Abstract

This article makes a key contribution to the comparative political economy literature by accounting for the macroeconomic role of household finance. Based on post-Keynesian theories of finance and the financialization literature, we place house prices and mortgage credit squarely at the center of the macroeconomy, as speculative house price cycles can facilitate homeowner consumption via the use of equity release mortgages. Through an econometric evaluation of eighteen advanced economies from 1980 to 2019, we demonstrate that household debt is determined by house price inflation, and that rising household debt contributes to GDP growth, while business debt has negative growth effects. These results are consistent across countries with different growth models and financial systems. This suggests that the varieties of capitalism's focus on corporate finance is misplaced and that the growth models approach needs a theory of house prices, mortgage credit, and financial cycles to adequately conceptualize how debt-driven growth operates across advanced economies.

In this article, we challenge the prevailing comparative political economy (CPE) accounts of how the financial sector contributes to macroeconomic growth in advanced economies, namely, the varieties of capitalism (VoC) approach and Baccaro and Pontusson's recent application of the growth model perspective to CPE. 1 The VoC framework made a major contribution by linking differences in finance and investment across market typologies to forms of comparative institutional advantage, which stimulates macroeconomic growth via national gains in competitiveness. 2 The VoC argue firms access investment capital either through corporate debt markets in liberal market economies (LMEs) or via more traditional relationship-based banking in coordinated market economies (CMEs). Therefore, the VoC approach emphasizes the importance of corporate debt to support economic growth in varieties of advanced economies. In contrast, Baccaro and Pontusson's application of the growth model perspective to CPE argues advanced economies are organized around specific demand-side growth regimes driven by consumption, exports, or a combination of the two. As such, Baccaro and Pontusson consider household debt a key mechanism to support growth in what they describe as consumption-led economies characterized by stagnating wages and rising inequality. 3

We contest that these CPE accounts do not sufficiently conceptualize the macroeconomic role of the financial sector in advanced economies. Although business and consumer credit are important channels of modern financial systems, mortgage provision has been one of the principal drivers of growth in the financial sector, and most household debt takes the form of mortgage debt. 4 This is in part due to the substantial returns on retail mortgage products that have seen bank lending largely reoriented away from productive investment toward lending to households in the form of mortgage credit. 5 Furthermore, as spectacularly demonstrated by the 2008 global financial crisis (GFC), house prices and household debt have been associated with cycles of boom and bust in various countries, which have significant macroeconomic effects especially in terms of financial instability. 6 However, the VoC's focus on the firm makes the framework incapable of accounting for the household as an actor and the significant macroeconomic effects of house prices and household debt. 7 While Baccaro and Pontusson do acknowledge the links between house prices and household debt, they consider this as an aside and essentially treat household debt as consumer credit. As such, they fail to provide a systematic account of how house prices and household debt interact to contribute to macroeconomic growth from a CPE perspective, which is where this article makes its contribution.

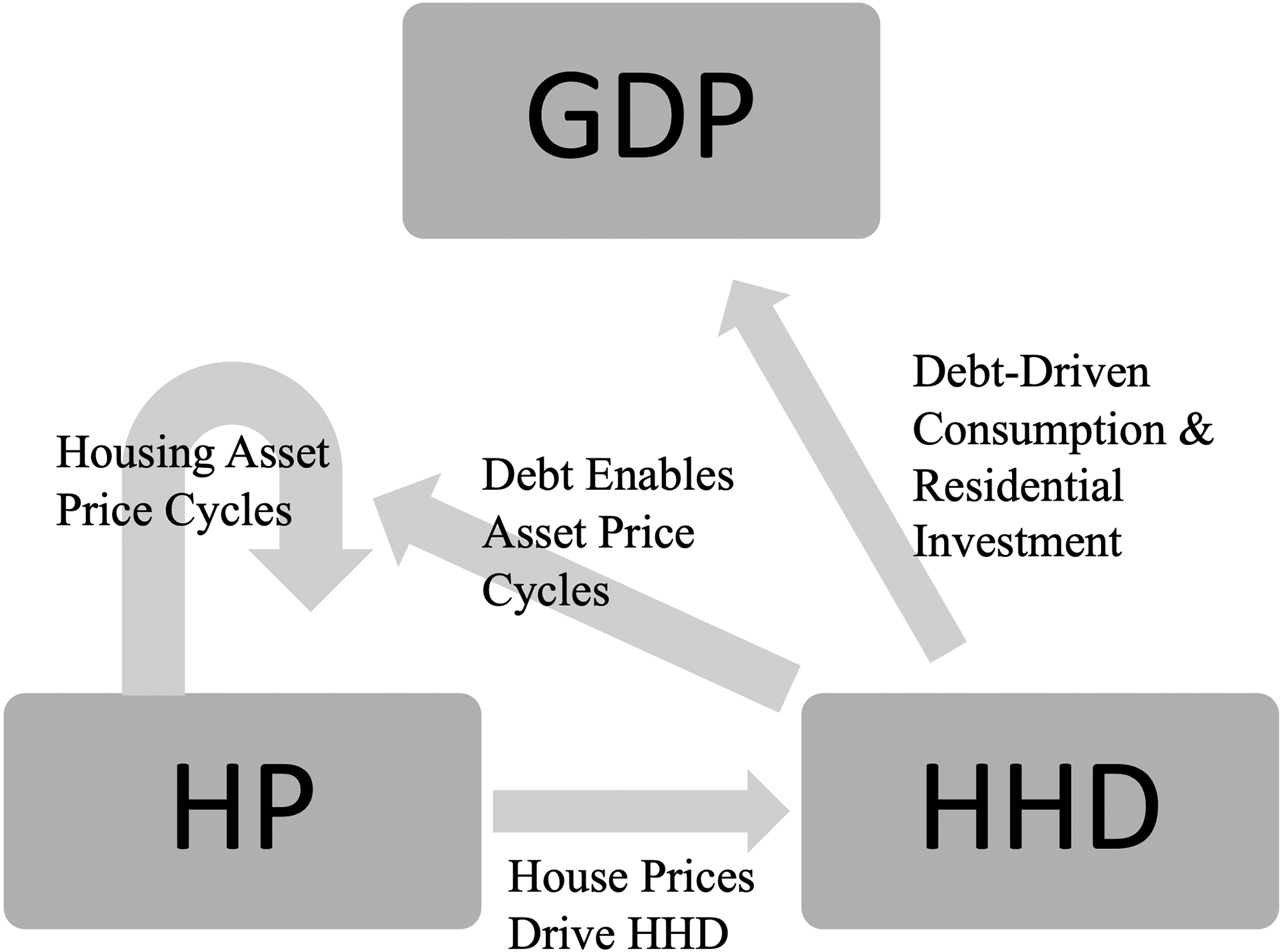

Based on post-Keynesian theories of finance and the financializaton literature, we propose placing house prices and mortgage credit squarely at the center of the macroeconomy. Specifically, we contend that four key mechanisms (visually summarized in Figure 1) explain the significant macroeconomic dynamics of house prices and household debt. First, house prices are a key financial variable for the macroeconomy that may construct, and be determined by, speculative asset price cycles. 8 Second, as real estate is often considered a secure form of collateral for financial institutions, house price increases will often induce bank lending to private households, driving mortgage debt growth. 9 Third, increases in mortgage debt, in conjunction with expectations of future house price increases, can reinforce house price inflation by facilitating increased demand for private housing. 10 Fourth, homeowners can realize the financial gains of rising house prices by taking out equity release mortgages to finance the consumption of goods and services, thus increasing economic (GDP) growth. 11 Rising house prices can also contribute to GDP growth via the residential investment channel by inducing the construction and sale of new homes.

Theoretical overview of the macroeconomic effects of house prices and household debt.

Our approach differs from the prevailing CPE accounts of the macroeconomic role of the financial sector. We deviate from the VoC's focus on corporate investment by placing an emphasis on the speculative demand for homeownership, facilitated by liberalized access to mortgage credit, as a fundamental activity of finance in contemporary economies. Our approach also addresses a significant gap in the growth models approach by analyzing house price and mortgage debt dynamics. Furthermore, we differ from the existing housing CPE literature by specifically examining the macroeconomic impact of housing and mortgage finance systems. 12 Finally, our approach deviates from mainstream economic theory as it allows for financial instability and boom-bust cycles.

Empirically, this article examines whether, and to what extent, household debt and house prices have macroeconomic growth effects in advanced economies. To formally evaluate this research question, we econometrically examine the interactions between GDP, household debt, and house prices using three distinct equations. The sample of our study covers eighteen advanced economies with highly developed financial sectors from 1980 to 2019. We also break down the analysis into subsample country groupings based on key typology sets in the CPE literature. From a comparative perspective, the rationale for these case selections is that any potential common outcomes in such different typologies could allow for the identification of possible key general mechanisms of advanced financialized capitalism. 13

Our results demonstrate that house prices are a major determinant of household debt, and household debt contributes to economic growth across the whole sample. We support this finding by demonstrating similar effects across both debt-driven and export-driven economies, as well as countries with bank-based and market-based financial systems. These results have three key implications for CPE. First, they suggest Baccaro and Pontusson's application of the growth model perspective to CPE could develop its conception of the macroeconomics of CPE further by placing household financial decisions more prominently in the analysis. 14 More specifically, we demonstrate the importance of moving beyond unsecured consumer lending to focus on the economic effects of house prices and mortgage debt, which is the most prominent way households engage with domestic and international financial sectors. Second, the generalizability of the macroeconomic effects of house prices and household debt suggests the growth models approach to CPE must move beyond the dichotomy of debt-driven versus export-driven economies. Third, our results challenge the macroeconomic underpinnings of the VoC, as the framework's focus on the firm makes it incapable of accounting for how house prices and household debt contribute to economic growth. Our results also show business debt has negative effects on economic growth, due to its drags on corporate investment, suggesting the VoC's emphasis on the financial sector's provision of investment credit to firms is misplaced. Third, the generalizability of the macroeconomic effects of house prices and household debt across countries associated with different CPE typologies challenges strict distinctions between countries. Overall, based on the results of our analysis, we consider household actors’ engagement with mortgage debt and housing to be the missing macroeconomic underpinnings of CPE.

The remainder of the article is structured as follows. The first section examines the missing macroeconomic role of housing and private debt from a CPE perspective. The second section outlines the empirical design of the econometric models deployed in the analysis, while the third section describes the results of the models. The fourth section situates the results in relation to the wider literature and is followed by a conclusion.

The Missing Macroeconomic Role of House Prices and Household Debt in CPE

The rise to prominence of the financial sector is one of the most significant structural transformations in the global economy since the 1970s. 15 The CPE literature has developed a clear account of how different financial sectors contribute to economic growth in advanced economies. Based on the typologies of financial systems identified by Zysman, 16 the influential VoC framework argues firms in LMEs access productive investment via capital markets, either by taking on corporate debt or selling equity shares, while in CMEs firms access capital via more traditional systems of bank-based finance. 17 Importantly, the VoC approach reduces the role of the financial sector to providing firms with investment capital, thus emphasizing the importance of business debt to support macroeconomic growth in advanced economies via gains in competitiveness. 18

Although the VoC approach remains one of the most prominent and widely cited means of comparing advanced economies, the macroeconomic analysis that underpins it has been challenged for either being underdeveloped or, more critically, having an incorrect conception of the financial sector. 19 In particular, the VoC's macroeconomic framework fails to sufficiently account for financial instability. 20 Furthermore, the VoC is incapable of accounting for households as economic actors, as well as the macroeconomic influence of household debt and house prices that was clearly demonstrated by the GFC. 21

The recent “macroeconomic turn” in the CPE literature partially addresses these issues by putting forward an alternative framework based on the growth model perspective. The Kalecki-inspired growth model literature initially put income distribution at the center of the analysis and categorized economies as having profit-led or wage-led demand regimes, depending on corporate investment or consumption effects respectively. 22 The contributions by Lavoie and Stockhammer generalize the approach and incorporate structural changes in the international economy since the 1980s, such as globalization and the rise of financialization. 23 Subsequently, two alternative growth models emerged, with modern advanced economies largely driven by either export-based industrial production or domestic-oriented systems of household debt, which support consumption and “in some cases, a residential investment boom.” 24

Although Hope and Soskice argue the VoC can be applied to the growth model perspective, 25 with CMEs considered to be export-driven and LMEs consumption-driven, Baccaro and Pontusson alternatively suggest that these growth models do not directly correspond to the VoC typologies in any systematic way. 26 Rather, they argue advanced economies are organized around specific demand-side growth regimes based on consumption, exports, or a combination of the two. Furthermore, unlike Hope and Soskice, Baccaro and Pontusson acknowledge the important macroeconomic role of household debt in directly stimulating growth in consumption-led economies. However, the predominant form household debt takes in advanced economies is mortgage debt, the growth of which is largely determined by house price increases. 27 While Baccaro and Pontusson acknowledge in passing that most household debt is mortgage debt, analytically they treat household debt as consumer debt, and do not further investigate the determinants or macroeconomic impact of house prices. The subsequent literature on growth models is more sensitive to the role of house prices, but usually only for so-called finance-led or consumption-led economies, which are often associated with the Anglosphere countries. 28

Since the GFC there has been a growing, if diverse, economics literature on financial instability and the role of debt and asset prices, partly drawing on Minsky's theory of financial cycles. The macroeconomic growth effects of private household debt and house prices via the consumption channel have been demonstrated empirically in econometric analyses of the British and US cases, 29 as well as several economies in southern Europe. 30 While large panel data studies have shown that household debt can contribute to economic growth in the short run (i.e., less than three years), they also report negative effects in the longer run. 31 Other longer-run analyses have also demonstrated the negative growth effects of household debt in several advanced economies. 32 With high debt-to-income ratios, the macroeconomy can become more vulnerable to asset-price changes, as rapidly depreciating house prices create collateral problems for financial institutions, leading to cycles of financial instability in advanced economies. 33 Although homeownership and household debt are key aspects of financialization, the CPE literature does not offer a sufficient account of how house prices and mortgage debt contribute to macroeconomic growth.

In this article, we address this issue by putting forward a vision of finance in contemporary capitalism that places housing finance and its macroeconomic impact at the center. Based on the post-Keynesian conceptions of finance, and the financialization literature, we suggest there are four core mechanisms that provide a clear structure for the macroeconomic effects of house prices and household debt. First, house prices are an important financial component of the macroeconomy, as they can produce speculative asset-price cycles. For many homeowners, and prospective homeowners, the owner-occupied home is their main financial asset. Households act as speculative investors if they form extrapolative expectations about rising house prices, whether they speculate intentionally or not. With extrapolative expectations house price inflation may create further demand for homeownership, resulting in an upward asset-price spiral of increasing house prices. 34 However, housing asset-price spirals may also contract sharply if investor households expect a reversion of prices. Such “housing bubbles” have been identified in many countries and often have severely negative consequences for the wider macroeconomy. 35

Second, rising house prices lead to household debt increases. 36 As house price inflation can lead the private owner-occupied home to be considered a secure form of collateral, this encourages financial institutions to lend mortgages to homeowners and potential homeowners in the belief a payment default by the borrower will not lead to any financial loss for the bank. At the micro level, financial institutions issue mortgages at specific loan-to-value ratios (i.e., 80 percent of the value of the home). Therefore, house price inflation will typically lead to an increase in the volume of mortgage debt a financial institution will lend to a borrower. When aggregated up to the macro level, this means house price increases may also increase the total volume of household debt present in an economy.

Third, liberalizations of mortgage credit can reinforce housing asset-price inflation through the demand channel. Because of the high cost of private homeownership most home purchases are funded using mortgage credit. If credit access is restrictive, this means that fewer potential borrowers can purchase homes, thus reducing demand for private homeownership. However, if homeowners, and potential homeowners, have expectations of future house price increases, any relaxation of mortgage credit restrictions can increase the pool of potential borrowers, reinforcing house price inflation by facilitating increased demand for private housing. 37 However, recent research has demonstrated that liberalizations of mortgage credit have not significantly increased homeownership rates. 38 Alternatively, relaxations of mortgage credit can take the form of increased loan-to-value ratios, which, rather than increasing homeownership rates, may just further drive housing asset-price inflation. 39

Fourth, rising house prices and household indebtedness will have positive effects on economic growth by fueling residential investment and consumption, at least over short to medium time horizons. House price inflation may contribute to the residential investment channel of GDP growth, as it creates incentives for developers to construct and sell new homes. Homeowners can partially realize the financial gains from house price inflation without selling their property by taking out equity release mortgages, which can increase economic growth by facilitating the consumption of nonhousing goods and services. 40 The “Anglo-liberal” growth model, adopted by countries such as the United Kingdom, the United States, and Ireland, is reliant on perpetual house price inflation and household debt increases to drive consumption. 41 The use of equity release mortgages in the Anglo-liberal growth model, is similar to Crouch's conception of “Privatised Keynesianism.” 42 However, rather than operating as a form of Keynesian countercyclical private economic stimulus, as Crouch suggests, the Anglo-liberal growth model resulted in a form of economic growth that is more pro-cyclical with respect to the financial cycle, ultimately, leading to financial instability. 43 Both Crouch and Hay restrict these mechanisms to the “Anglosphere” states, yet, as suggested by Barnes, 44 we assert these mechanisms operate across a much wider range of countries.

Our framework is orthogonal to a small but growing literature on the CPE systems of housing and mortgage finance. As noted by both Aalbers and Christophers and Johnston and Kurzer, 45 housing and mortgage finance have been largely absent from CPE analyses. The relatively small emerging literature can be organized into two main strands. The first focuses on classifications of national-level housing finance systems, resulting in the development of various different typology sets and country groupings. 46 The second strand examines the politics of housing, particularly welfare state retrenchment policies. 47 Although there has been a CPE examination of how housing contributes to economic instability and how different governments use housing to respond to macroeconomic instability, except for attempts from a handful of studies examining a narrow set of cases, there is no specific framework in the housing CPE literature that systematically conceptualizes the macroeconomic role of housing and mortgage credit. 48 It is this gap that this article seeks to address.

Empirical Design

Our empirical design examines the interactions between the three main variables of interest, gross domestic product (GDP), household debt, and house prices, using three separate equations. The first equation examines the effects of household debt and house prices on GDP. The second equation explains household debt as a function of house prices and GDP, while the third equation explains house prices as a function of household debt and GDP. While theoretically we posit specific mechanisms, empirically we use a more general framework that allows for the effects of all key variables using autoregressive distributed lag (ARDL) models, where the dependent variable is considered a function of its lagged values. ARDL models are widely used in time series econometric analyses as they allow for a flexible modeling strategy when the precise lag structure of the effects of key variables is not known. The sample consists of unbalanced panel data from 1980 to 2019 for eighteen advanced economies (Australia, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, the Netherlands, New Zealand, Norway, Spain, Sweden, Switzerland, the United Kingdom, and the United States). These cases were selected as the macroeconomic effects of household debt and house prices may be more clearly evaluated in countries with advanced financial systems that have liberalized debt policies. We selected 1980 as the starting year of this analysis, as it marks the broad reemergence of the financial sector as a key driver of growth in advanced economies.

As we use the same main variables in each equation, we face issues of mutual determination and possible endogeneity problems. We address these issues by only considering lagged effects for the GDP and house price equations, which are predetermined and considered, at worst, “weakly exogenous” in all dynamic panel specifications. 49 Therefore, our models construct a unidirectional mechanism that operates in a similar manner to Granger causality, which posits that changes in the lagged explanatory variable must occur prior to changes in the dependent variable. 50 There is also a theoretical justification for only using lags in these two equations, as the macroeconomic effects of household debt on both GDP and house prices are noncontemporaneous as they take time to manifest. 51 As mortgage lending volumes are determined by loan-to-value ratios at the application stage, we include the contemporaneous effects of house prices in the household debt equation, which is consistent with previous research. 52 The lag structure for each variable is chosen following a testing down procedure starting from five lags of each coefficient and eliminating the final lag if statistically insignificant. The statistical significance of the lagged coefficients, at 90 percent or above, suggests two lags are appropriate for each independent variable.

Pretesting suggests that each of the variables are nonstationary. We eliminate the stochastic trend by differencing and estimate ARDL models. Based on the results of the testing down procedure, we include two lags of the dependent variable in each equation. An alternative would be to estimate the error correction models in levels and allow (and test) for cointegration. However, we prefer the difference specifications because they are more parsimonious. Our analysis thus has a short- to medium-term focus and may not fully capture long-term effects.

One of the main research areas of CPE is the identification of key institutional differences between advanced economies. Most CPE time series analyses use pooled estimators, such as fixed effects OLS regression models. However, pooled OLS estimators lead to bias when examining heterogenous country groupings in dynamic specifications. In a static analysis, that is, in a specification without lags, a fixed effects OLS model provides an unbiased estimate of the average effects across countries. However, this does not hold under dynamic time series specifications with lags, and if left unaccounted for may induce serial correlation in the error term, thereby generating inconsistent estimates in models with lagged independent variables. To address these issues, we use the mean group (MG) estimator that allows for variations at the national level, thus, allowing for coefficient heterogeneity across countries. 53 The MG estimator does this by first estimating the relevant equation for each country individually and then averaging the coefficient across countries. We consider the MG estimator the “natural fit” for CPE, as the starting point (i.e., the null hypothesis) for CPE is that countries differ, requiring the model specifications to allow for country-level heterogeneity.

The first equation examines the effects of household debt and house prices on economic growth. Subsequently, the dependent variable in the baseline specification of the first equation is aggregate demand, modeled using GDP, a standard measure of economic growth in econometric analyses. The main independent variable of interest in the baseline specification of the first equation is the aggregate volume of outstanding household debt, which includes all credit provided to households. From the literature, 54 we would expect to find a positive relationship between household debt growth and GDP growth. However, high levels of debt have been also identified as having a destabilizing effect on the economy. Therefore, once temporal dynamics are taken into account, there may be a negative relationship between the variables. This is congruent with the results observed in previous analyses of household debt and economic growth, which demonstrate shorter-term positive growth effects of private debt but negative effects in the longer term. 55

Business debt is included as a second variable of interest in the baseline specification of the first equation to account for forms of private debt taken out by nonhousehold actors. Including business debt also allows us to formally evaluate the macroeconomic underpinnings of the VoC, which conceptualizes the macroeconomic role of the financial sector as providing corporate investment capital to firms. Based on the VoC framework, we would expect to see a positive relationship between increases in business debt and GDP growth. However, business debt is a liability for firms, which will have a negative impact on firm investment and macroeconomic growth. Indeed, in the Minskyan debt cycle, the negative effect of business debt on investment plays a key role. 56 Specification 2 of the first equation is the same as the baseline specification, but also includes house prices as a third key independent variable. House prices have been found to have positive macroeconomic growth effects in different advanced economies. 57 As such, we have similar expectations about the positive relationship between house prices on GDP.

To develop our CPE analysis, we also break down the sample into smaller country grouping subsets in specifications 3–8, based on the most relevant CPE typologies associated with how the financial sector contributes to macroeconomic growth. To assess the effects of household debt and house prices in terms of the growth model perspective, specification 3 examines countries associated export-driven growth models (Belgium, Canada, Denmark, Finland, Germany, Japan, the Netherlands, Norway, Sweden and Switzerland), while specification 4 contains the debt-driven economies (Australia, Ireland, New Zealand, Spain, the United States, and the United Kingdom), using the country classifications put forward by Hein et al. 58 To account for different financial systems, specification 5 examines countries associated with bank-based financial systems (Belgium, Denmark, Finland, France, Germany, Italy, Norway, Spain), while specification 6 evaluates the effects in countries associated with more market-based financial systems (Australia, Canada, Ireland, Japan, the Netherlands, New Zealand, Sweden, Switzerland, the United States, and the United Kingdom), based on the country classifications put forward by Levine. 59

We also account for country-level variations in housing systems. However, as the variables used by the housing CPE literature to categorize countries (i.e., owner-occupation rates and mortgage debt volumes) have changed considerably over time, leading to country groupings that would be substantively different now from how they were originally conceptualized, 60 we do not use the Varieties of Residential Capitalism country classifications. Rather we break up the sample according to a dimension in Schwartz and Seabrooke's analysis: 61 we use owner-occupation rates to account for differences between housing systems. Specification 7 examines countries with owner-occupation rates below the mean across the sample (Belgium, Denmark, Finland, France, Germany, Japan, the Netherlands, Sweden, and Switzerland), while specification 8 focuses on countries with above-mean owner-occupation rates (Australia, Canada, Ireland, Italy, New Zealand, Norway, Spain, the United States, and the United Kingdom).

To account for a potential positive feedback loop between house prices and mortgage debt, 62 the baseline specification of the second equation uses household debt as the dependent variable, with house prices and GDP as independent variables. While the baseline specification of the third equation uses house prices as the dependent variable with house prices and GDP as independent variables. The household debt and house price equations are also examined using the same comparative subset specifications as the GDP equation, which examine country groupings in terms of owner-occupation rates, financial systems, and dominant growth models. The small number of dependent variables suggests the baseline specifications of each equation may be subject to an omitted variable bias. However, the right-hand side of the equation includes time lags of the GDP dependent variable as part of the ARDL, which accounts for potential omitted variable bias issues and mitigates the need for additional control variables to be included in the analysis. 63

Real GDP and real house price index data were obtained from the OECD, 64 while nominal data for the household debt and business debt variables were obtained from the Bank of International Settlements. 65 The nominal data were adjusted for inflation using OECD's GDP deflator. 66 See Appendix A (online only) for a complete account of data sources and variable definitions. Before differencing the series, each of the dependent and independent variables are transformed using the natural-logarithmic scale, as the coefficient generated from such log transformations may be interpreted as a close approximation for the percentage change to provide elasticities for each variable, which is more relevant to this analysis than a single unit change. 67 Summary statistics for the variables used in this analysis can be found in Table 1 below.

Summary Statistics.

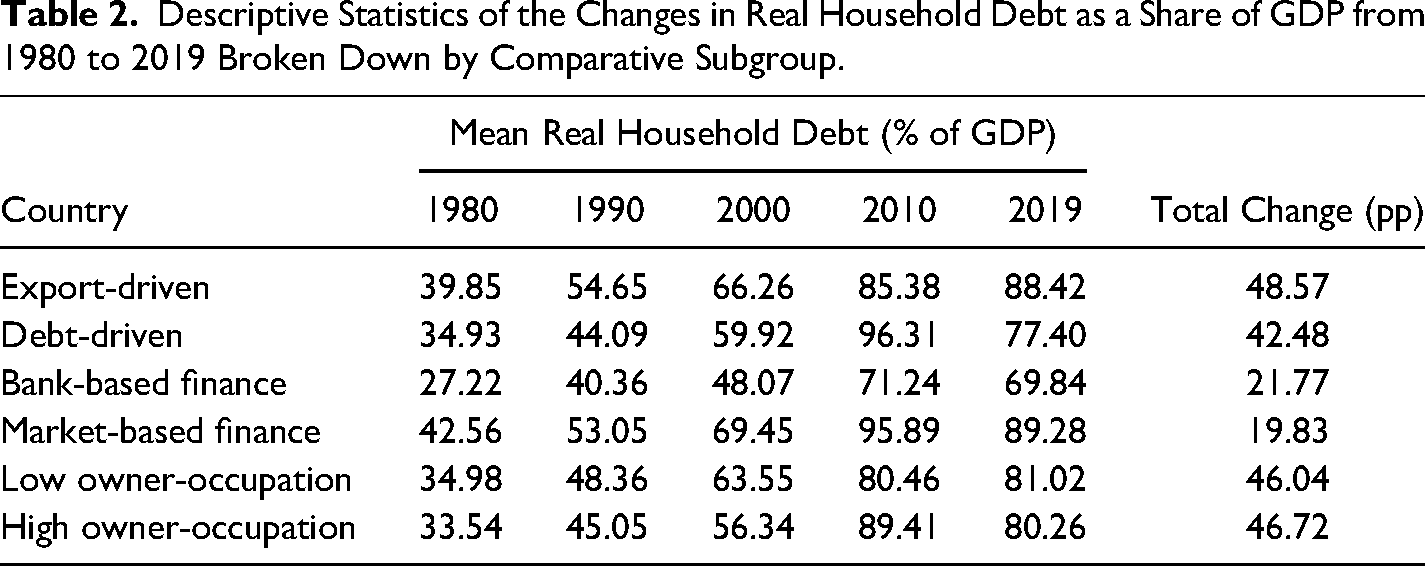

Table 2 describes the mean changes in real household debt between 1980 and 2019 in terms of the CPE subgroup classifications used in this analysis. The table shows that export-driven economies tend to have higher levels and growth rates of household debt as a share of GDP than debt-driven economies. We also observe that countries associated with market-based banking systems tend to have higher levels of household debt as a share of GDP (89.28) than bank-based financial systems (69.84 percent). However, countries with bank-based systems show a slightly larger growth rate of household debt shares of GDP (21.77 percentage points) than market-based financial systems (19.83 percentage points). Table 2 also demonstrates that countries with lower owner-occupation rates have similar levels and growth rates of household debt as a share of GDP to countries with higher owner occupation rates. The descriptive results presented in Table 2 are not in line with the expectations of the CPE and financialization literatures, which tend to consider the US and UK cases as the archetypes of debt-driven or financialized economies.

Descriptive Statistics of the Changes in Real Household Debt as a Share of GDP from 1980 to 2019 Broken Down by Comparative Subgroup.

When we examine the data for specific countries, we observe there are several economies that have much higher levels of household debt as a share of GDP in their economies than the United States (74.66%) and the United Kingdom (84.02%), such as Switzerland (124.62%), Norway (114.15%), Denmark (109.46%), the Netherlands (101.33%), and Sweden (96.57%). While the United States and the United Kingdom are widely considered debt-driven economies, each of these countries with higher levels of household debt than the United States and the United Kingdom are classed as export-led economies by Hein et al. From a comparative perspective, these descriptive statistics suggest household indebtedness is pervasive across advanced economies, and may have more general macroeconomic effects rather than being isolated to a narrow range of countries, such as those associated with the Anglosphere. 68 See Appendix B (online only) for the full country-level descriptive statistics pertaining to this analysis.

Econometric Results

Tables 3 to 5 provide the estimates of the coefficients from the econometric models performed in this analysis. The baseline specifications for each of the three equations are as follows:

GDP Equation Results.

***p < 0.01, **p < 0.05, *p < 0.10.

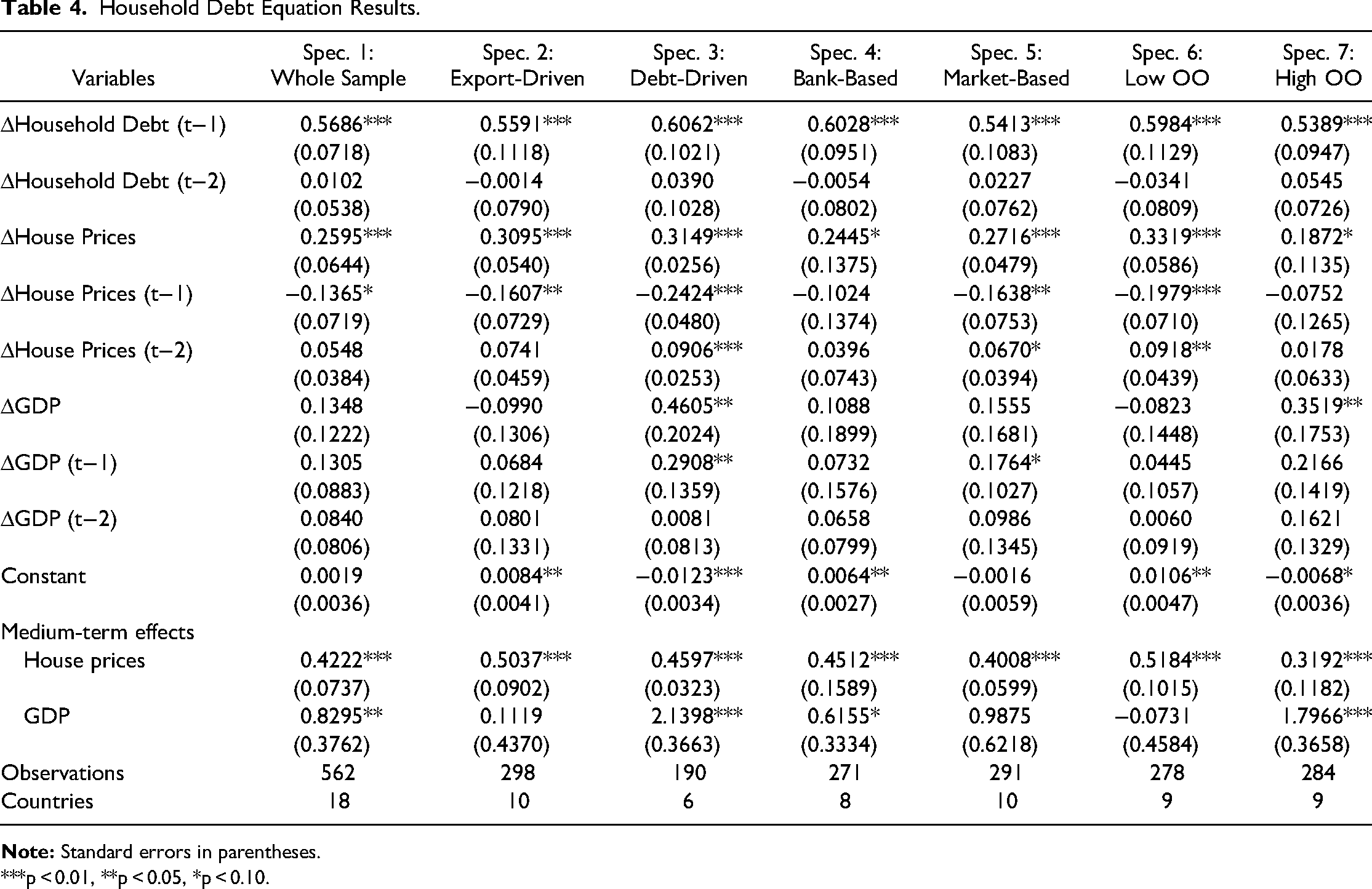

Household Debt Equation Results.

***p < 0.01, **p < 0.05, *p < 0.10.

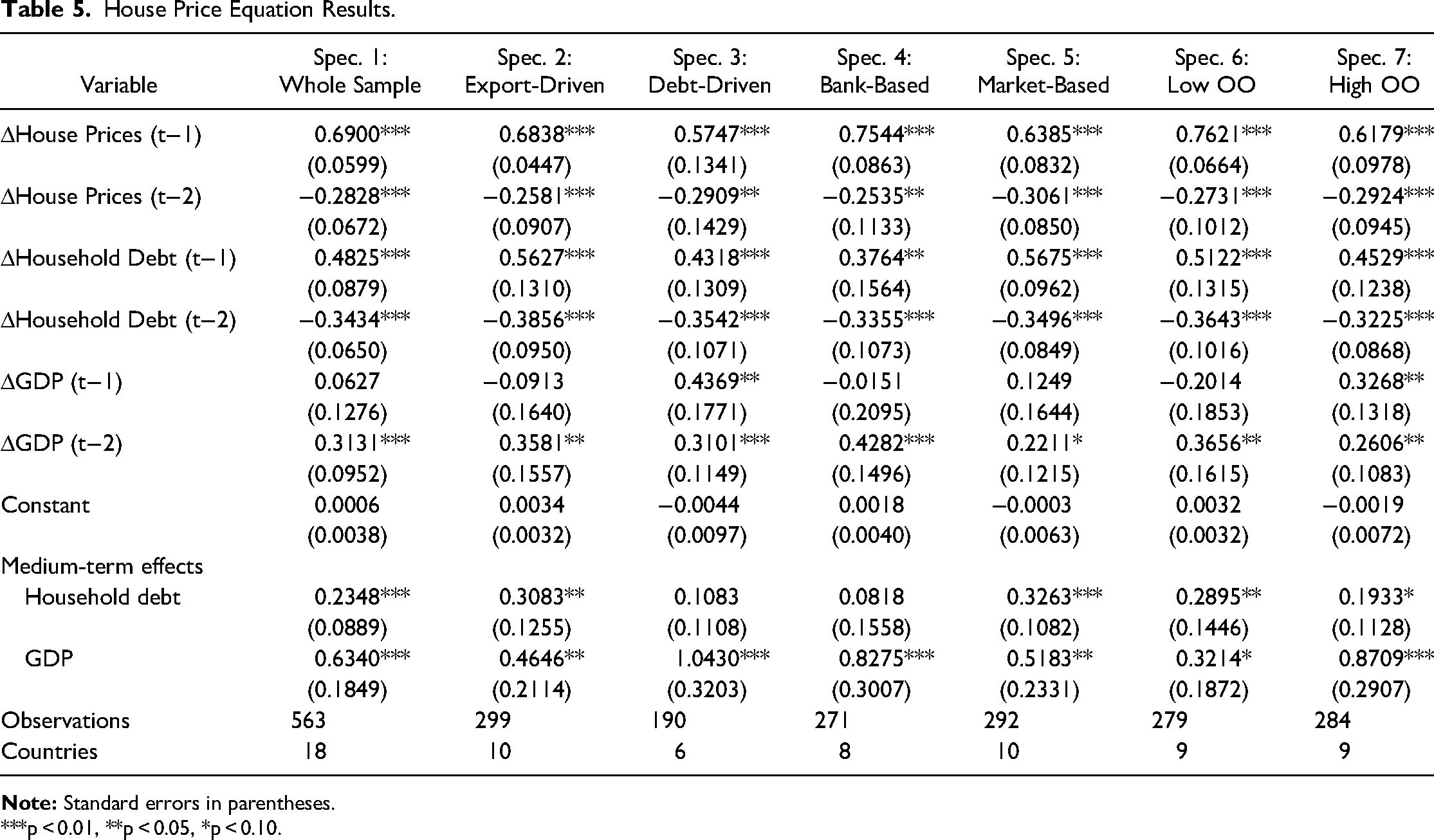

House Price Equation Results.

***p < 0.01, **p < 0.05, *p < 0.10.

(1) ΔGDP(t) = β1ΔGDP(t−1) + β2ΔGDP(t−2) + β3ΔHHD(t−1) + β4ΔHHD(t−2) + β5ΔBD(t−1) + β6ΔBD(t−2) + εt,

(2) ΔHHD(t) = β1ΔHHD(t−1) + β2ΔHHD(t−2) + β3ΔHP(t) + β4ΔHP(t−1) + β5ΔHP(t−2) + β6ΔGDP(t) + β7ΔGDP(t−1) + β8ΔGDP(t−2) + εt,

(3) ΔHP(t) = β1ΔHP(t−1) + β2ΔHP(t−2) + β3ΔHHD(t−1) + β4ΔHHD(t−2) + β5ΔGDP(t−1) + β6ΔGDP(t−2) + εt.

Here, GDP is the logarithm of real GDP, HHD is the logarithm of the real volume of household debt, HP is the logarithm of real house prices, and BD is the logarithm of the real volume of business debt.

We reparametrize the ARDL to produce a single coefficient for the medium-run effects (first and second round effects from each lag of the independent variables). We calculate these medium-run effects by taking the ratio of the sum of the coefficients of the two lags of the independent variable (as well as the coefficient of the contemporaneous effects in the household debt equation) to the sum of the coefficients of the lagged dependent variable). The adjustment speed is calculated by subtracting the sum of the coefficients of the two lags of the dependent variable from 1. Because the estimates of the medium-run coefficients are recalculations from the estimated coefficients, we also recalculate their standard errors to assess their statistical significance using the Stata command nlcom, as suggested by Vlandas. 69

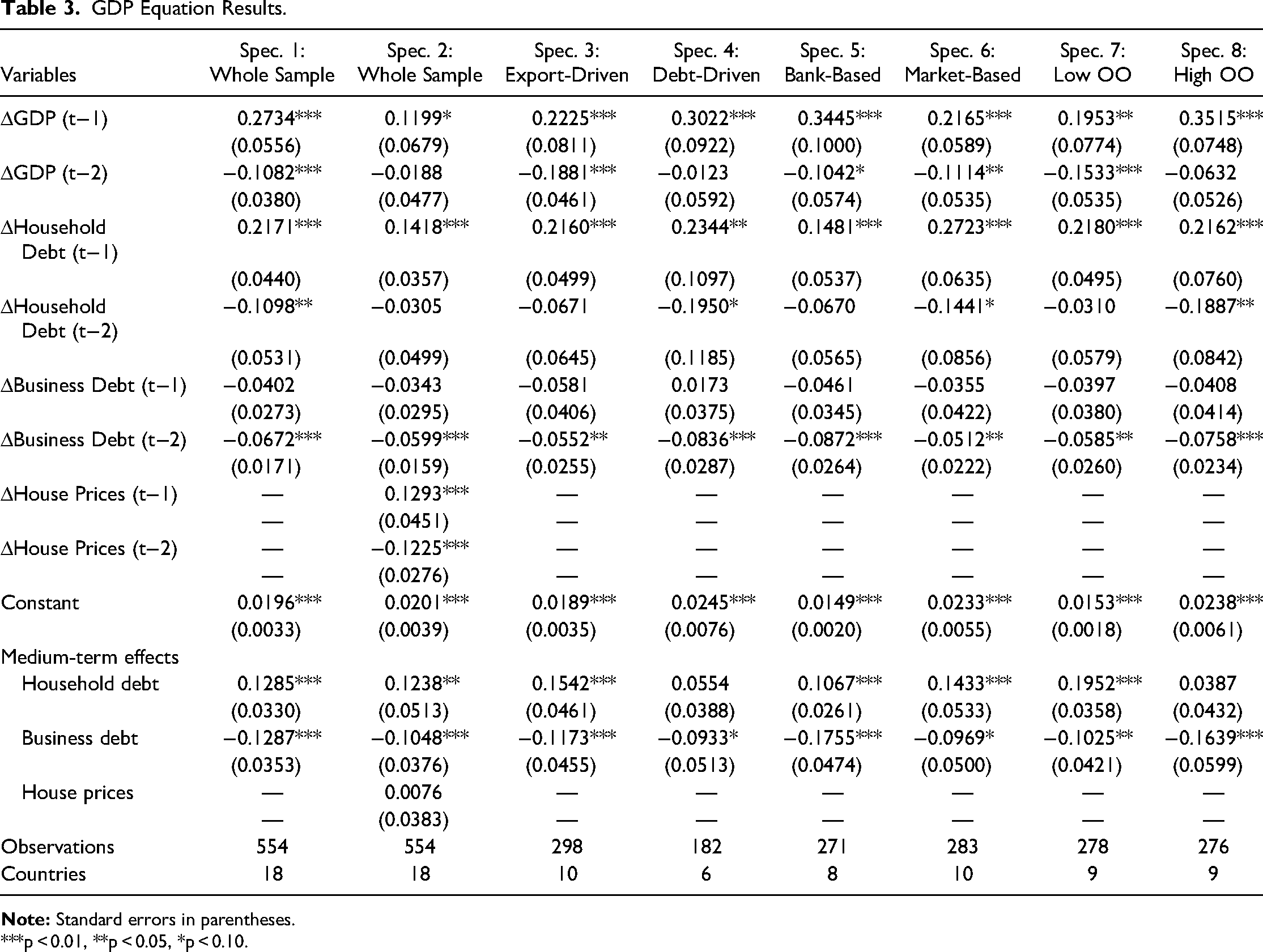

Table 3 summarizes the results of the GDP equation. Specification 1 presents the baseline result with two lags of household debt and business debt for the full sample. The results demonstrate that household debt has statistically significant positive effects (at the 1 percent level) on GDP for the whole sample. As the coefficients can be interpreted as elasticities, they suggest that a 1 percent increase in household debt leads to an increase in economic growth of 0.13 percent. In contrast, the results of specification 1 show that the coefficient of the business debt variable is negatively statistically significant at the 1 percent level, suggesting that a 1 percent increase in house prices leads to a 0.13 percent reduction in GDP across the sample.

Specification 2 is the same as specification 1 but also includes house prices as an additional variable. The results show similar effects of household debt and business debt to specification 1, with the same order of magnitude. However, house prices show no statistically significant direct effects on economic growth across the sample. Appendix C (online only) shows the results for the GDP equation including house prices broken down into the comparative groupings. We find no significant direct effects of house prices on economic growth in any of the subsamples, except for in bank-based economies. However, the coefficient is relatively small (0.07), and the effects are only significant at the 10 percent level. These results provide support for the main finding in specification 2 and suggest that house prices have little direct effect on economic growth.

Specifications 3 through 8 provide the results of the different CPE country subsample groupings. The results of specification 3 demonstrate that household debt has positive and significant (at the 1 percent level) effects on GDP growth in export-oriented economies, with a coefficient of 0.15. Surprisingly, the results of specification 4 show no significant effects of household debt in debt-driven economies. To further explore this, we excluded Ireland from the subsample, as the Irish GDP data fluctuates heavily because of the impact of multinational economies relocating to Ireland for tax purposes in the early 2000s. With Ireland excluded, we find there are positive and significant effects (at 1 percent) of household debt on GDP in debt-driven economies. However, the coefficient (0.09) is much smaller than that of export-driven economies. See Appendix D (online only) for the full breakdown of the results with Ireland excluded.

Specifications 5 and 6 show positive and significant effects (at the 1 per cent level) of household debt on GDP in both bank-based and market-based financial systems, with coefficients of 0.11 and 0.14, respectively. The results for specification 7 show positive and significant effects (at the 1 percent level) of household debt on GDP in countries with low homeownership rates. While specification 8 shows no statistically significant effects in countries with higher levels of homeownership. The coefficient of the lower owner-occupation rate countries was also much larger (0.20) than that of the higher homeownership countries (0.04). The results of all the subsamples show business debt has significant and negative effects on GDP growth, providing further support for the results observed across the whole sample.

Table 4 describes the results for the household debt equation. Specification 1 demonstrates house prices have positive and statistically significant effects on household debt at the 1 percent level across the sample. The parameter estimate suggests a 1 percent increase in house prices has an effect on household debt of 0.42 percent. We also observe that GDP has positive and significant effects at the 5 percent level on household debt, with a coefficient of 0.83. The results of the CPE subsample groupings all report positive and significant effects of house prices on household debt at the 1 percent level. The coefficients are larger in the export-driven economies (0.50), bank-based financial systems (0.45) and lower owner-occupation countries (0.52), than the debt-driven economies (0.46), market-based systems (0.40), and higher homeownership countries (0.32). Contrastingly, the effects of GDP on household debt were significant at the 1 percent level in debt-driven economies (2.14) and high homeownership countries (1.80) and significant at the 10 percent level in bank-based financial systems (0.62). The other CPE groupings report no significant effects.

Table 5 outlines the results of the house price equation. The results of specification 1 show that household debt has positive and significant effects on house prices at the 1 percent level across the sample. Here, a 1 percent increase in household debt is associated with a 0.24 percent increase in house prices. The results also show GDP has a positive and significant (at the 1 percent level) effect on house prices, with a coefficient of 0.63. The results of the CPE subgroups show positive effects of household debt on house prices in export-oriented economies, significant at the 1 percent level with a coefficient of 0.30. However, there are no significant effects of household debt on house prices in debt-driven economies. Household debt has significant and positive effects at the 1 percent level in market-based financial systems, with a coefficient of 0.33, with no significant effects shown in bank-based systems. Finally, household debt has positive and significant effects in low homeownership (at the 5 percent level) and high homeownership (at the 10 percent level) countries, with coefficients of 0.29 and 0.19, respectively. In contrast, GDP shows significant and positive effects on house prices across all the comparative subgroups.

In sum, our results provide three important findings. First, we demonstrate that household debt growth has significant and positive effects on economic growth across the sample. In contrast, business debt has significant negative effects on economic growth. Second, although there is a positive feedback loop between house prices and household debt, the effects of household debt on house prices are much smaller than the other way around. Therefore, we consider household debt growth to be a function of house prices. Furthermore, as house prices have no significant direct effects on economic growth, our results suggest that they influence macroeconomic outcomes through their effects on household debt growth. Third, from a CPE perspective, we demonstrate that the macroeconomic effects of household debt are observable in both export- and debt-driven economies, as well as countries with bank- and market-based financial systems. These results suggest the effects are generalizable across different countries and are not limited to a specific set of countries. That said, although we observe significant and positive effects of household debt on GDP in countries with low homeownership rates, there were no significant effects in countries associated with higher levels of homeownership.

The Macroeconomics of Household Debt and House Prices in CPE

Our main finding across the sample is that house price inflation drives household debt growth, which, in turn, drives economic growth. These findings have several significant consequences for CPE. First, our results support as well as challenge Baccaro and Pontusson's application of the growth model perspective to CPE. 70 In line with Baccaro and Pontusson, we find evidence to show household debt supports growth in consumption-driven economies. While our analysis demonstrates house prices are an important determinant of household debt, Baccaro and Pontusson do not provide an account of how rising house prices allow households to consume goods and services via increases in mortgage debt. The main theoretical framework of this article explains this mechanism by arguing that households with extrapolative expectations create an upward spiral of house price asset inflation, which homeowners can take advantage of through the use of equity release mortgages to consume goods and services, thus supporting economic growth.

While Baccaro and Pontusson treat what they call consumption-led growth as a distinct growth model, our results suggest that debt-driven growth is much more pervasive across advanced economies. Therefore, their selection of Germany as a “pure” export-driven economy not supported by debt-driven consumption may be the exception rather than the rule and many countries may be operating with more blended growth models. Similarly, as Hope and Soskice argue, 71 it is only LMEs that are consumption-driven, and in showing that export-driven CMEs are also driven by debt-supported consumption, our results also challenge their application of the growth model perspective to the VoC. However, it is important to note that neither house prices nor household debt factor into Hope and Soskice's macroeconomic framework. As such, our analysis highlights the shortcomings of how growth models are conceptualized from a CPE perspective and suggest that house prices and household debt must be accounted for in future examinations of the macroeconomic role of the financial sector.

Our analysis provides robust econometric evidence to support Hay's identification of a macroeconomic growth model driven by rising house prices and household debt. 72 However, we challenge Hay's assertion that this specific growth model is limited to “Anglo-liberal” states, such as the United States, the United Kingdom, and Ireland. Rather, we provide econometric evidence to support Barnes's suggestion that the Anglo-liberal growth model is much more pervasive, 73 as we demonstrate that household debt and house prices contribute to growth across the whole sample and in different types of financial systems and growth models. Our theoretical framework also offers a more comprehensive set of mechanisms than both Hay and Barnes to explain how the financial sector contributes to macroeconomic growth from a CPE perspective.

Second, our results also challenge the macroeconomic framework of the VoC in two specific ways. First, as the VoC focuses on the firm and institutional complementarities as the central drivers of economic growth, it is incapable of accounting for the household as an economic actor. In demonstrating that households contribute to economic growth through rising house prices and household indebtedness, our results suggest the VoC can only ever provide an incomplete account of how countries generate economic growth. Second, and potentially more damagingly, the VoC's conception of the financial sector is reduced to the provision of credit to firms. Yet, as the results of our analysis show, business debt reduces economic growth, which suggests that the VoC's emphasis on the firm as the main driver of growth is misplaced. Our results are in line with Stockhammer, 74 who suggests that the macroeconomic analysis underpinning the VoC is unsuitable for conceptualizing how financialized economies generate growth.

Third, our results have significant consequences for CPE beyond the growth model and VoC frameworks. Our results demonstrate that house prices drive household indebtedness, and that household debt has positive growth effects in both bank-based and market-based financial systems. From a comparative perspective, this suggests that the macro effects of house prices and household debt should be considered a generalizable feature of advanced financialized economies. However, this may also potentially be due to an observed convergence toward market-based financial systems in advanced economies, as identified by Hardie et al. 75 Our results also suggest the macroeconomic effects of household debt, as well as house price and household debt feedback dynamics, are larger in countries with lower levels of homeownership than those with higher owner-occupation rates. However, these results are surprising, as there is little in the housing CPE literature to explain how variations in owner-occupation rates would have such disparate effects. 76 Rather, based on the results from across the whole sample and the other CPE typology country groupings, our results suggest there are little cross-country differences and that our results are more generalizable across the sample.

Fourth and finally, our analysis provides econometric evidence as to the relationship between private debt, house prices, and macroeconomic growth. Our results support previous research demonstrating house price inflation is a major determinant of private household debt volumes in advanced economies. 77 We also support Stockhammer and Wildauer, 78 who show that household debt supports economic growth, especially before the 2008 GFC. However, our results suggest the positive macroeconomic effects of household debt go beyond the Anglosphere and southern European states. Although we show that household debt has positive short- to medium-run effects, we do not challenge previous studies showing that household debt has negative effects on GDP growth in the long run, 79 as these studies use different estimation methods. For example, Mian et al. use long differences of debt ratios and find that increases in household debt have positive short effects that turn negative after three to four years. 80 Our results focus on the shorter effects, but we acknowledge that there are important time dynamics that must be accounted for when it comes to understanding the macroeconomic effects of house prices and household debt.

Conclusion

Financialization is one of the major structural transformations of the global economy that have taken place in recent decades. Although the distributional consequences of financialization have been widely examined, its macroeconomic implications are much less well defined in CPE. The increased public engagement with financial services is a key element of the financialization of “everyday life,” which has seen a shift in banking activity away from lending to firms for production toward private households. This lending primarily takes the form of mortgage credit to finance private homeownership, which has increasingly been used as a financial asset in many economies. We address the “missing macro” of financialization in CPE by demonstrating that rising house prices drive household debt levels, and that household debt supports GDP growth across a sample of eighteen advanced economies from 1980 to 2019. These results are also consistent across key CPE subgroupings of debt-driven and export-driven economies, as well as bank-based and market-based financial systems. As such, our analysis places the seemingly mundane “everyday life” issues of homeownership and mortgage credit at the center of the macroeconomy in CPE.

Baccaro and Pontusson's application of the growth model perspective to CPE opened the field to examining demand drivers of growth and placed distributional issues more prominently at the center of the analysis, while also allowing for greater macroeconomic instability than the VoC approach. 81 However, our results demonstrate that their application of the growth model perspective to CPE needs to develop its conception of the financial sector further. In particular, while household debt supports consumption, unsecured consumer lending, such as credit cards, makes up a relatively small portion of financial institution lending to households, which is mainly oriented around mortgage provision. As Baccaro and Pontusson do not provide a clear mechanism explaining the links between house prices, mortgage debt, and growth, they do not identify the crucial role of house prices and thus cannot fully explain debt-driven growth dynamics. Our analysis makes a significant contribution in developing the macroeconomic underpinnings of CPE by putting forward an empirically substantiated theoretical argument explaining how rising house prices facilitate growth across advanced economies via the use of equity release mortgages.

We contend that the growth models approach must move beyond the dichotomy of debt-driven versus export-driven economies. While that distinction was helpful to understand certain macroeconomic dynamics in the decade prior to the GFC, the growth models approach needs a more general understanding of the drivers of economic growth. 82 This article provides a vital component for that by demonstrating the central role of house prices and household debt for the macroeconomy that holds across different countries, even in those classified previously as export-driven. Moreover, the coefficients we observe apply in the upswing as well as in the downswing of the financial cycle. Therefore, debt-driven growth has its counterpart in debt-driven stagnation in the event of a downturn in house prices or the financial cycle. In those periods, countries will seek (successfully or not) to activate other drivers of economic growth. As such, developing an understanding of the various mechanisms by which different economies activate debt-driven growth, as well as other drivers of growth in periods of downturn, could be important areas for future research.

Supplemental Material

sj-docx-1-pas-10.1177_00323292231201480 - Supplemental material for Bringing Household Finance Back In: House Prices and the Missing Macroeconomics of Comparative Political Economy

Supplemental material, sj-docx-1-pas-10.1177_00323292231201480 for Bringing Household Finance Back In: House Prices and the Missing Macroeconomics of Comparative Political Economy by James D. G. Wood and Engelbert Stockhammer in Politics & Society

Footnotes

Acknowledgments

We are grateful to Jason Sharman, Sebastian Kohl, Alex Reisenbichler, Andreas Wiedemann, and Karsten Kohler for their important comments on earlier drafts of this article. This article was presented at the International and Comparative Political Economy workshop at King's College London, the 2020 EAEPE conference, the 2020 SASE conference, and the 2020 British and Comparative Political Economy PSA Specialist Group workshop. We are grateful to the various participants for their constructive feedback. Responsibility for all errors and omissions made in this article must lie solely with the authors.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.