Abstract

Contemporary capitalist societies use different institutions to manage economic risks. While different public welfare state and financial institutions (banks, capital markets) have been studied across coordinated and liberal market economies, the different worlds of private insurance institutions have been understudied. Building on new insurance data sets (1880–2017), we find that countries with a Maritime (USA, GBR, CAN) in contrast to the more backward Alpine (AUT, DEU, CHE) insurance tradition developed bigger life and nonlife insurance earlier, with less state-associated and reinsurance enterprises, but riskier investments steered toward financial markets. We argue that the larger and more “Maritime” the insurance sector, the more it made welfare states liberal and securities markets large. Insurance is thus a hidden factor for countries’ varieties of capitalism and worlds of welfare. The recent convergence on the Maritime model, however, implies that the riskier and risk-individualizing type of private insurance has added to privatization and securitization trends everywhere.

Societies insure themselves against economic risks through different institutions. They offload risks onto collective welfare institutions, motivate private household savings, or incentivize homeownership. Business risks in turn can be borne by banks or capital markets. Liberal market economies (LMEs) such as that in the United States have been known to rely less on collective welfare arrangements and more on private savings and homeownership for households as well as capital-market risk-bearing for businesses. This implies a security arrangement with more individual risk-bearing and more exposure to short-term volatilities. Coordinated market economies (CMEs) like Germany are known for more collective welfare arrangements, savings through cooperative or public institutions and less homeownership as well as bank-based business finance. This implies a security arrangement with more solidaristic risk-sharing and a long-term orientation.

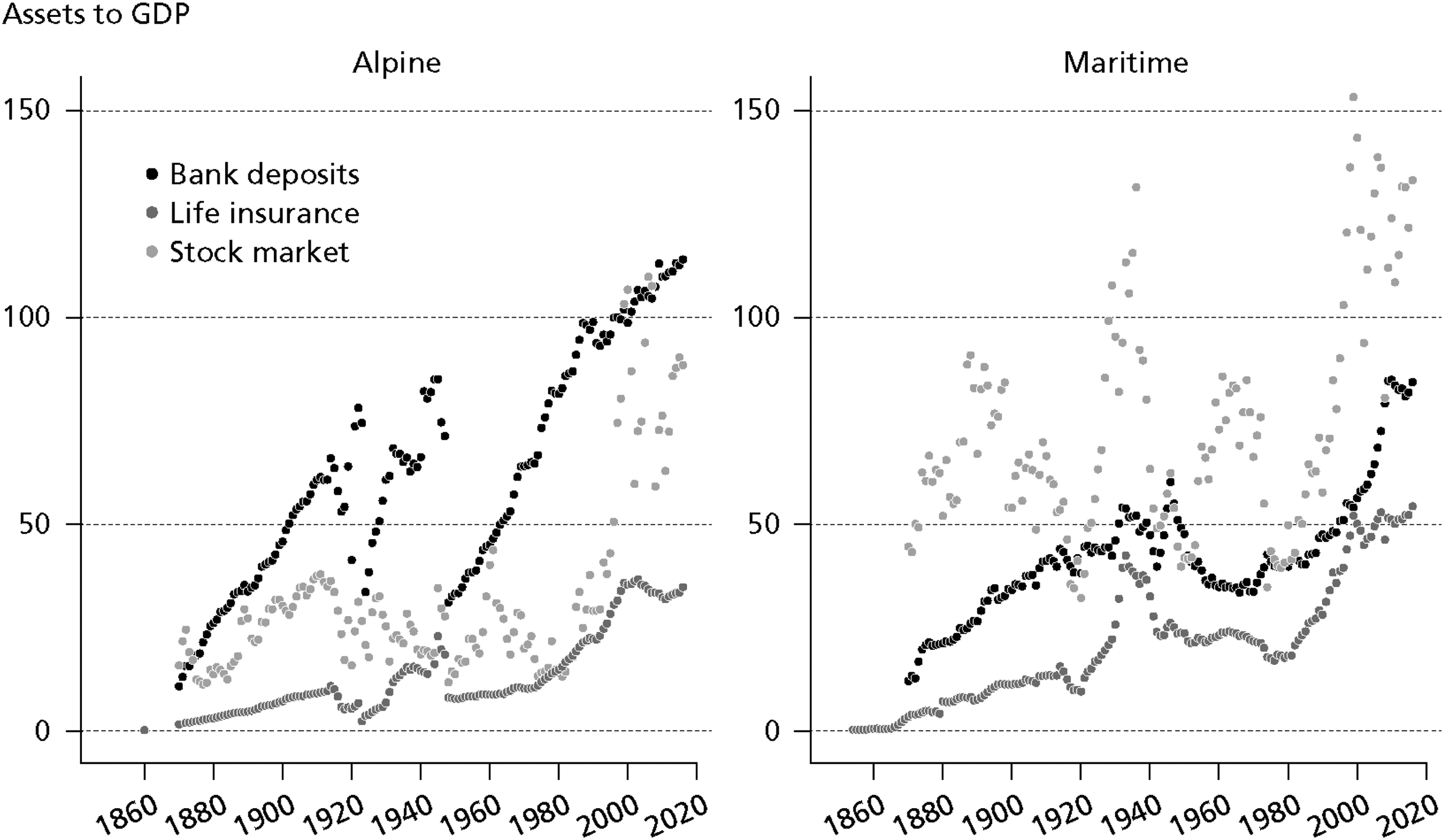

Among the private/public, financial/nonfinancial institutions allowing societies to cope with economic uncertainty, comparative political economy (CPE) has strangely ignored the institution created outright to manage economic risks: the insurance industry, which, historically, even preceded modern banking, welfare states, and homeownership societies. Presently, insurers’ annual premiums in life and nonlife insurance amount to about one-third of countries’ total social expenditure and life insurance assets alone equal to banking assets in LMEs and stock market capitalization in CMEs (see Figure 1). Contemporary societies spend more on private insurance than ever before, and ever-larger parts of the world population are enrolled in private insurance arrangements, 1 a development that may be associated with the individualization or desocialization of risk. 2 Yet, scholarship on insurance has largely focused on the state as the “ultimate risk manager,” 3 whereas financialization and CPE scholarship has ignored insurers in favor of banks, capital markets, or social insurances. 4 While most scholars in this CPE literature acknowledge the existence of insurance companies as important parts of financial and welfare systems, few have ascribed agency to private insurers in shaping the trajectories of capitalist societies.

Insurance, banks, and stock markets in Alpine/Maritime countries (percentage). (See the appendix for a full list of the sources.)

In this article, we aim to put private insurance on the CPE map by reviewing its role in shaping the trajectories of Western capitalist societies. First, we mobilize new long-run data to build on Michel Albert's intuitive but underexplored distinction between different insurance cultures and to mark out two types of insurance capitalism: German-speaking or “Alpine” countries were late and slower in adopting private insurance, retained many nonmarket, interventionist elements in the governance of the insurance business, and insurers’ investment portfolios tended to be less risky. Anglophone or “Maritime” countries, by contrast, were early insurance adopters, in size and demographic penetration, while having less state involvement in their more competition-oriented system of governance and a stronger focus on investment in financial market instruments. For most of the history of modern capitalist societies, the Alpines retained a more risk-sharing, stability-oriented private insurance sector. We hence show that there is a clear association between Maritime/Alpine varieties of private insurance and the existing LME/CME and liberal/continental welfare typologies.

While this association is perhaps not surprising, even if it is evidenced for the first time here, we secondly make the argument that insurers have had active agency in bringing it about. Depending on economic development, the existence of private insurance historically preceded both welfare states and the bank/capital-market distinction of financial systems and was important in their development by making available the relevant expertise, lobbying governments for privately administered welfare schemes, and by making available the capital for capital market development. With the growth of welfare states and financial systems in the twentieth century, they actively pushed for more privatization of the former and securitization of the latter, seeking safe assets to invest in. In the Maritime countries, though, the relatively larger and more advanced insurers were much more able to hinder the development of social security and enable the rise of securities markets. To the extent that the Alpine insurers have started to converge more on the Maritime model, trends toward welfare privatization and capital market investments have also been an increasingly widespread feature there.

The article fills an obvious private insurance gap that both comparative welfare and finance research have left open. It also fills the comparative gap within insurance research and points to potential complementarities with other institutions that make up countries’ arrangements to deal with economic risks: Maritime insurers allowed for smaller public welfare states and provided funds for capital markets to function, while Alpine countries could rather count on stronger public welfare states and channeled funds more into their larger mortgage markets. We observe, as in other domains of finance, that in recent decades the insurance sector has been affected by financialization, which has caused some degree of convergence between the Maritime and Alpine insurance industries toward the competition-oriented Maritime type. With this convergence on the Maritime type, not only have risks become individualized and shifted from the public to the private, 5 but the more risk-taking and competition-orientated model of insurance capitalism has gained the upper hand.

We proceed as follows: we first trace how CPE literature on the varieties of capitalism (VoC) and welfare direction has forgotten about the comparison of private insurance and then describe the historically divergent insurance trajectory of Alpine and Maritime countries along three dimensions—size, investment strategy, and degree of state involvement. In the following section, we propose a Gerschenkronian explanation of this initially diverging pattern and argue that insurers shaped the complementarity with capital markets and trade-off with welfare states. We conclude by pointing to potential consequences of the convergence on the riskier and risk-individualizing Maritime type.

Literature: Between Varieties of Capitalism and Insurance Studies

Throughout history, different forms of insurance have existed to protect against a broad range of risks, including the risks of seafaring expeditions, agricultural risks, risks associated with illness and death, natural hazards, and transportation. In its modern guise, insurance leverages the technology of risk to enable the pooling of resources, which can then be used to compensate individual participants in the pool for losses caused by prespecified events. 6 In this “actuarial conception” of insurance, individual contributions should reflect individual risk. That is, regardless of whether a risk actually materializes or not, the total premiums an individual policyholder is expected to pay should match the total loss the same individual is expected to incur plus an additional margin to cover the insurer's expenses, including the cost of capital. This basic intuition lies at the heart of a broad variety of insurance arrangements that characterize today's insurance societies.

Despite its ubiquity, little—if any—of the social science literature on insurance has so far analyzed the emergence of different varieties of insurance capitalism from a comparative perspective. By deliberately oversimplified terms, the vast literature on what we might call insurance studies can be subdivided into three broad categories. First, there are the country-specific and oftentimes also sector-specific or company-specific histories of the insurance business. 7 By focusing mostly on individual case studies, this literature, with a few exceptions of two-country or large-n studies, 8 has not explicitly addressed the question of how and why insurance industries across different countries have come to look so dissimilar for such a long period. A second body of literature rather tends to focus on the practice of insurance, examining, for instance, how insurers “make” risk and how they “market” it. 9 This literature has done much to clarify how insurance functions as an institution to produce specific kinds of solidarity among a large and heterogeneous set of subjects. While this literature has contributed to clarifying the institutional logic underpinning insurance, it has not examined the interaction between private insurance and other major capitalist institutions from a comparative perspective. Third and finally, there is the literature describing the larger trends in insurance, pointing, for instance, to the historical emergence of insurance institutions and their relation to broader societal changes, such as the rise of modern welfare states and the increased emphasis being put in modern “governmentalities” on individual responsibility. 10 This body of literature is perhaps closest to our objectives here but also lacks a comparative dimension.

While insurance studies themselves have thus largely missed out on comparative work, classical CPE accounts have largely omitted private insurance. This becomes particularly evident in the two adjacent and established comparative research fields on banking and the welfare state, or public insurance. Ever since the first CPE works on comparative finance, the juxtaposition of bank-based versus capital-market-based finance of (industrial) companies 11 —in late nineteenth-century industrialization, 12 after World War II, 13 and up to the modern VoC distinction of coordinated (i.e., bank-based) versus liberal market economies—has pervaded the literature. 14 With very few case-study exceptions, 15 the insurance sector has been completely left out of these comparative and also comparative-historical studies of finance in capitalism.

The comparative study of private insurance pales even more in light of the comparative history of the welfare state and the enormous industry of social science papers that has developed around the comparison of public insurance in the tradition of Esping-Andersen and followers. 16 Private insurance mostly figures in this literature as a private alternative to public welfare such that insurance comes into the picture as the “privatizer” of formerly public domains, most notably for pensions and health. 17 The crowding out of the public by the private has also been investigated through individuals’ attitudes toward private versus public provision of insurance services or through private insurance lobbying for welfare privatization. 18 Overall, it is fair to say that despite this research about the privatization of the public good, private insurance has very much stood in the shadow of its counterpart of comparative public-insurance research.

One central exception to this general insurance void in CPE is Michel Albert who, in his Capitalism against Capitalism, popularized the comparison of Rhenish with Anglo-style capitalism by comparing mainly Germany and the United States across many domains that would later figure in the VoC framework. 19 Albert was a longtime president of the French Assurances générales, and a chapter in his book—probably the most informed—introduced the distinction between Alpine and Maritime insurance cultures with the Rhine as a demarcation line and France split between them. The Alpines figure as the more risk-sharing, publicly regulated, and mutual insurance type emerging through Alpine cooperatives as opposed to the seafaring, risky insurers in Maritime nations. Albert normatively diagnoses the danger of France moving too much in the less gentle Maritime direction. While the distinction is regularly cited in technical insurance research, particularly in the European integration process, 20 fewer than 10 of Albert's 1,500 English and 2,150 French Google citations (July 2021) mention it, and then only en passant.

Another body of literature in the broader political economy literature that has touched on insurers, albeit with relatively little empirical detail, is the patient capital literature. This literature identifies insurance as a potential source of patient capital—that is, investments in equity or bonds with a long-term perspective that shield corporate management from short-term market fluctuations. 21 Deeg and Hardie suggest that like pension funds’, insurers’ liabilities are relatively fixed. 22 They invest “to meet specific liabilities, and the long-term nature of most of these liabilities results in higher levels of patience.” 23 While traditionally market-based countries, like the Maritime countries included in our analysis, relied on insurers and pension funds to supply patient capital, traditionally bank-based countries, like the Alpine countries, relied mostly on the banking system for it.

Overall, then, insurance studies, whether in sociology, history, or science and technology studies, lack a comparative dimension, while the CPE literature has largely ignored private insurance. Taking our cue from Albert's distinction between Alpine and Maritime insurance and the patient capital literature, we seek to fill the void by examining the role of insurance in different modes of capitalism. In the rest of this article, we provide empirical substance to Albert's distinction between Alpine and Maritime insurance varieties and use this distinction to understand how the development of private insurance relates to the development of welfare states and financial systems.

Alpine and Maritime Insurance Cultures

In this section, we characterize the Alpine and Maritime varieties of private insurance, which respectively tend to be characteristic of the CMEs and LMEs central in the VoC literature. It is important to note here that, unlike Albert, we see the Alpine and Maritime varieties of insurance capitalism as descriptive categories that do not point to deep-rooted cultural and geographical traditions of agrarian mountain cooperatives facing terrestrial risks in the Alpine region and of seafaring merchant communities facing maritime risks in Maritime countries. 24 This explanation reaches back to deep historical-comparative grounds we have very little empirical grasp on. The cultural explanation generally faces the problem of how insurance spreads across different countries despite relatively sticky cultural practices. We therefore rather take the historical association of different types of insurance capitalism with the Alpine and Maritime regions as the basis for developing the Alpine/Maritime varieties of insurance capitalism as descriptive categories that differ along three different dimensions: the size and timing of the insurance industry, the dominant investment strategy, and the degree of state involvement in the industry. 25

Our analysis focuses on six countries in particular, which can be considered the most similar cases within the “groups.” This will enable us to find the starkest differences between the Alpine and Maritime insurance varieties. We regard three of the countries, Germany, Switzerland, and Austria, as belonging to the Alpine type and Great Britain with its former colonies, Canada and the United States, as belonging to the Maritime type. In what follows, we examine how these country groups differ along the three dimensions mentioned above.

Insurance Size

Both Maritime and Alpine countries have long insurance traditions and look back to the first marine insurance exchanges in the early modern period, to the first fire insurers in the seventeenth century and the first life insurers in the eighteenth century. The role of the leading Maritime insurance nation was heavily linked with maritime power in general. Since the seventeenth century, therefore, Great Britain with its first incorporated maritime insurers and Lloyd's of London had a privileged position. When speaking of fire and life insurers as private stock companies using actuarial techniques, Great Britain can also be said to have historically led insurance development.

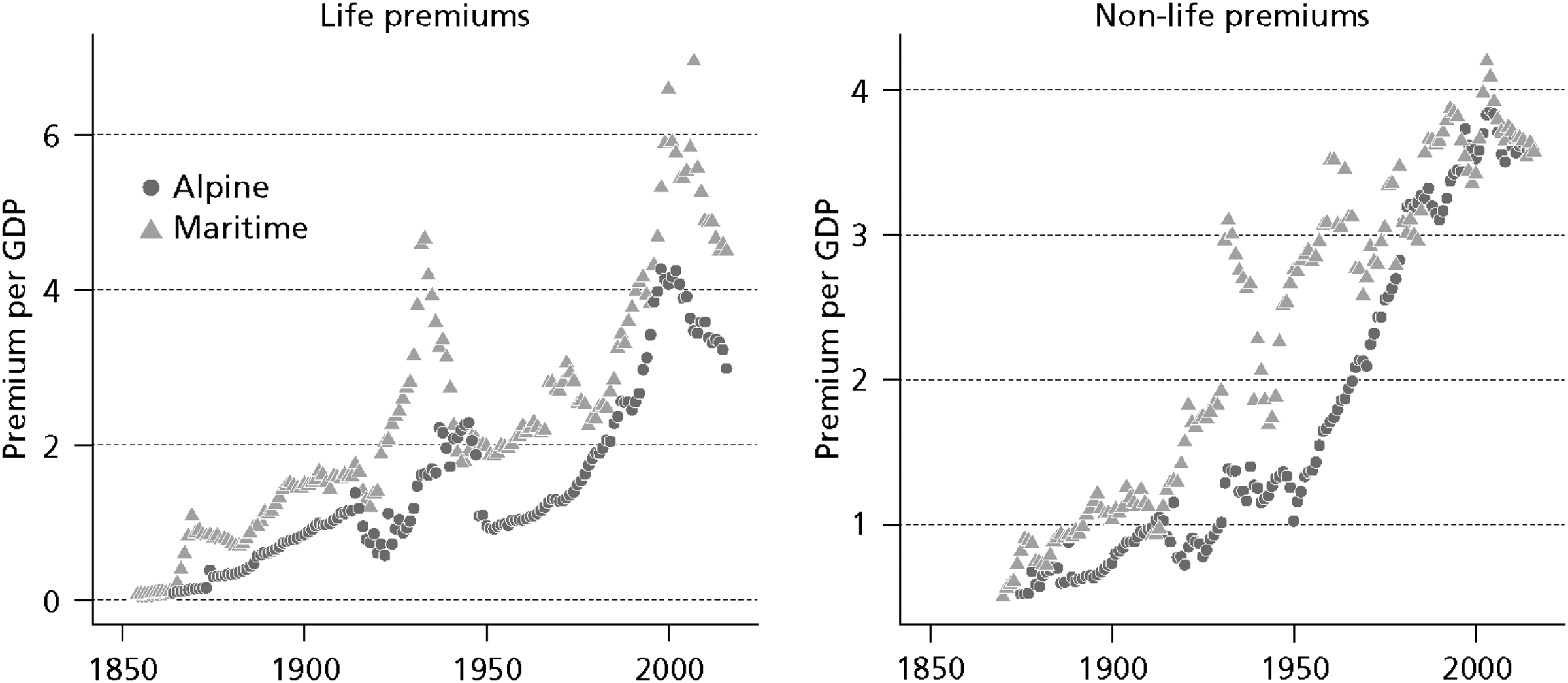

It is difficult to get a good comparative assessment of countries’ insurance size before the mid-nineteenth century. Reporting has improved since then, which allows us to trace the evolution of life and nonlife insurance by measuring “insurance penetration,” the annual premiums paid to insurers in relation to GDP (in percentages). Life insurance encompasses all the different kinds of policies offered by life companies, that is, whole life and annuity contracts in the nineteenth century, and later also industrial, group, credit and more investment-like insurance contracts like individual and group pension contracts. Nonlife premiums originally consisted only of maritime, transport and fire insurance and gradually expanded into ever more domains, particularly agricultural, automobile, accident, general liability and various other risks.

Figure 2 displays the evolution of life and nonlife penetration averaged over Maritime and Alpine countries since the late nineteenth century. Both country groups follow broad general trends: they both have a general growth trend, slower in the earlier years, particularly fast in the later twentieth century and plateauing or even declining in more recent years. In both country groups, the two world wars and the Great Depression also stand out as periods of troughs and peaks. During the wars, the international insurance business collapsed. Particularly in hyperinflation-ridden Germany and Austria, insurers lost the majority of their reserves. During the Depression, GDP declined rapidly, while premiums continued to flow because of contractual obligations, but also with a precautionary savings motive in light of failing banks. 26 Here also, the failure of the largest European life insurer, the Austrian Phönix, made life more difficult in Alpine than in Maritime countries. 27

Life and nonlife penetration by Maritime and Alpine type (percentage). (See the appendix for a full list of the sources.)

Beyond common trends, however, Maritime countries have had more pronounced insurance development in all domains, staying ahead of their Alpine counterparts in both mean and median (not shown) in almost all years with few war-time exceptions. The mean difference across all years is 0.7 percentage points per GDP for life and 0.5 for nonlife insurance. Similar figures could be shown for U.S. dollar–denoted insurance density, that is, per capita premiums, even though historical exchange rates do not control for purchasing power parity. These differences are driven more by some countries than others. In the Maritime group, it is first the United Kingdom, then Canada and the United States, that pushes this country group ahead, whereas it is Austria and Germany that pull down the average more than others in their group. However, even in Switzerland insurance penetration has been lower than in the Maritime countries throughout all periods. 28 Yet, differences in insurance penetration in Alpine and Maritime countries have decreased in recent decades. This is partly driven by the catch-up of the two hyperinflation victims, Austria and Germany, since the 1980s.

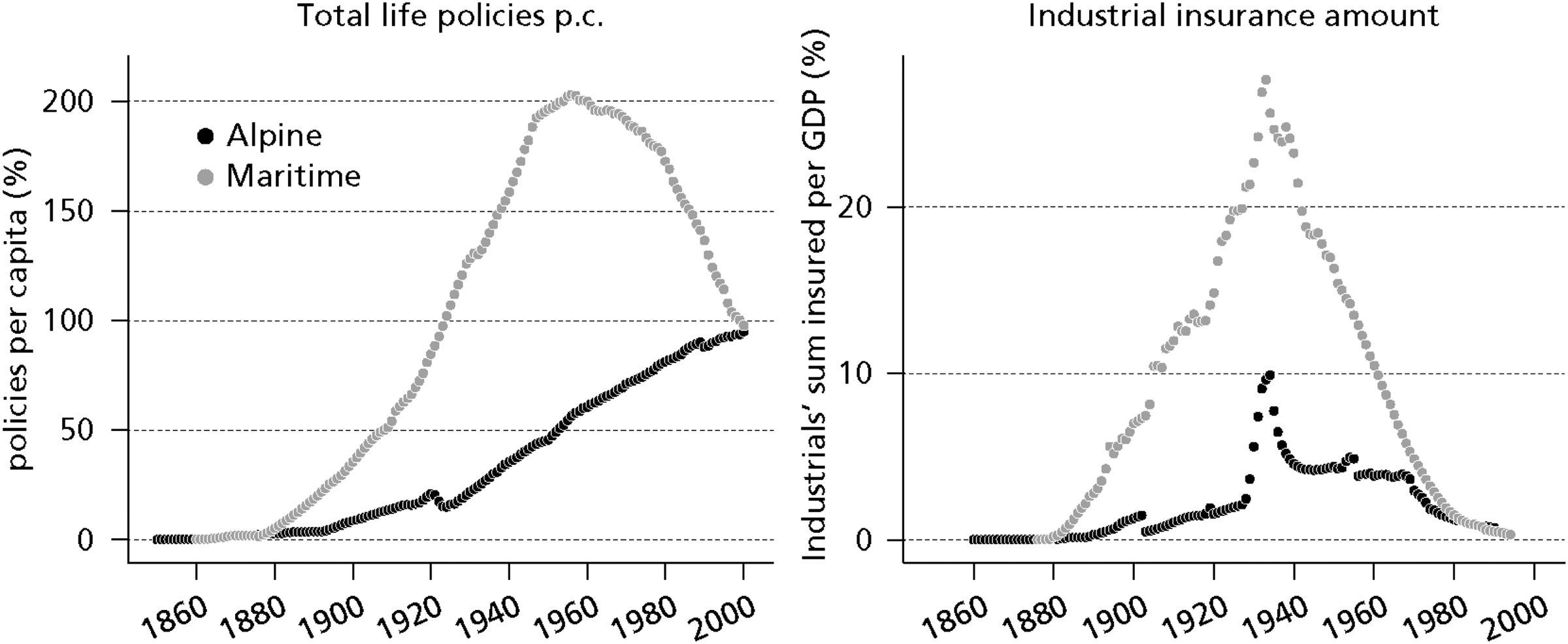

Insurance has also been relatively more widespread in Maritime countries. Policies can cover multiple persons and one person can buy more than one policy, but the share of policies by population still gives a rough idea of how broadly life insurance was spread within the population. As the left-hand panel of Figure 3 reveals, before 1880 life insurance covered less than 5 percent of the population, and the differences between countries were not so pronounced. As early as 1900, however, there was a clear divide between Maritime and Alpine countries, the former reaching more than 50 percent coverage by the interwar years, the latter lagging about twenty years behind in policies per population. The crucial factor driving the differential adoption speed in policy numbers was the faster spread of the industrial or small life insurances, which targeted lower-income populations. As the right-hand panel of Figure 3 shows, the total sums insured by these small insurances with weekly premium collection, used for burials in the Maritime countries and more generally in the Alpines, 29 was again clearly higher in the former than in the latter. After World War II, ordinary life policies became the standard, and industrials first stagnated and then declined. With their disappearance, the country-group differences were evened out in the 2000s.

Life insurance policies per capita (percentage) and industrial insurance amount (relative to GDP). Canada excluded; some missing postwar data in GBR/AUT were interpolated using Stineman's algorithm in R. (See the appendix for a full list of the sources.)

Market-Based versus Non-Market-Based Portfolios

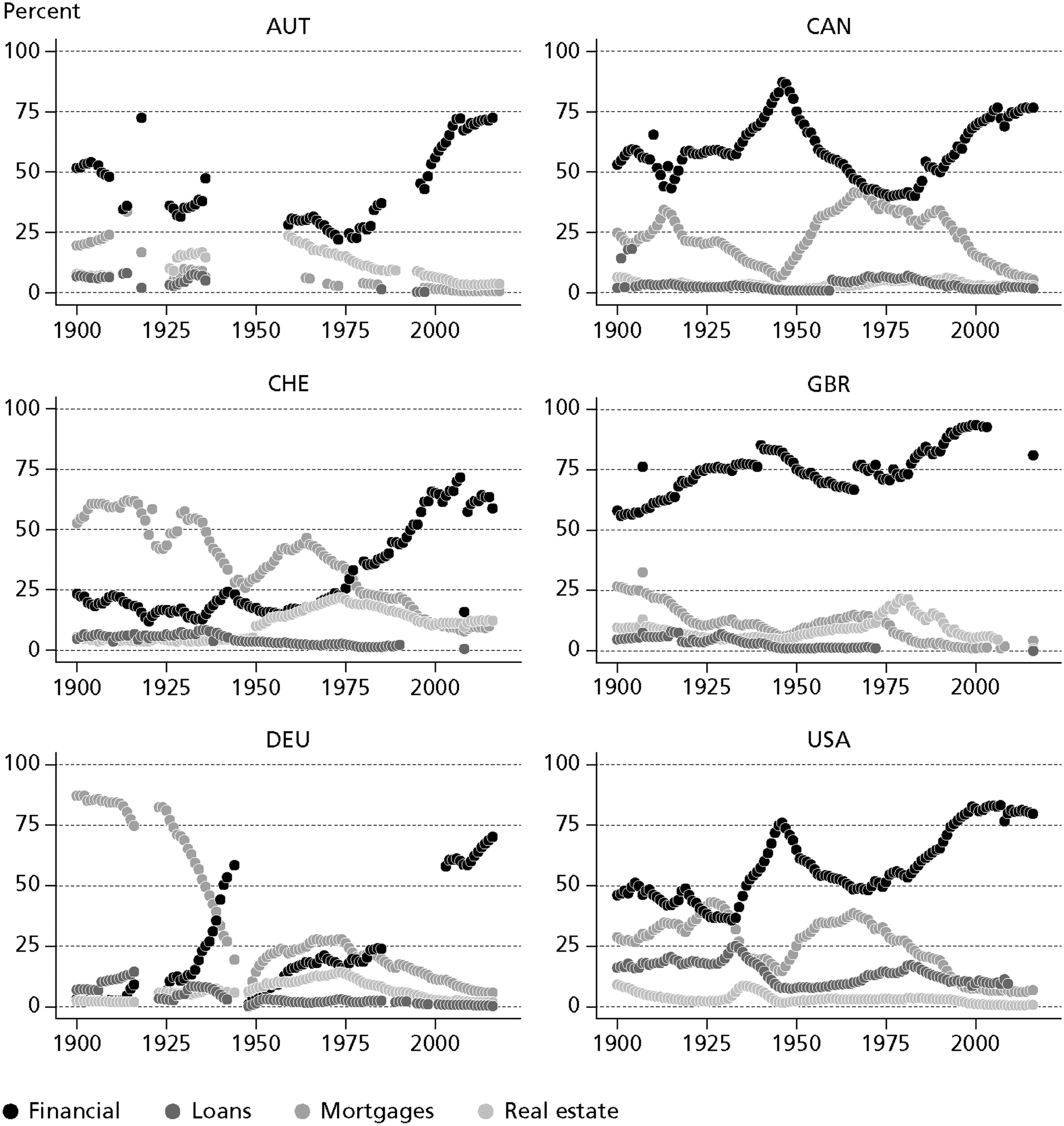

A second dimension along which Alpine and Maritime insurers differed was their investment behavior. Life insurers accumulate considerable assets over time, and their investment strategies tend to correlate with nationally specific regulations and patterns. Both Maritime and Alpine insurers generally follow a common trend: starting from mortgage-dominated portfolios in the nineteenth century, they gradually shift their assets to tradable financial securities such as stocks and bonds. 30 Figure 4 displays the portfolio breakdown by asset class in the different countries. Mortgages follow countries’ construction cycles, but overall, their share decreases to the point of not even figuring as a separate asset class in official statistics. Financial assets, by contrast, are the main beneficiary of this trend throughout countries: pushed by more or less compulsory investment in government bonds in wartime, insurers gradually shifted their assets to more bonds and stocks over time.

Portfolio shares of life insurers by asset class. (See the appendix for a full list of the sources.)

Beyond this common trend, however, there is a clear difference again with much earlier and larger portfolio shares in financial assets in Maritime countries and the Alpine countries, with much higher initial investment shares in mortgages/real estate and a slower transition to financial assets. Within country types, there are, of course, certain differences: Germany's historically almost 90 percent mortgage investment was extreme even among the Alpines. In Figure 4, Austro-Hungarian insurers seem to defy this neat distinction at first sight. Firstly, however, these insurers maintained large shares of direct ownership in real estate. And, secondly, the Alpine countries had a large secondary mortgage market, which was almost nonexistent in the English-speaking world. 31 Between 30 and 40 percent of the investments by Austro-Hungarian insurers in “financial assets” were covered mortgage-bonds issued by mortgage banks. 32 The overall dependency on the property sector is prevalent throughout the Alpine world and corresponds to the more pronounced development in fire rather than life insurance. Within the Maritime world, by contrast, American insurers were known for their strong investments into corporate, particularly railroad, bonds since the late nineteenth century, 33 whereas British insurance investors, and to an extent also Canadians, 34 shifted to stock investments already in the interwar years. 35

A convergence on portfolios dominated by investments in financial securities becomes noticeable only in the post-1980 world. This institutional difference is associated with insurers having different risk profiles: the stronger real estate–dependent Alpine insurers depend on fluctuations of real estate and potential mortgage defaults as the main financial risk, whereas Maritime insurers depend much more on the price volatility of bonds and stocks. 36

State Involvement in Insurance Markets

A final dimension along which the Alpine and Maritime worlds of insurance differ is the relationship of insurance with the state. We distinguish between three different aspects of states’ involvement in insurance: through ownership of public insurance companies, state supervision of insurers’ investment practices, and price regulation. In this section, we describe how the Alpine and Maritime varieties of insurance capitalism differ from each other on each of these three dimensions.

State-associated insurance enterprises. A distinct feature of Alpine insurance capitalism is the existence of state-associated insurance enterprises, which were founded either as independent insurance enterprises or were set up as the insurance branch of the public and cooperative banks characteristic of Alpine countries. The practice of state-owned insurance enterprises reaches back to the cameralist tradition of compulsory and state-owned fire insurers on the European continent at about the time England opted for the first private joint-stock companies after the Great Fire of London in 1666. 37 During much of the eighteenth century, Alpine fire insurance industries were composed of domestic municipal- or state-owned insurers and British private insurers. Only in the nineteenth century did domestic private insurers enter the market. Still in the twentieth century, state-based fire insurers could maintain about half of the property insurance market in Switzerland, whereas similar institutions were virtually absent in the Maritime countries. One prominent exception is US flood insurance, where the federal state became the main provider of flood insurance protection in the second half of the twentieth century because of commercial insurers’ unwillingness to provide protection; even so, these policies are increasingly based on private insurance models and are often sold through private insurance fronts, 38 meaning that the exception of flood insurance rather confirms the rule.

In the late nineteenth century, states also became active in the domain of life insurance. This was usually driven by social reformers who wanted to spread insurance throughout the country and among parts of the population usually not served by the then existing commercial life insurers, who catered mostly to the (upper) middle classes. Another reason for state intervention was war-related life insurance, which commercial insurers were unwilling to provide. State-associated life insurers were founded in different institutional arrangements: a corporatist public life insurer in Germany in 1911, postal insurance in Great Britain, state-led insurers in Denmark, and a nationalization of private insurers in Italy. The success of these institutions differed widely and generally depended on whether they imitated private competitors or not. In Germany, public insurers in life and nonlife have generally had slightly over 10 percent market share, in Austria cooperative insurers are among the top firms, while in Switzerland, public fire insurers still have a considerable market share.

Regulation and supervision. Another feature that distinguishes the Alpine and Maritime varieties of insurance capitalism concerns the financial supervision of insurance enterprises. The British style of insurance regulation emerged from the mid-nineteenth century onward and became known as a regime of “freedom with publicity.” The basis of this regime was laid by the 1844 Joint Stock Companies Act, and, in the case of life insurance, by the 1870 Life Assurance Companies Act. This regime basically refrained from imposing any restrictions on insurers’ business activities, as long as insurers made their financial statements publicly available, including the methodologies underpinning the actuarial valuations of life insurance liabilities. 39

In the United States and Canada, state supervision was more developed but still mainly aimed at setting the basic rules for competition among insurers. With the setting up of the first supervisory bodies in New Hampshire (1850), Massachusetts (1855), and New York (1859), US supervision became a state-level issue. 40 From the late eighteenth century onward, however, it also acquired a federal component with the setting up of the National Convention of Insurance Commissioners (NCIC, later renamed as the National Association of Insurance Commissioners or NAIC). 41 Although the stringency of solvency regulation varied from state to state, state-level supervisors often imposed deposit requirements, reporting requirements, a licensing system, and quantitative restrictions on insurers’ investments, capping, for instance, investments in stocks, real estate, and mortgages. Following the Armstrong Committee in 1906, for instance, New York prohibited investment in a number of assets including stocks, a restriction that was lifted in 1951. 42 Even if there has been a lively debate about whether and how these restrictions actually influenced insurers’ portfolio allocations, 43 the investment restrictions eased with the more general trend toward financial liberalization in the 1970s and 80s. The NAIC, however, still sets quantitative restrictions on insurers’ investment practices today. 44

Canadian insurance supervision developed a little later, from 1868 onward, and is characterized by a strong focus on protectionist measures preventing capital from flowing out of the country through its foreign-dominated insurance industry. 45 The two legislative acts of 1875 and 1877, for instance, required insurers to publish their financial accounts and to prove they held enough Canadian assets to back their Canadian insurance obligations. Supervisors, moreover, imposed investment restrictions that were skewed in favor of the large domestic insurance enterprises Sun Life and Canada Life until the Great Depression. After the near collapse of Sun Life in 1931, supervisors capped all insurers’ investments in common stock at 15 percent. 46 Even if the commercial freedoms enjoyed by insurance enterprises in Northern America paled in comparison to those on the British Isles, the main purview of supervision was to define the rules of the game (whether protectionist or not) in an otherwise competition-driven market.

Alpine governments, in contrast, adopted a more interventionist approach to insurance supervision, which became known under the label of materielle Staatsaufsicht (material state supervision). The Austrians were the first to adopt a major supervisory regulation with the Assekuranz-Regulativ of 1880 and the setting up of a specialist insurance bureau, the Assekuranzbüro. 47 Although this supervisory framework initially resembled a slightly more restrictive variation of the British “freedom with publicity approach,” a more interventionist style of regulation developed later. Switzerland made a major stride in this regard in 1885, when it set up the Federal Insurance Office (the Eidgenössisches Versicherungsamt), which was endowed with the power to impose restrictions on insurers’ investment choices as well as business practices more generally. The supervisory agency required insurers to ask the supervisor for approval of its tariffs, requiring them to pay license fees in proportion to overall business and standardized insurance contracts. 48 In 1901, the German government followed with the adoption of the Reichsgesetz über die privaten Versicherungsunternehmungen and set up the Kaiserliche Aufsichtsamt für Privatversicherung (Imperial Supervisory Office for Private Insurance), which later became the Bundesaufsichtsamt für das Versicherungswesen. Like the Austrian and Swiss regimes, the German regulatory regime was based on the “concession principle,” meaning that insurers could only conduct business when they had explicit regulatory approval. In its early years, the supervisory body required the separation of life and nonlife business, imposed stringent accounting rules (e.g., requiring insurers to discount their liabilities at 3.5 percent) and investment restrictions, 49 and standardized insurance contracts, 50 significantly curtailing space for product innovation and innovative investment strategies as competitive considerations.

Price regulation. Another aspect in which the Maritime and Alpine insurance traditions are distinct concerns the rules and regulations around insurance pricing. While regulators rarely dictate the terms of insurers’ policies in Maritime countries, enabling price- and design-based competition among insurers, we can again observe a more interventionist approach in the Alpine countries, where price regulation is seen as an important aspect of the material state supervision approach. Although it is difficult to assess the extent to which price-setting is controlled in practice—price control mechanisms need not be explicitly encoded in law but may, for instance, also come in the form of state-backed cartelization 51 —the presence of explicit price-setting regulations and the high degree of state-enforced standardization of insurance contracts nonetheless sets the Alpine variety of insurance capitalism apart from its Maritime counterpart.

Exemplary in this regard is the pricing of motor insurance, which in Germany was subject to a “unitary tariff” for motor insurance from 1938 onward. 52 Although the unitary tariff for motor insurance was abandoned in 1962, insurance supervisors continued to have a strong influence on insurers’ premium rates. 53 Up until the 1990s, they produced standardized risk calculations in collaboration with insurers who could then mark up these standardized rates within a prespecified range of 3 percent over the “economic cost” of the risk. 54 In the United Kingdom, in contrast, insurers determined their own rates, relying on both collectively produced risk knowledge and proprietary risk information. Though British insurers still came to collective agreements regulating competition, for instance, through fixed commissions on insurance sales agents, there was no regulatory enforcement of standardized premium setting. 55 This example illustrates the difference between the Maritime focus on actuarial fairness and risk calculation and the stability-oriented and competition-restraining approach in the Alpine countries.

Insurance: A Historical Life of Its Own and Force to Reckon With in Welfare and Corporate Finance

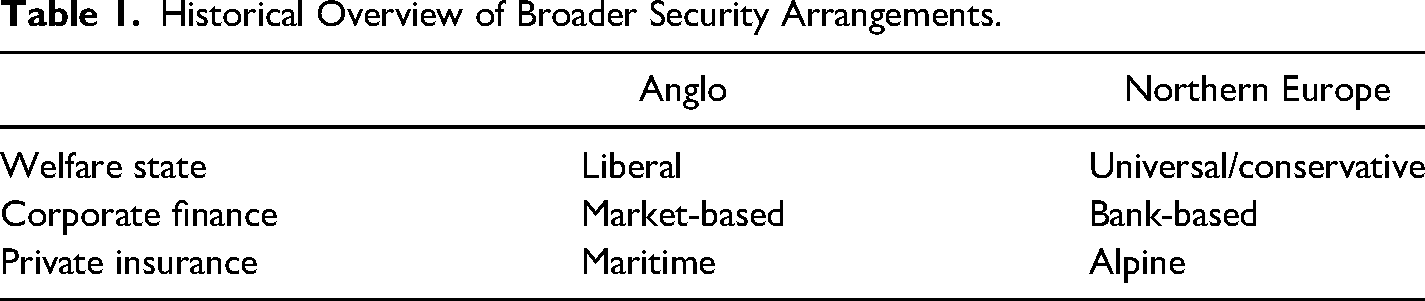

So far, we are in agreement with Michel Albert's intuition that the development of private insurance in Alpine and Maritime countries moved along different trajectories, comparing the development and composition of private insurance across six countries. At first sight, the distinct types of private insurance seem to fall in place nicely with the existing welfare and VoC typologies (see Table 1), where liberal welfare states and LMEs with market-based corporate financing (perhaps unsurprisingly) are also characterized by Maritime insurance features. This could give the impression that the distinct developmental trajectories of the Alpine and Maritime insurance industries are simply a symptom of the same underlying trends that differentiated liberal from universal/conservative welfare states, and market-based from bank-based financial systems.

Historical Overview of Broader Security Arrangements.

In this section, we oppose this view and argue for a distinct role of private insurance in shaping welfare states and parts of the VoC architecture in three moments. First, the existence of private insurance precedes welfare states and VoC, and the emergence of two types of insurance capitalism therefore cannot be explained by the existing typologies. Instead, we claim that a Gerschenkronian story of economic development best captures the Alpine/Maritime origins: the later a country developed, the more Alpine its insurance type. Second, by preceding the public welfare state and expanding massively alongside it, private insurance has influenced the rise and shape of public welfare: Maritime insurance has rather retarded public welfare and made it more rudimentary. Third, by co-originating with capital markets, insurers were important in creating and maintaining securities markets, first for corporate bond, then public bond and stock markets: Maritime insurers were more likely to foster the growth of securities markets, providing an alternative to bank-based corporate finance.

Causes of Divergence: Alpine and Maritime Insurance Trajectories

Because the rise of private insurance largely pre-dated the welfare and financial system typologies, the emergence of the two types of insurance capitalism cannot be explained by differences in public welfare and corporate finance regimes. Private insurance did not simply fill the gap left by states and banks confronted with a rising demand for welfare and financial capital but helped create it. The annual expenditure of life insurers, for instance, exceeded countries’ pension expenditure even in countries like Germany until the 1950s. 56 Why then have financial systems differed with regard to insurance?

Among the theories of financial system development, 57 a classical account is to start from a country's level of development. Richer countries have more possibilities and demand for a differentiated financial system, 58 and late developers have to overcome problems of scarcity by relying less on equity and more on banks or even state finance in their collective effort to catch up in a big economic spurt. 59 We suggest that economic development theories such as these also provide a model for explaining the differentiated development of insurance industries across Alpine and Maritime countries in a way that does not require the cultural/historical style of explanation found in the work of Albert.

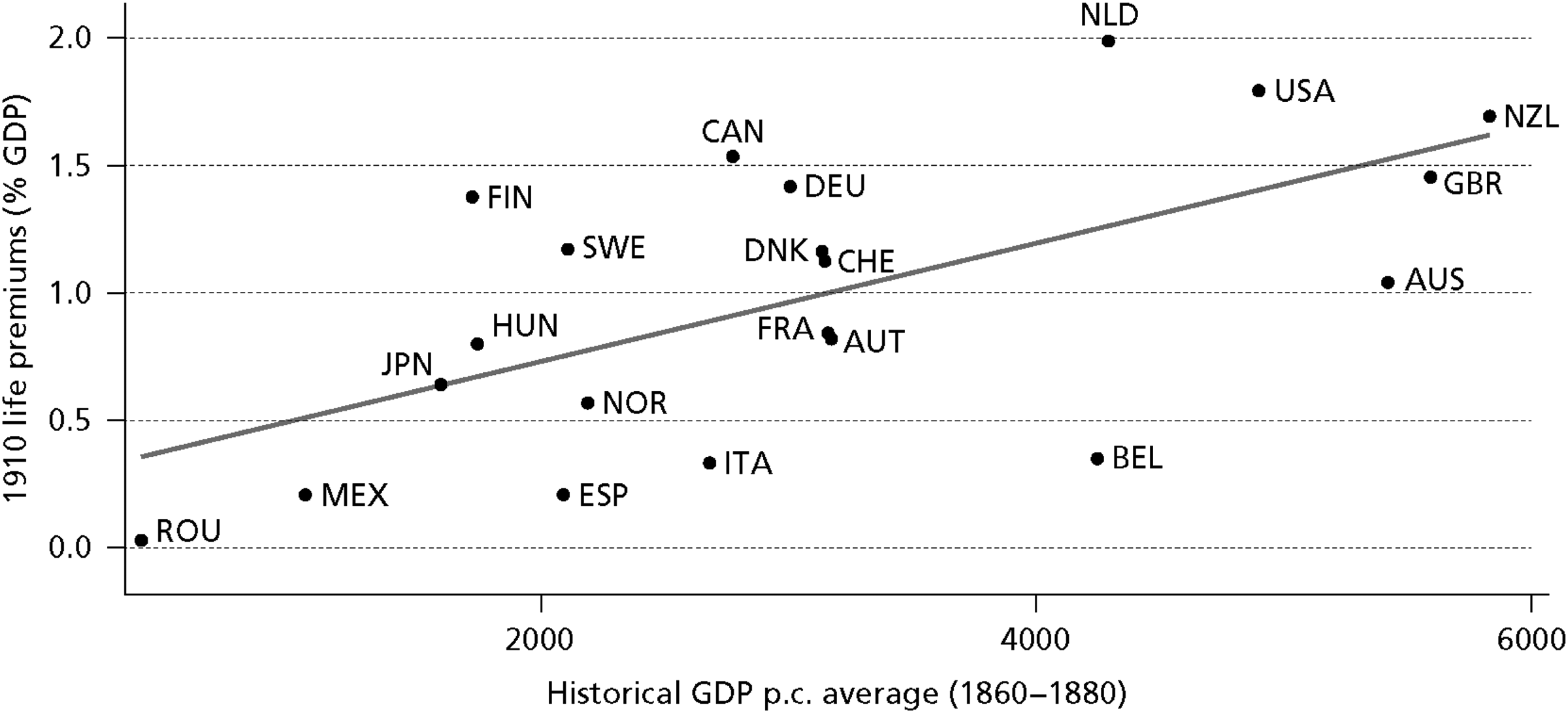

Historical GDP per capita in the mid-nineteenth century offers a relatively clear picture of insurance development until World War I, 60 with richer Maritime countries having on average the highest levels of (life) insurance penetration, that is, total premiums controlled for GDP, followed by their poorer Alpine counterparts. In a broader comparative perspective, Scandinavian countries and Japan are closer to Alpine insurance while Catholic countries are a distinct underinsured group (Figure 5). The picture looks similar for nonlife or total premiums, for which we have less country coverage. The insurance industry had to rely on a number of stable background conditions that earlier developers were more likely to provide, including stable currencies, stable mortality figures relatively undisturbed by pandemics, a cooperating banking sector, and markets for long-term investments. The more recent evidence on economic and insurance development supports the generally positive association between GDP growth and insurance development, often finding an S-shaped relationship: 61 steeper in the historical beginnings of lower insurance levels, it tends to level off in the more developed, insurance-saturated countries.

Historical economic development (in 1990 dollars) and insurance levels. (Maddison Project; see the appendix for a full list of other sources.)

The stage of economic and financial development not only explains the historically different depth of insurance penetration but also the second dimension separating the Alps from the sea: with less developed economies came less developed securities markets and the relative importance of tangible rather than financial wealth. Maritime insurers, consequently, were able to invest more in financial markets, whereas Alpine insurers remained more attuned to the property sector, investing above all in mortgages. Real estate was the dominant insurance investment in very late developers in Southern or Eastern Europe.

Finally, economic development was also an indirect determinant of how important direct and reinsurance markets were in the countries. The historian Robin Pearson describes how the early developer British insurers had started to capture primary insurance markets at home and even worldwide at a time when late developers often just had old-fashioned public fire and pension insurance. Once they developed private primary insurers as well, they were not able to compete with British insurers in export markets but had developed the reassurance institutions that instead were driven into worldwide risk diversification. 62

Where economic development was slow and capital for joint-stock companies was scarce, governments tended to support the insurance sector directly, which is the third dimension distinguishing Alpine from Maritime insurance. Large “baroque” bureaucracies in those countries, including civil servant pensions and state fire insurers, were important antecedents in late developers. 63 One key motivation behind setting up protectionism for one's own private insurance industry or founding state-related insurers outright was to prevent capital from flowing out of the country through foreign insurers. Hence many early regulations in later developers included protectionist measures either requiring foreign insurers to keep their assets in the country or giving domestic insurers a competitive advantage. Many state-related or public insurers were set up with the goal of providing the state or certain groups with insurance assets to be used for mortgage and public investments, for instance in Germany, or public finance in Italy. Late development hence correlates with an interventionist approach to insurance. 64

Insurance and Welfare

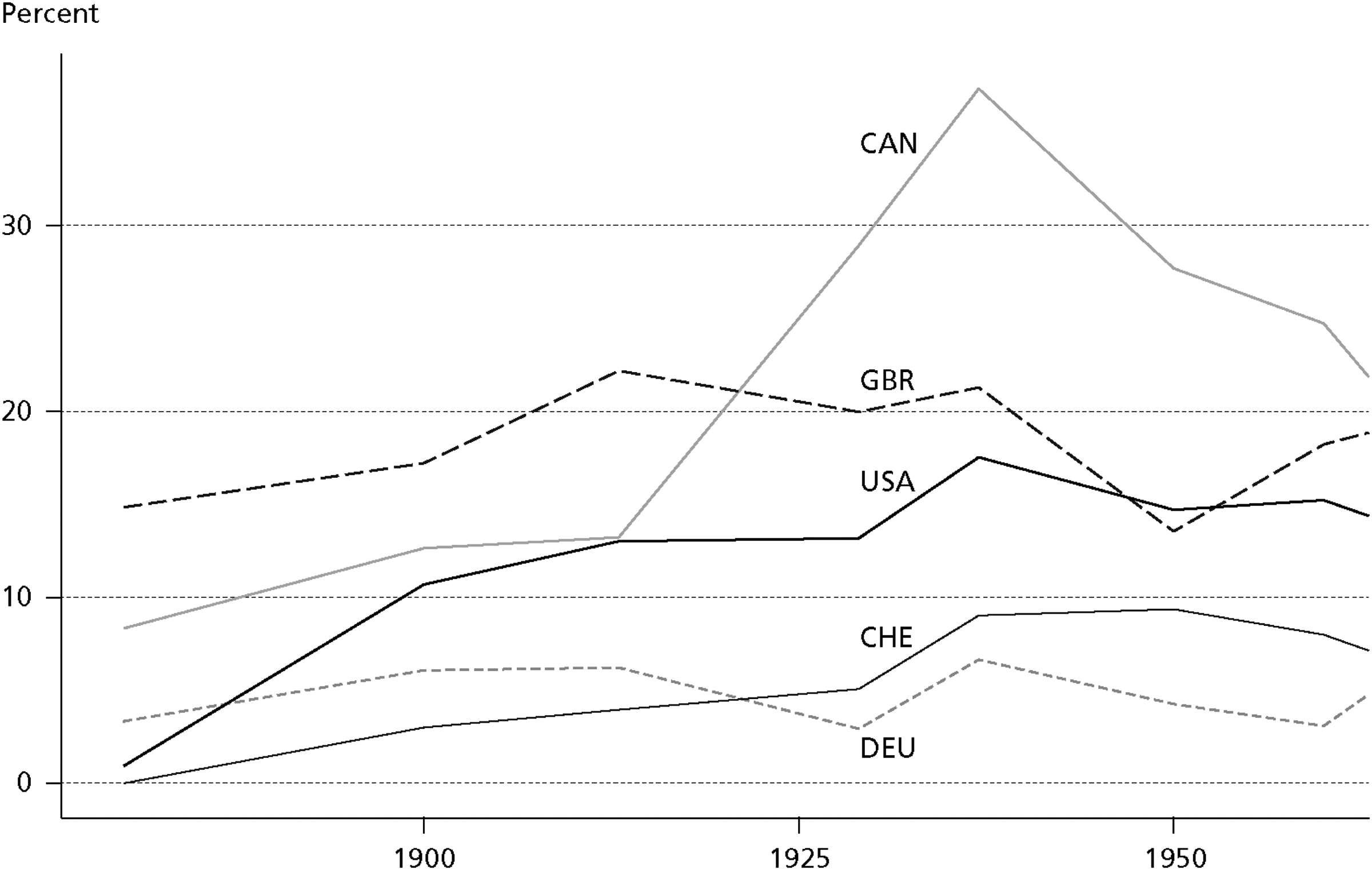

Since private insurance largely pre-dated and to a certain extent even preempted welfare reforms, welfare states are rather unimportant in understanding differences in the origins of the two insurance cultures. This was the case not only in Maritime countries but also in the Alpine ones. Fire insurance, for instance, pre-dates Bismarck's first insurance laws by more than two centuries, and the institutional form of fire insurance strongly resonates with the later twentieth-century welfare typologies in the social security domain: 65 there were private stock companies in Maritime countries, mandatory public insurers in Alpine countries, and hardly any in Catholic ones. When Bismarck implemented compulsory social insurance, he could draw on a century-long model practiced in fire insurance. The organizational form of preexisting insurance arrangements, in other words, provided a template for the welfare arrangements that developed from the late nineteenth century onward, which became instrumental in resolving conflicts between labor and capital. 66

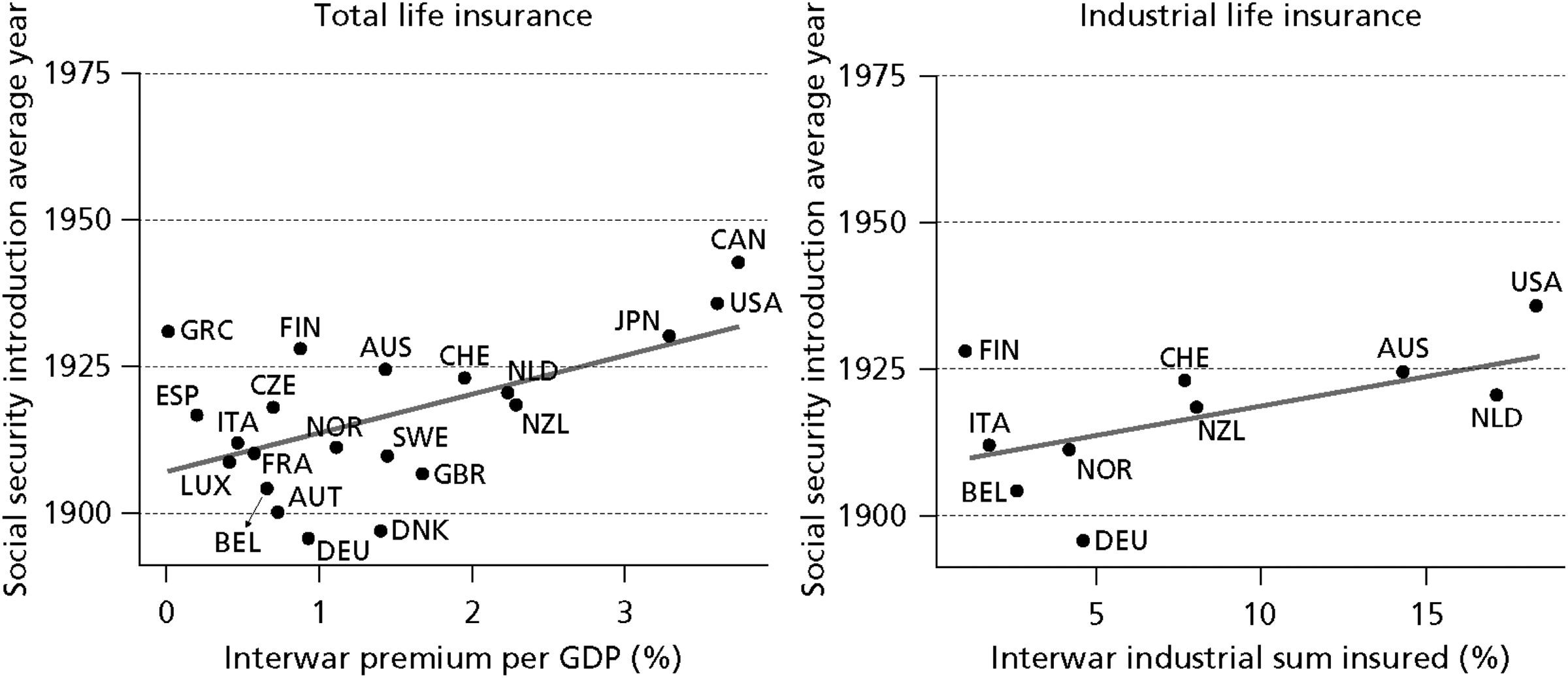

While the relation between public welfare and private insurance is often understood in terms of crowding out, the extent to which this is true varies over time. When public welfare arrangements were first created, the relation between public welfare arrangements and private insurance was predominantly competitive. Public insurance tended to limit the growth potential of private insurance, especially with respect to industrial insurance; 67 and the existence of private insurance in turn delayed welfare reforms or limited the scope of the reforms to basic security arrangements to be topped up by private products. This shows in the timing of welfare reforms: on average, the larger the life and industrial insurance sectors were before World War I, the later big social security reforms were passed (Figure 6). During the strong growth of public welfare in the 1950s, 1960s, and 1970s, however, private insurance saw a rapid expansion, especially in countries relying on privatized social insurance such as the Maritime ones. This is most obvious in the United States, but private insurance is also a prominent source of welfare in the United Kingdom and Canada, though more limited in scope and mostly focused on old age insurance. Since the 1970s, though, Alpine insurers have caught up with their Maritime counterparts, as governments in OECD countries increasingly sought to retrench welfare spending. 68

Social insurance introduction years and historic life insurance. (C. Schmitt, H. Lierse, H. Obinger, and L. Seelkopf, “The Global Emergence of Social Protection: Explaining Social Security Legislation, 1820–2013,” Politics & Society 43, no. 4 [2015]: 503–24. See the appendix for a full list of other sources.)

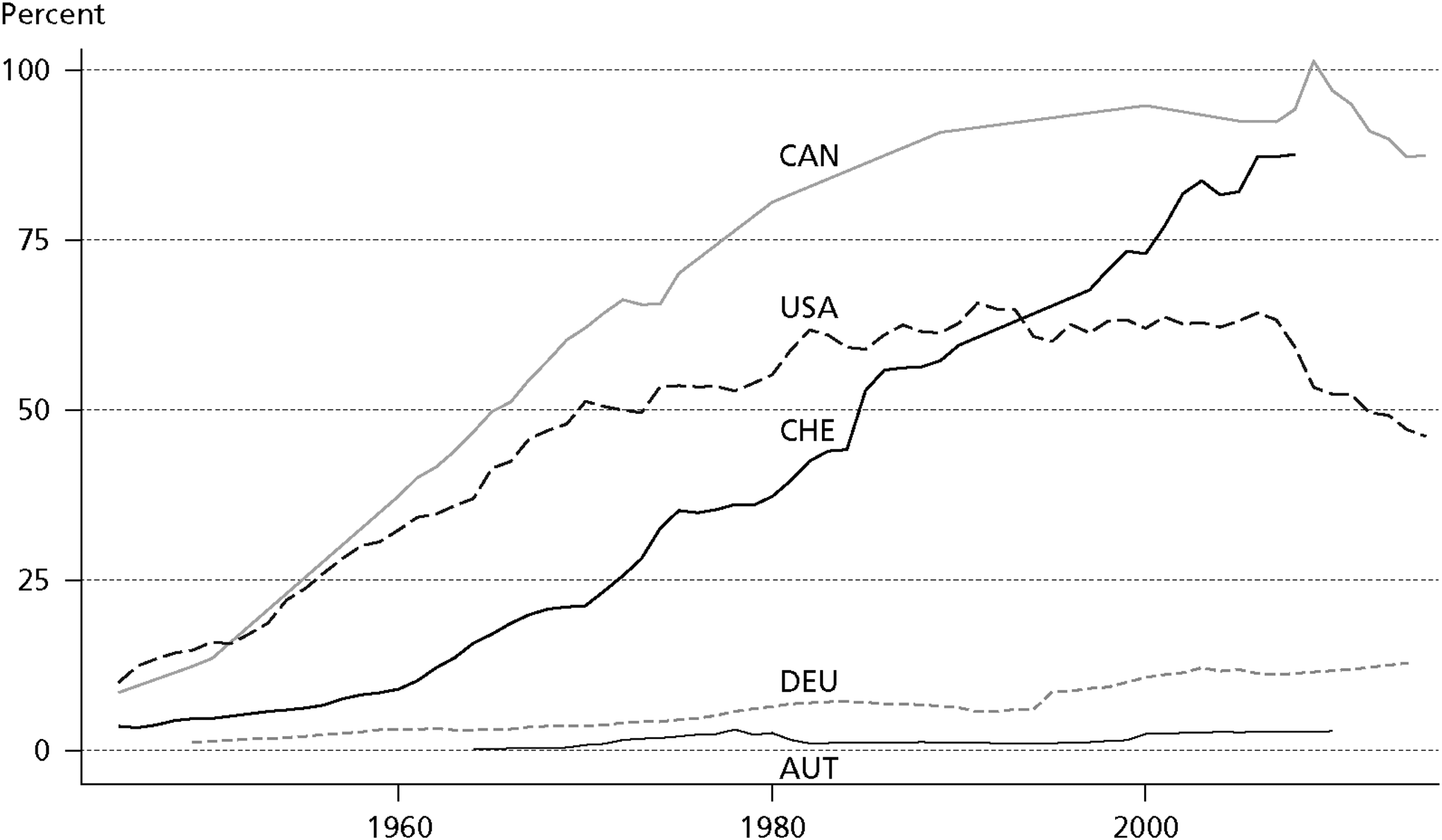

The differentiated paths of the insurance sectors during postwar economic development can perhaps best be explained by path dependencies. The Maritime model of insurance capitalism placed insurers in a good position to benefit from the expanding welfare arrangements. As noted earlier, the maritime variety of insurance capitalism was focused more on competition and product innovation, which enabled private insurers to respond quickly to the new demands of postwar industrial capitalism. Most insurers in Maritime countries, moreover, already had significant experience with underwriting relevant risks, partly in the form of industrial insurance and partly in the form of group insurance. American life insurers like the Equitable Life Assurance Society and Metropolitan Life, for instance, had already started selling group insurance to businesses as early as the 1910s and 1920s, providing coverage for life, accident, and sickness risks as well as pensions. 69 US business exported its model of corporate welfarism into Canada, where in the early twentieth century the business community similarly perceived group insurance as a means to do “away with a great many labor troubles, discouraging strikes and generally improving the morale of the employees.” 70 Through the UK branch of Metropolitan Life, group insurance for old age pensions was also introduced in the United Kingdom in the late 1920s, partially replacing endowment assurances as the dominant product sold by life insurers to enable saving for retirement. 71 For many social groups, the protean group-insurance schemes alleviated the necessity of setting up state-sponsored social insurance schemes. In Austria and Germany, by contrast, the generally weaker insurers had been devastated by a complete erosion of their assets through hyperinflation. Funded pensions through group insurances were also introduced after World War II but has not been adopted as a general product by businesses and insurers (see Figure 7), who were unable to prevent the PAYGO pension reforms after World War II.

Group insurance in force relative to GDP (percentage). (See the appendix for a full list of the sources.)

Switzerland is the exception that confirms the rule. The Swiss “labor relations and welfare configuration,” Leimgruber observes, “strikingly echo those in the United States.” 72 In the second half of the nineteenth century, close business coordination had led to the setting up of a mutual insurance firm that was intended “both as a vessel to centralize savings in a period of industrial expansion and as a way to ensure political and social stability by encouraging life insurance and thriftiness.” 73 It did so by selling group contracts and a Swiss version of industrial insurance well in advance of the development of modern social insurance schemes, thereby alleviating the necessity of more state-led social insurance arrangements. What the Swiss case suggests, then, is that the existence of a strong private insurance sector with the capacity to assert its preferences in the social policy domain matters greatly for the development of public welfare arrangements.

Countries with large private insurance sectors thus not only had the capacity to provide an alternative for public welfare schemes; they were also better equipped to collectively organize and lobby against public welfare solutions. 74 These insurance lobbies tended to tap into the emerging “politics of security” by emphasizing the role of private insurance as a supplement to basic public welfare arrangements, aiming at tax exemptions and limited public security, as shown for the United States and Canada. 75 In the United Kingdom, for instance, the Life Offices Association embarked on an expensive but successful PR campaign to thwart Labour Party proposals for an earnings-related national superannuation scheme. 76 Similarly, Swiss private insurers were able to insert their preferences in the making of a federal welfare state, for instance, through the mechanism of revolving doors: indeed, the careers of key policymakers “straddl[ed] the first two pillars of the old age provision.” 77

Another factor solidifying the path dependencies that put Maritime insurance culture on the path toward highly privatized welfare arrangements was insurers’ knowledge lead. Private insurance companies had been accumulating business experience and statistics on mortality, invalidity, and accidents, which made them important interlocutors when the first public welfare reforms were passed. 78 The epistemic foundations of public insurance thus directly rested on private business experience.

Actuarial knowledge and expertise played an important role in the design of the welfare states across countries. But this expertise served as a conduit for the preferences of private insurers in some countries more than in others. In the Maritime countries, the actuarial profession became formally institutionalized with the setting up of the English Institute of Actuaries in 1848, the Scottish Faculty of Actuaries in 1856, and the Actuarial Society of America in 1889. Although the actuarial profession in the Anglo-Saxon world benefited initially from its close ties to statistical theory, it later distanced itself from the world of science, occupying a more prominent role in the management and governance of private insurance business instead. 79 In the United Kingdom, for instance, actuaries took up prominent positions on the boards of insurance companies well into the late twentieth century. 80 Actuaries were also employed by the government, but rather than having a distinct professional identity, they seemed to serve more as an outpost of the profession. 81

In the Alpine world, the institutional embedding of actuarial expertise was quite different. In Germany, actuarial expertise became more firmly institutionalized in bureaucracy and the university system through the protean academic discipline of Versicherungswissenschaften or insurance sciences in the late eighteenth century. Within this setup, German actuarial expertise maintained closer ties to the related disciplines of statistics and political economy, and became wedded not mainly to the private insurance sector but to insurance more generally, encompassing both private and social insurance. 82 In Switzerland—again the exception that confirms the rule—the timing of the institutionalization of actuarial expertise was similar but attempts to develop an insurance science failed because of the fact that the development of a social insurance bureaucracy was much more protracted, which gave private insurance representatives (who tended to favor the more British model of actuarial sciences) a stronger say in the institutionalization of actuarial expertise. 83 Private insurance interests subsequently gained strong footing in the development of social policy by systematic representation in the commission of experts on social insurance. 84

While the differences between Alpine and Maritime social security arrangements were still clearly pronounced in the 1970s, from the 1980s onward they started to dissipate. One crucial factor in this process, we suggest, was the catching up of Alpine insurers and the concomitant disappearance of differences between the Maritime and Alpine insurance systems in terms of size, composition of investment portfolios, and regulation (see above). In Europe, the integration of insurance markets initiated a trend toward the liberalization of the German and Austrian insurance markets and facilitated cross-border entry among EU member states. 85 The 1970s and 1980s also saw the emergence and strengthening of international insurance groups, which became active proponents of harmonizing insurance practices across countries. Austrian and German insurers, moreover, had recovered much of their prewar capital base, allowing them to play a more prominent role in economic coordination. Illustrative in this regard is the history of Allianz, which pursued relentless international expansion from the 1970s onward and acquired a prominent role in German corporate governance. 86

The breaking down of barriers between different national insurance industries was by no means a smooth process. Until the late 1990s and early 2000s political negotiations around regulatory harmonization (regulatory differences were regarded as the main impediment to market integration) resembled a “battle of the systems” along the lines of the clash identified by Lengwiler that had existed since the late nineteenth and early twentieth century, 87 that is, a clash between a more interventionist continental approach and a more liberal approach to regulation dominant in the United Kingdom. 88 While regulatory harmonization was seen as key to further market integration, attempts to do so remained stuck in the trenches of different approaches to insurance. This only started to change in the late 1990s when the rise of integrated financial services supervisors, the increased authority of international accounting standards, the emergence of increasingly large international insurance groups, and the diffusion of financial expertise in Europe had facilitated the emergence of cross-country coalitions supporting a pan-European regulatory framework based on the principles of modern finance theory. 89 The three non-EU countries in our sample (excluding the United Kingdom) had already adopted a system of risk-based capital regulation in prior years: Canada in 1987, the United States in 1992, and Switzerland in 2009.

While the British, American, Swiss, and Canadian insurance industries had already succeeded in gaining a significant share of the welfare pie in the postwar period (although with different levels of success across sectors), lobbying efforts in Germany and Austria seemed to have become more effective in the 1980s and 1990s too. 90 Naczyk and Palier show for instance for Germany that private finance—and especially insurance companies—has actively lobbied for the privatization of old age insurance, making the case that the creation of large pools of private capital through funded occupational pension schemes would strengthen the competitive position of the domestic financial industry in an increasingly global financial system. 91 One way to do so has been through the advocacy for three-pillared pension systems, 92 which offered a clear framework for reform and enabled states first to encourage saving for retirement through private accounts by making it attractive for tax purposes and then to cut back on public pension promises. 93 Insurers, in other words, fostered the (public and private) retrenchment zeal of the 1980s and 1990s in both Maritime and Alpine countries by stepping in as alternative providers of old age economic security. Once privatization takes hold of welfare regimes, it becomes increasingly difficult to halt or even revert the process. Busemeyer and Iversen, for instance, show that the increased availability of private insurance alternatives “undermines support for universalistic public provision of social insurance among the middle and upper income classes,” 94 a finding confirmed with longitudinal data in Germany. 95

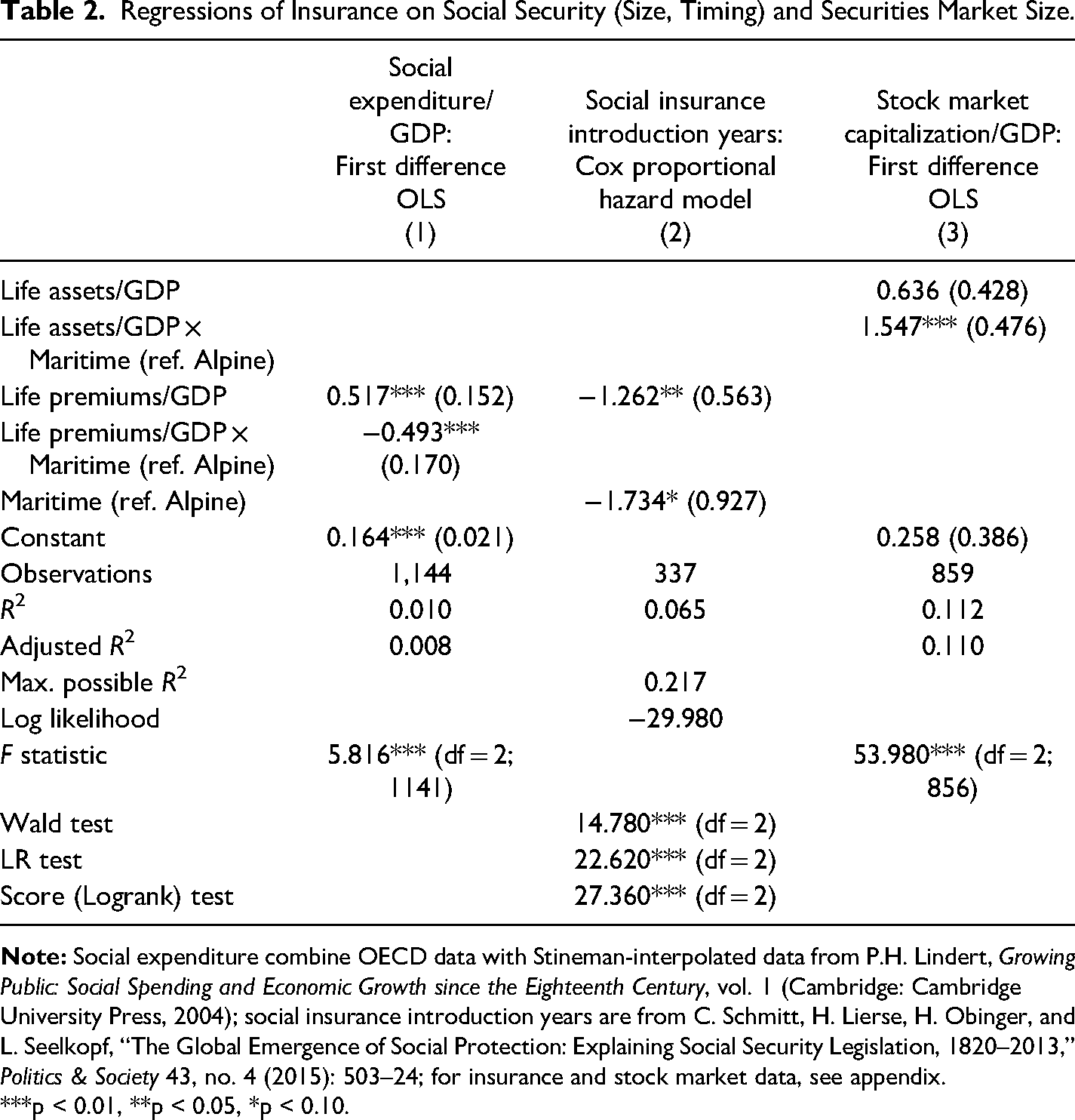

To substantiate these claims about the association between private insurance and the welfare state, we additionally ran two regressions: one first-difference ordinary least squares (OLS) regression of the size of private insurance (premiums per GDP) on the size of the welfare state (social expenditure per GDP) in column 1 of Table 2 and a Cox-hazard model on the post-1880 risk to introduce average social security legislation in column 2. We also add the interaction with Maritime (vs. Alpine) insurance countries, where we include Australia, New Zealand, and Italy, respectively, to achieve more statistical power.

Regressions of Insurance on Social Security (Size, Timing) and Securities Market Size.

***p < 0.01, **p < 0.05, *p < 0.10.

The results confirm that private insurance significantly retards the introduction of social security, significantly more so in interaction with Maritime countries, while leading to competitive growth of welfare states later, but very much dampened and neutralized in Maritime countries. Column 3's first difference OLS, in turn, quantitatively anticipates and supports the claim of the next section: the size of life insurance in terms of its total invested assets is positively associated with stock market capitalization, significantly more so in Maritime countries.

Insurers and Financial Systems

What lies qualitatively and historically behind this association? In this section, we focus on the interactions between the different varieties of insurance capitalism and the development of financial system. Here, we argue that private insurance did not just seize the investment opportunities offered by already existing national financial systems; instead, it has been a force to reckon with of its own, competing with banks and other deposit-taking institutions and shaping the direction of financial development by extending securities markets.

First, it should be noted that Maritime insurers have in the past been relatively more successful in attracting capital than their Alpine counterparts. We already noted that private insurance was relatively more sizable in Maritime countries, even when compared against GDP. Figure 8 shows, moreover, that it has also been more sizable relative to the comparatively larger Maritime financial systems, with assets over 15 percent of their country's financial system or double the Alpine shares. This is due mostly to the existence of long-term insurance arrangements—for example, most life insurance—which function as capital-mobilizing and capital-collecting institutions. 96 Historically, the relative success of Maritime insurers can be explained by the early development of private insurance relative to modern retail banking institutions. 97 It is no surprise, therefore, that American insurers, from early on, developed elements in insurance contracts that allowed the insured to draw on their capital when needed, through policy notes, policy loans, surrender values, and so on, making insurance suitable as an instrument for saving and investment. In contrast, in continental Europe, insurance contracts mostly served the purpose of protection and were liberalized in favor of saving and investing consumers only much later. Here, social reformers had spread a dense network of mutual, municipal, or cooperative savings banks, starting in the late eighteenth century and gaining momentum from then onward. 98 Anglophone countries also developed a combination of trustee, mutual, and postal savings banks, but on a considerably smaller scale than both their commercial counterparts and the continental savings banks. In the thinly settled American West, for instance, insurers could grow much more easily through their agency system in contrast to banks, which had to rely on branches and were moreover restricted to statewide operations. Growing through agents required less overhead, was more flexible, and was moreover driven by a stronger insurance desire to diversify risk. 99 Oversimplified, the Alpines were overbanked but underinsured, and the Maritimes, underbanked but overinsured.

Share of insurance assets in total financial system. (Raymond Goldsmith, Financial Structure and Development [New Haven, CT: Yale University Press, 1969].)

Where insurers competed with banks in deposit collection, they helped to create and complement securities markets from early on. First, the early private insurers in need of large capital reserves were among the first joint-stock companies, listed with trading companies, banks, and railroads on early stock exchanges. 100 Second, and perhaps more importantly, insurers were among the most important investors in early securities markets, as they could count on a more predictable inflow of capital and, through active trading in the range of one to two times this capital, guaranteed the necessary liquidity and efficiency of these markets because they often bought countercyclically. As insurers’ payouts are independent of financial market risks and insulated from “insurance runs,” they are often said to provide a stable source of funding for financial systems. 101 Third, through the actuarial profession, insurers were also actively involved in the construction of the knowledge infrastructures that made financial markets legible and actionable for increasingly large funds. In the United Kingdom, for instance, the Institute and Faculty of Actuaries constructed and maintained the Actuaries Index of yields on stocks and bonds from 1929, which was later supplanted by the influential FT Actuaries index first published in 1962. 102 These indices facilitated the rationalization and professionalization of investment policy, thereby strengthening the legitimacy of market-based finance.

Insurance capital was thus instrumental in the creation of financial markets. In the United States, life insurers facilitated the creation of both primary and secondary bond markets between the Civil War and World War I. 103 Investment banks relied on insurers as the most important syndicate members when placing new issues. 104 By 1905, securities—mainly railroad, then also industrial, utility, and government bonds—made up around 50 percent of insurers’ portfolios and 50 percent and more of the total securities market. 105 While US life insurers invested in bonds, fire and marine insurers invested predominantly in American stocks with 25 to 30 percent portfolio share over many decades. 106 In Canada, it took until the setting up of the first domestic company Canada Life, which unlike existing British and American firms bought domestic debentures and stocks, to create a domestic securities market, based even more on stocks than bonds. 107 This changed with the growth of government debt and the 1929 crash, when the exceptionally large Sun Life held more than 50 percent stocks, with all big companies maintaining large investment departments for active securities trading. 108 British insurers, in turn, have likewise had a long tradition of buying bonds and stocks from the nineteenth century, but the interwar years saw an increased focus toward more stock investment. 109

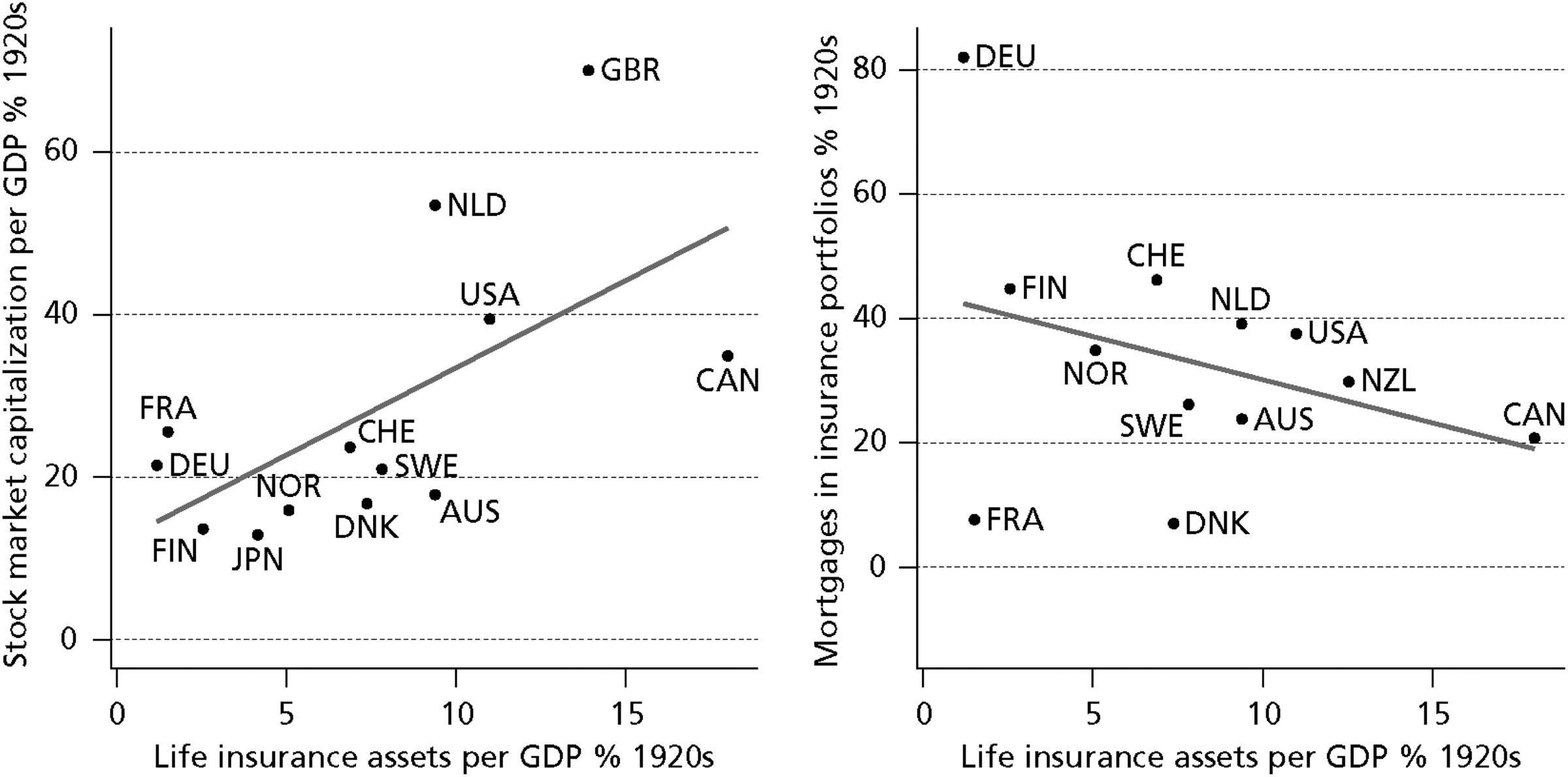

In Alpine countries, by contrast, the large majority of life investments was in direct mortgages or, in Austria, mortgage bonds, a feature that even the two intermezzi of forced war-bond investments did not change (see Figure 1). In Switzerland, insurers generally held few bank and mortgage bonds. 110 The growing protectionism of the insurance industry, particularly in Alpine countries, forcing foreign insurers to buy domestic securities, reveals the importance attributed to insurers for securities markets and capital mobilization. 111 Not surprisingly then, the historical insurance asset size of countries correlates positively with the historic stock market capitalization and negatively with the portfolio shares of direct mortgages (see Figure 9).

Life insurance assets per GDP and size of securities markets, average 1920s. (See the appendix for a full list of the sources.)

In postwar Germany and Austria, insurers continued to play a marginal role because much of their capital base had been destroyed by hyperinflation and the destruction of real estate and default on state bonds during the war: while Maritime life assets amounted to 16 percent of GDP by 1914 compared with 11 percent in Alpine countries, the comparison was 17 to 4 percent in 1925 and even 24 to 8 percent by 1950 (see Figure 1). In Germany, the retreat from mortgage investment was relatively slow given the housing reconstruction needs and rather gave way to corporate loans with additional securities instead of tradable securities. 112 Austrian insurers also rather gave out loans to corporations. 113 Banks remained primordial for corporate finance and underwriting of securities and the government for total investment; in the Maritime countries, in contrast, private insurers played a major role in capital formation and securities investments, taking up more than half of all the new security issues offered in the United Kingdom and similarly in Canada. 114

Since the 1970s, life assets have experienced an accelerated growth to more than 50 percent of GDP in Maritime and more than 30 percent in Alpine countries in 2015, with an unequivocal trend toward investment in financial securities (see Figure 4). While in Maritime countries, insurers now invest at least 75 percent of their assets in financial securities (with British insurers investing nearly all their assets in financial securities, mostly stocks), in Alpine countries, insurers now also invest most of their assets in financial securities, mostly bonds. The change in the composition of Alpine insurers’ investment portfolios was the result of a growing volume of investments in light of pension privatizations and the increased internationalization of the financial system. 115 In Germany, for instance, insurers held $125 billion in 1980, an amount that would nearly quadruple in the following decade to $453 billion, 116 which amounted to around a quarter of German GDP in 1990. This amount again doubled to €860 billion in 2000, making insurers “the most important institutional investors in Germany.” 117 Thus, in terms of assets, Alpine insurers—and especially German insurers—grew substantially, becoming increasingly important institutional investors heavily invested in financial assets, mostly in fixed-income but since the beginning of the 2000s also increasingly in equities. These assets were not just invested domestically but also increasingly across borders. The rise of securitization in the 1990s and of a highly internationalized financial system more generally meant that Alpine insurers enjoyed access to a larger pool of investible financial securities, which is reflected in increased investment in financial assets and a rising share of foreign assets. Moreover, the increased internationalization of the banking sector also meant that governments increasingly perceived pension privatization and the concomitant growing capital base of insurance companies and pension funds as an attractive policy option to compensate for the reduced capacity of the domestic banking sector to supply patient capital. 118

In the same period, the volume of Maritime insurers’ assets continued to grow apace. In the United Kingdom, the United States, and to a lesser extent in Canada, insurers were among the most sizable institutional investors, who took up an increasingly important role in corporate governance. In the United States, for instance, insurers owned 26.6 percent of $2.09 trillion assets owned by institutional investors in 1981, and in 1990, they owned 29.7 percent of $6.52 trillion. 119 In the United Kingdom, the share of institutional capital managed by insurers was even larger at 46 percent of £600 billion in 1990 and 54 percent of nearly £2 trillion in 2000 (ONS). While in the United States, a large share of savings ended up in mutual funds, British insurers managed to strengthen their hold of the savings market by offering investment in the functionally near-equivalent unit-trusts—often managed by the insurers themselves—through their insurance contracts. 120 Insurers, moreover, did not just continue to feed the expansion of Anglo-Saxon capital markets but also had an influence on the kind of instruments that were issued. A good example of this is the index-linked or inflation-linked bond, coupon payments of which are linked to an inflation index. This instrument, which was first issued by the British government in 1981, 121 is favored by insurance companies and pension funds, who may use these “linkers” to “match” their investments with their long-term inflation-linked liabilities (e.g., pension annuities). The government, in return, will likely be able to pay relatively low interest rates as long as they can keep inflation down.

Private insurance thus had—and continues to have—a strong influence on capital market development, both in terms of volumes purchased and traded as well as expertise and instruments. Countries with larger life industries are also home to larger stock markets. 122 Although Alpine insurers have started to catch up with their Maritime counterparts in terms of size and investment portfolios, differences still remain. While in Maritime countries long-term insurance arrangements are generally seen as vehicles for saving and investment enabling policyholders to “embrace” capital market risk, 123 the relative emphasis of long-term insurance arrangements in Alpine countries remains on protection, which privileges investment in fixed-income instruments rather than stocks. British insurers, for instance, are free to shift the burden of financial risk to the level of individual policyholders. 124 German life insurers, in contrast, must adopt a state-administered guaranteed interest rate and distribute additional profits directly to policyholders. 125 The nature of the insurance arrangements, in other words, continues to affect the functioning of insurers as financial intermediaries channeling savings into capital markets.

Conclusion

Private insurance is a potent but underappreciated force shaping the various social and economic security arrangements of modern capitalist societies. To make this point, we picked up on the work of Michel Albert, who perceived the existence of two distinct insurance cultures, to develop and substantiate a descriptive typology distinguishing between Alpine and Maritime varieties of insurance capitalism. Within this descriptive typology, the Maritime variety of insurance capitalism is much more oriented toward market competition, relies on a larger share of investments in financial market assets, is more oriented toward saving and investment, and developed much more quickly, especially in the early years. The Alpine variety, in contrast, is characterized by more direct state involvement through state-associated insurance enterprises and tight regulation of competition, direct investments in mortgages and loans to government, and a more protracted development. Perhaps unsurprisingly, this classification roughly corresponds to the more commonly discussed classifications in CPE of welfare states and financial systems and could geographically even be extended to include other English-speaking countries on the Maritime side and more CMEs on the Alpine one. The main point of this exercise, however, is not just to point to the correspondence between these different classifications but to think through the causal relation between the development of private insurance industries and the broader social and economic security arrangements characterizing contemporary national political economies.

The differential development of private insurance can be explained through Gerschenkronian development theory, with private insurance emerging in early developers as centers of capital accumulation. The differentiated timing and pace of private insurance development across Alpines and Maritimes, we suggest, has in turn played an important role in shaping the welfare arrangements and financial systems of these countries, which insurance largely preceded. The earlier and more fully a private insurance industry developed relative to public welfare institutions and financial institutions, the more likely a country would develop as a liberal welfare state with a market-based financial system and a private insurance sector of the Maritime kind. When private insurance developed more slowly relative to welfare institutions and financial systems, a country is more likely to have developed as a Bismarckian welfare state with a bank-based financial system and a private insurance sector of the Alpine kind. The distinct trajectories of the German and Austrian cases on the one hand and the Swiss case on the other confirms this point: while the hyperinflation of the 1930s set the German and Austrian insurance industries backward in their historical development, the Swiss insurance industry, which seemed clearly of a more Alpine kind, continued to grow and successfully pushed for a more privatized welfare regime based on the American model. 126 Private insurance, in other words, is a crucial link for understanding the association between the development of financial systems and welfare arrangements.

As the development of the Alpine private insurance industry is catching up with its Maritime counterpart, private insurers can well become a force to reckon with in shaping the future of the broader economic and social security arrangements in the Alpines (indeed, they have already been a force to reckon with in the Swiss case). Private insurers can do so by offering private alternatives to public welfare arrangements, by lobbying for the privatization of public welfare arrangements, and by providing the expertise through which many of today's policy choices are understood. From an economic policy perspective, moreover, the nurturing of a large private insurance sector can be seen as a clear path toward enhanced domestic capital market development. 127 The catching up of the Alpine with the Maritime insurance sector, in other words, makes it more likely that the social and economic security arrangements of these national political economies will (continue to) converge on a liberal welfare model and on market-based finance, both predominantly seen in the Maritimes. Under pressure from common European regulation and financialization, signs of convergence on a more Maritime model of insurance have already been visible, with increased financial market investment and a convergence on a risk-based model of regulation aimed at stimulating competition among insurers. 128 To what extent the Alpine countries will truly come to “embrace” risk as they do in their Maritime counterparts, however, remains to be seen. 129

Footnotes

Appendix

Acknowledgments

For the excellent feedback we have received on earlier drafts of this article, we owe a debt of gratitude to many of our colleagues. In particular, we wish to thank Brett Christophers, Vanessa Endrejat, Matthieu Leimgruber, Nils Röper, Michael Schwan, and the editors of this journal. We would also like to thank the Verband der Versicherungsunternehmen Österreichs for their help with the collection of statistical data.

Authors' Note

Arjen van der Heide is also affiliated at the Netherlands Institute for Social Research.

Sebastian Kohl is also affiliated at the Max Planck Institute for the Studies of Societies.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.