The trade unions were once again key lobbyists on behalf of the export sector growth coalition. IG Metall organized walkouts and action days in November 2023, asking for policies to protect steel production, aluminum, and foundries. 98 While Economy Minister Robert Habeck supported these demands, the liberal Minister of Finance Christian Lindner argued against the subsidy. Eventually, the government agreed in November 2023 to further lower the electricity tax for all manufacturing companies to the lowest acceptable level in the European Union.

This amounted to a substantial subsidy to the manufacturing sector of €3 billion, 99 leaving unprotected other electricity consumers who had also suffered from high prices. 100 For instance, hospitals were strongly affected by higher energy and wage costs. A survey among German hospitals in December 2023 concluded that three-quarters of all hospitals had a negative balance for 2023 and that they expected a record number of insolvencies for 2024 because of higher energy and staff costs. 101

However, not all estimated subsidies were actually paid out. Because gas and electricity prices recovered relatively quickly in 2023, the final bill for the federal budget was substantially lower. For 2023, the federal budget spent €14.3 billion for gas and €16.2 billion for electricity subsidies, only a fraction of what it was willing to spend and had budgeted. Nevertheless, the budget positions emphatically show the government's political will to grant substantial energy subsidies. 102

Subsidizing Firm-Level Inflation Premia

Wage restraint is crucial for the resilience of the German export-led growth model. In the domain of private sector wage setting, however, the government cannot intervene directly in collective bargaining as the social partners have exclusive right to collective bargaining autonomy (Tarifautonomie). Thus, the government intervened indirectly to help firms contain the increase in labor costs and, most fundamentally, to prevent a prospective price-wage spiral. It did so in two ways: first, by enhancing the capacity of sectoral wage-setters to accept a policy of wage moderation by compensating households across the economy through untargeted measures, restoring their losses of real income (see Table 1 for an overview); second, by incentivizing the sectoral social partners to make use of untaxed inflation bonuses paid by firms una tantum.

Again, the chemical sector, with its culture of compromise and bargaining, played a pivotal role. It did so by acting as pattern setter in collective bargaining developments after the Russian invasion of Ukraine. Amid the uncertain economic circumstances in 2022, the chemical sector union IG BCE had opted not to demand a specific wage increase. By April, IG BCE and the employers decided instead to extend the previous agreement to October 2022 and approve a one-time €1,400 payment for workers in May. This amount could be lowered to €1,000 if a company faced economic challenges.

Chancellor Scholz praised this approach as a solution against rising prices, promoting the broader use of one-off payments in the “concerted action against price pressure.” 103 In fact, one-off compensatory payments at the firm level promised to be a flexible adjustment tool, allowing the social partners and the government to find a compromise solution between two contrasting policy objectives: the need to sustain workers’ purchasing power, while escaping a wage-price inflationary spiral that risked damaging the country's cost competitiveness and further reducing workers’ real incomes in the medium term. This is because one-off payments consist of a fixed-sum bonus paid once by firms to employees. This is different and cheaper from the employers’ perspective from full-fledged wage increases enshrined in sectoral collective agreements, which permanently increase all income levels covered by the agreement by a given percentage. The measure was therefore an investment in future wage moderation.

Drawing on the example of the chemical sector's agreement, to sustain the actions of wage setters in other sectors the federal government decided to use its fiscal capacity to fund the exemption from taxes and social security contributions of one-off firm-level inflation bonuses for employees (up to €3,000). It would then be up to the sectoral social partners to agree on the level of the bonus, but it would be distributed only once by firms and would not alter the structure of pay levels within the given sectoral agreements. The measure was planned in consultation with the social partners.

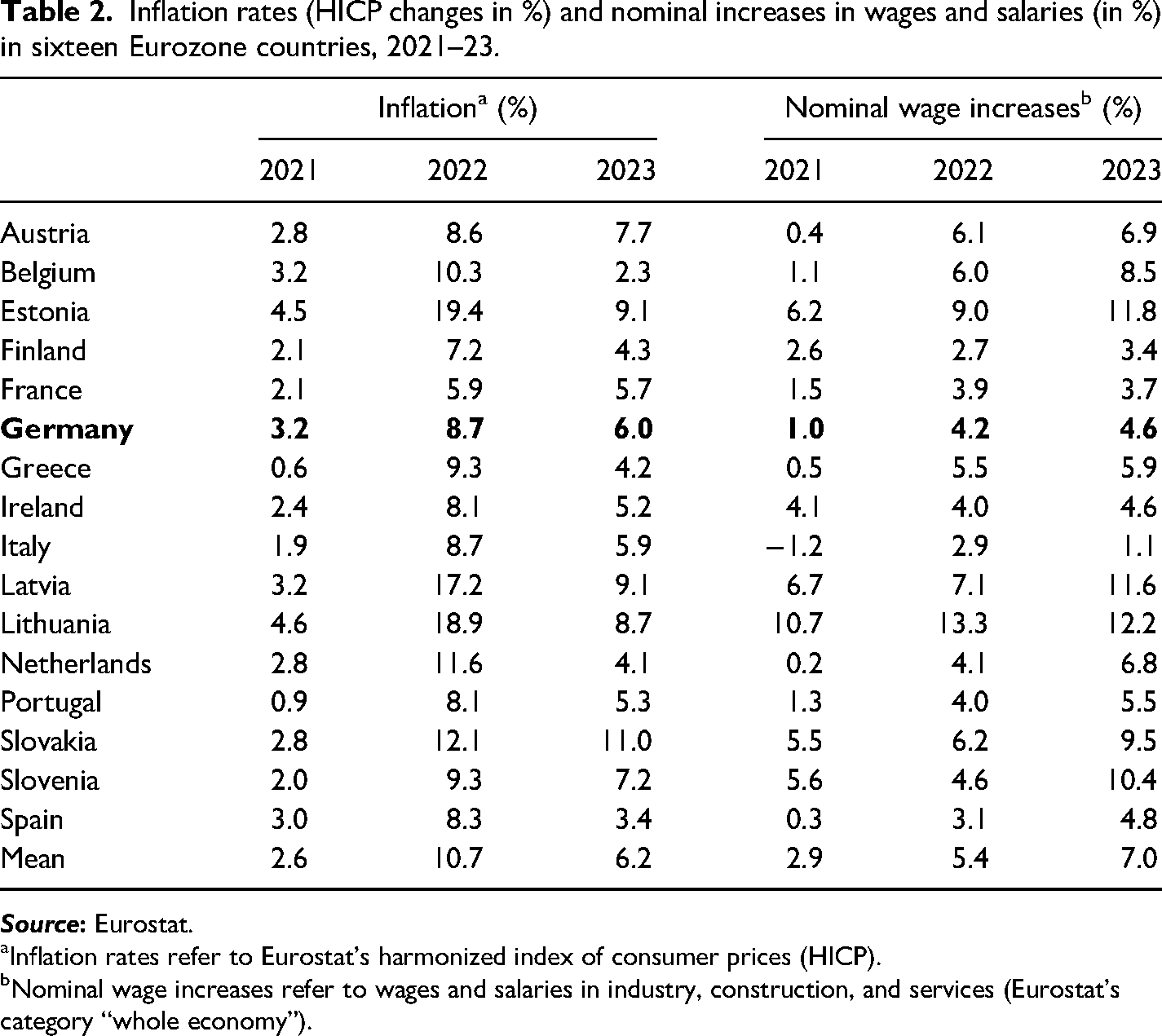

As a result, the use of untaxed one-off compensatory inflation bonuses at the firm level was soon incorporated into the subsequent sectoral agreements. Together with the social policy measures for households, firm-level one-off bonuses thus compensated workers for their lost purchasing power, easing the pressure from below on union leaders. Wage setters could reach moderate settlements in sectoral collective bargaining, which resulted in low nominal wage increases and high real wage losses (Table 2). This helped to stabilize wage-push inflation.

Inflation rates (HICP changes in %) and nominal increases in wages and salaries (in %) in sixteen Eurozone countries, 2021–23.

Inflation rates refer to Eurostat's harmonized index of consumer prices (HICP).

Nominal wage increases refer to wages and salaries in industry, construction, and services (Eurostat's category “whole economy”).

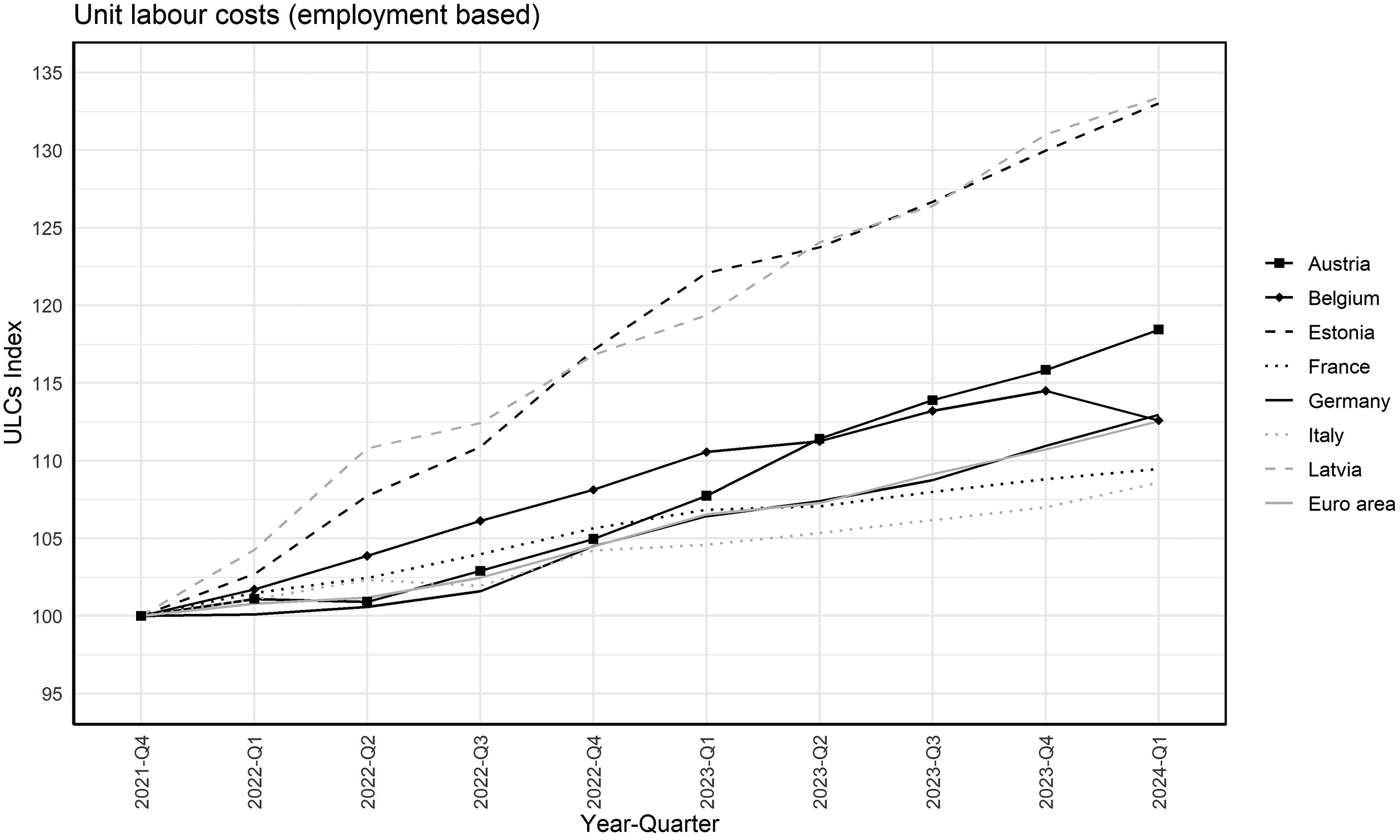

Overall, in the years of the inflation shock, Germany was able to contain the growth of unit labor costs in line with Eurozone levels, and well below the level of the Baltic countries which have been hit severely by the energy shock because of their exposure to Russia (Figure 4). Thus, Germany has kept its advantageous cost competitiveness, and its real effective exchange rate has remained roughly constant (see Figure 2, panel B). 104 This is remarkable because one might have expected above-average wage and prices increases from a country highly vulnerable to the energy shock and with almost full employment.

Quarterly unit labor costs (ULCs; employment based) in Germany and selected European countries, 2021–Q4 = 100.

The distributional struggle to prevent real wage losses for workers was fought mainly by groups in the service sector. Here, unions fought hard to protect incomes, particularly for the low-wage workers. 105 The wages of workers in low-productivity service sectors such as hospitality were more protected than those in high-productivity sectors. Studies indicate that Germany's low-paid service sector workers enjoyed real wage gains during 2019–22, 106 and that the protection of purchasing power in the low-wage sectors was more pronounced in Germany than the euro-zone average. 107

State Aid to Ailing Firms

Finally, the German government has made extensive use of new largesse for state aid measures to support the economy following the energy crisis. Already after Covid-19, the European Commission had loosened state aid prohibitions, enabling member states to assist companies and sectors severely harmed by serious exogeneous economic shocks. In the wake of the Ukraine war and its repercussions on energy markets, the European Commission has granted new regulatory flexibility via the Temporary Crisis Framework (TCF), adopted in March 2022, and subsequently under the Temporary Crisis and Transition Framework (TCTF) adopted in March 2023.

State aid in Germany had increased sharply with the onset of the Covid-19 pandemic in 2020. In March 2020, the government set up a fund with credit lines of up to €600 billion for stabilizing the economy (Wirtschaftstabilisierungsfond [WSF]) and subsidizing ailing firms. The fund was outside the federal budget and based on an emergency rule excepting it from the constitutional “debt-brake.” After Russia's invasion of Ukraine in February 2022, the WSF was expanded and converted to fund gas and electricity subsidies, the recapitalization of Uniper, and ongoing subsidies for ailing sectors. 108

In addition to the WSF, the government renamed and expanded another fund for decarbonizing the German economy (Klimatransformationsfond [KTF]) in July 2022. 109 The KTF uses revenues from carbon taxes and issues subsidies to improve the insulation of buildings, the decarbonization of industry, the development of hydrogen industries, electromobility infrastructure, and renewable energy.

According to the federal budget, both funds spent roughly €64 billion in 2023. 110 Laaser and Rosenschon estimated that all financial help from the federal government (including subsidies for consumers and households) rose from €85 to €154 billion between 2022 and 2023. 111 However, in November 2023, the Constitutional Court put an end to the possibility of establishing credit lines over several years and made the fund's use conditional on the declaration of a state of emergency for each budget year. 112 The credit lines for the WSF can therefore be activated only upon declaring a state of emergency and the funds may be used solely within the budgetary year during the state of emergency. For 2024, the government did not declare an emergency and had to reduce its access to the WSF accordingly.

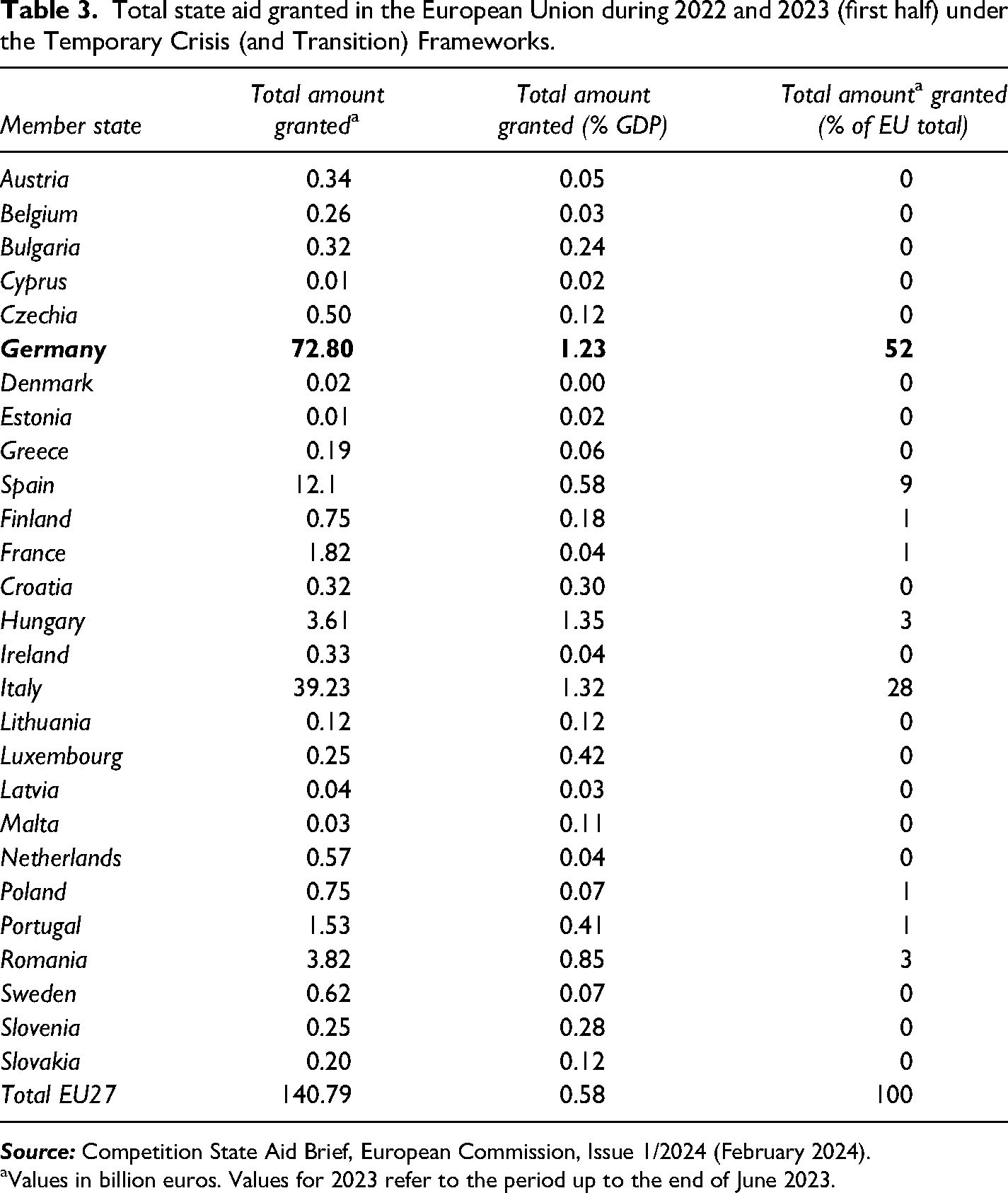

Looking specifically at state aid provided only to domestic firms—that is, excluding households and consumers—the most up-to-date data available on state aid granted across the European Union builds on surveys by the European Commission's DG Competition conducted with member states’ competition authorities. 113 Here, a distinction needs to be made between state aid approved de jure by the commission and state aid granted de facto by member states. The former consists of state aid notified by member states and approved by the commission, which provides a good proxy for national governments’ ex ante political willingness and readiness to spend on national subsidies. By contrast, granted state aid, however imperfect, provides ex post a proxy for companies’ economic needs and effective state aid absorption.

Over the period March 2022 to end of June 2023, state aid notified by member states and approved by the commission totaled €730 billion, of which only €141 billion were actually granted to firms. Germany accounted for 48.8 percent of approved aid (€356 billion), of which the German government spent “only” €73 billion. The large discrepancy between approved aid notified by Germany and the amounts of aid granted to German firms indicates the extent to which the German government was ready to employ federal fiscal resources to subsidize ailing domestic firms.

In absolute values, Germany was by far the largest provider of state aid during 2022 and the first half of 2023, accounting for 52 percent of the total amount of state aid granted across the European single market (Table 3). This amounted to 1.23 percent of GDP, surpassed only by Hungary (1.35 percent) and Italy (1.32 percent).

Total state aid granted in the European Union during 2022 and 2023 (first half) under the Temporary Crisis (and Transition) Frameworks.

Values in billion euros. Values for 2023 refer to the period up to the end of June 2023.

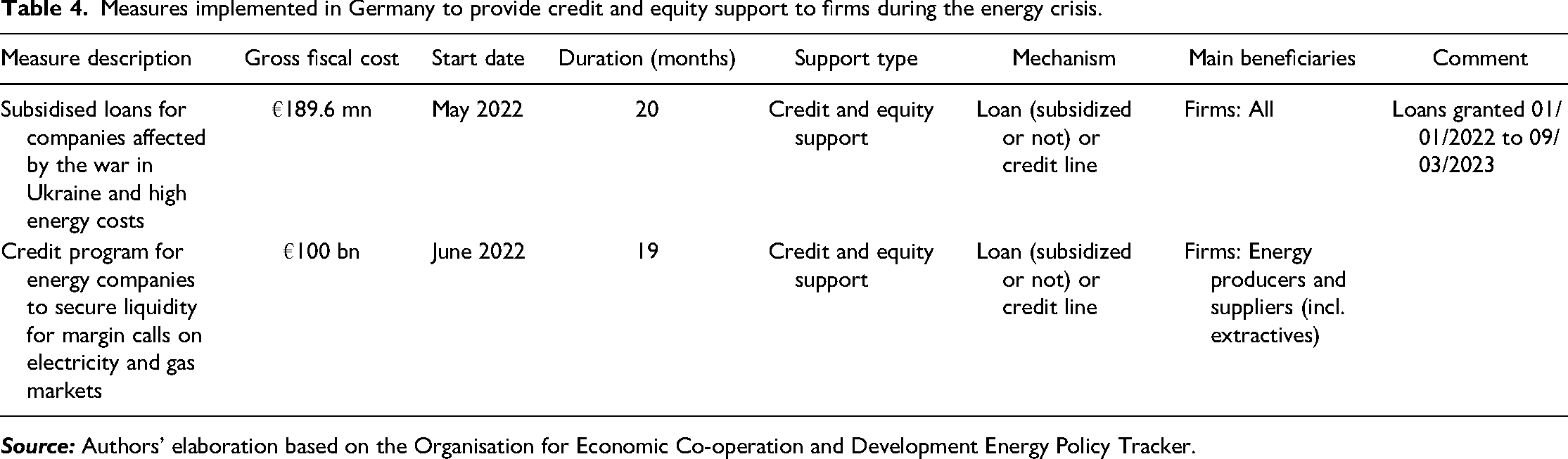

Among specific measures, most of the aid was employed to avoid the collapse of two German utility companies, Uniper SE and SEFE GmbH, which were heavily exposed to trade with Russia. Uniper SE received a recapitalization of €33 billion and loans worth €16 billion under a German umbrella scheme for guarantees and subsidized loans. Similarly, SEFE GmbH was recapitalized with €6.5 billion and obtained subsidized loans of €13.8 billion under the same scheme. 114 These measures were necessary to avoid the collapse of the country's major energy players, with further negative externalities for the rest of the country's manufacturing firms. Other interventions to provide credit and equity support included the provision of subsidized loans for companies affected by the war in Ukraine and high energy costs, as well as a credit program for energy companies to secure liquidity for margin calls on electricity and gas markets (Table 4).

Measures implemented in Germany to provide credit and equity support to firms during the energy crisis.

Concluding Discussion

This article has analyzed the political foundations of growth models. Germany exemplifies a paradigmatic case with its systematic pursuit of an export-oriented growth strategy, despite increasingly adverse circumstances. Signs of the vulnerability and exhaustion of the German model had already materialized in the years before the crisis. In principle, economic elites could have capitalized on the energy crisis to rebalance Germany's growth model and reduce the model's many vulnerabilities, that is, to pay greater attention toward domestic demand as opposed to export competitiveness. But such a third-order change, in the terminology of Peter A. Hall, did not occur. 115 The government remained within the preexisting economic paradigm and mobilized vast resources to protect its export-led growth model, fully in line with the interests of Germany's export sector growth coalition.

The growth coalition that has shaped the government's adjustment strategy displays remarkable characteristics. First, it builds on the cross-class alliance between unions and employers’ associations in the exporting, manufacturing sector. The sectoral nature of Germany's interest intermediation constitutes the crucial precondition for the formulation of particularistic economic preferences. Second, the relevant sectors during the energy crisis were the energy-intensive industries in the chemical, metalworking, and engineering sectors, represented by the two trade unions IG BCE and IG Metall, and the key employers’ associations. These sectors have been the key engines of growth for the German economy. Third, these actors have enjoyed privileged access to the decision-making arena, which materialized specifically in the “concerted action group” and in the Gas Price Commission, where manufacturing interests were clearly dominant.

As the dominant producer group of the German growth model, the manufacturing sector has great structural power. However, it also has specific instrumental power, in other words, the capacity to penetrate federal decision-making circles and have its economic preferences translated into public policy. As we have shown in detail, this holds particularly true for the chemical and metalworking sectors, in which the social partners have cultivated strategic networks with links to key political actors. The participants in these networks meet in political advisory committees, supervisory boards, and political parties. This contrasts with the fragmented representation of the domestic service sectors. In this way, a chemical-industrial power center has emerged in the “concerted action group” and the Gas Price Commission, and with it a hegemonic view of “what the economy needs” in order to grow. The needs of the manufacturing export sector are, in the logic of that view, synonymous with the imperatives of good economic policy for the whole country.

Our findings are consistent with the core insights of growth models research, which emphasizes the role of sectors as core protagonists behind government formulation of economic policies. The interesting observation is that in Germany, over time, the semicorporatist system of interest representation has changed its functional scope. Traditionally, tripartite peak-level concertation between social partners and governments is seen as the expression of comprehensive considerations of different social interests with an eye to balancing different preferences in the conduct of public policy toward the general interest. During the crisis adjustment in 2022–23, however, the sectoral corporatist decision-making mode followed quite a particularistic logic.

Instead of incorporating different sectoral interests and balancing them in peak-level negotiations, the policy response was heavily biased toward the manufacturing sector. Economic sectors have conflicting needs, which can cause political conflict along sectoral lines. Such cleavages become more apparent in exceptional moments of crisis, making the German case particularly interesting. Accordingly, one would have expected the peak-level government commissions to consider the expectations of all sectors. However, we find that dominant sectoral interests pursue their preferences independently of other groups such as domestic service sectors and consumers. As Mancur Olson suspected, corporatist decision-making arenas can protect particularistic interests when they are populated by powerful sectoral vested interests. In Germany, this was possible without formal changes in the prevalent mode of governing the political economy.

It would be mistaken to interpret these outcomes as a functionalist logic inherent in the German growth model. The fact that the export sector growth coalition was able to prevail in the choice of adjustment strategies does not mean that the export-led growth model is sustainable. As we have discussed in detail, this would require the continuation of external conditions outside the control of the growth coalition, above all cheap energy sources, sustained foreign demand for German exports, and a stable liberal trade regime. As things stand at present, there is little to suggest that German exports will suffice as the country’s main growth engine in the future. Concentrating on export growth as a means of overcoming stagnation may therefore prove costly for taxpayers and the neglected domestic sectors.

The German adjustment strategy disappoints those European observers who were hoping that Germany would relax its export-oriented strategy and stimulate domestic demand. Additionally, Germany's high industrial subsidies to shield its export sector carry both domestic and European implications. High subsidies for German industry against the backdrop of restrictive fiscal policies further risk crowding out much-needed public investment, on which industry, as much as other sectors, ultimately depends. At the European level, Germany's lax use of subsidies poses a threat to the integrity of the European single market.

A rebalancing of the German growth strategy is not impossible, but it is politically very difficult. During the energy crisis, the government de facto outsourced its decisions to the export sector growth coalition and was unable to develop an alternative medium- to long-term growth strategy, which would have run up against the resistance of the strong cross-class industrial coalition. None of the political parties called for such paradigm shift to rebalance Germany's export-led growth model. 116

The SPD, in opposition for only four out of the twenty-six years since the introduction of the euro, is the core political representative of the German exporting manufacturing industry, even more than the center-right Christian Democrats. This is because German social democracy has its roots in the labor movement, and the close connection to the manufacturing sector has remained strong over time. 117 The Greens started out as a postindustrial party but has since undergone a fundamental ideological change and now prefers green industry rather than a postindustrial economy. The green economy minister, Robert Habeck, has made the Greens vulnerable to the accusation of having promoted Germany's deindustrialization because of their push toward renewable energy. Against this backdrop, Habeck even became the biggest supporter of the large electricity price subsidy discussed in 2023, alongside the industrial sector's employers and trade unions. The populist fringes of the German party system do not criticize the German growth model, but rather accuse the government of not doing enough to protect German industry. It is the liberal party (FDP) that holds the most skeptical position within the German growth coalition. The FDP's fiscal conservatism has an inflation-reducing effect and therefore benefits a real effective exchange rate (REER) favorable to the export sector. The same conservatism, however, also comes with skepticism toward industrial subsidies, which would probably have been even higher had the FDP not been in government. This is because the FDP's core constituency consists of professionals in the service economy who do not benefit from manufacturing subsidies.

In short, a correction of the German growth strategy cannot be ruled out in theory, but it would require a fundamental rethinking of the country's growth strategy by the political parties. Currently, such a fundamental rethinking does not appear to be in sight.

Footnotes

Acknowledgments

We are grateful to Janis Jurgeleit for his excellent research assistance and to the authors of the Kieler Subventionsbericht 2023, Astrid Rosenschon und Claus-Friedrich Laaser, for their help with finding Germany's state aid data. Previous versions of this article were presented at the Council for European Studies in Reykjavík in 2023 and in Lyon in 2024. We are grateful to all the panel participants for their helpful comments and suggestions, especially Alison Johnston and Deborah Mabbett, who discussed our drafts. We are also grateful to Lucio Baccaro and Niccolo Durazzi for their helpful suggestions on a previous draft presented at the SISEC 2023 conference in Cagliari.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.