Abstract

This article offers a monetary perspective on capital flows and the Eurozone's north-south divide. It argues that finance-centric narratives in comparative political economy rightly emphasize financial instability in the periphery, but that the role of capital flows therein requires clarification. The article draws on post-Keynesian monetary theory, coherent accounting, and balance-of-payments data to make three points. First, the focus on the financial account as a driver of current accounts should be abandoned in favor of an analysis of gross capital flows. Gross flows need not stem from excess savings in core countries and can be independent from trade flows. Second, explanations of financial instability in the periphery should go beyond bank flows and consider speculative portfolio flows into bond markets and foreign direct investment into real estate. Third, rising spreads in the periphery during the Eurozone crisis and the outbreak of the pandemic were not triggered by balance-of-payments problems but by a reversal of speculative bond flows. Comparative political economy should thus dedicate more attention to institutions that render peripheral countries susceptible to speculative flows into asset markets.

Keywords

A decade has passed since the 2010–12 Eurozone crisis. Back then, rising spreads on government bonds put severe pressure on the public finances of southern Europe and Ireland, forcing several countries to request official financial assistance in return for painful adjustment programs. While the period from 2013 to 2019 was one of recovery (or acceptance of a new depressed normal in the case of Greece), the outbreak of the Covid-19 pandemic came with a temporary rebound of trouble in peripheral government bond markets. Indeed, the continued presence of a “north/south divide” 1 has become a key topic in comparative political economy (CPE) since the Eurozone crisis (EZC). 2

In CPE, the crisis is now commonly regarded as the outcome of two divergent growth models, an export-led regime in the core countries and a domestic demand-led regime in the periphery, whose monetary integration led to severe macroeconomic imbalances. The buildup of large current account deficits in the periphery has been identified as a main source of the EZC and the subsequent weak economic performance. Peripheral deficits, in turn, were attributed to a loss in price competitiveness due to uneven wage growth 3 or a lack of nonprice competitiveness in the form of weak technological capabilities. 4

A different strand of the literature proposes finance-centric interpretations that highlight financial instability as a source of divergence in the Eurozone. 5 Contrary to a popular view among European policymakers, finance-centric narratives argue that it was not excessive public but private debt that rendered the periphery sensitive to the 2008 global financial crisis (GFC). They identify unsustainable credit-financed economic booms as a main cause of financial vulnerabilities in the periphery. The institutional sources of divergence in the Eurozone should thus be sought in financial and banking systems rather than public debt or labor market institutions.

Finance-centric narratives often ascribe a key role to capital flows both in the buildup and the unraveling of financial fragilities. Several proponents argue that capital flows into the periphery, especially interbank flows, provided liquidity that was loaned to domestic borrowers and thereby induced a demand shock that fueled an unsustainable boom. 6 In some accounts, these flows are attributed to high saving rates and current account surpluses in the core countries 7 that were “recycled” in the periphery. 8 Some authors further propose an interpretation of the Eurozone crisis as a balance-of-payments (BoP) crisis that was triggered by a sudden stop in the capital flows that were needed to finance current account deficits. 9

The present article embraces the finance-centric view of the Eurozone's north-south divide, which rightly highlights destabilizing financial dynamics in the periphery's private sectors. However, it argues that the proposed mechanisms through which capital flows impact financial instability require clarification. There has been a tendency to borrow a bit too uncritically from mainstream economics, as reflected in metaphors such as the “recycling of surpluses.” The underlying neoclassical understanding of the economy, in which financial dynamics are driven by the supply of savings, leads to a fixation on current account imbalances. This has led to a narrow analysis of capital flows that focuses on net flows as measured by the financial account, which are the flip side of trade imbalances. The much broader gross flows not only contain trade-related flows but also flows that arise when financial assets are exchanged by residents of different countries. These gross financial flows are independent of the underlying current account position and leave the financial account unchanged. They are often speculative and can thus have destabilizing effects on asset markets, for example, for government bonds and real estate. The article will argue that the narrow focus on net flows overemphasizes the causal role of banks in surplus countries like Germany, which distracts from domestic financial and housing policies that peripheral countries could use to prevent speculative financial dynamics.

To examine the role of gross capital flows in the north-south divide in the Eurozone, the article draws on post-Keynesian (PK) theory. Contributing to recent efforts to integrate the PK theory of demand regimes into CPE, 10 this article utilizes the monetary aspects of PK theory. In this approach, money is created by commercial banks when new loans are made. 11 The financing of economic expenditures is thus not constrained by the supply of saving. While commercial banks therefore play a relatively passive role in the accommodation of credit demand, PK theory highlights the speculative nature of asset markets, where herd behavior and sudden changes in risk perceptions can give rise to booms and busts. The PK perspective provides an alternative to a neoclassical understanding of the economy. The neoclassical perspective, which arguably informs some of the finance-centric narratives, draws attention to export surpluses and bank liquidity as drivers of financial fragility but overlooks the role of speculative gross flows into asset markets.

Based on the PK monetary approach, three main arguments are made. First, the focus on net capital flows as drivers of current accounts should be abandoned in favor of an analysis of gross capital flows. From a monetary perspective, net inflows result from the demand for imports and are thus driven by trade. Net capital inflows (or equivalently financial account surpluses) are hence an outcome, not a cause of current account deficits. A consideration of potentially destabilizing financial flows requires a focus on gross capital flows that are independent of trade but can cause financial instability. These gross flows need not stem from a “recycling of surpluses” (or excess savings) of core countries in the Eurozone and may just as well originate from countries that are net borrowers.

Second, the causal role of different types of capital flows in driving unsustainable booms needs to be reconsidered. In particular, some authors have placed a strong focus on flows into peripheral banks, suggesting that the additional liquidity would automatically be loaned to domestic borrowers. In a PK monetary perspective, these interbank flows alone cannot fully explain the increase in demand for loans that drove the extraordinary financial booms in countries such as Ireland and Spain. The article suggests broadening the finance-centric narrative by also considering portfolio flows into government bond markets and foreign direct investment (FDI) in real estate as potential drivers of destabilizing speculative dynamics in the periphery.

Third, both the EZC and the recent rise in peripheral spreads during the outbreak of the pandemic should better be regarded as speculative attacks in government bond markets than BoP crises. A closer inspection of capital flows around these events suggests that they entailed a sudden stop in gross portfolio debt flows in government bond markets, which led to a fall in bond prices. By contrast, partly thanks to access to central bank liquidity, flows that were needed to finance trade deficits remained relatively stable for most peripheral countries during the 2010–12 EZC, casting doubt on the BoP crisis view.

The analysis has useful implications for CPE and economic policy, which are spelled out in detail in the conclusion. First, comparative analyses of financial instability should focus on cross-country differences in the size and risk appetite of domestic financial systems rather than current account positions. By the same token, policy measures to address the north-south divide in the Eurozone should curb unsustainable credit booms rather than rebalance current accounts through austerity. Second, institutions related to housing and the investment strategies of foreign investors may influence why peripheral countries are especially prone to speculative portfolio and FDI flows. Policies such as residence-specific taxes on property transactions may help shield peripheral countries from speculative flows into housing markets. Third, central banks play a critical role in preventing speculative attacks in peripheral government bonds markets. The European Central Bank (ECB) could backstop peripheral government bonds by unconditionally accepting them as collateral. Finally, domestic financial cycles in house prices and private debt may be quite independent from capital flows, warranting comparative analysis of domestic housing and financial institutions, such as weak social housing provision and easy access to mortgage credit that render those cycles more volatile in the Eurozone's south.

The article builds on a growing literature on gross capital flows 12 and on empirical studies that use an endogenous-money perspective to understand European imbalances. 13 It contributes by specifically engaging with finance-centric narratives of the Eurozone's north-south divide. It provides a theoretical discussion that not only encompasses the theory of endogenous money but also considers the impact of speculative capital flows on asset prices. It clarifies the relevant accounting relationships and offers an empirical illustration with disaggregated BoP data on gross flows in the Eurozone. Finally, it is noteworthy that while this article focuses on CPE debates, it is also relevant for research in international political economy where the “recycling of surpluses” argument has been adopted to explain global sources of financial instability. 14

Before presenting the three main arguments, the article briefly outlines the theoretical foundations of its PK monetary perspective and contrasts it with neoclassical loanable funds theory.

Neoclassical Loanable Funds Theory versus Post-Keynesian Monetary Theory

While the finance-centric narratives’ emphasis on financial instability generally dovetails with PK theory, this article argues that some of the proposed mechanisms have been borrowed from mainstream economics. This can be seen in the use of tropes such as a recycling of surpluses and a fueling of credit booms through loanable funds. 15 In mainstream loanable funds theory, banks collect funds (deposits) from savers that they then lend out to borrowers. 16 As deposits originate from saving, which in turn is real income that is not consumed, they are tightly linked to physical resources generated in economic production. Correspondingly, loanable funds tend to be scarce, and the demand and supply of funds are brought into equilibrium through a flexible rate of interest. If households decide to save more for a given rate of interest, the supply of loanable funds will increase, putting downward pressure on the interest rate until demand equals supply. An extension of this framework is the money multiplier theory that does allow for some money creation by banks. 17 In this extension, central banks inject reserves into the banking system, based on which banks then extend loans up to a limit that is determined by reserve requirements. Central banks can thus control the money supply by setting the amount of reserves. Loanable funds can thus also come from the central bank, but the direction of causality again runs from funds to credit provision.

Loanable funds theory is widely taught in economics 18 and is “almost universally used” in policy-oriented macroeconomics. 19 Brett Fiebiger and Marc Lavoie show that the quantitative easing policies pursued by central banks after the GFC were partly informed by the assumption that asset purchases would provide banks with loanable funds that could be loaned to borrowers. 20 Similarly, fiscal policy debates commonly evaluate the danger of a crowding-out of private through public investment, which is (implicitly) based on the idea of a limited amount of loanable funds available to finance investment. A particularly influential international version of loanable funds theory was made prominent before the GFC by a former chairman of the Federal Reserve, Ben Bernanke. According to Bernanke, a “global saving glut” stemmed from countries with current account surpluses (mostly in East Asia) and depressed interest rates in deficit countries (the United States), where it led to excessive borrowing. 21 As a remedy, Bernanke suggested making foreign investment in developing countries more attractive by removing barriers to capital flows, so that these countries could assume their “more natural role as borrowers, rather than as lenders.”

The PK monetary theory of credit is radically different from the loanable funds framework. At its heart is the principle of endogenous money according to which commercial banks endogenously create new deposit money when they make loans. 22 The creation of new loans, and by extension money, is driven by the demand for credit. Provided borrowers are deemed creditworthy, commercial banks accommodate the demand for credit at a given interest rate without first having to collect the deposits of savers. With private banks capable of creating money, the supply of purchasing power to finance expenditures is an elastic variable that is independent from the previous saving of physical resources, for example, export surpluses. Saving and financing are thus conceptually distinct: the latter is not constrained by the former. Having created new deposit money for borrowers, banks may in turn borrow reserves from the central bank to stay liquid. Short-term interest rates are not determined on the market for loanable funds but by monetary policy through the central bank's monopoly on the creation of new reserves. Central banks normally accommodate the demand for reserves to ensure a smooth operation of the payments systems. Unlike commercial banks, nonbank actors do not have access to central bank liquidity, nor can they issue deposit money.

Beyond assessing creditworthiness, commercial banks play a relatively passive role in this theory; hence, attention is drawn to the drivers of credit demand. Keynes and Minsky 23 regarded the interplay between speculative behavior and asset prices as key: 24 during periods of optimism, actors invest in risky assets whose prices thus go up. Rising asset prices improve creditworthiness and stimulate credit demand to finance further asset purchases. This increases financial fragility in the economy. Sudden changes in risk perceptions can then lead to fire sales of assets, which prick the bubble and force overindebted agents to deleverage. PK theory thereby draws attention to speculative asset markets as drivers of financial instability (as opposed to an increased availability of loanable funds through more saving). This comes with a focus on nonbank financial institutions such as institutional investors as key players in asset markets (as opposed to commercial banks). In contrast to the loanable funds view, the PK approach recommends active regulation of financial institutions and financial markets, domestically and internationally, with an aim to curb speculative dynamics.

In the following, a key analytical tool from this approach will be utilized: balance-sheet accounting that keeps track of the underlying financial relationships between actors. 25 The next section shows that such watertight accounting combined with the theory of endogenous money provides conceptual clarification of the relationship between net capital flows, current accounts, and excess savings.

On Capital Flows, Trade Flows, and the Recycling of Surpluses

Capital Flows and Trade Flows

Current account imbalances are widely regarded as a key factor in the Eurozone's north-south divide. Finance-centric narratives often emphasize capital flows as opposed to competitiveness as their main drivers. 26 The argument is sometimes framed using the BoP identity: “unsustainable current account imbalances were driven by changes in the capital account” 27 or “the financial account essentially clears ‘first’: it is the presence of extra capital which causally precedes the decision to import.” 28 Based on this idea, it is argued that the rising current account deficits after the introduction of the euro are the direct outcome of massive capital flows into the periphery. Gregory W. Fuller 29 justifies the causal primacy of the financial account with the claim that an importer cannot “conjure money from thin air” and thus needs to attract foreign saving before they can pay for (net) imports.

The argument that financial accounts drive current accounts implicitly builds on a loanable funds view that equates physical resources with financial resources. However, in monetary economies, domestic banks can indeed create purchasing power out of thin air, which in the Eurozone can be used to pay for imports that are invoiced in euros. The transfer of domestically generated deposits to a foreign exporter then constitutes a net capital inflow as the flip-side of the import. In a PK monetary perspective, it is thus the decision to import that generates accompanying net financial flows. 30

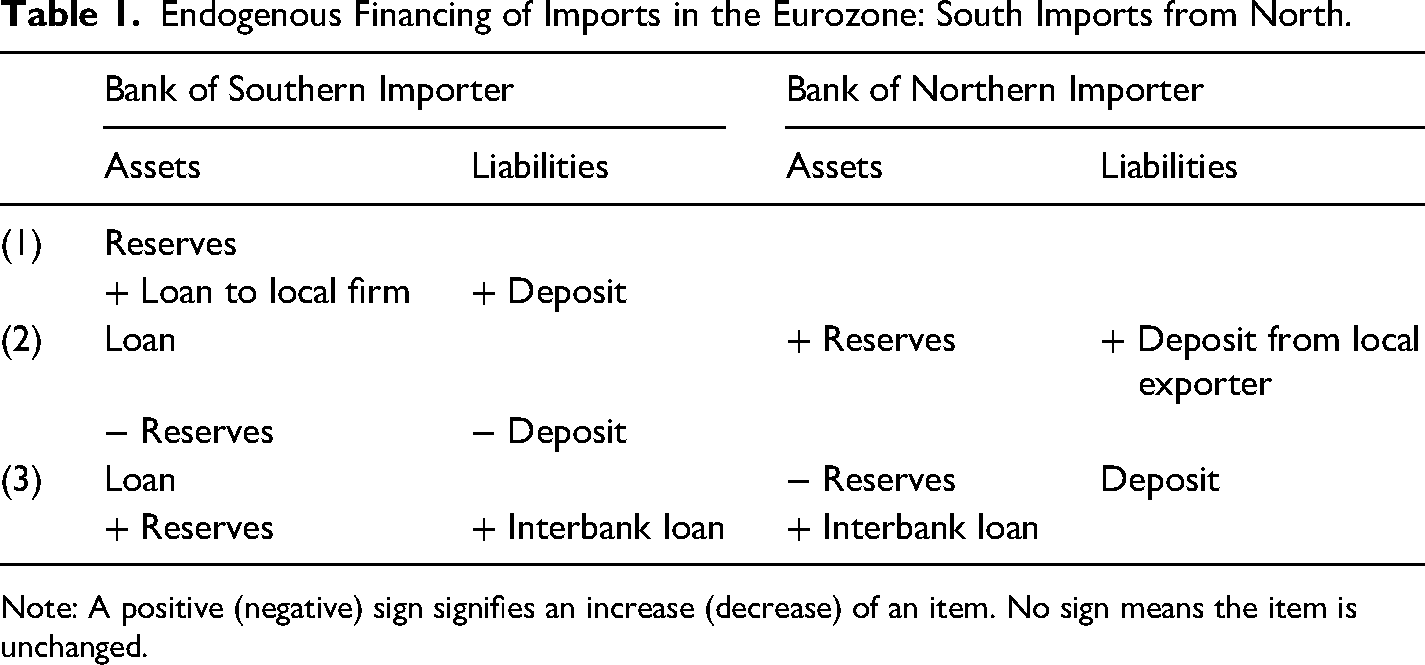

To clarify how trade flows drive net capital flows, consider how the principle of endogenous money plays out on the balance sheets of the trading partners’ commercial banks. Suppose a firm in a peripheral Eurozone country takes out a loan to finance the construction of new office buildings. The firm's bank correspondingly creates new euro deposits when making the loan (row 1 of Table 1). Importantly, when making the loan, the bank does not have to draw on any previously obtained liquid funds. It simply generates the deposit money that it lends to the borrower. In a second step, some of the deposits are used to import equipment from a firm located in the Eurozone's north (row 2). As a result, the southern bank loses some of its reserves with the national central bank, which end up in the reserve account of the northern bank. This is recorded as a net capital inflow for the southern country (see the online appendix for the corresponding BoP accounting). 31 To stay liquid and meet legal minimum reserve requirements, the southern bank will now want to replenish its reserves. There are several ways in which this can be accomplished, the most straightforward one being an interbank loan from the northern bank, which in turn is likely to want to get rid of its excess reserves (row 3). 32

Endogenous Financing of Imports in the Eurozone: South Imports from North.

Note: A positive (negative) sign signifies an increase (decrease) of an item. No sign means the item is unchanged.

The hypothetical example illustrates how the decision to import triggers an endogenous financing process that results in a net capital inflow for the importing country. In the PK monetary perspective, it is thus changes in the current account that drive changes of the financial account, not the other way around. Trade-related capital flows are demand-driven and therefore not causally prior to current account deficits. Importantly, this does not mean that the role of capital flows is confined to the accommodation of trade flows. As our analysis has shown, it is net capital flows that are related to trade. As will be discussed in more detail below, gross capital flows are a broader category that also entail pure financial flows that are unrelated to trade. Therefore, any analysis of capital flows must carefully distinguish gross financial flows from net capital flows that arise in the context of trade finance. Unfortunately, the popular “financial account drives current account” framing restricts the analysis of capital flows to trade-related net flows.

For the Eurozone, this means that the buildup of large current account deficits in countries such as Greece, Ireland, and Spain should not be understood as an outcome of the accumulation of surpluses in core countries such as Austria, Germany, and Finland. On the contrary, surpluses in the core, which translate into savings, were the result of rapidly increasing net imports of the periphery. To what extent this demand for imports was affected by gross capital flows will be discussed below. Before that, a second issue related to net flows and surpluses needs to be clarified.

Capital Flows and the Recycling of Surpluses

A concrete example of how loanable funds theory can lead to a misleading interpretation of empirical facts is the prominent metaphor of a “recycling of the surpluses.” 33 This is often used to identify the geographical direction of capital flows, specifically a “massive flow of funds from the surplus countries of northern Europe to the deficit countries of the European periphery.” 34 The recycling metaphor suggests that capital flows stem from surplus countries that invest their excess savings in foreign assets. Current account imbalances should thus be a strong indicator of the geographical direction of capital flows.

However, the recycling metaphor has theoretical and empirical weaknesses. On the theoretical side, it ignores that financial outflows are not constrained by the presence of excess saving or export surpluses. Balance-sheet accounting shows that it is entirely possible for a country to finance another country's current account deficit without having a surplus. 35 The recycling metaphor narrows the attention to flows from surplus into deficit countries, which can also lead to misleading implications on the empirical side. Alexandr Hobza and Stefan Zeugner show that prior to the GFC, France provided large flows to the southern European deficit countries despite having a roughly balanced current account—contrary to what the recycling metaphor suggests. 36 Moreover, the period before the GFC was characterized not only by flows into deficit countries but also by large flows into surplus countries. 37

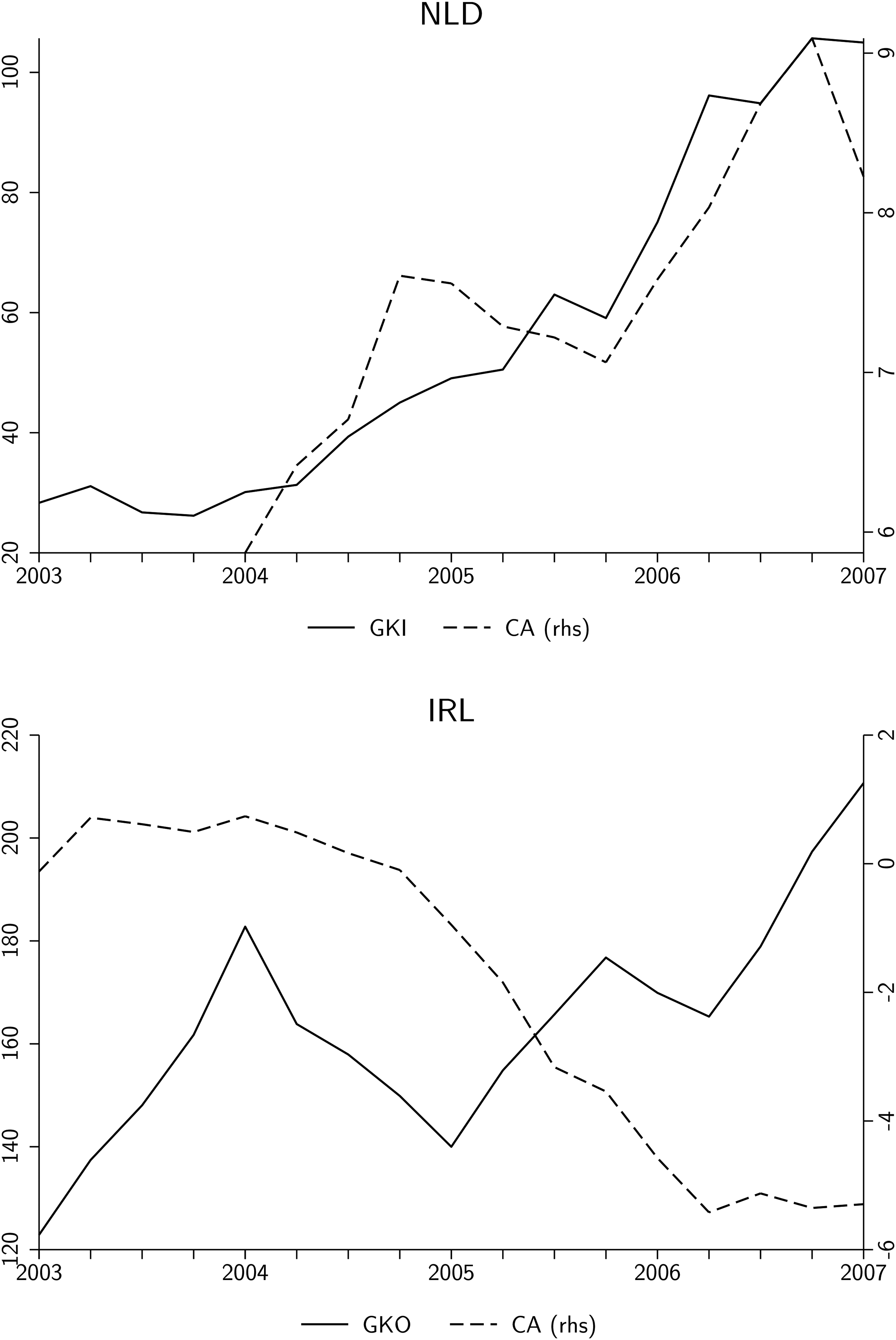

Figure 1 presents two cases that illustrate the independence of gross flows from the current account position. The upper panel shows that between 2004 and 2007, the Netherlands received a surge in gross inflows, which climbed from around 30 percent to more than 100 percent of GDP, while its current account surplus grew to a whopping 9 percent of GDP. The lower panel depicts the case of Ireland, whose gross outflows (as a percentage of GDP) increased by around 90 percentage points between 2003 and 2007, despite its current account balance deteriorating into a deficit of more than 5 percent of GDP.

Independence of gross flows from current accounts: the Netherlands and Ireland before the global financial crisis. Source: IMF-BOP, OECD; author's calculations. GKI: gross capital inflow (%GDP); GKO: gross capital outflow (%GDP); CA: current account (%GDP) (Y-axis on right-hand side). Gross flows are the sum of foreign direct investment, portfolio investment, and other investment. All variables are four-quarter moving sums.

Overall, both surplus (core) and deficit (peripheral) countries increased their foreign assets and liabilities in the pre-GFC period. Indeed, a substantial proportion of gross inflows into the periphery was neither used to finance net imports nor to sit on excess reserves, but to finance foreign investments into risky portfolio assets (see Figure A1 in the online appendix). 38 The “recycling of surpluses” metaphor is not helpful for understanding these patterns of cross-border financial integration.

On Gross Capital Flows and Asymmetric Booms in the Eurozone

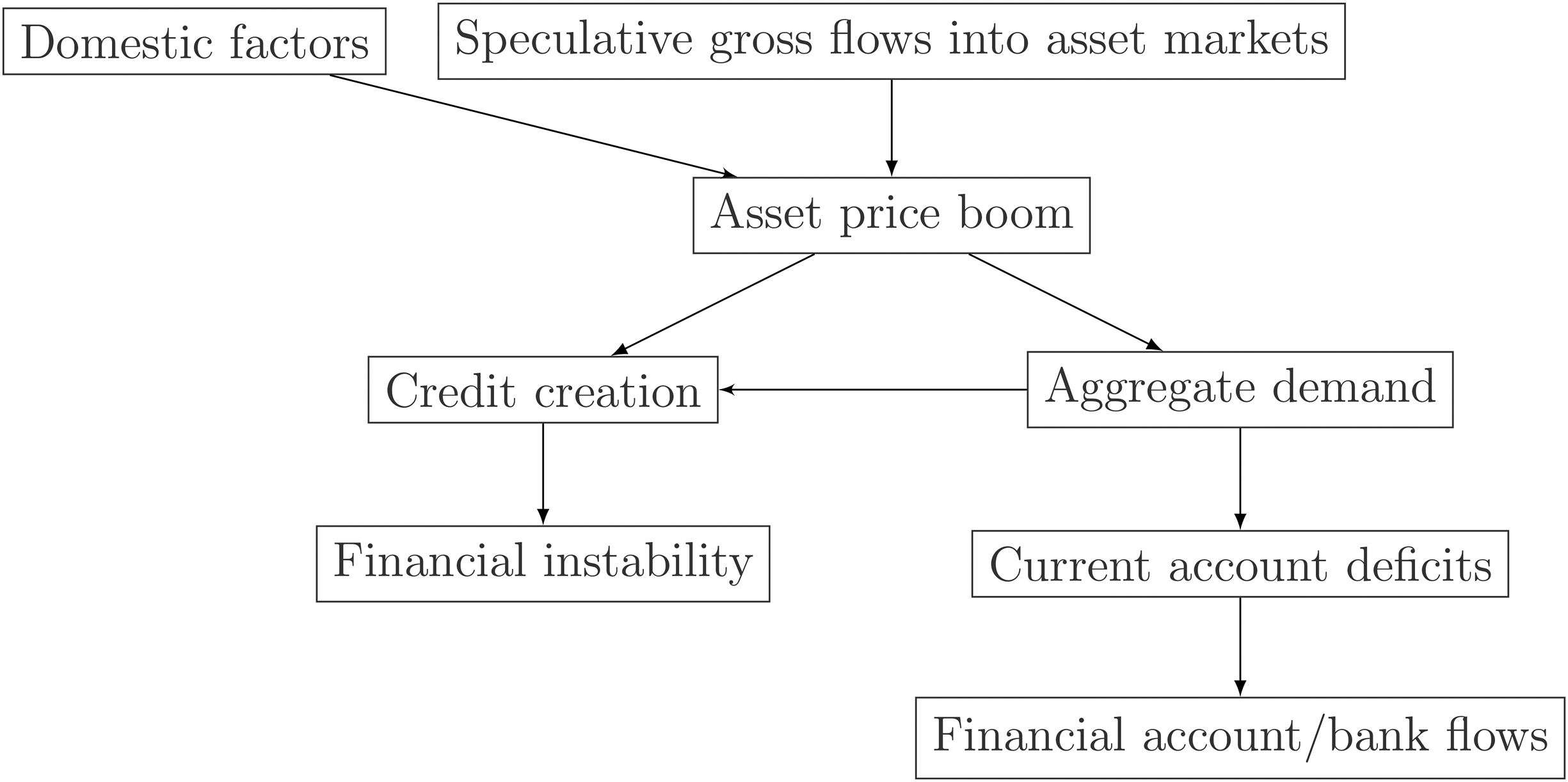

The previous section provides support for the point made by Sofia A. Pérez that “capital flows can be motivated quite independently of activity captured in the current account.” 39 A focus on such gross financial flows that are independent from trade should indeed be key to a finance-centric narrative. How such pure financial flows affect financial instability during boom periods requires clarification, however. For example, Torben Iversen, David Soskice, and David Hope express a widely held view that “the flow of capital from north to south increased the growth rate in the south and put upward pressure on southern inflation,” 40 but offer little discussion of the underlying mechanisms. This section discusses two channels through which different types of gross capital flows may contribute to the buildup of imbalances through booms that are asymmetric across north and south.

Interbank Flows and Domestic Lending

A first channel that is frequently discussed in finance-centric narratives is that interbank flows into the periphery would stimulate domestic credit booms. The underlying assumption is that these interbank flows provided domestic banks with additional liquidity, which induced them to increase lending to local borrowers, for example, in the form of mortgage credit. The increase in domestic credit would then boost demand (and inflation) and lead to current account deficits. 41

Indeed, Pérez identifies a “sharp rise in cross-border interbank flows as a cause—and not just a consequence—of Eurozone current account imbalances.” 42 Lucia Quaglia and Sebastián Royo argue that Spanish banks “borrowed on the interbank market and channelled this funding into the construction sector . . . sustaining a massive construction boom.” 43 Fuller emphasizes the sale of assets by southern banks that gave them a “boost in terms of loanable funds . . . which they would then lend to individuals and businesses.” 44

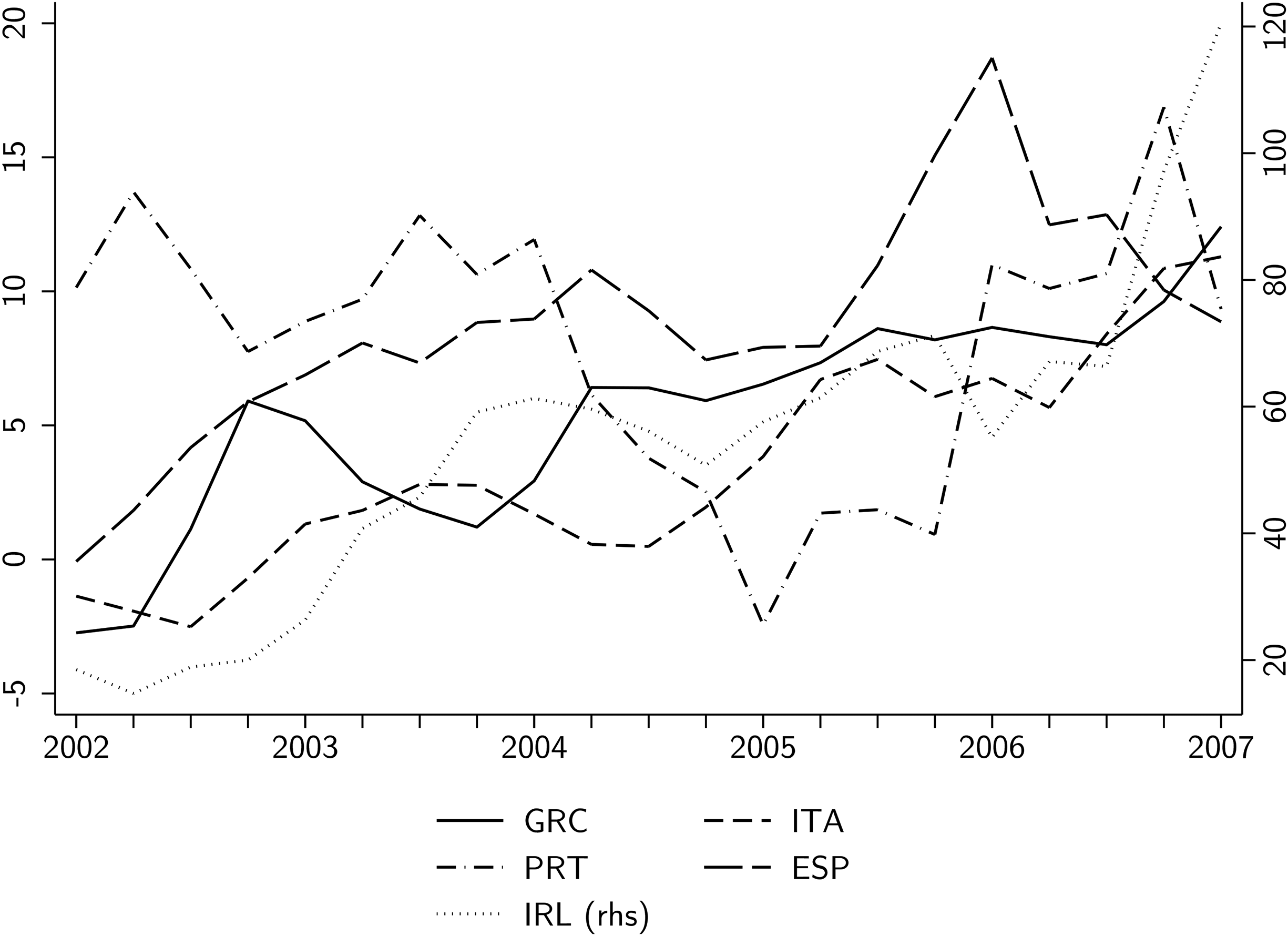

Figure 2 displays gross capital inflows into peripheral banking sectors before the GFC. Bank inflows indeed increased for all peripheral countries (except Portugal) in this period. This pattern is especially pronounced for Ireland and Spain, where inflows relative to GDP went up by as much as 100 and 20 percentage points, respectively.

Rising gross inflows into peripheral banking sectors before the global financial crisis. Note: Gross bank inflows are the sum of portfolio debt and other investment debt into the private banking sector (%GDP) and transformed into four-quarter moving sums. Y-axis for Ireland on the right-hand side. Data sources: Stefan Avdjiev, Bryan Hardy, Sebnem Kalemli-Özcan, and Luis Servén, “Gross Capital Flows by Banks, Corporates and Sovereigns,” Journal of the European Economic Association 20, no. 5 (2022): 2098–135; OECD (author's calculations).

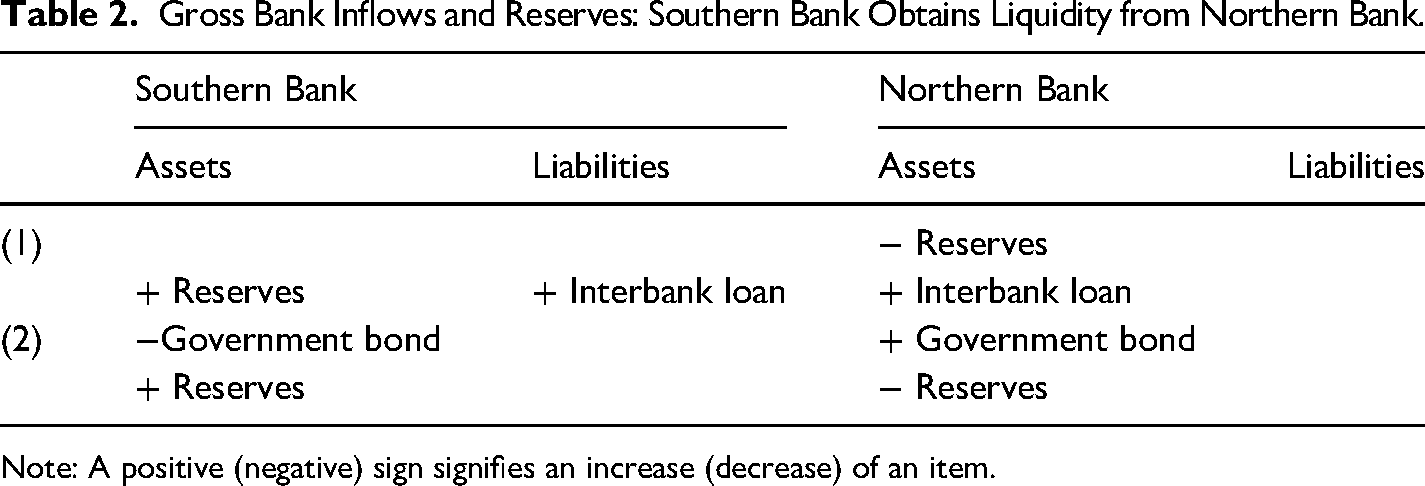

How would those inflows induce banks to increase domestic lending? Table 2 examines the proposed mechanism from a balance-sheet accounting perspective. Row 1 depicts the case where a southern bank takes out an interbank loan from a northern bank. Unlike in the example discussed in Table 1, this inflow does not compensate a prior loss in reserves due to the financing of imports. As a result, reserves held with the national central bank increase and the bank ends up in more liquid position. In the BoP, this leads to a simultaneous increase in gross capital inflows and gross capital outflows (see the online appendix).

Gross Bank Inflows and Reserves: Southern Bank Obtains Liquidity from Northern Bank.

Note: A positive (negative) sign signifies an increase (decrease) of an item.

Can such a pure financial flow, which leaves the financial account unchanged but increases bank liquidity, cause a domestic credit boom? Indeed, sufficient liquidity is a precondition for commercial banks to operate. It is also conceivable that the increased availability of liquidity via the European interbank market after the introduction of the euro created an optimistic environment that induced some banks to relax lending standards. In this way, bank flows may have contributed to domestic credit booms. However, the theoretical case for an independent causal role for such bank flows is much less straightforward than suggested by the proponents of the argument. In particular, it is misleading to suggest that intra-Eurozone bank flows automatically led to credit creation. A number of factors need to be considered that limit the explanatory power of bank flows for credit booms.

First, banks cannot lend out reserves to nonbanks. 45 This is a basic institutional feature of monetary systems in which only commercial banks hold reserve accounts with the central bank, while nonbank actors hold deposit accounts with commercial banks. To lend money to a nonbank, a commercial bank must credit the corresponding deposit account of the nonbank by making new money rather than transferring existing reserves to the borrower (as in row 1 of Table 1). As a result, increases in reserves do not automatically translate into more credit. Second, while additional liquidity could motivate banks to lower lending standards, liquidity as such does not mitigate the solvency risk that comes with the extension of credit to borrowers that were previously not considered creditworthy. A bank suffering from nonperforming loans needs equity to absorb any losses from borrowers that are unable to service their debts, not liquidity (reserves). Therefore, any effects from additional liquidity on lending standards are likely to be limited, unless solvency risk also changes. Changes in solvency risk could come about by rising collateral values, for example, in the case of house price inflation, but this channel is distinct from bank liquidity (and will be discussed below).

Third, the excess-liquidity argument overlooks that there was also ample liquidity in surplus countries like Germany, where it did not cause credit booms. Why did highly liquid core banks invest abroad rather than lend domestically? More generally, all commercial banks in the Eurozone with adequate collateral can access liquidity from their national central banks if need be, but this does not always lead to credit booms. This raises the question whether access to liquidity really was the limiting factor on bank lending during the pre-GFC boom period. Fourth, from a PK monetary perspective, a key constraint on credit creation by commercial banks is creditworthy demand for loans by households and firms. However, bank inflows do not alter credit demand, nor do they influence the creditworthiness of potential borrowers. To put it plainly, Eurozone banks do not need funds from abroad to increase lending, they need creditworthy customers.

In addition to these points, it must be noted that a large part of bank inflows are simply an outcome of the refinancing decisions of domestic banks. As shown in rows 2 and 3 of Table 1, whenever a domestic customer transfers bank deposits abroad by purchasing a foreign good or asset, the domestic bank will lose reserves and is likely to borrow them back from a foreign bank. Correspondingly, Eladio Febrero, Ignacio Álvarez, and Jorge Uxó have argued that the inflows into the Spanish banking system during the pre-GFC boom were largely driven by the current account deficit and foreign direct investment made by Spanish residents due to which domestic banks lost reserves. In their view, bank inflows were thus a consequence, not a cause of the boom. 46

In sum, an argument whereby intra-Eurozone interbank flows mechanically drove credit creation in the periphery is consistent with a neoclassical framework in which banks intermediate loanable funds. However, from a PK monetary perspective, interbank flows at best contributed but are unlikely to have been the sole cause for booms of the magnitude seen in Ireland and Spain prior to the GFC. In particular, bank inflows do not automatically translate into more domestic lending as suggested in parts of the literature. The bank-liquidity channel is thus an incomplete explanation from a PK perspective. 47 A more complete explanation of asymmetric credit booms must go beyond bank liquidity.

Portfolio and FDI Flows and Asset Prices

A second channel directs attention to capital flows as drivers of asset price dynamics. As discussed above, asset prices play a key role in a PK theory of financial fragility. Unlike loans whose prices (i.e., interest rates) are relatively rigid, trading of securities such as bonds as well as real estate comes with rapid price adjustment. Foreigners deciding to buy or sell domestic assets can thus easily impact price dynamics. Changes in asset prices can then influence credit demand and supply. This yields a more direct channel through which capital flows can impact asymmetric booms. It requires a shift in focus from interbank flows to portfolio and FDI flows into asset markets.

To examine this channel in more detail, consider now row 2 of Table 2, in which the southern bank sells a government bond to a northern bank. This transaction not only increases bank liquidity but also impacts financial markets. The decision by the northern bank to buy southern government bonds on the secondary market may push up bond prices and depress yields. Speculative behavior, whereby investors bet on further price increases, may reinforce such dynamics for a while. Lower yields may then stimulate aggregate demand and private borrowing insofar as they act as reference rates in private credit contracts, for example, for mortgage loans. 48 In addition, rising asset prices also improve collateral values of borrowers, for example, real estate, which reduces solvency risk and may thus relax credit constraints. The increase in economic activity then leads to increased net imports, which draws in net capital inflows via interbank lending as discussed above. The mechanism is summarized in Figure 3.

Capital flows in a post-Keynesian view of unstable financial booms in the Eurozone's periphery.

With respect to the Eurozone, some proponents of the finance-centric narrative have identified falling interest rates due to capital inflows as one of the drivers of credit booms in the periphery. 49 Indeed, there is statistical evidence that portfolio bond inflows can reduce long-term yields. 50 However, to what extent capital inflows were relevant in influencing yields in the Eurozone's periphery and whether this, in turn, had any effects on domestic lending is an empirical question that is rarely discussed. In the Eurozone, yields on ten-year government bonds had effectively converged by the time the euro was introduced in 1999. 51 Interest-rate convergence was also part of the Maastricht criteria. Such a uniform behavior of long-term rates does not fit a story where massive capital flows into the south after the introduction of the euro drove down relative borrowing cost.

A related question is by how much long-term yields impact credit conditions for private borrowers. Consider the example of Spain and Ireland, the two peripheral countries with the most spectacular housing booms prior to the GFC. In these countries, mortgage interest rates declined between 2001 and 2004, which arguably contributed to the mortgage-financed boom. A statistical exercise documented in the online appendix suggests that only 7 percent (Spain) and 3 percent (Ireland) of that fall in mortgage rates can be explained by falling yields. By contrast, 73 percent and 93 percent is explained by a reduction in the policy rate by the ECB. This result makes it difficult to attribute favorable borrowing costs to an asymmetric shock in portfolio bond inflows that drove down yields. A more plausible explanation relates to the ECB's expansionary one-size-fits-all monetary policy after the introduction of the euro in conjunction with specific national institutions. The level of Spanish and Irish mortgage rates was 2 to 3 percentage points lower than those in core countries at the time, 52 and there is empirical evidence that this mortgage rate gap is related to differences in institutions such as credit enforcement procedures, maximum loan-to-value ratios, and variable-rate mortgages. 53

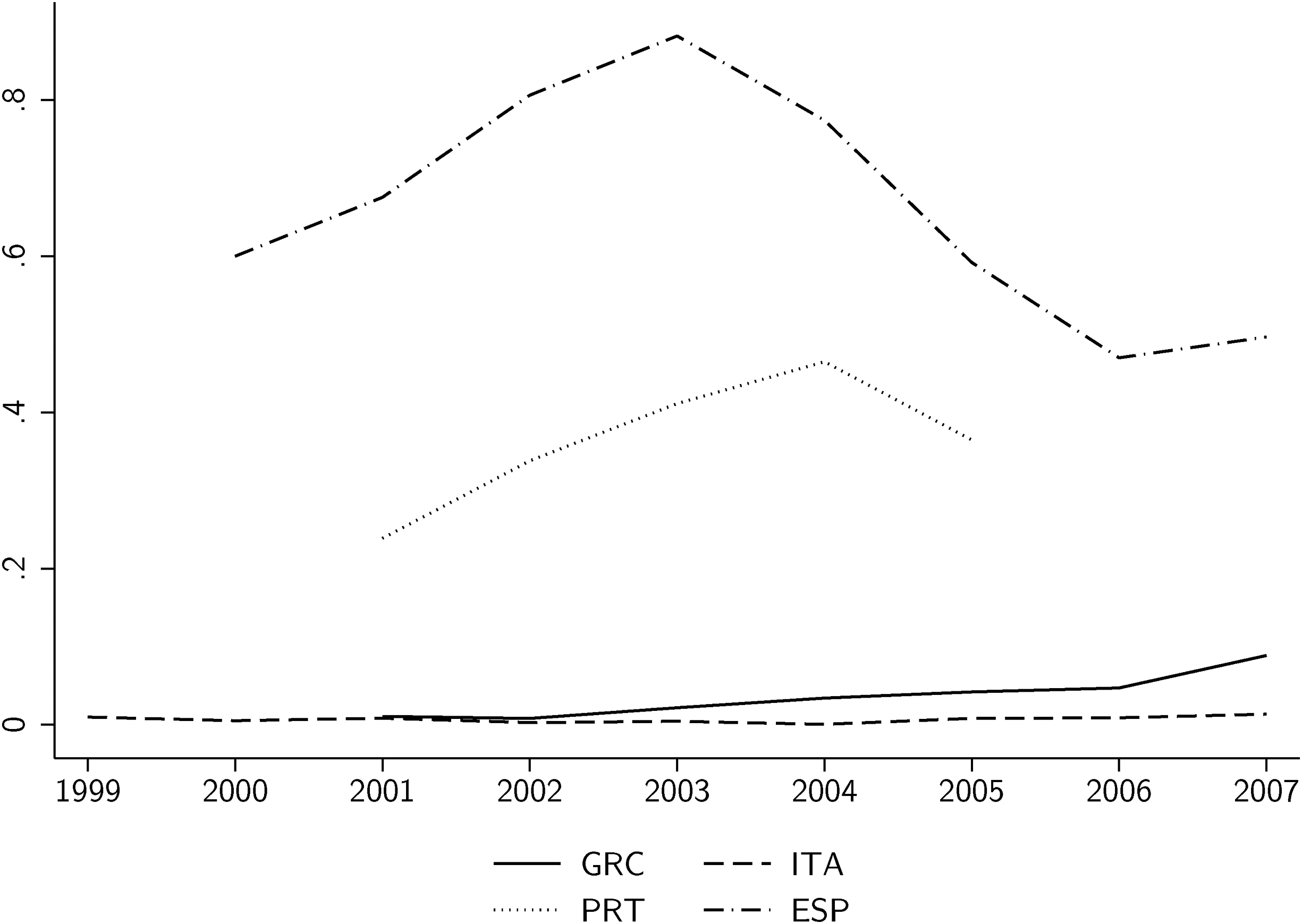

A key asset other than bonds that may be affected by capital flows is real estate. Foreign property investors may drive up local house prices, which can trigger expectations of sustained price growth and thereby stimulate housing booms. 54 Figure 4 displays private FDI in real estate (as a percentage of GDP) for the GIPS countries during the pre-crisis boom. It can be seen that compared to other countries Spain experienced rising inflows during its housing bubble in the early 2000s. Juan Rafael Ruiz and Oana Andreea Cristian argue that reforms such as a new Land Act together with income tax deductions triggered the Spanish housing boom. 55 Foreign residential investors, especially related to tourism, added to the surging demand for houses (by up to 12 percent of total demand in 2002) as they expected to benefit from capital gains. 56 FDI inflows were certainly not the only cause of peripheral housing booms. Fuller shows that Ireland and Spain had comparatively strong credit-encouraging institutions in the form of low taxes on housing transactions and the existence of secondary mortgage markets. 57 Sebastian Kohl and Alexander Spielau more generally characterize southern Europe (except Italy) as construction boom regimes with liberal or lax land regulations. 58

Foreign direct investment inflows into peripheral real estate before the global financial crisis. Note: Gross private inward foreign direct investment into domestic real estate (%GDP). No data for Ireland. Values of zero at the sample start for Portugal were dropped. Data sources: OECD, World Bank (author's calculations).

In sum, PK monetary theory highlights asset price dynamics as key drivers of financial instability. Asset prices influence the wealth of borrowers and lenders, and can thereby stimulate spending and borrowing. At the same time, they are a relatively independent causal factor as they are partly driven by the speculative behavior of investors. With respect to capital flows, this means that flows into asset markets may drive or amplify booms that are asymmetric across countries. Compared to bank flows, which are to a large extent an outcome of trade flows and the refinancing decisions of domestic banks, portfolio and FDI flows have a greater idiosyncratic component that can be unrelated to domestic macroeconomic factors and stem from the risk appetite of foreign investors. However, financial and housing institutions such as the size of the private housing market, capital gains taxes, and maximum loan-to-value ratios will impact how easily speculative dynamics emerge. In the Eurozone, flows into real estate may have added to housing booms in the periphery, but should be analyzed in conjunction with such country-specific factors.

On Gross Capital Flows and Crises in the Eurozone

A final issue that requires clarification is the role of capital flows in crises. Here, the 2010–12 EZC during which government bond yields of the Eurozone's periphery surged is a key episode of interest. According to a “consensus narrative” advanced by mainstream economists, the EZC should be understood as a BoP crisis. 59 This view has been adopted in several contributions by CPE scholars. 60 The BoP-crisis narrative characterizes the EZC as a sudden stop of capital inflows, specifically into the banking sector, that were needed to finance current account deficits in the periphery. As a result, current accounts were forced to rebalance. This section critically examines the BoP-crisis narrative and proposes an alternative explanation that highlights the role of speculative gross flows in government bond markets.

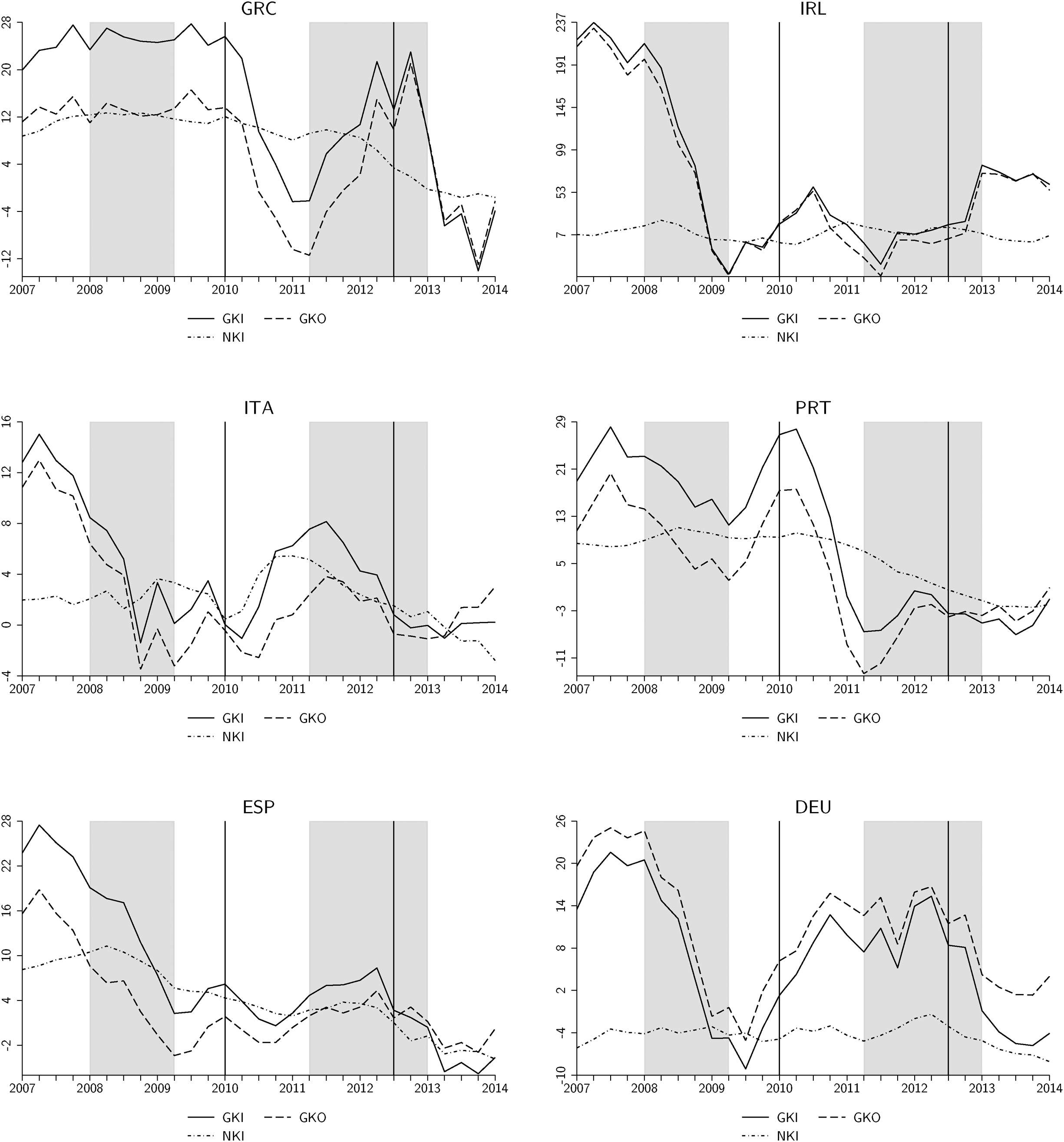

From a PK monetary perspective, the problem with the BoP-crisis view is that it focuses on the wrong type of capital flows. First, consider the distinction between net and gross capital flows as introduced above. While the literature is often ambiguous about this, the narrative of a BoP crisis that led to a drying-up of funds to sustain trade deficits would suggest a sudden stop in net capital flows. Figure 5 displays gross capital inflows and outflows as well as net flows for the GIIPS (Greece, Ireland, Italy, Portugal, and Spain) and Germany, for comparison. It can be seen that net flows did not change violently during the EZC (whose beginning and end are marked by vertical bars). Instead, most GIIPS already reduced their net inflows gradually since the 2008 GFC, especially Greece, Portugal, and Spain. Indeed, the economic contraction triggered by the GFC induced a slow reduction in current account deficits, which is reflected in declining net flows. Recessions are typically characterized by an improvement in current accounts due to a decline in import demand. In 2012–13, net inflows decreased somewhat faster in some of the peripheral countries, but the same happened in Germany. Indeed, at this time there was a general recession in the Eurozone (marked by the gray-shaded areas). Overall, Figure 5 does not support a story of an abrupt reduction in current account deficits during the EZC due to a sudden stop in net flows.

Gross versus net capital flows during the global financial and Eurozone crisis. Note: GKI: gross capital inflow (%GDP); GKO: gross capital outflow (%GDP); NKI: net capital inflow (gross inflows minus outflows) (%GDP). Gross flows are the sum of foreign direct investment, portfolio investment, and other investment. All variables are four-quarter moving sums. Gray-shaded areas mark Eurozone-wide recessions. Vertical bars mark the beginning and the end of the Eurozone crisis (divergence in government bond yields). Data sources: IMF-BOP, OECD (author's calculations).

Much more interesting are the gross flows dynamics, which are substantially more volatile than net flows. For many countries (Ireland, Italy, Spain, and Germany), the largest breakdown in gross flows happened during the GFC, not the EZC. Only Greece and Portugal underwent gross sudden stops during the EZC. A closer look reveals that the drastic reduction in gross inflows was often completely matched by a reduction in outflows, whereas net flows only declined slowly. If there was a sudden stop, it was in gross flows, not net flows.

Second, it is necessary to further separate gross flows into bank flows and portfolio flows. In the finance-centric narrative, the collapse in interbank flows to peripheral countries during the EZC has received much attention. Indeed, there was a gross sudden stop in private bank flows, reflecting a loss of confidence in peripheral banks that had experienced solvency problems since the GFC. 61 However, it has been well documented that this breakdown of the private interbank market was compensated by liquidity provision from national central banks of the Eurosystem. This was reflected in the much discussed TARGET2 imbalances, which are claims between the national central banks of the Eurosystem that arise when countries undergo sustained net outflows of bank reserves. 62

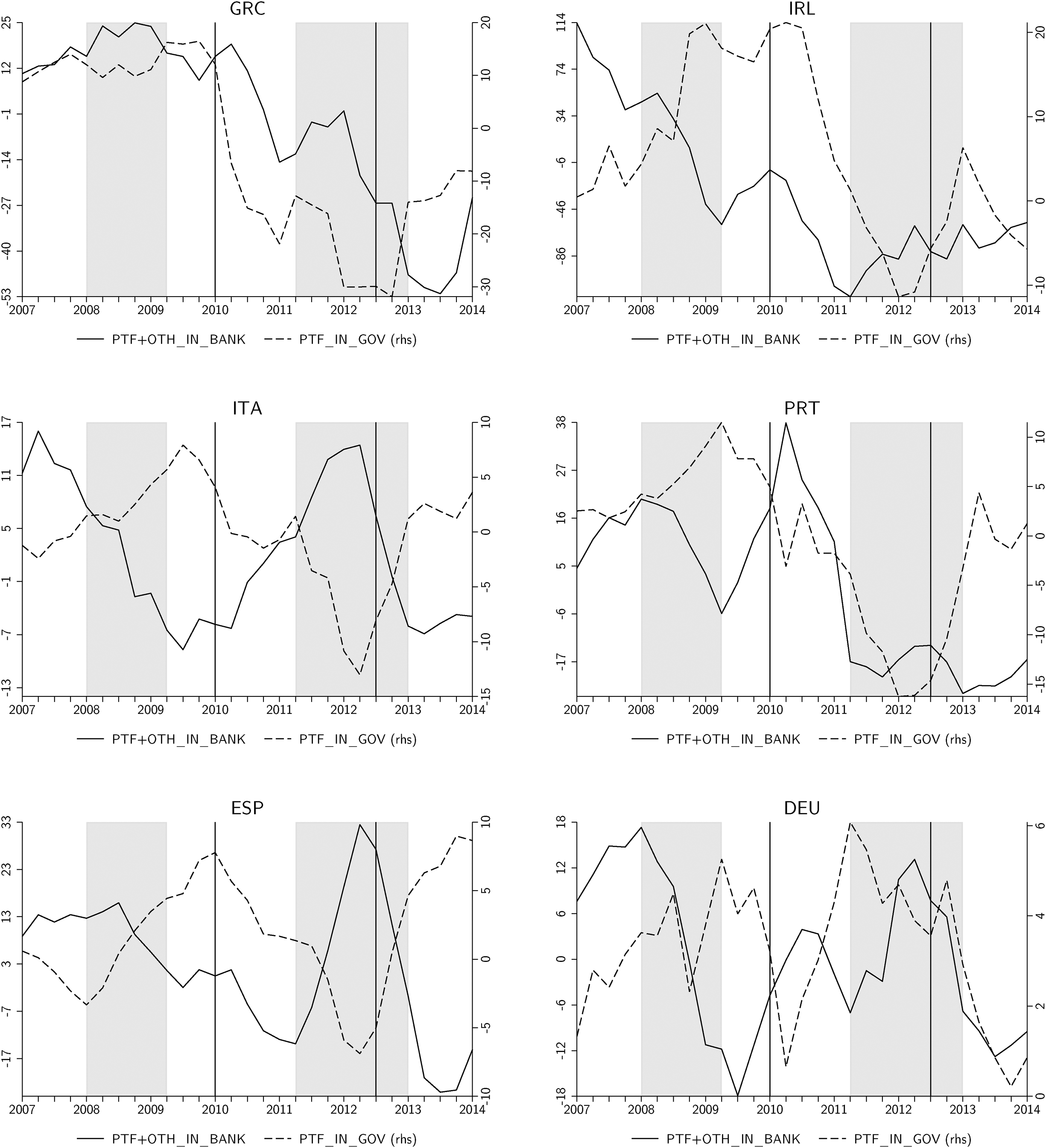

To assess the dynamics of bank liquidity, consider the solid lines in Figure 6, which display gross inflows into the banking sector during the GFC and EZC, covering portfolio and other investment debt inflows (mostly loans and deposits) into both private banks and national central banks (i.e., including net changes in TARGET2 balances). They reveal that flows into the banking system as a whole, that is, including national central banks, collapsed for all countries already during the 2008 GFC (except for Greece). The dynamics during the 2010–12 EZC were more varied: while there was a collapse for Greece and Portugal, total bank flows for Spain and Italy increased (likely due to central bank liquidity). Ireland's bank flows decreased further in the first years of the EZC, but their overall trajectory in this period is shaped by the GFC, after which Irish banks embarked on a process of deleveraging.

Total bank inflows versus government debt inflows during the global financial and Eurozone crisis. Note: PTF + OTH_IN_BANK: sum of gross portfolio debt and other investment debt inflows into the private banking sector and the national central bank (%GDP); PTF_IN_GOV: gross portfolio debt inflows into the government sector (%GDP) (four-quarter moving sums). Gray-shaded areas mark Eurozone-wide recessions. Vertical bars mark the beginning and the end of the Eurozone crisis (divergence in government bond yields). Data sources: Avdjiev et al., “Gross Capital Flows by Banks”; OECD (author's calculations).

Figure 6 thus suggests that the availability of central bank liquidity partly compensated for the decline in private bank flows in several countries. While the sudden stop in private bank flows certainly added to the disruption in peripheral banking sectors after the GFC, especially in Greece and Portugal, it cannot by itself explain the explosion in peripheral government bond yields that was at the heart of the EZC. Extending the PK perspective to the role of capital flows in crises again requires supplementing the focus on bank flows by a consideration of asset markets.

To this end, the dashed lines in Figure 6 display gross portfolio debt inflows into the government sector (mostly government bonds), which declined severely and became negative for all GIIPS in 2012. This is consistent with the view that the EZC was essentially a speculative attack on peripheral government bonds, 63 and Figure 6 reveals that this was partly driven by foreign investors, that is, capital flows. Speculation started with Greek bonds after the upward revision of previously forged budget deficit figures. The sell-off of government bonds in secondary markets led to a collapse in bond prices and an explosion of yields. As emphasized in Minskyan theory, once speculative dynamics are in motion, they are hard to stop due to herd behavior. This can render speculation quite detached from economic “fundamentals.” Indeed, speculation soon spilled over into the government bond markets of Ireland, Portugal, and eventually all peripheral Eurozone members. Paul De Grauwe and Yuemei Ji present empirical evidence that a large portion of the rise in peripheral spreads was disconnected from macroeconomic factors. 64 However, accumulated current account deficits became positively correlated with yields after 2008, suggesting that the redenomination risk associated with large net external debt burdens may have informed the choice of foreign investors which Eurozone countries to attack. 65

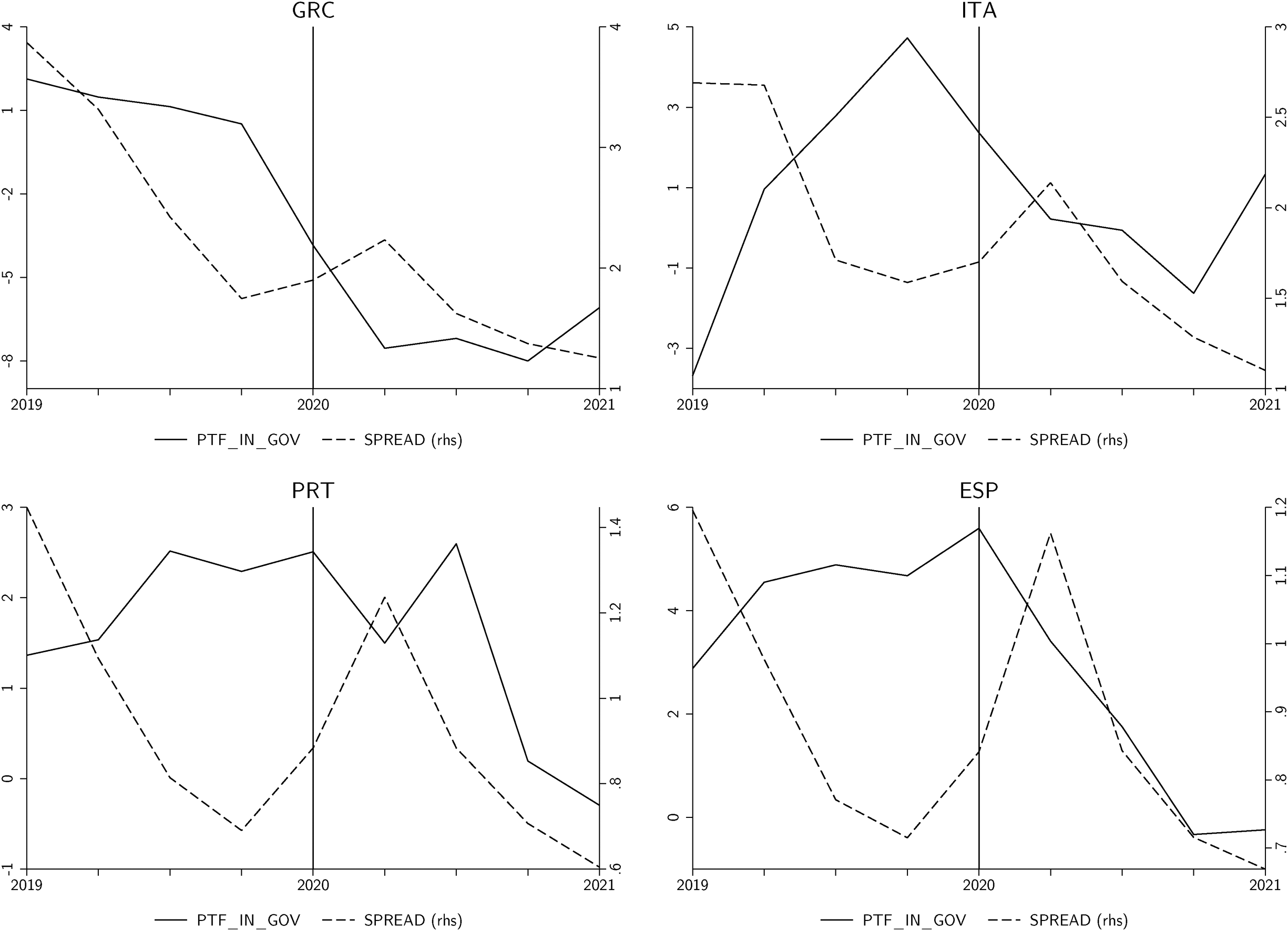

The continued relevance of such speculative portfolio flows for the Eurozone's north-south divide could again be observed during the outbreak of the Covid-19 pandemic. Despite a massive rebalancing of current accounts and a recapitalization of banks, Greece, Italy, Portugal, and Spain once again underwent rising yields in early 2020. Spreads of the latter two rose by, respectively, 44 percent and 38 percent between the last quarter of 2019 and the second quarter of 2020. Figure 7 suggests that speculative portfolio flows again contributed to these dynamics, illustrating the south's continued exposure to speculative attacks.

Government debt flows and peripheral spreads during the outbreak of the Covid-19 pandemic. Note: PTF_IN_GOV: gross portfolio debt inflows into the government sector (%GDP) (four-quarter moving sum); SPREAD: difference in ten-year government bond yields with respect to Germany. The vertical bars mark the Covid-19 outbreak in Europe in 2020 Q1. Data sources: IMF-BOP, OECD (author's calculations).

To conclude, while the EZC certainly involved a disruptive breakdown of private bank flows, it should not be regarded as a BoP crisis. As pointed out by Marc Lavoie and other PK economists, classic BoP crises cannot occur in the Eurozone as long as national central banks provide liquidity that can be used to finance intra-Eurozone current account deficits. 66 The BoP-crisis narrative distracts from the critical role of portfolio flows out of government bond markets that contributed to rising spreads on peripheral government bonds. The PK view highlights the special role of secondary markets for financial assets, where rapid price adjustment can invite speculative behavior. Such speculative portfolio flows can be entirely independent from flows related to the financing of current account deficits.

Concluding Discussion: Implications for Comparative Political Economy and Economic Policy

The article's main argument can be summarized as follows. Finance-centric narratives of macroeconomic divergence in the Eurozone rightly emphasize financial instability in the periphery's private sectors. 67 However, some of the arguments related to capital flows implicitly build on neoclassical loanable funds theory in which credit is driven by saving. The loanable funds approach not only entails a theoretically flawed description of the workings of money and finance, it can also mislead regarding the sources of financial instability. With respect to capital flows, it places too much emphasis on net flows and on interbank flows from surplus countries in the Eurozone. By contrast, the alternative post-Keynesian monetary perspective put forward in this article directs attention to gross financial flows into asset markets. Specifically, it was argued that net flows are mostly an outcome of trade flows, and that bank flows alone are an insufficient cause of unstable financial dynamics in the periphery. By contrast, speculative gross capital flows into real estate and government bond markets impact asset prices and can thus change both credit constraints and credit demand, constituting a channel through which capital flows can directly contribute to boom-bust cycle dynamics. For the Eurozone's north-south divide, capital flows have been most relevant in the form of speculative sales of peripheral bonds by foreign investors during the Eurozone crisis and the outbreak of the Covid-19 pandemic. If government bonds yields are exclusively determined by financial markets, peripheral countries will remain at risk of speculative attacks.

What are the implications for CPE and European economic policy? First, comparative political economists interested in financial instability should abandon the fixation on current accounts suggested by loanable funds theory. While current account balances can be interesting for cross-country analysis, they are poor indicators for countries’ gross international financial integration and underlying financial vulnerabilities. 68 With respect to economic policy, this means that efforts to rebalance current accounts are insufficient to address the Eurozone's north-south divide. Austerity policies imposed after the crisis have certainly helped reduce peripheral current account deficits, but this has not made these countries less vulnerable to financial instability. Take the example of Italy, which has run current account surpluses since 2011 but failed to escape a series of bank failures and speculative attacks on government bonds in 2020 and 2022.

A monetary perspective instead draws attention to cross-country differences in the size and risk appetite of domestic financial systems as a source for financial instability. 69 This calls for financial regulation beyond the current supervisory and resolution mechanisms of the European Banking Union. Dirk Bezemer, Josh Ryan-Collins, Frank van Lerven, and Lu Zhang discuss policies such as credit ceilings, credit quotas, and credit-directing policies that serve to limit loan creation and channel it into productive as opposed to speculative activities. 70 For example, maximum loan-to-value and loan-to-income ratios are macroprudential policy tools that are now implemented by many countries to regulate mortgage markets. Notably, they are still absent in peripheral countries such as Spain, Greece, and Italy. 71

Second, more attention should be dedicated to speculative gross flows into asset markets as opposed to trade-related flows. An important question for CPE is why peripheral countries are more prone to speculative asset price dynamics. For example, housing institutions such as a large private market relative to public housing as well as weak tenant protection legislation and nonexistent capital gains taxes on property may render some property markets more attractive to foreign speculators. Similarly, institutional factors such as the share of government bonds held by foreign institutional investors may influence how susceptible countries are to speculative attacks. 72 With respect to policy, our argument suggests that residence-specific taxes on housing transactions could make peripheral housing markets more resilient to capital flows. Countries such as Australia and Canada recently introduced fees for nonresident buyers, whereas Portugal went in the opposite direction by introducing a new tax regime in 2009 that attracts nonresidents into the housing market. 73

Third, the article underlines the crucial role of central banks in preventing speculative attacks in government bond markets. 74 It shows that these episodes are often driven by foreign investors. During the Eurozone crisis, it took two years of havoc in bond markets until the ECB eventually committed “to do whatever it takes,” thereby clearing doubts about the solvency of peripheral governments. In spring 2020, European monetary authorities responded much more decisively to rising spreads with the pandemic emergency purchase program (PEPP). 75 However, the ECB's president Christine Lagarde initially deemed it necessary to remind investors that “we’re not here to close spreads.” The ECB's collateral policies also still entail a disciplinary element that discriminates between securities of different ratings, which can amplify falls in government bond prices if peripheral bonds get downgraded. 76 For political economists, this raises the question of what political factors induce central banks to shield governments from speculative attacks. 77 For economic policy, the argument suggests that the ECB needs to unambiguously guarantee the fiscal solvency of the Eurozone's members—similar to other central banks like the Bank of England and Federal Reserve. While some economists have proposed to use the terms under which the ECB lends against collateral to impose fiscal discipline on member states, the argument put forth in this article suggests the opposite. Given the unstable nature of bond markets, the ECB should backstop government bonds by accepting them unconditionally as collateral for bank lending to reduce the risk of speculative attacks. 78

Finally, a finance-centric narrative of the Eurozone's north-south divide must not lose track of domestic factors. Post-Keynesian theory highlights the existence of country-specific financial cycles in house prices and private debt. 79 These domestic financial cycles can be quite independent from capital flows. 80 While their expansion phase may pull in capital flows, those flows are unlikely to be the sole driver of financial cycles. An understanding of why these cycles are often more pronounced in the Eurozone's periphery will require further comparative analyses of domestic housing and financial institutions. 81

Supplemental Material

sj-pdf-1-pas-10.1177_00323292231168251 - Supplemental material for Capital Flows and the Eurozone's North-South Divide

Supplemental material, sj-pdf-1-pas-10.1177_00323292231168251 for Capital Flows and the Eurozone's North-South Divide by Karsten Kohler in Politics & Society

Footnotes

Acknowledgments

I am grateful to the editorial board of Politics & Society, the coordinating editor Fred Block, and Guendalina Anzolin, Lucio Baccaro, Rob Calvert Jump, Alex Guschanski, Philipp Heimberger, Ian Lovering, Pedro Perfeita da Silva, Inga Rademacher, Engelbert Stockhammer, Ben Tippet, and Rafael Wildauer for helpful comments. All errors are mine.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Leverhulme Trust under Grant RPG-2021-045 (“The Political Economy of Growth Models in an Age of Stagnation”).

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.